ambank group results · pdf fileambank group results investors presentation 9mfy2011 results...

TRANSCRIPT

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011

AMMB Holdings Berhad

Cheah Tek KuangGroup Managing Director

AmBank Group Results

Investors Presentation

9MFY2011 Results Update18 February 2011

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 1(Conventional + Islamic)

AmBank Group:

• More than 30 years of banking franchise

• Top 20 Bursa Saham listing, ranked top 170 on globalbanking index

• 3 consecutive years of record performance (FY08-FY10), on track to deliver the 4th

FY2011 Performance:

• 9MFY2011 PATMI up 34%

• FY2011 PATMI expectations circa +30%

• Staying focused on profitable growth, diversificationand sustainability

• Ratings upgraded 1-notch recently1

FY2012 onwards:

• 2011 GDP expected to slow to 5-5.5%, with ETP providingsome support

• Well positioned for growth, will continue leveraging onour customer focused business models and ANZ todifferentiate

9MFY2011 Highlights

Note : Update since H1FY2011 Investors Presentation highlighted in italics and blue1 AmBank (M) and AmInvestment Bank upgraded to BBB/A-2/Stable by S&P on 15 December 2010

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 2(Conventional + Islamic)

Contents

9MFY2011 Group Financial Performance

Strategy & Outlook

Divisional Performance

Supplementary Information

Executive Summary

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 3(Conventional + Islamic)

Maintaining earnings growth momentumP

erf

orm

an

ce

Profit after Tax & MI (PATMI)

ROE

Ris

k, C

apit

al &

Fu

nd

ing

Pro

file

RWCA

Tier 1

Gross Impaired Loans

Gro

wth Net Lending / Financing 1

Customer Deposits 2

LD Ratio 3

EPS(basic, annualised)

95.5%

N/A

67,293 mil

64,239 mil

35.4 sen

11.9%

766.9 mil

9MFY10

90.5%

3.4%

76,852 mil

69,529 mil

45.3 sen

13.9%

1,026.5 mil

9MFY11

5.0%

N/A

14.2%

8.2% 4

28.0%

2.0%

34%

Change

ROA 1.15% 1.43% 0.28%

FY09 FY10

88.7%

9.7%

15.2%

N/A

65,192 mil

57,854 mil

31.6 sen

11.7%

860.8 mil

91.5%

10.3%

15.8%

3.8%

70,776 mil

64,772 mil

34.7 sen

11.5%

1,008.6 mil

1.04% 1.13%

15.3%

9.8%

Note :1 Includes Islamic loans sold with recourse : 9MFY10 = RM365mil and 9MFY11 =RM1,582mil 2 Adjusted customer deposits includes Senior Notes RM3.39 bil, credit-linked notes RM0.17bil, loans sold with and without recourse3 Based on net loans including loans sold with recourse, over adjusted customer deposits as above4 AmBank Group’s 2-year net loans growth CAGR = 9.6%; system 2-year loans growth CAGR = 10.1%

15.1% 0.2%

9.4% 0.4%

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 4(Conventional + Islamic)

Staying focused on profitable growth, diversification and sustainability

Staying Ahead

Strong 9M results Higher revenues and lower

allowances

Good loans & customer deposits

growth

FRS139 adopted under BNM transition

arrangements since April 2010

Implemented customer segmentation

and focus across all divisions

Well diversified Divisional contributions

Sound contributions from Retail and Business Banking Divisions

Diversified portfolios yielding higher profits in Life Assurance, General Insurance and Markets

Good pipeline for Corporate & Institutional Banking and Investment Banking

Improved risk, funding, and financial disciplines

Proactive risk management

Balance sheet positioned for rising interest rates and Basel III

Implemented new FTP* and FRS disciplines

FY 2011 Priorities

FY2011 : Profitable growth, diversification & rebalancing Faster non-interest income & CASA growth Taking opportunities in growth plans

MTA : Malaysia’s Preferred Banking Group with International Connectivity Customer satisfaction Sound financial performancesWell diversified and sustainable growth

* FTP = funds transfer pricing

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 5(Conventional + Islamic)

Note :1 In-house research2 Update since H1FY2011 Investors Presentation highlighted in italics and blue

Opportunity

• Malaysian economic recovery to continue (GDP CY 2010e :7.0%1, CY 2011e : 5-5.5%1) with higher retail consumption

• 2011 looking positive but not immune to possible globalshocks

• Supportive monetary policies, continued trade surplus;domestic demand leading the way

• Economic Transformation Programme (ETP) and recentlyannounced EPP’s (entry point projects) to mitigate global riskand moderating external demand

• System lending growth may moderate in CY 2011• Anticipating OPR hike of circa 50bps in CY2011• Higher common equity & stable funding requirements

under Basel III, but with longer transition period

• Execute to strategic themes and strengthen marketpositions

• Leverage opportunities available in domestic economygrowth plans

• Better positioned for rising interest rates• Leverage ANZ’s international connectivity

2Industry :Emerging

Opportunities & Challenges

1Malaysia :

Stable Outlook

3AHB :

Leveraging Tailwinds

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011

AMMB Holdings Berhad

Ashok RamamurthyDeputy Group Managing Director &

Group Chief Financial Officer

AmBank Group Results

Investors Presentation

9MFY2011 Results Update18 February 2011

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 7(Conventional + Islamic)

Contents

Executive Summary

Strategy & Outlook

Divisional Performance

9MFY2011 Group Financial Performance

Supplementary Information

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 8(Conventional + Islamic)

Strong and consistent financial performance for 9MFY2011

Business Performance

Income :

Good growth from most Divisions, 9MFY11 run-rate better than FY2010 full year

Higher trading income in 9MFY2010 due to a large gain on disposal of an underwritten bond issuance

Non interest income = 30.4% of total income

Expenses :

Salary & staffing increases, CPI & ongoing medium term investments but within CTI targets

Impairments / Allowances :

Lower individual & collective impairments (combined)

Includes PER, impairment losses & allowances for commitments & contingencies

Islamic banking contributed 17.7% to Group’s PAT, down from 30.7% due to large gain on disposal of an underwritten bond issuance in 9MFY10

9MFY10 results Positive growth in 9MFY11 Contraction in 9MFY11

Fee57%

Trading26%

Insurance

15%

Others1%

Non-Interest Income Composition

RM'mil 9MFY10 9MFY11

Net interest income 1,848.3 2,053.7 +11.1%

Fee and commission 468.8 513.0 +9.4%

Investment and trading 248.7 236.3 -5.0%

Insurance business 92.9 136.1 +46.5%

Others 11.3 12.4 +9.7%

Total Income 2,670.0 2,951.4 +10.5%

Expenses 1,089.9 1,165.9 +7.0%

PBP 1,580.0 1,785.5 +13.0%

Impairments / Allowances 512.2 345.9 -32.5%

PBT 1,067.9 1,439.6 +34.8%

PAT 791.5 1,064.7 +34.5%

PATMI 766.9 1,026.5 +34%

9MFY11 vs

9MFY10

GG

G

GG

G

G

G

G

G

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 9(Conventional + Islamic)

Retail, 44%

Business,14%CIB, 15%

Investment, 9%

Markets, 15%

Life, 5%

General,4%

Operating-6%

PATMI contribution %

Well diversified contributions

Business Performance

Retail Banking - profit growth via focus on viable segments

Business Banking - well-balanced profits with income growth and lower allowances

Investment banking – good pipeline, slower start in Q1FY11 but picked up in Q2 and Q3

CIB – higher incomes from lending and international businesses

Life Assurance and General Insurance - higher incomes from larger fund base and better efficiencies

Markets – higher contribution from Fx and Derivatives

Note 1 : Life Assurance surplus is transferred into life policy shareholders’ fund in overall Group accounts

PATMI (by division)

9MFY10 results Positive growth in 9MFY11 Contraction in 9MFY11

10%

RM'mil 9MFY10 9MFY11

Retail Banking 399.3 450.1 +12.7%

Business Banking 125.9 148.8 +18.2%

Corporate & Institutional

Banking (CIB) 124.8 153.5 +23.0%

Investment Banking 104.2 90.5 -13.1%

Markets 88.6 151.2 +70.7%

Assurance 56.7 97.8 +72.5%

Life Assurance 19.1 51.6 +>100%

General Insurance 37.6 46.2 +22.9%

Operating Segments (132.6) (65.4) +50.7%

9MFY11 vs

9MFY10

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 10(Conventional + Islamic)

