annual energy outlook 2019 - eia.gov · by law, eia's data, analyses, and forecasts are...

TRANSCRIPT

Annual Energy Outlook 2019with projections to 2050

January 24, 2019www.eia.gov/aeo#AEO2019

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

Annual Energy Outlook 2019with projections to 2050

January 2019U.S. Energy Information Administration

Office of Energy AnalysisU.S. Department of Energy

Washington, DC 20585

This publication is on the Web at:www.eia.gov/aeo

This report was prepared by the U.S. Energy Information Administration (EIA), the statistical and analytical agency within the U.S. Department of Energy. By law, EIA's data, analyses, and forecasts are independent of approval by any other officer or employee of the United States Government. The views in this report therefore should not be construed as representing those of the Department of Energy or other federal agencies.

3

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 4

• Projections in the Annual Energy Outlook 2019 (AEO2019) are not predictions of what will happen, but rather modeled projections of what may happen given certain assumptions and methodologies.

• The AEO is developed using the National Energy Modeling System (NEMS), an integrated model that captures interactions of economic changes and energy supply, demand, and prices.

• Energy market projections are subject to much uncertainty because many of the events that shape energy markets as well as future developments in technologies, demographics, and resources cannot be foreseen with certainty. To illustrate the importance of key assumptions, AEO2019 includes a Reference case and six side cases that systematically vary important underlying assumptions.

• More information about the assumptions used in developing these projections will be available shortly after the release of the AEO2019.

• The AEO is published to satisfy the Department of Energy Organization Act of 1977, which requires the Administrator of the U.S. Energy Information Administration to prepare annual reports on trends and projections for energy use and supply.

The Annual Energy Outlook provides long-term energy projections for the United States

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The AEO2019 Reference case represents EIA’s best assessment of how U.S. and world energy markets will operate through 2050, based on many key assumptions. For instance, the Reference case projection assumes improvement in known energy production, delivery, and consumption technology trends.

• The economic and demographic trends reflected in the Reference case reflect current views of leading economic forecasters and demographers.

• The Reference case generally assumes that current laws and regulations that affect the energy sector, including laws that have end dates, are unchanged throughout the projection period. This assumption is important because it permits EIA to use the Reference case as a benchmark to compare policy-based modeling.

• The potential impacts of proposed legislation, regulations, or standards are not included in the AEO2019 cases.

• The Reference case should be interpreted as a reasonable baseline case that can be compared with the cases that include alternative assumptions.

What is the Reference case?

5

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The side cases in AEO2019 show the effect that changing important model assumptions have on the projections when compared with the Reference case.

• Two AEO2019 side cases are the High and Low Oil Price cases, which represent international conditions outside the United States that could collectively drive prices to extreme, sustained deviations from the Reference case price path.

• Additional AEO2019 side cases are the High and Low Oil and Gas Resource and Technology cases, where production costs and resource availability within the United States are varied, allowing for more or less production at given world oil and natural gas prices.

• The two AEO2019 side cases that vary the effects of economic assumptions on energy consumption are the High and Low Economic Growth cases, which modify population growth and productivity assumptions throughout the projection period to yield higher or lower compound annual growth rates for U.S. gross domestic product than in the Reference case.

What are the side cases?

6

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

Key takeaways

Critical drivers and model updates

Petroleum and other liquids

Natural gas

Electricity generation

Transportation

Buildings

Industrial

References

7

Table of contents slide number

9

29

51

69

87

115

131

147

161

8

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

Key takeawaysEIA’s Annual Energy Outlook provides modeled projections of domestic energy markets through 2050, and it includes cases with different assumptions regarding macroeconomic growth, world oil prices, and technological progress.

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

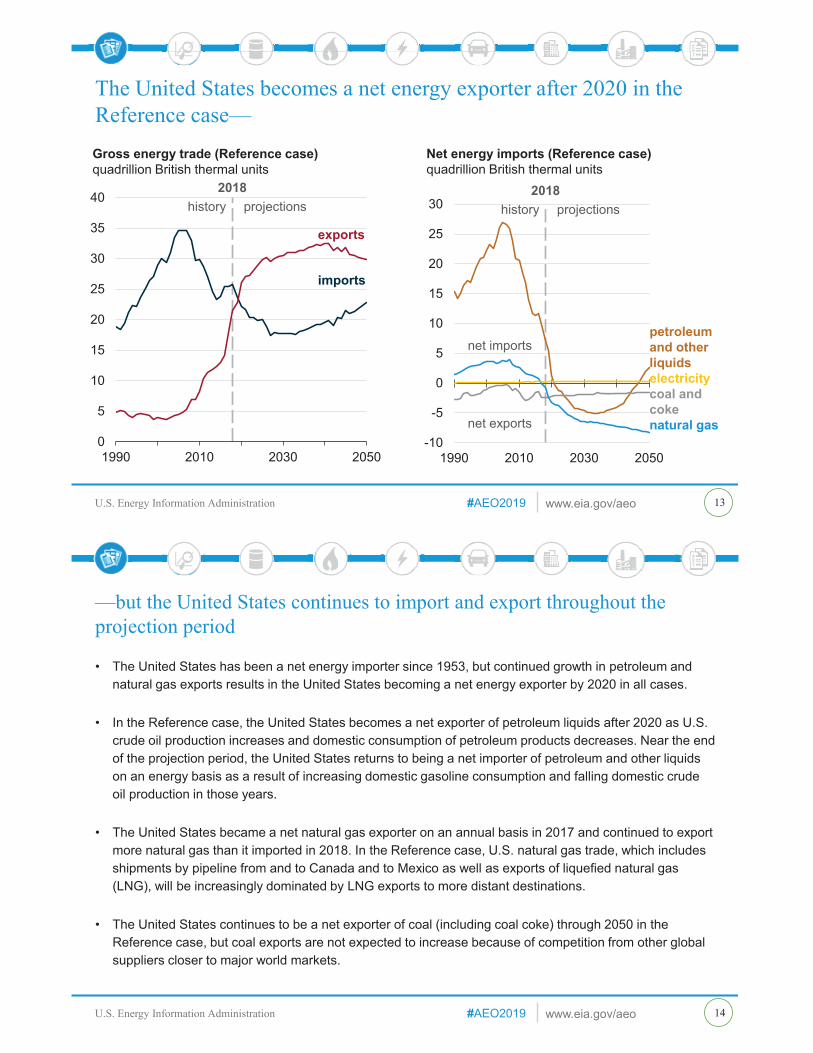

• The United States becomes a net energy exporter in 2020 and remains so throughout the projection period as a result of large increases in crude oil, natural gas, and natural gas plant liquids (NGPL) production coupled with slow growth in U.S. energy consumption.

• Of the fossil fuels, natural gas and NGPLs have the highest production growth, and NGPLs account for almost one-third of cumulative U.S. liquids production during the projection period.

• Natural gas prices remain comparatively low during the projection period compared with historical prices, leading to increased use of this fuel across end-use sectors and increased liquefied natural gas exports.

• The power sector experiences a notable shift in fuels used to generate electricity, driven in part by historically low natural gas prices. Increased natural gas-fired electricity generation; larger shares of intermittent renewables; and additional retirements of less economic existing coal and nuclear plants occur during the projection period.

• Increasing energy efficiency across end-use sectors keeps U.S. energy consumption relatively flat, even as the U.S. economy continues to expand.

Key takeaways from the Reference case

12

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 13

The United States becomes a net energy exporter after 2020 in the Reference case—

0

5

10

15

20

25

30

35

40

1990 2010 2030 2050

Gross energy trade (Reference case)quadrillion British thermal units

exports

imports

2018history projections

-10

-5

0

5

10

15

20

25

30

1990 2010 2030 2050

Net energy imports (Reference case)quadrillion British thermal units

petroleumand other liquidselectricitycoal and cokenatural gas

2018history projections

net imports

net exports

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The United States has been a net energy importer since 1953, but continued growth in petroleum and natural gas exports results in the United States becoming a net energy exporter by 2020 in all cases.

• In the Reference case, the United States becomes a net exporter of petroleum liquids after 2020 as U.S. crude oil production increases and domestic consumption of petroleum products decreases. Near the end of the projection period, the United States returns to being a net importer of petroleum and other liquids on an energy basis as a result of increasing domestic gasoline consumption and falling domestic crude oil production in those years.

• The United States became a net natural gas exporter on an annual basis in 2017 and continued to export more natural gas than it imported in 2018. In the Reference case, U.S. natural gas trade, which includes shipments by pipeline from and to Canada and to Mexico as well as exports of liquefied natural gas (LNG), will be increasingly dominated by LNG exports to more distant destinations.

• The United States continues to be a net exporter of coal (including coal coke) through 2050 in the Reference case, but coal exports are not expected to increase because of competition from other global suppliers closer to major world markets.

—but the United States continues to import and export throughout the projection period

14

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 15

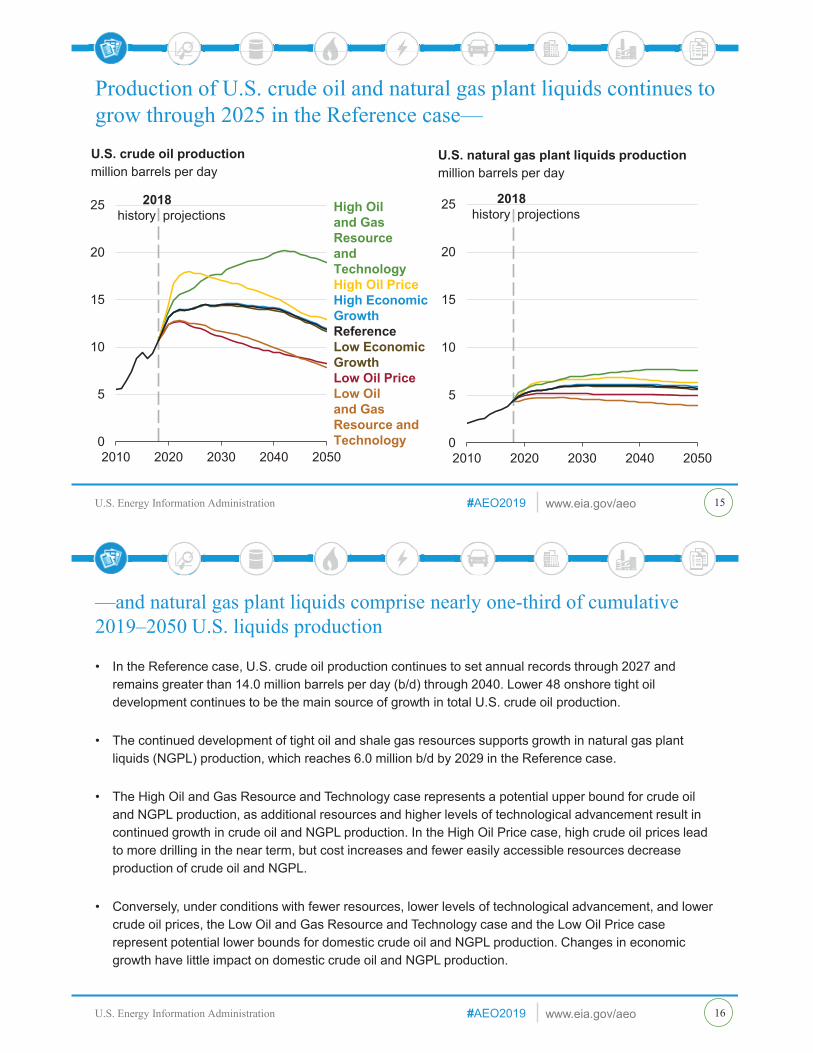

Production of U.S. crude oil and natural gas plant liquids continues to grow through 2025 in the Reference case—

0

5

10

15

20

25

2010 2020 2030 2040 2050

U.S. crude oil productionmillion barrels per day

2018history projections High Oil

and Gas Resource and TechnologyHigh Oil PriceHigh Economic GrowthReferenceLow EconomicGrowthLow Oil PriceLow Oil and Gas Resource and Technology 0

5

10

15

20

25

2010 2020 2030 2040 2050

U.S. natural gas plant liquids productionmillion barrels per day

2018history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, U.S. crude oil production continues to set annual records through 2027 and remains greater than 14.0 million barrels per day (b/d) through 2040. Lower 48 onshore tight oil development continues to be the main source of growth in total U.S. crude oil production.

• The continued development of tight oil and shale gas resources supports growth in natural gas plant liquids (NGPL) production, which reaches 6.0 million b/d by 2029 in the Reference case.

