an introduction to the brazilian agriculture and food sector · an introduction to the brazilian...

TRANSCRIPT

CONFIDENTIAL

FOR INTERNAL USE WITHIN CLIENT COMPANY ONLY

AN INTRODUCTION TO THE

BRAZILIAN AGRICULTURE

AND FOOD SECTOR

FACT PACK - AGRICULTURE AND FOOD INDUSTRY BRAZIL

São Paulo, Brazil

November 2015

BUSINESS SWEDEN 6 APRIL, 2016 2

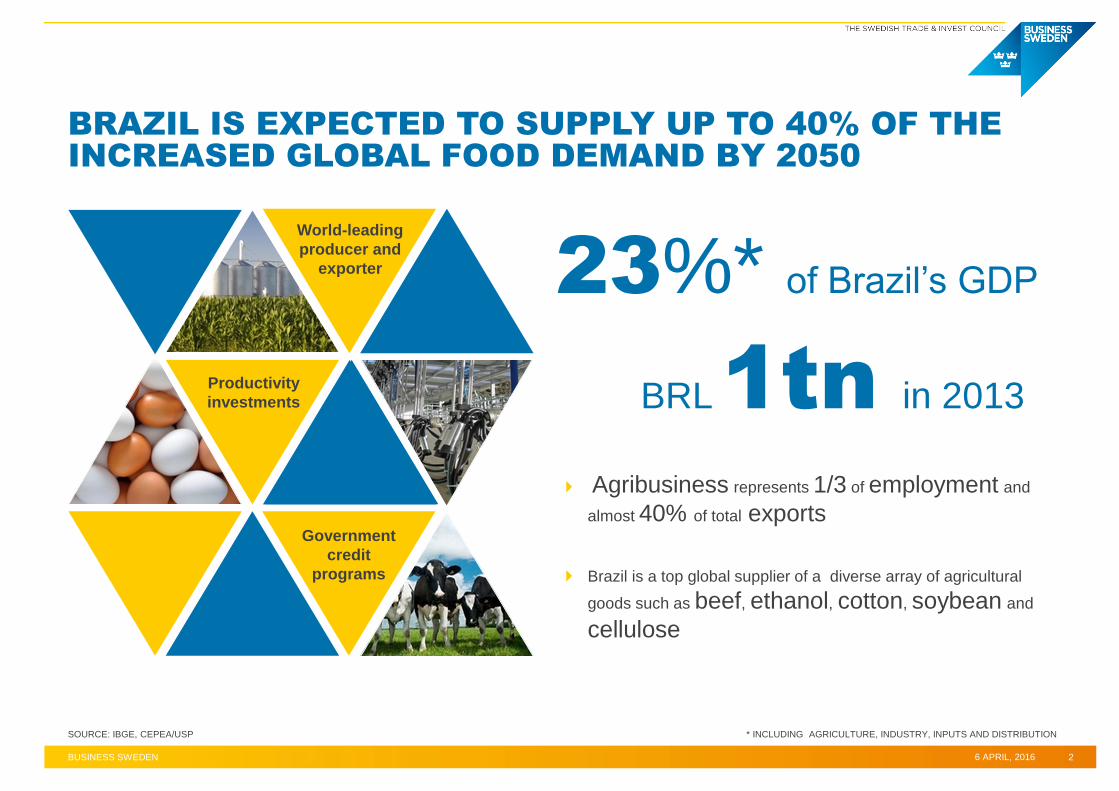

BRAZIL IS EXPECTED TO SUPPLY UP TO 40% OF THE

INCREASED GLOBAL FOOD DEMAND BY 2050

SOURCE: IBGE, CEPEA/USP

23%* of Brazil’s GDP

BRL 1tn in 2013

Agribusiness represents 1/3 of employment and

almost 40% of total exports

Productivity

investments

Government

credit

programs

World-leading

producer and

exporter

Brazil is a top global supplier of a diverse array of agricultural

goods such as beef, ethanol, cotton, soybean and

cellulose

* INCLUDING AGRICULTURE, INDUSTRY, INPUTS AND DISTRIBUTION

