analysis of the strategic interaction among established ... · through the interviews held with...

TRANSCRIPT

Supervisor:

Prof. ANTONIO GHEZZI

Master Graduation Thesis by:

ERIK SUDATI

837933

A.A. 2015/2016

Master of Science in Management Engineering

Analysis of the Strategic Interaction among

Established Corporations and Startups in Italy

TABLE OF CONTENTS ABSTRACT ................................................................................................................................... I

SOMMARIO ............................................................................................................................... II

EXECUTIVE SUMMARY ............................................................................................................... X

INTRODUCTION .......................................................................................................................... 1

LITERATURE REVIEW .................................................................................................................. 3

1. CORPORATE ENTREPRENEURSHIP ............................................................................................................. 3

2. CORPORATE VENTURE CAPITAL ................................................................................................................ 6

2.1 CORPORATE ENTREPRENEURSHIP AND CVC ....................................................................................... 6

2.2 HISTORY AND PHASES ......................................................................................................................... 7

2.3 DEFINITION AND CONTEXT .................................................................................................................. 8

2.4 CHARACTERISTICS OF CVC PROGRAMS ............................................................................................. 11

2.4.1 CVC OBJECTIVES.......................................................................................................................... 11

2.4.2 CVC STRUCTURE AND TYPOLOGY ............................................................................................... 12

2.5 FOUR INVESTOR COMPANY ARCHETYPES ......................................................................................... 14

3. OPEN INNOVATION AND CVC: A LOOK TO THE FUTURE ......................................................................... 17

3.1 R&D AND EXTERNAL INNOVATION .................................................................................................... 19

3.2 THE FUTURE OF CVC .......................................................................................................................... 20

4. HOW TO SET UP A STARTUP ENGAGEMENT SOLUTION.......................................................................... 22

4.1 STEP 1 – CLARIFY YOUR OBJECTIVES ............................................................................................. 22

4.2 STEP 2 – CONSIDER THE PROGRAM OPTIONS ............................................................................... 23

4.3 STEP 3 – CONNECT POTENTIAL RESOURCES .................................................................................. 25

THE FRAMEWORK .................................................................................................................... 27

5. CRITERION OF INCLUSION ....................................................................................................................... 27

6. STRUCTURE .............................................................................................................................................. 29

6.1 GENERAL INFORMATION ........................................................................................................... 30

6.2 SOLUTION CHARACTERISTICS .................................................................................................... 30

6.3 NOTES ........................................................................................................................................ 31

METHODOLOGY ....................................................................................................................... 32

7. TOOLS FOR DATA COLLECTION ................................................................................................................ 32

7.1. SECONDARY SOURCES INVESTIGATION ............................................................................................ 32

7.2 DIRECT PERSONAL INTERVIEWS ........................................................................................................ 33

7.2.1 THE SURVEY ................................................................................................................................ 33

RESEARCH AND ANALYSIS ........................................................................................................ 35

8. THE MAP .................................................................................................................................................. 35

8.1 MAP ................................................................................................................................................... 35

8.2 REMARKS AND INSIGHTS ................................................................................................................... 45

8.2.1 REMARKS .................................................................................................................................... 45

8.2.2 INSIGHTS ..................................................................................................................................... 45

9. CRITICAL ANALYSIS .................................................................................................................................. 48

9.1 RESULTS ............................................................................................................................................. 48

9.2 BENEFITS, LIMITS, AND OPPORTUNITIES ........................................................................................... 51

CONCLUSIONS .......................................................................................................................... 55

REFERENCES ............................................................................................................................. 59

LIST OF FIGURES Figure 2.1 – CVC phases (BCG, 2012)

Figure 2.2 – business opportunities framework (Volans, 2014)

Figure 2.3 – CVC models categorization (BVCA, 2012)

Figure 2.4 – Investment trajectory (Volans, 2014)

Figure 2.5 – CVC investments map (Chesbrough, 2002)

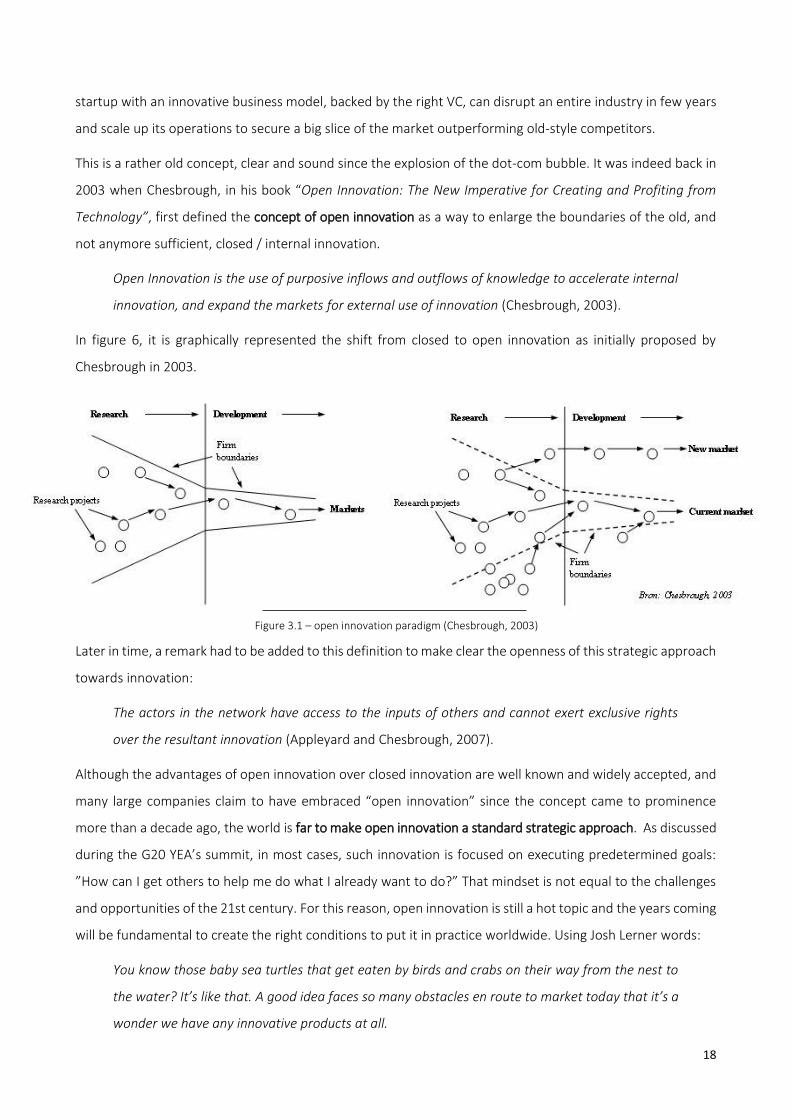

Figure 3.1 – open innovation paradigm (Chesbrough, 2003)

Figure 3.2 – evolution of open innovation (Accenture, 2015)

Figure 4.1 – startup engagement programs (Nesta, 2015)

Figure 4.2 – resource commitment through the various programs (Nesta, 2015)

Figure 9.1 – global quarterly CVC financing history (CB Insights, 2016)

Figure 9.2 – global quarterly CVC financing history (CB Insights, 2016)

Figure 9.3 – global corporate VC vs. Corporation financing (CB Insights, 2016)

LIST OF TABLES AND GRAPHS Table 1.1 – Corporate Entrepreneurship definitions (personal elaboration)

Table 6.1 – STRUCTURE, dimension of the framework (personal elaboration)

Table 6.2 – GROWTH STAGE, dimension of the framework (personal elaboration)

Table 8.1 – COLORS LEGEND of the solution category in the map (personal elaboration)

Table 8.2 – COMMITMENT OF THE COMPANY in terms of number of solutions and types of solution implemented (personal elaboration)

Table 8.3 – SYNTHETIC TABLE of the number of solutions (category and type) implemented by Italian companies (personal elaboration)

Graph 8.1 – PARETO CHART of the distribution of open innovation programs/practices. In red, the cumulative line as a percentage of the total (personal elaboration).

