an introduction to macroeconometrics: vec and var models prepared by vera tabakova, east carolina...

TRANSCRIPT

Chapter 13

An Introduction to Macroeconometrics: VEC and VAR Models

Prepared by Vera Tabakova, East Carolina University

Chapter 13: An Introduction to Macroeconometrics: VEC and VAR Models

13.1 VEC and VAR Models

13.2 Estimating a Vector Error Correction model

13.3 Estimating a VAR Model

13.4 Impulse Responses and Variance Decompositions

Slide 13-2Principles of Econometrics, 3rd Edition

Chapter 13: An Introduction to Macroeconometrics: VEC and VAR Models

Slide 13-3Principles of Econometrics, 3rd Edition

(13.1a)

(13.1b)

210 11 , ~ (0, )y y

t t t t yy x e e N

220 21 , ~ (0, )x x

t t t t xx y e e N

13.1 VEC and VAR Models

Slide 13-4Principles of Econometrics, 3rd Edition

(13.2)

(13.3)

10 11 1 12 1

20 21 1 22 1

yt t t t

xt t t t

y y x v

x y x v

11 1 12 1

21 1 22 1

yt t t t

xt t t t

y y x v

x y x v

13.1 VEC and VAR Models

Slide 13-5Principles of Econometrics, 3rd Edition

(13.4)

(13.5a)

0 1t t ty x e

10 11 1 0 1 1

20 21 1 0 1 1

( )

( )

yt t t t

xt t t t

y y x v

x y x v

13.1 VEC and VAR Models

Slide 13-6Principles of Econometrics, 3rd Edition

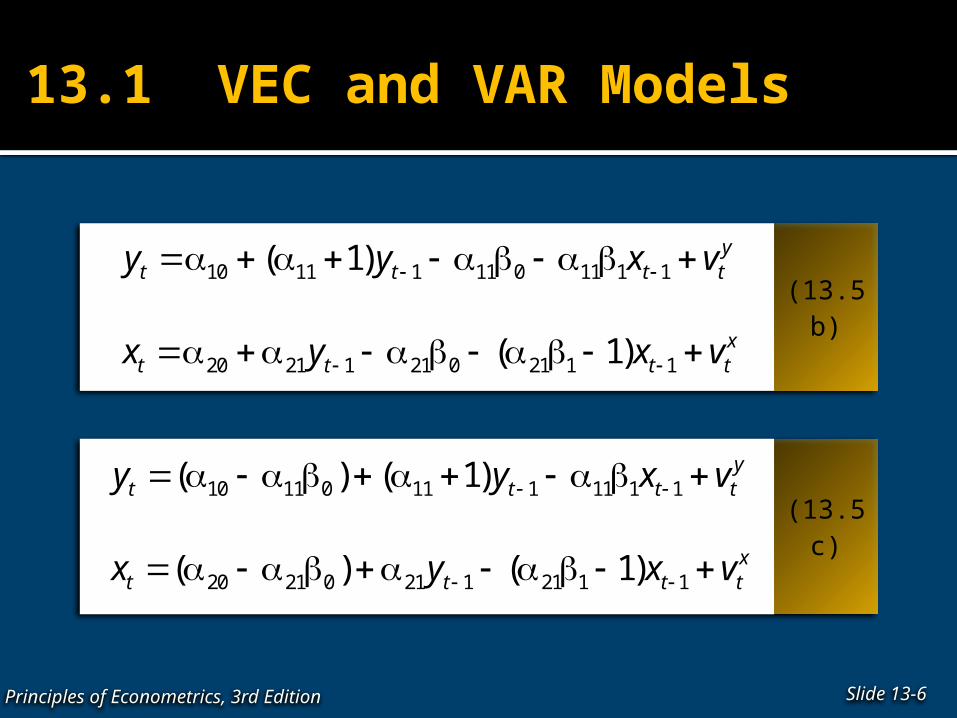

(13.5b)

(13.5c)

10 11 1 11 0 11 1 1

20 21 1 21 0 21 1 1

( 1)

( 1)

yt t t t

xt t t t

y y x v

x y x v

10 11 0 11 1 11 1 1

20 21 0 21 1 21 1 1

( ) ( 1)

