aim chaos · pdf fileaim chaos aim chaos is the @aim_chaos [email protected] research branch...

TRANSCRIPT

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 1 of 16

AIM CHAOS

N4 Pharma Plc

Ticker: N4P 31 July 2017 Buy-in Price (p): 5.25 Market cap (£m): 3.92 Rationale: Company’s value not recognized

Executive summary N4 Pharma Plc (‘N4’ or ‘the Company’) is a specialist pharmaceutical company which reformulates existing drugs and vaccines to improve their performance. N4 was founded in 2014 by its CEO and largest shareholder, Nigel Theobald, who has a strong track record in the healthcare and biotech industries. The Company listed on AIM in May this year via a reverse takeover of Onzima Ventures Plc, an investing company that had already acquired a 49% equity stake in N4 in 2016. The enlarged group raised £1.5m of new equity at a pre-new money valuation of £3.5m, therefore listing with a market capitalisation of £5.0m at the placing price of 7.0p. Since May, the Company has received a further £0.24m through the exercise of warrants. N4 operates under two divisions:

- Drug reformulation This division is focussed on developing new versions of existing widely used drugs, via reformulation, to provide an improved patient experience. Drugs targeted for reformulation are those that are off patent or soon-to-be off patent. The division’s lead product under development is a faster acting, longer lasting version of the drug sildenafil – commonly known by the brand name, Viagra. N4 has a further four products in earlier stages of development, and is seeking to add up to a further five in the next two years.

- Vaccine delivery N4 has acquired the exclusive rights from the University of Queensland to commercialise two patent-pending vaccine delivery systems. The Company is currently undertaking research to demonstrate that these vaccine delivery systems can protect the vaccine in the body and improve the ability of the vaccine to produce an immune response.

For both divisions, N4’s strategy is to achieve proof of concept for its products, and subsequently to partner with pharma majors to bring the products through to commercialisation. The model has the potential to generate very high returns on comparatively little capital expenditure. Despite rallying strongly in the weeks following listing, the Company’s share price has since dropped below the IPO price. We believe that the wider market does not fully comprehend N4’s business model and the quality of both its portfolio and workforce. In this note we attempt to justify our view that at its current market capitalisation of £3.92m, N4 is substantially undervalued.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 2 of 16

Drug reformulation division

Why drug reformulation? Bringing a novel drug to market is an inherently risky process. It usually costs in excess of £500m and can take 10 to 12 years to complete. Against this, it has recently been estimated that less than 10% of novel drugs ever reach the stage of commercialisation. Even when a drug is successfully developed, approved by the relevant regulatory bodies and at last commercialised, it is often the case that the drug is imperfect. However, the institution of patent protection renders this situation meaningless. Take for example sildenafil, the name of the generic drug widely used in the erectile dysfunction market. Sildenafil – branded by its owner Pfizer as ‘Viagra’ – was initially studied for use in hypertension (i.e. high blood pressure) and heart disorders. However, in clinical studies it was discovered that a side effect was its use in the erectile dysfunction market. Given that Viagra was under patent, it thus was the only product available to the consumer – despite not having the ideal characteristics that one would expect from a drug combatting erectile dysfunction, such as time to onset (circa one hour), time length of drug efficacy (only six hours) and not being able to eat food with it. The process of drug reformulation is most effective in a commercial sense when it is employed to develop an enhanced version of an existing widely used drug, crucially that is off patent or soon-to-be off patent. Continuing on from the example above, Viagra came off patent in Europe in 2013: already it has lost significant market share as other drugs have been able to compete. N4’s lead product, a reformulated version of sildenafil that enables quicker onset of action (15 minutes instead of an hour) and longer lifespan (12 hours+ as opposed to Viagra’s four hours), could potentially be one such drug. N4’s reformulated sildenafil could also receive worldwide patent protection. Strangely, it appears commonplace amongst Big Pharmas that in-house reformulation of their off patent or soon-to-be off patent branded drugs is not a priority. Accordingly, there exists a significant opportunity for smaller players to enhance the characteristics of well-known drugs through reformulation methodologies at a comparatively low cost, and to subsequently license these drugs back out to majors who can then rebrand and commercialise them. N4’s drug reformulation operations and the intended business model The Company’s reformulation division is founded on its relationship with Opal IP Ltd (‘Opal’), a drug reformulation patent-writing company. Opal co-founder and director Peter Lawton is one of the world’s leading drug patent writers – “having developed new patents that substantially extended the life cycle management of some of the world’s largest pharma brands such as Paxil and Augmentin. He has since used his expertise to write a vast number of patents for other drugs which can either extend their life cycle or be a rich source of differentiation for generic companies once the drug comes off patent.” In March 2016, N4 acquired the exclusive global rights to Opal’s extensive portfolio of novel patents for drug reformulations. Under the terms of the agreement, N4 has an exclusive agreement to evaluate the most commercially valuable patents and to file them for commercial development, in return for a royalty agreement with Opal. Having selected a particular ‘patent family’ (which contains a range of patents relating to various forms, formulations and uses of the generic drug in question) from Opal’s portfolio, N4 then

