around the world - valuewalk.com · \爀屲this isn’t all bad in that crisis creates ......

TRANSCRIPT

AROUNDTHE

WORLD

WITH KENNEDY WILSON

2

DISC

LOSU

RES

DISCLAIMER

The analyses and conclusions of Broyhill Asset Management, LLC (“BAM") contained in this presentation are based on publiclyavailable information. BAM recognizes that there may be confidential information in the possession of the companies discussed inthe presentation that could lead these companies to disagree with BAM’s conclusions. This presentation and the informationcontained herein is not a recommendation or solicitation to buy or sell any securities.

The analyses provided may include certain statements, estimates and projections prepared with respect to, among other things, thehistorical and anticipated operating performance of the companies, access to capital markets and the values of assets and liabilities.Such statements, estimates, and projections reflect various assumptions by BAM concerning anticipated results that are inherentlysubject to significant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrativepurposes. No representations, express or implied, are made as to the accuracy or completeness of such statements, estimates orprojections or with respect to any other materials herein. Actual results may vary materially from the estimates and projected resultscontained herein. Accordingly, no party should purchase or sell securities on the basis of the information contained in thispresentation. BAM expressly disclaims liability on account of any party’s reliance on the information contained herein with respect toany such purchases or sales.

Accounts managed by BAM and its affiliates have invested in the equity of Kennedy-Wilson Holdings, Inc (KW). It is possible thatthere will be developments in the future that cause BAM to change its position regarding the companies discussed in thispresentation. BAM may buy, sell, cover or otherwise change the form of its investment regarding such companies for any reason.BAM hereby disclaims any duty to provide any updates or changes to the analyses contained here including, without limitation, themanner or type of any BAM investment.

3

AG

EN

DA

Forever Blowing Bubbles

Kennedy Wilson Does Europe

Net Asset Value

Introduction

Appendix

INTRO

5

OU

RH

ISTORY

We are a boutique investment firm, established as afamily office and guided by a strict value orientation.Our family office foundation provides the security of astable capital base.

We invest alongside our clients as partners in ourprocess. As a result, we do not feel the constant pressureto gather assets, which ultimately results in poor short-term decisions.

Capital preservation is first and foremost our overridingpriority. We seek to provide consistent returns with alow probability of loss, through concentrated, long-termholdings.

We do not follow the crowd, but instead remainindependent in our decision-making. We are willing toaccept short-term underperformance in exchange forlong-term success.

6

STRIVE

FOR

BA

LAN

CE

If I could say one thing to your investors, it's try to achieve balance.

- Ray Dalio, Davos World Economic Forum

7

PE

RFORM

AN

CE

HISTO

RYGROWTH OF $10,000 INVESTED IN BROYHILL HIGH QUALITY COMPOSITE

8

CA

SHISK

ING

Cash is like oxygen. You don’t notice it 99% of the time, but if it’s absent it’s the only thing you notice.

9

TH

EV

ALU

EO

FE

XTE

RNA

LM

AN

AG

ERS

Our external investments with like-minded, long-term investors complement our internal capabilities, expand our investable universe, and deepen our understanding of financial

markets. Simply put, External Managers, expand our circle of competence.

BLOWINGBUBBLES

11

FO

REV

ER

BLO

WIN

GB

UBBLE

SCONNECTING THE DOTS BETWEEN “THE KING OF COOL” & “THE MAESTRO”

I'm forever blowing bubblesPretty bubbles in the air

They fly so high, nearly reach the skyThen like my dreams they fade and die

Fortune's always hidingI've looked everywhere

I'm forever blowing bubblesPretty bubbles in the air

Source: “I’m Forever Blowing Bubbles”