I

ABSTRACT In a highly competitive landscape marked by a rapid technological progress, today corporations all over the

world see the power of startups growing; they see newly created ventures grow exponentially and quickly

disrupting the industry where they operate. From here the need for established corporations to become more

entrepreneurial and to interiorize the power of disruption instead of fighting it. This study wants to capture an

updated image of the strategic interaction among corporations and startups in Italy by analyzing the startup

engagement solutions backed by Italian corporations; solutions that are seen as one – but not the only – stra-

tegic management practice to institutionalize entrepreneurship. The study presents a map of the Italian

startup engagement solutions backed by established corporations; it shows the level at which Italian corpora-

tions are involved in interaction with startups, what are the factors at the base of the current level of adoption,

the limits and the opportunities for future development.

The study gave as result that there are twenty-two Italian companies implementing disruptive open innovation

solutions through forty different programs or practices, and, under a deeper view, the four most committed

companies account for the 40% of the total corporate practices/programs implemented in Italy. The results

stemming from the map, when put in comparison with the level of adoption of startup engagement solutions

by companies in the world, shows how Italy is far behind the most developed countries, and is experiencing

an underdeveloped situation. Through the interviews held with some of the Italian corporate venture capital-

ists, it was possible to see that adopting a solution of strategic interaction with startups (in the case of the

interviews, CVC programs) brings always an advantage in terms of improvements of the current strategy or of

optionality for the future strategy. Regarding the limits and the reasons at the base of the low diffusion of the

solution of open innovation with startups In Italy, it came out that the phenomenon is underdeveloped due to

both problems related to the investors (the companies) and problems related to the investees (the startups).

The former are related to an old and risk-averse management culture coupled with a lack of preparation in

the field; the latter are related to a low-value startup ecosystem in the country triggered (also) by a suboptimal

funding by all the investors (institutional and private).

II

SOMMARIO Oggigiorno, in un panorama altamente competitivo segnato da un rapido progresso tecnologico, le aziende di

tutto il mondo vedono il potere delle startup crescere: vedono società appena create crescere esponenzial-

mente e sconvolgere velocemente i settori di mercato dove operano. Da qui il bisogno per le aziende consoli-

date di diventare più imprenditoriali e interiorizzare il potere di creare disruption invece che combatterlo. Lo

studio presenta come e a che livello le aziende italiane sono coinvolte in interazione con startup, quali sono i

fattori alla base di questo livello e le opportunità per lo sviluppo futuro. In dettaglio, lo studio si prefigge di:

1) mappare all’interno di un framework originale tutte le aziende che stanno attualmente implementando

programmi o pratiche di open innovation con startup, con l’obiettivo di internalizzare il potere di creare di-

sruption che queste nuove società portano in sé stesse. Tra le diverse soluzioni che una società può imple-

mentare per entrare in contatto con startups, il framework considererà, seguendo un definito criterio di inclu-

sione, CVC programs, incubatori/acceleratori, collaborazioni e startup competitions.

2) dare, alla luce della ricerca precedentemente condotta, una interpretazione critica del livello di adozione

dell’interazione tra aziende e startup in Italia come pratica strategica, presentando le ragioni dietro a questo

risultato e gli ostacoli che ne intralciano la diffusione, i benefici derivanti dall’implementazione e le possibili

opportunità di sviluppo futuro. Questa interpretazione critica del fenomeno sarà redatta tramite interviste

qualitative con manager a capo delle soluzioni di startup engagement più strutturate e di spicco.

STRUTTURA DEL PAPER – dopo l’introduzione, c’è la sezione Literature Review, che dà una solida base teoretica

al campo sotto investigazione e va a costituire l’insieme di ipotesi alla base della ricerca empirica. Il paper

continua con la sezione The Framework, dove, come suggerisce il titolo, è introdotto in dettaglio il framework

all’interno del quale le differenti soluzioni di startup engagement sono mappate. All’interno di questa sezione

è anche spiegato il criterio di inclusione che sta alla base della selezione dei tipi di soluzioni di startup engage-

ment. Segue la sezione Methodology, che dà una descrizione completa e accurata delle metodologie e delle

tecniche utilizzate per raccogliere i dati e analizzarli. Dopo aver impostato la metodologia adottata per l'analisi,

segue la sezione Research and Analysis, in cui i risultati della ricerca sono presentati e poi analizzati. Infine, la

carta si chiude con la sezione Conclusions dove è redatta una analisi critica dei risultati e si sottolinea Il contri-

buto che essi possono apportare e lo spazio che possono aprire a successive ricerche.

LITERATURE REVIEW

Questa sezione del documento mira a dare un solido basamento teorico all’oggetto di indagine: lo spazio in

cui le imprese incontrano l'ecosistema startup per perseguire obiettivi strategici. Inoltre, la Literature Review

III

rappresenta il fondamento della ricerca empirica, dal momento che il processo di mappatura prenderà riferi-

mento dagli aspetti e dimensioni illustrati in questa sezione. I programmi di CVC sono il primo tipo di soluzione

di startup engagement analizzato, in quanto più strutturati e di conseguenza quelli che meglio rappresentano

il fenomeno. CVC è innanzitutto inquadrato dal punto di vista teorico come pratica manageriale legata alla

corporate entrepreneurship, e successivamente analizzato da altri punti di vista. Dopo questa ampia analisi

della letteratura riguardante il CVC, vengono prese in considerazione le altre soluzioni di startup engagement

volte all’open innovation.

CORPORATE ENTREPRENEURSHIP – processo attraverso il quale una azienda si impegna in una diversificazione

attraverso uno sviluppo interno ed esterno. Tale diversificazione richiede nuove combinazioni di risorse per

estendere le attività della azienda in settori non correlati, o marginalmente legati, al suo attuale dominio di

competenza e le sue corrispondenti opportunità. Questo processo consiste nella realizzazione di attività di

innovazione (ad esempio la creazione e l'introduzione di prodotti, processi di produzione e sistemi organizza-

tivi), il rinnovo (ad esempio rivitalizzare le operazioni della società attraverso la creazione o acquisizione di

nuove capacità), e il venturing (entrare in nuovi business espandendo le operazioni in mercati nuovi o esi-

stenti).

CORPORATE VENTURE CAPITAL – i programmi di CVC possono essere inclusi nella lista delle possibili applica-

zioni della corporate entrepreneurship orientare all’esterno. CVC è un fenomeno che comporta la fusione e la

combinazione di risorse interne con quelle esterne al fine di individuare nuove opportunità e garantire il futuro

delle grandi imprese consolidate. Ci sono più di 1.200 aziende in tutto il mondo con programmi di CVC, più

della metà dei quali formate dal 2010 in poi. Le aziende stanno usando CVC come un modo per accedere a

nuovi e dirompenti tecnologie, per sviluppare nuovi modelli di business e per partecipare nei mercati emer-

genti; tutte strategie che possono fornire un contributo significativo alla crescita aziendale.

Tuttavia, potrebbe essere semplicistico affermare che il CVC è in crescita. Più corretto sarebbe dire che il CVC

è tornato in grande stile. Fin dalla sua comparsa nel 1960 ci sono stati in linea di massima tre ondate di svi-

luppo, con una emergente quarta onda in corso.

