annual report petroz limited and its controlled entities · petroz limited and its controlled...

TRANSCRIPT

PETROZ LIMITED

ABN 86 154 090 043

ANNUAL REPORT

PETROZ LIMITED AND ITS CONTROLLED ENTITIES

FOR THE FINANCIAL YEAR ENDED 30 JUNE 2016

PETROZ LIMITED DIRECTORS’ REPORT

1

DIRECTORS’ REPORT The Board of Directors of Petroz Limited (“the Company”) submit herewith the annual report of the company and its controlled entities for the financial year ended 30 June 2016. In order to comply with the provisions of the Corporations Act 2001, the directors’ report as follows: 1. Information about the directors

The names and particulars of the directors of the company during or since the end of the financial year are: Dr Jacob Poll Robert Connell Christian Singleton Dr Jacob Poll – Director Dr Poll, who holds a BSc, MSc, and a PhD in Structural Geology from the University of Leiden in Holland, commenced working in the petroleum industry in 1966. Since then he has held a number of technical and executive positions with Royal Dutch/Shell and Woodside Petroleum, and has been Chief Executive Officer, an advisor to and a Board member of a number of small and medium sized oil and gas companies, most notably Oil Search, Petroz NL (not a related body corporate of the Company), Otto Energy and Anzoil. His 46-year petroleum exploration and production management career has spanned the globe, including the Americas, Europe, the Middle East, South East Asia and Australia. Dr Poll is a certified professional member of the American Association of Petroleum Geology and a Distinguished Member of the Petroleum Exploration Society of Australia.

Robert Connell –Director and Company Secretary Robert Connell is an investment banker and qualified lawyer with more than 10 years’ experience in Australia, Asia and Europe in corporate advisory, strategic communications, regulatory affairs and law. He has worked with some of the world’s largest telecommunications and resources companies and led multinational corporate-government negotiations on the regulation of the communications infrastructure and equipment in Europe. Robert has been involved in large Australian domestic and cross border M&A transactions, advised on a series of private equity transactions and led capital raisings for a number of public companies.

PETROZ LIMITED DIRECTORS’ REPORT

2

Christian Singleton – Non-executive Director Chris Singleton has advice and deal experience spanning over 20 years. He has been the Managing Director and Executive Director of numerous listed and unlisted companies and has had extensive involvement in acquisitions and divestments, structuring, capital management, capital raisings, listings, spin offs, the acquisition and divestment of assets and restructuring. Chris has worked at a senior executive level with the world’s largest wireless carrier and operated, raised substantial capital for and divested a series of telecommunications, technology, energy and resources businesses.

2. Share options granted to directors and senior management No share options were granted to directors and senior management during the financial year.

3. Principal activities

The principal activities of the consolidated entity are to assess the viability of various investment opportunities in the oil and gas sector and, subsequently, to undertake investment in that sector and the development of oil and gas projects. No significant change in the nature of the consolidated entity’s principal activities occurred during the year.

4. Review of operations The consolidated entity continues to pursue the development of the Alasehir project in Turkey and other opportunities in the region. The consolidated loss of the consolidated entity for the year ended 30 June 2016 was $86,022 (2015: a loss of $520,805).

5. Changes in state of affairs There was no significant change in the state of affairs of the consolidated entity during the financial year.

PETROZ LIMITED DIRECTORS’ REPORT

3

6. Subsequent events

The Company’s wholly owned subsidiary, Petroz New Ventures Pty Ltd, was deregistered on 10 August 2016. Petroz New Ventures Pty Ltd had been dormant before deregistration. Other than the above, there has not been any matter or circumstance occurring subsequent to the end of the financial year that has significantly affected, or may significantly affect, the operations of the consolidated entity, the results of those operations, or the state of affairs of the consolidated entity in future financial years.

7. Likely developments

Other than as referred to in this report, further information as to likely developments in the operations of the consolidated entity and likely results of those operations would, in the opinion of directors, be speculative.

8. Environmental regulations

The consolidated entity is currently pursuing the development of the Alasehir Project in Turkey and as part of furthering the development of the project the Group has acquired Performance and Environmental bonds for a petroleum license and will be subject under Turkish Petroleum Law No. 6491.

9. Dividends

No dividends were declared or recommended but not paid during the financial year.

10. Shares under options or issued on exercise of options

The Company has no options on issue over ordinary shares.

11. Indemnifying officers and auditors

During or since the end of the financial year the company has not indemnified or made a relevant agreement to indemnify an officer or auditor of the company or of any related body corporate against a liability incurred as such an officer or auditor. In addition, the company has not paid, or agreed to pay, a premium in respect of a contract insuring against a liability incurred by an officer or auditor.

12. Directors' Meetings

During the year ended 30 June 2016, no meetings of directors were held. There were two circular resolution of directors made.

PETROZ LIMITED

7

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE FINANCIAL YEAR ENDED 30 JUNE 2016

NOTES 2016

2015 $ $

Continuing operations

Revenue - -

Travelling expense (10,808) (16,412) Consulting fee 4 (257) (489,686) Administration expense (18,490) (14,707) Exploration costs (18,167) -

Loss on foreign currency exchange 4 (38,300) -

Loss before income tax (86,022) (520,805)

Income tax expense 5 - -

Loss for the year (86,022) (520,805)

Other comprehensive income - -

Total comprehensive expense for the year (86,022) (520,805)

Loss for the year attributable to owners of the Company (86,022) (520,805) Total comprehensive expense attributable to owners of the Company

(86,022) (520,805)

The above Consolidated Statement of Profit or Loss and Other Comprehensive Income should be read in conjunction with

the accompanying notes.

PETROZ LIMITED

8

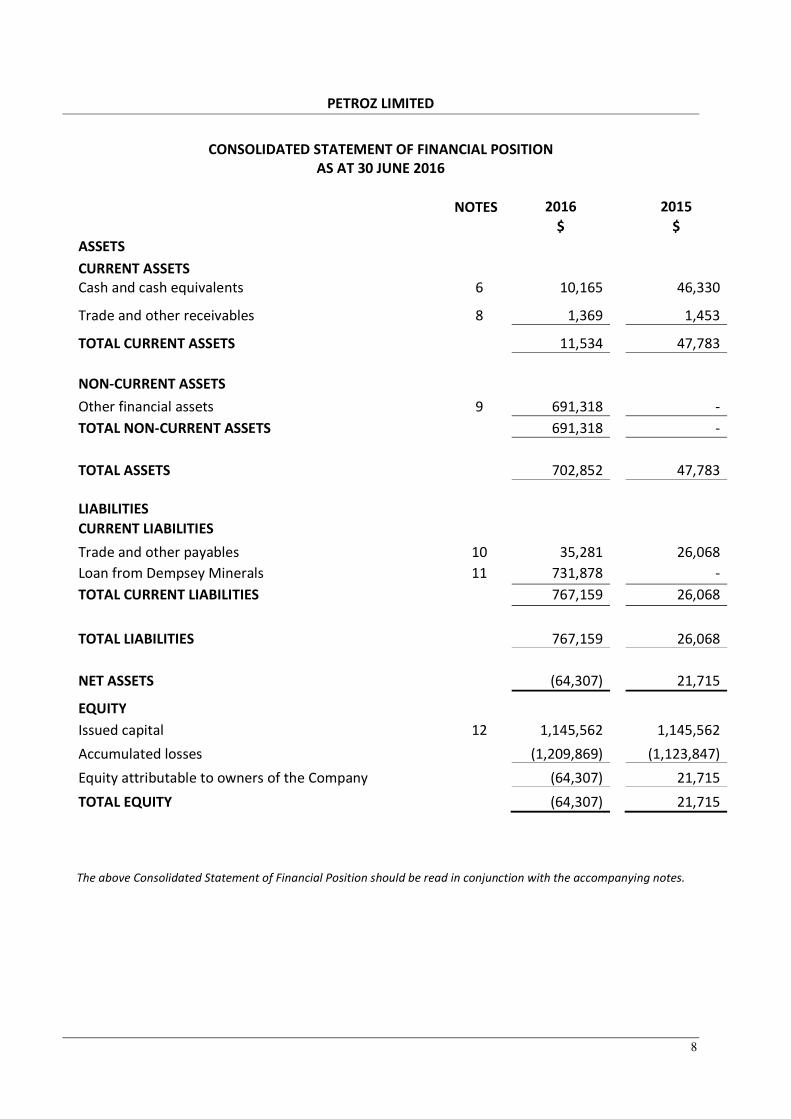

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2016 NOTES 2016 2015

$ $ ASSETS

CURRENT ASSETS

Cash and cash equivalents 6 10,165 46,330

Trade and other receivables 8 1,369 1,453

TOTAL CURRENT ASSETS 11,534 47,783 NON-CURRENT ASSETS Other financial assets 9 691,318 - TOTAL NON-CURRENT ASSETS 691,318 - TOTAL ASSETS 702,852 47,783

LIABILITIES

CURRENT LIABILITIES

Trade and other payables 10 35,281 26,068 Loan from Dempsey Minerals 11 731,878 - TOTAL CURRENT LIABILITIES 767,159 26,068 TOTAL LIABILITIES 767,159 26,068 NET ASSETS (64,307) 21,715

EQUITY

Issued capital 12 1,145,562 1,145,562 Accumulated losses (1,209,869) (1,123,847) Equity attributable to owners of the Company (64,307) 21,715 TOTAL EQUITY (64,307) 21,715

The above Consolidated Statement of Financial Position should be read in conjunction with the accompanying notes.