12

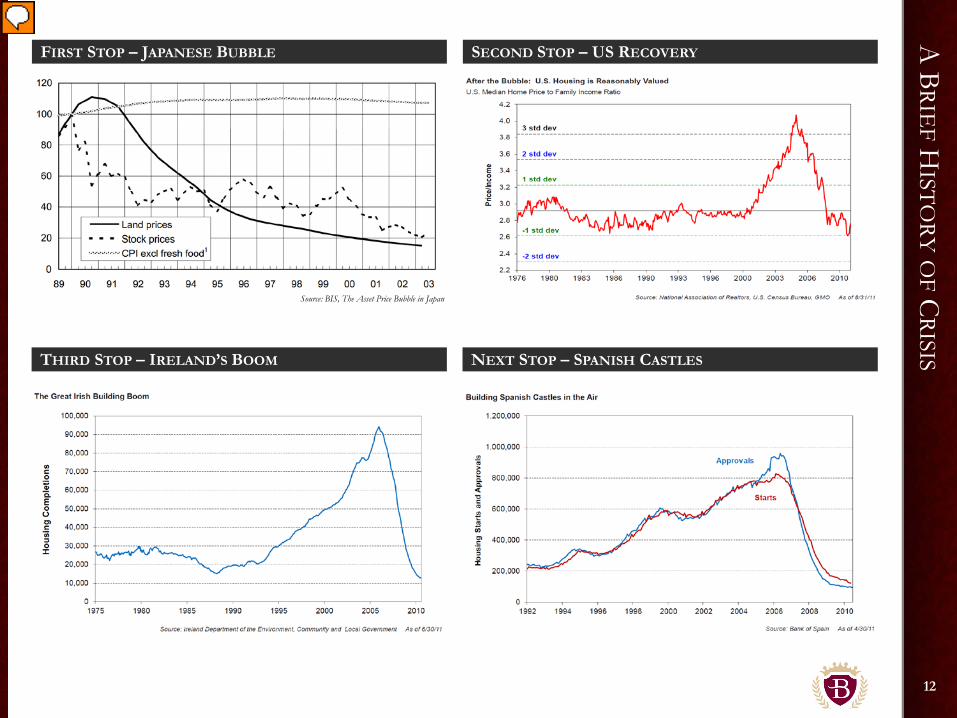

Source: BIS, The Asset Price Bubble in Japan

A B

RIEF

HISTO

RYO

FC

RISISFIRST STOP – JAPANESE BUBBLE

THIRD STOP – IRELAND’S BOOM

SECOND STOP – US RECOVERY

NEXT STOP – SPANISH CASTLES

13

SWIM

MIN

GL

ESSO

NS

The best swimming in the financial markets is when panic breaks loose. By

that time, the damage has been done and those with the courage to dive in head first will find it extremely rewarding.

The increasing number and magnitude of crises begs the question of whether central

bank policies are fanning the flames of destabilizing speculation.

Source: “MarketWatch”

14

SETTIN

GTH

ESTA

GE

15

NPL O

PPORTU

NITY

EUROPEAN BANKING SNAPSHOT

Source: E&Y

16

FLO

CK

ING

TOE

URO

PEA RECORD YEAR FOR NON CORE LOANS

Source: PwC

KWDOES

EUROPE

18

A T

ALE

NTE

DSW

IMM

ER

We’d like to introduce you to a very talented swimmer we recently discovered while surveying the investment landscape for sharks.

Kennedy Wilson went public in 2009 and remains underfollowed and misunderstood despite management’s investment success.

Management has a demonstrated nose for value and a proven track record of identifying and capitalizing on shark-infested waters.

Previous investments have systematically exploited the historical cycle of boom and bust.

WHO IS KENNEDY WILSON?

19

TH

ISSH

OU

LDSO

UN

DF

AM

ILIAR

INVESTING IN OUR CIRCLE OF COMPETENCE

We generally think that asset management is a terrific business.

There’s a natural growth in global demand for financial assets and while thebarriers to entry are fairly low, the barriers to success are fairly high.

Brand, distribution and long-term performance make a big difference.

That results in established companies for the most part generating high margins,high returns on capital and excellent free cash flow.

- Mario Gabelli

A SUSTAINABLE COMPETITIVE ADVANTAGE

Truly durable competitive advantages arise from the intersection of supply anddemand, from the linkages of economies of scale with customer captivity.

Competitive advantages based on economies of scale are in a class by themselves.They tend to be far longer lived than the other types and therefore more valuable.The best course is to establish dominance in a local market and then expandoutward from it. Economies of scale, especially in local markets, are the key tocreating sustainable competitive advantages.

The appropriate strategy is to identify niche markets, understanding that not allniches are equally attractive. Ideally, it will also be readily extendable at theedges. The key is to “think local.”

- Bruce Greenwald and Judd Kahn, “Competition Demystified”

STICKY ASSETS GENERATE DURABLE RETURNS

Those who seek to succeed as long-term investors need time, capital, and fortitude.

Time is important because gaps between fundamentals and expectations are notalways closed quickly.

A stable base of investment capital is also crucial because great investment ideasaren’t worth anything if you have no money to invest.