BUSINESS SWEDEN 6 APRIL, 2016 3

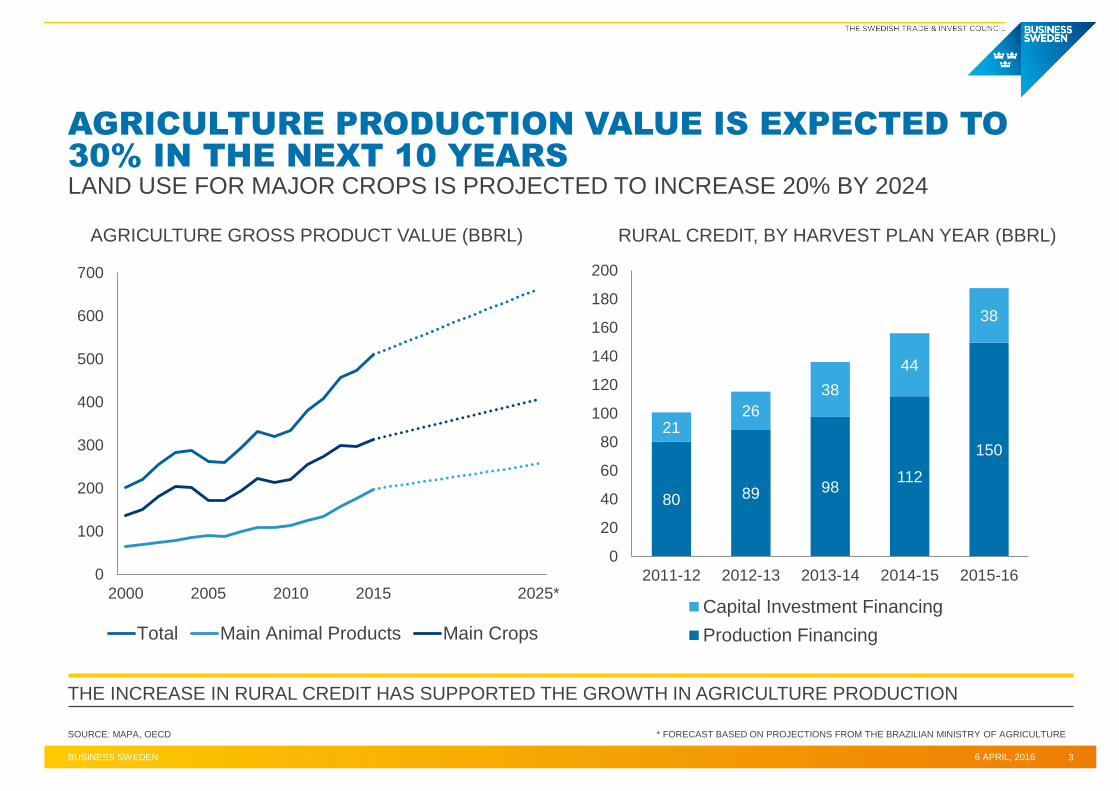

AGRICULTURE PRODUCTION VALUE IS EXPECTED TO

30% IN THE NEXT 10 YEARS

SOURCE: MAPA, OECD

0

100

200

300

400

500

600

700

2000 2005 2010 2015 2025*

Total Main Animal Products Main Crops

* FORECAST BASED ON PROJECTIONS FROM THE BRAZILIAN MINISTRY OF AGRICULTURE

AGRICULTURE GROSS PRODUCT VALUE (BBRL)

THE INCREASE IN RURAL CREDIT HAS SUPPORTED THE GROWTH IN AGRICULTURE PRODUCTION

80 89 98 112

150

21 26

38

44

38

0

20

40

60

80

100

120

140

160

180

200

2011-12 2012-13 2013-14 2014-15 2015-16

Capital Investment Financing

Production Financing

RURAL CREDIT, BY HARVEST PLAN YEAR (BBRL)

LAND USE FOR MAJOR CROPS IS PROJECTED TO INCREASE 20% BY 2024

BUSINESS SWEDEN 6 APRIL, 2016 4

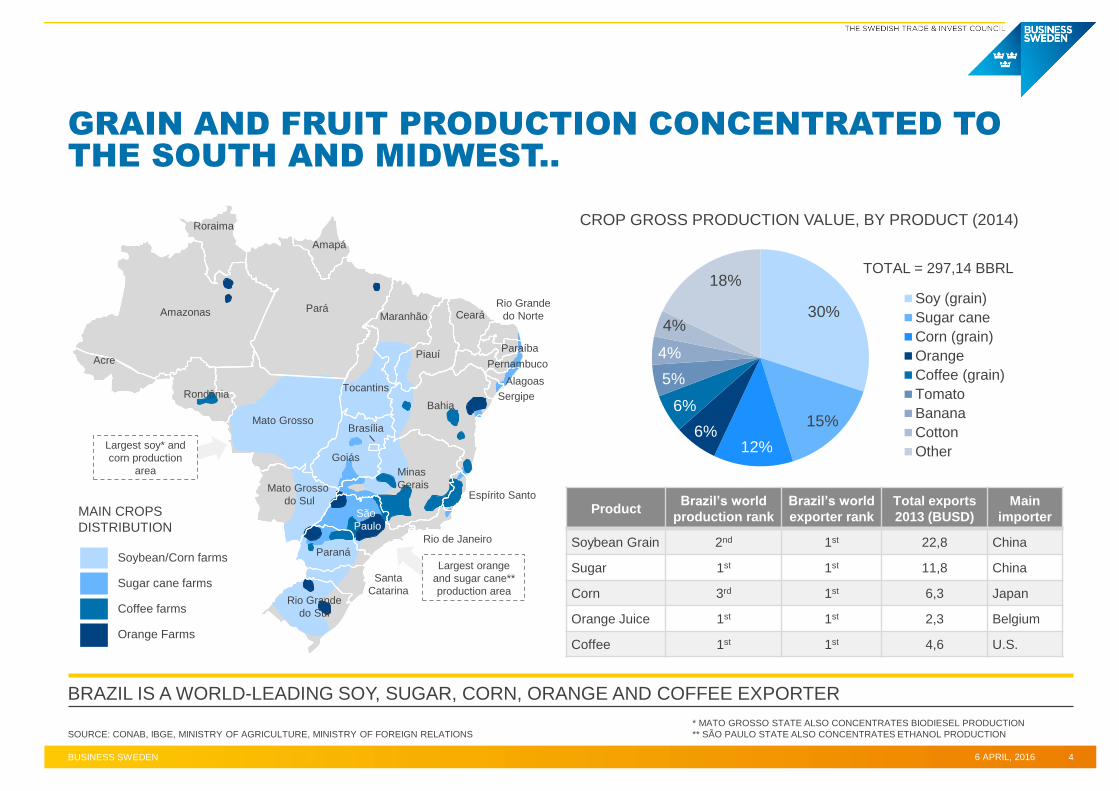

GRAIN AND FRUIT PRODUCTION CONCENTRATED TO

THE SOUTH AND MIDWEST..