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 3 of 16

initiates research and development in order to generate the required clinical proof of concept data. All R&D is outsourced in order to keep overheads to a minimum. The first stage is in-vitro formulation work, which lasts approximately six months and includes laboratory dissolution testing of the formulation to establish the correct dissolution profile required for the reformulated product. At the beginning of the process, N4 files the family of patent applications. Each family includes a ‘master’ UK patent application, which describes, in general terms, a wide range of forms, formulations and uses of the drug in question, and explains the envisaged advantages. The family of patent applications can be significant: in the sildenafil patent family for example, 45 patent applications were filed. It is assumed that many will be rejected, but the scattergun approach should ensure that some at the least are accepted. The rationale behind filing the master application even before in-vitro formulation work commences is that it establishes a ‘priority date’. This then gives the Company a further 12 months’ leeway to submit an international application under the Patent Cooperation Treaty (‘PCT’), which boasts over 150 countries worldwide as members. The PCT patent application is usually filed towards the end of the in-vitro formulation work: this enables it to be updated (above and beyond the master UK patent application) prior to submission. The PCT patent application replaces the master UK patent application. A granted PCT patent would effectively give worldwide protection to the Company’s reformulation methodology in question. We estimate that all outsourced in-vitro formulation laboratory work will cost N4 circa £0.2m per targeted drug. The second stage in generating the required clinical proof of concept data is to conduct small-scale (circa 10) human clinical trials (‘Phase I trials’). Phase I trials would last 3-4 months. N4’s lead product in its reformulation division, sildenafil, is currently being prepared for Phase I: the trials will be run early next year, with results expected by the end of April. We estimate that Phase I trials will cost N4 circa £0.75m per targeted drug. Assuming a positive outcome, using the data assembled thus far N4 would then seek pre-IND acceptance from the US Food and Drug Administration (‘FDA’). Pre-IND acceptance in short means that if an entity that is seeking IND acceptance and marketing approval (post carrying out Phase III trials) opens dialogue with the FDA prior to the commencement of Phase III trials, and sets out what it intends for Phase III trials and what its endpoints will be – then if those endpoints are met in the trials, IND acceptance and marketing approval will be granted. Once binding pre-IND clearance from the FDA has been granted, the Company is able to progress straight to Phase III trials (also known as ‘Pivotal’ trials), missing out Phase II trials entirely. Pivotal trials for a reformulated drug involve only 50 to 100 patients (in comparison to 300 to 3,000 for Phase III trials of a novel drug), and from initial planning to receipt of results take no more than 18 months. We estimate that Phase III trials for a reformulated drug that has already received pre-IND acceptance will cost circa £3.0m. We believe that N4 is most likely to seek to partner with a major pharma player in order to secure financing for the Phase III trials. In return, N4 will receive certain milestone payments along the development curve, and eventually royalties from sales.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 4 of 16

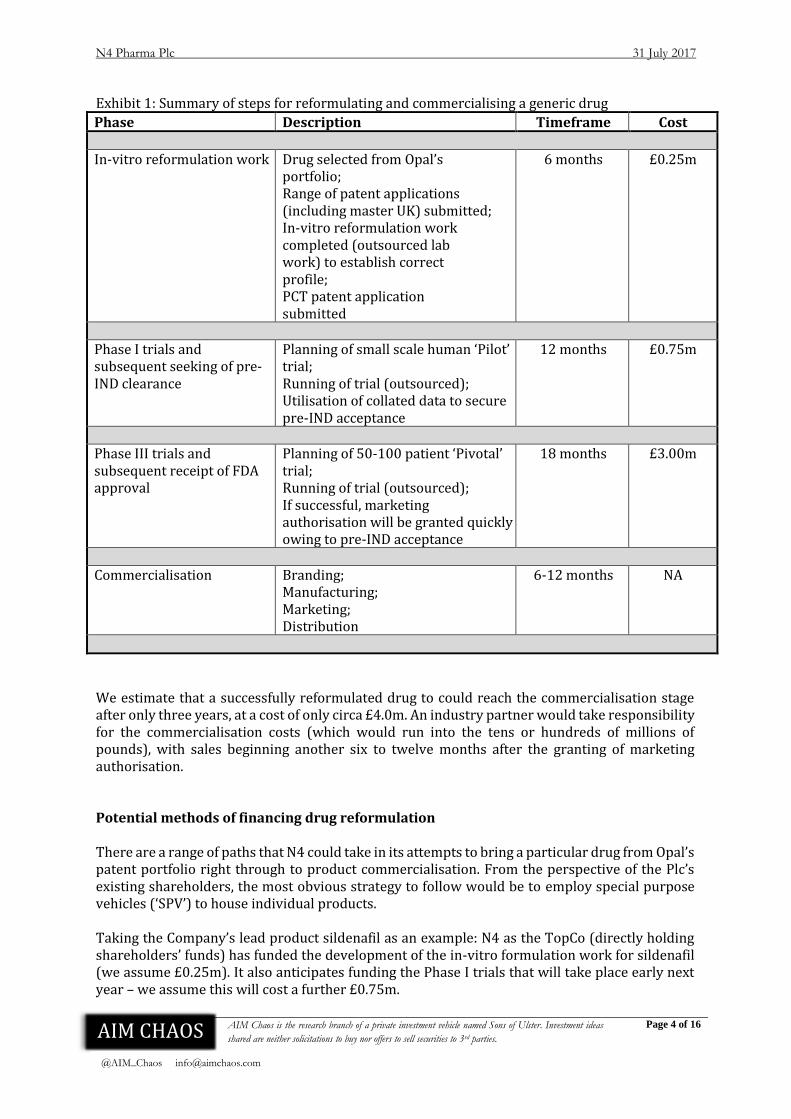

Exhibit 1: Summary of steps for reformulating and commercialising a generic drug

Phase Description Timeframe Cost

In-vitro reformulation work Drug selected from Opal’s

portfolio; Range of patent applications (including master UK) submitted; In-vitro reformulation work completed (outsourced lab work) to establish correct profile; PCT patent application submitted