Per quanto riguarda la definizione di CVC, ci sono diverse scuole di pensiero. Nel 2002 Chesbrough ha definito

CVC dando precise regole di inclusione ed esclusione. Al giorno d'oggi, al contrario, gli operatori del settore

preferiscono non dare una definizione troppo ristretta di CVC e hanno quindi rimosso la maggior parte delle

regole di confinamento specificate nel decennio precedente. Secondo la loro esperienza, confinando CVC in

una definizione eccessivamente restringente si escluderebbero di certo alcuni programmi di investimento che

potrebbero invece dare preziosi spunti al mercato. Con ciò presente, questo documento adotterà come rife-

rimento la seguente definizione sintetica proposta da Dushnitsky:

IV

CVC è definito come un investimento di minoranza in equity da parte di una impresa consolidata

in una impresa privata. Tre fattori sono comuni a tutti gli investimenti CVC. In primo luogo, mentre

i rendimenti finanziari sono una considerazione importante, ci sono spesso obiettivi strategici che

motivano le attività di CVC. In secondo luogo, le imprese finanziate sono tenute private e indipen-

denti (legalmente e non) dalla società di che ha investito. In terzo luogo, l'azienda che investe

riceve una quota di partecipazione azionaria di minoranza. (Dushnitsky, 2008)

I modelli di CVC possono essere sintetizzati in tre modelli principali. Quattro aspetti primari del fondo sono

descritti, come mostrato in figura, per ciascuno dei tre modelli. Inoltre, un quarto modello ibrido sarà aggiunto

ai seguenti tre.

Il quarto modello è chiamato Syndication e consiste in un co-investimento della società con altri investitori per

ridurre il rischio e aumentare il capitale investito. Questo tipo di co-investimento può essere fatto indiretta-

mente attraverso un fondo controllato o direttamente con un investimento di bilancio.

IL FUTURO DEL CVC - Oltre al ruolo chiave che il CVC ricopre nell’innovazione oggi, è importante capire l’evo-

luzione che può avere il CVC dal punto di vista dell’open innovation, intesa come pratica per generare inten-

zionalmente un flusso bi-direzionale di conoscenza che favorisca l’innovazione, utile sia all’interno dell’azienda

che verso l’esterno. Secondo il report G20 YEA summit, CVC rappresenta solo il primo passo che una grande

azienda può compiere per iniziare una strategia di open innovation. Come mostrato nella seguente figura,

l’open innovation è un cammino che si articola in quattro fasi e vede l'applicazione di quattro strumenti diversi.

Chiaramente l’uno non esclude l’altro, e la massima espressione si ottiene con l’adozione di tutti questi stru-

menti:

Categorizzazione dei modelli di CVC (BVCA, 2012)

V

COME IMPOSTARE UNA STARTUP ENGAGEMENT SOLUTION – In questo paragrafo si delineano tutti i modi at-

traverso i quali una società può scegliere di interagire con l'ecosistema startup. Prima di pensare a quale solu-

zione di startup engagement implementare, è necessario chiarire gli obiettivi che l'azienda vuole raggiungere:

ringiovanire la cultura aziendale, innovare grandi e vecchi brand, risolvere problemi di business, o espansione

futura in nuovi mercati. Una volta decisi gli obiettivi principali, è il momento di individuare un programma

adatto tra tutte le possibili opzioni: eventi a sé stanti, condivisione di risorse, supporto del business, collabo-

razione, investimento, acquisizione. L’ultimo step è quello di connettere le potenziali risorse per attuare il pro-

gramma: denaro, tempo degli impiegati dell’azienda, prodotti, asset intangibili.

IL FRAMEWORK

Come accennato nell'introduzione, questo documento ha come primo obiettivo quello di mappare in un fra-

mework originale tutte le aziende italiane che stanno attuando programmi o pratiche di open innovation con

startup. Tra le diverse soluzioni che una società può implementare per interagire con startup, il quadro pren-

derà in considerazione solo i programmi di CVC, incubatori / acceleratori e startup competition.

Nei paragrafi seguenti è spiegato il criterio di inclusione che governa la selezione delle soluzioni di startup

engagement che siano coerenti con l'obiettivo della ricerca. Inoltre, è presentato il framework nel quale le

soluzioni sono inquadrate e organizzate.

Evoluzione dell’open innovation (Accenture, 2015)

VI

CRITERIO DI INCLUSIONE - Lo studio si rivolge a tutte le soluzioni di open innovation guidate da scopi strategici:

quelli volti a sostenere la strategia corrente attraverso l'innovazione, o quelli volti ad assicurarsi opzioni future

per lo sviluppo del proprio business. In poche parole, queste soluzioni, per esser selezionate, devono essere

volte ad internalizzare il potere di creare disruption, riportando un approccio imprenditoriale all'interno di una

società consolidata e ormai rigida. Inoltre, per escludere tutte quelle pratiche occasionali, la ricerca si concentra

sulle soluzioni che sono istituzionalizzate, strutturate e attuate sistematicamente con continuo impegno.

STRUTTURA - Ora che il criterio di inclusione alla base della selezione è stato introdotto, è possibile spostarsi

sul come le informazioni raccolte sono inquadrate ed organizzate. In questo schema, tutte le soluzioni di open

innovation che includono una interazione con l'ecosistema startup - programmi di CVC, incubatori / accelera-

tori, partnership e concorsi di avvio - verranno mappati, e le loro caratteristiche delineate attraverso le dimen-

sioni a più livelli della mappa.

Al livello più alto, il quadro mostra quattro categorie di dimensioni:

Informazioni generali

Questa categoria identifica le soluzioni di startup engagement e le aziende che vi stanno alle spalle.

Comprende 2 dimensioni: azienda (il nome dell’azienda che implementa la soluzione), nome del pro-

gramma (il nome ufficiale del programma, se c’è).

Caratteristiche della soluzione

Questa categoria comprende tutte le dimensioni necessarie per descrivere una soluzione di intera-

zione strategica con startup. I modelli di struttura di un programma di CVC può riferirsi a: categoria

della soluzione (i 4 modelli di CVC programmi, partnership, incubatori / acceleratori , startup competi-

tion), settori target (aree di mercato su cui l'azienda sta convergendo i suoi sforzi), fase di crescita della

startup oggetto di interesse (pre-seed, seme, presto, tardi fase).

Note

Le note mostrano tutte le informazioni aggiuntive di contorno che potrebbero essere necessarie per

meglio illustrare le soluzioni, che in molti casi sono uniche. Informazioni aggiuntive (ciò che non può

essere detto attraverso i numeri; le peculiarità che caratterizzano la soluzione), contatti (contatti e-

mail della soluzione), link (il link al sito della soluzione, nel caso l'azienda abbia una pagina web dedi-

cata).

RICERCA E ANALISI

In questa sezione verrà presentato il vero e proprio centro del paper; ciò che la ricerca empirica ha portato

alla luce. Come accennato nell’introduzione, l'obiettivo di questo studio è distribuito su due fasi successive: la

mappatura e l'analisi critica dei risultati.

VII

Mappatura (The Map)

È fondamentale prima di tutto fare una considerazione per quanto riguarda il tipo di soluzione “partnership”.

La tabella sintetica riporta come risultato "NA", non disponibile, in quanto questo tipo di soluzione non è stato

inserito nella mappatura. Questo però non significa che in Italia non ci sono partnership con start-up, infatti si

possono individuare alcune aziende che attualmente investono in programmi di co-sviluppo, ma alcune diffi-

coltà hanno reso difficile inquadrare tutte queste aziende nella mappa: prima di tutto, le partnership sono

molto difficili da individuare, soprattutto quando sono l'unica soluzione che una società implementa; in se-

condo luogo, sono pratiche strategiche che una società spesso non vuole rivelare. Pertanto, nonostante sia

legittimo presumere che una società già impegnata in un programma di interazione con startup implementi

anche una partnership, non sarà mai possibile inquadrare tutte le aziende che in Italia attuano questo tipo di

soluzione. Inoltre, le partnership con startup possono essere implementate in infiniti modi, spesso personaliz-

zati a seconda degli attori coinvolti e questo rende difficile tenerne traccia. Per tutte queste ragioni, dato il

fatto che non è possibile presentare un quadro completo di tutte le collaborazioni attive in Italia, questa solu-

zione è stata totalmente omessa dalla mappatura.

