apresenta o base 13.08 - 2) · 1 bradesco presentation this presentation may contain...

TRANSCRIPT

1

Bradesco PresentationThis presentation may contain forward-looking statements. Such statements are not statements ofhistorical facts and reflect the beliefs and expectations of the Company's management. The words"anticipates”, "believes”, "estimates”, "expects”, "forecasts”, "plans”, "predicts”, "projects”, "targets"and similar words are intended to identify these statements, which necessarily involve known andunknown risks and uncertainties. Known risks and uncertainties include but are not limited to theimpact of competitive services and pricing market acceptance of services, service transactions by theCompany and its competitors, regulatory approval, currency fluctuations, changes in service mixoffered, and other risks described in the Company's registration statement and other Securities andExchange Commission filings. Forward-looking statements speak only as of the date they are madeand Banco Bradesco does not undertake any obligation to update them in light of new information orfuture developments.

2

For the complete schedule, please visit bradesco.com.br/ir

Upcoming Public Events

*Live online streaming with simultaneous translation to English

Aug 14: APIMEC – Brasília/DF*

Aug 21: APIMEC – Rio de Janeiro/RJ*

Aug 28: APIMEC – São Paulo/SP*

Sep 18: APIMEC – Recife/PE*

Oct 02: APIMEC – Uberlândia/MG*

3

Content

2010 Guidance x Realized 147 Delinquency Ratio > 90 days 88

2011 Guidance 148 Delinquency Ratio 61 to 90 days 89

Administrative Bodies 38 Distribution Network 30

Allowance for Loan Losses, Overdue Credits and

Coverage Ratio94

Distribution of borrowers by level of debt (total debt/annual

income) - 2011 20

Allowance for Loan Losses/ PLL / Write-off 92Distribution of Brazilian Families' Indebtedness: Social

Classes (2011) 19

Balance Sheet by Currency 75 Dividends 51

Balance Sheet by Maturity 76 Economic Indexes 24

Book Net Income x Adjusted Net Income 56 Efficiency Ratio 53

Bradesco Retail - Bradesco Expresso 33 EPS and Net Income 52

Bradesco Strategy 28 Evolution of Brazilian 23

Brazilian Exports (by Country of

destination)Productivity 22Expanded Loan Portfolio 81-82

Brazilian Financial System 25 Fee Income 65-66

Brazilian GDP 9 Hand-in-hand with Corporate Governance 41

Capital Markets 144-146 Highlights of Banco Bradesco 26

Cards 113-121 Impact on Efficiency 45

Client Base 35 Income Statement 55/58

Client Segmentation 36Indebtedness of Brazilian Families (% Income), Average

Maturity and Interest Rate for Individuals 18

Consolidated Balance Sheet 74 Insurance and Pension Plans 128-143

Consumer Financing 85Investments in Infrastructure, Information Technology and

Telecommunications47

Core NIM & NII 62 IT Revitalization Plan 44

CPI (IPCA) 6 Liquidity 49

Credit NII 64 Loan Portfolio 91

Credit Quality and Concentration 87 Loan Portfolio - Corporate 86

Daily transactions vs. availability 43

4

Content

Loan Portfolio – Individuals 84 Other Administrative Expenses 68

Loan Portfolio Breakdown 83 Payroll-Deductible Loans 122-127

Loan/Brazil 's GDP Ratio 16 Poverty Ratio 12

Loan/World's GDP Ratio 17 Presence Abroad 34

Loans and Funding 80 Provisioning Ratios 93

Macroeconomic Outlook 5 Real Wages 14

Main Funding 77-78 Renegotiated Portfolio 90

Main Ratings 40 Reserve Requirements and Restricted Loans 79

Market Capitalization 50 Shareholders’ Profile – Bradesco 39

Market Shares 29 Shareholders’ Structure 37

Mass of Salaries 15 Simulation of the impact of Basel 73

Mobility and Other Service Channels 32 Social Mobility in Brazil 13

Mortgage 95-102 Spread 63

Net Income and Efficiency Ratio 54 Stock Evolution 48

New System Architecture (NSA) – Profitability

Increase46 Tax Credit on Shareholders’ Equity Ratio and Capital 71

NII 59/61 Tax Expenses 70

NII- Interest /Trading Gains 60 The Top 10 Banking Brands in the World 27

Nominal and Real Interest Rates 8 Total Assets and Shareholders’ Equity 72

Nominal Interest Rates 7 Trade Balance 1991-2012 21

Operating Expenses 67 Transaction Breakdown 42

Operational Coverage Ratio 69 Unemployment Rate 10-11

Organic Growth of the Distribution Channels 31 Unrealized Gains 57

Vehicles 103-112

5

Macroeconomic Outlook

** Focus Forecast: As of 08/08/2012

* As of 08/13/2012

2013* 2012 2013

Bradesco Market Consensus**

2012 *

2.10%

5.21%

1.95

7.50%

4.00%

5.50%

2.00

8.50%

1.81%

5.11%

2.00

7.25%

2.73%

6.50%

1.88

11.00%

4.00%

5.50%

2.00

8.50%

2011

GDP

Interest Rate

(year-end Selic)

Inflation (CPI)

FX Rate

(year-end R$/US$)

6

%

CPI (IPCA)CPI (IPCA)

Prepared by / (*) Projections: Bradesco - DEPEC

As of 08/13/2012Source: IBGE

12.5

9.3

7.6

5.7

3.1

4.5

5.9

4.3

5.96.5

5.2 5.5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013*

7

Nominal Interest Rates

As of 08/13/2012Source: Brazilian Central Bank Prepared by/ (*) Projections: Bradesco - DEPEC

%

11.75

13.00

13.75

12.75

11.25

10.25

9.25

8.75

9.50

10.25

10.75

11.2511.75

12.0012.25

12.50

12.00

11.50

11.00

10.50

9.75

9.00

8.50

8.00

7.50 7.758.008.25

8.50

Feb-08

Apr-08

Jun-08

Aug-08

Oct-08

Dec-08

Feb-09

Apr-09

Jun-09

Aug-09

Oct-09

Dec-09

Feb-10

Apr-10

Jun-10

Aug-10

Oct-10

Dec-10

Feb-11

Apr-11

Jun-11

Aug-11

Oct-11

Dec-11

Feb-12

Apr-12

Jun-12

Aug-12

Oct-12

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

8

Nominal(1) and Real(2) Interest Rates

As of 08/13/2012

Notes: (1) Average Nominal Selic; (2) Average Nominal Selic deflationed by IPCAPrepared by/ (*) Projections: Bradesco - DEPEC

16.2

19.0

15.1

11.912.5

9.9 9.8

11.6

8.1 7.88.0

12.611.6

7.16.2

5.4

3.74.8

2.4 2.5

2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013*

Nominal Real

%

9

Brazilian GDP

Source: IBGE Prepared by / (*) Projections: Bradesco - DEPEC

As of 08/13/2012

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

3.5

-0.1

3.2

-4.3

1.0

-0.5

4.75.3

4.4

2.1

3.4

0.0 0.3

4.3

1.3

2.7

1.1

5.7

3.2

4.0

6.1

5.2

-0.3

7.5

2.7

2011

2.1

2012*

%

4.0

2013*

10

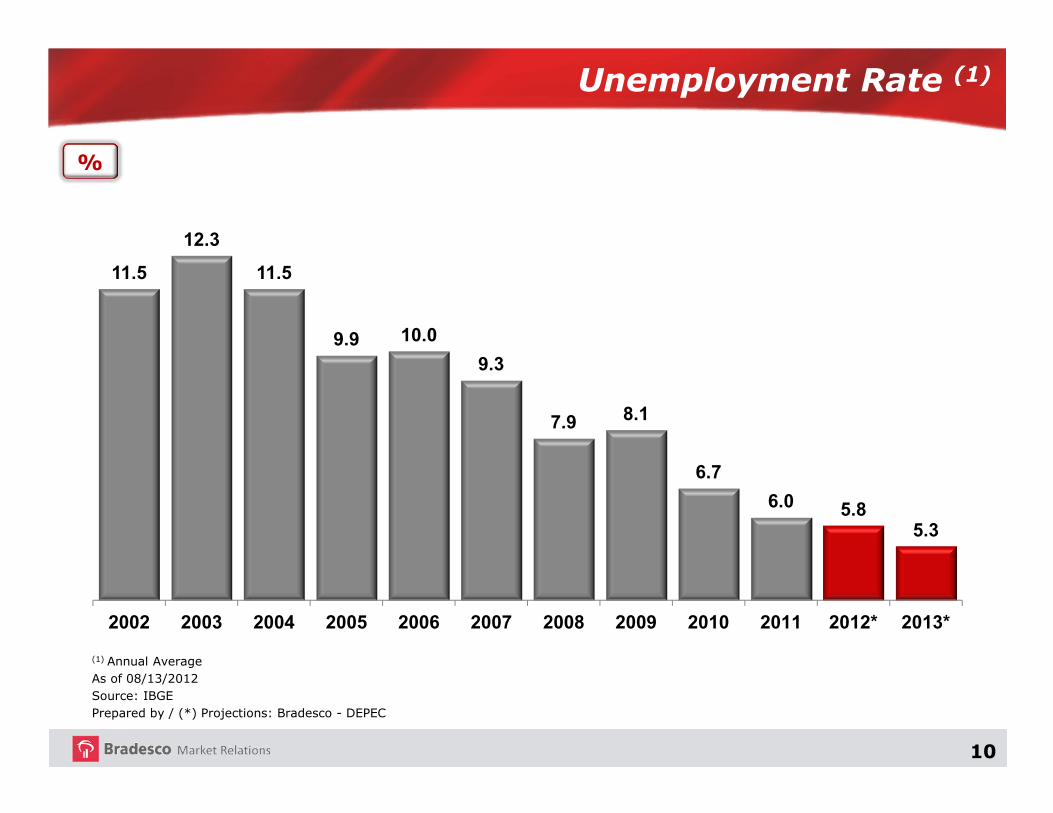

Unemployment Rate (1)

(1) Annual AverageAs of 08/13/2012Source: IBGE Prepared by / (*) Projections: Bradesco - DEPEC

11.5

12.3

11.5

9.9 10.0

9.3

7.9 8.1

6.7

6.0 5.85.3

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013*

%

11

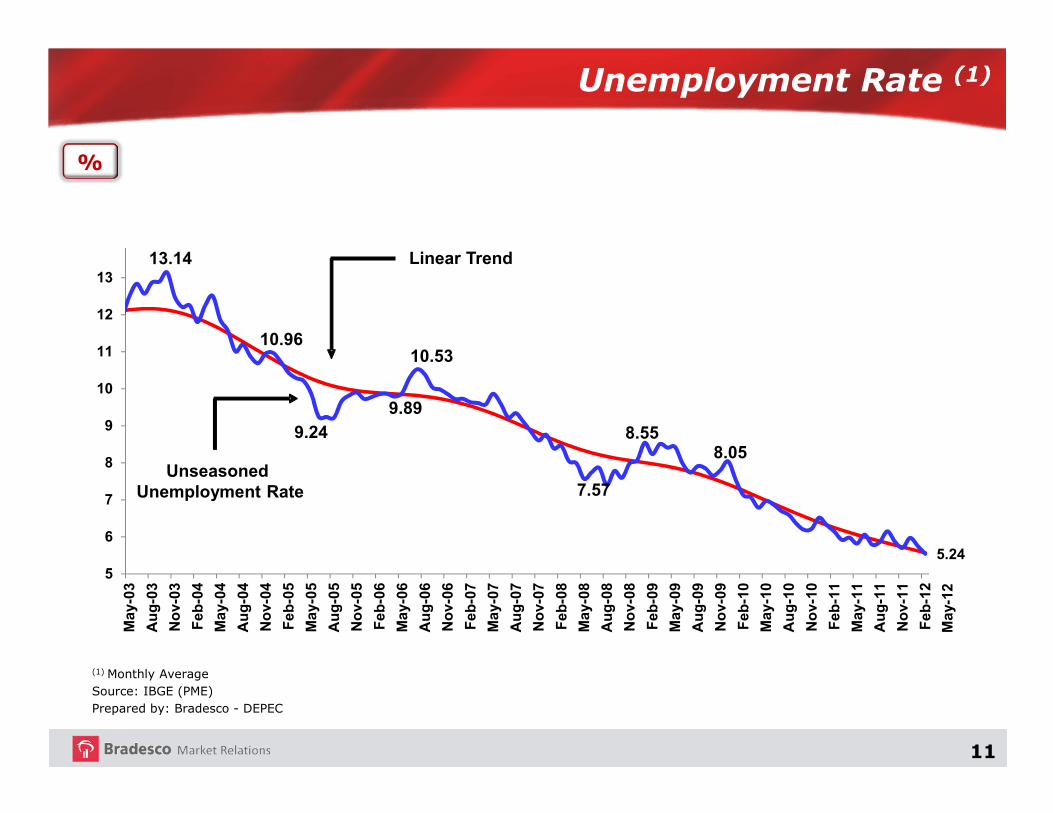

Unemployment Rate (1)

(1) Monthly AverageSource: IBGE (PME)Prepared by: Bradesco - DEPEC

Unseasoned Unemployment Rate

Linear Trend

%

13.14

10.96

9.24

9.89

10.53

7.57

8.558.05

5.245

6

7

8

9

10

11

12

13

May-03

Aug-03

Nov-03

Feb-04

May-04

Aug-04

Nov-04

Feb-05

May-05

Aug-05

Nov-05

Feb-06

May-06

Aug-06

Nov-06

Feb-07

May-07

Aug-07

Nov-07

Feb-08

May-08

Aug-08

Nov-08

Feb-09

May-09

Aug-09

Nov-09

Feb-10

May-10

Aug-10

Nov-10

Feb-11

May-11

Aug-11

Nov-11

Feb-12

May-12

12

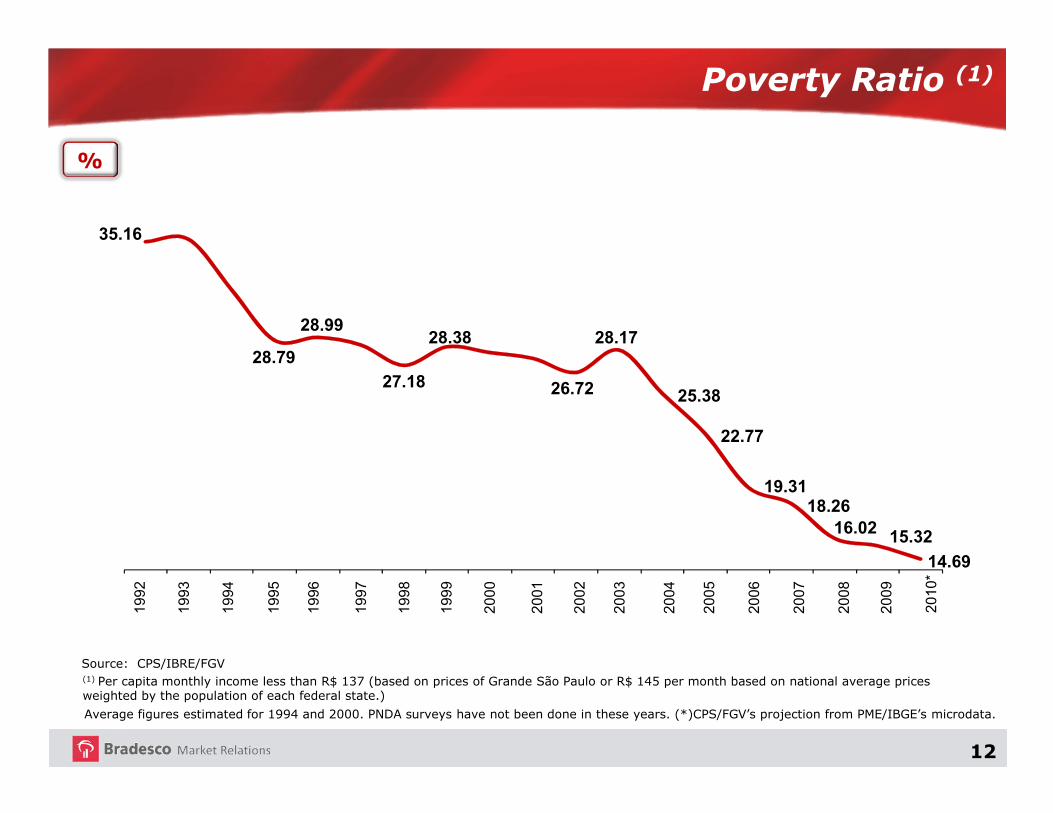

Poverty Ratio (1)

Average figures estimated for 1994 and 2000. PNDA surveys have not been done in these years. (*)CPS/FGV’s projection from PME/IBGE’s microdata.

(1) Per capita monthly income less than R$ 137 (based on prices of Grande São Paulo or R$ 145 per month based on national average prices weighted by the population of each federal state.)

Source: CPS/IBRE/FGV

35.16

28.79

28.99

27.18

28.38

26.72

28.17

25.38

22.77

19.3118.26

16.02 15.32

14.69

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010*

%

13

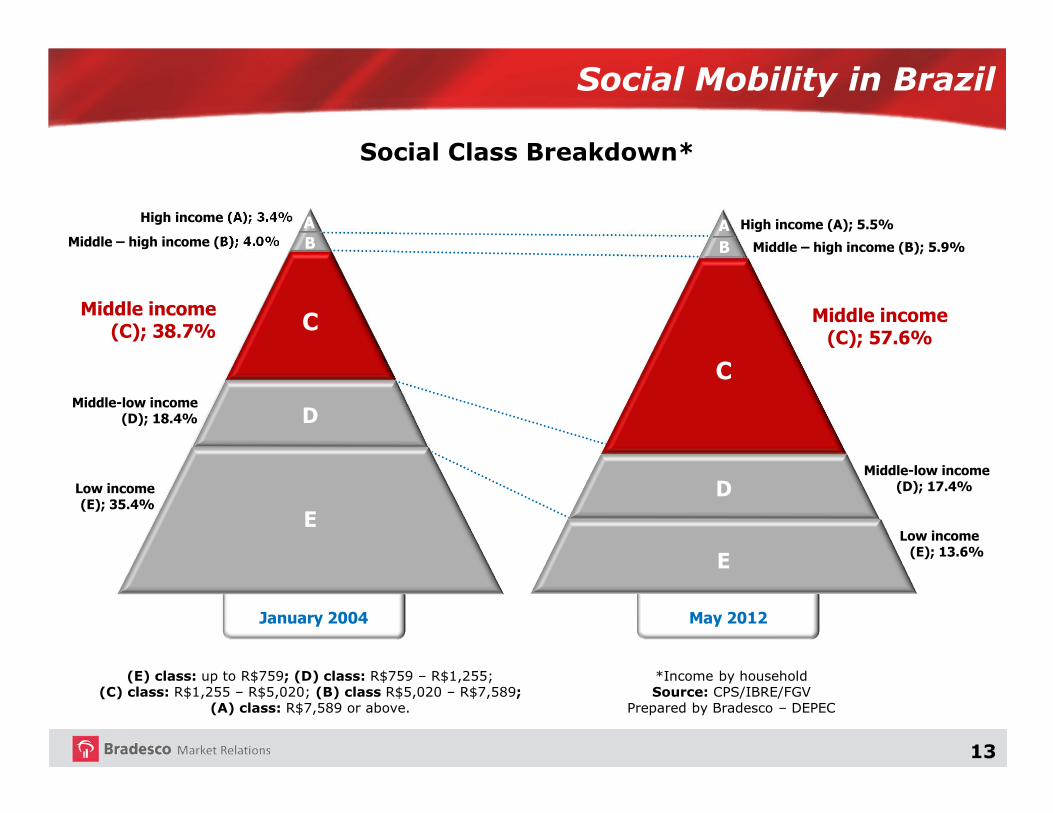

Social Mobility in Brazil

January 2004 May 2012

Social Class Breakdown*

(E) class: up to R$759; (D) class: R$759 – R$1,255; (C) class: R$1,255 – R$5,020; (B) class R$5,020 – R$7,589;

(A) class: R$7,589 or above.

*Income by householdSource: CPS/IBRE/FGV

Prepared by Bradesco – DEPEC

Middle income (C); 38.7%

Middle – high income (B); 4.0%

High income (A); 3.4% A

C

E

D

A

B

C

D

E

Low income(E); 35.4%

Middle-low income(D); 18.4%

High income (A); 5.5%

Middle – high income (B); 5.9%

Middle-low income(D); 17.4%

Low income (E); 13.6%

Middle income (C); 57.6%

B

14

As of 08/13/2012Source: IBGEPrepared by / (*) Projections: Bradesco - DEPEC

Real Wages

-1.3

1.5

4.0

3.23.4

3.2

3.8

2.7

3.8

2004 2005 2006 2007 2008 2009 2010 2011 2012*

%

15

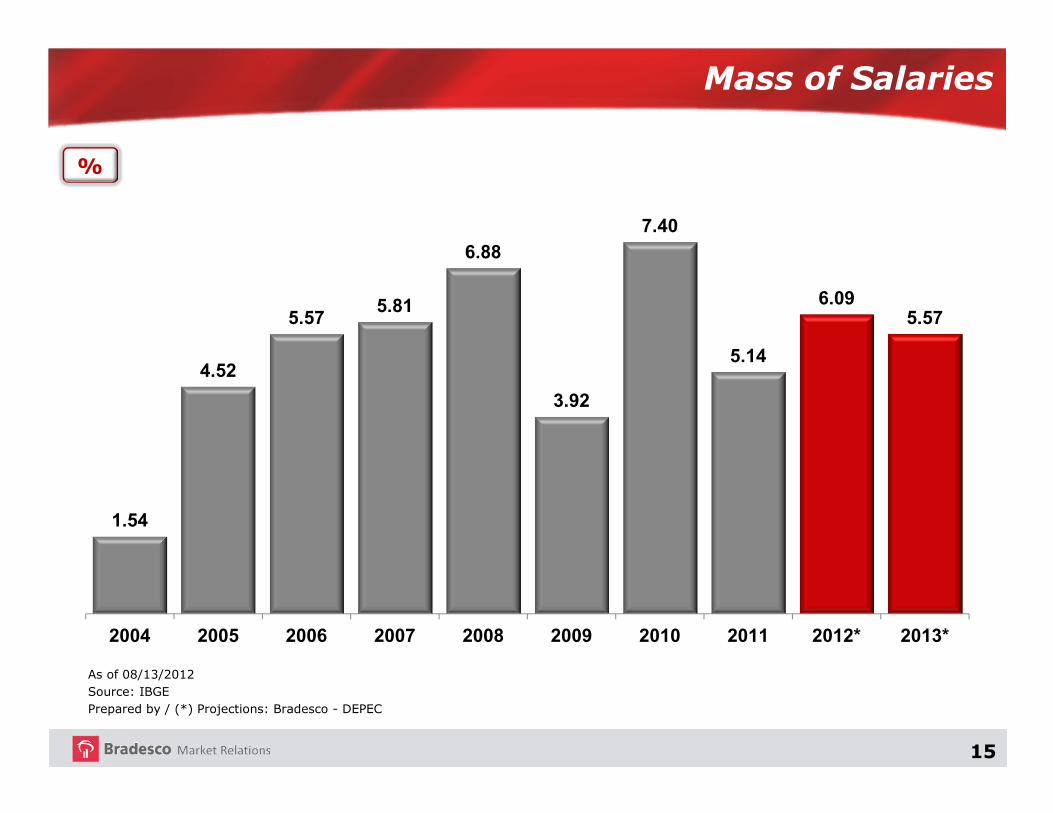

As of 08/13/2012Source: IBGEPrepared by / (*) Projections: Bradesco - DEPEC

Mass of Salaries

%

1.54

4.52

5.575.81

6.88

3.92

7.40

5.14

6.095.57

2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013*

16

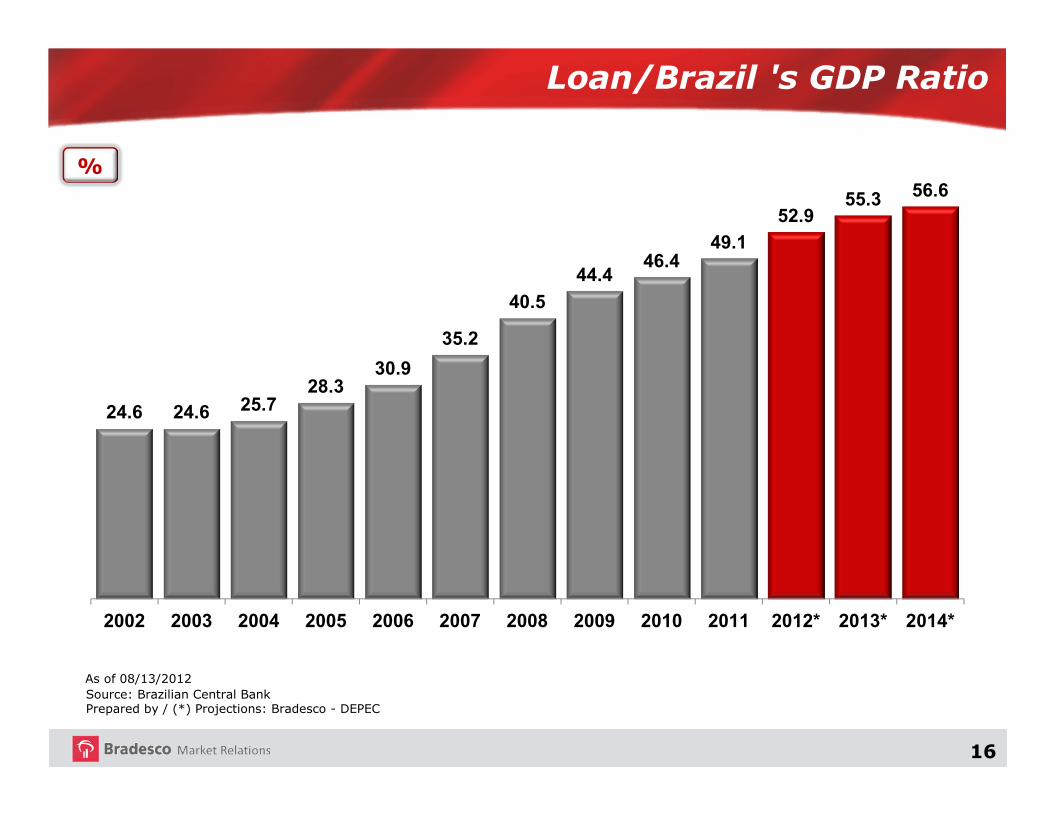

Loan/Brazil 's GDP Ratio

Source: Brazilian Central BankPrepared by / (*) Projections: Bradesco - DEPEC

As of 08/13/2012

%

24.6 24.6 25.728.3

30.9

35.2

40.5

44.446.4

49.1

52.955.3 56.6

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012* 2013* 2014*

17

Argentina

Ecuador

Mexico

Colombia

Brazil

Chile

Turkey

Russ

ia

Romania

Slovakia

Poland

Czech R

ep.