• The High Oil and Gas Resource and Technology case represents a potential upper bound for crude oil and NGPL production, as additional resources and higher levels of technological advancement result in continued growth in crude oil and NGPL production. In the High Oil Price case, high crude oil prices lead to more drilling in the near term, but cost increases and fewer easily accessible resources decrease production of crude oil and NGPL.

• Conversely, under conditions with fewer resources, lower levels of technological advancement, and lower crude oil prices, the Low Oil and Gas Resource and Technology case and the Low Oil Price case represent potential lower bounds for domestic crude oil and NGPL production. Changes in economic growth have little impact on domestic crude oil and NGPL production.

—and natural gas plant liquids comprise nearly one-third of cumulative 2019–2050 U.S. liquids production

16

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

1

2

3

4

5

6

7

8

9

10

2000 2010 2020 2030 2040 2050

Dry natural gas production from oil formationstrillion cubic feet

2018history projections

Southwest

Gulf Coast

Other

17

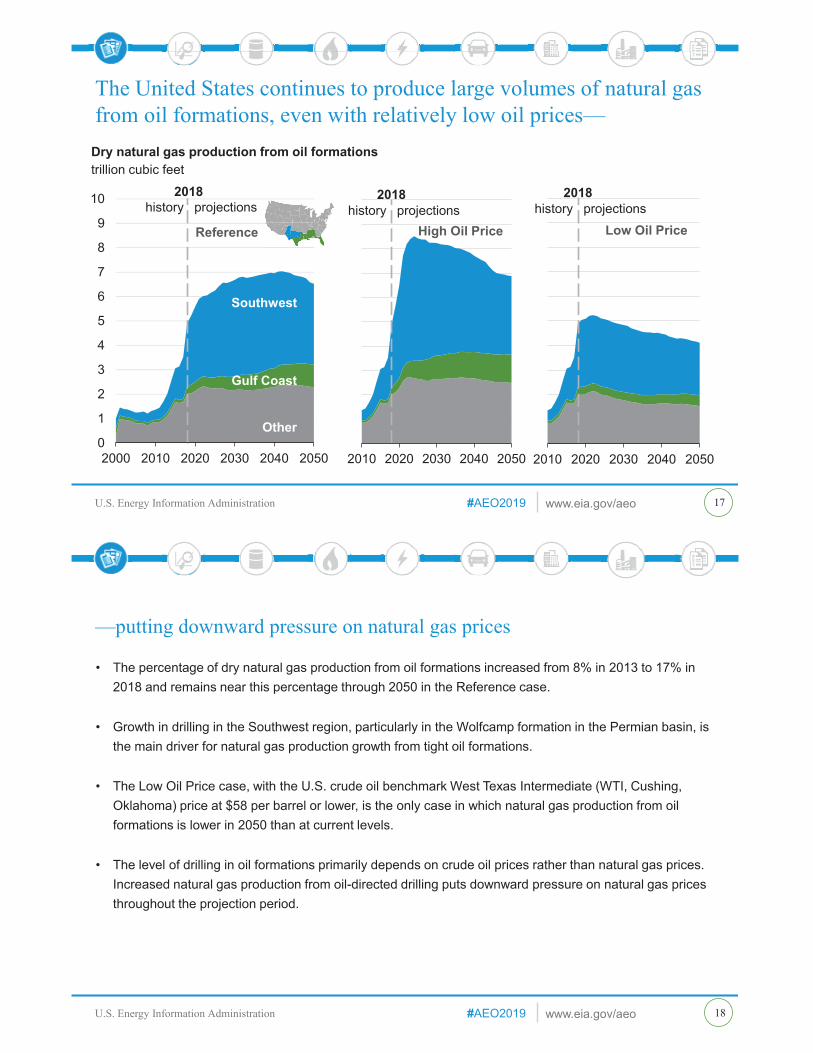

The United States continues to produce large volumes of natural gas from oil formations, even with relatively low oil prices—

2010 2020 2030 2040 2050

High Oil Price

2018history projections

2010 2020 2030 2040 2050

Low Oil Price

2018history projections

Reference

Southwest

Gulf Coast

Other

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The percentage of dry natural gas production from oil formations increased from 8% in 2013 to 17% in 2018 and remains near this percentage through 2050 in the Reference case.

• Growth in drilling in the Southwest region, particularly in the Wolfcamp formation in the Permian basin, is the main driver for natural gas production growth from tight oil formations.

• The Low Oil Price case, with the U.S. crude oil benchmark West Texas Intermediate (WTI, Cushing, Oklahoma) price at $58 per barrel or lower, is the only case in which natural gas production from oil formations is lower in 2050 than at current levels.

• The level of drilling in oil formations primarily depends on crude oil prices rather than natural gas prices. Increased natural gas production from oil-directed drilling puts downward pressure on natural gas prices throughout the projection period.

—putting downward pressure on natural gas prices

18

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 19

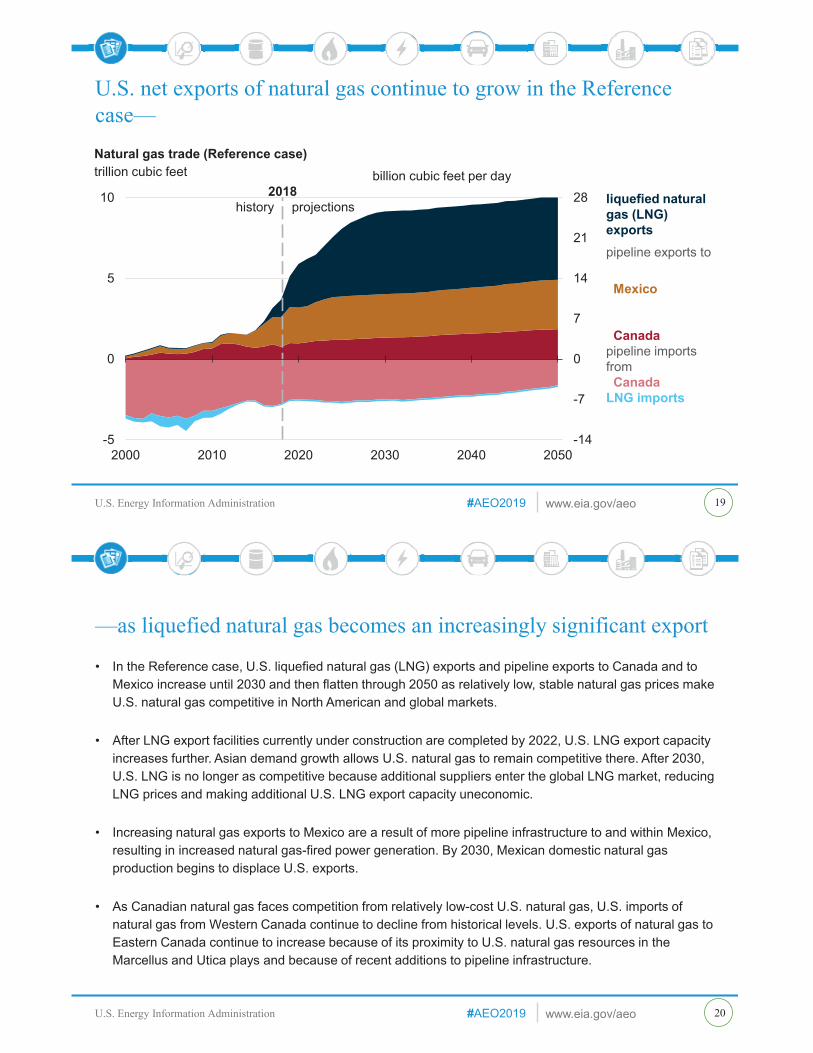

U.S. net exports of natural gas continue to grow in the Reference case—

-14

-7

0

7

14

21

28

-5

0

5

10

2000 2010 2020 2030 2040 2050

Natural gas trade (Reference case)trillion cubic feet

2018history projections liquefied natural

gas (LNG) exportspipeline exports to

Mexico

Canadapipeline imports fromCanada

LNG imports

billion cubic feet per day

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, U.S. liquefied natural gas (LNG) exports and pipeline exports to Canada and to Mexico increase until 2030 and then flatten through 2050 as relatively low, stable natural gas prices make U.S. natural gas competitive in North American and global markets.

• After LNG export facilities currently under construction are completed by 2022, U.S. LNG export capacity increases further. Asian demand growth allows U.S. natural gas to remain competitive there. After 2030, U.S. LNG is no longer as competitive because additional suppliers enter the global LNG market, reducing LNG prices and making additional U.S. LNG export capacity uneconomic.

• Increasing natural gas exports to Mexico are a result of more pipeline infrastructure to and within Mexico, resulting in increased natural gas-fired power generation. By 2030, Mexican domestic natural gas production begins to displace U.S. exports.

• As Canadian natural gas faces competition from relatively low-cost U.S. natural gas, U.S. imports of natural gas from Western Canada continue to decline from historical levels. U.S. exports of natural gas to Eastern Canada continue to increase because of its proximity to U.S. natural gas resources in the Marcellus and Utica plays and because of recent additions to pipeline infrastructure.

—as liquefied natural gas becomes an increasingly significant export

20

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 21

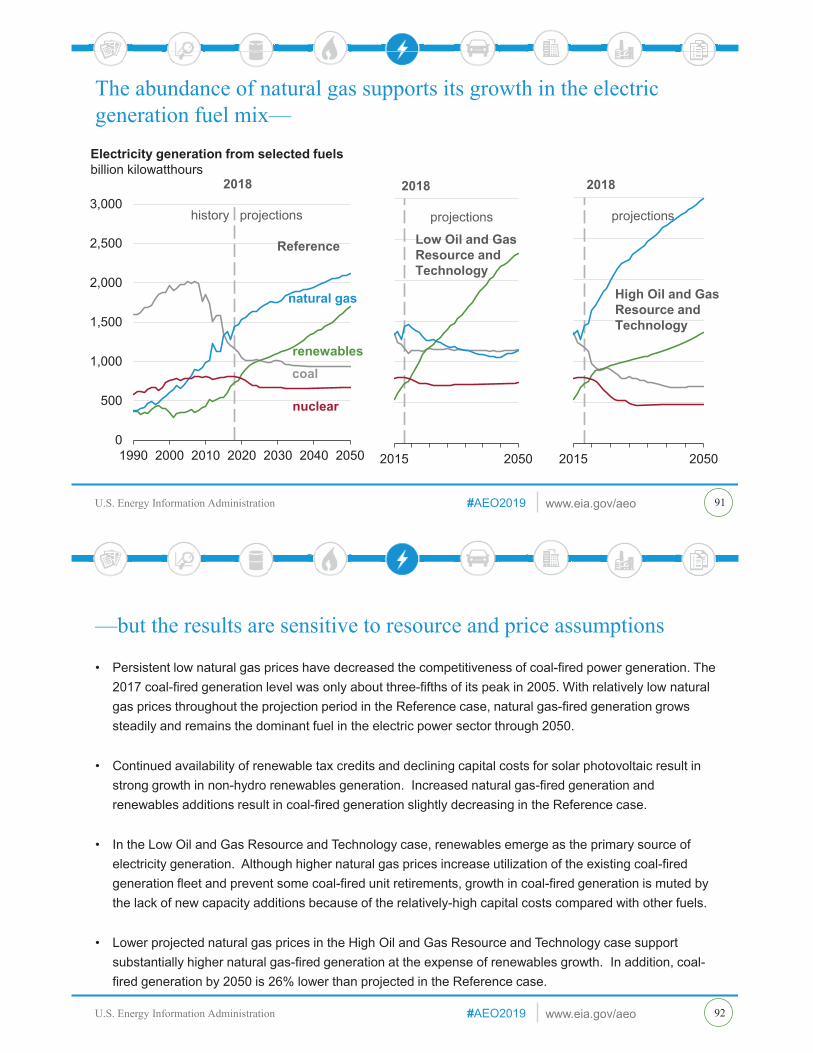

Electricity generation from natural gas and renewables increases, and the shares of nuclear and coal generation decrease—

0

1,000

2,000

3,000

4,000

5,000

6,000

2010 2020 2030 2040 2050

2018

history projections

Electricity generation from selected fuels (Reference case)billion kilowatthours

natural gasrenewablesnuclearcoal

39%

31%

12%

17%

19%

18%

34%

28%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2020 2030 2040 2050

Renewable electricity generation, including end-use (Reference case)billion kilowatthours

2018

history projections

solar PVwindgeothermalhydroelectricother

48%

37%

18%

25%

39%9%

13%

4%

5%

2%

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The continuing decline in natural gas prices and increasing penetration of renewable electricity generation have resulted in lower wholesale electricity prices, changes in utilization rates, and operating losses for a large number of baseload coal and nuclear generators.

