annual reportshriramhousing.in/pdf/annual-reports/shfl-ar-fy2016-17.pdfindusind bank kotak mahindra...

TRANSCRIPT

Building a Better Nation

with Affordable Housing

ANNUAL REPORT2

01

6-1

7

th7

In this Annual Report, we have disclosed forward-looking information to enable investors to comprehend our prospects and take investment decisions. This report and other statements - written and oral – that we periodically make contain forward-looking statements that set out anticipated results based on the management’s plans and assumptions. We have tried wherever possible to identify such statements by using words such as ‘anticipate’, ‘estimate’, ‘expects’, ‘projects’, ‘intends’, ‘plans’, ‘believes’, and words of similar substance in connection with any discussion of future performance. We cannot guarantee that these forward-looking statements will be realised, although we believe we have been prudent in assumptions. The achievements of results are subject to risks, uncertainties, and even inaccurate assumptions. Should known or unknown risks or uncertainties materialise, or should underlying assumptions prove inaccurate, actual results could vary materially from those anticipated, estimated, or projected. Readers should keep this in mind, we undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise.

FORWARD LOOKING STATEMENT

TABLE OF CONTENTS

S.No. Topic Page No.

01. Corporate Information 4-5

02. Our Mission 6-7

03. Milestones 8-9

04. Branch Presence 12-13

05. Products 14-14

06. Performance 15-15

07. Directors’ Profiles 16-16

08. Directors’ Report 17-24

09. Annexures to Directors’ Report 25-39

10. Management Discussion & Analysis 40-41

11. Auditor’s Report 42-43

12. Annexures to Auditor’s Report 44-47

13. Financial Statements (Standalone) 48-78

14. About the Shriram Group 79-79

15. About Shriram City Union Finance Limited 79-79

GROWING TOGETHER

WITH PEOPLE

THE

PIONEERS BEHIND THE

GROWTH

4 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Registered OfficeNo. 123, Angappa Naicken Street

Chennai – 600 001

Ph : + 91 44 2534 1431

Statutory AuditorsPijush Gupta & Co.Chartered Accountants

P-199, C.I.T. Road, Scheme IV–M,

Kolkata – 700 010.

Ms. Nikita HuleCompany Secretary

Head OfficeLevel 3, East Wing,

Wockhardt Towers,

Bandra Kurla Complex,

Mumbai – 400 051.

Ph : +91 22 4241 0400.

Mr. Arun MishraChief Operating Officer

Mr. Paresh AthalyeChief Human Resources OfficerManagement

Team

Axis Bank

Bank of Maharashtra

Barclays Bank

HDFC Bank

IDBI Bank

Indian Bank

IndusInd Bank

Kotak Mahindra Bank

Shinhan Bank

State Bank of India

Syndicate Bank

Union Bank of India

United Bank of India

Vijaya Bank

Banks

Mr. Sujan SinhaManaging Director &

Chief Executive Officer

Dr. Qudsia GandhiIndependent Director

Mr. Yalamati Srinivasa

ChakravartiDirector

Mr. Venkataraman MuraliIndependent Director

Ms. Subhasri SriramDirector

Mr. Khushru JijinaDirector

Board Of Directors

5Shriram Housing Finance Limited

Debenture TrusteeCatalyst Trusteeship Limited

(Formerly GDA Trusteeship Limited)

GDA House, Plot No. 85, Bhusari Colony (Right),

Paud Road, Pune - 411 038

CORPORATE INFORMATION

6 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

OUR MISSION

To serve the under-served population of the country in fulfilling

their aspirationof owning a dream

home by 'Finding Ways toFunding Homes'

7Shriram Housing Finance Limited

8 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

FROM STEPPING STONE TO MILESTONES

FY2014

Composite book size in excess of 1,250 Crores`

Recipient of ISO 27001:2005 for the management of information security in accounting and back office operations with all associated support functions -

Project Finance Loans introduced

Second tranche of investment received from our PE investor: Valiant Mauritius Partners FDI Limited. Crossed 100 Crores `

in disbursement

Private equity investment of 75 `Crores by Valiant

Mauritius Partners FDI Limited

Registered with National Housing Bank as a Housing Finance Company in August 2011; Commenced lending operations from December

2011

Shriram Housing Finance Limited incorporated as a

Company

FY2013

FY2015

FY2011

FY2016

9Shriram Housing Finance Limited

FY2012

MILESTONES

MAKING

DREAM HOMEA REALITY THROUGH

AFFORDABLE HOUSING

10 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Presently, the macro environment is extremely favourable for housing finance companies. The Government incentives in terms of allocation related to Pradhan Mantri Awas Yojana of 23000 crores `would provide the much needed momentum to the sector.

The recent Union Government budget has given a boost to affordable housing, both on the demand as well as the supply aspect. Infrastructure status to the sector would help affordable home developers access cheaper funds and help the home buyers with affordable cost, thus increasing the demand for housing finance.

Pradhan Mantri Awas Yojana has got increased budgetary allocations for both rural and urban component. Providing incentive to the housing sector is likely to have a multiplier effect on the economy and employment situation.

Supported by growth drivers such as rising disposable income, personal income tax benef i ts, increasing urbanisation and economic growth of Tier II and Tier III cities, housing sector is likely to see immense growth.

Government initiatives for “Housing for all” would give immense boost to the housing finance companies.

11Shriram Housing Finance Limited

FOCUS ON AFFORDABLE HOUSING

12 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

BRANCH PRESENCE PAN INDIA

13Shriram Housing Finance Limited

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

• ANDHRA PRADESHGuntur

Kurnool

Nellore

Rajahmundry

Tirupati

Vijayawada

Visakhapatnam

• CHANDIGARHChandigarh

• CHHATTISGARHBilaspur

Raipur

• DELHI / NCRDelhi

• GUJARATAhmedabad

Ahmedabad East

Bharuch

Bhavnagar

Himatnagar

Mehsana

Palanpur

Rajkot

Surat

Vadodra

• HARYANAAmbala

Karnal

• KARNATAKABanashankari

Bengaluru

Hubli

Mysore

• KERALAErnakulam

• MADHYA PRADESHBhopal

Indore

Neemuch

Ratlam

Ujjain

• MAHARASHTRAAhmednagar

Amravati

Aurangabad

Chandrapur

Kolhapur

Nagpur

Nasik

Navi Mumbai

Pune

Solapur

Viman Nagar

Wardha

• ODISHABhubaneshwar

• PUDUCHERRYPuducherry

• PUNJABAmritsar

Bathinda

Jalandhar

Ludhiana

• RAJASTHANAjmer

Alwar

Bikaner

Jaipur

Jodhpur

Kota

Udaipur

• TAMIL NADUChennai - Arumbakkam

Chennai - Mylapore

Coimbatore

Hosur

Kanchipuram

Madurai

Tiruchirapalli

Tiruvallur

Tirunelveli

• TELANGANAHyderabad

Karimnagar

Kukatpally

Secundarabad

Warangal

• UTTAR PRADESHAgra

Allahabad

Bareilly

Kanpur

Lucknow

Meerut

• UTTARAKHANDDehradun

Haldwani

Haridwar

• WEST BENGALBarasat

Durgapur

Kolkata

Siliguri

STATE-WISE BRANCH NETWORK

14 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Loan Against Property

We offer Loan Against Property on convenient terms. Customers can mortgage their existing

residential or commercial property to meet all their financial requirements.

Home LoansLoans with simple documentation

are provided for purchase of a new / resale house as well as purchase of

plot and construction of house thereon. Loans are also provided for self

construction of a house or extension / renovation of an existing property.

We also provide attractive schemes for takeover of existing home loan along

with additional finance options.

Project Finance

We provide financial assistance to builders / developers to meet the

construction cost of their project.

PRODUCTS

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

15Shriram Housing Finance Limited

PERFORMANCE

CAGR 70%

964.3

792.5

502.8

236.7

115.0

FY17FY16FY15FY14FY13

CAGR 358%

43.9

42.7

30.1

15.7

0.1

FY17FY16FY15FY14FY13

DISBURSEMENTS (` CRORES) PROFIT BEFORE TAX (` CRORES)

279.2

CAGR 102%

FY17FY16FY15FY14FY13

167.5

85.5

41.7

16.9

85

CAGR 19%

FY17FY16FY15FY14FY13

79

72

4742

TOTAL INCOME (` CRORES) BRANCHES (#)

2.59

1.82

FY17FY16FY15FY14FY13

1.26

2.05

2.76

1.991.68

0.00

CAGR 98%

1,775.0

FY17FY16FY15FY14FY13

1,275.0

737.2

320.3

115.40.00

ASSETS UNDER MANAGEMENT (` CRORES) NON PERFORMING ASSETS (%)

GROSS NPA NET NPA

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

16 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

DIRECTORS’ PROFILES

Mr. Sinha is the Managing Director and Chief Executive Officer of the Company. He holds a degree of

Bachelor of Science from Presidency College. He is in the financial services domain since 1981, primarily in

commercial banks and has been involved in the housing finance industry in India since the year 2000.