( ) ( 1)

yt t t t

xt t t t

y y x v

x y x v

13.2 Estimating a Vector Error Correction Model

Slide 13-7Principles of Econometrics, 3rd Edition

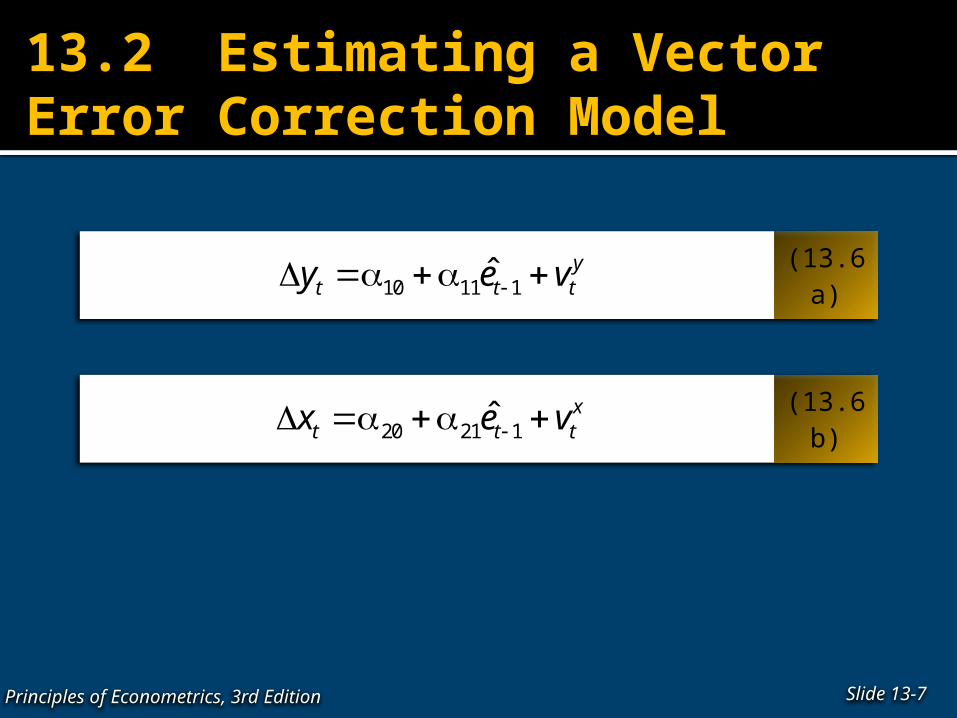

(13.6a)

(13.6b)

10 11 1ˆ yt t ty e v

20 21 1ˆ xt t tx e v

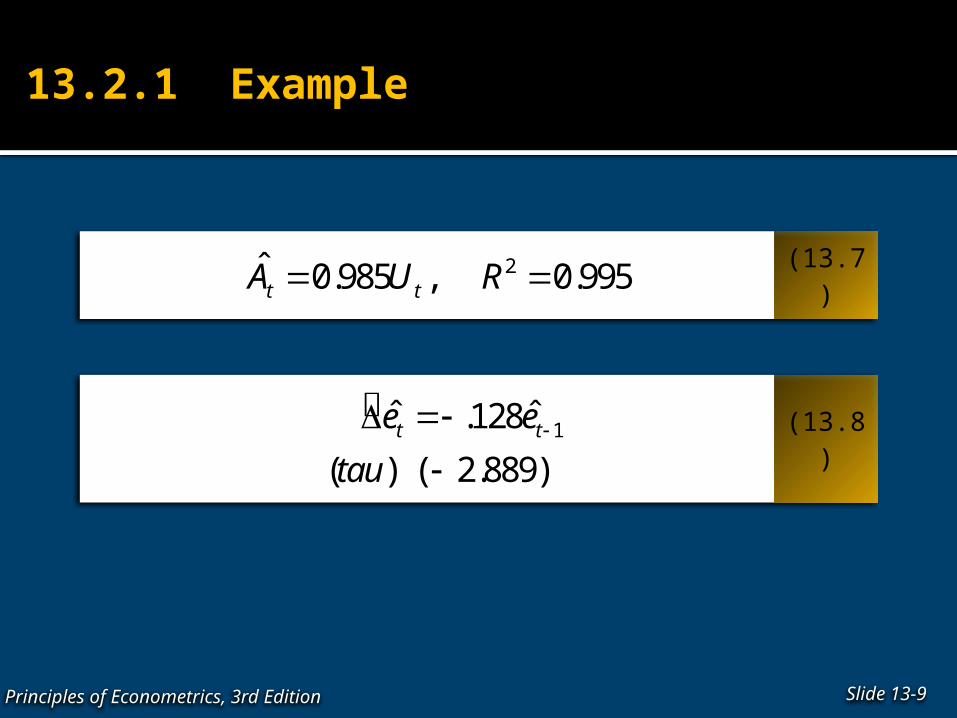

13.2.1 Example

Figure 13.1 Real Gross Domestic Products (GDP)