Bulgary

Hungary

South Africa

India

Thailand

Malays

ia

China

South Korea

Italy

Japan

Germ

any

France

Sweden

Australia

Canada

New Zealand

Portugal

Unite

d Kingdom

Spain

USA

As of: Brazil - May/11; Ecuador, South Korea – Dec/07; Colombia, Argentina, Mexico, Chile, China – Dec/09; Thailand – Sep/07; Malaysia, Hungary, India, Czech Republic, Poland – Dec/08; Others Countries – Mar/08.Source: Brazilian Central Bank, Ecowin

Loan/World's GDP Ratio

%

Latin America34.7

Emerging countriesEurope45.0

Emerging countriesAsia112.4

Developed Economies136.8

18

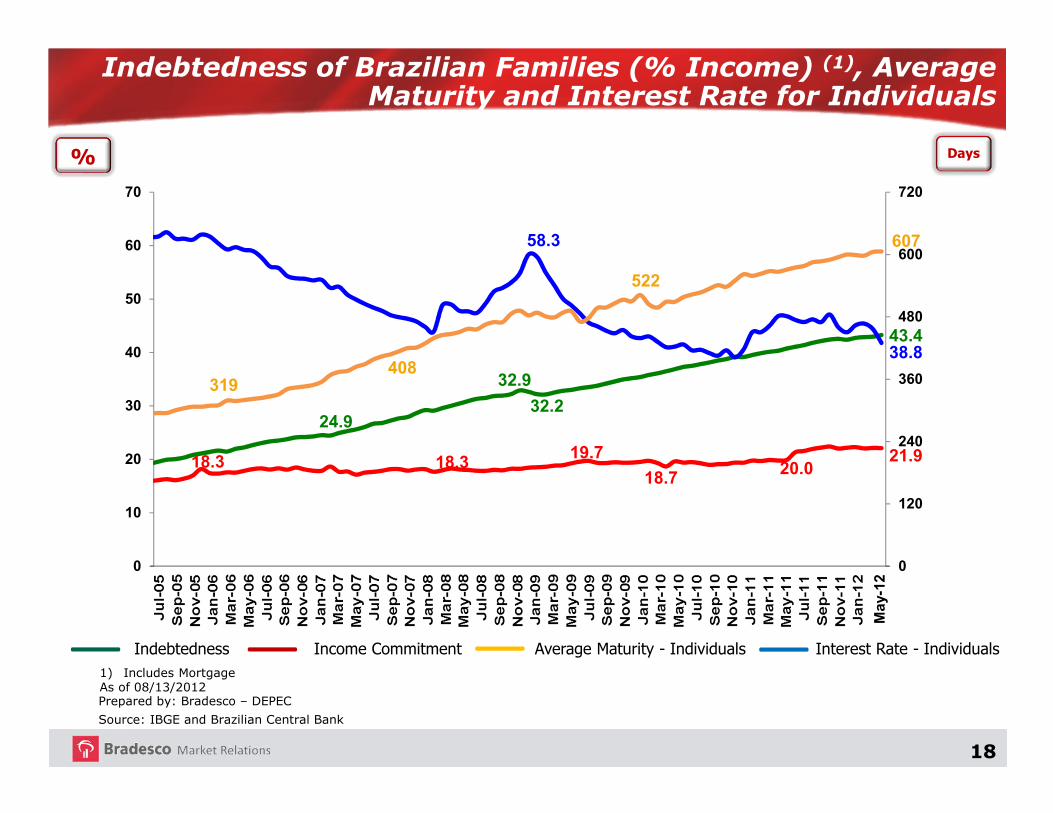

24.9

32.9

32.2

43.4

18.3 18.319.7

18.7 20.021.9

58.3

38.8

319408

522

607

0

120

240

360

480

600

720

0

10

20

30

40

50

60

70

Interest Rate - Individuals

Prepared by: Bradesco – DEPEC

Source: IBGE and Brazilian Central Bank

1) Includes MortgageAs of 08/13/2012

Indebtedness of Brazilian Families (% Income) (1), Average Maturity and Interest Rate for Individuals

Indebtedness Income Commitment Average Maturity - Individuals

Days%

May-12

19

* Disposable IncomeSource: Internal Research, Bradesco

Distribution of Brazilian Families’ Indebtedness*: Social Classes (2011)

28%

26%

28%

26%

18%

25%

38%

35%

48%

52%

36%

42%

0% 20% 40% 60%

E

D

C

B

A

Brazil 2011

2007

20

64%

13%

6%4%

2% 2% 1% 1% 1% 1% 1% 1% 0% 0% 0%3%

Até 10%

10%

- 20%

20%

- 30%

30%

- 40%

40%

- 50%

50%

- 60%

60%

- 70%

70%

- 80%

80%

- 90%

90%

- 100%

100% - 110%

110% - 120%

120% - 130%

130% - 140%

140% - 150%

> 150%

Pouco endividadoMais ou menos endividadoEndividadoMuito endividado

Distribution of borrowers by level of debt (total debt/annual income) - 2011

Source: Internal Research, Bradesco

Up

to10%

Low IndebtedMedium IndebtedIndebtedHigh Indebted

21

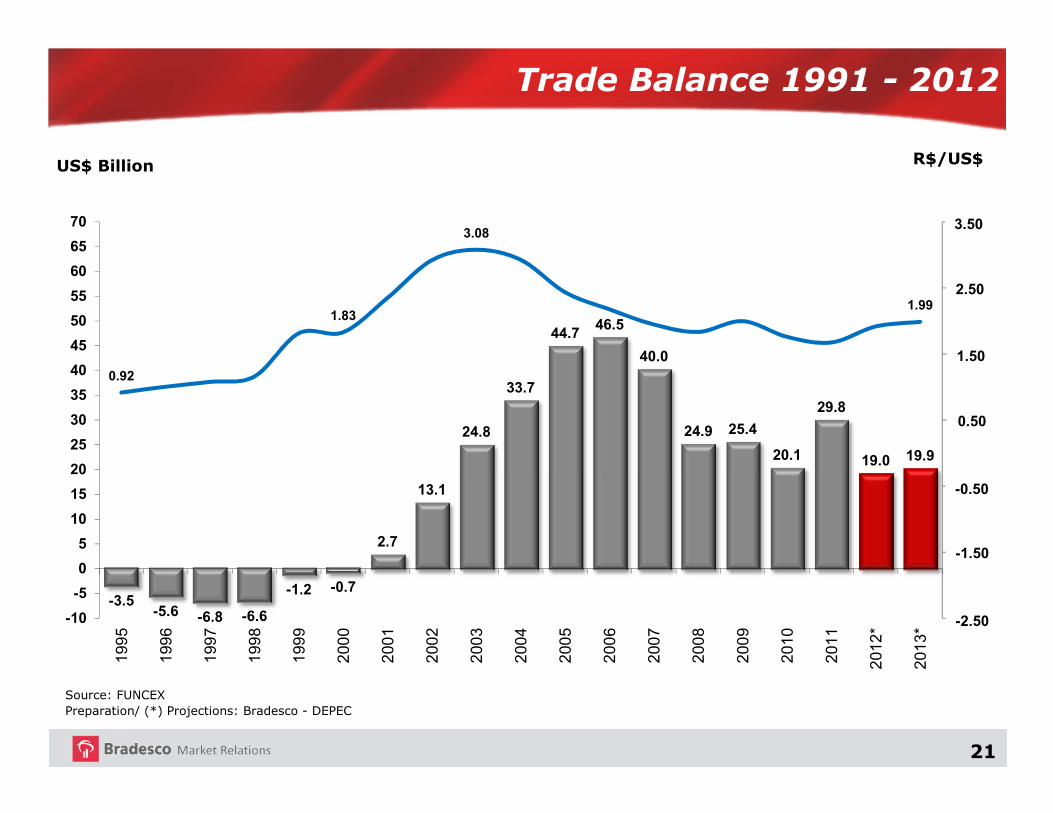

US$ Billion

Trade Balance 1991 - 2012

Source: FUNCEXPreparation/ (*) Projections: Bradesco - DEPEC

-3.5-5.6 -6.8 -6.6

-1.2 -0.7

2.7

13.1

24.8

33.7

44.746.5

40.0

24.9 25.4

20.1

29.8

19.0 19.9

0.92

1.83

3.08

1.99

-2,50

-1,50

-0,50

0,50

1,50

2,50

3,50

-10

-5

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012*

2013*

R$/US$

-2.50

-1.50

-0.50

0.50

1.50

2.50

3.50

22

Brazilian Exports (by most important countries(1) of destination)

* Including Puerto Rico** Including San Marino

%

15.9

12.1

7.9

6.4

3.2 3.0 2.62.1 1.9 1.8 1.8 1.8

Chin

a

USA*

Arg

entina

Net

her

lands

Ger

man

y

Japan

India

Italy*

*

Ven

ezuela

Chile

Mex

ico

Spain

(1) Other 206 countries with up to 1,7%Source: FUNCEX Preparation: Bradesco – DEPECAs of Apr12

23

Evolution of Brazilian Productivity

0.20

1.83

-0.20

1.030.89

0.69

-0.29

-0.10

-0.32

1.71

-0.27

2.07

0.42

1.45

2.12

0.85

0.24

1.24

1.00

1.50

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* 2012*

Source: IBGE, FGV, Seade/DieesePrepared by / (*) Projections: Bradesco - DEPEC

%

24

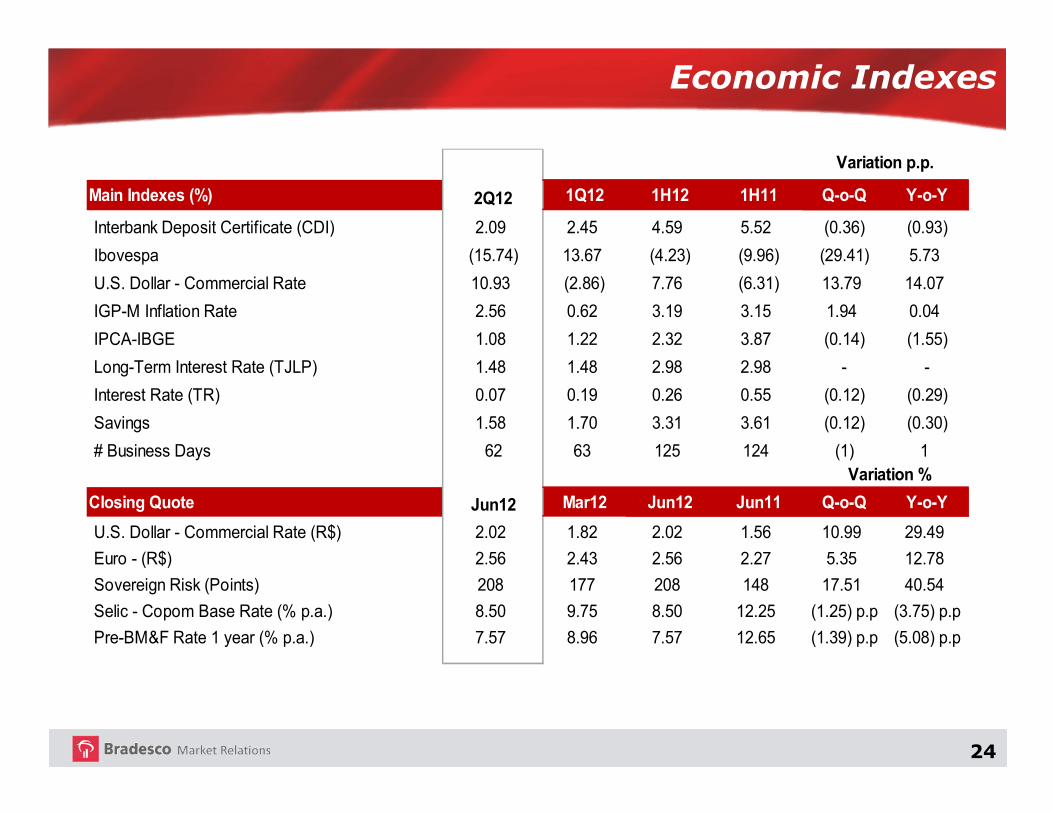

Economic Indexes

Main Indexes (%) 2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

Interbank Deposit Certificate (CDI) 2.09 2.45 4.59 5.52 (0.36) (0.93)

Ibovespa (15.74) 13.67 (4.23) (9.96) (29.41) 5.73

U.S. Dollar - Commercial Rate 10.93 (2.86) 7.76 (6.31) 13.79 14.07

IGP-M Inflation Rate 2.56 0.62 3.19 3.15 1.94 0.04

IPCA-IBGE 1.08 1.22 2.32 3.87 (0.14) (1.55)

Long-Term Interest Rate (TJLP) 1.48 1.48 2.98 2.98 - -

Interest Rate (TR) 0.07 0.19 0.26 0.55 (0.12) (0.29)

Savings 1.58 1.70 3.31 3.61 (0.12) (0.30)

# Business Days 62 63 125 124 (1) 1

Closing Quote Jun12 Mar12 Jun12 Jun11 Q-o-Q Y-o-Y

U.S. Dollar - Commercial Rate (R$) 2.02 1.82 2.02 1.56 10.99 29.49

Euro - (R$) 2.56 2.43 2.56 2.27 5.35 12.78

Sovereign Risk (Points) 208 177 208 148 17.51 40.54

Selic - Copom Base Rate (% p.a.) 8.50 9.75 8.50 12.25 (1.25) p.p (3.75) p.p

Pre-BM&F Rate 1 year (% p.a.) 7.57 8.96 7.57 12.65 (1.39) p.p (5.08) p.p

Variation %

Variation p.p.

25

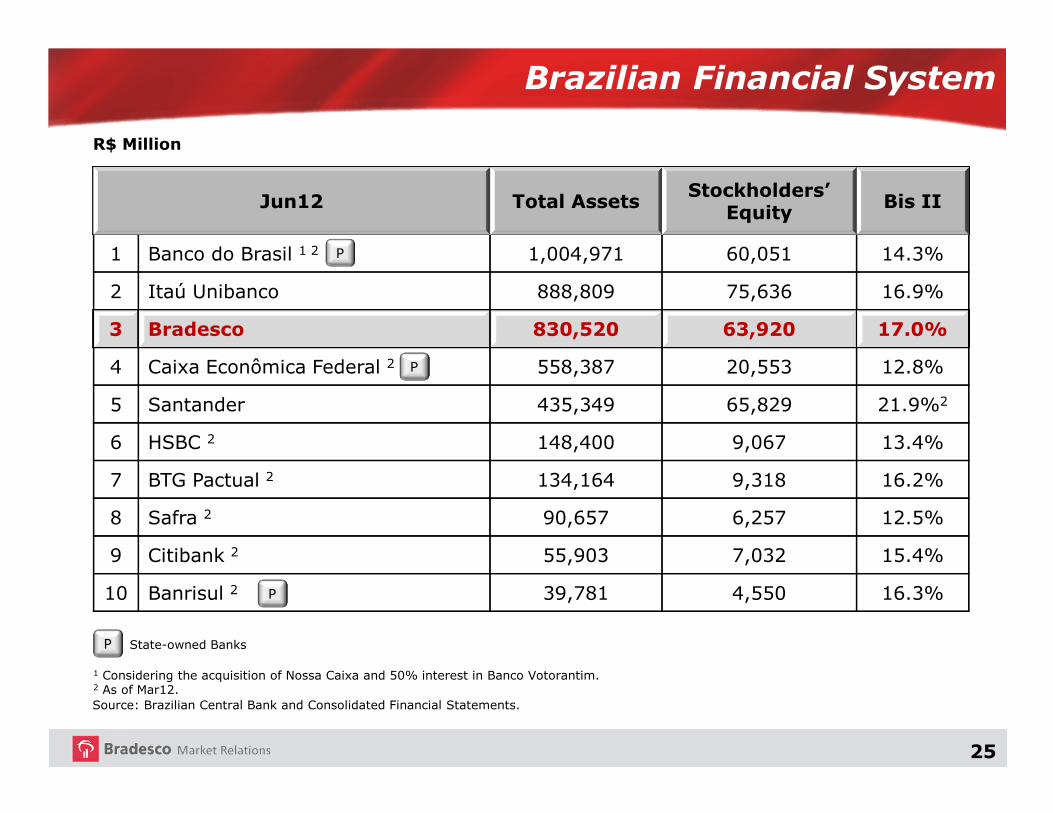

Brazilian Financial System

Source: Brazilian Central Bank and Consolidated Financial Statements.

State-owned Banks

R$ Million

P

1 Considering the acquisition of Nossa Caixa and 50% interest in Banco Votorantim.2 As of Mar12.

Jun12 Total AssetsStockholders’

EquityBis II

1 Banco do Brasil 1 2 1,004,971 60,051 14.3%

2 Itaú Unibanco 888,809 75,636 16.9%

3 Bradesco 830,520 63,920 17.0%

4 Caixa Econômica Federal 2 558,387 20,553 12.8%

5 Santander 435,349 65,829 21.9%2

6 HSBC 2 148,400 9,067 13.4%

7 BTG Pactual 2 134,164 9,318 16.2%

8 Safra 2 90,657 6,257 12.5%

9 Citibank 2 55,903 7,032 15.4%

10 Banrisul 2 39,781 4,550 16.3%

P

P

P

26

Highlights of Banco Bradesco

One of the Largest Private Banks in Latin America

Member of the Dow Jones Sustainability Index

For the sixth straight year, Bradesco shares were included in the “Corporate SustainabilityIndex (ISE),” of the BM&FBovespa

It is one of the 42 companies to comprise the “Carbon Efficient Index” (ICO2) of theBM&FBovespa

The most solid bank of Brazil and the 13th strongest in the World (Bloomberg News)

Market Capitalization: R$104,869 million (as of Jun12)

27

Bank of America

Wells Fargo

HSBC

Santander

Chase

Bradesco

Barclays

ICBC

Citi

China Construction Bank

The Top 10 Banking Brands in the World

AllSectors

BankingSector

6th1st

9th2nd

11th3rd

15th4th

26th5th

28th6th

34th7th

35th8th

36th9th

37th10th

30,619

28,944

27,632

26,150

19,150

18,678

17,358

17,194

17,133

17,092

CompanyLogo Country Brand Value(US$ Million)

Source: Brand FinanceAs of Jan11

28

Serving all social classes

Bradesco Strategy

A

B

C

D

E

Presence in all Brazilian cities

29

Market Shares

Loan Portfolio (1) (2)

Demand Deposits (2)

Savings Deposits (2)

Asset Management

Insurance, Private Pension Plans and Savings Bonds Premiums (2)

# Branches

Banking System

Private Banks

11.8%

16.5%

13.9%

18.0%

24.5%

21.9%

32.0% (3)

21.4%

30.7%

36.9%

37.2%

2Q12

Source: Brazilian Central Bank, Anbima, Susep and ANS.

(1) Bacen data for March 2012, May 2012 and June 2012 are preliminary (2) Reference date: May 2012(3) Excluding insurance’s participation of public banks

25.7%

30

▪ 66.7 million Clients▪ 104,531 Employees

Distribution Network

Branches Bradesco Expresso

Jun12

▪ 370.2 thousand Shareholders▪ 4,221 Suppliers (As of Dec11)

(1) Includes 3,243 PAs (Service Branch, a result from the consolidation of PAB, PAA and Exchange Points, according to CMN Resolution 4,072 of April26, 2012; and PAE: ATM located in the premises of a company) and 1,476 PAEs (ATM located on the premises of a company);

(2) Includes 10,459 ATMs Shared with other Banks and 1,061 Bradesco Promotora de Vendas service points.

� Branches/Subsidiaries Abroad

� Outside ATM Terminals

� ATM Terminals

� Branches

� PAs + PAEs (1)

� Bradesco Expresso

13

3,992

47,484

4,650

4,719

40,476

TOTAL DISTRIBUTION NETWORK 65,370

� Others (2) 11,520

31

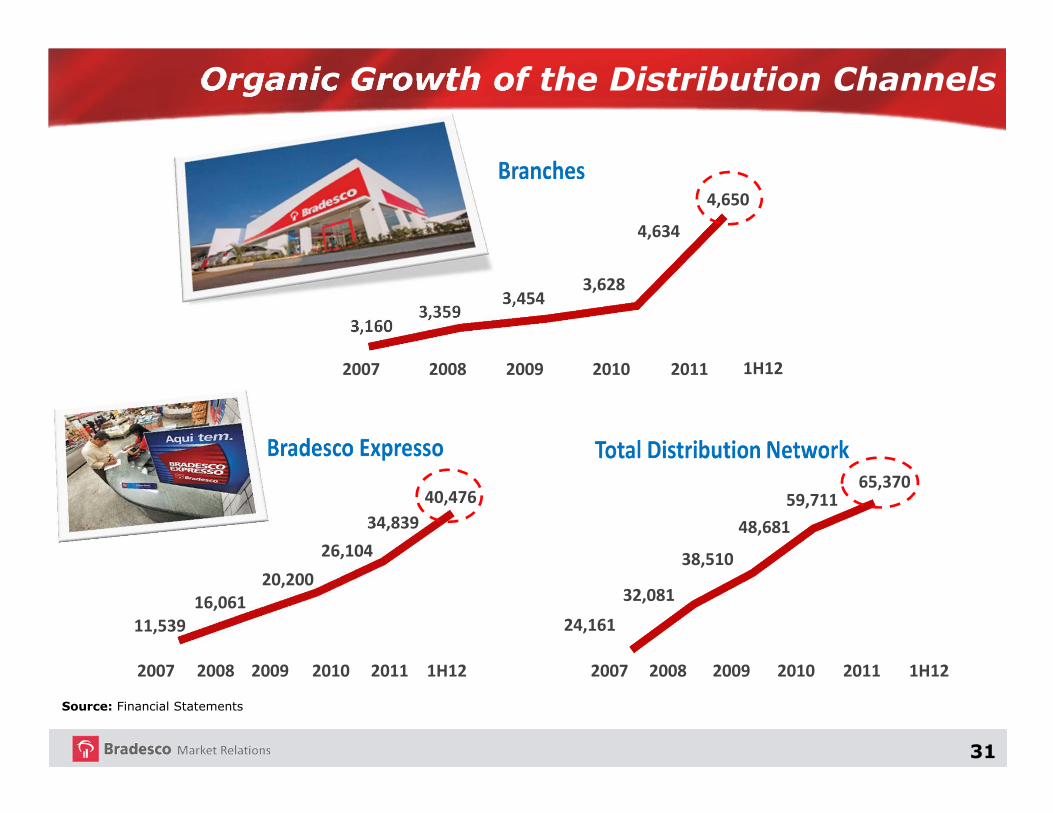

Organic Growth of the Distribution Channels

Source: Financial Statements

2007 2008 2009 2010 2011

11,539

16,061

20,200

26,104

40,476

2007 2008 2009 2010 2011

3,1603,359

3,4543,628

4,650

2007 2008 2009 2010 2011

24,161

32,081

38,510

48,681

65,370

4,634

1H12

1H121H12

34,839

59,711

32

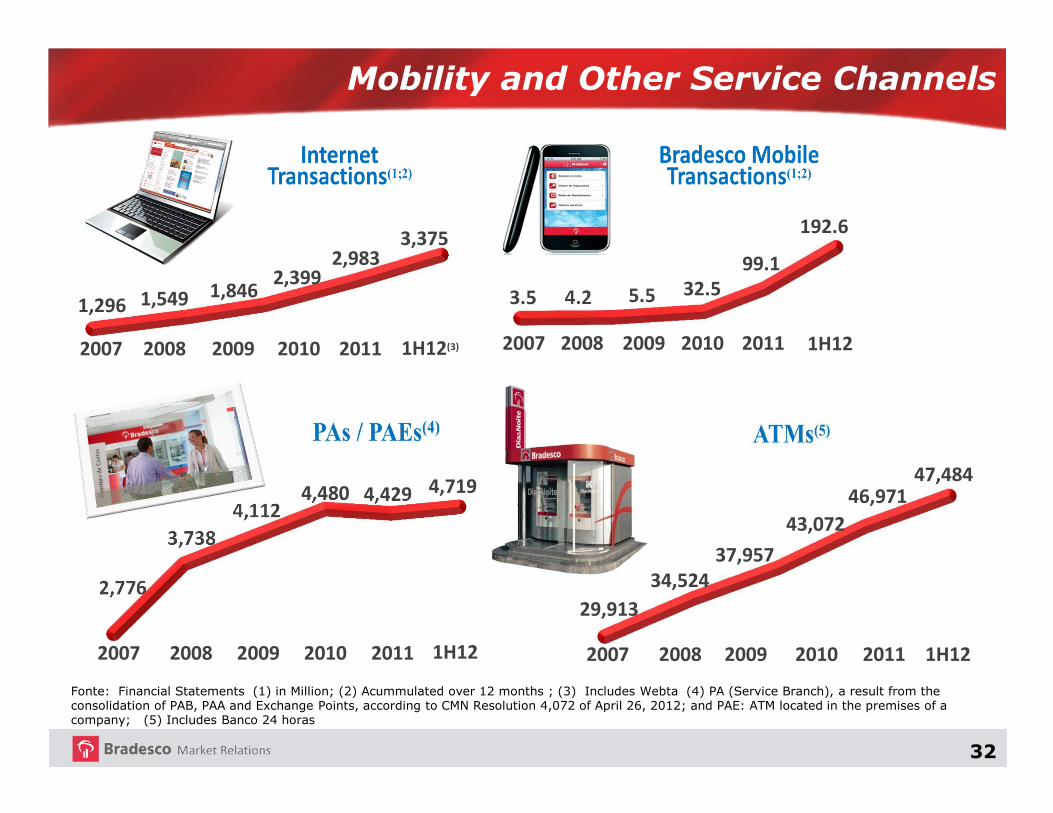

Mobility and Other Service Channels

29,913

34,524

37,957

43,072

46,971

2007 2008 2009 2010 2011 1H12

47,484

2,776

3,738

4,1124,480 4,429

2007 2008 2009 2010 2011 1H12

4,719

4.2

2007 2008 2009 2010 2011

3.5 5.5 32.5

99.1

192.6

1H122007 2008 2009 2010 2011

1,296 1,549 1,8462,399

2,983

1H12(3)

3,375

Fonte: Financial Statements (1) in Million; (2) Acummulated over 12 months ; (3) Includes Webta (4) PA (Service Branch), a result from the consolidation of PAB, PAA and Exchange Points, according to CMN Resolution 4,072 of April 26, 2012; and PAE: ATM located in the premises of a company; (5) Includes Banco 24 horas

33

Bradesco Retail - Bradesco Expresso

Bradesco has been expanding its presence in Correspondent Banks through its Bradesco Expresso

network, forming partnerships with supermarkets, drugstores, department

stores and other retail chains

34

Presence Abroad

New York

Banco Bradesco Argentina S.A.