Investors with a stable and countercyclical base of capital stand at a hugeadvantage to those who work with fleet-footed capital.

– Michael Mauboussin

SECULAR TAILWINDS

Alternative assets make up a small portion of global investable assets but areoutgrowing traditional assets for a number of reasons that we believe are likely tocontinue for some time. With interest rates at generational lows and public marketvolatility near generational highs, investors are diversifying away from conventionalasset classes with subpar returns.

The favorable return attributes of alternative assets are increasingly important asmany liability-matched funds face significant shortfalls. This problem isexacerbated by high rates of expected returns on pension assets - a hurdle that isincreasingly difficult to reach in today’s low return environment.

One way to achieve this return, however, is by committing assets for extendedperiods of time to managers with proven track records.

- Me

Source: Broyhill Asset Management, Solid as an Oak

20

BU

SINE

SSO

VE

RVIE

W

KENNEDY WILSON SERVICES KENNEDY WILSON INVESTMENTS

21

KW

’SC

OM

PETITIV

EA

DV

AN

TAG

EA PROVEN MODEL FOR CAPITAL ALLOCATION

Source: Company Filings

22

EX

CE

PTION

AL

RE

TURN

SO

NC

APITA

LRECENT EXITS DEMONSTRATE POTENTIAL FOR VALUE CREATION

Date Acquired

Purchase Price

($ millions)

Partners Equity

($ millions)

KW Equity

($ millions)Property Name

Sales Proceeds

KW Gains

KW Multiplier

Oct-08 $88.5 $27.8 $3.2(3) Saybrook Pointe, 324-unit apartment building, San Jose, California

$140.8 $2.2 1.7x

Jun-09 $33.5 $5.8 $5.9(3) The Mercury, LA condominiums $52.2 $9.4 2.6x

Sep-09 $210.4 $54.7 $17.5(3) Four multifamily properties in Western US $243.0 $7.9 1.5x

Dec-09 $218.0 $32.2 $44.3(3) 6 multifamily properties in Western US $251.7 $19.5 1.4x

Jun-10 $56.0(1) 9.6(2) $6.4NoHo, 180 unit apartment building; 11,000 sq. ft retail space; increased NOI from $2.3 to $3.1 million

$74.0 $7.2 2.1x

(3) Assume 1.85x Leverage where information is unavailable

(1) Calculated using 4.1% cap rate at sale and $2.1 million of NOI before acquisition(2) Assume 40% participation in partnerships based on company f ilings

Source: Company Filings, Broyhill Asset Management Estimates

“Major corrections create new opportunities that, if seized, can transform companies to even greater heights.”

- Bill McMorrow, 2009 Letter to Shareholders

23

TH

EK

EN

NE

DY

WILSO

NT

OU

CH

VIA VERDE THE ARTISAN

Source: ShowMeTheRent Source: The Artisan Apt Homes

24

GO

OD

CO

MPA

NY

FAIRFAX ANNUAL LETTER EXCERPTS

We continued to purchase commercial real estate investments with Bill McMorrow and his team at Kennedy Wilson. We purchased, 50/50 with Kennedy Wilson, perhaps the finest office building in Dublin, built in 2009 and 100% leased to State Street Bank for 25 years, for one-third of its construction cost with an unleveraged yield of approximately 8.5%. We also own, with Kennedy Wilson, some of the finest apartment buildings in Dublin with similar return characteristics. Rest assured we return Bill’s calls very promptly!

As I mentioned to you last year, one such call from Bill in 2011 led to our investment (along with W.L. Ross, Fidelity and Capital Research) in Bank of Ireland – the first significant investment in Ireland by foreign investors since the financial market collapse. Only one year later, Ireland and its economy have made significant strides towards recovery. The Bank of Ireland has been one of our most successful investments1

We continued to invest with Bill McMorrow from Kennedy Wilson in 2013. We invested in the Clancy Quay apartments and some well-leased office buildings in Dublin and we also invested in a U.K. loan pool. We have invested a net cumulative $305 million in real estate deals with Kennedy Wilson in California, Japan, the U.K. and Ireland – deals at significant discounts to replacement costs and with excellent unlevered cash on cash returns, in which Kennedy Wilson is the managing partner and an investor. Also, we continue to own a fully diluted 10.9% interest in Kennedy Wilson.2

