appendix cip - cengageappendix cip accounting for changes in prices objectives 1 understand the...

TRANSCRIPT

a p p e n d i x C I P

Accounting for Changes in Prices

o b j e c t i v e s

1 Understand the difference between current value andgeneral price level adjustments.

2 Explain the three alternatives to historical cost.

3 Understand issues related to the measurement ofcurrent cost, the adjustment of historical dollars forgeneral price-level changes, and the purchasing powergain or loss on net monetary items.

4 Explain the conceptual issues relating to the alternativesto historical cost.

5 Be aware of the disclosure requirements that haveexisted for alternative disclosures, including the reasonsfor the elimination of the required disclosures.

Current Value and the General Price Level CIP3

In Chapter 18, we focused on asset valuation and revenue recognition issues usinghistorical cost accounting. However, different methods of asset valuation providedifferent information to users if the prices of individual assets owned by companieschange with time. Suppose a company purchases a parcel of land for $100,000. A yearlater the value of the land is $120,000, but there has been inflation of 5%. Theoreti-cally, the company could value the land on its balance sheet either at its current valueof $120,000 or at $105,000—the historical cost of $100,000 adjusted for the 5% infla-tion. However, under generally accepted accounting principles, the company values theland on its balance sheet at $100,000. In other words, the change in the value of theland is ignored, as is the change in the value of the dollar due to inflation.

Furthermore, under historical cost accounting the effect of a change in value isgenerally recognized only when a transaction takes place, such as when the land is sold.Suppose that the company sells the land for $120,000. At this time, it recognizes a gainof $20,000 (the $120,000 selling price less the $100,000 original cost). However, shouldit recognize a gain of zero ($120,000 less the $120,000 current value) or of $15,000($120,000 less the $105,000 historical cost adjusted for the 5% inflation rate) instead?Which information is more useful to users of financial statements?

This Appendix briefly explains the concepts and procedures underlying the alterna-tive methods of accounting for changing prices. We also discuss the voluntary supple-mentary disclosures encouraged by FASB Statement No. 89.

CURRENT VALUE AND THE GENERAL PRICE LEVELTwo types of price changes are relevant for accounting purposes. First, the price of anindividual asset or liability, such as inventory, buildings, or bonds payable, changes inresponse to the dynamics of the market for that particular item. This is known as aspecific price change or a current value change. Second, there may be a change in thevalue, or purchasing power, of the dollar. Such a change is caused by the overall changein the prices of all goods and services in the economy and is known as a general price-level change. Changes in the general purchasing power of money are known as infla-tion or deflation. During inflation (deflation), the general purchasing power of moneydeclines (increases) as the general level of prices of goods and services rises (falls). Thegeneral purchasing power of money and the general price level are reciprocals.

For a company’s specific assets and liabilities, the price changes may be very differ-ent from the change in the general price level. For example, if the general price levelrises, the specific price of an inventory item (its current value) may increase faster orslower, or even decline, in comparison with the general price level.

So the two types of price changes are related, but it is important to understand thataccounting for the current value of assets and accounting for changes in the generalprice level are not alternatives or substitutes for each other. Each method represents theuse of a different concept and, therefore, has a different purpose. Although neithermethod is required under generally accepted accounting principles, selected current costand general price-level adjusted supplementary disclosures are encouraged (but notrequired) under FASB Statement No. 89, as we discuss later in this Appendix.

Current Value

Current value adjustments account for changes in the values of individual assets andliabilities and not for the change in the value of the dollar. As the specific currentvalues change, they are recognized in the financial statements by recording assets andliabilities on the balance sheet at their current values. In the income statement,expenses are matched against revenues at the current value of the assets used up orthe liabilities created. Therefore, this method significantly changes the basic conceptsof asset valuation and income measurement. Current value is a general concept andmay be measured in several ways, including (1) an exit value, such as net realizablevalue (the net amount that can be realized from sale), (2) the present value of futurecash flows, and (3) an input value, such as current cost. Our discussion concentrates

Understand thedifference be-tween currentvalue and gen-eral price leveladjustments.

1

CIP4 Appendix CIP Accounting for Changes in Prices

on current cost as the measure of current value because this method is the basis forthe current value disclosures encouraged by FASB Statement No. 89. Current cost isthe cost in the current period of replacing (i.e., acquiring or producing) the itemsconcerned, as we discuss later. Generally accepted accounting principles do allowoccasional uses of current value, such as when there is a decline in the price of inven-tory and the lower of cost or market rule is used, and for certain investments andfinancial instruments.

General Price Level

General price-level adjustments account for the change in the value of the dollar andnot for changes in the values of individual assets and liabilities. As the general pricelevel increases, the goods and services that can be purchased with a given number ofdollars decreases. Therefore, financial statements that include dollars measured at dif-ferent times are potentially misleading, because the dollars vary in purchasing power.The adjustments for changes in the general price level convert these dollars of differentpurchasing power into dollars of constant purchasing power. In essence, the adjustmentsaccount for changes in the size of the measuring unit used in accounting. In contrast toa physical measuring unit such as a foot or a meter which remains constant, the dollaris not a constant measure because its purchasing power changes. Just as no one advocatesadding and subtracting U.S. and Canadian dollars, for example, it can be argued thatit is equally inappropriate to add and subtract dollars of different purchasing power,even though they are always called U.S. dollars.

Four Alternative Concepts

Just as with historical costs, current costs may be measured in different time periods.Since the general price-level adjustments account only for the change in the value of thedollar over time, these adjustments are equally applicable to historical cost and currentcost financial statements. In both cases, amounts are included in the adjusted financialstatements (or selected supplemental disclosures) that are measured in dollars ofdifferent dates, and so of different values. Thus, there are four alternative accountingmethods to be considered (the common terminology used to differentiate the alterna-tives is in parentheses):

1. Historical cost2. Historical cost adjusted for changes in the general price level (historical cost/

constant purchasing power)3. Current value (current cost)4. Current value adjusted for changes in the general price level (current cost/

constant purchasing power)

Constant purchasing power amounts also are known as constant dollar amounts. Thehistorical cost concept, which is the basis of generally accepted accounting principles,is covered throughout this book. We discuss the other three alternatives in the followingsection.

THREE ALTERNATIVES TO HISTORICAL COSTTo briefly illustrate the differences between constant purchasing power and current costfinancial statements, consider the following sequence of events for the Hallas Company:

1. The company begins operations with $3,000 cash from issuing capital stock.2. The company purchases one unit of inventory for $1,000 cash.3. The current (replacement) cost of the inventory increases to $1,250 and the

general price-level index increases from 100 to 110, an increase of 10%.4. The company sells the inventory for $2,000 cash.5. The company purchases another unit of inventory for $1,250.

Explain thethree alterna-tives to historicalcost.

