asia oil & gas - jrj.com.cnpg.jrj.com.cn/acc/res/cn_res/indus/2012/9/24/a0a6c8… · ·...

TRANSCRIPT

Please refer to the important disclosures and analyst certification on inside back cover of this document, or on our website www.macquarie.com.au/disclosures.

ASIA Oil & Gas

Inside Cracking Times – Nexen – What’s the big deal? 2 Asia Oil & Gas Comparables Valuations 11 Crude Oil Price & Differentials 13 Asia Refining Margins & Cracks 14 China Oil Demand, Production & Imports 16 China Gas Demand, Production & Imports 20 Singapore Oil Product Inventories 21 US Oil Demand & Inventories 22 Global Oil & Gas Comparables Valuation 23 Global Oil Supply-Demand 25 China Gas Supply-Demand 26 Global LNG Supply-Demand 27

Asia Most Preferred CNOOC (OP, TP: HK$21.0) – MarQuee Buy List Kunlun (OP, TP: HK$14.5) PTTGC (OP, TP: Bt79.0) Inpex (OP, TP: Y720,000) BPCL (OP, TP: Rs. 457.0)

Asia Least Preferred Sinopec (N, TP: HK$7.1) COSL (UP, TP: HK$10.4) Petronet LNG (UP, TP: Rs.122.0) FCFC (UP, TP: NT$56.5)

Macquarie Capital Securities Limited James Hubbard, CFA +852 3922 1226 [email protected] Aditya Suresh, CFA +852 3922 1265 [email protected] Macquarie Securities (Thailand) Limited Trevor Buchinski, CFA +66 2 694 7829 [email protected] Macquarie Capital Securities India (Pvt) Ltd Jal Irani +91 22 6720 4080 [email protected] Macquarie Capital Securities Limited, Taiwan Branch Corinne Jian, CFA +886 2 2734 7522 [email protected] Macquarie Capital Securities (Japan) Limited Polina Diyachkina +81 3 3512 7886 [email protected] Macquarie Securities Korea Limited Brandon I Lee +82 2 3705 8669 [email protected]

24 September 2012

Asia Oil & Gas Cracking Times – Nexen – What’s the big deal?

Singapore GRM’s remain strong

Singapore GRM’s saw a small w/w improvement to $8.7/bbl (+$0.3/bbl w/w)

and remained near the top-end of the 5Y range; with strength in gasoline

($15.4/bbl, +$0.6/bbl w/w) and diesel cracks ($19.7/bbl, +$1/bbl w/w) more

than offsetting the decline in LPG cracks (-$23.5/bbl, -$1.7/bbl w/w). The

strength was in-part driven by the $3.9/bbl decline in Brent prices during the

week (weak PMI in China, Europe; weak US jobs data).

China GRM’s – spot margins turn positive

Chinese GRMs improved $1/bbl w/w to $8.5/bbl (3QTD average $3.4/bbl vs. -

$2.5/bbl in 2Q). Of note, following the material $7.7/bbl decrease in Dubai crude

prices during the week, spot China GRMs are now $4.3/bbl (i.e. above the $4/bbl

EBIT breakeven levels) – IF sustained, this would be a positive for Sinopec (see

chart of the week below).

CNOOC-Nexen – What’s the big deal?

CNOOC’s July announcement of its planned US$17.9bn (EV) purchase of

Canada’s Nexen is progressing through the approval process. Ultimately we

believe it is compelling enough for all the key stakeholders that it will go ahead,

essentially unaltered. It is certainly important for CNOOC; in one step it would

add 22% and 35% to 2013E production and 2P reserves (propelling it past

Sinopec) and improve its oft-maligned reserve life (2P) to 18.3 years (+11%).

Our pro forma CNOOC-Nexen sum-of-the-parts valuation would stay almost

unchanged at HK$21.2/sh but Nexen’s contingent resource offers significant

value upside (blue-sky CNOOC-Nexen valuation of HK$31/sh). We raise our

target price by HK$1.5/sh to HK$21.0 and reiterate our Outperform rating.

Chart of the week: Spot GRMs now above EBIT breakeven

Source: Bloomberg, Macquarie Research, September 2012

MacQ China GRM

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

Jan

Fe

b

Ma

r

Apr

Ma

y

Jun

Jul

Aug

Sep

Oct

Nov

Dec

($/bbl)

5Y Range (07-11) 5Y Ave 2011

2012 Implied Fwd Margin EBIT Breakeven

Macquarie Research Asia Oil & Gas

24 September 2012 2

Cracking Times – Nexen – What’s the big deal? Brent declined by $3.9/bbl on average and ended the week at $112.3/bbl mainly on

weak PMI data in China and Europe - HSBC China manufacturing PMI came in at 47.8;

Markit Euro-area PMI dropped to 45.9 (cons. 46.6) in September (14th consecutive month

below 50); and in US weekly jobless claims were higher than consensus expectations.

Singapore GRM’s saw a small w/w improvement to $8.7/bbl (+$0.3/bbl w/w) with

strength in gasoline ($15.4/bbl, +$0.6/bbl w/w) and diesel cracks ($19.7/bbl, +$1/bbl w/w)

more than offsetting the decline in LPG cracks (-$23.5/bbl, -$1.7/bbl w/w).

Chinese GRMs improved $1/bbl w/w to $8.5/bbl (3QTD average $3.4/bbl vs. -$2.5/bbl

in 2Q). Of note, following the material $7.7/bbl decrease in Dubai crude prices during the

week, spot China GRMs are now $4.3/bbl (i.e. above the $4/bbl EBIT breakeven levels) –

if sustained, this would be a positive for Sinopec shares.

In petchems, our benchmark NCC margin witnessed a big w/w increase (+18%) to end at

$270/t; mainly driven by the 6% decline in Naphtha prices during the week (on lower crude

prices).