Per quanto riguarda le altre soluzioni, la mappatura ha individuato ventidue aziende italiane che implemen-

tano soluzioni di open innovation attraverso quaranta diversi programmi o pratiche. Solamente dieci di queste

ventidue aziende portano avanti più di una soluzione (programmi o pratiche). Facendo un’analisi più appro-

fondita, le quattro imprese più virtuose (con più soluzioni all’attivo) contano per il 40% del totale delle pratiche

/ programmi. Tra queste, UniCredit è l'unica azienda in Italia ad implementare tutti i tipi di soluzioni di open

innovation (CVC, Incubatori/acceleratori e startup competition). Analizzando il tipo di soluzioni messe in atto

da queste ventidue imprese, è possibile trarre le seguenti conclusioni: tredici aziende stanno facendo investi-

menti in capitale di rischio di start-up attraverso l'attuazione di un totale di diciotto diversi programmi di CVC.

La maggioranza delle aziende che adotta uno dei quattro modelli di CVC implementa almeno un altro tipo di

SOLUTION CATEGORYN° OF SOLUTIONS

IMPLEMENTEDTYPE OF SOLUTION N° OF BACKING COMPANIES

CORPORATE DIRECT INVESTMENT 4

INTERNAL DEDICATED FUND 6

EXTERNAL FUND 3

SYNDICATION 5

ACCELERATOR / INCUBATOR 17 ACCELERATOR / INCUBATOR 13

STARTUP COMPETITION 5 STARTUP COMPETITION 5

PARTNERSHIP N/A PARTNERSHIP N/A

13CVC PROGRAM

Tabella sintetica del numero di soluzioni (categoria e tipo) implementate da aziende italiane

VIII

soluzione. Per quanto riguarda i diversi modelli di CVC, si può notare che i fondi dedicati sono maggiormente

concentrati su investimenti early / late stage, mentre gli investimenti diretti a bilancio sono più orientati sulla

fase pre-seed / seed. Interessante inoltre notare che Il terzo modello di CVC, la partecipazione come LP ad un

fondo esterno, è attuato solo da banche (Unicredit e Intesa San Paolo). Per quanto riguarda gli investimenti in

syndication con altri investitori, in quattro casi su cinque il co-investimento è attuato dalle imprese attraverso

investimenti diretti a bilancio. Muovendosi su un altro tipo di soluzione, incubatori / acceleratori, la ricerca

mostra che sono tredici le società che offrono un programma di incubazione / accelerazione per startup, e che

Alcune aziende stanno anche realizzando più di un programma di incubazione / accelerazione (Enel, Buon-

giorno, Zambon). Va inoltre sottolineato che Acceleratori / incubatori sono spesso gestiti in collaborazione con

altri soggetti, al fine di ottenere il massimo beneficio possibile dall’open innovation. Per concludere, cinque

aziende stanno proponendo startup competition. In tre casi su cinque, questi contest sono fini a sé stessi,

mentre nel resto dei casi si tratta di pratiche per selezionare startup e fare uno screening iniziale che sarà poi

seguito da incubazione, accelerazione, partnership o investimento in equity.

Analisi Critica

Quando i risultati derivanti dalla mappatura sono messi a confronto con il livello di adozione di soluzioni di

open innovation da parte di aziende in tutto il mondo, si vede chiaramente che l'Italia è molto indietro rispetto

ai paesi più sviluppati, e sta vivendo una evidente situazione di sottosviluppo. Attraverso le interviste fatte con

alcuni dei corporate venture capitalist italiani, è stato possibile indagare le ragioni alla base di questi risultati,

gli ostacoli che impediscono la diffusione di queste pratiche di interazione con startup e le possibili opportunità

di sviluppo futuro. Secondo gli intervistati, l'adozione di una soluzione di interazione strategica con startup (nel

caso delle interviste, programmi CVC) porta sempre un vantaggio in termini di miglioramento della strategia

corrente o di opzionalità per strategie future. Per quanto riguarda i limiti e le ragioni alla base della scarsa

diffusione di questo fenomeno in Italia, sono state evidenziate sia cause legate agli investitori (le aziende), che

problemi relativi alle partecipate (startup). I primi sono legati ad una cultura aziendale italiana inadeguata e

avversa al rischio, unita ad una chiara mancanza di preparazione su questi temi; i problemi esterni invece, sono

riconducibili a uno scarso valore dell’ecosistema startup nel paese, dovuto (anche) ad un finanziamento non

ottimale da parte di tutto il comparto di investitori (istituzionali e privati). Di conseguenza, dove il venture

capitalism ha una maggiore portata, è più facile per una società trovare startup nelle quali valga la pena inve-

stire. Pertanto, data una buona preparazione e la giusta cultura all'interno dell'azienda, più è di valore l'ecosi-

stema startup in cui l'azienda è situata, maggiori sono i vantaggi ottenibili dall'interazione con esso. Detto ciò,

da questa situazione italiana poco matura, alcune opportunità di sviluppo potrebbero ancora emergere se

venissero attuati gli interventi coretti: gli investitori dovrebbero riuscire a chiudere deal più redditizi, il governo

dovrebbe favorire e attirare gli investitori internazionali, e, inoltre, sarebbe necessario sia un cambiamento di

mentalità per superare la barriera culturale di avversione al rischio, sia un impegno costante da parte di tutti

gli attori del venture capitalism italiano.

IX

X

EXECUTIVE SUMMARY In a highly competitive landscape marked by a rapid technological progress, today corporations all over the

world see the power of startups growing; they see newly created ventures grow exponentially and quickly

disrupting the industry where they operate. From here the need for established corporations to become more

entrepreneurial and to interiorize the power of disruption instead of fighting it. The study presents how and

at which level Italian corporations are involved in interaction with startups, what are the factors at the base of

the current level of adoption and what are the opportunities for future development. In details, the study will:

1) Map within an original framework all the Italian companies that are currently implementing programs or

practices of open innovation with startups, with the aim of internalize the power of disruption that these new

ventures bring within themselves. Among the different solutions that a corporation can implement to engage

with startup, the framework will consider CVC programs, incubators/accelerators, partnerships and startup

competitions, following a defined criterion of inclusion.

2) Give, in light of the research previously conducted, a critical interpretation of the level of adoption of the

interaction among corporations and startups in Italy as a strategic practice, presenting the reasons behind

these results and the obstacles that hinder the diffusion, alongside with the benefits stemming from the im-

plementation and possible opportunities for future development. This critical interpretation of the phenome-

non will be outlined through qualitative interviews with the managers in charge of the most prominent and

structured corporate startup engagement programs (CVCs).

STRUCTURE OF THE PAPER – after the introduction, there is the section Literature Review, which gives solid

theoretical basement to the field under investigation and constitutes the set of assumptions at the base of the

empirical research. The paper continues with the section The Framework, where, as the title suggests, it is

introduced in details the framework under which the different corporate startup engagements solutions are

mapped. Within this section is also explained the criterion of inclusion at the base of the selection of the

corporate startup engagement solutions. It follows the Methodology, which gives a complete and accurate

description of the methodologies and techniques used for gathering the data, analyzing them, and reflecting

over their contribution. After having set the methodology adopted for the analysis, it follows the section Re-

search and Analysis, where the findings of the research are presented and then analyzed. Finally, the paper

closes with the section Conclusions, where the findings are presented under a critical view and it is highlighted

the contribution they can give and the space they can open to further studies and researches.

XI

LITERATURE REVIEW

This section of the paper aims at giving a solid theoretical basement to the field under investigation: the space

where corporations meet the startup ecosystem to pursue strategic goals. Moreover, the literature review

represents the foundation of the empirical research, as the process of mapping will take reference from the

aspects and dimensions outlined in this section. CVC program is the first startup engagement solution analyzed

in the Literature Review, as it is the most structured and consequently the one that best represents the phe-

nomenon of interaction corporation-startup. CVC is firstly framed as a management practice in the wider the-

oretical field of corporate entrepreneurship and then deeply analyzed under other different perspectives. Af-

ter this extensive analysis of the literature regarding CVC, the other startup engagement solutions are taken

into account, introduced and analyzed.