6 months £0.25m

Phase I trials and subsequent seeking of pre-IND clearance

Planning of small scale human ‘Pilot’ trial; Running of trial (outsourced); Utilisation of collated data to secure pre-IND acceptance

12 months £0.75m

Phase III trials and subsequent receipt of FDA approval

Planning of 50-100 patient ‘Pivotal’ trial; Running of trial (outsourced); If successful, marketing authorisation will be granted quickly owing to pre-IND acceptance

18 months £3.00m

Commercialisation Branding;

Manufacturing; Marketing; Distribution

6-12 months NA

We estimate that a successfully reformulated drug to could reach the commercialisation stage after only three years, at a cost of only circa £4.0m. An industry partner would take responsibility for the commercialisation costs (which would run into the tens or hundreds of millions of pounds), with sales beginning another six to twelve months after the granting of marketing authorisation. Potential methods of financing drug reformulation There are a range of paths that N4 could take in its attempts to bring a particular drug from Opal’s patent portfolio right through to product commercialisation. From the perspective of the Plc’s existing shareholders, the most obvious strategy to follow would be to employ special purpose vehicles (‘SPV’) to house individual products. Taking the Company’s lead product sildenafil as an example: N4 as the TopCo (directly holding shareholders’ funds) has funded the development of the in-vitro formulation work for sildenafil (we assume £0.25m). It also anticipates funding the Phase I trials that will take place early next year – we assume this will cost a further £0.75m.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 5 of 16

Assuming that this Pilot trial is successful and that subsequently pre-IND clearance is granted, the reformulated sildenafil product would be in an exceptionally strong position, in comparison to novel drugs in development that have just completed Phase I. After all, the reformulated sildenafil is only a modified version of Viagra, a drug that has already gone through the long and rigorous novel drug application process, and that has been in commercial use around the world for almost twenty years. In our opinion, given the current market capitalisation of N4 of 3.92m, raising the £3.0m in order to proceed with the Phase III trials via an equity placing in the TopCo would be very damaging to the positions of existing shareholders. At this juncture, it is important to note that CEO Nigel Theobald is N4’s largest shareholder with a 16.3% equity interest. Moreover, subject to meeting certain milestones (specifically, the share price remaining above 15.0p for 10 consecutive trading days within two years after the date of IPO), he will be entitled to 4.59m further consideration shares that would increase his holding to 21.1%. As such, it is reasonable to assume that the CEO is desirous of limiting equity dilution in N4, especially at the Company’s current valuation. The SPV structure would, we believe, best be employed once the reformulated sildenafil has received pre-IND acceptance. We envisage the following:

- All patents and IP for the reformulated sildenafil product injected into a newly created SPV

- A major pharma company farms into the SPV, taking a 90% stake (or else taking all but leaving N4 with a 10% royalty stream), in return for shouldering the £3.0m costs for Phase III trials and then all costs associated with product commercialisation

In this process, N4 will be expending around £1.0m over a period of 18 months on each drug that it targets for reformulation. In return, it will receive a 10% royalty stream on sales of all of its successfully reformulated and commercialised drugs. There is also the potential for receiving upfront milestone payments, whilst a drug is under the latter stages of development. Clearly, this would limit equity dilution in N4 tremendously and still provide potentially outstanding returns to shareholders. However, given that management has expressed its intention to build a portfolio of up to ten drugs that it will target for reformulation (it already has five under development), expenditure of circa £10m in the next three years or so – coming out of N4 (TopCo) funds – suddenly looks rather galling to existing shareholders. To combat this, there is another possible strategy to employ, namely the utilisation of SPVs after the completion of in-vitro reformulation, but before the commencement of Phase I trials. N4 would therefore be expending only £0.25m of shareholder funds per targeted drug. A SPV could be capitalised by outside investors with say £1.0m: the pre-new money valuation of the SPV could be derived from a risk-adjusted NPV. Given the potential returns from a reformulated drug that is successfully commercialised (which the market has currently failed to recognise but which we attempt to demonstrate overleaf), it would not be unreasonable to think that a pre-new money valuation of 5m to £10m could be achieved at this stage – therefore giving N4 retained ownership of the drug of 80% to 90%. The new investors in the SPV (who we envisage would be in the form of VCT funds, specialist biopharma investors, family offices, HNWs, etc.) would be entitled to receive the balance of 10% to 20% of the royalties and milestone payments. Building on this model, N4 could also then go on to raise the £3.0m for the Pivotal trials via the same SPV and the same pool of investors. The NPV – which would form the basis of the valuation for the fundraise – would be increased significantly, taken into account the granting of pre-IND clearance. In this manner, it is feasible that N4 could ultimately finance the development of one