Fig 1 Asia Oils 1W Share Performance Fig 2 Asia Oils 2012 Share Performance

Source: Bloomberg, Macquarie Research, September 2012 Source: Bloomberg, Macquarie Research, September 2012

Asia Oils 1W Performance

6.7%

6.4%

5.6%

4.1%

4.0%

3.9%

2.6%

2.6%

2.5%

2.1%

0.8%

0.3%

0.1%

0.0%

-0.7%

-0.7%

-0.9%

-1.5%

-2.0%

-2.0%

-2.1%

-2.3%

-2.5%

-2.9%

-3.8%

-4.1%

-4.3%

-4.3%

-4.6%

-4.5%

-1.8%

-1.7%

-0.6%

0.5%

1.1%

2.7%

Inpex Corp

RIL

JX Holdings

ONGC

Aban Offshore

Japan Petroleum

Petrochina

PTT E&P

Cairn India

Bangchak

NPC

COSL

PTT Global

CNOOC

PTT

FCFC

MSCI Asia (ex Japan)

GDG

Oil India

IOCL

Esso Thailand

FPC

Kunlun

Sinopec

Petronet LNG

Woodside

BPCL

Oil Search

Thai Oil

HPCL

Santos

S-Oil

SK Innovation

Caltex

Brent

GS Holdings

Asia Oils 2012 YTD Performance

45%

34%

31%

30%

26%

23%

21%

19%

18%

15%

15%

12%

11%

6%

6%

6%

5%

5%

4%

2%

1%

1%

0%

-1%

-2%

-6%

-6%

-6%

-49%

-12%

4%

5%

9%

13%

16%

24%

BPCL

Caltex

GS Holdings

Bangchak

Aban Offshore

Kunlun

RIL

Oil Search

SK Innovation

HPCL

CNOOC

ONGC

Thai Oil

MSCI Asia (ex Japan)

Woodside

Cairn India

COSL

Jpn Petro

PTT

Petronet LNG

PTT Global

Petrochina

S-Oil

Brent

FPC

Esso Thailand

Inpex Corp

Oil India

IOCL

FCFC

NPC

Santos

PTT E&P

JX Holdings

Sinopec

GDG

Key Macquarie Research

Taiwan petchems – prolonged weak

end-demand (4 Sept)

Asian Refining - Near-term trade;

medium-term played (24 Aug)

Offshore China – A glass still three-

quarters full (30 Jul)

China Oils – Downstream Blues (03 Jul)

Global Oil – A more gradual path to

$115/bbl (11 Jun)

For those seeking defensive oil names

(08 Jun)

The Chinese NGV (R)Evolution (22 May)

China Oil & Gas - “The Three Sisters”

(21 Oct)

Macquarie Research Asia Oil & Gas

24 September 2012 3

What’s new in the region?

CNOOC – Nexen – What’s the big deal? (James Hubbard, 24 Sept): CNOOC’s (883 HK,

OP, TP: HK$21.0) July announcement of its planned US$17.9bn (EV) purchase of Canada’s

Nexen (NXY CN, N, TP: C$27.50, analyst Chris Feltin) is progressing through the approval

process. Ultimately we believe it is compelling enough for all the key stakeholders that it will

go ahead, essentially unaltered. It is certainly important for CNOOC; in one step it would add

22% and 35% to 2013E production and 2P reserves (propelling it past Sinopec) and improve

its oft-maligned reserve life (2P) to 18.3 years (+11%). Our pro forma CNOOC-Nexen sum-of-

the-parts valuation would stay almost unchanged at HK$21.2/sh but Nexen’s contingent

resource offers significant value upside (blue-sky CNOOC-Nexen valuation of HK$31/sh).

We raise our target price by HK$1.5/sh to HK$21.0 and reiterate our Outperform rating.

ONGC – Mumbai High-er (Jal Irani, 24 Sept): We took a group of institutional investors to

ONGC’s (ONGC IN, OP, TP: Rs. 325) Mumbai High field 3D virtual reality room/geological

centre, which oversees ~40% of India’s oil/gas production, and almost all of ONGC’s offshore

operations. We believe that through quick monetization of the recent large D-1 find and

developing marginal fields in the basin, ONGC is firmly poised to reverse its sliding oil output

starting as early as FY14E. Maintain Outperform.

Japan PowerGen Series – upstream oil and gas alert (Polina Diyachkina, 18 Sept): The

Japanese government has decided to promote a 'zero-nuclear' policy by 2030s; our base

case has been for 10% nuclear vs 25% pre quake. Most of nuclear will be replaced by gas-

fired power plants, but there is also scope for an increase in alternative energy and coal-fired

power plants. Clear beneficiaries of the zero-nuclear policy are LNG plays – Inpex and Mitsui.

On the capex front, LNG engineering companies Chiyoda and JGC as well as MHI, Toshiba

and Hitachi would also benefit from both overseas LNG projects and a build-up of domestic

gas and coal-fired power plants.

PTTEP – Capital issuance clarity approaching (Trevor Buchinski, 19 Sept): On August

23, PTTEP (PTTEP TB, N, TP: Bt 165.0) delayed a shareholder vote on a proposed

US$3.1bn capital issuance. PTTEPs board is expected to decide on a new structure over the

next 10 days. Our NAV analysis that suggests fair value for PTTEP is closer to Bt200/sh.

Nevertheless and against our base case expectation we believe parent company PTT offers a

better risk/reward proposition.

