alternative research| | india | 1 july 2014 anshul...

TRANSCRIPT

– 1 of 31 –

Special Event Digest (Spe.E.D)

Alternative Research| | INDIA | 1 July 2014 ANSHUL BHARGAVA JIGNESH SHAH Head – Derivatives Research Director – Institution Derivatives & Equity Sales Trading Institution Desk Institution Desk Tel: +91 22 66679761 Tel: +91 22 66679735 [email protected] [email protected]

MONTHLY | INSTITUTIONAL USE ONLY

Prelude by Jignesh Shah, Director – Institution Derivatives & Equity Sales Trading [email protected] | +91 22 66679735

The markets continued their cheerful sprit (Election Results) and touched a

high of 7700, where some profit booking was seen. The month ended 5.3% higher. The underlying mood is bullish but after the recent run up (pre & post Election Results), expectations are also higher. This month, FIIs have added hedges through index puts. Till last week they had reduced their inflows cash markets. With expectations riding high, the Budget period is expected to see higher volatility.

The European & American austerity (rollback) measures, economic policies

continue to drive global sentiments. We hope you like this report and value your feedback & suggestions to make it

more useful. Do mail me your feedback at [email protected]. In case you would like to be added to our timely special events Reports mailing list, do let me know.

Major Events & Regulatory Updates by Anshul Bhargava, Head – Derivatives Research [email protected] | +91 22 66679761

As per our latest compilation, the Tata Motor DVR promoter holding had fallen to below 0.7%! We had said (and continue to maintain) that with the supply overhang (promoter supply) reducing significantly, spreads may not widen easily, while spread contractions are likely to be quicker in the future. In June it contracted to 27%!

On 10th April 2013, Tata Steel & Tata Metalik announced a merger. Currently TML is trading richer and one can switch from TML to TSL.

In April 2014, Diageo Plc announced an offer for 26% shares at Rs 3030 for United Spirits Ltd. As per revised schedule (pre-poned), the unaccepted shares are likely to be credit in a couple of days.

In April 2014, it was announced that Ranbaxy would merge into Sun Pharma. The share swap was fixed at 0.8. The management seeks to complete the transaction by CY 2014 – reiterated schedule in June’14.

In September 2013, the Board of Directors of UT & JPA approved the transfer of the Gujarat Cement Unit of Jaypee Cement Corporation Limited (JCCL), by way of a demerger. The merger is completed and trade closed.

In March 2014, the CPSE Index was constructed to facilitate disinvestment of GOI stake in selected Central PSEs. The government opted for ETF route for disinvestment. In its 1st tranche they sought to garner Rs30bn. The initial attraction for subscription to the ETF was a 5% discount – giving rise to a partly hedged strategy.

TABLE OF CONTENTS

Prelude

Pg. 1 | Prelude & Update

Special Events

Pg. 2 | TATA DVR SPREAD

Pg. 10 | STAN SPREAD

Pg. 16 | TATA STL MERGER

Pg. 19 | UT/JPA MERGER

Pg. 21 | UNSP OPEN OFFER

Pg. 23 | SUNP/RBXY MERGER

Pg. 26 | CPSE ETF

Pg. 27 | OFS

Pg. 28 | BUYBACKS

Pg. 29 | M&A ACTIVITY

Pg. 30 | PAST COVERAGE

SPECIAL EVENT DIGEST

– 2 of 31 –

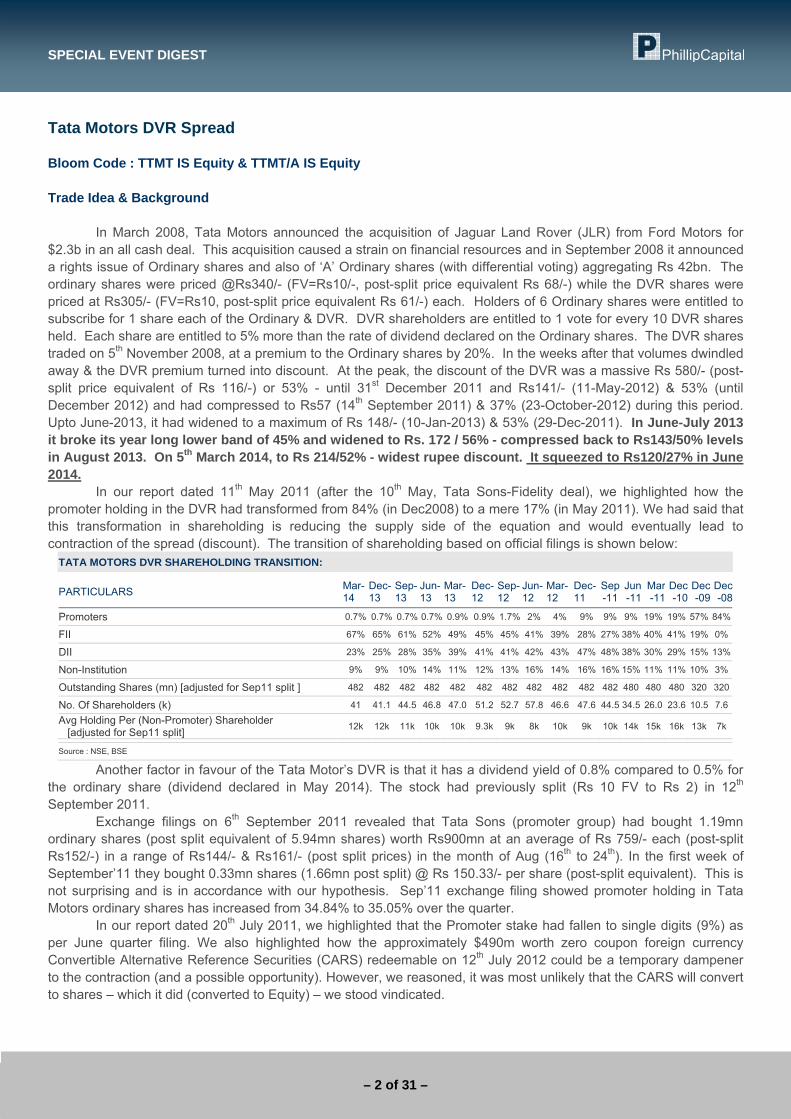

Tata Motors DVR Spread Bloom Code : TTMT IS Equity & TTMT/A IS Equity Trade Idea & Background

In March 2008, Tata Motors announced the acquisition of Jaguar Land Rover (JLR) from Ford Motors for $2.3b in an all cash deal. This acquisition caused a strain on financial resources and in September 2008 it announced a rights issue of Ordinary shares and also of ‘A’ Ordinary shares (with differential voting) aggregating Rs 42bn. The ordinary shares were priced @Rs340/- (FV=Rs10/-, post-split price equivalent Rs 68/-) while the DVR shares were priced at Rs305/- (FV=Rs10, post-split price equivalent Rs 61/-) each. Holders of 6 Ordinary shares were entitled to subscribe for 1 share each of the Ordinary & DVR. DVR shareholders are entitled to 1 vote for every 10 DVR shares held. Each share are entitled to 5% more than the rate of dividend declared on the Ordinary shares. The DVR shares traded on 5th November 2008, at a premium to the Ordinary shares by 20%. In the weeks after that volumes dwindled away & the DVR premium turned into discount. At the peak, the discount of the DVR was a massive Rs 580/- (post-split price equivalent of Rs 116/-) or 53% - until 31st December 2011 and Rs141/- (11-May-2012) & 53% (until December 2012) and had compressed to Rs57 (14th September 2011) & 37% (23-October-2012) during this period. Upto June-2013, it had widened to a maximum of Rs 148/- (10-Jan-2013) & 53% (29-Dec-2011). In June-July 2013 it broke its year long lower band of 45% and widened to Rs. 172 / 56% - compressed back to Rs143/50% levels in August 2013. On 5th March 2014, to Rs 214/52% - widest rupee discount. It squeezed to Rs120/27% in June 2014.

In our report dated 11th May 2011 (after the 10th May, Tata Sons-Fidelity deal), we highlighted how the promoter holding in the DVR had transformed from 84% (in Dec2008) to a mere 17% (in May 2011). We had said that this transformation in shareholding is reducing the supply side of the equation and would eventually lead to contraction of the spread (discount). The transition of shareholding based on official filings is shown below:

TATA MOTORS DVR SHAREHOLDING TRANSITION:

PARTICULARS Mar-14

Dec-13

Sep-13

Jun-13

Mar-13

Dec-12

Sep-12

Jun-12

Mar-12

Dec-11

Sep -11

Jun-11

Mar-11

Dec-10

Dec-09

Dec-08

Promoters 0.7% 0.7% 0.7% 0.7% 0.9% 0.9% 1.7% 2% 4% 9% 9% 9% 19% 19% 57% 84%

FII 67% 65% 61% 52% 49% 45% 45% 41% 39% 28% 27% 38% 40% 41% 19% 0%

DII 23% 25% 28% 35% 39% 41% 41% 42% 43% 47% 48% 38% 30% 29% 15% 13%

Non-Institution 9% 9% 10% 14% 11% 12% 13% 16% 14% 16% 16% 15% 11% 11% 10% 3%

Outstanding Shares (mn) [adjusted for Sep11 split ] 482 482 482 482 482 482 482 482 482 482 482 480 480 480 320 320

No. Of Shareholders (k) 41 41.1 44.5 46.8 47.0 51.2 52.7 57.8 46.6 47.6 44.5 34.5 26.0 23.6 10.5 7.6

Avg Holding Per (Non-Promoter) Shareholder [adjusted for Sep11 split] 12k 12k 11k 10k 10k 9.3k 9k 8k 10k 9k 10k 14k 15k 16k 13k 7k

Source : NSE, BSE

Another factor in favour of the Tata Motor’s DVR is that it has a dividend yield of 0.8% compared to 0.5% for the ordinary share (dividend declared in May 2014). The stock had previously split (Rs 10 FV to Rs 2) in 12th September 2011.

Exchange filings on 6th September 2011 revealed that Tata Sons (promoter group) had bought 1.19mn ordinary shares (post split equivalent of 5.94mn shares) worth Rs900mn at an average of Rs 759/- each (post-split Rs152/-) in a range of Rs144/- & Rs161/- (post split prices) in the month of Aug (16th to 24th). In the first week of September’11 they bought 0.33mn shares (1.66mn post split) @ Rs 150.33/- per share (post-split equivalent). This is not surprising and is in accordance with our hypothesis. Sep’11 exchange filing showed promoter holding in Tata Motors ordinary shares has increased from 34.84% to 35.05% over the quarter.

In our report dated 20th July 2011, we highlighted that the Promoter stake had fallen to single digits (9%) as per June quarter filing. We also highlighted how the approximately $490m worth zero coupon foreign currency Convertible Alternative Reference Securities (CARS) redeemable on 12th July 2012 could be a temporary dampener to the contraction (and a possible opportunity). However, we reasoned, it was most unlikely that the CARS will convert to shares – which it did (converted to Equity) – we stood vindicated.

SPECIAL EVENT DIGEST

– 3 of 31 –

Further, 8 Foreign Currency Convertible Notes due in 2014, were allotted 308,225 ordinary shares (representing 61,645 ADS) in February 2013. In May 2013 the company allotted 8.9mn underlying Ordinary shares (representing 1.8m ADSs) and 2.9m Ordinary share arising out of conversion of 306, 4% Foreign Currency Convertible Notes due in 2014 of US$100,000 each. In June 2013, the Company allotted 8mn underlying Ordinary Shares of Rs. 2/- each (representing 1.6mn ADSs of Rs. 10/- each at a premium of 590.595 each) and 8.8mn Ordinary Share of Rs. 2/- each at a premium of Rs. 118.119 each arising out of conversion of 435, 4% Foreign Currency Convertible Notes due in 2014 of US$100,000 each. With the above conversions, there would not be any outstanding Notes.

