“analysis of banking v/s non banking financial...

TRANSCRIPT

“Analysis of Banking V/S Non banking Financial Companies" Management Research Project -II

Submitted In the partial fulfillment of the Degree of Master of Business Administration

Semester-IV

By

1. Desai Mittal B. - 12044311019

2. Patel Hiren M. - 12044311088 3. Patel Kinjal P. - 12044311101 4. Patel Kinjal V. - 12044311102 5. Patel Krushnkant B. - 12044311104

Under the Guidance of

Prof. (Dr.) Mahendra Sharma Prof. & Head

V. M. Patel Institute of Management. &

Jayesh D. Patel Assistant Professor

V. M. Patel Institute of Management

Submitted To

V. M. Patel Institute of Management

(April 2014)

CERTIFICATE BY THE GUIDE

This is to certify that the contents of this report entitled “Analysis of Banking V/S

Non banking Financial Companies" submitted to V. M. Patel Institute of

Management for the Award of Master of Business Administration (MBA Sem-IV)

is original research work carried out by him/her/them under my supervision. This

report has not been submitted either partly or fully to any other University or

Institute for award of any degree or diploma.

Name Exam number

1. Desai Mittal B. - 12044311019

2. Patel Hiren M. - 12044311088 3. Patel Kinjal P. - 12044311101 4. Patel Kinjal V. - 12044311102 5. Patel Krushnkant B. - 12044311104

Professor & Head,

V. M. Patel Institute of Management,

Ganpat University.

Kherva.

Date:

Place: Kherva

CANDIDATE’S STATEMENT

We hereby declare that the work incorporated in this report entitled “Analysis of

Banking V/S Non banking Financial Companies" in partial fulfillment of the

requirements for the award of Master of Business Administration (Sem.-IV) is the

outcome of original study undertaken by us and it has not been submitted earlier to

any other University or Institution for the award of any Degree or Diploma.

Name Exam number Sign

1. Desai Mittal B. - 12044311019

2. Patel Hiren M. - 12044311088 3. Patel Kinjal P. - 12044311101 4. Patel Kinjal V. - 12044311102 5. Patel Krushnkant B. - 12044311104

Date:

Place: kherva

PREFACE

As a part of the MBA curriculum and in order to gain practical knowledge in the field of

management, we are required to make a report on any management research related topic.

One can deny for the importance of the practical exposure of the problem for its better

understanding and better grip of coming out with an industrially acceptable solution.

The basic objective behind doing this report is to gain the knowledge about the Banks and nbfc.

Now a day, management is an art, which we should learn by heart, and we believe that art by

studying it practically rather than reading the books. Management is must for every company,

every organization, not only this but also it is must for every person.

The Master of Business Administration is a professional course, which develops a new level of

knowledge & skills and sets & prepares those seeking challenging carriers in the new era of

Liberalization, and Globalization. MBA Programme imparts the knowledge of concept &

application skills of management.

In MBA Semester-IV, we are required to prepare a report on to fulfill this requirement of the

syllabus; we have prepared a report on “Analysis of Banking V/S Non banking

Financial Companies"

ACKNOWLEDGEMENT

Knowledge is itself a continuous process. But at this moment of our substantial enhancement we

find no words to express my gratitude to those who had helped me directly or indirectly in

making this report a success. We are indebted and thankful for the assistance received from

various individuals.

It is indeed of great moment to pleasure to express our sense of per found gratitude and ineptness

to all the people who have been instrumental in making our learning a rich experience. We got

the opportunity to do a challenging project in Management Research Project-II. The project is

the important part of our study and gives us a practical exposure to management research its

implementation and it is almost impossible to do the same without the guidance of people in and

around us.

We hereby take the pleasure of thanking all who have contributed to the making of this report.

Firstly we would like to thank Prof. (Dr.) Mahendra Sharma, Prof. Jayesh Patel, Prof.

Abhishek parikh, Who have provided us full liberty, co–operation during our Report and

sharing knowledge of his field with us always with a smile.

We are greatly thankful to my parent, seniors, friends and colleagues for their kind and constant

inspiration and loving support through many days when they wondered where the priorities lay.

Name Exam number

1. Desai Mittal B. - 12044311019

2. Patel Hiren M. - 12044311088 3. Patel Kinjal P. - 12044311101 4. Patel Kinjal V. - 12044311102 5. Patel Krushnkant B. - 12044311104

EXECUTIVE SUMMARY

The study presents a comparative study of NBFC’s in India. There are almost 13000 registered

NBFC’s in India. The study is aimed to provide an holistic view of the NBFC Industry. NBFC

fulfills the financial gap by providing loan at a lower rate of interest. The major players of each

field

1) Housing Finance Industry: LIC Housing Finance.

2) Infrastructure Finance Industry: IDFC

3) Asset Financing: Shriram Transport Finance

4) Composite: Reliance Capital

The study also compared the Indian Banks v/s NBFC. It was found that at even at the time of the

economic slowdown NBFC was more profitable. The industry is not tightly regulated as there

are many regulatory bodies. Hence, there was an important need to study the NBFC as the

industry plays an important role in the financial Services market of INDIA.

In our project, we can say that investors are more protecting investing in bank sectors comparing

non banking financial sectors.

CONTENTS

Certificate by the Guide I

Candidate’s Statement II

Preface III

Acknowledgments IV

Executive summary V

CH.No PARTICULAR PAGE NO.. 1.0 INTRODUCTION OF NON BANK FINANCIAL

COMPANIES 1

1.1 Background 2 1.2 NBFCs: Banking on new areas? 4 1.3 Regulation 5 1.4 Classification 5 1.5 NBFCs' strengths 6 1.6 Difference Between NBFC and Bank 8 1.7 Significance of NBFCs in India 9

2.0 REVIEW OF RELATED LITERATURE 11 2.1 Literature review 12

3.0 RESPONSIBILITIES OF NBFC 15 3.1 Guidelines for new deposits 16 3.2 NBFCs are typically into funding of 17 3.3 List of major products offered by NBFCs in India 18 3.4 Responsibilities 18

4.0 RESEARCH METHODOLOGY 19 4.1 Introduction 20 4.2 Motivation of the study 21 4.3 Statement of the problem & Objectives of the Study 22 4.4 Scope of the study 22 4.5 Significance of the study 23 4.6 Hypotheses of the study 24 4.7 Research Methodology 25 4.7.1 Sample Frame and Sample Size 25 4.7.2 Data Analysis 26 4.8 Limitation of the study 29

5.0 DATA ANALYSIS & INTERPRETATION 30 5.1 Analysis of banking vs. non banking financial companies 31

6.0 FINDINGS 44

7.0 CONCLUSION 47 APPENDICES 49 1. Bibliography 49 2. References 50

LIST OF TABLE

Table no. Name of Table Page No: 5.1 Descriptive Statistics For Stock Returns. 31 5.2 Levine’s Test For Equality Of Variances 31 5.3 Descriptive Statistics For Earning Per Share (EPS) 32 5.4 Levene's Test For Equality Of Variances 33 5.5 Group Statistics Return On Equity 34 5.6 Levene's Test For Equality Of Variances Returns On Equity 34 5.7 Group Statistics Earning Per Share (EPS) 35 5.8 Levene's Test For Equality Of Variances 35 5.9 Group Statistics Return On Equity 36 5.10 Levene's Test For Equality Of Variances Returns On Equity 37 5.11 Group Statistics Return On Stock 38 5.12 Levene's Test For Equality Of Variances Returns On Stock 38 5.13 Descriptive Of Small, Medium ,Large NBFC EPS 39 5.14 Test Of Homogeneity Of Variances 39 5.15 Anova 39 5.16 Robust Tests Of Equality Of Means 40 5.17 Descriptive Of Small, Medium, Large NBFC Return On Equity 41 5.18 Test Of Homogeneity Of Variances 41 5.19 Anova 41 5.20 Descriptive Of Small, Medium ,Large NBFC Return On Stock 43 5.21 Test Of Homogeneity Of Variances 43 5.22 Anova 43

1

CHAPTER 1

INTRODUCTION

OF

NON-BANK FINANCIAL

COMPANIES (NBFCs)

2

1.1 Background: Banking in India in the modern sense originated in the last decades of the 18th century. The

first banks were Bank of Hindustan (1770-1829) and The General Bank of India, established

1786 and since defunct.