CORPORATE ENTREPRENEURSHIP – both scholars and practitioners agree upon the necessity for a company to

implement corporate entrepreneurship activities to ensure the survival of the business. Despite this, the liter-

ature does not comprehend a commonly shared definition of corporate entrepreneurship and, in the last 30

years, many definitions have been proposed and even addressed with different terms: corporate entrepre-

neurship, corporate venturing, intrepreneuring, intrapreneurship, internal entrepreneurship, venturing, stra-

tegic renewal. Despite the definitions for corporate entrepreneurship are abundant, all of them are based on

the same elements and follow a common pattern. For this reason, corporate entrepreneurship can be broadly

defined so to include all the common core components. Merging Zahra and Burgelman’s definitions, the most

complete ones, it is possible to define corporate entrepreneurship in a more comprehensive way as:

The process whereby the firms engage in diversification through internal and external develop-

ment. Such diversification requires new resource combinations to extend the firm’s activities in

areas unrelated, or marginally related, to its current domain of competence and corresponding

opportunity. This process consists in the implementation of a company’s activities of innovation

(i.e. creating and introducing products, production processes and organizational systems), renewal

(i.e. revitalizing the company’s operations by building or acquiring new capabilities, and by chang-

ing the scope of its business or competitive approach), and venturing (i.e. entering new businesses

by expanding operations in existing or new markets).

CORPORATE VENTURE CAPITAL – CVC programs can be included in the list of the possible applications of ex-

ternally-oriented corporate entrepreneurship. A phenomenon that entails the fusion and combination of in-

ternal resources with external ones in order to spot out new opportunities and ensure the future of big con-

solidated corporations. There are more than 1,200 corporations worldwide with CVC programs, more than

half of which were formed since 2010. Companies are using CVC as a compelling way to drive outside-in inno-

vation to access new and disruptive technologies, to develop new business models and to participate in emerg-

ing markets; all strategies that may provide meaningful contributions to corporate growth.

XII

However, it might be simplistic to state that corporate venture capital investing is growing. More correct would

be saying CVC is back in style. Since its appearance in the 1960s there have been broadly three waves of de-

velopment, with an emergence of a fourth wave underway.

Regarding the definition of CVC, there are different school of thoughts. Chesbrough defined CVC in 2002

giving precise rules of inclusion and exclusions. Nowadays, conversely, practitioners prefer not to give a too

narrow definition of CVC and have then removed most of the exclusions and boundaries specified in the pre-

vious decade. According to them, further confining CVC would for sure exclude some investment programs

that could give valuable insights to the industry. Bearing in mind this issue from practitioners’ side, this paper

will adopt as reference the following syntheticalal definition proposed by Dushnitsky:

CVC is defined as a minority equity investment by an established corporation in a privately-held

entrepreneurial venture. Three factors are common to all CVC investments. First, while financial

returns are an important consideration, there are often strategic objectives that motivate CVC

CVC phases (BCG, 2012)

XIII

activities. Second, the funded ventures are privately held considerations and are independent (le-

gally and otherwise) from the investing corporation. Third, the investing firm receives a minority

equity stake in the venture. (Dushnitsky, 2008)

To be more precise on the space CVC covers within the corporate management activities, it is useful to un-

derstand how a CVC program sets itself in the framework that comprises all the possible ways of creating

new business opportunities (figure2).

Given the current approach of defining CVC as a more open phenomenon, it is indeed important not to con-

fuse CVC with private or independent venture capital (VC or IVC). The General Partners (GPs) of VC fund as-

sess and invest in high growth potential businesses by deploying funds raised from external investors known

as Limited Partners (LPs). They hold the committed capital in a fund for 10 years (typically) dispersing returns

gained from the sale of investment businesses both during and at the conclusion of the fund’s lifetime. The

sole objective of such a fund is financial return. Conversely, CVC has both a strategic and a financial objec-

tive.

- Financial objective: providing financial return for the corporation. With increasing cash on balance

sheets, financially-driven CVC investments are looking to take some risk in exchange for high returns.

In this situation CVC and VC overlap (Volans, 2014).

Business opportunities framework (Volans, 2014)

XIV

- Strategic objective: developing capabilities, access and / or markets of the parent company, aligning

with long-term strategy. Multiple CVC units may be created to focus on different aspects of the strat-

egy – and they often adapt and evolve over time. A strategic CVC investment will identify and amplify

synergies between itself and the venture. To do so, it will provide management skills and other forms

of expertise to the investee (Volans, 2014).

At the end of the day, financial objectives are necessary to maintain internal support, while CVC’s ability in

meeting strategic objectives will be vital to long-term success.

Given the different objectives a CVC program can pursue and the intrinsic characteristics of the corporation

that implements it, the CVC models can be synthetized under three main models, which will be in turn included

in two wider and more general categories. Four primary aspects of the fund are described, as shown in figure

3, for each of the three model. In addition, a fourth hybrid model will be added to the following three.

Let’s go deeper in each of the three main CVC models:

1. Corporate direct investment: given the direct nature of the investment, where the money out-

flow is accounted as a balance sheet invoice, this type of investment program is closely linked to the

company’s value chain and business divisions. It is an in-house venture program, managed by internal

corporate talents and clearly addressed to support the company in pursue its strategic goals. Financial

performances are therefore secondary compared to the strategic ones.

2. Internal dedicated fund: The corporate VC is set up as a separate unit of the parent corporation

with an independently defined budget. The fund is managed by internal employees of the company as

CVC models categorization (BVCA, 2012)

XV

well as newly hired people, usually from the VC world. The management team is to all extents the

General Partner of the fund that usually carry interests to produce financial returns. Because of the

greater autonomy of this model respect to the first one, there are less internal pressures to invest in

startups where the prospects for a financial return are secondary to other corporate interests. It is

clear how the financial and strategic goals of investment coexist in this situation.

3. External fund: The company invests in an external fund, such as an independent VC, and act as a

Limited Partner. This solution is almost merely financial as the company has a low influence on the

investment decision taken by the GP of the fund. For this reason, this model of CVC is not suitable to

be a strategic approach of open innovation.

The aforementioned classification is part of a broader one that sees two general classes of investment

approaches:

- direct / on-balance-sheet investment: investing money of the company through an annual

budget. The investment is hence listed as an expense line (first model, figure 3). The invest-

ment activities is managed by the company’s personnel. It is relevant to mention a further

sub-classification, which includes in the direct form of CVC investments also joint-ventures

with other companies, spin-offs and step-by-step investments (occasional investment carried

on without strategic nor financial, but for marketing and brand-awareness reason, to under-

line a company’s presence in an industry). Despite these are minority equity investments, the

occasional nature excludes them from a current definition of CVC program.

- indirect / off-balance-sheet investment: investing involves a third party or separate fully-

owned fund where money is committed for a longer period. The fully-owned fund is a 100%-

captive fund where the company creates an independent subsidiary to invest its own capital

only (second model, figure 3). The third party fund can be either a semi-captive fund where

the company opens the fund to other investors or an external VC fund where the company is

just a LP (third model, figure 3). In both cases, the investment activities is managed by external

personnel (subsidiary or VC).

4. Syndication: this fourth model consists in a co-investment of the company with other investors to

reduce the risk and increase the capital invested. In the technical language, this type of investment is

called Syndication and can be done indirectly through a subsidiary fund or directly with an investment

out of balance sheet. This last model can be clearly noticed by the investment trajectory graph (figure

4) where the CVC area overlaps with VC (and sometimes PE, when deals are bigger). The framework

below shows how the different investors distribute their investment over the lifecycle phases of the

investee.

XVI

OPEN INNOVATION AND CVC – there is a statistically significant correlation between collaboration, innovation

and growth, among both large companies and startups, in all the G20 countries. The continuous innovation

paradigm has become an imperative, a rule rather than an opinion of few: most innovations fail. Yet, in the

long run, the risk of not innovating is greater than that of innovating. Companies that don’t continuously in-

novate will die. It is nowadays manifest that innovating is not an option, but a necessity. It is likewise clear that

innovating internally is not enough to guarantee a company’s success – a small startup with an innovative

business model, backed by the right VC, can disrupt an entire industry in few years and scale up its operations

to secure a big slice of the market outperforming old-style competitors.

