annual report 2001 - sealaska corporation sealaska annual...sealaska corporation annual report 2001...

TRANSCRIPT

Annual Report 2001

Se

ala

ska

Co

rpo

rati

on

An

nu

al

Re

po

rt 2

001

IN THE PAST IT WAS OUR ORAL TRADITION, CARRIED

FROM VILLAGE TO VILLAGE BY CANOE THAT BROUGHT OUR

PEOPLE TOGETHER. TODAY THERE ARE MIRACLES OF

TECHNOLOGY THAT ENABLE US TO MAKE PHYSICAL DISTANCE

DISAPPEAR. HOWEVER, TRULY CONNECTING AS A PEOPLE

STILL DEPENDS ON REACHING OUT AND COMMUNICATING

WITH HONESTY AND CLARITY. IN GOOD TIMES AND BAD,

WE ARE COMMITTED TO USING ALL MEANS POSSIBLE TO

CONNECT EFFECTIVELY WITH OUR SHAREHOLDERS.

Visit us online at

www.sealaska.com to

get the latest news…

Look here for.

information on.

the Sealaska.

Heritage Institute.

Check on employment

possibilities; download

shareholder forms.

TODAY WE ARE CONFIDENT that Sealaska has rounded a difficult corner at a pivotal point in our

history. At no time in the 30 years since Sealaska was founded have we faced challenges as large

as the ones in 2001. For 2001, we are reporting a loss of $21 million on revenues of $146 million,

largely due to the last of writedowns of assets that began last year. However, we are pleased to

report that we have moved back into the path of profitability for the coming years.

WE HAVE WEATHERED THESE TIMES for several reasons. We have a strategic plan that will work

and we have the strength of our people and our culture. We are taking initiatives that ensure

that Sealaska remains financially strong as we rebuild this company for our future generations.

Last year we reported that significant amounts of year 2000 losses were due to writedowns of the

assets of discontinued operations. Major events over the past year in the U.S. and world economies

resulted in changes to our strategic deployment of these assets. As a result of our joint venture

with Nypro, Inc., our plastics business is no longer discontinued and we have reclassified our

financial statements for the operating results of TriQuest Corporation for FY 2000 and 1999. We

realize that reclassifying prior years complicates our financial statements, which can be confusing

and frustrating to our shareholders. However, this reclassification is required by Generally

Accepted Accounting Principles [GAAP] and the financial position of Sealaska that these financial

statements present is an accurate picture. The reclassification does not change the amount of our

net income or loss reported previously for 2000 or 1999.

2

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

WE ARE CONFIDENT THAT SEALASKA HAS ROUNDED A DIFFICULT

CORNER AND THAT WE HAVE A SOUND STRATEGIC PLAN. WE HAVE

THE DEPTH OF OUR NATIVE CULTURE AND A STRONG CONNECTION

WITH SHAREHOLDERS THAT FORM THE SOLID FOUNDATION ON WHICH

WE ARE BUILDING A FUTURE FOR ALL GENERATIONS TO COME.

SHAREHOLDER SUPPORT AND FEEDBACK is important to us and we take that as a great responsibility.

At the close of 2001, the board of directors conducted an extensive telephone survey as one step to

strengthen our connection with shareholders. We measured some baseline opinions that we have

tracked since our first survey in 1982, and we probed some current issues. Shareholders strongly

support including our shareholder descendants in Sealaska, and want the board to continue to hold

community meetings with shareholders. We also found that shareholder support for Sealaska continues

to be strong, despite the extreme business challenges and losses in 2000 and 2001. Our link to our

shareholders through Native culture is the strongest bond that we have as a community, We have the

collective strength of our people’s heritage and Sealaska will continue forward as a Native institution.

IN THE COMING YEAR we expect to see our Nypro joint venture plastics business grow using the

unique competitive advantages Sealaska and our subsidiaries have as minority-owned, diversity

suppliers. We are moving into contracting with the federal government using some of these same

advantages that ANCSA corporations have under federal law. We expect a positive resolution to

the legal disputes surrounding our investment in wireless telephone licenses that will return our

original investment plus accrued interest at a very high rate. A significant amount of this investment

will be returned to the shareholders’ permanent fund.

IN EARLY 2002 we sent all shareholders a document presenting our strategic plan for the coming

years. We have confidence that this plan will grow and strengthen Sealaska and prepare us for

expansion and greater profitability in the future. We know strong shareholder support for Sealaska is

crucial to our success, and we look forward to working with you to reach our goals together.

Sincerely,

Albert M. KookeshChairman of the Board

Chris E. McNeil, Jr.President & Chief Executive Officer

RECLASSIFICATION OF 2000 AND 1999 FINANCIALS

A significant portion of Sealaska’s 2000 loss was due

to writedowns of assets of discontinued operations.

However, major events over the past year in the U.S.

and world economies resulted in the redeployment

of some of these assets. Accordingly, we have

reclassified our 2000 and 1999 financial statements

to reflect the fact that our plastics business is no

longer discontinued.

The reclassification is required by Generally Accepted

Accounting Principles [GAAP] and accurately reflects

our most recent audited financial position.

4

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

OUR HERITAGE as Alaska Native

people is the strongest bond

we have. Our shareholders have

a very broad view of Sealaska

Corporation that includes a

strong belief that Sealaska is

vitally important to the survival

of Native people. We are

fortunate that our shareholders

clearly and unequivocally

include Sealaska as a

full-fledged family member.

Families are held together by

shared values, shared memories

and shared challenges.

Acceptance into the family and

in the Native community

includes a commitment to work

together for the benefit of all.

Sealaska will never back away

from its support of programs

that benefit shareholders and

issues that are important to

the Native community.

The results of our in-depth

shareholder survey reminded us

that Alaska Native identity is vital

to our people. This identity is why

Sealaska remains committed,

through the ups and downs of

corporate business, to provide

benefits and resources to keep

our culture strong.

Sealaska continues to

support the Sealaska Heritage

Institute (SHI), a leading cultural

force in Southeast Alaska. SHI

supports elders, youth and

adults through cultural and

language studies, culture

camps and in many other ways.

For over two decades, Sealaska

Corporation, through the

Sealaska Heritage Institute,

has provided over $5.5 million

in scholarships to look after the

dreams of our young people

through higher education. There

is no greater strategic invest-

ment that Sealaska can make

than in shareholder education.

Since 1991, our Elders

Settlement Trust has also

paid nearly $6 million to help

our Native elders when they

reach age 65.

Shareholders also look

to Sealaska to advocate for

broader issues that are vitally

important to the Alaska Native

community, including the

protection of Native subsistence

hunting and fishing. Support

of the Alaska Federation of

Natives and other organizations

complements our own political

initiatives and working together

strengthens our political

influence within the state of

Alaska and at the national level.

Shareholders also tell us

that Sealaska Corporation

means more to them than just

money and dividends. At the

same time, dividends are clearly

important to our shareholders.

We had 16 straight years of

profitable operations before

2000, and over 28 years of

continuous dividends and

distributions to shareholders.

Much of our attention this past

year has been driven by our

goal to return Sealaska to

profitability and to enable us to

pay meaningful dividends and

distributions to our shareholders.

SEALASKA CORPORATION AND OUR SHAREHOLDERS POSSESS A

RICH HERITAGE, FOUNDED ON NATIVE VALUES THAT ARTICULATE

OUR CARE FOR EACH OTHER AND THAT CALL ON EACH OF US TO

WORK TOGETHER TO BUILD STRONG FAMILIES AND COMMUNITIES.

6

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

WITH OVER 290,000 ACRES

of land and 590,000 acres

of mineral estate, Sealaska

is the largest private landowner

in Southeast Alaska. Our

connection to this resource

base will remain the foundation

of our business in perpetuity,

providing revenues and cash

flow for operations and benefits

to shareholders.

Sealaska Timber Corporation

(STC) has operated successfully

for over two decades, providing

consistent profits and cash flow

for overall Sealaska operations.

Our new strategic plan

includes re-engineering STC

to take better advantage of

global timber and wood-fiber

markets. The economics of the

global timber market are now

fluctuating beyond the ordinary

up and down market cycles

that have been the pattern

of the industry for decades.

We are re-examining STC from

top to bottom, and seeking ways

we can take better advantage

of new market opportunities

and technologies.

We are analyzing exactly how

much we need to re-engineer

STC. Can STC continue to be

successful by becoming more

efficient in harvesting and

marketing timber, or are there

other strategies we should

pursue to maximize the return

we get from our forest resources?

OUR VAST HOLDINGS OF NATURAL RESOURCES HAVE BEEN THE

BASIS OF ALL OUR BUSINESS DEVELOPMENTS FROM THE START.

TODAY, NEW STRATEGIES AND NEW OPPORTUNITIES CONTINUE TO

BE BUILT ON OUR FOUNDATION OF NATURAL RESOURCES AND LAND.

Beyond the development of

our timber resources, we are

constantly looking at innovative

ways to generate revenue

from our natural resource base,

increase the inherent value

of our resources and create

shareholder opportunities in the

process. Our natural resource

development creates revenue

and our current initiatives to

increase revenues include:

■ Marketing construction materials

like rock, sand and gravel

■ Contracting with the federal

government to survey

ANCSA lands

■ Leasing logging roads and

other timber development

infrastructure to third parties

and generating revenues from

easements across our lands

■ Pursuing land exchanges with

state, federal and private entities

■ Through a federal grant,

analyzing if the technology has

sufficiently developed to

generate fuel-grade ethanol

from wood waste and timber

development residue at a profit

■ Selecting the remaining acreage

entitlement from ANCSA

Prospective initiatives include:

■ Creating a “mitigation bank”

to enable the use of cut-over

lands that have been reforested

to offset national wetlands

that were disturbed as a result

of development

8

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

BUILDING STRATEGIC

PARTNERSHIPS is key to

developing our new investments.