The largest bank, and the oldest still in existence, is the State Bank of India, which originated in

the Bank of Calcutta in June 1806, which almost immediately became the Bank of Bengal. This

was one of the three presidency banks, the other two being the Bank of Bombay and the Bank of

Madras, all three of which were established under charters from the British East India Company.

The three banks merged in 1921 to form the Imperial Bank of India, which, upon India's

independence, became the State Bank of India in 1955. For many years the presidency banks

acted as quasi-central banks, as did their successors, until the Reserve Bank of India was

established in 1935.

Non Banking Finance Institutions is a constituent of the institutional structure of the

organized financial system in India the term ―Finance is often understood as being equivalent to

―money.

However, finance exactly is not money; it is the source of providing funds for a particular

activity. Providing or securing finance by itself is a distinct activity or function, which results in

Financial Management, Financial Services and Financial Institutions. Finance therefore

represents the resources by way funds are needed for a particular activity. We thus speak of

'finance' only in relation to a proposed activity. Finance goes with commerce, business, banking

etc.

Finance is also referred to as "Funds" or "Capital", when referring to the financial needs of a

corporate body. The Financial System of any country consists of financial markets, financial

intermediation and financial instruments or financial products. All these items facilitate transfer

of funds and are not always mutually exclusive. Inter -relationships between these are a part of

the system e.g. Financial Institutions operate in financial markets and are, therefore, a part of

such markets.

3

The Financial Intermediaries in the Financial System can broadly be said to comprise of:

Banks; and

NBFCs

NBFIs are different types of financial institutions that provide the following types of services:

1) Payments

2) Liquidity / credit

3) Divisibility: break up large denomination and aggregate small denomination

4) Store of value

5) Information: processing and assessing risks

6) Risk pooling: lower the risks of investors

Non-bank financial companies (NBFCs) are financial institutions that provide banking

services without meeting the legal definition of a bank, i.e. one that does not hold a banking

license. These institutions typically are restricted from taking deposits from the public depending

on the jurisdiction. Nonetheless, operations of these institutions are often still covered under

countries banking regulations.

The specific banking products that can be offered by NBFCs depends on the jurisdiction, and

may include services such as loans and credit facilities, savings products, investments and money

transfer services. In some jurisdictions, such as New Zealand, any company can engage in

banking business, except they are not allowed to use the word bank in their name. A company

can only call itself a bank if is a registered as such with the nation's central bank.

Non-Banking Financial Company (NBFC) in India began in a small way in the 1960s to serve

the need of the saver and investor whose financial need were not adequate covered by the

existing banking system in India. The NBFCs began to invite fixed deposit from investor and

work out leasing deal for larger industrial firms. In the early decade their operation were on a

limited scale and could not make a significant impact of financial system. However between

1980s and 1990s the NBFCs were well entered and began to attract a large number of investors

owing to them customer friendly reputation.

4

The scope of NBFCs is fast growing with multiplication of financial services. Some of NBFCs

are also engaged in underwriting through subsidiary unit and by offering allied financial services

including stock broking, investment banking, assets management and portfolio management.

Non-Banking Financial Companies are those companies, which are not banking companies under

the banking regulation Act, but carry out financial activities of providing finance. These

companies may or may not accepting deposit from the public. These provide lease finance,

housing finance, trade in share, general loan and advance for share trading, hire purchase

specially against automobile.

In recent times non- baking financial companies (NBFCs) have emerged substantial contributors

to the Indian economics growth by supplementing the effort of banks and other financial

institutions. They pay key role in the direction of saving and investment .in wave of rapid

industrial development &liberalization of the financial sector, key financial institution and

professional have promoted financial institution to create have promoted financial institution to

create a diversified and competitive financial system.

NBFCs intermediate between saver and investor. These companies also know as finance

companies, lease companies, loan companies etc.

1.2 NBFCs: Banking on new areas?

The last couple of years have seen significant developments in the financial sector that have

raised competition across-the-board. Non-banking finance companies (NBFCs) have perhaps felt

the pressure most. Consequently, top-rung NBFCs are changing tack, and initiating moves to

become financial supermarkets. They are seeking to provide as many services as possible, and

their fate will be decided by how successful they are Supermarkets in the making Leading

NBFCs have gradually extended their product portfolio to include asset management companies

(AMCs), housing finance firms and are now readying to enter insurance.

But the NBFCs' latest moves to increase the lines of business may be of a more permanent nature

despite the growing competition from the resource-rich banks and financial institutions in core

and emerging areas. The last few years saw the traditional boundaries between different

5

categories of financial intermediaries disappear. Thus, the NBFCs had to contend with heavy

competition even in areas that were their preserve.

Working capital loans were traditionally the preserve of banks, and term lending that of the

financial institutions. Now these sets of institutions move in and out each other's areas freely.

And both have also moved into retail financing, the traditional preserve of the NBFCs.

1.3 Regulation:

For European NCs the Payment Services Directive (PSD) is a regulatory initiative from the

European Commission to regulate payment services and payment service providers throughout

the European Union (EU) and Eurofff Economic Area (EEA). The PSD describes which type of

organizations can provide payment services in Europe (credit institutions (i.e. banks) and certain

authorities (e.g. Central Banks, government bodies), Electronic Money Institutions (EMI), and

also creates the new category of Payment Institutions). Organizations that are not credit

institutions or EMI, can apply for an authorization as Payment Institution in any EU country of

their URL choice (where they are established) and then passport their payment services into

other Member States across the EU.

1.4. Classification:

Based on their Liability Structure, NBFCs have been divided into two categories. 1. Category

‘A’ companies (NBFCs accepting public deposits or NBFCs-D), and 2. Category ‘B’ companies

(NBFCs not raising public deposits or NBFCs-ND).

NBFCs-D are subject to requirements of Capital adequacy, Liquid assets maintenance, Exposure

norms (including restrictions on exposure to investments in land, building and unquoted shares),

ALM discipline and reporting requirements; In contrast, until 2006 NBFCs-ND were subject to

minimal regulation. Since April 1, 2007, non-deposit taking NBFCs with assets of `1 billion and

above are being classified as Systemically Important Non-Deposit taking NBFCs (NBFCs-ND-

SI), and prudential regulations, such as capital adequacy requirements and exposure norms along

with reporting requirements, have been made applicable to them. The asset liability management

(ALM) reporting and disclosure norms have also been made applicable to them at different

points of time.

6

Depending upon their nature of activities, non- banking finance companies can be classified into

the following categories:

1) Development finance institutions

2) Leasing companies

3) Investment companies

4) Modaraba companies

5) House finance companies

6) Venture capital companies

1) Discount & guarantee houses

2) Corporate development companies

1.5 NBFCs' strengths: NBFCs that succeed are likely to do so by making the most of their ability to contain risk, adapt

to changes and tap demand in markets that are likely to be avoided by the bigger players.

Risk containment is critical in the financial sector. For a category supposed to cater to the

relatively riskier areas, top-rung NBFCs have proved the most adept at containing risks. The

industrial slowdown of the late 1990s saw the NPAs increasing sharply in the portfolio of banks

and financial institutions. Top-rung NBFCs which contained risk better were helped by two

factors: Lower proportion of loans to corporate and a more effective recovery mechanism.

The large size of a corporate loan means that a single default has a bigger impact. NBFCs that

lent mainly to the commercial vehicle segment were perhaps aided by the low proportion of loan

to each customer vis-a-vis the total disbursement. A default would, therefore, have limited

impact.

7

The small size of the loans coupled with a better collection mechanism resulted in effective risk

containment by the NBFCs. This was further aided by the greater flexibility of the NBFC

structure. The flexibility also enables the NBFCs to act with dispatch when they sense an

opportunity.

The other area where the NBFCs have an edge is the long experience in accessing fixed deposits

which gives them access to a database. Lack of reliable data has often tripped big names in the

corporate world.

The top-rung NBFCs have equipped themselves for the fast-changing environment where all

intermediaries are competing for retail finance. An outcome of the increased competition is that

profit margins of the NBFCs will decline. Moreover, with a huge resources committed to such

areas as insurance, which may take years to attain profitability, profit levels are unlikely to be as

high as they were.

Last year, the share price of quite a few NBFCs rose sharply only to fall rapidly. Share prices are

unlikely to witness any significant, sustained rise this year in the light of the low premium the

stock market attaches to financial services, in general, and especially with the prospect of a

decline in returns on investment in the near term.