PETROZ LIMITED

9

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE FINANCIAL YEAR ENDED 30 JUNE 2016

Attributable to owners of the Company

Issued Capital

Accumulated Losses

Total

Note $ $ $ Balance at 30 June 2014 656,612 (603,042) 53,570 Loss for the year - (520,805) (520,805) Total comprehensive expense for the year - (520,805) (520,805) Shares issued during the year 488,950 - 488,950 Balance at 30 June 2015 1,145,562 (1,123,847) 21,715 Loss for the year - (86,022) (86,022) Total comprehensive expense for the year - (86,022) (86,022) Balance at 30 June 2016 1,145,562 (1,209,869) (64,307)

The above Consolidated Statement of Changes in Equity should be read in conjunction with the accompanying notes.

PETROZ LIMITED

10

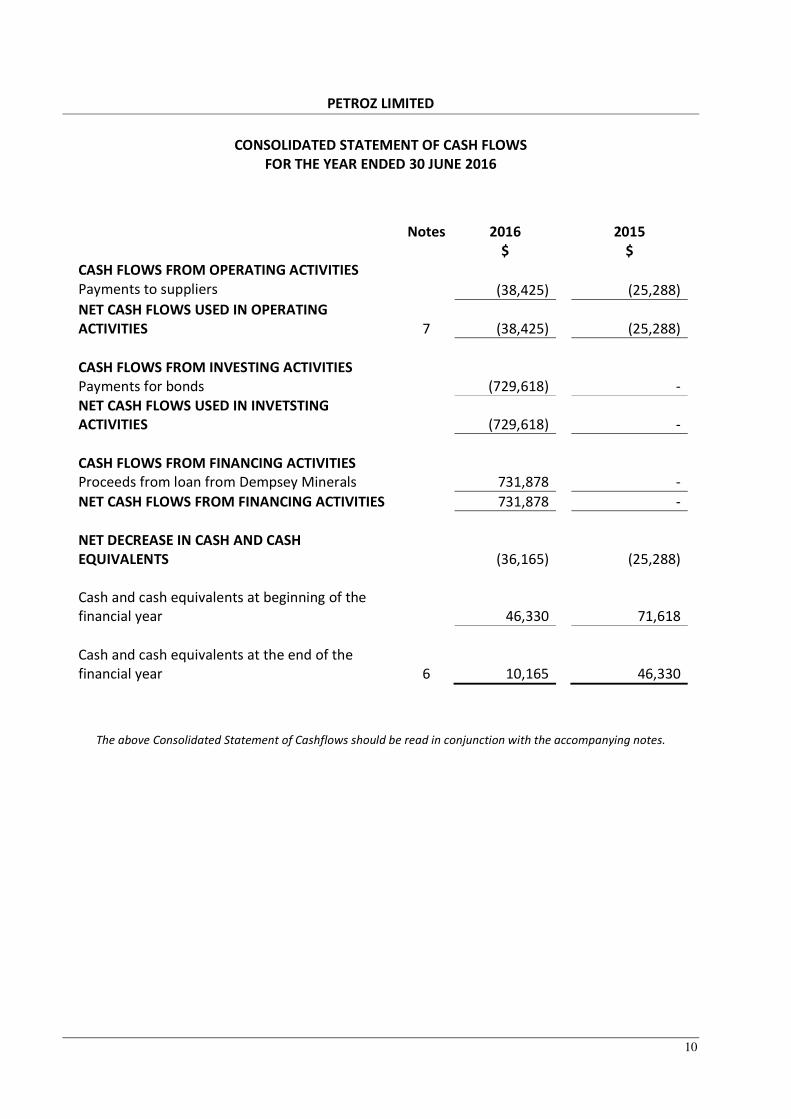

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30 JUNE 2016

Notes 2016

2015 $ $ CASH FLOWS FROM OPERATING ACTIVITIES Payments to suppliers (38,425) (25,288) NET CASH FLOWS USED IN OPERATING ACTIVITIES 7 (38,425) (25,288) CASH FLOWS FROM INVESTING ACTIVITIES Payments for bonds (729,618) - NET CASH FLOWS USED IN INVETSTING ACTIVITIES

(729,618) -

CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from loan from Dempsey Minerals 731,878 - NET CASH FLOWS FROM FINANCING ACTIVITIES 731,878 - NET DECREASE IN CASH AND CASH EQUIVALENTS

(36,165) (25,288) Cash and cash equivalents at beginning of the financial year

46,330 71,618 Cash and cash equivalents at the end of the financial year 6 10,165 46,330

The above Consolidated Statement of Cashflows should be read in conjunction with the accompanying notes.

PETROZ LIMITED

11

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS The consolidated financial statements and notes represent those of Petroz Limited and its controlled entities (“the Group”) for the year ended 30 June 2016. The financial statements were authorised for issue in accordance with a resolution by the board of directors. Petroz Limited is an unlisted public company limited by shares, incorporated and domiciled in Australia. Its registered office and principal place of business address is Level 4, 11 Harvet Terrace, West Perth WA 6005. 1. STATEMENT OF COMPLIANCE The financial report is a general purpose financial report which has been prepared in accordance with the Corporations Act 2001, Australian Accounting Standards and Interpretations, and comply with other requirements of the law.

The financial statements comprise the consolidated financial statements of the Group. For the purposes of preparing the consolidated financial statements, the Group is a for-profit entity.

Australian Accounting Standards set out accounting policies that result in the presentation of reliable and relevant information about transactions, events and conditions. Compliance with Australian Accounting Standards ensures that the financial statements and notes of the Company and the Group comply with International Financial Reporting Standards (‘IFRS’). The consolidated financial statements were authorised for issue by the directors on 31 October 2016. The directors have the power to amend and reissue the consolidated financial statements. 2. BASIS OF PREPARATION OF THE FINANCIAL REPORT The financial statements have been prepared on the basis of historical cost. Historical cost is generally based on the fair values of the consideration given in exchange for assets. All amounts are presented in Australian dollars, unless otherwise noted.

Going concern The financial statements have been prepared on the basis of going concern which assumes continuity of normal business activities and the realisation of assets and settlement of liabilities in the ordinary course of business. The Group has incurred net operating cash outflows of $38,425 and a net loss of $86,022 for the year ended 30 June 2016 as disclosed in the Consolidated Statement of Cash Flows and Consolidated Statement of Profit or Loss and Other Comprehensive Income, respectively. As at 30 June 2016 the Group also had a deficiency of working capital of $755,625, as disclosed in the Statement of Financial Position. Included in Current Liabilities at 30 June 2016 is a loan payable to Dempsey Minerals Limited (Dempsey) of $731,878 relating to an Option and Sale & Purchase Agreement which provides the

PETROZ LIMITED

12

option for Dempsey to acquire 100% of the Issued Capital of Petroz Limited. The Agreement states that if the option to complete the transaction is terminated by Dempsey at any time before 31 December 2017, the loan from Dempsey would be repayable within 30 days of termination. As a result of these matters the Directors have assessed the Group’s ability to continue as a going concern and to pay its debts as and when they fall due. The ability of the Group to continue as a going concern is dependent upon funding to provide adequate working capital for a further 12 months from the date of signature of the Financial Statements. Furthermore, in the event that Dempsey terminated the Option and Sale & Purchase Agreement the Group would need to seek additional funding within 30 days of the termination in order to comply with the agreed repayment terms. The Directors intend to undertake further borrowings or equity fundraising as and when required and are satisfied that the going concern basis of preparation is appropriate. Should the Company be unable to raise funding as and when required, there is a material uncertainty whether it will be able to continue as a going concern and, therefore, whether it will realise its assets and extinguish its liabilities in the normal course of business and at the amounts stated in the financial report.

The consolidated financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts or to the amounts and classification of liabilities that may be necessary should the Group be unable to continue as a going concern. 3. SIGNFICANT ACCOUNTING POLICIES

(a) Basis of consolidation (i) Subsidiaries The consolidated financial statements incorporate the financial statements of the Company and entities (including structured entities) controlled by the Company and its subsidiaries. Control is achieved when the Company:

- has power over the investee; - is exposed, or has rights, to variable returns from its involvement with the investee; and - has the ability to use its power to affect its returns.

The Company reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed above. When the Company has less than a majority of the voting rights of an investee, it has power over the investee when the voting rights are sufficient to give it the practical ability to direct the relevant activities of the investee unilaterally. The Company considers all relevant facts and circumstances in

PETROZ LIMITED

13

assessing whether or not the Company's voting rights in an investee are sufficient to give it power, including:

- the size of the Company's holding of voting rights relative to the size and dispersion of holdings of the other vote holders;

- potential voting rights held by the Company, other vote holders or other parties; - rights arising from other contractual arrangements; and - any additional facts and circumstances that indicate that the Company has, or does not have,

the current ability to direct the relevant activities at the time that decisions need to be made, including voting patterns at previous shareholders' meeting.