Mr. Sinha led the retail mortgage business for Axis Bank enabling it to grow exponentially. He has been on

the Board since December 2010.

Mr. Sujan Sinha

Mr. Khushru Jijina is a Non Executive, Non Independent Director on the Board. Mr. Jijina presently, is the

Managing Director of Piramal Finance Limited and has been with the Piramal Group for more than 15 years.

He also leads the family office for all proprietary investments and serves as the Group Treasurer. Mr. Jijina

was the Managing Director of Piramal Realty, Executive Director of Piramal Sunteck Realty, etc. He started

his career with Rallis, a TATA Group Company, where he held several important positions in corporate

finance and treasury over a span of more than a decade. He has been on the Board since January 2016.

Mr. Khushru Jijina

Ms. Sriram is a Non Executive, Non Independent Director on the Board. She holds a degree of Master of

Commerce, I.C.W.A and ACS. She is instrumental in setting up Retail Finance Vertical of Shriram Group.

She has over two decades of experience in retail and corporate finance, treasury & fund management and

corporate administration. She has been on the Board since November 2010.

Ms. Subhasri Sriram

Mr. Chakravarti is a Non Executive, Non Independent Director on the Board. He holds a degree of Bachelor

of Commerce and is a retail finance professional with proven skills and organizing abilities. He has worked

in various assignments in the field of financial services for over two decades. He serves on the Boards of

Shriram Chits Pvt Ltd and Shriram Chits (Maharashtra) Limited. He has been in the Board since November

2010.

Mr. Yalamati Srinivasa Chakravarti

Mr. Murali is a Non Executive, Independent Director on the Board. He holds degree of Bachelors of

Commerce, from Vivekananda College, Chennai. He is a fellow member of the Institute of Chartered

Accountants of India and an associate member of the Institute of Cost and Works Accountants of India and

has to his credit more than three decades of experience in the relevant fields. He is a six time elected central

council member of ICAI for the period 2004-16. He has been nominated by the Government and other

bodies for several assignments and has held various positions in Chambers of Commerce & Industry as

well as in the field of education. He has been on the Board since July 2013.

Mr. VenkataramanMurali

Dr. Gandhi is a Non Executive, Independent Director on the Board. She holds a degree in Masters of Arts,

M.A. (Applied Economics - Dev.Admn & Management) (Manchester UK). A retired member of the Indian

Administrative Services since 1977, Dr. Gandhi has vast experience of over 30 years in government

administration, in various fields such as treasury, accounts, training, health & family welfare. She has been

on the Board since November 2012.

Dr. Qudsia Gandhi

17Shriram Housing Finance Limited

To

The Members of

Shriram Housing Finance Limited

Your Directors are pleased to present the Seventh Annual Report along with the Audited Financial Statements for

the year ended March 31, 2017 of Shriram Housing Finance Limited ('the Company').

FINANCIAL RESULTS

The summary of financial performance of the Company for the Year is as under:

` in lacs

A. DIVIDEND

No Dividends were declared during the financial year 2016 - 2017.

B. PERFORMANCE REVIEW

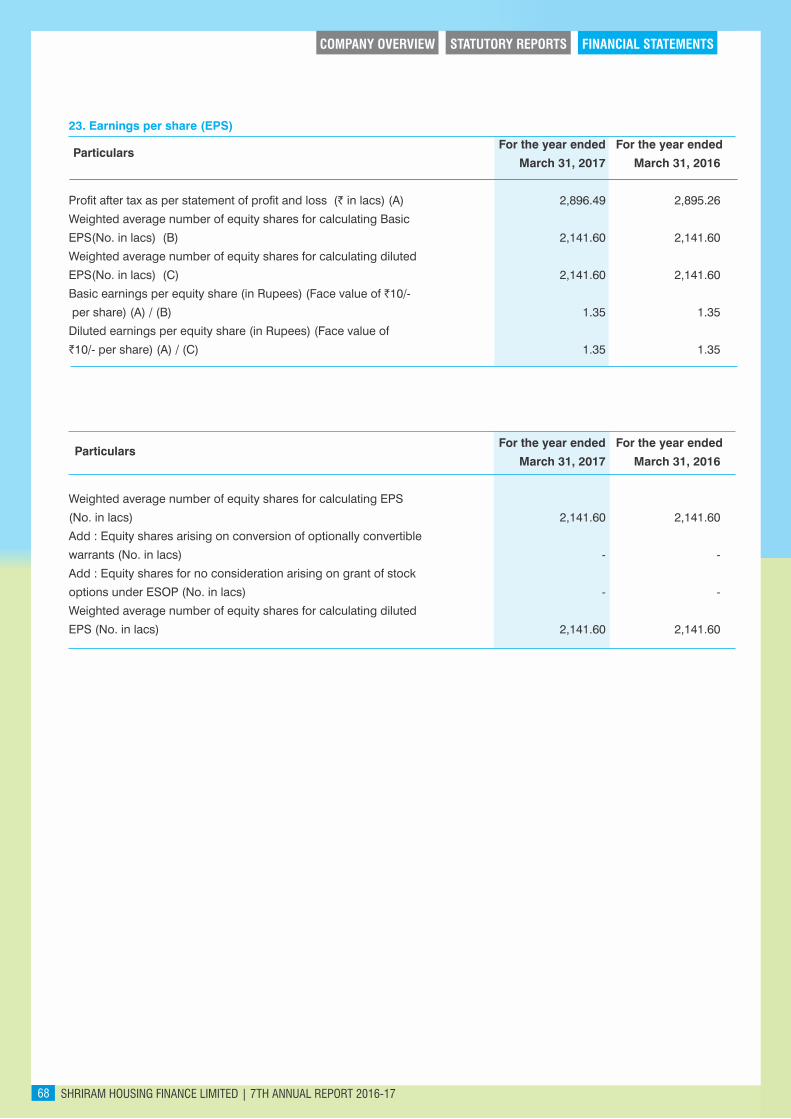

Total income for the year increased to ` 27,917.89 lacs as compared to ` 16,746.62 lacs in 2016. The revenue from operations for the year was 27,666.21 lacs as compared to 16,721.06 lacs in 2016. The profit before tax for the year was ` 4,391.22 lacs as compared to ` 4,273.40 lacs in 2016. The profit after tax for the year was ` 2,896.49 lacs as compared to 2,895.26 lacs in 2016.

C. SHARE CAPITAL

The paid up Equity Share Capital of the Company as on March 31, 2017 was ` 214.16 crores. During the year under review, the Company has not issued shares.

D. NON CONVERTIBLE DEBENTURES (NCDs):

During the year, the Company issued NCDs amounting to ` 424 crore on private placement basis which have been listed on the Wholesale Debt Segment of Bombay Stock Exchange (BSE) Ltd and NCDs amounting to ` 6 crore matured. The NCDs have been assigned rating of “CARE AA+” by Credit Analysis & Research Ltd (CARE) and “IND AA” by India Ratings & Research Private Limited.

As at March 31, 2017, NCDs amounting to ` 734/- crore were outstanding. The Company has been regular in making payment of principal and interest on the NCDs. As at March 31, 2017, there were no NCDs which have not been claimed by the Investors or not paid by the Company after the date on which the said NCDs became due for redemption. Hence the amount of NCDs remaining unclaimed or unpaid beyond due date is Nil.

Particulars 2016-17 2015-16

Profit before depreciation and taxation 4500.26 4344.07

Less: Depreciation 109.04 70.67

Profit before tax 4391.22 4273.40

Less: Provision for taxation 1494.73 1378.14

Profit after tax 2896.49 2895.26

Add: Profit brought forward from previous year 4570.27 2275.01

Profit available for appropriation 7466.76 5170.27

Earnings per share

(1) Basic 1.35 1.35

(2) Diluted 1.35 1.35

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

REPORT OF THE BOARD OF DIRECTORS

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

18 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Debenture Trust Agreement in favour of Catalyst Trusteeship Limited (formerly “GDA Trusteeship Limited”) for the aforesaid issues was executed.