Macquarie Research Asia Oil & Gas

24 September 2012 4

Asia Refining Summary

Fig 3 MacQ China GRM Fig 4 Singapore Complex GRM

Fig 5 Korea Complex GRM Fig 6 China vs. S'pore GRM

Fig 7 Asia Refining Margins Summary

Source: Bloomberg, Macquarie Research, September 2012. Note: Singapore GRM based on LPG 3%, Naphtha 7%, Gasoline 32%, Diesel 16%, Jet 19%, FO & Others 23%. China GRM based on - Diesel 0.30, Gasoline 0.20, Fuel Oil 0.09, LPG 0.02, Naphtha 0.02 using a regression analysis.

MacQ China GRM

-20.0

-12.0

-4.0

4.0

12.0

20.0

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

($/bbl)

MQ China GRM 5Y Range 5Y Ave

2011 2012 Fwd Margin

Singapore Complex GRM

0

3

6

9

12

15

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

($/bbl)

Sing GRM 5Y Range (07-11) 5Y Ave

2011 2012

Korea Complex GRM

-3

0

3

6

9

12

15

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

($/bbl)

Korea GRM 5Y Range (07-11) 5Y Ave

2011 2012

China vs. S'pore GRM

-10

-5

0

5

10

15Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep-1

0

No

v-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

Sep-1

1

No

v-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

Sep-1

2

($/bbl)

Delta China GRM Singapore GRM

Macquarie Research

Asia Refining Summary

21-Sep 14-Sep 07-Sep 31-Aug Jul-12 Jul-11 Y-o-Y % 3Q12TD 2Q12 %chg 2012-TD 2011 %chg

Crude Price & Differentials

Brent ($/bbl) 111.9 115.8 114.1 113.8 103.1 116.5 -11% 109.6 108.6 1% 112.4 111.1 1%

Dubai ($/bbl) 109.7 113.8 111.9 110.1 99.2 110.0 -10% 105.8 106.0 0% 109.4 106.1 3%

WTI ($/bbl) 93.7 97.6 95.8 95.7 87.9 97.2 -10% 92.1 93.1 -1% 96.1 95.1 1%

Duri ($/bbl) 112.0 116.1 114.6 115.2 108.9 123.3 -12% 112.3 112.0 0% 116.3 116.2 0%

Cinta ($/bbl) 113.8 117.9 116.4 116.5 108.7 125.0 -13% 113.2 113.1 0% 117.1 117.3 0%

Duri - Brent ($/bbl) 0.1 0.2 0.5 1.3 5.7 6.8 -16% 2.7 3.4 -22% 3.9 5.1 -24%

Arab Light - Heavy ($/bbl) 2.8 2.8 3.0 2.4 2.4 4.1 -41% 2.5 3.2 -23% 2.8 4.1 -32%

Brent - WTI ($/bbl) 18.2 18.2 18.2 18.2 15.3 19.3 -21% 17.4 15.5 13% 16.3 16.0 1%

GRM

Macquarie China GRM ($/bbl) 8.5 7.5 5.5 5.6 (2.0) 0.2 NM 3.4 (2.5) NM 1.0 1.0 -2%

Macquarie China GRM (RMB/t) 410 361 268 272 (95) 8 NM 166 (122) NM 48 51 -7%

Singapore Complex GRM ($/bbl) 8.7 8.4 8.7 9.8 7.6 8.3 -9% 8.8 6.1 43% 7.5 7.6 -2%

Korea Complex GRM ($/bbl) 7.2 7.1 8.3 8.9 6.0 7.0 -15% 7.2 4.4 63% 5.9 6.8 -12%

China Refined Product Cracks

Gasoline ($/bbl) 15.7 14.1 9.8 10.0 (1.1) 2.1 NM 7.0 (2.3) NM 2.8 2.8 1%

Diesel ($/bbl) 27.3 25.7 20.2 20.4 8.9 12.5 -29% 17.4 9.1 91% 13.5 12.9 5%

Fuel Oil ($/bbl) (21.2) (23.0) (18.6) (18.8) (34.0) (32.6) -4% (24.4) (38.4) 57% (28.5) (27.8) -2%

Singapore Refined Product Cracks

Gasoline ($/bbl) 15.4 14.8 12.2 15.2 14.4 16.4 -12% 16.0 14.2 12% 14.8 13.8 8%

Naphtha ($/bbl) (6.5) (4.7) (3.7) (4.1) (8.4) (3.6) -57% (6.6) (8.8) 35% (6.6) (3.7) -44%

Diesel ($/bbl) 19.7 18.7 21.2 22.7 17.8 18.4 -3% 19.5 15.6 25% 17.2 18.4 -7%

Jet Fuel ($/bbl) 21.2 21.4 23.2 22.9 18.4 19.1 -4% 20.4 16.2 26% 17.4 19.5 -11%

LPG ($/bbl) (23.5) (21.8) (22.0) (27.6) (38.0) (40.9) 8% (31.5) (45.1) 43% (34.9) (36.9) 6%

Fuel Oil ($/bbl) (5.8) (6.7) (5.5) (5.2) (4.0) (5.1) 28% (5.0) (3.8) -24% (3.6) (5.2) 45%

