italian matrix fdi in egypt and libya, a risk analysis in an historical perspective

DESCRIPTION

This essay will deal with a comparison of two countries’ risk analysis as they would be made by an Italian company that is considering to operate in those markets. I chose to refer to Egypt and Libya, in the period 1990-2010, before the Arab uprisings of 2011: they were both ruled by authoritarian regimes, not having fully implemented a process of economic modernization, both close neighbours for Italy, and they both had the potential to be profitable destination for investments. However, many key internal dynamics were different, as well as external factors: all those factors led to a completely different level of opening towards foreigners, as reinforced by the different kind of relations of those countries with the European Union. My argument will be that the main factor in creating a good business environment stays the political will of the government in charge to liberalize and modernize the political as well as the economic environment. The EU intervention, in the form of intra-regional policies and specifically with the Association Agreement in 2001, indeed facilitated the modernization of Egypt, both politically and economically, nonetheless, the level of risks to be faced by an Italian company in the country is still high. Egypt is still underdeveloped: the differences in term of economic outcomes with Libya are still too few, especially if looking at data from a comprehensive perspective (e.g. size of the markets). Libya provides even more serious hindrances, partly because of the aggravating circumstances of having had pariah status until 2004. The essay will assess what particular political and economic risks are taken into consideration the most by Italian companies, after having presented an overview about the whole region from both perspectives. My conclusions will reinforce the starting point of this essay: Egypt and Libya, though very different in nature, still present a very high level of risk whose causes can be identified primarily in the lack of political will of the previous regimes to liberalize the economy and also the lack of governance capability in implementing effective reforms, necessaries to have a more adequate share in the global market. However, these shortcomings are typical of a process of state building which is partially still in fieri, and this is ascribable to the overall condition of the national institutions and also to some historical factors.TRANSCRIPT

1

Italian matrix FDI in Egypt and Libya, a risk analysis in an historical perspective.

Cinzia Bianco

Postagraduate student in “Middle East and Mediterranean Studies”

King’s College London.

February, the 6th 2012.

London.

2

1 INTRODUCTION

This essay will deal with a comparison of two countries’ risk analysis as they would be made by an Italian

company that is considering to operate in those markets. I chose to refer to Egypt and Libya, in the period 1990-2010,

before the Arab uprisings of 2011: they were both ruled by authoritarian regimes, not having fully implemented a

process of economic modernization, both close neighbours for Italy, and they both had the potential to be profitable

destination for investments. However, many key internal dynamics were different, as well as external factors: all those

factors led to a completely different level of opening towards foreigners, as reinforced by the different kind of

relations of those countries with the European Union.

My argument will be that the main factor in creating a good business environment stays the political will of

the government in charge to liberalize and modernize the political as well as the economic environment. The EU

intervention, in the form of intra-regional policies and specifically with the Association Agreement in 2001, indeed

facilitated the modernization of Egypt, both politically and economically, nonetheless, the level of risks to be faced by

an Italian company in the country is still high. Egypt is still underdeveloped: the differences in term of economic

outcomes with Libya are still too few, especially if looking at data from a comprehensive perspective (e.g. size of the

markets). Libya provides even more serious hindrances, partly because of the aggravating circumstances of having had

pariah status until 2004.

The essay will assess what particular political and economic risks are taken into consideration the most by

Italian companies, after having presented an overview about the whole region from both perspectives. My

conclusions will reinforce the starting point of this essay: Egypt and Libya, though very different in nature, still present

a very high level of risk whose causes can be identified primarily in the lack of political will of the previous regimes to

liberalize the economy and also the lack of governance capability in implementing effective reforms, necessaries to

have a more adequate share in the global market. However, these shortcomings are typical of a process of state

building which is partially still in fieri, and this is ascribable to the overall condition of the national institutions and also

to some historical factors.

2 INTERNAZIONALIZATION IN THE MENA MARKET.

This paragraph presents the amount of Foreign Direct Investment addressed to the MENA region1 in the

period taken into consideration (1990-2010).

Foreign direct investment (FDI) is defined2 as a company’s investment of assets in a foreign country, which is

usually consistent and requires a durable commitment. It provides capital, technology, management and know-how to

the host country. Internationalizing some or all of a company’s operations is clearly included in the definition.

FDI is mostly directed to developed countries, but according to UNCTAD3 the share of FDI inflows to

developing countries has increased to its highest level since 1997. Nonetheless, and despite its size with

approximately 6 percent of the world population, and 2 percent of the global income ($1,198 billion)4, MENA region

seems to have difficulties in attracting foreign investors. The situation of the region’s FDI inflows in the last twenty

years has followed an unsteadily path. For instance, the inward FDI to the MENA region counted for $1.959 millions in

1990, increased substantially in 1997, following a global tendency and attesting itself at $6.942 millions, just to lower

again in 1999. The trend started changing in the 2000s, doubling its value each two years, from $12.601 in 2001 to

1 For the purpose of this study, the countries included as MENA region are: Algeria, Bahrain, Egypt, Iran, Jordan, Kuwait, Lebanon, Libya, Morocco, Oman, Qatar, Saudi Arabia, Sudan, Syria, Tunisia, Turkey, United Arab Emirates (UAE) and Yemen. 2 See Charles W. L. Hill (2008) “Global Business Today”, 5/e, McGraw-Hill, Washington DC.