From the start, Sealaska pursued

a strategy of purchasing and

managing a variety of operating

companies with mixed results.

Today our plan focuses on

sharing the risks and benefits

of business operations with

successful strategic partners.

These partnerships enable

us greater participation in the

fast-changing global economy.

Our strategic partners

bring to Sealaska a proven

track record in their particular

industries. Sealaska contributes

its share of capital and a set of

unique competitive advantages

derived from our special

recognition as an Alaska Native

owned company.

Federal contracting

opportunities

The U.S. government is the

largest purchaser of goods and

services in the world. Alaska

Native corporations have attrac-

tive federal contracting advan-

tages by law, and many ANCSA

corporations have aggressively

and successfully become

significant federal contractors.

ANCSA classifies Native

corporations as minority-owned

businesses. For example,

TriQuest is a member of the

National Minority Supplier

Development Council, and in

the private sector we expect

to bring more diversity supply

business to our plastics

company joint venture with

Nypro, Inc. ANCSA corporations

have these same competitive

advantages in the government-

contracting arena.

Alaska Native Wireless

AT&T Wireless Services, our

strategic partner with Alaska

Native Wireless, is a major player

in the telecommunications

industry. Sealaska Corporation,

Doyon, Ltd. and Arctic Slope

Regional Corporation, along

with AT&T Wireless Services

and others, formed Alaska

Native Wireless and competed

successfully for wireless

telecommunications licenses

in a number of major U.S.

markets, using Alaska Native-

owned “designated entity”

bidding credits.

In this investment, Alaska

Native Wireless is expected

to own the airwaves that the

industry needs to build out and

offer a wide range of wireless

communication services to

key U.S. markets. The value of

our licenses does not require

further investment of capital to

build the networks and offer the

wireless services to customers.

BUILDING STRATEGIC PARTNERSHIPS IS KEY TO DEVELOPING OUR

NEW INVESTMENTS. TODAY OUR PLAN FOCUSES ON SHARING THE

RISKS AND BENEFITS OF BUSINESS OPERATIONS WITH KNOWL-

EDGEABLE STRATEGIC PARTNERS. SEALASKA PROVIDES CAPITAL

AND A SET OF UNIQUE ADVANTAGES AS AN ANCSA CORPORATION.

Valley View Casino

Sealaska’s loan to the San

Pasqual Band of Mission Indians

near Escondido, California is

located in a fast-growing and

affluent market. Despite the

operational difficulties in 2001, we

are confident that the market

potential of the area is very

strong, and that the casino

will provide a healthy return to

Sealaska. In this investment,

Sealaska provided a portion of the

startup capital to the San Pasqual

Tribe, along with First Nation

Gaming and Wells Fargo Bank.

10

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

ANCSA CORPORATIONS are

celebrating the first 30 years

of the Alaska Native peoples’

experience in the world of

business as profit-making

corporations. ANCSA is an

experiment — an unprecedented

Congressional land claims

settlement with Native American

tribes in Alaska. Thirty years is

time enough to observe dramatic

change in the lives of Alaska

Natives, but it is also only a

short but recent chapter in the

centuries-long history of Alaska

Natives, our relationship to the

land, our relationship to each

other, and to the larger state,

national and world societies in

which they exist.

Yet Sealaska’s business

history is barely 23 years old.

Although Sealaska was formed

in June of 1972, the first seven

years of Sealaska’s existence

were consumed with setting up

the mechanics of a corporation

and, very importantly, gaining

title to the aboriginal lands we

retained in the settlement. The

first major land conveyance was

in 1979, and soon thereafter

Sealaska and the village corpo-

rations of Southeast Alaska

began developing timber. Today,

Sealaska Timber Corporation

remains the flagship subsidiary

of Sealaska, harvesting and

marketing timber, and gener-

ating income and cash flow

that has enabled virtually all

other business developments

Sealaska has undertaken.

Hands-on experience in

business has yielded lasting

expertise in a number of impor-

tant areas. But in 23 years, we

have also been reminded of the

importance of a Native value that

was articulated centuries ago:

THIRTY YEARS IS TIME ENOUGH TO OBSERVE DRAMATIC CHANGE

IN THE LIVES OF ALASKA NATIVES, BUT IT IS ONLY A RECENT

CHAPTER IN OUR HISTORY. WE HAVE ARRIVED AT A STRONG

CONFLUENCE WHERE BUSINESS AND CULTURE BLEND INTO

A POWERFUL FORMULA FOR SUCCESS.

the necessity of cooperation and

partnerships for survival. We

have developed a keen expertise

in harvesting and marketing

timber and in managing our

forest resources for the long

term. In other areas of business,

however, we have learned the

importance of forging relation-

ships with strategic partners

who bring to us their own

knowledge of certain businesses

and industries.

Thirty years later, we recog-

nize the competitive strength

of a business corporation

founded on Native culture and

Native values. It has taken three

decades to get here, but we

have arrived at a formula for

success, at a strong confluence

where business and culture

come together and push each

other toward success.

We have not arrived at this

point alone. We have reached

this point with the strong support

and backing of our shareholders.

It is because we share with

them a vision of the future for

Alaska Natives, and we have an

important part to play in

bringing that future to life.

“THROUGH FAMINE, ICE AGE,

SICKNESS, WAR AND OTHER

OBSTACLES, UNITY AND

SELF DETERMINATION ARE

ESSENTIAL TO SURVIVAL.”—Dr. Walter A. Soboleff, from his “Native Values”, as presented

in Sealaska Heritage Institute’s Tlingit Life Stories.

Patrick M. AndersonANCHORAGE

Joseph Demmert, Jr.KETCHIKAN

Clarence Jackson, Sr.KAKE

Gordon James, Sr.CRAIG

Byron I. MallottJUNEAU

12

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

Jacqueline JohnsonFAIRFAX, VA

Albert KookeshANGOON

Daniel M. LestonAUBURN, WA

Ethel M. LundJUNEAU

Richard J. Stitt, Sr.JUNEAU

Edward K. ThomasJUNEAU

Rosita F. WorlJUNEAU

Marjorie V. YoungCRAIG

William F.StraffordEXECUTIVE VICE PRESIDENT& CHIEF FINANCIALOFFICER

Chris E. McNeil, Jr.PRESIDENT & CHIEFEXECUTIVEOFFICER

Maxine RichertVICE PRESIDENT& CORPORATESECRETARY

Richard P. HarrisSENIOR VICEPRESIDENT,NATURALRESOURCES

E. Budd SimpsonOUTSIDECOUNSEL

Patrick W. Duke, CFATREASURER, & CORPORATE INVESTMENTOFFICER

Ross V. SoboleffVICE PRESIDENT,CORPORATECOMMUNICATIONS& ASSISTANT TOTHE PRESIDENT

LEFT TO RIGHT

14

Se

ala

ska

Co

rpo

rati

on

an

d S

ub

sid

iari

es

FIVE-YEAR SUMMARY OF SELECTED CONSOLIDATED FINANCIAL DATA

(in thousands of dollars, except per share amounts and ratios) 2001 2000 1999 1998 Short 1997

Total revenues $ 146,451 $ 150,774 $ 175,405 $ 189,466 $ 135,972

Net earnings (loss) (21,249) (122,410) 10,040 11,943 27,513

Total assets 189,887 246,536 354,600 345,916 372,496

Shareholders’ equity 103,293 124,542 254,806 253,937 251,374

Long-term bank debt 3,764 – 29,719 30,110 34,777

Short-term bank debt 40,203 53,941 19,838 15,595 19,391

Current ratio 1.13 0.57 1.00 1.20 1.40

Debt/equity ratio 0.43 0.43 0.39 0.32 0.43

Shareholders’ equity per share $ 66 $ 79 $ 162 $ 161 $ 159

Net earnings (loss) per share (13.49) (77.70) 6.37 7.57 17.45

Dividends per share $ 0.00 $ 5.08 $ 5.97 $ 5.70 $ 6.00

Book value per 100 shares 6,557 7,905 16,158 16,103 15,940

All historical financial information has been reclas-

sified to reflect the reclassification of TriQuest

Corporation (TriQuest) from a discontinued opera-

tion (as reported in the fiscal year 2000 annual

report) to a continuing operation, as a result of our

joint venture with Nypro, Inc. at TriQuest Mexico in

Guadalajara (see Note 2 to the Consolidated

Financial Statements).

Management’s Discussion and Analysis of

Financial Condition and Results of Operations

reviews operating results of Sealaska Corporation

(the Company) for each of the three fiscal years in the

period ended December 31, 2001 (fiscal 2001, 2000

and 1999), and its financial condition at December 31,

2001. This review may contain forward-looking

statements that involve risks and uncertainties, and

should be read in conjunction with the accompanying

Consolidated Financial Statements, the related Notes

to Consolidated Financial Statements, and the Five-

Year Summary of Selected Financial Data. Our actual

results could differ materially from those anticipated

in the forward-looking statements as a result

of certain factors including the risks discussed in

“Factors Affecting Business Performance” (pg. 21).

