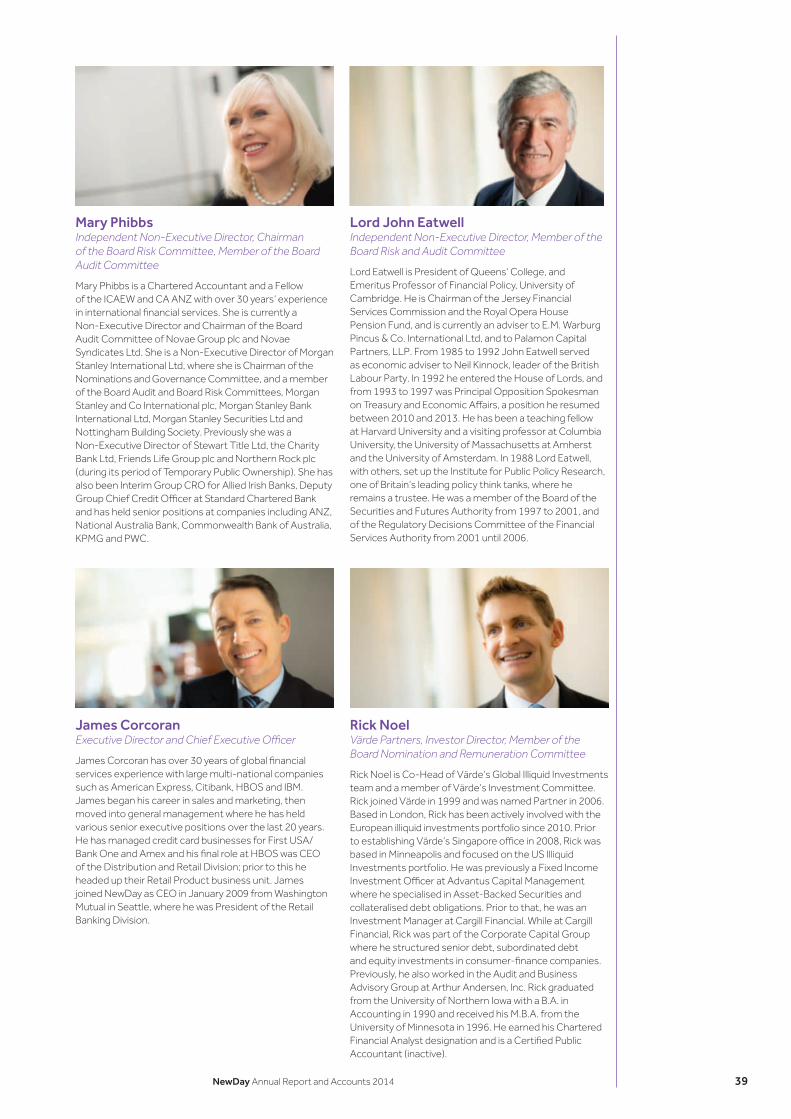

annual report and accounts 2014 - newday.co.uk · re-branded our company to newday, ... extensive...

TRANSCRIPT

Annual Report and Accounts 2014

Annual R

eport and A

ccounts 2014

NewDay Annual Report and Accounts 2014 1

Contents

Strategic report

Governance

Financials

OverviewOur history 2Business model 4Chairman’s statement 6

StrategyChief Executive Officer’s review 10People 14Social Responsibility 15

PerformanceKey performance indicators 18Financial review 20Risk management 26

Corporate governance 34Board of Directors 38Board Committee reports 40Executive and Governance Committees 47Management report 48Independent Auditor’s report 49

Consolidated statement of profit and loss and other comprehensive income

52

Consolidated statement of financial position 53Consolidated statement of changes in equity

54

Consolidated statement of cash flows 55Notes to the financial statements 56

Introduction

2014 was a year of significant transformation for our business. We successfully completed the migration of the Co-brand portfolio, re-branded our Company to NewDay, launched aqua start to further expand our Near-prime offers, and introduced a publicly issued Asset-Backed Securitisation programme to lower our cost of funding while delivering on our long-term diversified funding strategy.

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014 2015

We were founded in 2001 as SAV Credit, launching our fi rst credit card, aqua, in 2002. In 2014, we attracted circa 1 million new customers and now have a total customer base of 5.4 million.

SAV Credit founded

Sept 2001

Jan 2002Launched aqua credit card

Oct 2007marbles credit card portfolio acquired from HSBC

Jan 2009James Corcoran appointed CEO

June 2009Sir Malcolm Williamson appointed Chairman

March 2010Opus credit card portfolio acquired from Citibank

July 2011SAV Credit became an authorised payment institution

Nov 2011Värde Partners acquired SAV Credit

June 2012aqua advance and reward cards launched

May 2013Santander UK’s retail Co-brand card and point-of-sale fi nance business acquired

Our history

Growth built on solid foundations

2 NewDay Annual Report and Accounts 2014

2001 2003 2005 2007 2009 2010 2011 2012 2013 2014 2015

NewDay Cards Ltd

NewDay Group Ltd

100%

Structured entity1100%

100%

100%

NewDay Group

NewDay Group Holdings S.à r.l. is defined in these accounts as the “Company” and is the ultimate parent of the NewDay Group (the “Group”).

NewDay Group Holdings S.à r.l.

NewDay Partnership Transferor plc

NewDay Holdings Ltd

NewDay Ltd

100% 100%

NewDay Funding Reserve Ltd

NewDay Funding Transferor Ltd

Our structure

April 2014SAV Credit re-branded as NewDay

Nov 2014aqua start card launched

Dec 2014 – March 2015

May 2015

Co-brand portfolio securitisations

marbles re-launch

Sept 2014 Moved to new London headquarters

1. Subsequent to year end, NewDay Funding Transferor Ltd became a 100% owned entity of the Group.

NewDay Group Holdings S.à r.l.:The Luxembourg based parent company.

NewDay Partnership Transferor Plc:Holds the Co-brand segment.

NewDay Funding Transferor Ltd:Holds the Near-prime segment.

NewDay Group Ltd:Provides governance oversight in relation to the Group’s business.

NewDay Cards Ltd:Is the servicing company for the card business.

NewDay Ltd:Holds the regulatory licences which enable us to issue credit cards.

The Group is majority owned by Värde funds, managed by Värde Partners. Värde Partners is a $10 billion global alternative investment fi rm that employs a credit-oriented, value-based approach to investing across a broad array of geographies, segments and asset types, including real estate, corporate credit, residential mortgages, specialty fi nance, transportation and infrastructure. The fi rm provides the highest level of service to a select group of sophisticated global investors including foundations and endowments, pension plans, insurance companies, other institutional investors and private clients. Now in its third decade, Värde employs 200 people with main offi ces in Minneapolis, London and Singapore. Founded in 1993 by Marcia Page and George Hicks, the fi rm remains privately held and the founding partners continue as the key executives of the fi rm.

NewDay Annual Report and Accounts 2014 3

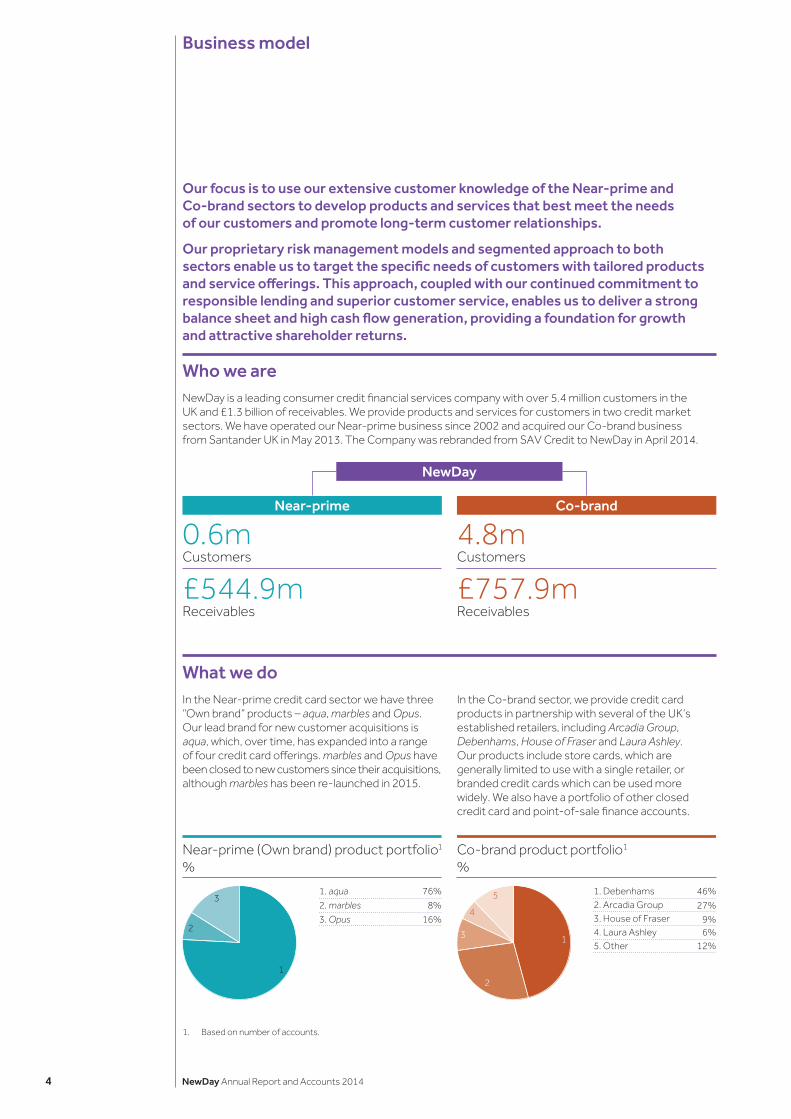

Business model

Our focus is to use our extensive customer knowledge of the Near-prime and Co-brand sectors to develop products and services that best meet the needs of our customers and promote long-term customer relationships.

Our proprietary risk management models and segmented approach to both sectors enable us to target the specific needs of customers with tailored products and service offerings. This approach, coupled with our continued commitment to responsible lending and superior customer service, enables us to deliver a strong balance sheet and high cash flow generation, providing a foundation for growth and attractive shareholder returns.

Who we areNewDay is a leading consumer credit financial services company with over 5.4 million customers in the UK and £1.3 billion of receivables. We provide products and services for customers in two credit market sectors. We have operated our Near-prime business since 2002 and acquired our Co-brand business from Santander UK in May 2013. The Company was rebranded from SAV Credit to NewDay in April 2014.