3 UNCTAD, (2005). World Investment Report. Geneva: United Nations Conference on Trade and Development

4 World Bank. 2007. World Development Indicators. Washington, DC: The World Bank.

3

$56.734 in 2005, hitting a peak in 2008, when the FDI inward flows in the region counted for $115.609 millions5. Then,

the following two years the value lowered again, as a cause of the global financial crisis .

Nonetheless, the Inward FDI Performance Index prepared by UNCTAD, shows that the MENA region is far

behind other developing regions in receiving FDI inflows, attracting an average of the 2% of the global FDI.

Furthermore, much of this investment volume goes to the oil & gas sector, and is unevenly distributed in the different

countries, being concentrated in a few countries such as Saudi Arabia, Egypt, Tunisia, Bahrain, and Morocco Turkey,

UAE. The least recipients instead include Libya, Kuwait, and Yemen.

2.1 Political challenges of the MENA market.

It is paramount in my opinion to have a broad idea of the region which is a unique combination of sharp

differences and core shared features. There are two perceived dimensions of political risks: the international and the

domestic level.

MENA countries, with regard to their International Relations, can be grouped in three categories: a) Strong

US allies, such as the Gulf Cooperation Council countries and Israel, followed by the less engaged Jordan, Mubarak’s

Egypt and Iraq after 2005. b) Rogue States or Fundamentalist cells: Syria, Iran and Islamist Militant Parties. Also Libya

(especially before 2004), Saddam Hussein’s Iraq, and to some extents Yemen. c) European Neighbours: states that

have been trying in the last decade to maintain good relations with the West and in particular with the EU. They are

the countries of Maghreb, Jordan, Lebanon, Occupied Palestinian Territories, Turkey. Syria and Libya are formally

included in the ENP, but the negotiations with Libya only started in 2008 and were interrupted in 2011, whereas the

partnership with Syria is very weak. It is easy to assess the influence of these relations, when looking back at the

classification of the top and least FDI recipients. The countries on the top are those that have a better political

relationship with the United States, the major investors into the region; whereas amongst the least recipients there is

Libya, a pariah state until 2004. The major concern related to the international political environment though, is the

security threat. Dating back to the decolonization period, MENA has been affected by a quasi perpetual state of

troubles. In the period hence taken into account, 1990-2010, several kinds of conflicts occurred. Civil wars, partly

correlated to the ethnic and historical artificiality of the states: political unrests spiraled out of control particularly in

Yemen (1994, 2004, 2009) and Lebanon (2005, 2008). External attacks, where the most explicative case is Iraq

(catalyst of violence in 1991, 1998, 2003), and regional wars whose protagonist was often Israel (e.g. Second Lebanon

War in 2006). Terrorism, pursued by various terroristic cells such as Hamas, Hezbollah, Al-Qaeda, Al-Gama’a al-

Islamiyya, Egyptian Islamic Jihad, the Salafist Group for Preaching and Combat hit in several countries, within the

region and abroad. This last menace in particular has been a plight that stained the region with blood each and every

year in the last two decades, hitting civil as well as military targets and killing Arabs as well as foreigners. Therefore, it

is hard to dismantle the perception of the MENA as dangerous (lacking rule of law) and hostile to foreigners, mainly to

Western companies.

This perception is somehow confirmed at a domestic level, where cases of expropriation, nationalization and

forced liquidation have been witnessed6, due to the lack of a clear differentiation between public and private sector

that, at different levels, causes a high level of political interference into the economy. As Onyewu7 points out,

corruption, a too intricate bureaucracy, the lack of democracy and transparency, inefficiency of institutions (that are

usually unaccountable) a low level of privatization and liberalization significantly affect the decision of a company to

5 Data taken from “World Investment Report 2010” UNCTAD, FDI/TNC database (www.unctad.org/fdistatistics), Annex Table: FDI inflows, by region

and economy (1990-2010).

6 Mishrif, A. (2010)“ Investing in the Middle East”, London

7 Onyeiwu, S. (2000). Foreign Direct Investment, Capital Outflows and Economic Development in the Arab World. Journal of Development and

Economic Policies, Vol.2 (2), 27-57.

4

run a business in the region. All major International Organizations, including World Bank and Transparency

International (in its Corruption Perception Index) suggests that the level of corruption in MENA countries is relatively

high and transparency relatively low8. The result is a high level of suspicion on investors’ side that are concerned with

the market being unfairly competitive and the rule of law not transparent enough and volatile.

