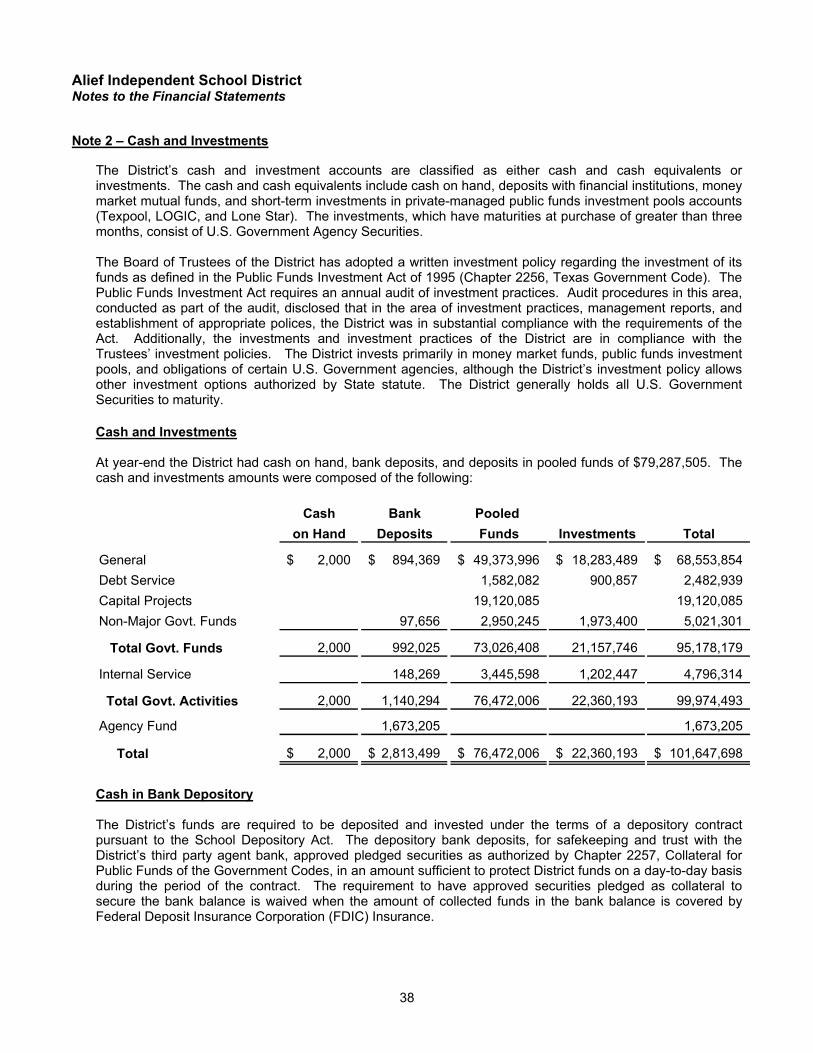

alief independent school district · alief independent school district has a population of...

TRANSCRIPT

Alief Independent School District – 12302 High Star – Houston, TX 77072

Alief Independent School District

Comprehensive Annual Financial Report

For the Year Ended August 31, 2003

Prepared by the Administrative Service Division: Johnny Tates

Deputy Superintendent for Administration Deanna Wentz, CPA

Assistant Superintendent for Finance Anne Faichtinger, CPA

Controller Julee Patterson, CPA

Accountant

Alief Independent School District Comprehensive Annual Financial Report

For the Year Ended August 31, 2003 Table of Contents

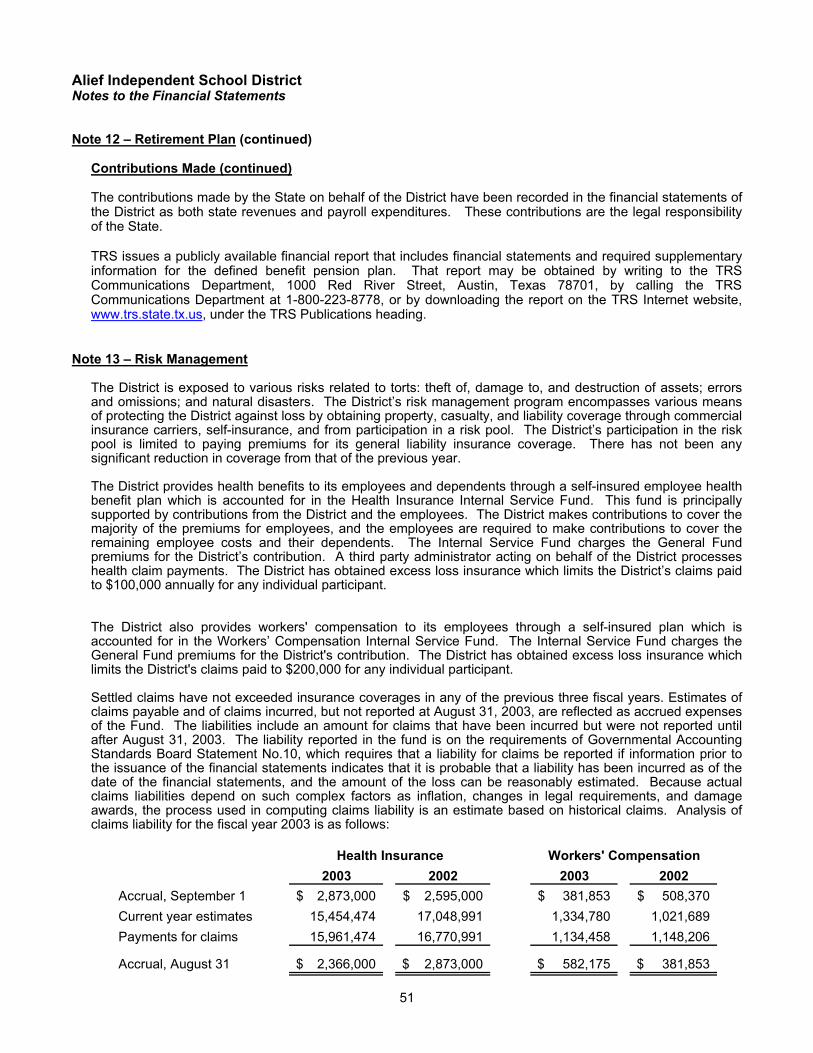

Exhibit Page

Introductory Section Title Page Table of Contents Principal Officials and Advisors 1 Organization Chart 2 Letter of Transmittal 3 Certificate of Achievement for Excellence in Financial Reporting 8 Certificate of Excellence in Financial Reporting 9 Certificate of Board 10

Financial Section Independent Auditors' Report 11

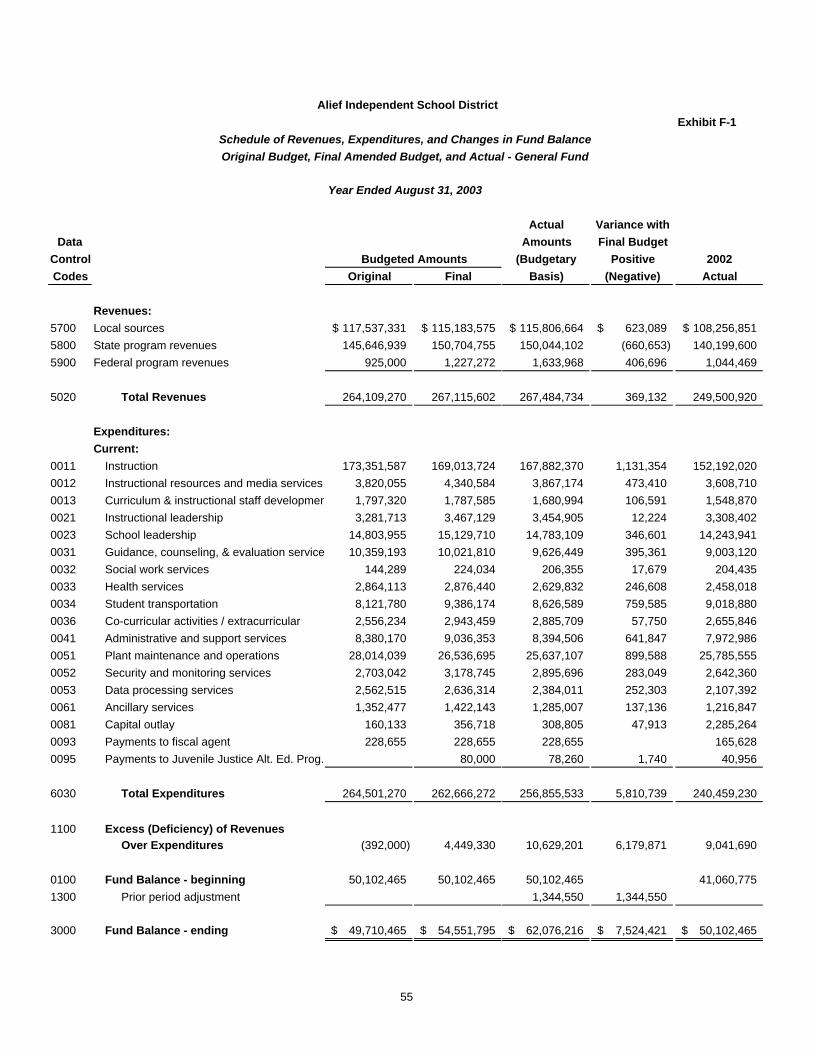

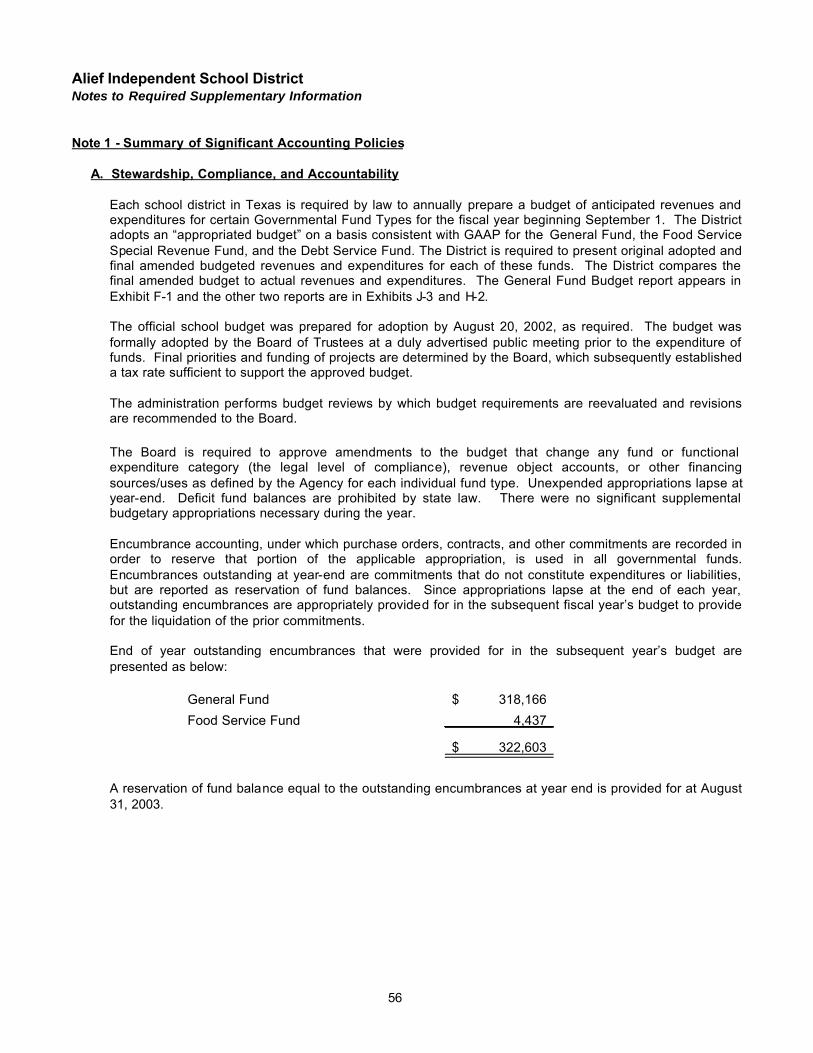

Management’s Discussion and Analysis 13 Basic Financial Statements Government-Wide Financial Statements Statement of Net Assets A-1 22 Statement of Activities B-1 23 Fund Financial Statements Governmental Funds Balance Sheet – Governmental Funds C-1 24 Reconciliation of the Governmental Funds Balance Sheet To the Statement of Net Assets C-2 25 Statement of Revenues, Expenditures, and Changes in Fund Balances – Governmental Funds C-3 26 Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities C-4 27 Proprietary Funds Statement of Net Assets – Proprietary Funds D-1 29 Statement of Revenues, Expenses, and Changes in Fund Net Assets - Proprietary Funds D-2 30 Statement of Cash Flows - Proprietary Funds D-3 31 Fiduciary Fund Statement of Assets and Liabilities E-1 32 Notes to Financial Statements 33 Required Supplementary Information: Schedule of Revenues, Expenditures, and Changes in Fund Balances - Original Budget, Amended Final, and Actual – General Fund F-1 55 Notes to Required Supplementary Information 56