3.63% 3.66%

3.44%

2.68%

2.89%

2.47%

2.83%3.04%

2.98% 2.97%

FY07 FY08 FY09 FY10 9MFY11

NIM and Cost of Funds

Cost of funds NIM

511.2

6.6 121.3

638.2 618.2

298.5

123.7

1,058.5

513.0

236.3 136.1

897.7

Fee income Trading & Investment income

Insurance business Total non-interest income

Non-Interest Income, RM'mil

FY09 FY10 9MFY11

Moderating NIM* and improving efficiency

Business Performance

* NIM up YoY, but reducing QoQ due to :

Interest in suspense being disclosed under

impairments per FRS139 requirements

Immediate benefit from BLR increases

Lagged impact of term deposit increase on cost of

funds

• Lower CTI mainly due to higher income

• Non-interest income / total income stable compared

to prior corresponding period, but higher than FY10

of 29.6%

9MFY10 results Positive growth in 9MFY11 Contraction in 9MFY11

Note :1 Net Interest Margin includes Net Financing Income from Islamic Banking business : 9MFY10 – 0.73% and 9MFY11 – 0.70%2 NIM FY07-FY10 as per reported in previous investors’ presentations3 COF FY07-FY08 based on data as disclosed in annual reports, FY09-9MFY11 based on internal data computation

% non-interest income / total incomeFY09 : 21.8% FY10 : 29.6% 9MFY11 : 30.4%

9MFY10 9MFY11

Net Interest Margin

(NIM & NFR composite) 2.92% 2.97% +0.05%

Cost-Income

(CTI) 40.8% 39.5% -1.3%

Cost-Asset

(CTA) 1.58% 1.56% -0.02%

Profit before Tax (PBT)

/ Employee (RM'mil) 0.14 0.18 30.3%

Non-interest income /

Total Income 30.8% 30.4% -0.4%

9MFY11 vs 9MFY10

GG

G

GGGGGGGGG

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 11(Conventional + Islamic)

40.2

51.658.4 62.4

67.35.3

6.3

6.88.4

9.5

FY07 FY08 FY09 FY10 9MFY11

RM'bil

Customer Deposits

CASA All other deposits

53.5 56.9 59.766.6

71.9

FY07 FY08 FY09 FY10 9MFY11

RM'bilGross Loans

Balancing loans and strong CASA / customer deposits growth

Business Performance

Loans growth targeting viable

and profitable segments

Improving funding profiles

LD ratio within acceptable levels

Note :1 Adjusted Customer Deposits : includes RM3.39 bil Senior Notes, RM0.17bil credit-linked notes, loans sold with and without recourse2 LD : net loans including loans sold with recourse / adjusted customer deposits + loans sold with and without recourse

9MFY10 results Positive growth in 9MFY11 Contraction in 9MFY11

Customer 45.5b 57.9b 65.2b 70.8b 76.9bdeposits 1

p 7.9%p 8.6%

RM'mil 9MFY10 9MFY11

Balance Sheet - Lending / Financing

Gross Loans / Financing 66,311.7 71,874.8 +8.4%

Net Loans / Financing 64,238.9 69,529.0 +8.2%

Balance Sheet - Deposits

Customer Deposits 67,292.6 76,851.6 +14.2%

LD Ratio 95.5% 90.5% -5.0%

CASA Deposits 8,227.8 9,540.2 +16.0%

CASA Proportion 12.3% 13.5% +1.2%

9MFY11 vs 9MFY10

1

2

2

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 12(Conventional + Islamic)

2.24%1.92% 1.73% 3.18%

0.97% 0.60%0.88%

0.56% 0.59% 0.69%

14.8%

17.4%

12.4%

10.4%

6.3%

4.1%2.8%

3.8% 3.6% 3.6% 3.4%

10.9%

13.8%

9.6%

6.2%

3.7%2.6%

1.5%

0%

5%

10%

15%

20%

4.28 5.78

4.60 3.18

2.02 1.50 1.01 2.54 2.47 2.56 2.41

39.3% 32.2% 36.7%

56.6%67.3%

75.1%

99.5% 89.1% 93.7% 95.5% 97.4%

-60%

-20%

20%

60%

100%

-

5.0

10.0

15.0

RM'bil

Asset quality : Benefitting from differentiated product growth strategies

Asset Quality Indicators

6.06

7.60

6.145.53

3.602.43

1.87

Net NPL Gross NPL Loan loss coverage Gross impaired loans Allowance coverage

FRS 139

FRS139 adopted under BNM transitional arrangements since April 2010

Historical figures under GP3 basis and not comparable

Continue to enhance :

Collections systems

Credit / risk tools

Risk / impaired loans management team

Allowance coverage9MFY11 / Day1 change h8.3%

Gross impaired loans9MFY11 / Day1 change i5.1%

FRS 139

Gross impaired loans %9MFY11 / Day1 change i0.4%

Gross impaired loans Loan loss chargeGross NPL ratio Net NPL ratio Net provisions charge

FY2004 FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY2010 Day 1 Q1FY11 H1FY11 9MFY11

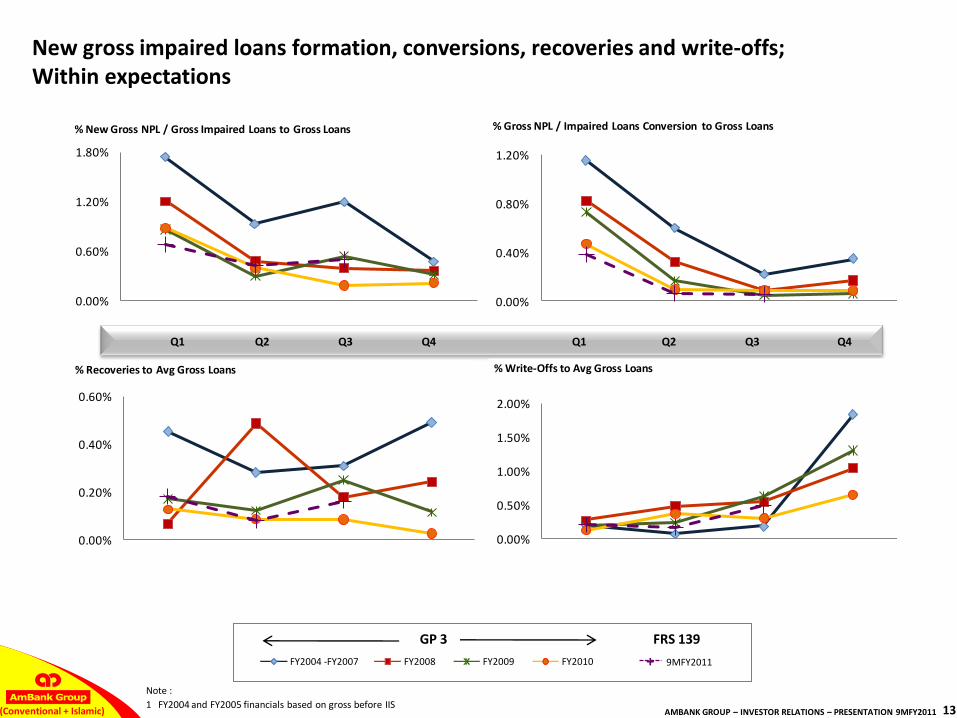

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 13(Conventional + Islamic)

0.00%

0.40%

0.80%

1.20%

Q1 Q2 Q3 Q4

% Gross NPL / Impaired Loans Conversion to Gross Loans

0.00%

0.60%

1.20%

1.80%

Q1 Q2 Q3 Q4

% New Gross NPL / Gross Impaired Loans to Gross Loans

New gross impaired loans formation, conversions, recoveries and write-offs; Within expectations

Note :

1 FY2004 and FY2005 financials based on gross before IIS

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

GP 3 FRS 139

FY2004 -FY2007 FY2008 FY2009 FY2010 9MFY2011+

0.00%

0.20%

0.40%

0.60%

Q1 Q2 Q3 Q4

% Recoveries to Avg Gross Loans

0.00%

0.50%

1.00%

1.50%

2.00%

Q1 Q2 Q3 Q4

% Write-Offs to Avg Gross Loans

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 14(Conventional + Islamic)

FY08

RM'bil

Retail

Biz / Corp & others10.8 9.9

1.2

13.8

11.6

1.4

Business Banking (ex GLR)