Buenos Aires

Banco Bradesco Europa S.A.

Luxembourg

Bradesco Services Co.Ltd.

Tokyo

Grand Cayman (2)

Bradesco Securities Inc.

New York(3)

Bradesco Securities UK Ltd.

London

Cidade Capital Markets Ltd.

Grand Cayman

Bradesco Trade Services Ltd.

Hong Kong

Branch Subsidiary

Bradescard Mexico – Sociedadde Responsabilidad Limitada

(1) Holding which controls Bradesco Securities and the New York Branch. (2) Includes 2 Branches(3) Includes 2 Subsidiaries As of Jun12

Bradesco North America (1)

Mexico

Bradesco Securities Hong Kong Ltd.

35

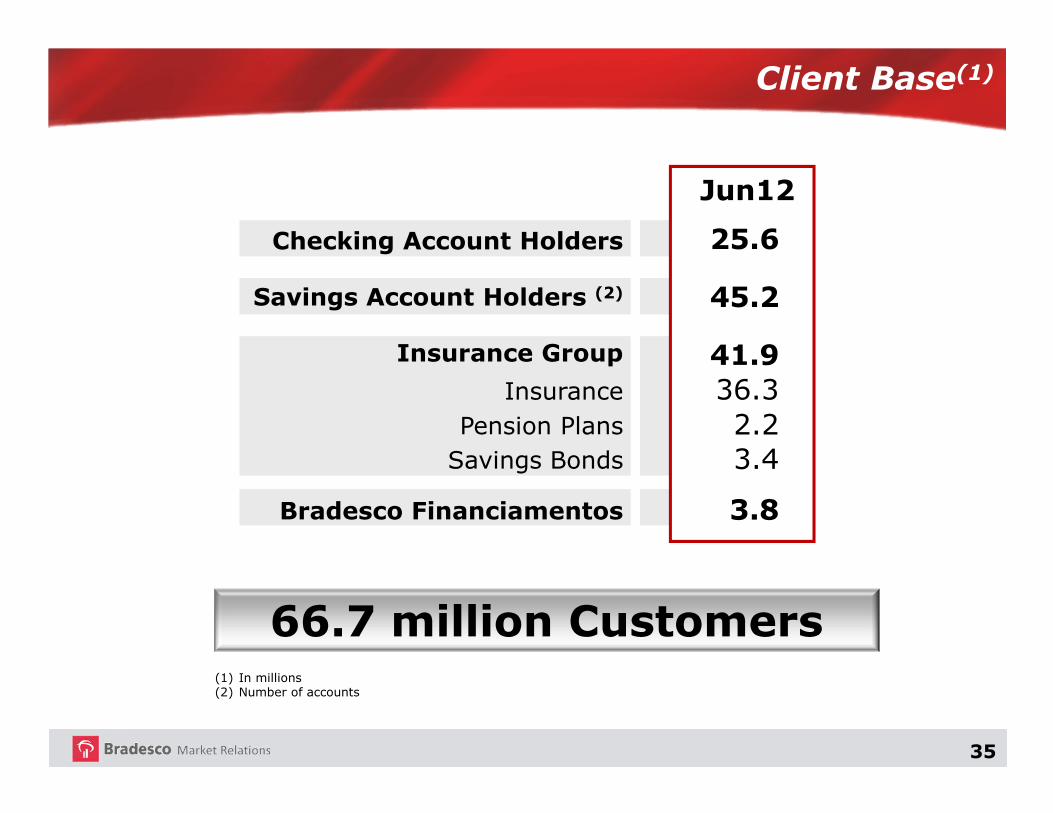

Client Base(1)

Checking Account Holders

Savings Account Holders (2)

InsurancePension Plans

Savings Bonds

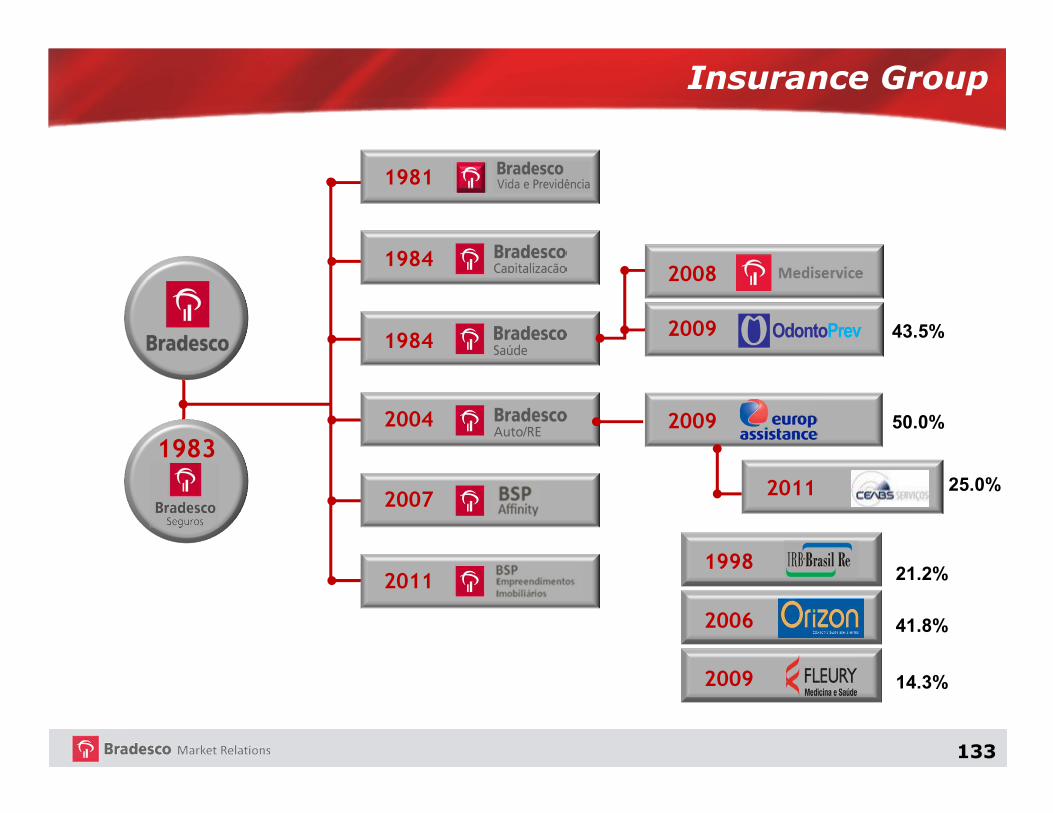

Insurance Group

Bradesco Financiamentos

Jun12

25.6

45.2

41.936.32.23.4

3.8

66.7 million Customers(1) In millions(2) Number of accounts

36

Client Segmentation

Monthly income starting at

R$ 7,000 or Investment

starting at R$ 80,000

Monthly income fromR$ 3,000 to R$ 6,999.99or Investment starting atR$ 30,000

Monthly income

up to R$ 2,999.99

Annual revenue over R$ 250 million

Annual revenue from R$ 30 million to R$ 250 million

Annual revenue up to

R$ 30 million

Exclusive

Bradesco Expresso and PAA

Small Business

Minimum investment of R$ 3 million

37

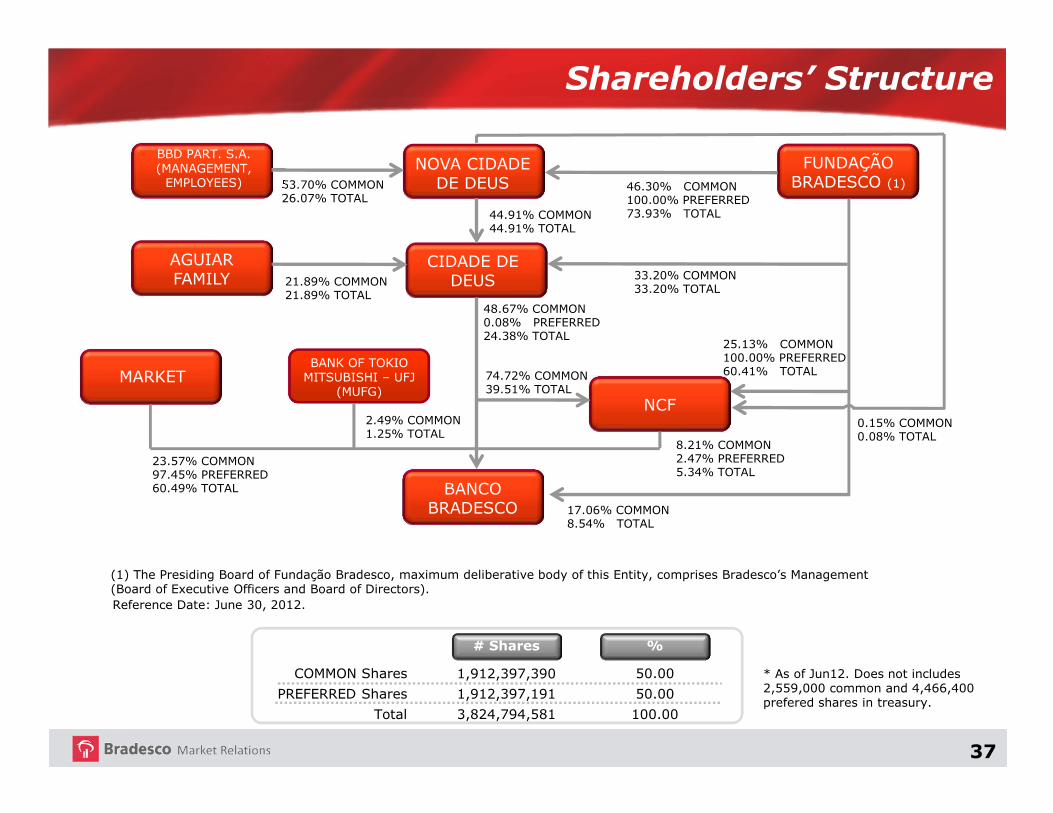

Shareholders’ Structure

100.00

50.00

50.00

3,824,794,581

1,912,397,191

1,912,397,390

Total

PREFERRED Shares

COMMON Shares

53.70% COMMON26.07% TOTAL

44.91% COMMON44.91% TOTAL

2.49% COMMON1.25% TOTAL

23.57% COMMON97.45% PREFERRED60.49% TOTAL

17.06% COMMON8.54% TOTAL

8.21% COMMON2.47% PREFERRED5.34% TOTAL

0.15% COMMON0.08% TOTAL

25.13% COMMON100.00% PREFERRED60.41% TOTAL

46.30% COMMON100.00% PREFERRED73.93% TOTAL

21.89% COMMON21.89% TOTAL

48.67% COMMON0.08% PREFERRED24.38% TOTAL

74.72% COMMON39.51% TOTAL

MARKET

BBD PART. S.A. (MANAGEMENT, EMPLOYEES)

AGUIAR FAMILY

BANCO BRADESCO

CIDADE DE DEUS

NOVA CIDADE DE DEUS

FUNDAÇÃO BRADESCO (1)

BANK OF TOKIO MITSUBISHI – UFJ

(MUFG)NCF

(1) The Presiding Board of Fundação Bradesco, maximum deliberative body of this Entity, comprises Bradesco’s Management(Board of Executive Officers and Board of Directors).

%# Shares

33.20% COMMON33.20% TOTAL

* As of Jun12. Does not includes 2,559,000 common and 4,466,400 prefered shares in treasury.

Reference Date: June 30, 2012.

38

Board of Directors

Board of Executive Officers

01

06

09

06

44

09

Chief Executive Officer

Executive Vice-Presidents

Managing Directors

Deputy Directors

Department Directors

Directors

# of Members

16 Regional Directors

Fiscal Council

03

03

01

Sitting

Deputy

Ombudsman

# of Members

Committees

07

04

10

11

14

11

Compensation Committee

Audit Committee

Compliance and Internal Controls Committee

Executive Disclosure Committee (Non-Statutory)

Ethical Conduct Committee

Integrated Risk Management and Capital Allocation Committee

# of Members

Administrative Bodies

# of Members

01

01

07

Chairman

Vice-Chairman

Members

July 10, 2012

39

Shareholders’ Profile – Bradesco

Jun12

Individuals 332,632 89.85 23.04

Companies 36,656 9.90 47.42

Foreigners 919 0.25 29.54

Total 370,207

% over Total Shareholders

ShareholdersBase

% over Total Shares

40

Main Ratings

(1) On June 27, 2012, due to changes in its methodology, the risk classifying agency Moody´s Investors Service changed three Bradesco ratings, as follows: (i) financial strength, from „B-‟ to „C-;‟ (ii) domestic currency deposits – long term, from „A1‟ to „A3;‟ and (iii) domestic currency deposit – short term, from „P-1‟ to „P-2.‟ These downgrades are due to agency‟s evaluation on the correlation between sovereign credit risk and rating of several entities in Brazil, accordingly, not referring to any change in Bank‟s financial bases.(2) On July 11, 2012, the risk classifying agency Standard & Poor´s upgraded Bradesco short-term foreign and domestic currency ratings from „A3„ to „A2,‟ as a result of the upgrade of sovereign short-term foreign currency rating after the agency changed its criteria of the connection between long and shortterm ratings attributed to sovereign governments.

Financial

Strength /

Individual Credit

Risk Profile

Foreign CurrencyDebt

Long-Term Long-Term Short-Term Long-Term Short-Term Long-Term Short-Term

Baa1 A3 P-2 Baa2 P-2 Aaa.br BR - 1

International Scale

C - / baa1

Moody's Investors Service (1)

Domestic Scale

Domestic Currency Deposit

Foreign CurrencyDeposit

DomesticCurrency

Long-Term Short-Term

Long-Term Short-Term Long-Term Short-Term Long-Term Short-Term

BBB A - 2 BBB A - 2 brAAA brA - 1

Standard & Poor's (2)

International Scale –Counterparty Rating Domestic Scale

Foreign Currency Domestic Currency Counterparty Rating

Austin Rating

AA+ AAA A -1

Domestic Scale

BBB

Issuer Rating

International Scale

R&I Inc.

Corporate Governance

Viability Support

Long-Term Short-Term Long-Term Short-Term Long-Term Short-Term

A- F1 BBB+ F2 AAA (bra) F1 + (bra)

Domestic ScaleInternational Scale

Fitch Ratings

a- 2

Domestic Currency Foreign Currency Domestic

41

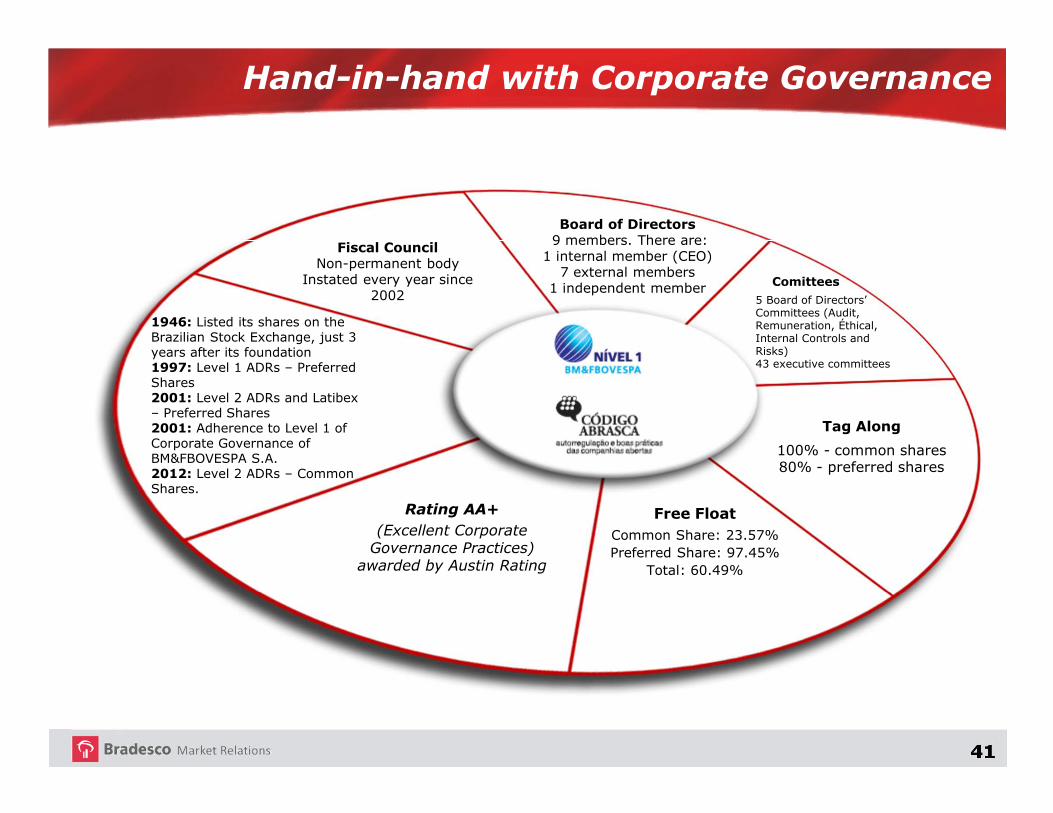

Rating AA+

(Excellent Corporate Governance Practices) awarded by Austin Rating

Tag Along

100% - common shares80% - preferred shares

1946: Listed its shares on theBrazilian Stock Exchange, just 3 years after its foundation1997: Level 1 ADRs – PreferredShares2001: Level 2 ADRs and Latibex– Preferred Shares2001: Adherence to Level 1 ofCorporate Governance ofBM&FBOVESPA S.A.2012: Level 2 ADRs – Common Shares.

Hand-in-hand with Corporate Governance

Free Float

Common Share: 23.57% Preferred Share: 97.45%

Total: 60.49%

Fiscal CouncilNon-permanent body

Instated every year since2002

Board of Directors9 members. There are:

1 internal member (CEO)7 external members

1 independent member Comittees

5 Board of Directors’ Committees (Audit, Remuneration, Éthical, Internal Controls andRisks)43 executive committees

42

Transaction Breakdown

As of 1H12

ATMs(Outside Branches)

9%

ATMs (Inside Branches)

21%

Branches8%

Call Center7%

Internet+FT50%

Automatic Debit1%

Mobile4%

43

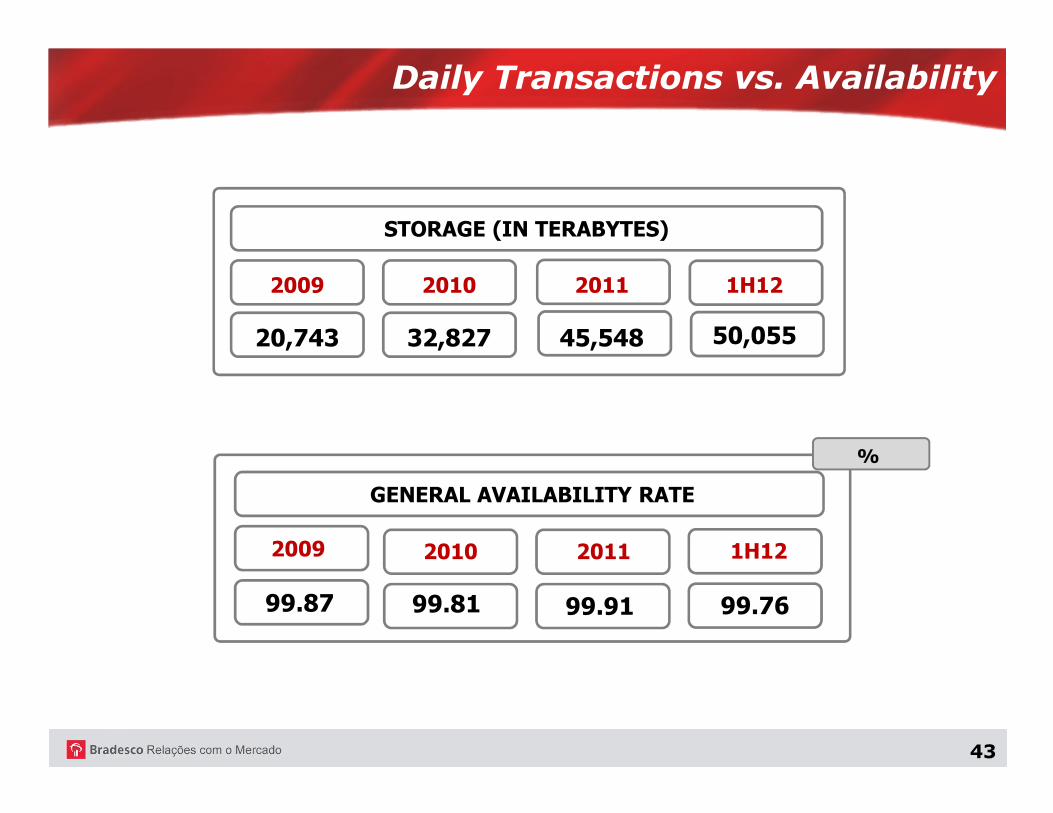

Daily Transactions vs. Availability

20,743

2009

32,827

2010

45,548

2011 1H12

STORAGE (IN TERABYTES)

%

99.87

2009

99.81

2010

99.91

2011

99.76

1H12

GENERAL AVAILABILITY RATE

50,055

44

IT Revitalization Plan

APPLICATIONS

PROCESSES

OPERATIONAL ENVIRONMENT

INFRASTRUCTURE

TECHNOLOGY

Internet

Departmental Servers

Logic Security

AUG 07

MAY 05

NOV 05

AUG 08

AUG 08

AUG 08

MAI/09

JUN/09

OCT 06

OCT 07

JUL 08

SET/09

SET/09

SET/09

SET/09

DEZ/10

DEC 05

JUN 08

JUN 08

FEB 07

FEB 08

MAY 08

IT Services Management

Profile of Competitor Channels

Capacity Management

Testing and Approval Environment

Pre-Production Environment

Channel Availability

Construction and Infrastructure

New/Brand New Site

Alphaville Site

Corporate Communication Network

Operational Centers

Contingency

MAY 09

JUN 09

SEP 09

SEP 09

SEP 09

SEP 09

DEC 10

Implem.

DEC 10

MAR 09

JUN 09

JUN 09

DEC 10

IT Governance

Information Access Management

Methods and Metrics

UN IT Alignment

Content Management

Branch Channel

Channel Certification

CI - Occupancy

Centers and Service Branches

Software Testing Environment

High Availability

Oper. Environment Management 82 Visits: BRA, USA, EUR

2,350 Allocated Professionals

3,937 Executive Meetings

43,000 Products/ Documents

9,871,941 Hours Worked

Numbers

Jun 2012

Implementing Completed

27

1

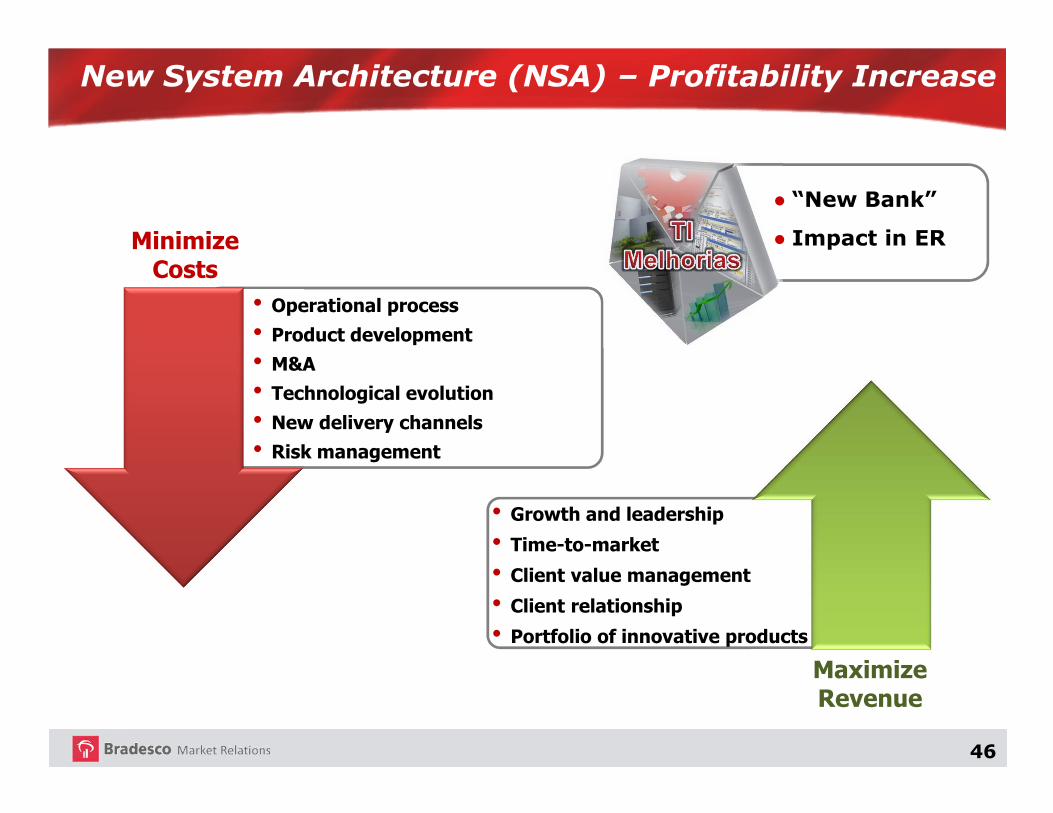

New System Architecture (NSA)

45

Management

Performance

• Enhanced satisfaction of users and clients

• Enhanced promptness to respond to the market

• Reduced rework and inefficiency

• Lower operational risks

• Costs and expenses reduction

• Better service level

• Management of factors that generate “incidents”

• Achievements in the flow of work

Medium and Long-Term Results

Short-Term Results

Impact on Efficiency

46

• Operational process• Product development• M&A• Technological evolution• New delivery channels

• Risk management

Minimize Costs

MaximizeRevenue

• Growth and leadership• Time-to-market• Client value management• Client relationship• Portfolio of innovative products

● “New Bank”

● Impact in ER

New System Architecture (NSA) – Profitability Increase

47

Investments in Infrastructure, Information Technology and Telecommunications

Source: Financial Statements.