Alief Independent School District

Comprehensive Annual Financial Report For the Year Ended August 31, 2003

Table of Contents

Exhibit Page

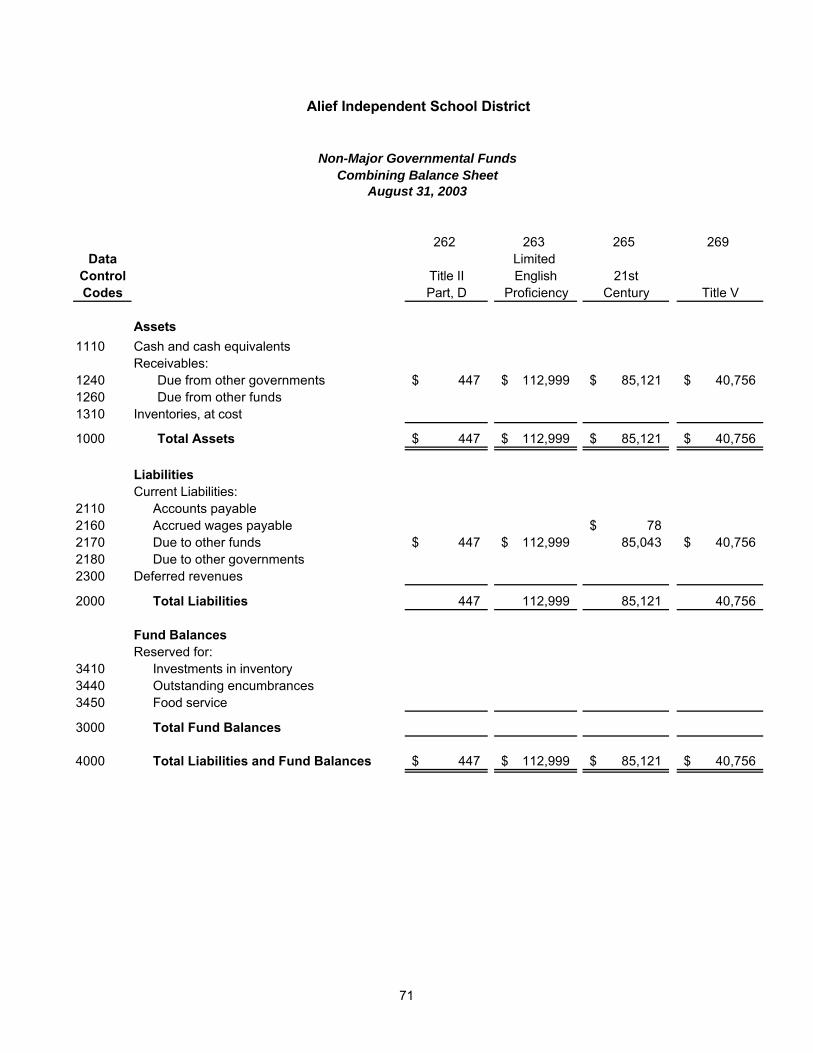

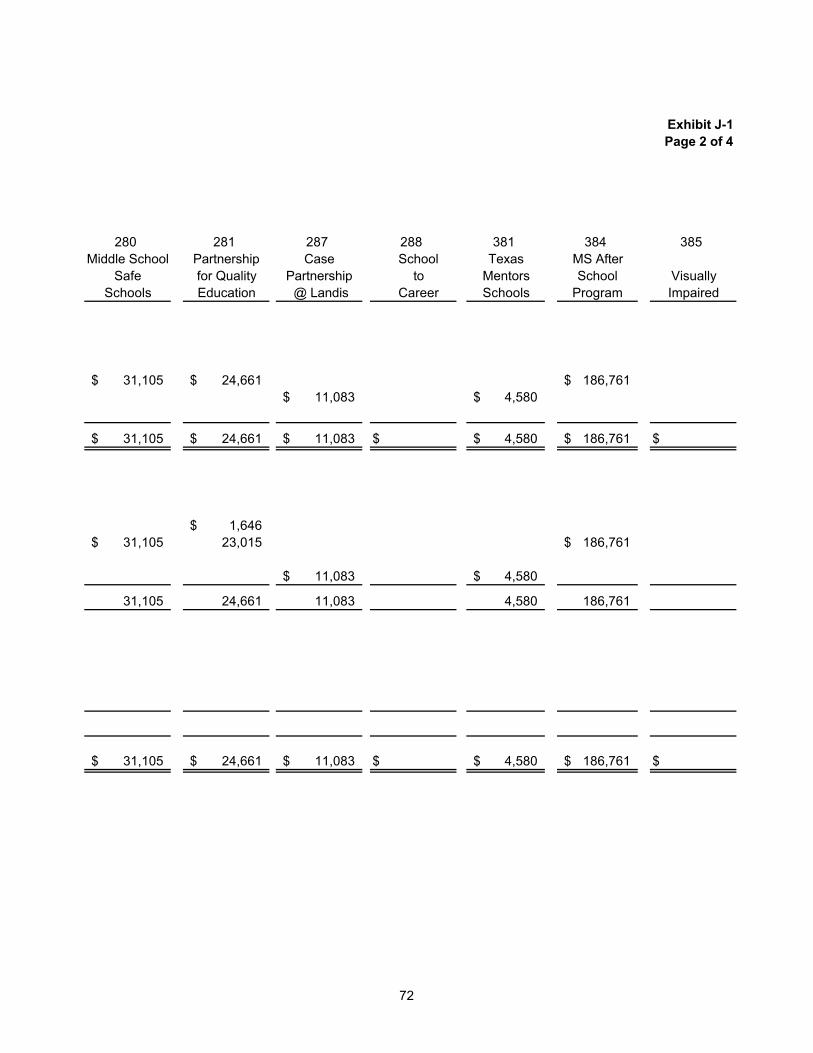

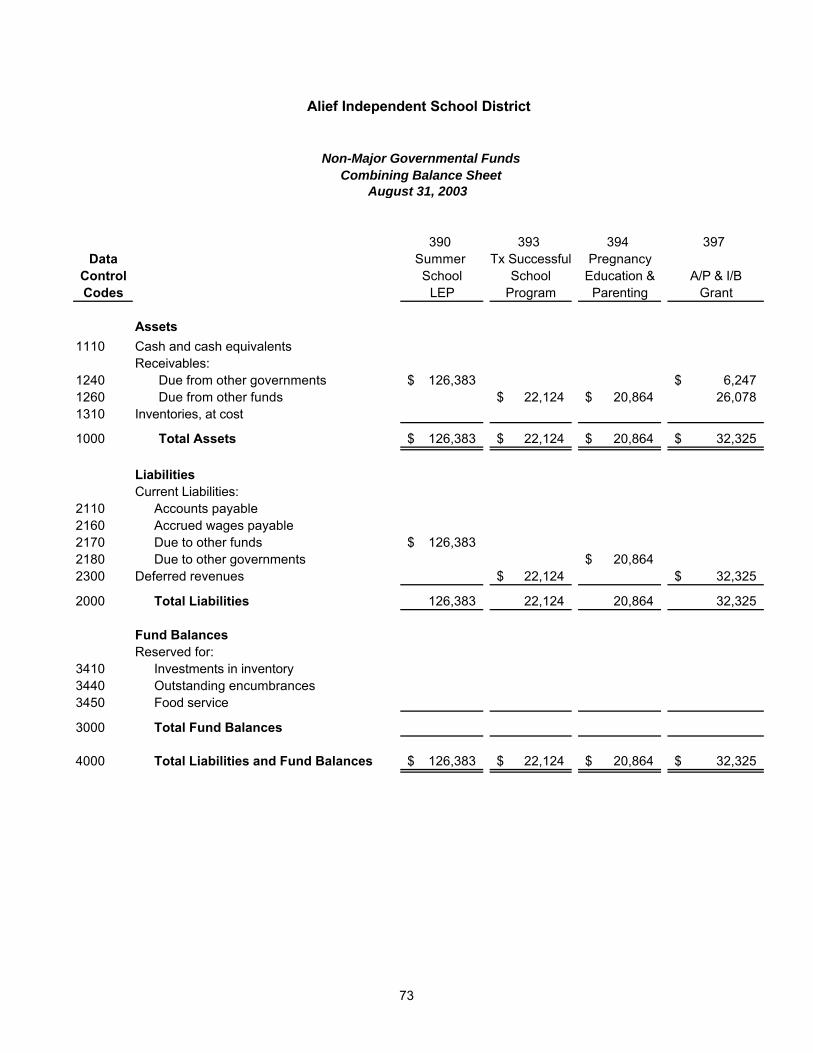

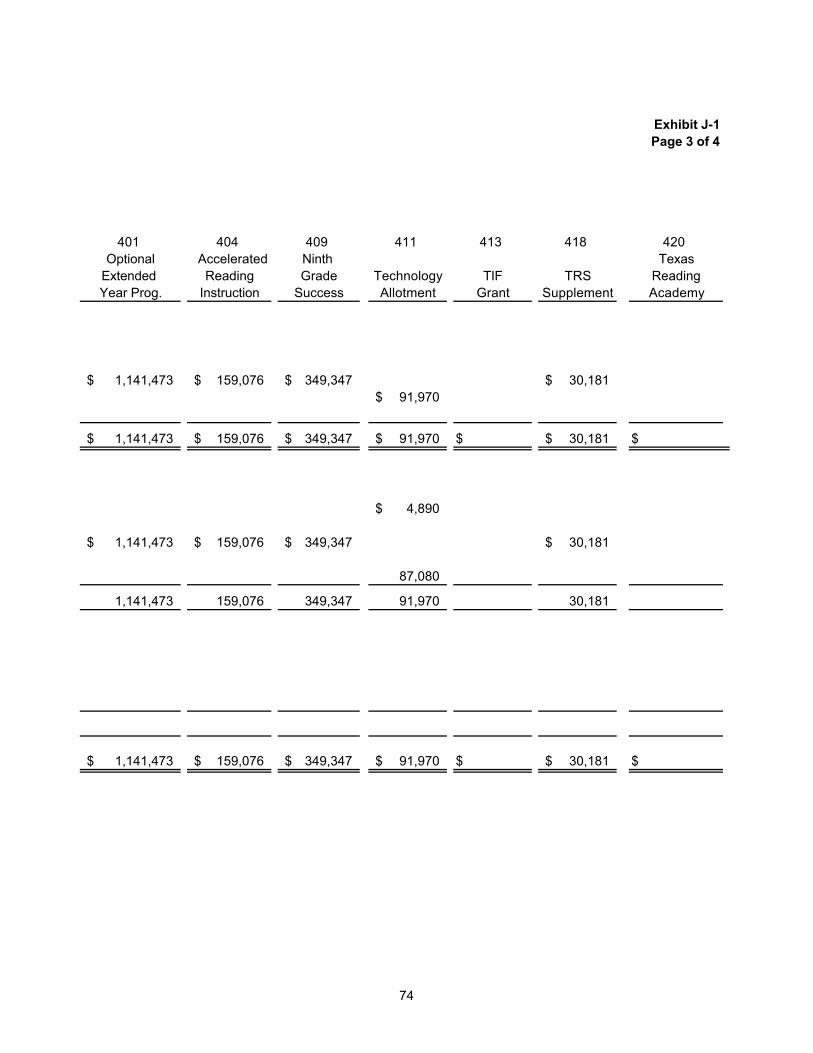

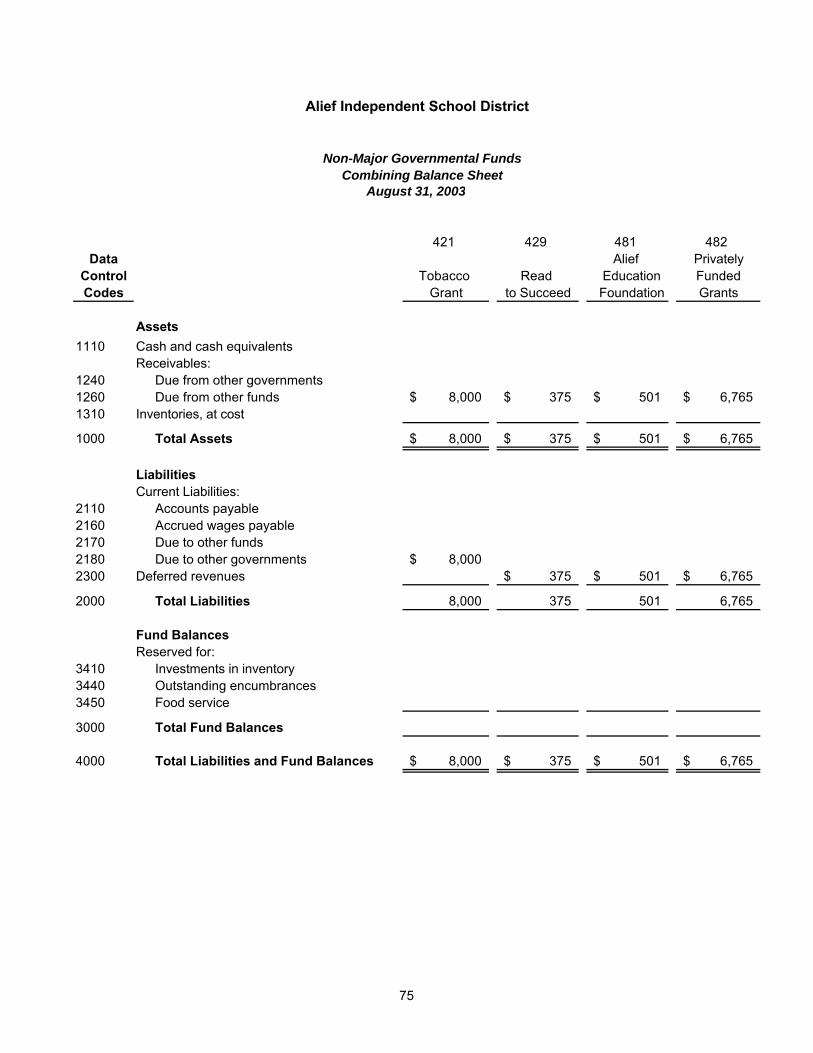

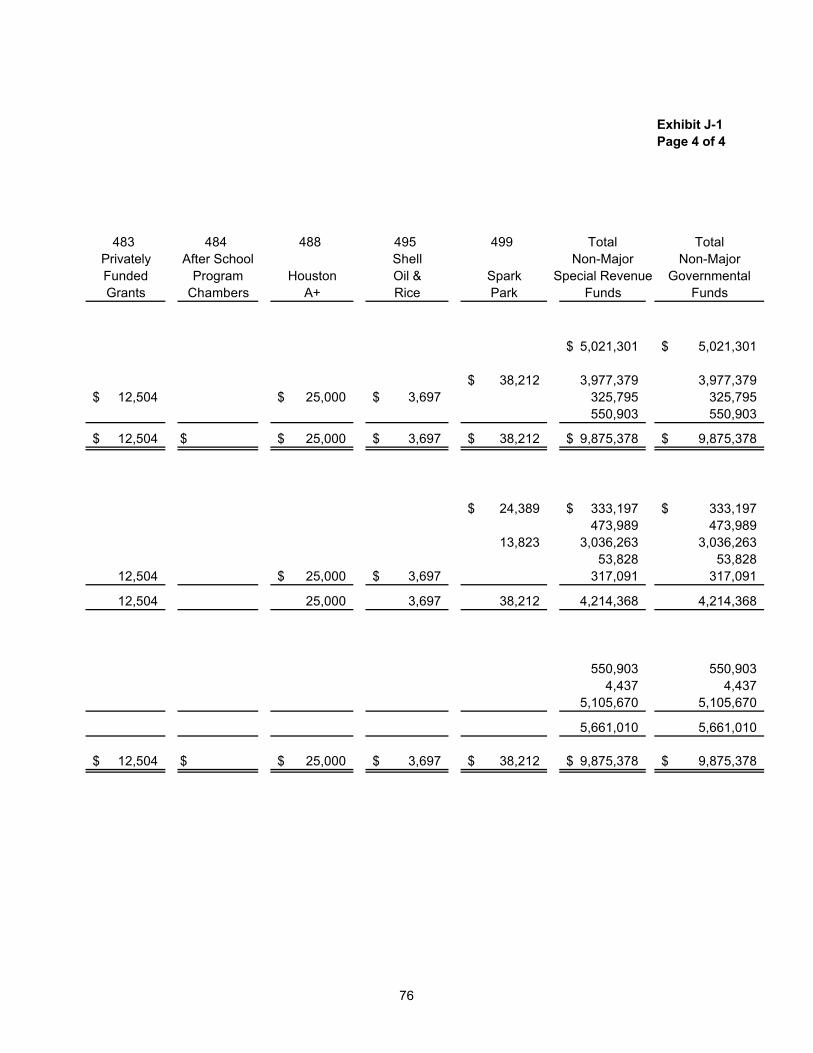

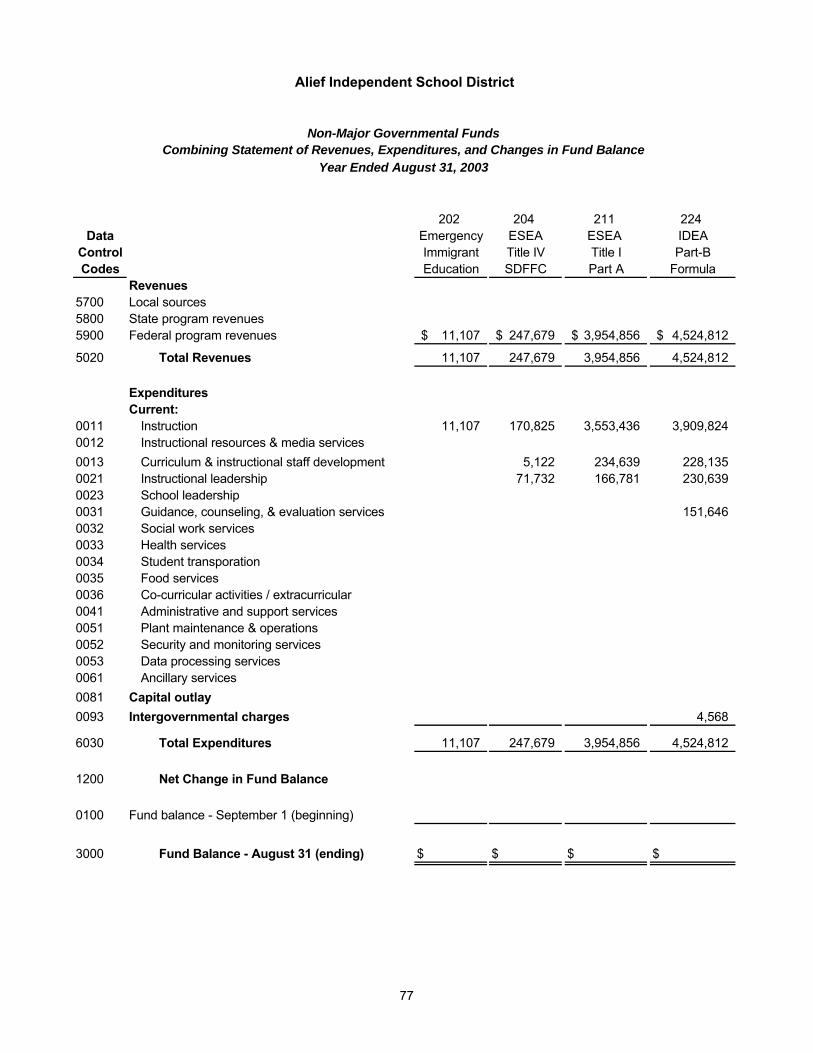

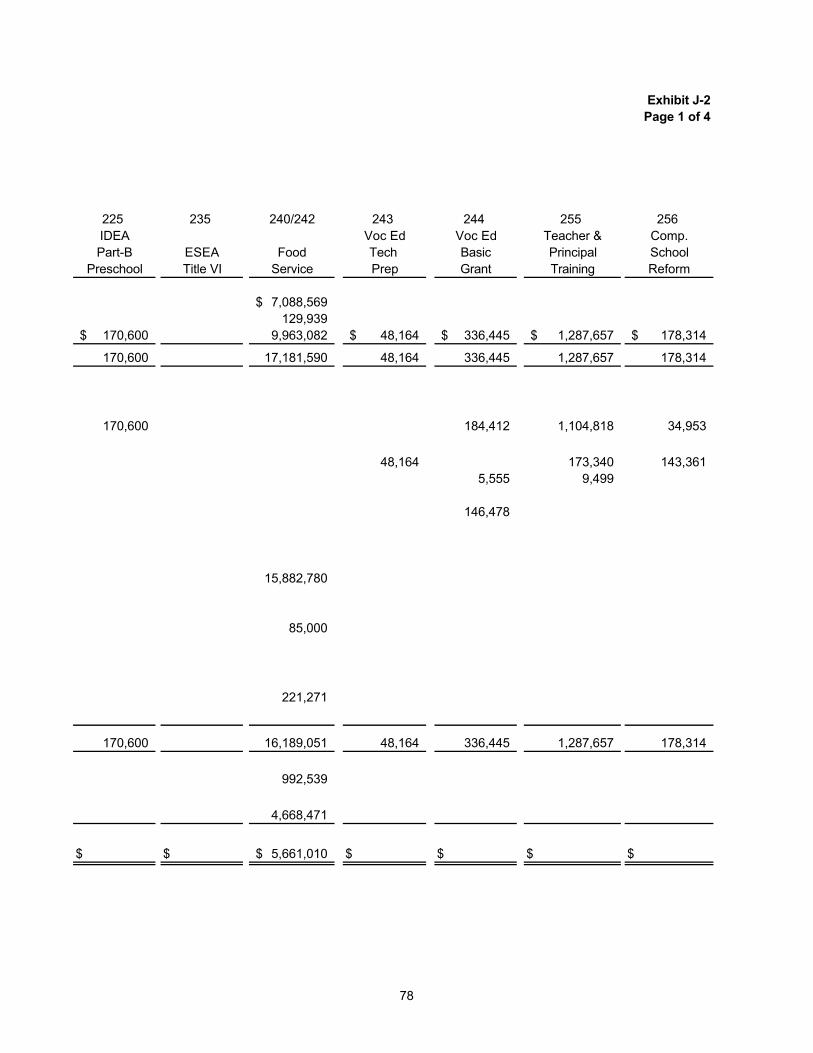

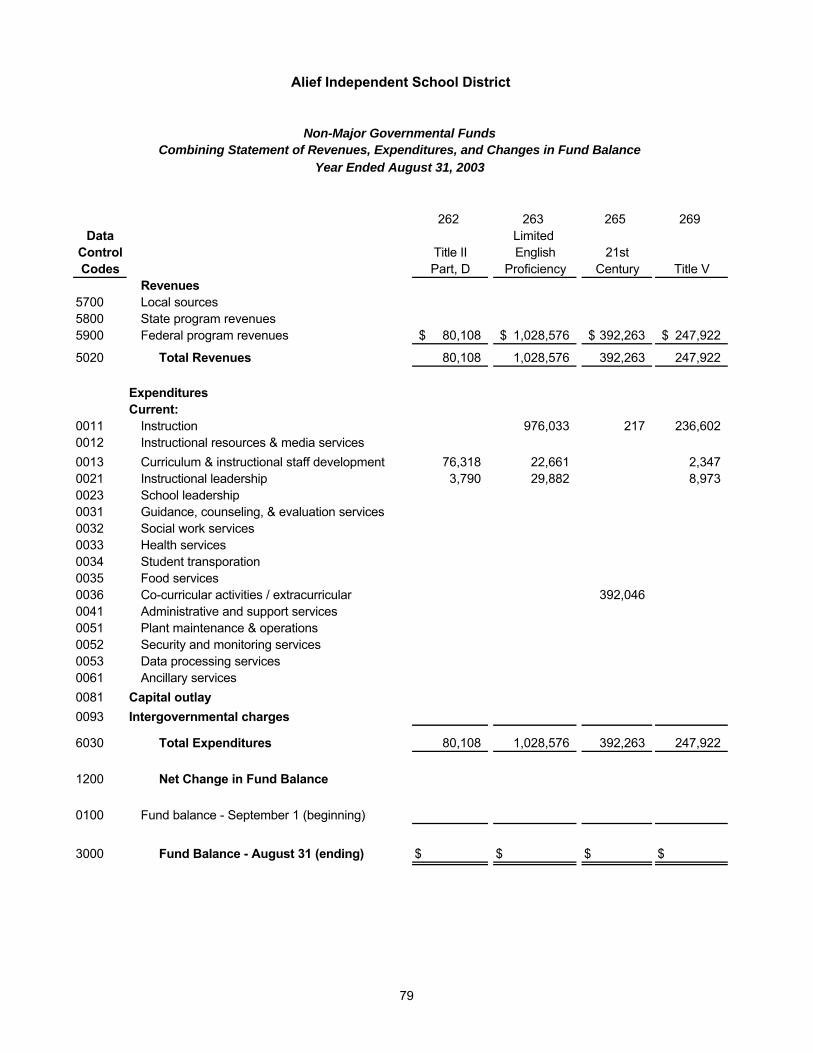

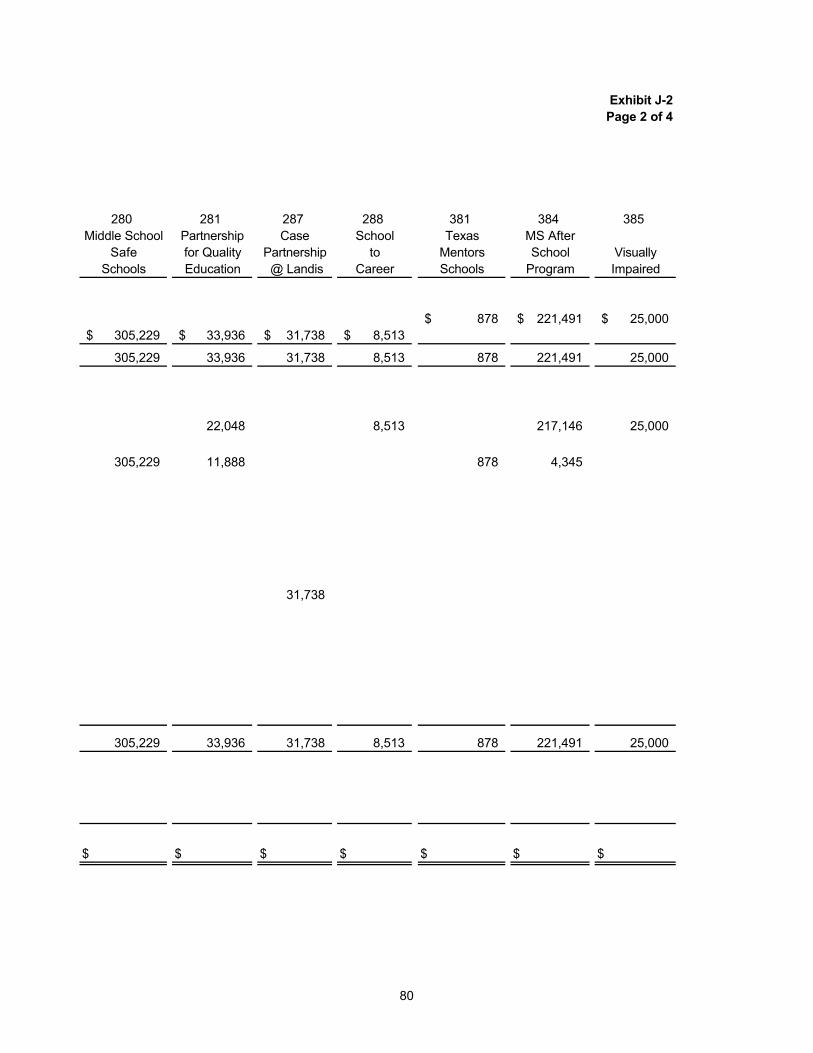

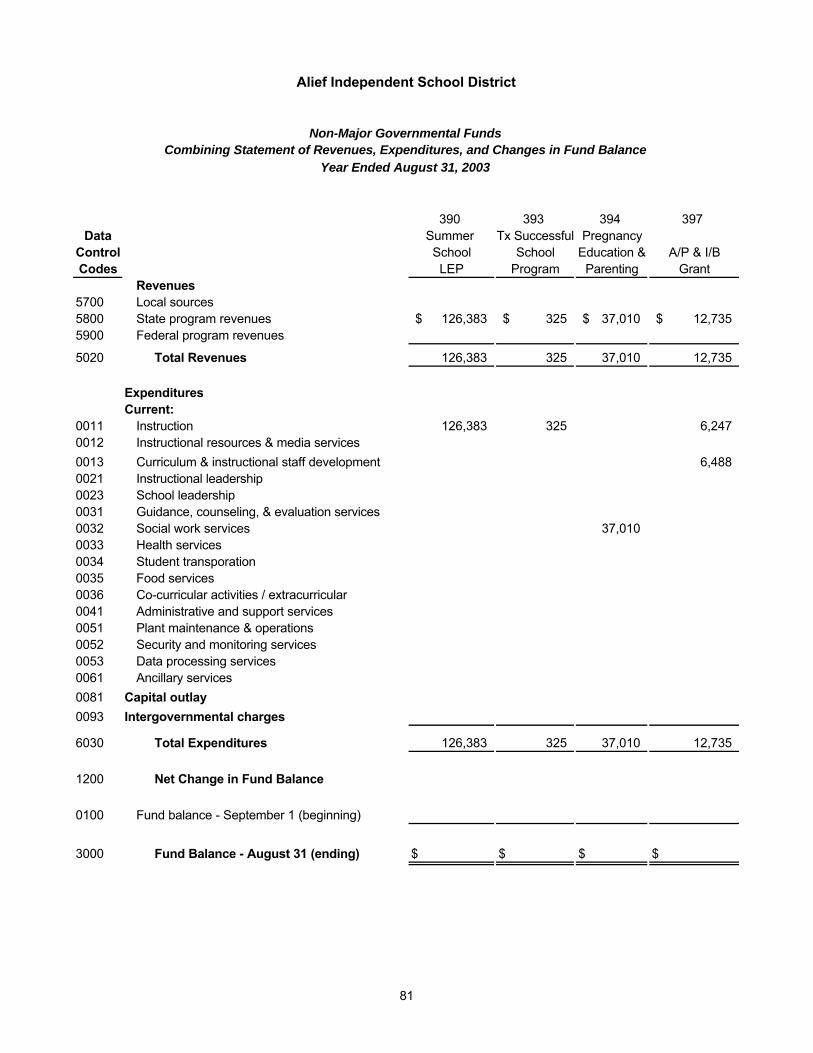

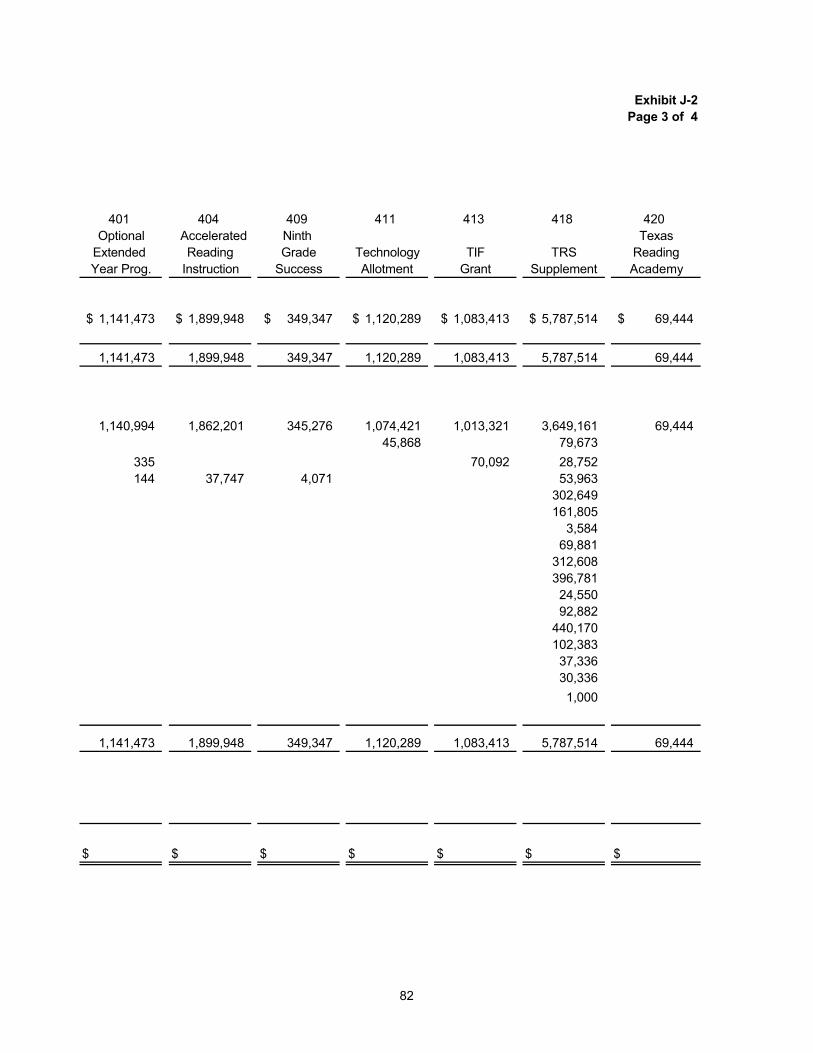

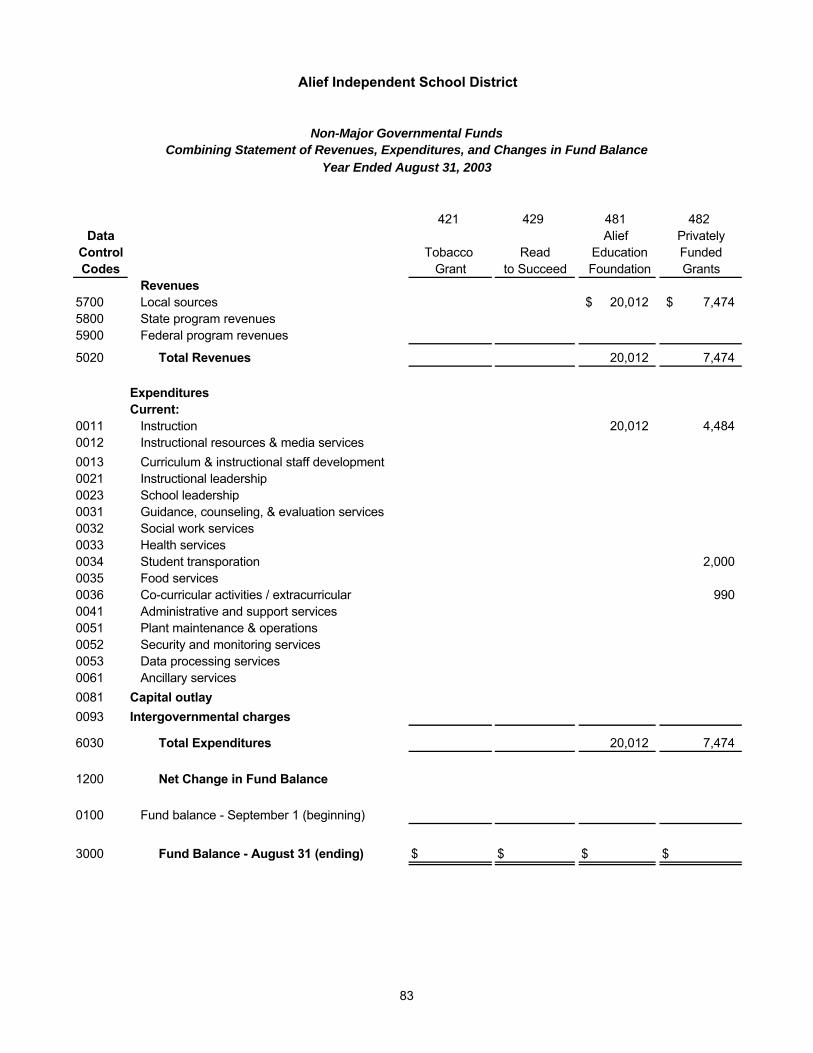

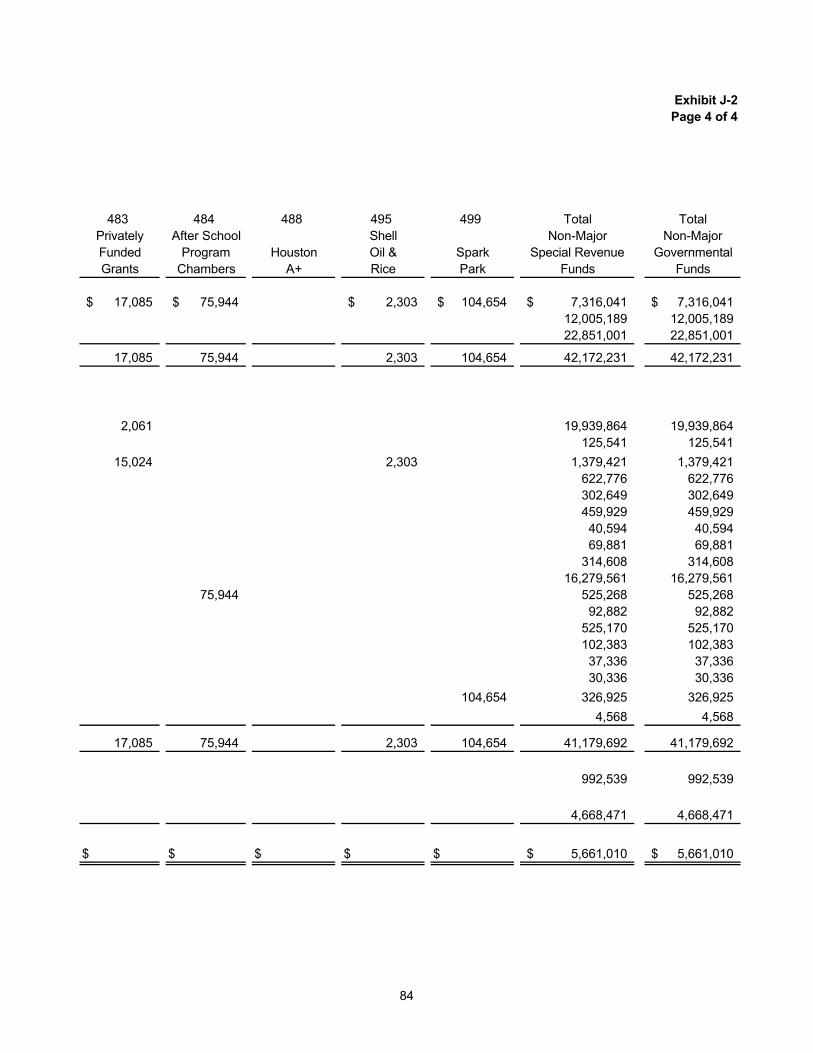

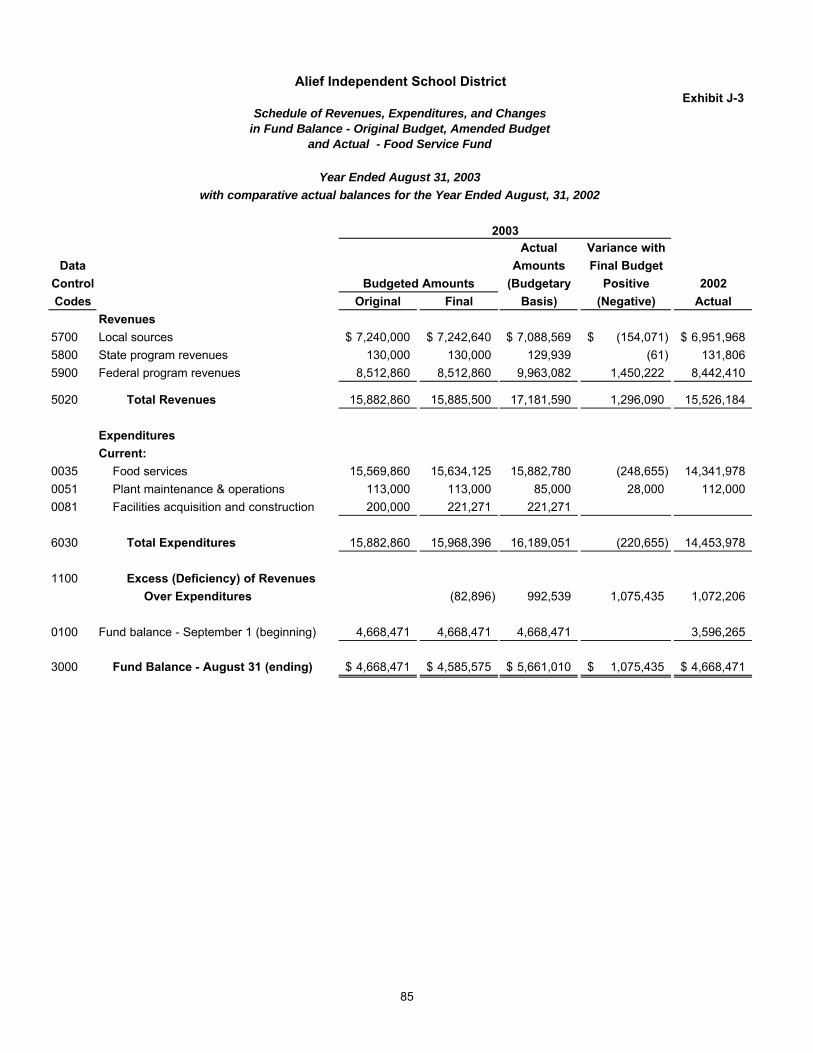

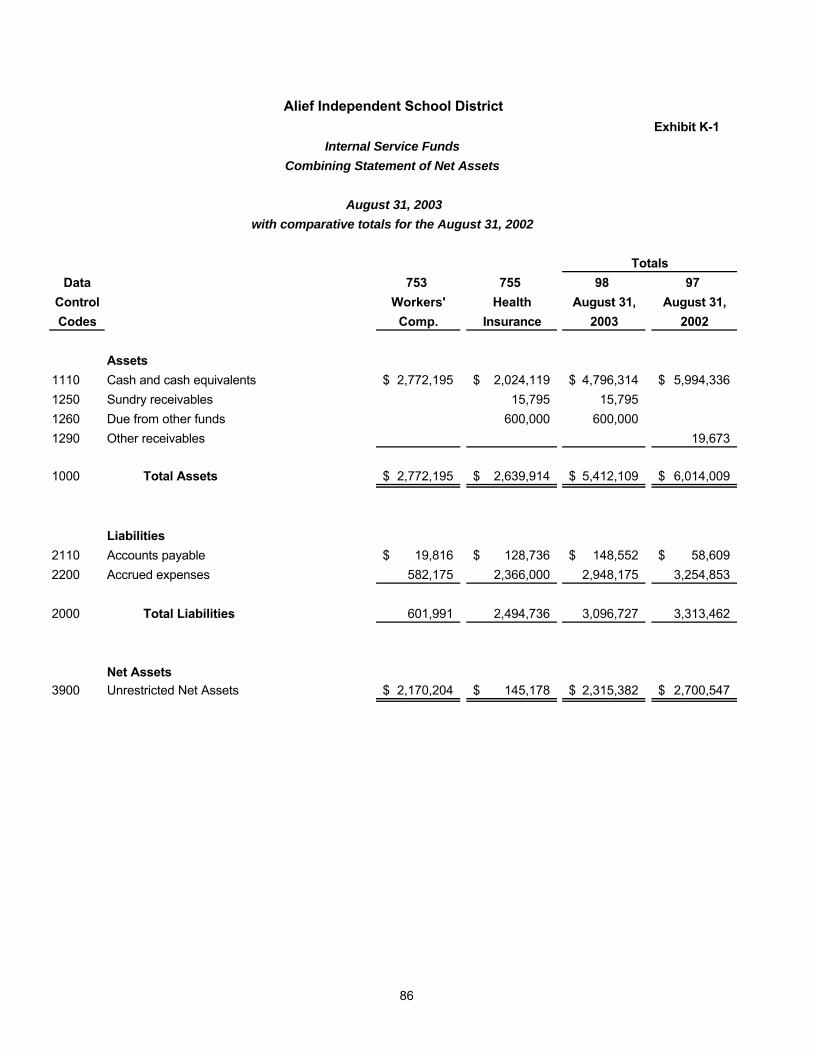

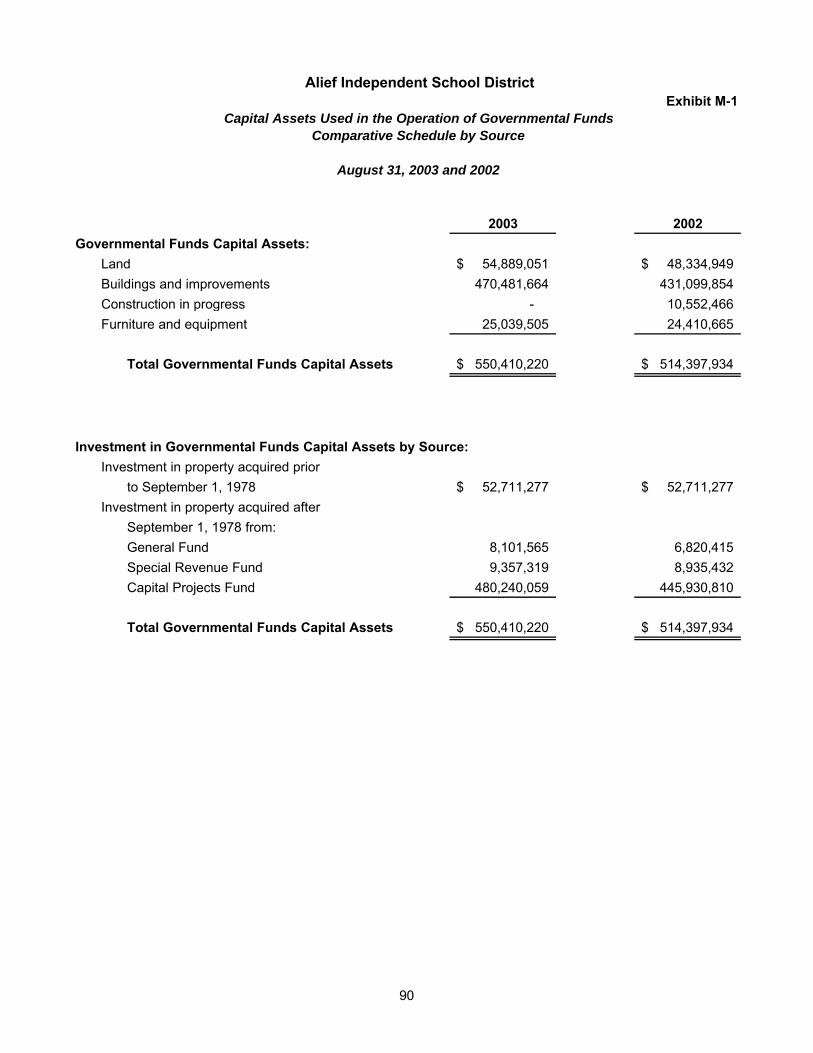

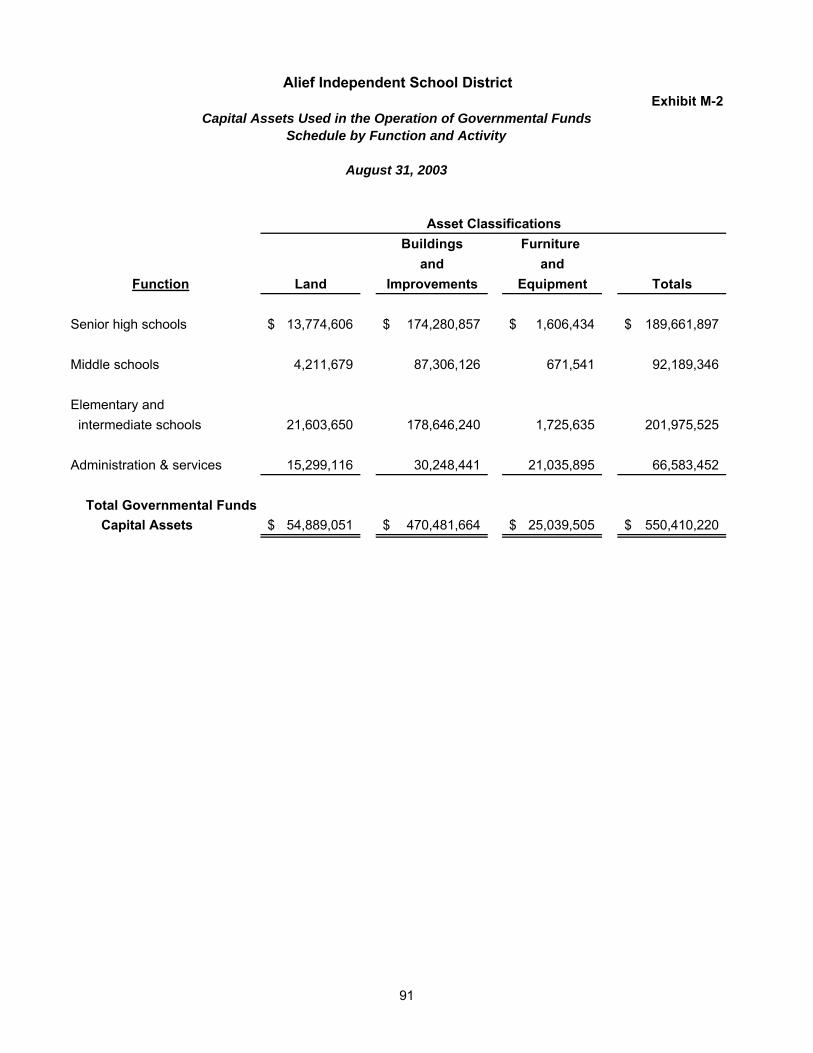

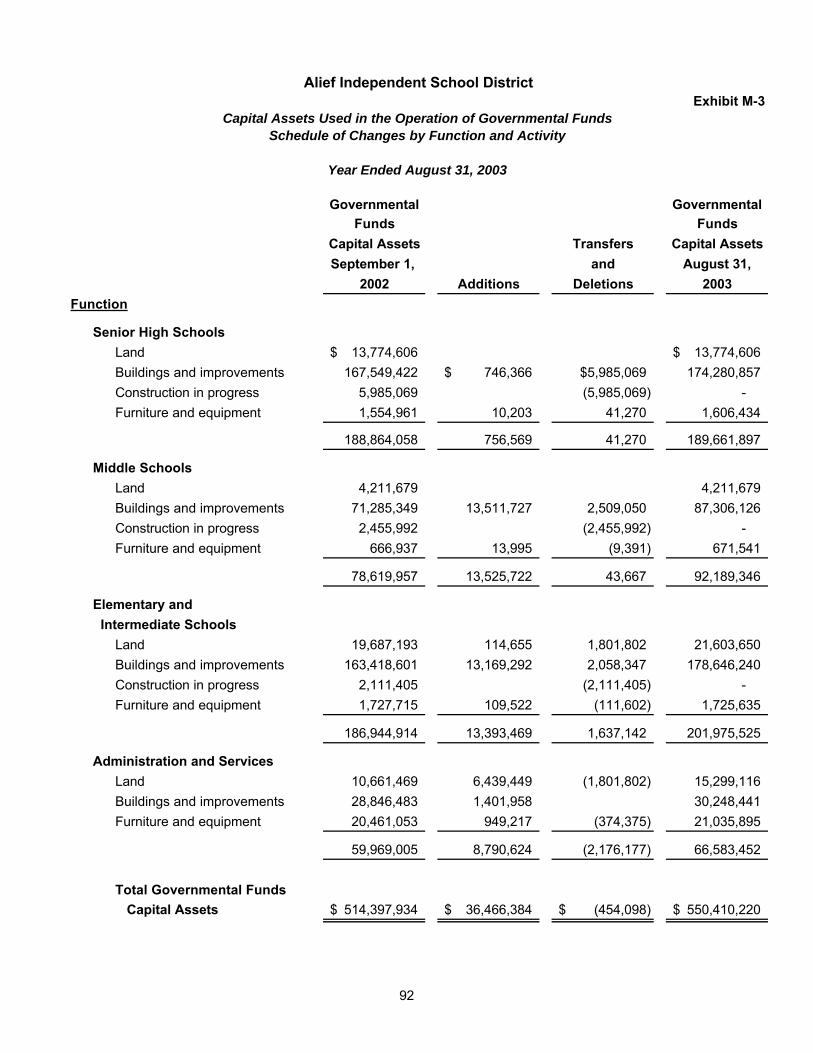

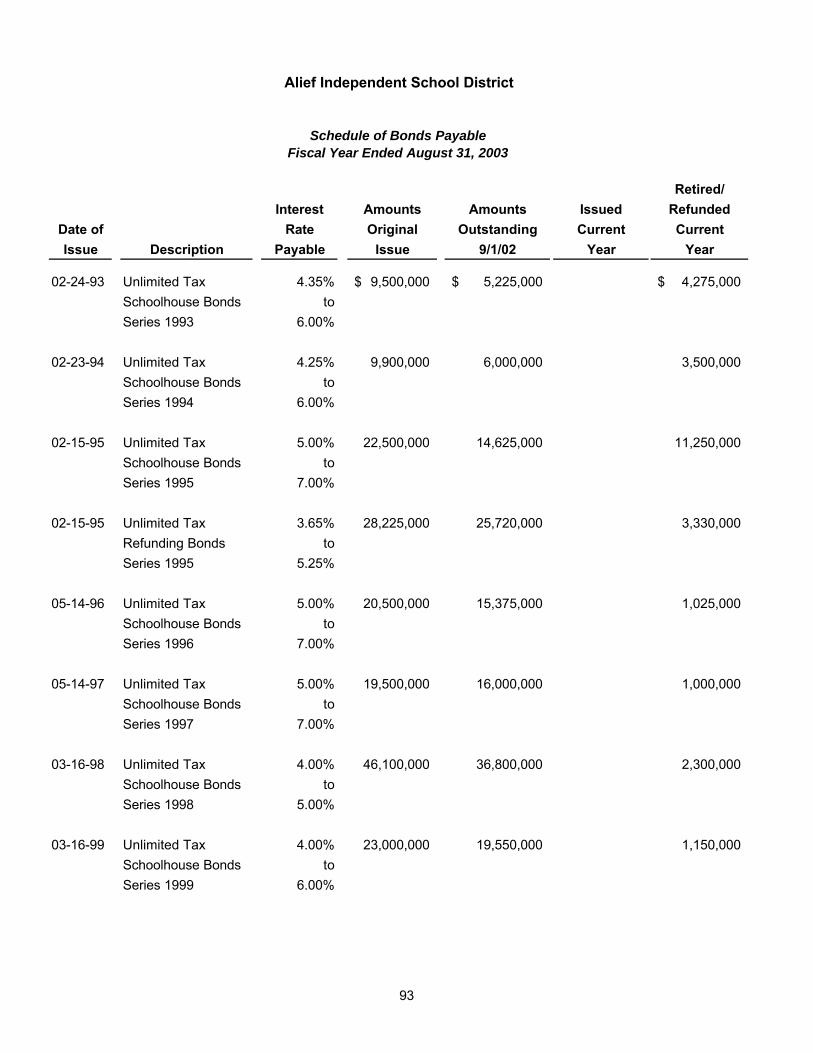

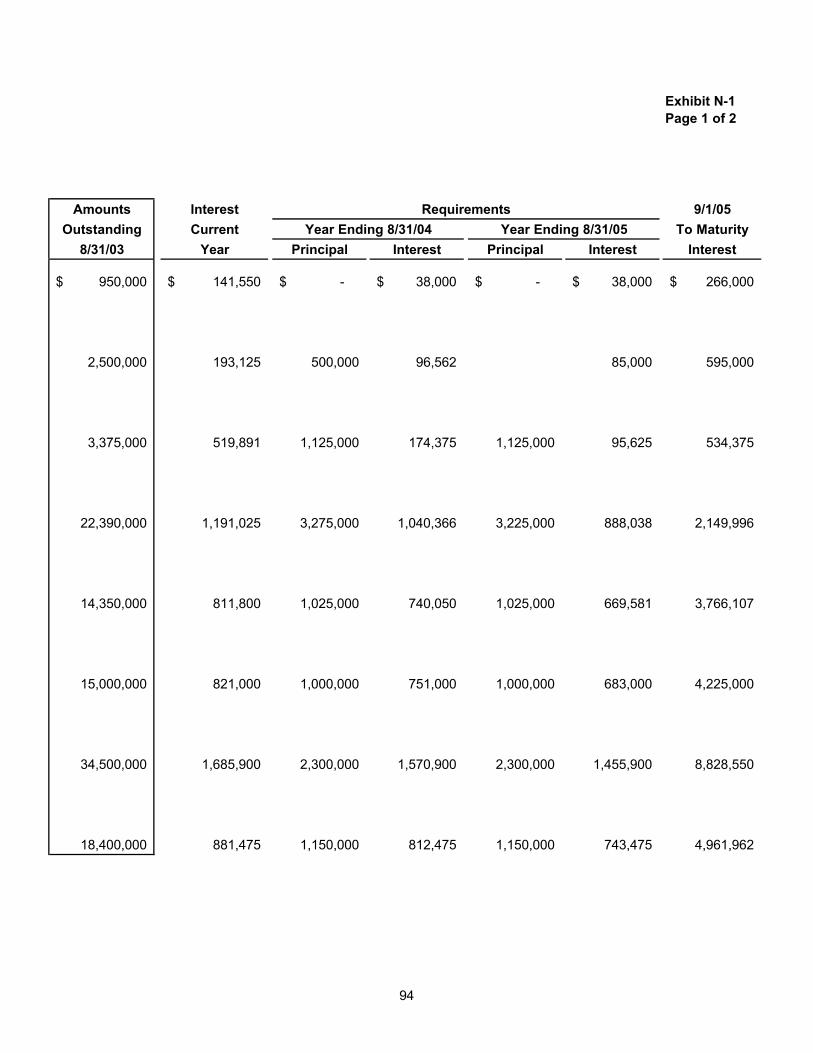

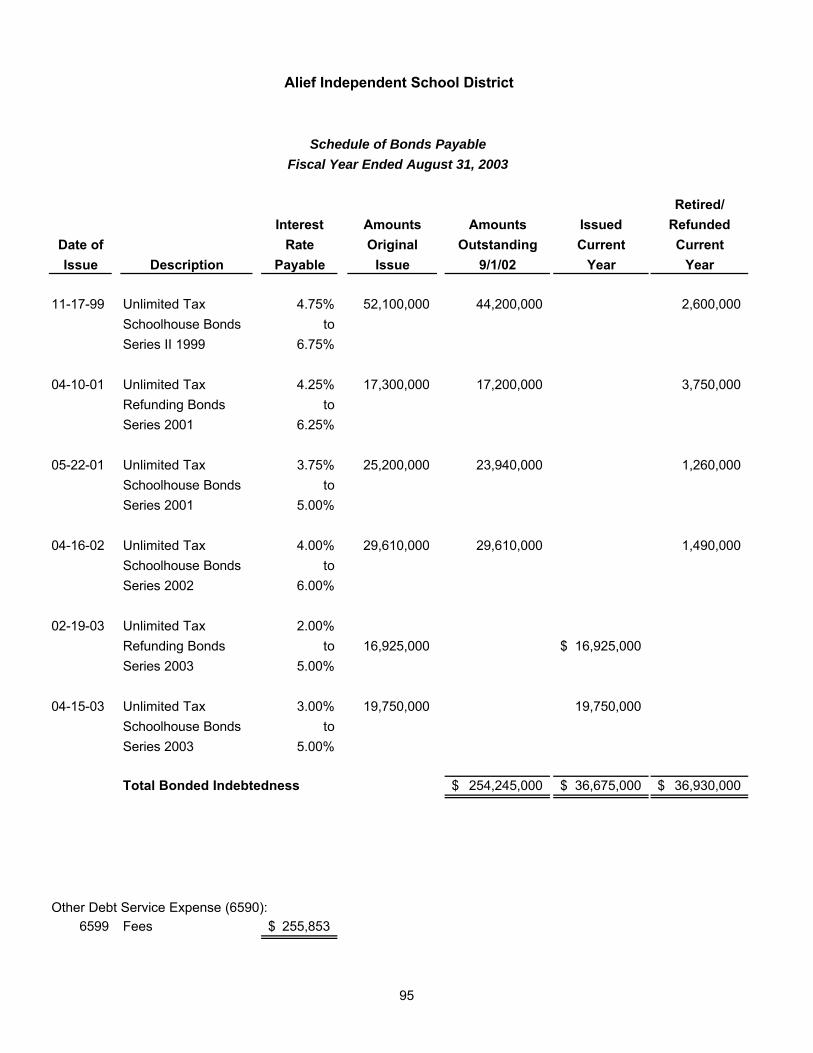

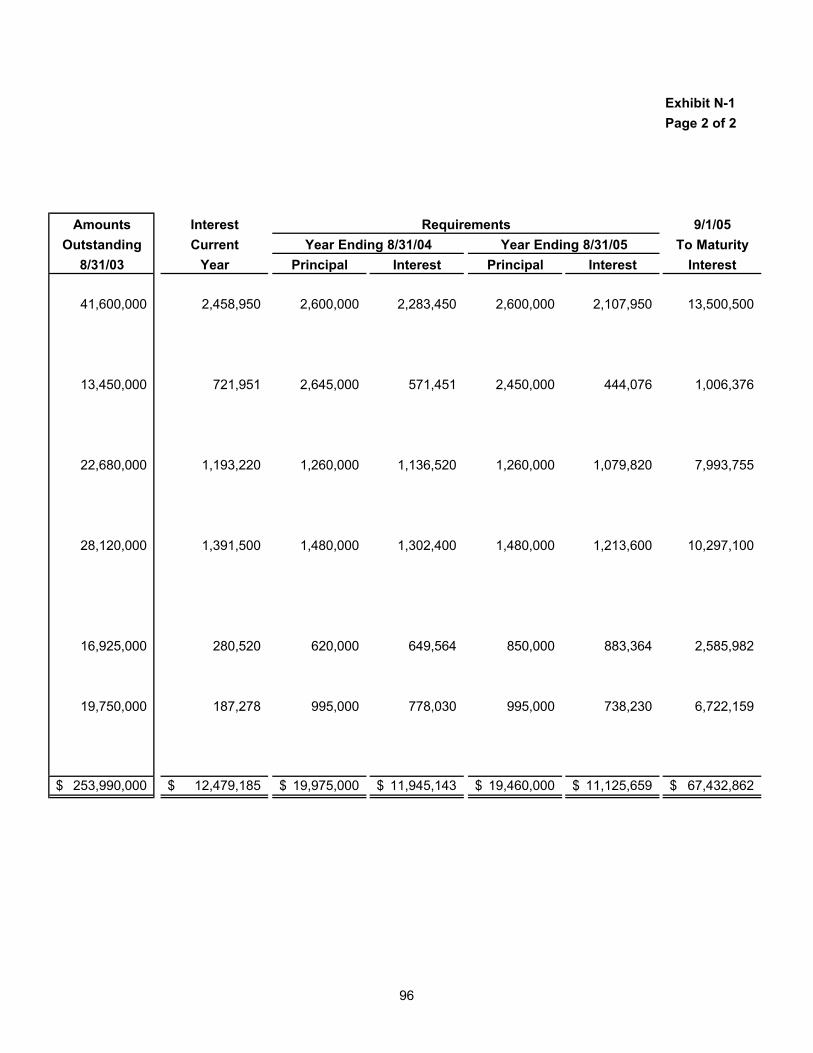

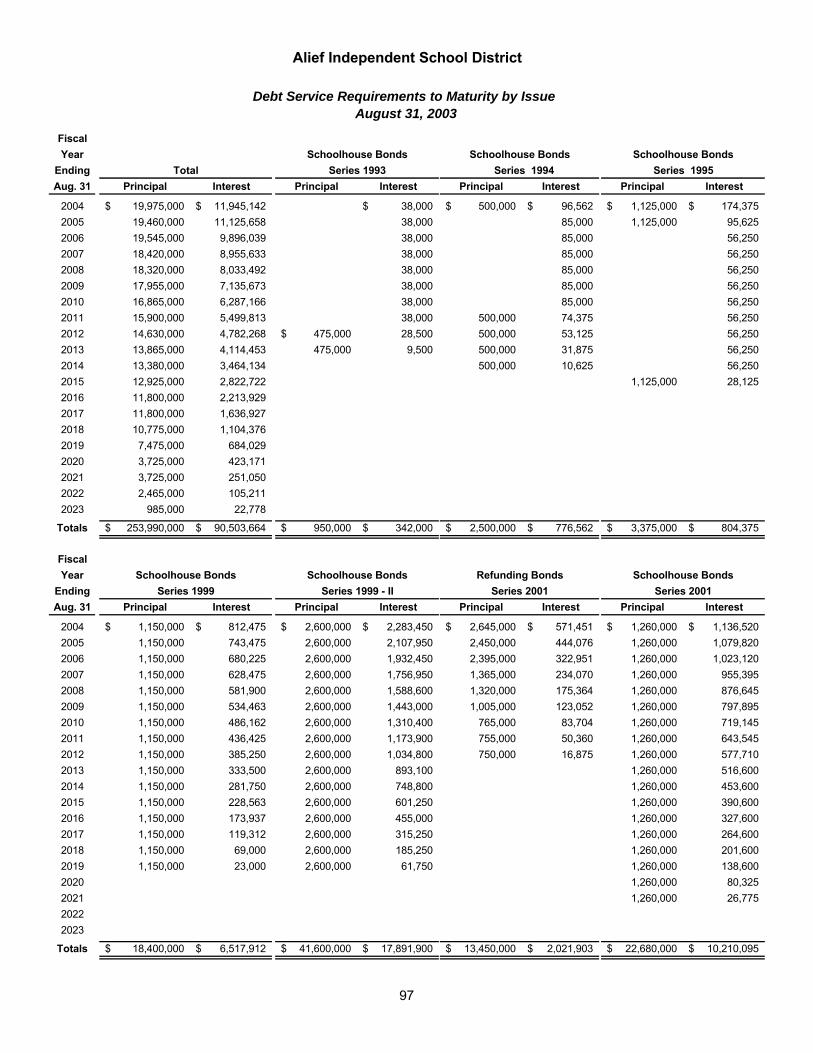

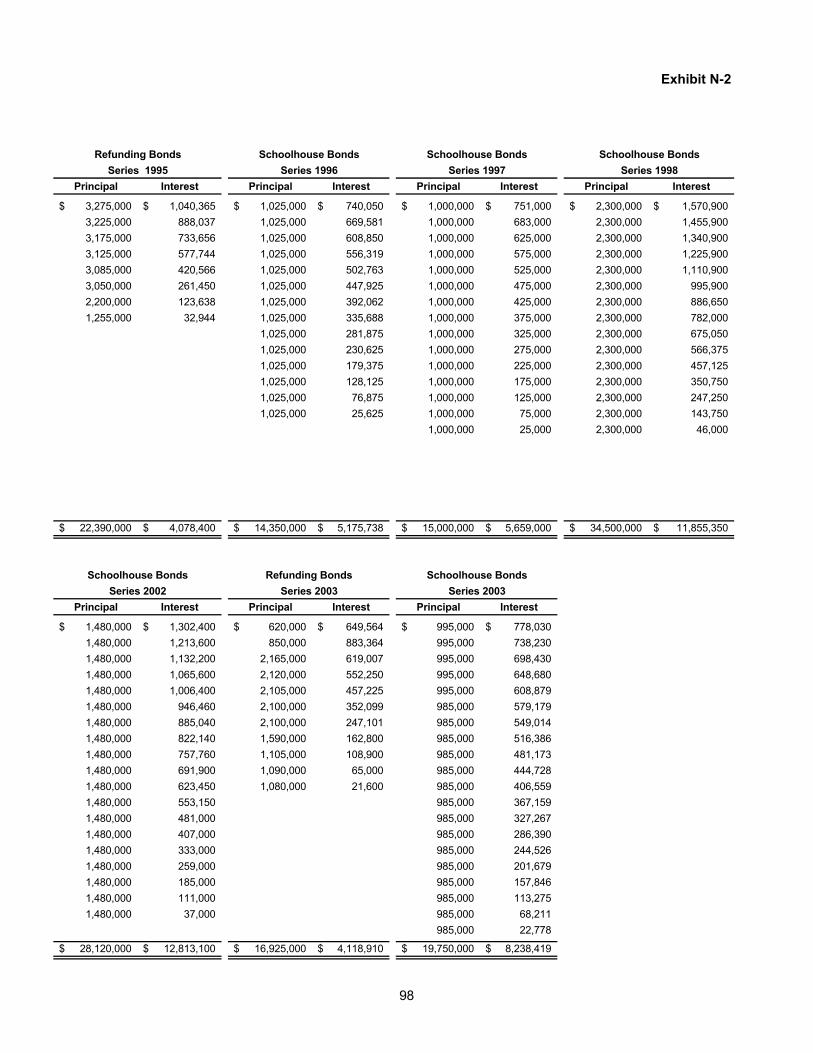

Financial Section (continued) Other Supplementary Information: Comparative Statements, Combining Statements, and Budget Comparisons: General Fund Comparative Balance Sheet G-1 57 Schedule of Revenues - Budget and Actual G-2 58 Schedule of Expenditures - Budget and Actual G-3 59 Debt Service Fund Comparative Balance Sheet H-1 65 Schedule of Revenues, Expenditures, and Changes