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 6 of 16

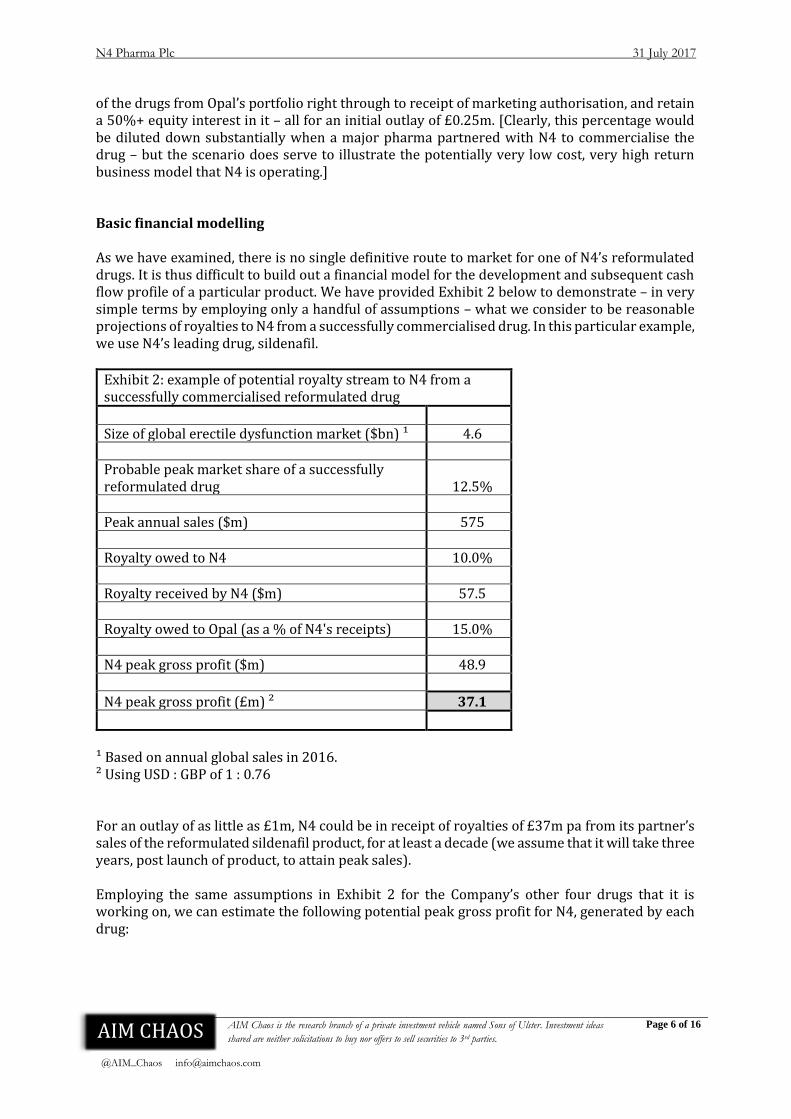

of the drugs from Opal’s portfolio right through to receipt of marketing authorisation, and retain a 50%+ equity interest in it – all for an initial outlay of £0.25m. [Clearly, this percentage would be diluted down substantially when a major pharma partnered with N4 to commercialise the drug – but the scenario does serve to illustrate the potentially very low cost, very high return business model that N4 is operating.] Basic financial modelling As we have examined, there is no single definitive route to market for one of N4’s reformulated drugs. It is thus difficult to build out a financial model for the development and subsequent cash flow profile of a particular product. We have provided Exhibit 2 below to demonstrate – in very simple terms by employing only a handful of assumptions – what we consider to be reasonable projections of royalties to N4 from a successfully commercialised drug. In this particular example, we use N4’s leading drug, sildenafil.

Exhibit 2: example of potential royalty stream to N4 from a successfully commercialised reformulated drug

Size of global erectile dysfunction market ($bn) ¹ 4.6 Probable peak market share of a successfully reformulated drug 12.5% Peak annual sales ($m) 575 Royalty owed to N4 10.0% Royalty received by N4 ($m) 57.5 Royalty owed to Opal (as a % of N4's receipts) 15.0% N4 peak gross profit ($m) 48.9

N4 peak gross profit (£m) ² 37.1

¹ Based on annual global sales in 2016. ² Using USD : GBP of 1 : 0.76 For an outlay of as little as £1m, N4 could be in receipt of royalties of £37m pa from its partner’s sales of the reformulated sildenafil product, for at least a decade (we assume that it will take three years, post launch of product, to attain peak sales). Employing the same assumptions in Exhibit 2 for the Company’s other four drugs that it is working on, we can estimate the following potential peak gross profit for N4, generated by each drug:

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 7 of 16

Exhibit 3: potential gross profits to N4 derived from royalties of successful commercialisation of drugs currently being worked upon

Drug being targeted for reformulation Target market

Target market size ($bn)

N4 gross profit (£m)