Your Company being a Housing Finance Company is exempted from the requirement of creating Debenture Redemption Reserve (DRR) in case of privately placed debentures. Since the Debenture issues of the Company till date are through private placement, no DRR has been created.

E. COMMERCIAL PAPER

The Commercial Paper (CP) programme of the Company have been assigned the rating of A1+ by CARE Ratings. As at March 31, 2017, Commercial Papers outstanding amount stood at NIL.

F. LOANS FROM BANKS

As at March 31, 2017, the company outstanding bank loan stood at 636 crore vis-a-vis 513 crore as at March 31, 2016. In the financial year 2016-17 funding with bank borrowings contributes to 46% approximately.

STATUTORY & REGULATORY COMPLIANCE

The Company has complied with the applicable statutory provisions, including those of the Companies Act, 2013 and the Income-tax Act, 1961. Further, the Company has complied with the NHB's Housing Finance Companies Directions, 2010, Housing Finance Companies issuance of Non-Convertible Debentures on private placement basis (NHB) Directions, 2014 and the Accounting Standards issued by the Institute of Chartered Accountants of India (ICAI).

PARTICULARS OF LOANS, GUARANTEES OR INVESTMENTS UNDER SECTION 186

Pursuant to Section 186 (11) of the Companies Act, 2013 loans made, guarantee given or security provided by a Housing Finance Company in the ordinary course of its business are exempted from disclosure in the Annual Report.

PARTICULARS OF CONTRACTS OR ARRANGEMENTS WITH RELATED PARTIES

All Related Party Transactions (RPT) that were entered during the financial year were in the ordinary course of business of the Company and were on arm's length basis. There were no materially significant related party transactions entered by the Company with Promoters, Directors, key managerial personnel or other persons which may have a potential conflict with the interest of the Company. Considering the nature of the industry in which the Company operates, transactions with related parties of the Company are in the ordinary course of business which are also on arm's length basis. All such Related Party Transactions are placed before the Audit and Risk Management Committee for approval, wherever applicable. The particulars of contracts or arrangements with related parties as referred in section 188(1) of the Act is attached to this Report in prescribed form AOC -2 as Annexure 1. Your Directors draw attention of the members to Note 24 of the financial statement which sets out related party disclosures.

BOARD OF DIRECTORS

The Company has six Directors consisting of two Non-Executive Independent Directors, three Non-Executive Non-Independent Directors and a Managing Director & CEO as Executive Director as on the date of adoption of this report.

Pursuant to Section 152(6) of the Companies Act, 2013, Mr. Y. S. Chakravarti (DIN: 02511019), Director, retires by rotation at the ensuing Annual General Meeting and is eligible for re-appointment.

KEY MANAGERIAL PERSONNEL

Mr. Sujan Sinha, Managing Director & Chief Executive Officer, Mr. Kunal Shah, Chief Financial Officer and Ms. Nikita Hule, Company Secretary of the Company are the Key Managerial Personnel of the Company as per the provisions of the Companies Act, 2013. Their appointment as Key Managerial Personnel have been duly formalized pursuant to section 203 of the Companies Act, 2013.

DECLARATION BY INDEPENDENT DIRECTORS

The Board has received declarations from all the Independent Directors as per the Section 149(7) of the Companies Act, 2013 and the Board is satisfied that all the Independent Directors meet the criterion of independence as mentioned in Section 149(6) of the Companies Act, 2013.

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

19Shriram Housing Finance Limited

COMPANY'S POLICY ON APPOINTMENT AND REMUNERATION OF DIRECTORS, KEY MANAGERIAL PERSONNEL AND OTHER EMPLOYEES:

The Nomination and Remuneration Committee has in place a policy on Board diversity for appointment of Directors, taking into consideration their qualification and wide experience in the fields of banking, finance, regulatory, administration, legal, commercial segment apart from compliance of legal requirements of the Company. The Company has laid down remuneration criteria for the Directors, key managerial personnel and other employees in the Nomination and Remuneration Policy. The Nomination and Remuneration Policy approved by the Board is available on the Company's website www.shriramhousing.in

NUMBER OF BOARD MEETINGS

The Board of Directors met 4 (Four) times (April 22, 2016, July 21, 2016, October 21, 2016 and January 23, 2017) during the financial year ended March 31, 2017.

BOARD EVALUATION

The Board of Directors has carried out an annual evaluation of its own performance, Board committees and individual Directors pursuant to the provisions of the Companies Act, 2013 and Rules.

The performance of the Board was evaluated by the Board after seeking inputs from all the Directors on the basis of the criteria such as the Board composition and structure, effectiveness of board processes, information and functioning, etc. The performance of the committees was evaluated by the Board after seeking inputs from the committee members on the basis of the criteria such as the composition of committees, effectiveness of committee meetings, etc.

In a separate meeting of Independent Directors, performance of non-independent Directors, performance of the Board as a whole and performance of the Chairman was evaluated, taking into account the views of Executive Director and Non Executive Directors.

COMMITTEES OF THE BOARD

The Company has various Committees which have been established as a part of the best corporate governance practices and are in compliance with the requirements of the relevant provisions of applicable laws and statutes.

• Audit and Risk Management Committee

• Nomination and Remuneration Committee

• Asset Liability Management Committee

• Corporate Social Responsibility Committee

• Banking and Finance Committee

• Whistle blower and Vigil mechanism Committee

• Internal Complaints Committee

• Credit Committee

20 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

AUDIT AND RISK MANAGEMENT COMMITTEE

The Audit and Risk Management Committee comprises of Mr. V. Murali – Chairman, Ms. Subhasri Sriram and Dr. Qudsia Gandhi as members. All the recommendations made by the Audit and Risk Management Committee were accepted by the Board.

Terms of reference:• Recommend appointment, re-appointment, terms of appointment/reappointment and remuneration (audit fees and

fees for other services) of Auditors.

• Review and monitor Auditor's independence and performance and effectiveness of audit process.

• Examine the Financial Statements, financial reporting process, proper disclosure in the financial statements and the auditor's report including the compliance of KYC thereon and management letters/letters of internal control weakness by the auditors.

• Evaluation of internal financial controls and risk management systems.

• Monitor the end use of funds raised through public offers and related matters.

• Review appointment, re-appointment, removal, terms of appointment/reappointment and remuneration of internal auditor.

• Review internal audit function (structure, staffing, process, coverage, activity etc), internal audit report, follow up on findings and the performance of the internal auditor.

• Review findings of any internal investigation reports of the Internal Auditors on suspected fraud or irregularity or a failure of internal control systems of a material nature and report it to the Board.

• Look into the defaults in the payment to the depositors, debenture holders, shareholders (in case of non-payment of declared dividends) and creditors.

• Review the functioning of the Whistle Blower Mechanism.

• Approve appointment of Chief Financial Officer (CFO) of the Company.

• Approval or any subsequent modification of any transaction with related parties.

• Scrutiny of intercorporate loans and investments.

• Valuation of the undertaking or assets, wherever necessary.

• To analyse economic conditions, industry-wise performance, guidelines issued by regulatory authorities, competitor's policies & alerting management to the possibility of any adverse/risky situation emerging.

• Review Asset Liability Management, capital adequacy, resources raised, credit ratings and management of Non-Performing Assets.

• Analyse trend of cost of funds, expenses and review action taken to mitigate risks thereof.

• Analyse performance of assets assigned/securitised, related party transactions, single party exposure & contingent liabilities.

• Review compliance with statutory & legal requirements.

• Review the credit policy for each product & to assess dovetailing of business done in accordance with overall credit policy.

• Review all major operational control/actionable points to handle failures and other exigencies.

• Carry out any other function as decided by the Board from time to time

An executive of Secretarial Department or the Company Secretary shall act as the secretary to the Committee.

NOMINATION AND REMUNERATION COMMITTEE

The Nomination and Remuneration Committee comprises of Mr. V. Murali – Chairman, Ms. Subhasri Sriram and Dr. Qudsia Gandhi as members.

Terms of reference:• Formulation of the criteria for determining qualifications, positive attributes and independence of a Director.

• Identify persons who qualify to become Directors and recommend their appointment to the Board, as and when vacancies arise.

• Recommend removal of a Director from the Board, in case if such need arises.

• Formulation of criteria for evaluation of performance of independent Directors and the Board of Directors.

• Carry out evaluation of performance of every Director on an annual basis.

• Identify persons who may be appointed as members of senior management.

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

21Shriram Housing Finance Limited

• Formulate policies for qualification, attributes and independence of Directors.

• To ensure 'fit and proper' status of Directors at the time of their appointment as well as on continuing basis.