2

Three Alternatives to Historical Cost CIP5

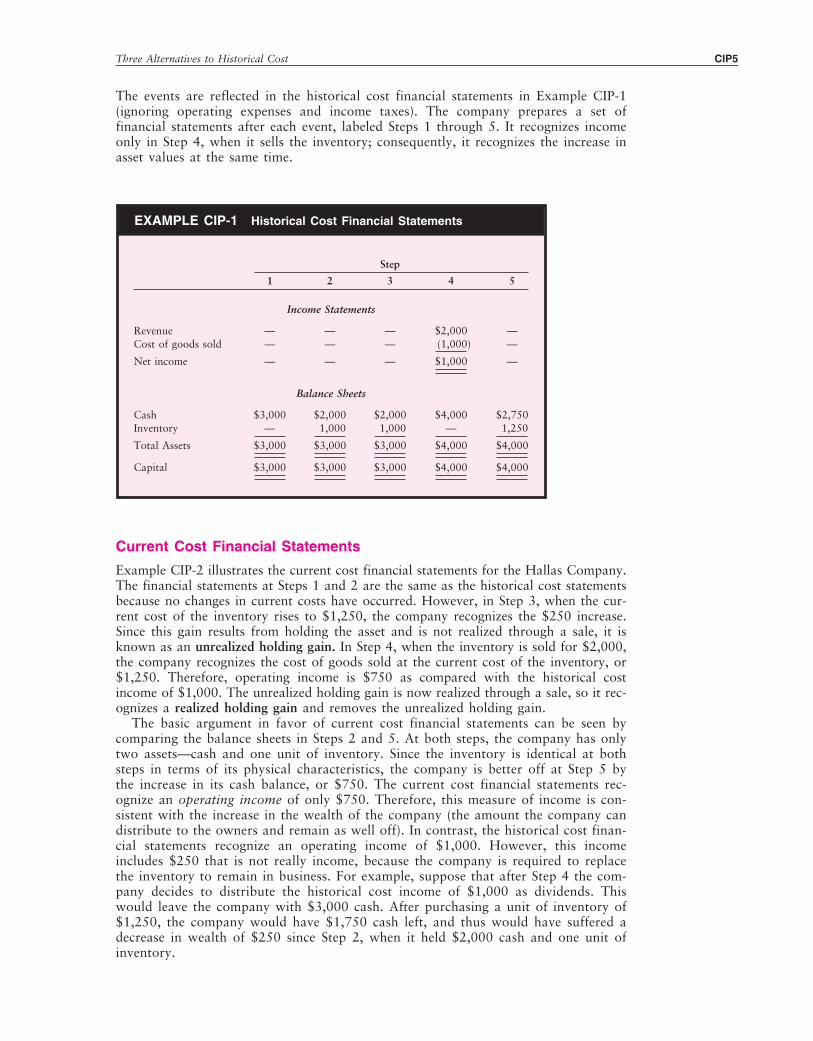

The events are reflected in the historical cost financial statements in Example CIP-1(ignoring operating expenses and income taxes). The company prepares a set offinancial statements after each event, labeled Steps 1 through 5. It recognizes incomeonly in Step 4, when it sells the inventory; consequently, it recognizes the increase inasset values at the same time.

EXAMPLE CIP-1 Historical Cost Financial Statements

Step

1 2 3 4 5

Income Statements

Revenue — — — $2,000 —Cost of goods sold — — — (1,000) —

Net income — — — $1,000 —

Balance Sheets

Cash $3,000 $2,000 $2,000 $4,000 $2,750Inventory — 1,000 1,000 — 1,250

Total Assets $3,000 $3,000 $3,000 $4,000 $4,000

Capital $3,000 $3,000 $3,000 $4,000 $4,000

Current Cost Financial Statements

Example CIP-2 illustrates the current cost financial statements for the Hallas Company.The financial statements at Steps 1 and 2 are the same as the historical cost statementsbecause no changes in current costs have occurred. However, in Step 3, when the cur-rent cost of the inventory rises to $1,250, the company recognizes the $250 increase.Since this gain results from holding the asset and is not realized through a sale, it isknown as an unrealized holding gain. In Step 4, when the inventory is sold for $2,000,the company recognizes the cost of goods sold at the current cost of the inventory, or$1,250. Therefore, operating income is $750 as compared with the historical costincome of $1,000. The unrealized holding gain is now realized through a sale, so it rec-ognizes a realized holding gain and removes the unrealized holding gain.

The basic argument in favor of current cost financial statements can be seen bycomparing the balance sheets in Steps 2 and 5. At both steps, the company has only two assets—cash and one unit of inventory. Since the inventory is identical at bothsteps in terms of its physical characteristics, the company is better off at Step 5 bythe increase in its cash balance, or $750. The current cost financial statements rec-ognize an operating income of only $750. Therefore, this measure of income is con-sistent with the increase in the wealth of the company (the amount the company candistribute to the owners and remain as well off). In contrast, the historical cost finan-cial statements recognize an operating income of $1,000. However, this incomeincludes $250 that is not really income, because the company is required to replacethe inventory to remain in business. For example, suppose that after Step 4 the com-pany decides to distribute the historical cost income of $1,000 as dividends. Thiswould leave the company with $3,000 cash. After purchasing a unit of inventory of$1,250, the company would have $1,750 cash left, and thus would have suffered adecrease in wealth of $250 since Step 2, when it held $2,000 cash and one unit ofinventory.

CIP6 Appendix CIP Accounting for Changes in Prices

Note that the company includes the unrealized and realized holding gains in incomein this example. Many accountants, however, argue that these gains are not really income,as we illustrated in the previous paragraph. Therefore, they argue, the gains should beexcluded from the income statement and reported directly in stockholders’ equity, or inother comprehensive income. Whichever way the gains (or losses) are classified, it is veryimportant to understand the nature of these gains in contrast to income that representsreal profit obtained through a sale.

Historical Cost/Constant Purchasing Power Financial Statements

Example CIP-3 illustrates the historical cost/constant purchasing power financial state-ments of the Hallas Company. Remember that this adjustment process is completelyseparate from the current cost financial statements we just discussed. The only changein the general price level is in Step 3, when the price-level index rises from 100 to 110,an increase of 10%. When the company originally prepared the financial statementsfor Steps 1 and 2, they were identical to the historical cost financial statements inExample CIP-1 because no change in the general price level had occurred. However,all the financial statements in Example CIP-3 are presented in terms of the value ofthe dollar after the 10% increase in the price level (that is, in Step 3 prices). There-fore, the cash and capital in Step 1, and the cash, inventory, and capital in Step 2 areall increased by 10% to reflect the increase in the general price level that has occurredsince these amounts were measured originally. For example, the $3,000 in the histor-ical cost balance sheet in Step 1 of Example CIP-1 is measured in dollars before therise in the general price level. This amount has a purchasing power that is equivalentto $3,300 after the price rise (an increase of 10%). The $3,000 measured in dollarsbefore the price rise is adjusted to $3,300 measured in dollars after the price rise, sothat the statements in Steps 1 and 3 reflect dollars of the same purchasing power.

The rise in the general price level takes place in Step 3. Thus, the $2,000 cash in thehistorical cost balance sheet is measured in dollars after the price-level increase. As aresult, the company has lost $200 ($2,200 � $2,000) of purchasing power because itheld the cash while the price level rose. This $200 loss is included in income, and italso reduces the purchasing power of the capital to $3,100. The inventory is measuredat the historical cost of $1,000 adjusted for the 10% increase in the general price level.

EXAMPLE CIP-2 Current Cost Financial Statements

Step

1 2 3 4 5

Income Statements

Revenue — — — $2,000 —Cost of goods sold — — — (1,250) —

Operating income — — — $ 750 —Unrealized holding gain — — $ 250 (250) —Realized holding gain — — — 250 —Net income — — $ 250 $ 750 —

Balance Sheets

Cash $3,000 $2,000 $2,000 $4,000 $2,750Inventory — 1,000 1,250 — 1,250

Total Assets $3,000 $3,000 $3,250 $4,000 $4,000

Capital $3,000 $3,000 $3,250 $4,000 $4,000

Three Alternatives to Historical Cost CIP7

The $1,100 is the current purchasing-power equivalent of the original $1,000. Nopurchasing-power gain or loss results from holding a nonmonetary asset such as inven-tory, as we discuss later in the appendix. In Step 4 the inventory is sold for $2,000.The cost of goods sold is recorded at the constant purchasing power of the inventory,$1,100, and therefore the net income is $900.

The major argument in favor of historical cost/constant purchasing power financialstatements can be illustrated by considering the income statement in Step 4 and the bal-ance sheets in Steps 1 and 4. In the historical cost income statement in Example CIP-1,dollars of one price level (the cost of goods sold) are subtracted from dollars of anotherprice level (the revenue). Since these dollars do not have the same purchasing power,subtracting one from the other may not be very relevant. In contrast, the constant pur-chasing power income is measured by comparing two amounts measured in dollars ofthe same purchasing power.

Comparing Steps 1 and 4 in the historical cost balance sheets in Example CIP-1 raisessimilar issues. The capital in Step 4 includes $3,000 original capital (and $1,000 retainedearnings). However, Step 1 also shows original capital of $3,000. Does this reflectreality? If it is agreed that the purpose of dollars is to purchase goods and services, thento show the contributed capital as $3,000 in both balance sheets may be misleading.The owners of the company contributed $3,000 of purchasing power in Step 1 whenthe company was formed. However, in Step 4 an appropriate measure of the capitalcontributed is in terms of the dollars existing at the time the financial statements areprepared. In these terms, the owners have contributed $3,300 of purchasing power. Thesame argument may be applied to inventory. Although the inventory cost $1,000, that$1,000 is equivalent to $1,100 of purchasing power after the price-level increase. Thus,the historical cost/constant purchasing power financial statements do not reflect currentvalue. They simply adjust the historical costs for changes in the purchasing power, orvalue, of the dollar that have occurred since the historical cost was recorded.