Sildenafil Erectile dysfunction 4.6 37.1 Sartans Hypertension 11.2 90.4

Aprepitant Post-surgery and cancer, as an antiemetic 0.55 4.4

Paroxetine Premature ejaculation 4.0 32.3

Duloxetine Hot flushes and night sweats in menopausal women 1.2 9.7

Total: 174.0

This does not take into account any milestone payments that might be due to N4 from its commercial partner for each drug: these payments might be made at successful completion of Phase III trials and granting of marketing authorisation; first sales made, etc. Valuation analysis of reformulation division Given the Company’s unique portfolio, we have found it difficult to locate listed peers. Coupled with its currently non-existent revenue profile and lossmaking position, it has been challenging to conduct relative valuation analysis on the Company specifically with regard to its reformulation division. We have thus opted to carry out intrinsic valuation analysis in order to arrive at a current fair value for the division. We use simplified discounted cash flow (‘DCF’) modelling to achieve this. As we have previously stated, bringing a novel drug from in-vitro formulation through to successful commercialisation is a very long, very expensive and very risky process (10+ years; £500m+ capital costs; <10% probability of success). Reformulation is superior to novel drug formulation in all of these aspects, although of course this is offset by the lower potential returns. The risk profile is a key differentiator between the development of novel and reformulated drugs: the latter can be attributed much greater value comparatively in the early stages of development, owing to the much higher probability of ultimate success. We have used the assumptions set out in Exhibit 2 in our DCF modelling. To our calculated NPVs, we have then attributed varying levels of discounts – dependent on the stage of development that the drug is at – to account for the probability of successful commercialisation:

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 8 of 16

Exhibit 4: probability assumptions used in DCF modelling

Stage Probability of successful commercialisation

Drug selected from Opal portfolio, pre in-vitro work 5.0% In-vitro formulation work successfully completed 10.0% Phase I trials successfully completed, and pre-IND acceptance granted 33.3% Phase III trials successfully completed, and marketing authorisation granted 90.0%

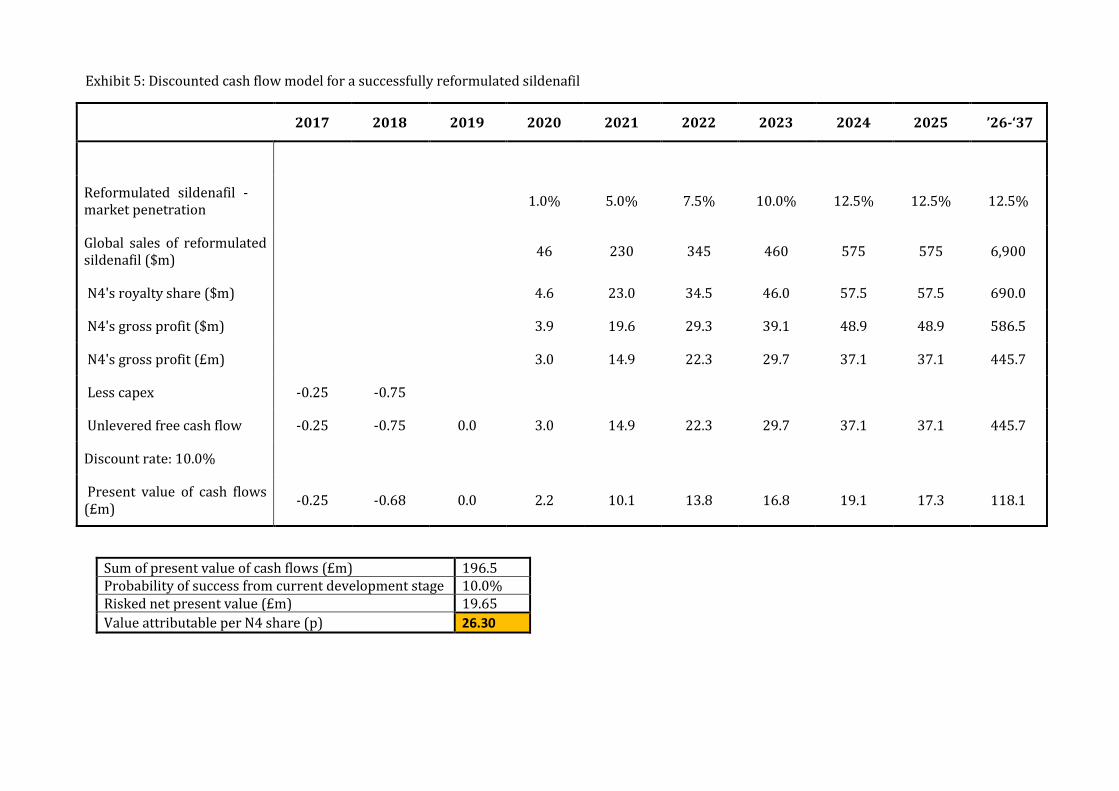

Our DCF model employs a 10% discount rate and runs for 20 years, from the date of the submission of the PCT patent application. We assume peak sales (12.5% global market penetration) are achieved in year 4, following launch of product, and are maintained until the drug comes off patent.