This is a rather old concept, clear and sound since the explosion of the dot-com bubble. It was indeed back in

2003 when Chesbrough, in his book “Open Innovation: The New Imperative for Creating and Profiting from

Technology”, first defined the concept of open innovation as a way to enlarge the boundaries of the old, and

not anymore sufficient, closed / internal innovation.

Open Innovation is the use of purposive inflows and outflows of knowledge to accelerate internal inno-

vation, and expand the markets for external use of innovation (Chesbrough, 2003).

Later in time, a remark had to be added to this definition to make clear the openness of this strategic approach

towards innovation:

The actors in the network have access to the inputs of others and cannot exert exclusive rights

over the resultant innovation (Appleyard and Chesbrough, 2007).

Although the advantages of open innovation over closed innovation are well known and widely accepted, and

many large companies claim to have embraced “open innovation” since the concept came to prominence

more than a decade ago, the world is far to make open innovation a standard strategic approach. As discussed

during the G20 YEA’s summit, in most cases, such innovation is focused on executing predetermined goals:

”How can I get others to help me do what I already want to do?” That mindset is not equal to the challenges

and opportunities of the 21st century. For this reason, open innovation is still a hot topic and the years coming

will be fundamental to create the right conditions to put it in practice worldwide.

Corporations have narrowed the focus of their R&D by pressing for clear, short-term wins; venture

capitalists are too quick to get caught up in the latest, hottest thing; and even the vaunted crowd-

funding option is pretty limited: It’s great if you’re an internet star, but try getting a crowd excited

about an innovative idea in industrial machinery. It doesn’t have to be this way. Effective means

of boosting innovation already exist, but not enough companies are making use of them (Lerner,

2013).

One of the means Lerner mentioned is corporate venture capital.

XVII

THE FUTURE OF CVC – Besides the key role of CVC in the innovation context today, it is important to understand

what the future evolution of CVC can be under the light of open innovation. According to the report of G20

YEA’s summit, CVC represents just the first step for a large corporation to begin a strategy of open innovation.

As shown in Figure 7, open innovation is a journey of four phases that sees the application of four different

tools:

However, the state-of-art of open innovation lays in the application of a cohesive strategy that include a mix

of these tools together. It is trivial to say that a company able to achieve ecosystem innovation has most

probably already went through the previous three phases applying the respective tools.

HOW TO SET UP A STARTUP ENGAGEMENT SOLUTION – In this paragraph are outlined all the ways a com-

pany can choose to interact with the startup ecosystem. The explanation will also highlight the main steps a

manager should follow to set up a program of interaction with startups. The first thing to do, is clarify the

objectives the company wants to achieve: Rejuvenating corporate culture, innovating big brands, solving

business problems, expanding into future markets. Once the core objectives have been decided, it is time to

identify a suitable program among all the possible options of startup engagement. The second step is to con-

sider which program option to implement:

evolution of open innovation (Accenture, 2015)

XVIII

One-off events

Some corporates choose to attract startups through relatively self–contained events, that can have

different natures, but often take the form of competitions where participants are asked to solve spe-

cific challenges. These tend to be good starting points to drive internal culture change by exposing

employees to the entrepreneurial mindset of startups, provide new perspectives of emerging business

trends and technologies, and also foster external association of the corporate brand with innovation.

However, it is important to understand that these programs provide less immediate return in terms

of business relationships and also require careful consideration of the needs of the startups (Nesta,

2015). As aforementioned, these events can be light solutions only aimed at bringing some fresh en-

trepreneurial air within the organization, but they can also be harder strategic solutions where the

company wants to set the foundation to continue the interaction overtime; events that constitute the

first step in a more structured program (of incubation or even equity-based investment) aimed at

backing the current strategy or exploring new strategic paths.

Sharing resources

Sharing resources with startups can be a comparatively cheap way for corporates to build a more

innovative brand. However, it is important to understand that these programs, especially supplying

free tools, provide less immediate return in terms of business relationships (Nesta, 2015). The re-

sources commonly shared are free tools for startups and co-working spaces. In the first case, a com-

pany can give discounted or free access to software, physical products or knowledge; sharing tools is

also a way to create positive network externalities for a company’s products. In the second case, a

company gives a space where more startups can work together in a common space, where they have

free internet access and other tools to cover basic needs.

Business support

Corporates also operate various forms of business support programs, in particular incubators and ac-

celerators, that help the growth of early–stage startups and make them ready for investment, market

entry and scale (see paragraph 3.2 for more detailed information). These programs can be powerful

tools to foster culture change and internal learning by engaging employees as mentors or advisors.

However, whether these programs should be run directly by corporates or only in partnership with

third parties is a hotly debated topic. In any case, business support programs have to be designed with

the startup needs in mind, and not solely oriented towards the growth of the corporate host (Nesta,

2015).

XIX

Partnerships

Business partnerships can take many different forms, and may sit on a spectrum from the relatively

short–term, transactional engagement to the long–term, committed relationship (Nesta, 2015). The

most common partnership programs are product co-development and procurement. While product

co-development takes more time and requires big efforts from both the parts, procurement is a

quicker and easier program – for the company it is a way to access a new technology on the market,

and for startups is a quick way to scale up its operations (even though can be quite risky). partnerships

do not involve any equity investment as they are just commercial agreements. These programs, when

done with multiple and diverse actors, are a powerful tool of open innovation and they can be put

under the category Joint Innovation outlined in section 3.2.

Investments

Investing in equity is one way to develop a company’s business strategy. As already explained in the

previous sections, CVC programs, in their various forms, are the way a corporation can invest in

startups.

Acquisitions

It is the logical extension of corporate venturing that, as previously said, serves as a pipeline for future

M&A’s. Acquiring startups can be a quick and impactful way of buying complementary technology or

capabilities that solve specific business problems and enter new markets. It often happens that acqui-

sitions are just a way to hire new ready-made talents. Acquisitions with this strategic objective are

called acqui-hiring (Nesta, 2015).

The third and last step is to connect potential resources. Each corporate, be they medium–sized or large, has

resources it can leverage to bring a startup program to life: cash, employee time, products, intangible assets.

THE FRAMEWORK

As mentioned in the introduction, this paper has as first objective the one of mapping within an original frame-

work all the Italian companies that are currently implementing strategic programs or practices of open inno-

vation with startups. Among the different solutions that a corporation can implement to engage with startup,

the framework will consider just CVC programs, incubators/accelerators and startup competitions. In the sec-

tion 4 of the Literature Analysis, the study shown how different can be the ways of interacting with startups

for a corporation. Given the variety of ways of interaction seen, and the consequent variety of objectives that

lies underneath the choice to be implemented (financial, strategic, commercial, etc…), it is necessary to draw

the boundaries of the research.

XX

In the following paragraphs of this section is explained the criterion of inclusion that rules the selection of the

startup engagement solutions that are consistent with the objective of the research. In addition is outlined the

framework in which the selected startup engagement solutions are framed and organized.

CRITERION OF INCLUSION – The study targets all the open innovation solutions driven by strategic purposes:

the ones aimed at supporting the current strategy through innovation, or the ones aimed at securing options

on future strategic directions. In few words, these solutions must be aimed at internalizing the power of creat-

ing disruption by bringing an entrepreneurial approach within a stiff corporation. In addition, to exclude all those

occasional practices, the research focuses on the solutions that are institutionalized, structured and systemat-

ically implemented overtime under a continuous commitment. If for heavy solutions – called programs – it is

legit to assume that a company systematically implements a defined plan of interaction, regarding lighter so-

lutions – called practices – it can’t be always said the same.