Current Cost/Constant Purchasing Power Financial Statements

The arguments in favor of current cost financial statements and of historical cost/constantpurchasing power statements are entirely separate. Current cost financial statements do

EXAMPLE CIP-3 Historical Cost/Constant Purchasing Power Financial Statements

Step

1 2 3 4 5

Income Statements

Revenue — — — $2,000 —Cost of goods sold — — — (1,100) —Purchasing power loss — — $ (200) — —

Net income — — $ (200) $ 900 —

Balance Sheets

Cash $3,300 $2,200 $2,000 $4,000 $2,750Inventory — 1,100 1,100 — 1,250

Total Assets $3,300 $3,300 $3,100 $4,000 $4,000

Capital $3,300 $3,300 $3,100 $4,000 $4,000

General price-level index: Step 1, 100; Step 2, 100; Step 3, 110; Step 4, 110; andStep 5, 110.

CIP8 Appendix CIP Accounting for Changes in Prices

not reflect the changing value of the dollar, and historical cost/constant purchasing powerstatements do not recognize the current cost of assets. However, the two concepts maybe combined so that financial statements prepared on the current cost basis are adjustedfor changes in the general price level. Example CIP-4 illustrates financial statements pre-pared on this basis.

EXAMPLE CIP-4 Current Cost/Constant Purchasing Power Financial Statements

Step

1 2 3 4 5

Income Statements

Revenue — — — $2,000 —Cost of goods sold — — — (1,250) —

Operating income — — — $ 750 —Unrealized holding gain — — $ 150 (150) —Realized holding gain — — — 150 —Purchasing-power loss — — (200) — —Net income — — $ (50) $ 750 —

Balance Sheets

Cash $3,300 $2,200 $2,000 $4,000 $2,750Inventory — 1,100 1,250 — 1,250

Total Assets $3,300 $3,300 $3,250 $4,000 $4,000

Capital $3,300 $3,300 $3,250 $4,000 $4,000

The financial statements in Steps 1 and 2 are prepared on a current cost/constantpurchasing power basis in terms of the price level existing after the rise in the generalprice level. That is, they are adjusted to reflect the 10% rise in the price level in the samemanner as the historical cost/constant purchasing power statements in Example CIP-3. InStep 3 the rise in the general price level is recognized through the purchasing-power lossfrom holding cash. In addition, the unrealized holding gain on the inventory is recog-nized, but in this situation it is $150. This is the difference between the current cost ofthe inventory ($1,250) and the constant purchasing power cost of the inventory ($1,100).In Step 4 the inventory is sold and the cost of goods sold is recorded at the current costof $1,250.

The advantages of this method may be understood by considering the income state-ment in Step 4 and by comparing the balance sheets in Steps 2 and 5. The $750 oper-ating income recognized in Step 4 is the real increase in value for the company, forexactly the same reasons as we discussed earlier for the unadjusted current cost finan-cial statements in Example CIP-2. A comparison of the balance sheets in Steps 2 and 5shows an increase in value of $550 since the cash has increased by $550 and one unitof inventory is held in each case. The $550 increase is the operating income of $750in Step 4 less the purchasing power loss of $200 in Step 3. The relationship betweenthe increase in wealth and the income statement is clearer if the holding gains are omit-ted from the income statement, which lends support to those accountants who advo-cate such exclusion.

Additional Measurement Issues CIP9

ADDITIONAL MEASUREMENT ISSUESThe previous section dealt with a simple example involving current cost and constantpurchasing power financial statements. We discuss several additional issues related tomeasuring current costs and constant purchasing power amounts in this section.

Measurement of Current Cost

In the previous examples we focused on a few simple transactions. The two most sig-nificant differences between current cost and historical cost usually occur for inventoryand property, plant, and equipment. The FASB defines the current cost of inventory asthe current cost of purchasing or producing the goods concerned. It defines the currentcost of property, plant, or equipment as the current cost of acquiring the same servicepotential (indicated by operating costs and physical output capacity) provided by theasset owned.1

Three alternative methods of measuring the current costs of inventory and property,plant, and equipment are:

1. Direct Pricing. Current invoice prices, vendors’ price lists, other quotations orestimates (e.g., appraisals), or standard manufacturing costs.

2. Functional or Unit Pricing. The estimation of construction (or acquisition) costsper unit (such as per square foot of building space) and multiplication by thenumber of units in the asset being measured.

3. Revision of Historical Acquisition Cost (Indexation). Using (a) externally (inde-pendently) generated specific price indexes2 for the class of goods or services being measured, or (b) internally generated indexes of cost changes for the classof goods or services being measured.3

A company might choose any one of the methods for any asset or liability. Generallydirect pricing would be used for inventory and readily available property, plant, andequipment such as office equipment. Functional, or unit, pricing would be used to esti-mate the current cost of a complete productive asset such as a building or a chemicalplant. A specific price index could be used for any asset, and often it is the simplest touse because once the index for the asset is selected, the adjustment process is arith-metically simple.

Because technology changes, the property, plant, and equipment (and perhaps someinventory) that would be purchased today do not have the same service potential as theassets the company owns. Therefore, the current cost of property, plant, and equipmentmay be determined by either (1) the current cost of a used asset of the same age andin the same condition as the asset owned, (2) the current cost of a new asset with thesame service potential as the used asset had when new, less a deduction for deprecia-tion, or (3) the current cost of a new asset with a different service potential, less adeduction for depreciation, and adjusted for the cost of the difference in service poten-tial due to differences in life, output capacity, and nature of service, including anyoperating cost savings.

Inventory is valued on the balance sheet at its current cost at the end of the period.The cost of goods sold is valued on the income statement at the average current cost,which is measured as the units sold � [(beginning current cost per unit � ending currentcost per unit) � 2]. Alternatively, the actual current costs incurred during the periodcould be used if the company recorded the current cost when each sale was made.

1. “Financial Reporting and Changing Prices,” FASB Statement of Financial Accounting Standards No. 89(Stamford, Conn.: FASB, 1986), par. 44.

2. The federal government publishes numerous specific price indexes.3. These are examples of a reproduction cost, which is the current cost of acquiring an asset identical to that

currently owned. An alternative concept is a replacement cost, which is the current cost of acquiring thebest asset available to undertake the function of the asset owned.

Understandissues related tothe measure-ment of currentcost, the adjust-ment of histori-cal dollars forgeneral price-level changes,and the pur-chasing powergain or loss onnet monetaryitems.

3

CIP10 Appendix CIP Accounting for Changes in Prices

Property, plant, and equipment are valued on the balance sheet at their current costsat the end of the period, less a proportional amount of accumulated depreciation. Thedepreciation expense on the income statement is based on the average current cost ofthe depreciable assets, which is measured as [(beginning current cost � ending currentcost) � 2] � estimated life. For both costs of goods sold and depreciation expense, anaverage is used because sales are made at prices current throughout the period, and itis appropriate to match the average current cost of the assets used during the periodagainst those sales.

Adjustment of Historical Dollars

The conversion of historical dollars to the purchasing power of the current period bymeans of a price-level index is a simple mathematical procedure. Dividing the index ofthe current period by the index of the period in which the historical dollar was origi-nally recorded provides a measure of the relative price change. Multiplying the histor-ical dollar amount by this relative price change gives the constant purchasing powerdollar amount. This computation is as follows:

Constant Purchasing Current Period Price-Level Index� Historical Dollars �

Power Dollars Historical Price-Level Index

For example, suppose a company purchased land for $24,000 when the price index was120 and that the index is now 150. The cost of the land in constant purchasing powerdollars is $30,000 [$24,000 � (150 � 120)].

The current period index depends on the financial statement. The use of the averageindex for the year is the most appropriate for the income statement and the cash flowstatement, which measure flows over a period of time. The use of the index at the endof the year is the most appropriate for the balance sheet, which measures amounts at theend of the year. The average Consumer Price Index for All Urban Consumers (CPI-U)is used for the disclosures encouraged by FASB Statement No. 89.