Slide 12-8Principles of Econometrics, 3rd Edition

13.2.1 Example

Slide 13-9Principles of Econometrics, 3rd Edition

(13.7)

(13.8)

2ˆ 0.985 , 0.995t tA U R

1ˆ ˆ.128

( ) ( 2.889)t te e

tau

13.2.1 Example

Slide 13-10Principles of Econometrics, 3rd Edition

(13.9)

1

1

ˆ0.492 0.099

( ) (2.077)

ˆ0.510 0.030

( ) (0.789)

t t

t t

A e

t

U e

t

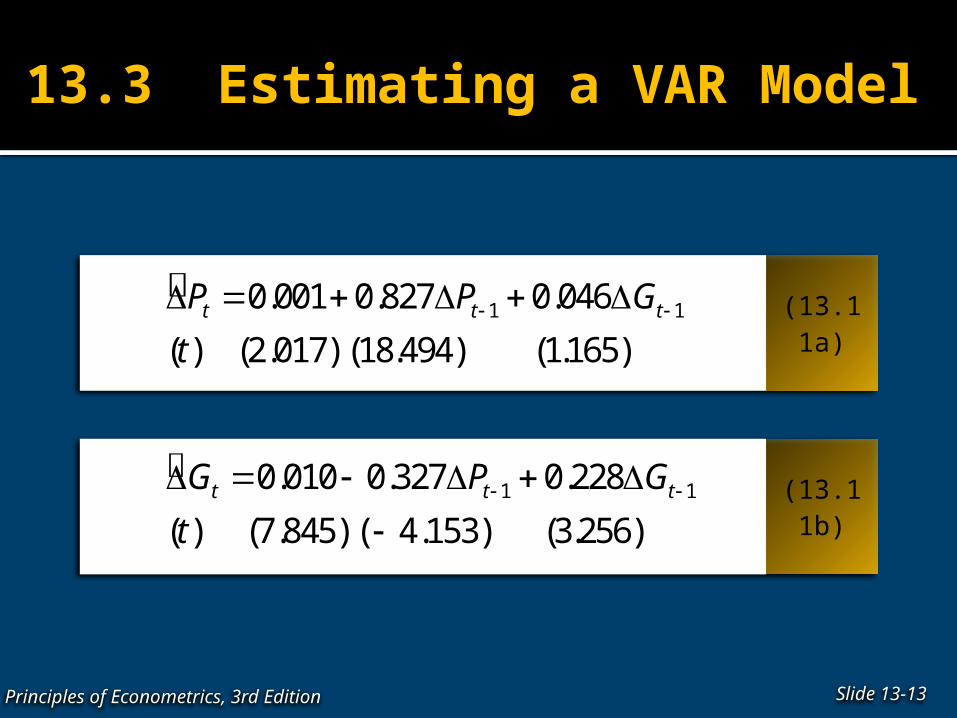

13.3 Estimating a VAR Model

Figure 13.2 Real GDP and the Consumer Price Index (CPI)

Slide 12-11Principles of Econometrics, 3rd Edition

13.3 Estimating a VAR Model

Slide 13-12Principles of Econometrics, 3rd Edition

(13.10)1

ˆ 1.631 0.623

ˆ ˆ0.009

( ) ( 0.977)

t t t

t t

e G P

e e

tau

13.3 Estimating a VAR Model

Slide 13-13Principles of Econometrics, 3rd Edition

(13.11a)

1 10.001 0.827 0.046

( ) (2.017) (18.494) (1.165) t t tP P G

t

(13.11b)

