an italian perspective

TRANSCRIPT

Excess Liquidity: drivers and costsAn Italian PerspectiveECB MMCGFrankfurt, 26 September 2017

1

The liability side of resident banks’ balance sheets is still changing (< bonds and RoW; >direct depos and domestic)

The main drivers of the excess cash (1)

01/2007 04/2011 08/2012 07/2013 12/2015 06/2017Capital & reserves 7% 10% 9% 9% 11% 11%Other liabilities 14% 9% 11% 10% 9% 8%Bonds 20% 22% 23% 22% 16% 13%Deposits: Rest of the World 7% 5% 3% 4% 3% 3%Deposits: other EA MFIs 8% 7% 5% 4% 4% 4%Deposits: Resident MFIs 15% 11% 15% 14% 14% 17%Deposits: Central Govt 0% 0% 1% 1% 1% 1%Deposits: Other residents 29% 37% 33% 36% 41% 42%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Capital & reserves

Other liabilities

Bonds

Deposits: Rest of theWorldDeposits: other EA MFIs

Deposits: Resident MFIs

Deposits: Central Govt

Deposits: Otherresidents

Source: ECB, Bloomberg, Intesa Sanpaolo.

2

Household deposits are stabilizing, against the backdrop of more relaxed liquidity conditions

The main drivers of the excess cash (2)

Overnight deposits (yoy % change)

Customer funding at Italian banks(yoy % change) (*)

Note: data referred to the liabilities of Italian MFIs towards Euro zone residents.Source: ECB.

-12-9-6-30369

12151821

Jul11 Jul12 Jul13 Jul14 Jul15 Jul16 Jul17

Overnight depositsof which: Non-financial companiesof which: Households

Note: excluding deposits with central counterparties and bonds purchased by Italian MFIs. Deposits and total funding exclude liabilities related to loans sold and not cancelled.Source: Bank of Italy, Intesa Sanpaolo.

-20

-16

-12

-8

-4

0

4

8

May13 May14 May15 May16 May17

Customer funding (*)Deposits (net of central counterparties)Bonds (net of bank bonds held by Italian MFIs)

3

TLTROs: a still cheap liability , in the process of being deployed

The main drivers of the excess cash (3)

4

A clear uptrend for householdsA blurred picture for NFCs

The main drivers of the excess cash (4)

-6

-4

-2

0

2

4

6

Jun11 Jun12 Jun13 Jun14 Jun15 Jun16 Jun17

Households

Non-financial corporations

Private sector

Loans to the private sector resident in Italy (Data adjusted for securitisations and net of central

counterparties, yoy % change)

Source: ECB, Bloomberg, Intesa Sanpaolo.

Loans to non-financial businesses by duration (Data referring to Italian bank customers residing in the Euro area, yoy % change)

-10

-8

-6

-4

-2

0

2

4

6

8

10

Jul11 Jul12 Jul13 Jul14 Jul15 Jul16

Up to 1 year

Over 1 year

Total loans

5

The somewhat bumpy but steady road towards lower domestic debt holdings.

The search for safe and remunerative alternatives…a mission impossible ? (1)

4%

9%

14%

19%

24%

29%

01/07 01/09 01/11 01/13 01/15 01/17

Debt securities % Total assetsGen Govt securities %Total assets

0

100

200

300

400

500

600

09/00 09/03 09/06 09/09 09/12 09/15

MFIs Domestic resident - non MFI

Source: ECB, Bloomberg, Intesa Sanpaolo.

Italian MFIs: holdings of debt securities issued by domestic residents (EUR billion)

Italian MFIs: holdings of debt securities (% of assets)

6

The somewhat bumpy but steady road towards lower domestic debt holdings.

The search for safe and remunerative alternatives…a mission impossible ? (2)