SOURCE: CONAB, IBGE, MINISTRY OF AGRICULTURE, MINISTRY OF FOREIGN RELATIONS

Soybean/Corn farms

Sugar cane farms

Coffee farms

Orange Farms

MAIN CROPS

DISTRIBUTION

30%

15%

12% 6%

6%

5%

4%

4%

18% Soy (grain)

Sugar cane

Corn (grain)

Orange

Coffee (grain)

Tomato

Banana

Cotton

Other

Product Brazil’s world

production rank

Brazil’s world

exporter rank

Total exports

2013 (BUSD)

Main

importer

Soybean Grain 2nd 1st 22,8 China

Sugar 1st 1st 11,8 China

Corn 3rd 1st 6,3 Japan

Orange Juice 1st 1st 2,3 Belgium

Coffee 1st 1st 4,6 U.S.

BRAZIL IS A WORLD-LEADING SOY, SUGAR, CORN, ORANGE AND COFFEE EXPORTER

Pará

Santa

Catarina

Tocantins

Bahia

Rio Grande

do Sul

Paraná

Mato Grosso

do Sul São

Paulo

Espírito Santo

Rio de Janeiro

Minas

Gerais

Mato Grosso

Rondônia

Acre

Amazonas

Roraima

Amapá

Maranhão

Piauí

Sergipe

Ceará

Alagoas

Pernambuco

Goiás

Paraíba

Rio Grande

do Norte

Brasília

CROP GROSS PRODUCTION VALUE, BY PRODUCT (2014)