in Fund Balance - Original Budget, Amended Budget, and Actual H-2 66 Capital Projects Fund Comparative Balance Sheet I-1 67 Comparative Schedule of Revenues, Expenditures, and Changes in Fund Balance I-2 68 Non-Major Governmental Funds Combining Balance Sheet J-1 69 Combining Statement of Revenues, Expenditures, and Changes in Fund Balance J-2 77 Schedule of Revenues, Expenditures, and Changes in Fund Balance – Original Budget, Amended Budget, and Actual – Food Service Fund J-3 85 Internal Service Funds Combining Statement of Net Assets K-1 86 Combining Statement of Revenues, Expenses, and Changes in Fund Net Assets K-2 87 Combining Statement of Cash Flows K-3 88 Agency Fund Statement of Changes in Assets and Liabilities L-1 89 Capital Assets Used in the Operation of Governmental Funds Comparative Schedule of General Fixed Assets by Source M-1 90 Schedule by Function and Activity M-2 91 Schedule of Changes by Function and Activity M-3 92 General Long-Term Debt on Governmental Funds Bond Schedule N-1 93 Debt Service Requirements to Maturity by Issue N-2 97

Alief Independent School District Comprehensive Annual Financial Report

For the Year Ended August 31, 2003 Table of Contents

Exhibit Page

Financial Section (continued)

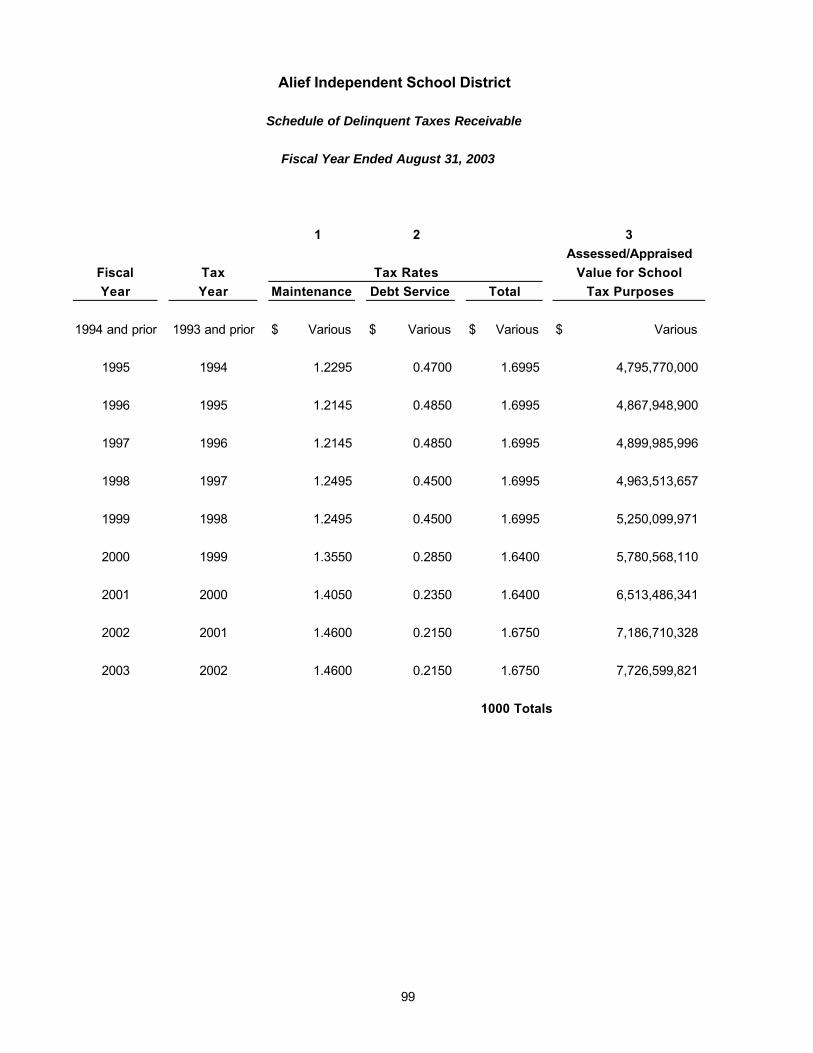

Other Supplementary Information (continued): Compliance Schedules Schedule of Delinquent Taxes Receivable O-1 99 Schedule of Expenditures for Computation of Indirect Costs for 2004-05 O-2 101 Fund Balance and Cash Flow Calculation Worksheet (Unaudited) - General Fund O-3 103