NewDay

0.6mCustomers

£544.9mReceivables

4.8mCustomers

£757.9mReceivables

Near-prime Co-brand

What we doIn the Near-prime credit card sector we have three “Own brand” products – aqua, marbles and Opus. Our lead brand for new customer acquisitions is aqua, which, over time, has expanded into a range of four credit card offerings. marbles and Opus have been closed to new customers since their acquisitions, although marbles has been re-launched in 2015.

In the Co-brand sector, we provide credit card products in partnership with several of the UK’s established retailers, including Arcadia Group, Debenhams, House of Fraser and Laura Ashley. Our products include store cards, which are generally limited to use with a single retailer, or branded credit cards which can be used more widely. We also have a portfolio of other closed credit card and point-of-sale finance accounts.

1

2

3

Near-prime (Own brand) product portfolio1

%

1. aqua 76%

2. marbles 8%

3. Opus 16%

1

2

3

4

5

Co-brand product portfolio1

%

1. Debenhams 46%2. Arcadia Group 27%3. House of Fraser4. Laura Ashley5. Other

9%6%

12%

1. Based on number of accounts.

4 NewDay Annual Report and Accounts 2014

How we do itWe design our products and service off erings based on in-depth knowledge of the needs of our customers. Extensive customer research and segmentation, coupled with our proprietary risk management models, enable us to develop product and service propositions that target the specifi c needs of our customers. Applying this customer insight and risk management approach promotes longer-term customer relationships and strong business growth.

Why we do itAccording to Experian data1, approximately 25% of UK credit card prospects are in the Near-prime sector. These customers are typically either new to credit or have a poor or limited credit history. Mainstream credit products are often unsuitable for such customers, who are seeking to establish or rebuild their credit history.

In the Co-brand sector, over 1 million new customers apply each year for our Co-brand products that off er rewards for loyalty to a particular brand. There has been a lack of traditional lenders in this sector who invest and develop products and services that are appropriately aligned to customers’ needs.

Our aim is to provide products and services that responsibly meet the needs of consumers in both sectors.

Our ManifestoWe want to establish long-term relationships with our customers. We believe that we will achieve this not only by providing products and services tailored to our customers’ needs, but also, as articulated in our Manifesto, by helping them make the most of their money by managing their fi nances better. This can include providing tools and support for customers to establish a positive credit record in our Near-prime portfolios and ensuring that brand loyalty is rewarded in our Co-brand portfolios (through our retailer relationships).

The Manifesto has the support of NewDay’s shareholders, Board and management, and is an important foundation of our business strategy.

We are a welcoming business

We are a rewarding business

We are a knowing business

We are an understanding

business

Customer insight

We will help people better manage their

money

Risk management

Productoff ering

Stronggrowth

1. Based on Experian Delphi for Mailing Scores between 595 and 760 on the UK Qualifi ed Audits in the Credit Card Market.

NewDay Annual Report and Accounts 2014 5

Chairman’s statement

I am pleased to present to you NewDay’s Annual Report and Accounts.

2014 was a year of significant transformation for our business. We successfully completed the migration of the Co-brand portfolio, launched aqua start to further expand our Near-prime offers, and introduced a publicly issued Asset-Backed Securitisation (ABS) programme to lower our cost of funding while delivering on our long-term diversified funding strategy. At the same time, we strengthened our Board and management team in line with the growing needs of the business, relocated to new headquarters in London and opened a new customer call centre in Leeds, onshored from India.

Our Manifesto, central to NewDay’s future success, will continue to play a key role as we move into the next phase of our growth. We believe it will become even more important in the ongoing development of our products and services and management of customers. In addition, our strong focus on responsible lending and our balanced approach to risk management will ensure that we continue to deliver positive outcomes for our customers and our business.

Performance overviewThe Group realised a total loss before tax of £13.1m for the year ended 31 December 2014. However, the Group realised a normalised profit before tax of £49.3m (2013: £51.6m), after adjusting for nonrecurring expenses such as the migration of the Co-brand business from Santander UK onto our operating platform and additional provisions made for Payment Protection Insurance (PPI). The decrease compared to 2013 was largely driven by increased costs as a result of the investment made to enhance our operational and servicing capabilities. We continue to maintain strong controls over our costs, including the governance of key investment programmes.

Our approach to responsible lendingOur credit-management expertise is well established, and we are continually developing our proprietary credit models to ensure we make informed decisions based on our customer knowledge. Customer creditworthiness and affordability criteria are essential components in the decision-making process that ensure we lend responsibly. Using this knowledge, we develop and provide tailored products, underpinned by strong customer service and support, to meet the needs of our customers. Responsible lending does not stop at the point of application; we believe that it continues throughout our relationships with customers.

Sir Malcolm WilliamsonChairman and Non-Executive Director

A year of transformation

For more information go to p.20

6 NewDay Annual Report and Accounts 2014

Continued commitment to governance, risk and internal controlsThe Board continues its commitment to strengthening its internal controls. During 2014, the Board approved the implementation of an enhanced risk governance model. In addition, an Enterprise Risk Function was established to ensure the delivery of effective risk oversight to the business.

2014 saw the transformation of the regulatory regime in the UK, as the Financial Conduct Authority (FCA) took over responsibility for the regulation of consumer credit from the Office of Fair Trading. The actions we have taken to further strengthen our corporate governance and transparent approach have put us in a strong position to meet the FCA’s new requirements and standards. Further discussion of the Group’s governance is provided on page 35.

Strengthening our leadershipI am proud of the leadership team at NewDay. It comprises a highly experienced and dedicated senior management who have detailed knowledge of the consumer credit finance industry. In 2014, we further strengthened the Board and management team to support the requirements of an expanding business and the delivery of our strategy for future growth. During the year, we appointed a new Chief Risk Officer, a Chief Commercial Officer, and a new independent Non-Executive Director. We are confident that we have the right mix of skill sets and experience to continue on our path of delivering strong growth and attractive shareholder returns.

A full list of Board biographies can be found on pages 38 and 39.

Future outlook2014 was a pivotal year for NewDay as we entered a new phase of growth, building upon the solid foundations established during 2013. We expect 2015 to be another significant year of development for the Group that will further advance our position as one of the UK’s major consumer credit finance companies.

I would like to take this opportunity to thank all of our people for their continuing hard work and dedication, and Värde Partners, our owners, for their constant support. Significant progress was made in 2014 and we look forward to realising further opportunities as we continue to embark on the delivery of our business strategy.

Sir Malcolm WilliamsonChairman and Non-Executive Director

For more information go to p.35

NewDay Annual Report and Accounts 2014 7

Our strategy allows us to meet responsibly the needs of our customers, creating long-term relationships with them that deliver strong growth for our business.

Our Co-brand products are integral to customers’ shopping experiences, strengthening their relationships with our partners by making them feel recognised and rewarded for their loyalty. Our Near-prime credit-building products support customers’ needs to establish or improve their credit histories, providing them with access to the flexibility and benefits that credit provides.

8 NewDay Annual Report and Accounts 2014

StrategyIn this sectionChief Executive Officer’s review 10• Strong performance in a year

of significant change10

• Enabling growth 11• Leveraging market growth 11• Changing regulatory regime 11• Our Manifesto 12• Outlook 12• Strategy 12People 14Social Responsibility 15

NewDay Annual Report and Accounts 2014 9

Chief Executive Officer’s review

Strong performance in a year of significant changeThis was a year of significant change for our business, which we faced head-on delivering a strong set of results. Growth in our aqua portfolio, driven by a record 234,000 new accounts, resulted in a year-end aqua receivables balance of £332.9m (2013: £180.2m). This was a significant contributor to our normalised profit before tax of £49.3m (2013: £51.6m). Robust credit risk management, a key focus area, resulted in impairment rates remaining stable across the Group at 6.0% (2013: 5.9%) despite the growth in our Near-prime business. This contributed to a strong risk adjusted margin (RAM) across the Group of 14.6% (2013: 14.8%). Encouragingly, risk adjusted incomes on our open book portfolios demonstrate solid growth. Near-prime and Co-brand open book RAM increased to 14.0% and 15.3% respectively (2013: 10.5% and 13.1% respectively).

Normalised return on equity was 12.4% in 2014 compared to 16.6% in 2013 driven by the reduction in normalised profit before tax referred to above. This was largely as a result of increased salaries, benefits and overheads of £15.6m reflecting the investment in our customer call centre. Gross receivables for the Group ended the year at £1,302.8m (2013: £1,348.0m) as the strong growth in our aqua portfolio offset the expected run-off on our closed portfolios.

We increased our provision for potential losses relating to PPI claims by £18.7m. We believe this adequately allows for potential future claims based on current market claim rates. Along with the significant investment in the cost base, principally relating to the integration of the Co-brand business acquired in May 2013 which is now complete, the PPI provision was the main driver of the £13.1m loss before tax for 2014.

We remain committed to enhancing the ongoing growth and performance of the Group. In 2014 we:

• launched the aqua start card to help customers at the start of their credit-building journey

• introduced visual DNA, a market-leading risk technique to further enhance our credit-scoring capabilities

• enhanced our digital capabilities through mobile-enabling all our web pages

• onshored our customer call centre in response to customer feedback

• further developed our strategy to leverage our offshore presence for back-office functions such as non-voice activities.

James CorcoranExecutive Director and Chief Executive Officer

Strong organic growth

For more information go to p.20

10 NewDay Annual Report and Accounts 2014

Enabling growthDuring 2014 we made significant headway in realising the ambitions of our growth strategy.

We successfully migrated the Santander UK Co-brand card and point-of-sale finance business, acquired in May 2013, onto our operating platform in August 2014. This migration was the culmination of a remarkable level of effort and determination across the business and its completion now allows us to focus on growing our Co-brand portfolio through continued collaboration with our current and potential retail partners.

In December 2014 we re-financed the Co-brand portfolio through an ABS programme, further demonstrating our ability to access diversified funding sources that support the continued robust growth of the business. This pivotal transaction further stabilised our strong capital base, lowered our reliance on the wholesale debt markets and reduced the overall funding cost of the business. These significant achievements have enhanced our ability to maintain growth and attractive shareholder returns from the Co-brand portfolio, one of our core strategic priorities.

In addition we re-branded the Company to NewDay in April and moved into our new headquarters in London’s King’s Cross in September.

Leveraging market growthWith improved consumer confidence, unsecured borrowing in the UK grew by £20bn in 2014. This was an increase of almost 9% compared to 2013 and the largest percentage rise in more than a decade1.

The Co-brand card market has experienced significant growth and our research demonstrates that it accounts for circa £5.5bn of the £60bn card market. We continue to enhance our proposition in the Co-brand sector, accessing a broader customer base through partnerships with established UK retailers and meeting customer needs with customer-tailored products and services.