TOTAL = 297,14 BBRL

Largest soy* and

corn production

area

Largest orange

and sugar cane**

production area

* MATO GROSSO STATE ALSO CONCENTRATES BIODIESEL PRODUCTION

** SÃO PAULO STATE ALSO CONCENTRATES ETHANOL PRODUCTION

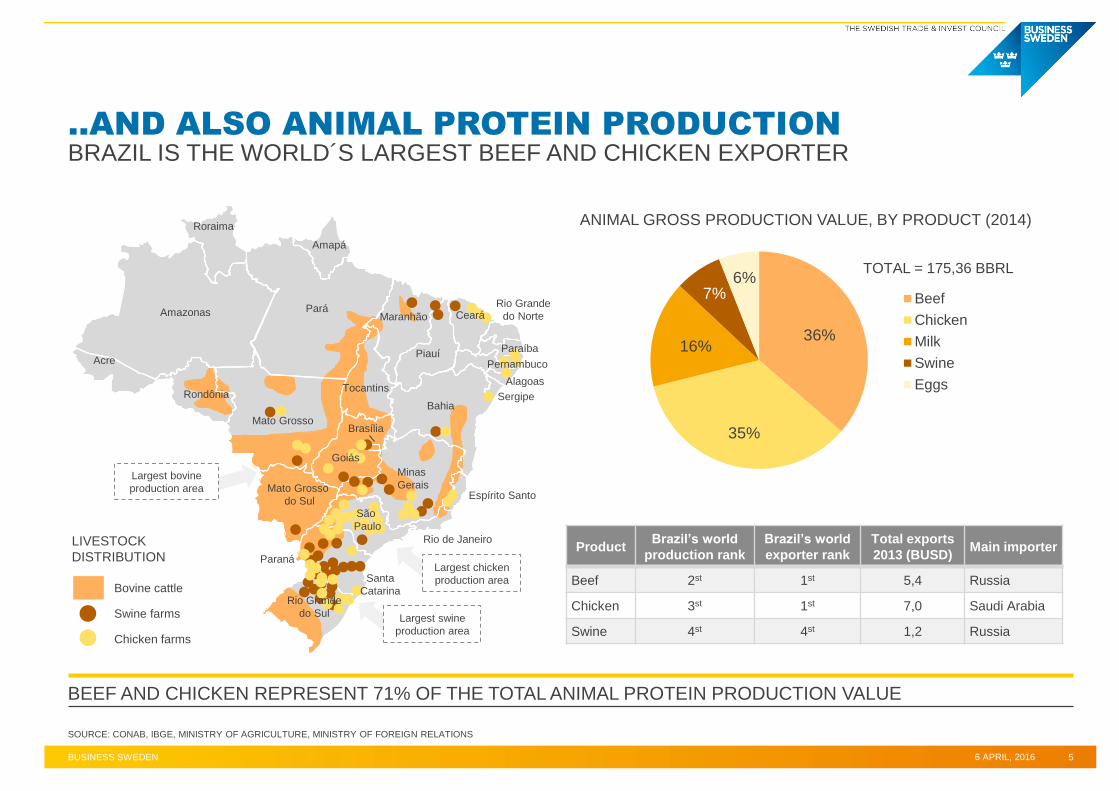

BRAZIL IS THE WORLD´S LARGEST BEEF AND CHICKEN EXPORTER

BUSINESS SWEDEN 6 APRIL, 2016 5

..AND ALSO ANIMAL PROTEIN PRODUCTION

SOURCE: CONAB, IBGE, MINISTRY OF AGRICULTURE, MINISTRY OF FOREIGN RELATIONS

Bovine cattle

Swine farms

Chicken farms

LIVESTOCK

DISTRIBUTION

BEEF AND CHICKEN REPRESENT 71% OF THE TOTAL ANIMAL PROTEIN PRODUCTION VALUE

Product Brazil’s world

production rank

Brazil’s world

exporter rank

Total exports

2013 (BUSD) Main importer

Beef 2st 1st 5,4 Russia

Chicken 3st 1st 7,0 Saudi Arabia

Swine 4st 4st 1,2 Russia

36%

35%

16%

7% 6%

Beef

Chicken

Milk

Swine

Eggs

Pará

Santa

Catarina

Tocantins

Bahia

Rio Grande

do Sul

Paraná

Mato Grosso

do Sul São

Paulo

Espírito Santo

Rio de Janeiro

Minas

Gerais

Mato Grosso

Rondônia

Acre

Amazonas

Roraima

Amapá

Maranhão

Piauí

Sergipe

Ceará

Alagoas

Pernambuco

Goiás

Paraíba

Rio Grande

do Norte

Brasília

ANIMAL GROSS PRODUCTION VALUE, BY PRODUCT (2014)

TOTAL = 175,36 BBRL

Largest bovine

production area

Largest swine

production area

Largest chicken

production area

BUSINESS SWEDEN 6 APRIL, 2016 6

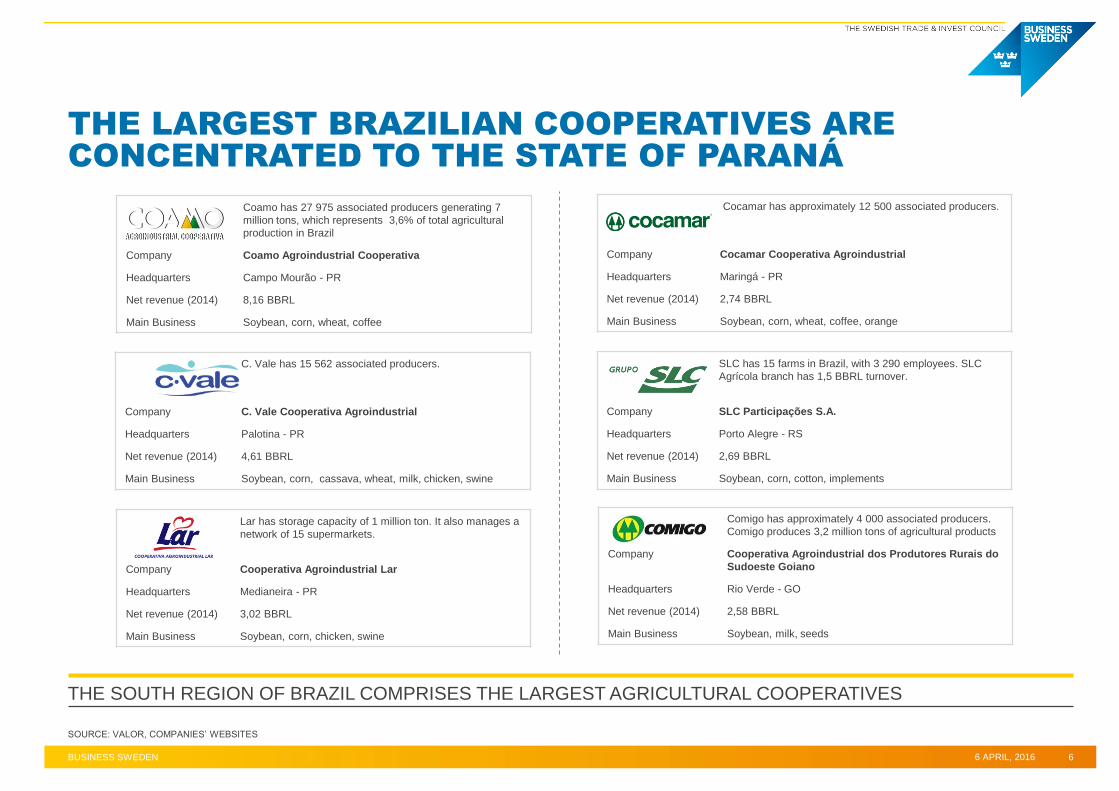

THE LARGEST BRAZILIAN COOPERATIVES ARE

CONCENTRATED TO THE STATE OF PARANÁ

SOURCE: VALOR, COMPANIES’ WEBSITES

SLC has 15 farms in Brazil, with 3 290 employees. SLC

Agrícola branch has 1,5 BBRL turnover.

Company SLC Participações S.A.

Headquarters Porto Alegre - RS

Net revenue (2014) 2,69 BBRL

Main Business Soybean, corn, cotton, implements

C. Vale has 15 562 associated producers.

Company C. Vale Cooperativa Agroindustrial

Headquarters Palotina - PR

Net revenue (2014) 4,61 BBRL

Main Business Soybean, corn, cassava, wheat, milk, chicken, swine

Coamo has 27 975 associated producers generating 7

million tons, which represents 3,6% of total agricultural

production in Brazil

Company Coamo Agroindustrial Cooperativa

Headquarters Campo Mourão - PR

Net revenue (2014) 8,16 BBRL

Main Business Soybean, corn, wheat, coffee

Lar has storage capacity of 1 million ton. It also manages a

network of 15 supermarkets.