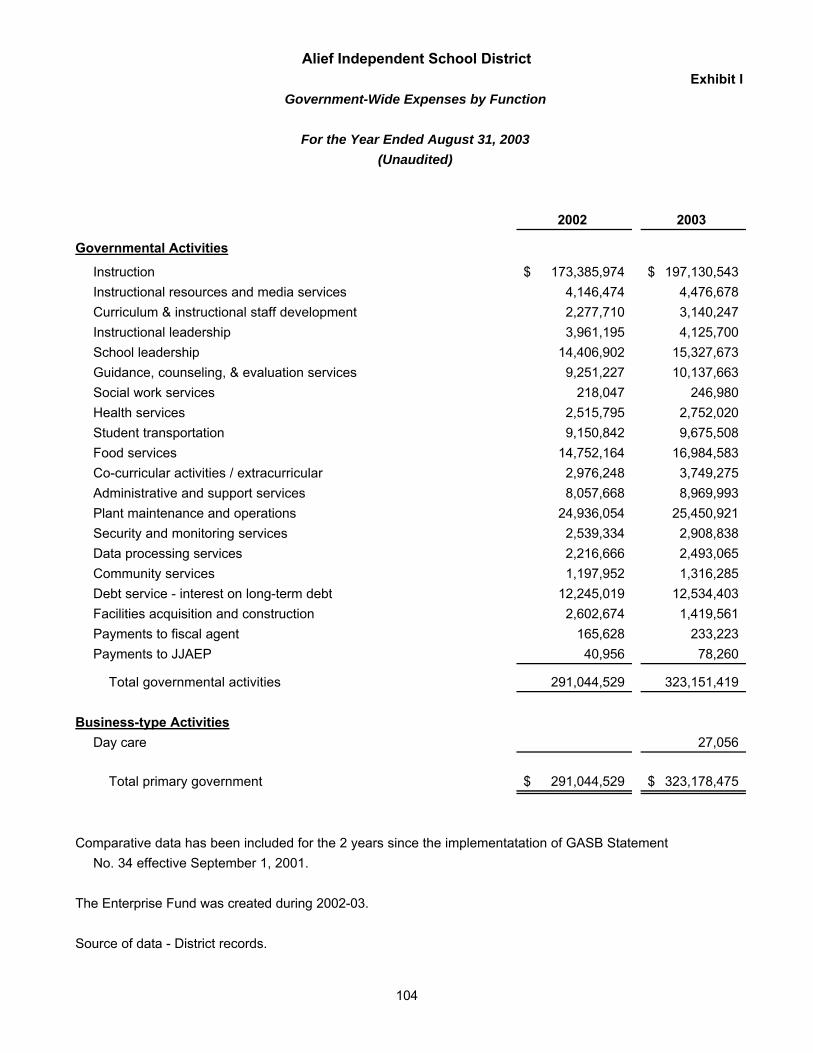

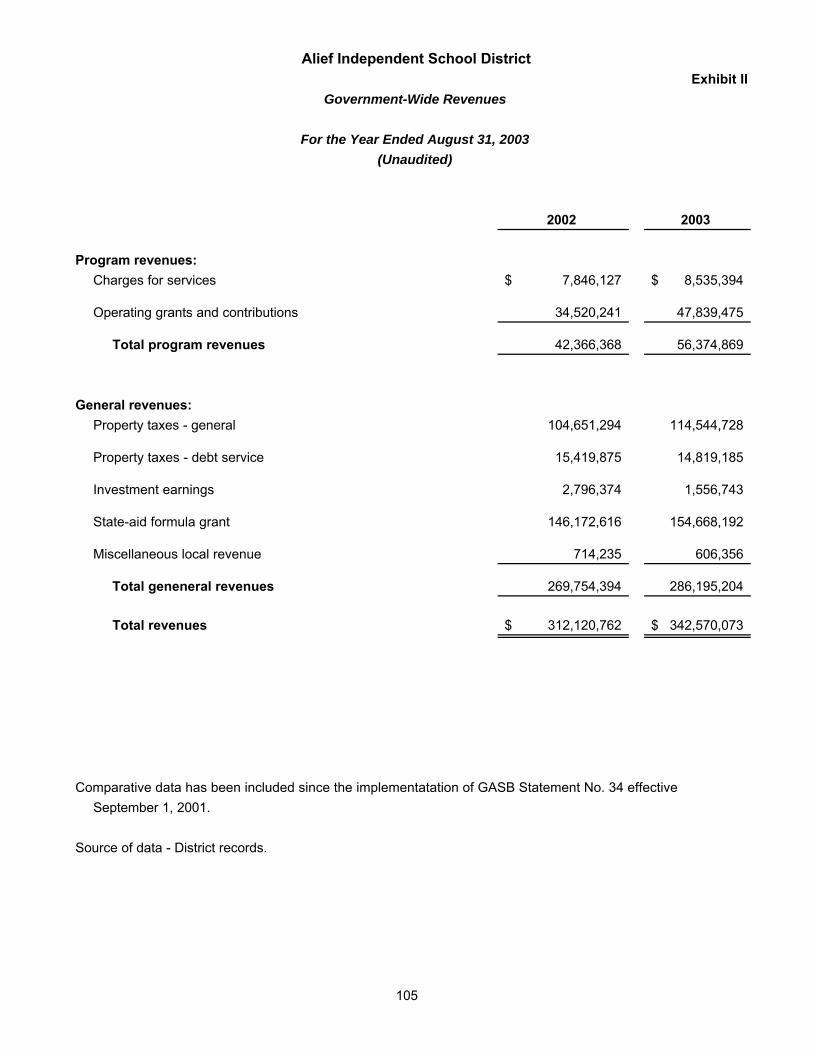

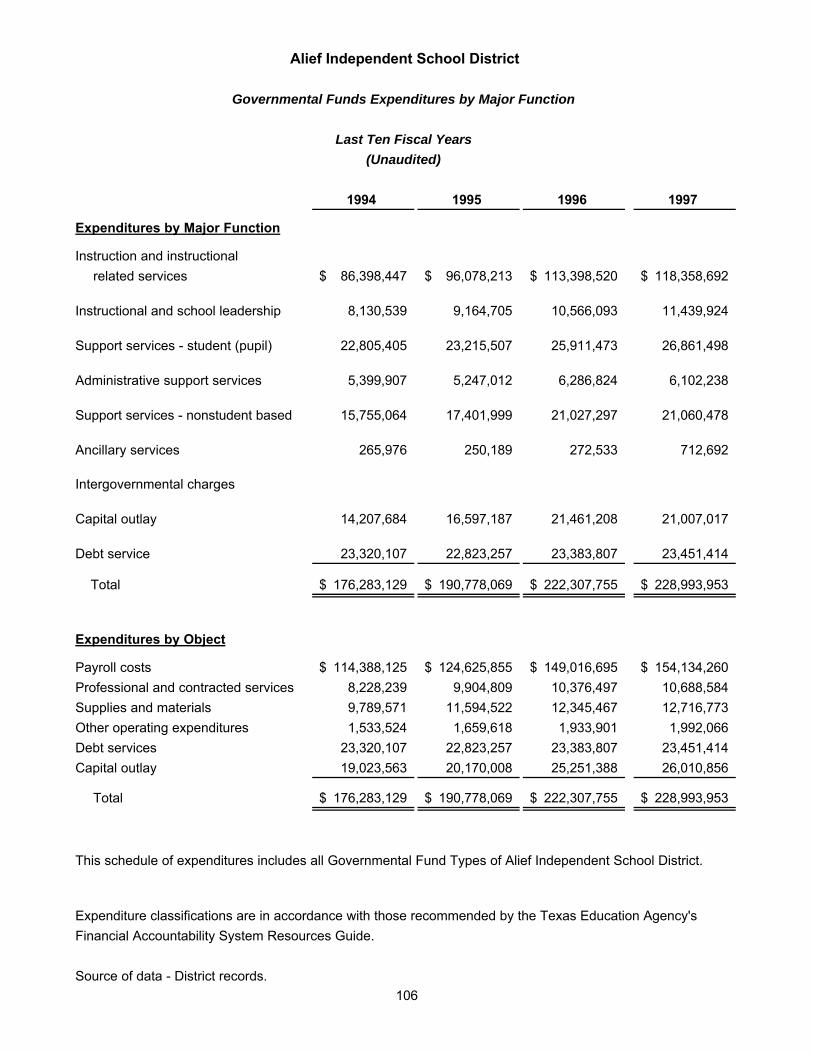

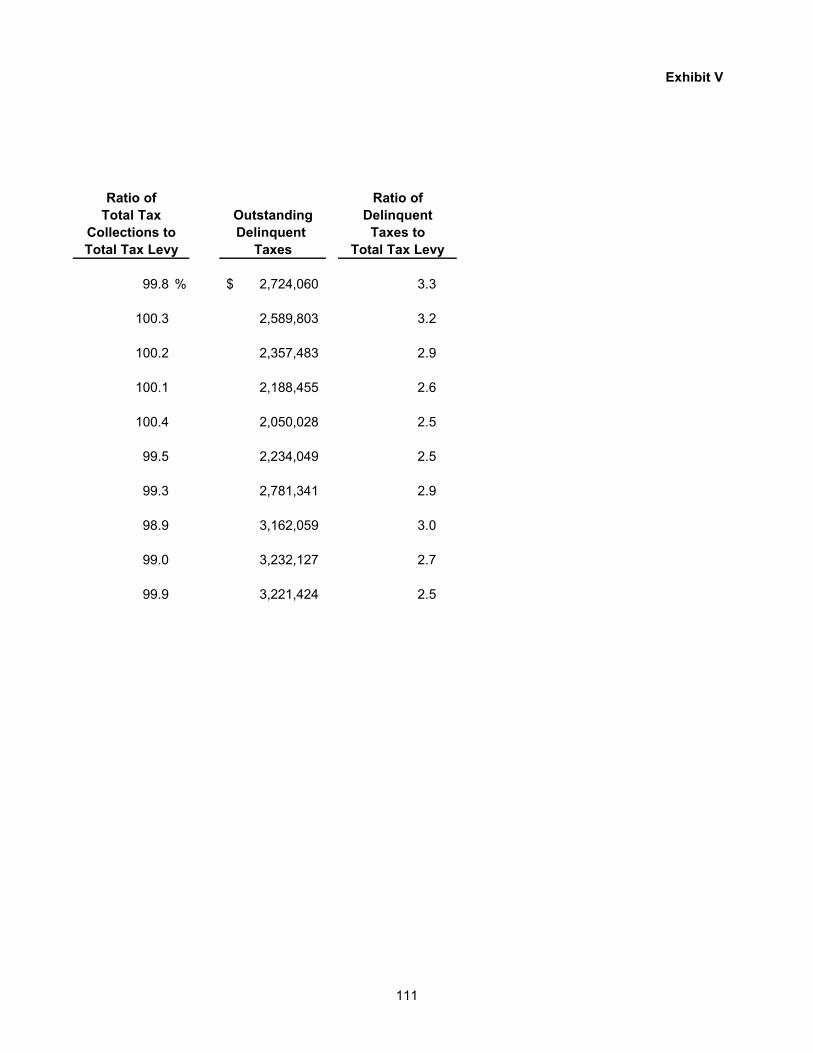

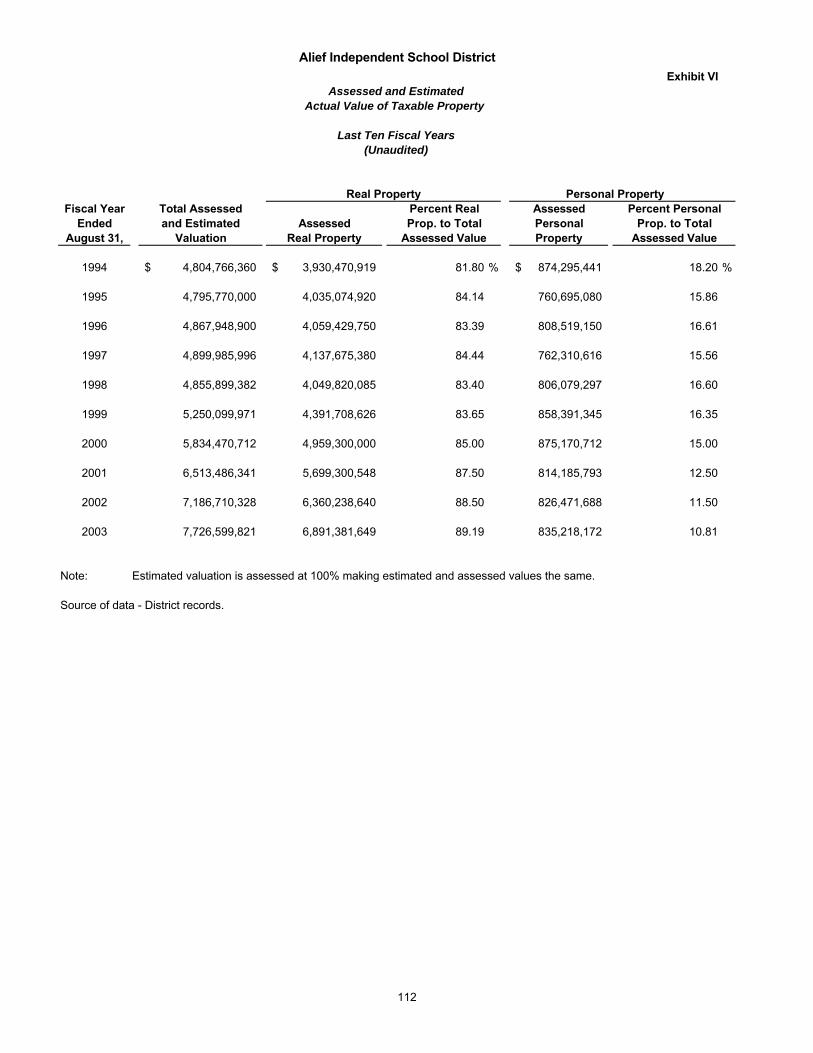

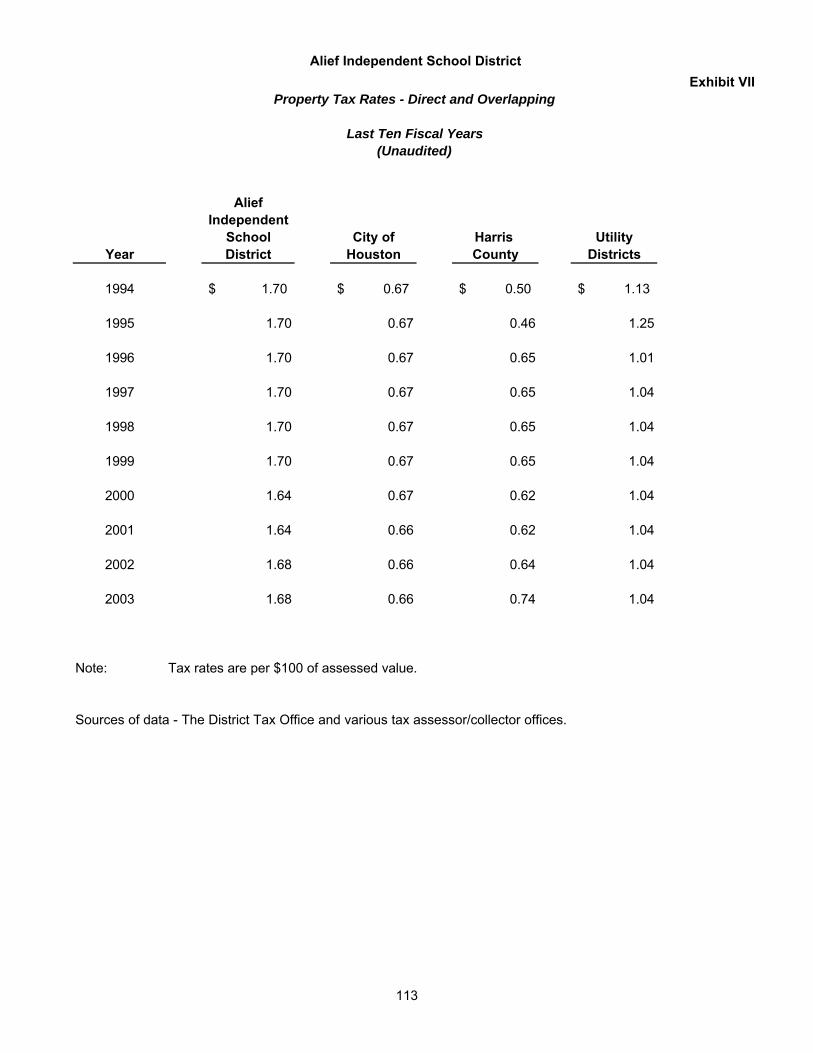

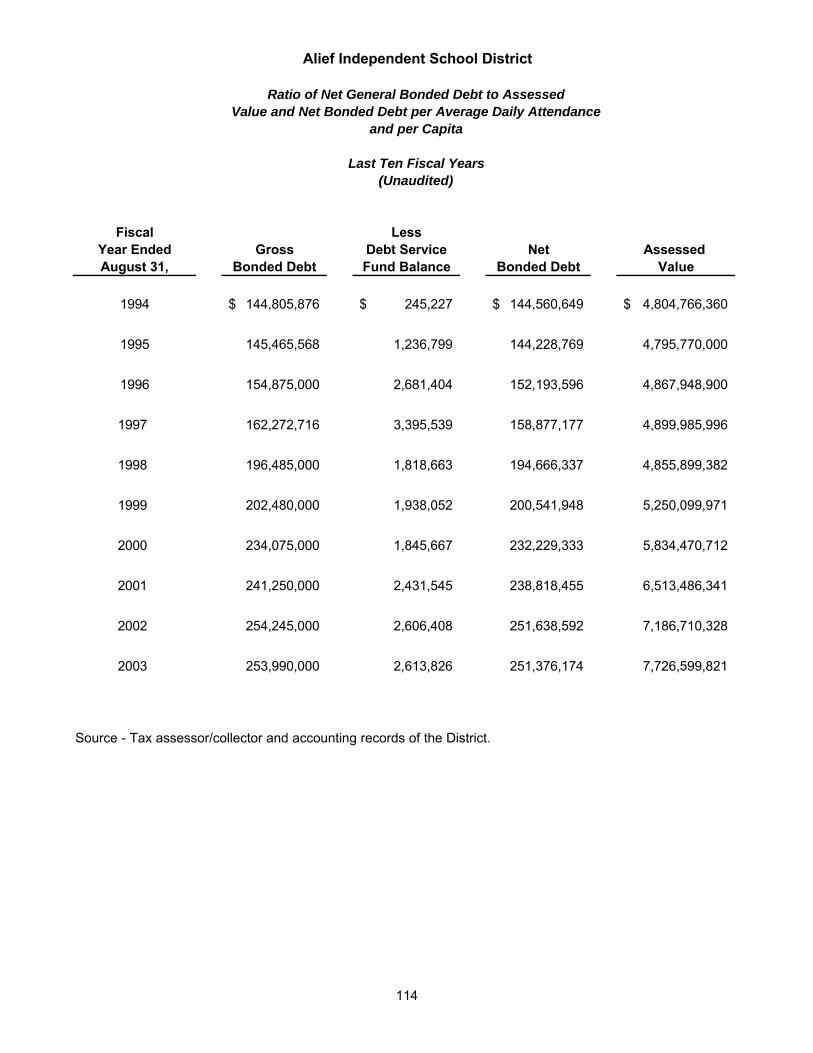

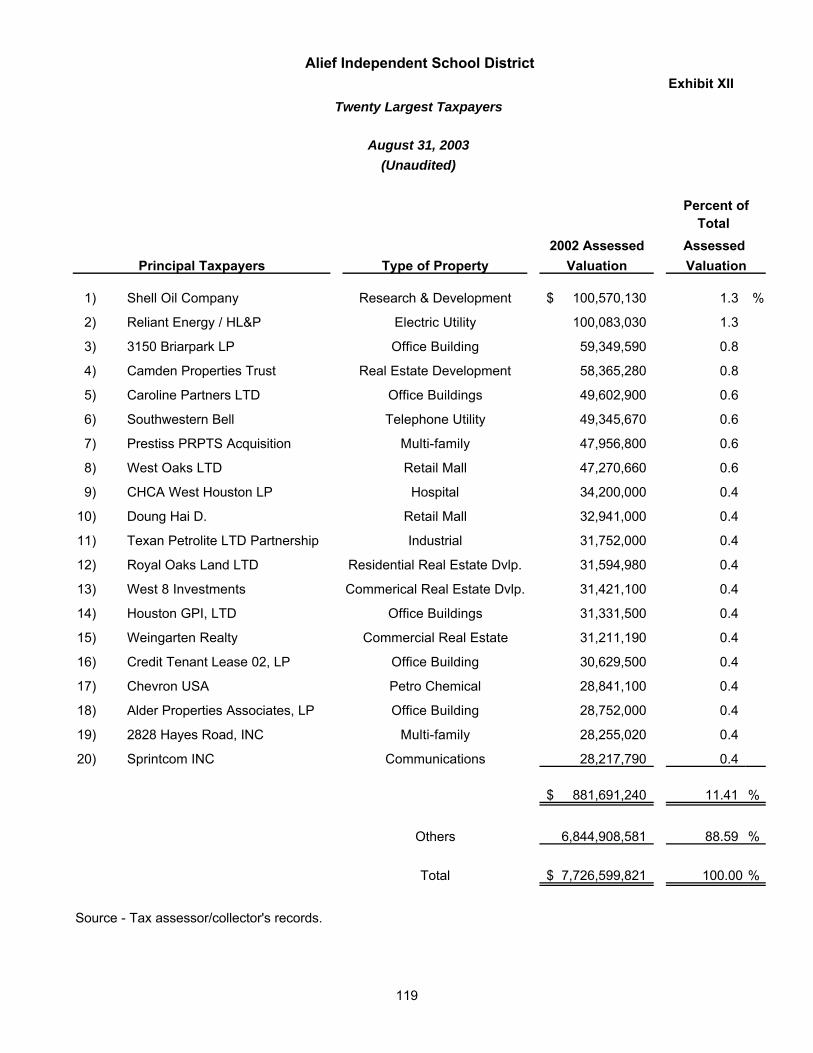

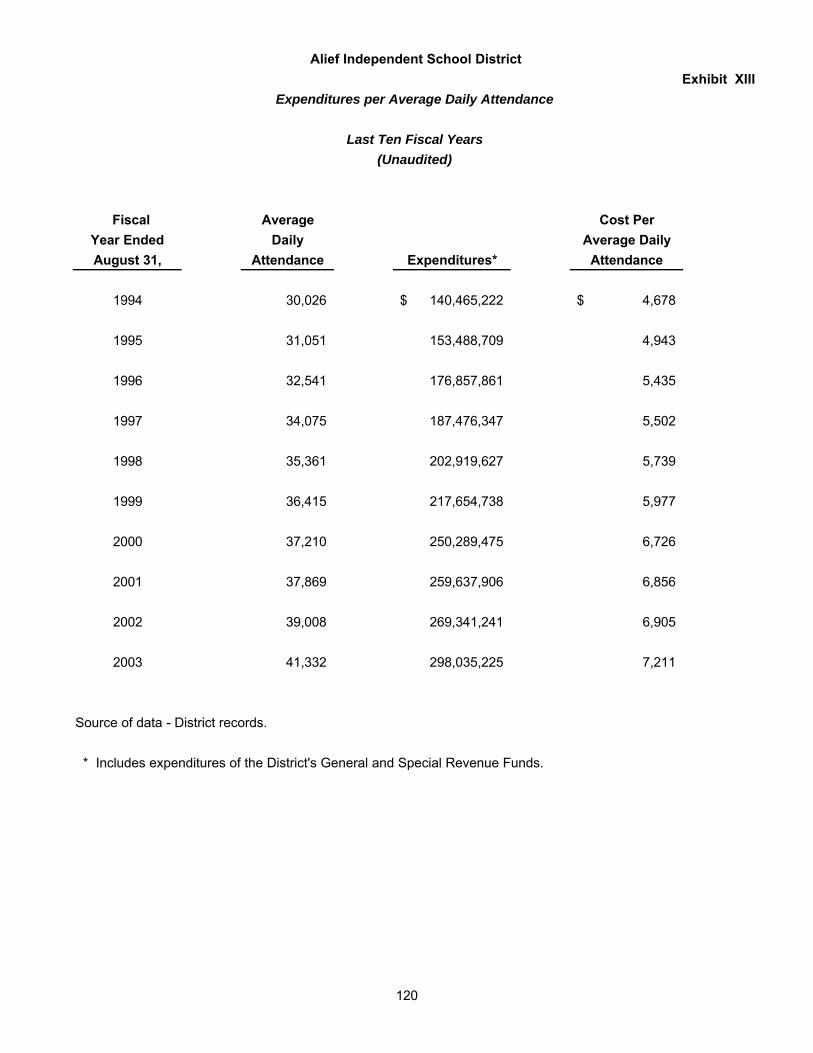

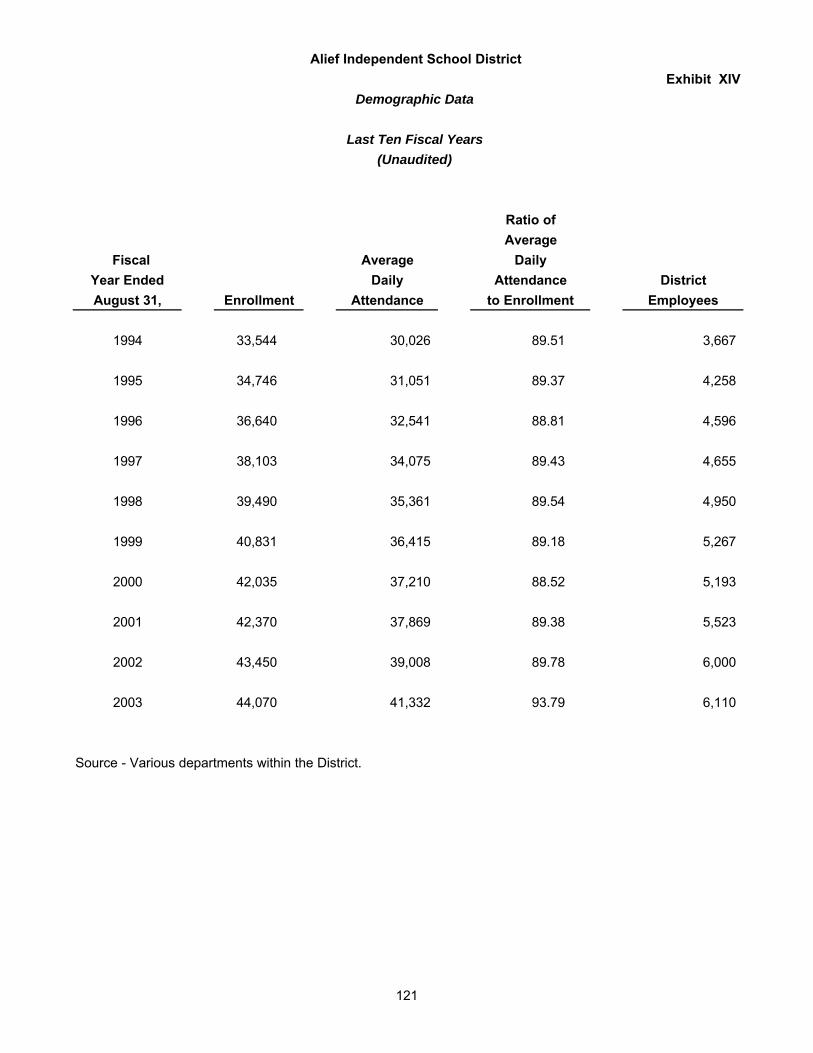

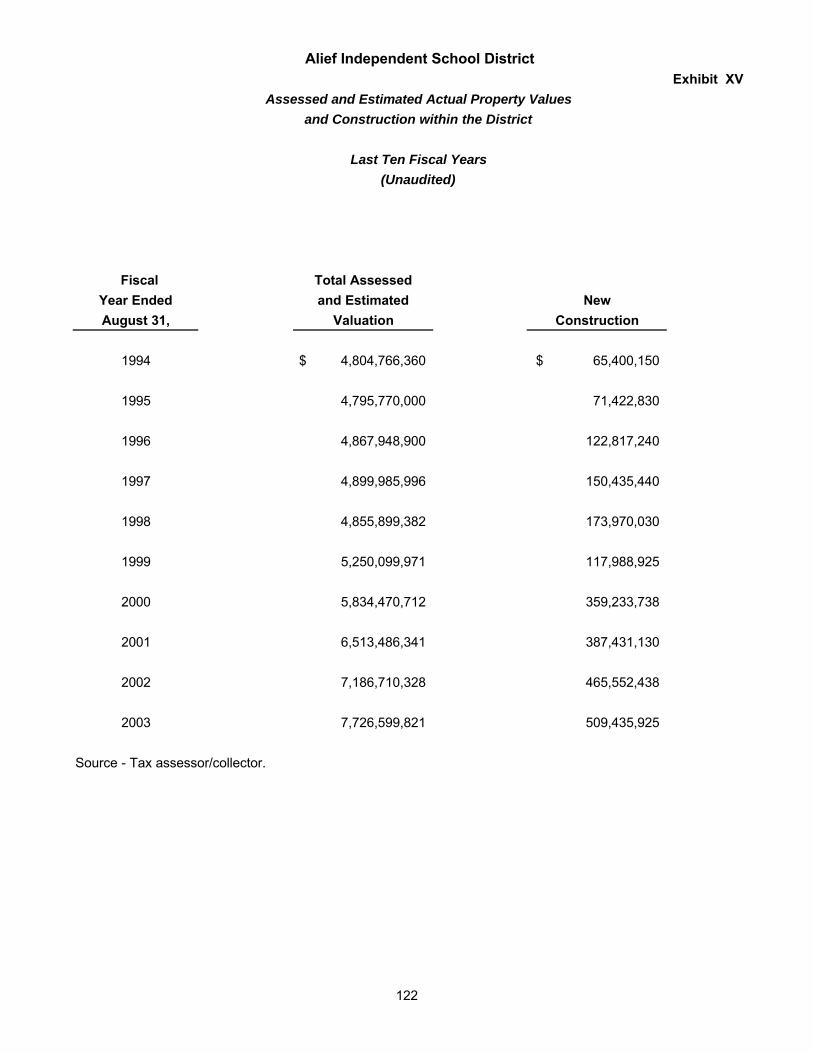

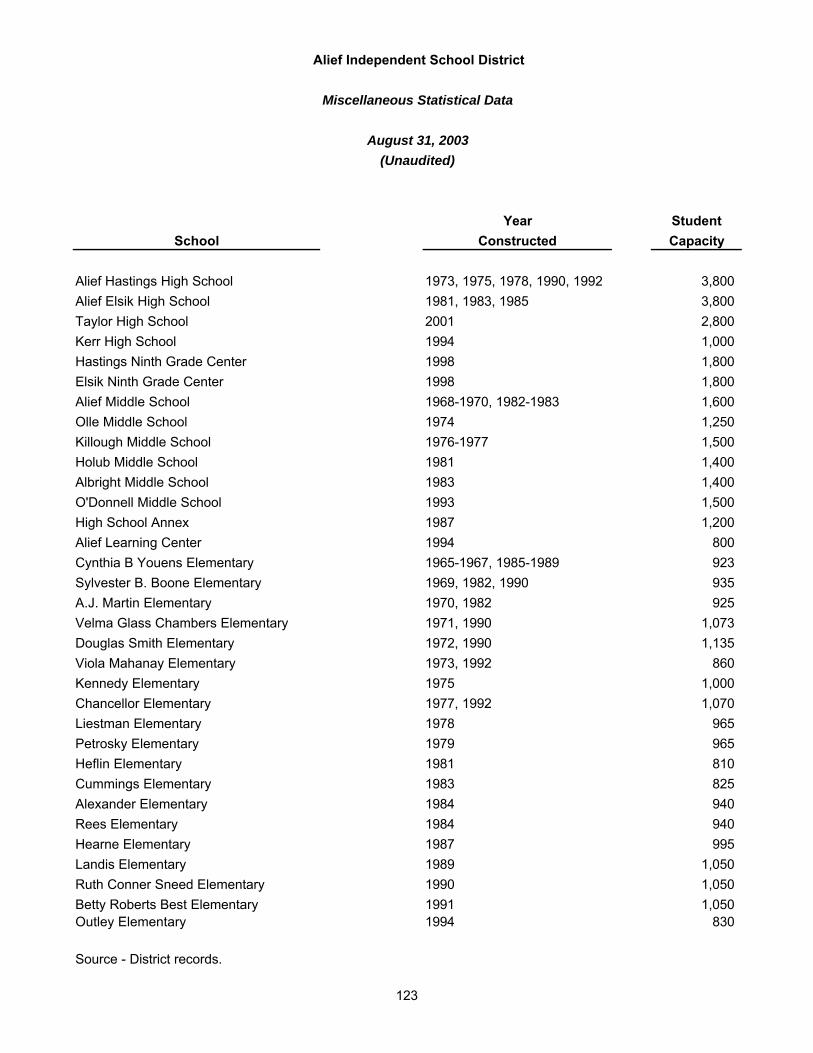

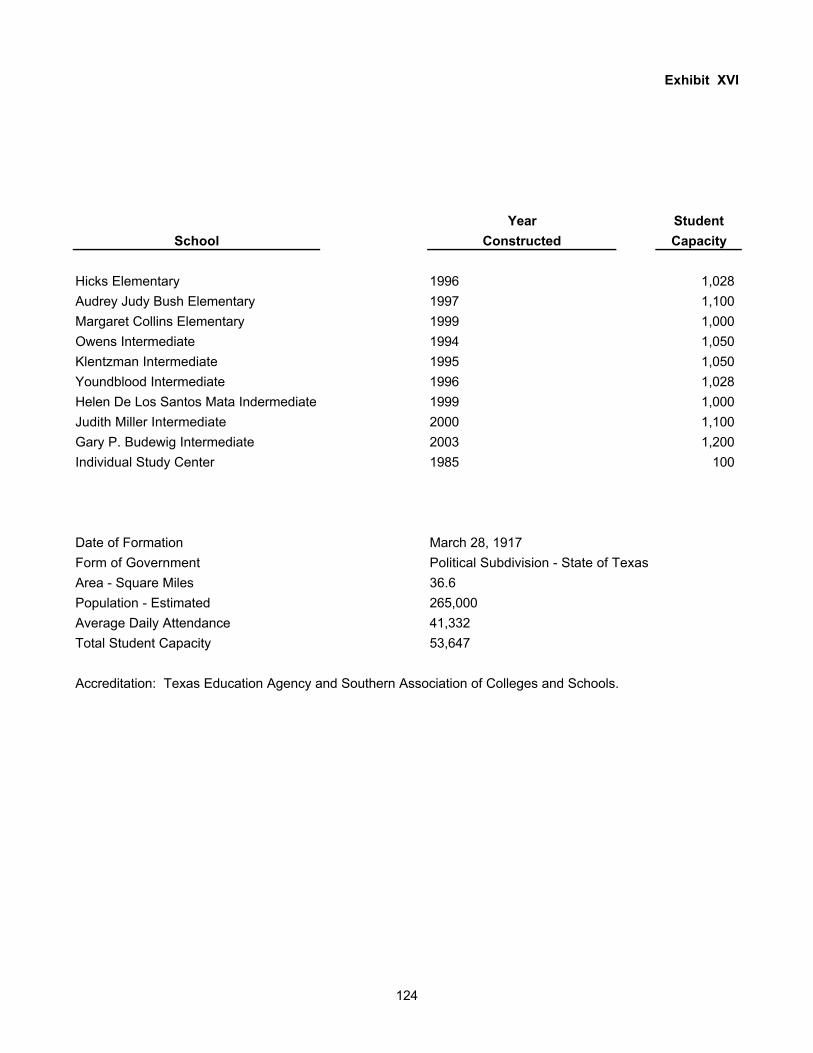

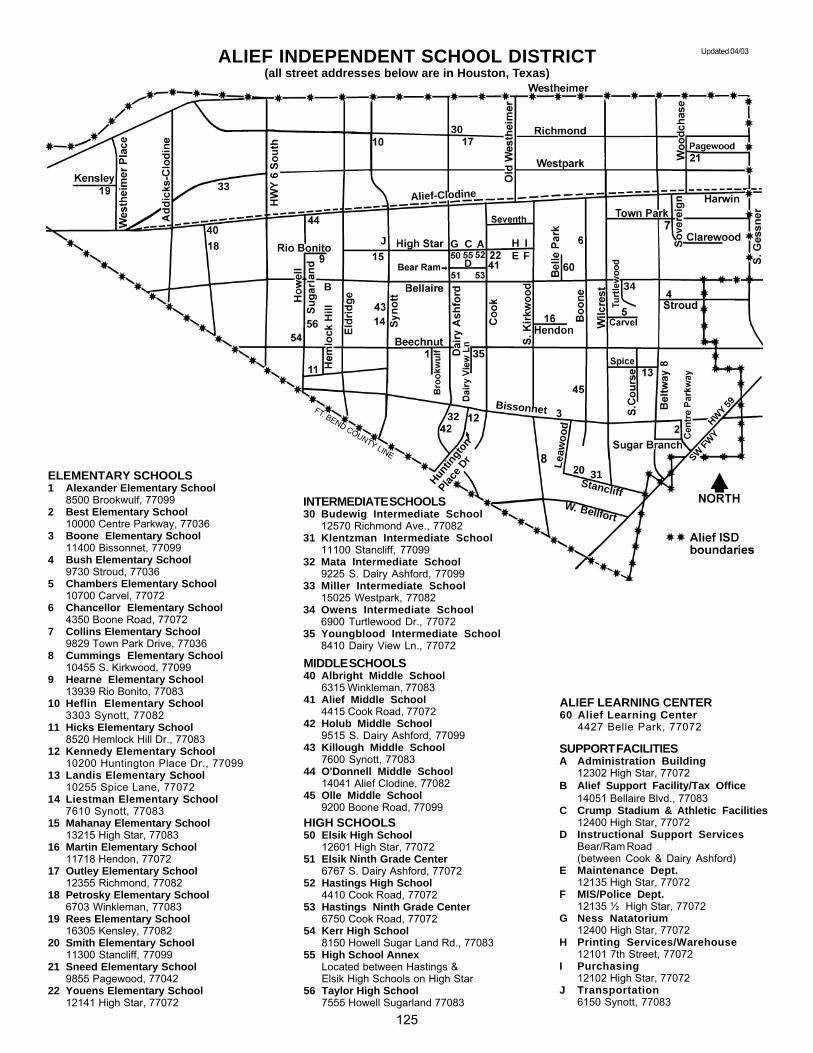

Unaudited Statistical Data Government-Wide Information: Government-Wide Expenses by Function I 104 Government-Wide Revenues II 105 Fund Information: Governmental Funds Expenditures by Major Function III 106 Governmental Funds Revenues by Source IV 108 Property Tax Levies and Collections V 110 Assessed and Estimated Actual Value of Taxable Property VI 112 Property Tax Rates - Direct and Overlapping VII 113 Ratio of Net General Bonded Debt to Assessed Value and Net Bonded Debt per Average Daily Attendance and Per Capita VIII 114 Computation of Legal Debt Margin IX 116 Ratio of Annual Debt Service Expenditures for General Bonded Debt to Total Expenditures X 117 Computation of Direct and Overlapping Debt XI 118 Twenty Largest Taxpayers XII 119 Expenditures per Average Daily Attendance XIII 120 Demographic Data XIV 121 Assessed and Estimated Actual Property Values and Construction within the District XV 122 Miscellaneous Statistical Data XVI 123 Location Map XVII 125