On 2nd April 2012 we highlighted that the March 2012 quarterly shareholdings were yet to be released, however our analysis indicated Tata Motors DVR promoter shareholding to have dropped to just 4%! Based on insider filings in March 2012, Tata Sons Ltd sold about $72mn worth Tata Motors DVR shares. Tata Sons Ltd bought about $10mn worth Equity shares. The low promoter shareholding was confirmed by the exchange filing of 20th April 2012. In April 2012, based on the insider activity we estimated that the promoter holding had fallen to 2%. This was confirmed by the 19 July 2012 official company filings. As per insider activity in September 2012, we estimated the promoter holding had fallen to 1.7%, which was confirmed in mid-October 2012. Based on insider activity in Q3 we expected it to have fallen to just 0.9%, which was confirmed in mid-January 2013. Based on insider activity in May’14, we estimate that the promoter holding has fallen further to 0.68% We summarise the recent insider/promoter disclosures:

TATA MOTORS EQUITY & TATA MOTORS DVR SHARES INSIDER/PROMOTER ACTIVITY

EQ/DVR B/S QTY SHARES PRICE (RS)

VALUE $MN COMMENTS

JUN 2014 na MAY 2014

DVR Sell 0.25mn 223.2 0.9 Tata Investment Corp sold some of its DVR holding. JUN 2013 – APR 2014 na MAY 2013 DVR Sell 0.63mn 166.9 1.9 Tata Investment Corp sold some of its DVR holding. APRIL 2013 DVR Sell 0.15mn 163.3 0.5 Tata Investment Corp sold some of its DVR holding. JANUARY, FEBRUARY & MARCH 2013 na

DECEMBER 2012 DVR Sell 3.3mn 166.12 10.1 Tata Industries sold all its DVR holding. Tata Sons Ltd also sold some EQ Sell 0.5mn 269.6 2.5 Tata Investment Corp Ltd sold

NOVEMBER 2012 DVR Sell 0.4mn 159.60 DVR Tata Sons Ltd

OCTOBER 2012 DVR Sell 0.2mn 169.2 0.7 Tata Industries Ltd & Sitmo Investment Ltd

SEPTEMBER 2012 DVR Sell 1.65mn 152.4 4.7 Tata Industries Ltd & Tata Investment

AUGUST 2012 na

JULY 2012 EQ Buy 2.3mn 242 10.1 Tata Sons Ltd

JUNE 2012 EQ Buy 2.4mn 244 10.7 Tata Sons Ltd EQ Buy 0.4mn 234 1.8 Mr Ratan Naval Tata

MAY 2012 DVR Sell 0.18mn 177 0.6 Tata Investment sold

SPECIAL EVENT DIGEST

– 4 of 31 –

APRIL 2012 DVR Sell 8.6mn 164 27 Tata Sons, Tata Investment & Tata Industries Ltd sold

MARCH 2012 EQ Buy 1.9mn 268 10 Tata Sons bought increasing stake to approx 25.51%

EQ Sell 2.5mn 270 13 Sold mainly by Tata Industries, Tata Investment, Kalimati Investment, Tata International

DVR Sell 24.5mn 152 73 Tata Sons & Tata Industries Ltd sold ~5%+

Source: PhillipCapital, NSE, BSE Note: Appropriate approximations made

Reasons for the DVR Spread :

The DVR shares will not be convertible into Ordinary Shares at any time (in normal circumstances). Also, we

do not advocate price parity between the 2 equity shares for a couple of factors in favour of the DVR discount remain. In general, any promoter would shy away from DVRs (sub-ordinate voting rights). No DVR shares are pledged by the Tata Motors promoters and are also off-loading the DVR shares since Dec 2008.

Reasons for subordinate-voting shares (DVR) to trade at a discount:

Timetable:

This is a trade idea based purely on demand-supply dynamics. There is no “schedule”. The company’s decision of whether, the CARS will convert to Ordinary shares, DVR shares or ADS was previously an important factor (for timing) which we had argued favorably. We reasoned that the conversion into DVR is unlikely. Further, Foreign Currency Notes due in 2014 were converted to ADS/Ordinary shares in February, May & June 2013. Current Returns & Trade Dynamics

The ordinary Tata motors stock futures traded at a discount till May’11 end and since then were trading mostly

at a premium till September’11 beginning – thereafter it traded mostly at a premium/mixed. Rolls have been mainly at a premium. April’12 Rolls of Tata Motors was soft. Roll spread thereafter were firm. Both scrip’s futures mostly trade at a healthy premium & roll also at a fairly good premium.

DISCUSSION & COUNTER REASONS S. NO. REASONS DISCUSSIONS & COUNTER REASONS

1. Ordinary share is part of indices (local & international) – thus long only funds, index arbitrageurs etc do not buy the DVR.

With a market cap of just $1.5bn, the DVR is unlikely to meet the criteria laid down by the major indices (NIFTY, Sensex, MSCI, FTSE) in the medium term.

2. Liquidity gets liquidity – DVRs are relatively new instruments while the ordinary share has been trading for decades. Investors generally flock to a more liquid instrument.

- Liquidity in Dec-2008 was slim indeed but has picked up. In terms of number of shares traded, on an average the DVR trades 29% of the ordinary share volumes. - In value terms, it now clocks an average of $6m-$10m per day. - The DVR’s inclusion in the F&O was a definite shot in the arm.

3. Control : A promoter is concerned about control & hence will “pay” an extra price for votes (prefer ordinary shares). As displayed, the promoters stake in the DVR fell ruthlessly from 84% in Nov-08 to less than 1% (Dec’12). The promoters hold 34% of the $15bn market cap (ordinary shares).

- Non-promoters (minority) may buy ordinary shares if there is a serious conflict between the promoters & the minority. Tata Motors does not seem to be in this category. - Another reason to buy the regular share is if there is a battle for control/buy-out etc in the offing – this also does not seem to be happening in the near future. - The supply side (promoters) of the equation is definitely slimming down. - Institutional holding in the DVR is 80%-90% which can be interpreted as a show of confidence in the management

4. The company is a vehicle for investors who are interested in the UK based Jaguar-Land Rover Automotive Plc.

Jaguar-Land Rover Automotive Plc is the holding company for Jaguar, LandRover and other investments (like Cherry JV) and owned by Tata motors. The regular shares/ADS provide the most obvious option.

SPECIAL EVENT DIGEST

– 5 of 31 –

The roll spreads are graphed below: TATAMOTORS PREMIUM/DISCOUNT (BPS) TATAMOTORS ROLL SPREAD (BPS)

DVR PREMIUM/DISCOUNT (BPS) DVR ROLL SPREAD (BPS)

LHS: Futures prices; RHS: bps / Roll bps

Source: PhillipCapital , NSE

The spread movement is graphed below: DVR SPREAD (RS & ALSO %)

Upper Graph LHS – Underlying share prices; RHS: Spread in Rs Lower Graph – RHS : Spread in %

Source: PhillipCapital , NSE, BSE

TATAMOTORS vs DVR Spread(Rs)

-250

-200

-150

-100

-50

0

50

30-J

un-1

419

-May

-14

31-M

ar-1

414

-Feb

-14

3-Ja

n-14

21-N

ov-1

38-

Oct

-13

23-A

ug-1

310

-Jul

-13

29-M

ay-1

315

-Apr

-13

28-F

eb-1

317

-Jan

-13

5-D

ec-1

219

-Oct

-12

6-Sep

-12

24-J

ul-1

212

-Jun

-12

30-A

pr-1

216

-Mar

-12

2-Fe

b-12

22-D

ec-1

18-

Nov

-11

22-S

ep-1

18-

Aug

-11

27-J

un-1

116

-May

-11

30-M

ar-1

115

-Feb

-11

3-Ja

n-11

19-N

ov-1

07-

Oct

-10

25-A

ug-1

014

-Jul

-10

2-Ju

n-10

21-A

pr-1

05-

Mar

-10

20-J

an-1

04-

Dec

-09

22-O

ct-0

94-

Sep

-09

24-J

ul-0

912

-Jun

-09

29-A

pr-0

912

-Mar

-09

23-J

an-0

910

-Dec

-08

Abs

olut

e Spr

ead

(Rs)

0

50

100

150

200

250

300

350

400

450

500

Pric

e

Spread_RsEQDVR

TATAMOTORS vs DVR Spread%

-60

-50

-40

-30

-20

-10

0

10

Spre

ad%

Spread%

11-MAY-2011

SPECIAL EVENT DIGEST

– 6 of 31 –

On 11th May 2011, when we first initiated coverage, the spread was Rs 103/- & 43%. Since then, the spread thereafter contracted to Rs 57/- in September 2011 & 37% in October 2012. Since then it has slid back to a maximum rupee discount of Rs 148/- (Jan’13) and a percent discount of 53% (Dec’11). After trading below 45% discount for about a year, it fell through those levels by mid-June 2013. As of close of June’13 the discounts were Rs140/- & 50% and by July-end it widened to Rs160/56%. In August 2013, it widened to Rs172/56%, but compressed to Rs143/50% soon after and ended @Rs154/51%. In September & October it ranged between 50%-53%. While from November 2013 to March 2014 it was between 48%-51% (maximum Rupee discount of Rs 214 in March – widest Rupee discount). In April 2014 it reduced to 45% while in May 2014 it initially expanded to 47%, later squeezed to 38%and further to 27% in June 2014.

We have noticed that the spread tends to compress in a falling phase while widening in a bullish phase for possible reasons mentioned previously.

On 31st October 2013, the RBI notified that the company had raised the FII limit of the DVR shares to 75%. From Sep’12 to Dec’13, the FII stake in the DVR has increased from 45% to 65%. The ordinary shares have reduced from 28.5% to 26.7%! FII limit of the ordinary shares is 35%. Status & Our Comments

As per latest filings the promoters are left with just 0.68%. We continue to suggest entering this trade, piecemeal. Promoters have been offloading DVR shares (more scanty now). The year-long band was broken in June’13 (45% discount), and at 56% discount there was a swift reduction to 50% seen in August 2013. We suggest piecemeal entry (especially when normal equity share is expected to weaken). FII limit in ordinary shares may add a new trigger to the spread (though some headroom still left for now). With the supply overhang (promoter supply) reducing significantly, spreads contractions are likely to be quicker in the future. In mid-June (2014), DVR shares jumped, compressing the spread further as reports suggested that DVR holders in the US would get an exit via ADS. Any such moves are likely to compress the spread further. Recommendation Summary:

DATE RECOMMENDATION REASON

2-Jun-2014 Use any widening as opportunity. Don’t expect much widening

~50% spread good level to enter

2-May-2014 Use any widening as opportunity. Don’t expect much widening

~50% spread good level to enter

1-Apr-2014 Use any widening as opportunity. Don’t expect much widening

~50%-56+ spread good level to enter

3-Mar-2014 Use any widening as opportunity. Don’t expect much widening

~50%-56+ spread good level to enter

3-Feb-2014 Use any widening as opportunity. Don’t expect much widening

~50%-56+ spread good level to enter

2-Jan-2014 Use any widening as opportunity. Don’t expect much widening

~50%-56+ spread good level to enter

2-Dec-2013 Use any widening as opportunity. Don’t expect much widening

~50%-56+ spread good level to enter

4-Nov-2013 Use any widening as opportunity. Don’t expect much widening

~50%-56+ spread good level to enter

1-Oct-2013 Use any widening as opportunity. Don’t expect much widening

~52%-56+ spread good level to enter

2-Sep-2013 Use any widening as opportunity. Don’t expect much widening

~56%+ spread good level to enter

1-Aug-2013 Use any widening as opportunity. Don’t expect much widening

~56%+ spread good level to enter

SPECIAL EVENT DIGEST

– 7 of 31 –

Miscellaneous Bulk Deals:

RECENT BULK DEALS IN TATAMTRDVR

DATE CLIENT NAME BUY / SELL

QTY (‘000)

VALUE (MN) PRICE

10-Apr-13 Merrill Lynch Capital Markets Espana SA BUY 6341 $17.8 151.85 10-Apr-13 The Royal Bank Of Scotland Asia Merchant Bank Singapore SELL 6341 $17.8 151.85 29-Nov-12 Morgan Stanley Asia (Singapore) PTE SELL 2500 $7.4 161.01

1-Jul-2013 45% levels broken. Use widening as opportunity. ~50%+ spread good level to enter

3-Jun-2013 Use any widening as opportunity. Don’t expect much widening

~45%+ spread is a good level to enter

2-May-2013 Use any widening as opportunity. Don’t expect much widening

~45%+ spread is a good level to enter

1-Apr-2013 Use any widening as opportunity. Don’t expect much widening

~45%+ spread is a good level to enter

4-Mar-2013 Use any widening as opportunity. Don’t expect much widening

~45%+ spread is a good level to enter

4-Feb-2013 Use any widening as opportunity. Don’t expect much widening

~45%+ spread is a good level to enter

2-Jan-2013 Use any widening as opportunity. Don’t expect much widening

~45%+ spread is a good level to enter

3-Dec-2012 Use any widening as opportunity. Don’t expect much widening

~43%+ spread is a good level to enter

1-Nov-2012 Use any widening as opportunity. Don’t expect much widening

~43%+ spread is a good level to enter

1-Oct-2012 Use any widening as opportunity. Don’t expect much widening

43%+ spread is a good level to enter

3-Sep-2012 Use any widening as opportunity. Don’t expect much widening

43-45%+ spread is a good level to enter

1-Aug-2012 Use any widening as opportunity. Don’t expect much widening

43-45%+ spread is a good level to enter

2-Jul-2012 Enter aggressively (gave 8% returns by 20th July) 46%+ spread is a good level to enter

4-Jun-2012 Recommended to enter if spread widens Spreads may not widen back to 53% levels.