• Generation from both coal and nuclear is expected to decline in all cases. In the Reference case, from a 28% share in 2018, coal generation drops to 17% of total generation by 2050. Nuclear generation declines from a 19% share of total generation in 2018 to 12% by 2050. The share of natural gas generation rises from 34% in 2018 to 39% in 2050, and the share of renewable generation increases from 18% to 31%.

• Assumptions of declining costs and improving performance make wind and solar increasingly competitive compared with other renewable resources in the Reference case. Most of the wind generation increase occurs in the near term, when new projects enter service ahead of the expiration of key federal production tax credits.

• Solar Investment Tax Credits (ITC) phase down after 2024, but solar generation growth continues because the costs for solar continue to fall faster than for other sources.

—as lower natural gas prices and declining costs of renewable capacity make these fuels increasingly competitive

22

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 23

End-use activities grow, and energy intensities decrease in all sectors in the Reference case—

0.00.20.40.60.81.01.21.41.61.82.0

Residential: households

2018 2050

energyintensity

demand

Commercial: floorspace

Industrial: value of shipments

Indexed end-use demand drivers and energy intensities by sector (2018–50) (Reference case)index (2018=1.0)

Note: Energy intensities are a lighter shade of the same color as the respective demand, and they are calculated as energy used per unit of respective demand.

Transportation: passenger and vehicle travel

bus, air, and rail passengermiles

energyintensity

Transportation: off-highway freight travel

highway vehicle miles

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Delivered U.S. energy consumption grows across all major end-use sectors, with electricity and natural gas growing fastest. However, increases in efficiency, represented by declines in energy intensity (the amount of energy consumed per unit of potential demand), partially offset growth in total U.S. energy consumption across all end-use sectors.

• The end-use sectors have different representative metrics for demand used to estimate energy intensity—number of households for the residential sector, floorspace for the commercial sector, industrial value of shipments for the industrial sector, and travel metrics for the transportation sector.

• Transportation travel is measured in three ways, depending on the mode: highway vehicle miles (light-and heavy-duty vehicles), passenger miles (bus, passenger rail, and air), and off-highway freight ton-miles (freight rail, air, and domestic shipping).

• The steepest decline in energy intensity is in the transportation sector, with the level of energy used per highway vehicle-mile traveled declining by 32% from 2018 to 2050 as a result of increasingly stringent fuel economy and energy efficiency standards for light- and heavy-duty vehicles.

—offsetting each other to limit energy consumption growth

24

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

35

40

45

50

55

60

65

70

75

1990 2000 2010 2020 2030 2040 2050

transportation

commercialresidential

industrial

electric power

Carbon dioxide intensity by end-use sector(Reference case)metric tons of carbon dioxide per billion British thermal units 2018

history projections

1990 2000 2010 2020 2030 2040 2050

Carbon dioxide intensity by end-use sector (Reference case)metric tons of carbon dioxide per billion British thermal units 2018

history projections

The electric power sector is redistributed to each end-use sector

25

Across end-use sectors, carbon dioxide intensity declines with changes in the fuel mix—

Note: Carbon dioxide intensities are calculated as carbon dioxide emissions per unit energy output (in British thermal units).

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Carbon dioxide (CO2) intensity can vary greatly depending on the mix of fuels the end-use sectors consume. Historically, the industrial sector has had the lowest CO2 intensity, as measured by CO2 emissions per British thermal unit (Btu). The transportation sector historically has had the highest CO2 intensity, which continues in the projection because carbon-intensive petroleum remains the dominant fuel used in vehicles throughout the projection period.

• The generation fuel mix in the electric power sector has changed since the mid-2000s, with lower generation from high-carbon intensive coal and higher generation from natural gas and carbon-free renewables, such as wind and solar. This change resulted in the overall CO2 intensity of the electric power sector declining by 25% from the mid-2000s to 2018 and continuing to decline through 2050.

• Accounting for the CO2 emissions from the electricity sector in the end-use sectors that consume the electricity results in larger declines in CO2 intensity across those sectors for all AEO2019 cases. In the Reference case, the CO2 intensities of the residential and commercial sectors decline less than 1% when only their direct CO2 intensities are counted. When the electric power sector energy is distributed to the end-use sectors, the residential and commercial sectors decline by 11% and 10%, respectively, while the industrial sector declines by 11%. Transportation carbon intensity declines by 5%.

—despite overall increases in energy consumption

26

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

5

10

15

20

25

30

35

40

45

1990 2000 2010 2020 2030 2040 2050

electric powerindustrial

transportation

residential

commercial

Energy consumption by sector (Reference case)quadrillion British thermal units

2018history projections

0

5

10

15

20

25

30

35

40

45

1990 2000 2010 2020 2030 2040 2050

Energy consumption by fuel (Reference case)quadrillion British thermal units

2018history projections petroleum

and other liquidsnatural gas

other renewable energycoalnuclearhydroliquidbiofuels

27

Policy, technology, and economics affect the mix of U.S. fuel consumption—

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In all cases, non-hydroelectric renewables consumption grows the most (on a percentage basis). Implementing policies at the state level (renewable portfolio standards) and at the federal level (production and investment tax credits) has encouraged the use of renewables. Growing renewable use has driven down the costs of renewables technologies (wind and solar photovoltaic), further supporting their expanding adoption by the electric power and buildings sectors.

• Natural gas consumption rises as well, driven by projected low natural gas prices. In the Reference case, the industrial sector becomes the largest consumer of natural gas starting in the early 2020s. This sector will expand the use of natural gas as feedstock in the chemical industries and as lease and plant fuel, for industrial heat and power, and for liquefied natural gas production. Natural gas consumption for electric power also increases significantly in the power sector in response to low natural gas prices and to installing lower cost natural gas-fired combined-cycle generating units.

• The transportation sector is the largest consumer of petroleum and other liquids, particularly motor gasoline and distillate fuel oil. Current fuel economy standards stop requiring additional efficiency increases in 2025 for light-duty vehicles and in 2027 for heavy-duty vehicles, but travel continues to rise, and as a result, consumption of petroleum and other liquids increases later in the projection period.

—which affects energy consumption patterns throughout the projection period

28

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

Critical drivers and model updatesMany factors influence the model results in AEO2019, including varying assumptions about domestic energy resources and production technology; global oil prices; macroeconomic growth; model improvements; and new and existing laws and regulations since AEO2018.

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Future oil prices are highly uncertain and are subject to international market conditions influenced by factors outside of the National Energy Modeling System. The High and Low Oil Price cases represent international conditions that could collectively drive prices to extreme, sustained deviations from the Reference case price path. Compared with the Reference case, in the High Oil Price case, non-U.S. demand is higher and non-U.S. supply is lower; in the Low Oil Price case, the opposite is true.

• Projections of tight oil and shale gas production are uncertain because large portions of the known formations have relatively little or no production history, and extraction technologies and practices continue to evolve rapidly. In the High Oil and Gas Resource and Technology case, lower production costs and higher resource availability than in the Reference case allow for higher production at lower prices. In the Low Oil and Gas Resource and Technology case, assumptions of lower resources and higher production costs are applied. These assumptions are not extended outside the United States.

• Economic growth particularly affects energy consumption, and those effects are addressed in the High and Low Economic Growth cases, which modify population growth and productivity assumptions throughout the projection period to yield higher or lower compound annual growth rates for U.S. gross domestic product than in the Reference case.

Critical drivers and uncertainty

32

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 33

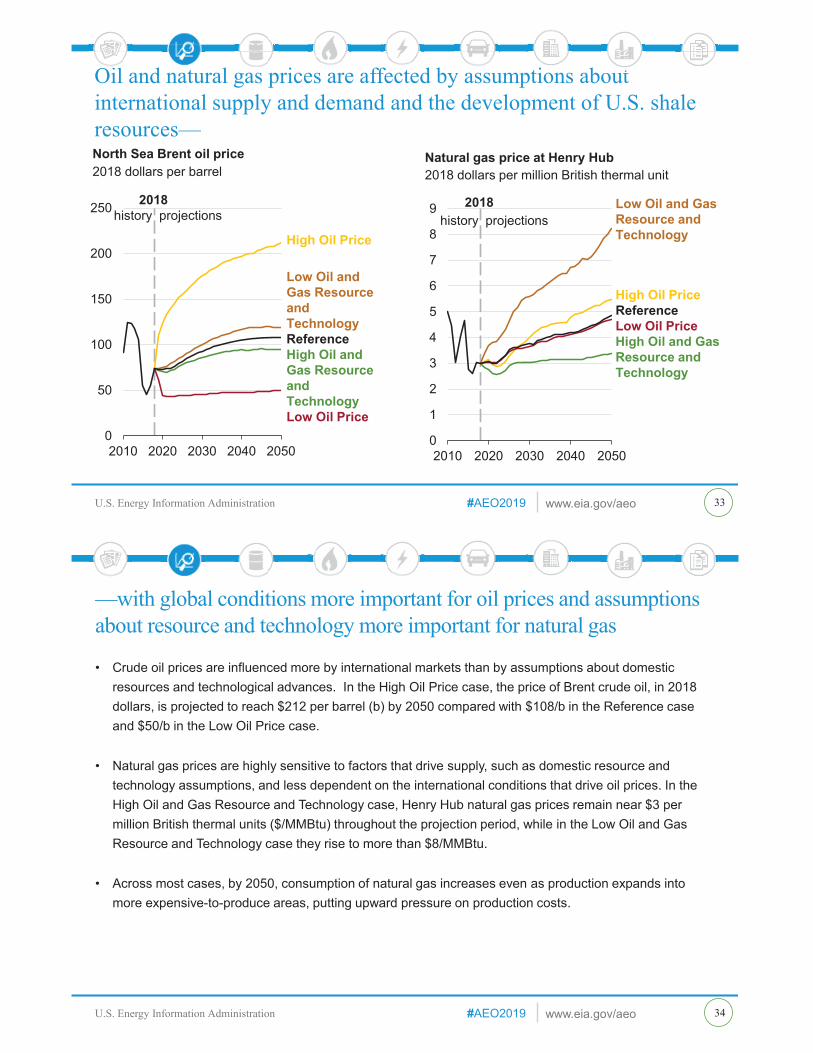

Oil and natural gas prices are affected by assumptions about international supply and demand and the development of U.S. shale resources—

titi o tt

0

50

100

150

200

250

2010 2020 2030 2040 2050

North Sea Brent oil price2018 dollars per barrel

High Oil Price

Low Oil and Gas Resource and TechnologyReferenceHigh Oil and Gas Resource and TechnologyLow Oil Price

2018history projections

0

1

2

3

4

5

6

7

8

9

2010 2020 2030 2040 2050

Natural gas price at Henry Hub2018 dollars per million British thermal unit

2018history projections

Low Oil and Gas Resource and Technology

High Oil PriceReferenceLow Oil PriceHigh Oil and Gas Resource and Technology

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Crude oil prices are influenced more by international markets than by assumptions about domestic resources and technological advances. In the High Oil Price case, the price of Brent crude oil, in 2018 dollars, is projected to reach $212 per barrel (b) by 2050 compared with $108/b in the Reference case and $50/b in the Low Oil Price case.

• Natural gas prices are highly sensitive to factors that drive supply, such as domestic resource and technology assumptions, and less dependent on the international conditions that drive oil prices. In the High Oil and Gas Resource and Technology case, Henry Hub natural gas prices remain near $3 per million British thermal units ($/MMBtu) throughout the projection period, while in the Low Oil and Gas Resource and Technology case they rise to more than $8/MMBtu.

• Across most cases, by 2050, consumption of natural gas increases even as production expands into more expensive-to-produce areas, putting upward pressure on production costs.