Purchasing-Power Gain or Loss on Net Monetary Items

Holding cash during periods of inflation results in a purchasing-power loss. If $100 canbuy a certain quantity of goods and services, and prices later rise, the $100 can thenbuy fewer goods and services, and purchasing power has been lost. The same principleapplies to all monetary assets. A monetary asset is defined as “money or a claim toreceive a sum of money, the amount of which is fixed or determinable without referenceto future prices of specific goods or services.”4 In addition to cash, principal monetaryassets are accounts receivable and notes receivable.

The reverse effect occurs with monetary liabilities. Since an obligation exists to repaya fixed amount of dollars in the future, inflation reduces the purchasing power of thedollars necessary to repay these liabilities, thus resulting in a purchasing-power gain.Principal monetary liabilities include accounts payable, notes payable, and bonds payable.5

Suppose Peter Cameron borrows $1,000 from a bank when the price index is 120.He has a monetary liability of $1,000 and the bank has a monetary asset of $1,000.Disregarding interest, if the money is repaid when the price index is 150, Peter Cameronhas a general purchasing-power gain. The equivalent purchasing power of the $1,000when it is repaid is $1,250 [$1,000 � (150 � 120)], and since he only has to repaythe $1,000, he has a gain of $250. Conversely, the bank has a general purchasing-powerloss because it has received $1,000 in full payment of a historical debt that now has acurrent purchasing-power equivalent of $1,250. Since the bank knows that inflation willoccur, it includes the expected level of inflation when it sets the interest rate.

4. FASB Statement No. 89, op. cit., par. 44.5. For a classification of items as monetary or nonmonetary, see FASB Statement of Financial Accounting

Standards No. 89, par. 96.

Conceptual Issues Relating to Alternatives to Historical Cost CIP11

Monetary assets and liabilities are combined to derive net monetary items on whichgains or losses from inflation are computed. The FASB calls these gains and losses purchasing-power gains and losses. (They are also known as monetary gains and losses,or general price-level gains and losses.) Purchasing-power gains result from holdingnegative net monetary items (liabilities exceed assets) and purchasing-power losses resultfrom holding positive net monetary items (assets exceed liabilities) during periods ofrising general prices.

In contrast to monetary items, holders of nonmonetary assets and liabilities do notgain or lose general purchasing power simply as a result of general price-level changes.If the price of a nonmonetary item changes at the same rate as the general price level,no gain or loss of general purchasing power results. Holders of nonmonetary assets andliabilities gain or lose general purchasing power if the specific price of the item ownedor owed rises or falls faster or slower than the change in the general price level.6

Historical cost financial statements usually report gains and losses on nonmonetaryitems only when the items are sold. Gains and losses from holding nonmonetary itemsare recognized in the period of the sale by inclusion in the profit or loss from the sale.7

CONCEPTUAL ISSUES RELATING TO ALTERNATIVESTO HISTORICAL COSTThe simple examples of the current cost, historical cost/constant purchasing power, andcurrent cost/constant purchasing power concepts discussed in this Appendix focus onthe logic underlying the adjustment processes and deliberately avoid the many com-plexities that would be involved in preparing comprehensive financial statements for acompany.8 In this section we evaluate the three methods in greater detail with respectto selected criteria and compare them with historical cost financial statements. Also, wediscuss the concept of using an exit value as a measure of current value.

Capital Maintenance Concept (Income Statement)

One of the major purposes of financial accounting is to measure a company’s income.But what is income? A common definition is that income for a year is

the amount the corporation can distribute to the owners of equity in the corporation and beas well off at the end of the year as at the beginning.9

This is a useful definition of income, but it does raise the question of what is meant bybeing “as well off.” In other words, what is the capital that is to be maintained duringthe year so that income may be measured as the excess above the capital maintained?Another way of looking at this issue is to consider the distinction between the mainte-nance of capital and the return on capital. During each period, a company first shouldearn enough to maintain the capital invested in the business. Then, any excess, or returnon capital, is considered income.

6. “Financial Statements Restated for General Price-Level Changes,” APB Statement No. 3 (New York:AICPA, 1969), par. 19.

7. Current cost financial statements report (holding) gains and losses on nonmonetary items in the period inwhich the gain or loss occurs. When current cost financial statements are adjusted for general price-levelchanges, the holding gain or loss is adjusted for the purchasing-power gain or loss from holding thenonmonetary items. For example, in Example CIP-4, the unrealized holding gain on the inventory in Step 3is $150. This is the increase in the current cost of $250, less the increase that results from inflation of$100 (10% � $1,000).

8. See APB Statement No. 3, op. cit., Appendix C, for an example of general price-level adjustments, and“Conceptual Framework for Financial Accounting and Reporting: Elements of Financial Statements andTheir Measurement,” FASB Discussion Memorandum (Stamford, Conn.: FASB, 1976), Appendix B, forexamples of general price-level, replacement cost, and general price-level adjusted replacement cost financialstatements.

9. Sydney S. Alexander, “Income Measurement in a Dynamic Economy,” Five Monographs on BusinessIncome (New York: Study Group on Business Income, AICPA, 1950), p. 15.

Explain theconceptualissues relatingto the alterna-tives to his-torical cost.

4

CIP12 Appendix CIP Accounting for Changes in Prices

The capital maintenance concepts underlying each type of financial statement thatwe illustrated in Examples CIP-1 through CIP-4 are as follows:

Financial Statements Capital Maintenance ConceptHistorical cost Historical dollars of capital at the

beginning of the yearHistorical cost/constant purchasing power Purchasing power of the capital at the

beginning of the yearCurrent cost Operating capacity (the ability to

provide goods and services) at thebeginning of the year, measured indollars

Current cost/constant purchasing power Operating capacity (the ability toprovide goods and services), measured in units of constantpurchasing power

Although it may not be reasonable to make a categorical statement that one of thealternative capital maintenance concepts is the best, it should be clear that they aredifferent, and that each has advantages and disadvantages. The historical cost concepthas the advantage of being the most verifiable and widely understood of the differentmethods, but it may not be the most relevant to the needs of the user of financialstatements. The user has no assurance that the purchasing power of a company’s cap-ital is maintained, or that the company can continue to operate at the same level. Inother words, income may be overstated since it is likely to include a return of some ofthe capital as well as a return on the capital.

To ensure that the company maintains the purchasing power of its capital probablywould be considered desirable by most stockholders. They did contribute a certain num-ber of dollars to the company, but they are more concerned about the purchasing powerof those dollars than about the number of their dollars originally contributed. Stock-holders would not be satisfied to get back the same number of dollars as they con-tributed if these dollars represent less purchasing power. Therefore, the stockholders arelikely to be interested in knowing that the purchasing power represented by the capitalof the company is maintained before income is reported as a return on capital. Historicalcost/constant purchasing power income statements disclose this information.

A company needs specific assets to conduct its operations, and it is possible that thecompany could be maintaining the general purchasing power of its capital but not itsability to replace the assets. Use of the current cost concept ensures that the operatingcapability of the company is maintained before it reports earnings as a return on cap-ital. However, when these results are reported in unadjusted dollars, a flexible measur-ing unit is being used. For example, cost of goods sold at its current cost is subtractedfrom sales. Both measures are in terms of current dollars, so no problem exists. But anyholding gain or loss is computed as the difference between the current cost and the his-torical cost of the inventory, and these two values are measured in terms of differentdollar values. Consequently, it is difficult to evaluate the meaning of the holding gain,and also to compare the holding gain with operating income; in each case the twoamounts being compared are measured in different dollar values. Use of currentcost/constant purchasing power income statements resolves these issues.

In summary, the historical dollar/constant purchasing power income statementsresolve one issue with the historical dollar measurement concept, and current costincome statements resolve a different issue. Only current cost/constant purchasing powerincome statements resolve both issues and ensure that income is the excess after thecapital is maintained in terms of operating capacity measured in units of constantpurchasing power.

The primary conceptual argument against the use of current costs is that those costsare not relevant if the intent of the company is to hold and use the asset rather thanto sell it. For example, a company purchases property, plant, and equipment to use it

Conceptual Issues Relating to Alternatives to Historical Cost CIP13

in its operations and not for sale. Therefore it may be argued that the current cost isnot relevant. Also the use of current costs would substantially change the revenue recog-nition and matching principles.