2.2 Economic challenges of the MENA market.

In this section, I will try to identify some of the economic reasons that lie at the heart of the lack of a

significant amount of investment flows to the MENA region, despite its comparative advantages.

Factors usually taken into consideration are: rate of return on investment, openness of the economy,

(including tariff barriers, and freedom of movement of capitals), fiscal policies, macroeconomic fundamentals such as

GDP, growth rate, external debt, inflation. The literature about the significance of these determinants is divided. The

lack of trade openness and underdeveloped physical infrastructure, especially transportation, are identified by

Kozlova and Smajlovic9 as significant determinants in the failure to attract FDI flows. In facts, the MENA region

maintains high tariffs, the regional average being 13% in 2006, and also high non-tariff barriers, such as special

charges and double taxation, that are mainly restrictions to intra-Arab trade10. Their findings are consistent with other

literature related to the determinants of FDI in the MENA region, as Onyeiwu11or Elfakhani and Matar12. Onyeiwu

argues that macroeconomic variables are not really significant in the MENA region: he states that this could be due to

the specific nature of investments which is mainly resource-seeking rather than market-seeking. The bulk of the FDI

inflows is indeed directed in oil & gas related activities. His findings seem to be endorsed by the World Investment

Report13 that identifies among the key factors for the sharp increase of FDI inflows, the improvement of

infrastructures, liberalization of the FDI regulatory regimes, incentives to foreign investment and improvement of

privatization programs by many countries in the region from the end of the 1990s. Furthermore, according to a

research made by Heritage Foundation14, the people of that region have the lowest level of overall economic freedom

compared to other regions: parameters taken into account were the opaqueness and ad hoc nature of some

privatization processes and restrictions on property rights. As with regards to the financial market, it results

underdeveloped and, being overwhelmingly of public ownership, exposed to government debt, fragmented, weakly

regulated and presenting partially flexible but still inappropriate exchange rates. One reason for that could be the

scarcity of technological resources that also contributes, together with an obsolete educational system, to the lack of

a skilled workforce, thus partly neutralizing one of the MENA’s comparative advantage: cheap labour force. Kamaly15,

in his study, points out that slow economic growth and the very low purchasing power were the only significant

determinants of FDI flows to the MENA region. These limits could still be overcome through the enlargement of the

single country’s market through free trade agreements (FTAs) or the creation Free Zones (FZs), to turn a country into a

hub from where to expand one firm’s business into a multinational market. Unfortunately, regional agreements for

8 In the 2003 CPI only Israel, Oman, Bahrain, Cyprus, Qatar, Kuwait, and Saudi Arabia can be said to be fairly transparent, having achieved a CPI

score of 5.0 and above. Most MENA countries achieved a score of 3.4 or less. A CPI score of 10.0 represents “Highly Clean” and 0 indicates “Highly Corrupt.” 9 Marina Kozlova, Lejla Smajlovic, June 2008 “Location-Specific Determinants of FDI: the case of the Middle East and North Africa countries”

INTERNATIONELLA HANDELSHÖGSKOLAN, HÖGSKOLAN I JÖNKÖPING

10 Devlin, Julia C. (2010) “Challenges of Economic Development in the Middle East and North Africa region”,World Scientific Stud ies in International

Economics, Volume n°8, p.291.

11 Onyeiwu, S. (2000). Foreign Direct Investment, Capital Outflows and Economic Development in the Arab World. Journal of Development and

Economic Policies, Vol.2 (2), 27-57.

12 ELFAKHANI, S.M. and. MATAR, L.M. (2007) 'Foreign direct investment in the Middle East and North Africa region, Journal for Global Business

Advancement, Volume 1, Issue 1, pg 49-70, 13

UNCTAD (2005), ibid.

14 Roberts, J.M. and Kim, A.B. (2008). Economic Freedom in Five Regions. In P. A. Gigot (Ed.), Index of Economic Freedom. Heritage Foundation.

15 Kamaly, A. (2002) “Essays on FDI Flows to Developing Countries” PhD Dissertation, Department of Economics, University of Maryland at College

Park.

5

free trade didn’t succeed, whereas the European Union initiatives for partnership succeeded only partially, having

been hindered by political consideration and commodities constrains.