Total Investments in the period(2006 through 1H12): R$ 20.3 billion

R$ Million

2006 2007 2008 2009 2010 2011 1S12

1,472 1,621 2,003

2,827 3,204 3,241

1,713

354 478

667

630

716 1,087

273

1,826 2,099

2,670

3,457

3,920 4,328

1,986

TI/Telecommunications Infrastructure

1H12

48

Stock Evolution *

Source: Economatica.

1H122007

-10%59% 46%

5%6% 3%

2008

-52%

-34%

Bradesco - ADR

Dow Jones

Accumulated

*Adjusted by dividends delivered. Calculated in US$.

2009

124%

19%

2010

13%

11%

2007 2008 2009 2010 2011

2011

-15%

6%

46%

3%

1H12

49

Liquidity

Trading Volume

R$ 352.4 Million / Day

Source: Economatica

2007

1H12

R$ 509.9 Million / Day

50

R$ Million

Market Capitalization

3.6x 1.9x

Multiple P/BV

2.5x 2.3x

15.2x 8.6x

Multiple P/E

13.6x 11.2x

1.9x

9.6x(1) Includes latest 12 months of adjusted net income.

109,463

65,354

103,192109,759 106,971

2007 2008 2009 2010 2011 2012

1.6x

9.2x (1)

1H12

104,869

51

Dividends

R$ Million

R$ 19.4 billionMore than

in dividendsover the period

2,160

2,823 2,692 2,718

3,369

3,740

1,916

31.5% 31.5%

33.1%

31.5% 31.5% 31.5% 31.5%

35.3%34.4%

37.2%

35.7% 35.4% 35.7% 35.6%

2006 2007 2008 2009 2010 2011 1H12

Dividends Net Pay Out(1) Gross Pay Out(1)

(1) Accumulated 12 months.

52

EPS (1) and Net Income

(1) For EPS comparison purposes, shares were adjusted in line with stock bonuses and splits.

R$ Million

2,738 2,825

2,864 2,771

2,845 2,867

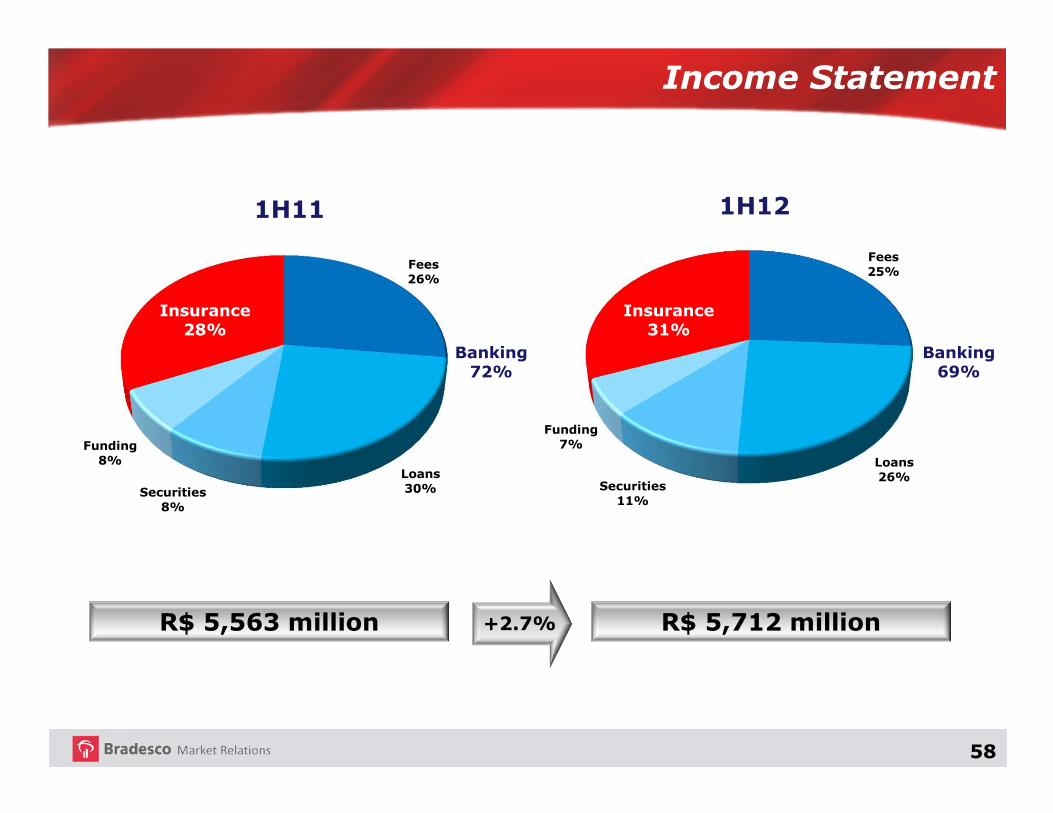

5,563 5,712

2.722.82

2.91 2.93 2.96 2.97

2.82

2.97

1Q11 2Q 3Q 4Q 1Q12 2Q 1H11 1H12

Adjusted Net Income Earnings per Share - in the last 12 months

53

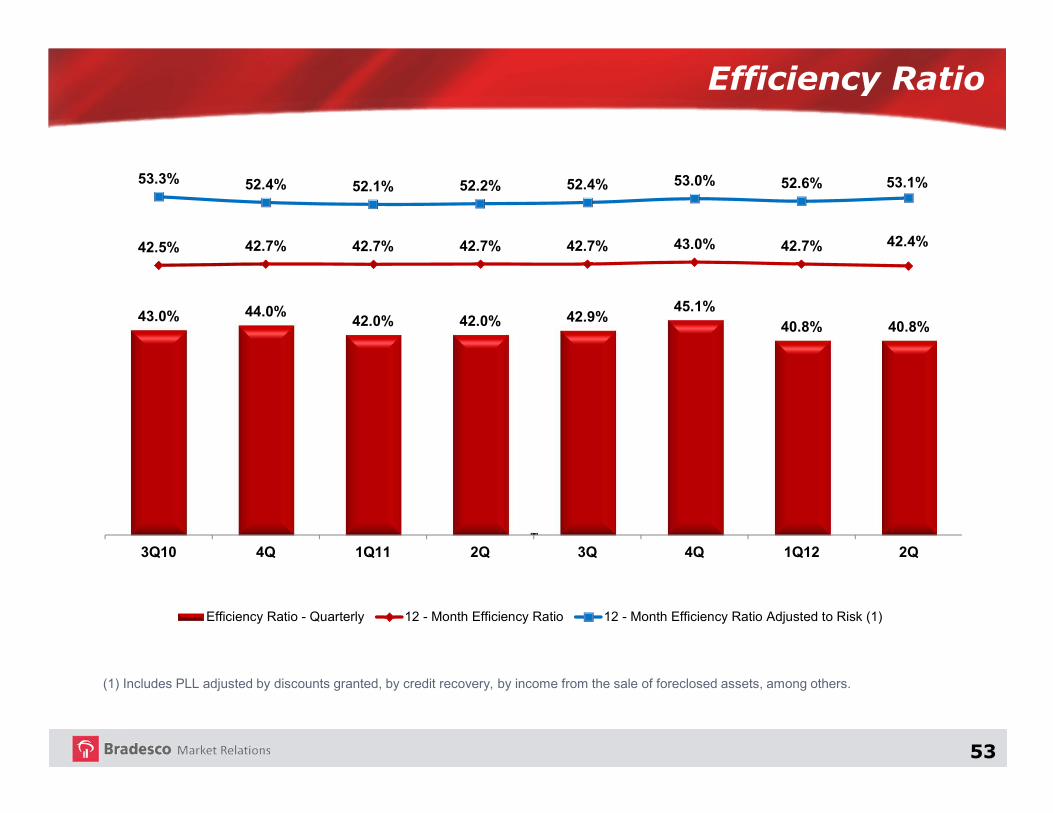

Efficiency Ratio

(1) Includes PLL adjusted by discounts granted, by credit recovery, by income from the sale of foreclosed assets, among others.

43.0% 44.0%42.0% 42.0% 42.9%

45.1%

40.8% 40.8%

42.5% 42.7% 42.7% 42.7% 42.7% 43.0% 42.7% 42.4%

53.3% 52.4% 52.1% 52.2% 52.4% 53.0% 52.6% 53.1%

3Q10 4Q 1Q11 2Q 3Q 4Q 1Q12 2Q

Efficiency Ratio - Quarterly 12 - Month Efficiency Ratio 12 - Month Efficiency Ratio Adjusted to Risk (1)

54

Net Income and Efficiency Ratio

Adjusted Net Income Efficiency Ratio (12 months)

R$ Million

43.1% 43.3%40.5%

42.7% 43.0% 42.7% 42.4%

7,210 7,625 7,586

9,804

11,198

5,563 5,712

2007 2008 2009 2010 2011 1H11 1H12

55

Income Statement

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

Net Interest Income 11,034 10,695 21,729 18,833 3.2 15.4

Provision for Loan Losses (3,407) (3,094) (6,501) (4,797) 10.1 35.5

Gross Income from Fin. Interm. 7,627 7,601 15,228 14,036 0.3 8.5

Insurance, Pension Plans, Saving Bonds 953 877 1,830 1,573 8.7 16.3

Fee Income 4,281 4,118 8,399 7,261 4.0 15.7

Personnel and Administrative Expenses (6,488) (6,279) (12,767) (11,360) 3.3 12.4

Tax Expenses (991) (1,012) (2,003) (1,793) (2.1) 11.7

Equity in the Earnings and Affiliated Companies 19 40 59 50 (52.5) 18.0

Other Operating Revenues/Expenses (1,035) (996) (2,031) (1,686) 3.9 20.5

Operating Income 4,366 4,349 8,715 8,081 0.4 7.8

Non-Operating Income (22) (18) (40) (11) 22.2 -

Inc. Tax/Social Contr., Minority Interest (1,477) (1,486) (2,963) (2,507) (0.6) 18.2

Adjusted Net Income 2,867 2,845 5,712 5,563 0.8 2.7

Non-Recurring Events 34 52 86 76 (34.6) 13.2

Book Net Income 2,833 2,793 5,626 5,487 1.4 2.5

Variation %

56

Book Net Income x Adjusted Net Income

(1) Annualized.

R$ Million

2Q12 1Q12 1H12 1H11

Book Net Income 2,833 2,793 5,626 5,487

Non-Recurring Events 34 52 86 76

- Provision for Civil Contingencies 57 86 143 123

- Tax Effects (23) (34) (57) (47)

Adjusted Net Income 2,867 2,845 5,712 5,563

ROAE % (1) 20.6 21.0 20.3 22.9

ROAE % (Adjusted) (1) 20.9 21.4 20.6 23.2

57

Unrealized Gains

R$ Million

Note: Excluding the unrecorded goodwill from real estate for own use, in the amount of R$ 3,030 million;(1) Includes advances on exchange contracts, leasing operations and other receivables with credit characteristics; and(2) Includes, basically, the goodwill of interest in Cielo, Odontoprev, BM&FBovespa, Fleury and Serasa.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Securities - Fixed Income 9,873 6,838 3,877 44.4 154.7

Securities - Equities (1,733) (1,127) (845) 53.8 105.1

Loan Operations (1) 1,537 (160) (574) - -

Investments (2) 12,711 11,316 7,313 12.3 73.8

Others (844) (737) (394) 14.5 114.2

Total 21,544 16,130 9,377 33.6 129.8

Variation %

58

R$ 5,563 million R$ 5,712 million

Banking 72%

Banking 69%

Income Statement

+2.7%

Fees26%

Loans 30%Securities

8%

Funding8%

1H11

Insurance28%

Fees25%

Loans 26%

Securities11%

Funding7%

1H12

Insurance31%

59

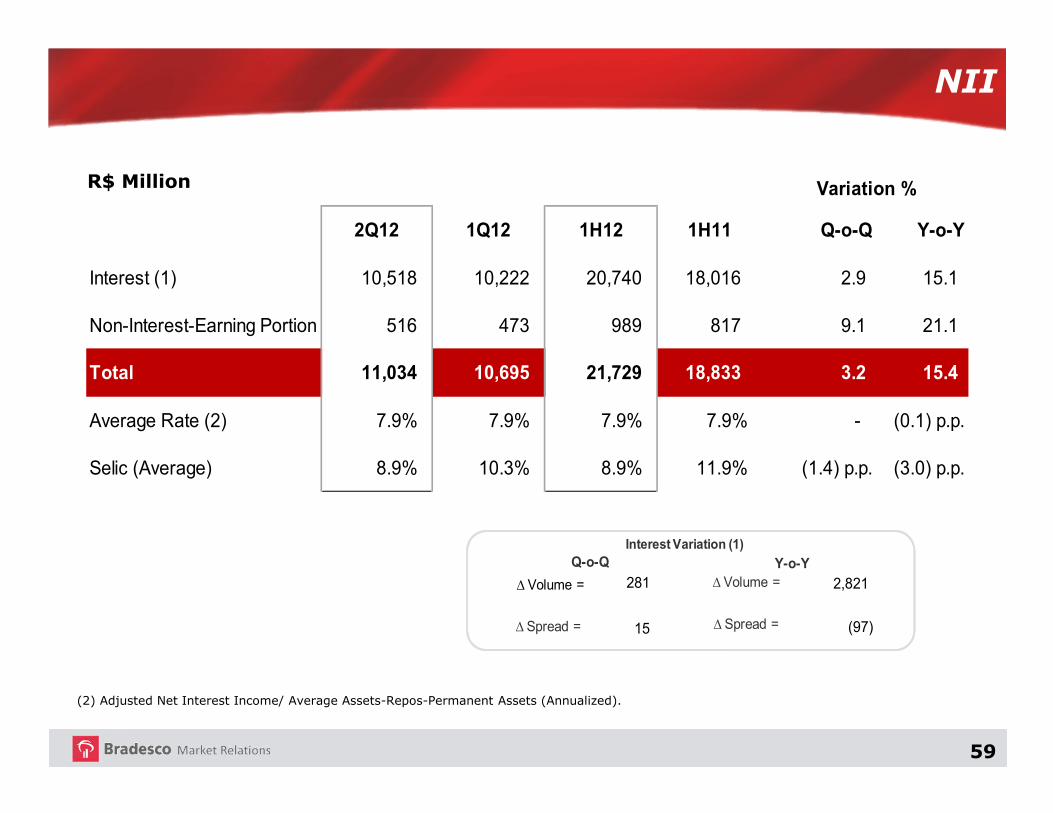

NII

(2) Adjusted Net Interest Income/ Average Assets-Repos-Permanent Assets (Annualized).

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

Interest (1) 10,518 10,222 20,740 18,016 2.9 15.1

Non-Interest-Earning Portion 516 473 989 817 9.1 21.1

Total 11,034 10,695 21,729 18,833 3.2 15.4

Average Rate (2) 7.9% 7.9% 7.9% 7.9% - (0.1) p.p.

Selic (Average) 8.9% 10.3% 8.9% 11.9% (1.4) p.p. (3.0) p.p.

∆ Volume = Interest Variation (1) ∆ Spread =

281 2,821

15 (97)

Variation %

∆ Spread = ∆ Spread =

Q-o-Q

∆ Volume =

Y-o-Y∆ Volume =

Interest Variation (1)

60

NII- Interest /Trading Gains

R$ Million

7,904 8,553 8,849 9,167

9,669 9,985 10,222 10,518

398

465 513

304

561 273 473

516

8888,,,,302 302 302 302 9,018 9,018 9,018 9,018

9,362 9,362 9,362 9,362 9,471 9,471 9,471 9,471

10,230 10,230 10,230 10,230 10,258 10,258 10,258 10,258 10,695 10,695 10,695 10,695 11,034 11,034 11,034 11,034

3Q10 4Q 1Q11 2Q 3Q 4Q 1Q12 2Q

Interest-Earning Portion Non-Interest-Earning Portion

61

NII

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

- Loans 7,362 7,181 14,543 12,728 2.5 14.3

- Funding 1,041 1,168 2,209 2,141 (10.9) 3.2

- Insurance 726 851 1,577 1,818 (14.7) (13.3)

- Securities / Others 1,389 1,022 2,411 1,329 35.9 81.4

NII - Interest-Earning Portion 10,518 10,222 20,740 18,016 2.9 15.1

Variation %

62

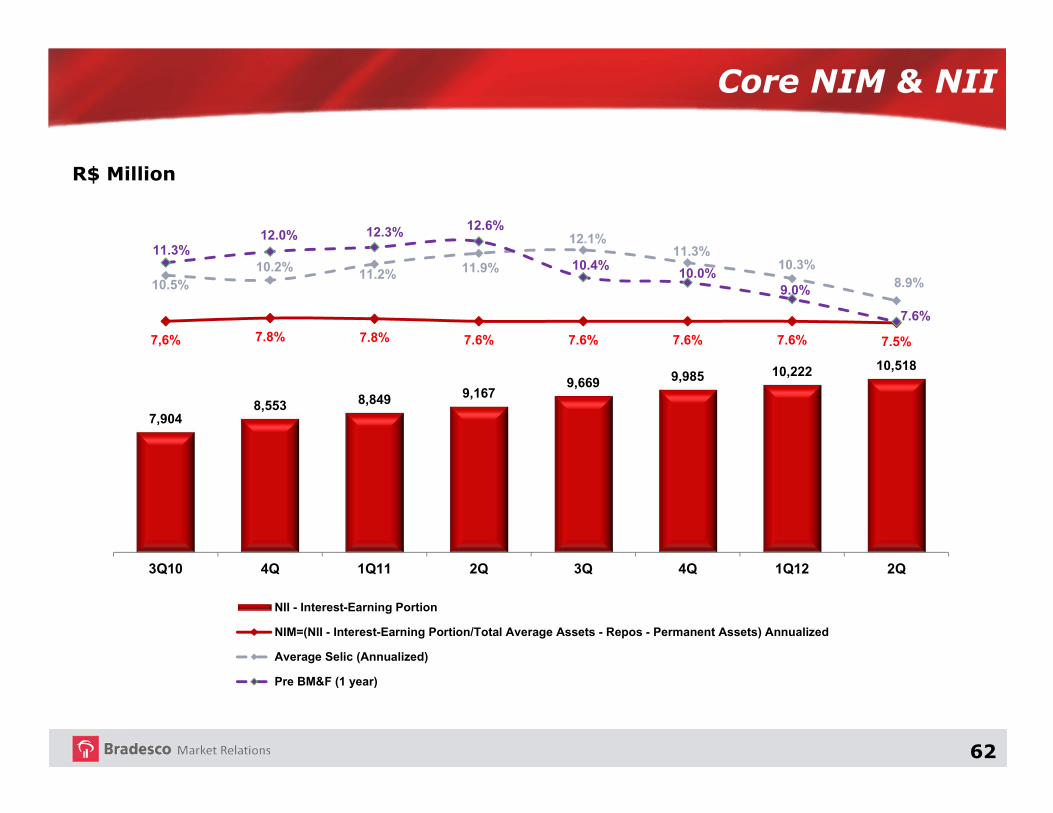

Core NIM & NII

R$ Million

7,904 8,553 8,849 9,167

9,669 9,985 10,222 10,518

7,6% 7.8% 7.8% 7.6% 7.6% 7.6% 7.6% 7.5%

10.5%10.2% 11.2% 11.9%

12.1%11.3%

10.3%8.9%

11.3%12.0% 12.3% 12.6%

10.4%10.0%

9.0%

7.6%

3Q10 4Q 1Q11 2Q 3Q 4Q 1Q12 2Q

NII - Interest-Earning Portion

NIM=(NII - Interest-Earning Portion/Total Average Assets - Repos - Permanent Assets) Annualized

Average Selic (Annualized)

Pre BM&F (1 year)

63

Spread

Source: Brazilian Central Bank´s Credit and Banking report 2010.

%

32.73

28.74

21.89

12.56

4.08

Net Interest Margin Deliquency Direct Taxes Administrative Costs Indirect Taxes

64

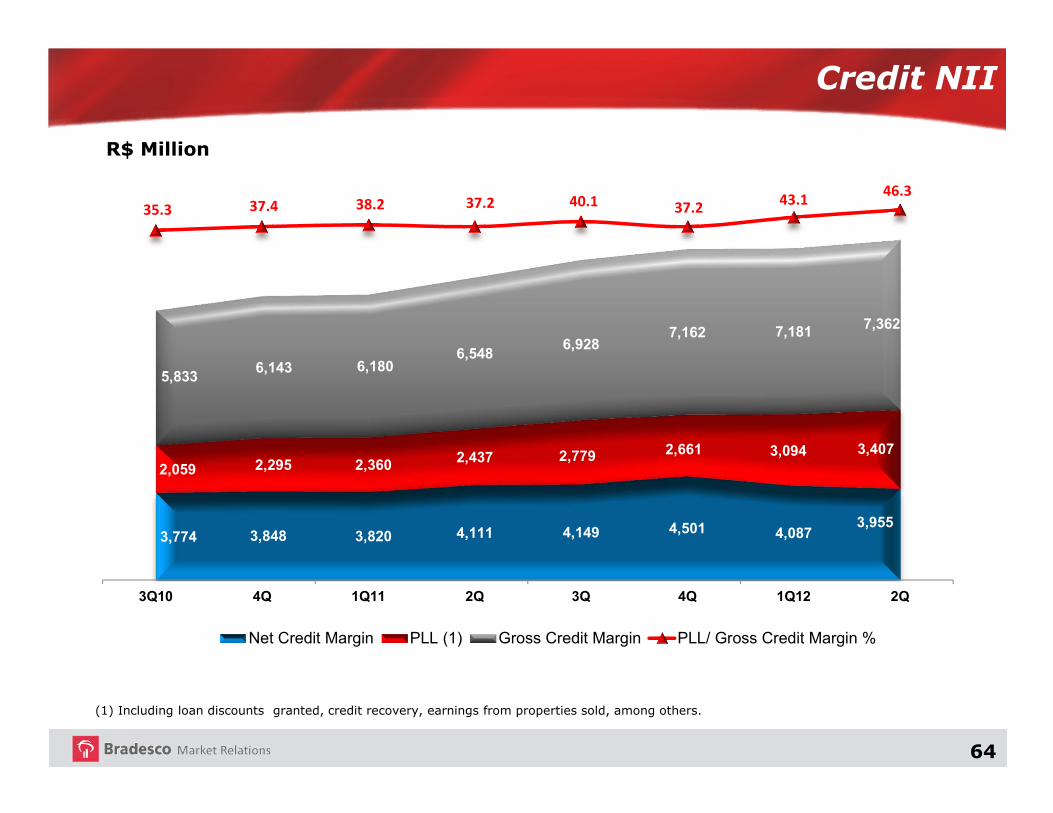

Credit NII

R$ Million

3,774 3,848 3,820 4,111 4,149 4,501 4,0873,955

2,059 2,295 2,360 2,437 2,779 2,661 3,094 3,407

5,8336,143 6,180

6,5486,928

7,162 7,181 7,362

35.3 37.4 38.2 37.2 40.1 37.2 43.1

46.3

3Q10 4Q 1Q11 2Q 3Q 4Q 1Q12 2Q

Net Credit Margin PLL (1) Gross Credit Margin PLL/ Gross Credit Margin %

(1) Including loan discounts granted, credit recovery, earnings from properties sold, among others.

65

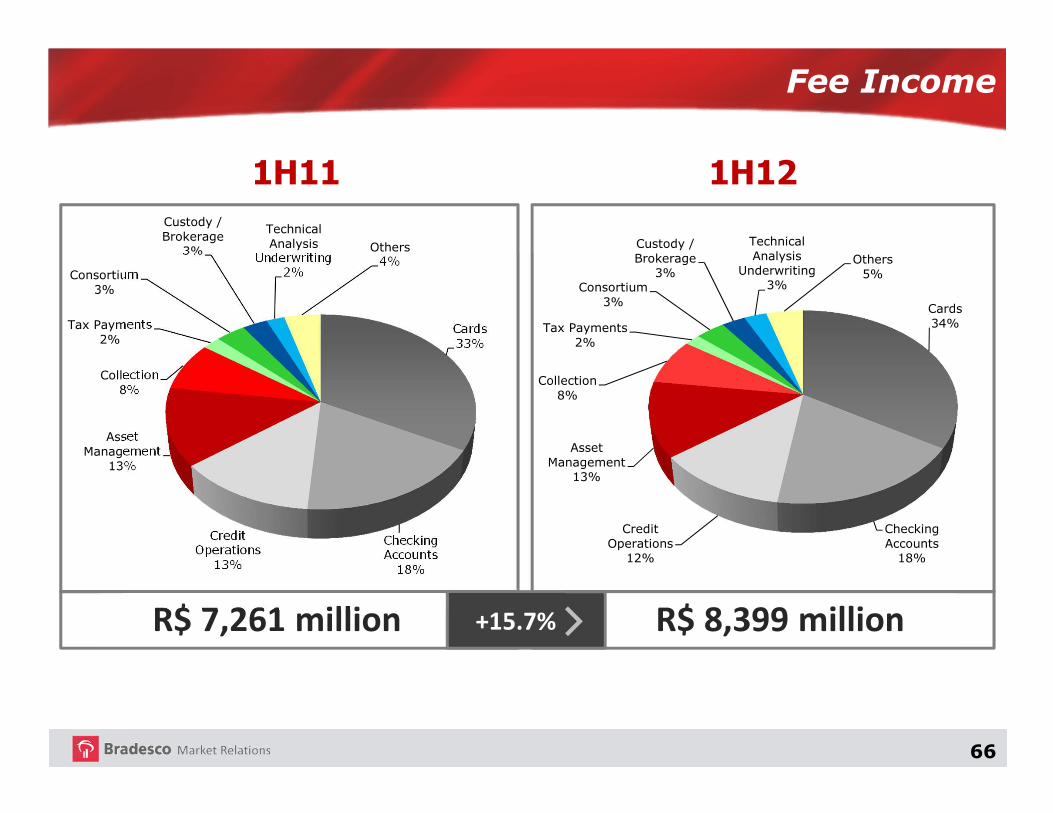

Fee Income

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

Cards 1,456 1,389 2,845 2,391 4.8 19.0

Checking Accounts 805 748 1,553 1,330 7.6 16.8

Asset Management 535 526 1,061 945 1.7 12.3

Loan Operations 524 501 1,025 951 4.6 7.8

Collection 322 313 636 575 2.9 10.6

Consortium 150 144 293 250 4.2 17.2

Custody / Brokerage 119 117 236 210 1.7 12.4

Technical Analysis / Underwriting 115 109 224 152 5.5 47.4

Tax Payments 80 78 158 153 2.6 3.3

Others 175 193 368 304 (9.3) 21.1

Total 4,281 4,118 8,399 7,261 4.0 15.7

Variation %

66

Fee Income

1H11 1H12

R$ 7,261 million R$ 8,399 million

Cards 33%

Checking Accounts

18%

Credit Operations

13%

Asset Management

13%

Collection 8%

Tax Payments2%

Consortium3%

Custody / Brokerage

3%

Technical Analysis

Underwriting2%

Others 4%

Cards34%

Checking Accounts

18%

Credit Operations

12%

Asset Management

13%

Collection 8%

Tax Payments2%

Consortium3%

Custody / Brokerage

3%

Technical Analysis

Underwriting3%

Others 5%

+15.7%

67

Operating Expenses

(1) Accumulated over 12 months

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

- Structural 2,436 2,351 4,786 4,097 3.6 16.8

- Non-Structural 611 527 1,139 944 15.9 20.7

Personnel 3,047 2,878 5,925 5,041 5.9 17.5

Administrative 3,441 3,401 6,842 6,319 1.2 8.3

Total 6,488 6,279 12,767 11,360 3.3 12.4

Op. Expenses(1) / Total Assets 3.1% 3.2% 3.1% 3.3% (0.1)p.p. (0.2)p.p.