Company Cooperativa Agroindustrial Lar

Headquarters Medianeira - PR

Net revenue (2014) 3,02 BBRL

Main Business Soybean, corn, chicken, swine

Cocamar has approximately 12 500 associated producers.

Company Cocamar Cooperativa Agroindustrial

Headquarters Maringá - PR

Net revenue (2014) 2,74 BBRL

Main Business Soybean, corn, wheat, coffee, orange

Comigo has approximately 4 000 associated producers.

Comigo produces 3,2 million tons of agricultural products

Company Cooperativa Agroindustrial dos Produtores Rurais do

Sudoeste Goiano

Headquarters Rio Verde - GO

Net revenue (2014) 2,58 BBRL

Main Business Soybean, milk, seeds

THE SOUTH REGION OF BRAZIL COMPRISES THE LARGEST AGRICULTURAL COOPERATIVES

LARGE CONSUMER MARKET AND EXPORTS SHOULD PUSH FOR GROWTH IN 2016

BUSINESS SWEDEN 6 APRIL, 2016 7

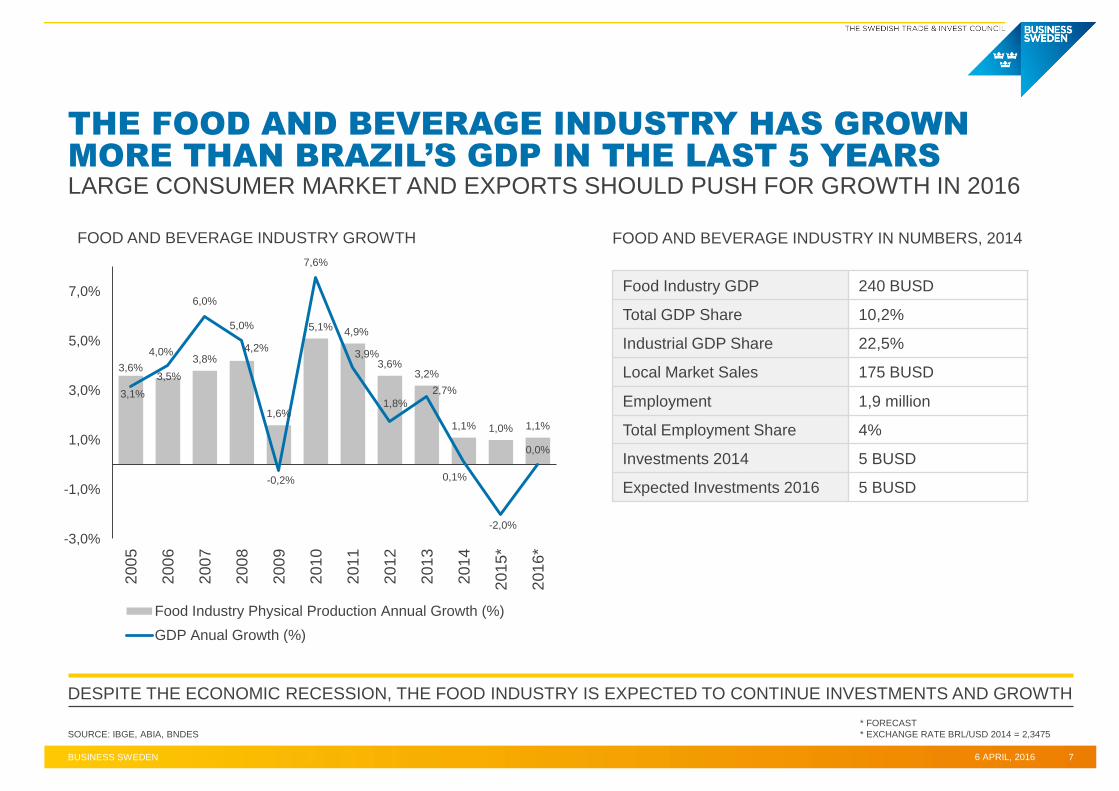

THE FOOD AND BEVERAGE INDUSTRY HAS GROWN

MORE THAN BRAZIL’S GDP IN THE LAST 5 YEARS

SOURCE: IBGE, ABIA, BNDES

3,6% 3,5%

3,8% 4,2%

1,6%

5,1% 4,9%

3,6% 3,2%

1,1% 1,0% 1,1%

3,1%

4,0%

6,0%

5,0%

-0,2%

7,6%

3,9%

1,8%

2,7%

0,1%

-2,0%

0,0%

-3,0%

-1,0%

1,0%

3,0%

5,0%

7,0%

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5*

201

6*

Food Industry Physical Production Annual Growth (%)

GDP Anual Growth (%)