Corporate & Institutional

Banking

Others

17.9%

12.7%

27.2%

FY08

RM'bil

Retail

Biz / Corp & others

24.4

13.6

0.9 0.9 2.0 2.5

14.0

1.02.3

Auto Financing Mortgage Credit Cards Line of Credit Co-Op Asset Financing

RM'bil Dec '10 Dec '09

3.3%

7.4%

4.9%11.0%

10.9%

0.2%

2.6

0.8

24.3

Retail : target viable and profitable segments

Biz & SME growth : stable and preferred growth sectors

CIB : project financing with government support, GLC’s & large MNC’s

Increasing composition of variable rate loans

Increasing composition of Business / Corporate loans

Portfolio rebalancing : Focus on viable segments and diversification

Gross Loan / Financing movement (gross before netting loans sold to Cagamas)

by Interest Rate Type

Loan Composition %33.9% 19.6% 1.4% 1.2% 3.7%3.1% 19.2% 16.2% 1.9%

Retail (63%) Business / Corporate (37%)

by Retail & Business / Corporate

Retail banking loans growth : 1.6%

RM'bil Mar-08 Mar-09 Mar-10 Dec-10

Retail 74% 72% 65% 63%

Biz / Corp & others 26% 28% 35% 37%

RM'bil Mar-08 Mar-09 Mar-10 Dec-10

Fixed rate :

Conventional 47% 43% 39% 36%

Islamic 15% 17% 17% 15%

62% 60% 56% 51%

Variable rate :

Conventional 38% 40% 43% 46%

Islamic 0.1% 0.3% 1.6% 3.7%

38% 40% 44% 49%

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 15(Conventional + Islamic)

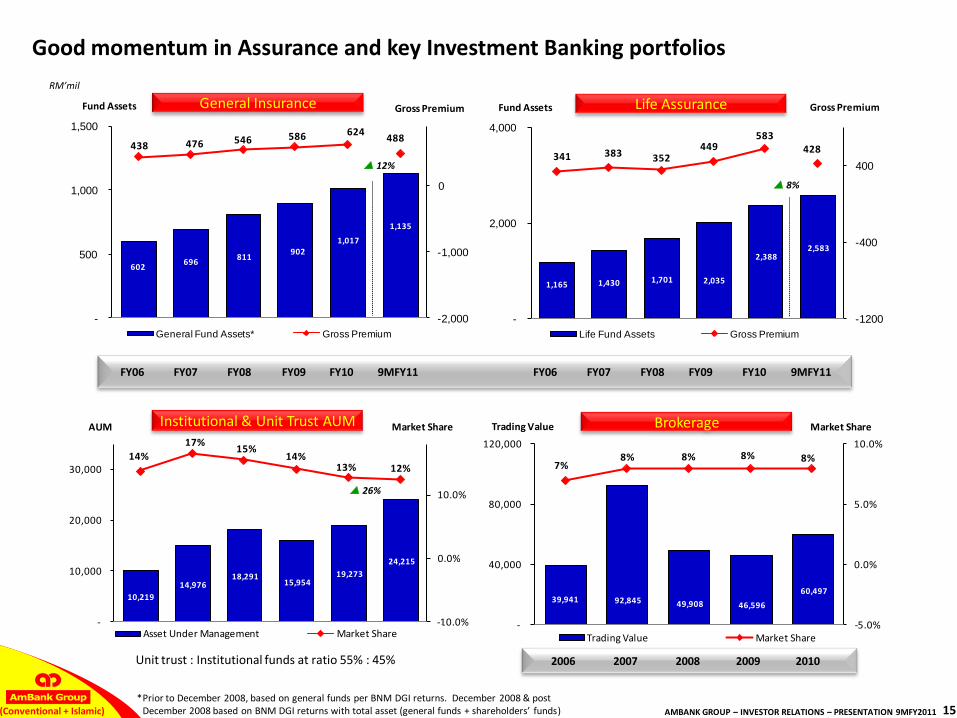

39,941 92,845 49,908 46,596

60,497

7%8% 8% 8% 8%

-5.0%

0.0%

5.0%

10.0%

-

40,000

80,000

120,000

Market ShareTrading Value

Trading Value Market Share

1,165 1,430 1,701 2,035

2,388 2,583

341 383 352 449

583 428

-1200

-400

400

-

2,000

4,000

Gross PremiumFund Assets

Life Fund Assets Gross Premium

602 696

811 902

1,017

1,135

438 476 546 586 624 488

-2,000

-1,000

0

-

500

1,000

1,500

Gross PremiumFund Assets

General Fund Assets* Gross Premium

10,219

14,976 18,291

15,954 19,273

24,215

14%

17%15%

14%13% 12%

-10.0%

0.0%

10.0%

-

10,000

20,000

30,000

Market ShareAUM

Asset Under Management Market Share

Institutional & Unit Trust AUM

p 26%

Good momentum in Assurance and key Investment Banking portfolios

FY06 FY07 FY08 FY09 FY10 9MFY11 FY06 FY07 FY08 FY09 FY10 9MFY11

General Insurance

*Prior to December 2008, based on general funds per BNM DGI returns. December 2008 & post December 2008 based on BNM DGI returns with total asset (general funds + shareholders’ funds)

RM’mil

2006 2007 2008 2009 2010

Brokerage

Life Assurance

p 8%

p 12%

Unit trust : Institutional funds at ratio 55% : 45%

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 16(Conventional + Islamic)

5.8% 7.6% 7.7% 8.1% 7.3%

6.8%8.5% 9.7% 10.3% 9.4%10.1%

14.1%15.2% 15.8% 15.1%

FY2007 FY2008 FY2009 FY2010 9MFY2011RWCA Tier 1 Ratio Common Equity Ratio

(13.3)

28.2 31.6 34.7 45.3

EPS, basicsen/share

-0.17%

1.02% 1.04% 1.13% 1.43%

ROA, %

Strong capital position and improving returns

AmBank (M) paid final dividend RM283mil (FY10) and interim dividend RM381mil (FY11) in 9MFY11 resulting in lower unappropriated profits for capital adequacy computation

Innovative T1 (AmBank (M) Berhad) :

Approved = RM500 mil

Q1FY10 issuance = RM300 mil

Q2FY10 issuance = RM185 mil

Tier 2 :

Q3FY10 : 7th tranche MTN RM98 mil, total to-date RM1.56 bil

Capital management plan :

1. Optimise capital profile & buffer

2. Increase scenario modeling

3. Streamline corporate structures

4. Develop dynamic dividend policy

5. Proactively manage Basel III requirements

FY07 FY08 FY09 FY10 9MFY11 FY07 FY08 FY09 FY10 9MFY11 FY07 FY08 FY09 FY10 9MFY11

9MFY11 / FY10 change h2.4%FY10 / FY09 change i0.2%

9MFY11 / FY10 change h0.30%FY10 / FY09 change h0.09%

9MFY11 / FY10 change h30.5%FY10 / FY09 change h9.8%

Improved ROE, ROA and EPS in 9MFY11

Capital adequacy : AHB

Tier 1 RWCA

AmBank (M) Berhad 10.1% 15.0%

AmInvestment Bank Berhad 25.1% 25.1%

AmIslamic Bank Berhad 9.1% 14.0%

Capital adequacy : by legal entity, 9MFY2011 (after proposed dividends)

Proforma 1

15.2%

9.5%

7.4%

Note :

1 Proforma including unappropriated profits of AmIslamic and AmInvestment Group

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 17(Conventional + Islamic)

Contents

Executive Summary

9MFY2011 Group Financial Performance

Divisional Performance

Strategy & Outlook

Supplementary Information

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 18(Conventional + Islamic)

*Conventional + Islamic

Medium Term Aspirations FY2011-2015

Develop a liability-led business, grow assets in targeted segments and expand wealth management

Grow diversified & profitable assets, increase liabilities, fee base business & international trade finance leveraging on ANZ

Deliver innovative and quality solutions, increase ‘share of wallet’, target high-impact and high-value clients and leverage ANZ for x-border businesses

Deliver comprehensive solutions, lead in capital markets, funds management, stock broking and enhance domestic & overseas distribution via ANZ

Leverage Friends Provident to deliver premium product & customer propositions & improve efficiencies

Leverage Insurance Australia Group to become a scale specialist in motor and niche specialist in commercial and non-motor lines

Deliver substantive, integrated and client-led business with full suite of FX, Rates, Commodities and FI offerings with ANZ collaborations

Divisional Aspirations

To become Malaysia’s Preferred Banking Group with International Connectivity• customer satisfaction