(ii) Joint Operation

The Company has an interest in a joint arrangement that is a jointly controlled operation. A joint arrangement is a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control. The Company recognises its interest in the joint operation by recognising the assets that it controls and the liabilities that it incurs. The Company also recognises the expenses that it incurs and its share of the income that it earns from the sale of goods or services by the joint operation. (b) New and Revised Accounting Standards

i. Amendments to Standards that are mandatorily effective for the current year

In the current year, the Group has applied one applicable amendment to AASBs issued by the Australian Accounting Standards Board (AASB) that are mandatorily effective for an accounting period that begins on or after 1 July 2015, and therefore relevant for the current year end. AASB 2015-3 ‘Amendments to Australian Accounting Standards arising from the Withdrawal of AASB 1031 Materiality’ This amendment completes the withdrawal of references to AASB 1031 in all Australian Accounting Standards and Interpretations, allowing that Standard to effectively be withdrawn. The application of the amendment does not have any material impact on the disclosures or on the amounts recognised in the Group’s financial statements.

ii. Standards in issue not yet adopted At the date of authorisation of the Financial Statements, the Standards and Interpretations applicable to the Group’s business listed below were in issue but not yet effective. The potential effect of the revised Standards on the Group’s financial statements has not yet been determined.

PETROZ LIMITED

14

AASB 9 ‘Financial Instruments’ and the relevant amending standards, effective for annual reporting periods beginning on or after 1 January 2018, expected to be initially applied in the financial year ending 30 June 2019; AASB 2014-3 ‘Amendments to Australian Accounting Standards – Accounting for Acquisitions of Interests in Joint Operations’, effective for annual reporting periods beginning on or after 1 January 2016, expected to be initially applied in the financial year ending 30 June 2017; AASB 2014-4 ‘Amendments to Australian Accounting Standards – Clarification of Acceptable Methods of Depreciation and Amortisation’, effective for annual reporting periods beginning on or after 1 January 2016, expected to be initially applied in the financial year ending 30 June 2017; AASB 2014-9 ‘Amendments to Australian Accounting Standards – Equity Method in Separate Financial Statements’, effective for annual reporting periods beginning on or after 1 January 2016, expected to be initially applied in the financial year ending 30 June 2017; AASB 2014-10 ‘Amendments to Australian Accounting Standards – Sale or Contribution of Assets between an Investor and its Associate or Joint Venture’, effective for annual reporting periods beginning on or after 1 January 2016, expected to be initially applied in the financial year ending 30 June 2017; AASB 2015-1 ‘Amendments to Australian Accounting Standards – Annual Improvements to Australian Accounting Standards 2012-2014Cycle’, effective for annual reporting periods beginning on or after 1 January 2016, expected to be initially applied in the financial year ending 30 June 2017; AASB 2015-2 ‘Amendments to Australian Accounting Standards – Disclosure Initiative: Amendments to AASB 101’, effective for annual reporting periods beginning on or after 1 January 2016, expected to be initially applied in the financial year ending 30 June 2017; AASB 2016-1 ‘Amendments to Australian Accounting Standards – Recognition of Deferred Tax Assets for Unrealised Losses’, effective for annual reporting periods beginning on or after 1 January 2017, expected to be initially applied in the financial year ending 30 June 2018; AASB 2016-2 ‘Amendments to Australian Accounting Standards – Disclosure Initiative: Amendments to AASB107’, effective for annual reporting periods beginning on or after 1 January 2017, expected to be initially applied in the financial year ending 30 June 2018.

(c) Revenue Recognition

Interest revenue is recognised on a time proportionate basis that takes into account the effective yield on the financial asset.

PETROZ LIMITED

15

(d) Income Taxes

The income tax expense for the period is the tax payable on the current period’s taxable income based on the applicable income tax rate adjusted by changes in deferred tax assets and liabilities attributable to temporary differences and to unused tax losses. The current income tax charge is calculated on the taxable profit for the year. Taxable profit differs from profit before tax as reported in the consolidated statement of profit or loss and other comprehensive income because of items of income or expense that are taxable or deductible in other years and items that are never taxable or deductible. The Group’s current tax is calculated using tax rates that have been enacted or substantively enacted by the end of the reporting period. Deferred tax is recognised on temporary differences between the carrying amounts of assets and liabilities in the consolidated financial statements and the corresponding tax bases used in the computation of taxable profit. Deferred tax liabilities are generally recognised for all taxable temporary differences. Deferred tax assets are generally recognised for all deductible temporary differences to the extent that it is probable that taxable profits will be available against which those deductible temporary differences can be utilised. Such deferred tax assets and liabilities are not recognised if the temporary difference arises from the initial recognition (other than in a business combination) of assets and liabilities in a transaction that affects neither the taxable profit nor the accounting profit. In addition, deferred tax liabilities are not recognised if the temporary difference arises from the initial recognition of goodwill.

Deferred tax assets are recognised for deductible temporary differences and unused tax losses only if it is probable that future taxable amounts will be available to utilise those temporary differences and losses. The carrying amount of deferred tax assets is reviewed at the end of each reporting period and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the period in which the liability is settled or the asset realised, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period. The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the manner in which the Group expects, at the end of the reporting period, to recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to offset current tax assets and liabilities and when the deferred tax balances relate to the same taxation authority. Current tax assets and tax liabilities are offset where the entity has a legally enforceable right to offset and intends either to settle on a net basis, or to realise the asset and settle the liability simultaneously

PETROZ LIMITED

16

Current and deferred tax is recognised in profit or loss, except to the extent that it relates to items recognised in other comprehensive income or directly in equity. In this case, the tax is also recognised in other comprehensive income or directly in equity, respectively.

(e) Impairment of Assets

At the end of each reporting period, the Group reviews the carrying amounts of its assets to determine whether there is any indication that those assets have suffered an impairment loss. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. An impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

When an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset in prior years. A reversal of an impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

(f) Cash and Cash Equivalents

Cash and cash equivalents includes cash on hand and deposits held at call with financial institutions which are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

(g) Trade and Other Receivables

Trade and other receivables are recognised initially at fair value and, other than those that meet the definition of equity instruments, are subsequently measured at amortised cost using the effective interest method, less allowance for impairment. An allowance for impairment of trade and other receivables is established when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of the debts. Loss events include financial difficulty or bankruptcy of the debtor, significant delay in payments and breaches of contracts. The impairment loss, measured as the difference between the debt’s carrying amount and the present value of estimated future cash flows discounted at the original effective interest rate, is recognised in profit or loss.

PETROZ LIMITED

17

When the debt becomes uncollectible in a subsequent period, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are recognised in profit or loss.

(h) Financial Assets

The Group classifies its financial assets as loans and receivables. Management determines the classification of its financial assets at initial recognition.

Loans and receivables are non-derivative financial assets with fixed or determinate payments that are not quoted in an active market. They are included in current assets, except for those with maturities greater than 12 months after the reporting date which are classified as non-current assets. Trade receivables, loans, and other receivables that have fixed or determinable payments that are not quoted in an active market are classified as ‘loans and receivables’. Loans and receivables are measured at amortised cost using the effective interest method, less any impairment. Interest income is recognised by applying the effective interest rate, except for short-term receivables when the effect of discounting is immaterial.

(i) Trade and Other Payables

These amounts represent liabilities for goods and services provided to the Company prior to the end of financial year that are unpaid. The amounts are unsecured and are usually paid within 30 days of recognition.

(j) Financial Liabilities

The Group classifies its financial liabilities as financial liabilities other than financial liabilities at FVTPL. Other financial liabilities, including borrowings and trade and other payables, are initially measured at fair value, net of transaction costs. Other financial liabilities are subsequently measured at amortised cost using the effective interest method, with interest expense recognised on an effective yield basis. The effective interest method is a method of calculating the amortised cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or (where appropriate) a shorter period, to the net carrying amount on initial recognition. The Group derecognises financial liabilities when, and only when, the Group’s obligations are discharged, cancelled or have expired. The difference between the carrying amount of the financial liability derecognised and the consideration paid and payable is recognised in profit or loss.

PETROZ LIMITED

18

(k) Contributed Equity Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction, net of tax, from the proceeds.

(l) Goods and Services Tax (GST)

Revenues, expenses and assets are recognised net of the amount of associated GST, unless the GST incurred is not recoverable from the taxation authority. In this case it is recognised as part of the cost of acquisition of the asset or as part of the expense. Receivables and payables are stated inclusive of the amount of GST receivable or payable. The net amount of GST recoverable from, or payable to, the taxation authority is included with other receivables or payables in the Statement of Financial Position. Cash flows are presented on a gross basis. The GST components of cash flows arising from investing or financing activities which are recoverable from, or payable to the taxation authority, are presented as operating cash flows.