• Recommend to the Board policy relating to remuneration for directors, key managerial personnel and employees keeping in view to attract, motivate and retain talent required for the progress of the Company.

• To determine if the term of appointment of the independent Director should be extended or continued, on the basis of the report of performance evaluation of independent Directors.

• Guide policies and practices in the talent management of the Company.

• Formulate, recommend to the Board and administer Employees Stock Option Plans (ESOP) and other incentive plans for employees and directors and interpret and adopt rules for the operation thereof.

• Approve employment agreements, severance arrangements and change in control agreements.

• To form Sub-committees and take matters as may be assigned by the Board from time to time.

An executive of Secretarial Department or the Company Secretary shall act as the secretary to the Committee.

ASSET LIABILITY MANAGEMENT COMMITTEE

The Asset Liability Management Committee comprises of Mr. Khushru Jijina – Chairman, Mr. Sujan Sinha, Ms. Subhasri Sriram and Mr. Kunal Shah as members.

Terms of reference:

• Funding and Capital, profit planning and growth projection

• Balance Sheet planning from risk-return perspective.

• Strategic management of interest and liquidity risk.

• Adoption of Asset-Liability management practices.

• Providing a comprehensive and dynamic framework for measuring, monitoring and managing liquidity and interest rate risks of major operators in the financial system.

• Forecasting and analysing 'What if scanerio' and preparation of contingency plans.

• Any other subject as may be specified by NHB form time to time.

An executive of Secretarial Department or the Company Secretary shall act as the Secretary to the Committee.

CORPORATE SOCIAL RESPONSIBILITY COMMITTEE

The Corporate Social Responsibility Committee comprises of Dr. Qudsia Gandhi – Chairperson, Ms. Subhasri Sriram, Mr. Sujan Sinha and Mr. Khushru Jijina as members.

Terms of reference:

• To formulate and recommend to the Board, a Corporate Social Responsibility Policy which shall indicate the activities to be undertaken by the company as specified in Schedule VII;

• To recommend the amount of expenditure to be incurred on the activities referred to in clause (a)

• To monitor the Corporate Social Responsibility Policy of the company from time to time.

An executive of Secretarial Department or the Company Secretary shall act as the Secretary to the Committee.

BANKING AND FINANCE COMMITTEE

The Banking and Finance Committee comprises of Mr. Sujan Sinha - Chairman, Ms. Subhasri Sriram, Mr. Khushru Jijina and Mr. Kunal Shah as members

Terms of reference:

• All types of banking operations including open, close, change, modify, transfer of Bank Accounts and to accept and confirm bank balances with any bank

• Borrow Money from Bank or any other Institution within the limit specified by the Board from time to time either by

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

22 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

short term loan or long term loan by whatever name called i. e. Working Capital Loan, Cash Credit, Working Capital Demand Loan, Short Term Loan, Over draft, Term Loan, Commercial Papers, Debentures, Subordinated Debt, Securitisation, Assignment and any other forms of Borrowings.

• Invest, deposit or otherwise the funds of the Company in Short Term Deposits/ Long Term Deposits with Banks/ Mutual Funds/ any other Funds any other institutions, in the form of Deposits, Debentures, Bonds, Certificate of Deposits/CPs/Units within the limit sanctioned by the Board and transfer/change/modify/encash/liquidate any or all of these.

• All matters relating to listing of any instruments/securities with stock exchanges and all matters relating to Depositories.

• Execution of documents required for Banking and Borrowing of any nature and such other activities.

• All activities required for any type of Banking/ Borrowing

• Sell down the assets of the Company.

• All matters relating to Issuing and Paying Agent, Merchant Bankers, Trustees, Registrar and Transfer Agents, Bankers, Credit Rating Agencies and related Agents for Banking, Borrowings including Debentures and other Securities.

• Decide, change modify and revise the terms of issue, allotment, rate of interest and any condition thereof on Debentures issued by the Company.

• Any other activity related to Banking and Borrowings or any activity of business importance.

An executive of Secretarial Department or the Company Secretary shall act as the secretary to the Committee.

WHISTLE BLOWER POLICY/VIGIL MECHANISM

The Company has framed a Whistle Blower Policy/Vigil Mechanism providing a mechanism under which an employee/ director of the Company may report violation of personnel policies of the Company, unethical behaviour, suspected or actual fraud, violation of code of conduct. The Vigil Mechanism ensures standards of professionalism, honesty, integrity and ethical behavior. The Mechanism adopted by the Company encourages the whistle blower to report genuine concerns or grievances and provides for adequate safeguards against victimisation of whistle blower who avails of such mechanism and also provides for direct access to the Chairman of the Audit and Risk Management Committee. The Whistle Blower Policy/ Vigil Mechanism is uploaded on the Company's website: www.shriramhousing.in

EMPLOYEES' STOCK OPTION SCHEME

Nomination and Remuneration Committee of the Board of Directors of the Company, inter alia administers and monitors the Employees' Stock Option Schemes of the Company in accordance with the provisions under Section 62(1) (b) of the Companies Act, 2013 read with Rule 12(9) of the Companies (Share Capital and Debentures) Rules, 2014.

The applicable disclosures as stipulated under the Rule 12(9) of the Companies (Share Capital and Debentures) Rules, 2014 as at March 31, 2017 are provided in Annexure - II to this Report. The Company has received a certificate from the Auditors of the Company that the Scheme has been implemented in accordance with the provisions of the Companies Act and other applicable rules and guidelines and the resolution passed by the shareholders.

CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION, FOREIGN EXCHANGE EARNING AND OUTGO DURING THE YEAR

The information on conservation of energy, technology absorption, foreign exchange earnings and out go as stipulated under Section 134 (3) (m) of the Act read with Rule 8 of the Companies (Accounts) Rules 2014 are furnished below.

The operations of the Company are not energy intensive. However, adequate measures for conservation of energy, usage of alternate sources of energy and investments for energy conservation, wherever required, have been taken.

The Company has not absorbed any technology. There were no foreign exchange earnings. There was an outgo of foreign exchange equivalent to 9 lacs during the year.

INTERNAL CONTROL SYSTEMS

Your Company has an adequate system of internal control procedures which is commensurate with the size and nature of business. Detailed procedural manuals are in place to ensure that all the assets are safeguarded, protected against loss and all transactions are authorized, recorded and reported correctly. The internal control systems of the Company are monitored and evaluated by internal auditors and their audit reports are periodically reviewed by the Audit and Risk Management Committee of the Board of Directors. The observations and comments of the Audit and Risk Management Committee are placed before the Board.

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

1. Dr. Qudsia Gandhi Independent Director Chairperson

2. Ms. Subhasri Sriram Director Member

3. Mr. Sujan Sinha Director Member

4. Mr. Khushru Jijina Director Member

DIRECTORS' RESPONSIBILITY STATEMENT

To the best of their knowledge and belief and according to the information and explanations obtained by them, your

Directors make the following statements in terms of Section 134(3) (c) of the Companies Act, 2013:

• that in the preparation of the Annual financial statements for the year ended March 31, 2017, the applicable accounting

standards have been followed along with proper explanation relating to material departures, if any;

• the Directors have taken proper and sufficient care for the maintenance of adequate accounting records in accordance

with the provisions of the Companies Act, 2013 for safeguarding the assets of the Company and for preventing and

detecting fraud and other irregularities; and

• the Annual accounts have been prepared on a going concern basis.

• that proper internal financial controls were in place and that the financial controls were adequate and were operating

effectively.

• that systems to ensure compliance with the provisions of all applicable laws were in place and were adequate and

operating effectively. In the opinion of the Board, there are no risks, which may threaten the existence of the Company.

HUMAN RESOURCE DEVELOPMENT

We owe our success to our employees. Our workforce defines our Company, and is the most vital asset in our possession.

The Company aims to align HR practices with business goals, motivate people for higher performance and build a

competitive working environment. Productive high performing employees are vital to the Company's success. The Board

values and appreciates the contribution and commitment of the employees towards performance of your Company during

the year. To create the leadership bench and for sustainable competitive advantage, the Company inducted / promoted

employees during the year. In pursuance of the Company's commitment to develop and retain the best available talent, the

Company had organised various training programmes for upgrading skill and knowledge of its employees. The Company

also has in place performance-linked incentives which reward outstanding performers who meet certain performance

targets. It has been sponsoring its employees for training programmes / seminars / conferences organized by reputed

professional institutions. Employee relations remained cordial and the work atmosphere remained congenial during the

year. The information required pursuant to Section 197(12) of the Act read with Rule 5(1) of the Companies (Appointment

and Remuneration of Managerial Personnel) Rule, 2014 on remuneration are attached as Annexure IV to this Report.