• sound financial performances

• well diversified and sustainable growth

As measured by

Retail *

Business *

Corporate & Institutional *

Investment *

Life Assurance

General Insurance

Markets *

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 19(Conventional + Islamic)

On track to meet FY2011 expectations

Retail Banking *

Business Banking *

Corp & Institutional

Banking *

Investment Banking *

Markets *

Life Assurance

General Insurance

Good CASA & deposit growth, profitable asset growth & lower credit costs Invest for medium term outcomes Good profit growth benefiting from lower impairments for FY2011

Income growth from larger asset base & growth in non-interest incomes Proactively managing existing accounts for cross-sell & transactional deposits Good profit growth underpinned by well diversified incomes for FY2011

Income growth from larger asset base & fees Increased focus on cross-selling & growing deposits Good profit growth underpinned by better quality loans for FY2011

Leverage upturn in capital markets Increasing regional biz via closer collaboration with ANZ Sound profit result for FY2011

New products, improve new biz IRR & leverage strategic partnership with Friends Provident Strong growth in profits transferred to Shareholders for FY2011

Higher contribution from new products, increase share of wallet from retail & biz customers Reasonable profit growth for FY2011

Momentum from FX & Derivatives set to increase Strong profit growth for FY2011

*Conventional + Islamic

Note : Update since H1FY2011 Investors Presentation highlighted in italics and blue

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 20(Conventional + Islamic)

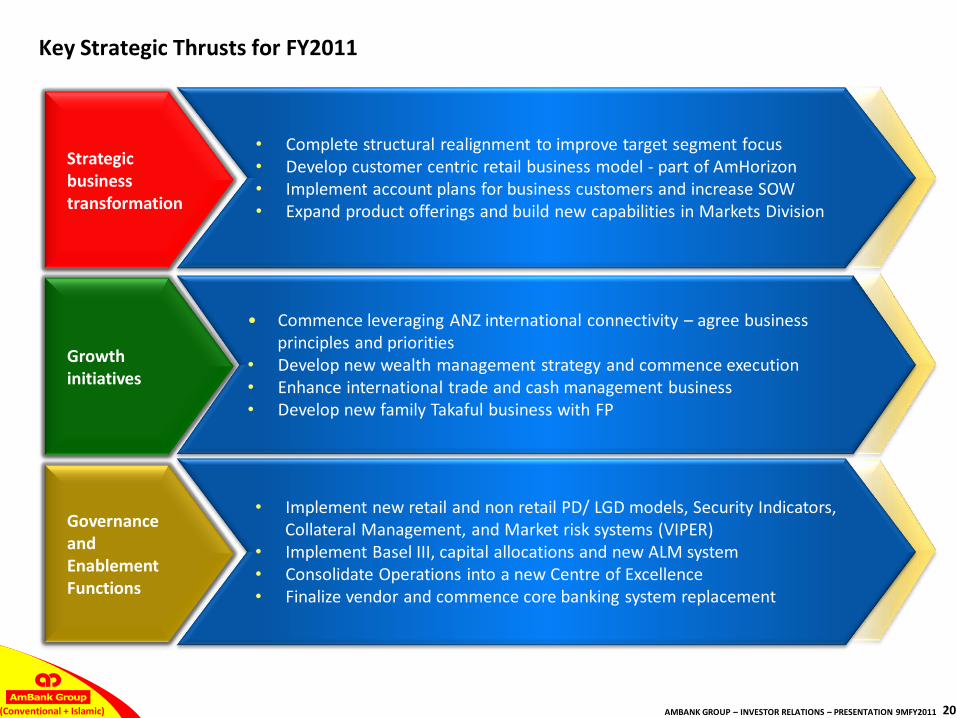

Key Strategic Thrusts for FY2011

Strategic business transformation

Growth initiatives

Governance and Enablement Functions

• Complete structural realignment to improve target segment focus• Develop customer centric retail business model - part of AmHorizon• Implement account plans for business customers and increase SOW• Expand product offerings and build new capabilities in Markets Division

• Commence leveraging ANZ international connectivity – agree business principles and priorities

• Develop new wealth management strategy and commence execution• Enhance international trade and cash management business• Develop new family Takaful business with FP

• Implement new retail and non retail PD/ LGD models, Security Indicators, Collateral Management, and Market risk systems (VIPER)

• Implement Basel III, capital allocations and new ALM system• Consolidate Operations into a new Centre of Excellence• Finalize vendor and commence core banking system replacement

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 21(Conventional + Islamic)

PATMI ~

ROE

CTI

Net NPL ratio /Gross impaired loans

Dividend:Gross

Payout

Medium Term Aspirations and estimates

# Previous guidance : 25-30%

* Adjusted for possible Basel III impacts on ACE^ Previously 12-15% sustainable profit growth

*

~ PATMI = profit after tax and minority interests

FY07 FY 08 FY 09 FY 10 9MFY 11 FY 2011 EstimateMedium Term

Aspirations (MTA)2012 - 2016

- RM282.5 mil

RM668.5

mil

RM860.8mil

RM1,008.6

mil

RM1,026.5

mil

circa 30%

#

14 – 18%

CAGR ^

- 5.8% 11.5% 11.7% 11.5% 13.9% circa 13% *FY13 onwards :

15 – 18% *

37.1% 39.6% 43.3% 42.0% 39.5% circa 40% 40 - 42%

6.2% 3.7% 2.6% 1.5% / 3.8% 3.4% circa 3.5% circa 2.5%

5.0 sen / share

(loss year)

6.0 sen / share

18.3%

8.0 sen / share

19.0%

10.5 sen / share

28.1%

H1FY11 interim

6.0 sen / share

25.8%

35 – 40% *

payout

≥ 40% *

payout

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 22(Conventional + Islamic)

Summary

1. Good 9MFY2011 performance, portfoliodiversification on track for FY2011

2. Growth momentum expected to moderate inFY2012 due to lower GDP growth (CY2011)

3. Strong foundations and clear medium termstrategies

4. International connectivity with ANZ and accessto world class “IP” and resources

5. Disciplined execution and governance requiredfor sustainable performance

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 23(Conventional + Islamic)

Executive Summary

9MFY2011 Group Financial Performance

Strategy & Outlook

Divisional Performance

Supplementary Information

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 24(Conventional + Islamic)

PATPBPExpensesIncome

Retail Banking Division : Improved asset quality main contributor to higher profits

Income performance – focusing on profitable segments and pricing for risk

Irrational pricing in selected segments

Expenses - growing footprints & channels, and upgrade in risk tools, people cost and IT systems

Lower impairments driving higher profits

9MFY2010 loans and deposits adjusted for segment realignment

Better than system CASA growth (7.1%)

Develop a liability-led business, grow assets in targeted segments and expand wealth management

Composition to Group 47.1% 46.0% 47.9% 42.3%

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Income 1,357.0 1,391.4 +2.5%

Expenses 520.6 536.2 +3.0%

PBP 836.4 855.2 +2.2%

Impairments / Allowances 303.3 255.0 -15.9%

PBT 533.0 600.2 +12.6%

PAT 399.3 450.1 +12.7%

Gross Loans / Financing 44,364.5 45,062.2 +1.6%

Net Loans / Financing 42,784.5 43,837.5 +2.5%

Gross Impaired Loans - 1,384.1 -

Customer Deposits 29,327.2 33,207.5 +13.2%

CASA Deposits 6,526.3 7,332.8 +12.4%

ROA 1.23% 1.35% +0.12%

CTI 38.4% 38.5% +0.1%

Allowance Coverage - 88.5% -

9MFY11 vs 9MFY10

G

3.07%

G

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 25(Conventional + Islamic)

PATPBPExpensesIncome

Business Banking Division : Good income growth partly offset by higher impairments

Income growth - lending to stable sectors, trade and transactional

Cost increase – mainly from expansion in relationship team

9MFY2010 loans and deposits adjusted for segment realignment

Strong CASA growth, leveraging on better relationship building and new products

Grow diversified & profitable assets, increase liabilities, fee base business & international trade finance leveraging on ANZ