(m) Foreign Currency Transactions and Balances Functional and presentation currency The functional currency of each of the Group’s entities is measured using the currency of the primary economic environment in which that entity operates. The consolidated financial statements are presented in Australian dollars, which is the parent entity’s functional currency. Transactions and balances Foreign currency transactions are translated into functional currency using the exchange rates prevailing at the date of the transaction. Foreign currency monetary items are translated at the year-end exchange rate. Non-monetary items measured at historical cost continue to be carried at the exchange rate at the date of the transaction. Non-monetary items measured at fair value are reported at the exchange rate at the date when fair values were determined. Exchange differences arising on the translation of monetary items are recognised in profit or loss, except where deferred in equity as a qualifying cash flow or net investment hedge. Exchange differences arising on the translation of non-monetary items are recognised directly in other comprehensive income to the extent that the underlying gain or loss is recognised in other comprehensive income; otherwise the exchange difference is recognised in profit or loss. Group companies The financial results and position of foreign operations, whose functional currency is different from the Group’s presentation currency, are translated as follows:

PETROZ LIMITED

19

- assets and liabilities are translated at exchange rates prevailing at the end of the reporting period;

- income and expenses are translated at average exchange rates for the period; and - retained earnings are translated at the exchange rates prevailing at the date of the

transaction. Exchange differences arising on translation of foreign operations with functional currencies other than Australian dollars are recognised in other comprehensive income and included in the foreign currency translation reserve in the statement of financial position. The cumulative amount of these differences is reclassified into profit or loss in the period in which the operation is disposed of.

(n) Share-based payments

Equity-settled share-based payment transactions with parties other than employees are measured at the fair value of the goods or services received, except where that fair value cannot be estimated reliably, in which case they are measured at the fair value of the equity instruments granted, measured at the date the entity obtains the goods or the counterparty renders the service. For cash-settled share-based payments, a liability is recognised for the goods or services acquired, measured initially at the fair value of the liability. At the end of each reporting period until the liability is settled, and at the date of settlement, the fair value of the liability is remeasured, with any changes in fair value recognised in profit or loss for the year.

(o) Critical Accounting Judgments, Estimates and Assumptions

The directors evaluate estimates and judgements incorporated into the financial report based on historical knowledge and best available current information. Estimates assume a reasonable expectation of future events and are based on current trends and economic data, obtained both externally and within the Group.

Taxation

Balances disclosed in the consolidated financial statements and the notes thereto related to taxation are based on the best estimates of the directors. These estimates take into account both the financial performance and position of the Group as they pertain to current income taxation legislation, and the directors’ understanding thereof. No adjustment has been made for pending or future taxation legislation. The current income tax position represents the directors’ best estimate, pending an assessment by the Australian Taxation Office.

PETROZ LIMITED

20

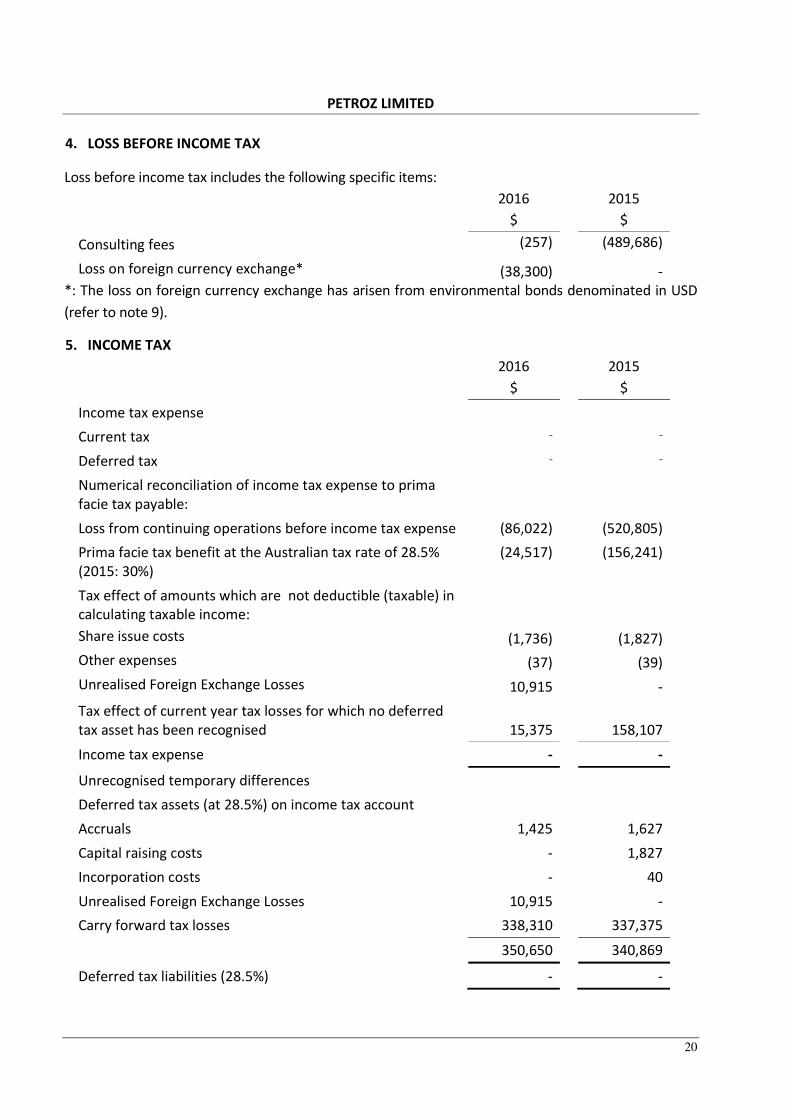

4. LOSS BEFORE INCOME TAX

Loss before income tax includes the following specific items:

2016 $

2015 $

Consulting fees (257) (489,686)

Loss on foreign currency exchange* (38,300) - *: The loss on foreign currency exchange has arisen from environmental bonds denominated in USD (refer to note 9).

5. INCOME TAX

2016 $

2015 $

Income tax expense

Current tax - -

Deferred tax - -

Numerical reconciliation of income tax expense to prima facie tax payable:

Loss from continuing operations before income tax expense (86,022) (520,805) Prima facie tax benefit at the Australian tax rate of 28.5% (2015: 30%)

(24,517) (156,241)

Tax effect of amounts which are not deductible (taxable) in calculating taxable income:

Share issue costs (1,736) (1,827) Other expenses (37) (39) Unrealised Foreign Exchange Losses 10,915 - Tax effect of current year tax losses for which no deferred tax asset has been recognised 15,375

158,107 Income tax expense - -

Unrecognised temporary differences

Deferred tax assets (at 28.5%) on income tax account

Accruals 1,425 1,627 Capital raising costs - 1,827 Incorporation costs - 40 Unrealised Foreign Exchange Losses 10,915 - Carry forward tax losses 338,310 337,375

350,650 340,869

Deferred tax liabilities (28.5%) - -

PETROZ LIMITED

21

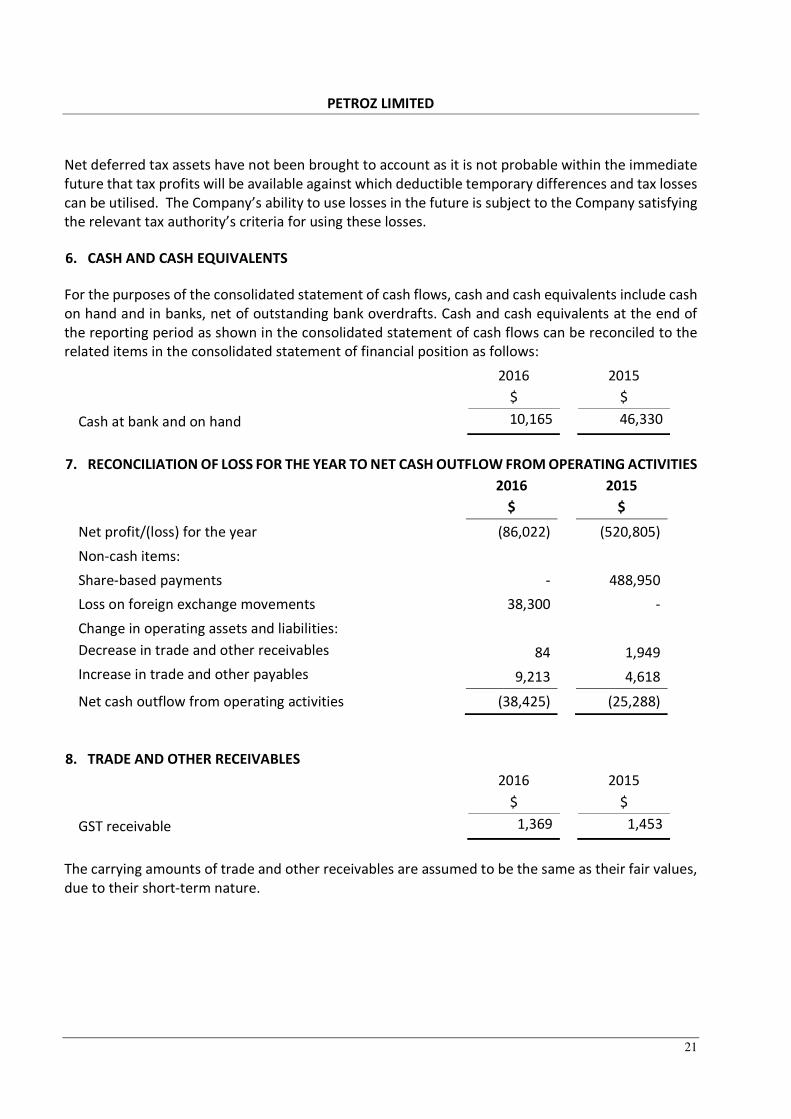

Net deferred tax assets have not been brought to account as it is not probable within the immediate future that tax profits will be available against which deductible temporary differences and tax losses can be utilised. The Company’s ability to use losses in the future is subject to the Company satisfying the relevant tax authority’s criteria for using these losses.