Variation %

68

Other Administrative Expenses

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

Third-Party Services 832 832 1,664 1,713 - (2.9)

Communication 415 410 825 769 1.2 7.3

Depreciation and Amortization 308 301 609 538 2.3 13.2

Data Processing 268 262 530 444 2.3 19.4

Transports 215 212 427 358 1.4 19.3

Rental 196 183 379 320 7.1 18.4

Financial System Services 163 163 326 235 - 38.7

Advertising 162 153 315 396 5.9 (20.5)

Maintenance and Repairs 145 146 291 261 (0.7) 11.5

Leasing 96 100 196 171 (4.0) 14.6

Others 641 639 1,280 1,114 0.3 14.9

Total 3,441 3,401 6,842 6,319 1.2 8.3

Variation %

69

Operational Coverage Ratio (1)

R$ Million

3Q09 4Q 1Q10 2Q 3Q 4Q 1Q11 2Q 3Q 4Q 1Q12 2Q

16,863

11,189

66.4

17,460 18,220

19,055 19,871

20,834 21,643

22,451

23,435 24,467

25,170 25,874

11,616 12,017 12,359 12,929 13,372

13,758 14,256 14,705

15,223 15,831 16,361

66.5 66.0 64.9 65.1 64.2 63.6 63.5 62.7 62.2 62.9 63.2

Admin + Personnel Expenses (a)

Fee Income (b)

Coverage Ratio % (b/a)(1) Accumulated over 12 months.

70

Tax Expenses

R$ Million

1Q12 Q-o-Q Y-o-Y

ISSQN 225 6.4 13.6

COFINS 1,382 (2.3) 14.7

PIS 233 (2.5) 14.8

IPTU 30 (50.0) 11.1

Total Tax Expenses 2,003 (2.1) 11.7

Variation %

Other – Misc. Taxes and Fees 133 1.6 (16.9)

1H12

109

699

118

20

1,012

66

2Q12

116

683

115

10

991

67

198

1,205

203

27

1,793

160

1H11

71

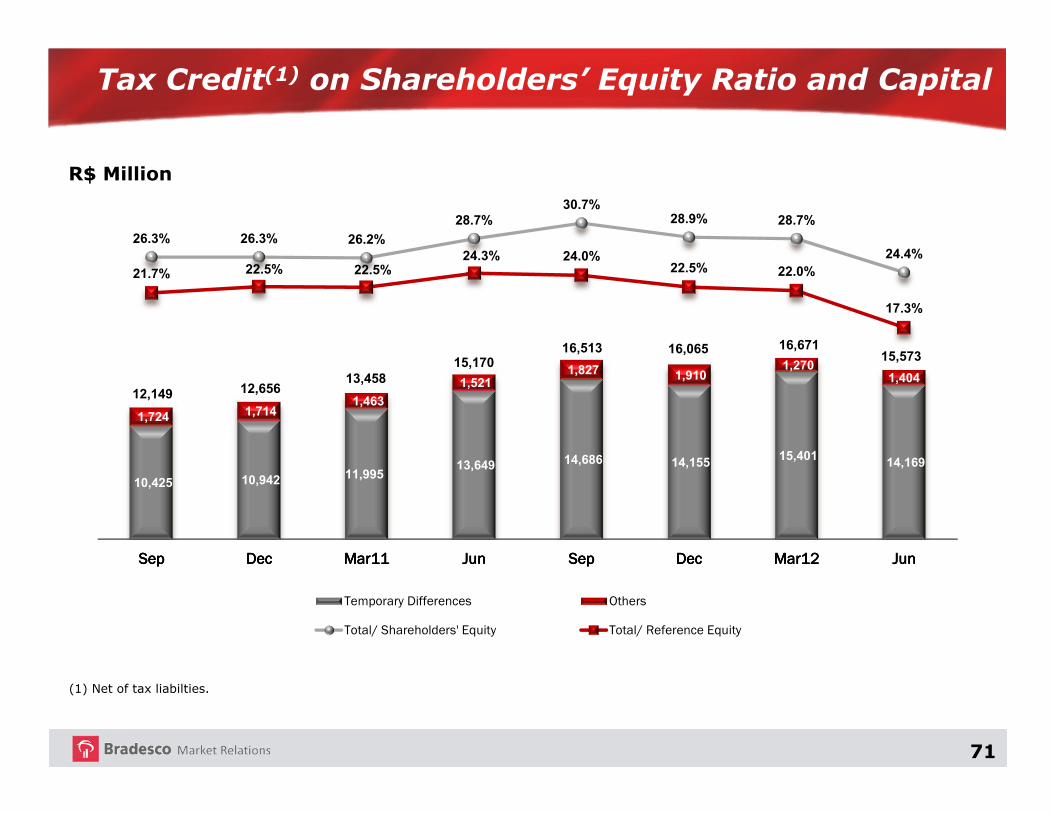

Tax Credit(1) on Shareholders’ Equity Ratio and Capital

(1) Net of tax liabilties.

R$ Million

10,425 10,942 11,995 13,649 14,686 14,155 15,401 14,169

1,724 1,714 1,463

1,521 1,827 1,910

1,270 1,404

26.3% 26.3% 26.2%

28.7%30.7%

28.9% 28.7%

24.4%

21.7% 22.5% 22.5%24.3% 24.0%

22.5% 22.0%

17.3%

12,149 12,656 13,458

15,170 16,513 16,065 16,671

15,573

SepSepSepSep DecDecDecDec Mar11Mar11Mar11Mar11 JunJunJunJun SepSepSepSep DecDecDecDec Mar12Mar12Mar12Mar12 JunJunJunJun

Temporary Differences Others

Total/ Shareholders' Equity Total/ Reference Equity

72

Total Assets and Shareholders’ Equity

R$ Million

689,307

789,550 830,520

1.7% 1.5% 1.4%

Jun11 Mar12 Jun12

Total Assets

Total Assets ROAA (1)

52,843

58,060

63,920

23.2%21.4% 20.6%

Jun11 Mar12 Jun12

Shareholders' Equity

Shareholders' Equity ROAE (1) (2)

(1) Accumulated Adjusted Net Income for the period;(2) Excludes mark-to-market effects of available-for-sale securities registered under Shareholders’ Equity; and(3) Consider the amount of R$ 7,878 million of subordinated financial bills to constitute Tier II Capital, ratified in the second quarter of 2012 by the Central Bank.

Jun11 Mar12 Jun12

Tier I 12.9 12.0 11.8

Tier II 1.8 3.0 5.2

Deductions - - -

BIS 14.7 15.0 17.0

Basel Ratio- BIS II %

73

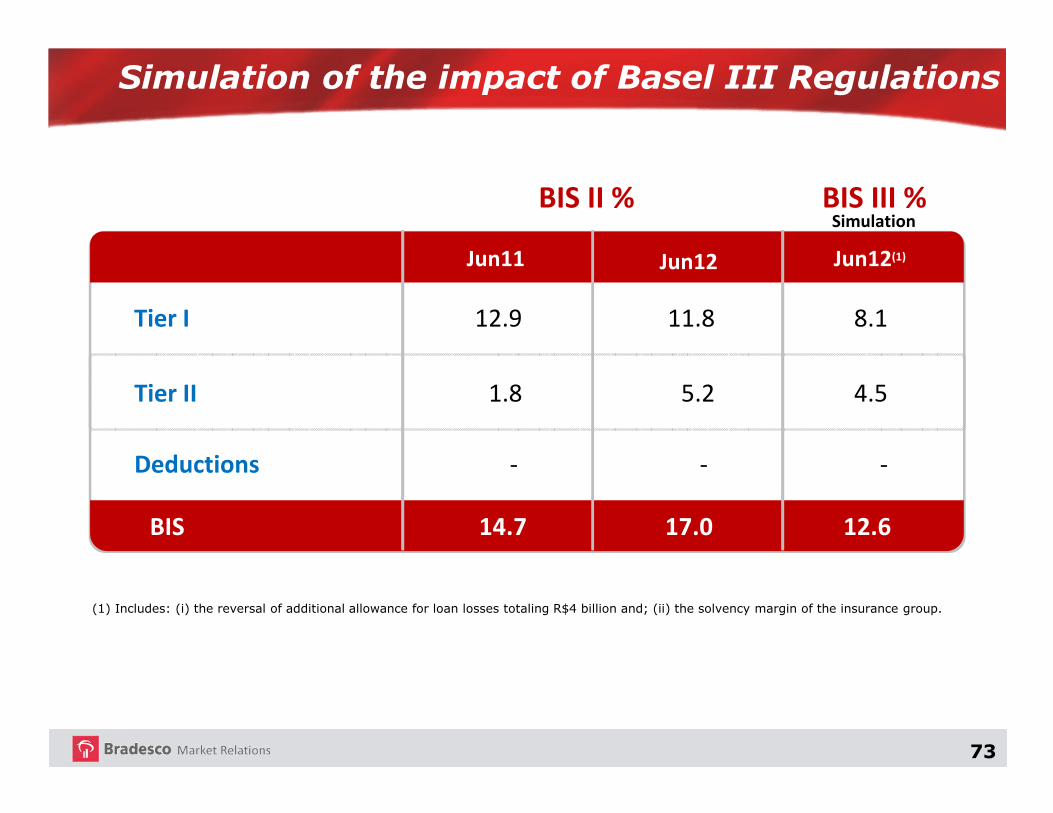

Simulation of the impact of Basel III Regulations

Simulation

Tier I 12.9 11.8 8.1

Tier II 1.8 5.2 4.5

Deductions - - -

BIS 14.7 17.0 12.6

BIS II % BIS III %

Jun11 Jun12 Jun12(1)

(1) Includes: (i) the reversal of additional allowance for loan losses totaling R$4 billion and; (ii) the solvency margin of the insurance group.

74

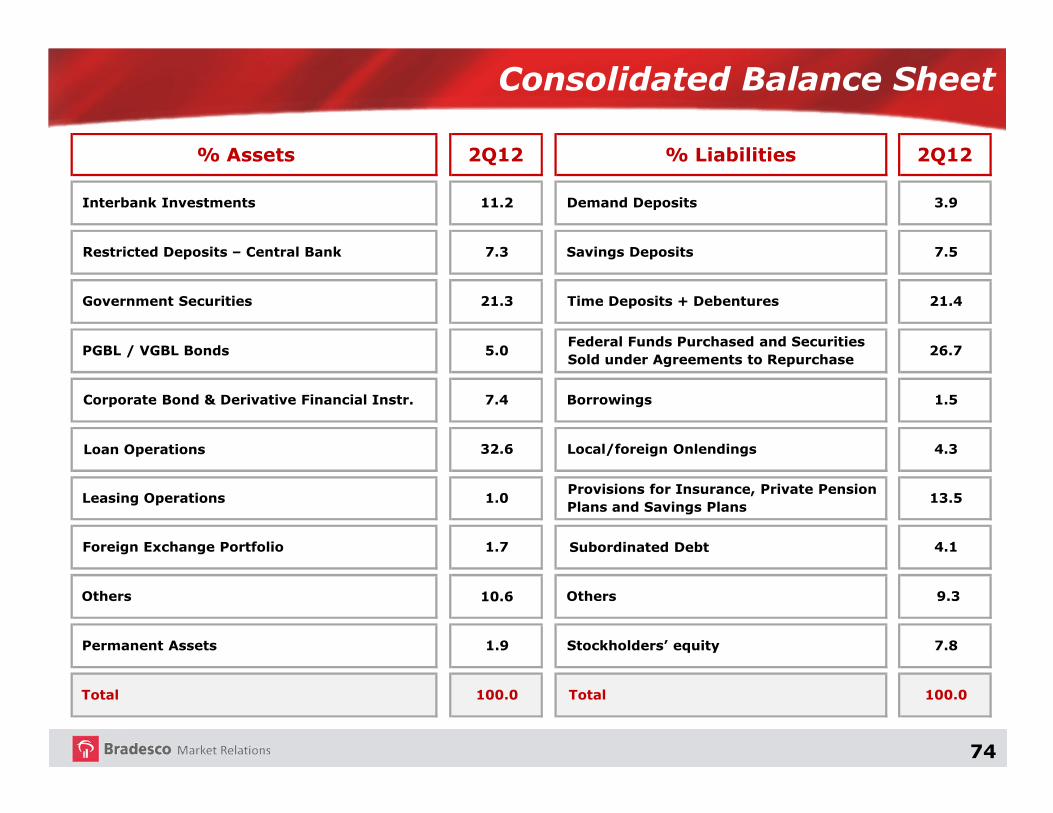

Consolidated Balance Sheet

% Assets 2Q12 % Liabilities 2Q12

Interbank Investments 11.2 Demand Deposits 3.9

Restricted Deposits – Central Bank 7.3 Savings Deposits 7.5

Government Securities 21.3 Time Deposits + Debentures 21.4

PGBL / VGBL Bonds 5.0Federal Funds Purchased and Securities

Sold under Agreements to Repurchase26.7

Corporate Bond & Derivative Financial Instr. 7.4 Borrowings 1.5

Loan Operations 32.6 Local/foreign Onlendings 4.3

Leasing Operations 1.0Provisions for Insurance, Private Pension

Plans and Savings Plans13.5

Foreign Exchange Portfolio 1.7 Subordinated Debt 4.1

Others 10.6 Others 9.3

Permanent Assets 1.9 Stockholders’ equity 7.8

Total 100.0 Total 100.0

75

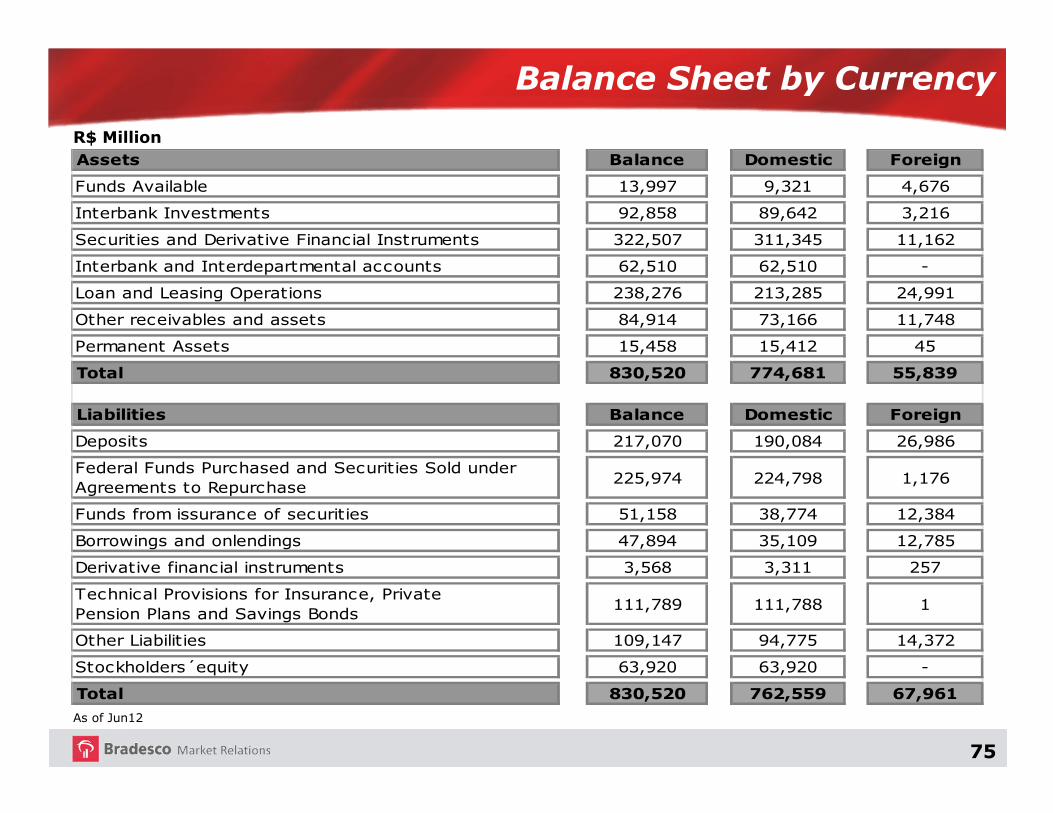

Balance Sheet by Currency

As of Jun12

R$ Million

Assets Balance Domestic Foreign

Funds Available 13,997 9,321 4,676

Interbank Investments 92,858 89,642 3,216

Securities and Derivative Financial Instruments 322,507 311,345 11,162

Interbank and Interdepartmental accounts 62,510 62,510 -

Loan and Leasing Operations 238,276 213,285 24,991

Other receivables and assets 84,914 73,166 11,748

Permanent Assets 15,458 15,412 45

Total 830,520 774,681 55,839

Liabilities Balance Domestic Foreign

Deposits 217,070 190,084 26,986

Federal Funds Purchased and Securities Sold under Agreements to Repurchase

225,974 224,798 1,176

Funds from issurance of securities 51,158 38,774 12,384

Borrowings and onlendings 47,894 35,109 12,785

Derivative financial instruments 3,568 3,311 257

Technical Provisions for Insurance, PrivatePension Plans and Savings Bonds

111,789 111,788 1

Other Liabilities 109,147 94,775 14,372

Stockholders´equity 63,920 63,920 -

Total 830,520 762,559 67,961

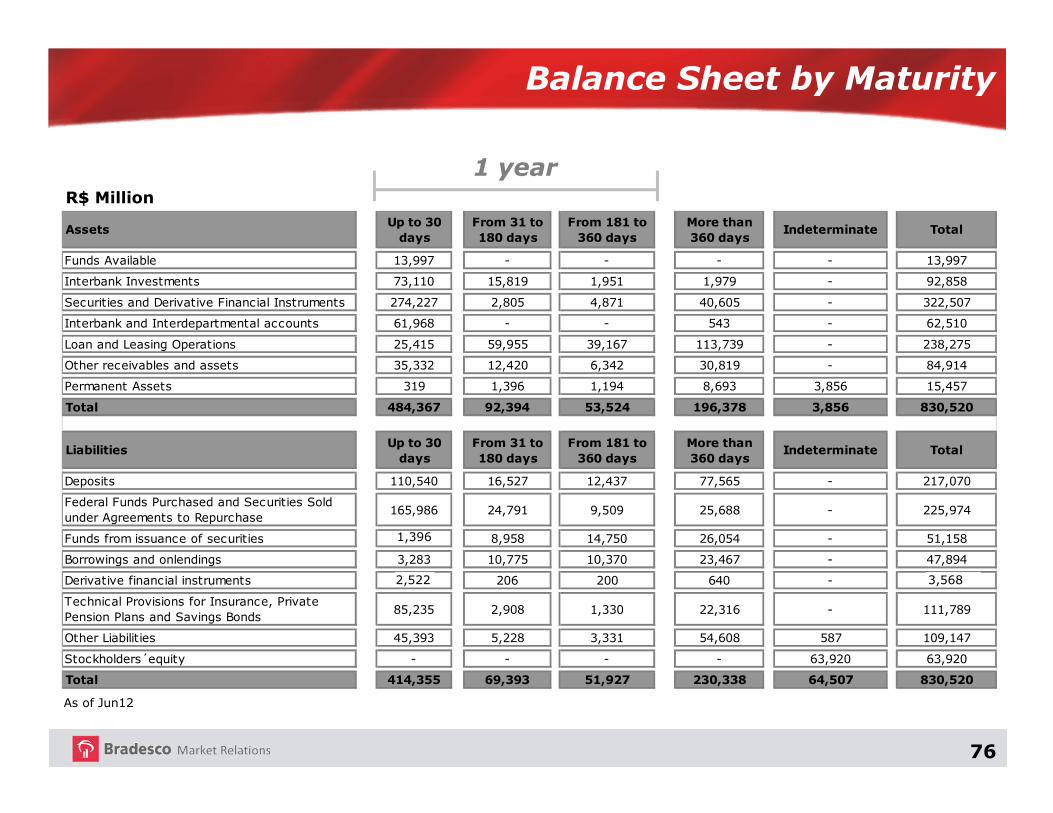

76

Balance Sheet by Maturity

R$ Million

As of Jun12

AssetsUp to 30

days

From 31 to

180 days

From 181 to

360 days

More than

360 daysIndeterminate Total

Funds Available 13,997 - - - - 13,997

Interbank Investments 73,110 15,819 1,951 1,979 - 92,858

Securities and Derivative Financial Instruments 274,227 2,805 4,871 40,605 - 322,507

Interbank and Interdepartmental accounts 61,968 - - 543 - 62,510

Loan and Leasing Operations 25,415 59,955 39,167 113,739 - 238,275

Other receivables and assets 35,332 12,420 6,342 30,819 - 84,914

Permanent Assets 319 1,396 1,194 8,693 3,856 15,457

Total 484,367 92,394 53,524 196,378 3,856 830,520

LiabilitiesUp to 30

days

From 31 to

180 days

From 181 to

360 days

More than

360 daysIndeterminate Total

Deposits 110,540 16,527 12,437 77,565 - 217,070

Federal Funds Purchased and Securities Sold under Agreements to Repurchase

165,986 24,791 9,509 25,688 - 225,974

Funds from issuance of securities 1396 8,958 14,750 26,054 - 51,158

Borrowings and onlendings 3,283 10,775 10,370 23,467 - 47,894

Derivative financial instruments 2522 206 200 640 - 3568

Technical Provisions for Insurance, PrivatePension Plans and Savings Bonds

85,235 2,908 1,330 22,316 - 111,789

Other Liabilities 45,393 5,228 3,331 54,608 587 109,147

Stockholders´equity - - - - 63,920 63,920

Total 414,355 69,393 51,927 230,338 64,507 830,520

1 year

1,396

2,522 3,568

77

Main Funding

R$ Billion

(*) Considers only debentures used to back purchase and sale commitments.

26.8 27.6 28.6 25.9 28.4 30.3 35.7 32.6 33.8 34.9 37.3 32.9 33.0 31.9 33.1 32.0 32.5

34.2 35.7 37.8 37.4 38.5 40.944.2 45.2 47.3 50.1 53.4 54.6 54.8 56.6 59.7 60.0 62.3

61.375.5

97.4 105.4 100.1 96.090.5 92.6 96.8

100.7102.2 116.0 125.4

135.8 124.1 121.5 121.8

16.7

17.7

19.7 20.3 20.4 22.9 23.1 23.523.4

25.726.3

24.424.6

26.2 26.9 30.1 34.1

34.0

35.0

34.6 31.7 28.5 34.0 36.9 40.840.9

43.246.0

48.447.1

47.5 49.8 55.4 55.7

24.7

32.0

32.0 30.429.1 27.0

27.330.2

35.038.0

38.2

41.545.2

49.0 53.2 47.1 47.9

5.4

6.5

9.0 9.37.7 7.1

7.58.5

12.713.7

17.7

21.7

29.1

32.941.5 48.5

51.2

203.1

230.0

259.1 260.4252.7 258.2 265.2

273.4289.9

306.3321.1

339.5

359.2

379.9388.4 394.6

405.5

Jun08 Sep Dec Mar09 Jun Sep Dec Mar10 Jun Sep Dec Mar11 Jun Sep Dec Mar12 Jun

Demand Deposits Saving Deposits

Time Deposits Debentures (*)

Borrowing and Onlending Funds from Issuance of Securities

Subordinated Debts Total

78

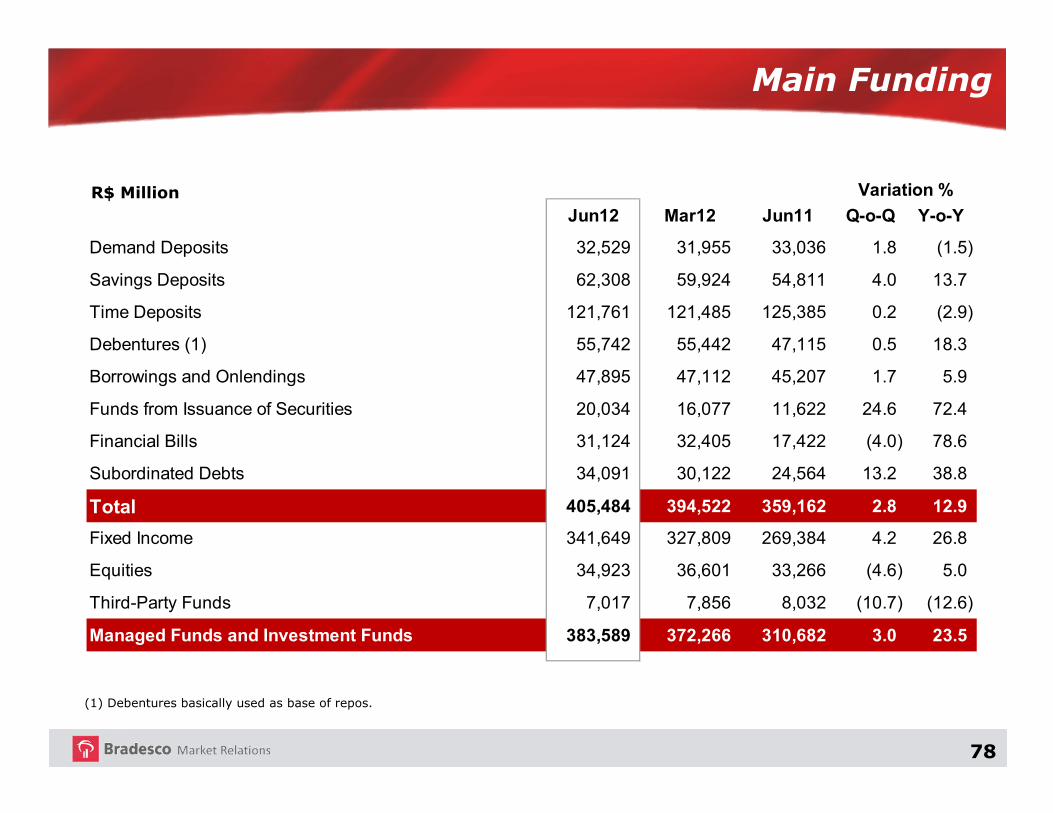

Main Funding

(1) Debentures basically used as base of repos.