1Fairfax 2012 Annual Letter2Fairfax 2013 Annual Letter

25

DE

ALSSO

URC

ED

FROM

AD

OZ

EN

INSTITU

TION

SKW HISTORY IN EUROPE

Source: Company Filings

26

WA

ITF

OR

IT

27

ATTRA

CTIV

EA

SSETS

AC

ROSS

THE

UK

& IRE

LAN

DKWE ACQUISITIONS SINCE IPO EXCEED £1 BILLION

Source: Company Filings, Broyhill Asset Management Estimates

28

NA

MA

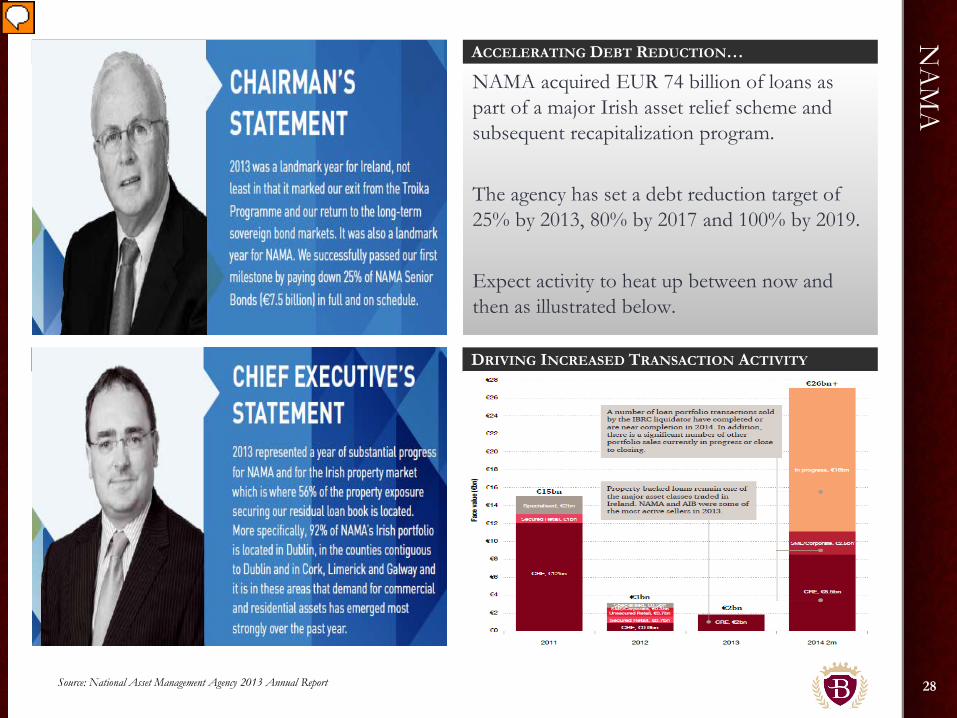

ACCELERATING DEBT REDUCTION…

NAMA acquired EUR 74 billion of loans as part of a major Irish asset relief scheme and subsequent recapitalization program.

The agency has set a debt reduction target of 25% by 2013, 80% by 2017 and 100% by 2019.

Expect activity to heat up between now and then as illustrated below.