7

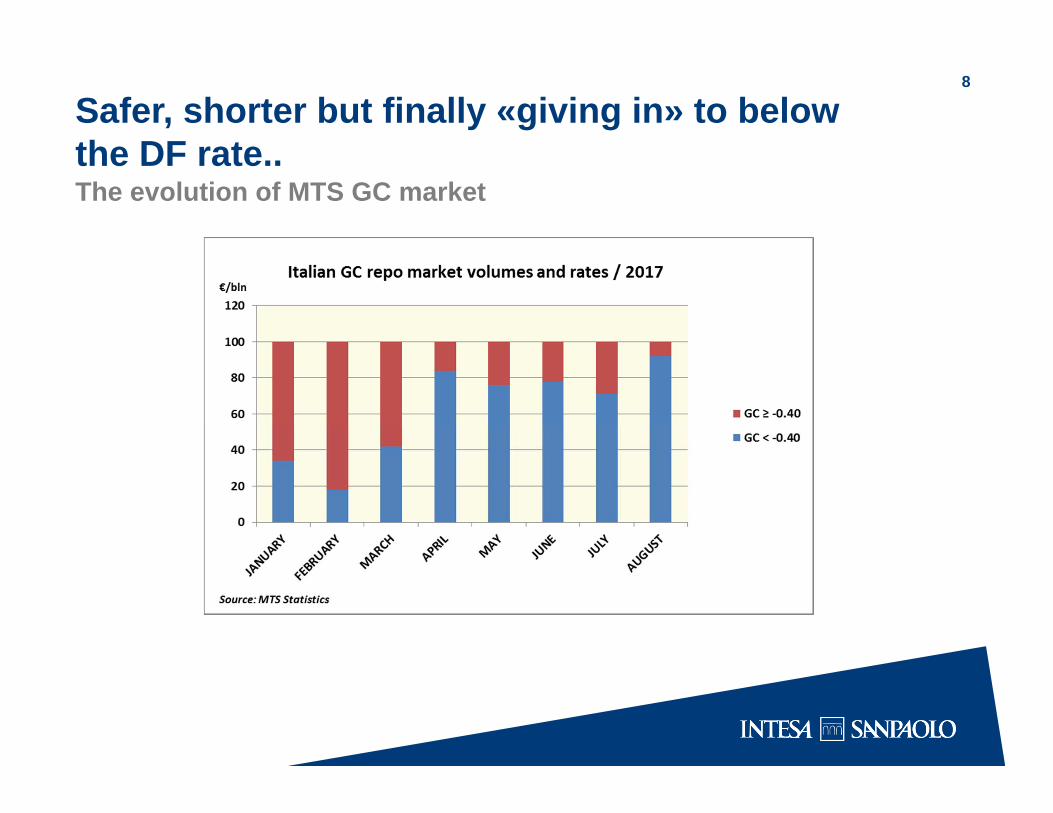

The evolution of MTS GC market

Safer, shorter but finally «giving in» to below the DF rate..

8

The evolution of MTS GC market

Safer, shorter but finally «giving in» to below the DF rate..

9

Summing-up: the unavoidable consequences of the surplus liquidity moving south..

10

Summing-up: .. with one notable «silver lining».

Target 2 imbalances partially in retreat

11

Implications for liquidity metrics- Stable deposits (Retail and SMEs):a funding source on which most banks have

historically relied upon, even more since the onset of the gov. crisis (2011). They still entail a nice cost/benefits trade-off, despite their IR floored at zero (90/95% ASF; 5% LCR runoff)

- Corporate deposits: less appealing (50% ASF-40% LCR o/flows) and bound to create noise for intraday liquidity management

- Central Bank Reserves: so well above the mandatory levels, they’re heavily compressing all intraday metrics , from «Available Liquidity at the start of the business day» to «Intraday Liquidity usage ratio»

- TLTROs will start maturing from mid-2020 (139 bn/eur the take-up of IT banks in TLTRO2/1 and 67 bn/eur in TLTRO2/4) and their attractiveness is easily explained by their rate and by the low-quality of the collateral pledged

- Portfolio diversification is fostering/intensifying the access to different repo markets , alleviating concerns of excessive concentration (a «plus» for intraday Liq. Mgmt)

- Risk Factors:- The proven stickiness of retail depos may be challenged by the «hunt for

fees/commissions»;- The reliance on TLTROs will have to be carefully assessed and factored

into the next strategic plans

12

Conclusions- The persistence of negative rates and the impossibility for banks to charge

negative rates on retail deposits are representing a big hurdle for MFIs, now even in the periphery

- Memories of the 2011 nasty developments, the risk of political instability next year and the perceived vulnerability of some parts of the Italian banking industry may represent factors justifying risk-aversion…

- ...but household disposable income and spending are at 5-year high, business confidence at 10-year high and residential real estate transactions continue to rise unabated since 2015 (prices of existing homes are stabilising)

- In this environment, net borrowers are benefiting at the detriment of net savers who are «trapped» into the zero- interest rate landscape

- Domestic banks are changing their business models, albeit gradually:

- a big switch from «direct deposits» into AuM is ongoing and is generating a sizeable growth in commissions;

- TLTROs still bear a good cost-opportunity trade-off;

- Fixed-income portfolio diversification has become a priority both in terms of countries and asset classes.