Balance Sheet

The values attached to items on the balance sheet are closely related to the capital main-tenance concept and the resulting rules of valuation and income realization. Historicalcost balance sheets disclose items at the historical dollars exchanged (except for securi-ties reported at fair value). The difficulty of interpreting the information on the balancesheet arises because the dollar figures represent different purchasing powers, and addingand subtracting them is as inappropriate as relating U.S. and Canadian dollars, as wediscussed earlier. Use of historical cost/constant purchasing power amounts does ensurethat all the values on the balance sheet represent equivalent purchasing power.

Current cost balance sheets present assets and liabilities at their current replacementcost or, in other words, at a measure of their current value at the balance sheet date.It is difficult to compare them over time (for example, on the balance sheets for twoyears), however, because of the changing value of the dollar. Only current cost/constantpurchasing power balance sheets value the assets at their current cost and also enhancecomparability over time by measuring current costs in dollars of constant purchasingpower.

Reliability

Historical cost financial statements clearly are the most reliable, and adjusting histori-cal dollars for changes in the general price level affects that reliability very little, if atall. Under FASB Statement No. 89, the historical dollars are adjusted by an indexpublished by the federal government, and all companies would use the same index andfollow established procedures.

Current cost financial statements are considerably less reliable than historical costfinancial statements. Several general approaches (discussed earlier in this Appendix) tothe determination of current cost are available. Although each approach is more suitablefor certain types of assets, there are no requirements that a particular method be usedin any given situation. For example, Shell Oil Company tested four indexes forestimating the current cost of refineries and found that the current cost varied by 25%.

Understandability

An argument frequently made in favor of historical cost financial statements is that theyare more understandable than financial statements prepared under other concepts. Thisis difficult to disagree with, because historical costs have been used for so many years.This argument suggests, however, that no change should ever take place, becauseinitially users would be less familiar with the new method than with the old.

There also is a trend toward giving greater consideration to the needs of sophisti-cated users of financial statements who presumably have, or would soon develop, theability to understand financial statements prepared on a different basis. Many support-ers of the use of a changed concept have argued that the historical cost financial state-ments should be continued and the new data supplied in supplementary form. Thiswould enable users to gain experience with the new methods and concepts and limitthe potential for misunderstandings from the adoption of alternative concepts. This isthe approach used by the FASB, as we discuss later.

Costs and Benefits

The implementation of each of the different concepts discussed in this appendix wouldinvolve additional costs for the company in preparing the data, and for audit fees if thefinancial statements are to be audited. For example, in a survey of companies, 62% of

CIP14 Appendix CIP Accounting for Changes in Prices

the respondents estimated that up to 800 hours of employee time would be necessaryto compute the supplementary disclosure requirements of FASB Statement No. 33.10

Although it may be expected that such costs would decline as experience increased, itwas still a significant cost, and the FASB requirements did not involve complete imple-mentation of current costs.

Historical cost/constant purchasing power financial statements would also involveadditional costs, but these would be much less than with current cost financial state-ments. Since the adjustment process involves the use of generally accepted accountingprinciples and a publicly available price-level index, the costs mainly result from mod-ifying accounting systems.

Current Cost and Operating Savings

Current cost net income includes depreciation expense based on the current cost of theproperty, plant, and equipment. If the current cost were based on the current produc-tive capacity of the assets, which incorporates technological changes, it is argued thatthe savings, as well as the higher depreciation charges, that would result from the tech-nological changes should be included. For example, suppose a company owns a fleet oftrucks. The current cost depreciation expense would be based on the higher purchaseprice of trucks. But if new trucks get better gas mileage and have lower repair and main-tenance costs, other operating expenses would be lower. Since the new trucks have notbeen acquired, the operating savings have not been realized and would have to be esti-mated. Complete implementation of this current cost framework would require thatthese lower costs, as well as the higher depreciation, be reflected in the income state-ment. However, it is difficult to estimate operating savings objectively. The SEC’srescinded requirements (which we discuss later) allowed estimation of such operatingsavings. Bethlehem Steel reported that its estimated cost savings were 167% of theexcess of current cost depreciation over historical cost depreciation. Sears reported sav-ings of 86% and the Ford Motor Company savings of 72%. You should also note thatthe operating savings might be offset to some extent by the increased interest costs onthe money that would have to be borrowed to finance the acquisition of the new prop-erty, plant, and equipment.

The FASB avoided this issue by requiring that a company measure current cost interms of the reproduction cost of currently owned assets, thereby ignoring any changesin technology and the operating savings that might result. This advantage is offset bythe fact that the current cost is measuring replacements that the company may not make.

Current Cost versus Partial Adjustments

Generally accepted accounting principles require several current cost methods that tendto modify the historical dollar concept, so that historical cost financial statementsachieve some of the objectives of current cost accounting. The LIFO inventory costingmethod matches approximately the current cost of the inventory (or a value close tothe current cost) as cost of goods sold against revenue. Accelerated depreciation meth-ods expense a high percentage of the historical cost of the asset against revenue earlyin the life of the asset, thus partially offsetting the effects of price changes on thoseassets. However, the extra amount of the expense may not be related in any rationalway to the change in the asset’s current cost. Also, the total depreciation expense overthe life of the asset is limited by the historical dollars paid for it. Furthermore, neitherLIFO nor accelerated depreciation methods reflect current costs in the balance sheet.The use of LIFO and accelerated depreciation do reduce income, so that it is likely tobe closer numerically to current cost income, but they should not be considered assubstitutes for current cost financial statements.

10. K. Evans and R. Freeman, “Statement 33 Disclosures Confirm Profit Illusion in Primary Statements,” FASBViewpoints (Stamford, Conn.: June 24, 1983), p. 13. FASB Statement No. 33 required certain supple-mentary disclosures, but was rescinded by FASB Statement No. 89, as discussed later.

Conceptual Issues Relating to Alternatives to Historical Cost CIP15

Generally accepted accounting principles also require the use of the lower of cost ormarket method for inventory (as we discussed in Chapter 9), fair value for impairednoncurrent assets (as we discussed in Chapters 11 and 12), fair value for investmentsin trading and available-for-sale securities (as we discussed in Chapter 15), and for somefinancial instruments and derivatives (as we discussed in Chapters 7 and 15). Both themarket value and fair value typically approximate current costs. A company is requiredto report the gains and losses on these items in its comprehensive income (either in netincome or other comprehensive income). So a company's comprehensive income has afew similarities to current cost income.

Current Exit Values

The three alternative measurement methods that we have discussed use entry, or input,values. An historical cost is, of course, the cost measured at the time of the acquisitionof the item. A constant purchasing power amount is an adjusted historical cost amount.A current cost is the amount that would have to be paid to purchase an item. In con-trast, some users of financial statements argue that it would be more appropriate to useexit values. A current exit value is the net cash amount that a company would receiveif it sold the item. An exit value often is referred to as the net realizable value becauseit is the net amount to be received from the sale after deducting any costs associatedwith the sale, such as transportation costs and sales commissions. The basic argumentin favor of the use of exit values in a company’s financial statements is that the companywill have to dispose of each item at some point in the future, and therefore the currentmeasure of the cash to be received from such sales is relevant to users of financialstatements. It is argued that exit values provide a better measure of the return oninvestment, liquidity, and financial flexibility.

Example CIP-5 illustrates the use of exit values using the facts for the Hallas Com-pany earlier in the Appendix. In addition, it is assumed that at Steps 2 and 5, the exitvalues of the inventory are $1,800 and $2,200, respectively. There are two componentsof income. The first is the purchasing margin, which is the difference between the exitvalue and the acquisition cost of the assets on the date of acquisition. The second isthe holding gain or loss, which is the change in the exit values of the assets. In theHallas Company example, inventory is acquired at Step 2 for $1,000 when its exit valueis $1,800, so that the company recognizes a purchasing margin of $800 and includesit in net income. At Step 4, when the inventory is sold, the exit value is $2,000 and the

EXAMPLE CIP-5 Exit Value Financial Statements

Step

1 2 3 4 5

Income Statements

Purchasing margin — $ 800 — — $ 950Holding gain — — — $ 200 —

Net Income — $ 800 — $ 200 $ 950

Balance Sheets

Cash $3,000 $2,000 $2,000 $4,000 $2,750Inventory — 1,800 1,800 — 2,200

$3,000 $3,800 $3,800 $4,000 $4,950

Capital $3,000 $3,800 $3,800 $4,000 $4,950

CIP16 Appendix CIP Accounting for Changes in Prices

company recognizes the holding gain of $200 (the increase in the exit value from$1,800). At Step 5 the company acquires inventory for $1,250 when its exit value is$2,200, so that it recognizes a purchasing margin of $950 and includes it in net income.At all times, the company includes the exit value of the inventory in its balance sheet.