Composition to Group12.4% 6.6% 16.2% 14.0%

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

9MFY11 RM'mil 9MFY10 9MFY11 9MFY10

Income 273.5 366.1 +33.9%

Expenses 65.5 76.4 +16.6%

PBP 208.0 289.6 +39.2%

Impairments / Allowances 40.1 91.6 +128.4%

PBT 167.9 198.1 +18.0%

PAT 125.9 148.8 +18.2%

Gross Loans / Financing 10,819.7 13,762.1 +27.2%

Net Loans / Financing 10,586.7 13,570.7 +28.2%

Gross Impaired Loans - 222.6 -

Customer Deposits 7,488.9 6,759.5 -9.7%

CASA Deposits 1,230.8 1,792.8 +45.7%

ROA 1.71% 1.60% -0.11%

CTI 24.0% 20.9% -3.1%

Allowance Coverage - 86.0% -

Term Loan & Revolving Credit 6,621.5 8,419.8 +27.2%

Trade Finance 3,115.4 3,245.8 +4.2%

1.62%

G

G

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 26(Conventional + Islamic)

PATPBPExpensesIncome

Corporate & Institutional Banking Division : Good income growth and lower impairments

Diversified loans portfolio – good support for income growth

Higher contribution from international business

Impairments benefitted from bad debts recovered and lower collective impairment

9MFY2010 loans adjusted for segment realignment

Note : 1 Singapore Stock Exchange2 Jakarta Stock Exchange3 AmFraser International Pte Ltd4 PT AmCapital Indonesia

* Services include : large corporate lending, large corporate deposits, financial institutions group, offshore banking, international business, private equity, REITs and loan syndication

Deliver innovative and quality solutions, increase ‘share of wallet’, target high-impact and high-value clients and leverage ANZ for x-border businesses

Composition to Group9.4% 6.0% 11.6% 14.4%

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Income 249.2 278.4 +11.7%

Expenses 61.8 70.4 +13.9%

PBP 187.3 208.0 +11.1%

Impairments / Allowances 23.9 8.4 -64.9%

PBT 163.4 199.6 +22.2%

PAT 124.8 153.5 +23.0%

CTI 24.8% 25.3% +0.5%

Net Loans / Financing 9,706.3 11,519.3 +18.7%

Ave Assets Management 992.2 1,010.7 +1.9%

Ave Volume / Contract Traded (RM'mil/month)

S'pore SE 162,394.7 162,516.5 +0.1%

Jakarta SE 64,089.2 73,016.6 +13.9%

AmFIPL 1,994.6 1,768.0 -11.4%

PTAMCI 564.5 585.2 +3.7%

Market Share as at:

AmFIPL 1.3% 1.1% -0.2%

PTAMCI 0.9% 0.8% -0.1%

9MFY11 vs 9MFY10

G

G

G

G

G

1

2

3

4

G

3

4

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 27(Conventional + Islamic)

PATPBPExpensesIncome

Investment Banking Division : Subdued debt market but other businesses have done well

Higher income in 9MFY10 partly due to a one-time gain on disposal of a bond holding

Good contributions from asset management and corporate finance

Note :1 Including AmInvestment Management, AmInvestment

Services, AmIslamic Funds Management & private banking

Deliver comprehensive solutions, lead in capital markets, funds management, stock broking and enhance domestic & overseas distribution via ANZ

Composition to Group8.7% 11.5% 6.9% 8.5%

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Income 259.7 256.7 -1.2%

Expenses 116.0 134.2 +15.7%

PBP 143.7 122.6 -14.7%

Impairments / Allowances 4.1 1.1 -73.2%

PBT 139.6 121.5 -13.0%

PAT 104.2 90.5 -13.1%

CTI 44.7% 52.3% +7.5%

Ave Assets Management 19,981.9 24,823.8 +24.2%

Ave Volume / Contract Traded (RM'mil/month)

Bursa M'sia 55,572.6 67,280.2 +21.1%

Future KL index 335.8 347.1 +3.3%

IB Broking 4,254.6 5,290.4 +24.3%

AmFuture 66.2 79.6 +20.2%

Market Share as at:

IB Broking 7.7% 7.8% +0.1%

AmFuture 20.1% 23.1% +3.0%

9MFY11 vs 9MFY10

G

G

G

G

1

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 28(Conventional + Islamic)

PATPBPExpensesIncome

Markets : Income diversification and good momentum

Higher income from FX & derivatives and fixed income

Expenses reflect continuous investment in FX, rates, derivatives & commodities establishment

Lower AFS impairment

Deliver substantive, integrated and client-led business with full-suite of FX, Rates, Commodities and FI offerings with ANZ collaborations

Composition to Group8.6% 4.2% 11.5% 14.2%

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Income 190.3 254.6 +33.8%

Expenses 34.1 48.6 +42.5%

PBP 156.2 206.0 +31.9%

Impairments / Allowances 34.2 4.7 -86.3%

PBT 122.0 201.2 +64.9%

PAT 88.6 151.2 +70.7%

CTI 17.9% 19.1% +1.2%

PAT : Fx and Derivatives 8.0 35.0 +>100%

Total Group:

Financial assets HFT 2,048.8 7,100.2 +>100%

Financial investments

AFS 7,792.6 7,123.2 -8.6%

Financial investments

HTM 574.8 183.7 -68.0%

9MFY11 vs 9MFY10

GGG

G

G

G

GGG

G

G

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 29(Conventional + Islamic)

PATIncome

Life Assurance : Stronger contribution to Shareholders, sound capital adequacy

Higher income - larger fund assets, from enhanced agency network, product bundling and cross selling

Increase in CAR due to reduction in total capital requirement from MGS curve movement (reducing interest rate risk and liability capital charges)

Marginal decline in gross written premium from lower margin single premium businesses

Change in definition of ROE computation where 9MFY11 is based on higher total value of new business of each product

Leverage Friends Provident to deliver premium product & customer propositions & improve efficiencies

Composition to Group2.1% 4.8%

* Life assurance shareholders’ fund accounts

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Net Income 27.6 61.9 +>100.0%

PAT 19.1 51.6 +>100.0%

Life Assurance

fund assets 2,300.3 2,582.9 +12.3%

CAR ratio 181.0% 237.7% +56.7%

Gross written

premium 441.5 427.6 -3.1%

ROE 28.0% 63.4% +>100.0%

9MFY11 vs

9MFY10

GG

G

G

G

G

G

G

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 30(Conventional + Islamic)

PATPBPExpensesIncome

General Insurance : Higher income and improved efficiencies

Higher income - larger gross written premium, from enhanced up- and cross-selling, and established distribution network

Higher tax impact in 9MFY2011 due to late audit adjustment in respect of FY2010, for transfer of deferred tax assets to life assurance

Leverage Insurance Australia Group to become a scale specialist in motor and niche specialist in commercial and non-motor lines

Composition to Group4.3% 5.4% 3.6% 4.3%

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Income 101.3 128.1 +26.5%

Expenses 57.1 63.1 +10.5%

PBP 44.2 65.0 +47.1%

Impairments / Allowances (0.2) (1.4) ->100.0%

PBT 44.5 66.4 +51.2%

PAT 37.6 46.2 +22.9%

CTI 56.4% 49.3% -7.1%

General Insurance fund

assets982.2 1,135.3 +15.6%

Claim ratio 71.2% 69.2% -2.0%

Management expense

/ earned premium 15.0% 14.3% -0.7%

ROE 21.4% 19.4% -2.0%

9MFY11 vs 9MFY10

GG

G

G

G

GGGG

GGG

GGG

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 31(Conventional + Islamic)

PATPBPExpensesIncome

Group Operating Segments

Higher income from :

Shareholders fund, Corporate & Shared Services

- consolidation adjustments

Lower income from Loan Rehab units

- recovery rate as scheduled

Composition to Group 7.3% 20.2% -1.2% -2.5%

Defining the journey to a Customer Service Delivery Channel

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

RM'mil 9MFY10 9MFY11

Income 211.4 214.2 +1.3%

Expenses 232.7 235.8 +1.3%

PBP (21.2) (21.6) -1.9%

Impairments / Allowances 106.8 (13.5) ->100.0%

PBT (128.1) (8.1) +93.7%

PAT (108.1) (27.1) +74.9%

PATMI (132.6) (65.4) +50.7%

9MFY11 vs 9MFY10

G

G

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 32(Conventional + Islamic)

PATPBPExpensesIncome

Islamic Banking : Higher collective impairments

Underlying branding position remains strong and expected to provide growth support

* Results incorporated under respective business divisions

To become the Islamic Bank of choice and ensure a high degree of value for our customers, employees & stakeholders