2-May-2012 Recommended to enter as promoter holding only 2% (as per our estimate)! CARS also not converting to DVR.

Rs 137/-/44% is a favourable level to enter the spread trade.

2-Apr-2012 Recommended to enter as promoter holding only 4% (as per our estimate)!

Rs 119/-/43% is a favourable level to enter the spread trade – 50%+ seems unlikely as promoter holding dipped to 4%.

1-Mar-2012 Recommended to enter Rs 115/-+ is a favourable level to enter the spread trade.

1-Feb-2012 Recommended to enter aggressively Rs 124/-+ is very good level to enter the spread trade.

3-Jan-2012 Recommended to enter Rs 94/- is favourable level to enter the spread trade.

2-Dec-2011 Recommended to enter but, degree of aggression low Rs 80/- is not so good a level to enter the spread trade.

2-Nov-2011 Recommended to enter more aggressively around Rs 94/- levels.

Good level to enter.

3-Oct-2011 Spread has compressed in favour, however room still left.

Spread has room left.

5-Sep-2011 Build position The spread is of large magnitude

5-Aug-2011 Build position The spread is of large magnitude

Report initiating coverage (Buy) on the spread : 11-May-2011 ; updates on 20th & 21st July 2011

SPECIAL EVENT DIGEST

– 8 of 31 –

29-Nov-12 Morgan Stanley Asia (Singapore) PTE SELL 2500 $7.4 161.07 06-Nov-12 The Royal Bank Of Scotland Asia Merchant Bank Singapore

Ltd BUY 3025 $9.2 165.75 06-Nov-12 ABN Amro Bank NV SELL 3025 $9.2 165.75 10-May-11 Fidelity Investment Trust Fidelity Series Emerging Markets BUY 745 $11.3 680.9 10-May-11 Tata Sons Ltd SELL 1700 $25.7 680.5

07-Jul-11 Waddell And Reed Investment Management Company A/C Ivy Fund SELL 1345 $17.1 573.3

07-Jul-11 Waddell And Reed Investment Management Company A/C Ivy Fund SELL 2572 $32.7 573.0

07-Jul-11 Bajaj Allianz Life Insurance Company Limited BUY 1500 $19.1 573.0

None Since July-2011

Source: NSE, BSE

Shareholding in December 2008:

As on 31st Dec 2008, the Shareholding of the Ordinary & DVR shares was as under: SHAREHOLDING AS ON DECEMBER 31, 2008

PARTICULARS TATA MOTORS DVR Promoter 48% 84% Institution 30% 13% Non-Institution 22% 3% Total outstanding shares (Not adjusted for Sep’11 split)

450 mn shares 64 mn shares

No. of Share Holders 377k 7.6k Avg holding per (Non-Promoter) shareholder (Not adjusted for Sep’11 split)

620 1350

Source: NSE, BSE

As on 31st Dec 2008, other than the promoters, IFCI Ltd & JM Financial held stakes of 12.8% & 2.2% respectively

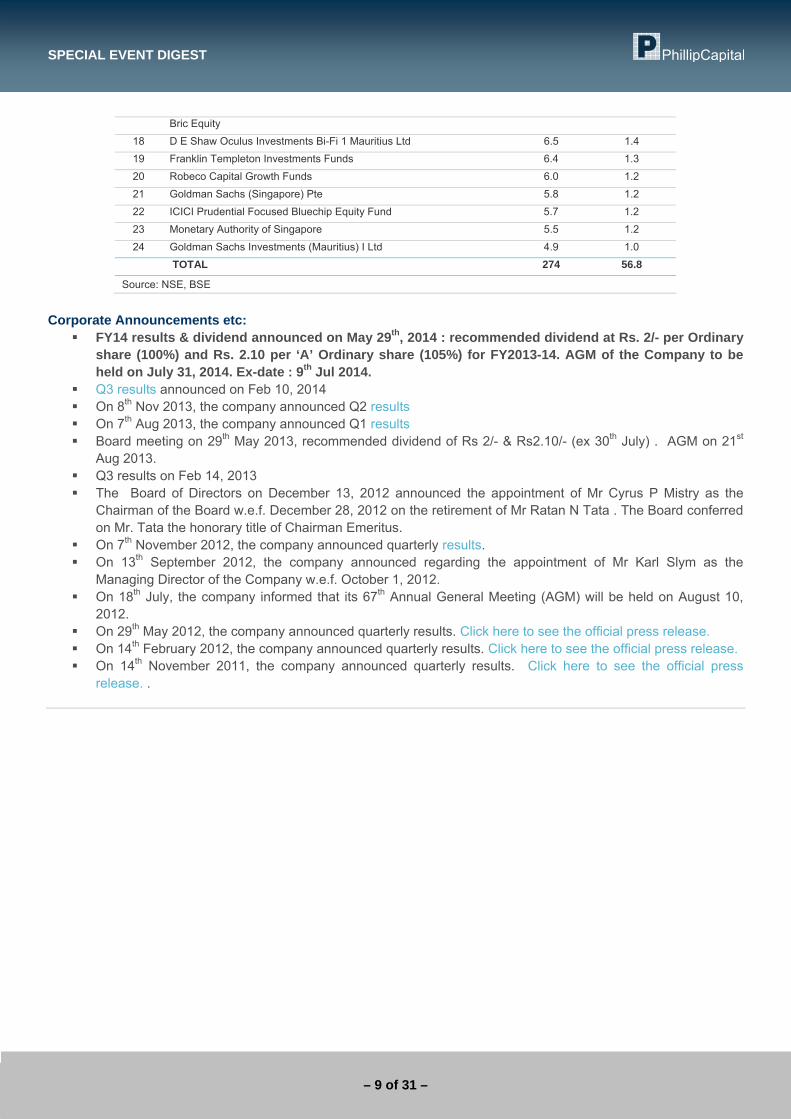

Major Shareholding:

The shareholding is mainly held by institutions (89.9%) and only 9.4% with non-institutions. The major (>1%) holders are:

TATA MOTORS DVR SHAREHOLDING AS ON MARCH 31, 2014

S.NO. NAME OF THE SHAREHOLDER

NO. OF SHARES

(MN)

SHARES AS % OF TOTAL NO.

OF SHARES 1 Mathews Asia Dividend Fund 33.4 6.9 2 HSBC Global Investment Funds A/c HSBC GlF Mauritius Limited 29.1 6.0 3 HDFC Trustee Company Ltd HDFC Top 200 Fund 21.8 4.5 4 HDFC Trustee Company Ltd -HDFC Equity Fund 21.4 4.4 5 Government of Singapore 16.8 3.5 6 Merrill Lynch Capital Market Espana S A S V 15.3 3.2 7 Government Pension Fund Global 13.2 2.7 8 Swiss Finance Corporation (Mauritius) Ltd 11.3 2.4 9 HDFC Trustee Company Ltd - HDFC Prudence Fund 9.0 1.9

10 Pioneer Asset Management S A A/C Pioneer Asset Management S A On Be half of Pioneer Funds Emerging Markets Equity

8.9 1.9

11 Skagen Global Verdipapirfond 8.2 1.7 12 Master Trust Bank of Japan Ltd A/c HSBCIndian Equity Mother Fund 8.2 1.7 13 SBI Magnum Taxgain Scheme 8.0 1.7 14 Citigroup Global Markets Mauritus Pvt Ltd 7.8 1.6 15 Eastspring Investments India Equity Open Ltd 7.0 1.5 16 HDFC Trustee Company Ltd - HDFC Tax Saver Fund 6.7 1.4 17 HSBC Global Investment Funds A/c HSBC Global Investment Fund 6.6 1.4

SPECIAL EVENT DIGEST

– 9 of 31 –

Bric Equity 18 D E Shaw Oculus Investments Bi-Fi 1 Mauritius Ltd 6.5 1.4 19 Franklin Templeton Investments Funds 6.4 1.3 20 Robeco Capital Growth Funds 6.0 1.2 21 Goldman Sachs (Singapore) Pte 5.8 1.2 22 ICICI Prudential Focused Bluechip Equity Fund 5.7 1.2 23 Monetary Authority of Singapore 5.5 1.2 24 Goldman Sachs Investments (Mauritius) I Ltd 4.9 1.0

TOTAL 274 56.8

Source: NSE, BSE

Corporate Announcements etc:

FY14 results & dividend announced on May 29th, 2014 : recommended dividend at Rs. 2/- per Ordinary share (100%) and Rs. 2.10 per ‘A’ Ordinary share (105%) for FY2013-14. AGM of the Company to be held on July 31, 2014. Ex-date : 9th Jul 2014.

Q3 results announced on Feb 10, 2014 On 8th Nov 2013, the company announced Q2 results On 7th Aug 2013, the company announced Q1 results Board meeting on 29th May 2013, recommended dividend of Rs 2/- & Rs2.10/- (ex 30th July) . AGM on 21st

Aug 2013. Q3 results on Feb 14, 2013 The Board of Directors on December 13, 2012 announced the appointment of Mr Cyrus P Mistry as the

Chairman of the Board w.e.f. December 28, 2012 on the retirement of Mr Ratan N Tata . The Board conferred on Mr. Tata the honorary title of Chairman Emeritus.

On 7th November 2012, the company announced quarterly results. On 13th September 2012, the company announced regarding the appointment of Mr Karl Slym as the

Managing Director of the Company w.e.f. October 1, 2012. On 18th July, the company informed that its 67th Annual General Meeting (AGM) will be held on August 10,

2012. On 29th May 2012, the company announced quarterly results. Click here to see the official press release. On 14th February 2012, the company announced quarterly results. Click here to see the official press release. On 14th November 2011, the company announced quarterly results. Click here to see the official press

release. .

SPECIAL EVENT DIGEST

– 10 of 31 –

STAN Spread Bloom Code : STAN IS Equity / STAN UK Equity / 2888 HK Equity Trade Idea & Background

On June 11, 2010, the first (till now the only) IDRs (India Depository Receipts) of Standard Chartered Bank

were listed on the Indian bourses – an issue of 240mn IDRs priced at Rs104/-. Ten STAN DR are equivalent to 1 STAN Equity shares. We had released a note comparing the 3 listings of STAN on 24th May 2010. There was a 1 year restriction for converting the IDR to the Equity share. Vice versa was not permitted by RBI.