1

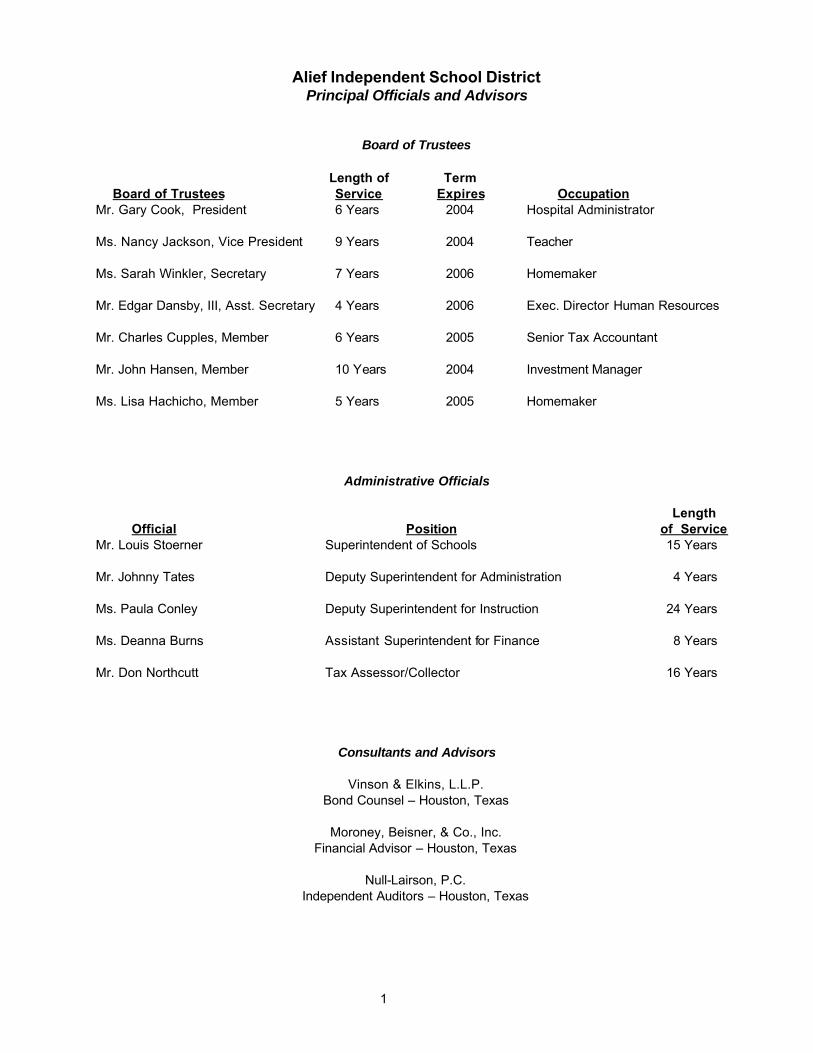

Alief Independent School District Principal Officials and Advisors

Board of Trustees Length of Term Board of Trustees Service Expires Occupation Mr. Gary Cook, President 6 Years 2004 Hospital Administrator Ms. Nancy Jackson, Vice President 9 Years 2004 Teacher Ms. Sarah Winkler, Secretary 7 Years 2006 Homemaker Mr. Edgar Dansby, III, Asst. Secretary 4 Years 2006 Exec. Director Human Resources Mr. Charles Cupples, Member 6 Years 2005 Senior Tax Accountant Mr. John Hansen, Member 10 Years 2004 Investment Manager Ms. Lisa Hachicho, Member 5 Years 2005 Homemaker

Administrative Officials Length Official Position of Service Mr. Louis Stoerner Superintendent of Schools 15 Years Mr. Johnny Tates Deputy Superintendent for Administration 4 Years Ms. Paula Conley Deputy Superintendent for Instruction 24 Years Ms. Deanna Burns Assistant Superintendent for Finance 8 Years Mr. Don Northcutt Tax Assessor/Collector 16 Years

Consultants and Advisors

Vinson & Elkins, L.L.P. Bond Counsel – Houston, Texas

Moroney, Beisner, & Co., Inc.

Financial Advisor – Houston, Texas

Null-Lairson, P.C. Independent Auditors – Houston, Texas

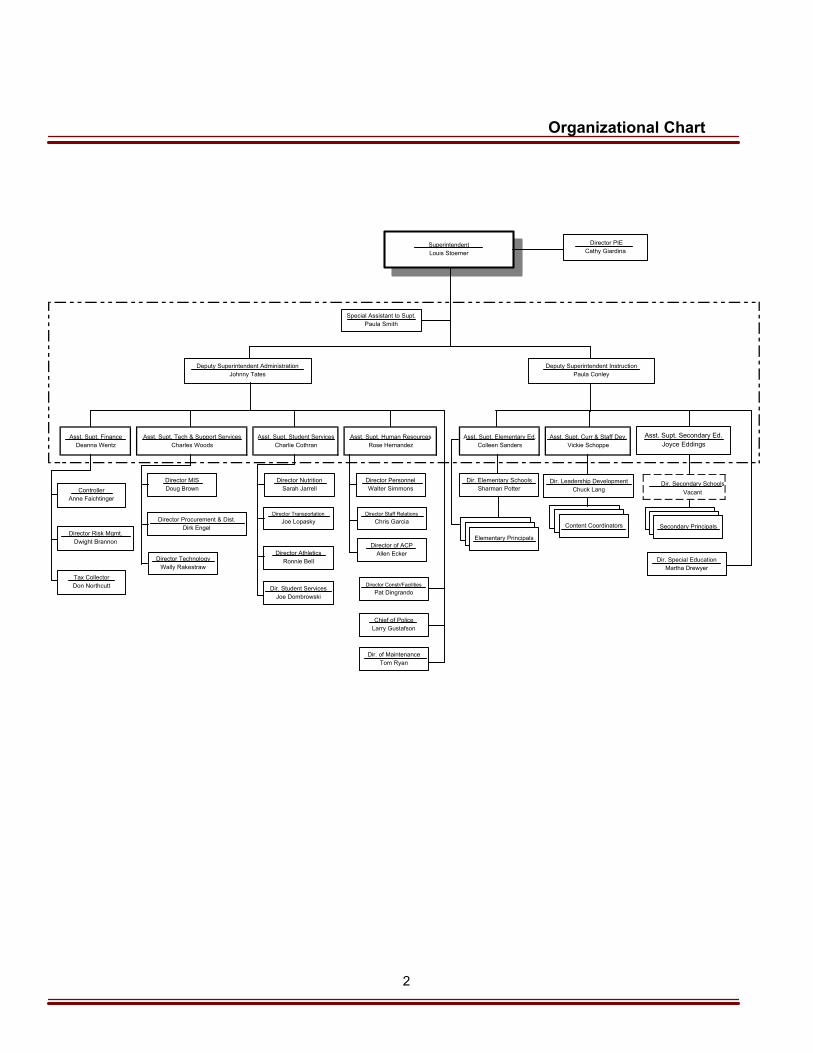

Organizational Chart

Asst. Supt. Finance Deanna Wentz

Asst. Supt. Tech & Support Services Charles Woods

Asst. Supt. Student Services Charlie Cothran

Asst. Supt. Human Resources Rose Hernandez

Asst. Supt. Elementary Ed. Colleen Sanders

Asst. Supt. Curr & Staff Dev. Vickie Schoppe

Dir. Secondary SchoolsVacant

Deputy Superintendent AdministrationJohnny Tates

Deputy Superintendent InstructionPaula Conley

Special Assistant to Supt.Paula Smith

SuperintendentLouis Stoerner

Director PIECathy Giardina

Director MISDoug Brown

Director Procurement & Dist.Dirk Engel

Director TechnologyWally Rakestraw

Director NutritionSarah Jarrell

Director TransportationJoe Lopasky

Director AthleticsRonnie Bell

Dir. Student ServicesJoe Dombrowski

Director PersonnelWalter Simmons

Director Staff RelationsChris Garcia

Director Constr/FacilitiesPat Dingrando

Chief of PoliceLarry Gustafson

Dir. of MaintenanceTom Ryan

Dir. Elementary SchoolsSharman Potter

Dir. Leadership Development Chuck Lang

Content Coordinators Secondary Principals

Elementary Principals

Dir. Special EducationMartha Drewyer

ControllerAnne Faichtinger

Director Risk Mgmt.Dwight Brannon

Asst. Supt. Secondary Ed.Joyce Eddings

Director of ACPAllen Ecker

Tax CollectorDon Northcutt

2

3

“Preparing students for tomorrow—Caring for them today”

P.O. Box 68 * Alief, Texas 77411 * (281) 498-8110 * Fax : (281) 498-4051

Administrative Services Division November 17, 2003 Board of Trustees Alief Independent School District Harris County, Texas Dear Board Members: State law requires that all general-purpose local governments publish within six months of the close of each fiscal year a complete set of financial statements presented in conformity with generally accepted accounting principals (GAAP) and audited in accordance with generally accepted auditing standards by a firm of licensed certified public accountants. Pursuant to that requirement, we hereby issue the comprehensive annual financial report of the Alief Independent School District for the fiscal year ended August 31, 2003. This report consists of management’s representations concerning the finances of the District. Consequently, management assumes full responsibility for the completeness and reliability of all of the information presented in this report. In order to provide a reasonable basis for making those representations, management of the District has established a comprehensive internal control framework that is designed to protect the government’s assets from loss, theft, or misuse. Additionally, the internal control framework is designed to compile sufficient reliable information for the preparation of the District’s financial statements in conformity with GAAP. Because the costs of internal controls should not outweigh their benefits, the District’s comprehensive framework of internal controls has been designed to provide reasonable assurance rather than absolute assurance that the financial statements will be free from material misstatement. To the best of our knowledge and belief, this financial report is complete and reliable in all material respects. The financial statements of the District have been audited by Null-Lairson, P.C., a firm of licensed certified public accountants. The goal of the independent audit is to provide reasonable assurance that the financial statements of the District for the fiscal year ended August 31, 2003 are free of material misstatement. The independent audit involves examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; assessing the accounting principals used and significant estimates made by management; and evaluating the overall financial statement presentation. The independent auditors concluded, based upon the audit, that there was a reasonable basis for rendering an unqualified opinion that the District’s financial statements for the fiscal year ended August 31, 2003 are fairly presented in conformity with GAAP. The independent auditors’ report is presented as the first component of the financial section of this report. The independent audit of the financial statements is part of a broader, federally mandated “Single Audit” designed to meet the special needs of federal grantor agencies. The standards governing Single Audit engagements require the independent auditor to report not only the fair presentation of the financial statements, but also on the audited government’s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal awards. These reports are available in the District’s separately issued Single Audit Report.

4

GAAP require that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The District’s MD&A can be found immediately following the report of the independent auditors. Profile of the District The Alief Independent School District, established in 1917, encompasses 36.6 square miles in southwest Harris County. The District is an independent political subdivision of the State of Texas governed by an elected board of trustees. The board is elected to staggered three-year terms by the District’s residents. The District is located primarily within the City of Houston and totally within Harris County, Texas. The Alief Independent School District has a population of approximately 265,000. The District employs 6,110 employees, of which 3,701 are classified as professional employees and 2,409 are classified as support personnel. These employees adequately provide educational services for the 44,070 students enrolled in the Alief Independent School District. The twenty-two elementary schools (pre-kindergarten through fourth or fifth grade), six intermediate schools (fifth and sixth grades), six middle schools (sixth or seventh grade through eighth grade), two ninth grade centers, and four high schools (tenth grade through twelfth grade) are accredited by the Southern Association of Colleges and Schools and the Texas Education Agency. The Alief Independent School District provides a full range of educational services appropriate to grade levels pre-kindergarten through twelfth grade. These include regular and enriched academic education, special education for handicapped students, occupational education, and educational servi ces for those with limited English proficiency. These basic programs are supplemented by a wide variety of offerings in fine arts, athletics, and other extracurricular programs. The annual budget serves as the foundation for the District’s financial planning and control. The budget process begins in January when the Long-Range Plan is presented to the Board of Trustees. The enrollment projections contained in this plan form the basis for significant budgetary decisions including per pupil allocations to each campus, instructional staffing allocations, and other required service levels. Once the Long-Range Plan is approved, the Board of Trustees can begin discussions concerning budget strategies and priorities, and establish the budget calendar. Personnel units are allocated to each campus based on projected student enrollment following state mandated ratios, as applicable. Each campus receives a basic allotment per student to be used for supplies, materials, equipment, staff development and other appropriate instructional costs. Decisions concerning utilization of this allocation are made by the site-based decision making teams. Budgets for non-campus units are developed by department heads and reviewed by the Budget Committee. Following the budget development process, consolidated budgetary information is presented to the Board of Trustees in workshops and regular meetings. The proposed budget must be prepared by August 20th for a September 1st fiscal year start date. The Board President must call a board meeting for the purpose of discussing and adopting the budget and the tax rate. A notice of this meeting is required to be published at least 10 days, but not more than 30 days before the public meeting. Budget-to-actual comparisons are provided in this report for each individual governmental fund for which an appropriated annual budget has been adopted. Factors Affecting Financial Condition The information presented in the financial statements is perhaps best understood when it is considered from the broader perspective of the specific environment within which the District operates. Local Economy Recent economic growth in both our District and the entire Houston area provide for an optimistic economic outlook. Key economic indicators, such as unemployment rates, sales tax receipts, and commercial and residential development, reflect the growth of the area. The District continues to experience significant growth in new home construction. Based on current information, it appears this growth will continue for the next two to three years. The subdivisions that will produce a significant number of students are not large developments; however, when combined, these developments may produce a moderate increase in enrollment. The majority of the development is located west of Dairy Ashford and will impact the schools located in the west part of the district.

5

Local Economy (continued) This will somewhat reverse the trend of student growth, which for several years was in the eastern part of the district, primarily along the Sam Houston Tollway. The homes prices vary, with the average in the mid $100,000 range This revitalization of our area is encouraging. The District’s property values, which peaked in the early 1980’s, are continuing to rebound, with growth rates over 7.5% for the last five years. State Funding Continued increases in enrollment are projected for the foreseeable future in the District. The current system in the State of Texas provides funding for public education via a financing formula which weights student attendance levels, property value per student, the District’s tax effort, and regional variations in payroll and other costs. The District is considered a “property-poor” school district because the assessed value of property per student is lower than the statewide average. The statewide taxable value per student for 2002-03 was $242,809, while the comparable value for the District was $174,157. Cash Management Cash available in excess of cash requirements was invested in the one of three investment pools used by the District and government agency securities. The District participates in Texpool, the Local Government Investment Cooperative (LOGIC), and Lone Star investment pools. The average yield on investments was 2.00% while the average yield on the one year U.S. Treasury bill was 1.29% for the year ended August, 31, 2003. The District’s investment policy is to minimize risk while maintaining a competitive yield on its portfolio. The District’s deposits were entirely covered by Federal Deposit Insurance Corporation (FDIC) insurance and pledged collateral for the year ended August 31, 2003. Risk Management The District’s risk management program encompasses various means of protecting the District against loss. Property and casualty insurance is provided by commercial carriers and liability insurance coverage is provided by participation in a public entity risk pool administered by the Texas Association of School Boards. The Risk Management Department of the District strives to ensure the safety and health of the students and employees through its accident prevention programs, safety education programs, and safety inspections. In addition, the District strives to maintain employee benefit programs designed to retain and attract qualified personnel. To achieve this, the District operates a self-funded health insurance program and is covered by an excess loss insurance policy for claims exceeding a specified limit. Various types of insurance coverages are made available to employees. Portions of the coverages available, such as medical and life insurance, are partially paid by the District. The District also operates a self-funded workers compensation program with an emphasis on cost control of claims. Major Initiatives and Accomplishments In September 2003, the voters in the Alief Independent School District approved a $175 million bond referendum. The bonds will begin to be issued in the spring, 2004. These proceeds will be used to support construction of new facilities, including Elementary #23, Elementary #24, Intermediate #7, and Middle School #7 as well as purchase land for future schools. The proceeds will also be used for renovations, additions, and maintenance to existing campuses including enclosing classrooms at the elementary schools. Implementation of the Long-Range Technology Plan is still in effect, which will enable children to experience hands on learning utilizing leading edge technologies. New computer labs are being installed to improve academic success through computer-assisted learning. The success of these and many other programs is evident in the continued improvement of TAAS scores recently released by the Texas Education Agency.

6

Major Initiatives and Accomplishments (continued) The 2002-03 financial structure of the Alief Independent School District provided support to work toward or accomplish the following goals: 1. Provided competitive salary and benefit increases to District employees. A $1,346 across the

board increase was approved for all employees paid from the teacher salary schedule. For all other personnel, a 3% of the midpoint increase was approved by the Board of Trustees. Additionally, all employees will receive an additional $80/month for benefits. As a result of both of these changes, most employees will see significant increases in their net pay.

2. The successful continuation of the Special Campus Instructional Grant Program which began in

fiscal year 1998-99. Each campus is allocated an additional $25 per pupil based on enrollment estimates. The purpose of these funds is to supplement the basic campus allocation in a manner that enhances the educational program through the implementation of new programs or projects.

3. Structured fiscally responsible debt retirement schedules. When compared with other “fast

growth” districts, Alief continues to retire debt at a much faster pace. Within the next 10 years, Alief will retire approximately 69.41% of the currently issued debt compared to the state average of 43.2%.

Awards and Acknowledgements The Association of School Business Officials International (ASBO) awarded a Certificate of Excellence in Financial Reporting to the Alief Independent School District for its Comprehensive Annual Financial Report for the fiscal year ended August 31, 2002. We believe that our current report continues to conform to the high standards of the certificate of excellence program, and we are submitting it to ASBO. In addition, the Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to Alief Independent School District for its Comprehensive Annual Financial Report for the fiscal year ended August 31, 2002. In order to be awarded a Certificate of Achievement, a government unit must publish an easily readable and efficiently organized Comprehensive Annual Financial Report, whose contents conform to program standards. Such reports must satisfy both accounting principles generally accepted in the United States of America and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe our current report continues to conform to the Certificate of Achievement Program requirements, and we are submitting it to the GFOA. The District also received the GFOA’s Distinguished Budget Presentation Award and the ASBO’s Meritorious Budget Award for its annual budget document. In order to qualify for these budget awards the budget document was judged to be proficient in several categories as specified by these two organizations.

7

Awards and Acknowledgements (continued) The financial management staff of the Alief Independent School District wishes to express its appreciation to the Board of Trustees for their concern in providing fiscal accountability to the patrons of the District and thereby contributing their full support in the development of one of the best educational financial operations within the State of Texas. The preparation of this report could not have been accomplished without the dedicated services of the District’s Accounting Department as well as the technical support provided by the independent auditing firm of Null-Lairson, P.C. Sincere appreciation is extended to those personnel who assisted and contributed to the preparation of the Comprehensive Annual Financial Report. Sincerely, Mr. Louis B. Stoerner Mr. Johnny Tates Superintendent Deputy Superintendent, Administrative Services Division

Ms. Deanna Wentz Assistant Superintendent for Finance

8

9

This page intentionally blank.

10

This page intentionally blank.

11 Greenway Plaza, Suite 1515 Houston, TX 77046

(713) 621-1515 Fax: (713) 621-1570

One Sugar Creek Blvd., Suite 920 Sugar Land, TX 77478

(281) 242-8600 Fax: (281) 242-7333

11

Independent Auditors’ Report To the Board of Trustees Alief Independent School District Alief, Texas We have audited the accompanying financial statements of the governmental activities, the business- type activities, each major fund, and the aggregate remaining fund information of Alief Independent School District as of August 31, 2003, and for the year then ended, which collectively comprise the District’s basic financial statements as listed in the table of contents. These financial statements are the responsibility of Alief Independent School District’s management. Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the provisions of the Office of Management and Budget (OMB) Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations; and applicable provisions of the Texas Education Agency’s “Financial Accountability System Resource Guide”. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions. In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund and the aggregate remaining fund information of Alief Independent School District, as of August 31, 2003, and the respective changes in financial position results and cash flows, where applicable, thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America. In accordance with Government Auditing Standards, we have also issued reports dated October 30, 2003, on our consideration of Alief Independent School District’s internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts, and grants. That report, which has been issued separately from this document, is an integral part of an audit performed in accordance with Government Auditing Standards and should be read in conjunction with this report in considering the results of our audit. The Management’s Discussion and Analysis, on page 13 through 21, and the Schedule of Revenues, Expenditures and Changes in Fund Balances Original Budget, Amended Final and Actual – General Fund, on pages 55 through 56, are not a required part of the basic financial statements but are supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it.

12

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the District’s basic financial statements. The Comparative Statements, Combining Statements and Budget Comparisons, Capital Assets used in the Operation of Governmental Funds, Compliance Schedules, and other schedules listed under Other Supplementary Information in the Table of Contents are presented for purposes of additional analysis and are not a required part of the basic financial statements. The Comparative Statements, Combining Statements and Budget Comparisons, Capital Assets used in the Operation of Governmental Funds, Compliance Schedules, and other schedules listed under Other Supplementary Information in the Table of Contents have been subjected to the auditing procedures applied in the audit of the basic financial statements and in our opinion are fairly stated in all material respects in relation to the basic financial statements taken as a whole. The Introductory Section and Statistical Data Section listed in the foregoing Table of Contents are presented for the purpose of additional analysis and are not a required part of the basic financial statements of the District. Such additional information has not been subjected to the auditing procedures applied in our audit of the basic financial statements and, accordingly, we express no opinion on them.

Houston, Texas October 30, 2003

Alief

Basic Financial Statements

This page intentionally blank.

13

Management's Discussion and Analysis In this section of the Annual Financial and Compliance Report, we offer readers of the District’s financial statements a narrative overview and analysis of the financial activities of the District for the fiscal year ended August 31, 2003. Please read it in conjunction with the independent auditors' report and the District's financial statements, which follow this section.

Financial Highlights · The assets of the District exceeded its liabilities at the close of the fiscal year by $189,237,911 (net

assets). Of this amount, $64,247,773 (unrestricted net assets) may be used to meet the District’s ongoing obligations.

· The District’s net assets increased by $19,391,598 as a result of this year’s operations. · The District’s governmental funds reported combined ending fund balances of $86,782,237.

Approximately 66% of this total amount, $57,001,529, is available for spending at the government’s discretion (unreserved, undesignated fund balance).

· The combined ending fund balances for the District’s governmental funds decreased $3,869,317 due

to normal operations. Offsetting this decrease in fund balances is an increase of $1,344,550 created by a prior period adjustment.

· The General Fund ended the year with an unreserved, undesignated fund balance of $57,001,529, or

22% of the total general fund expenditures.

Overview of the Financial Statements This annual report consists of a series of financial statements plus additional supplemental information as required by its state oversight agency, the Texas Education Agency. The District’s basic financial statements consist of three sections: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. The following sections describe the measurement focus of the two types of statements and the significant differences in the information they provide. Government-wide Financial Statements The focus of government-wide financial statements is on the overall financial position and activities of the District. The District’s government-wide financial statements include the statement of net assets and the statement of activities (on pages 22 and 23), which are prepared using accounting principles that are similar to commercial enterprises. These statements provide information about the activities of the District as a whole and present a longer-term view of the District's property and debt obligations and other financial matters. The statement of net assets includes all the District's assets and liabilities at the end of the year, with the difference between the two reported as net assets. This difference is similar to the total owners’ equity presented by a commercial enterprise. All the District's assets are reported, whether they serve the current year or future years. Liabilities are considered regardless of whether they must be paid in the current or future years. Although the purpose of the District is not to accumulate net assets, in general, as the amount increases, it may indicate that the financial position of the District is improving over time. To fully assess the overall health of the District, however, you should consider other factors as well, such as changes in the District's average daily attendance or its property tax base and the condition of the District's facilities.

14

Management’s Discussion and Analysis (continued) The purpose of the statement of activities is to present the revenues and expenses of the District. Again, the items presented on the statement of activities are measured in a manner similar to the approach used by a commercial enterprise in that revenues are recognized when earned or established criteria are satisfied, and expenses are reported when incurred by the District. Thus, revenues are reported even when they may not be collected for several months or years after the end of the accounting period, and expenses are recorded even though they may not have used cash during the current period. The District's revenues are divided into those provided by outside parties who share the costs of some programs, such as tuition received for summer school and grants provided by the U.S. Department of Education to assist children with disabilities or from disadvantaged backgrounds (program revenues), and revenues provided by the taxpayers or by TEA in the equalization funding processes (general revenues). Although the statement of activities looks different from a commercial enterprise’s income statements, the financial statement is different only in format, not substance. The financial information for the year ended August 31, 2003 includes start up costs for the District’s new day care facility. The facility will offer child care services to employees. The costs associated with the day care are accounted for as a business-type activity. Once the facility becomes operational, fees charged to employees are intended to recover all or a significant portion of costs incurred. The District has no component units for which it is financially accountable. Fund Financial Statements Fund financial statements (starting on page 24) report the District's operations in more detail than the government-wide statements by providing information about the District's most significant funds – not the District as a whole. For governmental activities, these statements tell how services were financed in the short term, as well as what resources remain for future spending. They reflect the flow of current financial resources, and supply the basis for tax levies and the appropriations budget. For proprietary activities, fund financial statements tell how goods or services of the District were sold to departments within the District or outside parties and how the sales revenues covered the expenses of the goods or services. The remaining statements, fiduciary statements, provide financial information about activities for which the District acts solely as a trustee or agent for the benefit of those outside of the district. Laws and contracts require the District to establish some funds, such as the debt service fund. The District's administration establishes many other funds to help it control and manage money for particular purposes. All of the District’s funds can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds.

· Governmental funds – Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities.