Changing regulatory regimeThe regulatory environment has undergone significant change in recent years, most notably with the establishment of the FCA as the regulator of consumer credit, replacing the Office of Fair Trading. The new regulatory regime has had a strong impact on the financial services industry, one that is expected to continue. Indeed, it is anticipated that many consumer credit companies will choose to exit the market, while others will fail to attain full FCA authorisation.

At the end of 2014, the FCA commenced its Credit Card Market Study, focused on investigating effective competition, how and where firms make money and sources of customer detriment within the consumer finance market. In addition, firms’ cultural and conduct arrangements, including how they support the needs of vulnerable and high-risk customers, will be scrutinised. This study may result in further changes to consumer credit regulation and potentially to company-specific requirements.

We believe that we are well positioned to respond to this increased level of regulatory scrutiny. Our application for full FCA authorisation (which was submitted on 2 April 2015) coincides with the Credit Card Market Study, to which we have provided full information and support. Several factors contribute to us being well placed to operate successfully in this new regulatory environment, including our internal governance framework enabling compliance with all regulatory principles and codes, our commitment to communicating openly with customers, our control and risk management systems, our clear and transparent engagement with regulators and our underlying customer focus driven by our Manifesto.

1. Based on the PwC report: How Britons fell back in love with borrowing.

NewDay Annual Report and Accounts 2014 11

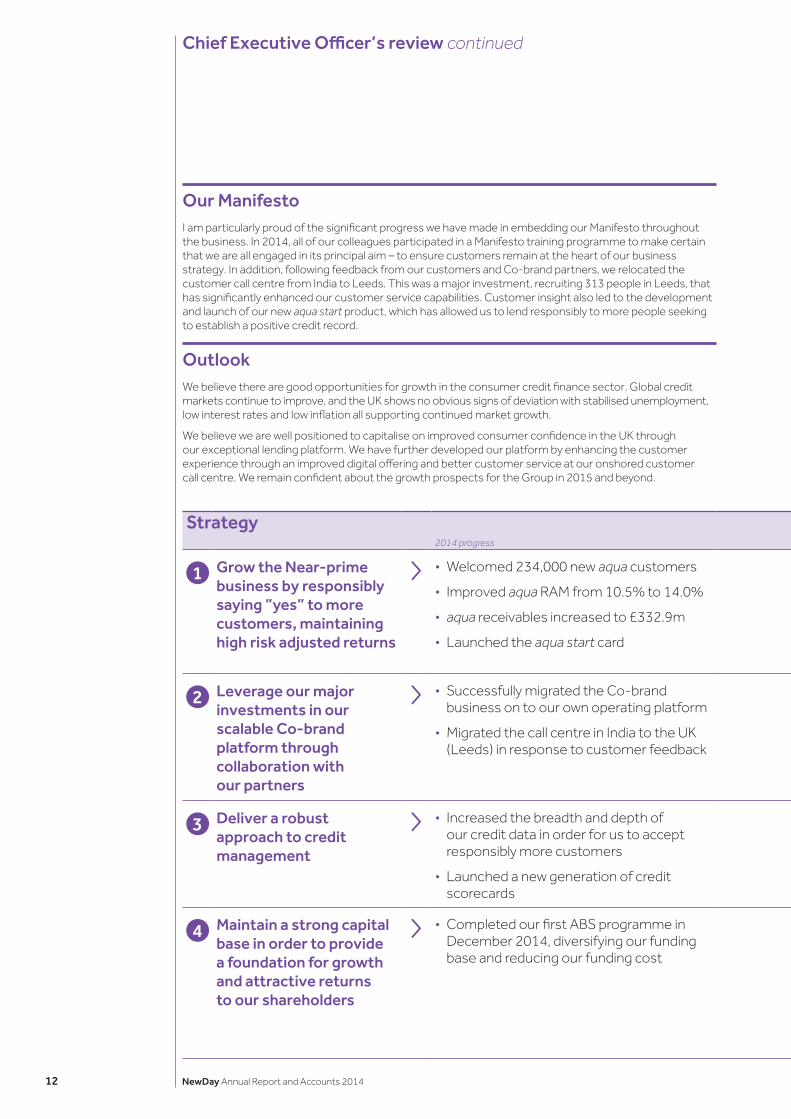

Strategy2014 progress 2014 performance Future goals

1 Grow the Near-prime business by responsibly saying ”yes” to more customers, maintaining high risk adjusted returns

• Welcomed 234,000 new aqua customers

• Improved aqua RAM from 10.5% to 14.0%

• aqua receivables increased to £332.9m

• Launched the aqua start card

aqua receivables

£332.9m(2013: £180.2m)

• Continue strong organic growth in the Near-prime portfolios through aqua account origination and the re-launch of the marbles brand

• Reach more borrowers through an enhanced digital distribution capability

2 Leverage our major investments in our scalable Co-brand platform through collaboration with our partners

• Successfully migrated the Co-brand business on to our own operating platform

• Migrated the call centre in India to the UK (Leeds) in response to customer feedback

Normalised cost-to-income ratio

51.6%(2013: 45.3%)

• Continue to drive efficiency savings in the cost base through: - automation of manual processes - enablement of customer self-service through digital solutions - enhancing our digital capability

3 Deliver a robust approach to credit management

• Increased the breadth and depth of our credit data in order for us to accept responsibly more customers

• Launched a new generation of credit scorecards

Impairment rate

6.0%(2013: 5.9%)

• Continue to improve our expert credit capabilities by leveraging richer data and adopting new techniques such as Visual DNA

4 Maintain a strong capital base in order to provide a foundation for growth and attractive returns to our shareholders

• Completed our first ABS programme in December 2014, diversifying our funding base and reducing our funding cost

Normalised return on equity

12.4%(2013: 16.6%)

• Continue to optimise the capital structure through the second issue from our Co-brand ABS programme and the launch of the Own brand ABS programme

• Enhance profitability through continued receivables growth and leveraging the investment made in the Co-brand cost base in 2014

Chief Executive Officer’s review continued

Our ManifestoI am particularly proud of the significant progress we have made in embedding our Manifesto throughout the business. In 2014, all of our colleagues participated in a Manifesto training programme to make certain that we are all engaged in its principal aim – to ensure customers remain at the heart of our business strategy. In addition, following feedback from our customers and Co-brand partners, we relocated the customer call centre from India to Leeds. This was a major investment, recruiting 313 people in Leeds, that has significantly enhanced our customer service capabilities. Customer insight also led to the development and launch of our new aqua start product, which has allowed us to lend responsibly to more people seeking to establish a positive credit record.

OutlookWe believe there are good opportunities for growth in the consumer credit finance sector. Global credit markets continue to improve, and the UK shows no obvious signs of deviation with stabilised unemployment, low interest rates and low inflation all supporting continued market growth.

We believe we are well positioned to capitalise on improved consumer confidence in the UK through our exceptional lending platform. We have further developed our platform by enhancing the customer experience through an improved digital offering and better customer service at our onshored customer call centre. We remain confident about the growth prospects for the Group in 2015 and beyond.

12 NewDay Annual Report and Accounts 2014

We firmly believe that our expert credit management capabilities, developed over the last 14 years of operating in the Near-prime space, and our significant investments in our scalable Co-brand platform, place us in a strong position to withstand any competitive pressure and to develop and grow the business successfully.

After a period of significant transformation in 2014, we remain optimistic about the year ahead. With a clear business strategy, a strong financial base and a highly experienced Board and management team, we believe we have the foundations in place and the momentum within the business to achieve our future growth ambitions.

James CorcoranExecutive Director and Chief Executive Officer

Strategy2014 progress 2014 performance Future goals

1 Grow the Near-prime business by responsibly saying ”yes” to more customers, maintaining high risk adjusted returns

• Welcomed 234,000 new aqua customers

• Improved aqua RAM from 10.5% to 14.0%

• aqua receivables increased to £332.9m

• Launched the aqua start card

aqua receivables

£332.9m(2013: £180.2m)

• Continue strong organic growth in the Near-prime portfolios through aqua account origination and the re-launch of the marbles brand

• Reach more borrowers through an enhanced digital distribution capability

2 Leverage our major investments in our scalable Co-brand platform through collaboration with our partners

• Successfully migrated the Co-brand business on to our own operating platform

• Migrated the call centre in India to the UK (Leeds) in response to customer feedback

Normalised cost-to-income ratio

51.6%(2013: 45.3%)

• Continue to drive efficiency savings in the cost base through: - automation of manual processes - enablement of customer self-service through digital solutions - enhancing our digital capability

3 Deliver a robust approach to credit management

• Increased the breadth and depth of our credit data in order for us to accept responsibly more customers

• Launched a new generation of credit scorecards

Impairment rate

6.0%(2013: 5.9%)

• Continue to improve our expert credit capabilities by leveraging richer data and adopting new techniques such as Visual DNA

4 Maintain a strong capital base in order to provide a foundation for growth and attractive returns to our shareholders

• Completed our first ABS programme in December 2014, diversifying our funding base and reducing our funding cost

Normalised return on equity

12.4%(2013: 16.6%)

• Continue to optimise the capital structure through the second issue from our Co-brand ABS programme and the launch of the Own brand ABS programme

• Enhance profitability through continued receivables growth and leveraging the investment made in the Co-brand cost base in 2014

KPI

KPI

KPI

NewDay Annual Report and Accounts 2014 13

People

Our success at NewDay is driven by our strategy to attract, engage and retain the best talent to drive a successful and customer-focused organisation. Our people proposition, based on our Values, supports the aims of our Manifesto – to be a Welcoming, Understanding, Knowing and Rewarding business.

Developing talentWe continue to enhance our recruitment and induction programmes for new colleagues to ensure that people have a welcoming experience from the moment they engage with us. We are committed to identifying and recruiting people with the skills required to support our growing business. We are also focused on creating a comprehensive learning and development strategy for all of our colleagues.

Colleague engagementWe track our colleague engagement through an annual Pulse Survey and despite a year of significant transformation in 2014, we achieved an Engagement Index Score of 71%, exceeding the market norm of 64%. We communicate and act on the results, working with our colleagues in local teams and on business-wide priorities to explore and address any issues and identify opportunities for improvement.

Empowering colleaguesAs a result of feedback from our colleagues, we are introducing more informal opportunities for people to recognise each other’s achievements. We have launched ASPIRE, a new career pathway and reward structure for our contact centre colleagues.

We have also appointed ”Manifesto Champions” from across the business to empower colleagues to develop and lead initiatives that further embed the aims of our Manifesto. In addition, we have developed an on-line internal community discussion and feedback forum to facilitate greater collaboration and knowledge-sharing across NewDay.