The spread began trading around 10%-16% (DR trading at a discount), and over the year, the spread reduced to around 3% a couple of days before the eligibility date. The reduction being on account of the opportunity to �ummar DRs into Equity Shares i.e. Buy DRs in India, sell short in UK; apply to redeem DRs to Equity shares; get shares in CREST account within 10days and cover short in UK.

However, two working days before the eligibility date, the SEBI changed the regulation to “redemption of the IDRs shall be permitted only if the IDRs are infrequently traded on the stock exchange(s) in India”. This caused the spread (& price) to go haywire. The DR gapped down by ~20% as an initial reaction.

Other drawback of IDRs was that they were not allowed to participate in the rights issues. The rights issue in 2010 saw IDR holders receive Rs 4.60/- in lieu of the rights entitlements (Nov2010). The new regulation (23rd September) enables IDR investors to participate in right issues. The amendment has been made vide Chapter XA and can be seen here. On March 16, 2012, in the Budget speech, the Finance Minister, said that changes in the IDR regulations will be made permitting two-way-fungibility. This was received by the STAN IDR holders with much cheer as prices hit the upper circuit. One may recollect that in our interactions in April/May 2011 with the RBI, they had indicated that they were comfortable in allowing conversion of IDRs into foreign equity after the initial 1-year period (as per the law prevalent then). On 28th August, 2012, the SEBI announced proposal to permit 25% of the original issue size per financial year. Legal framework to implement this and also reverse conversion is to be announced in the future.

On 8th October 2012, the Ministry of Corporate Affairs (MCA) notified modifications in the Companies (Issue of Indian Depository Receipts) Rules, have come into effect from October 1 – a holder of IDRs may transfer the IDRs, may ask the domestic depository to redeem them or, any person may seek re-issuance of IDRs by conversion of underlying equity shares, subject to the provisions of Foreign Exchange Management Act and SEBI rules at the time.

On 27th February 2013, the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations were amended to permit fungibility of IDRs. Shortly thereafter on 1st March 2013, the SEBI issued Guidelines for enabling partial Two-Way fungibility of Indian Depository Receipts. Click here for the detailed guidelines, a summary is given below:

• 25% of the 240mn (i.e.60mn) IDRs are eligible for redemption/conversion into equity shares every year. For this, the issuer (STAN) will issue advertisement inviting interest in the same. The SEBI has given 3-months time for this. 7-day (minimum) window to be available in a (minimum) every quarter.

• Option by issuer to IDR holders: o Converting IDRs into equity shares, and/or o Converting IDRs into equity shares, selling the shares in the foreign market & providing the

sale proceeds to the IDR holders (max cost 5% of sale proceeds). • IDRs available for fungibility in that window will be disclosed before opening of that window. • Excess requests for conversion to be done on a proportionate basis • 20% reservation for Retail investors • Issuer may convert shares to IDRs depending on headroom & RBI rules. • Available headroom, significant conversion & reconversions shall be disclosed on continuous basis • Quarterly option (11Mar/11Jun/11Sep/11Dec – quarterly listing anniversaries) of STAN to switch to

“guidelines issued for new issues” giving 1-month advance notice. Once exercised, it cannot be reversed. New IDR issues-guidelines provide that (after a year of listing) the fungibility should be on a continuous basis.

• STAN to lay down detailed procedure

SPECIAL EVENT DIGEST

– 11 of 31 –

On 29th April 2013, STAN announced operating guidelines of two-way fungibility, as summarized below: Window open : 31MAY to 7JUN 2013 IDRs redeemable : 60mn (25% of 240mn) Minimum : 10 IDRs & multiples therof Allocation : Proportionate if it exceeds limit Reservation : 20% (12mn) reserved for Retail (Rs 200k i.e. 1730 IDRs) Fee : Rs0.303 (~USD0.05/share, incl service tax) Schedule:

> Redemption Window : T to T+7 > Finalise basis : ~T+14 > Announcement of results : ~T+17 > Credit to UK CREST account : ~T+18/T+19 > Intimation to IDR holders : ~T+20

On 27th September 2013, STAN released the detailed operating guidelines and FAQ.

Prior to the redemption window opening we had analysed the shareholding pattern identifying the likely candidates that may redeem the IDRs are given below (As of 31st March 2013). The estimated outcome is also shown:

Particulars SH 31 March 2013 Comment Ahead of Window (31May)

Redeemed (Estimated) shares

Redeemed %

SH 30 JUNE 2013

FII 83.5% many may look to convert 50 mn 83% 83.6%

MF 9.5% May look to convert 8 mn 13.5% 8.2%

Banks, FI, Insurance 0.0% Few may convert - - 0.0%

NRIs 0.3% - 0.2 mn 0.3% 0.3%

Others 6.7% Few may convert 1.8 mn 3.2% 7.9%

Total 100% 240mn o/s 60 mn 100% 100%

Source : NSE, BSE, PhillipCapital

Conversion of Equity to IDR has been NIL In January-February 2014, STAN released the detailed new operating guidelines and FAQ. Timetable:

The previous law (phased out) permitted redemption only if the DR were illiquid and this test was applied on 30th June & 31st December of each year. It failed this test in June 2011, December 2011, June 2012 & December 2012. In terms of the new guidelines, the 1st window for conversion of IDRs to shares opened on 31st May 2013 for 7 days which received a huge response. From 1-July-2013, window for conversion of equity shares to IDR was opened (till headroom left) on a continuous basis. The 2nd window (60mn IDRs) for conversion of IDRs to shares was opened between 21st -28th March 2014 (both inclusive). Fee was Rs 0.349 per IDR. 20% (12mn) was reserved for retail individuals (Rs 200k). Current Returns & Trade Dynamics

The spread had gone haywire in the first quarter of 2012 and widened to 60%+. After 16th March 2012, it has traded around 30-40%. In April 2012, the spread contracted to 26% but as the rupee depreciated to 85, the spread widened to 34%.

Till February 2013, the spread ranged between 20%-35% with a contracting drift. March 2013 onwards, the spread ranged between 13-20%. In November’13 it ranged between 14%-18%.

While in December’13 it was between 10%-16%. The range squeezed further from 15% to 7% in January 2014! The range initially expanded to 14% then squeezed back to 7% in February 2014! The spread squeezed to 4.5% ahead of the March’14 window and expanded to 10% thereafter and has been in the range of 8%-12% since.

SPECIAL EVENT DIGEST

– 12 of 31 –

First half of December 2011 saw $38m worth bulk deals were reported, while $11m worth deals were reported in January (see next page for details) & $5mn in March 2012. Thereafter, the bulk deals took place in May’13 & August’13. STAN SPREAD MOVEMENT VS GBP

LHS – Spread % (blue area); RHS – GBPINR (black line) Source: PhillipCapital , NSE, BSE

We had analyzed the shareholding pattern identifying the likely candidates that may redeem the IDRs are given below (As of 31st March 2014) :

Particulars SH 31 March 2014 Comment Ahead of Window (31May) FII 90.3% Most will look to convert MF 3.4% Not many may look to convert Banks, FI, Insurance 0.01% - NRIs 0.1% - Others 6.2% Very few may convert Total 100% 180mn o/s

Source : NSE, BSE, PhillipCapital

Status & Our Comments

With the GBPINR crossing 75 and further depreciating to 80+ levels, had caused the spread to widen to 50%. The spread compressed from 53% to 33% in early January 2012. However, it had again widened to 63%+ on 1st Feb 2012. After dipping to 55% in early-March it again widened to 64% by mid-March 2012. Over the months it has reduced to sub-20% levels.

The first conversion window (IDR to shares) was opened for 7 days beginning 31st May 2013 for 25% of the outstanding shares (60mn IDRs). It saw a full response and 60mn IDRs were converted to 6mn shares accordingly. The 2nd conversion window opened on 21st March 2014 and also saw full response and 60mn IDRs were converted to 6m shares accordingly. After the redemption window closed, initially, STAN IDR is expected to see lower interest, which may pick up towards corporate announcements, wider spreads and the next conversion window. With the new regulations there seems to be some more room left for compression but limited. Conversion trades can be looked at closer to next window. Equity to IDR conversion window seems irrelevant at this point. Recommendation Summary:

DATE RECOMMENDATION REASON

2-Jun-2014 With next conversion window still months away use expansion to enter trade

2nd Redemption window opened in March’14

2-May-2014 With next conversion window still months away use 2nd Redemption window opened in March’14

0%

10%

20%

30%

40%

50%

60%

70%

6/11

/201

0

8/11

/201

0

10/1

1/20

10

12/1

1/20

10

2/11

/201

1

4/11

/201

1

6/11

/201

1

8/11

/201

1

10/1

1/20

11

12/1

1/20

11

2/11

/201

2

4/11

/201

2

6/11

/201

2

8/11

/201

2

10/1

1/20

12

12/1

1/20

12

2/11

/201

3

4/11

/201

3

6/11

/201

3

8/11

/201

3

10/1

1/20

13

12/1

1/20

13

2/11

/201

4

4/11

/201

4

6/11

/201

4

Gro

ss S

prea

d %

65

70

75

80

85

90

95

100

105

GB

P IN

R R

ate

GBPINR Steep depreciation

SPECIAL EVENT DIGEST

– 13 of 31 –

expansion to enter trade

1-Apr-2014 With next conversion window still months away use expansion to enter trade

2nd Redemption window opened in March’14

3-Mar-2014 Conversion trade setup on expansions Next conversion window upcoming

3-Feb-2014 Conversion trade setup on expansions Next conversion window upcoming

2-Jan-2014 With next conversion window still 5 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

2-Dec-2013 With next conversion window still 6 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

4-Nov-2013 With next conversion window still 7 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

1-Oct-2013 With next conversion window still 8 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

1-Sep-2013 With next conversion window still 9 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

1-Aug-2013 With next conversion window still 10 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

1-Jul-2013 With next conversion window still 11 months+ use expansion to enter trade

Next conversion window to be in May/Jun 2014

3-Jun-2013 Initiate spread; Conversion trade possible. New legislation announced, can compress more – although limited (12%-15%)

2-May-2013 Initiate spread; Conversion trade possible. New legislation announced, can compress more – although limited (12%-15%)

1-Apr-2013 Initiate spread New legislation announced, can compress more – although limited (12%-15%)

4-Mar-2013 Initiate spread New legislation announced, can compress more – although limited

4-Feb-2013 Initiate spread New legislation on way, use rupee weakness to enter

2-Jan-2013 Initiate spread New legislation on way, use rupee weakness to enter

3-Dec-2012 Initiate spread New legislation on way, use rupee weakness to enter

1-Nov-2012 Initiate spread New legislation on way, use rupee weakness to enter

1-Oct-2012 Initiate spread New legislation on way, use rupee weakness to enter

3-Sep-2012 Initiate spread New legislation on way, use rupee weakness to enter

1-Aug-2012 Initiate spread New legislation on way, use rupee weakness to enter

2-Jul-2012 Initiate spread New legislation on way, use rupee weakness to enter

4-Jun-2012 Initiate spread New legislation on way, use rupee weakness to enter

2-May-2012 Initiate spread New legislation on way, use rupee weakness to enter

2-Apr-2012 Initiate spread New legislation on way, likely to add to reasons for compression

1-Mar-2012 One can initiate spread Though, the rupee has come back to reasonable levels, the spread has not followed yet.