—with global conditions more important for oil prices and assumptions about resource and technology more important for natural gas

34

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

5

10

15

20

25

30

35

40

2010 2030 2050

Gross domestic producttrillion 2009 dollars

2018history projections

High Economic GrowthReference Low Economic Growth

0

100

200

300

400

500

2010 2030 2050

Populationmillions

2018

history projections

35

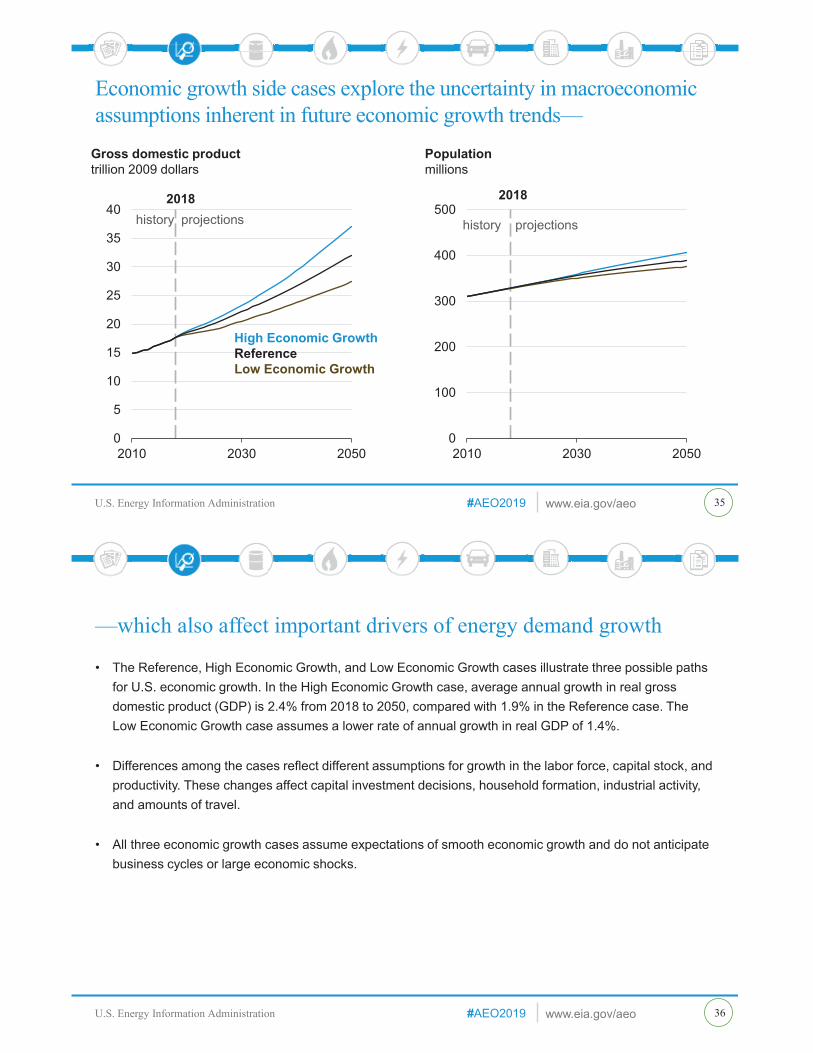

Economic growth side cases explore the uncertainty in macroeconomic assumptions inherent in future economic growth trends—

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The Reference, High Economic Growth, and Low Economic Growth cases illustrate three possible paths for U.S. economic growth. In the High Economic Growth case, average annual growth in real gross domestic product (GDP) is 2.4% from 2018 to 2050, compared with 1.9% in the Reference case. The Low Economic Growth case assumes a lower rate of annual growth in real GDP of 1.4%.

• Differences among the cases reflect different assumptions for growth in the labor force, capital stock, and productivity. These changes affect capital investment decisions, household formation, industrial activity, and amounts of travel.

• All three economic growth cases assume expectations of smooth economic growth and do not anticipate business cycles or large economic shocks.

—which also affect important drivers of energy demand growth

36

37

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• EIA released data from its 2015 Residential Energy Consumption Survey (RECS) in May 2018, and introduced estimates of energy consumption for an expanded list of energy end uses. Incorporating these updated estimates resulted in revised total housing units and end-use energy consumption shares.

• EIA updated residential and commercial technology efficiency and cost characteristics for space heating, space cooling, water heating, cooking equipment, and appliances based on reports Navigant Consulting, Inc. prepared for EIA.

• EIA updated vehicle stock data and related inputs such as vehicle scrappage and annual travel by vintage, which affected stock fuel economy and vehicle-miles traveled. Along with improved modeling of fleet-operated automated vehicles, these changes resulted in higher estimates of the number of light-duty vehicles on the road and higher vehicle-miles traveled.

Significant data and model updates

38

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• EIA updated its modeling of the Annex VI of the International Convention for the Prevention of Pollution from Ships (MARPOL Convention), which limits sulfur emissions to 0.5% by weight, compared with the current 3.5% by weight, for ocean-going ships by 2020. The new modeling reflects expectations that U.S. refiners will supply a larger share of the low-sulfur fuel market. EIA also lowered the initial penetration of marine scrubbers and added a 60/40 blend of high sulfur fuel oil and distillate as a 2020 global sulfur-compliant fuel.

• In December 2017, Congress enacted the Tax Cuts and Jobs Act of 2017 (P.L. 115-97). Although this act is mainly associated with reducing the maximum marginal tax rate for corporations from 38% to 21% and temporarily allowing immediate expensing of major capital expenditures, it also established an oil and natural gas program for the leasing, development, production, and transportation of oil and natural gas in and from the coastal plain (1002 Area) of the Arctic National Wildlife Refuge (ANWR). Modeling the opening of ANWR to drilling increases Alaskan crude oil production after 2030.

New laws and regulations reflected in the Reference case as of October 2018

39

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The Internal Revenue Service issued safe harbor guidance for solar facilities to qualify for the Investment Tax Credit (ITC) as it phases down from 30% to 10% after 2020. Under the new guidance, utility-scale solar photovoltaic (PV) projects starting construction before January 1, 2020, have up to four years to bring the plant online, while still qualifying for the full 30% ITC. Projects entering service after January 1, 2024, receive a 10% ITC, including those starting construction after 2020. Modeling the safe harbor guidance results in later additions of solar PV systems as developers postpone in-service dates and in higher total solar PV builds.

• A number of new state and regional policies were enacted in the past year. These policies included California’s requirement for 100% clean energy generation by 2045 and New Jersey’s and Massachusetts’s increased renewable portfolio standard (RPS) requirements that renewables contribute 50% and 35% of generation, respectively, by 2030. Even with the stricter requirements, EIA projects compliance to be easily met.

• EIA did not include the effects of the existing 45Q federal tax credits for carbon capture and sequestration in AEO2019 because the credits, although recently doubled, still do not appear large enough to encourage substantial market penetration of carbon capture in the scenarios modeled.

New laws and regulations reflected in the Reference case as of October 2018 (continued)

40

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 41

New limit on global sulfur emissions affects refinery operations and maritime transport—

0

200

400

600

800

1,000

1,200

2010 2020 2030 2040 2050

International marine shipping fuel consumption (Reference case)trillion British thermal units

low-sulfur fuel oil

distillate fuel oil

liquefied natural gas

high-sulfur fuel oil

2018history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Annex VI of the International Convention for the Prevention of Pollution from Ships (MARPOL Convention) limits emissions for ocean-going ships by 2020 (IMO 2020). From January 1, 2020, the limit for sulfur in fuel used on board ships operating outside designated emission control areas will be reduced to 0.5% m/m (mass by mass), a reduction of more than 85% from its present level of 3.5% m/m. Ships can meet the new global sulfur limit by installing pollutant-control equipment (scrubbers); by using a low-sulfur, petroleum-based marine fuel; or by switching to an alternative non-petroleum fuel such as liquefied natural gas (LNG).

• Shippers that install scrubbers have remained limited, and refineries continue to announce plans to upgrade high-sulfur fuel oils into higher quality products and increase availability of low-sulfur compliant fuel oils. Some shippers have also announced plans to address the costs associated with higher quality fuels by shifting those costs to their customers.

• Although some price swings and fuel availability issues are expected when the regulations take effect in 2020, by 2030 more than 83% of international marine fuel purchases in U.S. ports are for low-sulfur compliant fuel in the Reference case, and the share of LNG increases from negligible levels in 2018 to 7% in 2030.

—as refiners and marine transporters adapt to meet the new requirements

42

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 43

Refinery utilization in the Reference case peaks in 2020—

0

10

20

30

40

50

60

70

80

90

100

2010 2020 2030 2040 2050

U.S. refinery utilization (Reference case)percent

portion of throughput

exported

portion of throughputconsumed

domestically

utilization

2018history projections

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2010 2020 2030 2040 2050

U.S. diesel and residual fuel exports and unfinished oils imports (Reference case)million barrels per day

2018history projections

diesel and residualfuel exports

unfinished oils imports

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• U.S. refinery utilization peaks in most cases in 2020 as complex refineries in the United States that can process high-sulfur fuel oil in downstream units take advantage of the increased price spread between light and heavy crude oil. In the Reference case, refinery utilization peaks at 96% in 2020, gradually decreases between 2020 and 2026, and remains between 90% and 92% for the rest of the projection.

• The share of U.S. refinery throughput that is exported increases as more petroleum products are exported from 2020 to 2036 and as domestic consumption of refined products decreases. The trend reverses after 2036 when domestic consumption (especially of gasoline) increases.

• Imports of unfinished oils peak in 2020 as U.S. refineries take advantage of the increased discount of the heavy, high-sulfur residual fuel oil available on the global market.

—as a result of sulfur emissions regulations that take effect in 2020

44

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 45

Development of the Arctic National Wildlife Refuge increases Alaskan crude oil production in AEO2019—

0.0

0.5

1.0

1.5

2.0

2.5

2000 2010 2020 2030 2040 2050

Alaskan crude oil productionmillion barrels per day

2018history projections

AEO2018Reference

High Oil and Gas Resource and Technology

High Oil Price

ReferenceLow Oil PriceLow Oil and Gas Resource and Technology

2010 2020 2030 2040 2050

ANWR crude oil productionmillion barrels per day

2018history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• The passage of Public Law 115-97 required the Secretary of the Interior to establish a program to lease and develop oil and natural gas from the coastal plain (1002 Area) of the Arctic National Wildlife Refuge (ANWR). Previously, ANWR was effectively under a drilling moratorium.

• Opening ANWR is not expected to have a significant impact on crude oil production before the 2030s because of the time needed to acquire leases, explore, and develop the required production infrastructure. Alaskan crude oil production in AEO2019 is 90% higher (3.2 billion barrels) from 2031 to 2050 than previously forecasted for that period in last year’s AEO Reference case.

• The ANWR projections are highly uncertain because of several factors that affect the timing and cost of development, little direct knowledge of the resource size and quality that exists in ANWR, and inherent uncertainty about market dynamics. Cumulative ANWR crude oil production from 2031 to 2050 is 6.8 billion barrels, 0.7 billion barrels, and zero in the High Oil and Gas Resource and Technology, Low Oil and Gas Resource and Technology, and Low Oil Price cases, respectively.

• A more in-depth analysis exploring the effect of this law on U.S. crude oil production projections was published in May 2018 as part of the AEO2018 Issues in Focus series.

—but only after 2030 because of the time needed to acquire leases and develop infrastructure

46

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0%

5%

10%

15%

20%

25%

30%

35%

2015 2020 2025 2030

Tax credit assumptions for utility-scale solar percentage of installed cost

Jan-15 Jan-20 Jan-25 // Jan-50

AEO2019

AEO2018

Legislative milestone

(begin construction)

EIA assumedtwo-year lead time

four-year safe harbor

0

10

20

30

40

50

60

70

80

2020 2021 2022 2023

AEO2018 Reference caseAEO2019 Reference case

Power sector solar photovoltaic installed capacitygigawatts

47

Recently issued IRS guidance effectively eliminates the Investment Tax Credit phasedown in AEO2019—

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In June 2018, the Internal Revenue Service (IRS) issued safe harbor guidance for solar facilities to qualify for the Investment Tax Credit (ITC).

• Under current law, utility-scale solar plants that are under construction before January 1, 2020, receive the full 30% ITC, while those under construction before January 1, 2021, receive a 26% ITC and those under construction before January 1, 2022, receive a 22% ITC. For AEO2018, before the IRS issued its guidance, EIA assumed a two-year construction lead time for new solar photovoltaic (PV) plants, so that PV plants entering service in 2023 received a 22% ITC.

• With the new IRS guidance, EIA assumes that utility-scale solar plants starting construction before January 1, 2020, and entering service before January 1, 2024, receive the full 30% ITC. This assumption results in 21 gigawatts of additional solar PV capacity coming online before January 1, 2024, in AEO2019 as compared with AEO2018.

• The figure shown above applies to utility-owned solar PV installations. Residential systems individuals own have a different treatment under the ITC, and systems that commercial or other non-utility entities own have different financial considerations, and so are not shown above.