6. CASH AND CASH EQUIVALENTS

For the purposes of the consolidated statement of cash flows, cash and cash equivalents include cash on hand and in banks, net of outstanding bank overdrafts. Cash and cash equivalents at the end of the reporting period as shown in the consolidated statement of cash flows can be reconciled to the related items in the consolidated statement of financial position as follows:

2016 $

2015 $

Cash at bank and on hand 10,165 46,330

7. RECONCILIATION OF LOSS FOR THE YEAR TO NET CASH OUTFLOW FROM OPERATING ACTIVITIES

2016 $

2015 $

Net profit/(loss) for the year (86,022) (520,805) Non-cash items: Share-based payments - 488,950 Loss on foreign exchange movements 38,300 - Change in operating assets and liabilities: Decrease in trade and other receivables 84 1,949 Increase in trade and other payables 9,213 4,618

Net cash outflow from operating activities (38,425) (25,288)

8. TRADE AND OTHER RECEIVABLES

2016 $

2015 $

GST receivable 1,369 1,453

The carrying amounts of trade and other receivables are assumed to be the same as their fair values, due to their short-term nature.

PETROZ LIMITED

22

9. OTHER FINANCIAL ASSETS

Other financial assets represented the Performance and Environmental bonds for a petroleum license required by Turkish Oil regulatory organization under Turkish Petroleum Law No. 6491. The Preformance Bonds are held in escrow by a financial institution in Turkey. The Environment Bonds are held by the Turkish Government. Total value of these bonds held in two accounts as at 30 June 2016 was USD633,000 and TRY139,937. The Group had 75% interest in these bonds. The Performance Bonds represent 2% of the Expected Capital Expenditure of the Alasehir Project. Once each year’s expected expenditure has been met, the funds held in escrow relating to that particular year will be released. Additionally, for every dollar that is not expended, the Group Forfeits 2% of the committed expenditure that has not been met. This is paid directly from the Performance Bonds to the Turkish Government. Also included under other financial assets is a Damage and Investment Bond which total value at 30 June 2016 was USD2,356. 10. TRADE AND OTHER PAYABLES Trade payables are unsecured and are usually paid within 30 days of recognition. The carrying amounts of trade and other payables are assumed to be the same as their fair values, due to their short-term nature. 11. LOAN FROM DEMPSEY MINERALS

During the year, the Group received a loan from Dempsey Minerals a public listed company incorporated in Australia, under a conditional exclusive Option and Sale & Purchase Agreement through which Dempsey Minerals has an option to acquire 100% of the issued capital of the Company. The Company has recently granted an extension to the Option period to 31 December 2017. The loan from Dempsey Minerals is unsecured, non-interest bearing and will be treated as an intercompany loan by Dempsey Minerals if the acquisition of the Company is completed. As part of the exclusive option and sale purchase agreement, it was agreed that the loan was utilized in the environmental bonds under Turkish Petroleum Law (refer to note 9). If Dempsey Minerals does not exercise the option, or if the acquisition is not completed, the loan must be repaid in full within one (1) month to the relevant circumstance occurring and is payable in either cash or converted into fully paid ordinary shares in the Company at the set price of $0.05 per share. The conversion of the loan into shares is solely at the discretion of Dempsey Minerals.

PETROZ LIMITED

23

12. ISSUED CAPITAL 2016 2015 Number $ Number $

Ordinary shares fully paid 30,660,107 1,145,562 30,660,107 1,145,562

Movements in ordinary share capital: 2016 2015 Number $ Number $

Beginning of the year 30,660,107 1,145,562 24,140,767 656,612 Issued during the year: - - 6,519,340 488,950

End of the year 30,660,107 1,145,562 30,660,107 1,145,562 At the shareholders’ meetings each ordinary share is entitled to one vote when a poll is called, otherwise each shareholder has one vote on a show of hands. Ordinary shares participate in dividends and the proceeds on winding up in proportion to the number of shares held. The Group’s debt and capital includes ordinary share capital, and financial liabilities, supported by financial assets. There are no externally imposed capital requirements.

Management effectively manages the Group’s capital by assessing the Group’s financial risks and adjusting its capital structure in response to changes in these risks and in the market. These responses include the management of debt levels, distributions to shareholders and share issues. 13. DIVIDENDS No dividends were paid during the financial year. No recommendation for payment of dividends has been made. 14. REMUNERATION OF AUDITOR

During the year the following fees were paid or payable for services provided by the auditor of the Company, its related practices and non-related audit services:

2016 $

2015 $

Audit services 5,000 6,125

Non-audit services - -

Total remuneration for auditors 5,000 6,125

PETROZ LIMITED

24

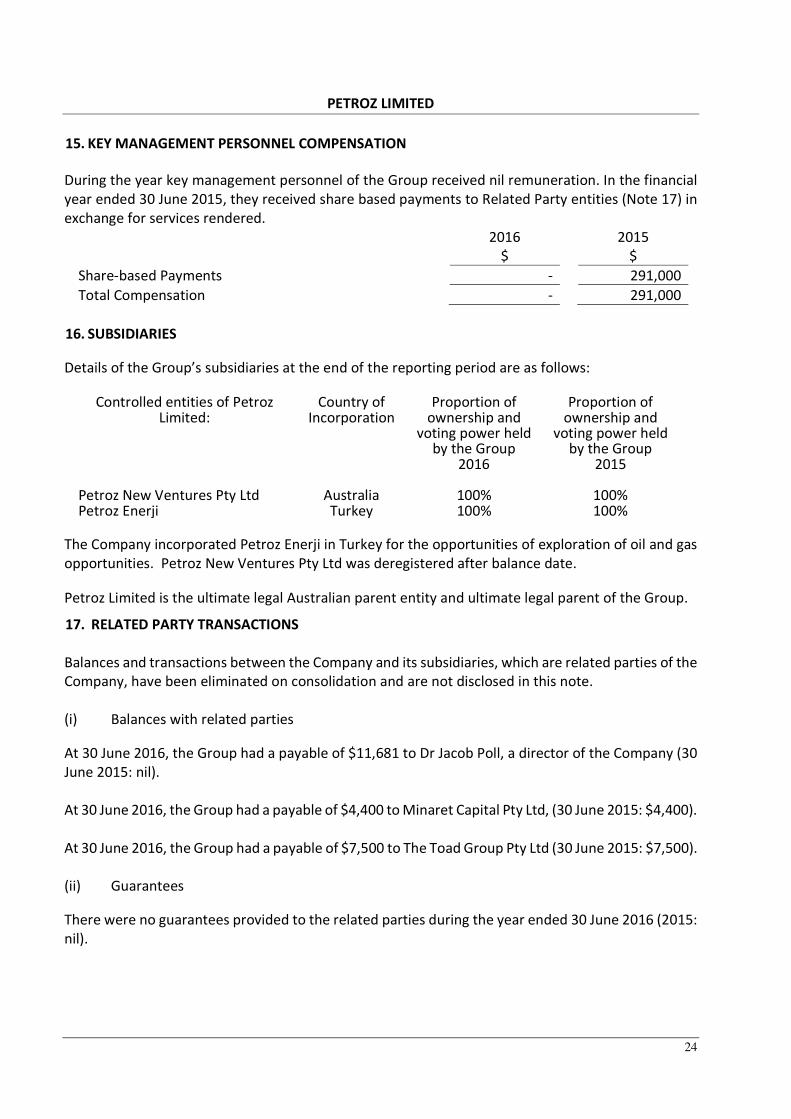

15. KEY MANAGEMENT PERSONNEL COMPENSATION

During the year key management personnel of the Group received nil remuneration. In the financial year ended 30 June 2015, they received share based payments to Related Party entities (Note 17) in exchange for services rendered.

2016 $

2015 $

Share-based Payments - 291,000 Total Compensation - 291,000

16. SUBSIDIARIES

Details of the Group’s subsidiaries at the end of the reporting period are as follows:

Controlled entities of Petroz Limited:

Country of Incorporation

Proportion of ownership and

voting power held by the Group

Proportion of ownership and

voting power held by the Group

2016 2015 Petroz New Ventures Pty Ltd Australia 100% 100% Petroz Enerji Turkey 100% 100%

The Company incorporated Petroz Enerji in Turkey for the opportunities of exploration of oil and gas opportunities. Petroz New Ventures Pty Ltd was deregistered after balance date.

