an analysis of the imo 2020 sulphur limit · 2018-10-24 · based on limited additional...

TRANSCRIPT

An Analysis of the IMO 2020 Sulphur Limit

Christophe Barret, Senior Oil Market Analyst

London 23 October 2018

© IEA 2016

Contents

• “Oil 2018 – Analysis and Forecasts to 2023” scenario (March 2018)

• New developments in the gasoil market

• Price impact

• Today versus Oil 2018 scenario

© IEA 2016

Oil 2018 outlook*

*“Oil 2018 – Analysis and Forecasts to 2023”, March 2018. IEA’s annual five-year oil market forecast.

• Need to understand how fuel oil and diesel demand will be impacted by

IMO 2020 in order to project future consumption.

• Starting point: lack of low sulfur molecules (marine gasoil or fuel oil) in

2020 will be the main constraint.

• We estimated c. 1 mb/d of diesel (in addition to inland requirements) will

be available for marine demand in 2020 from:

Refinery capacity developments

Crude availability

Refinery flexibility (yield shifts)

© IEA 2016

Oil 2018 scenario- HSFO Switch to MGO and VLSFO in 2020

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2015 2016 2017 2018 2019 2020 2021 2022 2023

kb/d

Bunker HS FO Marine gasoil Marine VLSFO

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2015 2016 2017 2018 2019 2020 2021 2022 2023

OECD and major-non-OECD bunker fuel switch by 2020

kb/d 2015 2016 2017 2018 2019 2020 2021 2022 2023

Marine gasoil 773 729 745 756 767 1,736 1,229 905 773

Marine VLSFO 0 0 0 0 0 969 1,496 1,849 2,018

Bunker HS FO 2,883 3,049 3,126 3,180 3,231 1,292 1,292 1,292 1,292

Total 3,656 3,778 3,872 3,937 3,997 3,997 4,017 4,047 4,084

Growth 3.3% 2.5% 1.7% 1.5% 0.0% 0.5% 0.7% 0.9%

© IEA 2016

Oil 2018 to Oil 2019l)

Based on limited additional availability of low sulfur molecules (~1 mb/d gasoil in 2020)

Comparison vs. 2019 (kb/d)2020 2021 2022 2023

A Drop in HSFO demand 1,939 1,939 1,939 1,939

B Additional marine gasoil 969 462 139 7

C = D + E + F New 0.5% Marine fuel 969 1,496 1,849 2,018

D HSFO blended in new 0.5% fuel 74 179 250 284

E Gasoil blended in new 0.5% fuel 295 717 999 1,134

F Very low sulfur fuel oil blended in 0.5% fuel 600 600 600 600

B+E Total gasoil needed 1,265 1,179 1,138 1,141

A-D Total HSFO surplus 1,865 1,759 1,689 1,655

= C+ B - A Total bunker 0 19 49 86

© IEA 2016

Changes in diesel demand – Europe’s disaffection

Diesel demand drop has happened faster than anticipated

• Slowdown in European gasoil demand

• German share of diesel cars in vehicle sales

fell from 41% in 1H17 to 31 % in 1H18.

• The disaffection towards diesel engine cars

is spreading all over Europe.

• EU economies are slowing

• Trade tensions and Brexit

• Strong deterioration in business

sentiment in Germany.