Generally accepted accounting principles require the use of exit values in thefinancial statements of a company for reporting certain investments (as we discussedin Chapter 15) because the securities are readily saleable. In this case, the exit valueand the current cost are the same, except for transaction costs. Many people arguethat the use of exit values for other items would not provide relevant information,however. Consider two examples. If a company used an exit value for its inventory, itwould record that inventory at its selling price (less costs of disposal) before any saletransaction occurred and therefore would recognize income simply by acquiring inven-tory. Second, suppose that a company acquired a specialized machine for use in itsactivities. If the machine has no value to another company, its value would immedi-ately be recorded as zero and its entire purchase price expensed in the period of acqui-sition, even though the company intends to use the machine for several years.

Alternatively, it can be argued that in certain situations (in addition to certain invest-ments) exit values have more relevance than input values. For example, if a companyis to be liquidated, then exit values are more relevant. Of course, in this case the goingconcern (continuity) assumption is no longer valid. Furthermore, when a company isbeing sold in its entirety, many purchasers are interested in exit values because they mayintend to sell some of the assets. Regardless of their position on the relevance of exitvalues, few accountants argue that exit values should be the basis of the accountingprinciples for financial statements used in most investment and lending decisions.

DISCLOSURESThe APB, FASB, and SEC have recommended or required various disclosures of theeffects of changing prices. In 1969 the APB issued APB Statement No. 3, which statedthat general price-level adjusted historical cost financial statements present useful infor-mation not available from historical cost financial statements and concluded that:

General price-level information may be presented in addition to the basic historical dollarfinancial statements, but general price-level financial statements should not be presented as thebasic statements.11

In 1977 the Securities and Exchange Commission adopted a requirement forsupplementary disclosure on the annual 10-K report of the current replacement cost ofthe inventories, cost of goods sold, net productive assets, and depreciation. Companieswith inventories and gross property, plant, and equipment of more than $100 millionthat represented more than 10% of their total assets were required to make these dis-closures. These requirements were rescinded when FASB Statement No. 33 was issued.

In 1979 the FASB issued FASB Statement No. 33, “Financial Reporting and Chang-ing Prices,” which required disclosure of the effects of changing prices as a supplementto the basic historical cost financial statements.12 Public companies having $1 billion ofassets (after deducting accumulated depreciation) or $125 million of inventories andproperty, plant, and equipment (before deducting accumulated depreciation) wererequired to make such disclosures, although all companies were encouraged to do so.Then, in 1986 FASB Statement No. 89 rescinded the requirement that qualifying com-panies disclose the information specified in FASB Statement No. 33 as amended. How-ever, FASB Statement No. 89 encourages the continued disclosure of information aboutthe effects of changing prices and includes guidelines for measurement and disclosure.We discuss the reasons for making the disclosures voluntary in the next section.

11. APB Statement No. 3, op. cit., par. 25.12. “Financial Reporting and Changing Prices,” FASB Statement of Financial Accounting Standards No. 33

(Stamford, Conn.: FASB, 1979).

Be aware of thedisclosure re-quirements thathave existed foralternative dis-closures, in-cluding thereasons for theelimination ofthe requireddisclosures.

5

Disclosures CIP17

If a company decides to voluntarily report supplementary information on the effectsof changing prices, the FASB disclosure guidelines for the current year and for a 5-yearsummary are as follows:

The selected disclosures for the current year are (1) income from continuing opera-tions under the current cost basis, including disclosure of the current cost amounts ofcost of goods sold, and depreciation, depletion, and amortization expense, (2) pur-chasing power gain or loss on net monetary items (excluded from income from con-tinuing operations), (3) current cost (or lower recoverable) amount of inventory and ofproperty, plant, and equipment at the end of the current year, (4) increase or decreasein the current cost (or lower recoverable) amount of inventory and of property, plant,and equipment, before and after eliminating the effects of inflation (excluded fromincome from continuing operations), and (5) aggregate foreign currency translationadjustment on a current cost basis, if applicable.

The selected disclosures included in a 5-year summary, adjusted to average-for-the-year, end-of-year, or base-period constant purchasing power are (1) net sales and otheroperating revenues, (2) income from continuing operations (and related earnings pershare) under the current cost basis, (3) purchasing power gain or loss on net monetaryitems, (4) increase or decrease in the current cost (or lower recoverable) amount ofinventory and of property, plant, and equipment, net of inflation, (5) aggregate foreigncurrency translation adjustment on a current cost basis, if applicable, (6) net assets atyear-end on a current cost basis, (7) cash dividends declared per common share, and(8) market price per common share at year-end.13

Additional disclosures include (1) the principal types of information used to calculatethe current costs, and (2) differences between the depreciation methods, estimates ofuseful lives, and residual values used for calculations of current cost depreciation andthe methods and estimates used in the primary financial statements (there is a pre-sumption that the methods and estimates should be the same).

The FASB states that the objective of the calculations is “to obtain a reasonabledegree of accuracy” and that “preparers are encouraged to devise short-cut methods.”14

The Statement requires that the constant purchasing power adjustments use the averageConsumer Price Index for All Urban Consumers (CPI-U) for the year.

Conceptual Evaluation of the Elimination of the Required Disclosures

When FASB Statement No. 33 was adopted in 1979, it was intended that its provisionswould be reviewed after a period of not more than five years. Consequently, the FASBsponsored and monitored research to help assess the usefulness of information aboutthe effects of changing prices. In 1983 the FASB issued an Invitation to Comment onthe need for disclosures of information on the effects of changing prices and the bestway to meet that need. In 1984 the FASB responded to the related comments andresearch results by issuing FASB Statement No. 82, which eliminated certain disclosurerequirements. Then, in 1986 FASB Statement No. 89 eliminated the requirement forthe remaining disclosures. This Statement was adopted by a 4-to-3 majority.

There were several arguments in favor of eliminating the required disclosures. First,there was evidence that the disclosures were not widely used. Among the reasons for thelack of use were concerns that the information was not relevant. It was argued that theconcept of current cost (the cost of replacing existing service potential) was not relevantbecause many companies intended to replace their assets with others that had a differ-ent service potential. It was also argued that applying a specific price index to thehistorical cost did not provide a relevant value because technological change may not beappropriately reflected in the index. The lack of use also resulted from concerns aboutthe reliability of the information. For example, the determination of the current cost

13. FASB Statement No. 89, op. cit., par. 7, 8, 11–13.14. Ibid., par. 48.

CIP18 Appendix CIP Accounting for Changes in Prices

when an asset with equivalent service potential was not available required considerablejudgment and therefore could be viewed as unreliable. Also, the determination of therecoverable amount required substantial judgment. Furthermore, since the disclosureswere labeled “unaudited” and “supplementary,” they were considered to lack reliability.

Second, responses to the Invitation to Comment expressed the concern that the costsof providing the information exceeded the benefits. Because neither the costs nor thebenefits could be accurately measured, it was appropriate for the FASB to suspenddisclosure requirements if preparers and users perceive an unfavorable cost/benefit rela-tionship. Third, it was argued that the disclosures lacked comparability. This situationresulted from the degree of flexibility in methods of application, from differences in thequality of the raw data used to prepare the disclosures, and from failure to disclose theassumptions used. Fourth, concern was expressed that the disclosures lacked under-standability because they were overly complex. Also, it was argued that the disclosureswere difficult to understand because they were not adequately explained and did notinclude comprehensive financial statements. Fifth, many users of financial statementsindicated that they used information about changing prices in their decisions but haddeveloped their own methods for making the adjustments. Therefore, additional dis-closures might not be useful because users had information that was better or differentfrom that required by FASB Statement No. 33.