THE STRUCTURE – Now that the rule of inclusion at the base of the selection has been introduced, it is possible

to move more in details on how the information collected is framed and organized. Under this framework, all

the Open Innovation solutions that include an interaction with the startup ecosystem – CVC programs, Incu-

bators/accelerators, partnerships and startup contests – will be mapped, and their characteristics outlined

through the multi-leveled dimensions of the map. At the higher level, the framework displays four dimensions:

General information

This category identifies the Open Innovation solutions – or solutions, if more than one – and the com-

pany that backs it. It includes 2 dimensions: backing company (the name of the company, or holding,

that is running the program), program name (the official name of the program, if it exists).

Solution characteristics

This category includes all the dimensions necessary to describe a startup engagement solution, from

the type to its characteristics. The first four dimensions relate to all the types of solution, while the

last six dimensions relate to any of the four models of structure a CVC program can refer to: Solution

category (the 4 models of CVC programs, partnerships, incubators/accelerators, startup competitions),

target industries (market areas the company is converging its efforts in), target startup growth stage

(pre-seed, seed, early, late stage).

Notes

Here the framework displays all the additional information that might be necessary to explain the

solutions, as in many cases they are unique: additional information (what can’t be said through num-

bers. This dimension contains all the peculiarities that characterize the Open Innovation solution),

contacts (email contacts of the solution), links (the link to the website of the solution, if the company

has a dedicated webpage).

XXI

METHODOLOGY

Before entering in the core results of the research, it is necessary to explain how data were collected. This

way, it will be made clear how it was possible to give an answer to each of the two research questions set as

objective of this paper. The following paragraph presents the main tools used for collecting data, making dis-

tinctions between the first objective – The Map – and the second one – The Critical Analysis.

TOOLS FOR DATA COLLECTION – Seen the novelty of the phenomenon in Italy, and since no previous researches

were done on it, it was necessary to implement and combine different approaches to have a more complete

understanding and to better tackle the dual nature of the objective.

Secondary sources investigation

Regarding the creation of The Map, it is necessary to identify among all the Italian companies the ones

with at least one active startup engagement solution. It is obvious that the most exhaustive way to do

so would be directly approaching all the Italian companies. However, due to the large width of the

dataset and the difficulties of getting in contact with companies the most viable solution is the inves-

tigation through secondary sources. Secondary sources investigation is done through the scanning of

the articles of the main Italian journals and magazines of innovation and finance. Once a company is

identified, the information gathering is done directly on the company’s website or the website of the

specific startup engagement program/practice (if available).

Direct personal interviews

While The Map is just a methodical, organized presentation of information, The Critical Analysis is

meant to be a subjective interpretation of the phenomenon, aimed at presenting the reasons behind

the results obtained, the benefits stemming from the implementation of startup engagement solu-

tions, the limits of the diffusion of this phenomenon and possible opportunities for future develop-

ment. Therefore, regarding this second part of the research objective, a more direct approach is re-

quired; the tool chosen is the direct personal interviews. In the same way the second part of the ob-

jective serves as complement for the first one, this tool is complementary to the secondary sources

investigation.

RESEARCH AND ANALYSIS

In this section will be shown the core of the paper; what the empirical research brought to the surface. As

mentioned at the beginning of the paper in the introduction, the objective of this study is deployed over two

subsequent steps: The Map and The Critical Analysis.

XXII

The Map

Fundamental is to make a consideration regarding the category Partnership. The synthetical table reports as

result “NA”, not available, as no such programs were framed in the map. This outcome does not mean that

there are no partnerships with startups aimed at joint innovation in Italy, in fact, there are some companies

currently investing in co-development programs with startups, but some difficulties made it hard to frame

them in the map. First of all, partnerships are very hard to be spotted when they are the only solution a com-

pany implements to engage with startups; they are strategic practices that a company often do not want to

disclose. Therefore, even if it is legit to assume that a company already implementing a program of interaction

with startups also implements partnerships, it will never be possible to frame all the companies in Italy imple-

menting this program. In addition, partnerships with startups can be implemented in infinite ways, suited and

personalized depending on the actors involved; this makes it hard to keep track of them, as it is not easy to

distinguish clearly which ones are aimed at joint innovation. For these reasons, given the fact that is not pos-

sible to present a complete picture of all the active partnerships aimed at joint innovation with startups, this

solution has been omitted from the mapping.

Regarding the other solutions, the overall view sees twenty-two Italian companies implementing disruptive

open innovation solutions through forty different programs or practices. Just ten of them bring on more than

one solution (program or practice). Under a deeper view, the four most committed companies account for the

40% of the total practices/programs, where Unicredit is the only company in Italy implementing all the three

types of open innovation solution. Analyzing the type of solutions implemented by the set of companies, it is

possible to draw the following conclusions: thirteen companies are making equity investments in startups,

implementing a total of eighteen different programs of CVC. the clear majority of the companies that adopted

one of the four models of CVC program bring on also at least one other type of solution. Regarding the models

of the CVC solutions, it can be noticed that internal dedicated funds are more focused on early/later stage

SOLUTION CATEGORYN° OF SOLUTIONS

IMPLEMENTEDTYPE OF SOLUTION N° OF BACKING COMPANIES

CORPORATE DIRECT INVESTMENT 4

INTERNAL DEDICATED FUND 6

EXTERNAL FUND 3

SYNDICATION 5

ACCELERATOR / INCUBATOR 17 ACCELERATOR / INCUBATOR 13

STARTUP COMPETITION 5 STARTUP COMPETITION 5

PARTNERSHIP N/A PARTNERSHIP N/A

13CVC PROGRAM

SYNTHETIC TABLE of the number of solutions (category and type) implemented by Italian companies

XXIII

investment, while corporate direct investments are more focused on pre-seed/seed stage. The external fund

model is implemented by banks only (Unicredit and Intesa San Paolo). About investments in syndication with

other investors, in four out of five cases the syndication is done through corporate direct investment. Moving

to incubators/accelerators, thirteen companies implementing an acceleration or incubation program for

startups, and some companies are even implementing more than one program of incubation/acceleration

(Enel, Buongiorno, Zambon). It should be highlighted that accelerators/incubators are run in collaboration with

other actors in order to get the most out of open innovation. Finally, five companies are implementing a prac-

tice of startup competition for startups. In three cases out of five they are standalone competitions, while the

remainder are practices to select startups for further equity investments or partnerships.

Critical Analysis

When the results stemming from the map are put in comparison with the level of adoption of the open inno-

vation with startups by companies in the world, it comes clear Italy is far behind the most developed countries,

and is experiencing an underdeveloped situation. Through the interviews held with some of the Italian corpo-

rate venture capitalists, it was possible to investigate the reasons behind these results and the obstacles that

hinder the diffusion, alongside with the benefits stemming from the implementation and possible opportuni-

ties for future development. Adopting a solution of strategic interaction with startups (in the case of the inter-

views, CVC programs) brings always an advantage in terms of improvements of the current strategy or of op-

tionality for the future strategy. Regarding the limits and the reasons at the base of the low diffusion of the

solution of open innovation with startups In Italy, it came out that the phenomenon is underdeveloped due to

both problems related to the investors (the companies) and problems related to the investees (the startups).

The former are related to an old and risk-averse management culture coupled with a lack of preparation in

the field; the latter are related to a low-value startup ecosystem in the country triggered (also) by a suboptimal

funding by all the investors (institutional and private). Where the venture capitalism has a greater magnitude,

it is consequently easier for a corporation to find valuable ventures to invest in. Therefore, given a good prep-

aration and the right culture inside the company, the more valuable the startup ecosystem where the company

is set, the greater the advantages a company can gain from the interaction. Said so, however, from this under-

developed situation some opportunities of development can still emerge if the right intervention are taken;

Investors must succeed in closing very profitable deals, the government should favor and attract international

investors, a change of mindset is as well needed to overcome the cultural barrier of risk aversion, and, at last,

a continuous commitment by all the players in the Italian venture capitalism.