1-Feb-2012 Rupee appreciated to 79.5 one can initiate spread New trading range as depreciation of the Rupee beyond recent levels

3-Jan-2012 If rupee appreciates to 79.5 than one can look to initiate spread

New trading range as depreciation of the Rupee beyond recent levels

2-Dec-2011 If rupee appreciates to 79.5 than one can look to initiate spread

New trading range as depreciation of the Rupee beyond recent levels

2-Nov-2011 Trade spread within 25-30% range, more towards lower end

Post June’2011, this is the new trading range

3-Oct-2011 Trade spread within 20-28% range, more towards lower end

Post June’2011, this is the new trading range

SPECIAL EVENT DIGEST

– 14 of 31 –

5-Sep-2011 Trade spread within 20-27% range Post June’2011, this is the new trading range

5-Aug-2011 Trade spread within 20-27% range Post June’2011, this is the new trading range

Report initiating coverage on the STAN DR (India) listing/spread : 24-May-2010

Miscellaneous Recent bulk-deal activity is given below:

BULK DEALS IN STAN

DATE CLIENT NAME BUY / SELL

QTY (‘000 SHARES)

VALUE (MN) PRICE

13-Aug-13 Morgan Stanley Asia (Singapore) Pte SELL 2863 $ 5.6 130.1 13-Aug-13 Morgan Stanley Mauritius Company Ltd BUY 2863 $ 5.6 130.1 28-May-13 Macquarie Bank Limited BUY 1533 $ 3.2 116 28-May-13 Merrill Lynch Capital Markets Espana S.A. Svb BUY 1247 $ 2.6 116 02-Feb-11 Swiss Finance Corporation (Mauritius) Limited BUY 1650 $ 4.3 116.2 18-Feb-11 Swiss Finance Corporation (Mauritius) Limited BUY 1450 $ 3.7 114.5

18-Feb-11 Reliance Mutual Fund SELL 1450 $ 3.7 114.5

19-May-11 Swiss Finance Corporation (Mauritius) Limited BUY 2000 $ 4.9 111.0

23-May-11 The Royal Bank Of Scotland N.V. BUY 1985 $ 4.9 111.5

06-Jun-11 Credit Suisse (Singapore) Limited A/C Credit Suisse (Sing SELL 3498 $ 7.3 94.4

06-Jun-11 Swiss Finance Corporation (Mauritius) Limited BUY 750 $ 1.6 93.7

06-Jun-11 ICICI Prudential M F A/C Dynamic Fund BUY 2982 $ 6.4 97.0

06-Jun-11 Credit Suisse (Singapore) Limited A/C Credit Suisse (Sing SELL 2051 $ 4.4 97.5

06-Jun-11 Swiss Finance Corporation (Mauritius) Limited SELL 4545 $ 9.6 95.3

06-Jun-11 Swiss Finance Corporation (Mauritius) Limited SELL 7006 $ 14.9 95.7

06-Jun-11 Deutsche Securities Mauritius Ltd. SELL 1300 $ 2.8 96.3

07-Jun-11 Credit Suisse (Singapore) Limited A/C Credit Suisse (Sing BUY 1206 $ 2.6 97.5

07-Jun-11 Goldman Sachs Investments Mauritius I Ltd BUY 4232 $ 9.2 97.7

07-Jun-11 UBS AG Swiss Finance Corporation (Mauritius) Ltd SELL 3050 $ 6.6 97.1

07-Jun-11 Credit Suisse (Singapore) Limited A/C Credit Suisse (Sing SELL 1013 $ 2.2 96.6

16-Jun-11 Deutsche Securities Mauritius Limited SELL 2029 $ 4.2 92.1

20-Jul-11 Goldman Sachs Investments Mauritius I Ltd SELL 1420 $ 2.9 93.1

15-Sep-11 Goldman Sachs Investments Mauritius I Ltd SELL 1638 $ 2.7 80.0

2-Dec-11 Bnp Paribas Arbitrage SELL 1942 $ 3.0 83.0

2-Dec-11 Morgan Stanley Mauritius Company Ltd BUY 2942 $ 4.6 83.0

13-Dec-11 Goldman Sachs Investments Mauritius I Ltd SELL 3000 $ 4.6 82.0

13-Dec-11 Morgan Stanley Mauritius Company Ltd BUY 3049 $ 4.7 82.0

14-Dec-11 Global Strategic Investments Ltd SELL 6978 $ 10.7 81.0

14-Dec-11 Integrated Core Strategies (Asia) Pte.Ltd. BUY 6978 $ 10.7 81.0

4-Jan-12 Macquarie Bank Limited BUY 1450 $ 2.3 82.5

17-Jan-12 Goldman Sachs Investments Mauritius I Ltd BUY 2685 $ 4.4 84

17-Jan-12 Integrated Core Strategies (Asia) Pte.Ltd. SELL 2685 $ 4.4 84

19-Mar-12 Deutsche Securities Mauritius Limited BUY 2371 $ 4.8 102.6 None Since Sep-2011

Source : NSE, BSE

Corporate Announcements etc:

SPECIAL EVENT DIGEST

– 15 of 31 –

The company filed major shareholding as on 31st March 2014 (Link) The Company fixed March 14, 2014 as the Record Date for the purpose of Payment of Final Dividend (INR

3.354626 per IDR). AGM on 8 May 2014. The company filed major shareholding as on 31st December 2013 (Link) The Company confirmed the 2013 interim dividend of 28.80 US$ cents and a dividend record date of August 16,

2013. The Indian Rupee conversion will be made on October 07, 2013. The dividend paid to the IDR holders on October 17, 2013.

The Company announced that in its board meeting on 5th March 2013, it would consider declaring final dividend. Consequently, the ex-date is 14th March 2013. 56.77 US$ cents per ordinary share equivalent dividend payable to IDR holders by 14 May 2013.

On 17th July, The Company announced that in its board meeting on 1st August 2012, it will consider declaring interim dividend. Consequently, the ex-date was 9th August 2012.

The company filed major shareholding as on 30th June 2012 (Link) The company filed major shareholding as on 31st March 2012 (Link) The company announced announcement its results for the year ended December 31, 2011 and also confirms the

2011 final dividend of 51.25 US$ cents and a dividend record date of March 09, 2012 (please note the dividend of 51.25 US$ cents is per ordinary share and that ten IDRs represent one ordinary share). The Indian Rupee conversion will be made on May 04, 2012. The dividend of Rs 2.67 per IDR was paid to the IDR holders on May 15, 2012.

It went ex-dividend on 11-Aug-2011 with the IDR holders receiving only cash dividends in INR. Other shareholders had an option to accept share dividend or in either currency (GBP/USD/HKD). On 29th September, the company announced “In reference to the Company’s 2011 Interim Dividend payable on October 07, 2011, the Company confirms that IDR holders will receive INR 1.13797125 per IDR”.

SPECIAL EVENT DIGEST

– 16 of 31 –

Tata Steel – Tata Metaliks Merger Bloom Code : TATA IS Equity / TML IS Equity Trade Idea & Background On 10th April 2013, the Board of Directors of Tata Steel Limited (TATA), Tata Metaliks Limited (TML) & Tata Metaliks Kubota Pipes Limited (subsidiary of TML) at their respective meetings, proposed to merge the three companies, subject to approvals from requisite statutory and regulatory authorities, the shareholders of the Companies, the High Courts. Public shareholders of TML will be issued 4 shares of TATA for every 29 shares of TML.

TML & TMKPL would be dissolved on the merger taking effect. TSL holds 50.09% (directly + indirectly) and these shares shall be extinguished. The shareholding structure is expected to change as under:

SHAREHOLDING AS ON MARCH 31, 2013

PARTICULARS TATA STEEL

TATA METALIK

MERGED

Promoter 31.4% 50.1% 31.3% FII 13.9% 0.1% 13.8% DII 27.2% 3.4% 27.2% Non-Institution 25.3% 46.4% 25.4% GDR 2.2% - 2.2% Total outstanding shares (mn shares) 971.2 1.74 972.9 Source: PhillipCapital India, NSE, BSE

Timetable:

Since amalgamation requires approvals of shareholders, High Courts (Bombay & Calcutta) etc. However, our

experience with earlier amalgamations in the merger trades suggests a minimum 5-7 months (if no major hindrance). However, the progress since the beginning has been slow and the management hasn’t given any timeline as yet.

The NSE & BSE gave their no-objection in mid-June 2012. On 1st Feb it was announced that the Court Convened Meeting of the Equity Shareholders of the TML will be

held on February 18, 2014 in Kolkata. The meeting was rescheduled to 25th March 2014. On 17th April 2014, the Bombay High Court has approved the amalgamation – Calcutta pending. The Court Convened meeting for shareholders of Tata Steel was be held on 16th May.

Current Returns & Trade Dynamics

In April 2013, the spread began @-7% (TML trading expensive) and within a week reached parity. It moved

slowly to +3% by month end. The monthly ranges were: MERGER SPREAD - RANGES MONTH HIGH LOW COMMENTS

April-2013 +3.5% -7.2% Post-announcement began @ -7%

May-2013 +4.2% +7.1% -

June-2013 +8.5% +4.6% -

July-2013 +9% +1.3% Highest spread since announcement

August-2013 +4.6% +0.9% -

September-2013 +5.4% +0.8% -

October-2013 +5.1% +2.6% -

November-2013 +6.5% +3.5% -

December-2013 +6.0% +4.3% -

January-2014 +6.4% +3.2% -

February-2014 +6.4% +2.0% -

SPECIAL EVENT DIGEST

– 17 of 31 –

March-2014 +4.4% +1% -

April-2014 +4.5% -9% Highest reverse spread

May-2014 +1.7% -6.3% -

June-2014 +0.1% -4.6% -

Merger trade setup positions are to be built with 7250 shares of TML for 1 future (1000 shares) of

TATA STEEL. Tata Metalik was shifted to trade-to-trade segment between 30 August to 28 November 2013. TML hasn’t declared dividend since 2008. TATA Steel declares dividend every year and goes ex in July. On

23rd May 2013, the company declared dividend of Rs 8 which went ex on 17th July 2013. On 14th May 2014, the company announced a dividend of Rs 10 with book closure from 16th July 2014.

Historically, TATASTEEL rolls (bps) have been fairly healthy.

Status & Our Comments

Once favourable spread is available, we suggest buying shares of TML and hedging with TATASTEEL futures. Those holding shares of TATASTEEL can convert to TML or vice versa when favourable. Since the shares of TML are trading richer than TATASTEEL, those holding TML can switch to Tata Steel or its futures. If the spread returns (to TML cheaper), one can initiate the spread around +5 - +7% range (higher allocation at higher levels) and unwind trade around +1% - +3%.

Also, we keep watch on the open interest for initiating a short roll. Recommendation Summary:

DATE RECOMMENDATION REASON

2-Jun-2014 Initiate @+5% to 7% range, keep watch for roll spread Initial part of merger process

2-May-2014 Initiate @+5% to 7% range, keep watch for roll spread Initial part of merger process

1-Apr-2014 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

3-Mar-2014 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

3-Feb-2014 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

2-Jan-2014 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

2-Dec-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

4-Nov-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

1-Oct-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

2-Sep-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

1-Aug-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

1-Jul-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

TATASTEEL ROLL SPREAD (BPS)

LHS: Futures prices; RHS: Roll bps Source: PhillipCapital , NSE

SPECIAL EVENT DIGEST

– 18 of 31 –

3-Jun-2013 Initiate @+7% to 10% range, keep watch for roll spread Initial part of merger process

2-May-2013 Wait for favourable spread +3% is too low at this stage

11-Apr-2013 Switch from TML (cash) to Tata Steel (cash/futures); went to parity in a weeks time

TML trading ~7% premium

Report Initiating coverage on the spread : 11th April 2013

Miscellaneous Recent bulk-deal activity is given below:

BULK DEALS IN TATA METALIK

DATE CLIENT NAME BUY / SELL

QTY (‘000 SHARES)

VALUE (MN) PRICE

No bulk deal since April 2013

Source : NSE, BSE

Corporate Announcements etc:

On 16th May 2014, L&T Infrastructure Development Projects Limited and Tata Steel Limited announced that they have executed a definitive agreement with Adani Ports & Special Economic Zone (“Adani Ports”) to sell 100% stake in the Dhamra Port Company Limited for an Enterprise Value of around Rs 5,500 crore.