SIGNIFICANT AND MATERIAL ORDERS PASSED BY REGULATORS OR COURT

There are no material order passed by Regulators/Courts, which would impact the going concern status of the Company

and it's future operations.

23Shriram Housing Finance Limited

In compliance with Section 135 of the Companies Act, 2013 read with the Companies (Corporate Social Responsibility Policy) Rules, 2014, the Company has established Corporate Social Responsibility Committee and statutory disclosures with respect to the CSR Committee and an annual report on CSR activities is annexed as Annexure - III to this report.

The CSR policy approved by the Board is available on the Company's website www.shriramhousing.in

The present constitution of the Committee is as follows:

CORPORATE SOCIAL RESPONSIBILITY (CSR):

PUBLIC DEPOSITS:

Your Company has not accepted deposits from public since its inception.

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

Sr.No. Name of Director Category Designation in the Committee

AUDITORS

A) Statutory Auditors:

M/s. Pijush Gupta & Co, Chartered Accountants, Kolkata, (FRN 309015E), Statutory Auditors of the Company retire at the

conclusion of the ensuing Annual General Meeting and are eligible for re-appointment. Certificates have been received

from them to the effect that their re-appointment as Auditors of the Company, if made, would be within the limits prescribed

under Section 139 and 141 of the Companies Act, 2013. Members are requested to consider their reappointment. The

Auditors' Report to the Shareholders for the year under review does not contain any qualification

B) Secretarial Audit:

The Board had appointed M/s P. Sriram & Associates, Practicing Company Secretary (Certificate of Practice No. 3310)

(Membership No. FCS 4862) to carry out Secretarial Audit under the provisions of Section 204 of the Companies Act, 2013

for the financial year 2016-17. The Secretarial Audit Report is annexed to this report as Annexure- V. The report does not

contain any qualification

EXTRACT OF ANNUAL RETURN

The extract of the Annual Return in the Form MGT 9 is annexed to this report as Annexure- VI.

CEO AND CFO CERTIFICATION

The Managing Director & CEO and Chief Financial Officer of the Company have furnished the certificate relating to the

financial statements and the same was placed before the Board of Directors at its meeting held on April 22, 2017 and the

copy of the certificate is appended as Annexure VII to this report.

ACKNOWLEDGMENT

The Board expresses gratitude for the guidance and cooperation extended by National Housing Bank, statutory authorities

and regulators. The Board appreciates the excellent co-operation and assistance received from Banks and Financial

Institutions. The Board is thankful to the auditors of the Company. The Board is pleased to record its appreciation for the

enthusiasm, commitment, dedicated efforts of the employees of the Company at all levels. The Board is also deeply

grateful for the continued confidence and faith reposed in the Company by the shareholders, depositors, debenture

holders and debt holders.

For and on behalf of the Board of Directors

Place: Mumbai Sujan Sinha Subhasri SriramDate: April 22, 2017 Managing Director & CEO Director (DIN: 02033322) (DIN: 01998599)

24 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

25Shriram Housing Finance Limited

ANNEXURE I

Form No. AOC - 2

(Pursuant to clause (h) of sub-section (3) of section 134 of the Act and Rule 8 (2) of the

Companies (Accounts) Rules, 2014)

Form for disclosure of particulars of contracts/arrangements entered into by the company with related parties referred to

in sub-section (1) of section 188 of the Companies Act, 2013 including certain arms length transactions under third

proviso thereto

1. Details of contracts or arrangements or transactions not arm's length basis:- NIL

(a) Name (s) of the related party and nature of relationship: NA

(b) Nature of contracts/arrangements/transactions : NA

(c) Duration of the contracts/arrangements/transactions : NA

(d) Salient terms of the contracts or arrangements or transactions including the value, if any : NA

(e) Justification for entering into such contracts or arrangements or transactions : NA

(f) Date(s) of approval by the Board : NA

(g) Amount paid as advances, if any : : NA

(h) Date on which the special resolution was passed in general meeting as required under first proviso to section 188 : NA

2. Details of material contracts or arrangements or transactions at arm's length basis

(a) Date (s) of approval by the Board – July 21, 2016

Sr. No

Nature of contracts/arrangements/transactions

Name of Related Party

Nature of Relationship

Duration of Contracts

Salient terms of contacts/transactions

` in Lacs

1. Shriarm City Union Finance Limited

Shriram Capital Limited

Holding Company

Others

Various maturities

Various maturities

Rental expense for sharing space at various locations

Rental expense for sharing space at various locations

17.96

190.51

Rental Expenses

2. Shriarm City Union Finance Limited

Holding Company

Various maturities

Rent received for occupying Space

210.25Rental Income

3. Shriarm City Union Finance Limited

Shriram Capital Limited

Holding Company

Others

Common corporate expenses and sharing charges

Common corporate expenses and sharing charges

12.14

58.13

Reimbursementof expenses

4. Shriarm City Union Finance Limited

Holding Company

Common corporate expenses and sharing charges

35.94Reimbursement of expenses received

5. Shriarm City Union Finance Limited

Holding Company

Unit termination

1.5% of net business 1.02Commission

6. Shriram OwnershipTrust

Others 5 years 1% of total income or ` 50 lacs whichever higher

321.06Use ofIntellectual Property

7. Shriram City UnionFinance Limited

Holding Company

5 years Transfer of liability for employee benefits as per actuarial valuation on transfer date

23.69Transfer of employees

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

26 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Disclosure pursuant to the provisions under Section 62(1) (b) of the Companies Act, 2013 read with Rule 12(9) of the Companies

(Share Capital and Debentures) Rules, 2014 as at March 31, 2017.

PARTICULARS

a) Options Granted 5,20,000 equity shares of 10/- each

b) Options vested Nil

c) Options exercised Nil

d) The total number of shares arising as a result of exercise of option Nil

e) Options lapsed 1,20,000

f) The Exercise price ` 10/- per share

g) Variation of terms of options Nil

h) Total number of options in force (As on March 31, 2017) 4,00,000 equity shares

I) Director and employee wise details of options granted to:

j) i) Key Managerial Personnel 1. Mr. Sujan Sinha, Managing Director & CEO

2. Mr. Kunal Shah, Chief Financial Officer

ii) Any other employee who receives a grant of option in any one year

of option amounting to 5% or more of option granted during that year Nil

iii) Identified employees who were granted option, during any one year,

equal to or exceeding 1% of the issued capital (excluding outstanding

warrants and conversions) of the Company at the time of grant Nil

SHFL Employees Stock Option Scheme, 2013

PARTICULARS

a) Options Granted 3,35,000 equity shares of 10/- each

b) Options vested Nil

c) Options exercised Nil

d) The total number of shares arising as a result of exercise of option Nil

e) Options lapsed Nil

f) The Exercise price ` 35/- per share

g) Variation of terms of options Nil

h) Total number of options in force (As on March 31, 2017) 3,35,000 equity shares

I) Director and employee wise details of options granted to:

j) i) Key Managerial Personnel 1. Mr. Sujan Sinha, Managing Director & CEO

ii) Any other employee who receives a grant of option in any one year

of option amounting to 5% or more of option granted during that year Nil

iii) Identified employees who were granted option, during any one year,

equal to or exceeding 1% of the issued capital (excluding outstanding

warrants and conversions) of the Company at the time of grant Nil

SHFL Employees Stock Option Scheme, 2016

ANNEXURE II

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

27Shriram Housing Finance Limited

Annual Disclosure on Corporate Social Responsibility (CSR) activities for the financial year 2016-17

A brief outline of the Company's CSR Policy including overview of projects or

programs proposed to be undertaken and a reference to the web-link to the

CSR Policy and projects or programs and the composition of CSR

Committee.

CSR Policy is stated herein below:

Weblink:

www.shriramhousing.in

1.

Composition of the CSR Committee Dr. Qudsia Gandhi - Chairperson

Ms. Subhasri Sriram – Member

Mr. Sujan Sinha – Member

Mr. Khushru Jijina - Member

2.

Average net profit of the Company for last three financial years ` 2952.71 Lacs3.

Prescribed CSR expenditure

(two percent of the amount mentioned in item 3 above)

` 59.05 Lacs4.

Details of CSR spent during the financial year:

Total amount to be spent for the financial year

Amount unspent, if any

` 4.20 Lacs

` 54.85 Lacs

5.