DRIVING INCREASED TRANSACTION ACTIVITY

Source: National Asset Management Agency 2013 Annual Report

29

TH

EL

UC

KO

FTH

EIRISH

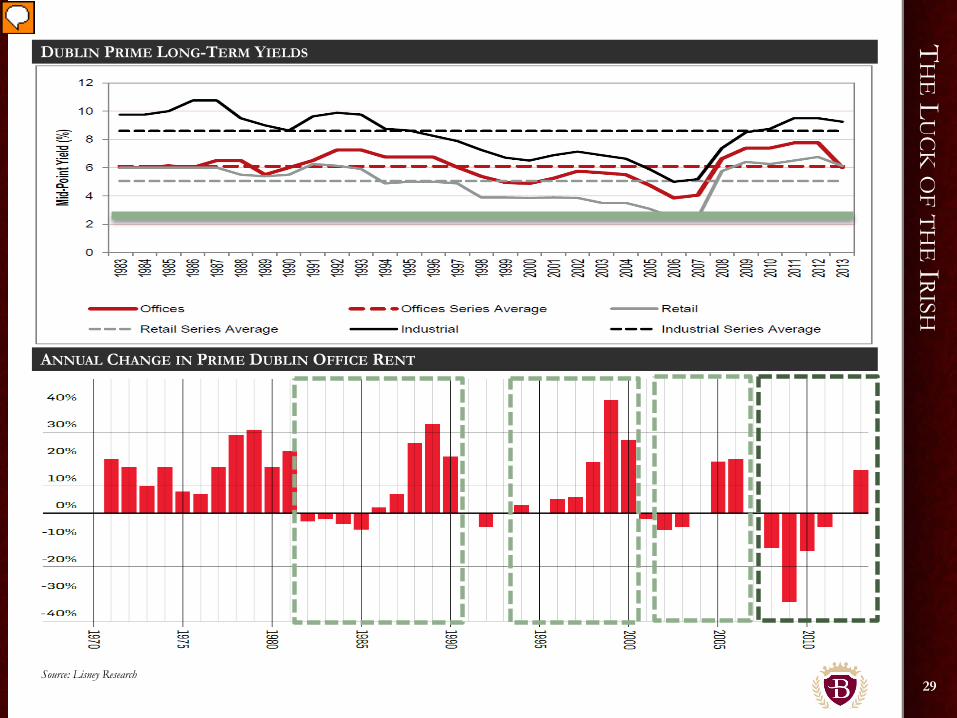

DUBLIN PRIME LONG-TERM YIELDS

ANNUAL CHANGE IN PRIME DUBLIN OFFICE RENT

Source: Lisney Research

30

UPSID

EIN

SEC

ON

DA

RYM

ARK

ETS

UK YIELDS & INTEREST RATES

PRIME PROPERTY PERFORMANCE PRIME INVESTMENT YIELDS

Source: Cushman & Wakefield

31

“PO

PULA

R” GRO

WTH

INM

AD

RID

On December 27, 2013, Banco Popular, SA sold the real-estate management business unit and some of the Bank’s debt related to the property sector to a newly incorporated company, with a majority shareholding by Värde Partners, Inc. and Kennedy Wilson. The sale includes the transfer of all resources required to independently carry out the real-estate management business. This business had been carried out by the group with the objective of maximizing the sale price of property assets and maximizing the recovery of debt related to the real estate sector. This will allow the Bank to benefit from its partner’s broad management experience with these types of assets with the objective of attaining the maximum yield from the management of this business.

Investments in Europe have been sourced directly through extensive relationships with financial institutions in theUK and Ireland. Going forward, we expect that KW’s team in Madrid will provide a long runway for futuregrowth. In line with KW’s time tested business model, management dusted off the Irish playbook and launchedits operations in Spain in 2012 through the real estate auction business followed by a major strategic acquisitionlast year. Here’s the summary from Banco Popular’s Annual Report:

On December 27, 2013, Banco Popular, SA sold the real-estate management business unit and some of the Bank’s debt related tothe property sector to a newly incorporated company, with a majority shareholding by Värde Partners, Inc. and Kennedy Wilson. Thesale includes the transfer of all resources required to independently carry out the real-estate management business. This business hadbeen carried out by the group with the objective of maximizing the sale price of property assets and maximizing the recovery of debtrelated to the real estate sector. This will allow the Bank to benefit from its partner’s broad management experience with these types ofassets with the objective of attaining the maximum yield from the management of this business.

32

SARE

B

NETASSETVALUE

34

A R

ATIO

NA

LA

PPROA

CH

MODERN SECURITY ANALYSIS

“It seems very hard to try to beat the market consistentlyby trying to beat the market. Rather it seems to us a morerational approach is to be value conscious rather thanoutlook conscious.”

- Martin J. Whitman, Modern Security Analysis

35

$0

$5

$10

$15

$20

$25

$30

$35

$11

$32$7

$4

$5

$5

$0

$5

$10

$15

$20

$25

$30

$35

Net LTInvestments

STInvestments

KWServices

KWEMgmt Fees

IncentiveFees

UpsidePotential

NET ASSET VALUE & UPSIDE POTENTIAL

Source: Company Filings, Broyhill Asset Management Estimates

Valued at 1.4x-1.6x Book

Value Net of Debt and

Non-controlling Interests

Cash & Receivables

14x–18xNOI

14x–18xNOI

Assuming Fully

Invested Assets

4x-8x Incentive

Fee-Related Earnings Assuming

1.6x Multiple Over 3 Year

Holding Period

WH

AT’S

ITW

ORTH?