1 10.010 0.327 0.228

( ) (7.845) ( 4.153) (3.256) t t tG P G

t

13.4 Impulse Responses and Variance Decompositions 13.4.1 Impulse Response Functions

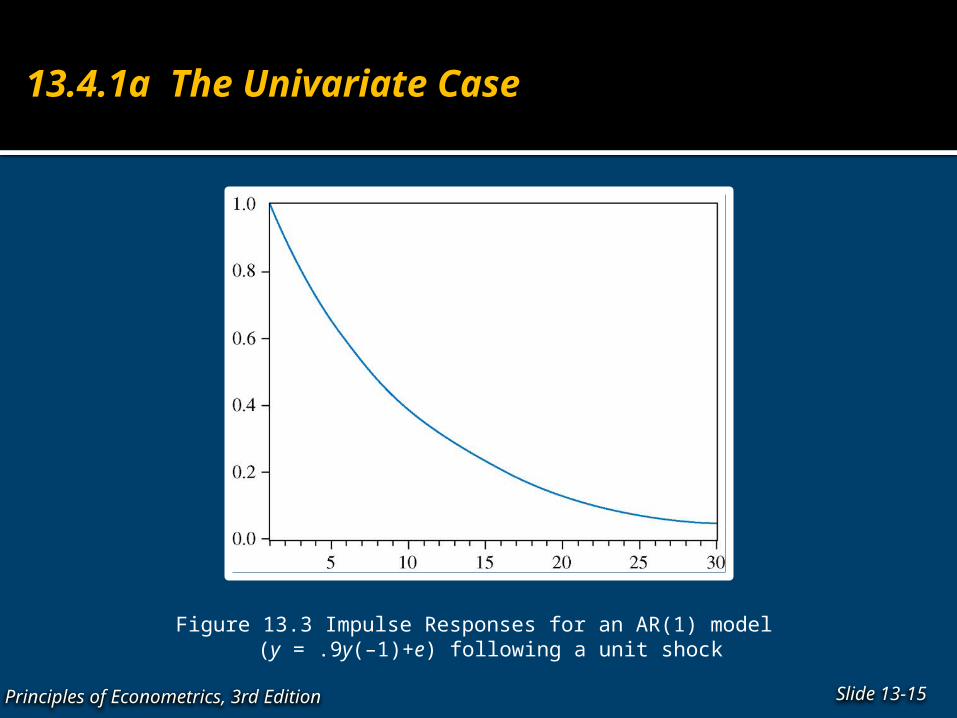

13.4.1a The Univariate Case

The series is subject it to a shock of size ν in period 1.

Slide 13-14Principles of Econometrics, 3rd Edition

1t t ty y v

1 0 1

2 1

23 2 1

2

1,

2,

3, ( )

...

the shock is , , ,

t y y v v

t y y v

t y y y v

v v v

13.4.1a The Univariate Case

Figure 13.3 Impulse Responses for an AR(1) model (y = .9y(–1)+e) following a unit shock

Slide 13-15Principles of Econometrics, 3rd Edition

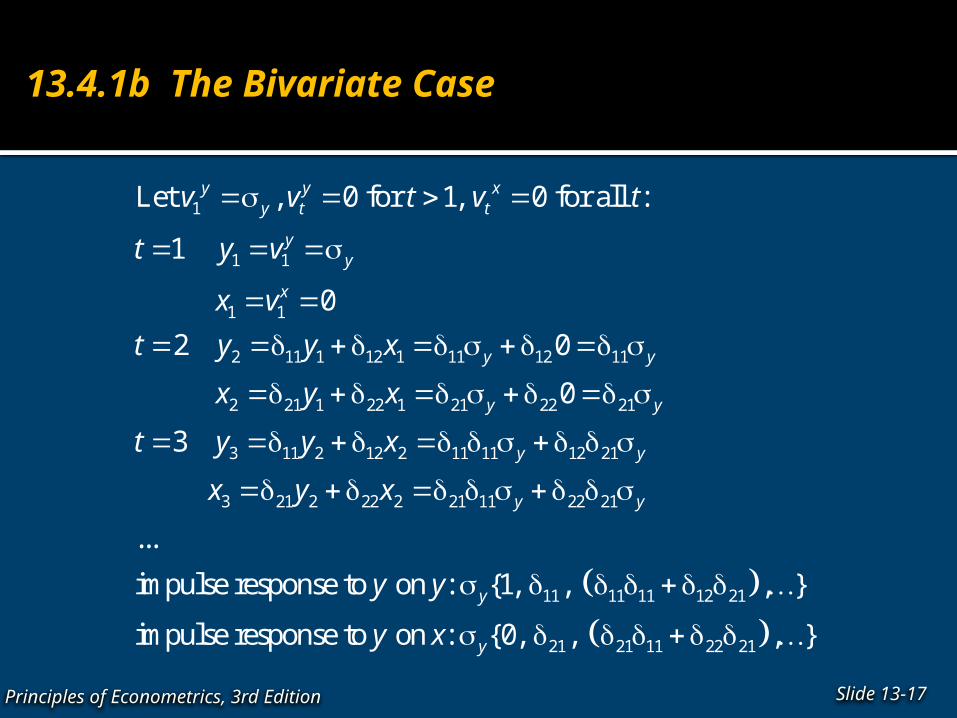

13.4.1b The Bivariate Case

Slide 13-16Principles of Econometrics, 3rd Edition

(13.12)