Performance managementRewarding and motivating our people is important to us. We benchmark our compensation with other companies in the financial services market to ensure that we remain competitive. In 2014, we enhanced our rewards package to include a new bonus structure, a defined contribution pension plan, private medical insurance, life assurance, income protection and an Employee Assistance Programme.

We are assessed on the achievement of our corporate goals and reward our people through an incentive scheme which is based on the Company’s overall team goals and also recognises in equal measure the achievement of individual business deliverables and commitment to our Values and Manifesto. Consequently, all of our colleagues benefit from working together to deliver a strong company performance.

Engage and retain

Our Values

14 NewDay Annual Report and Accounts 2014

Building our organisation in a transitional yearThe scale of the people challenge in this transformational year for the business cannot be underestimated. We increased headcount from 95 in 2013 to 809 in 2014, which included 420 colleagues transitioned from Santander UK and 313 new hires in our new Leeds-based customer call centre. In addition, we relocated our headquarters from Kings Hill, Kent to our new office space in London’s King’s Cross, facilitating a seamless transition for all colleagues.

Colleagues from Santander UK were transferred in August under the Transfer of Undertakings (Protection of Employment) Regulations. We introduced a new set of core people policies, processes and systems and upgraded our performance management systems. Additionally,

prior to the migration of colleagues from Santander UK, we created our people proposition and designed and implemented a new reward programme to attract and retain key talent.

To help embed our Values and ensure that all new colleagues were engaged during a period of such rapid change, we introduced a robust internal communications programme. This included regular Town Hall meetings, Manifesto training and the launch of a new intranet site, The Hub.

With a defined people proposition now in place, we have established the foundations to support our growth strategy. Our focus is to further enhance our proposition and establish our employer brand in order to drive our colleague engagement.

Embracing diversityWe operate an equal opportunities policy and oppose all forms of unlawful discrimination on the grounds of gender, marital status, sexual orientation, disability, race, creed, colour, nationality, religion, age or any other personal characteristics. We are committed to encouraging the recruitment, training, career development and promotion of disabled persons having regard to their particular aptitudes and abilities, and to retain and retrain colleagues who become disabled whilst in our employment.

NewDay’s selection criteria and procedures ensure that individuals are treated on the basis of their abilities so that all colleagues are given an equal opportunity to progress within the business. We encourage gender diversity across all levels of the business.

Our 2015 prioritiesOur priority in 2015 is to continue to develop our people proposition and to continue to invest in the needs of our growing business. From welcoming new talent, to promoting an open and transparent culture and rewarding our people for their achievements, we are committed to ensuring that NewDay remains a great place to work.

Social ResponsibilityOur social purposeTo date, NewDay’s principal social purpose is to enable our Near-prime customers, who historically have been underserved by the mainstream lenders, to access appropriate credit products that allow them to better manage their finances and establish a positive credit record. We do this by utilising our extensive customer knowledge that enables us to offer our customers appropriate amounts of credit, to work with our customers through subsequent changes in their circumstances to ensure our products and services are appropriate for their needs, and to promote long-term relationships with our customers.

With our new office sites in Leeds and London, we are now looking forward to working with the local communities in these areas.

Environmental impactWe recognise that we have a duty to minimise our impact on the environment. We encourage electronic rather than paper-based communication and we have significantly reduced the environmental impact of our day-to-day operation through the move to our new ultra environmentally friendly head office in London. The new development at King’s Cross is one of the most environmentally friendly in the capital through the use of the very latest technology and renewable energy sources. The Building Research Establishment Environmental Assessment Method (BREEAM), which is the world’s most widely used environmental assessment method, rates it “Outstanding”.

Transparency in reportingNewDay’s Annual Report and Accounts comply with all aspects of the Guidelines for Disclosure and Transparency in Private Equity, established to provide oversight on disclosure issues related to reporting by entities held by private equity companies, specifically adequate disclosures and transparency.

NewDay Annual Report and Accounts 2014 15

16 NewDay Annual Report and Accounts 2014

Perform

ance

In this sectionKey performance indicators 18Financial review 20Risk management 26

NewDay Annual Report and Accounts 2014 17

Key performance indicators

Risk adjusted income/Average gross receivables

Normalised costs/ Net interest income and fees

Risk adjusted income – Normalised costs

Normalised profit before tax/Average gross receivables

The Group’s RAM marginally decreased to 14.6%. This was principally due to a fall in the Group’s interest yield which decreased to 20.8% reflecting, in part, the full-year impact of the point-of-sale portfolios acquired from Santander UK, an element of which is non-interest bearing.

The 2014 cost-to-income ratio of 51.6% increased from 45.3% in 2013 with higher income for the Group more than offset by an increase in the normalised cost base as we transformed the business by setting up our Leeds-based customer call centre with a 313-strong customer service team and welcomed 420 former Santander UK employees following the 2013 acquisition. This investment in our operational capabilities was an essential part of our transformation. Following this investment, we expect to see the cost-to-income ratio decline as a consequence of efficiency measures and scale.

Normalised profit before tax decreased to £49.3m from £51.6m, with a significant increase in Near-prime profitability through organic growth and consistent credit performance offset by the increase in normalised costs as we transformed our operating model to support future growth in the business.

Return on assets decreased to 3.9% from 5.4% with the higher contribution of aqua to the Group’s results and consistent credit performance offset by the impact of the non-interest bearing portion of the closed portfolios in the Co-brand sector and the additional costs incurred following the completion of the Co-brand migration and investment in our operational capabilities.

Performance

Definition

Metric

Explanation

14.6% 51.6% £49.3m 3.9%

201420132012

Risk adjusted margin (RAM) %

10.7 14.8 14.6

201420132012

Normalised cost-to-income ratio %

47.6 45.3 51.6

201420132012

Normalised profit before tax £m

15.0 51.6 49.3

201420132012

Normalised return on assets %

3.0 5.4 3.9

18 NewDay Annual Report and Accounts 2014

Normalised profit after tax/Average equity

Total impairments/Average gross receivables

Net debt/Closing equity Customer balances

Normalised return on equity was 12.4% in 2014 (2013: 16.6%). The primary reasons for the decrease were the higher average equity base for the Group (£245.8m to £313.5m) together with increased costs following the completion of the Co-brand migration, set-up of a customer call centre, and the increased costs associated with building our operational capabilities.

The overall Group impairment rate remained consistent at 6.0% compared to 5.9% in the prior year notwithstanding the change in business mix towards Near-prime. This reflects our continued focus on credit-risk management, the improved economic fundamentals in the UK and the increasing maturity of the books.

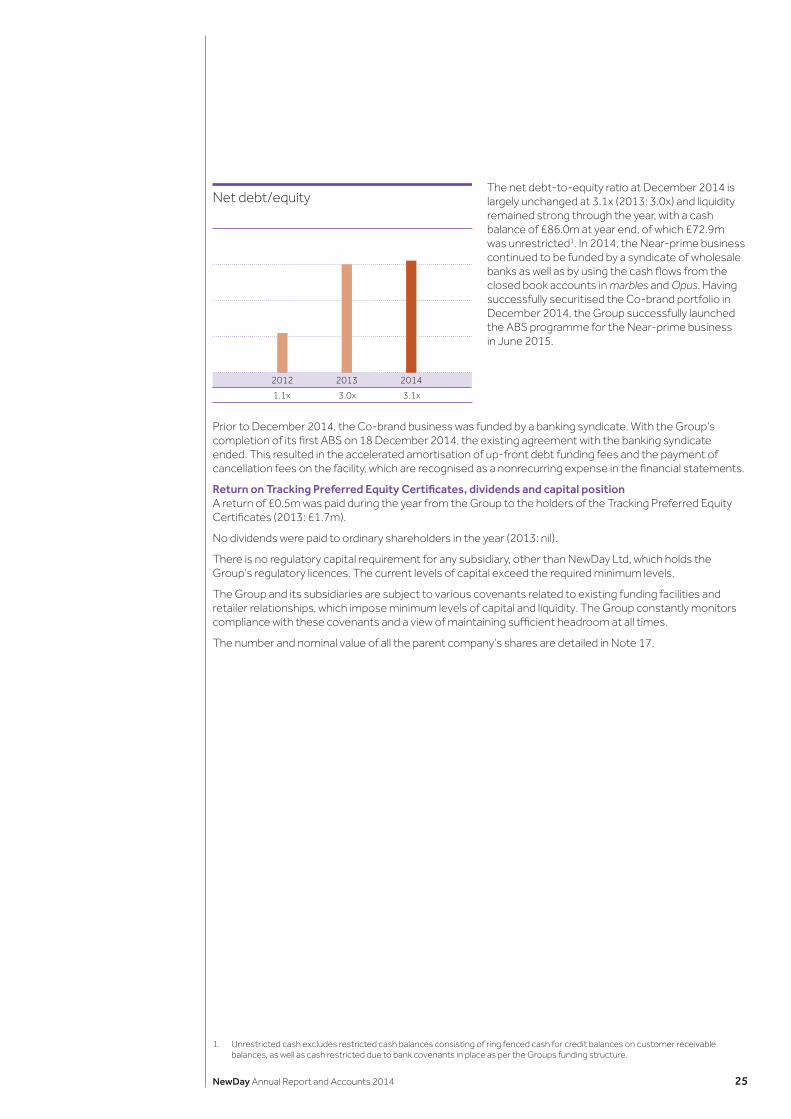

The increase in the net debt-to-equity ratio from 3.0x at the start of the year to 3.1x in December 2014 was mainly driven by the increase in overall leverage as a result of the Co-brand ABS programme which was launched in December 2014.

Group receivables decreased to £1,302.8m (2013: £1,348.0m) as growth in the open books was offset by run-off on the closed portfolios. Open book receivables increased by 16% to £970.4m (2013: £835.8m) and now comprise 74.5% of total Group receivables (2013: 62.0%).

12.4% 6.0% 3.1x £1,302.8m

201420132012

Normalised returnon equity %

6.8 16.6 12.4

201420132012

Impairment rate %

5.5 5.9 6.0

201420132012

Net debt/equity

1.1x 3.0x 3.1x

201420132012

Closing receivables£m

421.8 1,348.0 1,302.8

NewDay Annual Report and Accounts 2014 19

Financial review

OverviewFor the year ended 31 December 2014, the Group recorded a total loss before tax of £13.1m (2013: profit of £116.9m). The presentation of normalised profit before tax has been revised to exclude large one-off costs previously included in normalised costs; these are now treated as nonrecurring expenses. The 2012 and 2013 comparatives for normalised profit before tax have been restated accordingly to £15.0m for 2012 and £51.6m for 2013 (previously £25.6m and £48.5m respectively). This restatement is to ensure comparability with the 2014 normalised profit before tax.