DESPITE THE ECONOMIC RECESSION, THE FOOD INDUSTRY IS EXPECTED TO CONTINUE INVESTMENTS AND GROWTH

* FORECAST

* EXCHANGE RATE BRL/USD 2014 = 2,3475

Food Industry GDP 240 BUSD

Total GDP Share 10,2%

Industrial GDP Share 22,5%

Local Market Sales 175 BUSD

Employment 1,9 million

Total Employment Share 4%

Investments 2014 5 BUSD

Expected Investments 2016 5 BUSD

FOOD AND BEVERAGE INDUSTRY IN NUMBERS, 2014 FOOD AND BEVERAGE INDUSTRY GROWTH

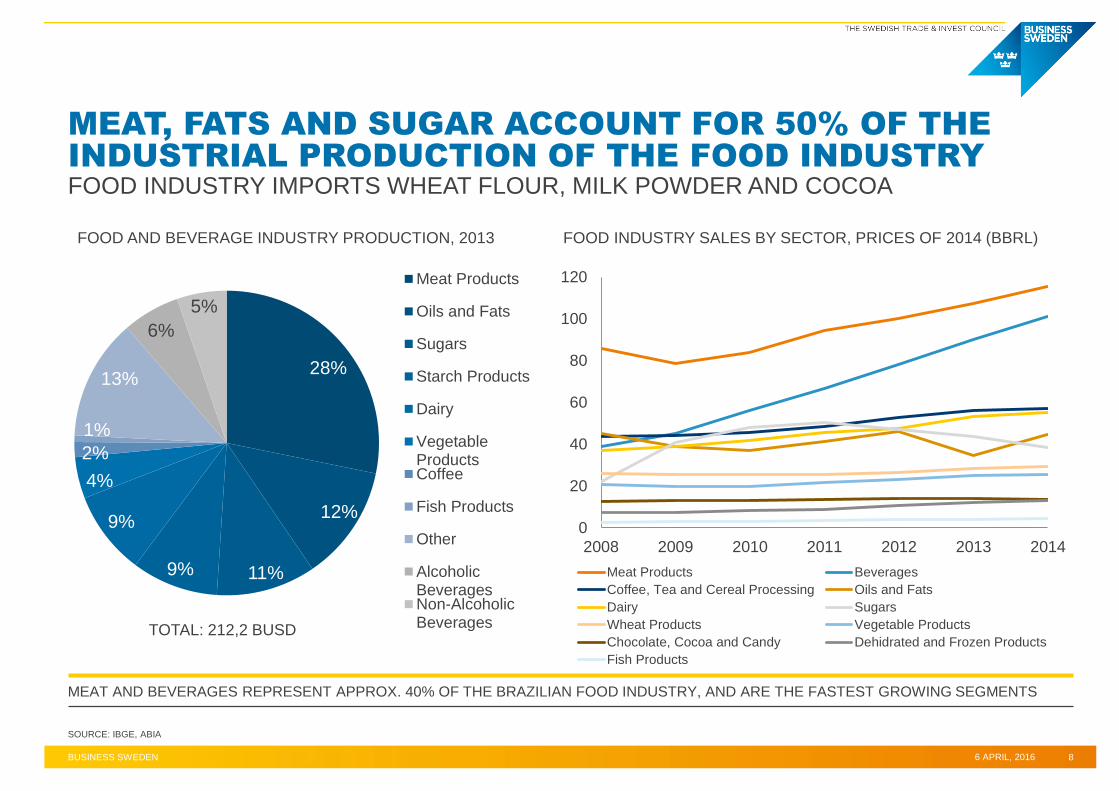

FOOD INDUSTRY IMPORTS WHEAT FLOUR, MILK POWDER AND COCOA

28%

12%

11% 9%

9%

4%

2%

1%

13%

6%

5%

Meat Products

Oils and Fats

Sugars

Starch Products

Dairy

VegetableProductsCoffee

Fish Products

Other

AlcoholicBeveragesNon-AlcoholicBeverages

BUSINESS SWEDEN 6 APRIL, 2016 8

MEAT, FATS AND SUGAR ACCOUNT FOR 50% OF THE

INDUSTRIAL PRODUCTION OF THE FOOD INDUSTRY

SOURCE: IBGE, ABIA

MEAT AND BEVERAGES REPRESENT APPROX. 40% OF THE BRAZILIAN FOOD INDUSTRY, AND ARE THE FASTEST GROWING SEGMENTS

TOTAL: 212,2 BUSD

FOOD AND BEVERAGE INDUSTRY PRODUCTION, 2013 FOOD INDUSTRY SALES BY SECTOR, PRICES OF 2014 (BBRL)

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013 2014

Meat Products Beverages

Coffee, Tea and Cereal Processing Oils and Fats

Dairy Sugars

Wheat Products Vegetable Products

Chocolate, Cocoa and Candy Dehidrated and Frozen Products

Fish Products

São Paulo and Minas Gerais are the main food producing states

The main obstacle to the expansion of investments is the poor

logistics infrastructure. Lack of roads, railways and ports and

expensive freight make prices go up in distant regions

Logistics explain the existence of small regional food companies

across the country, which supply the local demand

Large companies, local and foreign are acquiring smaller

companies; the number of fusions of food companies tripled in

1T2015

There are strong Brazilian companies consolidated in the local

market, which are exporting and expanding to foreign countries

Many companies, including large ones, produce “food commodities”,

which can practice limited price differentiation compared to

competitors. Thus, competition takes place on the lowest price.