15

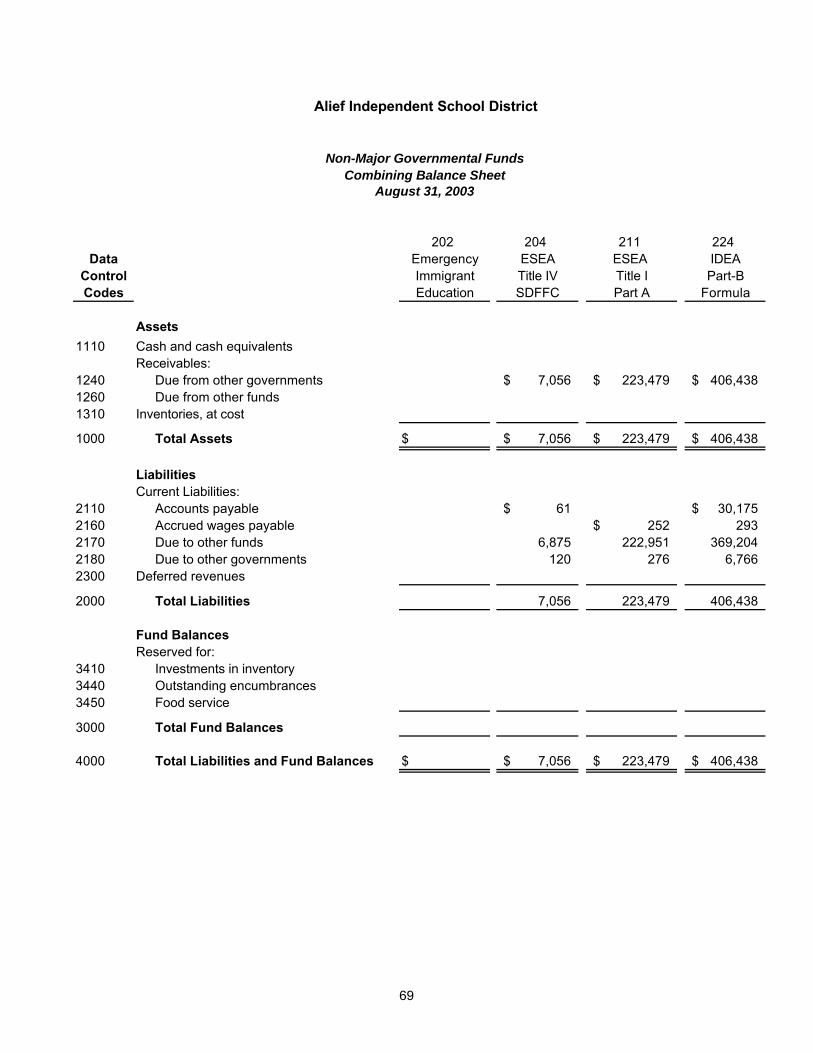

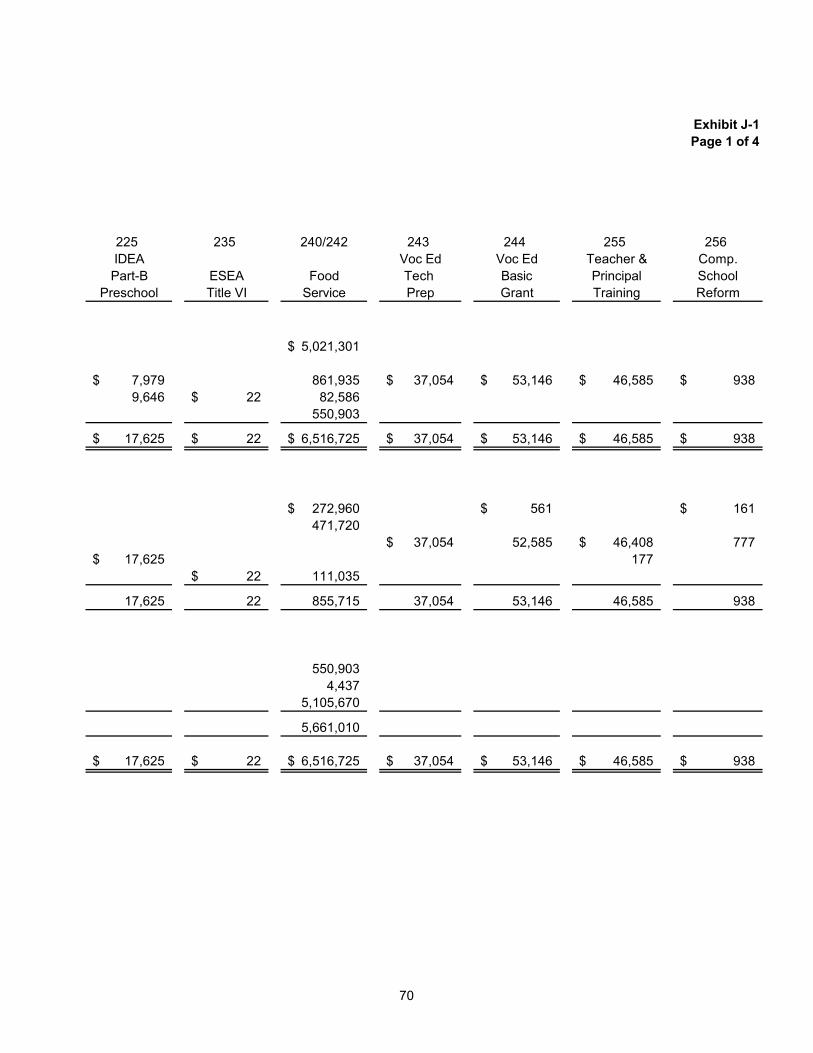

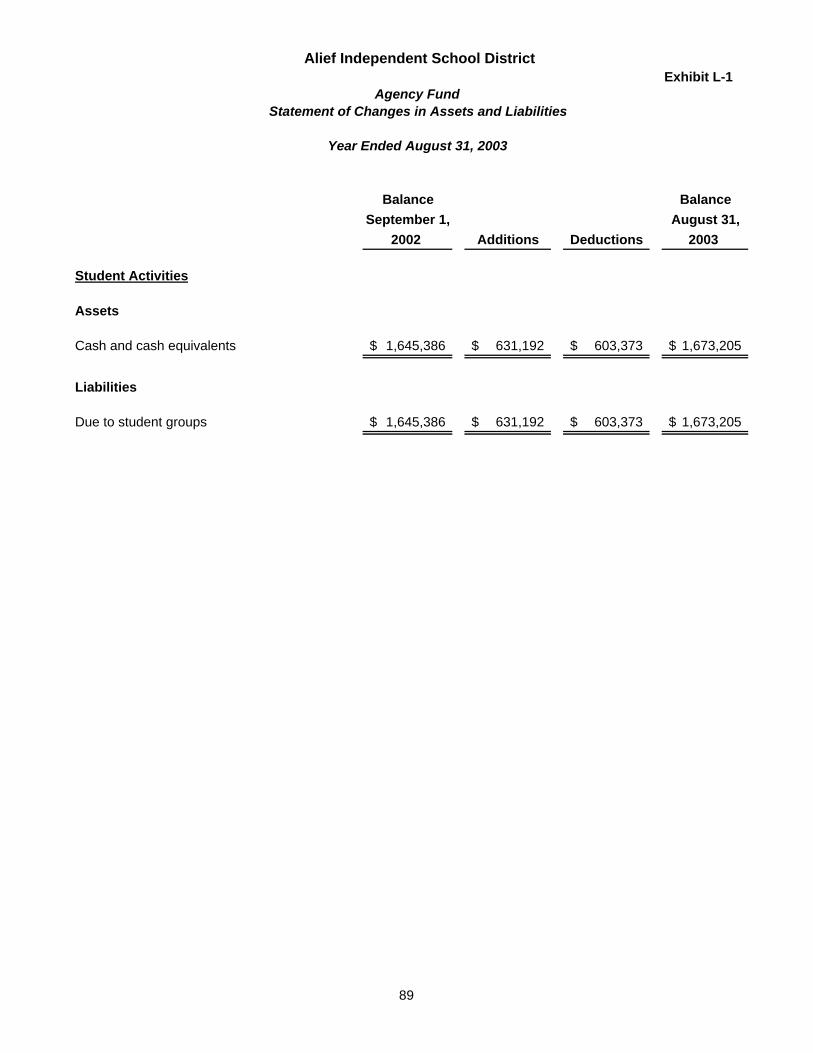

Management’s Discussion and Analysis (continued) The District maintains 45 governmental funds. Information is presented separately in fund financial statements for the general fund, debt service fund, and the capital projects fund, all of which are considered to be major funds. Data from the other 42 non-major governmental funds are combined into a single, aggregated presentation. Individual fund data for each of the non-major governmental funds is provided in the form of combining statements elsewhere in this report. The District adopts an annual appropriated budget for its general fund, debt service fund, and food service fund. Budgetary comparison schedules have been provided to demonstrate compliance with these budgets. · Proprietary funds – Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. There are two proprietary fund types – enterprise and internal service funds. The District’s enterprise fund is used to account for its business-type activity, a day care facility. The internal service funds are an accounting device used to accumulate and allocate costs internally among the various functions. The District uses the internal service fund to report activities for its self-funded insurance program. The basic proprietary fund financial statements can be found on pages 29-31 of this report. · Fiduciary funds – Fiduciary funds are used to account for resources held for the benefit of parties outside the government. The District is the trustee, or fiduciary, for money raised by student activities. All of the District’s fiduciary activities are reported in a separate Statement of Assets and Liabilities on page 32. We exclude these resources from the District’s other financial statements because the District cannot use these assets to finance its operations. The district is only responsible for ensuring that the assets reported in these funds are used for their intended purposes.

Notes to the financial statements The notes to the financial statements (starting on page 33) provide narrative explanations or additional data needed for full disclosure in the government-wide statements or the fund financial statements. Other information In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information that further explains and supports the information in the financial statements. Required supplementary information can be found on page 55 of this report. The combining statements referred to earlier in connection with nonmajor governmental funds are presented following the required supplementary information. Comparative statements, combining statements, budget comparisons, and compliance schedules can be found on pages 57-103 of this report.

Government-Wide Financial Analysis The government-wide financial statements for the fiscal year ended August 31, 2003 are the second annual financial statements presented under new governmental accounting standards. The District’s overall financial position and operations for the past year two years are summarized as follows, based on the information included in the government-wide financial statements.

16

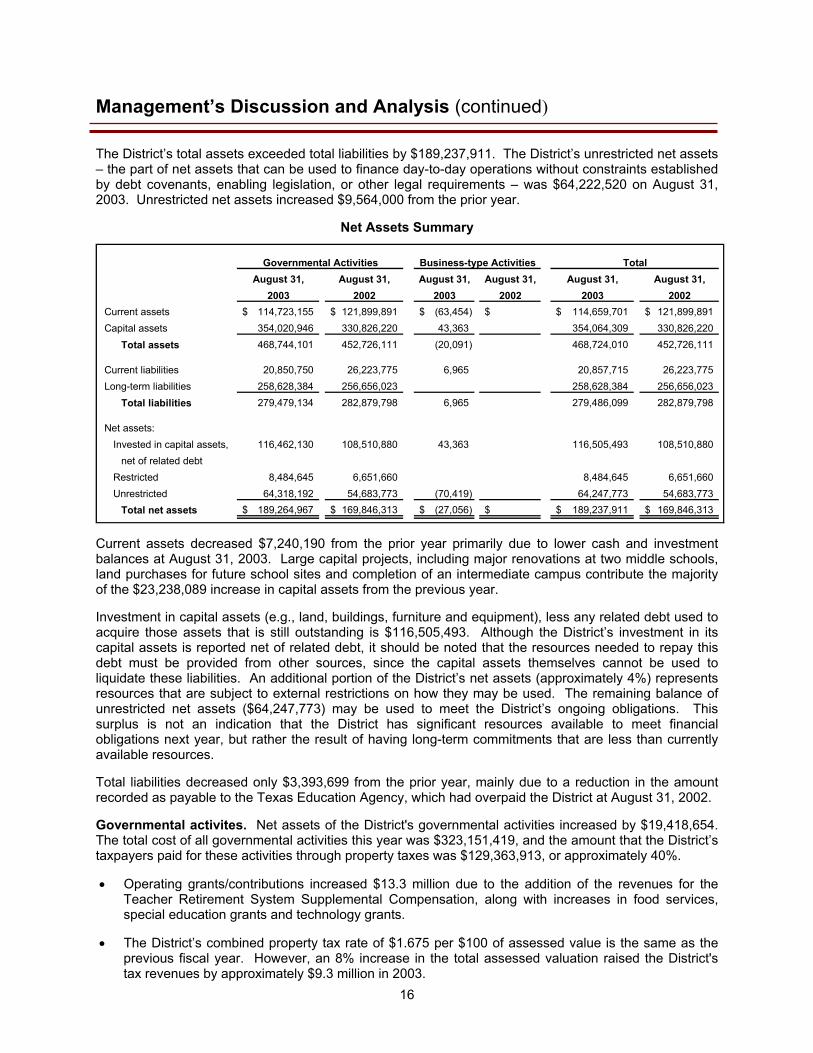

Management’s Discussion and Analysis (continued) The District’s total assets exceeded total liabilities by $189,237,911. The District’s unrestricted net assets – the part of net assets that can be used to finance day-to-day operations without constraints established by debt covenants, enabling legislation, or other legal requirements – was $64,222,520 on August 31, 2003. Unrestricted net assets increased $9,564,000 from the prior year.

Net Assets Summary

Governmental Activities Business-type Activities TotalAugust 31, August 31, August 31, August 31, August 31, August 31,

2003 2002 2003 2002 2003 2002Current assets 114,723,155$ 121,899,891$ (63,454)$ $ 114,659,701$ 121,899,891$ Capital assets 354,020,946 330,826,220 43,363 354,064,309 330,826,220

Total assets 468,744,101 452,726,111 (20,091) 468,724,010 452,726,111

Current liabilities 20,850,750 26,223,775 6,965 20,857,715 26,223,775 Long-term liabilities 258,628,384 256,656,023 258,628,384 256,656,023

Total liabilities 279,479,134 282,879,798 6,965 279,486,099 282,879,798

Net assets:Invested in capital assets, 116,462,130 108,510,880 43,363 116,505,493 108,510,880

net of related debtRestricted 8,484,645 6,651,660 8,484,645 6,651,660 Unrestricted 64,318,192 54,683,773 (70,419) 64,247,773 54,683,773

Total net assets 189,264,967$ 169,846,313$ (27,056)$ $ 189,237,911$ 169,846,313$

Current assets decreased $7,240,190 from the prior year primarily due to lower cash and investment balances at August 31, 2003. Large capital projects, including major renovations at two middle schools, land purchases for future school sites and completion of an intermediate campus contribute the majority of the $23,238,089 increase in capital assets from the previous year. Investment in capital assets (e.g., land, buildings, furniture and equipment), less any related debt used to acquire those assets that is still outstanding is $116,505,493. Although the District’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the District’s net assets (approximately 4%) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net assets ($64,247,773) may be used to meet the District’s ongoing obligations. This surplus is not an indication that the District has significant resources available to meet financial obligations next year, but rather the result of having long-term commitments that are less than currently available resources. Total liabilities decreased only $3,393,699 from the prior year, mainly due to a reduction in the amount recorded as payable to the Texas Education Agency, which had overpaid the District at August 31, 2002. Governmental activites. Net assets of the District's governmental activities increased by $19,418,654. The total cost of all governmental activities this year was $323,151,419, and the amount that the District’s taxpayers paid for these activities through property taxes was $129,363,913, or approximately 40%. • Operating grants/contributions increased $13.3 million due to the addition of the revenues for the

Teacher Retirement System Supplemental Compensation, along with increases in food services, special education grants and technology grants.

• The District’s combined property tax rate of $1.675 per $100 of assessed value is the same as the

previous fiscal year. However, an 8% increase in the total assessed valuation raised the District's tax revenues by approximately $9.3 million in 2003.

17

Management’s Discussion and Analysis (continued)

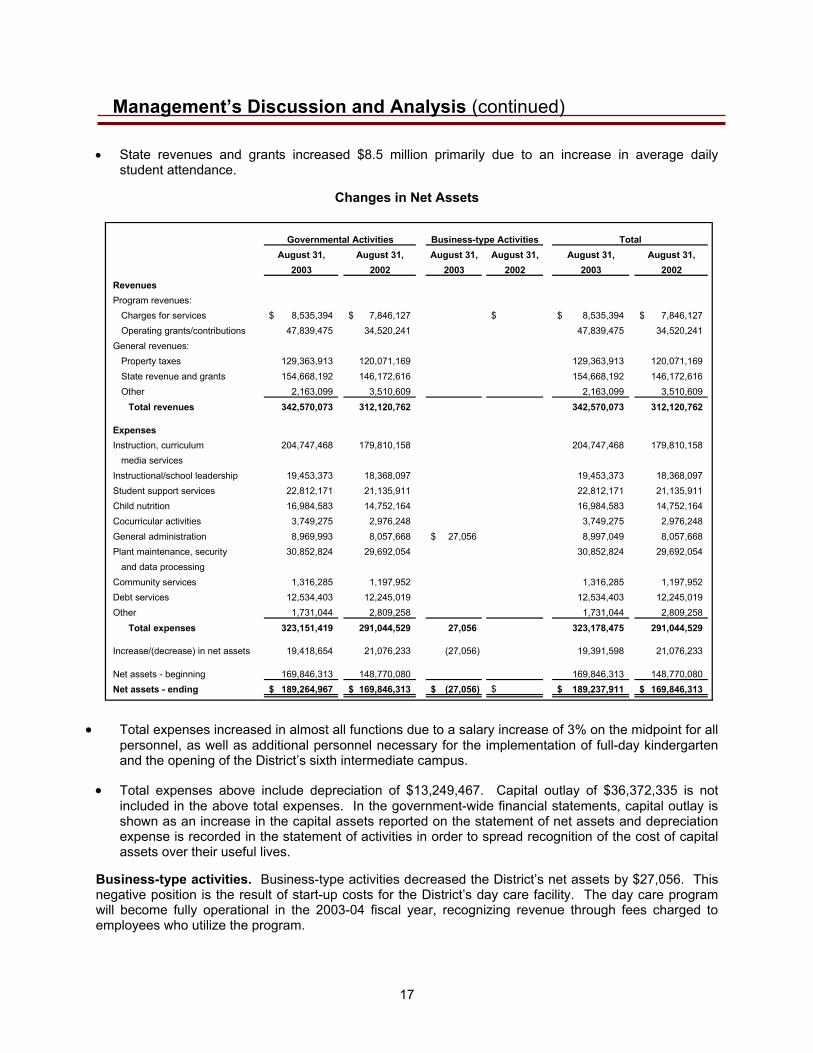

• State revenues and grants increased $8.5 million primarily due to an increase in average daily

student attendance.

Changes in Net Assets

Governmental Activities Business-type Activities TotalAugust 31, August 31, August 31, August 31, August 31, August 31,

2003 2002 2003 2002 2003 2002RevenuesProgram revenues:

Charges for services 8,535,394$ 7,846,127$ $ 8,535,394$ 7,846,127$ Operating grants/contributions 47,839,475 34,520,241 47,839,475 34,520,241

General revenues:Property taxes 129,363,913 120,071,169 129,363,913 120,071,169 State revenue and grants 154,668,192 146,172,616 154,668,192 146,172,616 Other 2,163,099 3,510,609 2,163,099 3,510,609

Total revenues 342,570,073 312,120,762 342,570,073 312,120,762

ExpensesInstruction, curriculum 204,747,468 179,810,158 204,747,468 179,810,158

media servicesInstructional/school leadership 19,453,373 18,368,097 19,453,373 18,368,097 Student support services 22,812,171 21,135,911 22,812,171 21,135,911 Child nutrition 16,984,583 14,752,164 16,984,583 14,752,164 Cocurricular activities 3,749,275 2,976,248 3,749,275 2,976,248 General administration 8,969,993 8,057,668 27,056$ 8,997,049 8,057,668 Plant maintenance, security 30,852,824 29,692,054 30,852,824 29,692,054

and data processingCommunity services 1,316,285 1,197,952 1,316,285 1,197,952 Debt services 12,534,403 12,245,019 12,534,403 12,245,019 Other 1,731,044 2,809,258 1,731,044 2,809,258

Total expenses 323,151,419 291,044,529 27,056 323,178,475 291,044,529

Increase/(decrease) in net assets 19,418,654 21,076,233 (27,056) 19,391,598 21,076,233

Net assets - beginning 169,846,313 148,770,080 169,846,313 148,770,080 Net assets - ending 189,264,967$ 169,846,313$ (27,056)$ $ 189,237,911$ 169,846,313$

• Total expenses increased in almost all functions due to a salary increase of 3% on the midpoint for all

personnel, as well as additional personnel necessary for the implementation of full-day kindergarten and the opening of the District’s sixth intermediate campus.

• Total expenses above include depreciation of $13,249,467. Capital outlay of $36,372,335 is not

included in the above total expenses. In the government-wide financial statements, capital outlay is shown as an increase in the capital assets reported on the statement of net assets and depreciation expense is recorded in the statement of activities in order to spread recognition of the cost of capital assets over their useful lives.

Business-type activities. Business-type activities decreased the District’s net assets by $27,056. This negative position is the result of start-up costs for the District’s day care facility. The day care program will become fully operational in the 2003-04 fiscal year, recognizing revenue through fees charged to employees who utilize the program.

18

Management’s Discussion and Analysis (continued)

Financial Analysis of the District’s Funds As noted earlier, the District uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental funds. The focus of the District’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the District’s financing requirements. In particular, unreserved fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. As of the end of the current fiscal year, the District’s governmental funds reported combined ending fund balances of $86,782,237, a decrease of $3,869,317. Approximately 66% of this total amount ($57,001,529) constitutes unreserved, undesignated fund balance. The remainder of fund balance is reserved or designated to indicate that it is not available for new spending because it has already been committed 1) for inventory - $1,607,424, 2) to pay debt service - $2,613,826, 3) to liquidate purchase orders of the prior period - $322,603, 4) for food service - $5,105,670, and 5) for capital projects -$20,131,185. Offsetting the operating decrease in fund balance is an increase created by a prior period adjustment. This increase of $1,344,550 is the result of the District’s implementation of Governmental Accounting Standards Board Interpretation No. 6. Compensated absences not currently due and payable, which were previously accrued within the governmental funds will now be reported only in the government-wide statements. The general fund is the primary operating fund of the District. At the end of the current fiscal year, unreserved, undesignated fund balance of the general fund was $57,001,529, while the total fund balance was $62,076,216. As a measure of the general fund’s liquidity, it may be useful to compare unreserved, undesignated fund balance to the total fund expenditures. Unreserved, undesignated fund balance represents 22.2% of the total general fund expenditures. During the current fiscal year, the fund balance of the general fund increased by $10,629,201, exclusive of the prior period adjustment. Key factors related to this change are as follows:

• The District’s taxable value increased over $6.7 million providing approximately $113 million of tax revenue, or 42% of total general fund revenue.

• State funding of $150 million, or 56.1% of total general fund revenue, is earned based primarily

on average daily attendance (ADA). ADA increased by approximately 6% over the prior fiscal year.

• The majority (88.7%) of the District’s expenditures are for personnel costs. Personnel costs grew

during the current fiscal year due to a salary increase of 3% on the midpoint for all employees as well as an increase in the number of employees due to growth.

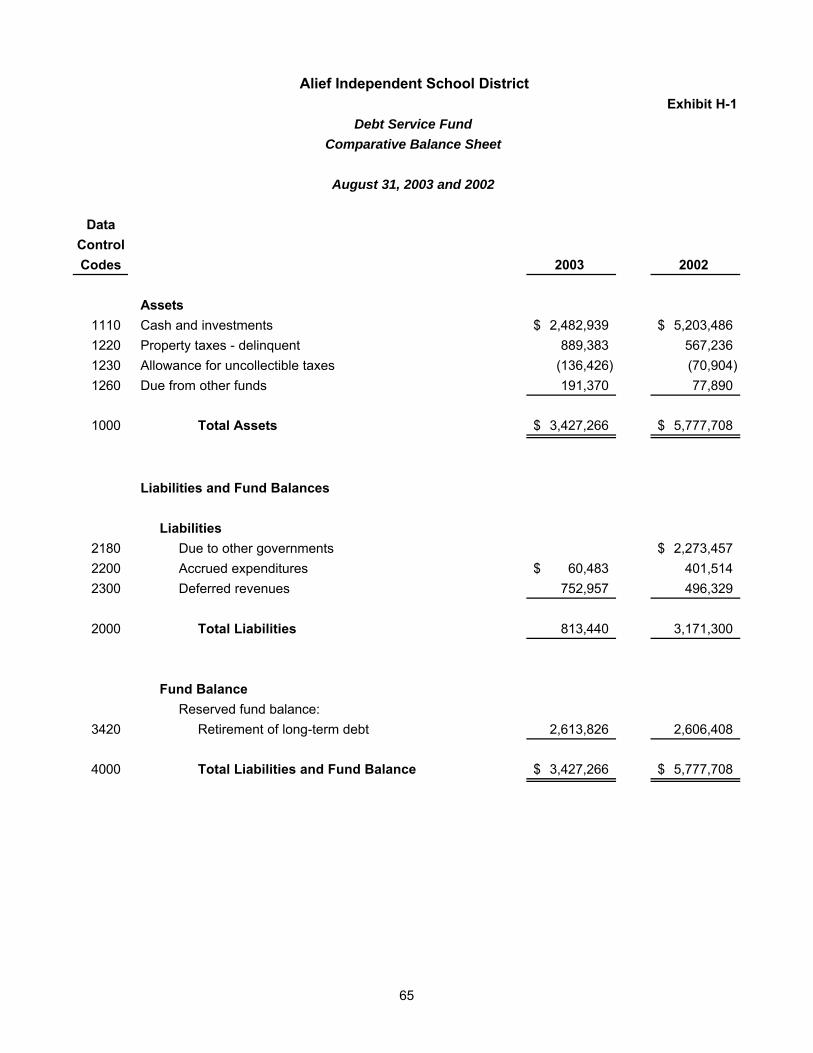

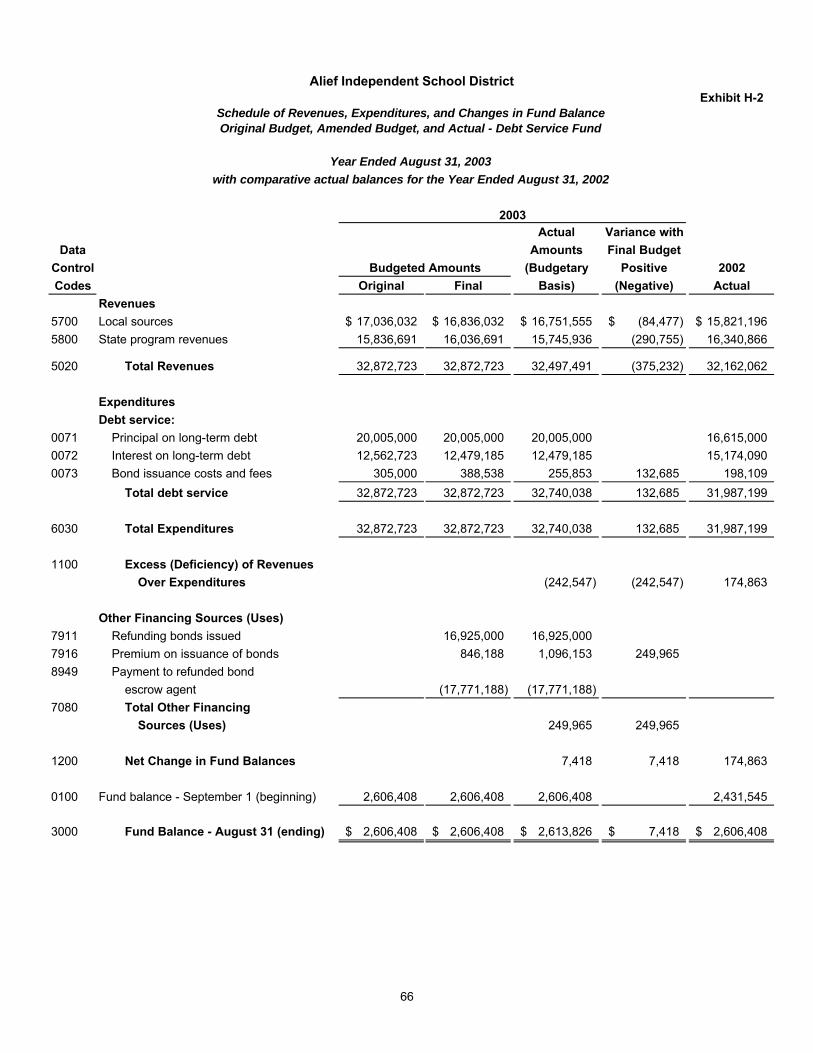

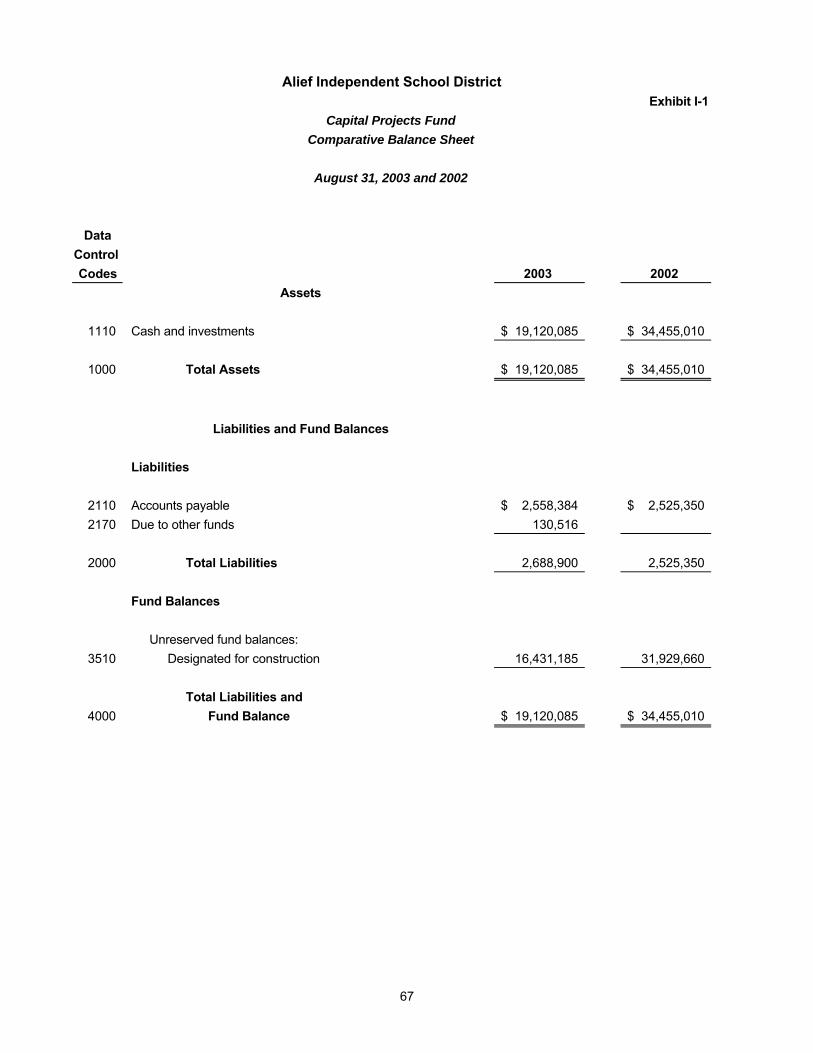

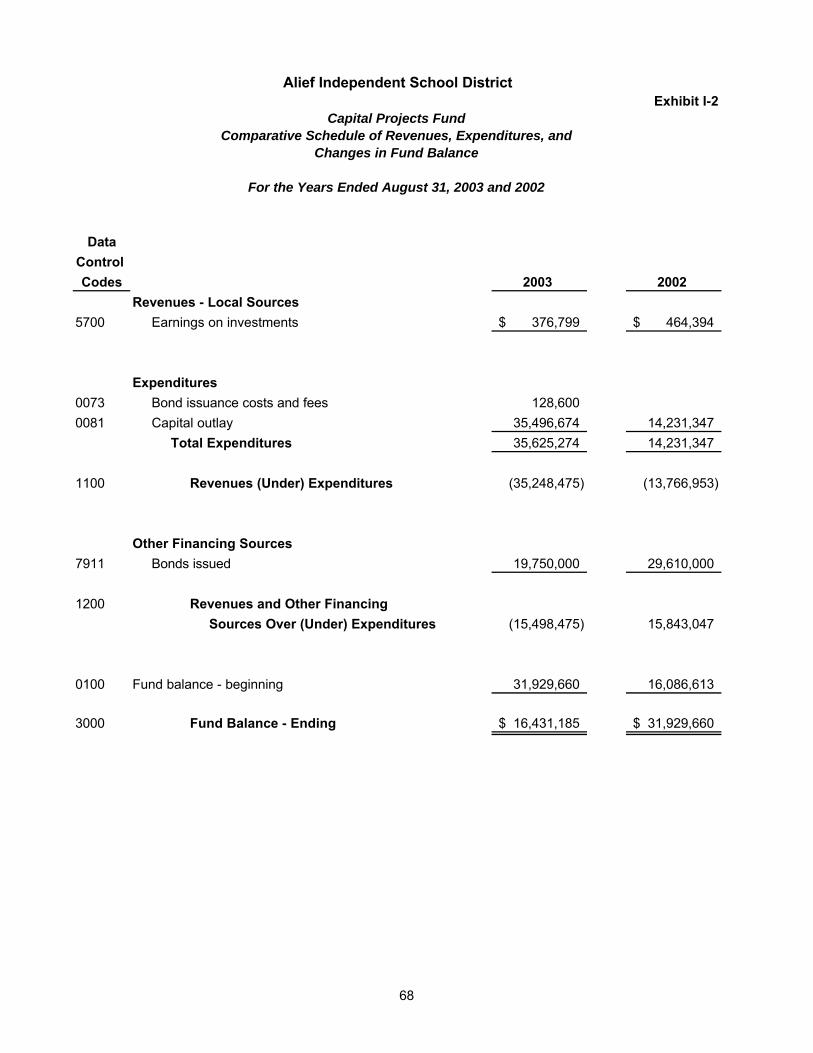

The debt service fund has a total fund balance of $2,613,826, all of which is reserved for the payment of debt service. The District’s goal is to maintain this fund balance at a fairly constant level; therefore, the tax rate for this fund was left unchanged at $0.215, resulting in revenues exceeding expenditures by only $7,418. Fund balance for the capital projects fund at August 31, 2003 was $16,431,185. As a result of unspent bond proceeds in previous years, the funds began the year with $31,929,660 in fund balance. The District received $19,750,000 in bond proceeds and spent $35,496,674 in the current year on capital outlay. The remaining fund balance is designated for future construction projects, including building additions at several elementary campuses and miscellaneous other campus projects.