Petroz Limited is the ultimate legal Australian parent entity and ultimate legal parent of the Group.

17. RELATED PARTY TRANSACTIONS Balances and transactions between the Company and its subsidiaries, which are related parties of the Company, have been eliminated on consolidation and are not disclosed in this note. (i) Balances with related parties At 30 June 2016, the Group had a payable of $11,681 to Dr Jacob Poll, a director of the Company (30 June 2015: nil). At 30 June 2016, the Group had a payable of $4,400 to Minaret Capital Pty Ltd, (30 June 2015: $4,400). At 30 June 2016, the Group had a payable of $7,500 to The Toad Group Pty Ltd (30 June 2015: $7,500). (ii) Guarantees

There were no guarantees provided to the related parties during the year ended 30 June 2016 (2015: nil).

PETROZ LIMITED

25

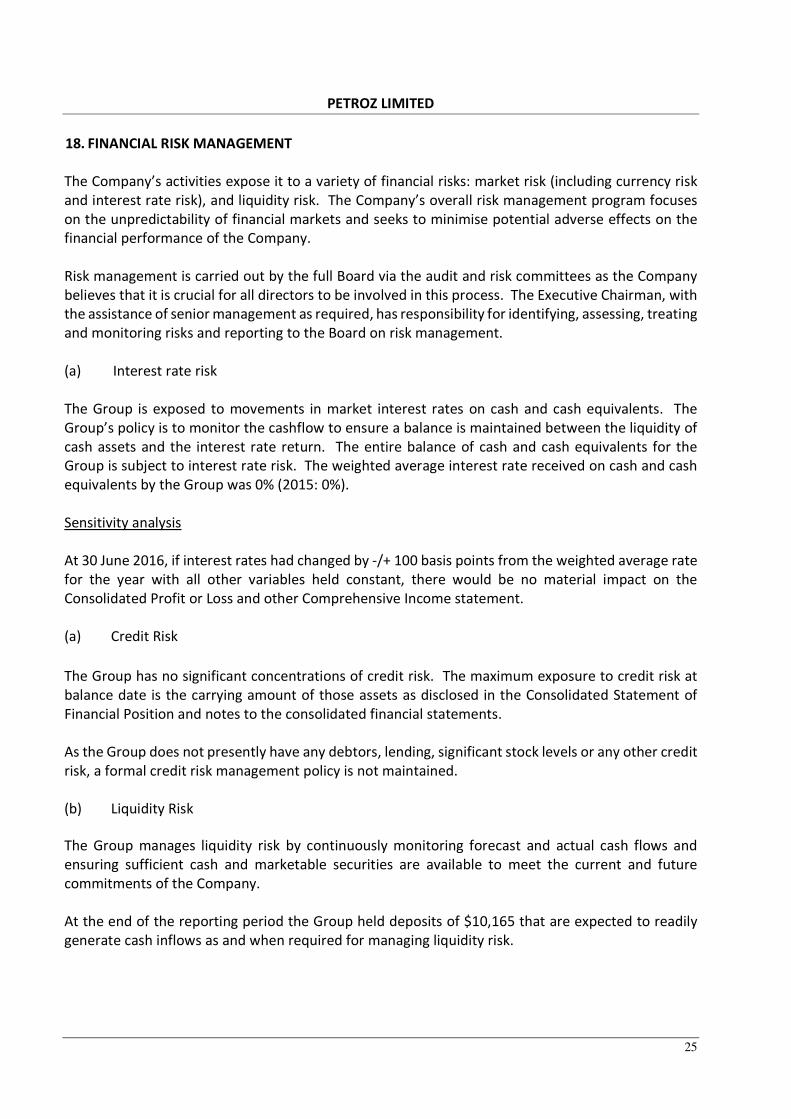

18. FINANCIAL RISK MANAGEMENT

The Company’s activities expose it to a variety of financial risks: market risk (including currency risk and interest rate risk), and liquidity risk. The Company’s overall risk management program focuses on the unpredictability of financial markets and seeks to minimise potential adverse effects on the financial performance of the Company. Risk management is carried out by the full Board via the audit and risk committees as the Company believes that it is crucial for all directors to be involved in this process. The Executive Chairman, with the assistance of senior management as required, has responsibility for identifying, assessing, treating and monitoring risks and reporting to the Board on risk management. (a) Interest rate risk The Group is exposed to movements in market interest rates on cash and cash equivalents. The Group’s policy is to monitor the cashflow to ensure a balance is maintained between the liquidity of cash assets and the interest rate return. The entire balance of cash and cash equivalents for the Group is subject to interest rate risk. The weighted average interest rate received on cash and cash equivalents by the Group was 0% (2015: 0%). Sensitivity analysis At 30 June 2016, if interest rates had changed by -/+ 100 basis points from the weighted average rate for the year with all other variables held constant, there would be no material impact on the Consolidated Profit or Loss and other Comprehensive Income statement.

(a) Credit Risk

The Group has no significant concentrations of credit risk. The maximum exposure to credit risk at balance date is the carrying amount of those assets as disclosed in the Consolidated Statement of Financial Position and notes to the consolidated financial statements. As the Group does not presently have any debtors, lending, significant stock levels or any other credit risk, a formal credit risk management policy is not maintained. (b) Liquidity Risk

The Group manages liquidity risk by continuously monitoring forecast and actual cash flows and ensuring sufficient cash and marketable securities are available to meet the current and future commitments of the Company. At the end of the reporting period the Group held deposits of $10,165 that are expected to readily generate cash inflows as and when required for managing liquidity risk.

PETROZ LIMITED

26

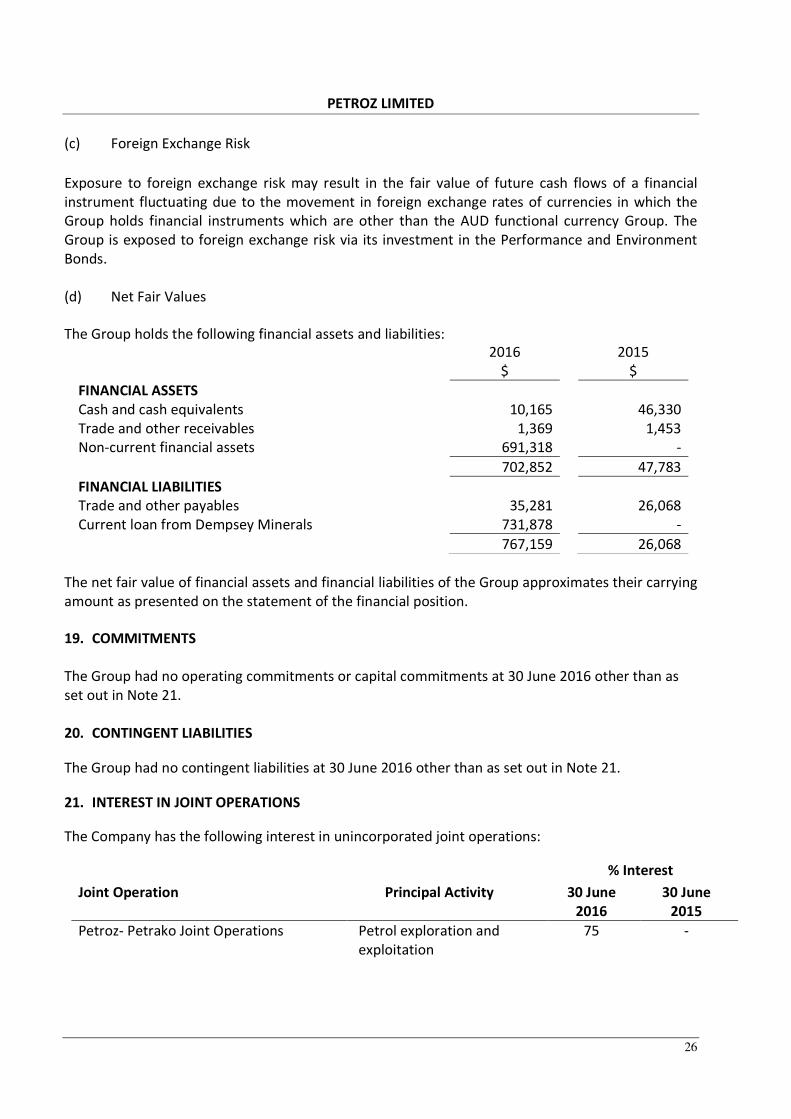

(c) Foreign Exchange Risk

Exposure to foreign exchange risk may result in the fair value of future cash flows of a financial instrument fluctuating due to the movement in foreign exchange rates of currencies in which the Group holds financial instruments which are other than the AUD functional currency Group. The Group is exposed to foreign exchange risk via its investment in the Performance and Environment Bonds. (d) Net Fair Values

The Group holds the following financial assets and liabilities: 2016

$ 2015

$ FINANCIAL ASSETS Cash and cash equivalents 10,165 46,330 Trade and other receivables 1,369 1,453 Non-current financial assets 691,318 - 702,852 47,783 FINANCIAL LIABILITIES Trade and other payables 35,281 26,068 Current loan from Dempsey Minerals 731,878 - 767,159 26,068

The net fair value of financial assets and financial liabilities of the Group approximates their carrying amount as presented on the statement of the financial position.