Week Month Quarter Year

Macquarie Research Asia Oil & Gas

24 September 2012 5

Asia Petchems Summary

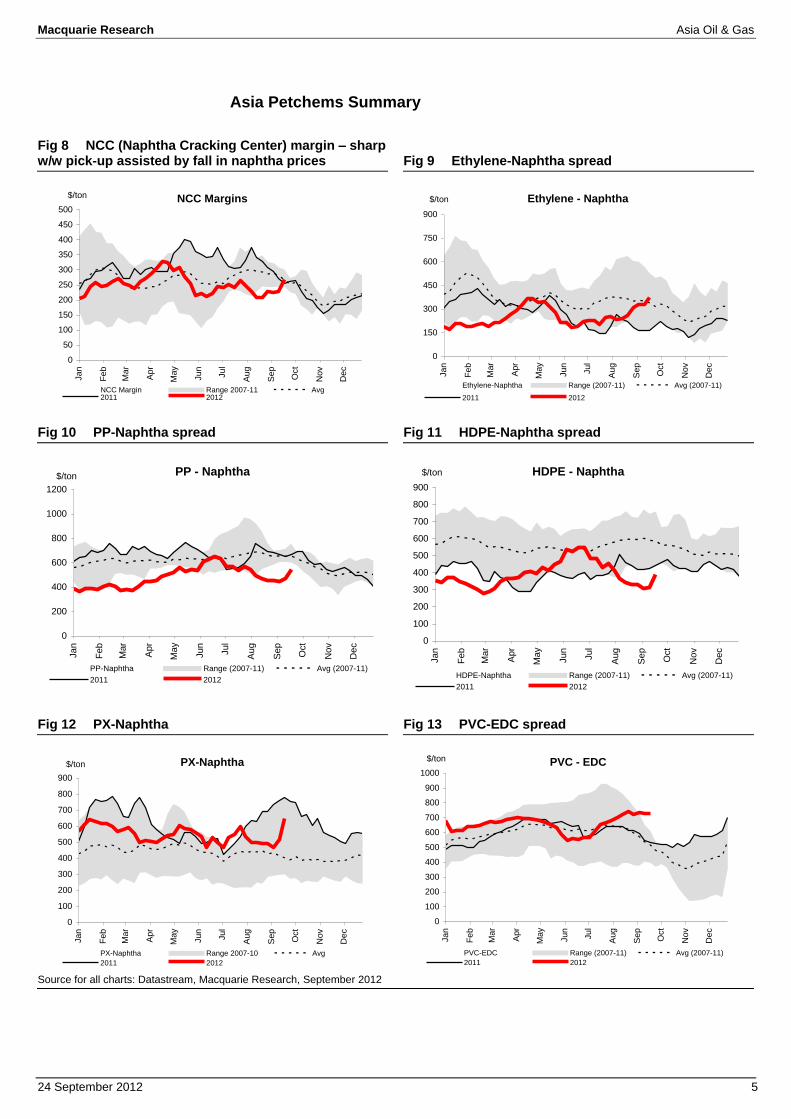

Fig 8 NCC (Naphtha Cracking Center) margin – sharp w/w pick-up assisted by fall in naphtha prices

Fig 9 Ethylene-Naphtha spread

Fig 10 PP-Naphtha spread Fig 11 HDPE-Naphtha spread

Fig 12 PX-Naphtha Fig 13 PVC-EDC spread

Source for all charts: Datastream, Macquarie Research, September 2012

NCC Margins

0

50

100

150

200

250

300

350

400

450

500

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

$/ton

NCC Margin Range 2007-11 Avg2011 2012

Ethylene - Naphtha

0

150

300

450

600

750

900

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

$/ton

Ethylene-Naphtha Range (2007-11) Avg (2007-11)

2011 2012

PP - Naphtha

0

200

400

600

800

1000

1200

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

$/ton

PP-Naphtha Range (2007-11) Avg (2007-11)

2011 2012

HDPE - Naphtha

0

100

200

300

400

500

600

700

800

900

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

$/ton

HDPE-Naphtha Range (2007-11) Avg (2007-11)

2011 2012

PX-Naphtha

0

100

200

300

400

500

600

700

800

900

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

$/ton

PX-Naphtha Range 2007-10 Avg

2011 2012

PVC - EDC

0

100

200

300

400

500

600

700

800

900

1000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

$/ton

PVC-EDC Range (2007-11) Avg (2007-11)