Year 2001 in Review■ A joint venture with Nypro, Inc. was negotiated to

include the TriQuest Guadalajara, Mexico plant,

resulting in TriQuest Corporation being reclassi-

fied as a continuing business from discontinued

status, as reported last year.

■ Alaska Native Wireless (ANW) invested

$85 million into the wireless spectrum

telecommunications business with AT&T

Wireless Services. Sealaska’s share of this

investment is $40 million.

■ Valley View Casino, owned by the San Pasqual

Band of Mission Indians, opened in April 2001

with 760 slot machines.

■ TriQuest-Puget Plastics, LLC operations in

Vancouver, WA, which was formed in fiscal year

2000, will be closed by June 2002 by the mutual

agreement of its owners, Sealaska Corporation

and Arctic Slope Regional Corporation.

■ Chris E. McNeil, Jr., was appointed President &

Chief Executive Officer of Sealaska Corporation

on February 23, 2001.

■ SeaCal completed sale of its calcium carbonate

inventory and is continuing negotiations for sale

of the company and its assets.

■ In 2001 Sealaska Timber Corporation and its

contractors, for the first time, maintained a

shareholder hire rate in excess of 53% of the total

workforce employed in our logging operations.

■ Through Sealaska Heritage Institute, Sealaska

awarded $550,000 in scholarships and grants to

497 students in 2001.

16

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

MANAGEMENT’S DISCUSSION AND ANALYSIS O F F I N A N C I A L C O N D I T I O N A N D R E S U LT S O F O P E R AT I O N S

Results of OperationsIn thousands, except per share/dividend amounts

Change ChangeYr 2001 from Yr 2000 from Yr 1999

Total Revenues $146,451 –2.9% $ 150,774 –14.0% $175,405

Combined Operating and SG&A Expenses $160,745 –30.4% $ 230,856 41.2% $163,468

Operating Income(Loss) $ (14,294) 82.2% $ (80,082) –770.9% $ 11,937

Operating Margin Percentage –9.8% –53.1% 6.8%

Income (Loss) from continuing operations before revenue sharing, equity in net losses of affiliates, income taxes and cumulative effect of changes inaccounting principles $ (15,022) 81.8% $ (82,448) –758.5% $ 12,521

Natural Resource Sharing $ 6,269 12.0% $ 5,596 –7.5% $ 6,052

Net Income (Loss) $ (21,249) 82.6% $(122,410) –1,319.2% $ 10,040

% of Total Revenues –14.5% –81.2% 5.7%

Income (loss) pershare $ (13.49) 82.6% $ (77.70) –1,319.8% $ 6.37

Dividends per share $ – –100.0% $ 5.08 –14.9% $ 5.97

Comparison of Fiscal 2001 to Fiscal Years 2000 and 1999Continuing operations generated revenues of

$146 million from our timber, plastics, telecommu-

nications, other natural resources, and investments.

Revenues from our casino loan were deferred

to a later period. Total revenues for 2001 were

$146 million, a decrease of 3% and 17%, from fiscal

years 2000 and 1999, respectively. The decrease

in revenues was a result of downsizing, the sale

and closure of various TriQuest operations and

decreased investment earnings.

The Company’s net loss for fiscal year 2001 was

$21 million, which included a loss of $3 million

combined from Sealaska Timber Corporation (STC),

investments, and headquarters operations; and a

loss on operations and writedowns at TriQuest

Corporation of $24 million and including a reversal of

a $6 million accrued discontinued operations reserve.

The fiscal year consolidated net loss of $21 million

compares to a net loss of $122 million and income

of $10 million in fiscal 2000 and 1999, respectively.

The significantly decreased loss in fiscal year

2001 was a result of downsizing and selling various

components of TriQuest Corporation, and a result of

earnings from our ANW investment in the telecom-

munications business. Overall operations improved

when compared to fiscal year 2000. These included:

Operations – Comparisons of Fiscal Year 2001 to Fiscal Year 2000I N V E S T M E N T P O R T FO L I O

Our investment portfolio earned $1.8 million in fiscal

year 2001 (including ANW income and writedown

on the casino investment) as compared to losses

of $12.7 million in fiscal year 2000. While the U.S.

equity markets continued to incur substantial losses

during the year, our portfolio, as a result of

moving investment funds to the ANW investment

($40 million) and the casino investment ($10 million)

early in the fiscal year, avoided all but the January

2001 investment market setback, and a $5 million

writedown on the casino investment.

T I M B E R O P E R AT I O N S

STC had another successful year with a return of $14

million before Alaska Native Claims Settlement Act

(ANCSA) Section 7(i) expense and a net income of

$5 million after ANCSA Section 7(i) expenses. These

results compare to a fiscal year 2000 return of

$14 million before 7(i) expense and a net income of

$6 million after 7(i) expenses and before adjustments.

In part, STC’s success in 2001 was due to its

efforts to reduce its operating and contracting cost

and to become more cost competitive in the world

markets that we serve. STC is a major economic

force in Southeast Alaska and particularly in the

Native communities where we operate. A recent

study by the McDowell Group found that STC activi-

ties cause it to be the largest private employer in

Southeast Alaska. In the Native communities where

we operate, STC provides the community with 18%

to 30% of the personal income for those communi-

ties’ residents. STC and its contractors continue to

achieve in excess of 50% shareholder hire rate by

maintaining a 53% shareholder work force during

2001. In addition, shareholder owned companies

in logging, towing and ship tending continue

to successfully provide competitive contractual

services for STC.

N AT U R A L R E S O U R C E S

Our natural resource division ended the year

with income of $0.5 million, primarily from rock

sales, resource escrows, silviculture contracts

and federal grants for researching technical and

economic feasibility of producing fuel-grade

ethanol. This compares to the previous year’s net

17

income of $0.8 million. The department continues

to realize individually small but collectively important

income opportunities from the Company’s non-timber

land and other resources.

CO R P O R AT E H E A D Q U A R T E R S

Corporate general and administrative expenses

amounted to $11 million excluding natural resources

costs, which were included in the paragraph above.

This compares to prior year total expenses of

$12.5 million. The reduction was achieved through

various cost-cutting initiatives such as staff reduc-

tions, reduced travel expenses and reduced

consulting and legal expenses.

VA L L E Y V I E W C A S I N O I N V E S T M E N T

The San Pasqual Band’s Valley View (temporary)

Casino near Escondido, CA opened in April 2001

with 760 slot machines. As of the end of fiscal year

2001, the casino had 784 slot machines and was

continuing to increase the EBITDAC (Earnings

Before Interest, Taxes, Depreciation, Amortization

and Consulting fees), and the balance of cash in the

depository (available cash) account on a monthly

basis, while operating costs have continued to fall.

But, on April 19, 2002, the San Pasqual tribe informed

us that the plans for the larger permanent casino

had been shelved and that the costs ($2.7 million)

advanced by the Company for pre-construction and

development expenses were being written off. As a

result, the casino’s auditors recorded an impairment

of this amount and other related costs, totaling

approximately $4.8 million, against the casino’s

balance sheet as of December 31, 2001. The result

of this action impacted Sealaska’s fiscal year 2001

financial statements because generally accepted

accounting principles require us to account for our

$14,700,000 loan to the casino as if it were a real

estate joint venture investment as described in

Note 10 to our consolidated financial statements.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I S ( c o n t’d )

Consequently, we recorded a reduction to our

carrying value of amounts owed for principal,

interest and fees for an allocation of the losses

incurred by the casino during 2001 from initial

operations and for the termination of its plans for

a permanent facility.

None the less, our total investment of $14.7

million is expected to be recovered in full, with

accrued interest, during the next two years.

A N W S P E CT R U M I N V E S T M E N T

Our partnership with AT&T Wireless Services

contributed significant profit to the Company with

recorded interest income of $8,861,000 on our

$40 million investment made in February 2001. The

cash from the reported accrued interest income will

be paid to Sealaska at the end of the partnership.

T R I Q U E S T CO R P O R AT I O N

During fiscal year 2001, the Company negotiated

a joint venture with Nypro, Inc., a plastics company

operating 26 plants worldwide, for management

services at our Guadalajara, Mexico plant. This

agreement was signed in January 2002. During

fiscal year 2001, TriQuest had a consolidated

net loss of $24 million at TriQuest Guadalajara,

TriQuest Monterrey, Mexico, Synergy Systems in

Redmond, WA, TriQuest-Puget Plastics, LLC, and

the Vancouver, WA headquarters location. Included

in the $24 million loss is a $7 million write-down on

the value of TriQuest assets, bringing the value of

each TriQuest component to its current market

value; this compares to fiscal year 2000 when

TriQuest lost $26 million on operations and an

additional $31 million write-down was taken. The

Vancouver headquarters location was closed during

fiscal year 2001 at an annual saving going forward

of $4 million; the Monterrey, Mexico plant is in the

process of being sold, resulting in positive cash

flow, which should be completed by the summer of

18

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

2002, and the TriQuest-Puget Plastics, LLC plant is

shut down with final closure also expected by the

summer of 2002.