19

Management’s Discussion and Analysis (continued)

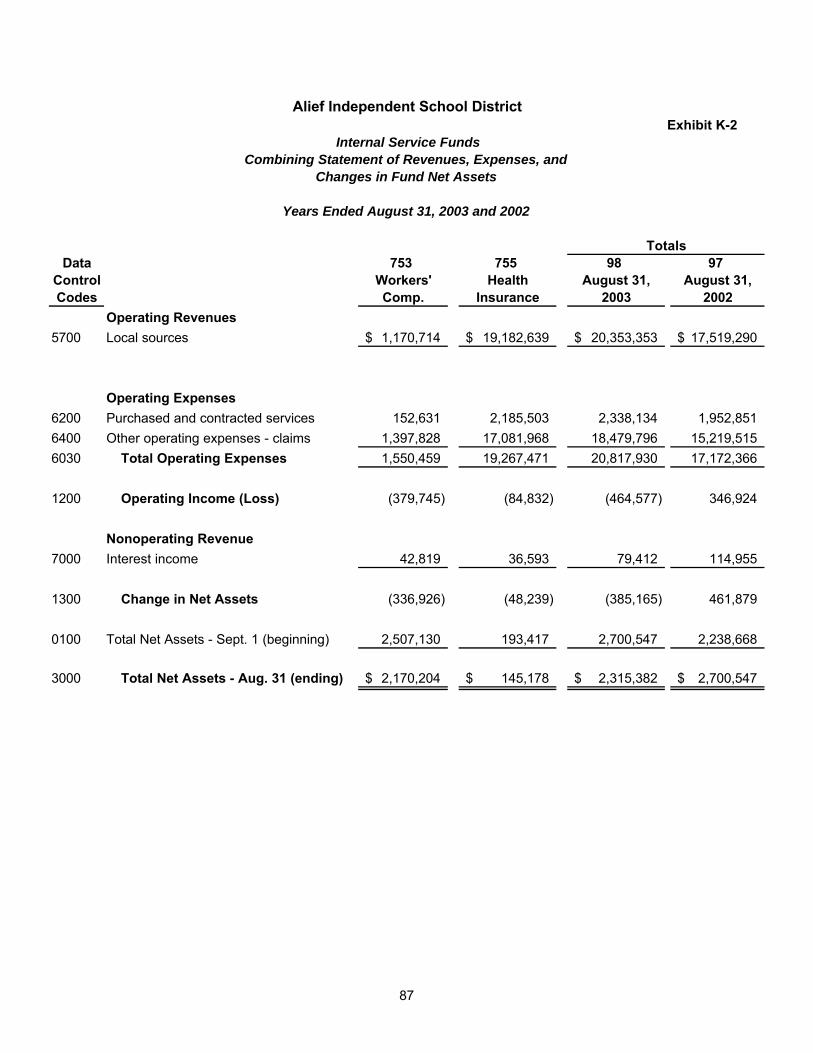

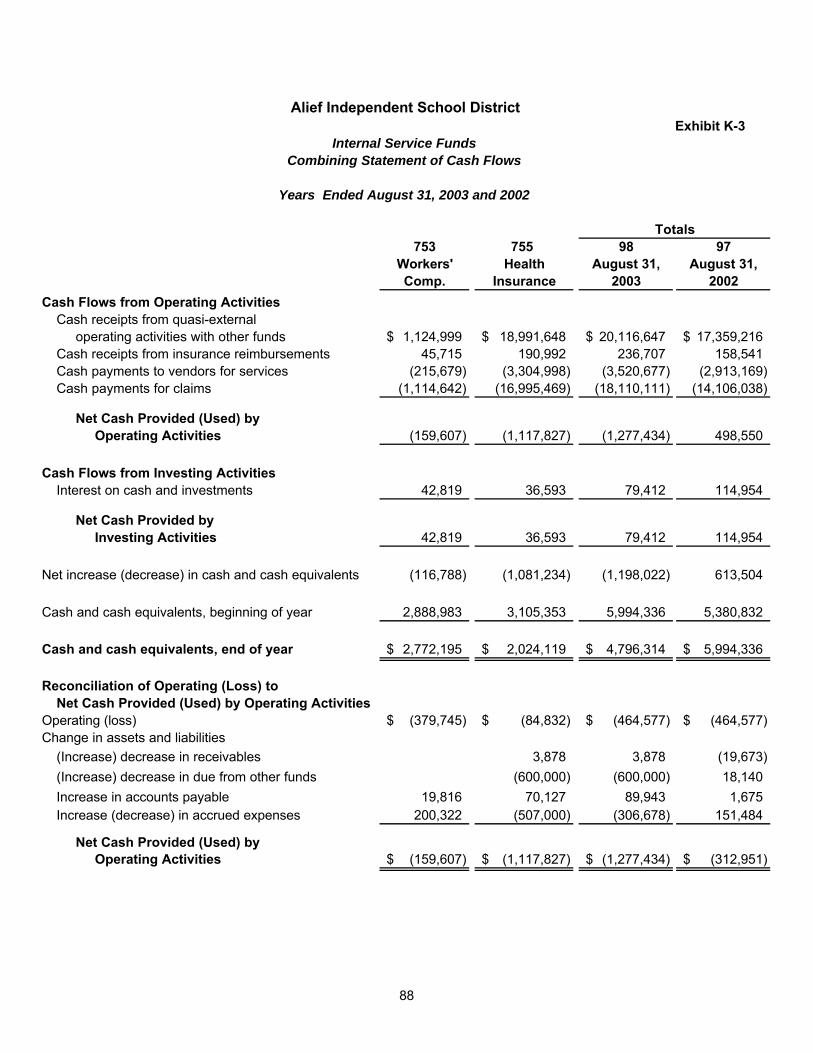

Proprietary Funds. The District’s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail. Unrestricted net assets of the District’s enterprise fund (day care facility) at the end of the year were negative in the amount of $70,419. As discussed earlier, this deficit position is the result of start up costs charged to the program, while operating fees will not be charged until the next fiscal year. The internal service fund used to account for the District’s self-funded insurance programs experienced a slight decrease in net assets from $2,700,547 to a balance of $2,315,382 at August 31, 2003.

General Fund Budgetary Highlights

Over the course of the year, District personnel recommended, and the Board of Trustees approved, several revisions to budgeted revenue and appropriations. Revisions to the revenue budget are necessary due to changes in estimates for local and state revenue, based on updated information concerning student attendance and tax collections. Revisions to appropriations are necessary due to staffing adjustments based on actual enrollment, changes in spending needs over the course of the year, and other unexpected occurrences. The District’s major budget amendments during the year are summarized as follows:

• The local revenue budget was decreased by $2.35 million due to an anticipated decline in the tax collection rate and a decrease in the estimated interest revenue because of falling interest rates.

• The state revenue budget was increased by approximately $5 million due primarily to an

increase in average daily attendance. The original budget was based on an ADA of 40,972. The final budget was based on an ADA of 41,369.

• The expenditure budget was decreased by a net of $1.8 million. This was due primarily to

decreased estimates for instructional payroll costs and reduced electrical costs realized as a result of the District’s participation in a local utility consortium.

After revenue budgets and appropriations were adjusted as described above, the District’s general fund balance of $62,076,216 differs from the final budgetary fund balance of $54,551,795 reported in the budgetary comparison schedule on page 55. This is primarily due to the following factors:

• Payroll costs were $2.1 million, or approximately 1%, less than the final budget. Factors such as unfilled positions and high turnover, resulting in hiring of less experienced teachers (at a lower than projected salary), caused this variance.

• Utilities were $1.75 million less than the final budget. In January 2002 the District entered

into a new contract through Region IV for energy services. The billing pattern was fairly erratic during the first few months as the new system was put into place. Although cost savings were realized in the second half of the 2001-2002 school year, savings surpassed estimates in 2002-2003.

Capital Asset and Debt Administration

Capital Assets The District’s investment in capital assets for its governmental and business-type activities as of August 31, 2003, amounts to $354,064,309 (net of accumulated depreciation of $196,389,274). This investment in capital assets includes facilities and equipment for instruction, transportation, athletics, administration, and maintenance. The total increase in the District’s investment in capital assets for the current year was 8 percent.

20

Management’s Discussion and Analysis (continued)

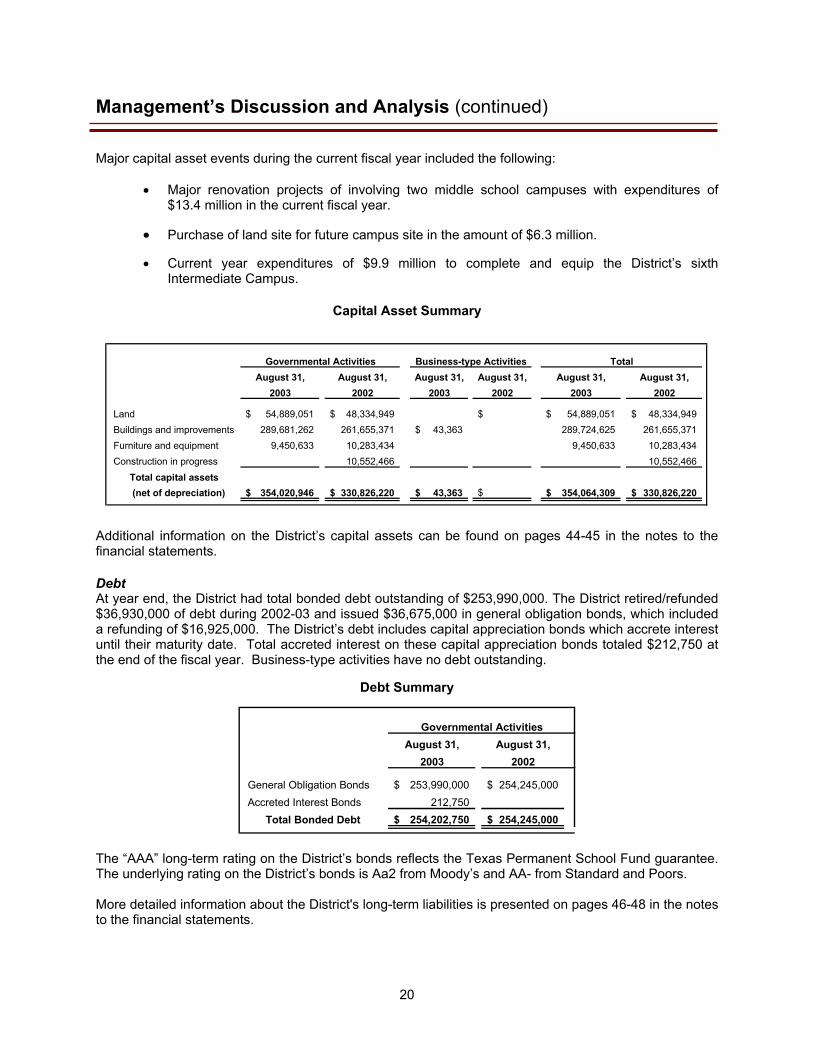

Major capital asset events during the current fiscal year included the following:

• Major renovation projects of involving two middle school campuses with expenditures of $13.4 million in the current fiscal year.

• Purchase of land site for future campus site in the amount of $6.3 million.

• Current year expenditures of $9.9 million to complete and equip the District’s sixth

Intermediate Campus.

Capital Asset Summary

Governmental Activities Business-type Activities TotalAugust 31, August 31, August 31, August 31, August 31, August 31,

2003 2002 2003 2002 2003 2002

Land 54,889,051$ 48,334,949$ $ 54,889,051$ 48,334,949$ Buildings and improvements 289,681,262 261,655,371 43,363$ 289,724,625 261,655,371 Furniture and equipment 9,450,633 10,283,434 9,450,633 10,283,434 Construction in progress 10,552,466 10,552,466

Total capital assets (net of depreciation) 354,020,946$ 330,826,220$ 43,363$ $ 354,064,309$ 330,826,220$

Additional information on the District’s capital assets can be found on pages 44-45 in the notes to the financial statements. Debt At year end, the District had total bonded debt outstanding of $253,990,000. The District retired/refunded $36,930,000 of debt during 2002-03 and issued $36,675,000 in general obligation bonds, which included a refunding of $16,925,000. The District’s debt includes capital appreciation bonds which accrete interest until their maturity date. Total accreted interest on these capital appreciation bonds totaled $212,750 at the end of the fiscal year. Business-type activities have no debt outstanding.

Debt Summary

Governmental ActivitiesAugust 31, August 31,

2003 2002

General Obligation Bonds 253,990,000$ 254,245,000$ Accreted Interest Bonds 212,750

Total Bonded Debt 254,202,750$ 254,245,000$

The “AAA” long-term rating on the District’s bonds reflects the Texas Permanent School Fund guarantee. The underlying rating on the District’s bonds is Aa2 from Moody’s and AA- from Standard and Poors. More detailed information about the District's long-term liabilities is presented on pages 46-48 in the notes to the financial statements.

21

Management’s Discussion and Analysis (continued)

Economic Factors and Next Year's Budgets and Rates

Economic factors can have a significant impact on the District’s finances. The unemployment rate for this region is 6.1% while the state and national rates are 6.0% and 6.5% percent, respectively. Increases in the unemployment rate could result in a reduction in the District’s tax collections. Inflationary trends in the region tend to be somewhat lower than the national consumer price index (CPI). This positive factor helps the District keep costs low, in general. However, two specific trends have required significant increases in school district expenditures. First, property insurance rates in the State have increased dramatically. Second, the teacher shortage in this area has mandated significant salary and benefit increases as Districts attempt to attract and retain the most qualified personnel. The District's elected and appointed officials considered many factors when setting the fiscal year 2004 general fund budget and tax rate. The adopted budget is based on the following significant assumptions:

• The District’s enrollment was projected to increase to 45,513, or approximately 1,443 students, at the time the budget was adopted. This estimate still appears reasonable based on a current enrollment (as of October 31, 2003) of 45,472.

• General fund expenditures are budgeted to increase by $12.6 million over the final 2002-03

budget. Major factors causing this increase include:

o Salary increase of 4% on the midpoint for all personnel, costing approximately $8.5 million.

o The addition of other new personnel units, due primarily to the opening of Budewig Intermediate, are estimated to cost approximately $4.1 million.

If these estimates are realized, the District's budgetary General Fund balance is expected to remain fairly constant at the close of 2004.

Requests for Information This financial report is designed to provide our citizens, taxpayers, customers, investors, and creditors with a general overview of the District's finances and to show the District's accountability for the money it receives. Questions concerning any of the information provided in this report, or requests for additional information, should be addressed to the Office of the Assistant Superintendent for Finance, Alief I.S.D., 12302 High Star, Houston, Texas, 77072.

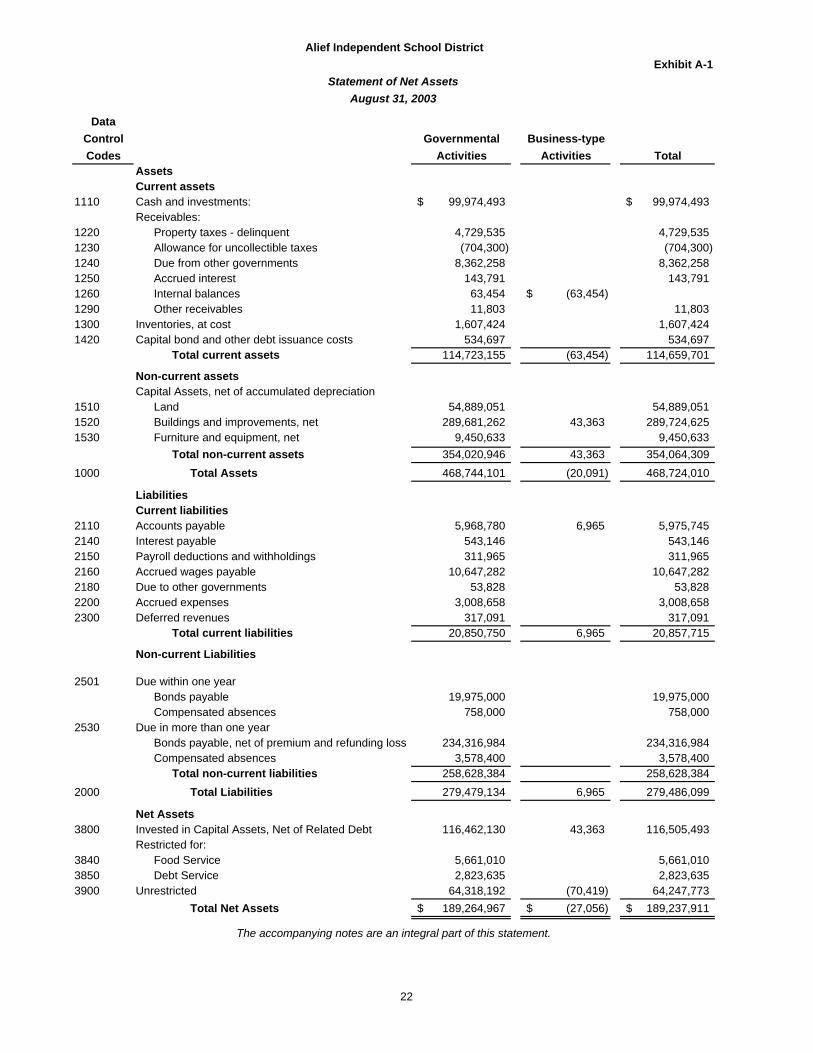

Exhibit A-1

DataControl Governmental Business-typeCodes Activities Activities Total

Current assets1110 Cash and investments: 99,974,493$ 99,974,493$

Receivables:1220 Property taxes - delinquent 4,729,535 4,729,535 1230 Allowance for uncollectible taxes (704,300) (704,300)1240 Due from other governments 8,362,258 8,362,258 1250 Accrued interest 143,791 143,791 1260 Internal balances 63,454 (63,454)$ 1290 Other receivables 11,803 11,803 1300 Inventories, at cost 1,607,424 1,607,424 1420 Capital bond and other debt issuance costs 534,697 534,697

Total current assets 114,723,155 (63,454) 114,659,701

Non-current assetsCapital Assets, net of accumulated depreciation

1510 Land 54,889,051 54,889,051 1520 Buildings and improvements, net 289,681,262 43,363 289,724,625 1530 Furniture and equipment, net 9,450,633 9,450,633

Total non-current assets 354,020,946 43,363 354,064,309 1000 Total Assets 468,744,101 (20,091) 468,724,010

Current liabilities2110 Accounts payable 5,968,780 6,965 5,975,745 2140 Interest payable 543,146 543,146 2150 Payroll deductions and withholdings 311,965 311,965 2160 Accrued wages payable 10,647,282 10,647,282 2180 Due to other governments 53,828 53,828 2200 Accrued expenses 3,008,658 3,008,658 2300 Deferred revenues 317,091 317,091

Total current liabilities 20,850,750 6,965 20,857,715

Non-current Liabilities

2501 Due within one yearBonds payable 19,975,000 19,975,000 Compensated absences 758,000 758,000

2530 Due in more than one yearBonds payable, net of premium and refunding loss 234,316,984 234,316,984 Compensated absences 3,578,400 3,578,400

Total non-current liabilities 258,628,384 258,628,384 2000 Total Liabilities 279,479,134 6,965 279,486,099

Net Assets3800 Invested in Capital Assets, Net of Related Debt 116,462,130 43,363 116,505,493

Restricted for:3840 Food Service 5,661,010 5,661,0103850 Debt Service 2,823,635 2,823,635 3900 Unrestricted 64,318,192 (70,419) 64,247,773

Total Net Assets 189,264,967$ (27,056)$ 189,237,911$

The accompanying notes are an integral part of this statement.

Assets

Liabilities

Alief Independent School District

Statement of Net AssetsAugust 31, 2003

22

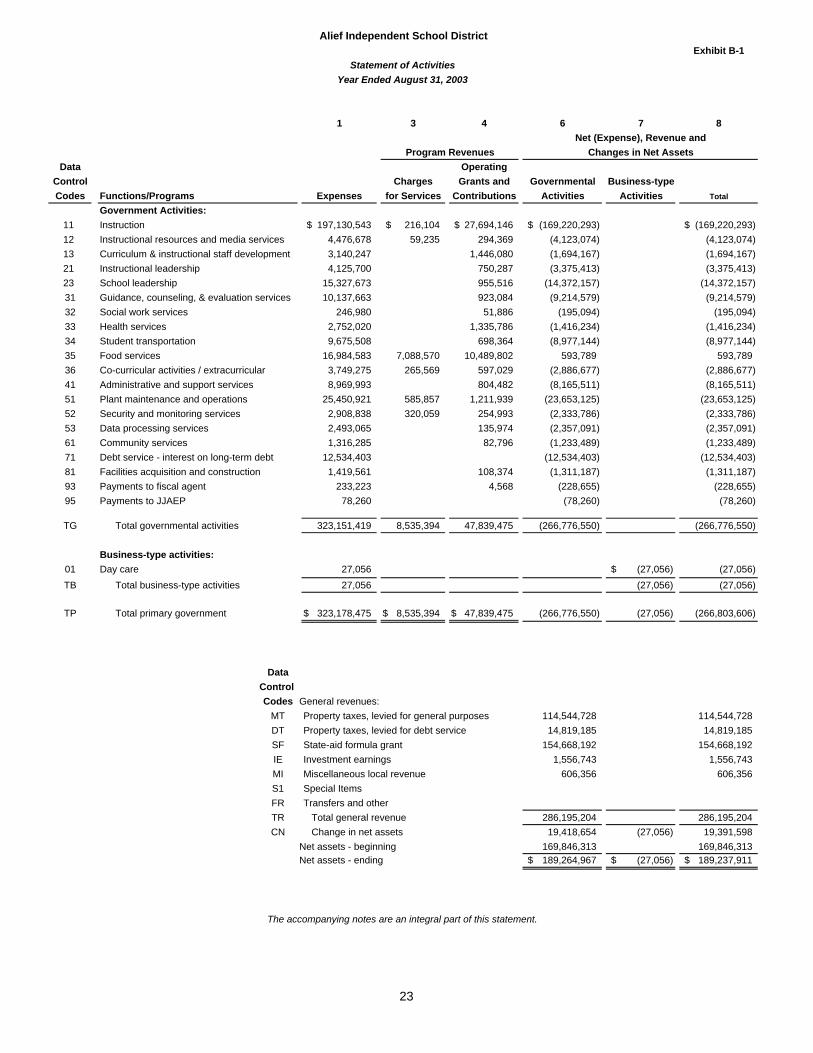

Exhibit B-1

1 3 4 6 7 8Net (Expense), Revenue and

Changes in Net AssetsData Operating

Control Charges Grants and Governmental Business-typeCodes Functions/Programs Expenses for Services Contributions Activities Activities Total

11 Instruction 197,130,543$ 216,104$ 27,694,146$ (169,220,293)$ (169,220,293)$ 12 Instructional resources and media services 4,476,678 59,235 294,369 (4,123,074) (4,123,074) 13 Curriculum & instructional staff development 3,140,247 1,446,080 (1,694,167) (1,694,167) 21 Instructional leadership 4,125,700 750,287 (3,375,413) (3,375,413) 23 School leadership 15,327,673 955,516 (14,372,157) (14,372,157) 31 Guidance, counseling, & evaluation services 10,137,663 923,084 (9,214,579) (9,214,579) 32 Social work services 246,980 51,886 (195,094) (195,094) 33 Health services 2,752,020 1,335,786 (1,416,234) (1,416,234) 34 Student transportation 9,675,508 698,364 (8,977,144) (8,977,144) 35 Food services 16,984,583 7,088,570 10,489,802 593,789 593,789 36 Co-curricular activities / extracurricular 3,749,275 265,569 597,029 (2,886,677) (2,886,677) 41 Administrative and support services 8,969,993 804,482 (8,165,511) (8,165,511) 51 Plant maintenance and operations 25,450,921 585,857 1,211,939 (23,653,125) (23,653,125) 52 Security and monitoring services 2,908,838 320,059 254,993 (2,333,786) (2,333,786) 53 Data processing services 2,493,065 135,974 (2,357,091) (2,357,091) 61 Community services 1,316,285 82,796 (1,233,489) (1,233,489) 71 Debt service - interest on long-term debt 12,534,403 (12,534,403) (12,534,403) 81 Facilities acquisition and construction 1,419,561 108,374 (1,311,187) (1,311,187) 93 Payments to fiscal agent 233,223 4,568 (228,655) (228,655) 95 Payments to JJAEP 78,260 (78,260) (78,260)

TG Total governmental activities 323,151,419 8,535,394 47,839,475 (266,776,550) (266,776,550)

Business-type activities:01 Day care 27,056 (27,056)$ (27,056)TB Total business-type activities 27,056 (27,056) (27,056)

TP Total primary government 323,178,475$ 8,535,394$ 47,839,475$ (266,776,550) (27,056) (266,803,606)

DataControl Codes General revenues:

MT Property taxes, levied for general purposes 114,544,728 114,544,728 DT Property taxes, levied for debt service 14,819,185 14,819,185SF State-aid formula grant 154,668,192 154,668,192IE Investment earnings 1,556,743 1,556,743MI Miscellaneous local revenue 606,356 606,356S1 Special ItemsFR Transfers and otherTR Total general revenue 286,195,204 286,195,204 CN Change in net assets 19,418,654 (27,056) 19,391,598

Net assets - beginning 169,846,313 169,846,313 Net assets - ending 189,264,967$ (27,056)$ 189,237,911$

Alief Independent School District

Statement of ActivitiesYear Ended August 31, 2003

The accompanying notes are an integral part of this statement.

Program Revenues

Government Activities:

23

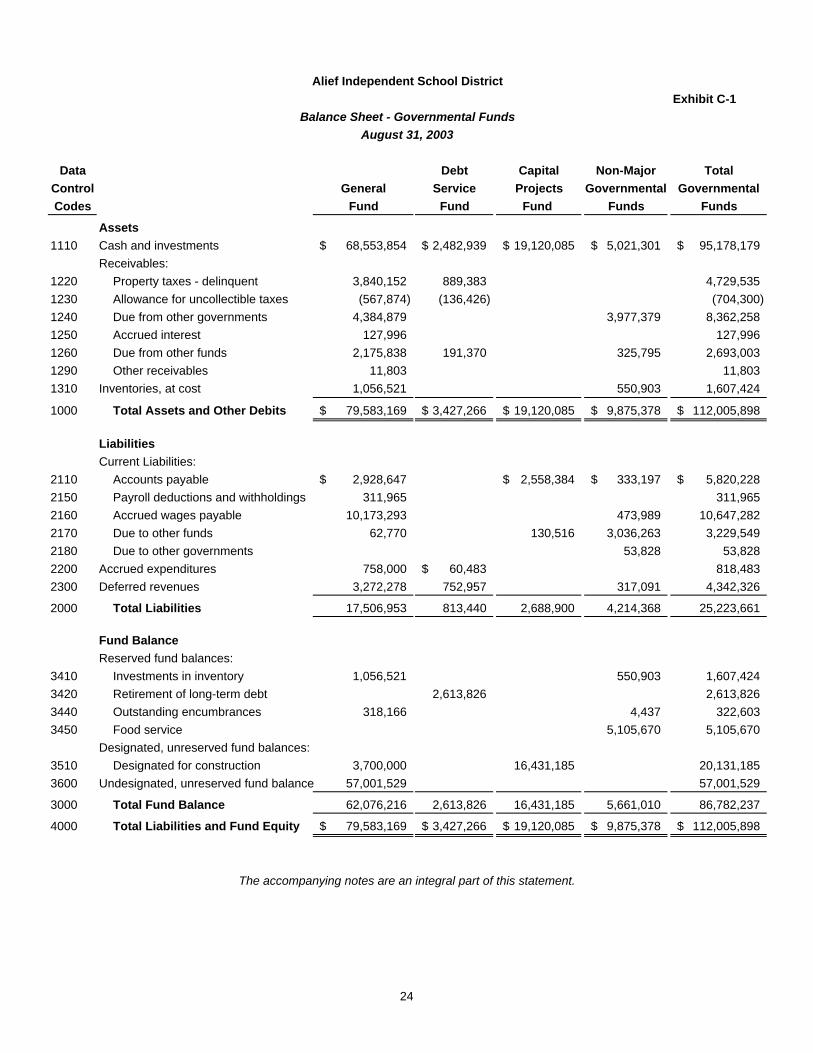

Exhibit C-1

Data Debt Capital Non-Major TotalControl General Service Projects Governmental GovernmentalCodes Fund Fund Fund Funds Funds

1110 Cash and investments 68,553,854$ 2,482,939$ 19,120,085$ 5,021,301$ 95,178,179$ Receivables:

1220 Property taxes - delinquent 3,840,152 889,383 4,729,5351230 Allowance for uncollectible taxes (567,874) (136,426) (704,300)1240 Due from other governments 4,384,879 3,977,379 8,362,2581250 Accrued interest 127,996 127,9961260 Due from other funds 2,175,838 191,370 325,795 2,693,0031290 Other receivables 11,803 11,8031310 Inventories, at cost 1,056,521 550,903 1,607,424

1000 Total Assets and Other Debits 79,583,169$ 3,427,266$ 19,120,085$ 9,875,378$ 112,005,898$

Current Liabilities:2110 Accounts payable 2,928,647$ 2,558,384$ 333,197$ 5,820,228$ 2150 Payroll deductions and withholdings 311,965 311,965 2160 Accrued wages payable 10,173,293 473,989 10,647,282 2170 Due to other funds 62,770 130,516 3,036,263 3,229,549 2180 Due to other governments 53,828 53,828 2200 Accrued expenditures 758,000 60,483$ 818,483 2300 Deferred revenues 3,272,278 752,957 317,091 4,342,326

2000 Total Liabilities 17,506,953 813,440 2,688,900 4,214,368 25,223,661

Fund BalanceReserved fund balances:

3410 Investments in inventory 1,056,521 550,903 1,607,424 3420 Retirement of long-term debt 2,613,826 2,613,826 3440 Outstanding encumbrances 318,166 4,437 322,603 3450 Food service 5,105,670 5,105,670

Designated, unreserved fund balances:3510 Designated for construction 3,700,000 16,431,185 20,131,185 3600 Undesignated, unreserved fund balance 57,001,529 57,001,529

3000 Total Fund Balance 62,076,216 2,613,826 16,431,185 5,661,010 86,782,237

4000 Total Liabilities and Fund Equity 79,583,169$ 3,427,266$ 19,120,085$ 9,875,378$ 112,005,898$

The accompanying notes are an integral part of this statement.