Details of amount spent on CSR activities during the financial year 2016-17

Sr. No

CSR projector ActivityIdentified

Sector in whichthe project iscovered(clause no. ofSchedule VII tothe CompaniesAct, 2013,as amended

Project of Program(1) Local Area orOther(2) Specify theState and districtwhere projectsor programs wasundertaken

AmountOutlay(Budget)Project orProgramWise (`)

Amount spenton the Projectsor ProgramsSub Heads:(1) DirectExpenditureon Projects orPrograms (2) Overheads (`)

AmountSpent Director throughImplementingAgency

CumulativeExpenditureupto thereportingperiod i.e.FY 2016-2017 (`)

Care of children suffering from cancer

Healthcare Navi Mumbai 3,00,000 3,00,000 3,00,000 Implementing Agency

1.

Care of children suffering from malnutrition

Healthcare Singbhum District, Jharkhand

1,20,000 1,20,000 1,20,000 Implementing Agency

2.

In case the Company has failed to spend the two percent of the average net profit of the last three financial year or any part thereof, the company shall provide the reasons for not spending the amount in its Board Report.

6.

The Company is in the process of evaluating certain CSR projects. The Company alongwith its holding company and other group companies has formed the Shriram Seva Sankalp Foundation a Section 8 Company to evaluate and conduct CSR activities. This will ensure that the amount as per the required CSR spent and also the incremental expenditure accruing from year to year would be absorbed appropriately.

We hereby affirm that the CSR Policy (“Policy”) of the Company as approved by the Board of Directors of the Company is monitored by the CSR Committee and the CSR activities have been implemented in accordance with the Policy.

Dr. Qudsia Gandhi(DIN : 02568631)Chairperson of the Corporate Social Responsibility Committee

Ms. Subhasri Sriram(DIN : 01998599)Member of the Corporate Social Responsibility Committee

ANNEXURE III

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

28 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Disclosure under Rule 5 (1) of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014

Sr. No

Name of Directors & KMPs

Designation Category Remunerationduring the year (2016-17)

% of increaseduring the year2016-17

Ratio of remuneration of each Director to median remuneration of employees

Mr. Sujan Sinha1. Managing Director &

CEO

E, NI 95.58 30 27.75

2. Mr. Khushru Jijina Director NE,NI - - -

3. Dr. Qudsia Gandhi Director NE,I 1.20 100 0.35

4. Ms. Subhasri Sriram Director NE,NI - - -

5. Mr.Venkataraman Murali Director NE,I 1.80 100 0.52

6. Mr. Y.S.Chakravarti Director NE,NI - - -

7. Mr. Duruvasan Ramachandra*

Director NE,NI - - -

8. Mr. G. S. Sundararajan* Director NE,NI - - -

9. Mr. Kunal Shah CFO - 74.15 31.74 -

10. Ms. Nikita Hule CS - 6.56 - -

Managing Director (“MD”), Chief Executive Officer (“CEO”) , Chief Financial Officer ("CFO") and Company Secretary (“CS”).Non Executive (“NE”), Executive (“E”), Non Independent (“NI”) and Independent (“I”).

* Ceased to be a Director w.e.f July 28, 2016

There was a percentage decrease in the median remuneration of employees in the financial year came to (13.43%). This decrease could be attributed to the increase in employees from last financial year.

The number of permanent employees on the rolls of company as on March 31, 2017 was 772.

The average increase in remuneration of employees was 23% and the average increase in the remuneration of the Managerial personnel was 30%. There was no exceptional circumstances for increasing the managerial remuneration.

The remuneration of directors did not contain any variable component. No employee was paid in excess of the remuneration paid to the Managing Director, who is the highest paid Director.

It is affirmed that the remuneration paid is as per the remuneration policy for Directors, Key Managerial Personnel and Employees of the Company.

ANNEXURE IV

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

ANNEXURE V

29Shriram Housing Finance Limited

Form No.MR-3

SECRETARIAL AUDIT REPORTFINANCIAL YEAR ENDED MARCH 31, 2017

[Pursuant to section 204(1) of the Companies Act, 2013 and Rule No.9 of the Companies(Appointment and Remuneration Personnel) Rules, 2014]

To,

THE MEMBERS,SHRIRAM HOUSING FINANCE LIMITED123,ANGAPPA NAICKEN STREET,CHENNAI -600001

I have conducted the secretarial audit of the compliance of applicable statutory provisions and the adherence to good corporate

practices by Shriram Housing Finance Limited (hereinafter called the company). Secretarial Audit was conducted in a manner

that provided us a reasonable basis for evaluating the corporate conducts/statutory compliances and expressing our opinion

thereon.

Based on my verification of Company's books, papers, minute books, forms and returns filed and other records maintained by

the company and also the information provided by the Company, its officers, agents and authorized representatives during the

conduct of secretarial audit, We hereby report that in our opinion, the company has, during the audit period covering the financial

year ended on March 31, 2017 complied with the statutory provisions listed here under and also that the Company has proper

Board-processes and compliance-mechanism in place to the extent, in the manner and subject to the reporting made hereinafter.

I have examined the books, papers, minute books, forms and returns filed and other records maintained by the Company for the

financial year ended on March 31, 2017 according to the provisions of:

1) The Companies Act, 2013 (the Act) and the rules made there under;

2) The Securities Contracts(Regulation) Act, 1956 ('SCRA') and the rules made thereunder;

3) The Depositories Act, 1996 and the Regulations and Bye-laws framed thereunder;

4) Foreign Exchange Management Act, 1999 and the rules and regulations made thereunder to the extent of Foreign

Direct Investment;

5) The following Regulations and Guidelines prescribed under the Securities and Exchange Board of India Act, 1992

('SEBI Act') :-

(a) The Securities and Exchange Board of India (Issue and Listing of Debt Securities) Regulations, 2008;

(b) The Securities and Exchange Board of India (Registrars to an Issue and Share Transfer Agents) Regulations, 1993

regarding the Companies Act and dealing with client;

(c) The Securities and Exchange Board of India (Listing Obligation and Disclosure Requirements) Regulation, 2015

6) The National Housing Bank Act, 1987 including Housing Finance Companies ( NHB) Directions, 2014

7) Reserve Bank of India Act, 1934

We have also examined compliance with the applicable clauses of the following:

(i) Secretarial Standards issued by The Institute of Company Secretaries of India.

(ii) The Debt Listing Agreements entered into by the Company with BSE Limited;

During the period under review the Company has complied with the provisions of the Act, Rules, Regulations, Guidelines,

Standards, etc. mentioned above.

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

30 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

I further report that

The Board of Directors of the Company is duly constituted with proper balance of Executive Directors, Non-Executive Directors

and Independent Directors. The changes in the composition of the Board of Directors that took place during the period under

review were carried out in compliance with the provisions of the Act.

Adequate notice is given to all directors to schedule the Board Meetings, agenda and detailed notes on agenda were sent at least

seven days in advance, and a system exists for seeking and obtaining further information and clarifications on the agenda items

before the meeting and for meaningful participation at the meeting.

All decisions were carried out with unanimous approval of the Board and there was no instance of dissent voting by any member

during the period under review. I have examined the systems and processes established by the Company to ensure the compliance with general laws including

Labour Laws, Employees Provident Funds Act, Employees State Insurance Act & other State Laws, considering and relying upon

representations made by the Company and its Officers for systems and mechanisms formed by the Company for compliance

under these laws and other applicable sector specific Acts, Laws, Rules and Regulations applicable to the Company and its

observance by them.

I further report that there are adequate systems and processes in the company commensurate with the size and operations of the

company to monitor and ensure compliance with applicable laws, rules, regulations and guidelines.

I further report that during the audit period, there were no specific events / actions having major bearing on the Company's affairs

in pursuance of the above referred laws, rules, regulations, guidelines, etc.

(P. Sriram)

P. Sriram & Associates

FCS No. 4862/C.P. No: 3310

Place: ChennaiDate: April 22, 2017

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

ANNEXURE A

31Shriram Housing Finance Limited

To,

THE MEMBERS,SHRIRAM HOUSING FINANCE LIMITED

My report of even date is to be read along with this supplementary testimony.

1. Maintenance of secretarial record is the responsibility of the management of the company. My responsibility is to express an

opinion on these secretarial records based on our audit.

2. I have followed the audit practices and processes as were appropriate to obtain reasonable assurance about the correctness

of the contents of the Secretarial records. The verification was done on test basis to ensure that correct facts are reflected in

secretarial records. I believe that the processes and practices, the company had followed provide a reasonable basis for our

opinion.