—increasing projected photovoltaic capacity in the near term

48

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

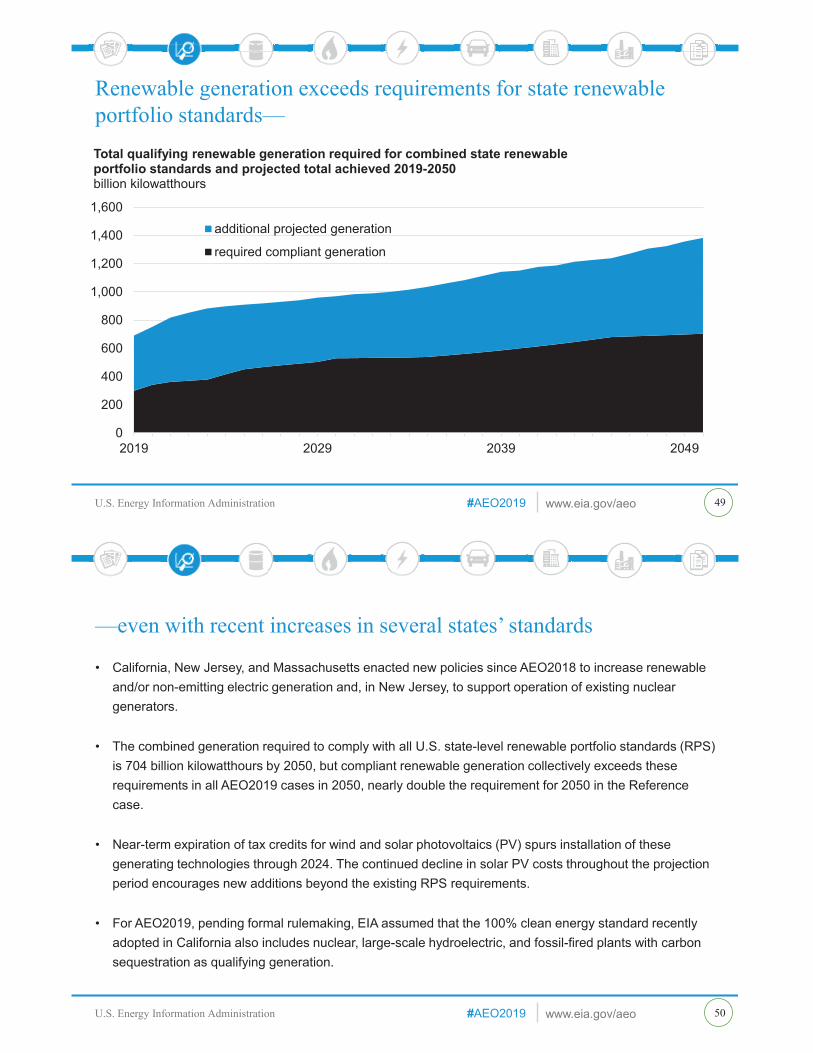

Renewable generation exceeds requirements for state renewable portfolio standards—

49

0

200

400

600

800

1,000

1,200

1,400

1,600

2019 2029 2039 2049

Total qualifying renewable generation required for combined state renewable portfolio standards and projected total achieved 2019-2050 billion kilowatthours

additional projected generation

required compliant generation

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• California, New Jersey, and Massachusetts enacted new policies since AEO2018 to increase renewable and/or non-emitting electric generation and, in New Jersey, to support operation of existing nuclear generators.

• The combined generation required to comply with all U.S. state-level renewable portfolio standards (RPS) is 704 billion kilowatthours by 2050, but compliant renewable generation collectively exceeds these requirements in all AEO2019 cases in 2050, nearly double the requirement for 2050 in the Reference case.

• Near-term expiration of tax credits for wind and solar photovoltaics (PV) spurs installation of these generating technologies through 2024. The continued decline in solar PV costs throughout the projection period encourages new additions beyond the existing RPS requirements.

• For AEO2019, pending formal rulemaking, EIA assumed that the 100% clean energy standard recently adopted in California also includes nuclear, large-scale hydroelectric, and fossil-fired plants with carbon sequestration as qualifying generation.

—even with recent increases in several states’ standards

50

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

Petroleum and other liquidsU.S. crude oil and natural gas plant liquids production continues to grow as a result of the further development of tight oil resources during the projection period. During the same period, domestic consumption falls, making the United States a net exporter of liquid fuels in the Reference case.

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

5

10

15

20

25

30

2000 2010 2020 2030 2040 2050

2018history projections

U.S. crude oil and natural gas plant liquids productionmillion barrels per day

High Oil and Gas Resource and TechnologyHigh Oil PriceHigh Economic GrowthReferenceLow EconomicGrowthLow Oil PriceLow Oil and Gas Resource and TechnologyReference, crude oil only

1970 crude oil production level

0

5

10

15

20

25

30

2000 2010 2020 2030 2040 2050

Petroleum and other liquids consumptionmillion barrels per day

2018history projections

Low Oil PriceHigh Economic GrowthHigh Oil and Gas Resource and TechnologyReferenceLow Oil and Gas Resource and TechnologyLow EconomicGrowthHigh Oil Price

53

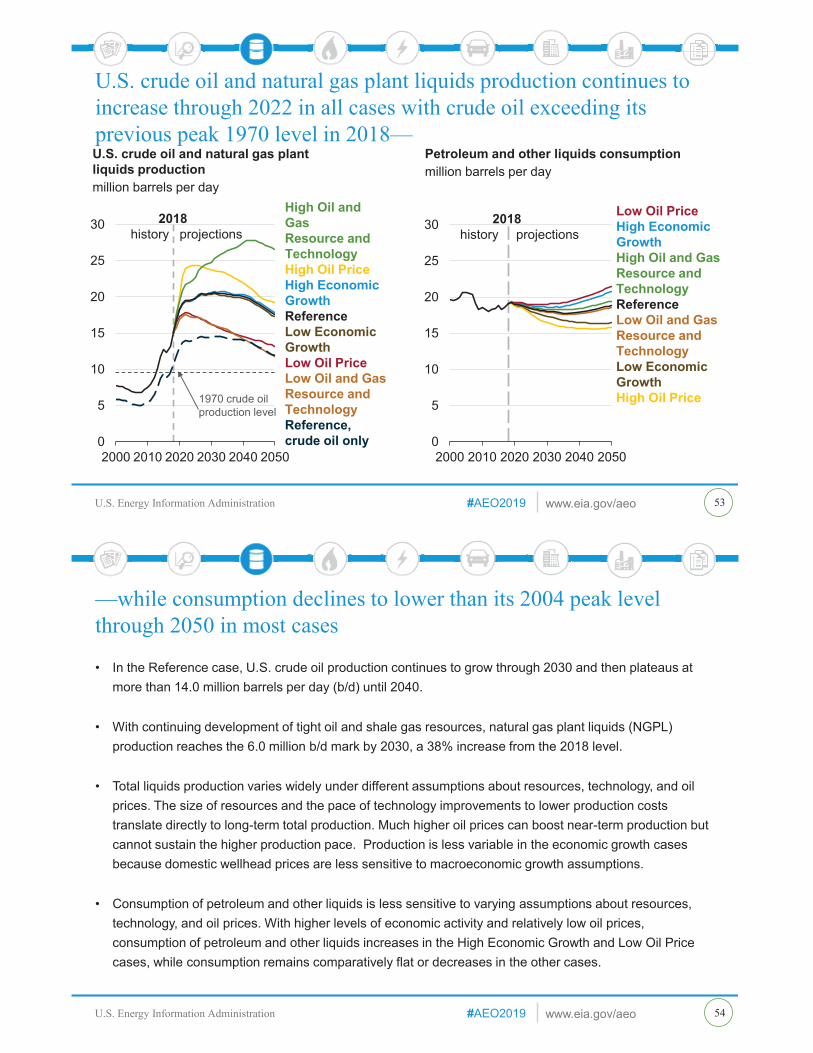

U.S. crude oil and natural gas plant liquids production continues to increase through 2022 in all cases with crude oil exceeding its previous peak 1970 level in 2018—

i

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, U.S. crude oil production continues to grow through 2030 and then plateaus at more than 14.0 million barrels per day (b/d) until 2040.

• With continuing development of tight oil and shale gas resources, natural gas plant liquids (NGPL) production reaches the 6.0 million b/d mark by 2030, a 38% increase from the 2018 level.

• Total liquids production varies widely under different assumptions about resources, technology, and oil prices. The size of resources and the pace of technology improvements to lower production costs translate directly to long-term total production. Much higher oil prices can boost near-term production but cannot sustain the higher production pace. Production is less variable in the economic growth cases because domestic wellhead prices are less sensitive to macroeconomic growth assumptions.

• Consumption of petroleum and other liquids is less sensitive to varying assumptions about resources, technology, and oil prices. With higher levels of economic activity and relatively low oil prices, consumption of petroleum and other liquids increases in the High Economic Growth and Low Oil Price cases, while consumption remains comparatively flat or decreases in the other cases.

—while consumption declines to lower than its 2004 peak level through 2050 in most cases

54

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 55

Tight oil development drives U.S. crude oil production from 2018 to 2050—

2010 2020 2030 2040 2050

Low Oil and Gas Resourceand Technology2018

history projections

0

5

10

15

20

25

2000 2010 2020 2030 2040 2050

Crude oil productionmillion barrels per day

tight oil

AlaskaGulf of Mexicoother

Reference2018history projections

2010 2020 2030 2040 2050

High Oil and Gas Resource and Technology2018

history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Lower 48 onshore tight oil development continues to be the main driver of total U.S. crude oil production, accounting for about 68% of cumulative domestic production in the Reference case during the projection period.

• U.S. crude oil production levels off at about 14 million barrels per day (b/d) through 2040 in the Reference case as tight oil development moves into less productive areas and well productivity declines.

• In the Reference case, oil and natural gas resource discoveries in deepwater in the Gulf of Mexico lead Lower 48 states offshore production to reach a record 2.4 million b/d in 2022. Many of these discoveries resulted from exploration when oil prices were higher than $100 per barrel before the oil price collapse in 2015 and are being developed as oil prices rise. Offshore production then declines through 2035 before flattening through 2050 as a result of new discoveries offsetting declines in legacy fields.

• Alaska crude oil production increases through 2030, driven primarily by the development of fields in the National Petroleum Reserve–Alaska (NPR-A), and after 2030, the development of fields in the 1002 Section of the Arctic National Wildlife Refuge (ANWR). Exploration and development of fields in ANWR is not economical in the Low Oil Price case.

—a result consistent across all side cases

56

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

1

2

3

4

5

6

2000 2010 2020 2030 2040 2050

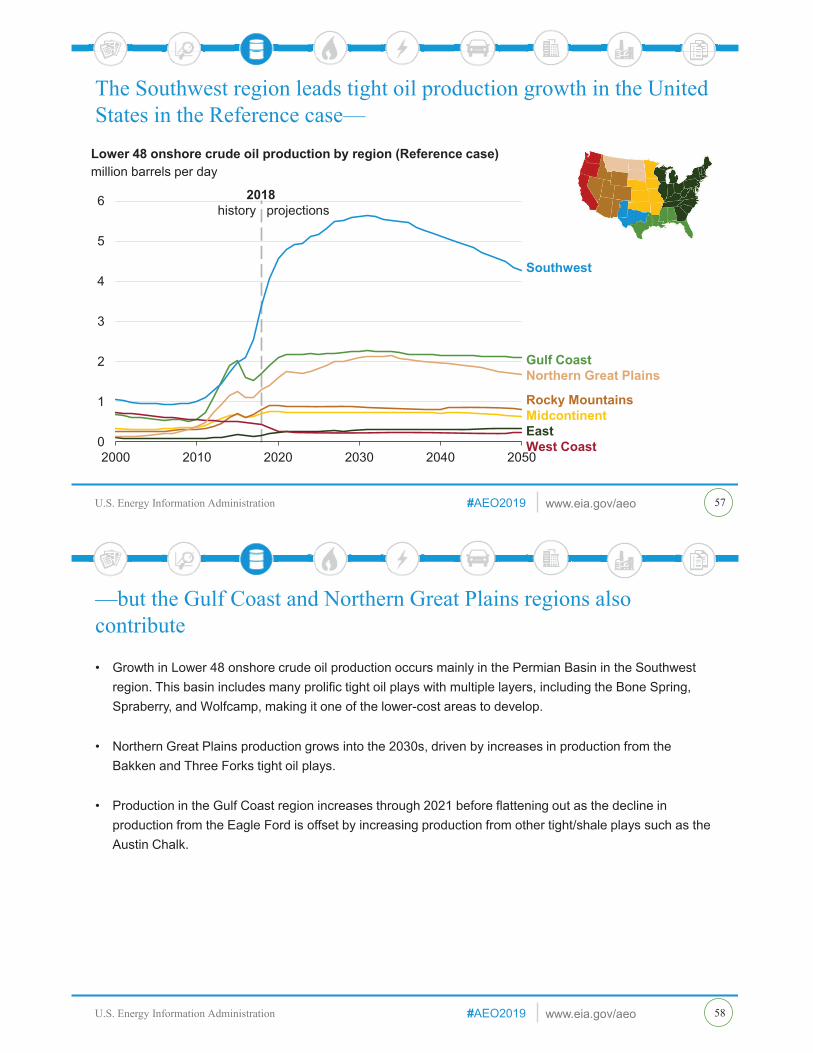

Lower 48 onshore crude oil production by region (Reference case)million barrels per day

2018history projections

Southwest

Gulf CoastNorthern Great Plains

Rocky Mountains MidcontinentEast West Coast

The Southwest region leads tight oil production growth in the United States in the Reference case—

57

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Growth in Lower 48 onshore crude oil production occurs mainly in the Permian Basin in the Southwest region. This basin includes many prolific tight oil plays with multiple layers, including the Bone Spring, Spraberry, and Wolfcamp, making it one of the lower-cost areas to develop.