36

SUPE

RM

ARIO

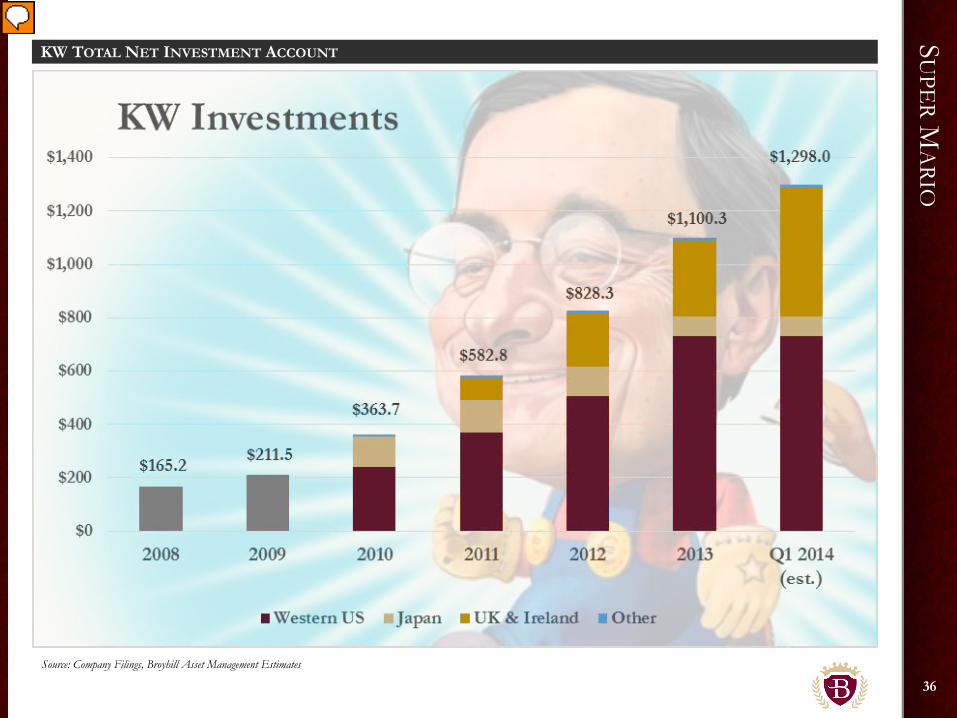

KW TOTAL NET INVESTMENT ACCOUNT

Source: Company Filings, Broyhill Asset Management Estimates

APPENDICES

38

UPSID

EIN

RE

NT

GRO

WTH

& C

AP

RA

TES

KWE SENSITIVITY ANALYSIS

Annual Rent Growth

£ 1.8 0% 2% 4% 6% 8% 10% 12% 14%

9.00% 0.63 0.74 0.87 1.00 1.13 1.28 1.43 1.59

Exi

t Cap

Rat

e

8.50% 0.72 0.85 0.98 1.11 1.26 1.41 1.57 1.74

8.00% 0.83 0.96 1.10 1.25 1.40 1.56 1.73 1.91

7.50% 0.95 1.09 1.24 1.40 1.56 1.73 1.91 2.10

7.00% 1.09 1.24 1.40 1.57 1.74 1.93 2.12 2.32

6.50% 1.25 1.41 1.58 1.76 1.95 2.15 2.36 2.58

6.00% 1.44 1.61 1.80 2.00 2.20 2.42 2.64 2.88

5.50% 1.66 1.85 2.05 2.27 2.49 2.73 2.97 3.23

5.00% 1.93 2.14 2.36 2.59 2.84 3.10 3.37 3.65

Source: Company Filings, Broyhill Asset Management Estimates

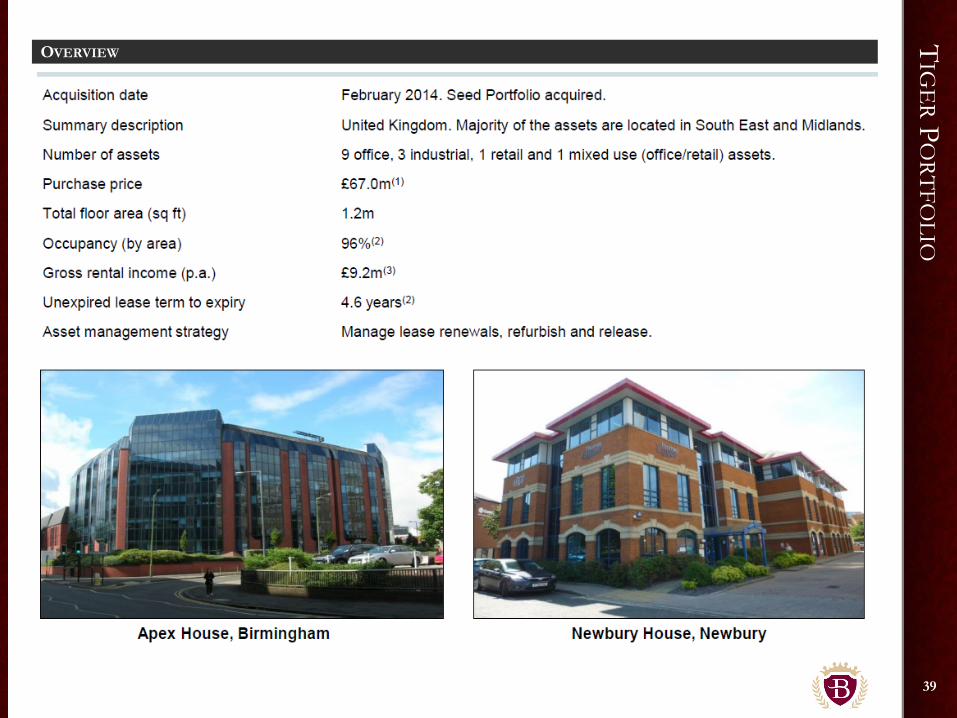

39

TIG

ER

PO

RTFOLIO

OVERVIEW

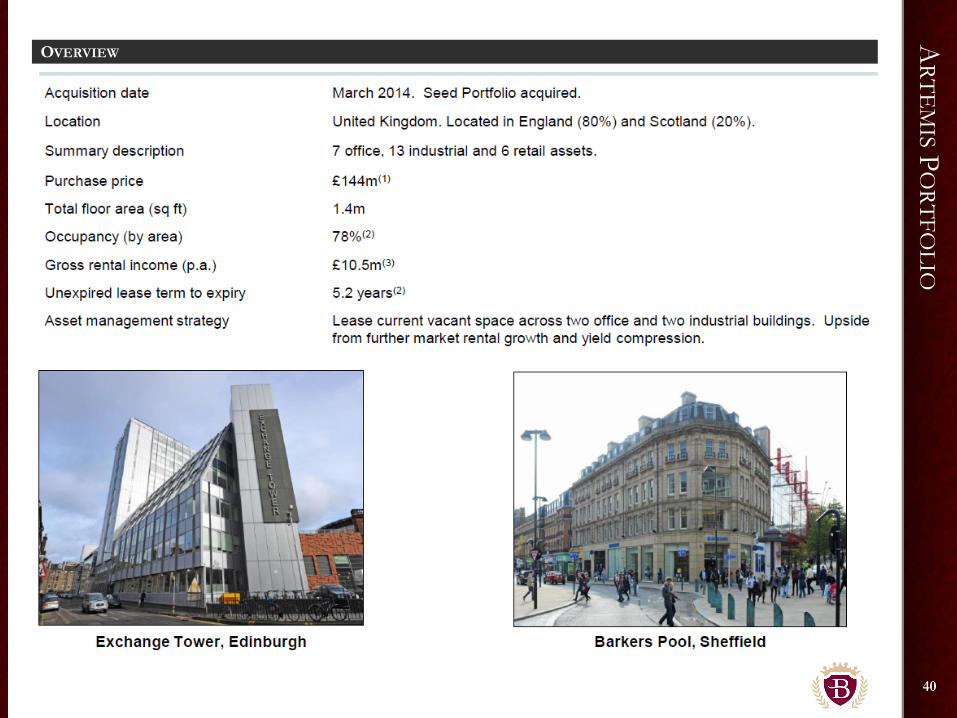

40

ARTE

MISP

ORTFO

LIOOVERVIEW

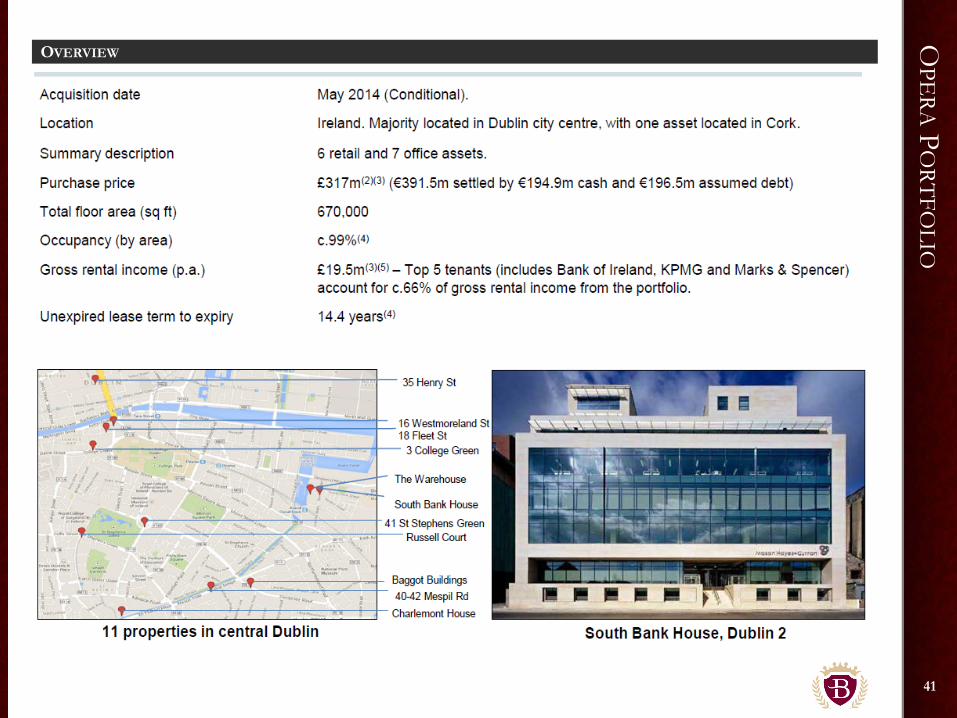

41

OPE

RAP

ORTFO

LIOOVERVIEW

42

CE

NTRA

LP

ARK

PO

RTFOLIO

OVERVIEW

43

PO

RTMA

RNO

CK

HO

TEL

& G

OLF

LIN

KS

OVERVIEW

44

LIFFE

YT

RUST

BU

ILDIN

GOVERVIEW

45

FO

RDG

ATE

JUPITE

ROVERVIEW

46

AV

ON

LO

AN

PO

RTFOLIO

OVERVIEW

47

DISC

LAIM

ER

DISCLAIMER

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