3. I have not verified the correctness and appropriateness of financial records and Books of Accounts of the company.

4. Wherever required, I have obtained the Management representation about the compliance of laws, rules and regulations and

happening of events etc.,

5. The compliance of the provisions of Corporate and other applicable laws, rules, regulations, standards is the responsibility of

management. My examination was limited to the verification of procedures on test basis.

6. The Secretarial Audit report is neither an assurance as to the future viability of the company nor of the efficacy or effectiveness

with which the management has conducted the affairs of the company

(P. Sriram)

P. Sriram & Associates

FCS No. 4862/C.P. No: 3310

Place: ChennaiDate: April 22, 2017

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

32 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

Form No. MGT - 9

EXTRACT OF ANNUAL RETURN as on the financial year ended on March 31, 2017

[Pursuant to section 92 (3) of the Companies Act, 2013 and rule 12(1) of the Companies

(Management and Administration) Rules, 2014]

I. REGISTRATION AND OTHER DETAILS :

i) CIN U65929TN2010PLC078004

ii) Incorporation Date November 9, 2010

iii) Name of the Company Shriram Housing Finance Limited

iv) Category/Sub- Category of the Company Company Limited by Shares / Indian Non

Government Company

v) Address of the Registered Office and contact details 123, Angappa Naicken Street, Chennai – 600 001

Contact No. 044- 2534 1431

vi) Whether listed company Listed on the Wholesale Debt Segment of Bombay

Stock Exchange

vii) Name, Address and Contact details of Registrar and Integrated Enterprises (India) Limited,

Transfer Agent, if any 2nd Floor, 'Kences Towers',No.1 Ramakrishna Street,

North Usman Road, T Nagar, Chennai – 600 017

Shriram Insight Share Brokers Limited

Mookambika Complex 4, Lady Desika Road, Mylapore

Chennai – 600 004

II. PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY

All the business activities contributing 10% or more of the total turnover of the Company shall be stated

Sl. No. Name and Description of main products / services

% to total turnover of the Company

1 Interest income on Loans 93%

2 Fees Income 6%

NIC Code of the Product/ Service

65922

65922

III. PARTICULARS OF HOLDING, SUBSIDIARY AND ASSOCIATE COMPANIES

Sl. No. Name and Address of the Company

HOLDING/ SUBSIDIARY / ASSOCIATE

1 Shriram City Union Finance Limited, 123, Angappa Naicken Street, Chennai – 600 001

CIN/GLN

L65191TN1986PLC012840

% of shares held

Applicable section

Holding Company 77.25% 2(46)

ANNEXURE VI

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

33Shriram Housing Finance Limited

IV. S

HA

RE

HO

LD

ING

PA

TT

ER

N (

Eq

uit

y S

hare

Cap

ital B

reaku

p a

s p

erc

en

tag

e t

o T

ota

l E

qu

ity)

(i)

Cate

go

ry-w

ise s

hare

ho

ldin

g

Sl. N

o.

Cate

go

ry o

f sh

are

ho

lde

rsN

o. o

f sh

are

s h

eld

at

the

b

eg

inn

ing

of

the

ye

ar

No

. o

f sh

are

s h

eld

at

the

e

nd

of

the

ye

ar

%

Ch

an

ge

d

uri

ng

th

e y

ear

Dem

at

Ph

ysi

cal

Tota

l %

of

Dem

at

Ph

ysi

cal

Tota

l %

of

to

tal

to

tal

sh

are

s

share

s

A.

Pro

mo

ters

1.

Ind

ian

a)

Ind

ivid

ual/ H

UF

-

6

6

0

- 6

6

0

N

il

b)

Cen

tral G

ovt

-

- -

- -

- -

- -

c)

Sta

te G

ovt

(s)

-

- -

- -

- -

- -

d)

Bo

die

s C

orp

ora

te

- 1

65

43

99

94

1

65

43

99

94

7

7.2

5

- 1

65

43

99

94

1

65

43

99

94

7

7.2

5

Nil

e)

Ban

ks/

FIs

-

- -

- -

- -

- -

f)

An

y o

ther

- -

- -

- -

- -

-

S

ub

-to

tal (A

) (1

) :-

-

16

54

40

00

0

16

54

40

00

0

77

.25

-

16

54

40

00

0

16

54

40

00

0

77

.25

N

il

2.

Fo

reig

n

a)

NR

Is

-

- -

- -

- -

- -

In

div

idu

als

c)

B

od

ies

-

- -

- -

- -

- -

C

orp

ora

te

d)

B

an

ks

/FIs

-

- -

- -

- -

- -

e)

An

y o

ther

- -

- -

- -

- -

-

S

ub

-to

tal

- -

- -

- -

- -

-

(A

) (2

) :-

To

tal

-

16

54

40

00

0

16

54

40

00

0

77

.25

-

16

54

40

00

0

16

54

40

00

0

77

.25

N

il

Sh

are

ho

ldin

g

o

f P

rom

ote

r (A

) =

(A)

(1)

+ (

A)

(2)

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

34

Sl. N

o.

Cate

go

ry o

f sh

are

ho

lde

rsN

o. o

f sh

are

s h

eld

at

the

b

eg

inn

ing

of

the

ye

ar

No

. o

f sh

are

s h

eld

at

the

e

nd

of

the

ye

ar

%

Ch

an

ge

d

uri

ng

th

e y

ear

Dem

at

Ph

ysi

cal

Tota

l %

of

Dem

at

Ph

ysi

cal

Tota

l %

of

to

tal

to

tal

sh

are

s

share

sB

. P

ub

lic S

hare

ho

ldin

g1.

Insti

tuti

on

s

- -

- -

- -

- -

-a)

Mu

tual F

un

ds

- -

- -

- -

- -

-b

) B

an

ks

/ F

I -

- -

- -

- -

- -

c)

Cen

tral G

ovt

.

- -

- -

- -

- -

-d

) S

tate

Go

vt (

s)

- -

- -

- -

- -

-e)

Ven

ture

- -

- -

- -

- -

-

Cap

ital

F

un

ds

f)

Insu

ran

ce

- -

- -

- -

- -

-

Co

mp

an

ies

g)

FIIs

- -

- -

- -

- -

-h

)

Fo

reig

n

-

- -

- -

- -

- -

V

en

ture

C

ap

ital F

un

ds

i)

Oth

ers

(sp

ecify

) -

- -

- -

- -

- -

S

ub

-to

tal (B

) (1

) :-

-

- -

- -

- -

-2.

No

n -

In

sti

tuti

on

s

a)

Bo

die

s C

orp

ora

te

- -

- -

- -

- -

-i)

In

dia

n

- -

- -

- -

- -

-ii)

O

vers

eas

- 4

87

20

00

0

48

72

00

00

2

2.7

5%

-

48

72

00

00

4

87

20

00

0

22

.75

%

Nil

b)

Ind

ivid

uals

-

- -

- -

- i)

In

div

idu

al

- -

- -

- -

- -

sh

are

ho

lders

h

old

ing

no

min

al

S

hare

Cap

ital u

pto

Rs.

1 L

akh

ii)

Ind

ivid

ual

- -

- -

- -

- -

sh

are

ho

lders

ho

ldin

g n

om

inal s

hare

cap

ital i

n e

xcess

of

R

s. 1

Lakh

c)

Oth

ers

(sp

ecify

) -

- -

- -

--

-

Su

b-t

ota

l (B

) (2

) :-

-

48

72

00

00

4

87

20

00

0

22

.75

%

- 4

87

20

00

0

48

72

00

00

2

2.7

5%

N

il

Tota

l Pu

blic

-

- -

- -

- -

- -

S

hare

ho

ldin

g

(B)

= (

B)

(1)

+ (

B)

(2)

- 4

87

20

00

0

48

72

00

00

2

2.7

5%

-

48

72

00

00

4

87

20

00

0

22

.75

%

Nil

C.

Sh

are

s h

eld

by

C

ust

od

ian

fo

r G

DR

s

& A

DR

s

Gra

nd

To

tal (

A+

B+

C)

- 2

14

16

00

00

2

14

16

00

00

1

00

%

- 2

14

16

00

00

2

14

16

00

00

1

00

%

-

SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

27Shriram Housing Finance Limited

ii) Shareholding of Promoters

Shareholding at thebeginning of the year

Name of Shareholder

Sl. No.

No. of % to total % of shares No. of % to total % of shares shares shares of Pledged/ shares shares of Pledged/ the Encumbered the Encumbered company to total shares company to total shares

1. Shriram City 165439994 77.25 Nil 165439994 77.25 Nil Union Finance Limited

iii) Change in Promoters' Shareholding (please specify, if there is no change) - NIL

Cumulative Shareholding during the year

Shareholding at the beginning of the year

Sl. No.