TML results announced on 24-Apr-2014 TATA results announced on 14-May-2014 TATA : Q3 results on Feb 11, 2014 TML : Q3 results announced on Jan 20, 2014

SPECIAL EVENT DIGEST

– 19 of 31 –

UltratechCem Acquisition of unit OF JP Associates Bloom Code : UTCEM IS Equity / JPA IS Equity Trade Idea & Background

On 11th September 2013, The Board of Directors at their meeting approved the acquisition of the Gujarat Cement Unit of Jaypee Cement Corporation Limited (JCCL), by way of a demerger, comprising of an integrated cement unit at Sewagram and Grinding Unit at Wanakbori. JCCL is a wholly-owned subsidiary of Jaiprakash Associates Limited (JAL).

The enterprise value is Rs.38bn besides the actual net working capital at closing. UltraTech will take over all the assets and the liabilities of the Unit at Closing and the net amount of enterprise value less liabilities taken over will be the consideration. Such consideration will be discharged by allotment of equity shares of UltraTech to the shareholders of JCCL, subject to a maximum value of such equity shares to be Rs.1.50 bn Timetable:

The proposed transaction is subject to the approval of shareholders and creditors, sanction of the Scheme of Arrangement by the High Courts, approval of the Competition Commission of India and all other statutory approvals. The management of UTCEM & JPA anticipates the transaction to close in 7 to 9 months (April’14 – June’14).

Court convened meeting of shareholders of Ultratech Cement was held on 20th January 2014. No meeting of shareholders of JCCL needs to be held.

The Company received an order on 23rd December 2013, that the Competition Commission had approved the combination.

The Scheme filed by the Transferee Company, namely UCL, before Hon’ble High Court of Judicature at Bombay had already been sanctioned on April 04, 2014.

The Scheme of Arrangement between Jaypee Cement Corporation Limited (JCCL) and UltraTech Cement Limited (UCL) and their respective Shareholders & Creditors, Jaiprakash Associates Ltd has been approved by the Hon’ble High Court of Judicature at Allahabad has sanctioned the Scheme filed by JCCL on April 17, 2014, which was uploaded on the site on April 28, 2014.

After all approvals, the scheme was declared effective from June 12, 2014. Further, the Demerger

Implementation Committee also allotted 114,382 equity shares of the Company of Rs.10/- each credited as fully paid-up to the equity and preference share holders of JCCL in terms of the Scheme. Current Returns & Trade Dynamics

Further details are awaited. Recently UTCEM roll (bps) have been softer than JPA rolls (bps). UTCEM ROLL SPREAD (BPS) JPA ROLL SPREAD (BPS)

Status & Our Comments

SPECIAL EVENT DIGEST

– 20 of 31 –

We had recommended initiating reverse arbitrage strategies on UT. They are now unwinding at a premium (profit) now. Recommendation Summary:

DATE RECOMMENDATION REASON

2-Jun-2014 One can initiate reverse arbitrage strategies Nearing completion

2-May-2014 One can initiate reverse arbitrage strategies Nearing completion

1-Apr-2014 NA Moving forward

3-Mar-2014 NA Further details awaited

3-Feb-2014 NA Further details awaited

2-Jan-2014 NA Further details awaited

2-Dec-2013 NA Further details awaited

4-Nov-2013 NA Further details awaited

Miscellaneous Recent bulk-deal activity is given below:

BULK DEALS IN UTCEM or JPA

DATE CLIENT NAME BUY / SELL

QTY (‘000 SHARES)

VALUE (MN) PRICE

No bulk deal since September 2013

Source : NSE, BSE

Corporate Announcements etc: JPA Board meeting on 27th May 2014. On 23rd April 2014, the Board of UT declared results & dividend of Rs 9/-. On 24th March 2014, the Board of Directors of Jaiprakash Associates Limited (JAL) approved signing of Share

Purchase Agreement with M/s. Dalmia Cement (Bharat) Limited for sale of 74% stake (9,89,01,000 equity shares owned by it) in the paid-up equity share capital of Bokaro Jaypee Cement Limited (BoJCL) [a joint venture between JAL and Steel Authority of India Ltd (SAIL)] to M/s. Dalmia Cement (Bharat) Limited or any of its Associates / Affiliates. The above stake sale is subject to the approval of SAIL and such other approvals, as may be necessary from lenders of BoJCL and concerned authorities. The consideration for the transaction works out to approximately Rs. 69.74 per share (against its cost of Rs. 18.57 per share).

JPA : Q3 results announced on Feb 10, 2014 UT : Q3 results were released on Jan 20, 2013

SPECIAL EVENT DIGEST

– 21 of 31 –

United Spirits Open Offer

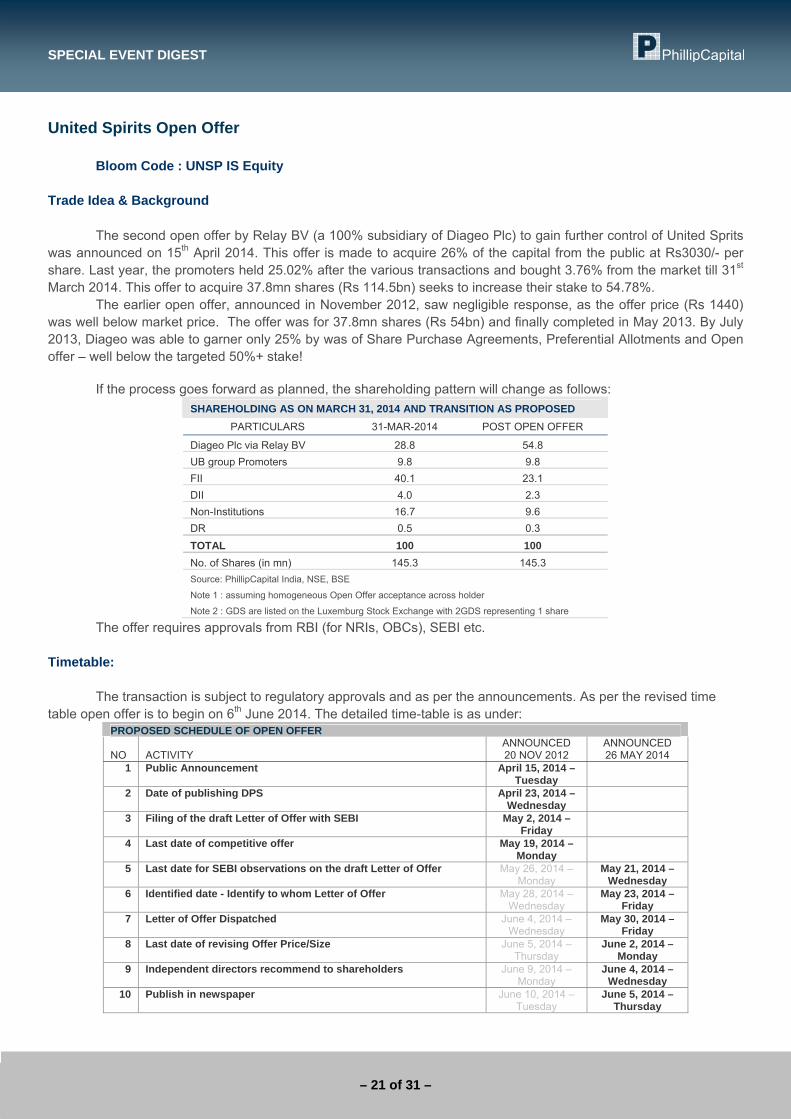

Bloom Code : UNSP IS Equity Trade Idea & Background

The second open offer by Relay BV (a 100% subsidiary of Diageo Plc) to gain further control of United Sprits was announced on 15th April 2014. This offer is made to acquire 26% of the capital from the public at Rs3030/- per share. Last year, the promoters held 25.02% after the various transactions and bought 3.76% from the market till 31st March 2014. This offer to acquire 37.8mn shares (Rs 114.5bn) seeks to increase their stake to 54.78%.

The earlier open offer, announced in November 2012, saw negligible response, as the offer price (Rs 1440) was well below market price. The offer was for 37.8mn shares (Rs 54bn) and finally completed in May 2013. By July 2013, Diageo was able to garner only 25% by was of Share Purchase Agreements, Preferential Allotments and Open offer – well below the targeted 50%+ stake!

If the process goes forward as planned, the shareholding pattern will change as follows:

SHAREHOLDING AS ON MARCH 31, 2014 AND TRANSITION AS PROPOSED PARTICULARS 31-MAR-2014 POST OPEN OFFER

Diageo Plc via Relay BV 28.8 54.8 UB group Promoters 9.8 9.8 FII 40.1 23.1 DII 4.0 2.3 Non-Institutions 16.7 9.6 DR 0.5 0.3 TOTAL 100 100 No. of Shares (in mn) 145.3 145.3 Source: PhillipCapital India, NSE, BSE

Note 1 : assuming homogeneous Open Offer acceptance across holder

Note 2 : GDS are listed on the Luxemburg Stock Exchange with 2GDS representing 1 share

The offer requires approvals from RBI (for NRIs, OBCs), SEBI etc. Timetable:

The transaction is subject to regulatory approvals and as per the announcements. As per the revised time

table open offer is to begin on 6th June 2014. The detailed time-table is as under: PROPOSED SCHEDULE OF OPEN OFFER

NO ACTIVITY ANNOUNCED 20 NOV 2012

ANNOUNCED 26 MAY 2014

1 Public Announcement April 15, 2014 – Tuesday

2 Date of publishing DPS April 23, 2014 – Wednesday

3 Filing of the draft Letter of Offer with SEBI May 2, 2014 – Friday

4 Last date of competitive offer May 19, 2014 – Monday

5 Last date for SEBI observations on the draft Letter of Offer May 26, 2014 – Monday

May 21, 2014 – Wednesday

6 Identified date - Identify to whom Letter of Offer May 28, 2014 – Wednesday

May 23, 2014 – Friday

7 Letter of Offer Dispatched June 4, 2014 – Wednesday

May 30, 2014 – Friday

8 Last date of revising Offer Price/Size June 5, 2014 – Thursday

June 2, 2014 – Monday

9 Independent directors recommend to shareholders June 9, 2014 – Monday

June 4, 2014 – Wednesday

10 Publish in newspaper June 10, 2014 – Tuesday

June 5, 2014 – Thursday

SPECIAL EVENT DIGEST

– 22 of 31 –

11 Offer Opening Date June 11, 2014 – Wednesday

June 6, 2014 – Friday

12 Offer Closing Date June 24, 2014 – Tuesday

June 19, 2014 – Thursday

13 last date of communicating the rejection/acceptance and completion of payment of consideration or refund of Equity shares

July 8, 2014 – Tuesday

July 3, 2014 – Thursday

14 Publication of Post-offer announcement July 15, 2014 – Tuesday

July 10, 2014 – Thursday

Source: announcement by acquirer(s) Current Returns & Trade Dynamics

The open offer’s minimum acceptance ratio (MAR) is calculated at 44%. However, entities with pledged

shares may also tender (if they get requisite approvals & guarantees) hence reducing the MAR further (~38%). The open offer trade (gross) profit was 1.1% at the MAR (with July Futures). Status & Our Comments

We had recommended to investors (of UNSP), on 13th June 2014, to initiate reverse arbitrage @Rs

230/- (July futures). We had also calculated that it was more beneficial to do reverse arbitrage than tender the shares in open offer. Reverse arbitrage strategy is unwinding @60bps premium – profit of ~9%.

The stock price is factoring a low Acceptance Ratio. The shares and money are expected to be credited within the next 2-days. Recommendation Summary:

DATE RECOMMENDATION REASON

2-Jun-2014 Initiate Open Offer trade with July Futures (3%-5%) Expected to complete in time.

2-May-2014 Initiate Open Offer trade with July Futures (3%-5%) Expected to complete in time.