1

INTRODUCTION The competitive landscape in many industries is marked today by a fierce growing competition. The market is

characterized by a rapid technological progress in many fields that quickly makes current solutions to cus-

tomer’s problems obsolete. For large companies in this scenario, creating new businesses is the challenge of

the day. Tweaking existing offerings, taking over rivals, downsizing, or moving into developing countries is no

more enough to survive. Corporations have realized that any player that is not continually developing, acquir-

ing, and adapting to the changing business environment, may be out of business within a few years.

These changes have highlighted the need for companies to become more entrepreneurial (Dess, Lumpkin and

McGee, 1999; Brazel and Herbert, 1999) in order to spot out and exploit new business opportunities. Corpo-

rations must become Janus-like, looking in two directions at once, with one face focused on the old and the

other seeking out the new (D. Garvin, L. Levesque, 2006). A new, ad hoc strategic approach is needed, which

must be based on entrepreneurship, along with the constant ability to change and innovate. Here lies the

biggest challenge for a consolidated corporation: to guarantee constancy in keeping this entrepreneurial effort

alive while growing. Institutionalizing entrepreneurship requires the right cultural approach and sure a cleared-

eye strategic view right at the C-level positions. It is an organizational paradox that, while the existing capabil-

ities provide the basis for the current performance of a company, without renewal, they are likely to constrain

the future ability to compete (Leonard Barton, 1992). Most organizations lose their entrepreneurial spirit once

they cross the start-up phase. The transition from an entrepreneurial growth company to a ‘well-managed’

business is usually accompanied by a decreasing ability to identify and pursue opportunities. Initiatives and

excitement give place to structure and systems. Organizations become blind to opportunities in the process

(Ramachandran, 2006).

In this light, the paper sees the dialogue with startups by consolidated corporations as one – but not the only

– management practice to institutionalize entrepreneurship and consequently to implement a strategy of con-

tinuous innovation. When mentioning the dialogue with startups and corporations, the research includes sys-

tematic open innovation programs and practices that involve the interaction with the startup ecosystem (i.e.

corporate venturing activities such as corporate incubators/accelerators, and corporate startup competitions).

Big companies are lately waking up to the fact that their industries are disrupted by the innova-

tions led by startups. Instead of thinking ‘some incumbents are gonna lose, some startups are

gonna win’, startups should be seen as potential partners. Partners to create more value for your

company, more value for the consumer, and for the whole industry.

Giuseppe Zocco, co–founder of Index Ventures

2

This study wants to capture an updated image of the strategic interaction among corporations and startups in

Italy by analyzing the startup engagement solutions backed by Italian corporations. The study presents how and

at which level Italian corporations are involved in interaction with startups, what are the factors at the base of

the current level of adoption and what are the opportunities for future development. In details, the study will:

1) Map within an original framework all the Italian companies that are currently implementing programs or

practices of open innovation with startups, with the aim of internalize the power of disruption that these new

ventures bring within themselves. Among the different solutions that a corporation can implement to engage

with startup, the framework will consider CVC programs, incubators/accelerators, partnerships and startup

competitions, following a defined criterion of inclusion.

2) Give, in light of the research previously conducted, a critical interpretation of the level of adoption of the

interaction among corporations and startups in Italy as a strategic practice, presenting the reasons behind

these results and the obstacles that hinder the diffusion, alongside with the benefits stemming from the im-

plementation and possible opportunities for future development. This critical interpretation of the phenome-

non will be outlined through qualitative interviews with the managers in charge of the most prominent and

structured corporate startup engagement programs (CVCs).

For the sake of simplicity, the first part of the objective – the map of the Italian corporations that implement

open innovation solutions with startups – will be addressed as The map; the second part of the objective – the

critical interpretation of the results coming from the first step of the research – will be addressed as Critical

analysis.

STRUCTURE OF THE PAPER – after this introduction, there is the section Literature Review, which gives solid

theoretical basement to the field under investigation and constitutes the set of assumptions at the base of the

empirical research. The paper continues with the section The Framework, where, as the title suggests, it is

introduced in details the framework under which the different corporate startup engagements solutions are

mapped. Within this section is also explained the criterion of inclusion at the base of the selection of the

corporate startup engagement solutions. It follows the Methodology, which gives a complete and accurate

description of the methodologies and techniques used for gathering the data, analyzing them, and reflecting

over their contribution. After having set the methodology adopted for the analysis, it follows the section Re-

search and Analysis, where the findings of the research are presented and then analyzed. Finally, the paper

closes with the section Conclusions, where the findings are presented under a critical view and it is highlighted

the contribution they can give and the space they can open to further studies and researches.

3

LITERATURE REVIEW

This section of the paper aims at giving a solid theoretical basement to the field under investigation: the space

where corporations meet the startup ecosystem to pursue strategic goals. Moreover, the literature review

represents the foundation of the empirical research, as the process of mapping will take reference from the

aspects and dimensions outlined in this section.

CVC program is the first startup engagement solution analyzed in the Literature Review, as it is the most struc-

tured and consequently the one that best represents the phenomenon of interaction corporation-startup.

Despite the booming of the startup ecosystem in the last years, CVC is a relatively old phenomenon, which is

now living a new wave under a different, more strategic form. For this reason, the subject can sure find refer-

ence in management theories of the ‘80s, but it needs to be integrated with the latest trend known as open

innovation in order to be outlined under a more contemporary view.

CVC is here firstly framed as a management practice in the wider theoretical field of corporate entrepreneur-

ship. After an analysis from the historical point of view, where the main phases of this phenomenon are iden-

tified, CVC is also defined and collocated within the corporate strategy of a company. CVC is then examined

through an analytical evaluation of its main aspects (i.e. objectives, structure, and typologies), along with the

identification of four archetypes of investor company.

As previously anticipated, after having outlined corporate venture capital in itself, the phenomenon is investi-

gated in relation to the “hottest” and widely spoken concept of open innovation to give the most updated

overview possible. As an innovation practice, CVC is here studied in conjunction with the most traditional R&D

and then projected into the future through a prediction of its evolution under the open innovation approach.

To conclude, follows a general overview of the most common ways for a corporation to interact with startups.

1. CORPORATE ENTREPRENEURSHIP

Over the years, a large and growing consensus has been built around the importance of corporate entrepre-

neurship in today’s competitive landscape. As explained in the introduction to this paper, both scholars and

practitioners agree upon the necessity for a company to implement corporate entrepreneurship activities to

ensure the survival of the business. Despite this, the literature does not comprehend a commonly shared defi-

nition of corporate entrepreneurship and, in the last 30 years, many definitions have been proposed and even

addressed with different terms: corporate entrepreneurship, corporate venturing, intrepreneuring, intrapre-

neurship, internal entrepreneurship, venturing, strategic renewal (see Table 1).

4

PINCHOT, 1985 Corporate entrepreneurship can be defined as start-up entrepreneurship turned inward.

SPANN, ADAMS & WORTHMAN, 1988

Corporate entrepreneurship is the establishment of a separate corporate organization (often in the form of a profit center, strategic business unit, division, or subsidiary) to introduce a new product, serve or create a new market, or utilize a new technology (p.149).

COVIN & SLEVIN, 1991 Corporate entrepreneurship involves extending the firm’s domain of competence and corresponding opportunity set through internally generated new resource combination (p.7, quoting Burgelman).

GUTH & GINSBERG, 1990

Corporate entrepreneurship encompasses two types of phenomena and the processes surrounding them (1) the birth of new business within existing organization, i.e. internal innovation or venturing, and (2) the transformation of organization through renewal of the key ideas on which they are built, i.e. strategic renewal (p.5). strategic renewal involves the creation of new wealth through combinations of resources (p.6).

SCHOLLHAMMER, 1982

Internal (or intra-corporate) entrepreneurship refers to all formalized entrepreneurial activities within existing business organizations. Formalized internal entrepreneurial activities are those, which receive explicit organizational sanction and resource commitment for the purpose of innovative corpo-rate endeavor - new product developments, product improvements, new methods or procedures (p.211).

BURGELMAN, 1983