Investors with exposures in such top-rung NBFCs as Sundaram Finance, Tata Finance or Kotak

Mahindra may stay invested as there are possibilities of moderate gains in the medium term.

However, fresh exposures may be avoided.

8

1.6 Difference between NBFC and Bank: In a country like India with a huge population, it is impossible for banks to cater to all sections of

the society as many areas are inaccessible and remote. Also, to provide banking facilities to the

illiterate and the poor, finance institutions that work on similar lines as banks are required. In

India, this requirement has traditionally been fulfilled by NBFC, or non banking financial

company. As the name suggests, NBFC is not a bank though it performs many functions similar

to that of banks. This article intends to find out the major differences between NBFC and banks

and other features of these entities.

NBFC were created by the government of India as it felt the need to provide banking facilities to

the poor and underprivileged who could not get access to banks. NBFC is required to be

registered under the Companies Act 1956 to be able to perform functions similar to a bank.

Normally, a NBFC is engaged in the business of loans and advances, acquisition of shares,

debentures, stocks, bonds and securities issued by the government. It also indulges in hire-

purchase, leasing, insurance and chit business.

9

However, there are several notable differences between NBFC and a bank.

1) NBFC cannot collect deposits in the manner of a bank

2) NBFC cannot issue checks drawn on itself

3) NBFC cannot issue Demand Drafts like banks

4) NBFC cannot indulge primarily in agricultural or industrial activity

5) NBFC cannot engage in construction of immovable property

6) NBFC cannot accept demand deposits

7) While banks are incorporated under banking companies act, NBFC is incorporated under company act 1956.

1.7 Significance of NBFCs in India: According to the Economic Survey 2010-11, it has been reported that NBFCs as a whole account

for 11.2 per cent of assets of the total financial system. With the growing importance assigned to

financial inclusion, NBFCs have come to be regarded as important financial intermediaries

particularly for the small-scale and retail sectors. In the multi-tier financial system of India,

importance of NBFCs in the Indian financial system is much discussed by various committees

appointed by RBI in the past and RBI has been modifying its regulatory and supervising policies

from time to time to keep with the changes in the system. NBFCs have turned out to be engines

of growth and are integral part of the Indian financial system, enhancing competition and

diversification in the financial spreading risks specifically at times of financial distress and have

been increasingly recognized as complementary of banking system at competitive prices. The

Banking sector has always been highly regulated, however simplified sanction procedures,

flexibility and timeliness in meeting the credit needs and low cost operations result the NBFCs

getting an edge over banks in providing funding.

Since the 90s crisis the market has seen explosive growth, as per a Fitch Report1 the

compounded annual growth rate of NBFCs was 40% in comparison to the CA banks being 22%

only.

10

NBFCs have been pioneering at retail asset backed lending, lending against securities

microfinance etc and have been extending credit to retail customers in under-served are and to

unbanked customers.

(AFP) study has examined and compared the profitability of banks with NBFCs during the

financial year 2012-13. Simple average and profitability ratio of the other segments have been

studied.

11

CHAPTER 2 REVIEW

OF

LITERATURE

12

2.1 LITERATURE REVIEW:

The concept of chit funds according to Simcox (1894) is originated more than 1000 years ago.

And it is mentioned, Dravidian kuri is used for raising money for some special purposes.

Subbarama aiyar (1925) has described the working of ‘changati kuri’, where lot decides the

person every month to which the amount is to be paid. The chit fund offers money at a flexible

interest rate and the interest rate depends on the demand of the money.

The Travancore Banking Enquiry Commission and Travancore Companies Act (1938)

recommended that the banks in the state were prohibited from conducting kuri business. But

after Independence following the extension of the Indian Companies Act (1913) to Travancore

State, the position changed and banks restarted the kuri business with effect from 1st April 1951.

Banking Companies Act (1949) regarded kuries as an agency business which banks could take

up and therefore, chit fund business re-emerged as an essential segment of the operations of

several banks in South India.

William Logan (1951) mentioned the presence of a flourishing Kuri or lottery system existing in

the society. He also described the operation of kuri system among friends known as ‘Changaathi

Kuri’.

According to S.K.Basu (1961) A Non-Banking Financial Company (NBFC) is a company

incorporated under the companies Act, 1956, and conducting the financial business as its

principal business. In India, the Non-Banking Financial sector comprises a multiplicity of

institutions, which are defined under section 45 I (a) of the Reserve Bank of India Act, 1934.

According to R.G. Saraiya (1974) the annual savings mobilization through chit funds is in

multiples of 100 crore. Though these savings are less comparing with commercial banks, the

number of people benefited by chit funds is quite large. He has bring forth the recommendations

of the Banking Commission, which has recommended that the State Governments may consider

13

Starting Chit Funds at strategic places as model foremen with the object of offering effective

competition to private chit funds and thus acting as a disciplining factor.

Nayar (1986) pointed out that Chit Funds have come to stay as a unique non-banking financial

intermediary in India especially in South India. He also pointed out that the rationale of an

auction Chitty or Business Chitty is that the borrowers and lenders meet to fix the rate of interest

and since there is more than one borrower competing for the same amount, a competitive rate of

interest is offered. Only the members enjoy the benefits of the scheme. The study highlighted the

fact that for the subscribers, the return on subscriptions was not the only consideration. The

possibility of getting a lump-sum on easy terms at short notice was a great inducement. Hence, it

is advisable to retain these within the frame work of non-banking financial institutions controlled

under chit funds act 1982, by the state government.

The RBI reports in Trend and Progress of Banking in India (2008) indicates that even after the

four decades of banks’ nationalization, country’s 41 per cent adult population remained outside

the banking system but is surmised to be covered by the NBFCs wise Chit Funds’.

Dr.Jafor Ali Akhan (2009) stated that the Non-Banking Financial Companies (NBFCs) have

been playing a very significant role in the present day rigorous money-market conditions. They

are serving the nation by supporting the economic reconstruction and giving a booster to

industrial production. They are engaged into the business of providing loans and advances of

small amounts for a short-period to small borrowers. The Non-Banking Financial Companies

(NBFCs) play an important role in channelizing these savings into investment. They have

supplemented the role played by the banks.

According to Y.Bala Bharathi and Sanjoy De (2009) NBFCs are financial entities that provide

banking services without meeting the legal definition of a bank. They are typically not allowed to

take deposits from general public and hence have to seek other means of funding. These NBFCs

have matured a lot and even withstood the recent deadly crisis with a lot of resilience. NBFCs

can reach the unorganized segments of society with their ability to provide innovative financial

services. These entities play a critical role in disbursing credit to the rural sector, thus preventing

14

the concentration of credit risk in banks. In urban areas too, NBFCs focus on non-salaried

individuals, traders, transporters and stock brokers who are neglected by banks.

Dr.Amrit Patel and Dr.Gopal Kalkoti(2010) mentioned that according to RBI, the major

reason for increase in overall household debt and increase in the share of rural household

indebtedness to non- institutional sources was a significant increase in the current farm

expenditure and household expenditure for which households found it difficult to obtain loans

from banks. In addition to that the cumbersome procedure of submitting various documents with

loan applications and documentation process led to an average of 33 weeks taken by commercial

banks to approve loans. And this scenario is the niche forchit fund like entities under the banner

of NBFCs.

Dr.Jatinder Kaur(2010) reveals that, despite the phenomenal growth of banking sector, the

extent of rural indebtedness in India has been on a continuous rise. About one-third of the rural

credit requirements are still met by non-institutional sources, like moneylenders. The favoring

factor of moneylenders is that banks will not sanction loans for consumption purposes and

default of repayment of previous loan makes it ineligible for further assistance from banks.

Usha Thorat (2010) states that non-banking entities can be either non-banking non financial

entities or non-banking financial entities. In case of non-banking financial entities, there mare

deposit taking and non-deposit taking financial companies is there. Considering the difficulties in

ensuring the effective supervision of large number of small deposit-taking entities, fresh

approvals to NBFCs for accepting deposits are not considered.

15

CHAPTER 3

RESPONSIBILITIES

Of

NBFC

16

3.1 Guidelines for new deposits :

Customer identification: 'Know The Customer' (KYC) should be the key guiding principle for

identification of an individual / corporate customer (depositor or borrower).