2011 2012

Macquarie Research Asia Oil & Gas

24 September 2012 6

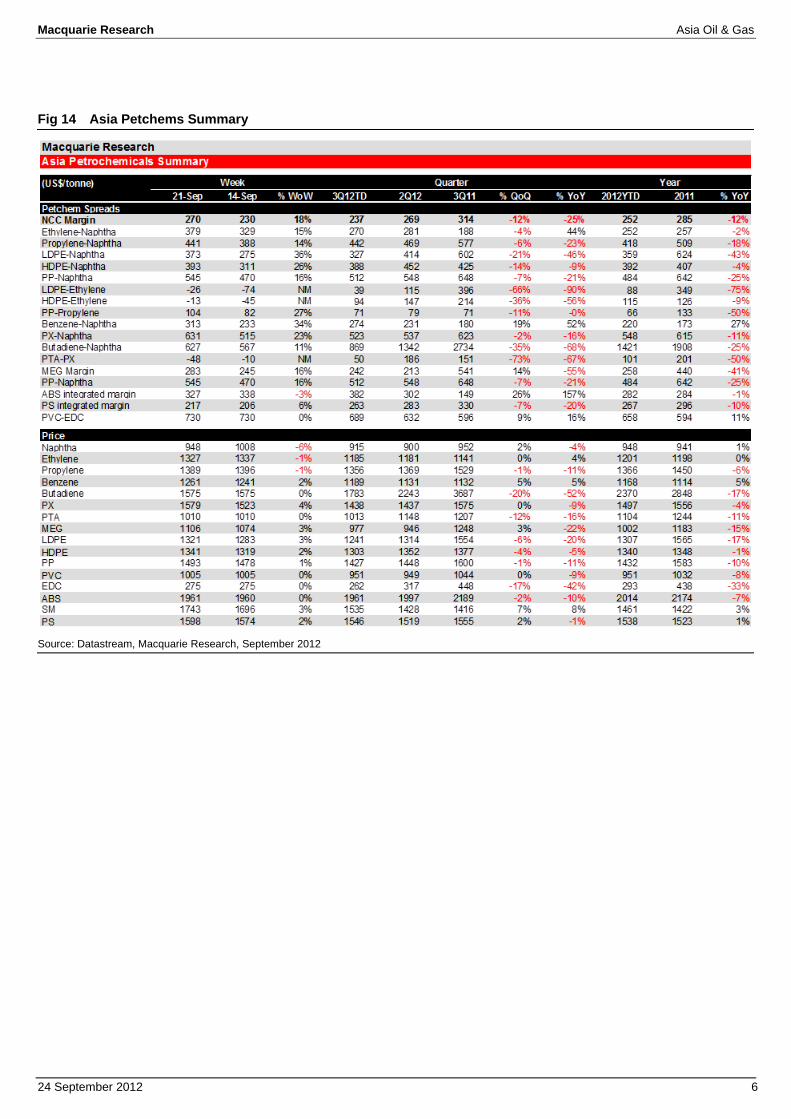

Fig 14 Asia Petchems Summary

Source: Datastream, Macquarie Research, September 2012

Macquarie Research Asia Oil & Gas

24 September 2012 7

Macro – from bad to a bit worse

Fig 15 OECD LI

Fig 16 China GDP estimates – 2012 on a downward trajectory

Fig 17 Unemployment rate – relatively stable Fig 18 Manufacturing PMI – China, US, Euro in contraction mode

Fig 19 China PMI breakdown

Fig 20 China Industrial Production – remains at c.9% for a fourth consecutive month (avg. 15% 2005-11)

Source for all charts: Datastream, Macquarie Research, September 2012

OECD LI

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

(Y-o-Y)

G7 Composite US China Eurozone

China GDP

7.5

7.8

8.1

8.4

8.7

9.0

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Aug-1

2

Y-o-Y %

2012 2013

Unemployment Rate

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

%

China Korea Japan

Manufacturing PMI

20

30

40

50

60

70

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

US China Eurozone

China PMI

35

40

45

50

55

60

65

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

New Export Orders Finished Goods

Raw Materials

China Industrial Production

0

5

10

15

20

25

Dec-

06

Jun-

07

Dec-

07

Jun-

08

Dec-

08

Jun-

09

Dec-

09

Jun-

10

Dec-

10

Jun-

11

Dec-

11

Jun-

12

% (Y-o-Y)

Macquarie Research Asia Oil & Gas

24 September 2012 8

Fig 21 China consumer confidence index Fig 22 China real estate climate index

Fig 23 China textile production

Fig 24 Taiwan computers and electronics manufacturing index

Fig 25 China passenger car sales Fig 26 China tyre output

Source for all charts: Datastream, Macquarie Research, September 2012

China consumer confidence index

85.0

90.0

95.0

100.0

105.0

110.0

115.0

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

China Real Estate Climate Index

90

92

94

96

98

100

102

104

106

108

110

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

China Textile Production

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan-

10

Apr-

10

Jul-

10

Oct-

10

Jan-

11

Apr-

11

Jul-

11

Oct-

11

Jan-

12

Apr-

12

Jul-

12

Y-o-Y %

Yarn Cloth Garment Polyester

Taiwan Computers & Electronics

Manufacturing Index

0

20

40

60

80

100

120

140

160

180

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

Index

(2006=100)

China Passenger Car Sales

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

mn

7Y Range Avg (2005-11)

2010 2011 2012

China Tyre Output

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

mn

7Y Range Avg (2005-11) 2011 2012

Macquarie Research Asia Oil & Gas

24 September 2012 9

Oil – Commitment of Traders (COT) Summary

Fig 27 Fund Net Positions vs. Oil Price Fig 28 Hedge Net Positions vs. Oil Price

Source: Bloomberg, Macquarie Research, September 2012. Note: Fund category covers large speculators or CFTC’s “non-commercial positions”

Source: Bloomberg, Macquarie Research, September 2012. Note: Hedge category covers oil industry traders or CFTC’s “commercial positions”

Fig 29 Small Speculators Net Positions vs. Oil Price Fig 30 Open Interest (futures + options) vs. Oil Price

Source: Bloomberg, Macquarie Research, September 2012. Note: Fund category covers small speculators or CFTC’s “non-reportable positions”

Source: Bloomberg, Macquarie Research, September 2012

Fund Net Positions vs. Oil Price

-100

-50

0

50

100

150

200

250

300

350

400

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

(klots)

0

20

40

60

80

100

120

140

160

($/bbl)

Speculators (LHS) Oil Price (RHS)

Hedge Net Positions vs. Oil Price

-500

-400

-300

-200

-100

0

100

Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep-1

0

No

v-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

Sep-1

1

No

v-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

(klots)

0

20

40

60

80

100

120

WTI $/bbl

Hedge Net Positions (LHS) WTI (RHS)

Small Speculators Net Positions vs. Oil Price

-60

-30

0

30

60

90

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Speculators Net

Position (klots)

0

35

70

105

140

175WTI ($/bbl)

Speculators (Net Position) WTI (RHS)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Open Interest

(klots)

0

20

40

60

80

100

120

140

160WTI $/bbl

Open Interest WTI (RHS)

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

30 J

an

uary

20

12

10

Asia Oil & Gas Comparables Valuations Fig 31 Asia Oil and Gas Comparables Valuation

Source: Bloomberg, Macquarie Research, September 2012

Macquarie Research

Asia Oil & Gas Sector - Valuation, Performance and Operational MetricsMarket

Company Local Price Mcap Reco. Target Upside

Curr (local) (US$ bn) Price 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E

HANG SENG INDEX 20,626 1,551 10.1 x 9.1 x

PetroChina HKD 10.0 240.3 Outperform 12.0 +19.8% 5.3 x 5.0 x 10.8 x 8.7 x 1.3 x 1.2 x 3.9% 4.8% -8.9% 4.3% 10.2% 10.6% 27.0% 26.0%