3 COMPARATIVE STUDY CASES: Italian business in Libya and Egypt

There are 103 Italian-Egyptian joint ventures in Egypt, 67 of which are controlled by an Italian company

against the 9 Italian-Libyan joint ventures of which 6 are directly controlled by Italians16. The first observation to be

made with regards to these data is the striking difference between the Italian presence in Egypt and in Libya. This

difference is due to a number of factors that I will hence highlight. Moreover, if we take into account that the Italian

businesses operating in Hong Kong are 333, it’s clear how little these numbers are. The scarcity is significantly

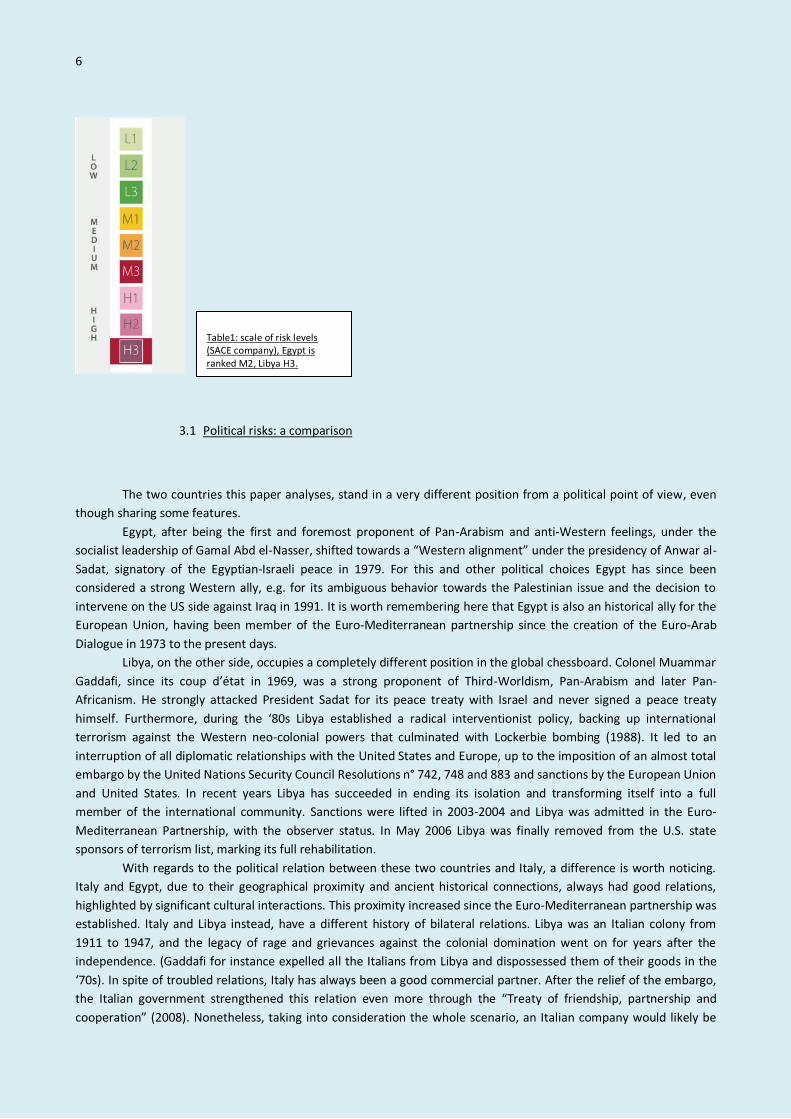

interwoven to the evaluation, by Italian companies, of an high degree of risk in the countries. This is confirmed by the

most important company of capital insurance services in Italy, SACE, who categorized Egypt as a Medium and Libya as

a High risk country (refer to Table 1 for a visual categorization of risk levels by SACE, ranking from Low-1 to High-3).

For what concerns Egypt, the bigger opportunities for Italian companies17 are in industrial supplies, semi-

manufactured products, services (e.g. tourism), energy sector, chemical industry. Resource availability and low

production costs makes it a destination for delocalization and import-substitution industry. Libyan economy instead

results dependent on oil, counting for the 45% of its exports, whereby agriculture and industry count for 5-10% and

the rest is made by tertiary sector. National Oil Corporation lawfully has to own at least 50% of each oilfield, but

Italian ENI managed to have a significant market share in oil & gas field. The richness of resources guaranteed to the

Libya population, which is definitely smaller than the one of Egypt, a good living standard. Nonetheless, the country

exports more than imports, thus Italian companies were unable to penetrate the market, especially in consumer

goods and the “Made in Italy”.

A feature shared by both countries is that the Italian presence is mainly connected to very large groups, such

as ENI, Intesa San Paolo, Olivetti, IVECO, whereas Italian economy is dominated by Small and Medium Enterprises.

Those SMEs are more keen to invest were risks are very low, as they couldn’t survive in troubled waters. Furthermore,

their concerns are worsened by cultural stereotypes and outdated conceptions, which are hard to dismantle at a

grassroot level18

. These elements has to be taken into consideration together with the ones presented in the following

paragraphs to explain why the Italian presence is so scarce.

16

Data taken from the “Istituto nazionale per il Commercio Estero” data bank: REPRINT-Politecnico di Milano-ICE. Last data update, 1.1. 2009.

17 As identified by the Italian-Arab Chamber of Commerce in its “Profili paese della Camera di Commercio Italo-Araba: Egitto”, April 2008.