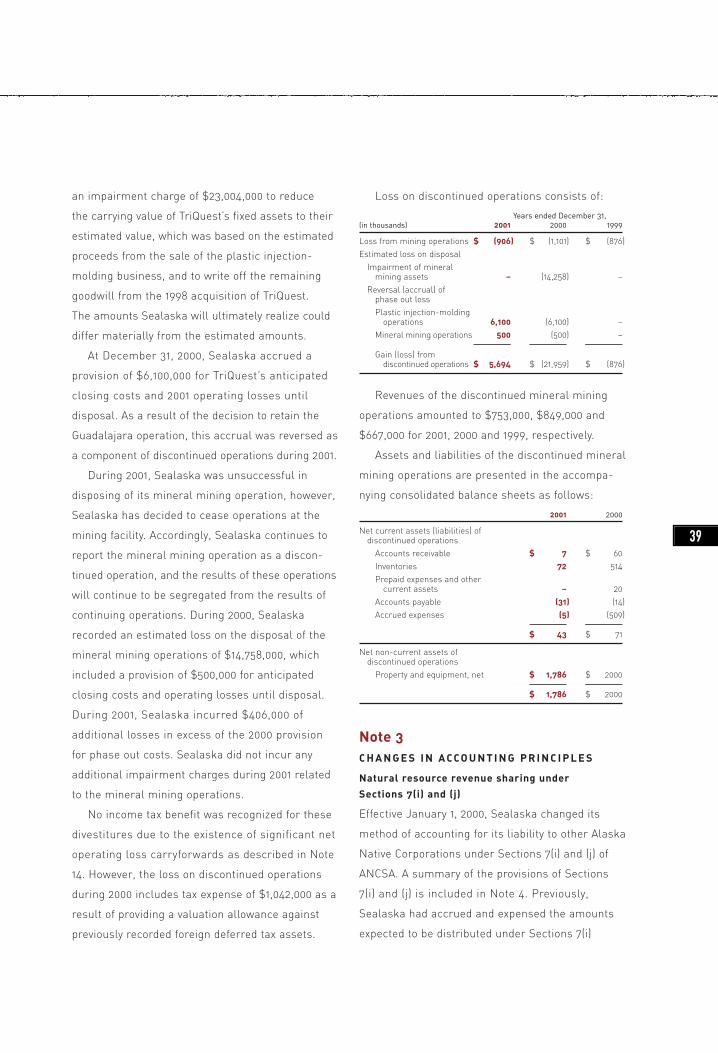

D I S CO N T I N U E D O P E R AT I O N — S E A C A L, L LC

Our SeaCal mining operation at Calder (on Prince

of Wales Island in Southeast Alaska) continued to

be marketed for sale during the year as we sold

remaining stockpiled inventories. Operations during

the year reported a net loss of $406,000 (net of

fiscal year 2000 reserves) as compared to the fiscal

year 2000 loss on operations of $1.1 million and a

writedown of $15 million. No further production is

planned and we expect either the company or the

remaining assets to be sold by the summer of 2002.

A N C S A S E CT I O N 7 ( i ) D I S T R I B U T I O N

Our ANCSA Section 7(i) expense totaled $7.3 million

for the other eleven ANCSA regional corporations

and another $990,000 ANCSA Section 7(j) to our

shareholders, as compared to a combined distribu-

tion of $6 million in fiscal year 2000. In addition we

received a total of $3.2 million from other ANCSA

regional corporations during 2001, of which 50%

has been distributed to our shareholders. We have

also deferred the Company’s own fiscal year 2001

Section 7(i) and 7(j) distributions, due March 30,

2002, until the summer of 2002.

I N CO M E TA X E S

The Company does not expect to pay domestic

federal and state income taxes because of depletion

deductions from harvesting ANCSA timber. Net

operating loss carry forwards in excess of $390

million are available for future offset of federal

income tax on taxable income. During fiscal year

2000, a $1 million non-cash income tax expense as

a result of a valuation allowance for a discontinued

operation’s foreign deferred tax assets was recorded.

N E T E A R N I N G S ( LO S S ) P E R S H A R E

Net loss per share totaled $(13.49) for fiscal year

2001. This is compared to net loss per share of

$(77.70) in fiscal year 2000, and net earnings per

share of $6.37 in fiscal year 1999.

D I V I D E N D S P E R S H A R E

No dividends for fiscal year 2001 were paid to

shareholders, as a result of the losses incurred

in fiscal year 2001 and 2000. This compares

to dividends paid of $5.08 per share (a total of

$8 million) and $5.97 per share (a total of $9.4 million)

in fiscal years 2000 and 1999, respectively.

Analysis of Financial PositionA S S E T S

Total assets of $190 million at the end of fiscal year

2001 decreased 23 percent from $247 million at the

end of fiscal year 2000. Included in the total assets

at the end of 2001 are net non-current assets of

$1.8 million from discontinued (SeaCal) operations

expected to be sold in fiscal year 2002, and $123

million of investment capital and trust funds, including

the investments in ANW and the casino. Current

assets are $76 million and $60 million for 2001 and

2000, respectively. As reported in Notes 4 and 9, the

value of Sealaska’s ANCSA land and timber assets

are not included in our asset totals, although they

have significant economic value to Sealaska.

L I A B I L I T I E S

Total liabilities of $87 million decreased 29 percent

from the fiscal 2000 total of $122 million. Current

liabilities were $67 million at fiscal year-end 2001, a

36% decrease from $105 million in fiscal year 2000.

Of the current liability total, $40 million consists of

current notes payable to banks (lines of credit), and

ANCSA total Section 7(i) liabilities, including short

term deferred payments of $10 million; long term

Section 7(i) liabilities also total $10 million.

19

S H A R E H O L D E R S ’ E Q U I T Y

Total shareholders’ equity was $103 million at fiscal

year-end 2001 and $125 million for fiscal year 2000.

The change in shareholders’ equity came from the

loss of $21 million reported during fiscal year 2001.

D I V I D E N D S D I S T R I B U T E D

No dividends were distributed in fiscal year 2001

as a result of negative earnings in 2001 and 2000.

This compares to dividends of $8 million, $9.4

million, $9 million and $9.5 million distributed in

fiscal years 2000, 1999, 1998 and short fiscal year

1997, respectively.

L I Q U I D I T Y A N D C A P I TA L R E S O U R C E S

At December 31, 2001, the Company had cash on

hand and current investment securities of $56

million including $40 million on hand to pay current

bank debt. In addition, another $67 million was held

in our other investments including ANW, Valley

View Casino and venture capital funds.

The Company had positive operating cash flow

of approximately $26 million in fiscal year 2001 as

compared to positive cash flow from operations of

$5 million and $9 million in fiscal years 2000 and

1999, respectively. This is due to the decreased

levels of receivables and inventory, as well as the

liquidation of certain marketable securities. In

addition, the Company repaid $10 million of long-

term debt in fiscal year 2001 as compared to net

additional borrowings of $4 million in each of

fiscal years 2000 and 1999.

At December 31, 2001, our current ratio (current

assets compared to current liabilities) was

1.13 compared to 0.57 at December 31, 2000. The

current ratio increased because of the need for

liquidity to fund operations and bank debt for 2002

and because part of the short-term bank debt was

paid in 2001. At December 31, 2001, Sealaska’s only

long-term debt is the Sealaska Plaza mortgage.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I S ( c o n t’d )

As of December 31, 2001, we had short-term

bank lines of credit (LOC) of $33 million at Sealaska

corporate and $7 million at TriQuest, totaling

$40 million. Investment securities of $36 million

were collateral for the corporate debt. One of the

corporate lines of credit expired in February 2002

and we paid off the $33 million liability. The other

line of credit (TriQuest), which will expire in July

2002, is being paid at the rate of $1 million per

month. Another available $5 million Corporate

LOC has been extended through June 2002. Any

proceeds from the sale of discontinued operations

or other operations will be used to assist in the

pay-down of the short-term bank debt.

The Company’s liquidity for fiscal year 2002 will

be affected by the operating performance of timber

operations, natural resource department activity, the

plastic companies’ requirements and proceeds from

the casino investment. Our exposure to changes in

the stock market performance has been lessened

by the investments in other passive activities and

through liquidation of investment securities to pay

down on short-term bank debt both in fiscal year

2001 and in fiscal year 2002. Additionally, we expect

to invest up to $4 million of new operating and

working capital into the TriQuest Guadalajara plant

in fiscal year 2002, and the TriQuest-Puget Plastics,

LLC will require an additional $1.4 million investment,

payable in April 2002. Offsetting these investments

should be proceeds from the sale of SeaCal and the

TriQuest Monterrey, Mexico plant. The Company

anticipates that its available financial resources are

sufficient to meet its anticipated liquidity needs for

fiscal year 2002. The Company is currently seeking

a new line of credit to fund operations and capital

needs, and we expect to have entered into a new

credit facility by the summer of 2002.