Sinopec HKD 7.1 80.3 Neutral 7.1 +0.6% 4.1 x 3.2 x 9.2 x 6.5 x 1.0 x 0.9 x 2.7% 3.8% -9.0% 4.8% 9.5% 11.7% 28.1% 26.2%

CNOOC HKD 15.7 90.6 Outperform 21.0 +33.4% 4.4 x 4.1 x 8.0 x 7.6 x 1.7 x 1.5 x 2.0% 3.1% 3.7% 4.0% 20.4% 18.3% 8.6% 5.5%

COSL HKD 13.4 7.8 Underperform 10.4 -22.5% 7.4 x 6.9 x 10.1 x 9.1 x 1.5 x 1.3 x 1.7% 2.1% 4.9% 8.9% 9.1% 9.4% 36.3% 29.3%

Kunlun Energy HKD 13.6 14.2 Outperform 14.5 +6.6% 6.5 x 6.0 x 14.9 x 13.5 x 3.2 x 2.6 x 1.7% 1.8% -7.1% 2.3% 14.4% 14.4% 14.0% 10.1%

Anton HKD 1.9 0.5 Not Rated NM NM 8.9 x 7.0 x 15.7 x 11.2 x

ASX INDEX 4,381.1 1,139.6 11.7 x 10.8 x

Woodside AUD 33.8 29.5 Neutral 37.5 +11.0% 8.2 x 7.1 x 16.5 x 15.5 x 2.0 x 1.9 x 3.7% 4.1% 5.5% 10.0% 9.8% 10.1% 12.4% 5.6%

Santos AUD 11.4 11.5 Outperform 16.00 +40.8% 5.6 x 4.8 x 20.2 x 17.8 x 1.2 x 1.1 x 2.6% 2.6% -18.4% -18.4% 5.2% 5.3% 8.8% 24.9%

Oil Search AUD 7.4 10.6 Outperform 9.0 +21.5% 23.7 x 24.7 x 76.2 x 73.2 x 3.3 x 3.2 x 0.5% 0.5% -5.1% 1.2% 2.7% 2.4% 43.4% 45.5%

Caltex AUD 15.5 4.4 Neutral 16.0 +3.1% 7.3 x 6.2 x 12.6 x 10.9 x 2.1 x 1.8 x 2.0% 2.5% -0.4% 1.8% 13.5% 14.1% 29.3% 26.5%

BSE SENSEX INDEX 18,752.8 581.0 13.1 x 11.9 x

RIL INR 850.3 51.4 Neutral 759.0 -10.7% 7.9 x 7.5 x 11.8 x 11.7 x 1.4 x 1.3 x 1.1% 1.1% 18.1% 1.5% 9.7% 9.3% 19.8% 16.2%

ONGC INR 294.5 46.9 Outperform 325.0 +10.4% 3.8 x 4.4 x 9.5 x 9.6 x 2.0 x 1.9 x 3.3% 3.4% 6.2% 5.7% 19.9% 18.5% -16.2% -18.1%

IOCL INR 252.7 11.5 Outperform 333.0 +31.8% 4.6 x 5.3 x 5.2 x 8.1 x 1.0 x 0.9 x 2.3% 1.5% 21.6% 27.0% 15.4% 9.6% 41.0% 29.7%

Cairn India INR 349.7 12.5 Neutral 322.0 -7.9% 6.3 x 5.5 x 8.7 x 8.5 x 1.3 x 1.2 x 0.0% 2.6% 3.6% 4.6% 16.4% 14.7% -11.9% -20.7%

BPCL INR 347.3 2.3 Outperform 457.0 +31.6% 12.4 x 7.9 x 30.3 x 12.1 x 1.6 x 1.6 x 1.9% 2.1% -59.7% -34.7% 6.9% 9.8% 65.0% 66.0%

HPCL INR 299.0 1.9 Outperform 412.0 +37.8% 10.9 x 6.4 x 69.1 x 6.5 x 0.8 x 0.7 x 3.3% 5.2% -51.7% 14.9% 5.5% 10.7% 72.7% 70.1%

Petronet LNG INR 165.1 2.3 Underperform 122.0 -26.1% 9.0 x 8.3 x 11.5 x 11.3 x 3.4 x 2.7 x 1.8% 1.9% 1.7% -23.8% 19.8% 16.7% 36.8% 52.7%

Aban Offshore INR 430.4 0.3 Underperform 315.0 -26.8% 7.3 x 5.7 x 7.2 x 6.2 x 0.8 x 0.7 x 0.8% 0.8% 20.2% 28.3% 8.3% 9.5% 83.5% 81.3%

SET INDEX 1,286.3 340.3 11.7 x 10.4 x

PTT THB 337.0 31.3 Outperform 409.0 +21.4% 4.3 x 3.7 x 7.5 x 6.4 x 1.5 x 1.3 x 4.5% 5.3% 5.4% 8.3% 15.7% 16.7% 26.1% 21.8%

PTT E&P THB 158.0 17.0 Neutral 165.0 +4.4% 4.2 x 3.5 x 9.7 x 8.5 x 2.1 x 1.8 x 3.6% 3.9% -0.4% 4.2% 16.9% 17.6% 25.5% 22.7%

PTT Global Chem THB 64.3 9.4 Outperform 79.0 +23.0% 6.8 x 6.3 x 8.2 x 8.1 x 1.3 x 1.2 x 4.2% 4.7% 5.3% 9.4% 11.9% 11.9% 29.8% 26.1%

Thai Oil THB 67.0 4.4 Neutral 66.0 -1.5% 7.5 x 6.1 x 12.3 x 9.0 x 1.6 x 1.4 x 3.6% 5.0% 8.0% 8.1% 9.9% 12.2% 18.6% 14.2%