18 For a comprehensive analysis of the effect of cultural stereotypes on business see: Tekin-Koru, A. (2007) “Unexplained Differences in the FDI

Receipts of Middle East and North Africa”, Oregon State University.

6

3.1 Political risks: a comparison

The two countries this paper analyses, stand in a very different position from a political point of view, even

though sharing some features.

Egypt, after being the first and foremost proponent of Pan-Arabism and anti-Western feelings, under the

socialist leadership of Gamal Abd el-Nasser, shifted towards a “Western alignment” under the presidency of Anwar al-

Sadat, signatory of the Egyptian-Israeli peace in 1979. For this and other political choices Egypt has since been

considered a strong Western ally, e.g. for its ambiguous behavior towards the Palestinian issue and the decision to

intervene on the US side against Iraq in 1991. It is worth remembering here that Egypt is also an historical ally for the

European Union, having been member of the Euro-Mediterranean partnership since the creation of the Euro-Arab

Dialogue in 1973 to the present days.

Libya, on the other side, occupies a completely different position in the global chessboard. Colonel Muammar

Gaddafi, since its coup d’état in 1969, was a strong proponent of Third-Worldism, Pan-Arabism and later Pan-

Africanism. He strongly attacked President Sadat for its peace treaty with Israel and never signed a peace treaty

himself. Furthermore, during the ‘80s Libya established a radical interventionist policy, backing up international

terrorism against the Western neo-colonial powers that culminated with Lockerbie bombing (1988). It led to an

interruption of all diplomatic relationships with the United States and Europe, up to the imposition of an almost total

embargo by the United Nations Security Council Resolutions n° 742, 748 and 883 and sanctions by the European Union

and United States. In recent years Libya has succeeded in ending its isolation and transforming itself into a full

member of the international community. Sanctions were lifted in 2003-2004 and Libya was admitted in the Euro-

Mediterranean Partnership, with the observer status. In May 2006 Libya was finally removed from the U.S. state

sponsors of terrorism list, marking its full rehabilitation.

With regards to the political relation between these two countries and Italy, a difference is worth noticing.

Italy and Egypt, due to their geographical proximity and ancient historical connections, always had good relations,

highlighted by significant cultural interactions. This proximity increased since the Euro-Mediterranean partnership was

established. Italy and Libya instead, have a different history of bilateral relations. Libya was an Italian colony from

1911 to 1947, and the legacy of rage and grievances against the colonial domination went on for years after the

independence. (Gaddafi for instance expelled all the Italians from Libya and dispossessed them of their goods in the

‘70s). In spite of troubled relations, Italy has always been a good commercial partner. After the relief of the embargo,

the Italian government strengthened this relation even more through the “Treaty of friendship, partnership and

cooperation” (2008). Nonetheless, taking into consideration the whole scenario, an Italian company would likely be

Table1: scale of risk levels (SACE company), Egypt is ranked M2, Libya H3.

7

more comfortable to establish a business in Egypt than in Libya, because Italy, in the globalization era, can’t prescind

from the regional Euro-Mediterranean context, neither from the wider global perspective, in both of which Libya has

too long acted as a state supporting terrorism, being hostile to the US, Israel and his Arab neighbours (especially Saudi

Arabia). Furthermore, at a grassroot level, the environment for foreigners, especially former colonial rulers, is

perceived not to be welcoming19.

On a domestic level as well, there are various dimensions to take into account when looking at Egyptian and

Libyan political systems. Both of the leaders established authoritarian regimes. Both leaders were faced with the

necessity to open up their political system towards a façade of liberalization, for economic and pragmatic reasons.

Nonetheless they acted as defensive modernizers, operating a controlled opening, so as to reconciliate change on

rational economic ground with political rationality, e.g. the imperative for retaining power. Anyhow, Egypt started its

process of modernization and liberalization already in the ‘70s, whereas Libya has started only less than 10 years ago

Hosni Mubarak was appointed President after the assassination of Anwar el-Sadat, and run the country in a

system of single party until 2005, when the first multi-parties elections were held. However, the electoral law made it

extremely difficult to present candidacies, favouring very much the re-election of Mubarak. The turnout was indeed

only of 23% of voters and there were allegations of gerrymandering, coercion and vote buying of the ruling party’s

side. Mubarak’s regime was born out of the 1952 Free Officiers military coup d’état, and still retained the legacy of a

repressive military regime and of the British colonization. To gain its legitimacy, the regime made a widespread use of

clientelism, especially in the rural areas, suppressed freedom of speech, and maintained a strong control over

economy, media, society, religion, thus guarantying a very large personal power to the President20. Freedom House

declared in its 2007 Annual Report that the regime “routinely violates its citizens’ civil and political rights, including

freedoms of assembly and association, as well as the right to participate in the political process as a candidate or

elector. Torture and arbitrary detentions are not uncommon.” 21 It translated into, among other things: an intricate

bureaucracy, the prominent role of military and security police, a very scarce transparency, reluctance towards

modernization and privatization, the use of judiciary and legislation as a tool to prevent pluralism. Repression caused,

in turn, the expression of opposition through violence (Egypt witnessed 14 terroristic attacks in the period 1992-2005,

the most severe being the Luxor massacre, against a touristic resort in 1997). Security, therefore, is still an issue,

especially in Upper Egypt.