Accordingly, the KYC framework should have two- fold objective, (I) to ensure customer

identification and verifying his identity and residential address; and (ii) to monitor transactions

of a suspicious nature.

NBFCs should ensure that the identity of the customer, including beneficial owner is done based

on disclosures by customers themselves.

Typically easy means of establishing identity would be documents such as Permanent Account

Number (PAN), ration card, driving licence, Election Commission's identity card, passport, et

cetera in case of individuals and registration certificate, partnership deed/agreement, et cetera

and other reliable documents in respect of companies, firms and other bodies.

Verification through such documents should be in addition to the introduction by a person known

to the NBFC.

Procedures for existing customers :

In respect of existing customers, NBFCs should ensure that gaps and missing

information in compliance of KYC guidelines on customer identification procedure is

filled up and completed before June 30, 2004.

Ceiling and monitoring of cash transactions :

NBFCs would normally not have large cash withdrawals and deposits. However,

wherever transactions of Rs 10 lakh (Rs 1 million) and above are undertaken, they should

keep record of these transactions in a separate register maintained at branch, as well as at

Registered Office. Such information should be made available to regulatory and

investigating authorities, when demanded.

17

Guidelines and monitoring procedures :

The board of directors of NBFCs should formulate policies and procedures to

operationalise the guidelines and put in place an effective monitoring system to ensure

compliance by their branches. Early computerization of branch/office reporting will

facilitate prompt generation of such reports and monitoring.

Internal audit/inspection :

Internal auditors must specifically scrutinize and comment on the effectiveness of the

measures taken by branches / offices of NBFC in adoption of KYC norms and steps

towards prevention of money laundering. Specific cases of violation should be

immediately brought to the notice of head / controlling / registered office.

Record keeping :

NBFCs should prepare and maintain proper documentation on their customer

relationships and cash transactions of Rs 10 lakh and above. The records of all such

transactions should be retained for at least ten years after the transaction has taken place

and should be available for perusal and scrutiny by audit functionaries as well as

regulators and law enforcement authorities; as and when required, at the branch as well as

at registered office.

Training of staff and management :

It is important that all the operating and management staff is made fully aware of the

implications and understand the need for strict adherence to KYC norms. NBFCs may

take suitable steps to impart training to their operational staff on anti-money laundering

measures.

3.2 NBFCs are typically into funding of: Construction equipment

Commercial vehicles and cars

Gold loans

Microfinance

18

Consumer durables and two wheelers

Loan against shares, etc.

3.3 List of major products offered by NBFCs in India: Funding of commercial vehicles

Funding of infrastructure assets

Retail financing

Loan against shares

Funding of plant and machinery

3.4 Responsibilities : The NBFCs accepting public deposits should furnish to RBI Audited balance sheet of each

financial year and an audited profit and loss account in respect of that year as passed in the

annual general meeting together with a copy of the report of the Board of Directors and a copy of

the report and the notes on accounts furnished by its Auditors;

Statutory Annual Return on deposits - NBS 1;

Certificate from the Auditors that the company is in a position to repay the deposits as

and when the claims arise;

Quarterly Return on liquid assets; Half-yearly Return on prudential norms;

Half-yearly ALM Returns by companies having public deposits of Rs. 20 crore and

above or with assets of Rs. 100 crore and above irrespective of the size of deposits ;

Monthly return on exposure to capital market by companies having public deposits of

Rs. 50 crore and above; and

A copy of the Credit Rating obtained once a year along with one of the Half-yearly

Returns on prudential norms as at (v) above.

19

CHAPTER 4

RESEARCH

METHODOLOGY

20

4.1. Introduction:

This is an introduction to research and research methods and will outline some, but not all, key

areas of research and research methods:

A. Definitions

B. Research approaches

C. Stages of the research process

D. Background reading & information gathering

E. Data collection

F. Ethical issues in research

This covers a number of important areas of the Research process, particularly,

• Data analysis

THE PURPOSE OF RESEARCH IS TO.

1. Review or synthesize existing knowledge

2. Investigate existing situations or problems

3. Provide solutions to problems

4. Explore and analyze more general issues

5. Construct or create new procedures or systems

6. Explain new phenomenon

7. Generate new knowledge

Research Design:

A research design is a pattern or an outline of a research project’s workings. It is a statement of

only the essential elements of a study, those that provide the basic guidelines for the details of

the project.

21

If there were no research design, the research would have only foggy notion about what is to be

done. There are numerous specific designs, which can be classified into three broad categories.

• Descriptive Design

• Quasi Experimental Design

• Experimental Design

• Descriptive Design:

These designs have its name because they describe a phenomenon without establishing

association between the factors. Hence these designs are utilized when a need is to

produce accurate description of variables.

• Quasi Experimental Design:

These designs as the name implies lacks the vigorous qualities of real experiments

particularly valid demonstration of variable association. Still they are not descriptive

ones.

• Experimental Design:

These designs are intended to demonstrate cause and effect relationship such designs can

measure communicate variation i.e. degree of change in one variable ‘y’ when another

variable ‘x’ is changed.

In context of our project study research design would be descriptive design.

4.2. Motivation of the study

Motivation is the process of arousing the action sustaining the activity in process and regulation

the pattern of activity. In this project we are analysis Nbfcs companies because Nbfcs is the most

important in india.so we are motivated for this factor.

22

4.3. Statement of the problem:

Research being a logical process definitely follows predetermined or steps in order to obtain

the desired results or outcomes. Though the entire process of research is quite complex and

requires a considerable degree of knowledge and skill, the step of problem formulation is most

challenging and critical one for the researcher as well as the research. Indian Government is

hesitant to introduce banking system and non banking financial corporations for Indian financial

system in the Indian Economy. It is rightly said that a problem, well defined is half solved.

The Research topic undertaken by me is “analysis of banking v/s non banking financial

companies.

Research Objectives of the Study:

Our goal is to investigate the banking and nonbank finance corporations (NBFCs) in India to

understand.

• Comparison of banking vs. none banks financial companies.

• Comparison of private banks vs. public banks.

• Comparison of small, medium, large NBFCs.

The main objective of my research is to “ Analysis of Banking V/S Non Banking Financial

Companies”.

4.4. Scope of the Study:

To study covered in banking v/s NBFCs. 20012-13 was a difficult year, especially for the

financial segment across the globe. However, India’s strong macro-economic fundamentals and

financial policies have shielded it from the turmoil. As the fiscal year 2008-09 comes to an end,

ASSOCHAM Research Bureau has analyzed corporate results of the Indian Banks and Non-

Banking Financial Companies (NBFCs). The study considered those banks that have announced

their results between 15th April -20th May 2008- 09 posted on the website of Bombay Stock

Exchange.

23

The ASSOCHAM Research Bureau (ARB) have analyzed in total banks (both public & private

sector) and all NBFCs those are listed.

The Assocham Financial Pulse (AFP) study has examined and compared the profitability of

banks with NBFCs during the financial year 2012-13. Simple average and profitability ratio of

the other segments have been studied.

4.5. Significance of the study:

According to the Economic Survey 2010-11, it has been reported that NBFCs as a whole account

for 11.2 per cent of assets of the total financial system. With the growing importance assigned to

financial inclusion, NBFCs have come to be regarded as important financial intermediaries

particularly for the small-scale and retail sectors.

In the multi- tier financial system of India, importance of NBFCs in the Indian financial system is

much discussed by various committees appointed by RBI in the past and RBI has been

modifying its regulatory and supervising policies from time to time to keep pace with the

changes in the system.

NBFCs have turned out to be engines of growth and are integral part of the Indian financial

system, enhancing competition and diversification in the financial sector, spreading risks

specifically at times of financial distress and have been increasingly recognized as

complementary of banking system at competitive prices. The Banking sector has always been

highly regulated, however simplified sanction procedures, flexibility and timeliness in meeting

the credit needs and low cost operations resulted in the NBFCs getting an edge over banks in

providing funding.

24

4.6. Hypotheses of the study: 1. Hypothesis:-

H0: There is no significance difference between stock return of Banks and stock returns of

NBFCs.

H1: There is significance difference between stock return of Banks and stock returns of NBFCs

2. Hypothesis:-

H0: There is no significance difference between EPS of Banks and EPS of NBFCs.

H1: There is significance difference between EPS of Banks and EPS of NBFCs.