10 11 1 12 1

20 21 1 22 1

yt t t t

xt t t t

y y x v

x y x v

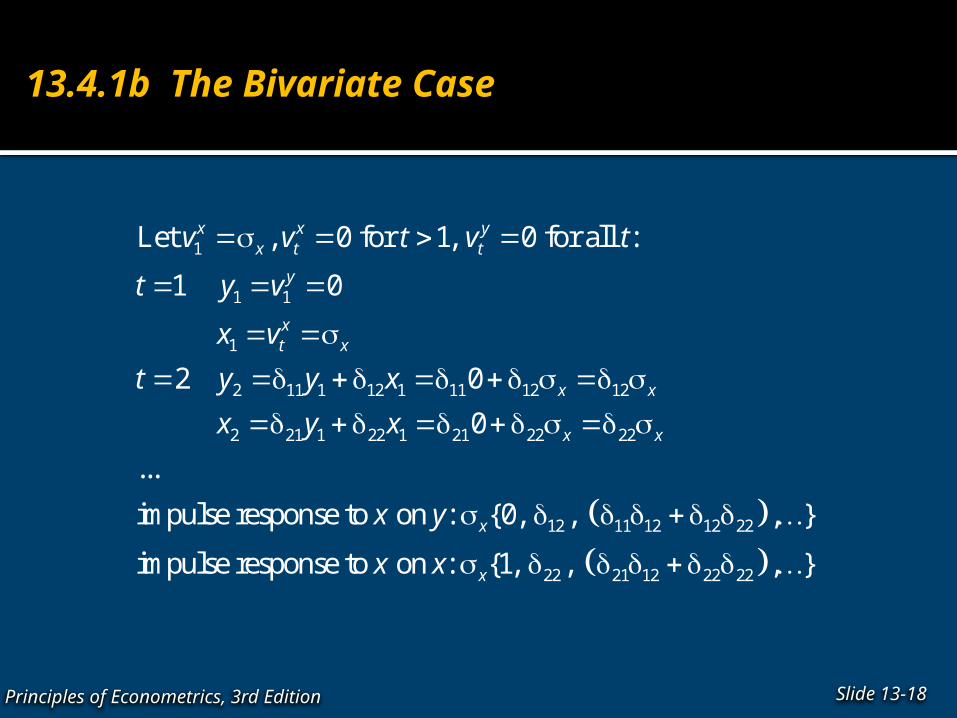

13.4.1b The Bivariate Case

Slide 13-17Principles of Econometrics, 3rd Edition

1

1 1

1 1

2 11 1 12 1 11 12 11

2 21 1 22 1 21 22 21

3 11 2 12 2 11 11 12 21

Let , 0 for 1, 0 for all :

1

0

2 0

0

3

y y xy t t

yy

x

y y

y y

y y

v v t v t

t y v

x v

t y y x

x y x

t y y x

3 21 2 22 2 21 11 22 21

11 11 11 12 21

21 21 11 22 21

...

impulse response to on : {1, , , }

impulse response to on : {0, , , }

y y

y

y

x y x

y y

y x

13.4.1b The Bivariate Case

Slide 13-18Principles of Econometrics, 3rd Edition

1

1 1

1

2 11 1 12 1 11 12 12

2 21 1 22 1 21 22 22

12

Let , 0 for 1, 0 for all :

1 0

2 0

0

...