Composition to Group

9MFY10 results

Positive growth in 9MFY11

Contraction in 9MFY11

19.8% 18.3% 20.8% 17.7%

RM'mil 9MFY10 9MFY11

Income 581.5 585.0 +0.6%

Expenses 191.3 212.9 +11.3%

PBP 390.2 372.2 -4.6%

Impairments / Allowances 58.4 124.9 +>100%

PBT 331.8 247.3 -25.5%

PAT 243.2 188.4 -22.5%

Net Financing 11,991.7 12,683.1 +5.8%

Gross Impaired Financing - 279.6 -

Customer Deposits 12,715.6 12,924.1 +1.6%

CASA Deposits 2,078.4 2,327.2 +12.0%

ROA 2.15% 1.45% -0.70%

CTI 32.9% 36.4% 3.5%

Allowance Coverage - 151.5% -

9MFY11 vs 9MFY10

G

1.90%

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 33(Conventional + Islamic)

Contents

Executive Summary

9MFY2011 Group Financial Performance

Strategy & Outlook

Divisional Performance

Supplementary Information

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 34(Conventional + Islamic)

Oil & Gas• Exxon Mobil• Shell Malaysia• Dialog Group, deepwater petroleum terminal• Malaysia Nuclear Power Corporation

> RM 10.0 bil investment5.1 bil5.0 bil

-

•Enhance Tapis oil recovery, Telok gas development•1,650 jobs during facility building & construction•5,000 jobs; 5mil cubic metres storage terminal•Study feasibility of nuclear energy, 11-12 years

Electrical & Electronics• AUO Sunpower 2.2 bil •4,069 jobs by 2012, high-efficiency solar cells

Wholesale & Retail• Mines Wellness City, Country Heights Group 3.0 bil •11,000 jobs in 10 years, integrated health resort

Greater KL• Guocoland, Damansara City 2• Mass Rapid Transit• Talent Corporation

1.9 bil36.6 bil (3 lines, excl land)

-

•2 office & 1 retail block, 1 hotel, 1 serviced apartment•130,000 jobs, support public transport share to 50%•New government agency to fill 3.3 mil NKEA positions

Tourism• Teluk Datai Development Plan• YTL, Pulau Gaya development

1.0 bil75.0 mil

•Develop 300 acres land in Langkawi•World-class hillside-seafront villa, rainforest theme

Agriculture• Pasir Raja high-value herbal plantation - •285 jobs, cultivate 7 types of high demand herbs

Education• Skills Malaysia 2011 - •Showcase opportunities post-SPM

Communications Content & Infrastructure• Select TV, Hospitality IPTV 30.0 mil •Advanced entertainment distribution to hotels

Healthcare• Universiti Malaya Health Metropolis• Hovid Objective Pharmaceutical Excellent

1.25 bil (excl land)-

•10,400 jobs, premier medical hub•Collaboration with Sanofi-Aventis to develop drugs

Business Services• MyTelehaus Sdn Bhd• CSF Group• Teliti Datacentres

671.6 mil total250.0 mil

21.6 mil400.0 mil

•Malaysia as world-class data centre hub

Economic Transformation Programme : in overdrive with 19 projects worth RM67 bil

Day 100 announcement : 11 January 2011

19 projectsacross

10 NKEA’s

1

2

3

4

5

6

7

8

9

10

Note :NKEA = National Key Economic ActivitiesSource : media, AmResearch, www.pemandu.gov.my/etp

Banking sector positives :

Loans growth - working capital & bridging financing Private debt market boost, higher PDS issuances Benefit to interest & non-interest income growth

35,000 new job creation in total

RM67 bil investmentsin total

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 35(Conventional + Islamic)

102.3 165.9 268.2

473.7

741.8

104.9 184.6

289.6

504.1

793.6

Savings Current Account CASA Fixed Deposits Core Deposits

Industry Deposits by Type Dec '09 Dec '10

11.3% 8.0%2.6% 6.4% 7.0%

121.9 210.1 26.4 37.2

395.6 387.9

783.5

132.3 237.8

30.1 42.3

442.5 441.1

883.6

Purchase of Transport Vehicles

Purchase of Residential Properties

Credit Cards + LOC Personal Use Retail Loans Business & Corporate Loans

Total Loans

Industry Loans Growth by Purpose Dec '09 Dec '10

13.2% 14.2% 13.5% 11.9%8.5% 13.7% 12.8%

Industry Growth : Loans by Sector, Deposits by Type

RM’bil

Source : BNM

AmBank Group’sgrowth : +1.2% +5.4% -3.7% -23.8% +0.3% +22.4% +8.4%

Industry Loans Growth by Purpose

Industry Deposits Growth by Type

AmBank Group’sgrowth : +8.4% +22.6% +16.0% +5.1% +6.5%

Industry growth

Industry growth

15.0%

26.9%

3.4%4.8%

49.9%

Industry Loans Composition

Purchase of Transport Vehicles Purchase of Residential Properties Credit Cards + LOC Personal Use Business & Corporate Loans

13.2%

23.3%

63.5%

Industry Deposits Composition

Savings

Current Account

Fixed Deposits

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 36(Conventional + Islamic)

25.3

11.4

1.8 3.1 3.6 2.5 1.4 0.0 1.6

10.7 5.1

25.5

12.1

4.51.8

14.4

6.2

Purchase of Transport Vehicles

Purchase of Residential Properties

Credit Cards Personal Use Purchase of Non-Residential Properties

Purchase of Securities

Fixed Assets Consumer Durables

Construction Working Capital Other purpose

AmBank Group Loans Growth by Economic Purpose Dec-09 Dec-10

1.7 2.4 2.3 1.2 0.0

1.2% 5.4% -3.7% 23.8% 23.8% -7.1% -14.8% -15.0% 13.4% 34.7% 22.5%

121.9

210.1

26.4 37.2 74.1

34.6 0.1 19.0

209.5

41.8

132.3

237.8

30.1 42.3

90.7

37.9 21.6

226.7

55.1

Purchase of Transport Vehicles

Purchase of Residential Properties

Credit Cards Personal Use Purchase of Non-Residential Properties

Purchase of Securities

Fixed Assets Consumer Durables

Construction Working Capital Other purpose

Industry Loans Growth by Economic Purpose Dec-09 Dec-10

8.9 8.8

8.5% 13.2% 14.2% 13.5% 22.5% 9.4% 1.4% -6.8% 13.6% 8.2% 31.8%

0.1

Loans by Economic Purpose : AMMB vis-à-vis Industry

composition : 35.5% 16.7% 2.4% 3.3% 6.2% 3.2% 1.6% 0.0% 2.4% 20.0% 8.6%

RM’bil

Source : BNM, internal reports

composition : 15.0% 26.9% 3.4% 4.8% 10.3% 4.3% 1.0% 0.0% 2.4% 25.7% 6.2%

RM’bil

AmBank Group Loans Growth by Economic Purpose

Industry Loans Growth by Economic Purpose

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 37(Conventional + Islamic)

Competitive Positioning : Sound size and market position in key businesses (as at end 2010)

Investment Banking

Business Banking

Life Assurance

Islamic Banking

Corporate & Institutional Banking

# 2

# 4[9.7%]

# 5[6.5%]

# 9

# 5[7.3%]

Life

# 3 auto financier [20.8%]

# 8 in housing loans (incl foreign banks) [ 4.9%]

# 7 in credit cards (incl foreign banks) [ 5.7%]

# 5 in no. of branches & # 4 in no. of ATM’s

Nationwide network - 4 regional business & 12 commercial centres

Lead in cash management, trade and SME financing

# 2 in M&A league [33.3%]

# 3 in Debt League [18.9%]

# 3 in Malaysian RM Islamic bonds [12.5%]

# 3 in brokerage turnover [ 7.8%]

# 4 in funds under management [12.5%]

# 4 in Malaysia Loans mandated arranger [ 8.5%]

Award-winning equity house, private bank, asset management company & Islamic asset management house

Focus - GLC’s, MNC’s and financial institution groups (FIG’s)

Niche international businesses - Singapore, Indonesia & Brunei

Other businesses - REITs and private equity

# 9 in life assurance new biz premiums [ 4.4%]

Strategic partner - Friends Provident

BNM approval for rights to establish Takaful company

Syariah based banking products and services

# 2 in Islamic credit cards [28.5%]

Retail Banking

Note :[ ] denotes market share

General Insurance # 7 # 7 in general ins new biz premiums [ 5.1%]

# 3 in motor ins new biz premiums [ 8.6%]

Strategic partner – IAG

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 38(Conventional + Islamic)