20

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

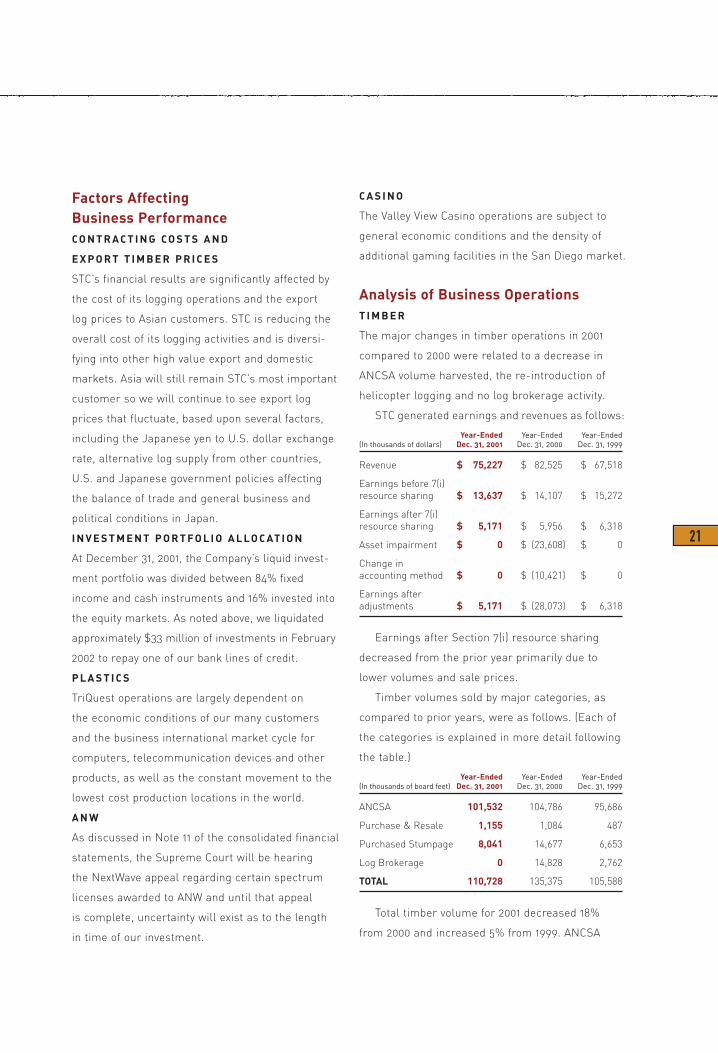

Factors Affecting Business PerformanceCO N T R A CT I N G CO S T S A N D

E X P O R T T I M B E R P R I C E S

STC’s financial results are significantly affected by

the cost of its logging operations and the export

log prices to Asian customers. STC is reducing the

overall cost of its logging activities and is diversi-

fying into other high value export and domestic

markets. Asia will still remain STC’s most important

customer so we will continue to see export log

prices that fluctuate, based upon several factors,

including the Japanese yen to U.S. dollar exchange

rate, alternative log supply from other countries,

U.S. and Japanese government policies affecting

the balance of trade and general business and

political conditions in Japan.

I N V E S T M E N T P O R T FO L I O A L LO C AT I O N

At December 31, 2001, the Company’s liquid invest-

ment portfolio was divided between 84% fixed

income and cash instruments and 16% invested into

the equity markets. As noted above, we liquidated

approximately $33 million of investments in February

2002 to repay one of our bank lines of credit.

P L A S T I C S

TriQuest operations are largely dependent on

the economic conditions of our many customers

and the business international market cycle for

computers, telecommunication devices and other

products, as well as the constant movement to the

lowest cost production locations in the world.

A N W

As discussed in Note 11 of the consolidated financial

statements, the Supreme Court will be hearing

the NextWave appeal regarding certain spectrum

licenses awarded to ANW and until that appeal

is complete, uncertainty will exist as to the length

in time of our investment.

C A S I N O

The Valley View Casino operations are subject to

general economic conditions and the density of

additional gaming facilities in the San Diego market.

Analysis of Business OperationsT I M B E R

The major changes in timber operations in 2001

compared to 2000 were related to a decrease in

ANCSA volume harvested, the re-introduction of

helicopter logging and no log brokerage activity.

STC generated earnings and revenues as follows:

Year-Ended Year-Ended Year-Ended(In thousands of dollars) Dec. 31, 2001 Dec. 31, 2000 Dec. 31, 1999

Revenue $ 75,227 $ 82,525 $ 67,518

Earnings before 7(i) resource sharing $ 13,637 $ 14,107 $ 15,272

Earnings after 7(i) resource sharing $ 5,171 $ 5,956 $ 6,318

Asset impairment $ 0 $ (23,608) $ 0

Change in accounting method $ 0 $ (10,421) $ 0

Earnings after adjustments $ 5,171 $ (28,073) $ 6,318

Earnings after Section 7(i) resource sharing

decreased from the prior year primarily due to

lower volumes and sale prices.

Timber volumes sold by major categories, as

compared to prior years, were as follows. (Each of

the categories is explained in more detail following

the table.)

Year-Ended Year-Ended Year-Ended(In thousands of board feet) Dec. 31, 2001 Dec. 31, 2000 Dec. 31, 1999

ANCSA 101,532 104,786 95,686

Purchase & Resale 1,155 1,084 487

Purchased Stumpage 8,041 14,677 6,653

Log Brokerage 0 14,828 2,762

TOTAL 110,728 135,375 105,588

Total timber volume for 2001 decreased 18%

from 2000 and increased 5% from 1999. ANCSA

21

volumes sold during 2001 decreased 3% from 2000

and increased 6% compared to 1999. STC decreased

its harvest and sale of timber from stumpage

acquired from others by 45% compared with 2000.

Purchase and resale activities remained consistent

with 2000. Log brokerage for other private sources

decreased substantially from 2000.

Harvest of ANCSA timber in 2001 was conducted

in Southeast Alaska on approximately 5,016 acres in

the Hoonah, Hydaburg, Dall Island and Kake areas.

The total acres cut includes almost 700 acres of

helicopter partial cuts. Approximately 4,244 and

3,632 acres were harvested in 2000 and 1999,

respectively. These figures do not include harvest

acreage on non-ANCSA stumpage purchases.

Since 1980, the Company has harvested timber

from 71,389 acres of its current ANCSA conveyance

of 290,000 acres on its ANCSA lands. Of the total

ANCSA acres harvested, 10,123, or 14%, are partial

cuts using primarily helicopter logging methods

and 61,266 were harvested using clear-cut

harvesting methods.

In Southeast Alaska, young forests naturally

regenerate after harvesting, but in some site-specific

situations we plant trees to speed regeneration

and to enhance environmental protection. Sealaska

has replanted approximately 3,700 acres.

Approximately 12 to 18 years after harvest, the

young forests are precommercially thinned to speed

growth and to benefit wildlife habitat. Such work

has been completed on 14,665 acres of forest stands.

The Company has continued with techniques to

improve the quality of wood from second-growth

forests by pruning lower branches, thereby

speeding the development of clear wood. Pruning

areas totaling 661 acres have been established.

The purchase and resale activity includes the

purchase of logs from private landowners in

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I S ( c o n t’d )

Southeast Alaska and subsequent sales to STC

customers, either in conjunction with, or separate

from, ANCSA and purchased stumpage timber.

The harvest and sale of purchased stumpage is

a direct result of our efforts to diversify the sources

of timber, and therefore, extend the life of our

ANCSA timber. STC harvested stumpage purchased

on 400 acres in 2001, compared to 416 acres and

445 acres in 2000 and 1999, respectively.

STC’s logging, road construction, towing, and

stevedoring contractors employed an average of

292 workers during 2001 compared to 372 and 289

in 2000, and 1999 respectively. The percentage of

shareholder employees during 2001, 2000, and 1999

was 53%, 52% and 40%, respectively.

I N V E S T M E N T P O R T FO L I O

Domestic equity market

For the second consecutive year, the domestic

equity markets posted negative returns. The reces-

sion, the events of September 11 and worries over

corporate accounting irregularities all helped to

drive the market lower. For 2001, the S&P 500 lost

11.8% and the technology-laden NASDAQ lost 20.8%.

Domestic bond market

Bond markets rallied for the second straight year

as bonds benefited from lower interest rates and

reallocation of assets from the equity market. The

domestic fixed income market, as measured by

the Lehman Aggregate Index, returned 8.42%.

P L A S T I C S

The Company negotiated a joint venture agreement

with Nypro, Inc., for the TriQuest Guadalajara

plant during fiscal year 2001. This agreement,

signed in January 2002, gives Nypro 20% ownership

of TriQuest’s Guadalajara plant in exchange for

management services. Nypro has an option to

acquire an additional 29% ownership interest,

which includes a payment to Sealaska for at least

22

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

$4 million of intercompany loans. In addition, Nypro

can purchase the other 51% after five years at the

fair market value (FMV) of the Guadalajara plant

operations, plus another $4 million (plus accrued

interest) repayment of intercompany debt.

TriQuest had consolidated revenues of $67

million and a loss on operations of $22 million

during 2001 as a result of the continued and deep

recessionary economic conditions, which affected

all industries that TriQuest competes in, including

computers, cell phones, desktop phones and other

plastic components.

Included in the loss reported above were the

operating results of the Monterrey plant, which is

for sale. The Company expects to complete the sale

by the summer of 2002. Additionally, the TriQuest-

Puget Plastics, LLC operation in Vancouver, WA

announced in February 2002 that it will be closing

and the plant should be completely shut down by

the summer of 2002.

During 2001, there was an additional asset

write-down of $7 million due to the continuing

losses and declining market. This compared

to the $31 million impairment write-down taken

during 2000.

Discontinued OperationsM I N I N G

The SeaCal subsidiary has been reported as a

discontinued operation. Total sales of 47,354 tons

brought in sales revenues of $753,000. SeaCal

recorded a net loss of $406,000, primarily due to

sales prices below production and shipping costs.

The liquidation of the inventories generated positive

cash flow of $40,000. During 2001, SeaCal focused

on selling remaining inventories and implementing

a process for divestiture of the SeaCal operations.

Several interested companies continue to evaluate

business models that will allow them to acquire

the property and continue its production as an

operating calcium carbonate mine. If a buyer cannot

be found during the first half of 2002, Sealaska will

begin a systematic liquidation of the capital assets.