The final argument against continuing the required disclosures was that the signifi-cance of the disclosures had decreased because prices were changing much less than inprevious years. Therefore, other concerns were more important to users, such as theability of the company to finance replacements of productive capacity or the effects ofchanging interest rates on monetary assets and liabilities.

There were several arguments in favor of continuing the required disclosures. First,it was argued that the basic concept underlying FASB Statement No. 33 (inflation causeshistorical cost financial statements to show illusory profits and to mask the erosion ofcapital) is virtually undisputed. Second, although there was evidence of limited use ofthe disclosures, five years is an insufficient time to assess the usefulness of the infor-mation. Therefore, an effort should be made to improve any shortcomings of the infor-mation. Third, suspension of the required disclosures will encourage companies toremove the systems used to develop the information. Therefore, information will nolonger be available for research on the relevance and reliability of the information.

The final argument against the elimination of the required disclosures was that wheninflation rates increase at some time in the future, the FASB will again be asked torequire supplementary disclosures of the effects of changing prices. The effort requiredat that time will be as difficult, time-consuming, and costly as the implementation ofFASB Statement No. 33 disclosures.

International Accounting Differences

International accounting standards require that the primary financial statements of acompany that reports in the currency of a hyperinflationary economy are prepared interms of the currency at the balance sheet date; that is, the statements are adjusted in away similar to the constant dollar process we discussed in this Appendix. The standardsalso require that the company include the purchasing power gain or loss on net mone-tary items in its net income.

At the beginning of the appendix, we identified several objectives you would accomplish after reading the appendix.The objectives are listed below, each followed by a brief summary of the key points in the appendix discussion.1. Understand the difference between current value and general price level adjustments. A current value (or specific price

change) is the change in the price of an individual asset or liability caused by changes in the dynamics of the marketfor that particular item. A general price-level change is the change in the value, or purchasing power, of the dollar.

SUMMARY

Cases CIP19

2. Explain the three alternatives to historical cost. The three alternatives to historical cost are (1) current cost financialstatements, (2) historical cost/constant purchasing power financial statements, and (3) current cost/constant purchasingpower financial statements.

3. Understand issues related to the measurement of current cost, the adjustment of historical dollars for general price-level changes, and the purchasing power gain or loss on net monetary items. Current cost may be measured by directpricing, functional or unit pricing, or a specific-price index. Historical dollars are adjusted to constant purchasingpower amounts by multiplying by the ratio of the current period price-level index to the historical price-level index.A purchasing power gain (loss) results from holding net monetary liabilities (assets) during a period of inflation.

4. Explain the conceptual issues relating to the alternatives to historical cost. The conceptual issues include the capitalmaintenance concept for each of the three alternatives, the related values on the balance sheet, reliability,understandability, costs and benefits, current cost and operating savings, current cost versus partial adjustments, andcurrent exit values.

5. Be aware of the disclosure requirements that have existed for alternative disclosures, including the reasons for theelimination of the required disclosures. The supplementary disclosures required by FASB Statement No. 33 weresuspended by FASB Statement No. 89. Among the reasons were concerns that the information was not relevant orreliable, the costs exceeded the benefits, the disclosures lacked comparability and understandability, users made theirown adjustments, and the significance of the disclosures had decreased because price changes were small.

QUESTIONS

QCIP-1 Distinguish between a general price-level changeand a specific price change. What, if any, is the relationshipbetween them?

QCIP-2 List the four alternative accounting methods dis-cussed in the appendix. What is the appropriate capitalmaintenance concept for each?

QCIP-3 What is a realized holding gain? How is it mea-sured? Where should it appear in current cost financialstatements?

QCIP-4 What is an unrealized holding gain for an ac-counting period? How is it measured? Where should itappear in current cost financial statements?

QCIP-5 What is the major argument in favor of histori-cal cost/constant purchasing power financial statements?Of current cost financial statements?

QCIP-6 How may historical cost net income include areturn of capital in income?

QCIP-7 What causes a purchasing-power gain or loss?

QCIP-8 Distinguish between monetary and nonmonetaryitems.

QCIP-9 Consider the major items included in the incomestatement. Which are most nearly measured on a currentcost basis on historical cost financial statements? Whichare least?

QCIP-10 Are historical cost constant/purchasing powerfinancial statements allowed under generally acceptedaccounting principles? Explain.

QCIP-11 What is an exit value? What are the two com-ponents of income when exit value financial statements areprepared?

CASES

CCIP-1 Four Alternative Accounting MethodsPart a. Advocates of current value accounting proposeseveral methods for determining the valuation of assets toapproximate current values. Two of the methods proposedare replacement cost and present value of future cash flows.

Required Describe each of the two previously cited meth-ods and discuss the pros and cons of the various proceduresused to arrive at the valuation for each method.

Part b. The financial statements of a business entity couldbe prepared by using historical cost or current value as abasis. In addition, the basis could be stated in terms ofunadjusted dollars or dollars restated for changes in

purchasing power. The various permutations of these twoseparate and distinct areas are shown in the followingmatrix:

Dollars RestatedUnadjusted for Changes in

Dollars Purchasing Power

Historical cost 1 2Current value 3 4

Block number 1 of the matrix represents the traditionalmethod of accounting for transactions in accounting today,

CIP20 Appendix CIP Accounting for Changes in Prices

balance sheet as of December 31, 2007 and a statement ofincome and retained earnings for 2007, both restated forchanges in the general price level.

Required1. On what basis can it be contended that Barden’s

conventional statements should be restated for changesin the general price level?

2. Distinguish between historical cost/constant purchasingpower financial statements and current value financialstatements.

3. Distinguish between monetary and nonmonetary assetsand liabilities, as the terms are used in general price-level accounting. Give examples of each.

4. Outline the procedures the Barden Corp. should followin preparing the proposed supplementary statements.

5. Indicate the major similarities and differences betweenthe proposed supplementary statements and the corre-sponding conventional statements.

6. Assuming that in the future Barden will want to presentcomparative supplementary statements, can the 2007supplementary statements be presented in 2008 withoutadjustment? Explain. (AICPA adapted)

CCIP-4 Current CostsThe controller of the Robinson Company is discussing acomment you made in the course of presenting your auditreport.

“. . . and frankly,” Mr. Fisher continued, “I agree thatwe, too, are responsible for finding ways to produce morerelevant financial statements which are as reliable as theones we now produce.

“For example, suppose the company acquired a finisheditem for inventory for $40 when the general price-levelindex was 110. And, later, the item was sold for $75 whenthe general price-level index was 121 and the currentreplacement cost was $54. We could calculate a ‘holdinggain.’ ”

Required1. Explain to what extent and how current replacement

costs already are used within generally accepted ac-counting principles to value inventories.

2. Calculate in good form the amount of the holding gainin Fisher’s example.

3. Explain why the use of current replacement cost forboth inventories and cost of goods sold is preferred bysome accounting authorities to the generally accepteduse of FIFO or LIFO. (AICPA adapted)

CCIP-5 Constant Purchasing Power AdjustmentsPublished financial statements of United States companiesare currently prepared on a stable dollar assumption, eventhough the general purchasing power of the dollar hasdeclined because of inflation in recent years. To account forthis changing value of the dollar, many accountants suggestthat financial statements should be adjusted for generalprice-level changes. Three independent, unrelated statementsregarding constant purchasing power financial statementsfollow. Each statement contains some fallacious reasoning.

wherein the absolute (unadjusted) amount of dollars givenup or received is recorded for the asset or liability obtained(relationship between resources). Amounts recorded in themethod described in block 1 reflect the original cost of theasset or liability and do not give effect to any change invalue of the unit of measure (standard of comparison). Thismethod assumes the validity of the accounting concepts ofgoing concern and stable monetary unit. Any gain or loss(including holding and purchasing-power gains or losses)resulting from the sale or satisfaction of amounts recordedunder this method is deferred in its entirety until sale orsatisfaction.

Required For each of the remaining matrix blocks (2, 3,and 4), respond to the following questions. Limit yourdiscussion to nonmonetary assets only.1. Explain how this method of recording assets will affect

the relationship between resources and the standard ofcomparison.