R$ Million

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Demand Deposits 32,529 31,955 33,036 1.8 (1.5)

Savings Deposits 62,308 59,924 54,811 4.0 13.7

Time Deposits 121,761 121,485 125,385 0.2 (2.9)

Debentures (1) 55,742 55,442 47,115 0.5 18.3

Borrowings and Onlendings 47,895 47,112 45,207 1.7 5.9

Funds from Issuance of Securities 20,034 16,077 11,622 24.6 72.4

Financial Bills 31,124 32,405 17,422 (4.0) 78.6

Subordinated Debts 34,091 30,122 24,564 13.2 38.8

Total 405,484 394,522 359,162 2.8 12.9

Fixed Income 341,649 327,809 269,384 4.2 26.8

Equities 34,923 36,601 33,266 (4.6) 5.0

Third-Party Funds 7,017 7,856 8,032 (10.7) (12.6)

Managed Funds and Investment Funds 383,589 372,266 310,682 3.0 23.5

Variation %

79

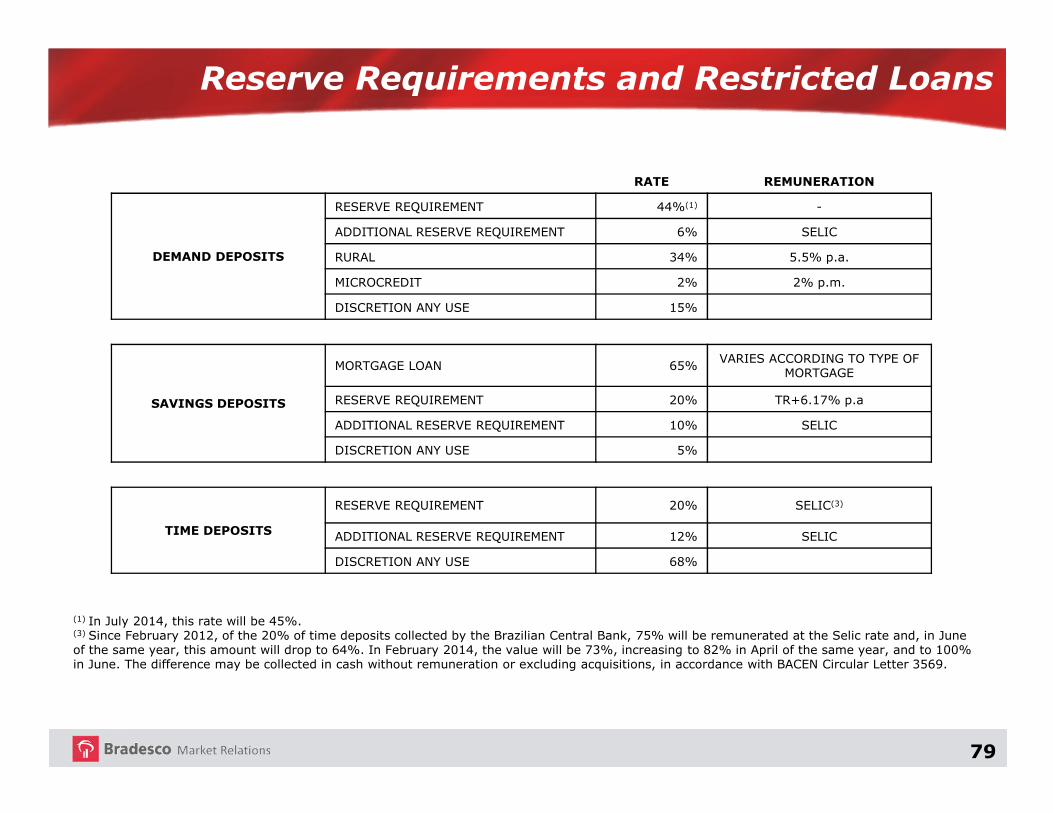

Reserve Requirements and Restricted Loans

RATE REMUNERATION

DEMAND DEPOSITS

RESERVE REQUIREMENT 44%(1) -

ADDITIONAL RESERVE REQUIREMENT 6% SELIC

RURAL 34% 5.5% p.a.

MICROCREDIT 2% 2% p.m.

DISCRETION ANY USE 15%

SAVINGS DEPOSITS

MORTGAGE LOAN 65% VARIES ACCORDING TO TYPE OF MORTGAGE

RESERVE REQUIREMENT 20% TR+6.17% p.a

ADDITIONAL RESERVE REQUIREMENT 10% SELIC

DISCRETION ANY USE 5%

TIME DEPOSITS

RESERVE REQUIREMENT 20% SELIC(3)

ADDITIONAL RESERVE REQUIREMENT 12% SELIC

DISCRETION ANY USE 68%

(1) In July 2014, this rate will be 45%. (3) Since February 2012, of the 20% of time deposits collected by the Brazilian Central Bank, 75% will be remunerated at the Selic rate and, in June of the same year, this amount will drop to 64%. In February 2014, the value will be 73%, increasing to 82% in April of the same year, and to 100% in June. The difference may be collected in cash without remuneration or excluding acquisitions, in accordance with BACEN Circular Letter 3569.

80

Loans and Funding

R$ Million

(1) Debentures basically used as base of repos;

(2) Does not include public sector’s securities linked to saving; and

(3) Comprises amounts relative to card operations (cash and installment purchases at merchants), amounts related to interbank deposit certificates (CDI) to abate from the compulsory and debenture amount.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Demand Deposits 32,529 31,955 33,036 1.8 (1.5)

Sundry Floating 4,122 6,948 4,308 (40.7) (4.3)

Savings Deposits 62,308 59,924 54,811 4.0 13.7

Time Deposits + Debentures (1) 177,503 176,927 172,500 0.3 2.9

Financial Bills 31,124 32,405 17,422 (4.0) 78.6

Others 19,799 18,283 15,565 8.3 27.2

Funding from Clients 327,385 326,442 297,642 0.3 10.0

(-)Reserve Requirements / Funds Available (2) (67,210) (79,159) (65,065) (15.1) 3.3

Funding from Clients - Net of Reserve Requirements 260,175 247,283 232,577 5.2 11.9

Mandatory onlendings 32,122 32,490 33,520 (1.1) (4.2)

Foreign Credit Lines 17,018 11,423 15,851 49.0 7.4

Funding Overseas 51,411 42,648 34,738 20.5 48.0

Total Funding (A) 360,726 333,844 316,686 8.1 13.9

322,962 308,251 277,371 4.8 16.4

B / A (%) 89.5 92.3 87.6 (2.8) p.p. 1.9 p.p.x

Loan Portfolio / Leasing / Cards (Other Credits) / Acquired Interbank Deposit Certificate (B) (3)

Variation %

81

Expanded Loan Portfolio (1)

R$ Billion

(1) Includes sureties, guarantees, letters of credit, and advances of credit card receivables, debentures, and promissory notes, assignment ofreceivables-backed investment funds and mortgage-backed receivables and ruracredit. Further information can be found on page 38 of the Reportof Economic and Financial Analysis.

33% 34% 34% 35% 34% 33% 33% 32% 32% 31% 31% 31%

40% 38% 38% 37% 37%38% 38% 39% 39% 38% 38%

39%27%

28%28%

28%29%

29%29%

29%29%

31% 31%30%

227.6238.8

249.8259.7

272.5

295.2306.1

319.8332.3

345.7 350.8365.0

Sep09 Dec Mar10 Jun Sep Dec Mar11 Jun Sep Dec Mar12 Jun

SMEs Large Corporates Individuals

82

R$ Million

Expanded Loan Portfolio

(1) Includes sureties and guarantees, letters of credit, anticipation of credit card receivables, debentures, promissory notes, creditassignment with recourse (FIDC - Receivables Securitization Fund and CRI - Real Estate Receivables Certificate), and rural credit.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y LARGE CORPORATES 143,830 134,451 124,057 7.0 15.9

SMEs 108,898 106,730 92,830 2.0 17.3

INDIVIDUALS 112,235 109,651 102,915 2.4 9.1

Expanded Loan Portfolio - Total (1) 364,963 350,831 319,802 4.0 14.1

Variation %

83

Loan Portfolio Breakdown

Jun12Individuals Corporate

Working Capital17%

Export Financing5%

BNDES Onlendings /

Finame12%

Operations Abroad

9%Overdraft Accounts

4%

Leasing3%

Credit Card6%

Rural2%

Vehicles - CDC2%

Mortgage (4)4%

Sureties and Guarantees (5)

21%

Commercial Portfolio(6)

11%

Others(7)4%

Vehicles - CDC26%

Leasing3%

Credit Card17%

Personal Loans13%

Payroll-Deductible Loans (1)

17%

Rural6%

BNDES Onlendings/ Finame

5%

Mortgage (2)8%

Overdraft Accounts3%

Sureties and Guarantees

1%

Others (3)3%

R$ 112,235 million R$ 252,728 million

Including:

(1) Loan assignment (FIDC): R$339 million;(2) Loan assignment (CRI): R$182 million;(3) Loan assignment (FIDC) for the acquisition of assets: R$2 million and Rural loan assignment: R$112 million;(4) Loan assignment (CRI): R$239 million;(5) 91.5% of sureties and guarantees from corporate customers were contracted by corporations;(6) Operations with debentures and promissory notes;(7) Letters of credit: R$1,779 million.

84

Loan Portfolio – Individuals

R$ Million

Includes:(1) Credit assignments (FIDC): R$ 339 million in Jun/12, R$ 420 million in Mar/12 and R$ 439 million in Jun/11;(2) Credit assignments (CRI): R$ 182 million in Jun/12, R$ 198 million in Mar/12 and R$ 248 million in Jun/11; and(3) Credit assignments (FIDC), for the acquisition of assets: R$ 2 million in Jun/12, R$ 2 million in mar/12 and R$ 3 million in Jun/11; and rural credit assignments :R$ 112 million in Jun/12, R$ 112 million in Mar/12 and R$ 121 million in Jun/11.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Vehicles - CDC 29,324 29,075 26,804 0.9 9.4

Payroll-Deductible Loans (1) 19,243 18,398 16,886 4.6 14.0

Credit Cards 18,545 17,903 17,141 3.6 8.2

Personal Loans 14,465 13,771 12,658 5.0 14.3

Mortgage (2) 8,768 7,994 5,521 9.7 58.8

Rural 6,367 6,599 6,009 (3.5) 6.0

BNDES/Finame Onlendings 5,515 5,494 4,930 0.4 11.9

Overdraft Accounts 3,204 3,217 3,013 (0.4) 6.4

Leasing 2,871 3,510 5,946 (18.2) (51.7)

Sureties and Guarantees 650 598 641 8.6 1.4

Others (3) 3,282 3,091 3,366 6.2 (2.5)

Total 112,235 109,651 102,915 2.4 9.1

Variation %

85

Consumer Financing

R$ Million

(1) Includes: Credit assignments (FIDC): R$ 339 million in Jun/12, R$ 420 million in Mar/12 and R$ 439 million in Jun/11.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

CDC/ Leasing - Vehicles 32,195 32,585 32,750 (1.2) (1.7)

Credit Cards 18,545 17,903 17,141 3.6 8.2

Payroll-Deductible Loans (1) 19,243 18,398 16,886 4.6 14.0

Personal Loans 14,465 13,771 12,658 5.0 14.3

Financing of Goods 392 388 562 1.0 (30.2)

Total 84,841 83,045 79,997 2.2 6.1

Variation %

86

Loan Portfolio - Corporate

R$ Million

(1) Including loan assignments (CRI) of R$ 239 million in Jun/12, R$ 280 million in Mar/12 and R$ 304 million in Jun11;

(2) 91.5 % of Surety and Guarantee Corporate transactions are carried out with Large Corporations;

(3) Includes operations with Debentures and Promissory Notes; and

(4) Letters of Credit: R$ 1,779 million in Jun/12, R$ 1,556 million in Mar/12 and R$ 1,630 million in Jun/11.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Working Capital 42,533 41,551 37,863 2.4 12.3

BNDES/Finame Onlendings 29,474 29,812 28,359 (1.1) 3.9

Operations Abroad 23,615 21,670 19,650 9.0 20.2

Credit Cards 14,385 13,916 12,069 3.4 19.2

Export Financing 12,408 10,479 9,367 18.4 32.5

Mortgages - Corporate Plans (1) 11,047 10,068 7,687 9.7 43.7

Overdraft Accounts 10,437 10,631 10,073 (1.8) 3.6

Leasing 6,722 7,008 7,773 (4.1) (13.5)

Vehicles - CDC 6,245 5,965 4,568 4.7 36.7

Rural 4,539 4,358 4,738 4.1 (4.2)

Sureties and Guarantees (2) 52,226 50,334 42,802 3.8 22.0

Operations Credit Risk - Commercial Portfolio (3) 28,043 25,403 21,473 10.4 30.6

Others (4) 11,054 9,983 10,465 10.7 5.6

Total 252,728 241,181 216,887 4.8 16.5

Variation %

87

Credit Quality and Concentration

AA-C: 91.5%

Loan Portfolio BreakdownBy Rating

Concentration ofLoan Operations - % (1)

AA18.5%

A40.5%

B14.5%

C18.0%

D2.5%

E-H5.9%

0.9

5.0

8.2

13.1

17.1

LargestBorrower

10 Larg.Borrow.

20 Larg.Borrow.

50 Larg.Borrow.

100 Larg.Borrow.

Jun12

(1) Concept defined by the Brazilian Central Bank.

88

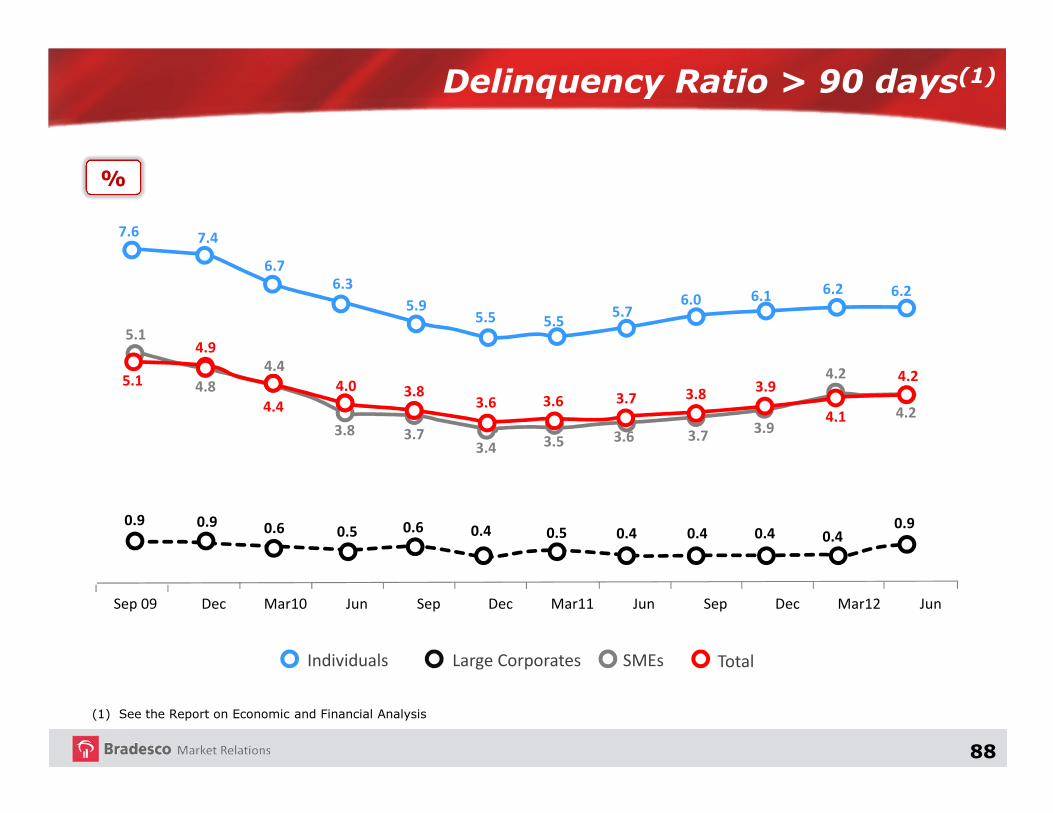

Delinquency Ratio > 90 days(1)

%

7.6 7.4

6.76.3

5.95.5 5.5

5.76.0 6.1 6.2 6.2

5.1

4.8

4.4

3.8 3.73.4 3.5 3.6 3.7

3.9

4.2

4.2

5.1

4.9

4.4

4.0 3.83.6 3.6 3.7 3.8

3.9

4.1

4.2

0.9 0.9 0.6 0.5 0.6 0.4 0.5 0.4 0.4 0.4 0.40.9

(1) See the Report on Economic and Financial Analysis

Large Corporates TotalIndividuals SMEs

Sep 09 Dec Mar10 Jun Sep Dec Mar11 Jun Sep Dec Mar12 Jun

89

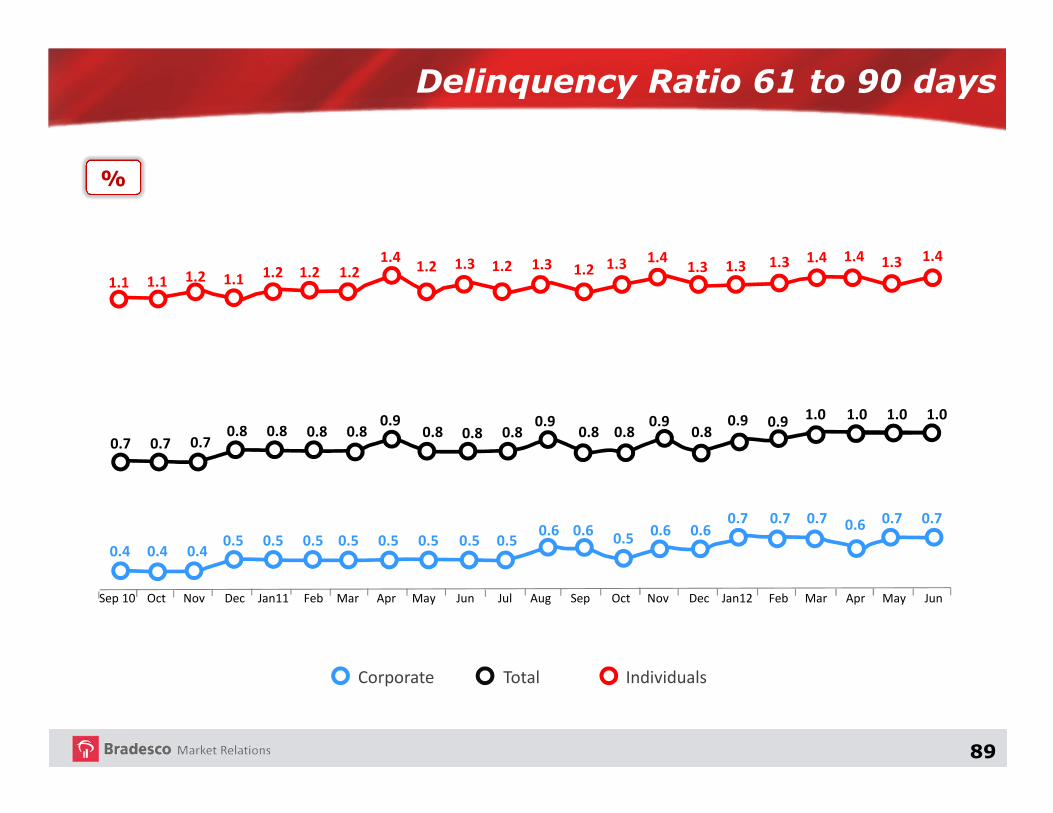

Delinquency Ratio 61 to 90 days

%

1.1 1.1 1.2 1.1 1.2 1.2 1.21.4

1.2 1.3 1.2 1.3 1.2 1.3 1.41.3 1.3 1.3 1.4 1.4 1.3 1.4

0.70.8

0.9 0.9 0.9 0.9 0.9 1.0 1.0 1.0 1.0

0.7 0.70.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8 0.8

0.40.5

0.60.5

0.7 0.6

0.4 0.40.5 0.5 0.5 0.5 0.5 0.5 0.5

0.6 0.6 0.60.7 0.7 0.7 0.7

Total IndividualsCorporate

Sep 10 Oct Nov Dec Jan11 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan12 Feb Mar Apr May Jun

90

Renegotiated Portfolio

R$ Billion

Sep10 Mar11 Jun Sep Dec Mar12 JunDec

Deliquency ratio over 90 daysAllowance for Loan Losses as a % of the Renegotiated PortfolioRenegotiated Portfolio (R$ Billion)

6.7

62.9

25.724.6 26.0

24.4 24.727.6

29.2 29.4

62.8 63.0 62.2 62.363.8 64.1 63.6

6.97.3 7.8 8.3 8.7 8.9 9.1

91

Loan Portfolio(1)

(1) According to Brazilian Central Bank criteria.

Loan Portfolio excluding RenegotiationDeliquency ratio over 90 daysLoan Potfolio (1)Deliquency ratio over 90 days

excluding Renegotiation

R$ Billion

Sep10 Mar11 Jun Sep Dec Mar12 JunDec

217

231240

251261

269 270279

211

224233

243252

260 261270

3.8% 3.6% 3.6% 3.7% 3.8% 3.9% 4.1% 4.2%

3.2% 2.9% 2.9% 3.0% 3.1% 3.2% 3.3% 3.3%

92

Allowance for Loan Losses/ PLL / Write-off

R$ Million

2Q12 1Q12 1H12 1H11 Q-o-Q Y-o-Y

OPENING BALANCE 20,117 19,540 19,540 16,290 3.0 20.0

RECORDED 3,651 3,298 6,949 5,219 10.7 33.1

WRITTEN-OFF (3,086) (2,721) (5,807) (4,144) 13.4 40.1

CLOSING BALANCE 20,682 20,117 20,682 17,365 2.8 19.1

SPECIFIC PROVISION 10,809 10,576 10,809 8,669 2.2 24.7

GENERIC PROVISION 5,863 5,530 5,863 5,692 6.0 3.0

EXCESS PROVISION 4,010 4,012 4,010 3,003 - 33.5

CREDIT RECOVERY 785 653 1,438 1,318 20.2 9.1

Variation %

93

Provisioning Ratios(1)

%

(1) See the Report on Economic and Financial Analysis.