Risk adjusted income now excludes cost recovery fees as these are presented as a component of servicing costs on the basis that they represent recoveries against these costs. The risk adjusted margins for 2012 and 2013 have been restated to exclude the impact of cost recovery fees. To ensure consistency, the normalised cost income ratios for 2012 and 2013 have been restated to treat cost recovery fees as a component of costs rather than income. In arriving at a normalised profit before tax of £49.3m, the following exceptional or nonrecurring items have been excluded:

£m2014

£m2013

£m Reference

Total (loss)/profit before tax (13.1) 116.9Purchase accounting and fair value unwind (24.0) (107.6) Notes 3,4Fair value losses/(gains) on derivatives 5.1 (4.9)Large one-off costs 16.5 5.8Co-brand migration costs 32.1 13.2Movement in provisions (excluding impairment losses on loans and advances to customers) 17.5 11.3 Note 7Co-brand acquisition costs 11.0Exceptional debt funding fees 13.0Other nonrecurring items 2.2 5.9Normalised profit before tax 49.3 51.6

Purchase accounting and fair value unwind reflect the amortisation of a fair value adjustment on the Group’s acquired portfolios.

Large one-off items include the transactional costs associated with the launch of the ABS programme, the costs relating to our new London and Leeds offices and the cost of rebranding the Group to NewDay.

The Co-brand migration costs principally reflect the one-off cost of migrating the acquired Co-brand business on to NewDay’s own platform. The migration programme was successfully completed on time in August 2014 and we do not expect to incur any significant additional costs in relation to the migration.

Provisions for PPI mis-selling claims were further increased due to higher claim volumes than initially expected and regulatory guidance.

Exceptional debt funding fees relate to the accelerated amortisation of up-front debt funding fees and the cancellation fees incurred upon the refinancing of the Co-brand business in December 2014.

Highlights

• Normalised profit before tax of £49.3m (2013: £51.6m)

• Normalised ROE of 12.4% (2013: 16.6%)

• Normalised cost-to-income ratio of 51.6% (2013: 45.3%)

• Successful migration of the Co-brand business

• Launched our first public ABS programme

20 NewDay Annual Report and Accounts 2014

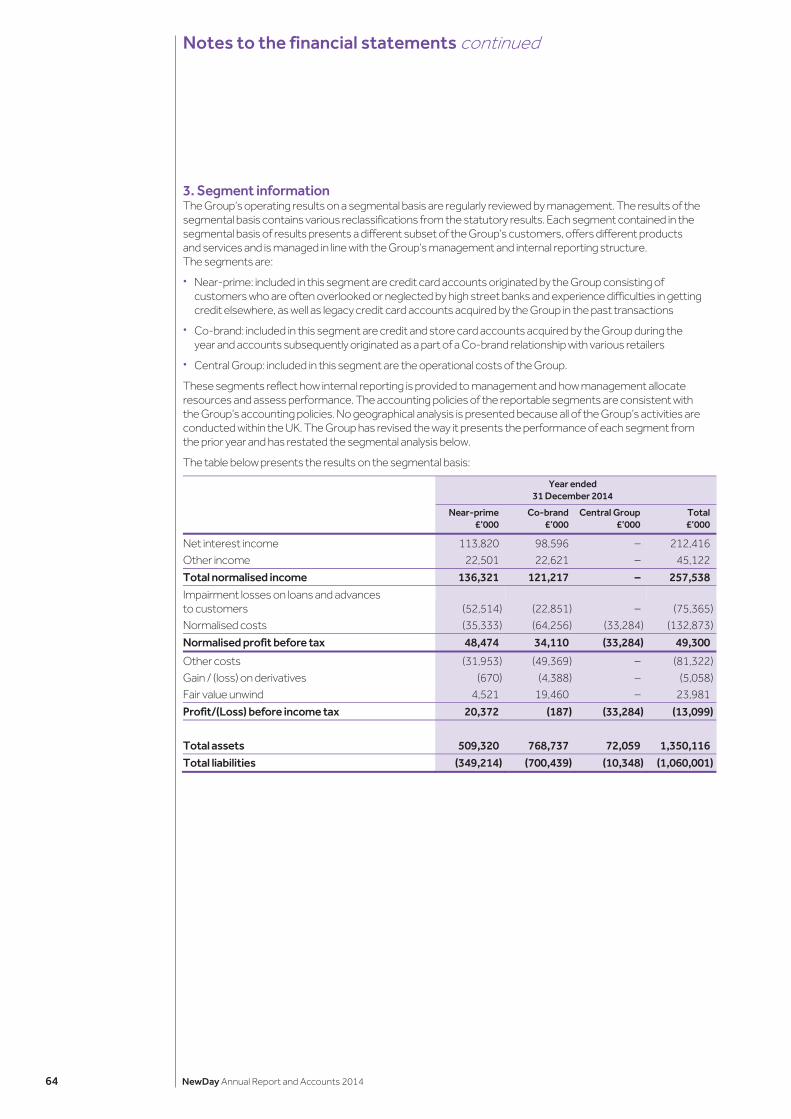

Segment performance

201420132012

Group receivables (books)£m

324.497.4Open books

512.2835.8

332.4970.4

Closed books

£m 2014 2013

Management basis income statement Near-prime Co-brand Group Near-prime Co-brand Group

Interest income 129.7 130.4 260.1 109.8 91.5 201.3Cost of funds (15.9) (31.8) (47.7) (14.5) (21.1) (35.6)Net interest income 113.8 98.6 212.4 95.3 70.4 165.7Fee income 22.5 22.6 45.1 15.4 15.3 30.7Total income 136.3 121.2 257.5 110.7 85.7 196.4Total impairment (52.5) (22.9) (75.4) (38.4) (17.4) (55.8)Risk adjusted income 83.8 98.3 182.1 72.3 68.3 140.6Servicing costs (14.8) (24.6) (39.4) (14.4) (10.5) (24.9)Investment costs (16.7) (35.4) (52.1) (15.5) (25.7) (41.2)Normalised contribution 52.3 38.3 90.6 42.4 32.1 74.5Salaries, benefits and overheads (33.3) (17.7)Debt funding fees (8.0) (5.2)Normalised profit before tax 49.3 51.6Other costs (81.3) (47.0)(Losses)/gains on derivatives (5.1) 4.9Fair value unwind 24.0 107.6(Loss)/profit before tax (13.1) 116.9Tax (0.5) (0.1)(Loss)/profit after tax (13.6) 116.8

KPIs Near-prime Co-brand Group Near-prime Co-brand Group

Average receivables £468.7m £779.9m £1,248.6m £410.9m £538.9m £949.8mNew accounts (’000) 234 746 980 190 557 747Average equity £313.5m £245.8m

Risk adjusted margin 17.9% 12.6% 14.6% 17.6% 12.7% 14.8%Impairment rate 11.2% 2.9% 6.0% 9.3% 3.2% 5.9%Cost-to-income ratio 51.6% 45.3%Normalised return on assets 3.9% 5.4%Normalised return on equity 12.4% 16.6%Year-end headcount 809 95

In preparing the management basis income statement, cost recoveries have been presented as a component of servicing costs rather than as income. Additionally, receivables disclosed in this section are gross receivables (customer balances excluding any impairment provision). Average receivables and average equity are based on the monthly average over the year. As a result, the 2013 comparatives, including KPIs presented, have been restated to ensure comparability with the 2014 information.

201420132012

Group receivables (sectors)£m

N/A421.8Near-prime

917.9430.1

757.9544.9

Co-brand

For more information go to p.18

NewDay Annual Report and Accounts 2014 21

Financial review continued

Near-prime (Own brand)

201420132012

Near-prime receivables£m

324.497.4aqua

249.9180.2

212.0332.9

Closed books

The Near-prime gross receivables balance increased by 26.7% to £544.9m at year end (2013: £430.1m). This substantial increase was driven by growth in the number of aqua customers, with 234,000 new accounts originated during the year, bringing the total outstanding gross receivables in the open book portion of the Near-prime segment to £332.9m at year end, an 84.7% increase over 2013. The closed book balances continued to run off in line with expectations, with £212.0m (2013: £249.9m) in gross receivables outstanding at the year end.

aqua’s growing contribution to the performance of the Near-prime segment was the main driver behind the segment’s increase in risk adjusted income for the year to £83.8m (2013: £72.3m), with aqua now accounting for 40.1% of the total (2013: 19.1%). In line with expectations, the closed books, comprising the acquired marbles and Opus portfolios, continue to run off profitably with risk adjusted income generated by this segment for the year totalling £50.2m (2013: £58.5m).

Improvement in the Near-prime segment’s risk adjusted margin for the year to 17.9% (2013: 17.6%) was predominantly as a result of aqua’s margin expansion as the income yield (interest and fee yield) increased to 29.1% (2013: 26.9%) partly offset by the impact of the impairment rate increasing to 11.2% (2013: 9.3%).

The credit performance is closely monitored for each product within the Near-prime segment. As a result of improvements in the overall credit-risk management, the charge-off rate, which excludes the impact of movements in impairment provisions, recoveries and fraud, continues to drop, with 12.6% of customer balances charging off during the year, compared to 14.4% for 2013.

In 2014, our customer research highlighted further potential customer needs in the Near-prime market segment. As a result, we re-launched the marbles brand in 2015 to complement our existing range of aqua credit cards and strengthen our Near-prime proposition.

201420132012

Near-prime risk adjusted income£m

44.68.8aqua

58.513.8

50.233.6

Closed

22 NewDay Annual Report and Accounts 2014

Co-brand

20142013

Co-brand receivables£m

262.4655.5Open

120.4637.5

Closed

Co-brand gross receivables decreased by 17.4% to £757.9m (2013: £917.9m) during 2014, principally due to run-off on the closed portfolios. Open book receivables fell to £637.5m (2013: £655.5m) as customer spend decreased for part of the year before resuming growth towards the end of 2014. In addition, customer repayments were higher than anticipated, further contributing to the overall decrease in receivables balances.

Open book risk adjusted income increased significantly during the year to £91.2m (2013: £49.4m), representing 93% of the year’s £98.3m total for the Co-brand segment (2013: £68.3m). This considerable improvement reflects the first full year of NewDay’s ownership post-acquisition in 2013 and our ability to implement our strategies, policies and Risk Management Framework.

The marginal decrease in overall risk adjusted margin for the year to 12.6% (2013: 12.7%) was primarily driven by a decrease in the income yield to 15.5% (2013: 15.9%). This fall is primarily due to the full-year post-acquisition impact of a number of point-of-sale finance portfolios acquired from Santander UK which are non-interest bearing and thereby reduced the overall Co-brand risk adjusted margin. The impairment rate remained stable at 2.9% (2013: 3.2%).