impulse response to on : {0, ,

x x yx t t

y

xt x

x x

x x

x

v v t v t

t y v

x v

t y y x

x y x

x y

11 12 12 22

22 21 12 22 22

, }

impulse response to on : {1, , , }xx x

13.4.1b The Bivariate Case

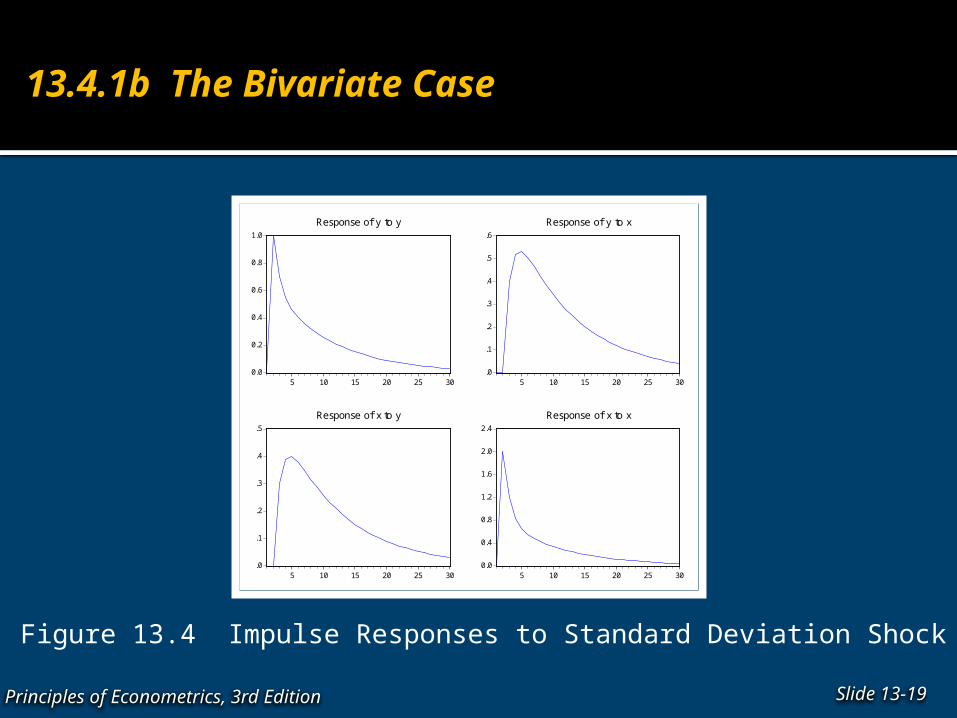

Figure 13.4 Impulse Responses to Standard Deviation Shock

Slide 13-19Principles of Econometrics, 3rd Edition

0.0

0.2

0.4

0.6

0.8

1.0

5 10 15 20 25 30

Response of y to y

.0

.1

.2

.3

.4

.5

.6

5 10 15 20 25 30

Response of y to x

.0

.1

.2

.3

.4

.5

5 10 15 20 25 30

Response of x to y

0.0

0.4

0.8

1.2

1.6

2.0

2.4

5 10 15 20 25 30

Response of x to x

13.4.2 Forecast Error Variance Decompositions

13.4.2a The Univariate Case

Slide 13-20Principles of Econometrics, 3rd Edition

1

1 1

1 1 1 1

22 1 2 1 2

22 2 2 1 2

[ ]

[ ]

[ ] [ ( ) ]

[ ]

t t t

Ft t t t

t t t t t t

Ft t t t t t t t t

t t t t t t t

y y v

y E y v

y E y y y v

y E y v E y v v y

y E y y y v v

13.4.2 Forecast Error Variance Decompositions

13.4.2b The Bivariate Case

Slide 13-21Principles of Econometrics, 3rd Edition

1 11 12 1 11 12

1 21 22 1 21 22

21 1 1 1 1

21 1 1 1 1

[ ]

[ ]

[ ] ; var( )

[ ] ; var( )

F yt t t t t t t

F xt t t t t t t

y y yt t t t y

x x xt t t t x

y E y x v y x

x E y x v y x

FE y E y v FE

FE x E x v FE

13.4.2 Forecast Error Variance Decompositions

13.4.2b The Bivariate Case

Slide 13-22Principles of Econometrics, 3rd Edition

2 11 1 12 1 2

11 11 12 1 12 21 22 1 2

11 11 12 12 21 22

[ ]

[ ]

F yt t t t t

y x yt t t t t t t t

t t t t

y E y x v

E y x v y x v v

y x y x

13.4.2 Forecast Error Variance Decompositions

13.4.2b The Bivariate Case

Slide 13-23Principles of Econometrics, 3rd Edition

2 21 1 22 1 2

21 11 12 1 22 21 22 1 2

21 11 12 22 21 22

[ ]

[ ( ) ( ) ]

( ) ( )