Muammar Gaddafi, on the other side, gained power by a military coup d’état in 1969 on a strong

idiosyncratic ideological basis made of populism, Arabism and Islam. The most radical turning point occurred in 1973

with the arrest of thousands of opponents among communists, the Muslim Brotherhood and Ba’athist and the

formation of Basic People’s Congresses, local institutions that is supposed to express the popular will. Actually, these

Congresses have no influence on the decision-making process and Gaddafi and his entourage are the real

powerbrokers in the country. He was indeed able to manipulate informal power networks, a complex hierarchy of

security structures and the country’s tribal alliances, relying heavily on his relatives. According to Freedom House22,

civil rights are not guaranteed: there is not effective protection against arbitrary arrests, torture is still employed in

some cases by the security services (even if in 2006 Saif al-Gaddafi publicly blamed the use of torture) and protests are

crushed with force. In 2004 the regime introduced a new electoral system that, it claimed, would increase

transparency. Nonetheless no effective mechanisms were used to prevent those with economic privilege from

exerting influence on the voting process. Libya legislated against public sector corruption and control institutions were

created, but there was no significant initiatives in deeds to curb corruption. Citizens do not have the legal right to

access government information, and basic statistical data had been made available only recently. Even if some

19

Di Ernesto, F. (2010) “Petrolio, cammelli e finanza. Cent’anni di storia e di affari tra Italia e Libia”, Fuoco Edizioni, Roma.

20 Owen, R. (2000) “State Power and Politics in the Making of the Modern Middle East”, London: Routledge.

21 Freedom House 2007 annual report “Countries at a Crossroad”, consultable at:

http://freedomhouse.org/template.cfm?page=140&edition=8&ccrpage=37&ccrcountry=154

22 Freedom House 2007 annual report “Countries at a Crossroad”, consultable at:

http://freedomhouse.org/template.cfm?page=140&edition=8&ccrpage=37&ccrcountry=154

8

progresses were made in 2006, the judicial system is deeply intertwined with politics so the right of a just process is

not guaranteed.

3.2 Economic risks: a comparison

Bearing in mind what previously said about the whole MENA region, this paragraph will try to expound the

single countries’ peculiarities.

With the purpose of incrementing investments, Egypt has adopted a liberal legislation23 removing restrictions

to foreign investments in a bunch of sectors. A project has to be presented to the Investment and Free Zones

Authority, that has no authority in the evaluation of it and is responsible for all bureaucratic matters, including access

to incentives. There are no formal restrictions to capital flows. Procedures should take one working day, but

administrative delays are common as well as a lack of transparency. Investments in protected sectors are subject to

more controls and restrictions. Foreign ownership is guaranteed at 100%24, but foreigners are not allowed to engage

in commercial activities or public auctions (in which Egyptian companies are privileged) without a local agent. Law

8/1997 also protects investments against nationalization or expropriation made without legal reasons or public

interest, in absence of an appropriate compensation. Investors can also own estates and are free in the management

of their businesses. In addition to these national laws, there is a specific BIT stipulated between Italy and Egypt to

protect and promote investments (1990), parallel to the Treaty of Benghazi signed by Italy and Libya in 2008, that also

offers interesting opportunities to Italian enterprises, but in fewer sectors. Libyan law encouraging investments is the

Law on Investment Promotion n.9 (2010). It is a significant step towards liberalization, even if it only applies to sectors

considered beneficial to the development of the country. Incentives to investments include: exemption from custom

duties, service charges and import fees especially for production assets and supplies, free export of the products,

simplification of commercial bureaucracy, a 5 year period of income tax exemption, the freedom to repatriate the

capital. On major innovation is the explicit guarantee against arbitrary nationalization or expropriation. Despite the

clear convenience of these articles, there are still constrains to investments: Libyan Foreign Investment Board and

especially the Secretary have the power to evaluate every phase of the project that, in order to be approved, has to

bring tangible benefits to the country, according to a logic that still suffers from the legacy of a planned economy.

Furthermore, the norm is subject to interpretation and the investor’s freedom of action limited by the necessity to

work in partnership with the locals, to get through the intricate bureaucracy, and also to comply with the law n° 443

(2006) that obliges all foreign companies to operate in joint venture with local companies. This whole legal frame

work requires long operative times and a feeling of uncertainty towards a significant interference of politics into

private businesses.