• Northern Great Plains production grows into the 2030s, driven by increases in production from the Bakken and Three Forks tight oil plays.

• Production in the Gulf Coast region increases through 2021 before flattening out as the decline in production from the Eagle Ford is offset by increasing production from other tight/shale plays such as the Austin Chalk.

—but the Gulf Coast and Northern Great Plains regions also contribute

58

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 59

Natural gas plant liquids production increases in most AEO cases—

0

1

2

3

4

5

6

7

8

9

1980 1990 2000 2010 2020 2030 2040 2050

U.S. natural gas plant liquids productionmillion barrels per day

2018history projections High Oil and Gas

Resource and TechnologyHigh Oil PriceHigh Economic GrowthReferenceLow EconomicGrowthLow Oil PriceLow Oil and Gas Resource and Technology

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, natural gas plant liquids (NGPL) production grows by 32% between 2018 and 2050 as a result of demand increases in the global petrochemical industry.

• Most NGPL production growth in the Reference case occurs before 2025 as producers focus on natural gas liquids-rich plays, where NGPL-to-gas ratios are highest and increased demand spurs higher ethane recovery.

• NGPL production is sensitive to changes in resource and technology assumptions. In the High Oil and Gas Resource and Technology case, which has higher rates of technological improvement, higher recovery estimates, and additional tight oil and shale gas resources, NGPL production grows by 73% between 2018 and 2050. In contrast, in the Low Oil and Gas Resource and Technology, which has lower rates of technological improvement and lower recovery estimates, NGPL production declines by 10% between 2018 and 2050.

—because of higher levels of drilling in liquid-rich natural gas formations and increased demand

60

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 61

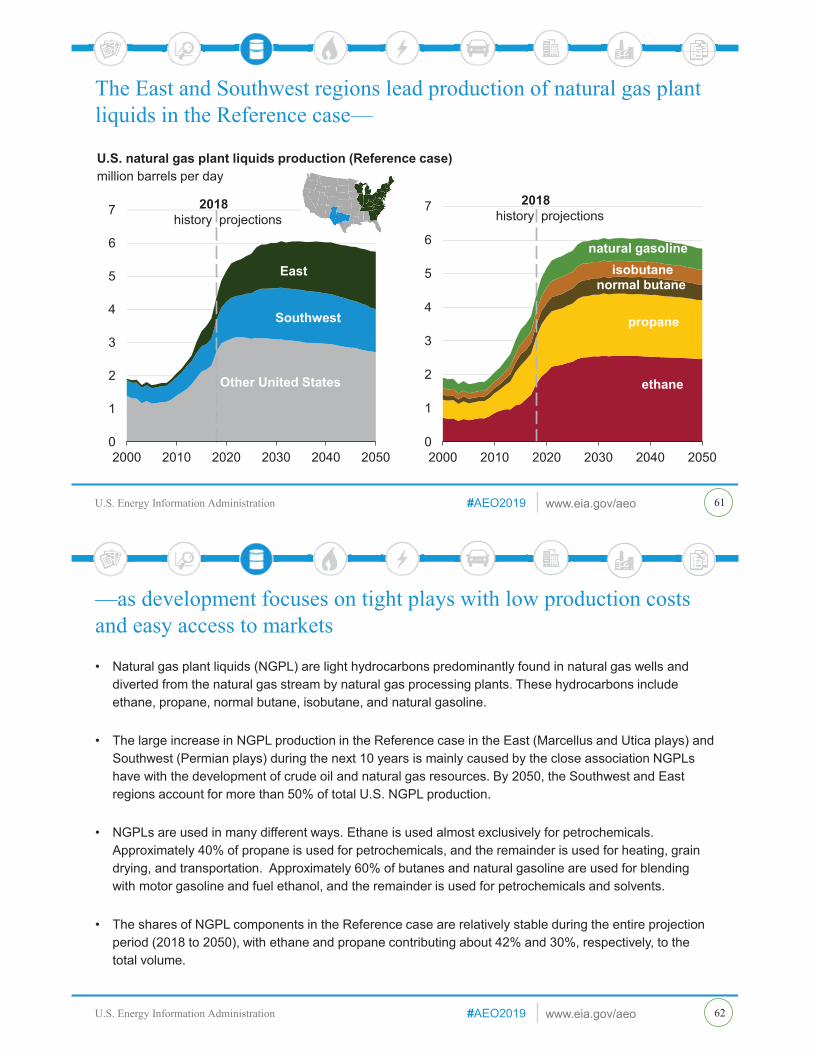

The East and Southwest regions lead production of natural gas plant liquids in the Reference case—

0

1

2

3

4

5

6

7

2000 2010 2020 2030 2040 2050

2018history projections

normal butaneisobutane

propane

ethane

natural gasoline

0

1

2

3

4

5

6

7

2000 2010 2020 2030 2040 2050

2018history projections

East

Southwest

Other United States

U.S. natural gas plant liquids production (Reference case)million barrels per day

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Natural gas plant liquids (NGPL) are light hydrocarbons predominantly found in natural gas wells and diverted from the natural gas stream by natural gas processing plants. These hydrocarbons include ethane, propane, normal butane, isobutane, and natural gasoline.

• The large increase in NGPL production in the Reference case in the East (Marcellus and Utica plays) and Southwest (Permian plays) during the next 10 years is mainly caused by the close association NGPLs have with the development of crude oil and natural gas resources. By 2050, the Southwest and East regions account for more than 50% of total U.S. NGPL production.

• NGPLs are used in many different ways. Ethane is used almost exclusively for petrochemicals. Approximately 40% of propane is used for petrochemicals, and the remainder is used for heating, grain drying, and transportation. Approximately 60% of butanes and natural gasoline are used for blending with motor gasoline and fuel ethanol, and the remainder is used for petrochemicals and solvents.

• The shares of NGPL components in the Reference case are relatively stable during the entire projection period (2018 to 2050), with ethane and propane contributing about 42% and 30%, respectively, to the total volume.

—as development focuses on tight plays with low production costs and easy access to markets

62

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 63

Most natural gas liquids in the Reference case serve as feedstocks to the bulk chemical industry—

0

1

2

3

4

5

6

2000 2010 2020 2030 2040 2050

U.S. industrial NGL consumption (Reference case)quadrillion British thermal units

2018history projections

chemical feedstocks

heat and power

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Consumption of ethane, propane, and butane used as bulk chemical feedstock grows an average of 1.5% per year between 2018 and 2050 in the Reference case, compared with 3.1% per year from 2010 to 2018.

• The consumption of natural gas liquids (NGL) as feedstock grows faster in the High Economic Growth case (1.9% per year) and the High Resource and Technology case (1.8% per year). In the High Economic Growth case, demand for all goods is higher than in the Reference case, including bulk chemicals for domestic use and export. In the High Resource and Technology case, NGL are more abundant and less expensive. As a result, shipments of bulk chemicals are greater.

• Most NGL feedstock is ethane, which is processed almost exclusively into ethylene, a building block for plastics, resins, and other industrial products. Propane, normal butane, and isobutane are also used to produce propylene and butadiene, respectively, but in much smaller quantities compared with ethane.

• Propane is used in the agriculture sector for grain drying and heating and in the construction industry for heating and for powering vehicles and equipment.

—although a small proportion is also used as fuel

64

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

-15

-10

-5

0

5

10

15

2000 2010 2020 2030 2040 2050

U.S. petroleum and other liquids net imports/exportsmillion barrels per day

2018history projections

net imports

net exports

Low Oil PriceLow Oil and GasResource and TechnologyReference

High Oil PriceHigh Oil and GasResource and Technology

In the Reference case, the United States becomes a net exporter of petroleum on a volume basis from 2020 to 2049—

65

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Net U.S. imports of crude oil and liquid fuels will fall between 2018 and 2034 in the Reference case as strong production growth and decreasing domestic demand result in the United States becoming a net exporter.

• In the Reference case, net exports from the United States peak at more than 3.68 million barrels per day (b/d) in 2034 before gradually reversing as domestic consumption rises. The United States returns to being a net importer in 2050 on a volume basis.

• Additional resources and higher levels of technological improvement in the High Oil and Gas Resource and Technology case results in higher crude oil production and higher exports, with exports reaching a high of 10.26 million b/d in 2041. Projected net exports reach a high of 8.39 million b/d in 2033 in the High Oil Price case as a result of higher prices that support higher domestic production. Conversely, low oil prices in the Low Oil Price case drive projected net imports up from 2.37 million b/d in 2018 to 7.17 million b/d in 2050.

—but side case results vary significantly using different assumptions

66

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 67

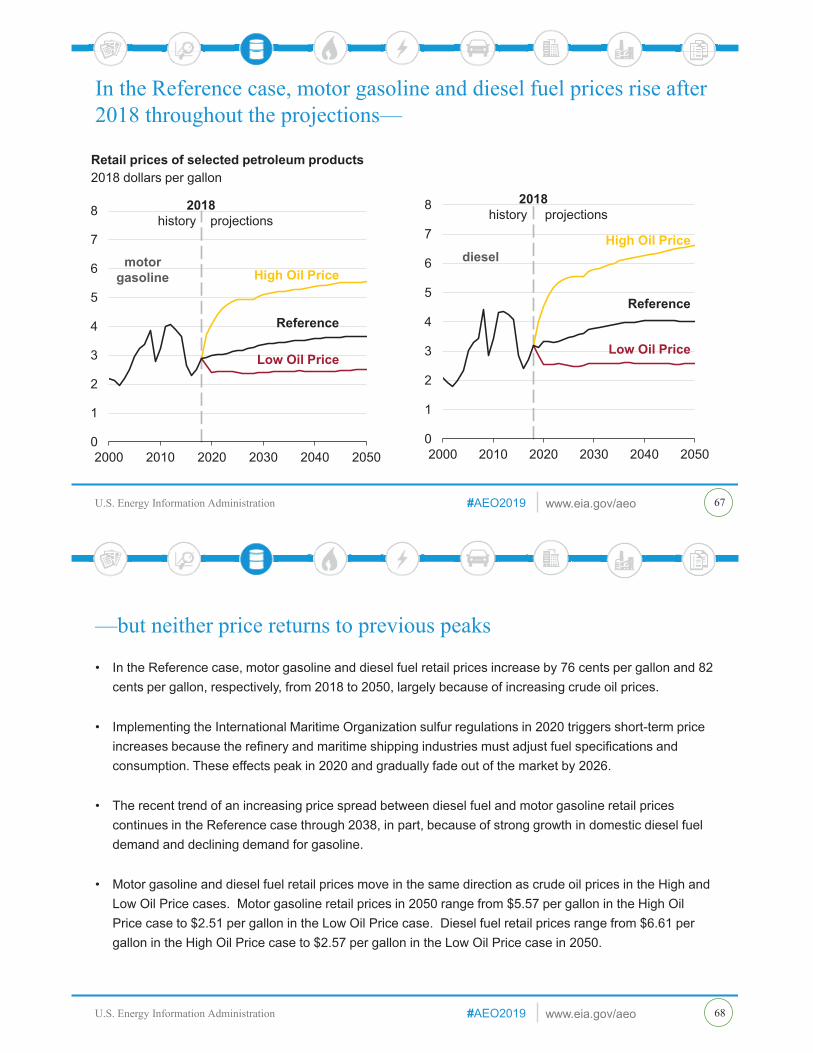

In the Reference case, motor gasoline and diesel fuel prices rise after 2018 throughout the projections—

0

1

2

3

4

5

6

7

8

2000 2010 2020 2030 2040 2050

2018history projections

motor gasoline High Oil Price

Reference

Low Oil Price

Retail prices of selected petroleum products2018 dollars per gallon

0

1

2

3

4

5

6

7

8

2000 2010 2020 2030 2040 2050

diesel

2018history projections

High Oil Price

Reference

Low Oil Price

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, motor gasoline and diesel fuel retail prices increase by 76 cents per gallon and 82 cents per gallon, respectively, from 2018 to 2050, largely because of increasing crude oil prices.