The credit performance in the Co-brand segment remains strong, with robust credit-risk management reducing the charge-off rate for the year to 5.0% (2013: 6.3%). As with the Near-prime business, the charge-off rate excludes the impact of movements in impairment provisions, recoveries and fraud.

With the successful migration of the acquired business onto our own platform, we are well positioned to benefit from increased retail activity as the UK economy continues to improve.

20142013

Co-brand risk adjusted income£m

18.949.4Open

7.291.2

Closed

NewDay Annual Report and Accounts 2014 23

Financial review continued

Investment in our platform

201420132012

Normalised cost-to-income ratio%

47.6 45.3 51.6

We made significant progress in transforming our target operating model in 2014. As part of the transition to becoming a much larger business we brought on board 420 former Santander UK employees and established a customer call centre in Leeds with 313 new staff, increasing our headcount to 809 for 2014 (2013: 95). This investment in our future operational capabilities has driven an increase in the normalised cost-to-income ratio to 51.6% (2013: 45.3%). However, the Group now has a scalable platform to accommodate further growth in our Co-brand business with our existing and potential new retail partners. As a result, we expect to see a material reduction in the cost-to-income ratio over time.

The Group is in the early stages of a multi-year comprehensive growth plan which involves a number of key initiatives and programmes. We have completed the first stage through building a new infrastructure and operating model. The focus now is on strategic actions to lay the foundation for the growth of the aqua and Co-brand portfolios. The aim for 2015 and beyond is to deliver incremental financial benefits by leveraging our operating platform.

Supporting growth via a diversified funding strategyWe made significant headway in delivering our long-term diversified funding strategy in 2014, with the launch of our publicly issued ABS programme for the Co-brand business. As a result, we issued £652m of Asset-Backed Securities and raised sufficient debt financing to fund the Co-brand business for the next three years at projected receivable balances.

Along with a second issue of five-year bonds completed in March 2015, this re-financing has significantly lowered our funding cost and reduced our re-financing risk through a staggered maturity profile.

2014

2013

Funding mix%

Bank facilities

Asset-backed securities

67%

33%

100%

24 NewDay Annual Report and Accounts 2014

201420132012

Net debt/equity

1.1x 3.0x 3.1x

The net debt-to-equity ratio at December 2014 is largely unchanged at 3.1x (2013: 3.0x) and liquidity remained strong through the year, with a cash balance of £86.0m at year end, of which £72.9m was unrestricted1. In 2014, the Near-prime business continued to be funded by a syndicate of wholesale banks as well as by using the cash flows from the closed book accounts in marbles and Opus. Having successfully securitised the Co-brand portfolio in December 2014, the Group successfully launched the ABS programme for the Near-prime business in June 2015.

Prior to December 2014, the Co-brand business was funded by a banking syndicate. With the Group’s completion of its first ABS on 18 December 2014, the existing agreement with the banking syndicate ended. This resulted in the accelerated amortisation of up-front debt funding fees and the payment of cancellation fees on the facility, which are recognised as a nonrecurring expense in the financial statements.

Return on Tracking Preferred Equity Certificates, dividends and capital positionA return of £0.5m was paid during the year from the Group to the holders of the Tracking Preferred Equity Certificates (2013: £1.7m).

No dividends were paid to ordinary shareholders in the year (2013: nil).

There is no regulatory capital requirement for any subsidiary, other than NewDay Ltd, which holds the Group’s regulatory licences. The current levels of capital exceed the required minimum levels.

The Group and its subsidiaries are subject to various covenants related to existing funding facilities and retailer relationships, which impose minimum levels of capital and liquidity. The Group constantly monitors compliance with these covenants and a view of maintaining sufficient headroom at all times.

The number and nominal value of all the parent company’s shares are detailed in Note 17.

1. Unrestricted cash excludes restricted cash balances consisting of ring fenced cash for credit balances on customer receivable balances, as well as cash restricted due to bank covenants in place as per the Groups funding structure.

NewDay Annual Report and Accounts 2014 25

Risk management

In a year of significant change in the business, the Board prioritised the enhancement of our corporate governance and Risk Management Framework, with emphasis on oversight, challenge and control. This framework seeks to ensure that we strike a balance between business strategy implementation, our risk appetite and strong business performance. In addition to the recruitment of a Chief Risk Officer in 2014, an Enterprise Risk Function was established to support the business in delivering effective risk oversight, and development and implementation of the Risk Management Framework continues.

Good progress has been made, building on our expertise in credit risk, to further develop our proprietary credit models to ensure we make informed decisions based on our customer knowledge in order that we lend responsibly and treat our customers fairly. In addition, we refined and enhanced risk management throughout the business to successfully support the mitigation of the risks associated with, for example, our business transformation through the acquisition of the Santander UK portfolio and the regulatory cap on Interchange fees. We have enhanced our conduct risk governance to include our newly acquired retail partners who originate new accounts under their own FCA authorisation. In 2015, we are focusing on further embedding our risk operating model, our Risk Appetite and our Risk Management Framework based on the foundations that were put in place throughout 2014.

Monitoring customer outcomesIn order to monitor appropriate customer outcomes consistent with our Conduct Risk Management Framework, we developed a “Customer Outcomes Radar” (Radar) in 2014.

Working with industry experts, colleagues from all levels across the business were engaged to map out the customer journey and understand the key touch points which would enable us to effectively measure customer outcomes. The Board and executive team provided insight and challenge through the development of this monitoring framework.

The Radar is mapped from our Manifesto pillars, whose principal aim is to ensure customers remain at the heart of our business, to seven customer outcomes each of which has specific measures with agreed triggers for each, with reporting to the Customer and Conduct Risk Committee and subsequently to the Enterprise Risk Management Committee, the Board Risk Committee and the Board, to enable the review of the adequacy and appropriateness of the resourcing, systems and processes.

Culture and behaviours

Manifesto

Welcoming Knowing Understanding Rewarding

Outcomes/success factors

Customer outcomes radar

Operating modelC

usto

mer service

Custom

er lifecycle Product lifecy

cle

Business conduct

Insights

Customer

Enhancing our risk capability

The diagram to the right demonstrates the alignment with our Manifesto.

26 NewDay Annual Report and Accounts 2014

Risk management philosophyThe cornerstone of NewDay’s risk management philosophy is based on three key principles: accountability, transparency, and independent oversight.

Our risk management philosophy includes independent Board oversight and business-line accountability, constant communication, application of judgement and expert knowledge of the business and the environment within which it operates. Senior management takes an active role in identifying, assessing and managing various risks that affect the Group and our partners.

NewDay defines itself as operating within the Near-prime and Co-brand consumer credit market and actively accepts credit risk within a Board-set credit risk appetite. Our approach is to optimise other risks inherent in our business to achieve our target returns, such as operational risk.

We actively seek to appropriately manage or minimise exposure to any material risks through risk-control processes, utilising reputable UK organisations which specialise in the management of card services, credit-loss mitigation and the selective use of transfer instruments, such as insurance. We have tested disaster-recovery plans in place.

The Group has no exposure to trading risk, nor does it engage in any other speculative activity in the financial markets. We actively seek to comply with all relevant statutory regulation and to safeguard our reputation with our customers through responsibly lending.

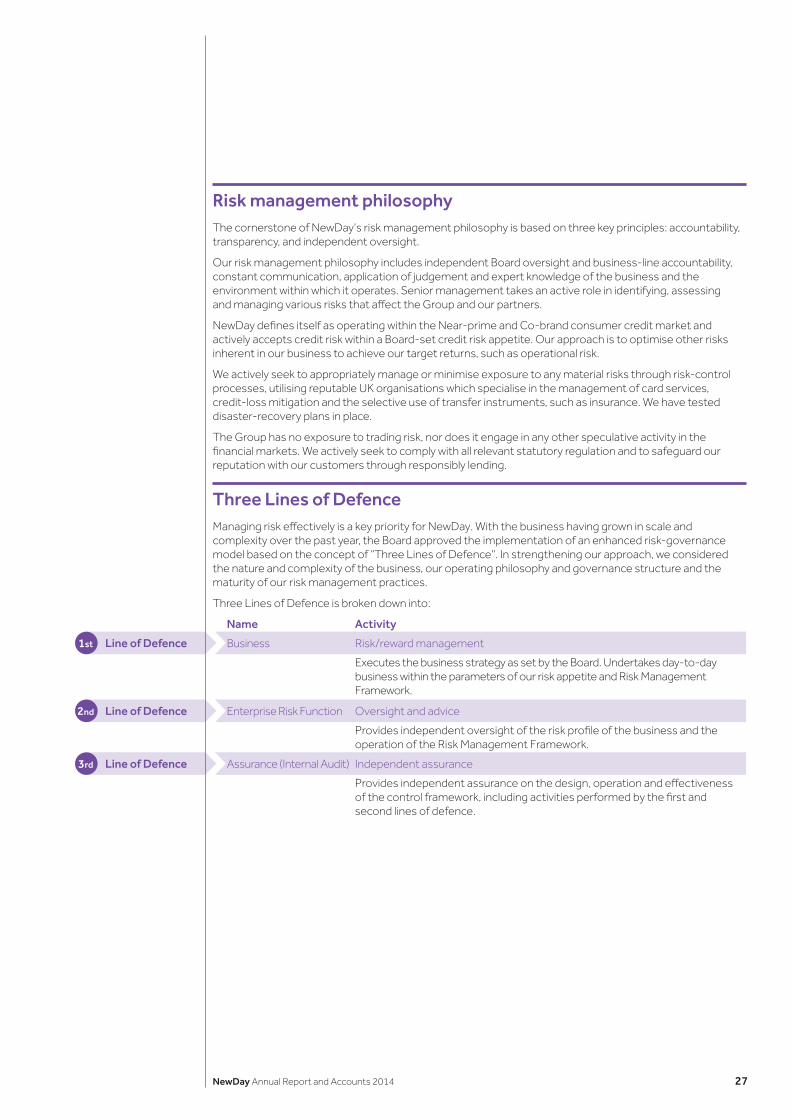

Three Lines of Defence Managing risk effectively is a key priority for NewDay. With the business having grown in scale and complexity over the past year, the Board approved the implementation of an enhanced risk-governance model based on the concept of “Three Lines of Defence”. In strengthening our approach, we considered the nature and complexity of the business, our operating philosophy and governance structure and the maturity of our risk management practices.

Three Lines of Defence is broken down into:

Executes the business strategy as set by the Board. Undertakes day-to-day business within the parameters of our risk appetite and Risk Management Framework.

Provides independent oversight of the risk profile of the business and the operation of the Risk Management Framework.