6 APRIL, 2016 BUSINESS SWEDEN 9

THE BRAZILIAN FOOD INDUSTRY IS CONCENTRATED TO

THE SOUTH AND SOUTHEAST REGIONS…

SOURCE: IBGE, VALOR, ABIA, BNDES

Pará

Santa

Catarina

Tocantins

Bahia

Rio Grande

do Sul

Paraná

Mato Grosso

do Sul São

Paulo

Espírito Santo

Rio de Janeiro

Minas

Gerais

Mato Grosso

Rondônia

Acre

Amazonas

Roraima

Amapá

Maranhão

Piauí

Sergipe

Ceará

Alagoas

Pernambuco

Goiás

Paraíba

Rio Grande

do Norte

Brasília

THE INDUSTRY IS GOING THROUGH A CONSOLIDATION PROCESS OF LARGE COMPANIES ACQUIRING SMALLER

0-375

375-750

750-1500

1500-3000

3000-4500

+4500

Number of

manufacturing plants

by state

FOOD INDUSTRY COMPANIES IN BRAZIL

MEAT, GRAINS AND BEVERAGES ARE THE MAIN BUSINESS OF THE LARGEST FOOD COMPANIES

BUSINESS SWEDEN 6 APRIL, 2016 10

… AND IS DOMINATED BY GIANT FOOD COMPANIES

SOURCE: VALOR, COMPANIES’ WEBSITES, MEDIA OUTLETS

BRF is the 7th largest food company in the world, present

in 110 countries. BRF has 60 industrial plants in Brazil,

and 95% penetration in Brazilian households.

Company BRF S.A.

Capital control Brazilian

Net revenue (2014) 29 BBRL

Business Animal protein, processed food

Cargill maintains 19 industrial plants in Brazil, as well as 10

000 employees. Cargill is the 2nd largest soybean exporter

in Brazil.

Company Cargill Agrícola S.A.

Capital control US

Net revenue (2014) 26,2 BBRL

Business Processed food, storage and reselling of grains

Marfrig has an operational exports to over 100 countries,

and is the 4th largest beef producer in the world.

Company Marfrig Global Foods S.A.

Capital control Brazilian

Net revenue (2014) 21 BBRL

Business Animal protein

JBS was the 2nd largest food company in the world in

2013, with 43,2 BUSD in annual sales, only behind Nestlé.

JBS has 216 000 employees, acting in 22 countries.

Company JBS S.A.

Capital control Brazilian

Net revenue (2014) 120,5 BBRL

Business Animal protein, dairy, cosmetics, cleaning products

THE BRAZILIAN FOOD INDUSTRY COMPRISES LARGE COMPANIES CAPABLE OF INVESTING IN HIGH-TECH PRODUCTS

Ambev is the largest brewery in Latin America and the 5th

in the world, operating in 14 countries. Ambev is part of AB

InBev, the largest brewer in the world.

Company Ambev S.A.

Capital control Brazilian/Belgian

Net revenue (2014) 38,1 BBRL

Business Beers, soft drinks

Bunge operates more than 100 manufacturing plants in

Brazil, with 20 000 employees. Bunge is the largest

agribusiness exporter in Brazil.

Company Bunge Alimentos S.A.