In addition, the 572-acre non-ANCSA SeaCal

property has high amenity and recreation values

that provide an opportunity to subdivide the

property for recreational lot sales.

OutlookThe matters discussed in this section are

forward-looking statements that involve risks

and uncertainties including, but not limited to,

economic, competitive, governmental and

technological factors affecting the Company’s opera-

tions, markets, products, services and prices.

T I M B E R

At the start of 2002, the outlook for STC’s log

sales is somewhat brighter than during 2001.

Housing starts and lumber demand in the United

States remain robust, while supply from Canada

continues to be constricted by high import taxes

into the U.S. markets.

In the Pacific Northwest, strong demand and

new sawmill capacity will create tight supply

for hemlock logs. In Japan, low inventories and

concern over reliability of Canadian log supply

have outweighed weakness in the yen and allowed

hemlock prices to rise. Relatively stronger buying

from Korea and decreased supply from Alaska

also will help create diversity and balance in STC’s

hemlock markets this year.

The overall economic outlook in Japan remains

rather poor and if the yen weakens further, it is

doubtful that recent price increases for some items

can be maintained throughout 2002. Even though

STC has partially insulated itself from further

23

downturns in Japan through greater market diver-

sification, STC’s performance remains strongly

linked to log prices in Japan. Overall housing starts

in Japan are expected to slow another 5% from

2001. Total Japanese softwood log imports may also

decrease by up to 10%, as imported lumber continues

to gain market share. For specialty items such as

high value spruce, STC faces less threat of substi-

tution and also will also benefit from less competi-

tion from other suppliers in Alaska and Canada.

STC will seek ways to minimize the impact of

poor pulp markets and continue to develop emerging

softwood log markets in China. Maintaining direct

market access and strengthening customer service

to end-users in Japan will help STC to remain

largely unaffected by the wave of restructuring

among trading companies that is expected to occur

in Japan this year.

Recognizing the evolving timber markets and

fundamental changes in STC’s traditional markets,

STC is undergoing a strategic planning process to

chart its future direction. This process builds on

STC’s current strengths, identifies new markets,

products, business opportunities and partnerships

and plots a course for continued success of STC.

Key markets and opportunities identified in this

planning process are already being served. British

Columbia is negotiating with its First Nations bands

to settle their land claims. This would create

opportunities for STC to work closely with Natives

in Canada to sell their logs into the distribution

channels already established by STC. Also, the

U.S. Government is a major purchaser of wood

and paper products. The use of Small Business

Administration (SBA) preferences is being tested

to determine if finished products from STC logs

can capture these market opportunities.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I S ( c o n t’d )

M I N E R A L S A N D M I N I N G

The Company has almost 590,000 acres of subsur-

face rights that are rich in sand, rock, gravel and

industrial and precious metals. The production and

sales of sand, rock and gravel (materials) is the

world’s largest mining activity in terms of volume

and sales. The economic opportunity for the further

development of material resources continues to

grow because the existing material sources near

major urban centers along the Pacific Coast of the

United States have been depleted, environmental

restrictions prohibit opening of new mines or the

cost of transport to the urban centers by truck

or rail is becoming cost prohibitive. The extensive

shoreline, easy access to these materials and

ability to transport large quantities by barge is

expanding the potential opportunities for us to

become a key supplier to the major West Coast

urban centers. A key challenge is that our mineral

resources are in remote areas with high cost of

development and transportation, which hinders our

ability to produce at positive margins.

Federal highway, port and development projects

are major purchasers of sand, rock and gravel

resources. The Company is qualified to become a

preferential supplier of these materials through

the SBA and other programs that are intended to

advance minority business opportunities.

N AT U R A L R E S O U R C E S

The focus of the Natural Resources division

is directed toward initiating strategies that

create revenue and cash flow and provide

asset enhancement.

Land Entitlement

The Alaska Native Claims Settlement Act was

passed on December 18, 1971. Since that time, the

Company has selected and received conveyance

24

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

to approximately 290,000 acres of land toward

fulfilling its entitlement under ANCSA. Largely due

to the mechanism that allocates land under the

provisions of section 14(h)(8) of ANCSA, the selection

and conveyance process is becoming significantly

encumbered despite the fact that 30 years have

passed since ANCSA was enacted. We foresee a

prolonged process with a minimum of ten or more

years before the final entitlement can be calculated,

and subsequently selected and conveyed. Therefore,

the Company has initiated negotiations with the

Bureau of Land Management in an effort to estab-

lish our final entitlement. Finalizing this entitlement

would provide us with an additional 50,000 acres of

land with a potential for 750 million board feet of

merchantable timber.

Wetland Mitigation Bank

Federal law requires that most land development

activities that involve filling or disturbance of

wetlands must compensate for lost wetlands. One

form of compensation is the purchase of “wetland

mitigation credits” from an approved “wetland

mitigation bank.” A bank typically restores degraded

wetlands, receives credits for the restoration and

is able to sell the credits to third parties who are

seeking the easiest, most cost effective way to

meet their wetland requirement. The Company, as

a major landowner, is uniquely suited to develop

these banks and sell the credits to third parties

and create substantial positive income.

Ethanol

The problem of wood residue management currently

encountered by the timber industry in Southeast

Alaska provides an opportunity to generate

additional revenues, reduce costs and assist in

maintaining the viability of the timber and woods

manufacturing industry in the region by converting

this material into a value-added product. We have

received substantial federal grants to continue

our investigation into the feasibility of converting

these wood residues into fuel-grade ethanol and

electricity for sale into the Alaskan market.

Land Stewardship

Establishing and implementing an effective

environmental management program is critical to

achieving the goals of being environmentally

responsible and sensitive to the impacts that may

occur from the Company’s resource development

activities. We strive to prevent and mitigate these

impacts through development planning, compliance

monitoring and promotion of innovative technology

and operating practices to protect the environment.

For example, we are undertaking studies to evaluate

the extent of quality wildlife habitat that exists in

second-growth stands and whether silviculture

practices can sustain and enhance those habitats,

the effect of precommercial thinning and brush

growth on early timber regeneration and to

evaluate the effectiveness of the Alaska Forest

Practices Act in the protection of fish habitat

and water quality. Maintaining a commitment to

environmental management is critical to protecting

our ability to responsibly develop resources.

I N V E S T M E N T P O R T FO L I O

Economic recovery, corporate accounting reform

and the war on terrorism will be dominant factors

affecting investment portfolio performance. A

tightening bias by the Federal Reserve Board and

correspondingly higher interest rates could nega-

tively affect the domestic bond market. However,

signs of economic growth should translate into

strong corporate earnings and higher equity prices.

25

P L A S T I C S

Nypro, Inc., our partner at the TriQuest

Guadalajara, Mexico plant, has made significant

operational improvements since being on site and

we expect that operations will be able to generate

positive cash flow and income before the fourth

quarter of fiscal year 2002. In addition, we expect

that our other plastics operations will be shut down

or sold by the summer of 2002, thereby eliminating

the need for further cash infusions. The operations

at Guadalajara require substantial additional

product orders, which we expect to occur during

the second half of fiscal year 2002.

M I N I N G

The SeaCal, LLC subsidiary has been reported as

a discontinued operation.

C A S I N O

Disregarding the write-down on the costs of the

permanent casino (construction since abandoned)

and other adjustments, of $5 million, the Valley

View Casino’s operations and cash flows have

improved considerably since last fall. The EBITDAC

(Earnings Before Interest, Taxes, Depreciation,

Amortization and Consulting fees) has continued to

improve monthly through March 2002. The senior

bank debt balance could be paid off before the end

of fiscal year 2002, which at that time would allow

the Company to begin receiving substantial cash

payments against our full $14.7 million loan

(investment). However, there are other casino

facilities being constructed in the general area.

This new competition will not be noticed in the

market until the summer of 2002, at which time

Valley View’s future monthly cash flow results could

be impacted. At the same time, the Valley View

Casino is considering expansion, and discussions

as to this and other operational management

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A LY S I S ( c o n t’d )

changes are ongoing with the Company and other

lenders.

W I R E L E S S I N V E S T M E N T

Our Alaska Native Wireless investment is secure

and generating a 24.7% compounded return at

this time. Barring a decision by the U.S. Supreme

Court (expected in 2003), or a renegotiation of

the agreement by AT&T Wireless Services, the

investment will continue to allow us to recognize

significant deferred-interest income throughout

fiscal year 2002 although no cash payments are

expected until 2007.

26

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

To the Board of Directors andShareholders of Sealaska CorporationWe have audited the accompanying consolidated

balance sheets of Sealaska Corporation and its

subsidiaries (“the Corporation”) as of December

31, 2001 and 2000, and the related consolidated

statements of income, of shareholders’ equity and

of cash flows for each of the three years in the

period ended December 31, 2001. These financial

statements are the responsibility of the Corporation’s

management. Our responsibility is to express

an opinion on these financial statements based

on our audits.

We conducted our audits in accordance with

auditing standards generally accepted in the United

States of America. Those standards require that we

plan and perform the audit to obtain reasonable

assurance about whether the financial statements

are free of material misstatement. An audit includes

examining, on a test basis, evidence supporting

the amounts and disclosures in the financial

statements. An audit also includes assessing

the accounting principles used and significant

estimates made by management, as well

as evaluating the overall financial statement

presentation. We believe that our audits provide

a reasonable basis for our opinion.

As described in Notes 4 and 9, the Corporation

has received or is entitled to receive surface and

subsurface rights to certain lands in Alaska.