Bangchak Petro. THB 24.6 1.1 Underperform 18.1 -26.4% 4.6 x 4.5 x 6.6 x 7.7 x 1.0 x 0.9 x 4.2% 4.9% 13.7% -10.8% 12.6% 11.4% 6.4% 22.7%

NIKKEI INDEX 9,033.3 2,217.0 12.7 x 10.6 x

Inpex Corp JPY 479,000.0 22.3 Outperform 720,000.0 +50.3% 2.0 x 2.1 x 18.6 x 10.1 x 0.7 x 0.9 x 1.4% 1.4% -2.0% -1.4% 5.0% 8.2% 1.6% 10.1%

JX Holdings JPY 433.0 13.9 Outperform 600.0 +38.6% 4.1 x 5.4 x 4.5 x 10.6 x 0.6 x 0.6 x 3.7% 3.7% 7.4% -13.5% 8.0% 3.9% 40.4% 43.1%

Japan Petro. Expln JPY 3,165.0 2.3 Outperform 4,600.0 +45.3% 4.4 x 4.9 x 10.3 x 11.3 x 0.4 x 0.4 x 1.3% 1.3% 7.3% -12.3% 4.1% 3.7% -0.9% 4.8%

TWSE Index 7,722.9 723.3 14.1 x 12.4 x

FPCC TWD 87.5 28.7 Underperform 65.0 -25.7% 26.2 x 16.8 x 250.3 x 44.9 x 3.8 x 3.6 x 0.5% 1.9% 3.0% 2.7% 1.6% 5.3% 42.0% 37.2%

FPC TWD 82.8 17.5 Neutral 68.5 -17.3% 17.2 x 15.0 x 28.7 x 21.6 x 2.1 x 2.0 x 2.5% 3.1% 5.1% 2.7% 5.9% 7.6% 4.3% 5.8%

NPC TWD 57.6 15.7 Neutral 50.0 -13.2% 28.5 x 14.9 x 56.0 x 19.3 x 1.7 x 1.6 x 1.2% 3.5% 5.1% 4.2% 2.6% 6.5% 20.5% 17.5%

FCFC TWD 77.7 15.3 Underperform 56.5 -27.3% 19.3 x 13.3 x 38.2 x 20.0 x 1.8 x 1.7 x 1.7% 3.3% 2.9% 4.6% 3.8% 6.6% 14.0% 11.3%

KOSPI INDEX 1,981.8 1,002.5 9.3 x 8.1 x

SK Innovation KRW 164,000.0 13.9 Outperform 222,000.0 +35.4% 6.9 x 6.5 x 10.2 x 7.6 x 1.0 x 0.9 x 1.7% 1.7% 6.3% 3.7% 7.6% 8.9% 19.6% 14.9%

S-Oil KRW 103,000.0 10.6 Neutral 105,000.0 +1.9% 9.8 x 7.7 x 13.0 x 8.8 x 2.2 x 1.9 x 2.8% 4.3% 9.7% 14.1% 10.6% 14.5% 28.7% 14.6%

GS Holdings KRW 65,000.0 5.5 Neutral 67,000.0 +3.1% 6.0 x 4.8 x 9.3 x 7.4 x 0.9 x 0.8 x 2.1% 2.2% 13.1% 10.6% 8.3% 9.3% 14.6% 4.8%

Honam KRW 255,000.0 7.5 Outperform 320,000.0 +25.5% 8.0 x 5.0 x 16.7 x 8.7 x 1.4 x 1.2 x 0.7% 0.7% -3.7% 6.6% 7.0% 12.2% 11.2% 4.1%

LG Chem KRW 323,000.0 19.5 Outperform 400,000.0 +23.8% 8.0 x 6.6 x 14.0 x 11.1 x 2.1 x 1.8 x 1.2% 1.2% 2.8% 0.4% 13.1% 14.5% 6.9% 7.1%

Hanwha Chem KRW 21,850.0 2.8 Neutral 20,000.0 -8.5% 11.5 x 7.6 x 21.9 x 8.9 x 0.8 x 0.7 x 2.0% 2.0% -18.4% -9.3% 2.8% 5.3% 49.6% 49.0%

HK/China 433.7 +17.9% 5.0 x 4.6 x 10.1 x 8.2 x 1.4 x 1.2 x 3.1% 4.1% -6.0% 4.3% 12.3% 12.5% 23.1% 21.3%

Australia 56.0 +18.5% 10.5 x 9.9 x 28.2 x 26.5 x 2.1 x 2.0 x 2.8% 3.0% -1.9% 1.9% 7.8% 8.0% 18.8% 18.7%

India 129.1 +2.1% 6.1 x 6.0 x 11.3 x 10.2 x 1.6 x 1.5 x 2.0% 2.2% 10.0% 4.8% 14.6% 13.4% 7.6% 3.9%

Thailand 63.2 +14.6% 4.9 x 4.2 x 8.5 x 7.4 x 1.6 x 1.4 x 4.1% 4.8% 4.1% 7.0% 15.0% 15.8% 25.6% 22.1%

Japan 38.5 +45.8% 2.9 x 3.4 x 13.0 x 10.4 x 0.7 x 0.7 x 2.2% 2.2% 2.0% -6.4% 6.0% 6.4% 15.4% 21.6%

Taiwan 77.2 -21.6% 23.3 x 15.3 x 118.5 x 29.4 x 2.6 x 2.5 x 1.3% 2.8% 3.9% 3.4% 3.2% 6.4% 23.5% 20.9%

Korea 30.0 +17.7% 8.1 x 6.5 x 13.2 x 9.1 x 1.6 x 1.4 x 1.7% 1.9% 4.0% 4.9% 9.7% 12.0% 17.0% 11.6%

APAC 827.7 +12.8% 7.3 x 6.1 x 21.7 x 11.8 x 1.6 x 1.4 x 2.7% 3.5% -0.8% 3.9% 11.3% 11.7% 20.1% 18.1%

21 September 12

EV/EBITDA Ratio ROACE GearingFCF YieldDividend YieldP/B RatioP/E Ratio

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

30 J

an

uary

20

12

11

Fig 32 Asia Oil and Gas Performance Summary, EPS, MacQ vs. Consensus

Source: Bloomberg, Macquarie Research, September 2012

Macquarie Research

Asia Oil & Gas Sector - Valuation, Performance and Operational Metrics

Company Local Price Target Upside Cons. Macq. vs.