2. Explain the conceptual justification for using eachmethod.

3. Explain how each method of asset valuation will affectthe recognition of gain or loss during the life of theasset and ultimately from the sale or abandonmentof the asset. Your response should include a discussionof the timing and magnitude of the gain or loss andconceptual reasons for any difference from the gain orloss computed using the traditional method. (AICPAadapted)

CCIP-2 Current Value and Fair Presentation ofFinancial StatementsThe total assets of the Sunset Land Company were $2�

1

2� mil-

lion on December 31, 2007, including land of $150,000.Net income was negligible because no land sales took placeand none were planned.

The land consisted of 50,000 acres valued at its acqui-sition cost in the early part of the century of $3 per acre.The market value of the land is now believed to exceed$15 million.

The auditor’s opinion attached to the financial state-ments states, in part, “The financial statements presentfairly the financial position of the Sunset Land Company. . . in conformity with generally accepted accountingprinciples.”

Required Explain whether the use of generally acceptedaccounting principles enables the financial position of theSunset Land Company to be presented fairly.

CCIP-3 Constant Purchasing Power AdjustmentsBarden Corp., a manufacturer with large investments inplant and equipment, began operations in 1944. The com-pany’s history has been one of expansion in sales, pro-duction, and physical facilities. Recently, some concern hasbeen expressed that the conventional financial statementsdo not provide sufficient information for decisions by in-vestors. After consideration of proposals for various typesof supplementary financial statements to be included in the2007 annual report, management has decided to present a

Exercises CIP21

Statement IThe accounting profession has not seriously considered con-stant purchasing power financial statements before, becausethe rate of inflation usually has been so small from year toyear that the adjustments would have been immaterial inamount. Constant purchasing power financial statementsrepresent a departure from the historical cost basis ofaccounting. Financial statements should be prepared fromfacts, not estimates.

Statement IIIf financial statements were adjusted for general price-levelchanges, depreciation charges in the earnings statementwould permit the recovery of dollars of current purchasingpower and, thereby, equal the cost of new assets to replacethe old ones. General price-level adjusted data would yieldstatement-of-financial-position amounts closely approxi-mating current values. Furthermore, management can makebetter decisions if constant purchasing power financialstatements are published.

Statement IIIWhen adjusting financial data for general price-levelchanges, a distinction must be made between monetary andnonmonetary assets and liabilities, which, under the his-torical cost basis of accounting, have been identified as“current” and “noncurrent.” When using the historicalcost basis of accounting, no purchasing power gain or lossis recognized in the accounting process, but when financialstatements are adjusted for general price-level changes, apurchasing-power gain or loss will be recognized on mon-etary and nonmonetary items.

Required Evaluate each of the independent statementsand identify the areas of fallacious reasoning in each andexplain why the reasoning is incorrect. Complete your dis-cussion of each statement before proceeding to the nextstatement. (AICPA adapted)

CCIP-6 Constant Dollar and Current CostFinancial reporting should provide information to helpinvestors, creditors, and other users of financial statements.Statement of Financial Accounting Standards No. 89 en-courages companies to disclose certain supplementaryinformation.

Required1. Describe the historical cost/constant purchasing

power method of accounting. Include in your discus-sion how historical cost amounts are used to makehistorical cost/constant purchasing power measure-ments.

2. Describe the principal advantage of the historicalcost/constant purchasing power method of accountingover the historical cost method of accounting.

3. Describe the current cost method of accounting.4. Why would depreciation expense for a given year differ

using the current cost method of accounting instead ofthe historical cost method of accounting? Include inyour discussion whether depreciation expense is likelyto be higher or lower using the current cost method ofaccounting instead of the historical cost method ofaccounting in a period of rising prices, and why.(AICPA adapted)

ECIP-1 Four Alternative Accounting Methods A company purchased inventory for $10,000 at the beginning of theyear when the CPI-U was 100. It sold the inventory in the middle of the year for $15,000 at which time theindex was 110 and the current cost was $13,000.

Required Compute the gross profit on the sale of the inventory under each of the following methods (computethe constant purchasing power amounts in terms of the average CPI-U of 110): (1) historical cost, (2) historicalcost/constant purchasing power, (3) current cost, and (4) current cost/constant purchasing power.

ECIP-2 Constant Purchasing Power Adjustments to Balance Sheet Items The Desmond Company is preparing aconstant purchasing power balance sheet at the average CPI-U for the year of 150. The CPI-U at the end of theyear is 155. The following are the amounts in selected accounts and the index when the amount was recorded:

Amount Index

Accounts receivable (net) $10,000 155Machinery 50,000 130Accumulated depreciation on machinery 10,000 130Patent (net) 5,000 125Accounts payable 20,000 155Bonds payable 50,000 120Common stock 40,000 80

Required Compute the amounts that would appear in the constant purchasing power year-end balance sheet.

ECIP-3 Constant Purchasing Power Adjustments to Property, Plant, and Equipment The Grembar Companypurchased a building on January 1, 2007 for $100,000 when the CPI-U was 125. The building has an expected

EXERCISES

CIP22 Appendix CIP Accounting for Changes in Prices

residual value of zero and a life of 10 years, and straight-line depreciation is used. The December 2007 priceindex is 135 and the December 2008 index is 145, and the price index rose evenly during each year.

Required1. What is the depreciation expense for 2007 and 2008 if the company prepares a constant purchasing power

income statement adjusted to the average index for each year?2. What is the carrying value of the asset at December 31, 2007 and December 31, 2008, if the company

prepares a constant purchasing power balance sheet each year at the average index for the year?3. How will the company adjust the amounts in its 2007 constant purchasing power financial statements when

those statements are published in 2008 for comparison with the constant purchasing power financialstatements of 2008?

ECIP-4 Current Costs—Inventory The following is the cost of goods sold section of the 2007 income statement forthe Higgins Company:

Inventory, 12/31/2006 $ 39,000Purchases 138,000

Cost of goods available for sale $177,000Less: Inventory, 12/31/2007 (60,000)

Cost of goods sold $117,000

Additional information:1. The December 31, 2006 inventory consisted of 11,000 units purchased in August 2006.2. The December 31, 2007 inventory consisted of 13,000 units purchased in October 2007.3. Purchases of 30,000 units were made during the year.4. The current cost of the inventory was $4.10 per unit in December 2006 and $5.10 per unit in December

2007.

Required Prepare the following 2007 disclosures for the Higgins Company:1. Cost of goods sold on an average current cost basis.2. Current cost of ending inventory.

ECIP-5 Current Costs—Property and Plant The Turner Company has the following fixed assets at the end of2007:

Land: Purchased for $15,000 in January 2001Current cost, December 2006: $25,000Current cost, December 2007: $30,000

Building: Purchased for $100,000 in January 2001Estimated life: 25 yearsDepreciation method: Straight-line (no residual value)Current cost, December 2006: $180,000Current cost, December 2007: $200,000

No land or buildings were acquired or sold in 2007.

Required Prepare the following 2007 disclosures for the Turner Company:1. Depreciation expense on an average current cost basis.2. Current cost (net) of property and plant.

ECIP-6 Current Cost and Sale of an Asset The Marino Company purchased some land for $100,000 on January 1,2007. In December 2007 and December 2008, the current cost of the land was $110,000 and $130,000,respectively. The land was sold on January 5, 2009 for $140,000.

Required If the company prepares current cost financial statements,1. What is the realized holding gain on the land in 2007 and 2008?2. What is the unrealized holding gain on the land in 2007 and 2008?3. What is the gain on the sale of the land in 2009?

Problems CIP23

PCIP-1 Inventory and the Four Alternative Accounting Methods The Turner Company, a retail company, began op-erations on January 1, 2007 and engaged in the following transactions:

January 1, 2007 Purchased 100 units of inventory for $200 per unit. The general price-level indexwas 110.

First quarter 2007 Sold 50 units for $400 per unit. The average replacement cost of the inventory was$220 per unit and the general price-level index was 115.

Second quarter 2007 Purchased 200 units for $250 per unit. The general price-level index was 118.Third quarter 2007 Sold 100 units for $450 per unit. The average replacement cost of the inventory

was $260 per unit and the general price-level index was 120.Fourth quarter 2007 No purchases or sales were made. The average replacement cost of the inventory

was $275 per unit and the general price-level index was 120.