• Implementing the International Maritime Organization sulfur regulations in 2020 triggers short-term price increases because the refinery and maritime shipping industries must adjust fuel specifications and consumption. These effects peak in 2020 and gradually fade out of the market by 2026.

• The recent trend of an increasing price spread between diesel fuel and motor gasoline retail prices continues in the Reference case through 2038, in part, because of strong growth in domestic diesel fuel demand and declining demand for gasoline.

• Motor gasoline and diesel fuel retail prices move in the same direction as crude oil prices in the High and Low Oil Price cases. Motor gasoline retail prices in 2050 range from $5.57 per gallon in the High Oil Price case to $2.51 per gallon in the Low Oil Price case. Diesel fuel retail prices range from $6.61 per gallon in the High Oil Price case to $2.57 per gallon in the Low Oil Price case in 2050.

—but neither price returns to previous peaks

68

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

Natural gasNatural gas experiences the largest production increase of all fossil fuels during the projection period across all cases, driven by continued development of lower-cost shale gas and tight oil resources. The growth in natural gas production supports increasing domestic consumption, particularly in the industrial and electric power sectors, and higher levels of natural gas exports.

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 71

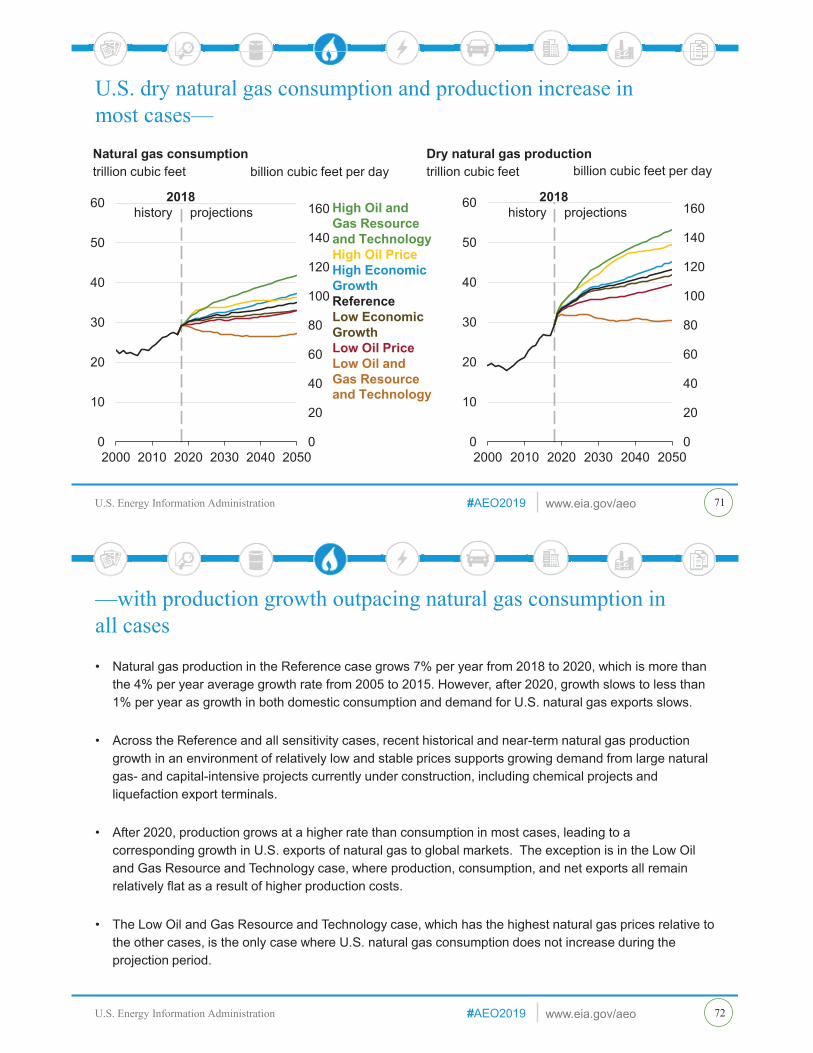

U.S. dry natural gas consumption and production increase in most cases—

0

20

40

60

80

100

120

140

160

0

10

20

30

40

50

60

2000 2010 2020 2030 2040 2050

Natural gas consumptiontrillion cubic feet

2018history projections High Oil and

Gas Resource and TechnologyHigh Oil PriceHigh Economic GrowthReferenceLow EconomicGrowthLow Oil PriceLow Oil and Gas Resource and Technology

billion cubic feet per day

0

20

40

60

80

100

120

140

160

0

10

20

30

40

50

60

2000 2010 2020 2030 2040 2050

Dry natural gas productiontrillion cubic feet billion cubic feet per day

2018history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Natural gas production in the Reference case grows 7% per year from 2018 to 2020, which is more than the 4% per year average growth rate from 2005 to 2015. However, after 2020, growth slows to less than 1% per year as growth in both domestic consumption and demand for U.S. natural gas exports slows.

• Across the Reference and all sensitivity cases, recent historical and near-term natural gas production growth in an environment of relatively low and stable prices supports growing demand from large natural gas- and capital-intensive projects currently under construction, including chemical projects and liquefaction export terminals.

• After 2020, production grows at a higher rate than consumption in most cases, leading to a corresponding growth in U.S. exports of natural gas to global markets. The exception is in the Low Oil and Gas Resource and Technology case, where production, consumption, and net exports all remain relatively flat as a result of higher production costs.

• The Low Oil and Gas Resource and Technology case, which has the highest natural gas prices relative to the other cases, is the only case where U.S. natural gas consumption does not increase during the projection period.

—with production growth outpacing natural gas consumption in all cases

72

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

10

20

30

40

50

60

2000 2010 2020 2030 2040 2050

Dry natural gas productiontrillion cubic feet

2018history projections

ReferenceHigh Oil and

Gas Resource and Technology

Low Oil and Gas Resource and Technology

0

2

4

6

8

10

12

2000 2010 2020 2030 2040 2050

Natural gas spot price at Henry Hub2

2018 dollars per million British thermal unit

2018history projections

Low Oil and Gas Resource and Technology

Reference

High Oil and Gas Resource and Technology

73

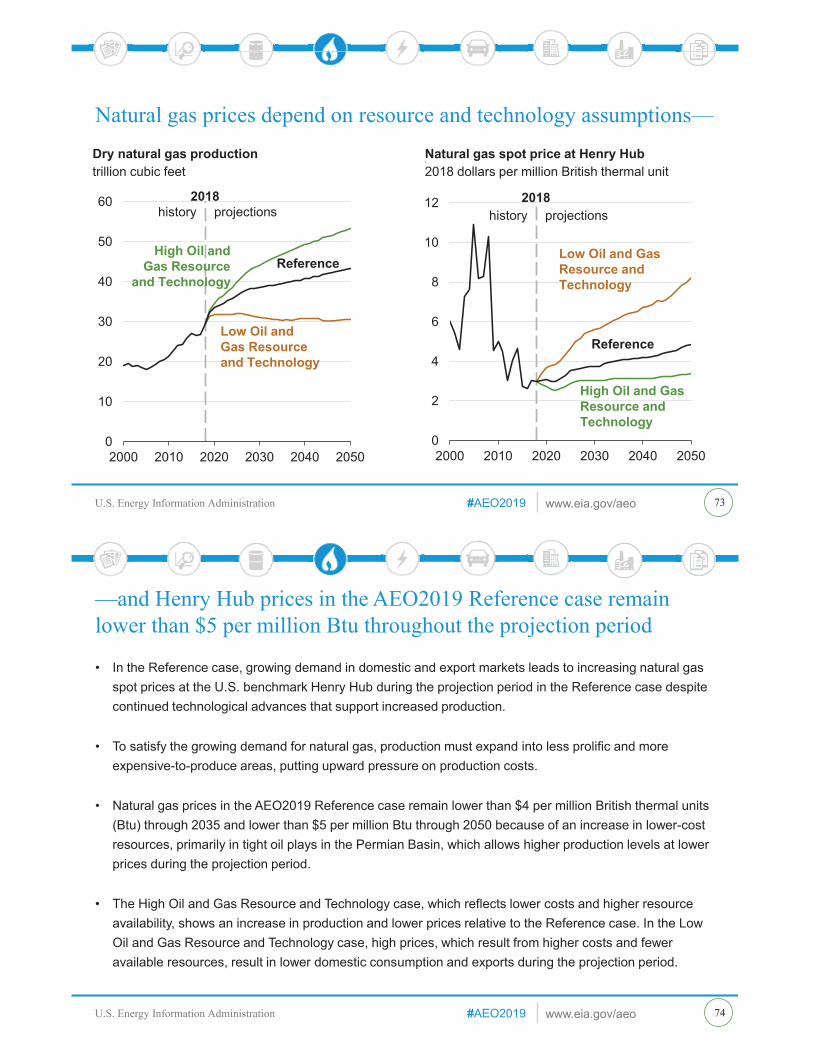

Natural gas prices depend on resource and technology assumptions—

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, growing demand in domestic and export markets leads to increasing natural gas spot prices at the U.S. benchmark Henry Hub during the projection period in the Reference case despite continued technological advances that support increased production.

• To satisfy the growing demand for natural gas, production must expand into less prolific and more expensive-to-produce areas, putting upward pressure on production costs.

• Natural gas prices in the AEO2019 Reference case remain lower than $4 per million British thermal units (Btu) through 2035 and lower than $5 per million Btu through 2050 because of an increase in lower-cost resources, primarily in tight oil plays in the Permian Basin, which allows higher production levels at lower prices during the projection period.

• The High Oil and Gas Resource and Technology case, which reflects lower costs and higher resource availability, shows an increase in production and lower prices relative to the Reference case. In the Low Oil and Gas Resource and Technology case, high prices, which result from higher costs and fewer available resources, result in lower domestic consumption and exports during the projection period.

—and Henry Hub prices in the AEO2019 Reference case remain lower than $5 per million Btu throughout the projection period

74

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 75

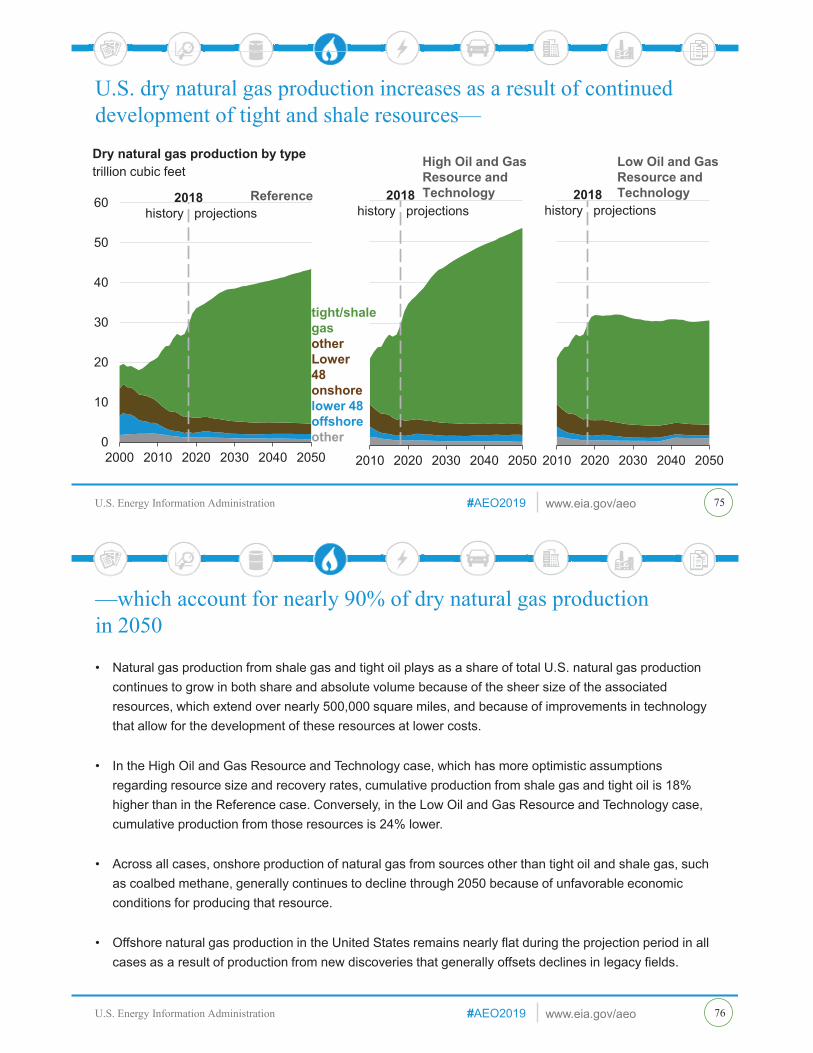

U.S. dry natural gas production increases as a result of continued development of tight and shale resources—

0

10

20

30

40

50

60

2000 2010 2020 2030 2040 2050

Dry natural gas production by typetrillion cubic feet

Reference

tight/shale gasotherLower 48 onshorelower 48 offshoreother

2018history projections

2010 2020 2030 2040 2050

High Oil and Gas Resource and Technology2018

history projections

2010 2020 2030 2040 2050

Low Oil and Gas Resource and Technology2018

history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Natural gas production from shale gas and tight oil plays as a share of total U.S. natural gas production continues to grow in both share and absolute volume because of the sheer size of the associated resources, which extend over nearly 500,000 square miles, and because of improvements in technology that allow for the development of these resources at lower costs.