3. Hypothesis:-

H0: There is no significance difference between ROE of Banks and ROE of NBFCs.

H1: There is significance difference between ROE of Banks and ROE of NBFCs.

ANOVA FOR ROE :

H0:- there is no significant difference between return of equity small, medium, large NBFCs.

H1:- there is significant difference between return of equity small, medium, large NBFCs.

ANOVA FOR EPS :

H0:- there is no significant difference between earning per share of small, medium, large

NBFCs.

H1:- there is significant difference between earning per share of small, medium, large NBFC

ANOVA FOR ROS :

H0:- there is no significant difference between stock return of small, medium, large NBFCs.

H1:- there is significant difference between stock return of small, medium, large NBFCs.

25

4.7 RESEARCH METHODOLOGY

Here we have done analysis of Indian banks and NBFC s ( Non Banking Financial Companies)

history based on total available Private bank in India are 148 and Public bank are 33. NBFCs

Small is 1081, NBFCs medium are 54 and NBFCs large are 8.

Here we have done a research on secondary based so available EPS of Private Bank are 36,

Public Bank are 35, and NBFCs small are 527, NBFCs medium 26, NBFCs large 7.Data are

available so we have select total number of bank are 71 and total number of NBFCs 560 are

taken in our research report.

Here we have done a research on secondary based so available ROE of Private Bank are 156,

Public Bank are 31, and NBFCs small are 54, NBFCs medium 54, NBFCs large 9. Data are

available so we have select total number of bank are 187 and total number of NBFCs 117 are

taken in our research report.

Here we have done a research on secondary based so available Stock Return of Private Bank are

18, Public Bank are 25, and NBFCs small are 110, NBFCs medium 6, NBFCs large 6. Data are

available so we have select total number of bank are 43 and total number of NBFCs 122 are

taken in our research report.

4.7.1. Sample frame and sample size.

EPS of fin. Large:7 companies

EPS of fin. Medium:26 companies

EPS of fin. Small:527 companies

EPS of private bank: 36 companies

EPS of public bank: 35 companies

ROE of NBFC FIN. Large : 9 companies

ROE of NBFC FIN. Small: 54 companies

26

ROE of NBFC FIN. medium:54 companies

ROE Of Private bank: 156 companies

ROE Of Public bank: 31 companies

Stock Return Of Public Bank:25 companies

Stock Return Of Private Bank:18 companies

Stock Return Of NBFC FIN. Small Bank:110 companies

Stock Return Of NBFC FIN. Medium Bank:6 companies

Stock Return Of NBFC FIN. Large Bank:6 companies

Data source:

The sources of collection of secondary data are:

• Capitaline

Plan of data analysis:

The data is analyzed on the basis of spss software by using mathematical techniques. The

technique that we will use and also secondary data is use.

Tools for Data Analysis

Spss software has been used for testing the favorable or unfavorable situation of bank

V/s NBFC

27

4.7.2. Data analysis:

4.7.2.1. ANOVA Test

Analysis of variance (ANOVA) is a collection of statistical models used to analyze the

differences between group means and their associated procedures (such as "variation" among and

between groups), developed by R.A. Fisher. In the ANOVA setting, the observed variance in a

particular variable is partitioned into components attributable to different sources of variation. In

its simplest form, ANOVA provides a statistical test of whether or not the means of several

groups are equal, and therefore generalizes the t-test to more than two groups. Doing multiple

two-sample t-tests would result in an increased chance of committing a type I error. For this

reason, ANOVAs are useful in comparing (testing) three or more means (groups or variables) for

statistical significance.

Assumptions of ANOVA

The normal-model based ANOVA analysis assumes the independence, normality and

homogeneity of the variances of the residuals. The randomization-based analysis assumes only

the homogeneity of the variances of the residuals (as a consequence of unit-treatment additively)

and uses the randomization procedure of the experiment. Both these analyses require

homoscedasticity, as an assumption for the normal-model analysis and as a consequence of

randomization and additively for the randomization-based analysis.

Problems which do not satisfy the assumptions of ANOVA can often be transformed to satisfy

the assumptions. The property of unit-treatment additively is not invariant under a "change of

scale", so statisticians often use transformations to achieve unit-treatment additively. If the

response variable is expected to follow a parametric family of probability distributions, then the

statistician may specify (in the protocol for the experiment or observational study) that the

responses be transformed to stabilize the variance.[25] Also, a statistician may specify that

logarithmic transforms be applied to the responses, which are believed to follow a multiplicative

model.[16][26] According to Cauchy's functional equation theorem, the logarithm is the only

continuous transformation that transforms real multiplication to addition.

28

Characteristics of ANOVA

ANOVA is used in the analysis of comparative experiments, those in which only the difference

in outcomes is of interest. The statistical significance of the experiment is determined by a ratio

of two variances. This ratio is independent of several possible alterations to the experimental

observations: Adding a constant to all observations does not alter significance. Multiplying all

observations by a constant does not alter significance. So ANOVA statistical significance results

are independent of constant bias and scaling errors as well as the units used in expressing

observations. In the era of mechanical calculation it was common to subtract a constant from all

observations (when equivalent to dropping leading digits) to simplify data entry. This is an

example of data coding.

Why use the ANOVA over a t-test?

The t-test compares the means between 2 samples and is simple to conduct, but if there is more

than 2 conditions in an experiment an ANOVA is required. The fact the ANOVA can test more

than one treatment is a major advantage over other statistical analysis such as the t-test, it opens

up many testing capabilities but it certainly doesn’t help with mathematical headaches. It is

important to know that when looking at the analysis of variance an IV is called a factor, the

treatment conditions or groups in an experiment are called the levels of the factor. ANOVA’s use

an F-ratio as its significance statistic which is variance because it is impossible to calculate the

sample means difference with more than two samples.

ANOVA test assumes three things:

• The population sample must be normal

• The observations must be independent in each sample

• The population the samples are selected from have equal variance a.k.a. homogeneity of

variance.

4.7.2.2. Independent Sample Two Test:

Independent samples, the two samples of scores are from different unrelated groups. In

other words, scores in the two groups are not matched or paired. We say that these

29

samples are statistically independent. This is a common situation in social science

research. For example, when comparing experimental (receives treatment) and control

(does not receive treatment) groups that have been randomly assigned, we have two

independent samples. When we, as researchers, compare two groups.

Purpose of the t-test:

The general purpose of the indepent measures t test is to determine whether the sample mean

difference obtained is a real difference between the two populations or simply the result of

sampling error.

The assumption of the independent sample two tests are :

• The observation within each sample must be independent

• Population variance are equal

• Population distribution are normal in shape.

4.8. Limitation of the study:

The limitations of the study are those characteristics of design or methodology that impacted or

influenced the application or interpretation of the results of your study. They are the constraints

on generalizability and utility of findings that are the result of the ways in which you chose to

design the study and/or the method used to establish internal and external validity.

• Sample size – Our sample size is too long, it will be difficult to find significant

relationships from the data

• Measure used to collect the data : The limitation for the study is to collect long data. So

it is difficult for the project.