Competitive positioning :Shareholding structure

No. 15 (Malaysia –market capitalisation) & 161 (global – 1,000 banks by market capitalisation) :

RM21.19 billion, Bursa SahamMalaysia (1)

US$6.93 billion, Bloomberg (2)

1 Apr 2010 : 100% equity in AmInvestmentBank Bhd transferred to AHB from AmInvestment Group Bhd

The due diligence to acquire the general insurance business of a local insurance company has been mutually discontinued

As at 31 December 2010

Foreign shareholding excluding ANZ :

Mar 09 : 28.4% Mar 10 : 27.1% Dec 10 : 32.1%

100% 70%*100%

100%

AmInvestmentBank Berhad

16.8% 11.8% 47.6%

Employees Provident Fund Board

AMMB Holdings Bhd

Amcorp Group Bhd

Other shareholders

AmBank (M) Berhad

AmIslamicBank Bhd

^ Insurance Australia Group Ltd –49%

ANZ Funds Pty Ltd #

23.8%

AMFB Holdings Bhd

100%

51%^

AMAB Holdings Sdn Bhd

100%

AmG Insurance Berhad

AmLife Insurance Berhad

* Friends Provident Fund PLC –30%

Source :1 Starbiz dated 3 January 20112 Bloomberg Global 1,000 banks by Market Capitalization as at 3 January 2011

# ANZ Funds Pty Ltd : a wholly owned subsidiary of Australia and New Zealand Banking Group Limited (“ANZ”)

AmInvestmentGroup Berhad

100%

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 39(Conventional + Islamic)

Competitive positioning :Strategic partnership with global partner, ANZ

Super regional strategic intent

Launched Dec 2007

Asia Pacific growth focus : Retail, Wealth, Commercial,

Institutional

Director

Dr. Robert John

Edgar

BoardDirector

Alex Thursby

Senior

Management

Deputy Group MD & Group CFO

Ashok Ramamurthy

Chief Risk Officer

Andrew Kerr

Head, Retail Sales & Distribution

Brad GravellManagement

Head, Group Risk Models

Glenn Saunders

Head, Market Risk

Jonathan Manifold

Head, Systems Accounting

Ignatius Lim

Chief Operations Officer

Ross Neil Foden

Director

Mark Whelan

Head, FX & Derivatives

Peter Trumper

ANZ has provided key resources and support

ANZ’s Regional Aspiration :

Create a leading Super Regional bank

Global quality, regional focus

( ) – number of branches & representative offices in each country

AmBank Group 1 of 5 key partnerships that is expanding ANZ’s organic agenda

AHB’s market cap increased 56.4% in 2008/2010

Partnerships model, ANZ adds value :

leadership & management

product development

technical expertise

2-way customer flows

ANZ is committed to AmBank Group’s long-term success and aspirations

1 – 2 years Restore Drive Asia profit

2 – 5 years Outperform In-fill M&A in Asia (core geography)

5+ years TRANSFORM

Head, Transaction Banking (Trade &

Cash)

Tan Chin AunNote : as at June 2010

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 40(Conventional + Islamic)

Strategic Business Transformation : Good Progress

12 months (FY 2008)

24 months

(FY 2009)

36 months (FY 2010)

• Set Group’s vision & aspirations

• Agreed Group’s transformation strategy, agenda and targets

• Realigned auto financing business towards profitable growth

• Improved asset quality

• Realigned growth towards profitable and viable segments only

• Realigned Markets Fixed Income business model

• Reset Mortgage business strategy and action plans

• Consolidated Group balance sheet activities within commercial bank

• Split composite insurance license to General and Life

• Created deposits as a profit centre

• Realigned customer ownerships and focus across all business Divisions

• Proactively strengthened capital and liquidity management

• Repositioned balance sheet for rising interest rates

Strategic Business

Transformation

High Priority

Growth Initiatives

Governance &

Enablement

Functions

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 41(Conventional + Islamic)

High Priority Growth Initiatives : Implemented To-Date

• Accelerated growth from GLC, GLIC and MNC

• Build scale

• Developed a new Rates business in collaboration with ANZ

• Expanding distribution footprint with particular focus on 7-11 ATM’s

• Created a separate Corporate and Institutional Banking Division (CIB)

• Developed a new FX business in collaboration with ANZ

• Enhanced cash management offering via Gross Payroll system

• Split General and Life, brought in a new life business partner, Friends Provident Fund plc

• Implemented new profit centre based retail branch distribution model

• Accelerated CASA growth via aligning profitability and incentives

12 months (FY 2008)

24 months (FY 2009)

36 months (FY 2010)

Strategic Business

Transformation

High Priority Growth

Initiatives

Governance &

Enablement

Functions

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 42(Conventional + Islamic)

Governance and Enablement Functions Streamlined :Supports Better Decision Making

• Privatised AmInvestment Bank

• Consolidated some Group support into Centres of Excellence

• Consolidated / simplified governance committee structures across entities

• Delivered line of business budgets and performance reporting

• Created a Group PMO to prioritise and manage key strategic initiatives

• Established Advance Risk Recognition Program (ARRP)

• Strengthened risk disciplines via Group Risk Appetite Frameworks

• Separated ALCO, capital and balance sheet management from Markets

• Delivered Peer Bank relative performance benchmarks

• Implemented short and long term incentives aligned to performance via MTA

• Delivered 8 new generation retail scorecards and new market risk models

• Commenced PD, LGD & EAD models for retail and non-retail, non-retail security indicators

• Implemented a new FTP system aligned to balance sheet strategies

• Developed leadership bench-strength and succession planning

• Implemented Operational Risk Incident Reporting system and Basel II capital calculator

12 months (FY 2008)

24 months (FY 2009)

36 months (FY 2010)

Strategic Business

Transformation

High Priority

Growth Initiatives

Governance and

Enablement Functions

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 43(Conventional + Islamic)

Strategic partnership with global partner, ANZ

Competitive positioning : continues to strengthen

Sound size and market position in key business

segments

1

2

3

4

5

6

Well diversified universal bank & # 4 largest banking group (market capitalization) # 4 retail bank, # 5 business and CIB lending Top 2 investment bank, #5 Islamic banking, #7 general insurance Strong customer-focus, lead in

customer satisfaction

Segmentation focus and positioning strategies & differentiating through products & services

Large retail and corporate client base provides high cross-selling potential

Award-winning products and services

Improving “Top of Mind” brand recall

Expanding distribution footprint (branch network –190), #4 largest ATM network (804), 402 ATMs @ 7/11 and 143 EBC’s

eChannels : internet banking, mobile banking and 24 hours call centre

Pioneer in weekend banking concept

~7,500 sales agents, direct sales teams, marketing & personal bankers, financial services and insurance agents

Strategic partnership with ANZ (since May 07), 1 of 10 AA rated global banks Leveraging ANZ : strengthen strategy formulation, financial management, risk

management, distribution channel management, deposits strategy and product development

Strong key shareholders, common aspirations

AIGB privatisation & internal business restructuring completed

Insurance biz partnership (2009)

Improvement in stock valuation & upgrades in credit ratings

Experienced management team with key ANZappointments

Industry experts, international and domestic best practices

Performance based culture, all levels

Strengtheningcompetitive positioning

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 44(Conventional + Islamic)

Wide market reach and multiple distribution channels

Source : Company websites of peer banks / MEPS informationNote : Peer groups as at December 2010; AmBank as at latest practicable date

Total #

ATM’s at 7 Eleven 402

Electronic Banking Centers (EBC) 143

Assurance offices 74

AmInvestment offices 15

Number of Branches#5

Number of ATMs2,848

2,066

1,058 804486 344 277 171

Maybank CIMB RHB AmBank PBB HLB EON Alliance

#4

381 369 249 242 190 185 140 104 91

Maybank CIMB Public RHB AmBank HLB EON Alliance Affin

Strategic initiatives , expanding distribution footprints

Increased customer satisfaction via integrated & seamless channels model Expand branch network & SSM footprint Further build & improve sales & service capabilities

Aspirations

Branch Banking

189 branches, 5 in progress

Expand electronic banking centre (EBC) at 90% of branches, and maintain position as the no. 1 provider of ATMs at 7-Eleven

Maximize outbound sales productivity via award winning contact centre

Expand revenue streams via add-ons (interbank loan, bill payment, full-suite prepaid top-up)

Enhance experience via innovative mobile & internet banking

E- Channels & Contact Centre (incl. Internet & Mobile Banking)