The fair value of these lands and related natural

resources is not reasonably determinable and,

accordingly, is not included in the accompanying

consolidated financial statements.

As described in Note 14 to the consolidated

financial statements, the Corporation applies a

method of accounting for income taxes associated

with certain natural resources received pursuant

to the Alaska Native Claims Settlement Act, which

is not in accordance with Statement of Financial

Accounting Standard (SFAS) No. 109, Accounting

for Income Taxes.

In our opinion, except for the effects of the

matter described in the fourth paragraph above, the

consolidated financial statements referred to above

present fairly, in all material respects, the financial

position of the Corporation at December 31, 2001

and 2000, and the results of its operations and its

cash flows for each of the three years in the period

ended December 31, 2001 in conformity with

accounting principles generally accepted in the

United States of America.

As described in Note 3 to the consolidated

financial statements, effective January 1, 2000, the

Corporation changed its method of accounting

for its Section 7(i) expense and liability, and,

effective January 1, 1999, the Corporation changed

its method of accounting for silviculture and

reforestation costs.

Seattle, Washington

April 24, 2002

27

REPORT OF INDEPENDENT ACCOUNTANTS

December 31,(Dollars in thousands) 2001 2000

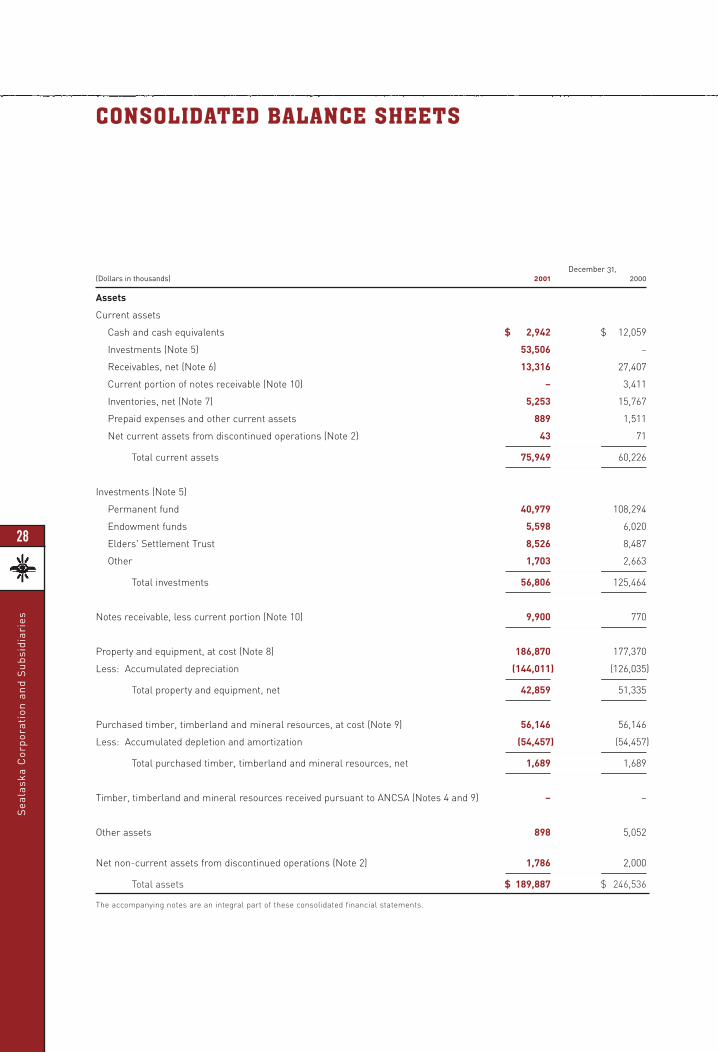

Assets

Current assets

Cash and cash equivalents $ 2,942 $ 12,059

Investments (Note 5) 53,506 –

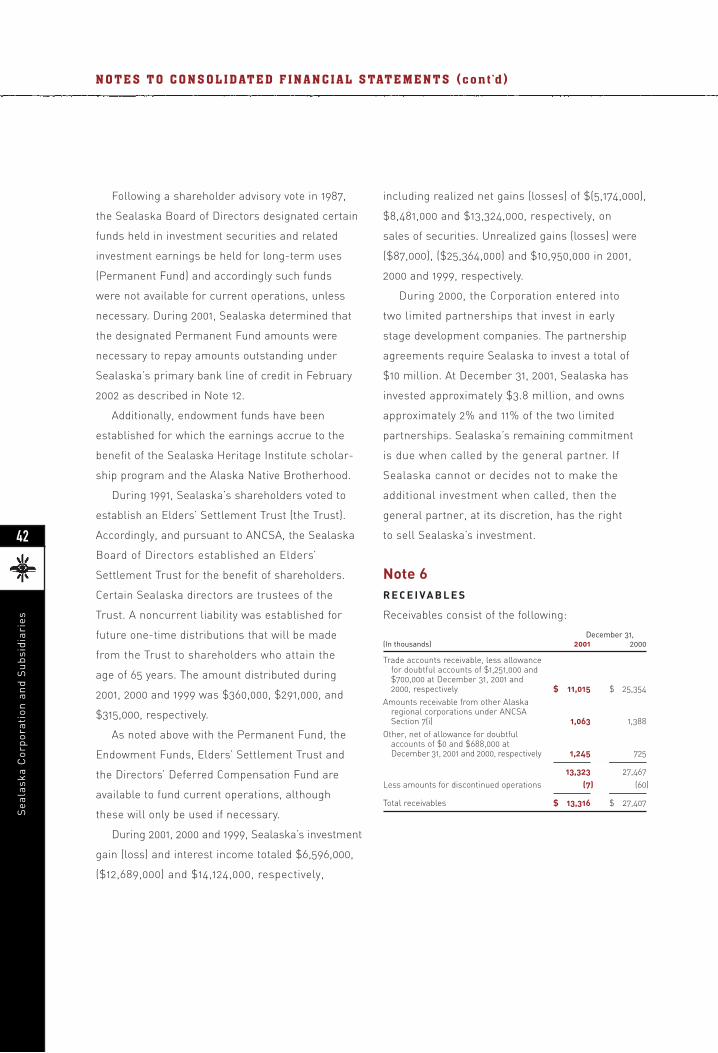

Receivables, net (Note 6) 13,316 27,407

Current portion of notes receivable (Note 10) – 3,411

Inventories, net (Note 7) 5,253 15,767

Prepaid expenses and other current assets 889 1,511

Net current assets from discontinued operations (Note 2) 43 71

Total current assets 75,949 60,226

Investments (Note 5)

Permanent fund 40,979 108,294

Endowment funds 5,598 6,020

Elders' Settlement Trust 8,526 8,487

Other 1,703 2,663

Total investments 56,806 125,464

Notes receivable, less current portion (Note 10) 9,900 770

Property and equipment, at cost (Note 8) 186,870 177,370

Less: Accumulated depreciation (144,011) (126,035)

Total property and equipment, net 42,859 51,335

Purchased timber, timberland and mineral resources, at cost (Note 9) 56,146 56,146

Less: Accumulated depletion and amortization (54,457) (54,457)

Total purchased timber, timberland and mineral resources, net 1,689 1,689

Timber, timberland and mineral resources received pursuant to ANCSA (Notes 4 and 9) – –

Other assets 898 5,052

Net non-current assets from discontinued operations (Note 2) 1,786 2,000

Total assets $ 189,887 $ 246,536

The accompanying notes are an integral part of these consolidated financial statements.

CONSOLIDATED BALANCE SHEETS

28

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

CONSOLIDATED BALANCE SHEETS

29

December 31,(Dollars in thousands) 2001 2000

Liabilities and Shareholders’ Equity

Current liabilities

Current portion of long-term debt (Note 12) $ 40,203 $ 53,941

Accounts payable 5,987 16,395

Amounts payable under ANCSA Section 7(i) and 7(j) (Notes 3 and 4) 9,890 7,585

Other accrued expenses 11,033 27,146

Total current liabilities 67,113 105,067

Non-current liabilities

Amounts payable under ANCSA Section 7(i) and 7(j) (Notes 3 and 4) 10,453 10,919

Long-term debt, less current portion (Note 12) 3,764 –

Other non-current liabilities 5,264 6,008

Total liabilities 86,594 121,994

Commitments and contingencies (Note 17) – –

Shareholders' equity (Notes 3 and 16)

Common stock, no par or stated value; authorized 2,000,000 shares; issued 1,575,226 shares

Contributed capital 93,162 93,162

Retained earnings 10,131 31,380

Total shareholders' equity 103,293 124,542

Total liabilities and shareholders' equity $ 189,887 $ 246,536

The accompanying notes are an integral part of these consolidated financial statements.