30

CHAPTER 5

DATA ANALYSIS

&

INTERPRETATION

31

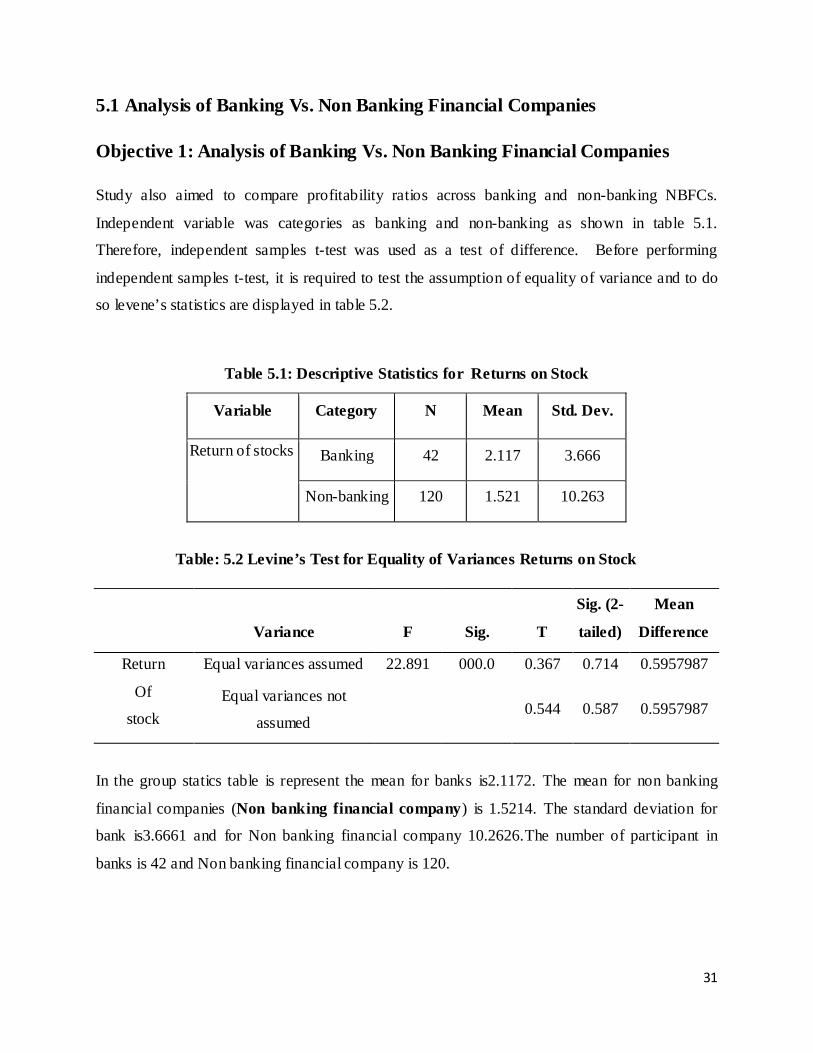

5.1 Analysis of Banking Vs. Non Banking Financial Companies

Objective 1: Analysis of Banking Vs. Non Banking Financial Companies

Study also aimed to compare profitability ratios across banking and non-banking NBFCs.

Independent variable was categories as banking and non-banking as shown in table 5.1.

Therefore, independent samples t-test was used as a test of difference. Before performing

independent samples t-test, it is required to test the assumption of equality of variance and to do

so levene’s statistics are displayed in table 5.2.

Table 5.1: Descriptive Statistics for Returns on Stock

Variable Category N Mean Std. Dev.

Return of stocks Banking 42 2.117 3.666

Non-banking 120 1.521 10.263

Table: 5.2 Levine’s Test for Equality of Variances Returns on Stock

In the group statics table is represent the mean for banks is2.1172. The mean for non banking

financial companies (Non banking financial company) is 1.5214. The standard deviation for

bank is3.6661 and for Non banking financial company 10.2626.The number of participant in

banks is 42 and Non banking financial company is 120.

F Sig. T

Sig. (2-

tailed)

Mean

Difference Variance

Return

Of

stock

Equal variances assumed 22.891 000.0 0.367 0.714 0.5957987

Equal variances not

assumed

0.544 0.587 0.5957987

32

The significant (2-tailed) in our table is 0.000. This value is less than 0.05, because of this we

can conclude that there is a statistically significant difference between the mean number of bank

and Non banking financial company .since our group statics box revealed that the mean for the

banks was greater than the mean for Non banking financial company, we can conclude that

return on stock is Non banking financial company is different than banks stock return.

2. Hypothesis:-

Study also aimed to compare profitability ratios across banking and non-banking NBFCs.

Independent variable was categories as banking and non-banking as shown in table 5.. Therefore,

independent samples t-test was used as a test of difference. Before performing independent

samples t-test, it is required to test the assumption of equality of variance and to do so levene’s

statistics are displayed in table of 5.4.

H0: There is no significance difference between EPS of Banks and EPS of NON BANKING

FINANCIAL COMPANYs.

H1: There is significance difference between EPS of Banks and EPS of NON BANKING

FINANCIAL COMPANYs.

Table 5.3: Descriptive Statistics for Earning per Share (EPS)

Variable Category N Mean Std. Deviation

EPS Bank 69 3.0596E2 1502.17672

NBFC 579 1.3589E2 3234.96060

33

Table 5.4 Levene's Test for Equality of Variances

Variance F Sig. T

Sig. (2-

tailed)

Mean

Difference

EPS Equal variances assumed .366 .545 .431 0.667 170.0692

Equal variances not assumed 0.755 0.452 170.0692

In the group statics table is represent the mean for banks is 3.0596. The mean for non banking

financial companies (Non banking financial company) is 1.3589. The standard deviation for bank

is1502.17672 and for none banking financial company 3234.96060.The number of participant in

banks is 69 and Non banking financial company is 579.

The significant (2-tailed) in our table is 0.545. This value is more than 0.05, because of this we

can conclude that there is a statistically no significant difference between the mean number of

bank and Non banking financial company .since our group statics box revealed that the mean for

the banks was greater than the mean for Non banking financial company, we can conclude that

earning per share in Non banking financial company is different than banks earning per share.

3. Hypothesis:-

Study also aimed to compare profitability ratios across banking and non-banking NBFCs.

Independent variable was categories as banking and non-banking as shown in table 5.5.

Therefore, independent samples t-test was used as a test of difference. Before performing

independent samples t-test, it is required to test the assumption of equality of variance and to do

so levene’s statistics are displayed in table 5.6.

H0: There is no significance difference between ROE of Banks and ROE of NBFCs.

H1: There is significance difference between ROE of Banks and ROE of NBFCs.

34

Table: 5.5 Group Statistics Return on Equity

Variable category N Mean Std. Deviation

Return

on equity

bank 185 8.03 12.049

NBFCs 114 6.92 9.639

Table: 5.6 Levene's Test for Equality of Variances Returns on Equity

variances T Df Sig. (2-tailed)

Mean

Difference

Return on equity Equal variances assumed 0.835 297 0.405 1.112

Equal variances not

assumed 0.880 277.415 0.380 1.112

In the group statics table is represent the mean for banks 8.03. The mean for non banking

financial companies (Non banking financial company) is 6.92. The standard deviation for bank is

12.049 and for Non banking financial company 9.639. The number of participant in banks is 185

and Non banking financial company is 114.

The significant (2-tailed) in our table is 0.265. This value is more than 0.05, because of this we

can conclude that there is a statistically no significant difference between the mean number of

bank and Non banking financial company .since our group statics box revealed that the mean for

the banks was greater than the mean for Non banking financial company, we can conclude that

return on equity of Non banking financial company is different than banks stock equity.

35

Objectives 2:- comparison of public sector banks v/s. private sector banks companies.

1. Hypothesis:-

Study also aimed to compare profitability ratios across banking and non-banking NBFCs.

Independent variable was categories as banking and non-banking as shown in table 5.7.

Therefore, independent samples t-test was used as a test of difference. Before performing

independent samples t-test, it is required to test the assumption of equality of variance

and to do so levene’s statistics are displayed in table 5.8.

H0: There is no significance difference between EPS of public sector banks and EPS of private

sector banks.

H1: There is significance difference between EPS of public sector banks and EPS of private

sector banks.

Table:5.7 Group Statistics Earning per Share (EPS)

category N Mean Std. Deviation Std. Error Mean

EPS Private 35 3.43065E2 1858.358656 314.119945

Public 34 2.67764E2 1043.416424 178.944440

Table:5.8 Levene's Test for Equality of Variances

36

Variances F Sig. T Sig. (2-

tailed)

Mean

Difference

EPS Equal variances assumed 0.37 0.55 0.21 0.837 75.301017

Equal variances not assumed 0.21 0.836 75.301017

In the group statics table is represent the mean for private banks is 3.43065. The mean for public

bank is 2.67764. The standard deviation for private bank is 1858.358656 and for public bank1043.416424

.The number of participant in private banks is 35 and public bank is 34.

The significant (2-tailed) in our table is 0.546. This value is more than 0.05, because of this we

can conclude that there is a statistically no significant difference between the mean number of

private bank and public bank .since our group statics box revealed that the mean for the private

banks was greater than the mean for public bank, we can conclude that esp. of private bank is

different than public bank earnings per share.

2. Hypothesis:-

Study also aimed to compare profitability ratios across banking and non-banking NBFCs.

Independent variable was categories as banking and non-banking as shown in table 5.9.

Therefore, independent samples t-test was used as a test of difference. Before performing

independent samples t-test, it is required to test the assumption of equality of variance

and to do so levene’s statistics are displayed in table5.10.