12 – Month Write-Offs (Gross)

E-H Past Dues/Loan Portfolio

12 – Month Write-Offs (Net)

Minimun Required Allowance for Loan LosssesAllowance for Loan Losses

R$ 4.0 bn

R$ 7.8 bn

R$ 11.2 bn

8.38.5

8.0

7.6 7.47.1 7.0 6.9

7.3 7.37.5 7.4

6.6

5.5

5.2

3.8

7.0

6.5

6.1 6.05.8 5.7 5.7 5.8

6.0 6.0

5.5

4.9

4.54.3

4.1 4.1 4.2

4.2

4.44.7 4.7

4.7

4.33.9 3.8 3.8

3.94.2 4.4 4.5 4.6

3.32.9 2.6 2.6 2.6

2.8 3.0 3.1 3.2 3.3 3.4

Sep09 Dec Mar10 Jun Sep Dec Mar11 Jun Sep Dec Mar12 Jun

5.8

4.3

94

Allowance for Loan Losses, Overdue Credits and Coverage Ratio

R$ Million

16,019 16,290 16,740 17,365

19,091 19,540 20,117 20,682

9,886 9,973 10,520

11,272 11,963

12,870 13,718

14,365

8,351 8,243 8,648 9,172 9,839

10,598 11,070 11,662

191.8% 197.6% 193.6% 189.3% 194.0%184.4%

181.7% 177.4%162.0% 163.3% 159.1% 154.0%

159.6%151.8% 146.6% 144.0%

Sep10 Dec Mar11 Jun Sep Dec Mar12 Jun

Allowance for Loan Losses (1)

Loan Portfolio Overdue > 60 days (2)

Loan Portfolio Overdue > 90 days (3)

Coverage Ratio > 90 days (1/3)

Coverage Ratio > 60 days (1/2)

95

High Growth Products

Payroll Deductible Loans

Vehicles Financing

Real Estate Lending and Mortgage

Cards

Insurance and Pension Plans

Capital Markets

96

Projected Share of GDP

Source: Brazilian Central BankPrepared by / (*) Projections: Bradesco - DEPEC

%

1.40 1.50 1.702.10

2.90

3.80

4.68

5.57

6.53

7.44

8.35

8.99

9.649.99

10.33 10.47

2005 2006 2007 2008 2009 2010 2011* 2012* 2013* 2014* 2015* 2016* 2017* 2018* 2019* 2020*

97

Share Of GDP

88.9

74.7

59.2

53.6

39.436.0

30.524.0

17.0 16.5

10.08.2 7.0 6.0

4.1 1.7 1.10

10

20

30

40

50

60

70

80

90

100

New

Zealand

United King

dom

USA

Portug

al

Spain

Australia

Canada

Germany

France

Japan

Hon

g Ko

ng

Korea

Thailand

Italy

Chile

Hun

gary

China

Poland

Mexico

Czech Repub

lic

Bulgaria

India

Turkey

Brazil

Colombia

Argentin

a

Russia

As of: Brazil - Jan/11; Colombia – Dec/07; Bulgaria, Czech Republic, Poland, Japan – Dec/06; Others Countries – Mar/08;

%

98

Housing Deficit (Brazil)

7.9 Million Homes

ABOVE 10MINIMUM WAGES;

1.6

BETWEEN 5 AND 10 MINIMUM WAGES;

6.9

BELOW 5 MINIMUM WAGES;

91.5

%

99

Annual Production

Market

9,340

18,283

30,032 34,017

56,198

2006 2007 2008 2009 2010

79,917

2011

29,226 29,628

1H11 1H12

R$ Million

100

Bradesco’s Annual Origination

R$ Million # homes

4,043

5,993

4,707

9,128

14,907

2007 2008 2009 2010 2011

33,673

49,252

34,627

64,449

76,346

2007 2008 2009 2010 2011

7,207 7,212

1H11 1H12

39,195 41,268

1H11 1H12

101

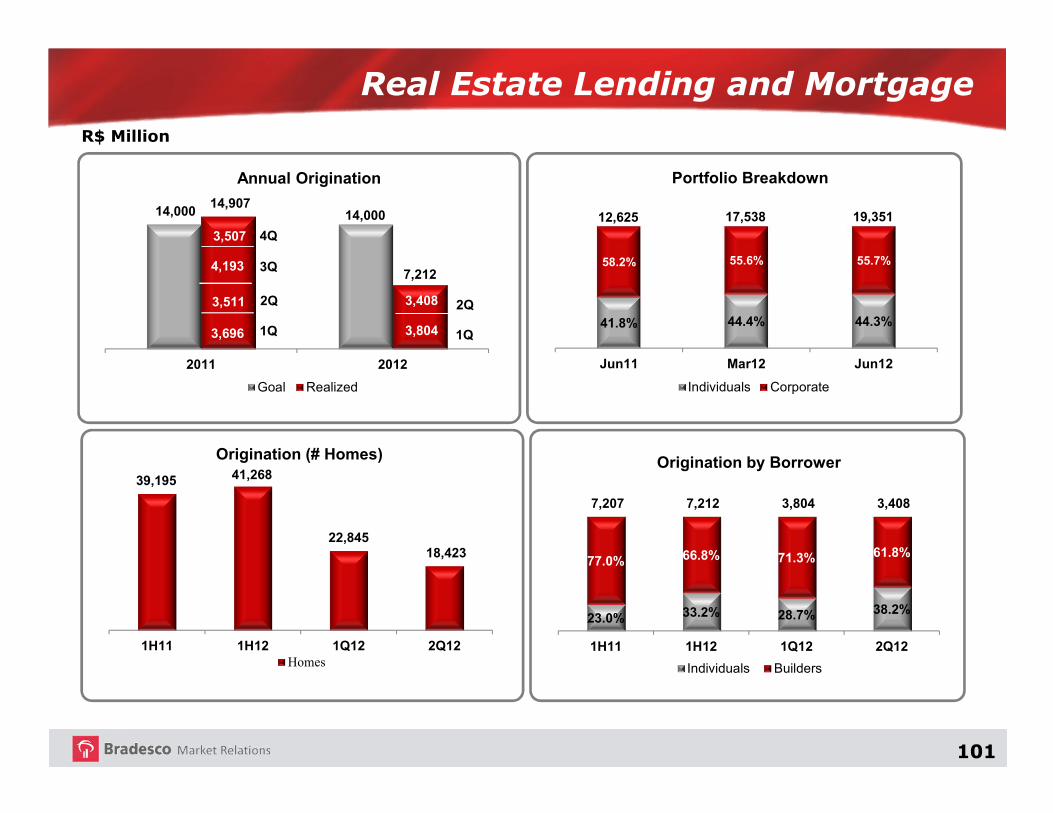

Real Estate Lending and Mortgage

R$ Million

14,000 14,000 14,907

7,212

2011 2012

Annual Origination

Goal Realized

1Q

2Q

3Q

4Q

1Q

2Q41.8% 44.4% 44.3%

58.2% 55.6% 55.7%

12,625 17,538 19,351

Jun11 Mar12 Jun12

Portfolio Breakdown

Individuals Corporate

39,195 41,268

22,84518,423

1H11 1H12 1Q12 2Q12

Origination (# Homes)

Homes

23.0% 33.2% 28.7% 38.2%

77.0% 66.8% 71.3% 61.8%

7,207 7,212 3,804 3,408

1H11 1H12 1Q12 2Q12

Origination by Borrower

Individuals Builders

3,696

3,511

4,193

3,507

3,804

3,408

102

Delinquency

Secured Fiduciary SalePre-Fixed and Post-Fixed Agreements at Bradesco

Amount % Amount % Amount %

On time 51,385 87.7% 5,298 78.4% 46,087 88.9%

1 to 3 6,042 10.3% 1,136 16.8% 4,906 9.5%

4 to 6 575 1.0% 106 1.6% 469 0.9%

7 to 12 295 0.5% 78 1.2% 217 0.4%

Over 12 325 0.6% 136 2.0% 189 0.4%

Total overdue 7,237 12.3% 1,456 21.6% 5,781 11.1%

Overall Total 58,622 6,754 51,868

1,195 2.0% 320 4.7% 875 1.7%

Total Pre PostInstallments

As of Jun12

Over 3

103

Payroll Deductible Loans

Vehicles Financing

Real Estate Lending and Mortgage

Cards

Insurance and Pension Plans

Capital Markets

High Growth Products

104

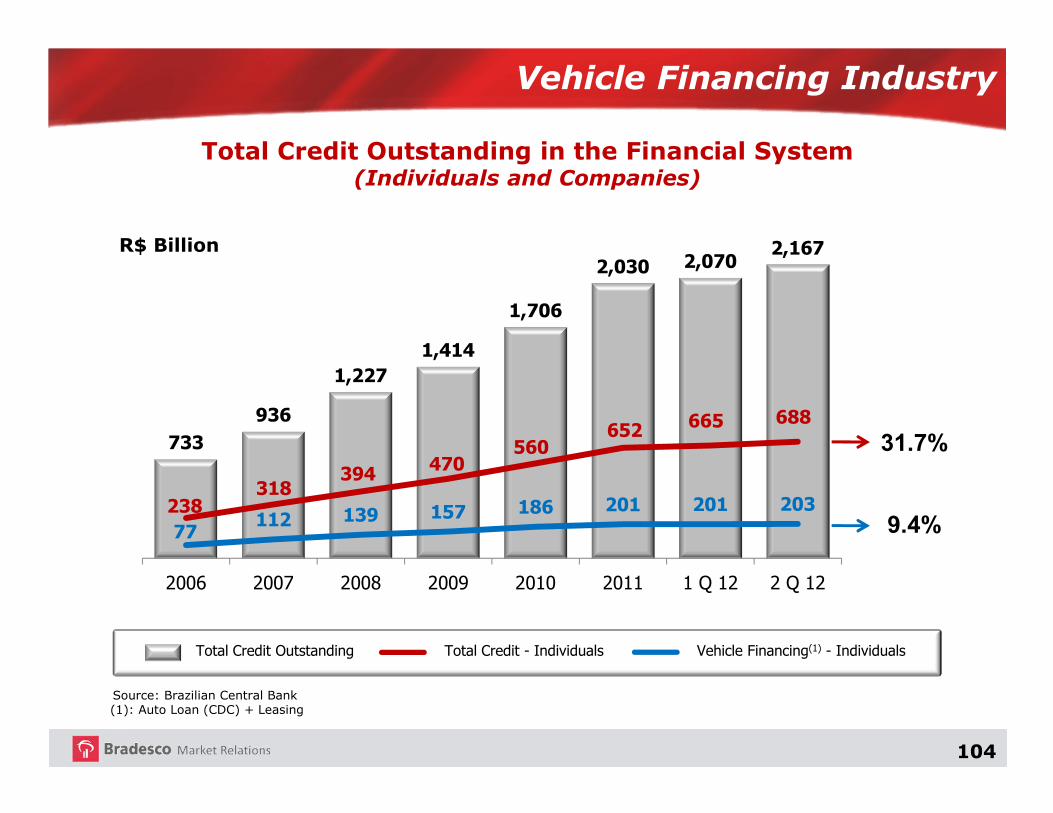

Vehicle Financing Industry

Total Credit Outstanding in the Financial System(Individuals and Companies)

Source: Brazilian Central Bank(1): Auto Loan (CDC) + Leasing

Total Credit Outstanding Vehicle Financing(1) - IndividualsTotal Credit - Individuals

31.7%

9.4%

R$ Billion

733

936

1,227

1,414

1,706

2,030 2,0702,167

238318

394470

560652

665 688

77112 139 157 186 201 201 203

2006 2007 2008 2009 2010 2011 1 Q 12 2 Q 12

105

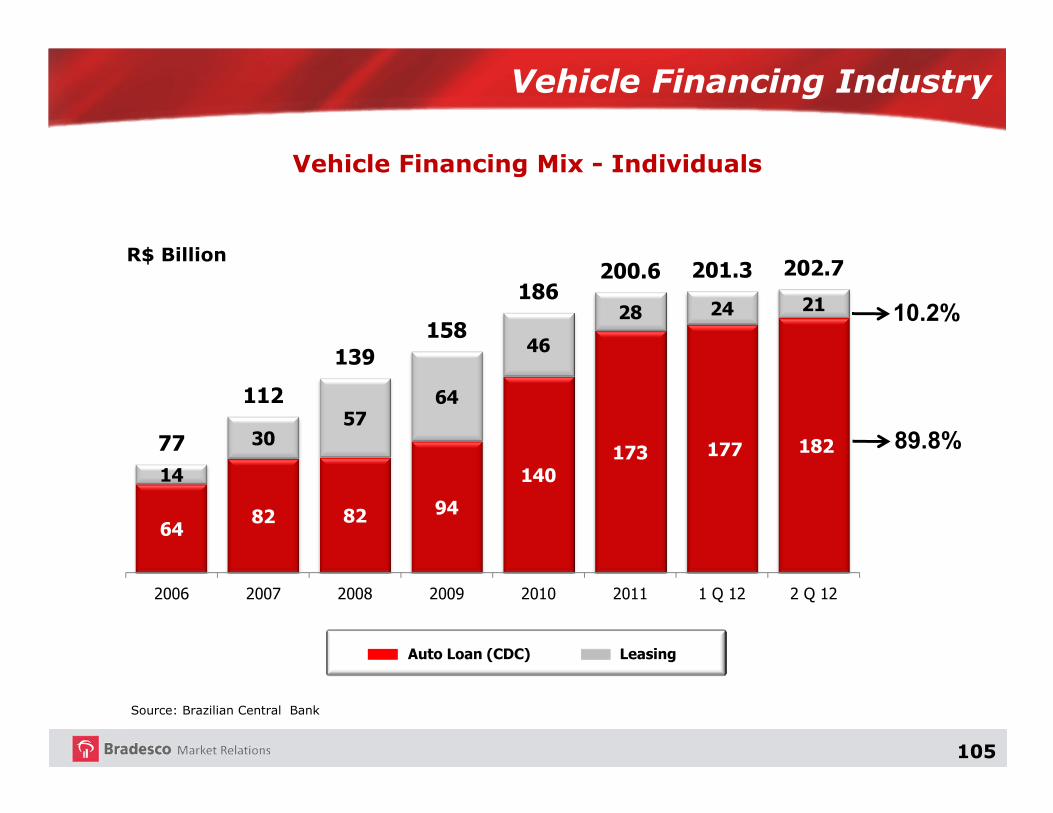

Vehicle Financing Mix - Individuals

Auto Loan (CDC) Leasing

Vehicle Financing Industry

Source: Brazilian Central Bank

R$ Billion

10.2%

89.8%

6482 82 94

140173 177 182

14

3057

64

46

28 24 21

77

112

139

158

186200.6 201.3 202.7

2006 2007 2008 2009 2010 2011 1 Q 12 2 Q 12

106

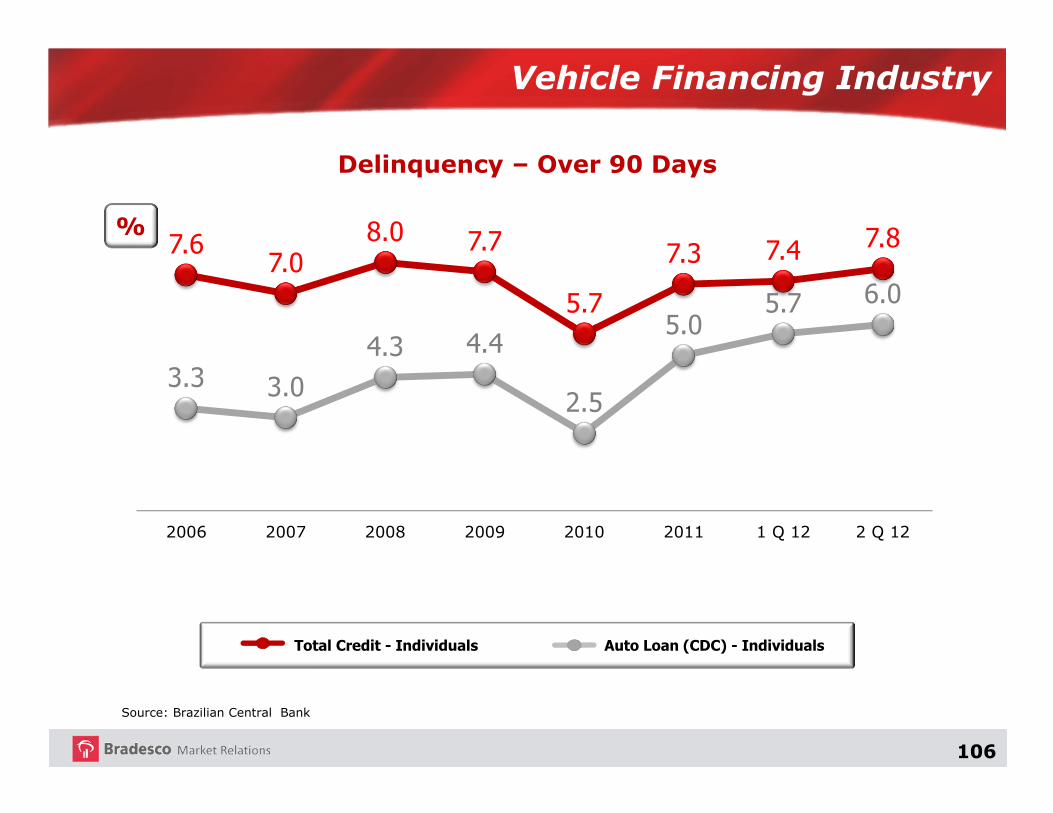

Vehicle Financing Industry

Delinquency – Over 90 Days

Source: Brazilian Central Bank

%

Auto Loan (CDC) - IndividualsTotal Credit - Individuals

3.3 3.0

4.3 4.4

2.5

5.05.7 6.0

7.67.0

8.0 7.7

5.7

7.3 7.4 7.8

2006 2007 2008 2009 2010 2011 1 Q 12 2 Q 12

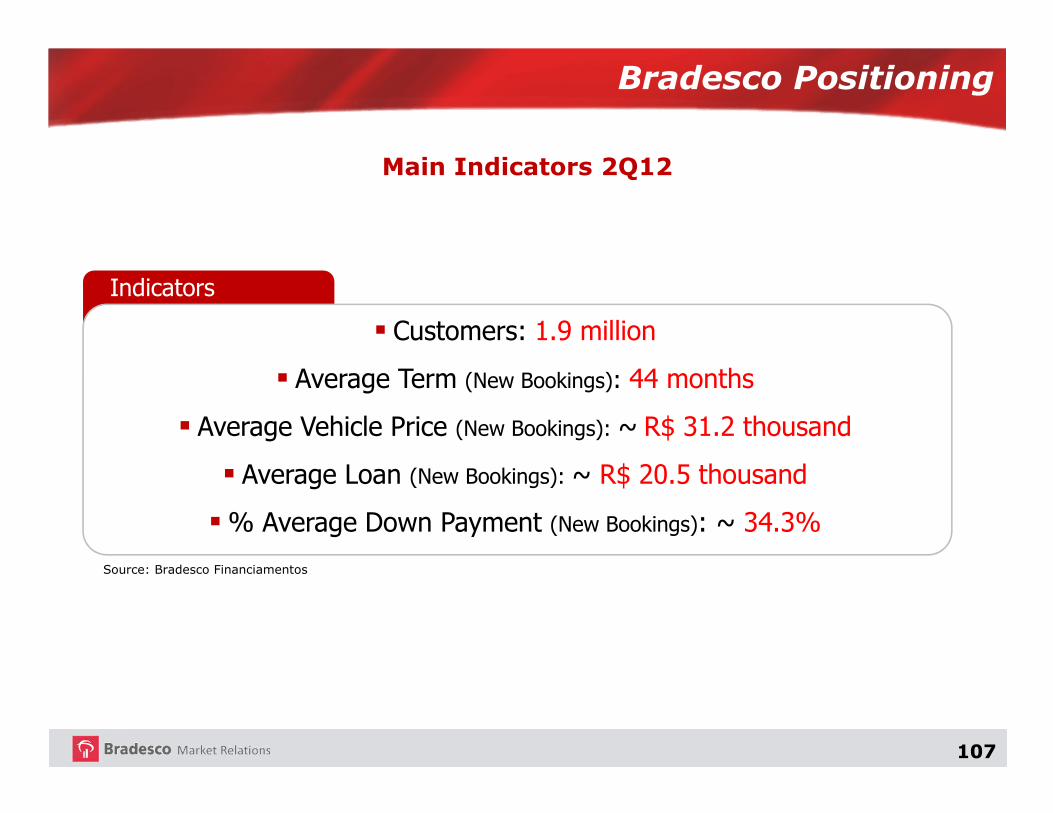

107

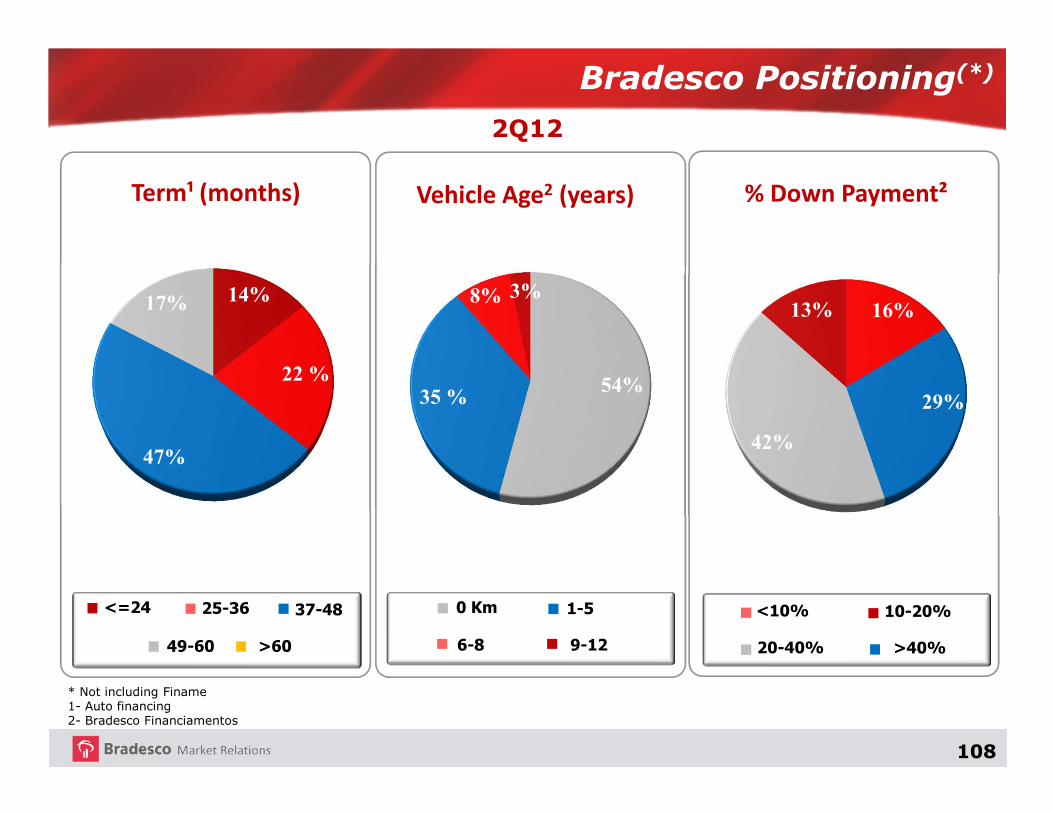

Main Indicators 2Q12

Indicators

� Customers: 1.9 million

� Average Term (New Bookings): 44 months

� Average Vehicle Price (New Bookings): ~ R$ 31.2 thousand

� Average Loan (New Bookings): ~ R$ 20.5 thousand

�% Average Down Payment (New Bookings): ~ 34.3%

Bradesco Positioning

Source: Bradesco Financiamentos

108

2Q12

<=24 37-4825-36

49-60 >60

Term¹ (months) Vehicle Age2 (years)

0 Km

6-8

1-5

9-12

<10%

20-40%

10-20%

>40%

% Down Payment²

* Not including Finame1- Auto financing2- Bradesco Financiamentos

Bradesco Positioning(*)

14%

22 %

17%

47%

54%35 %

8% 3%16%

29%

42%

13%

109

Positioning

Bradesco Portfolio (Individuals + Companies)

(R$ billion)

Individuals(R$ billion)

Vehicle Market Share – Bradesco & Bradesco Financiamentos (Auto Loan - CDC and Leasing)(1)

Source : Bacen/Bradesco/Cetip

Ranking by Segment(2)

� 1st Transportation/Agrobusiness

� 1st Motorcycle

� 3th Automobile

(1) Individuals (2) Accumulated until Jun’12(3) Not including renegociation

Bradesco & Brad. Financ.

MarketBradesco & Brad. Financ

Share~16%

(3)

(3)41.9

2Q12 2Q12

202.7

(3)

32.6

170.5

110

Outlook

Motorcycle(Licensed units)

2009

1.6 Million

Source: FENABRAVE

2010

1.8 Million

2011

1.94 Million

2012

1.88 Million

Decrease of -3.2%

Automobile(Licensed units)

2009

3.1 Million

2010

3.3 Million

2011

3.4 Million

2012

3.4 Million

Decrease of -0.4%

Transportation(Licensed Trucks)

2009

110 Thousand

2010

158 Thousand

2011

173 Thousand

2012

161 Thousand

Decrease of -6.9%

Forecast

111

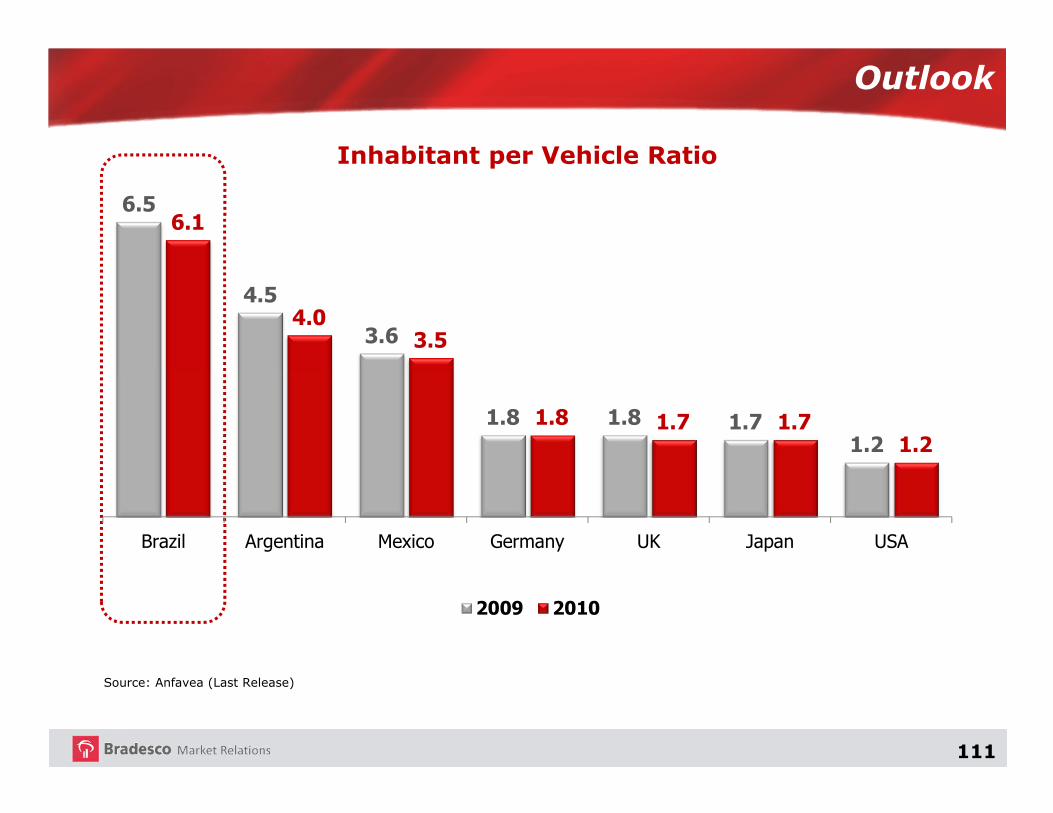

Inhabitant per Vehicle Ratio

Source: Anfavea (Last Release)