Exhibit 5: Discounted cash flow model for a successfully reformulated sildenafil

Sum of present value of cash flows (£m) 196.5 Probability of success from current development stage 10.0% Risked net present value (£m) 19.65

Value attributable per N4 share (p) 26.30

2017 2018 2019 2020 2021 2022 2023 2024 2025 ’26-‘37

Reformulated sildenafil - market penetration

1.0% 5.0% 7.5% 10.0% 12.5% 12.5% 12.5%

Global sales of reformulated sildenafil ($m)

46 230 345 460 575 575 6,900

N4's royalty share ($m)

4.6 23.0 34.5 46.0 57.5 57.5 690.0

N4's gross profit ($m)

3.9 19.6 29.3 39.1 48.9 48.9 586.5

N4's gross profit (£m) 3.0 14.9 22.3 29.7 37.1 37.1 445.7

Less capex -0.25 -0.75

Unlevered free cash flow -0.25 -0.75 0.0 3.0 14.9 22.3 29.7 37.1 37.1 445.7

Discount rate: 10.0%

Present value of cash flows (£m)

-0.25 -0.68 0.0 2.2 10.1 13.8 16.8 19.1 17.3 118.1

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 11 of 16

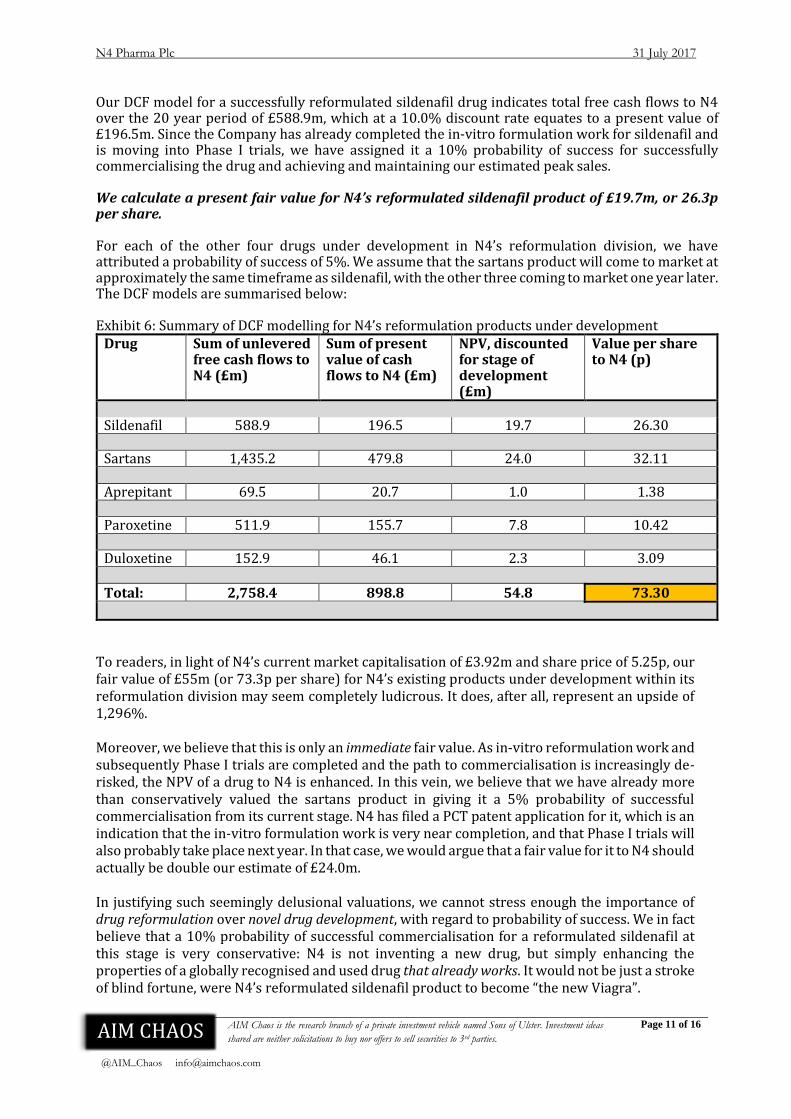

Our DCF model for a successfully reformulated sildenafil drug indicates total free cash flows to N4 over the 20 year period of £588.9m, which at a 10.0% discount rate equates to a present value of £196.5m. Since the Company has already completed the in-vitro formulation work for sildenafil and is moving into Phase I trials, we have assigned it a 10% probability of success for successfully commercialising the drug and achieving and maintaining our estimated peak sales. We calculate a present fair value for N4’s reformulated sildenafil product of £19.7m, or 26.3p per share. For each of the other four drugs under development in N4’s reformulation division, we have attributed a probability of success of 5%. We assume that the sartans product will come to market at approximately the same timeframe as sildenafil, with the other three coming to market one year later. The DCF models are summarised below: Exhibit 6: Summary of DCF modelling for N4’s reformulation products under development

Drug Sum of unlevered free cash flows to N4 (£m)

Sum of present value of cash flows to N4 (£m)

NPV, discounted for stage of development (£m)

Value per share to N4 (p)

Sildenafil 588.9 196.5 19.7 26.30 Sartans 1,435.2 479.8 24.0 32.11 Aprepitant 69.5 20.7 1.0 1.38 Paroxetine 511.9 155.7 7.8 10.42 Duloxetine 152.9 46.1 2.3 3.09 Total: 2,758.4 898.8 54.8 73.30