H0: There is no significance difference between ROE of public sector banks and ROE of private

sector banks.

H1: There is significance difference between ROE of public sector banks and ROE of private

sector banks.

Table:5.9 Group Statistics Return on Equity

Variable categories N Mean Std. Deviation

return on equity private 155 7.071 12.812401

public 30 12.987 4.365155

37

38

Table:5.10 Levene's Test for Equality of Variances Returns on Equity

t-test for Equality of Means

Variance F Sig. T Df Sig. (2-

tailed)

Mean

Difference

Return on

equity Equal variances assumed 2.071 0.152 -2.497 183 0.013 -5.916419

Equal variances not assumed -4.545 135.43 0 -5.916419

In the group statics table is represent the mean for private banks is 7.07058. The mean for public

bank is1.29870. The standard deviation for private bank is 12.812401 and for public bank 4.365155.

The number of participant in private banks is 155 and public bank is 30.

The significant (2-tailed) in our table is 0.152. This value is more than 0.05, because of this we

can conclude that there is a statistically no significant difference between the mean number of

private bank and public bank .since our group statics box revealed that the mean for the private

banks was greater than the mean for public bank, we can conclude that return on equity of

private bank is different than public bank return.

3. Hypothesis:-

Study also aimed to compare profitability ratios across banking and non-banking NBFCs.

Independent variable was categories as banking and non-banking as shown in table 5.11.

Therefore, independent samples t-test was used as a test of difference. Before performing

independent samples t-test, it is required to test the assumption of equality of variance and to

do so levene’s statistics are displayed in table 5.12.

H0: There is no significance difference between ROS of public sector banks and ROS of private

sector banks.

H1: There is significance difference between ROS of public sector banks and ROS of private

sector banks.

39

Table:5.11 Group Statistics Return on Stock

Variable Categories N Mean Std. Deviation

Return on stock Private 17 3.101 4.9523098

Public 24 1.425 2.3837577

Table:5.12 Levene's Test for Equality of Variances Returns on Stock

t-test for Equality of Means

Variable F Sig. T

Sig. (2-

tailed)

Mean

Difference

Return on

stock

Equal variances assumed 11.536 0.002 1.444 0.157 1.676144

Equal variances not assumed 1.293 0.21 1.676144

In the group statics table is represent the mean for private banks is 3.101424. The mean for public

bank is 1.425279. The standard deviation for private bank is4.9523098 and for public bank is

2.3837577.The number of participant in private banks is 17 and public bank is 24.

The significant (2-tailed) in our table is 0.002. This value is less than 0.05, because of this we

can conclude that there is a statistically significant difference between the mean number of

private bank and public bank .since our group statics box revealed that the mean for the private

banks was greater than the mean for public bank, we can conclude that return on stock of private

bank is different than public bank.

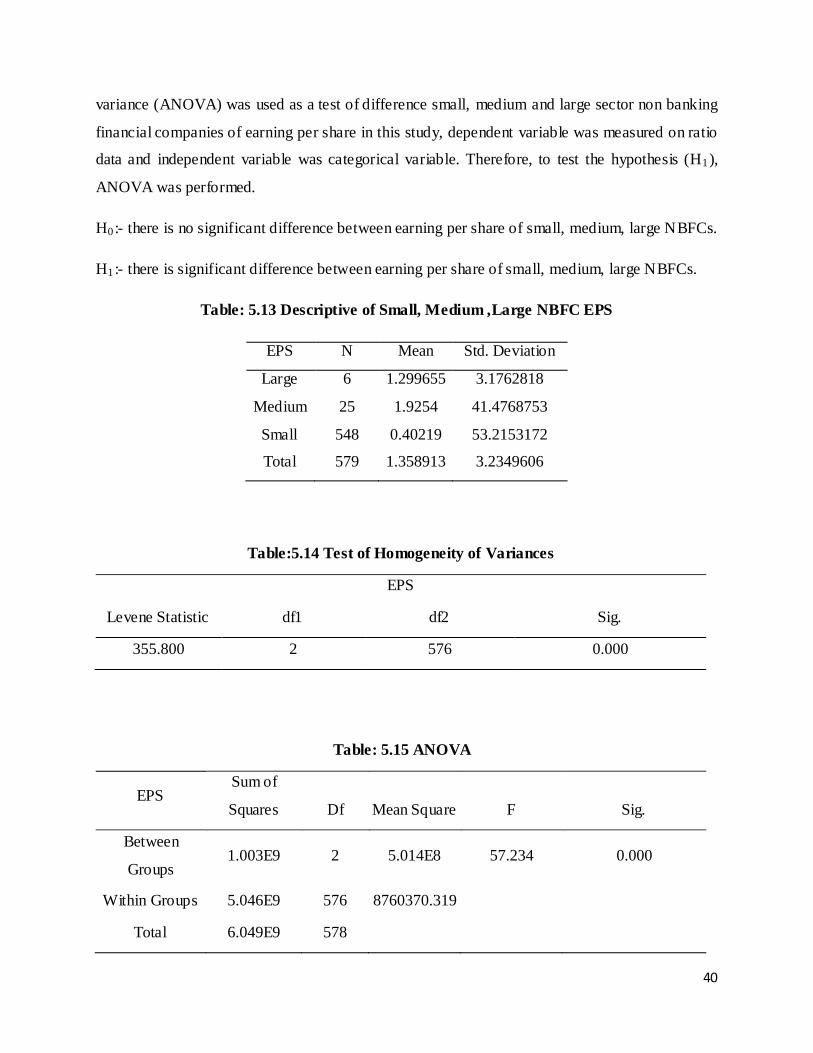

Objectives 3:- Comparison of small, medium, large NBFCs.

ANOVA FOR EPS

Study aimed to investigate the impact of size on profitability. In this study, profitability was

measured with EPS, ROE and ROS. The size was categorized as large size, medium size and

small size. The profitability was compared across different size of NBFCs. Therefore, analysis of

40

variance (ANOVA) was used as a test of difference small, medium and large sector non banking

financial companies of earning per share in this study, dependent variable was measured on ratio

data and independent variable was categorical variable. Therefore, to test the hypothesis (H1),

ANOVA was performed.

H0:- there is no significant difference between earning per share of small, medium, large NBFCs.

H1:- there is significant difference between earning per share of small, medium, large NBFCs.

Table: 5.13 Descriptive of Small, Medium ,Large NBFC EPS

EPS N Mean Std. Deviation

Large 6 1.299655 3.1762818

Medium 25 1.9254 41.4768753

Small 548 0.40219 53.2153172

Total 579 1.358913 3.2349606

Table:5.14 Test of Homogeneity of Variances

EPS

Levene Statistic df1 df2 Sig.

355.800 2 576 0.000

Table: 5.15 ANOVA

EPS Sum of

Squares Df Mean Square F Sig.

Between

Groups 1.003E9 2 5.014E8 57.234 0.000

Within Groups 5.046E9 576 8760370.319

Total 6.049E9 578

41

Table:5.16 Robust Tests of Equality of Means

EPS

Statistica df1 df2 Sig.

Welch 2.742 2 11.297 0.107

a. Asymptotically F distributed.

From the above analysis we can conclude that as the earning per share increases risk also

increase. In case of small NBFCs earning per share is 0.402190 and risk is 53.2153172. Same for

medium NBFCs return is 1.925400, risk is 41.4768753. And for large NBFCs return 1.299655, risk

is3.1762818. So there is no need of further analysis. This is descriptive analysis and we are not

taking whole population, its sample based so there is no need of further analysis.

From above homogeneity of variance is 0.000 which less than 0.05 so there is significance

difference between the earning per share variance of small, medium, large NBFCs. Thus, one can

compare means of earning per share through ANOVA. But From the above ANOVA table we

have found that significance value is 0.000 which is less than 0.05.

Robust Tests of Equality of Means is 0.107 which is more than 0.05. So the null hypothesis is

accepted. Therefore we can conclude that there is no significance difference between earning per

share of small, medium and large NBFCs.

ANOVA FOR ROE

Study aimed to investigate the impact of size on profitability. In this study, profitability was

measured with EPS, ROE and ROS. The size was categorized as large size, medium size and

small size. The profitability was compared across different size of NBFCs. Therefore, analysis of

variance (ANOVA) was used as a test of difference small, medium and large sector non banking

financial companies of return on equity. In this study, dependent variable was measured on ratio

42

data and independent variable was categorical variable. Therefore, to test the hypothesis (H1),

ANOVA was performed.