Provides independent assurance on the design, operation and effectiveness of the control framework, including activities performed by the first and second lines of defence.

Business Risk/reward management

Oversight and advice

Independent assurance

Enterprise Risk Function

Assurance (Internal Audit)

1st

2nd

3rd

Name Activity

Line of Defence

Line of Defence

Line of Defence

NewDay Annual Report and Accounts 2014 27

Risk management continued

Principal risks As part of the development of the Risk Management Framework, the Board has identified the key risk areas which impact the business. These are set out below along with mitigation in place.

Financial Risk (a) Credit Risk – the risk that the Group will incur a loss because its customers or counterparties fail to

discharge their contractual obligations.

Mitigation includes:

• Credit Risk Committee oversees the Credit Risk Framework

• Credit Risk Policies and Strategies in place

• Defined modelling for Credit Risk

• Collections and Recovery Strategies

(b) Liquidity/Funding and Cash Management Risk – the risk resulting from sub-optimal identification, assessment, monitoring and control processes to ensure the Group has sufficient liquidity for the short, medium and long-term objectives of the Company.

Mitigation includes:

• Asset & Liquidity Committee oversees the Liquidity Risk Framework

• Funding, Liquidity & Cash Management Policies in place

• The Company’s securitisation programme

(c) Market Risk – the risk of market movements that will negatively affect the value of the Group’s assets and liabilities.

NewDay does not undertake activities which expose the company to trading risk.

Mitigation includes:

• Fixed/floating swaps used to cover securitisation liabilities

Operational Risk The risk of loss/negative impact to NewDay resulting from inadequate or failed internal processes, people and systems, or from external events including legal, internal and external fraud but excluding application fraud and strategic/business risks. This also extends to services and processes provided by third parties.

Mitigation includes:

• Operational Risk Committee oversees the Operational Risk Framework

• Supplier governance programme established

• New product approval processes

• Process quality checking (QA)

• Financial reconciliation controls

• Change Governance and dedicated project management resources

• Business Continuity Management

• Logical Access Management

• Information Security Framework

• IT Incident Management

• Physical Security

Conduct RiskThe risk of customer detriment arising from inappropriate culture, products and processes, including legal, regulatory and compliance risk.

Mitigation includes:

• Customer & Conduct Risk Committee oversees the Conduct Risk Framework

• Supplier governance programme monitored

• Retail partner monitoring and relationship management

• New product approval processes

• Process quality checking

• Company Manifesto & Values workshops and training

• Policy and processes for vulnerable customers

28 NewDay Annual Report and Accounts 2014

Regulatory Risk The risk that a change in laws or regulations governing the Group will have a material impact on the business.

Mitigation includes:

• Review of legislative and regulation changes and ongoing compliance by the Legal and Conduct Advisory Team

• External legal advice sought where circumstances dictate

• Engagement with relevant regulatory bodies

• Participation in consultative reviews/market reviews

• Project management of large-scale regulatory projects, for example business readiness for FCA regulation

Strategic RiskThe risks arising from a sub-optimal business strategy or business model that may lead to financial loss, reputational damage or failure to meet internal and/or public policy objectives.

Mitigation includes:

• Documented business strategy and annual review process

• Business budgets defined, allocated and monitored to align with strategic objectives

• Risk Appetite aligned with strategic objectives and business planning

• Diversification of Co-Brand partners and product offerings

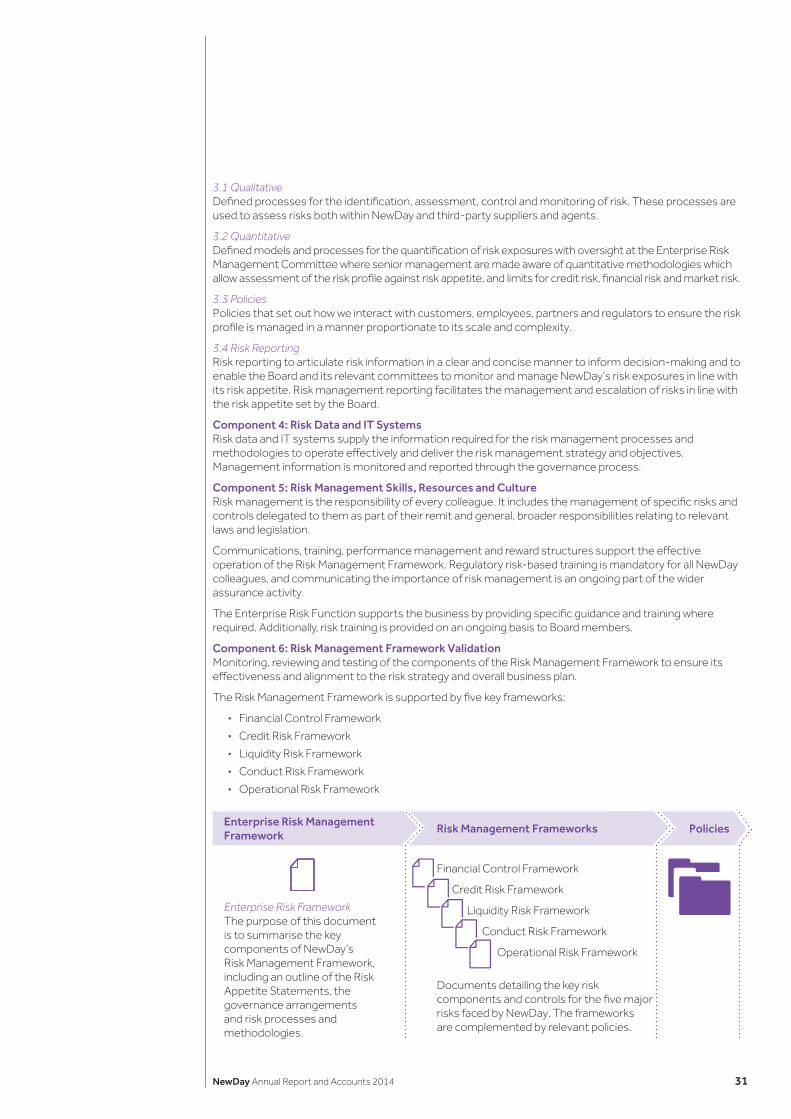

Risk Management FrameworkNewDay’s Risk Management Framework is a collection of day-to-day tools, processes and methodologies. The Framework documents the governance of risk and identifies risk processes and methodologies to assess, monitor and control risks. This Framework informs the development of the risk infrastructure and provides a sound basis for more informed risk-based decision-making across the business.

NewDay’s Risk Management Framework was re-codified during 2014 and will be further built out and embedded in 2015. NewDay’s Risk Management Framework comprises the following six core components:

1. Risk Appetite Statements

2. Risk Governance

6. R

isk

Man

agem

ent

Fram

ewor

k V

alid

atio

n3. Risk Processes and Methodologies

Identify

Monitor

AssessControl

Aggregation

4. Risk Data and IT Systems

5. Risk Management Skills, Resources and Culture

Reporting

Qualitative

Quantitative

Stress Testing

Change

NewDay Annual Report and Accounts 2014 29

Strategy

• Grow the Near-prime business by responsibly saying “yes” to more customers, maintaining high risk adjusted returns

• Leverage our major investments in our scalable Co-brand platform through collaboration with our partners

• Deliver a robust approach to credit management

• Maintain a strong capital base in order to provide a foundation for growth and attractive returns to our shareholders

Risk management continued

Component 1: Risk Appetite StatementsThe Board agrees its desired risk strategy and identifi es the risk areas that could impact the strategic objectives and sets its risk appetite in accordance with this assessment. Our Risk Appetite Statements are therefore the link between the overall business strategy and the management of risk through the Risk Management Framework.

The Statements are cascaded down into their component parts, including risk appetite objectives and triggers. This enables the appetite to inform day-to-day decision-making.

Informed risk-based decision-making

Three risk appetite objectives for NewDay underpin the delivery of our strategic objectives:

• Business Conduct (includes legal, regulatory and compliance risk): NewDay’s objective is to treat its customers fairly and to ensure that they remain at the heart of everything we do. NewDay will work to ensure that its customers do not suff er detrimental outcomes as a result of its product design or sales or post-sales processes correcting identifi ed errors. It seeks to embed its customer-focused ethos within the governance and culture of the organisation.

• Operational Performance (includes operational risk): NewDay’s objective is to fulfi l its customer commitments through systems and processes that are appropriately controlled, scalable, cost-eff ective and comply with applicable external and internal rules, laws and regulations. This includes having the right number of skilled, motivated people in place and developing and retaining talent. It seeks to have appropriate oversight, challenge and governance in place over planned changes.

• Financial Strength (includes credit, fi nancial control and liquidity/funding and cash management risk): NewDay’s objective is to maintain a strong fi nancial position by managing profi tability, credit quality and cash generation and ensuring that its fi nancial strength and liquidity are maintained at levels that refl ect NewDay’s desired fi nancial and credit risk profi le, comply with bank covenants and regulatory requirements, and enable planned growth in both normal and stressed conditions.

The Board has a number of measures to monitor performance under each objective, both quantitative and qualitative.

Risk appetite measures are monitored monthly by the relevant business committees and holistically by the Enterprise Risk Management Committee and the Board Risk Committee, with appropriate actions being taken where triggers have been breached. Risk appetite is set by the Board and approved at least annually as part of the business planning process and refl ects the Group’s latest commercial, economic and regulatory thinking.

Component 2: Risk GovernanceNewDay employs the Risk Management Framework in its approach to risk governance, assuring management that the business strategy is executed within its stated risk appetite. Risk management oversight is provided by the Board Risk Committee, utilising control structures and management information.

Component 3: Risk Processes and MethodologiesRisk management processes and methodologies are central to the framework allowing for the identifi cation, assessment, control and monitoring of risk. As part of the further build-out and embedding of the Risk Management Framework at NewDay, the following processes and methodologies will be further developed:

Risk Management Framework

Risk Appetite Statements

• Holistic risk assessment• Translated into measures• Ongoing assessment

• Risk governance• Tools, processes and

methodologies• Assess and control risks• Informed risk-based

decision-making

30 NewDay Annual Report and Accounts 2014

3.1 QualitativeDefined processes for the identification, assessment, control and monitoring of risk. These processes are used to assess risks both within NewDay and third-party suppliers and agents.

3.2 QuantitativeDefined models and processes for the quantification of risk exposures with oversight at the Enterprise Risk Management Committee where senior management are made aware of quantitative methodologies which allow assessment of the risk profile against risk appetite, and limits for credit risk, financial risk and market risk.

3.3 PoliciesPolicies that set out how we interact with customers, employees, partners and regulators to ensure the risk profile is managed in a manner proportionate to its scale and complexity.