5.0

5.5

6.0

6.5

7.0

JAN APR JUL OCT

mb/d OECD Europe: Gasoil/Diesel Demand

Range 13-17 20172018 5-year avg

0.8

0.9

1.0

1.1

1.2

1.3

JAN APR JUL OCT

mb/d Germany: Gasoil/Diesel Demand

Range 13-17 20172018 5-year avg

© IEA 2016

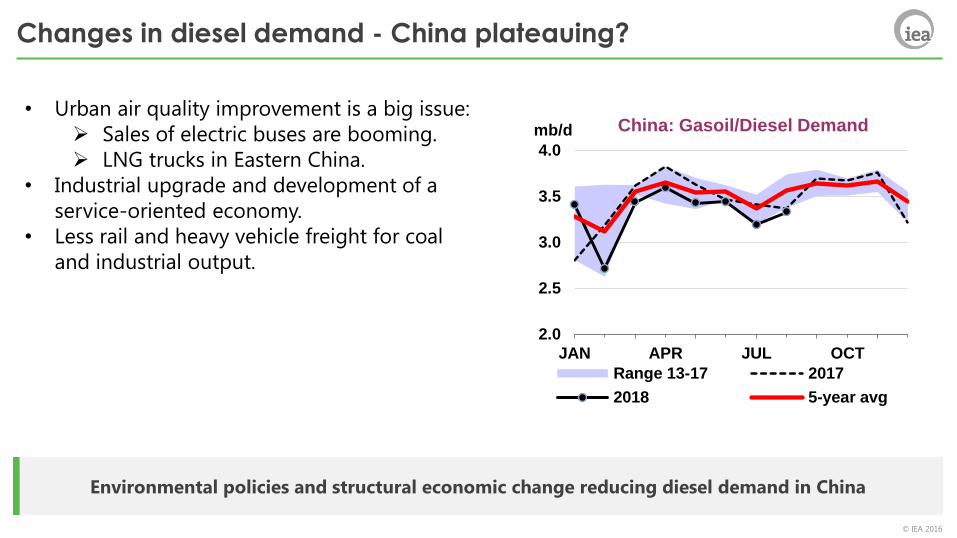

Changes in diesel demand - China plateauing?

Environmental policies and structural economic change reducing diesel demand in China

2.0

2.5

3.0

3.5

4.0

JAN APR JUL OCT

mb/d China: Gasoil/Diesel Demand

Range 13-17 2017

2018 5-year avg

• Urban air quality improvement is a big issue:

Sales of electric buses are booming.

LNG trucks in Eastern China.

• Industrial upgrade and development of a

service-oriented economy.

• Less rail and heavy vehicle freight for coal

and industrial output.

© IEA 2016

Changes in diesel demand – strength in the US

Diesel demand in the US should slow by 2020

• US diesel demand supported by rising imports of

goods and strong growth in industrial production.

• Shale oil production pipeline bottlenecks increased

reliance on trucks/rail to move crude oil.

• Diesel demand should slow in 2020:

Pipeline bottlenecks should ease in 2H19.

Trade flows likely to slow.

US fiscal expenses likely to slow in 2020.

3.4

3.6

3.8

4.0

4.2

4.4

4.6

JAN APR JUL OCT

mb/d US50: Gasoil/Diesel Demand

Range 13-17 20172018 5-year avg

© IEA 2016

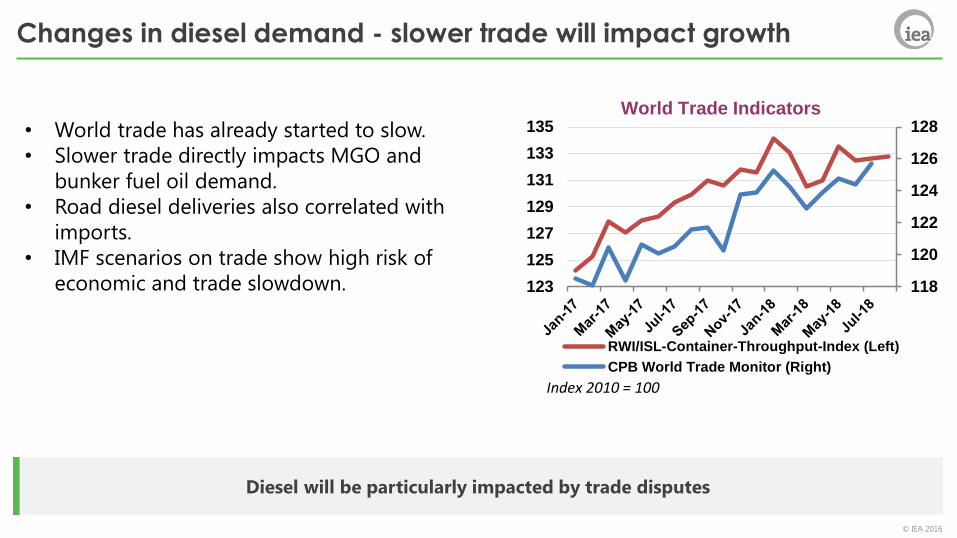

Changes in diesel demand - slower trade will impact growth

Diesel will be particularly impacted by trade disputes

118

120

122

124

126

128

123

125

127

129

131

133

135World Trade Indicators

RWI/ISL-Container-Throughput-Index (Left)

CPB World Trade Monitor (Right)

Index 2010 = 100

• World trade has already started to slow.