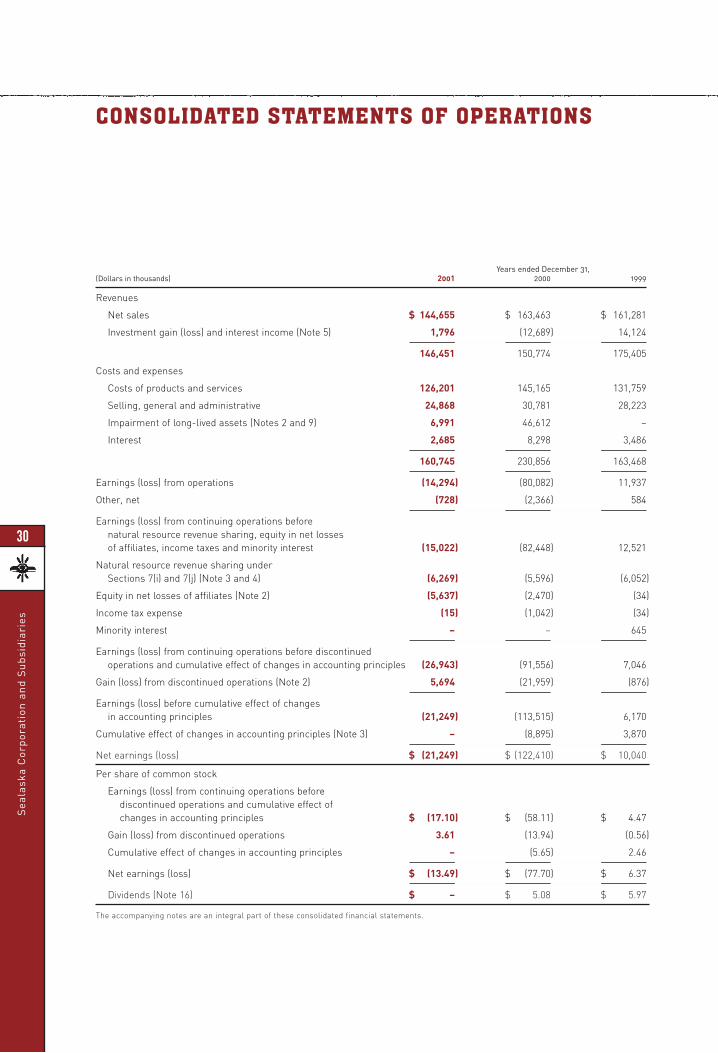

Years ended December 31,(Dollars in thousands) 2001 2000 1999

Revenues

Net sales $ 144,655 $ 163,463 $ 161,281

Investment gain (loss) and interest income (Note 5) 1,796 (12,689) 14,124

146,451 150,774 175,405

Costs and expenses

Costs of products and services 126,201 145,165 131,759

Selling, general and administrative 24,868 30,781 28,223

Impairment of long-lived assets (Notes 2 and 9) 6,991 46,612 –

Interest 2,685 8,298 3,486

160,745 230,856 163,468

Earnings (loss) from operations (14,294) (80,082) 11,937

Other, net (728) (2,366) 584

Earnings (loss) from continuing operations beforenatural resource revenue sharing, equity in net lossesof affiliates, income taxes and minority interest (15,022) (82,448) 12,521

Natural resource revenue sharing under Sections 7(i) and 7(j) (Note 3 and 4) (6,269) (5,596) (6,052)

Equity in net losses of affiliates (Note 2) (5,637) (2,470) (34)

Income tax expense (15) (1,042) (34)

Minority interest – – 645

Earnings (loss) from continuing operations before discontinued operations and cumulative effect of changes in accounting principles (26,943) (91,556) 7,046

Gain (loss) from discontinued operations (Note 2) 5,694 (21,959) (876)

Earnings (loss) before cumulative effect of changes in accounting principles (21,249) (113,515) 6,170

Cumulative effect of changes in accounting principles (Note 3) – (8,895) 3,870

Net earnings (loss) $ (21,249) $ (122,410) $ 10,040

Per share of common stock

Earnings (loss) from continuing operations before discontinued operations and cumulative effect of changes in accounting principles $ (17.10) $ (58.11) $ 4.47

Gain (loss) from discontinued operations 3.61 (13.94) (0.56)

Cumulative effect of changes in accounting principles – (5.65) 2.46

Net earnings (loss) $ (13.49) $ (77.70) $ 6.37

Dividends (Note 16) $ – $ 5.08 $ 5.97

The accompanying notes are an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF OPERATIONS

30

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

Accumulated other TotalContributed Retained comprehensive shareholders’

(Dollars in thousands) capital earnings income (loss) equity

Balance at January 1, 1999 $ 93,162 $ 161,163 $ (388) $ 253,937

Net earnings 10,040

Other comprehensive loss, net of taxForeign currency translation adjustment 237

Comprehensive income 10,277

Dividends to shareholders (9,408) (9,408)

Balance at December 31, 1999 93,162 161,795 (151) 254,806

Net loss (122,410)

Other comprehensive income, net of taxForeign currency translation adjustment 151

Comprehensive loss (122,259)

Dividends to shareholders (8,005) (8,005)

Balance at December 31, 2000 93,162 31,380 – 124,542

Net loss (21,249) (21,249)

Balance at December 31, 2001 $ 93,162 $ 10,131 $ – $ 103,293

The accompanying notes are an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

31

Years ended December 31,(Dollars in thousands) 2001 2000 1999

Cash flows from operating activities

Net earnings (loss) $ (21,249) $ (122,410) $ 10,040

Adjustments to reconcile net earnings (loss) tonet cash provided by (used in) operating activities

Cumulative effect of changes in accounting principles – 8,895 (3,870)

Depreciation, amortization and depletion 14,186 21,391 14,793

Impairment of long-lived assets 6,991 46,612 –

Non-cash (gain) loss from discontinued operations (6,600) 20,858 –

Unrealized loss (gain) on investments 4,713 25,364 (10,950)

Net proceeds from investments 15,239 133 2,457

Equity in net losses of affiliates 5,637 2,470 –

Deferred taxes – 1,184 (910)

Decrease (increase) in current assets

Receivables 14,144 467 (4,219)

Inventories 10,956 (5,336) (991)

Prepaid expenses and other current assets 642 221 (464)

Increase (decrease) in current liabilities

Accounts payable (8,733) (777) 6,094

Other accrued expenses (11,402) 3,954 281

Amounts payable under ANCSA Sections 7(i) and 7(j) 1,839 214 (1,678)

Other, net (687) 1,429 (1,527)

Net cash provided by operating activities $ 25,676 $ 4,669 $ 9,056

The accompanying notes are an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF CASH FLOWS

32

Sea

lask

a C

orpo

rati

on a

nd

Su

bsid

iari

es

Years ended December 31, (Dollars in thousands) 2001 2000 1999

Cash flows from investing activities

Capital expenditures $ (12,535) $ (22,144) $ (10,437)

Issuance of notes receivable (10,626) (4,074) –

Net cash used in investing activities (23,161) (26,218) (10,437)

Cash flows from financing activities

Change in book overdraft (1,658) 516 (287)

Dividends to shareholders – (8,005) (9,408)

Repayments of long-term debt (13,974) (30,267) (539)

Borrowings on long-term debt 4,000 34,103 4,243

Net cash used in financing activities (11,632) (3,653) (5,991)

Net decrease in cash and cash equivalents (9,117) (25,202) (7,372)

Cash and cash equivalents at beginning of year 12,059 37,261 44,633

Cash and cash equivalents at end of year $ 2,942 $ 12,059 $ 37,261

Supplemental disclosure of cash flow information

Cash paid during the year for interest $ 4,384 $ 4,683 $ 3,518

Cash paid during the year for income taxes $ 16 $ 648 $ 645

The accompanying notes are an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENTS OF CASH FLOWS

33

Note 1O P E R AT I O N S A N D S U M M A R Y O F

S I G N I F I C A N T A CCO U N T I N G P O L I C I E S

Operations

Sealaska Corporation (Sealaska or the Corporation)

is a regional Alaska Native Corporation formed

under the Alaska Native Claims Settlement Act

(ANCSA). Sealaska’s primary continuing business

activities relate to the development, production and

sale of natural resources, primarily timber, and the

management of its investment portfolio. ANCSA is

further described in Note 4.

At December 31, 2001, Sealaska also has a

wholly owned subsidiary, TriQuest Corporation

(TriQuest), which is a plastic injection-molding

manufacturer that has operations in Guadalajara

and Monterrey, Mexico and through a 50% owned

LLC, in Vancouver, Washington. As further described

in Note 2, in December 2001, Sealaska and its

LLC partner determined that the LLC would be

liquidated, and in January 2002, Sealaska sold

a 20% interest in the Guadalajara operation.

Sealaska also owns a mineral mining business in

Southeast Alaska, which is being closed down.

B A S I S O F P R E S E N TAT I O N

The consolidated financial statements include

the accounts of Sealaska and its wholly owned

subsidiaries. All significant intercompany

balances and transactions have been eliminated

in consolidation.

As described in Note 2, during 2000, the

Corporation adopted plans to divest of both its

plastic injection-molding and mineral mining

operations. Accordingly, both operations were

presented as discontinued operations in accordance

with Accounting Principles Board Opinion No. 30,

Reporting the Results of Operations – Reporting the

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Effects of Disposal of a Segment of a Business and

Extraordinary, Unusual and Infrequently Occurring

Events and Transactions (APB 30). During 2001,

Sealaska decided to retain a majority interest in its

plastic injection-molding operations in Guadalajara.

As a result, presentation of the plastic injection-

molding business as a discontinued operation

under APB 30 is no longer appropriate and the

accompanying 2000 and 1999 financial statements

have been reclassified to reflect it as a component

of continuing operations.

Revenue recognition

Sealaska owns and manages timber, timberlands

and mineral resources. Revenues from timber and

mineral resources are recognized when earned,

and the risks of ownership have been transferred

to the buyer, which is generally upon shipment

to the customer. Revenue from the sale of plastic

products is also recognized upon shipment to

the customer. Sealaska records shipping revenues

and costs in Net Sales and Costs of Products