Wealth Management

Tapping affluent segment - Priority banking setup Multi-campaigns / product launches for different segments Increase sales efficiency through introduction of WM System Reorganize WM Structure to increase sales productivity & efficiencies Growing FOS via Mobile Sales Force (MSF) & additional Wealth Specialists (WS)

To complete product suite offering (E-FD, Debit Card, Foreign Currency Account, loyalty points)

Develop segment based solutions (Small Biz Solution, Life Stage segment solutions) Mobilising and optimising sales channels through branch engagement, incentive

schemes and introduction of Biz Relationship Managers Accelerate payroll acquisition though AmBank@ Work Leveraging relationship and alliances by cross-selling deposit products to other line-

of-business customer base

Deposit & Customer Solutions

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 45(Conventional + Islamic)

0

2

4

6

8

2007 2008 2009 2010

BBB-

BBB

BBB+

BB+

BBB-/A3/Stable

BBB-/A3/Stable

BBB/A3/Stable

BBB-/A3/Positive

0

2

4

6

8

2007 2008 2009 2010

0

2

4

6

8

2007 2008 2009 2010

0

2

4

6

8

2007 2008 2009 2010

0

2

4

6

8

2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0

A1

AA3

AA2

A2

A2/P1/Stable

A1/P1/Stable

AA3/P1/Stable

BBB-

BBB

BBB+

BB+

BBB-/F3/Stable

BBB-/F3/Positive BBB-/F3/

Stable

BBB-

BBB

BBB+

BB+

BBB-/A-3/Stable

BBB-/A-3/Stable

BBB-/A-3/Positive

Baa2

Baa1

A3

Baa3

Baa2/P-3/D-Stable

Baa2/P-3/D-Stable

Baa2/P-3/D-Stable

AA3/P1/Stable

BBB/F3/Stable

BBB/A-2/Stable

Baa2/P-3/DStable

0

2

4

6

8

2007 2008 2009 2010

A1

AA3

AA2

A2

AA3/P1/Stable

AA3/P1/Stable

AA3/P1/Stable

AA3/P1/Stable

0

2

4

6

8

2007 2008 2009 2010

BBB-

BBB

BBB+

BB+

BB+/B/Stable

BBB-/F3/StableBB+/B/

Positive

BBB/F3/Stable

0

2

4

6

8

2007 2008 2009 2010

BBB

BBB+

BB+

BBB-BB+/B/Stable

BB+/B/Stable

BBB-/A-3/Positive

BBB/A-2/Stable

0

2

4

6

8

2007 2008 2009 2010

AA-

AA

AA+

A+

AA-/MARC-1/Stable

AA-/MARC-1/Stable

AA-/MARC-1/Stable

AA-/MARC-1/Positive

Ratings upgraded

AmBank (M) Berhad AmInvestment Bank Berhad

AmIslamic Bank Berhad

0

2

4

6

8

2007 2008 2009 2010

A1

AA3

AA2

A2

AA3/P1/Stable

AA3/P1/StableA1/P1/

StableA2/P1/Stable

RAM

Fitch

S&P

Moody’s

RAM

MARC

S&P

Fitch

RAM

reflected system outlook

negative outlook issued in July 2009 but moved up to stable in December 2009

CI

*

Note * : Based on report dated 21 Jan 2011

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 46(Conventional + Islamic)

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

May-07 Jul-07 Sep-07 Nov-07 Jan-08 Mar-08 May-08 Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10 Jul-10 Sep-10 Nov-10

Date

MBB PBB CIMB RHBC AMMB HLFG KLCI Index

Banking sector share price movement / Target price and recommendations

RM’mil 9MFY2011

Share Capital 3,014.2

Reserves 6,948.6

Shareholders’ Equity 9,962.8

Less: Intangible Assets (1,829.2)

NTA 8,133.6

NTA Per Ordinary Share (RM) 2.70

Net Asset Per Ordinary Share (RM)

3.31

Market Price (RM) 7.03

Price to Book, PBV [NTA / Net Asset]

2.12 / 2.60

EPS (sen) – basic, annualised 45.3

Price to earnings, PE 15.52

Dividend (gross sen / share)H1FY11 Interim

6 sen / share

p/q index change at close of 30 December 10 vs 18 May 07

(strategic partnership with ANZ)

30 December 1018 May 07 (strategic partnership with ANZ)

Banking Sector Share Price Movement

Index Movement (May 07 = 100)

Source : Bloomberg

As at 30 December 2010

100% base index

RHBC p + 84.7% (RM8.72)

AMMB p + 79.6% (RM7.03)

CIMB p + 42.9% (RM8.50)

PBB p + 37.3% (RM13.02)

HLFG p + 30.7% (RM8.89)

KLCI Index p + 11.9% (1,518.91)

MBB q – 5.4% (RM8.50)

Index change market price close of 30 December 10 vs. 24 December 10 Buy/Outperform/Overweight/AddP/EPS : EPS annualized Oct 09- Sept 10 P/BV : BV as at 30 September 10

Notes: TP: target price CP: weekly average closing price

Sell/Underperform/Fully valued/Reduce/Underweight

Hold / Neutral / Market perform

Target Price and Recommendations

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011 47(Conventional + Islamic)

Glossary / Disclaimer of warranty and limitation of liability

Reported PerformanceReported performance refers to the financial performance as reported in the audited financial statements and disclosed to the market

One OffsOne offs comprise those impacts on financial performance that arise from changes to :

• accounting and provisioning policies (eg 5 and 7 year rules)• differences between economic and accounting hedges• prior period catch ups (eg backdated salary costs)• strategic investments and divestments (eg ANZ partnership), and • tax and regulatory regimes (eg deferred tax asset write off due to reduction in corporate tax rates)

Underlying PerformanceUnderlying performance refers to the financial performance adjusted for one off impacts as above

Business DivisionsBusiness divisions

• comprise AmBank Group’s core operating businesses that generate profits from direct customer transactions and interactions• have relatively more stable income streams, incur the bulk of the costs and typically have a lower risk profile• in most instances have market shares and growth metrics that can be measured and benchmarked externally

Operating SegmentsOperating segments

• have more volatile and lumpy income streams, with the former a direct function of risk appetite • include

• income and expenses associated with shareholder funds, loan rehabilitation and legacy businesses, plus• costs associated with corporate, shared services and governance functions currently not charged back to the business units

The information provided is believed to be correct at the time of presentation. AMMB Holdings Berhad or AMMB Holdings or “AHB” or its affiliates do not make any representation or warranty, express or implied, as to the adequacy, accuracy, completeness or fairness of any such information and opinion contained and shall not be liable for any consequences of any reliance thereon. Neither AMMB Holdings nor its affiliates are acting as your financial advisor or agent. The individual is responsible to make your own independent assessment of the information herein and should not treat such content as advice relating to legal, accounting, and taxation or investment matters and should consult your own advisers.

Forward looking statements are based upon the current beliefs and expectations of the AMMB Holdings and are subject to signif icant risks and uncertainties. Actual results may differ from those set forth in the forward looking statements. AMMB Holdings does not undertake to update the forward looking statements to reflect impact of circumstances or events that may arise after the date of this presentation.

The information in the presentation is not and should not be construed as an offer or recommendation to buy or sell securitie s. Neither does this presentation purport to contain all the information that a prospective investor may require. Because it is not possible for AMMB Holdings or its affiliates to have r egard to the investment objectives, financial situation and particular needs of each individual who reads the information contained thus the information presented may not be appropriate for all pe rsons.

The information contained is not allowed to be reproduced, redistributed, transmitted or passed on, directly or indirectly, to any other person or published electronically or via print, in whole or in part, for any purpose.

The term "AMMB Holdings" and “AmBank Group” denotes all Group companies within the AMMB Holdings Group and this Disclaimer of Warranty and Limitation of Liability policy applies to the financial institutions under AMMB Holdings.

Disclaimer of Warranty and Limitation of Liability

AMBANK GROUP – INVESTOR RELATIONS – PRESENTATION 9MFY2011

The material in this presentation is general background information about AmBank Group’s activities current at the date of the presentation. It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor.

These should be considered, with or without professional advice when deciding if an investment is appropriate.

For further information, visit :

www.ambankgroup.com

or contact

Ganesh Kumar Nadarajah

Head, Group Investor Relations

Tel : +603 2036 1435 Fax : +603 2031 7384 e-mail : [email protected] or+6012 2974799 [email protected]