H0:- there is no significant difference between return of equity small, medium, large NBFCs.

H1:- there is significant difference between return of equity small, medium, large NBFCs.

Table: 5.17 Descriptive of Small, Medium, Large NBFC Return on Equity

ROE N Mean Std. Deviation Std. Error

Large 8 1.103250 9.8585043 3.4855076

Medium 53 6.606981 9.6443243 1.3247498

Small 53 6.606981 9.6443243 1.3247498

Total 114 6.917544 9.6392305 .9027966

Table:5.18

Test of Homogeneity of Variances

ROE

Levene Statistic df1 df2 Sig.

.177 2 111 0.838

Table: 5.19

ANOVA

ROE Sum of

Squares Df

Mean

Square F Sig.

Between Groups 145.687 2 72.843 0.781 0.460

Within Groups 10353.682 111 93.276

Total 10499.368 113

43

From the above analysis we can conclude that as the return increases risk also increases. In case

of small NBFCs return on equity is 6.606981 and risk is9.6443243.same for medium NBFCs

return is 6.606981, risk is 9.6443243. And for large NBFCs return is1.103250, risk is 9.6443243.

So there is no need of further analysis. This is descriptive analysis and we are not taking whole

population, its sample based so there is no need of further analysis.

From above homogeneity of variance is 0.838 which more than 0.05 so there is no significance

difference between the equity variance of small, medium, large NBFCs. Thus, one can compare

means of equity returns through ANOVA.

From the above ANOVA table we have found that significance value is 0.460 which is more

than 0.05 so the null hypothesis is accepted. Therefore we can conclude that there is no

significance difference between stock returns of small, medium and large NBFCs.

ANOVA FOR ROS

Study aimed to investigate the impact of size on profitability. In this study, profitability was

measured with EPS, ROE and ROS. The size was categorized as large size, medium size and

small size. The profitability was compared across different size of NBFCs. Therefore, analysis of

variance (ANOVA) was used as a test of difference small, medium and large sector non banking

financial companies of stock on return. In this study, dependent variable was measured on ratio

data and independent variable was categorical variable. Therefore, to test the hypothesis (H1),

ANOVA was performed.

H0:- there is no significant difference between stock return of small, medium, large NBFCs.

H1:- there is significant difference between stock return of small, medium, large NBFCs.

44

Table: 5.20 Descriptive of Small, Medium ,Large NBFC Return on Stock

ROS N Mean Std. Deviation

Large 5 1.47642 3.6294720

Medium 5 0.660840 4.8718062

Small 109 1.67366 10.6762216

Total 119 1.62282 10.2769574

Table: 5.21 Test of Homogeneity of Variances

ROS

Levene Statistic df1 df2 Sig.

2.617 2 116 0.077

Table: 5.22

ANOVA

ROS Sum of Squares Df Mean Square F Sig.

Between Groups 5.016 2 2.508 0.023 0.977

Within Groups 12457.655 116 107.394

Total 12462.671 118

From the above analysis we can conclude that as the return increases risk also increases. In case

of small NBFCs stock on return is1.67366 and risk is 10.6762216. For medium NBFCs return on

stock is 0.660840 and risk is 4.8718062, and for large NBFCs return on stock is1.47642 and risk

45

are 3.6294720. So there is no need of further analysis. This is descriptive analysis and we are not

taking whole population, its sample based so there is no need of further analysis.

From above homogeneity of variance is 0.077 which more than 0.05 so there is no significance

difference between the stock variance of small, medium, large NBFCs. Thus, one can compare

means of stock returns through ANOVA.

From the above ANOVA table we have found that significance value is 0.977 which is more

than 0.05 so the null hypothesis is accepted. Therefore we can conclude that there is no

significance difference between stock returns of small, medium and large NBFCs.

46

CHAPTER 6

FINDINGS

47

The significant (2-tailed) in our table is 0.000. This value is less than 0.05; because of

this we can conclude that return on stock is Non banking financial company is different

than banks stock return.

The significant (2-tailed) in our table is 0.545. This value is more than 0.05, because of

this we can conclude that earning per share in Non banking financial company is different

than banks earning per share.

The significant (2-tailed) in our table is 0.265. This value is more than 0.05, because of

this we can conclude that return on equity of Non banking financial company is different

than banks stock equity.

The significant (2-tailed) in our table is 0.546. This value is more than 0.05, because of

this we can conclude that esp. of private bank is different than public bank earnings per

share.

The significant (2-tailed) in our table is 0.152. This value is more than 0.05; because of

this we can conclude that return on equity of private bank is different than public bank

return.

The significant (2-tailed) in our table is 0.002. This value is less than 0.05; because of

this we can conclude that return on stock of private bank is different than public bank.

From the homogeneity of variance is 0.000 which less than 0.05 so there is significance

difference between the earning per share variance of small, medium, large NBFCs.

Robust Tests of Equality of Means is 0.107 which is more than 0.05. So Therefore we

can conclude that there is no significance difference between earning per share of small,

medium and large NBFCs.

From the ANOVA table we have found that significance value is 0.460 which is more

than 0.05 so therefore we can conclude that there is no significance difference between

stock returns of small, medium and large NBFCs.

48

From the ANOVA table we have found that significance value is 0.977 which is more

than 0.05 so therefore we can conclude that there is no significance difference between

stock returns of small, medium and large NBFCs.

49

CHAPTER 7

CONCLUSIONS

50

The research study title is “Banking v/s nonbanking financial companies analysis “On the

basis of the study, analysis of the financial data it can be concluded the comparison of banks and

NBFCs segment. The return of stock is bank is more comparing Non banking financial company,

so investor’s point of view is investment on bank companies more become they give more return.

The earnings per share bank are same as Non banking financial company. And the return on

equity is bank and Non banking financial company are also same as so bank is most of the

financial performance is same Non banking financial company but return on stock is different.

It can conclude the comparison of private bank and public bank segment. The return of stock is

private bank are more than the public bank. So investors point of view is investment private bank

more than public bank become they give more return. The earnings per share private are same as

public bank. And the return on equity is private bank and public bank are also same, so private

bank is most of the financial performance is same public bank but return on stock is different.

We can say that investors are more protecting investing in bank sectors comparing non banking

financial sectors.

51

APPENDICES

1. BIBLIOGRAPHY BOOKS:

1. Philip Kotler, “Marketing Management” 12 Edition Person Education.

2. I M PANDEY, “Financial Management” 10 Edition.

WEBLINK:

http://www.rbi.org.in/scripts/PublicationReportDetails.aspx?ID=456

http://www.rbi.org.in/scripts/FAQView.aspx?Id=58 http://habibahmadazmi.blogspot.in/

52

REFERENCES:

• Simcox, “Primitive Civilization or Outlines of the History of Ownership in Archaic

Communities, Vol. I, Swan Sonnensichein and Co., London (1894)

• Subarea aiyar, “Economic Life in a Malabar Village. The Bangalore Printing and

Publishing Co. Ltd., Bangalore, (1925). P.66

• Logan, William.The Malabar Manual, 1887, reprinted as Malabar by the Government of

Madras, Vol.1, (1951), p.173.

• V.Krishnan, “Indigenous Banking in South India, The Bombay State Co-operative Union,

Bombay, (1959)

• S.K. Basu, Non- Banking Financial Intermediaries and Monetary Policy, the Banker

(New Delhi), February 1961, pp. 755-761.

• C.D.Campbell and C.S. Ahn, “Kyes and Mujin-Financial Intermediaries in South Korea,”

Economic Development and Cultural Change 11 (1962): pp.55-68.

• Ardener,“ The Evolution of an Informal Financial Institution: The Rotating Savings and

Credit Associations in Cameroon” (1964)

• M.S. Joshi, “Financial Intermediaries in India”, University of Bombay, Series in

Monetary and International Economics, No. 8, 1965.

• Srinivas and Higuchi, “A Continuum of Informality of Credit: What Can Informal

Lenders Teach Us?” Savings and Development, No. 2 XX, Fin Africa, (1966).

• Sreedharan Menon, K.A.Schemes for starting Chitties under State Auspecies,

• Government of Kerala, (1967), p.16.