Miscellaneous Corporate Announcements etc:

FY14 results on 27th May 2014 – they were indefinitely postponed. Major Shareholding as on 31st March 2014

Major shareholders (>1%) include:

Name Shares

(mn) % Morgan Stanley Asia (Singapore) Pte. 4.00 2.75

Merrill Lynch Capital Markets Espana Sa. S.V. 2.86 1.97

The Bank Of Nova Scotia Asia Limited 2.45 1.69

CLSA (Mauritius) Limited 2.30 1.58

New World Fund Inc 2.10 1.45

Government Of Singapore 1.65 1.14

Morgan Stanley Mauritius Company Limited 1.60 1.1

New Perspective Fund 1.59 1.1

Deutsche Securities Mauritius Limited 1.55 1.06

Vanguard Emerging Markets Stock Index Fund A series Of Vanguard 1.54 1.06

Shivanand Shankar Mankekar 1.49 1.02

USL Benefit Trust 3.46 2.38

Source: PhillipCapital, NSE, BSE

SPECIAL EVENT DIGEST

– 23 of 31 –

SUNPHARMA - RANBAXY Merger

Bloom Code : SUNP IS Equity & RBXY IS Equity Trade Idea & Background On 7th April 2014, the Board of Directors of Sun Pharma & Ranbaxy approved a merger between the companies. Pursuant to the merger, Ranbaxy will merge into Sun Pharma creating the world’s 5th largest Specialty Generic Pharma Company and the biggest in India. Ranbaxy shareholders (1 share) will get 0.8 shares of Sun Pharma.

The deal size is estimated at $4.2bn. Daiichi Sankyo, which has a 63.5% stake in Ranbaxy, would become the second-largest shareholder in the company and continue strategic business relationships with the merged entity. Additionally, Daiichi has agreed to indemnify Sun Pharma & Ranbaxy for, among other things, certain costs and expenses that may arise from the recent subpoena which Ranbaxy has received from the United States Attorney for the Toansa facility. The managements anticipates closure of the deal by end of 2014. Amongst others, the following approvals are required:

- Indian Central Government, State Governments - High Courts of Gujarat, Punjab and Haryana - Competition Commission of India - Expiration of the waiting period under the Hart-Scott-Rodino Antitrust Improvement Act in the United

States. - Approval of 75% of the shares voted by both Sun Pharma and Ranbaxy shareholders - Both Daiichi-Sankyo (63.4% of Ranbaxy) and Sun Pharma promoters (63.7%) have agreed to vote in

favor of transaction On the 9th April 2014, Sun Pharma clarified in relation to the to purchase of shares of Ranbaxy by Silverstreet Developers LLP and that it does not violate Insider Trading Rules:

· Mr. Sudhir Valia is not and was not a partner of Silverstreet Developers LLP when purchase of shares of Ranbaxy Laboratories Ltd was affected by LLP. · Silverstreet Developers LLP has two partners. Both are 100% subsidiaries of Sun Pharma. Hence, all the benefits flowing from the investment in Ranbaxy shall accrue to Sun Pharma.

Incidental to the merger, Sun Pharma (announced on 11th April 2014) would make an open offer for 28.1% of the equity capital of Zenotech Laboratories Ltd, as Ranbaxy owns 46.8%. . The offer would be at Rs 19 per share. The shares are listed on BSE. The shareholding structure is expected to change as under:

SHAREHOLDING AS ON 31st MARCH, 2014

PARTICULARS SUN PHARMA RANBAXY MERGED Sun Pharma promoters 63.7 -* 54.7 Ranbaxy promoters - 63.4 8.9 FII 22.5 11.8 21.0 DII 5.5 8.3 5.9 Non-Institution 8.3 15.0 9.2 GDR 0.0 1.5 0.2 Total outstanding shares (mn shares) 2071 424 2410

MAJOR SHAREHOLDERS

Genesis Indian Investment Company Ltd General Sub Fund 2.3 - 2.0

SPECIAL EVENT DIGEST

– 24 of 31 –

Lakshdeep Investments & Finance Pvt Ltd 1.1 - 0.9 Skagen Kon-Tiki Verdipapirfond - 1.2 0.2 Life Insurance Corporation of India - 6.0 0.8 Orange Mauritius Investments Ltd - 1.1 0.2 Silverstreet Developers LLP - 1.6* 0.2 Source: NSE, BSE, PhillipCapital

• * Clarification of treatment of shares issued to Silverstreet Developers LLP

• 1 RBXY GDR = 1 equity share; Unsponsored GDR listed on the Luxemburg Stock Exchange Current Returns & Trade Dynamics

The proposed deal involves the shareholders & multiple government agencies (India & US) and is therefore susceptible to delays. The promoters have a 63%+ stake each in the companies and hence are close to the 75% mark for passing a resolution in favour of the merger.

On 29th April 2014, the high court of Andhra Pradesh, ordered an "interim status quo" on the deal and asked all the involved companies, the regulator, and the stock exchanges for details. A couple of weeks earlier, two individuals filed the petition in the high court, requesting the court ask the market regulator and the two main stock exchanges to halt the deal and order the probe. On 24th May 2014, the Court vacated the Status Quo order and directed SEBI to probe into the allegations.

On 28th June 2014, at an awards function, Uday Baldota, Senior Vice President of Finance & Accounts,

Sun Pharma commented “All the approvals that are there, we are moving along - till now the journey has been relatively smooth. We would expect that the original deal timetable that we laid out of closing by December 2014, more or less we are there”.

SUNPHARMA & RANBAXY futures rolls trade mostly at a premium as shown in the graph below:

SUNPHARMA ROLL SPREAD (BPS) RANBAXY ROLL SPREAD (BPS)

LHS: Futures prices; RHS: Roll bps

Source: PhillipCapital , NSE

Status & Our Comments

Within a month of the announcement of the merger, litigation had emerged but was sorted out swiftly. As the deal is in the preliminary stage we would recommend to spreads in excess of 7-11% to initiate with smaller allocation (especially at the lower end of the band). Recommendation Summary:

DATE RECOMMENDATION REASON

2-Jun-2014 Initiate spreads around 9-12% with smaller allocation at the lower end of the band.

Early part of the merger process

2-May-2014 Initiate spreads around 9-12% with smaller allocation at the lower end of the band.

Early part of the merger process

SPECIAL EVENT DIGEST

– 25 of 31 –

Miscellaneous Corporate Announcements etc:

Ranbaxy : FY14 results on May 29, 2014 SunPharma : FY14 results on 29th May 2014.

SPECIAL EVENT DIGEST

– 26 of 31 –

ETF on the CPSE Index Bloom Code : CPSE Index Trade Idea & Background In March 2014, the CPSE Index was constructed in order to facilitate Government of India’s initiative to dis-invest some of its stake in selected CPSEs. The government opted for ETF route for disinvestment. The ETF would track the performance of the CPSE index and is managed by Goldman AMC. In its 1st tranche they sought to garner Rs30bn. They collected Rs8.5bn from Anchor investors on 18th March and a total of Rs 40bn (non-anchor 19th to 21st March 2014). The initial attraction for subscription to the ETF was a 5% discount being offered by the Government to the ETF holders. One could subscribe in the NFO & hedge with constituent stock futures (of ~83% value of the index). Around 17% of the position would be unhedged. On listing of CPSE ETF one can square up the positions. Timetable:

The 1st tranche was listed on the exchanges on 4th April 2014. Tap Structure : At the beginning of each quarter, the maximum amount of units available for subscription &

discount offered will be announced. In this the investors can purchase in multiple of 100k units and pricing will be determined as per “Tap Structure Reference Market Price” (daily VWAP). Current Returns & Trade Dynamics

The futures rolls of the constituents initially softened but picked up later and were as follows: ROLL SPREADS PARTICULARS \ SCRIP ONGC GAIL COALINDIA RECLTD IOC OIL CONCOR PFC BEL ENGINERSIN APPROX WEIGHTAGE 27.6 17.8 17.3 7.1 7.0 7.0 6.6 6.4 2.1 1.3 MAR’14 : Roll Bps (High) 85 70 91 81 80 na na 87 na na MAR’14 : Roll Bps (Low) 23 -14 2 5 -16 na na 0 na na MAR’14 : Reference Price 313.6 358.1 263.0 209.6 254.5 483.3 833.1 176.2 1017.3 188.2

Apr'14 : Roll Bps (High) 98 97 100 94 94 na na 102 na na Apr'14 : Roll Bps (Low) 84 81 89 78 74 na na 84 na na May'14 : Roll Bps (High) 67 68 68 68 66 na na 68 na na

May’14 : Roll Bps (Low) 53 50 52 48 51 na na 34 na na

Jun'14 : Roll Bps (High) 84 81 83 80 83 na na 84 na na Jun’14 : Roll Bps (Low) 64 58 71 67 67 na na 68 na na

Corporate Action: Dividend Dividend na Dividend Dividend Dividend Dividend Dividend Dividend Dividend

Rs/Ratio Rs4.25 Rs5.90 Rs1.75 Rs8.70 Rs0.50 Rs5.30 Rs0.20 Rs17.30 Rs3.5 Ex-date 27/3/14 TBA TBA TBA TBA TBA TBA TBA 20/3/14

Source: PhillipCapital India, NSE

Status & Our Comments One can subscribe to CPSE ETF & sell constituent futures (partial hedge) in the tap structure issue in the future. Recommendation Summary:

DATE RECOMMENDATION REASON

Mar’14 Subscribe ETF & hedge (partial) Attractive pricing.

Miscellaneous

SPECIAL EVENT DIGEST

– 27 of 31 –

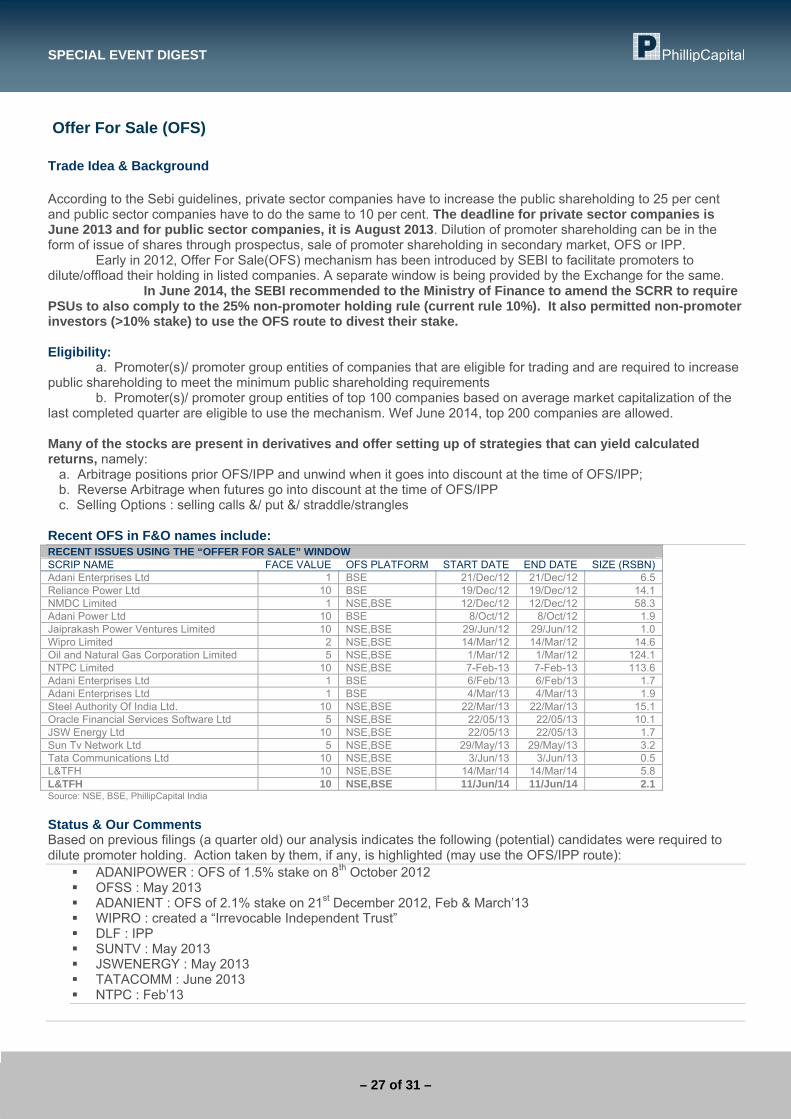

Offer For Sale (OFS) Trade Idea & Background According to the Sebi guidelines, private sector companies have to increase the public shareholding to 25 per cent and public sector companies have to do the same to 10 per cent. The deadline for private sector companies is June 2013 and for public sector companies, it is August 2013. Dilution of promoter shareholding can be in the form of issue of shares through prospectus, sale of promoter shareholding in secondary market, OFS or IPP.