F xt t t t t

y x xt t t t t t t t

t t t t

x E y x v

E y x v y x v v

y x y x

13.4.2 Forecast Error Variance Decompositions

13.4.2b The Bivariate Case

Slide 13-24Principles of Econometrics, 3rd Edition

2 2 2 11 1 12 1 2

2 2 2 2 22 11 12

2 2 2 21 1 22 1 2

2 2 2 2 22 21 22

[ ] [ ]

var( )

[ ] [ ]

var( )

y y x yt t t t t t

yy x y

x y x xt t t t t t

xy x x

FE y E y v v v

FE

FE x E x v v v

FE

13.4.2 Forecast Error Variance Decompositions

13.4.2c The General Case

The example above assumes that x and y are not contemporaneously related and that the shocks are uncorrelated. There is no identification problem and the generation and interpretation of the impulse response functions and decomposition of the forecast error variance are straightforward. In general, this is unlikely to be the case. Contemporaneous interactions and correlated errors complicate the identification of the nature of shocks and hence the interpretation of the impulses and decomposition of the causes of the forecast error variance.

Slide 13-25Principles of Econometrics, 3rd Edition

Keywords

Slide 13-26Principles of Econometrics, 3rd Edition

Dynamic relationships Error Correction Forecast Error Variance

Decomposition Identification problem Impulse Response Functions VAR model VEC Model

Chapter 13 Appendix

Slide 13-27Principles of Econometrics, 3rd Edition

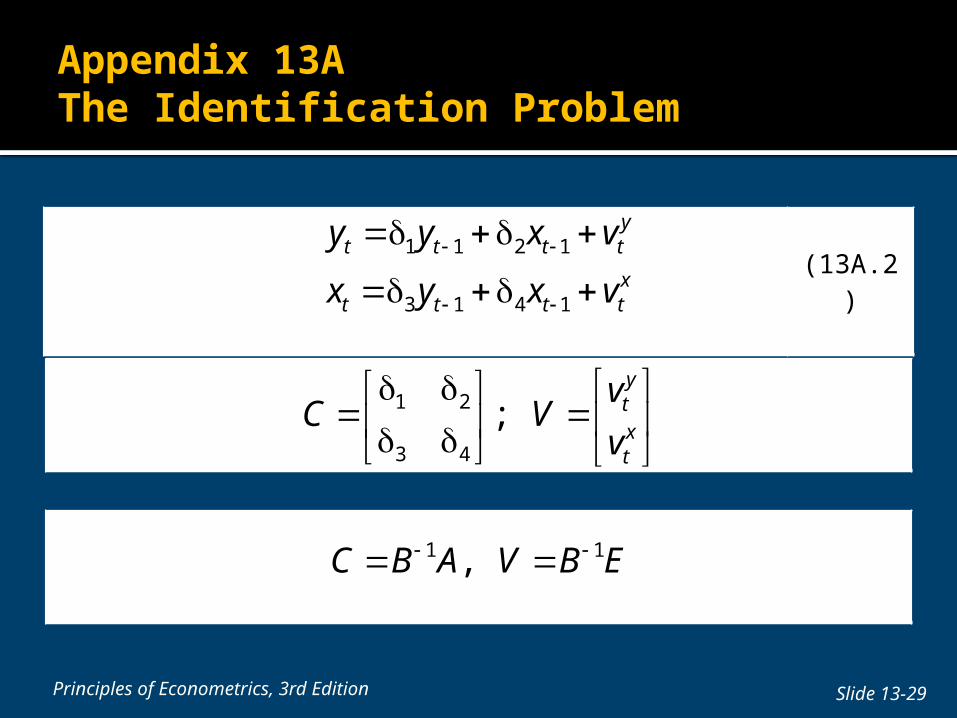

Appendix 13A The Identification Problem

Appendix 13A The Identification Problem

Principles of Econometrics, 3rd Edition Slide 13-28

(13A.1)1 1 1 2 1

2 3 1 4 1

yt t t t t

xt t t t t

y x y x e

x y y x e

1 2 11

3 4 12

1

1

yt t t

xt t t

y y e

x x e

1 21

3 42

1; ;

1

ytxt

eB A E

e

Appendix 13A The Identification Problem

Principles of Econometrics, 3rd Edition Slide 13-29

(13A.2)1 1 2 1

3 1 4 1

yt t t t

xt t t t

y y x v

x y x v

1 2

3 4

; ytxt

vC V

v

1 1, C B A V B E