Operating in a foreign country, a company is directly affected by the host country’s import-export policy. In

Egypt25, import restrictions are applied to very few commodities (e.g. restrictions on textile sector have been lifted in

2002) but custom clearance is still slow and unpredictable, especially when goods have to go through inspections or

technical control, whose number highly increased recently. Custom duties, on the other hand, have been lowered to a

reasonable level (6.9 %) in many sectors, whereas others are still protected by high tariffs (e.g. textiles or cars).

Custom norms have been recently updated also in Libya26 aiming at a simplification of procedures and a limitation on

the discretionary power of the Authorities in which tariff to apply (the range is between 4% and 10%). Anyway, it is

23

Law 8/1997 and Decree 740/2000

25 Data on Egyptian import-export policy are taken from “Profili paese della Camera di Commercio Italo-Araba: Egitto”, April 2008. Camera di

Commercio Italo-Araba, Rome. 26

Law n°10 (2010)

9

not allowed to import in Libya around 30 kinds of commodities, partly for religious, partly for protectionist reasons.

For what concerns Italian imports, the Benghazi Treaty erased some discriminatory policies, that previously

subordinated Italian companies to the Prime Minister’s as well as to the Minister of Economy’s clearance. The import

of some “protected” commodities is reserved to the Libyan Al Inma for Service Investment Holding Company.

Another significant factor for an Italian company operating abroad is the chance to turn the host country into

a hub to gain access to a larger market. Egypt is member of COMESA (Common market for Southern and Eastern

Africa), that should establish a common market in 2014. Mubarak also signed the Association Agreement, that gives

the country full access to the EU market. In 2004 Egypt established three Qualified Industrial Zones (Qiz), to freely

export in the United States a product that has at least one Israeli component. It is also member of the Agadir

Agreement, that aimed at establishing a free trade area among Egypt, Tunisia, Morocco and Jordan. Both Egypt and

Libya are members of the Greater Arab Free Trade Area (GAFTA), which, unfortunately, has not yet accomplished its

purposes, due to technical constrains and political clashes among members. On the other hand Libya is also making

efforts to enlarge its market, by signing the Trade and Investment Framework Agreement with the US, joining

COMESA, negotiating a more comprehensive membership in the Euro-Med Partnership and establishing the first two

Free Trade Zones.27

Nonetheless, at this regard, Libya has narrower perspectives, also because of its far lower

integration in the International Community.

Another significant element for foreign companies, is the level of fairness in competition, fully guaranteed

only by a market economy. Privatization is thus an issue. Privatizations in Egypt formally started in 1991, and reached

an acceptable level, but the process is still unfinished and slow, as confirmed by the stalemate in the privatization of

Banque du Cairo. Some major industries haven’t been touched by privatization, such as Suez Canal Co (transits though

the Suez Canal are a major sources of revenues for the State), Egyptair, General Petroleum Co. Privatization were

undertaken also due to the high public deficit (-8% of GDP) or the higher public debt (at 81.4% of GDP in 2008)28. On

the other hand, Libya has been really reluctant towards privatization, not only for ideological reasons but also due to

its macroeconomic fundamentals: in 2010 public debt was at 3.5% of GDP, whereas the public budget in surplus of

4.4%29. In 2002 Saif Gaddafi announced a wave of modernizing reforms and privatizations, that would have touched

infrastructures, telecommunications, finance and transportations. Little moved, also because of the scarce interest of

investors. Lately, the country shifted more decisively to open its economy to the private sector, to diversify its

economy and render it less dependent on import, in particular in the food commodities. Anyway, particularly in this

respect, Egypt is far more advanced than Libya, having started the process of privatization much longer before.

27

Laws n° 215 and n° 32 (2006). 28

Data taken from the CIA World Factbook, 2010. 29

Data taken from CIA World Factbook, 2010.

10

4 CONCLUSIONS

Having made a comparison between the political and economic situation in Egypt and Libya, these

conclusions evaluate the present risks for an Italian business to operate in those markets as still considerably high. The

primary causes for that are represented not only by the lack of governance capability of the former governments, but

also by muddled political and economic regional and domestic scenarios.

The domestic political environment of these countries present severe challenges for an Italian company to set

up its business. The lack of political accountability and the high degree of corruption and bribery do not set the basis

for a fair competition in business. An absolutely intricate bureaucratic system, functional to opaque manoeuvres,

makes the process of establishing the business definitely too slow for the tempo of the globalization era.

Middle Eastern economic policies seem still partly anchored to their mistrust towards Western company: the

fear that economic colonization would be the next means to political lobbying. Furthermore, they also are resentful of

a state-assisted economy.

For these reason, only an abrupt political change could offer the chance to cease being stuck into dynamics of

the past, and to implement reforms that would boost the economic relations between their countries and Italy, as

well as others. The European Union should try harder to conciliate economic and trade agreements with an emphasis

on the necessity to create political conditions that would enable European companies to contribute, in a profitable

way, further to the development of the Middle East.