19. COMMITMENTS The Group had no operating commitments or capital commitments at 30 June 2016 other than as set out in Note 21. 20. CONTINGENT LIABILITIES The Group had no contingent liabilities at 30 June 2016 other than as set out in Note 21. 21. INTEREST IN JOINT OPERATIONS

The Company has the following interest in unincorporated joint operations:

% Interest Joint Operation Principal Activity 30 June

2016 30 June

2015 Petroz- Petrako Joint Operations Petrol exploration and

exploitation 75 -

PETROZ LIMITED

27

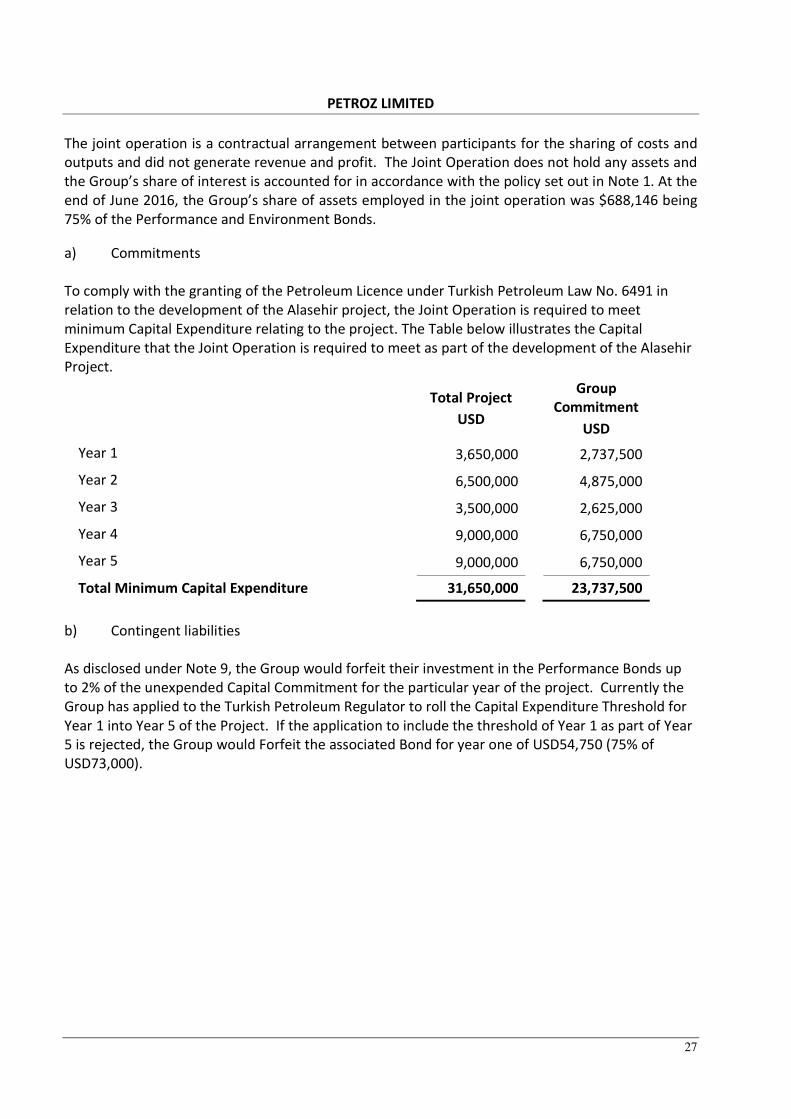

The joint operation is a contractual arrangement between participants for the sharing of costs and outputs and did not generate revenue and profit. The Joint Operation does not hold any assets and the Group’s share of interest is accounted for in accordance with the policy set out in Note 1. At the end of June 2016, the Group’s share of assets employed in the joint operation was $688,146 being 75% of the Performance and Environment Bonds.

a) Commitments To comply with the granting of the Petroleum Licence under Turkish Petroleum Law No. 6491 in relation to the development of the Alasehir project, the Joint Operation is required to meet minimum Capital Expenditure relating to the project. The Table below illustrates the Capital Expenditure that the Joint Operation is required to meet as part of the development of the Alasehir Project.

Total Project USD

Group

Commitment USD

Year 1 3,650,000 2,737,500

Year 2 6,500,000 4,875,000

Year 3 3,500,000 2,625,000

Year 4 9,000,000 6,750,000

Year 5 9,000,000 6,750,000

Total Minimum Capital Expenditure 31,650,000 23,737,500 b) Contingent liabilities As disclosed under Note 9, the Group would forfeit their investment in the Performance Bonds up to 2% of the unexpended Capital Commitment for the particular year of the project. Currently the Group has applied to the Turkish Petroleum Regulator to roll the Capital Expenditure Threshold for Year 1 into Year 5 of the Project. If the application to include the threshold of Year 1 as part of Year 5 is rejected, the Group would Forfeit the associated Bond for year one of USD54,750 (75% of USD73,000).

PETROZ LIMITED

28

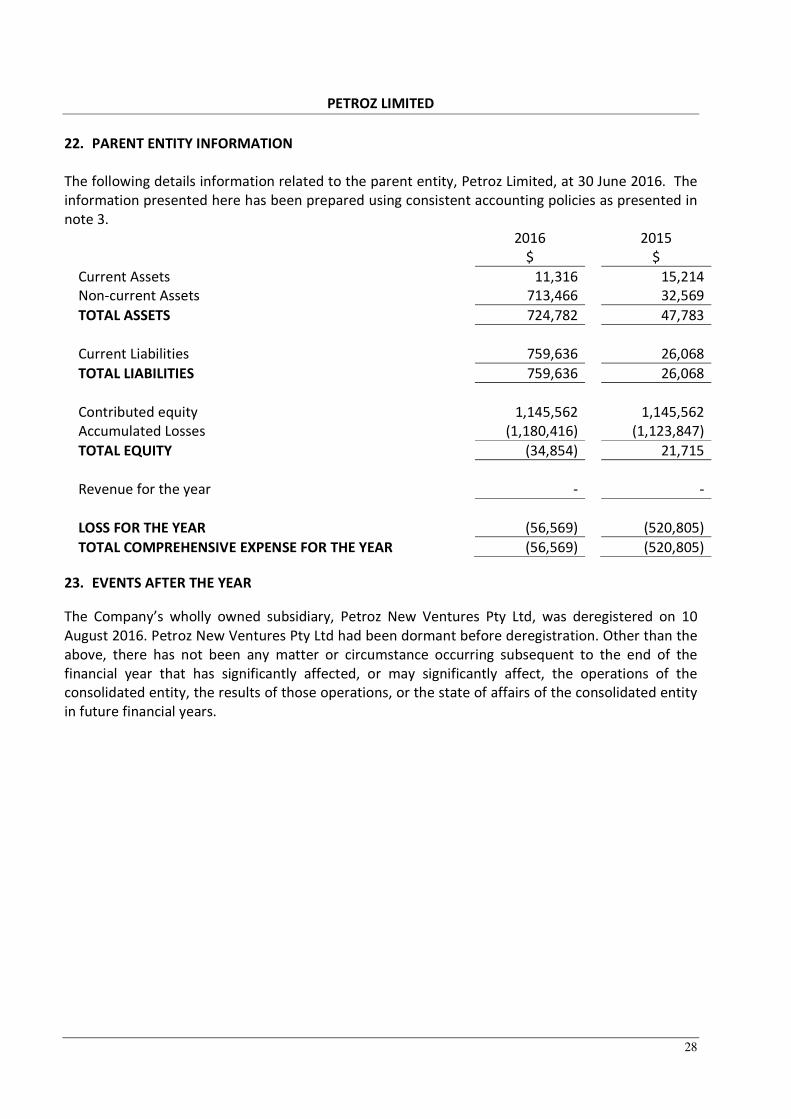

22. PARENT ENTITY INFORMATION

The following details information related to the parent entity, Petroz Limited, at 30 June 2016. The information presented here has been prepared using consistent accounting policies as presented in note 3.

2016 2015 $ $ Current Assets 11,316 15,214 Non-current Assets 713,466 32,569 TOTAL ASSETS 724,782 47,783 Current Liabilities 759,636 26,068 TOTAL LIABILITIES 759,636 26,068 Contributed equity 1,145,562 1,145,562 Accumulated Losses (1,180,416) (1,123,847) TOTAL EQUITY (34,854) 21,715 Revenue for the year - - LOSS FOR THE YEAR (56,569) (520,805) TOTAL COMPREHENSIVE EXPENSE FOR THE YEAR (56,569) (520,805)

23. EVENTS AFTER THE YEAR

The Company’s wholly owned subsidiary, Petroz New Ventures Pty Ltd, was deregistered on 10 August 2016. Petroz New Ventures Pty Ltd had been dormant before deregistration. Other than the above, there has not been any matter or circumstance occurring subsequent to the end of the financial year that has significantly affected, or may significantly affect, the operations of the consolidated entity, the results of those operations, or the state of affairs of the consolidated entity in future financial years.