Capital control Brazilian/Belgian

Net revenue (2014) 34,1 BBRL

Business Food, oils, grains

An

ima

l P

rote

in

Fo

od

& G

rain

s

Beve

rag

es

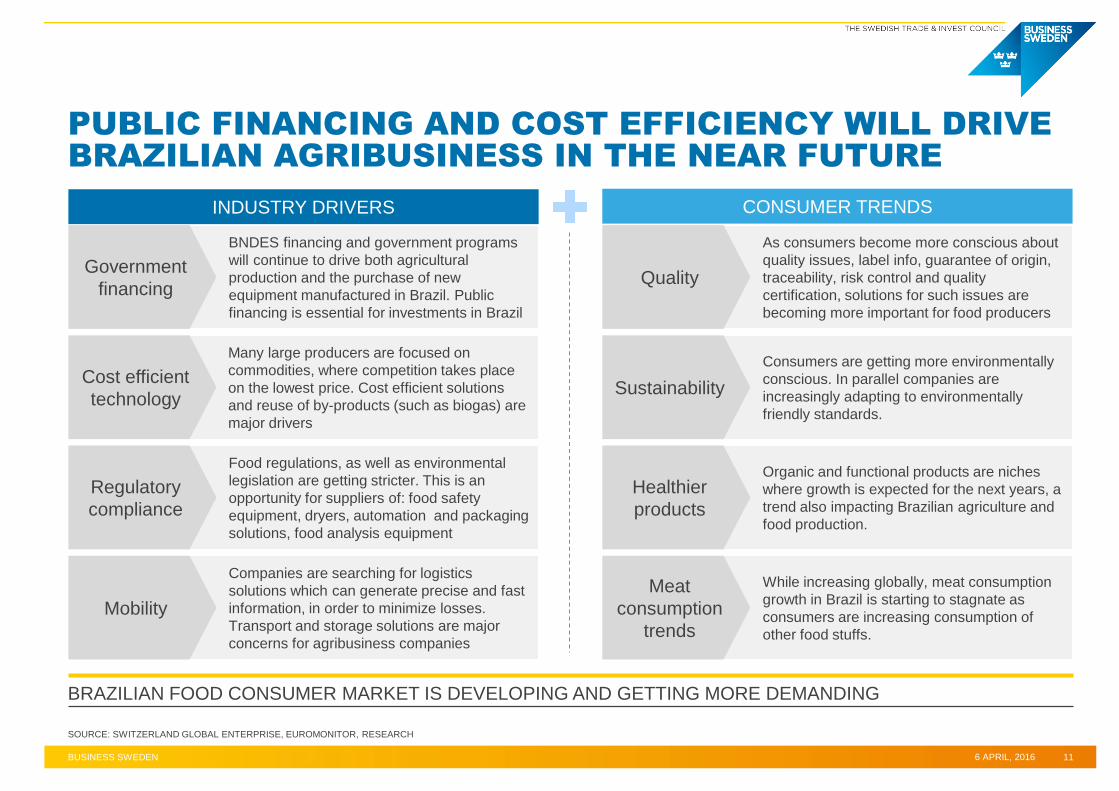

Many large producers are focused on

commodities, where competition takes place

on the lowest price. Cost efficient solutions

and reuse of by-products (such as biogas) are

major drivers

BNDES financing and government programs

will continue to drive both agricultural

production and the purchase of new

equipment manufactured in Brazil. Public

financing is essential for investments in Brazil

BUSINESS SWEDEN 6 APRIL, 2016 11

PUBLIC FINANCING AND COST EFFICIENCY WILL DRIVE

BRAZILIAN AGRIBUSINESS IN THE NEAR FUTURE

SOURCE: SWITZERLAND GLOBAL ENTERPRISE, EUROMONITOR, RESEARCH

BRAZILIAN FOOD CONSUMER MARKET IS DEVELOPING AND GETTING MORE DEMANDING

Government

financing

Cost efficient

technology

Companies are searching for logistics

solutions which can generate precise and fast

information, in order to minimize losses.

Transport and storage solutions are major

concerns for agribusiness companies

Food regulations, as well as environmental

legislation are getting stricter. This is an

opportunity for suppliers of: food safety

equipment, dryers, automation and packaging

solutions, food analysis equipment

Regulatory

compliance

Mobility

Consumers are getting more environmentally

conscious. In parallel companies are

increasingly adapting to environmentally

friendly standards.

As consumers become more conscious about

quality issues, label info, guarantee of origin,

traceability, risk control and quality

certification, solutions for such issues are

becoming more important for food producers

Quality

Sustainability

While increasing globally, meat consumption

growth in Brazil is starting to stagnate as

consumers are increasing consumption of

other food stuffs.

Organic and functional products are niches

where growth is expected for the next years, a

trend also impacting Brazilian agriculture and

food production.

Healthier

products

Meat

consumption

trends

INDUSTRY DRIVERS CONSUMER TRENDS

BUSINESS SWEDEN 6 APRIL, 2016 12

FOOD AND AGRICULTURE OFFERS GREAT

OPPORTUNITIES FOR SWEDISH COMPANIES IN BRAZIL

Which

opportunities

make Brazil

interesting?

What

challenges

should companies

be ready to face?

Confusing and excessively bureaucratic food

regulations

Complex tax system

High import tariffs and other taxes

Protection of local industry

Poor infrastructure for

roads, energy, ports and

airports

Language barrier, mainly

for agriculture

BNDES and government financing programs for

clients of locally established manufacturers

Pursue of clean and cost efficient technology

Production of healthier products and innovation

Large agribusiness market, internationally integrated

Advantages: diverse climate and land availability

Diversified production and growth

Devaluated BRL is stimulating exports

Investments

Players

Market

Demand

Business in Brazil

Market

Recent economic slowdown and higher inflation in Brazil

Lower commodities price

Beef production to slow down due to local demand

saturation

LARGE AND GROWING AGRICULTURE AND FOOD PRODUCER WITH INCREASING DEMAND FOR TECHNOLOGY

Large organized

cooperatives who need

to invest (e.g. storage,

transport, implements)

Brazilian large exporters

who want to grow

BUSINESS SWEDEN OFFERS A FULL SERVICE

PORTFOLIO FOR EFFICIENT MARKET ENTRY

* BSO SERVICES INCLUDE: OFFICE PLACE & SERVICE, ADMINISTRATION, COMPANY ESTABLISHMENT (INCL

LEGAL ADRESS) , DELEGATE MANAGER AND FINANCIAL ANALYSIS

6 APRIL, 2016 BUSINESS SWEDEN 13

ICT

OUR INDUSTRY FOCUS

HEALTH CARE &

LIFE SCIENCE

MATERIALS &

MANUFACTURI

NG

SECURITY AGRICULTURE,

FOOD & FOREST

ENERGY &

ENVIRONMENT

TRANSPORT

SYSTEMS

OUR CUSTOMERS

SWEDISH COMPANIES EXPANDING

INTO BRAZIL LOCAL SUBSIDIARIES OF

SWEDISH COMPANIES SWEDISH GOVERNMENT

OUR MARKET OFFERING

MARKET ENTRY

STRATEGY

OUR STRENGTH

PARTNER

SEARCH STAKEHOLDER

MANAGEMENT

IMPORT

ANALYSIS

SOURCING

ANALYSIS

ACQUISITION

SUPPORT

MARKET

ANALYSIS

BUSINESS

SUPPORT

OFFICE *

RECRUITING

EXPERIENCED

TEAM WITH

INDUSTRY FOCUS

UNIQUE OWNERSHIP PROVIDE

ACCESS TO THE SWEDISH

GOVERNM.& FUNDING STRUCTURE

GLOBAL

PRESENCE

LOCAL& SWEDISH

PERSPECTIVE TO

BUSINESS OPPORTUNITIES

ACCESS TO HIGH LEVEL

AUTHORITIES & BUSINESS

NETWORKS IN BRAZIL

CONTACT US

BUSINESS SWEDEN IN BRAZIL

Rua Joaquim Floriano, 466 – cj 1908 – Ed. Office

BR 04534-002 – São Paulo - Brazil

Phone: +55 11 2137 4400

Fax: +55 11 2137 4425