3.4 Risk ReportingRisk reporting to articulate risk information in a clear and concise manner to inform decision-making and to enable the Board and its relevant committees to monitor and manage NewDay’s risk exposures in line with its risk appetite. Risk management reporting facilitates the management and escalation of risks in line with the risk appetite set by the Board.

Component 4: Risk Data and IT SystemsRisk data and IT systems supply the information required for the risk management processes and methodologies to operate effectively and deliver the risk management strategy and objectives. Management information is monitored and reported through the governance process.

Component 5: Risk Management Skills, Resources and CultureRisk management is the responsibility of every colleague. It includes the management of specific risks and controls delegated to them as part of their remit and general, broader responsibilities relating to relevant laws and legislation.

Communications, training, performance management and reward structures support the effective operation of the Risk Management Framework. Regulatory risk-based training is mandatory for all NewDay colleagues, and communicating the importance of risk management is an ongoing part of the wider assurance activity.

The Enterprise Risk Function supports the business by providing specific guidance and training where required. Additionally, risk training is provided on an ongoing basis to Board members.

Component 6: Risk Management Framework ValidationMonitoring, reviewing and testing of the components of the Risk Management Framework to ensure its effectiveness and alignment to the risk strategy and overall business plan.

The Risk Management Framework is supported by five key frameworks:

• Financial Control Framework

• Credit Risk Framework

• Liquidity Risk Framework

• Conduct Risk Framework

• Operational Risk Framework

Enterprise Risk Management Framework

Policies

Enterprise Risk FrameworkThe purpose of this document is to summarise the key components of NewDay’s Risk Management Framework, including an outline of the Risk Appetite Statements, the governance arrangements and risk processes and methodologies.

Risk Management Frameworks

Financial Control Framework

Credit Risk Framework

Liquidity Risk Framework

Conduct Risk Framework

Operational Risk Framework

Documents detailing the key risk components and controls for the five major risks faced by NewDay. The frameworks are complemented by relevant policies.

NewDay Annual Report and Accounts 2014 31

32 NewDay Annual Report and Accounts 2014

A number of enhancements to our corporate governance took place during 2014.

We have worked hard to ensure that our corporate governance and risk framework is built to scale.

NewDay Annual Report and Accounts 2014 33

Go

vernance

In this sectionCorporate governance 34Board of Directors 38Board Committee reports 40Executive and Governance Committees 47Management report 48Independent Auditor’s report 49

34 NewDay Annual Report and Accounts 2014

Corporate governance

I am pleased to update you on 2014’s key corporate governance highlights. Given that NewDay has grown considerably in size and complexity over the past year, we have worked hard to ensure that our corporate governance and risk framework is built to scale and applied throughout the business.

In building this framework, we consider the balance of interests between members, customers, colleagues and the community at large. In addition, we also ensure that our governance framework strikes a balance between implementing the business’s strategy, our risk appetite and strong business performance.

During the year, the Board oversaw a number of enhancements to corporate governance including the implementation of a more disciplined Three Lines of Defence risk governance model, enhancement of the Risk Management Framework and the establishment of the Enterprise Risk Function to support the business. We also welcomed Mark Eyre as Chief Risk Officer and appointed Alison Reed, our Chairman of the Board Audit Committee, as Senior Independent Non-Executive Director. In addition, Rupert Keeley was appointed as an Independent Non-Executive Director. Rupert brings significant payment systems and digital expertise to the Board and was appointed Chairman of the Remuneration and Nomination Committee in February 2015. All Board members have been submitted as Approved Persons for NewDay Ltd and NewDay Cards Ltd as part of NewDay’s application for full authorisation by the FCA.

After a period of considerable change, we continue to look ahead and adapt our governance and risk model and frameworks to accommodate a growing business. Our plans for 2015 include: introducing annual Disclosure and Barring Service (DBS) checks for all Approved Persons, Executives and Board members; subscribing to CIFAS, the UK’s fraud-prevention service, conducting checks on all employees, and introducing the Customer Outcomes Radar, which will provide key insights to the Board on conduct matters.

Sir Malcolm WilliamsonChairman and Non-Executive Director

Sir Malcolm WilliamsonChairman and Non-Executive Director

NewDay Annual Report and Accounts 2014 35

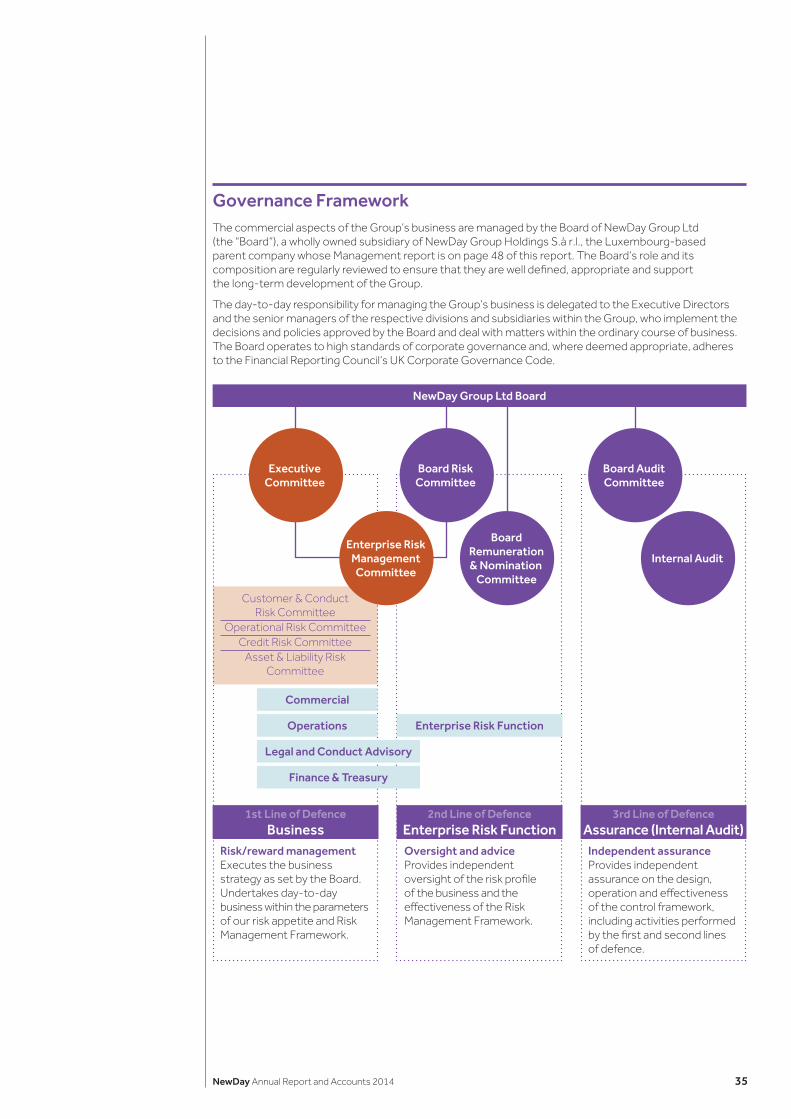

Governance Framework The commercial aspects of the Group’s business are managed by the Board of NewDay Group Ltd (the “Board”), a wholly owned subsidiary of NewDay Group Holdings S.à r.l., the Luxembourg-based parent company whose Management report is on page 48 of this report. The Board’s role and its composition are regularly reviewed to ensure that they are well defined, appropriate and support the long-term development of the Group.

The day-to-day responsibility for managing the Group’s business is delegated to the Executive Directors and the senior managers of the respective divisions and subsidiaries within the Group, who implement the decisions and policies approved by the Board and deal with matters within the ordinary course of business. The Board operates to high standards of corporate governance and, where deemed appropriate, adheres to the Financial Reporting Council’s UK Corporate Governance Code.

Customer & Conduct Risk Committee

Operational Risk CommitteeCredit Risk Committee

Asset & Liability Risk Committee

NewDay Group Ltd Board

Commercial

Operations

Legal and Conduct Advisory

Finance & Treasury

Enterprise Risk Function

Risk/reward managementExecutes the business strategy as set by the Board. Undertakes day-to-day business within the parameters of our risk appetite and Risk Management Framework.

Oversight and adviceProvides independent oversight of the risk profile of the business and the effectiveness of the Risk Management Framework.

Independent assuranceProvides independent assurance on the design, operation and effectiveness of the control framework, including activities performed by the first and second lines of defence.

Executive Committee

Enterprise Risk Management

Committee

Board Risk Committee

Board Remuneration & Nomination

Committee

Internal Audit

Board Audit Committee

1st Line of Defence Business

2nd Line of Defence Enterprise Risk Function

3rd Line of Defence Assurance (Internal Audit)

36 NewDay Annual Report and Accounts 2014

Corporate governance continued

The Board The Board aims to meet more than eight times a year, when Directors are apprised of operational performance metrics, risk matters, customer and conduct-related matters, and the Board receive reports on current strategic initiatives. Scheduled meetings are occasionally supplemented with strategic planning sessions, or project-specific Board meetings.

The Board has three sub-committees: the Audit Committee, the Risk Committee and the Remuneration and Nomination Committee. The roles and responsibilities of each committee are documented in Board-approved Terms of Reference. However, some matters are reserved for consideration by the Board, including strategy and management, structure, capital and funding, financial reporting and controls, internal controls and risk management, capital expenditure, external communications requiring Board sign-off, changes to Board structure and senior management arrangements.

The Directors bring many skills and much experience to the Board, including strategic experience, commercial knowledge, retail banking experience, UK regulatory knowledge, treasury and funding experience, risk management expertise, operational IT and accounting experience. This mix of skill sets enables Board members to make informed decisions on key issues facing the business. The Group maintains appropriate insurance cover in the unlikely event of legal action being brought against the Directors.

Role of the Board The Board is the leadership team behind NewDay that seeks to create a foundation for growth and attractive shareholder returns. It determines the vision, strategy and high-level policies of the Group, striking an appropriate balance between risk and reward and positive customer outcomes. It sets out the guidelines within which the business, including those parts of the business that are outsourced, is managed and controlled. It monitors business performance against agreed targets and the associated statements, consistent with the Strategy to Execution Plan (STEP), which sets out management’s key activities, within an agreed budget, to support the strategic objectives of the business; and it provides oversight and independent challenge, particularly with regard to the business’s culture and values.

The outcomes of the Board’s actions cascade down through the business. Frameworks must therefore be in place to ensure effective decision-making and adherence to high standards of corporate governance. They must also ensure that, in the delivery of products and services, NewDay aligns its responsible lending practices and customer support with the FCA’s Treating Customers Fairly principles and operates within the spirit of FCA regulation.