PETROZ LIMITED

29

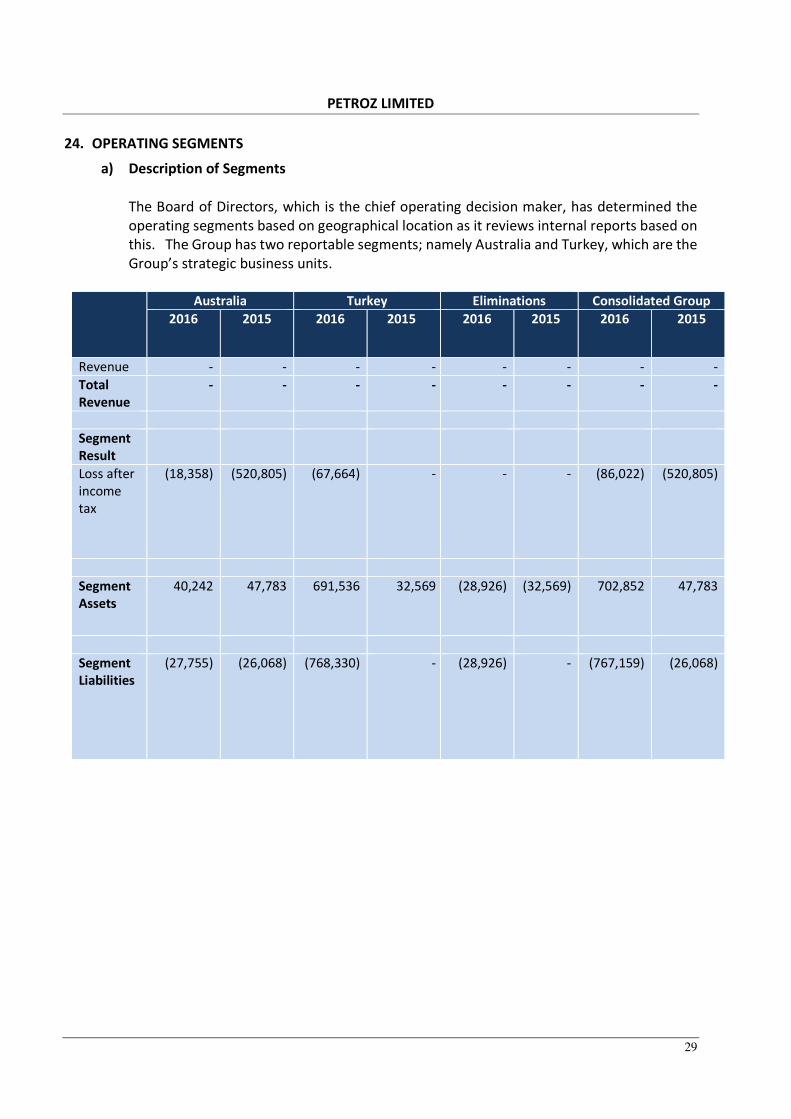

24. OPERATING SEGMENTS

a) Description of Segments The Board of Directors, which is the chief operating decision maker, has determined the

operating segments based on geographical location as it reviews internal reports based on this. The Group has two reportable segments; namely Australia and Turkey, which are the Group’s strategic business units.

Australia Turkey Eliminations Consolidated Group

2016 2015 2016 2015 2016 2015 2016 2015

Revenue - - - - - - - - Total Revenue

- - - - - - - -

Segment Result

Loss after income tax

(18,358) (520,805) (67,664) - - - (86,022) (520,805)

Segment Assets

40,242 47,783 691,536 32,569 (28,926) (32,569) 702,852 47,783

Segment Liabilities

(27,755) (26,068) (768,330) - (28,926) - (767,159) (26,068)

PETROZ LIMITED

30

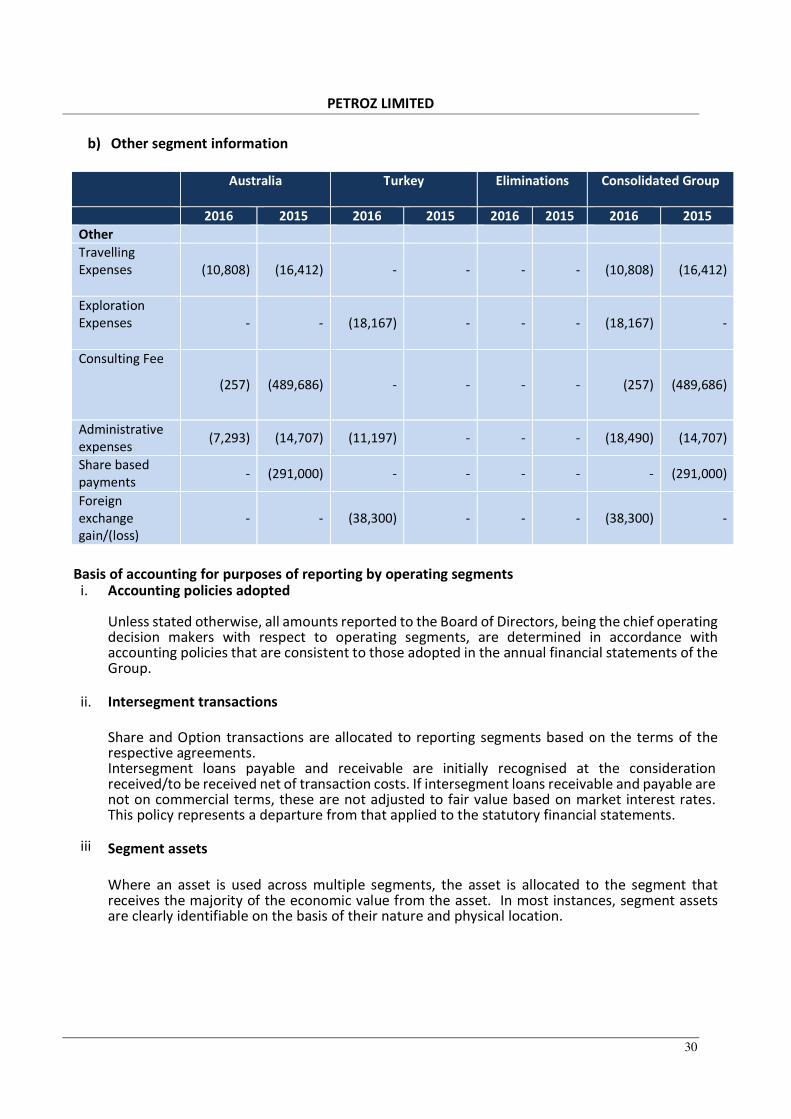

b) Other segment information

Australia Turkey Eliminations Consolidated Group

2016 2015 2016 2015 2016 2015 2016 2015 Other Travelling Expenses (10,808) (16,412) - - - - (10,808) (16,412)

Exploration Expenses - - (18,167) - - - (18,167) -

Consulting Fee

(257) (489,686) - - - - (257) (489,686)

Administrative expenses (7,293) (14,707) (11,197) - - - (18,490) (14,707)

Share based payments - (291,000) - - - - - (291,000)

Foreign exchange gain/(loss)

- - (38,300) - - - (38,300) -

Basis of accounting for purposes of reporting by operating segments

i. Accounting policies adopted

Unless stated otherwise, all amounts reported to the Board of Directors, being the chief operating decision makers with respect to operating segments, are determined in accordance with accounting policies that are consistent to those adopted in the annual financial statements of the Group.

ii. Intersegment transactions

Share and Option transactions are allocated to reporting segments based on the terms of the respective agreements.

Intersegment loans payable and receivable are initially recognised at the consideration received/to be received net of transaction costs. If intersegment loans receivable and payable are not on commercial terms, these are not adjusted to fair value based on market interest rates. This policy represents a departure from that applied to the statutory financial statements.

iii Segment assets

Where an asset is used across multiple segments, the asset is allocated to the segment that receives the majority of the economic value from the asset. In most instances, segment assets are clearly identifiable on the basis of their nature and physical location.

PETROZ LIMITED

31

iv Segment liabilities

Liabilities are allocated to segments where there is a direct nexus between the incurrence of the liability and the operations of the segment. Borrowings and tax liabilities are generally considered to relate to the Group as a whole and are not allocated. Segment liabilities include trade and other payables and certain direct borrowings.

v. Unallocated items

The following items of revenue, expenses, assets and liabilities (if applicable) are not allocated to operating segments as they are not considered part of the core operations of any segment: • impairment of assets and other non-recurring items of revenue or expense; • income tax expense; • deferred tax assets and liabilities; • current tax liabilities; • other financial liabilities; • intangible assets;