To readers, in light of N4’s current market capitalisation of £3.92m and share price of 5.25p, our fair value of £55m (or 73.3p per share) for N4’s existing products under development within its reformulation division may seem completely ludicrous. It does, after all, represent an upside of 1,296%. Moreover, we believe that this is only an immediate fair value. As in-vitro reformulation work and subsequently Phase I trials are completed and the path to commercialisation is increasingly de-risked, the NPV of a drug to N4 is enhanced. In this vein, we believe that we have already more than conservatively valued the sartans product in giving it a 5% probability of successful commercialisation from its current stage. N4 has filed a PCT patent application for it, which is an indication that the in-vitro formulation work is very near completion, and that Phase I trials will also probably take place next year. In that case, we would argue that a fair value for it to N4 should actually be double our estimate of £24.0m. In justifying such seemingly delusional valuations, we cannot stress enough the importance of drug reformulation over novel drug development, with regard to probability of success. We in fact believe that a 10% probability of successful commercialisation for a reformulated sildenafil at this stage is very conservative: N4 is not inventing a new drug, but simply enhancing the properties of a globally recognised and used drug that already works. It would not be just a stroke of blind fortune, were N4’s reformulated sildenafil product to become “the new Viagra”.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 12 of 16

Vaccines delivery division

Overview N4 has acquired the exclusive global rights from the University of Queensland to commercialise two patent applications for its vaccines delivery division. The patent applications concern two similar vaccine delivery systems that are designed to protect the vaccine in the body and to improve the ability of the vaccine to produce an immune response. The Company is in the process of developing commercially relevant results through research and development so that it will be able to engage with partners who would then be able to use the delivery systems for their own vaccine development programmes. The two technology platforms are known as Nuvac and Nuvec. Nuvac Nuvac is a nano-carrier delivery system for vaccines. The antigen for the vaccine is loaded into tiny nano-sized silica vesicles which provide a sustained and improved performance of the vaccine. The improved vaccine has been shown to increase both the production of the antibodies needed to fight the vaccine and to kill the virus cells directly. As such the platform is ideal for subunit vaccine reformulation. The platform will allow for single dose vaccines to be developed for vaccines that traditionally require three or more doses: this is particularly relevant in third world countries where multiple dosing is often a major obstacle to overcome. The first subunit vaccine being developed by N4 using the Nuvac platform is a single dose reformulation of the existing Hepatitis B surface antigen vaccine. Nuvec Nuvec is a variation of the Nuvac platform. It has been designed for the intracellular delivery of large nucleic acids such as plasmid DNA and messenger RNA. The intention of the system is to effectively deliver nucleic acids into cells leading to the cellular production of proteins with potential activity as therapeutic entities or antigens for cancer vaccines. In November 2016, N4 announced that it had successfully demonstrated in-vitro transfection efficiency for the Nuvec vector system comparable to industry standard transfection reagents. In June this year, the Company announced that it had successfully demonstrated through in-vivo studies that there is no systemic toxicity caused by the Nuvec platform. N4 is now in the process of demonstrating transfection efficiency via in-vivo studies. We believe that Nuvec is presently at a more advanced stage than Nuvac, and offers the prospect of nearer term value generation for N4 shareholders.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 13 of 16

The intended business model N4 is outsourcing the necessary R&D work for Nuvac and Nuvec to an expert team based in Manchester. The R&D programme is intended to demonstrate the functionality, transfection efficiency and safety profile of the two technology platforms. Subsequently, it is management’s intention to secure commercial partners. Partners would then use the platforms for enhancing their own vaccines under development: any new DNA or RNA vaccine must – as with new drugs – go through the process of pre-clinical trials followed by Phases I to III of clinical trials. N4 will be looking to earn revenues (through licensing agreements) right through these phases, from pre-clinical trials to commercialised vaccine product. Basic financial modelling and valuation analyses It is unclear as to the timeframes to monetisation of the Nuvac and Nuvec platforms. We believe that once the in-vivo work has been completed (with both safety and transfection efficacy successfully demonstrated in animal testing), the platforms will be marketed to the vaccine community. For Nuvec, this could be as early as Q4 of this year, given that in-vivo studies demonstrating the safety of the platform have already been complete, and that in-vivo studies demonstrating transfection capability are (or will shortly be) underway. Assuming that these studies are likewise successful, we see the first partner for Nuvec being struck in H1 2018. We envisage an immediate upfront payment, as well as subsequent milestone payments as the partner’s vaccine under development (which it is enhancing using the Nuvec delivery system) moves through Phases I to III clinical trials. Thereafter, once the vaccine has been commercially launched, N4 might also enjoy royalties and/or annual licence fees. For now, we have not attributed any value to either Nuvac or Nuvec for N4, as it is very difficult to quantify by how much the platforms might enhance the value of a particular vaccine under development; or indeed for which vaccines the platform technologies might be used. However, it is worth highlighting that numerous transactions in the cancer vaccine market in the past several years have included upfront payments of sums that are many multiples of N4’s current market capitalisation. To clarify, that is upfront payments alone: the sum of the potential subsequent milestone payments and royalties / licensing agreements are usually many multiples again of the upfront payments. Accordingly, the striking of a first commercial deal for Nuvec – which could potentially come even in 2017 – has the potential to be transformational for N4, eradicating any funding concerns for the foreseeable future.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 14 of 16

Rationale for current (under)valuation It is most often the case that analysts and brokers are more than happy to provide investors with valuations that suggest that a business is undervalued or overvalued. What they rarely provide is the rationale as to why the business is trading at its current valuation. We believe that this is an integral tool for the investor to better appreciate the potential upside or downside. Below, we highlight what we consider to be the key reasons as to why N4P is trading at its currently suppressed valuation, and in tandem provide what we feel are mitigating factors, where applicable.