Early in 2012, Offer For Sale(OFS) mechanism has been introduced by SEBI to facilitate promoters to dilute/offload their holding in listed companies. A separate window is being provided by the Exchange for the same. In June 2014, the SEBI recommended to the Ministry of Finance to amend the SCRR to require PSUs to also comply to the 25% non-promoter holding rule (current rule 10%). It also permitted non-promoter investors (>10% stake) to use the OFS route to divest their stake. Eligibility:

a. Promoter(s)/ promoter group entities of companies that are eligible for trading and are required to increase public shareholding to meet the minimum public shareholding requirements

b. Promoter(s)/ promoter group entities of top 100 companies based on average market capitalization of the last completed quarter are eligible to use the mechanism. Wef June 2014, top 200 companies are allowed. Many of the stocks are present in derivatives and offer setting up of strategies that can yield calculated returns, namely: a. Arbitrage positions prior OFS/IPP and unwind when it goes into discount at the time of OFS/IPP; b. Reverse Arbitrage when futures go into discount at the time of OFS/IPP c. Selling Options : selling calls &/ put &/ straddle/strangles Recent OFS in F&O names include: RECENT ISSUES USING THE “OFFER FOR SALE” WINDOW SCRIP NAME FACE VALUE OFS PLATFORM START DATE END DATE SIZE (RSBN) Adani Enterprises Ltd 1 BSE 21/Dec/12 21/Dec/12 6.5 Reliance Power Ltd 10 BSE 19/Dec/12 19/Dec/12 14.1 NMDC Limited 1 NSE,BSE 12/Dec/12 12/Dec/12 58.3 Adani Power Ltd 10 BSE 8/Oct/12 8/Oct/12 1.9 Jaiprakash Power Ventures Limited 10 NSE,BSE 29/Jun/12 29/Jun/12 1.0 Wipro Limited 2 NSE,BSE 14/Mar/12 14/Mar/12 14.6 Oil and Natural Gas Corporation Limited 5 NSE,BSE 1/Mar/12 1/Mar/12 124.1 NTPC Limited 10 NSE,BSE 7-Feb-13 7-Feb-13 113.6 Adani Enterprises Ltd 1 BSE 6/Feb/13 6/Feb/13 1.7 Adani Enterprises Ltd 1 BSE 4/Mar/13 4/Mar/13 1.9 Steel Authority Of India Ltd. 10 NSE,BSE 22/Mar/13 22/Mar/13 15.1 Oracle Financial Services Software Ltd 5 NSE,BSE 22/05/13 22/05/13 10.1 JSW Energy Ltd 10 NSE,BSE 22/05/13 22/05/13 1.7 Sun Tv Network Ltd 5 NSE,BSE 29/May/13 29/May/13 3.2 Tata Communications Ltd 10 NSE,BSE 3/Jun/13 3/Jun/13 0.5 L&TFH 10 NSE,BSE 14/Mar/14 14/Mar/14 5.8 L&TFH 10 NSE,BSE 11/Jun/14 11/Jun/14 2.1 Source: NSE, BSE, PhillipCapital India Status & Our Comments Based on previous filings (a quarter old) our analysis indicates the following (potential) candidates were required to dilute promoter holding. Action taken by them, if any, is highlighted (may use the OFS/IPP route):

ADANIPOWER : OFS of 1.5% stake on 8th October 2012 OFSS : May 2013 ADANIENT : OFS of 2.1% stake on 21st December 2012, Feb & March’13 WIPRO : created a “Irrevocable Independent Trust” DLF : IPP SUNTV : May 2013 JSWENERGY : May 2013 TATACOMM : June 2013 NTPC : Feb’13

SPECIAL EVENT DIGEST

– 28 of 31 –

CORPORATE BUY-BACK PROGRAMMES NOT ACTIVELY COVERED

OPEN MARKET BUYBACKS

P U B L I C A N N O U N C E M E N T

SCRIP DATE CMP PA

START DT

CLOSE DT

BB PRICE

MIN%

MAX%

SIZE (Mn)

NPH%

PROMO INCL CURRENT STATUS

CROMPGREAV

28-Jun-13

Rs 87.3

16-Jul-2013

15-Jan-2014

Rs 125 1.7% 3.3% $40 58% No Closed wef 15 Jan 2014

JINDALSTEL 30-

Aug-13

Rs 221.9

16-Sep-2013

15-Mar-2014

Rs 261 2% 4.1% $150 49% No 52.09% completed & closed on

18Feb'14

UPL 30-Dec 196.55 9/Jan

2014 9/Jul 2014

Rs 220 1.6% 3.2% $50 71% No Completed & Closed on 3rd Feb

2014

CAIRN 26-Nov 324.2 23/Jan

2014 22/Jul 2014

Rs 335 4.5% 8.9% $910 41% No 22% complete

SPECIAL EVENT DIGEST

– 29 of 31 –

CORPORATE MERGERS & ACQUISITIONS ETC NOT ACTIVELY COVERED Stake Sale of Govt Stake in Hindustan Zinc

Announced on : 20th January 2014

The CCEA decided to sell the residual stake of the Government in Hindustan Zinc. As per the latest exchange filings, the promoter (Vedanta) holds 64.92% & the Govt holds 29.54%. If Vedanta buys the Government stake, its holding will go up to 94.46%, well below the permissible limits (75%) and may trigger a delisting offer. However, since the said deal is with the Government as a counter-party, variations/exemptions are possible from the rule. RCOM demerger

Announced on : 7th July 2013 Reliance Communications (RCOM) announced that its Board of Directors had in-principle decided on a demerger of the real estate held by RCOM into a separate unit, Reliance Properties Ltd., to unlock substantial value for the benefit of its approx. 2 million institutional and retail shareholders.

The proposed separation of real estate into a separate unit is part of RCOM’s strategic plan to divest non-core assets, and focus on its core wireless and enterprise business. Reliance Properties Ltd. Will be a separate listed Company. All shareholders of RCOM will receive fully tradeable pro-rata shareholding in Reliance Properties Ltd., based on their existing shareholding in RCOM. The preliminary and indicative monetisable value of RCOM’s real estate on development is estimated by independent valuers at over Rs. 12,000 crore (US$ 2 billion), which is equal to Rs. 60 (US$ 1) per RCOM share. SBIN Expected to be announced in the future State Bank of Saurashtra was merged with SBI in 2008 and State Bank of Indore in 2010. The State Bank of India has five associate banks — State Bank of Patiala, State Bank of Hyderabad, State Bank of Mysore, State Bank Travancore and State Bank of Bikaner & Jaipur. SBM, SBT & SBBJ are listed. Over time these are expected to be merged into SBI. The Government holds 94.5% in SBM, 77% in SBT & 77.5% in SBBJ. Bonus & Right Announcements - Expect PSBs are expected to issue right shares in FY14 - KTKBANK announced a rights issue on 14th September 2012. Details & record date is yet to be announced. - UNIONBANK announced a rights issue on 27th December 2012. Details & record date is yet to be announced. Miscellaneous We keep lookout for the announcements relating to the PSUs, PSBs FPO.

SPECIAL EVENT DIGEST

– 30 of 31 –

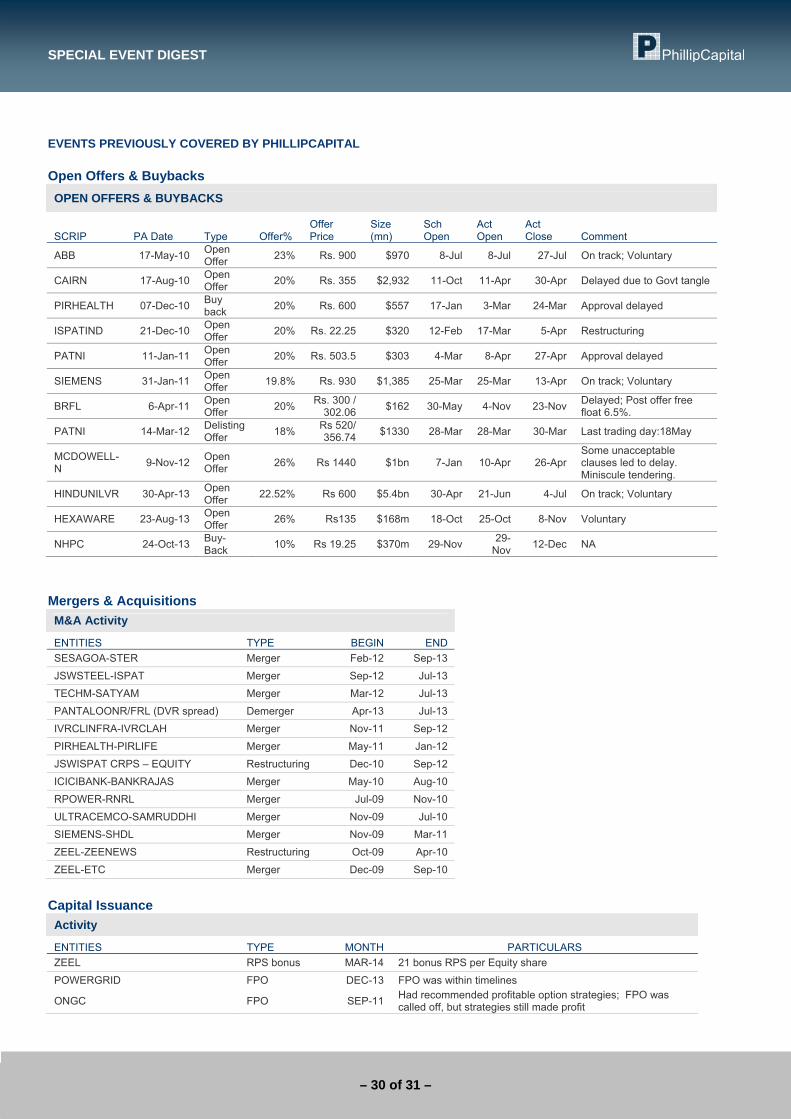

EVENTS PREVIOUSLY COVERED BY PHILLIPCAPITAL Open Offers & Buybacks OPEN OFFERS & BUYBACKS

SCRIP PA Date Type Offer% Offer Price

Size (mn)

Sch Open

Act Open

Act Close Comment

ABB 17-May-10 Open Offer 23% Rs. 900 $970 8-Jul 8-Jul 27-Jul On track; Voluntary

CAIRN 17-Aug-10 Open Offer 20% Rs. 355 $2,932 11-Oct 11-Apr 30-Apr Delayed due to Govt tangle

PIRHEALTH 07-Dec-10 Buy back 20% Rs. 600 $557 17-Jan 3-Mar 24-Mar Approval delayed

ISPATIND 21-Dec-10 Open Offer 20% Rs. 22.25 $320 12-Feb 17-Mar 5-Apr Restructuring

PATNI 11-Jan-11 Open Offer 20% Rs. 503.5 $303 4-Mar 8-Apr 27-Apr Approval delayed

SIEMENS 31-Jan-11 Open Offer 19.8% Rs. 930 $1,385 25-Mar 25-Mar 13-Apr On track; Voluntary

BRFL 6-Apr-11 Open Offer 20% Rs. 300 /

302.06 $162 30-May 4-Nov 23-Nov Delayed; Post offer free float 6.5%.

PATNI 14-Mar-12 Delisting Offer 18% Rs 520/