Outlook

6.5

4.5

3.6

1.8 1.8 1.71.2

6.1

4.03.5

1.8 1.7 1.71.2

Brazil Argentina Mexico Germany UK Japan USA

2009 2010

112

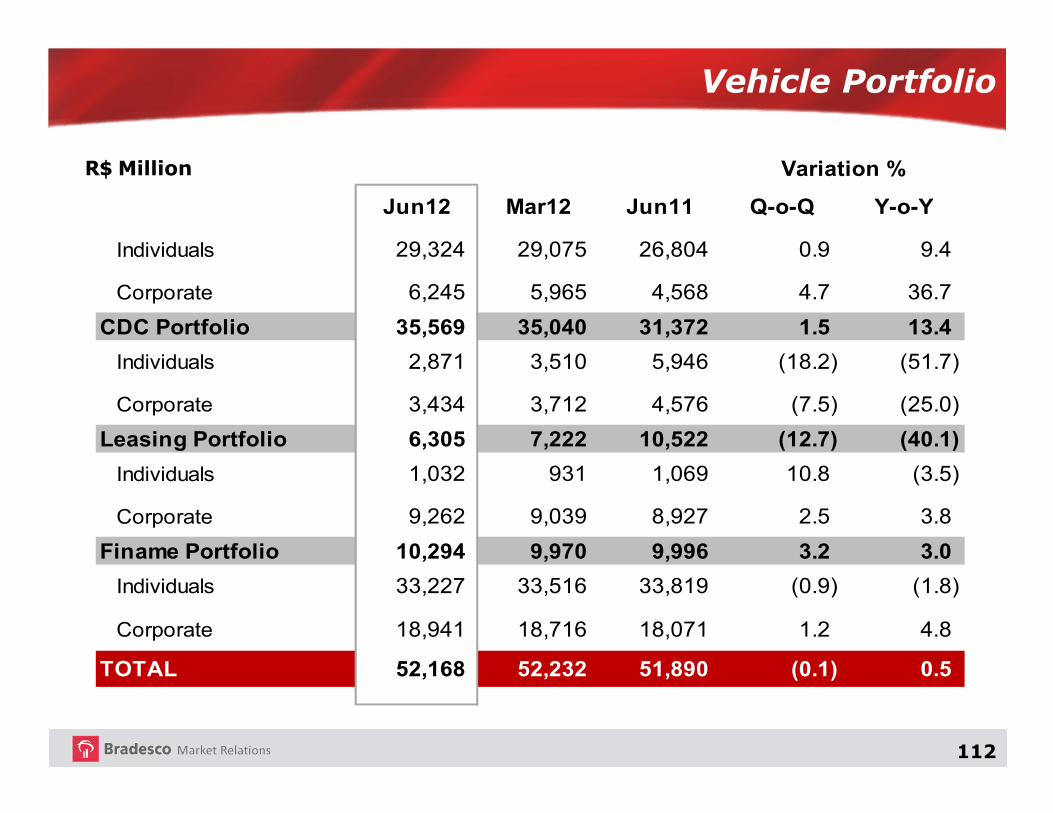

Vehicle Portfolio

R$ Million

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Individuals 29,324 29,075 26,804 0.9 9.4

Corporate 6,245 5,965 4,568 4.7 36.7

CDC Portfolio 35,569 35,040 31,372 1.5 13.4

Individuals 2,871 3,510 5,946 (18.2) (51.7)

Corporate 3,434 3,712 4,576 (7.5) (25.0)

Leasing Portfolio 6,305 7,222 10,522 (12.7) (40.1)

Individuals 1,032 931 1,069 10.8 (3.5)

Corporate 9,262 9,039 8,927 2.5 3.8

Finame Portfolio 10,294 9,970 9,996 3.2 3.0

Individuals 33,227 33,516 33,819 (0.9) (1.8)

Corporate 18,941 18,716 18,071 1.2 4.8

TOTAL 52,168 52,232 51,890 (0.1) 0.5

Variation %

113

Payroll Deductible Loans

Real Estate Lending and Mortgage

Cards

Insurance and Pension Plans

Capital Markets

High Growth Products

Vehicles Financing

114

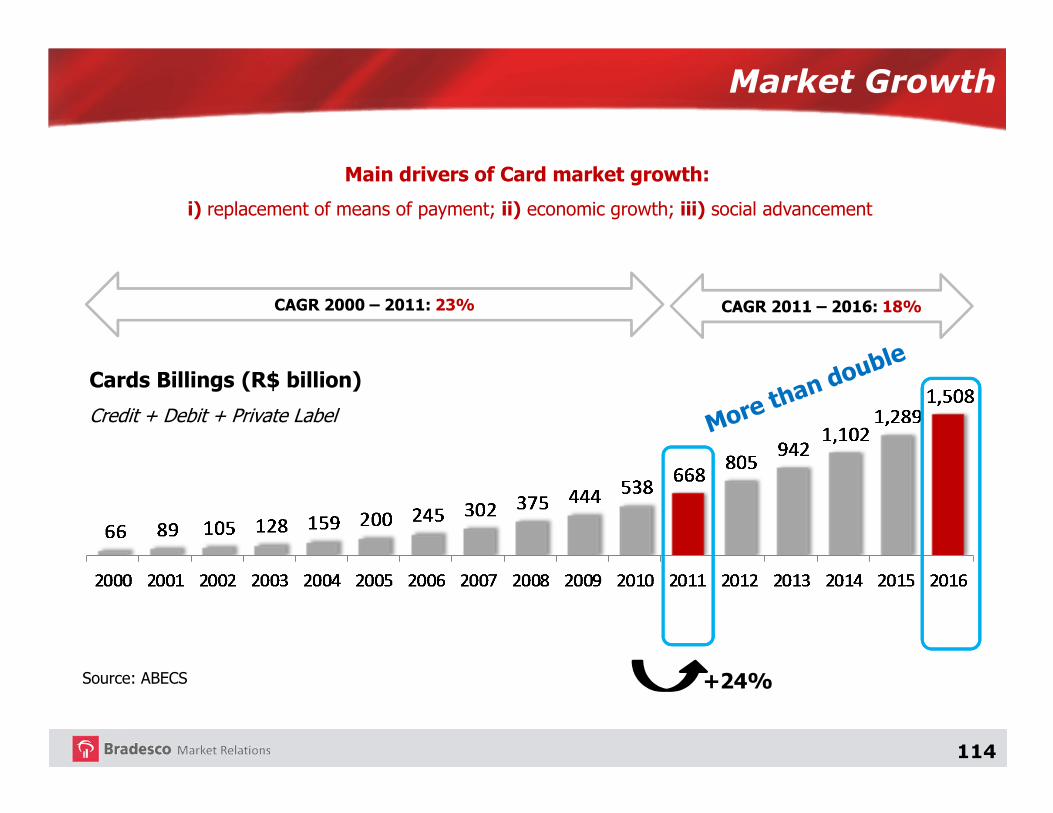

Market Growth

CAGR 2011 – 2016: 18%CAGR 2000 – 2011: 23%

Cards Billings (R$ billion)

Credit + Debit + Private Label

Source: ABECS +24%

Main drivers of Card market growth:

i) replacement of means of payment; ii) economic growth; iii) social advancement

115

1.1 1.4 1.6 1.9

2.53.2

3.74.4

5.3

6.17.1

8.1

2.6 2.6 2.4 2.2

2.1 1.9 1.7 1.5 1.4 1.2 1.1 1.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: ABECS / BACEN

Cards replacing checks

Number of transactions with cards and checks (bn)

Brazilian Payments

Cards Checks

116

France

USA

Source: ABECS / IBGE / BACEN / BIS / The Nilson Report

Compared to other countries, Brazil still has a lot of room for growth. Maintaining current trend, actual level of Canada should be achieved only in 2030

International Comparison

Australia

Canada

South Korea

UK

%

117

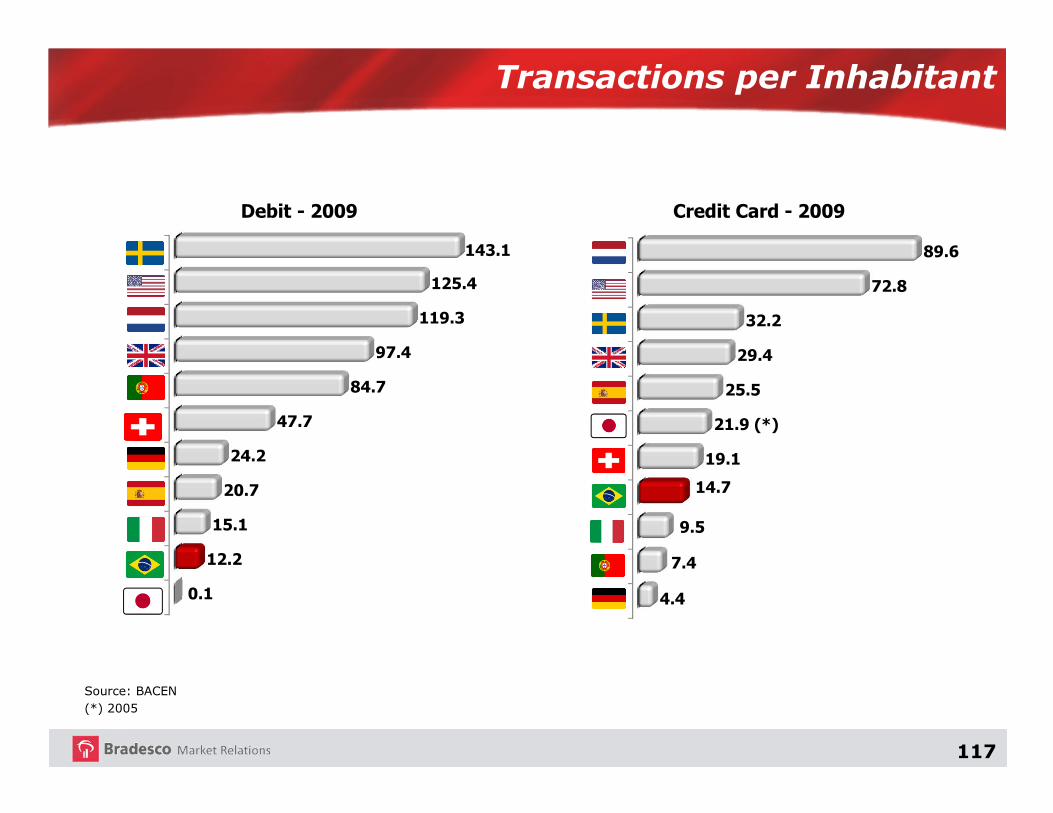

Transactions per Inhabitant

0.1

12.2

15.1

20.7

24.2

47.7

84.7

97.4

119.3

125.4

143.1

Source: BACEN (*) 2005

Credit Card - 2009

4.4

7.4

9.5

14.7

19.1

21.9 (*)

25.5

29.4

32.2

72.8

89.6

Debit - 2009

118

5

6

7

8

9

10

11

Jan-04

Nov-04

Sep-05

Jul-06

May-07

Mar-08

Jan-09

Nov-09

Sep-10

Jul-11

May-12

Consumer finance Cards

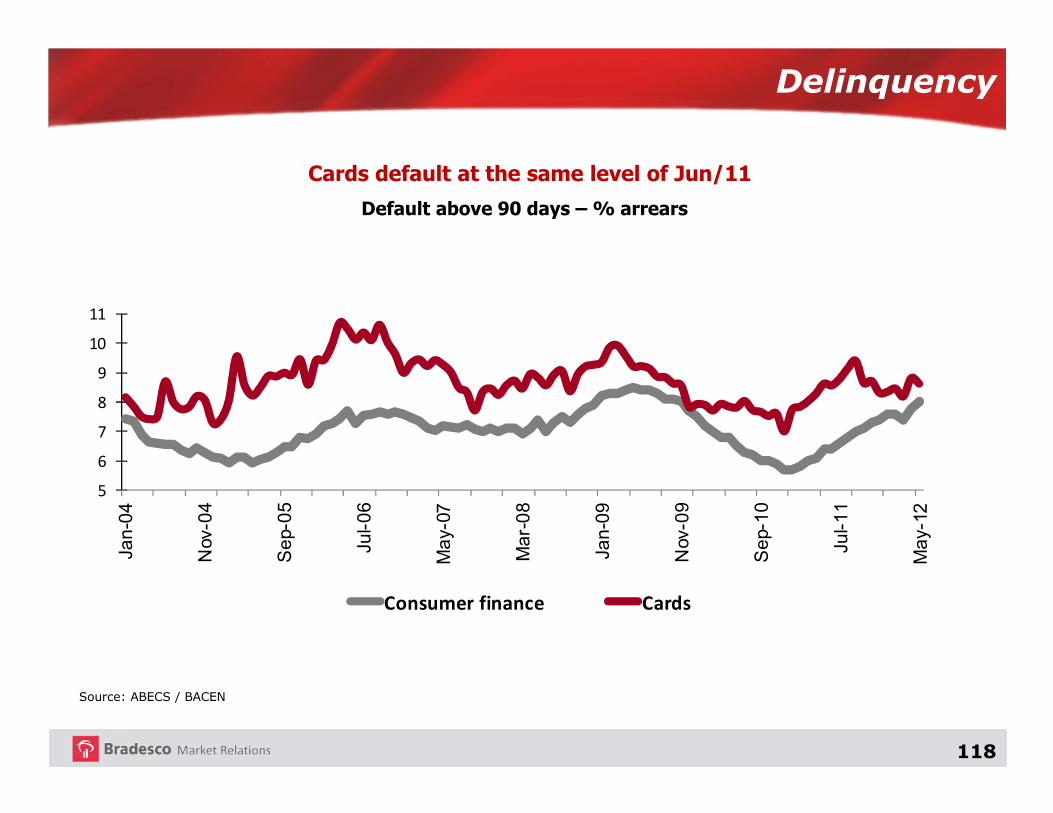

Default above 90 days – % arrears

Source: ABECS / BACEN

Cards default at the same level of Jun/11

Delinquency

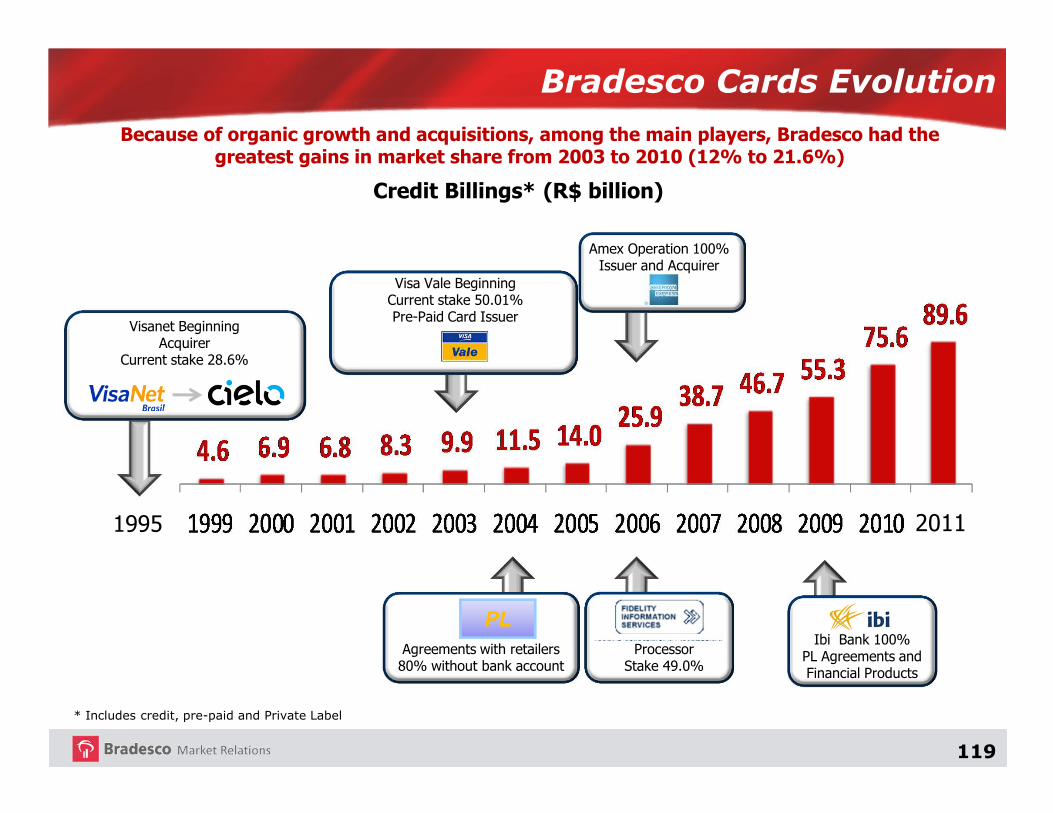

119

Because of organic growth and acquisitions, among the main players, Bradesco had the greatest gains in market share from 2003 to 2010 (12% to 21.6%)

1995

Visanet BeginningAcquirer

Current stake 28.6%

Visa Vale BeginningCurrent stake 50.01%Pre-Paid Card Issuer

Agreements with retailers 80% without bank account

ProcessorStake 49.0%

Ibi Bank 100%PL Agreements and Financial Products

Credit Billings* (R$ billion)

Amex Operation 100%Issuer and Acquirer

Bradesco Cards Evolution

* Includes credit, pre-paid and Private Label

PL

2011

120

Bradesco creates value and participates in the entire value chain of the cards industry

Integrated Card Business

150.2 MM Cards: 95.3 MM Credit | 54.8 MM Debit

ISSUER ASSOCIATED COMPANIESPRIVATE LABEL

More than 30 partners

Participation:

Bradesco Cards

Partners:

Companies that are part of

the Holding Elo

Fidelity 49.00%

50.01%

Elo bandeira 33.33%

28.65%

Elo Participações50.01%

• Ibi Promotora

• Banco CBSS (to be created)

121

Performance

Bradesco Cards Main Indicators

Total Number of Credit Cards

7%

MMCredit Card Billings

15%

R$ bn

Card Loans

13%

Service Revenue

19%

R$ MMR$ bn

89.0

95.3

42.2

48.6

2,391

2,84532.9

29.1

jun/11 jun/12 1S11 1S12

jun/11 jun/12 1S11 1S12

1H11 1H12

1H11 1H12

122

Payroll-Deductible Loans

Real Estate Lending and Mortgage

Cards

Insurance and Pension Plans

Capital Markets

High Growth Products

Vehicles Financing

123

Source: Brazilian Central Bank

Change in Nominal Stock of Payroll Loans

Payroll-deductible loans generated R$175.2 bn in Jun/12,

representing 58.8% of the personal loan market

R$ Million

124

Market Information

Credit to individuals has been strongly driven by

payroll loans

Credit to Individuals

R$ Million

Source: Brazilian Central Bank As of Jun/11 to Jun/12

125

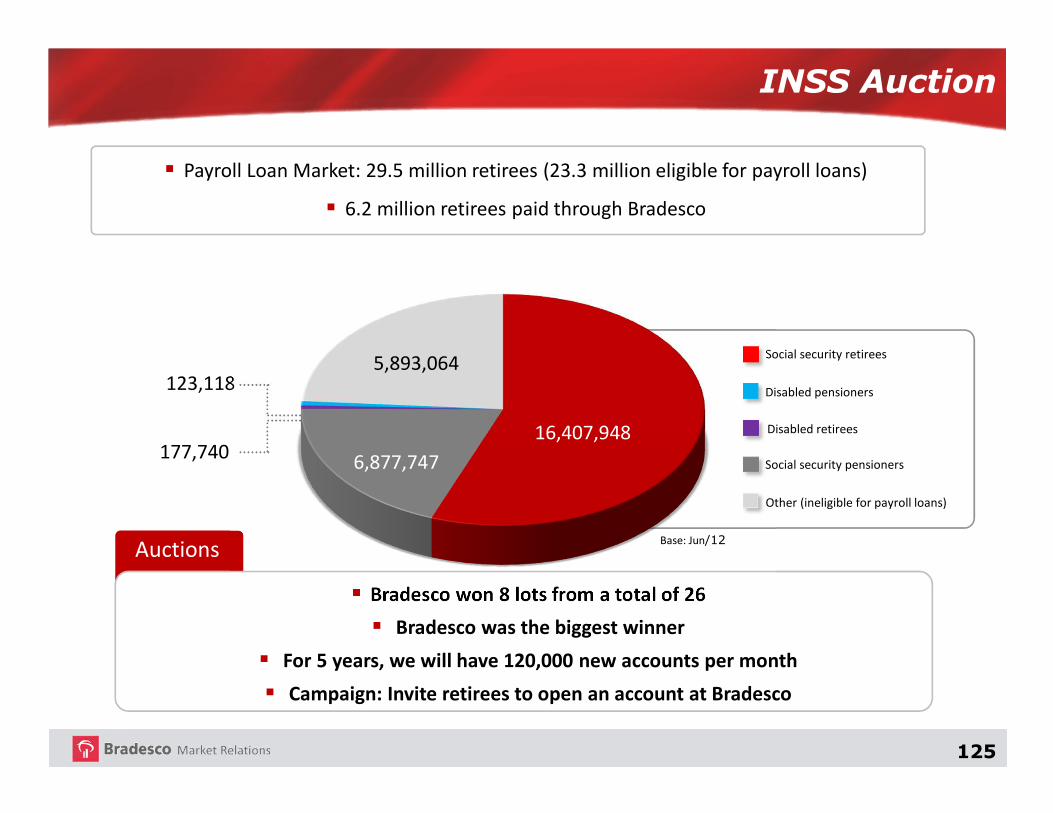

INSS Auction

� Payroll Loan Market: 29.5 million retirees (23.3 million eligible for payroll loans)

� 6.2 million retirees paid through Bradesco

Auctions

� Bradesco won 8 lots from a total of 26

� Bradesco was the biggest winner

� For 5 years, we will have 120,000 new accounts per month

� Campaign: Invite retirees to open an account at Bradesco

123,118

177,74016,407,948

6,877,747

5,893,064Social security retirees

Disabled pensioners

Disabled retirees

Social security pensioners

Other (ineligible for payroll loans)

Base: Jun/12

126

Market Share

Jun/11 Jun/12 Variation

R$ 149.1 Bn R$ 175.3 Bn 17.5%Market

R$ 16.5 Bn R$ 19.5 Bn 18.3%Bradesco

11.0% 11.1% 0.07 p.p.Share

127

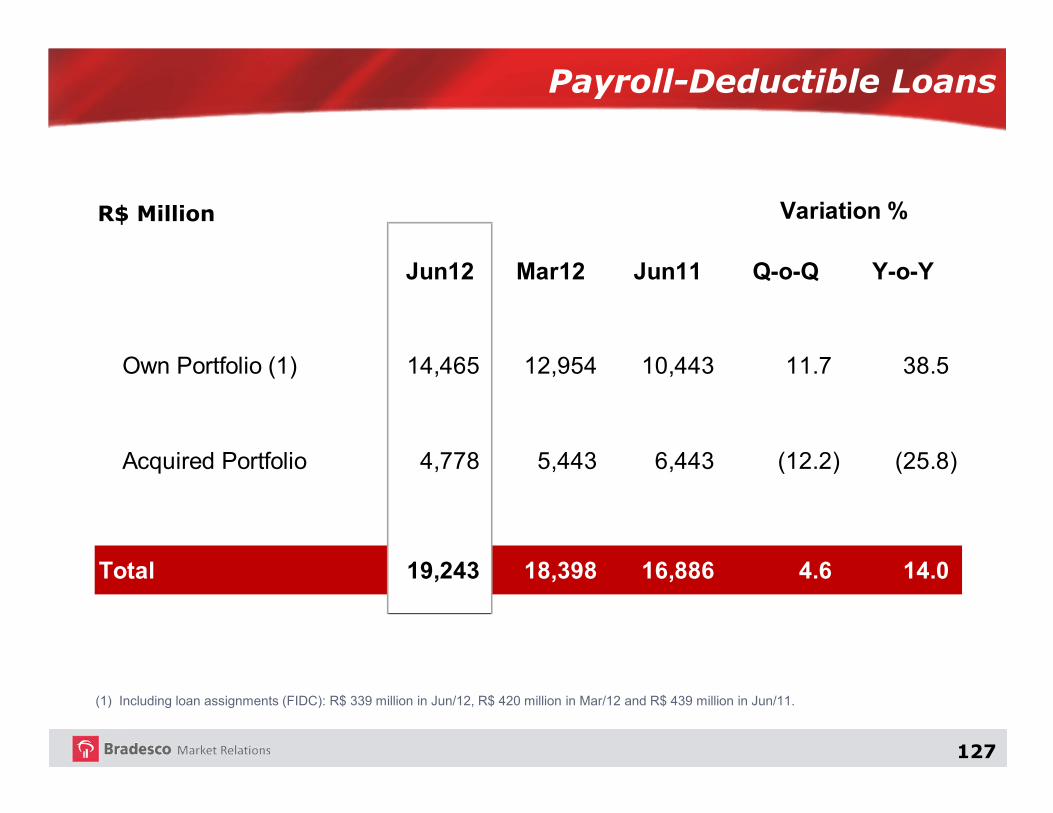

Payroll-Deductible Loans

R$ Million

(1) Including loan assignments (FIDC): R$ 339 million in Jun/12, R$ 420 million in Mar/12 and R$ 439 million in Jun/11.

Jun12 Mar12 Jun11 Q-o-Q Y-o-Y

Own Portfolio (1) 14,465 12,954 10,443 11.7 38.5

Acquired Portfolio 4,778 5,443 6,443 (12.2) (25.8)

Total 19,243 18,398 16,886 4.6 14.0

Variation %

128

Payroll Deductible Loans

Real Estate Lending and Mortgage

Cards

Insurance and Pension Plans

Capital Markets

High Growth Products

Vehicles Financing

129

ITALY

Brazil and World Insurance Market (1)

(1) Not including Savings Bonds

GDP

WRITTEN PREMIUMS% WRITTEN

PREMIUMS/GDP

1st

1st

8.1%

2nd

6th

3.0%

3rd

2nd

11.0%

4th

5th

6.8%

5th

4th

9.5%

6th

3rd

11.8%

7th

14th

3.2%

8th

7th

7.0%

Source: Swiss RE

Insured Homes: 10%

Health Plans Cover 24%

of the population

Insured vehicles: 30%

8% of the population has dental insurance

UKFRANCEGERMANYJAPANCHINAUSA

1.70%

of Global

Market

BRAZIL

130

Saving Bonds

Health

Auto

P&C

Pension Plans

Life

6.2%

47.0%

13.7%

22.2%

29.3%

17.3%

Market

Share

TOTAL 24.5%

Domestic Market Share*

6th

1st

3rd

2nd

1st

2nd

Ranking

1st

* Market Share by RevenueSource: Susep/ANS Data Base: May/12

131

Insurance Group by Region

South

NortheastNorth Midwest

Southeast

32.5%

25.5%

20.6%

26.1%

17.2%

Up to May/12Source: Susep / ANS

Written Premiums of theInsurance Group