Assets

Liabilities

Alief Independent School District

Balance Sheet - Governmental FundsAugust 31, 2003

24

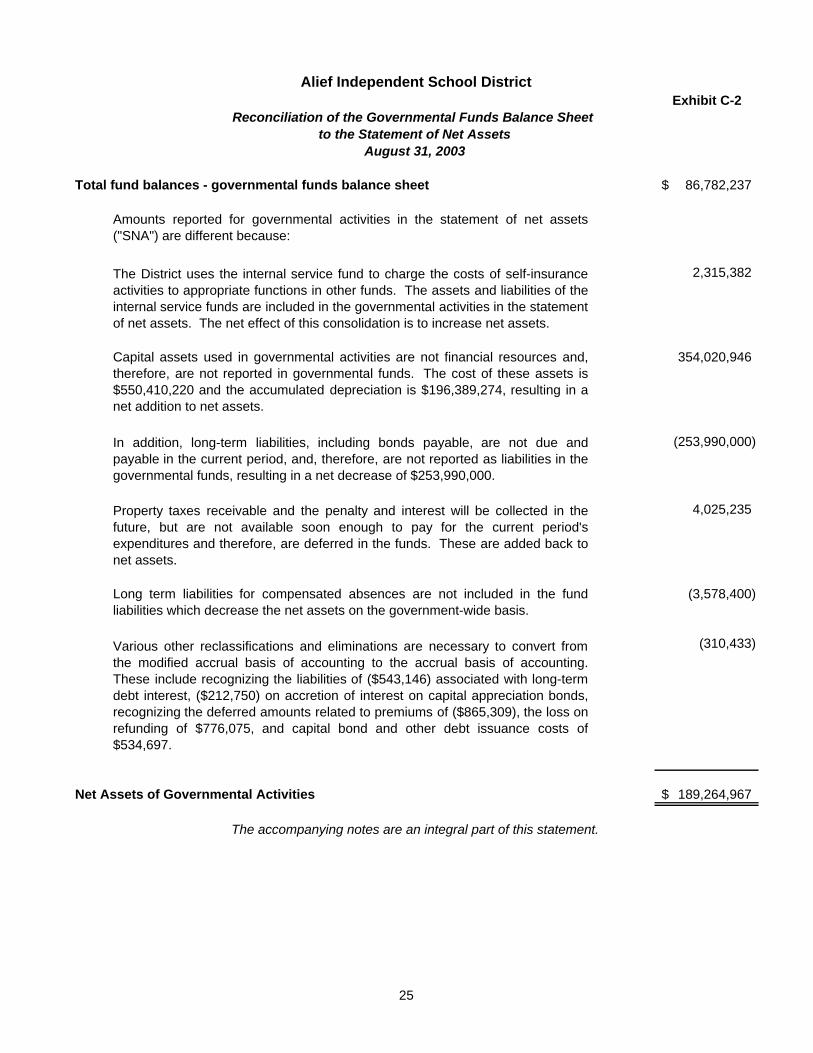

Exhibit C-2

Total fund balances - governmental funds balance sheet 86,782,237$

2,315,382

354,020,946

(253,990,000)

4,025,235

(3,578,400)

(310,433)

Net Assets of Governmental Activities 189,264,967$

The accompanying notes are an integral part of this statement.

Capital assets used in governmental activities are not financial resources and,therefore, are not reported in governmental funds. The cost of these assets is$550,410,220 and the accumulated depreciation is $196,389,274, resulting in anet addition to net assets.

In addition, long-term liabilities, including bonds payable, are not due andpayable in the current period, and, therefore, are not reported as liabilities in thegovernmental funds, resulting in a net decrease of $253,990,000.

Property taxes receivable and the penalty and interest will be collected in thefuture, but are not available soon enough to pay for the current period'sexpenditures and therefore, are deferred in the funds. These are added back tonet assets.

Long term liabilities for compensated absences are not included in the fundliabilities which decrease the net assets on the government-wide basis.

The District uses the internal service fund to charge the costs of self-insuranceactivities to appropriate functions in other funds. The assets and liabilities of theinternal service funds are included in the governmental activities in the statementof net assets. The net effect of this consolidation is to increase net assets.

Various other reclassifications and eliminations are necessary to convert fromthe modified accrual basis of accounting to the accrual basis of accounting.These include recognizing the liabilities of ($543,146) associated with long-termdebt interest, ($212,750) on accretion of interest on capital appreciation bonds,recognizing the deferred amounts related to premiums of ($865,309), the loss onrefunding of $776,075, and capital bond and other debt issuance costs of$534,697.

Alief Independent School District

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets

August 31, 2003

Amounts reported for governmental activities in the statement of net assets("SNA") are different because:

25

This page intentionally blank.

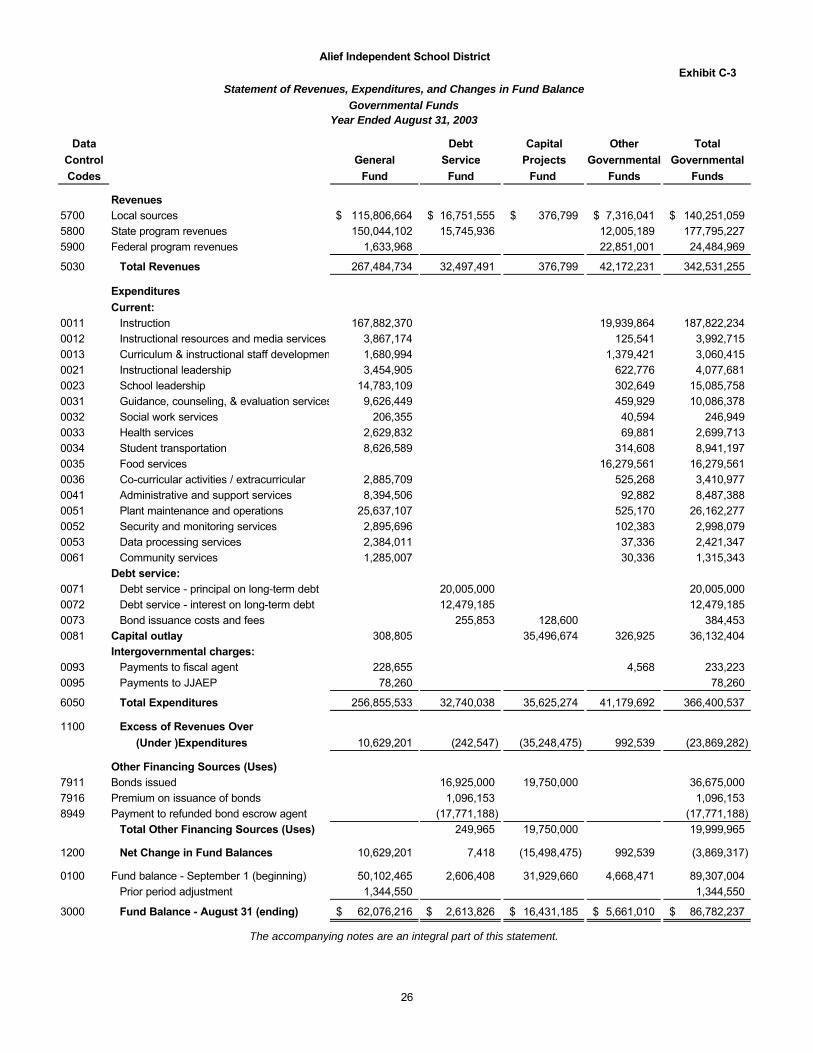

Exhibit C-3

Data Debt Capital Other TotalControl General Service Projects Governmental GovernmentalCodes Fund Fund Fund Funds Funds

Revenues5700 Local sources 115,806,664$ 16,751,555$ 376,799$ 7,316,041$ 140,251,059$ 5800 State program revenues 150,044,102 15,745,936 12,005,189 177,795,2275900 Federal program revenues 1,633,968 22,851,001 24,484,969

5030 Total Revenues 267,484,734 32,497,491 376,799 42,172,231 342,531,255

ExpendituresCurrent:

0011 Instruction 167,882,370 19,939,864 187,822,2340012 Instructional resources and media services 3,867,174 125,541 3,992,7150013 Curriculum & instructional staff development 1,680,994 1,379,421 3,060,4150021 Instructional leadership 3,454,905 622,776 4,077,6810023 School leadership 14,783,109 302,649 15,085,7580031 Guidance, counseling, & evaluation services 9,626,449 459,929 10,086,3780032 Social work services 206,355 40,594 246,9490033 Health services 2,629,832 69,881 2,699,7130034 Student transportation 8,626,589 314,608 8,941,1970035 Food services 16,279,561 16,279,5610036 Co-curricular activities / extracurricular 2,885,709 525,268 3,410,9770041 Administrative and support services 8,394,506 92,882 8,487,3880051 Plant maintenance and operations 25,637,107 525,170 26,162,2770052 Security and monitoring services 2,895,696 102,383 2,998,0790053 Data processing services 2,384,011 37,336 2,421,3470061 Community services 1,285,007 30,336 1,315,343

Debt service:0071 Debt service - principal on long-term debt 20,005,000 20,005,0000072 Debt service - interest on long-term debt 12,479,185 12,479,1850073 Bond issuance costs and fees 255,853 128,600 384,4530081 Capital outlay 308,805 35,496,674 326,925 36,132,404

Intergovernmental charges:0093 Payments to fiscal agent 228,655 4,568 233,2230095 Payments to JJAEP 78,260 78,260

6050 Total Expenditures 256,855,533 32,740,038 35,625,274 41,179,692 366,400,537

1100 Excess of Revenues Over(Under )Expenditures 10,629,201 (242,547) (35,248,475) 992,539 (23,869,282)

Other Financing Sources (Uses)7911 Bonds issued 16,925,000 19,750,000 36,675,0007916 Premium on issuance of bonds 1,096,153 1,096,1538949 Payment to refunded bond escrow agent (17,771,188) (17,771,188)

Total Other Financing Sources (Uses) 249,965 19,750,000 19,999,965

1200 Net Change in Fund Balances 10,629,201 7,418 (15,498,475) 992,539 (3,869,317)

0100 Fund balance - September 1 (beginning) 50,102,465 2,606,408 31,929,660 4,668,471 89,307,004Prior period adjustment 1,344,550 1,344,550

3000 Fund Balance - August 31 (ending) 62,076,216$ 2,613,826$ 16,431,185$ 5,661,010$ 86,782,237$

The accompanying notes are an integral part of this statement.

Alief Independent School District

Statement of Revenues, Expenditures, and Changes in Fund BalanceGovernmental Funds

Year Ended August 31, 2003

26

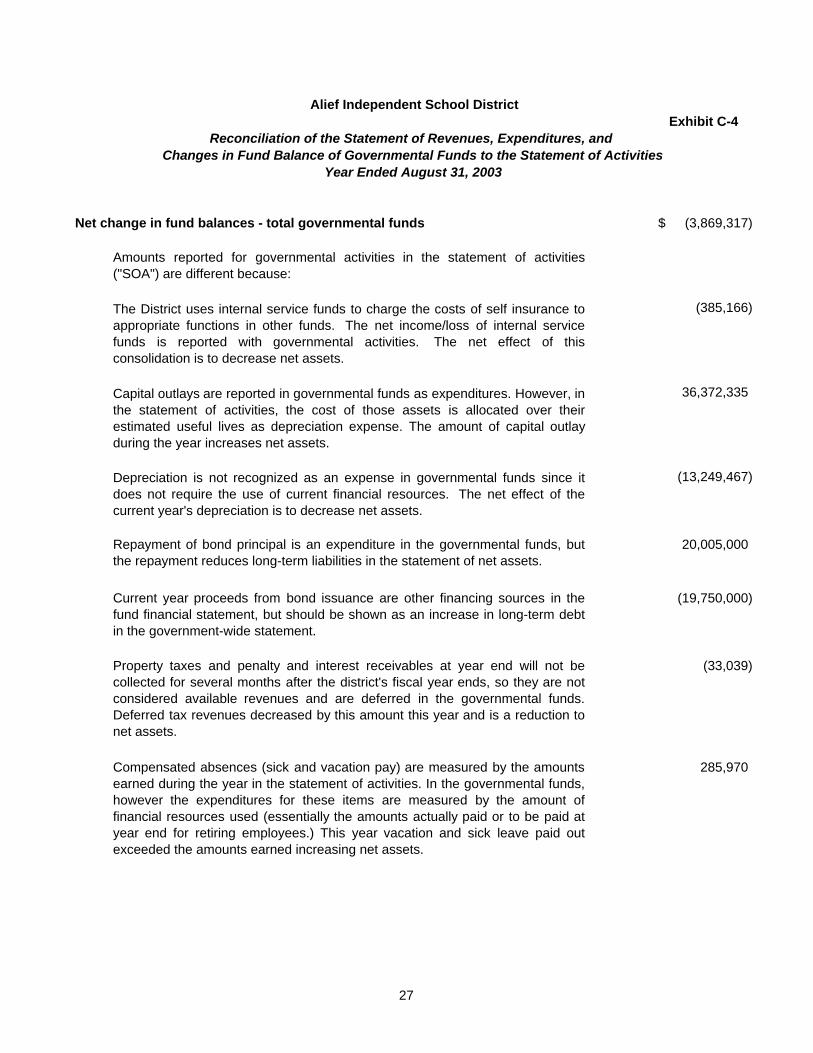

Exhibit C-4

Net change in fund balances - total governmental funds (3,869,317)$

(385,166)

36,372,335

(13,249,467)

20,005,000

(19,750,000)

(33,039)

285,970

Alief Independent School District

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balance of Governmental Funds to the Statement of Activities

Year Ended August 31, 2003

Property taxes and penalty and interest receivables at year end will not becollected for several months after the district's fiscal year ends, so they are notconsidered available revenues and are deferred in the governmental funds.Deferred tax revenues decreased by this amount this year and is a reduction tonet assets.

Compensated absences (sick and vacation pay) are measured by the amountsearned during the year in the statement of activities. In the governmental funds,however the expenditures for these items are measured by the amount offinancial resources used (essentially the amounts actually paid or to be paid atyear end for retiring employees.) This year vacation and sick leave paid outexceeded the amounts earned increasing net assets.

Amounts reported for governmental activities in the statement of activities("SOA") are different because:

The District uses internal service funds to charge the costs of self insurance toappropriate functions in other funds. The net income/loss of internal servicefunds is reported with governmental activities. The net effect of thisconsolidation is to decrease net assets.

Capital outlays are reported in governmental funds as expenditures. However, inthe statement of activities, the cost of those assets is allocated over theirestimated useful lives as depreciation expense. The amount of capital outlayduring the year increases net assets.

Depreciation is not recognized as an expense in governmental funds since itdoes not require the use of current financial resources. The net effect of thecurrent year's depreciation is to decrease net assets.

Repayment of bond principal is an expenditure in the governmental funds, butthe repayment reduces long-term liabilities in the statement of net assets.

Current year proceeds from bond issuance are other financing sources in thefund financial statement, but should be shown as an increase in long-term debtin the government-wide statement.

27

Net change in fund balances - total governmental funds (continued)

13,844

270,426

(205,000)

(36,932)

Change in Net Assets of Governmental Activities 19,418,654$

Bond issuance costs, deferred charges on bond refunding, and other debtcharges which are treated as expenditures in the fund basis are set up as assets and amortized in the statement of net assets. The net change for bond issuancecosts, deferred charges, and amortization is an increase in net assets.

Various other reclassifications and eliminations are necessary to convert fromthe modified accrual basis of accounting to the accrual basis of accounting.Amounts recognized in the governmental fund basis and the statement of netassts differ due to sales and retirement of assets.

The accompanying notes are an integral part of this statement.

An accrual for interest expense is not recognized in the governmental fund basisbut is in the statement of activities. Interest accrual includes interest on longterm debt and accreted interest on capital appreciation bonds. The interestaccrual was lower this year than last year thereby increasing net assets.

Proceeds on capital appreciation bonds are included in other sources in the fundfinancials, but are set up as a long term liability in statement of net assets.

28

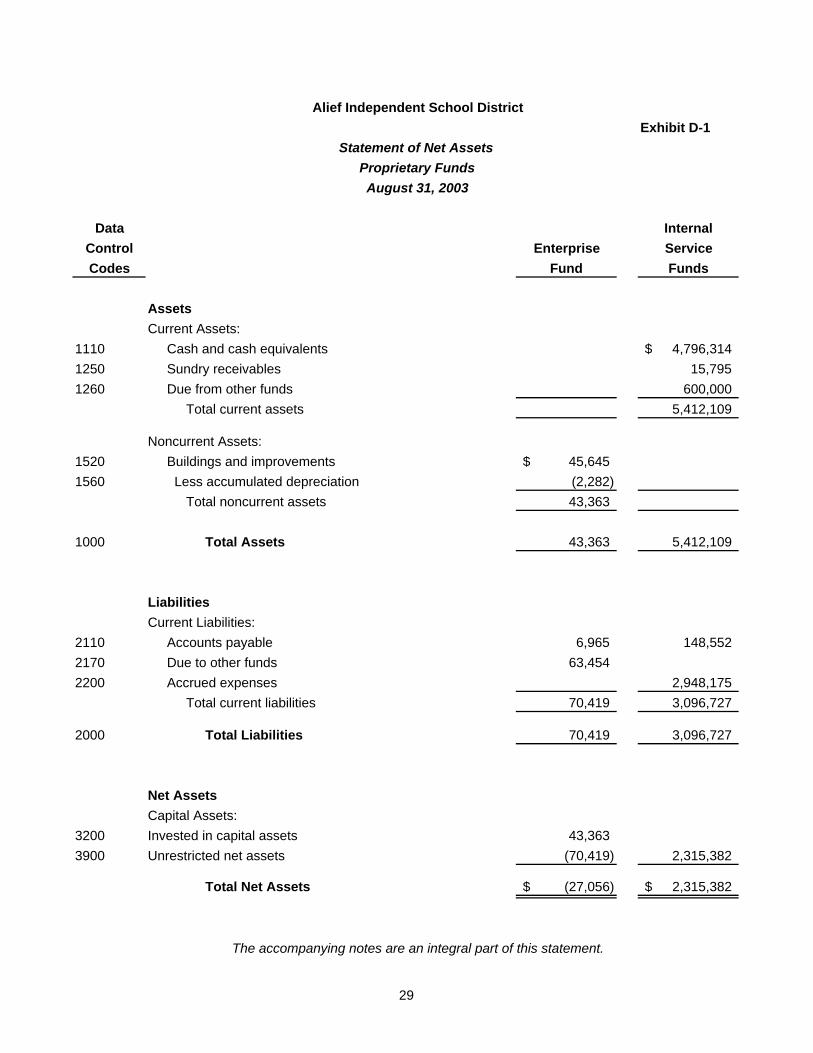

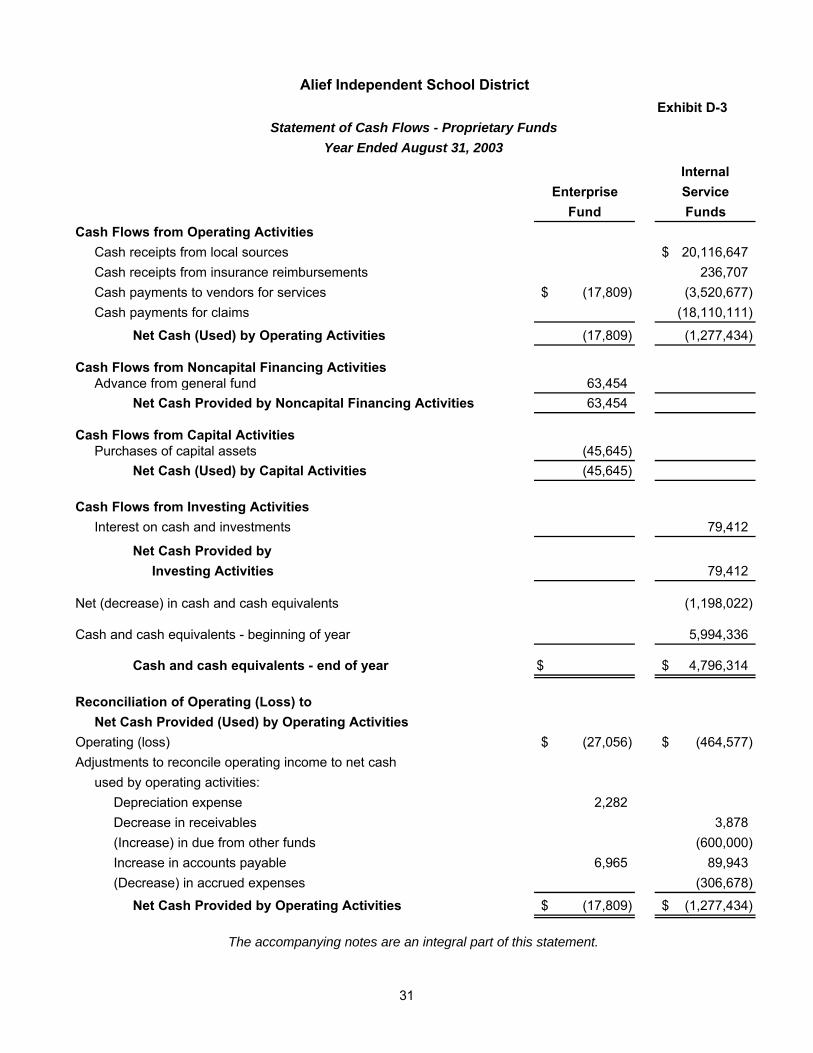

Exhibit D-1

Data InternalControl Enterprise ServiceCodes Fund Funds

AssetsCurrent Assets:

1110 Cash and cash equivalents 4,796,314$ 1250 Sundry receivables 15,795 1260 Due from other funds 600,000

Total current assets 5,412,109

Noncurrent Assets:1520 Buildings and improvements 45,645$ 1560 Less accumulated depreciation (2,282)

Total noncurrent assets 43,363

1000 Total Assets 43,363 5,412,109

LiabilitiesCurrent Liabilities:

2110 Accounts payable 6,965 148,552 2170 Due to other funds 63,4542200 Accrued expenses 2,948,175

Total current liabilities 70,419 3,096,727

2000 Total Liabilities 70,419 3,096,727

Net AssetsCapital Assets:

3200 Invested in capital assets 43,363 3900 Unrestricted net assets (70,419) 2,315,382

Total Net Assets (27,056)$ 2,315,382$

The accompanying notes are an integral part of this statement.

Alief Independent School District

Statement of Net Assets

August 31, 2003Proprietary Funds

29

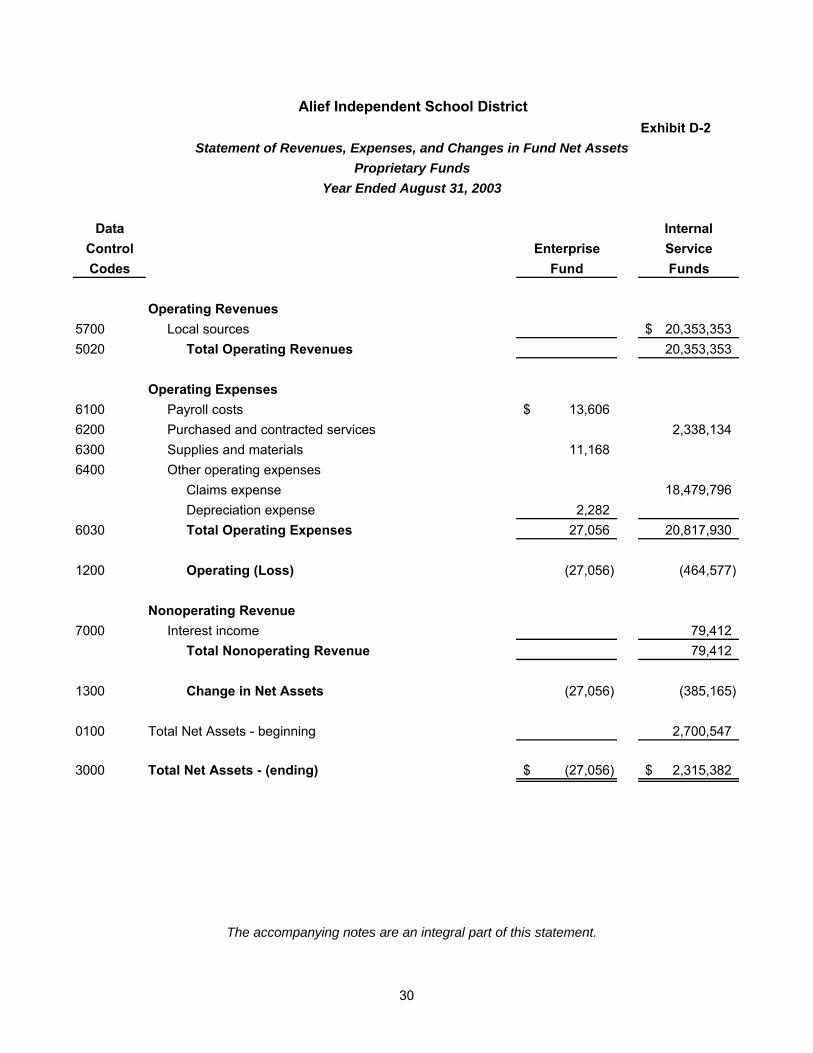

Exhibit D-2

Data InternalControl Enterprise ServiceCodes Fund Funds

Operating Revenues5700 Local sources 20,353,353$ 5020 Total Operating Revenues 20,353,353

Operating Expenses6100 Payroll costs 13,606$ 6200 Purchased and contracted services 2,338,1346300 Supplies and materials 11,1686400 Other operating expenses

Claims expense 18,479,796Depreciation expense 2,282

6030 Total Operating Expenses 27,056 20,817,930

1200 Operating (Loss) (27,056) (464,577)

Nonoperating Revenue7000 Interest income 79,412

Total Nonoperating Revenue 79,412

1300 Change in Net Assets (27,056) (385,165)

0100 Total Net Assets - beginning 2,700,547

3000 Total Net Assets - (ending) (27,056)$ 2,315,382$

The accompanying notes are an integral part of this statement.

Alief Independent School District

Statement of Revenues, Expenses, and Changes in Fund Net AssetsProprietary Funds

Year Ended August 31, 2003

30

Exhibit D-3

InternalEnterprise Service

Fund FundsCash Flows from Operating Activities

Cash receipts from local sources 20,116,647$ Cash receipts from insurance reimbursements 236,707 Cash payments to vendors for services (17,809)$ (3,520,677)Cash payments for claims (18,110,111)

Net Cash (Used) by Operating Activities (17,809) (1,277,434)

Cash Flows from Noncapital Financing ActivitiesAdvance from general fund 63,454

Net Cash Provided by Noncapital Financing Activities 63,454

Cash Flows from Capital ActivitiesPurchases of capital assets (45,645)

Net Cash (Used) by Capital Activities (45,645)

Cash Flows from Investing ActivitiesInterest on cash and investments 79,412

Net Cash Provided byInvesting Activities 79,412

Net (decrease) in cash and cash equivalents (1,198,022)

Cash and cash equivalents - beginning of year 5,994,336

Cash and cash equivalents - end of year $ 4,796,314$

Reconciliation of Operating (Loss) to Net Cash Provided (Used) by Operating Activities

Operating (loss) (27,056)$ (464,577)$ Adjustments to reconcile operating income to net cash

used by operating activities:Depreciation expense 2,282Decrease in receivables 3,878(Increase) in due from other funds (600,000)Increase in accounts payable 6,965 89,943(Decrease) in accrued expenses (306,678)

Net Cash Provided by Operating Activities (17,809)$ (1,277,434)$

The accompanying notes are an integral part of this statement.

Alief Independent School District

Statement of Cash Flows - Proprietary FundsYear Ended August 31, 2003

31

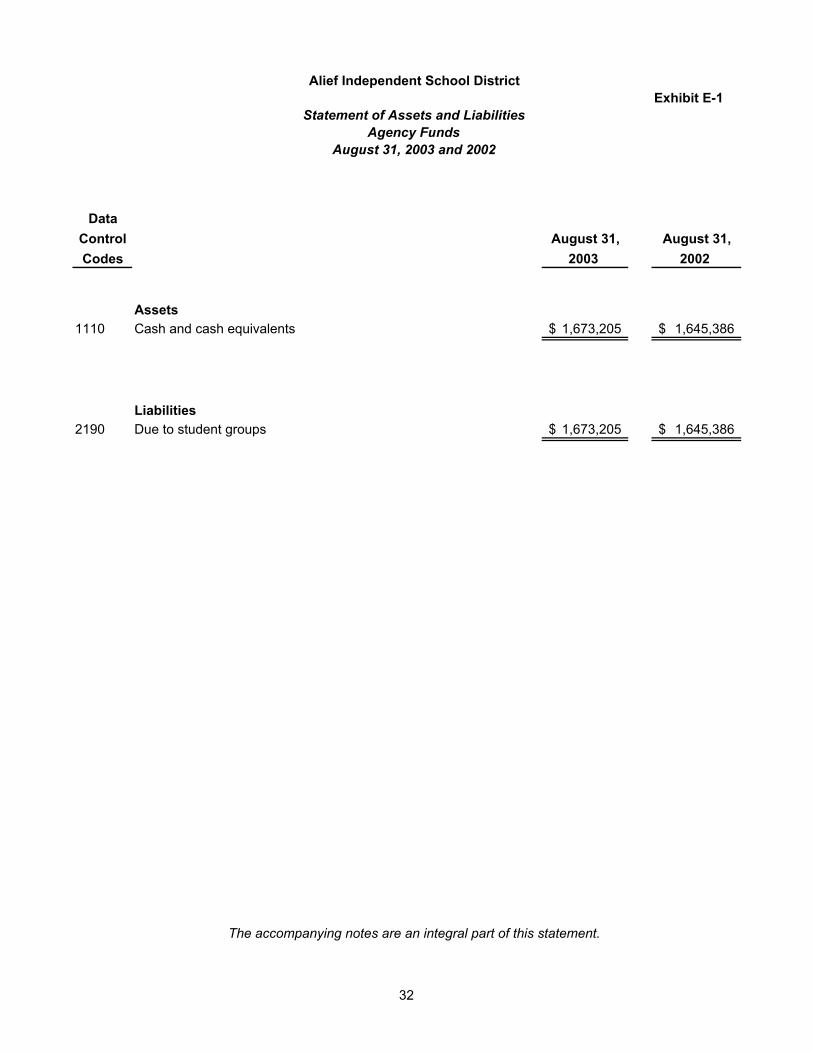

Exhibit E-1

DataControl August 31, August 31,Codes 2003 2002

1110 Cash and cash equivalents 1,673,205$ 1,645,386$

2190 Due to student groups 1,673,205$ 1,645,386$

Assets

Liabilities

The accompanying notes are an integral part of this statement.

Alief Independent School District

Statement of Assets and LiabilitiesAgency Funds

August 31, 2003 and 2002

32

33

Alief Independent School District Notes to the Financial Statements Note 1 - Summary of Significant Accounting Policies

The Alief Independent School District (the "District") is an independent public educational agency operating under applicable laws and regulations of the State of Texas. The District is autonomously governed by a seven member Board of Trustees elected to staggered three-year terms by the District's residents.