Cinzia Bianco

Postgraduate Student in Middle East and Mediterranean Studies

King’s College London.

11

5.0 REFERENCES

BIBLIOGRAPHY:

Abed, G. & Davoodi H. (2003), Challenges of Growth and Globalization in the Middle East and North Africa, Washington D.C.: International Monetary Fund.

Backer, Arno (2005) The impact of the Barcelona process on trade and foreign direct investment, paper presented at

the conference of Middle Eastern and North African Economies: Past Perspectives and Future Challenges, Brussels, 2-4

June 2005

Charles W. L. Hill (2008) “Global Business Today”, 5/e, McGraw-Hill, Washington DC

Devlin, Julia C. (2010) “Challenges of Economic Development in the Middle East and North Africa region”,World Scientific Studies in International Economics, Volume n°8.

Di Ernesto, F. (2010) “Petrolio, cammelli e finanza. Cent’anni di storia e di affari tra Italia e Libia”, Fuoco Edizioni, Roma.

“Egitto”, RAPPORTI PAESE CONGIUNTI, (2010) Ministero Affari Esteri e Istituto nazionale per il Commercio Estero.

Ehteshami, A. (2007), Globalization and geopolitics in the Middle East: old games, new rules, London:Routledge

ELFAKHANI, S.M. and. MATAR, L.M. (2007) 'Foreign direct investment in the Middle East and North Africa region,

Journal for Global Business Advancement, Volume 1, Issue 1, pg 49-70

Henry C. & Springborg R. (2010) Globalization and the Politics of Development in the Middle East, Cambridge

University Press

Kamaly, A. (2002) “Essays on FDI Flows to Developing Countries” PhD Dissertation, Department of Economics,

University of Maryland at College Park.

Kuran T.(2004) “Why the Middle East is economically underdeveloped: historical mechanisms of institutional

stagnation” The Journal of Economic Perspective Vol 18, N°3

“Libia”, RAPPORTI PAESE CONGIUNTI, (2010) Ministero Affari Esteri e Istituto nazionale per il Commercio Estero.

Marina Kozlova, Lejla Smajlovic, June 2008 “Location-Specific Determinants of FDI: the case of the Middle East and North Africa countries” INTERNATIONELLA HANDELSHÖGSKOLAN, HÖGSKOLAN I JÖNKÖPING

Miller, R. and Mishrif A. (2005), “The Barcelona Process and Euro-Arab Economic Relations: 1995-2005” Middle East

Review of International Affairs, Vol.9, N°2

Mishrif, A. (2010) Investing in the Middle East: the Political Economy of European Direct Investment in Egypt, London:

Tauris Academic Studies

Onyeiwu, S. (2000). Foreign Direct Investment, Capital Outflows and Economic Development in the Arab World.

Journal of Development and Economic Policies, Vol.2 (2), 27-57.

Paesi Arabi-notizie economiche e commerciali, October 2011 – Year XII –N° 238, Published by Camera di commercio italo-araba.

Russo Paola, Policies for Business in the Mediterranean Countries: GREAT ARAB POPULAR SOCIALIST LYBIAN

JAMAHYRIA, C.A.I.MED. Pubblication

12

Soliman Armany (2011) “The Euro Med Partnership and the Arab Israeli Conflict”, The Atkin Paper Series, ICRS

Trotta, E. (2006), Guida Paese: Libia, Roma: GLOBE Research and Publishing S.r.l.

UNCTAD, (2006, 2007, 2008). World Investment Report. Geneva: United Nations Conference on Trade and Development.

World Bank (2007) World Development Indicators. Washington, DC: The World Bank.

Varvelli, A “Relazioni economiche italo-libiche “, Osservatorio di Politica Internazionale, Note di Analisi N°5, 17 Dicembre 2008

ORAL SOURCES:

Special thanks goes to Italian officers that helped my guiding my understanding through their experience and

kindness.

Inteview with Dr. Federica Pocek, SACE company, 20/12/2011, Rome.

Interview with Dr. Enzo Petralia, Arab-Italian Chamber of Commerce, 21/12/2011, Rome.

INTERNET RESOURCES:

Freedom House 2007 annual report “Countries at a Crossroad”, consultable at: http://freedomhouse.org/template.cfm?page=140&edition=8&ccrpage=37&ccrcountry=154 The World Bank at www.worldbank.org The United Nations Conference on Trade and Develpoment at www.unctad.org European Neighborhood Policy website at http://ec.europa.eu/world/enp/index_en.htm CIA World Factbook at https://www.cia.gov/library/publications/the-world-factbook/index.html Arab-Italian Chamber of Commerce at www.cameraitaloaraba.org Società Italiana per le Imprese all’Estero at www.simest.it Istituto Nazionale per il Commercio Estero at www.ice.it