1. Valiant Mauritius Partners 48720000 22.75 48720000 22.75 FDI Limited

No. of shares % of total shares of the Company

No. of shares % of total shares of the Company

No Change

At the beginning of the year

Date wise Increase/ Decrease in Promoters Share holding during the year specifying the reasons for increase/decrease (e.g. Allotment/ transfer/ bonus/ sweat equity etc)

At the end of the year

% Change

inshare

holdingduring

the year

No. of shares held atthe end of the year

Nil

iv) Shareholding Pattern of top ten shareholders (other than Directors, Promoters and Holders of GDRs and ADRs):

Cumulative Shareholding during the year

Shareholding at the beginning of the year

Sl. No.

No. of shares % of total shares of the Company

No. of shares % of total shares of the Company

35Shriram Housing Finance Limited

Name of Shareholder

Name of Shareholder

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

V) Shareholding of Directors and Key Managerial Personnel

Indebtedness at the

beginning of the

financial year

i) Principal Amount 84321.33 1000 - 85321.33

ii)Interest due but not paid - - - -

iii) Interest accrued but not due 1174.28 1.02 - 1175.30

Total (i+ii+iii) 85495.61 1001.02 - 86496.63

Change in Indebtedness

during the financial year

Addition 76731.32 45.07 - 76776.39

Reduction 19801.18 1046.09 - 20847.27

Net Change 56930.14 (1001.02) - 55929.12

Indebtedness at the

end of the financial year

i) Principal Amount 138797.69 - - 138797.69

ii) Interest due but not paid - - - -

i)Interest accrued but not due 3628.06 - - 3628.06

Total (i+ii+iii) 142425.75 - - 142425.75

1. Ms. Subhasri Sriram 1 negligible 1 negligible2. Mr. Y. S. Chakravarthi 1 negligible 1 negligible

Cumulative Shareholding during at the end of the year

Name of the Directors and Key Manageral Personnel

Sl. No.

No. of shares No. of shares% of total shares of the Company

Shareholding at the beginning of the year

% of total shares of the Company

V. INDEBTEDNESS

Indebtedness of the Company including interest outstanding/accrued but not due for payment

Secured Loans excluding deposits

Unsecured Loans

Deposits TotalIndebtedness

` in lacs

36 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

VI. REMUNERATION OF DIRECTORS AND KEY MANAGERIAL PERSONNEL

A. REMUNERATION TO MANAGING DIRECTOR, WHOLE TIME DIRECTOR AND / OR MANAGER : ` in lacs

Sl. No. Particulars of Remuneration Name of MD/WTD/Manager

Sujan Sinha – Total Amount

Managing Director & CEO

1. Gross Salary

(a) Salary as per provisions contained 84.59 84.59

in Section 17(1) of the Income Tax Act, 1961

(b) Value of perquisites u/s 17(2) of the Income 39.04* 39.04*

Tax Act, 1961

(c) Profits in lieu of salary under section 17(3)1 - -

of the Income Tax Act, 1961

2. Stock Option - -

3. Sweat Equity - -

4. Commission -

- As % of profit - -

- Others, specify - -

5. Others, please specify:

Variable Pay 11.00 11.00

Total (A) 134.64 134.64

Ceiling as per the Act

*includes perquisite value of stock options received from holding company

37Shriram Housing Finance Limited

B. REMUNERATION TO OTHER DIRECTORS: ` in lacs

Sl. No. Particulars of Remuneration Name of MD/WTD/Manager Total Amount

1. Independent Directors Venkataraman Murali Qudsia Gandhi

• Fee for attending Board Committee 1.80 1.20 3.00

• Meetings Commission - - -

• Others, please specify

Total (1) 1.80 1.20 3.00

2. Other Non-Executive Directors

• Fee for attending Board Committee meetings - - -

• Commission - - -

• Others, please specify - - -

Total (2) - - -

Total (B) = (1+2) 1.80 1.20 3.00

Total Managerial Remuneration 1.80 1.20 3.00

Ceiling as per the Act

The remuneration payable to any one managing director;

or whole-time director or manager in terms of the

provisions of the CA 2013, shall not exceed 5% of the net

profit of the Company. The remuneration paid to Managing

Director & CEO is well within the said limit.

In terms of the provisions of the Companies Act, 2013,

the remuneration payable to directors other than

executive directors shall not exceed 1% of the net profit

of the Company. The Remuneration paid to the directors

is well within the said limits

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

VII. PENALITIES / PUNISHMENT / COMPOUNDING OF OFFENCES

Type Section Brief Details of Authority [RD/ Appeal made, if

of the Description Penalty/ NCLT/ COURT] any (give details)

Companies Compounding/

Act fees imposed

A. COMPANY

Penalty Nil Nil Nil Nil Nil

Punishment Nil Nil Nil Nil Nil

Compounding Nil Nil Ni lNil Nil

B. DIRECTORS

Penalty Nil Nil Nil Nil Nil

Punishment Nil Nil Nil Nil Nil

Compounding Nil Nil Nil Nil Nil

C. OTHER OFFICERS IN DEFAULT

Penalty Nil Nil Nil Nil Nil

Punishment Nil Nil Nil Nil Nil

Compounding Nil Nil Nil Nil Nil

38 SHRIRAM HOUSING FINANCE LIMITED | 7TH ANNUAL REPORT 2016-17

C. REMUNERATION TO KEY MANAGERIAL PERSONNEL OTHER THAN MD/MANAGER/WTD

Sl. No. Particulars of Remuneration Company Chief Financial Total Amount

Secretary Officer

1. Gross Salary

(a) Salary as per provisions 6.56 62.11 68.67

contained in Section 17(1) of the

Income Tax Act, 1961

(b) Value of perquisites u/s 17(2) Income Tax Act, 1961 - - -

(c ) Profits in lieu of salary under section 17(3) - - -

of Income Tax, 1961

2. Stock Option - - -

3. Sweat Equity - - -

4. Commission - As % of profit - - -

- Others, specify - - -

5. Others, please, specify :

Variable Pay - 12.04 12.04

Total 6.56 74.15 80.71

` in lacs

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

39Shriram Housing Finance Limited

Mr. Sujan Sinha

Managing Director & CEO

Mr. Kunal Shah

Chief Financial Officer

ANNEXURE VII

We the undersigned Sujan Sinha, Managing Director & CEO and Kunal Shah, Chief Financial Officer hereby certify that

for the financial year ended March 31, 2017, we have reviewed Annual accounts, financial statement and the cash flow

statement and to the best of our knowledge and belief:

1. These statements do not contain any materially untrue statement or omit any material fact or contain statements that

might be misleading.

2. These statements together present a true and fair view of the Company's affairs and are in compliance with existing

accounting standard, applicable laws and regulations.

3. There are no transaction entered into by the Company during the year which are fraudulent, illegal or violate the

Company's Policies.

4. We accept responsibility for establishing and maintaining internal controls and that we have evaluated the

effectiveness of internal control system of the Company and we have disclosed to the auditors and the Audit

Committee the deficiencies, of which we are aware, in the design or operation of the internal control system and we

have taken the steps to rectify these deficiencies.

5. We further certify that:

a. There have been no significant changes in internal control during this year.

b. There have been no significant changes in the accounting policies during this year except as mentioned in the

significant accounting policies and notes to accounts.

CEO and CFO Certification

Place: MumbaiDate: April 22, 2017

COMPANY OVERVIEW STATUTORY REPORTS FINANCIAL STATEMENTS

Overview of the Indian Economy

The global economy is in the midst of a decade long slow growth environment characterized by an imminent productivity growth

crisis. Global growth reported by World Bank in 2016 is estimated at a post-crisis low of 2.3 % and is projected to rise to 2.7 % in

2017. Stagnant global trade, subdued investment, and heightened policy uncertainty marked another difficult year for the world

economy. For emerging markets and developing economies, the rise in interest rates in the US and the strengthening dollar also

led to a 'notable tightening of financing conditions' which means that credit is either more expensive or harder to get.

The World Bank has cut its economic growth forecast for India to 7% in 2016-17, followed by further acceleration to 7.6 % in 2017-

18 and 7.8% in 2018-19.The acceleration of structural reforms, the move towards a rule-based policy framework and low

commodity prices have provided a strong growth impetus. Recent deregulation measures and efforts to improve the ease of

doing business have boosted foreign investment.