• Slower trade directly impacts MGO and

bunker fuel oil demand.

• Road diesel deliveries also correlated with

imports.

• IMF scenarios on trade show high risk of

economic and trade slowdown.

© IEA 2016

Price impact - history or elasticity

Diesel prices more than doubled in 2008. Lower spike anticipated in Oil 2018

0

20

40

60

80

100

120

140

160

180

Jan

2005

May 2

00

5

Se

p 2

005

Jan

2006

May 2

00

6

Se

p 2

006

Jan

2007

May 2

00

7

Se

p 2

007

Jan

2008

May 2

00

8

Se

p 2

008

Jan

2009

May 2

00

9

Se

p 2

009

Jan

2010

May 2

01

0

Se

p 2

010

Jan

2011

May 2

01

1

Se

p 2

011

Jan

2012

May 2

01

2

Se

p 2

012

Jan

2013

May 2

01

3

Se

p 2

013

Jan

2014

May 2

01

4

Se

p 2

014

Jan

2015

May 2

01

5

Se

p 2

015

Jan

2016

May 2

01

6

Se

p 2

016

Jan

2017

May 2

01

7

Se

p 2

017

Jan

2018

May 2

01

8

Se

p 2

018

Gasoil prices ands cracks in Europe

gasoil prices ($/bl) gasoil cracks ($/bl)

• With low demand response to prices,

diesel prices must significantly

increase to cut demand.

• In Oil 2018 we assumed bunkers

would need 200-250 kb/d of diesel

from inland demand to achieve the 1.2

mb/d -1.3 mb/d needed for the

switch.

• Equivalent to 20% to 30% increase in

prices.

• To switch all remaining HSFO to diesel,

prices would have to ~double to

balance 1 mb/d additional marine

gasoil use.

© IEA 2016

Possible Price Impact

Price increase needed to rebalance markets depends on scrubbers, compliance and diesel availability

-1,600

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

0.00% 50.00% 100.00% 150.00% 200.00%

Die

sel

Cu

ts (

kb/d

)

Price increases

kb/d

HSFO to switch 3200 3200 3200 3200 3200 3200 3200 3200

VLSFO 1000 1000 1000 1000 1000 1000 1000 1000

Existing fo ls 600 600 600 600 600 600 600 600

blend for VLSFO 400 400 400 400 400 400 400 400

HSFO in blend 80 80 80 80 80 80 80 80

Gasoil in Blend 320 320 320 320 320 320 320 320

Scrubbers 200 250 300 350 400 450 500 550

Compliance 90% 88% 86% 84% 82% 80% 78% 76%

MGO needed 2000 1886 1772 1658 1544 1430 1316 1202

Gasoil availability 950 980 1010 1040 1070 1100 1130 1160

Gasoil Deficit -1050 -906 -762 -618 -474 -330 -186 -42

Diesel price increase 125% 108% 91% 74% 56% 39% 22% 5%

With Gasoil demand at 28

mb/d and Ep at -0.03

© IEA 2016

Conclusion: differences today vs. Oil 2018

• Higher oil prices, weaker economic outlook – mean lower demand growth &

higher supply e.g. US.

• Slightly more diesel – VLSFO could be available from refining.

• Diesel demand fundamentals have deteriorated.

• Under a scenario similar to that of Oil 2018 (100% HSFO 30% VLSFO, 30%

MGO, 40% HSFO):

Diesel may be less stretched due to lower inland demand growth.

Realistic scenario today may be closer to 30% VLSFO, 40% MGO and 30%

HSFO.

• Given recent market developments, impact on prices will depend on:

Scrubbers installed – some recent acceleration in orders.

Logistical constraints

Compliance