• In the High Oil and Gas Resource and Technology case, which has more optimistic assumptions regarding resource size and recovery rates, cumulative production from shale gas and tight oil is 18% higher than in the Reference case. Conversely, in the Low Oil and Gas Resource and Technology case, cumulative production from those resources is 24% lower.

• Across all cases, onshore production of natural gas from sources other than tight oil and shale gas, such as coalbed methane, generally continues to decline through 2050 because of unfavorable economic conditions for producing that resource.

• Offshore natural gas production in the United States remains nearly flat during the projection period in all cases as a result of production from new discoveries that generally offsets declines in legacy fields.

—which account for nearly 90% of dry natural gas production in 2050

76

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 77

Eastern U.S. production of natural gas from shale resources leads growth in the Reference case—

0

5

10

15

20

25

30

35

40

45

2000 2010 2020 2030 2040 2050

Dry shale gas production by regiontrillion cubic feet

2018history projections

Southwest

East

Gulf Coast

rest of U.S.

Reference

2010 2020 2030 2040 2050

High Oil and Gas Resource and Technology2018

history projections

2010 2020 2030 2040 2050

Low Oil and Gas Resource and Technology2018

history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Total U.S. natural gas production across most cases is driven by continued development of the Marcellus and Utica shale plays in the East.

• Natural gas from the Eagle Ford (co-produced with oil) and the Haynesville plays in the Gulf Coast region also contributes to domestic dry natural gas production.

• Associated natural gas production from tight oil production in the Permian Basin in the Southwest region grows strongly in the early part of the projection period but remains relatively flat after 2030.

• Technological advancements and improvements in industry practices lower production costs in the Reference case and increase the volume of oil and natural gas recovery per well. These advancements have a significant cumulative effect in plays that extend over wide areas and that have large undeveloped resources (Marcellus, Utica, and Haynesville).

• Natural gas production from regions with shale and tight resources show higher levels of variability across the resource and technology cases, compared with the Reference case because assumptions in those cases target those specific resources.

—followed by growth in Gulf Coast onshore production

78

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 79

Natural gas production flows increase from the Mid-Atlantic and Ohio to the South Central through the Eastern Midwest—

0

1

2

3

4

5

6

7

8

2010 2020 2030 2040 2050

to Eastern Midwest

to Southeastto New England

Flows of natural gas from theMid-Atlantic and Ohio (Reference case)trillion cubic feet

2018history projections

st

0

1

2

3

4

5

6

7

8

2010 2020 2030 2040 2050

2018history projections

Flows of natural gas to the South Central (Reference case)trillion cubic feet

from Eastern Midwestfrom Arizona/New Mexicofrom Rocky Mountain Great Plains

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Reference case growth of natural gas production in the Mid-Atlantic and Ohio region, from the Marcellus and Utica formations, continues the trend of more natural gas flowing out of the region. This trend

• Although historically a net supplier of natural gas to U.S. markets, the South Central region’s demand growth outpaces production growth throughout the projection period. In addition to increased natural gas consumption in both the industrial and electric power sectors during the projection period in this region, U.S. natural gas exports to Mexico and U.S. liquefied natural gas exports from Gulf Coast facilities also rise. As a result, the Gulf Coast will become the fastest-growing demand market in the United States.

• To transport increased volumes of natural gas from the Mid-Atlantic and Ohio region to demand in the South Central region, additional natural gas pipeline capacity will be built from the Mid-Atlantic through the Eastern Midwest region.

—as growth in domestic consumption and exports is concentrated in the Gulf Coast

80

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

0

20

40

60

80

100

0

5

10

15

20

25

30

35

40

2000 2010 2020 2030 2040 2050

Natural gas consumption by sector (Reference case) trillion cubic feet billion cubic feet per day

2018history projections

residential

electric power

industrialliquefactionlease and plantother

commercialtransportation

Industrial and electric power demand drives natural gas consumption growth—

81

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Natural gas prices that are relatively low compared with historical prices lead to growing use of natural gas across most end-use sectors.

• The industrial sector, which includes fuel used for liquefaction at export facilities and in lease and plant operations, is the largest consumer of natural gas in the Reference case. Major natural gas consumers in this sector include the chemical industry (where natural gas is used as a feedstock to produce methanol and ammonia), industrial heat and power, and lease and plant fuel.

• Natural gas used for electric power generation generally increases during the projection period but at a slower rate than in the industrial sector. This growth is supported by the scheduled expiration of renewable tax credits in the mid-2020s, as well as the retirement of coal-fired and nuclear generation capacity during the projection period.

• Natural gas consumption in the residential and commercial sectors remains largely flat because of efficiency gains and population shifts that counterbalance demand growth. Although natural gas use rises in the transportation sector, particularly for freight trucks and rail and marine shipping, it remains a small share of both transportation fuel demand and total natural gas consumption.

—while consumption in the residential and commercial sectors remains relatively flat across the projection period in the Reference case

82

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 83

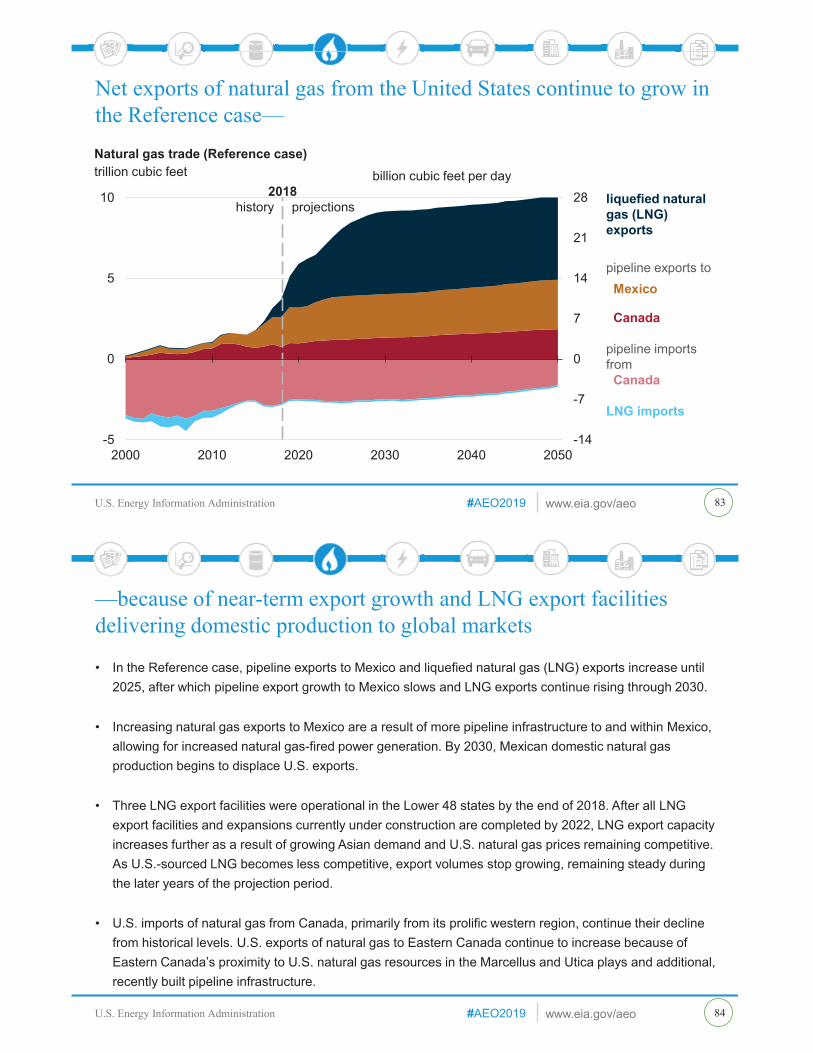

Net exports of natural gas from the United States continue to grow in the Reference case—

-14

-7

0

7

14

21

28

-5

0

5

10

2000 2010 2020 2030 2040 2050

Natural gas trade (Reference case)trillion cubic feet

2018history projections liquefied natural

gas (LNG) exports

pipeline exports to Mexico

Canada

pipeline imports fromCanada

LNG imports

billion cubic feet per day

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• In the Reference case, pipeline exports to Mexico and liquefied natural gas (LNG) exports increase until 2025, after which pipeline export growth to Mexico slows and LNG exports continue rising through 2030.

• Increasing natural gas exports to Mexico are a result of more pipeline infrastructure to and within Mexico, allowing for increased natural gas-fired power generation. By 2030, Mexican domestic natural gas production begins to displace U.S. exports.

• Three LNG export facilities were operational in the Lower 48 states by the end of 2018. After all LNG export facilities and expansions currently under construction are completed by 2022, LNG export capacity increases further as a result of growing Asian demand and U.S. natural gas prices remaining competitive. As U.S.-sourced LNG becomes less competitive, export volumes stop growing, remaining steady during the later years of the projection period.

• U.S. imports of natural gas from Canada, primarily from its prolific western region, continue their decline from historical levels. U.S. exports of natural gas to Eastern Canada continue to increase because of Eastern Canada’s proximity to U.S. natural gas resources in the Marcellus and Utica plays and additional, recently built pipeline infrastructure.

—because of near-term export growth and LNG export facilities delivering domestic production to global markets

84

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration 85

U.S. LNG exports are sensitive to both oil and natural gas prices—

0

5

10

15

20

25

30

35

0

2

4

6

8

10

12

2000 2010 2020 2030 2040 2050

Liquefied natural gas exportstrillion cubic feet

2018history projections

billion cubic feet per day

High OilPriceHigh Oil and Gas Resource and TechnologyReferenceLow Oil and Gas Resource and TechnologyLow OilPrice 0

1

2

3

4

5

6

7

8

9

2000 2010 2020 2030 2040 2050

Brent crude oil price to Henry Hub natural gas price ratioenergy-equivalent terms

2018history projections

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration

• Historically, most liquefied natural gas (LNG) was traded under long-term contracts linked to crude oil prices because the regional nature of natural gas markets prevented the development of a natural gas price index that could be used globally. In addition to providing a liquid pricing benchmark, crude oil to some degree can substitute for natural gas in industry and for power generation.

• When the crude oil-to-natural gas price ratio is highest, such as in the High Oil Price case, U.S. LNG exports are at their highest levels. U.S. LNG supplies have the advantage of being priced based on relatively low domestic spot prices instead of oil-linked contracts. Also, demand for LNG increases, in part, as a result of consumers moving away from petroleum products.

• In the High Oil and Gas Resource and Technology case, low U.S. natural gas prices make U.S. LNG exports competitive relative to other suppliers. Conversely, higher U.S. natural gas prices in the Low Oil and Gas Resource and Technology case result in lower U.S. LNG exports.

• As more natural gas is traded via short-term contracts or traded on the spot market, the link between LNG and oil prices weakens over time, making U.S. LNG exports less sensitive to the crude oil-to-natural gas price ratio and causing growth in U.S. LNG exports to slow in all cases.

—resulting in a wide range of U.S. LNG export levels across cases

86

U.S. Energy Information Administration www.eia.gov/aeo#AEO2019U.S. Energy Information Administration