This material has been prepared solely for the purposes of illustration and discussion. “Broyhill Asset Management” is the marketing name forthe investment management business conducted by Broyhill Asset Management, LLC. and its affiliates. Broyhill Asset Management, LLC is anSEC Registered Investment Advisor.

Under no circumstances should the information contained herein be used or considered as an offer to sell, or solicitation of an offer to buy anysecurity. Any security offering is subject to certain investor eligibility criteria as detailed in the applicable offering documents. The informationcontained herein is confidential and may not be reproduced or circulated in whole or in part. The information is in summary form forconvenience of presentation, it is not complete and should not be relied upon as such.

Any information, data, statement, opinions, or projections made herein may contain certain forward looking statements, projections, andinformation that are based on the beliefs of Broyhill Asset Management as well as assumptions made by, and information currently available to,Broyhill Asset Management. Such statements reflect the view of Broyhill Asset Management with respect to future events and are subject tocertain risks, uncertainties and assumptions (including, but not limited to, changes in general economic and business conditions, interest rate andsecurities market fluctuations, competition from within and without the investment industry, new products and services in the investmentindustry, changes in customer profiles, and changes in laws and regulations applicable to Broyhill Asset Management). Should one or more ofthese other risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from thosedescribed herein.

All information, including performance information, has been prepared in good faith; there are no representations or warranty expressed orimplied, as to the accuracy or completeness, of the information, and nothing herein shall be relied upon as a promise or representation as to thepast or future performance. This material may include information that is based, in part or in full, on hypothetical assumptions, models, and/orother analysis (which may not necessarily be described herein). No representations or warranty are made as to the reasonableness of any suchassumptions, models, or analysis. The information set forth herein was gathered from various sources which are believed, but not guaranteed, tobe reliable. Unless stated otherwise, any opinions expressed herein are current as of the date hereof and are subject to change at any time.Accordingly, neither Broyhill Asset Management nor its principals or affiliates make any representations as to the timeliness of any information inthis presentation.

Broyhill Asset Management

Christopher R. Pavese, CFA