- Business model still in proof of concept stage As we have highlighted, the potential value of N4’s business divisions is substantial, amounting to many multiples of the Company’s market capitalisation. We believe that one of the key reasons for this disconnect is that N4 is yet to prove that its business model does in fact work. A commercial deal has not yet been struck within either division: once this does occur (which will likely first be for sildenafil in the reformulation division and for Nuvec in the vaccines delivery division), we believe that the market will quickly attribute fairer values to the products still in development. As investors ourselves, we do not require this confirmation. The process of generic drug reformulation is a well-trodden path: indeed, N4’s reformulation partner, Opal, has one of the best minds in the reformulation business in Peter Lawton. In extending the life cycles of Paxil and Augmentin at GlaxoSmithKline, he played a key role in generating a further several billion dollars in revenues for the business.

- Comparatively small peer group restricts relative valuation analysis A lack of direct competitors renders it difficult to calculate a fair value for N4, without using discounted cash flow modelling. There are several UK-listed reformulation businesses and vaccine delivery businesses, but owing to both the differences in product portfolios, and to both N4 and the peers generating nil or negligible revenues, any form of relative valuation analysis is largely pointless. For the reformulation business at least, we have demonstrated though DCF analysis that the product portfolio – even after very conservatively assuming that four of the five products each only stand a one in twenty chance of being successfully commercialised, and the fifth a one in ten chance – is being valued at a small fraction of its worth.

- Poor broking and promotion of stock

We have read only one significant research report on N4, namely the initiation note published in February 2017 by the Company’s Nomad, Stockdale Securities Plc. In our opinion, the note failed to clearly explain the Company’s intended business model. More importantly, it failed to demonstrate the blue-sky potential value of N4’s product portfolio. We believe that the Nomad’s and broker’s sales teams were thus ill-equipped to really promote the N4 story at the time of the RTO and fundraise. Given the valuations we have portrayed in this note, we find it almost unforgiveable that professional fundraisers were only able to raise fresh equity at a pre-new money valuation of only £3.5m.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 15 of 16

- Short term outlook of majority of AIM focussed investors The £1.50m equity placing at the time of the reverse takeover was achieved at a price of 7.0p per share. Additionally, placing warrants were issued on a one for one basis at an exercise price of 8.50p. We feel that a number of the placees might have taken profits in the weeks after relisting, when the share price rallied to 12p+. We believe that the selling by placees might have continued to even below the placing price, given that the warrants offer cheap access to any upside for a period of two years. It also appears that a number of investors have become increasingly concerned by the length of time that it will take for N4’s reformulated drugs to reach commercialisation. This was evinced in the selloff last week, following the announcement that the Pilot trials for sildenafil will not take place until early next year, and that following that larger scale human trials will take a further 18 months. Unfortunately this short termist outlook is becoming increasingly synonymous with AIM, and there is little one can do to escape it. The positive to be taken is that the impatience of some existing investors grants others the opportunity to acquire shares at an astonishingly cheap price.

- Distressed / legacy seller? Over the course of July, N4’s share price has crashed by circa 50%. Whilst the aforementioned panic over time-to-market for the sildenafil product was evidently a partial cause of the sell-off, we do not think that that was the only catalyst. Given the selling pressure over the past four weeks, we are of the opinion that a distressed seller is or has been at work.

Our mitigating factor in this instance is extremely basic: at some point, the seller will clear. When that occurs, the share price will likely rebound very sharply. Until that moment arrives, the cheap entry price will remain.

- Concern over future financing of the business It appears that a number of market participants are concerned that the Company will require additional funding in the near future. As is also synonymous with AIM, the thought of an equity placing has spooked both existing shareholders and prospective investors alike. We find this funding concern strange, given that N4 raised £1.5m only three months ago, took over a listed shell that already had £0.4m of cash in it, and has subsequently received £0.24m of additional cash through the exercise of warrants. Moreover, a Nomad requires that a business listing on AIM must have at least 12 months of sufficient working capital (12 months under AIM rules; but in practise Nomads in fact require 18 months from their clients). Going forward, the Company has access to cash of up to £1.82m via the exercise of warrants at 8.50p. As we have previously indicated, there is also the prospect of Nuvec generating income within six to twelve months. It is also worth re-iterating at this point the CEO’s significant shareholding, and his likely unwillingness to dilute his holding at such a suppressed valuation.

AIM CHAOS

@AIM_Chaos [email protected]

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. Investment ideas

shared are neither solicitations to buy nor offers to sell securities to 3rd parties.

N4 Pharma Plc 31 July 2017

Page 16 of 16

Disclosure

AIM Chaos is the research branch of a private investment vehicle named Sons of Ulster. It is responsible for generating investment ideas and subsequently monitoring held investments. The assembled information disseminated in this report is intended for internal use, and is neither a solicitation to buy nor an offer to sell securities to outside parties. All information collated and utilised in this report has been sourced from the public domain. AIM Chaos has no business relationship with N4 Pharma Plc or with any other company referred to in this report, and has received no compensation from any party for writing this report. Sons of Ulster, which wholly owns AIM Chaos, does currently hold shares in N4 Pharma Plc. Consequently this report should not be regarded as independent research.