Curr (local) Price 1 M 3 M 6 M 1 Y YTD 2011A 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E TP Cons.

HANG SENG INDEX +3.2% +7.6% -0.6% +10.2% +12.5%

PetroChina HKD 10.02 12.0 +19.8% +3.2% -2.7% -8.8% +7.7% +5.3% 0.73 0.71 0.88 -2.1% +23.7% 0.75 0.83 -5.3% +6.2% 11.4 5.5%

Sinopec HKD 7.06 7.1 +0.6% -3.2% +2.6% -16.7% -5.2% -12.1% 0.85 0.62 0.88 -26.6% +41.3% 0.69 0.86 -9.4% +2.8% 8.1 -12.2%

CNOOC HKD 15.74 21.0 +33.4% +4.2% +5.1% -5.9% +21.5% +15.9% 1.57 1.49 1.58 -5.1% +6.0% 1.45 1.44 +3.1% +9.8% 17.2 21.8%

COSL HKD 13.42 10.4 -22.5% +6.0% +20.9% +16.5% +32.7% +9.3% 0.90 1.05 1.16 +16.9% +10.8% 1.03 1.17 +1.7% -0.1% 14.5 -28.5%

Kunlun Energy HKD 13.60 14.5 +6.6% +4.9% +8.2% -1.4% +23.4% +23.9% 0.78 0.91 1.01 +16.6% +10.4% 0.90 1.06 +1.2% -5.1% 16.0 -9.5%

Anton HKD 1.86 NM NM +18.8% +63.8% +91.9% +134.6% +120.9% 0.10 0.14 2.2

ASX INDEX +0.6% +7.8% +3.6% +8.3% +8.7%

Woodside AUD 33.78 37.5 +11.0% -5.1% +6.5% -2.1% +1.4% +11.5% 2.09 2.20 2.35 +5.7% +6.6% 2.52 2.66 -12.4% -11.6% 39.0 -3.9%

Santos AUD 11.36 16.00 +40.8% -4.7% -0.7% -20.1% +0.0% -6.1% 0.50 0.58 0.69 +14.0% +19.5% 0.61 0.59 -5.8% +16.4% 15.0 6.4%

Oil Search AUD 7.41 9.0 +21.5% +5.7% +14.9% +9.4% +26.2% +21.1% 0.18 0.10 0.11 -41.3% +4.7% 0.13 0.12 -17.9% -11.3% 8.7 3.1%

Caltex AUD 15.52 16.0 +3.1% +1.3% +19.5% +12.5% +47.3% +33.6% 0.98 1.29 1.55 +32.3% +19.5% 1.35 1.35 -4.0% +15.0% 14.9 7.3%

BSE SENSEX INDEX +4.9% +10.1% +6.5% +9.9% +21.3%

RIL INR 850.30 759.0 -10.7% +4.4% +18.3% +10.7% +1.5% +22.7% 73.80 66.75 67.54 -9.6% +1.2% 62.29 67.07 +7.2% +0.7% 798.2 -4.9%

ONGC INR 294.50 325.0 +10.4% +2.6% +7.0% +8.5% +12.8% +14.8% 10.31 29.22 29.61 NM +1.3% 30.65 33.03 -4.7% -10.4% 312.2 4.1%

IOCL INR 252.70 333.0 +31.8% +0.3% -3.5% -6.6% -18.0% -0.4% 32.25 49.15 31.29 +52.4% -36.3% 29.31 33.25 +67.7% -5.9% 294.3 13.2%

Cairn India INR 349.65 322.0 -7.9% +5.4% +7.2% -2.0% +17.3% +11.3% 33.04 39.13 40.24 +18.4% +2.8% 54.48 50.34 -28.2% -20.1% 373.2 -13.7%

BPCL INR 347.30 457.0 +31.6% +2.5% -9.0% -0.1% +4.7% +45.4% 22.61 11.53 28.94 -49.0% NM 20.26 24.85 -43.1% +16.4% 392.7 16.4%

HPCL INR 299.00 412.0 +37.8% -4.2% -11.0% +0.6% -19.2% +18.2% 51.22 4.50 47.53 -91.2% NM 32.19 43.04 -86.0% +10.4% 346.9 18.8%

Petronet LNG INR 165.10 122.0 -26.1% +10.0% +21.2% +2.2% -7.2% +6.0% 8.26 14.10 14.24 +70.7% +1.0% 14.08 15.13 +0.1% -5.9% 173.7 -29.8%

Aban Offshore INR 430.40 315.0 -26.8% +1.5% +22.0% -8.4% +10.2% +25.6% 107.26 58.52 68.58 -45.4% +17.2% 81.94 85.54 -28.6% -19.8% 447.0 -29.5%

SET INDEX +4.4% +11.0% +6.5% +24.9% +25.4%

PTT THB 337.00 409.0 +21.4% -1.2% +5.0% -4.8% +8.0% +6.0% 36.86 43.68 51.47 +18.5% +17.8% 38.82 43.79 +12.5% +17.5% 378.0 8.2%

PTT E&P THB 158.00 165.0 +4.4% +3.6% -6.5% -11.2% -2.8% -6.2% 13.63 15.54 17.62 +14.0% +13.4% 15.93 17.96 -2.4% -1.9% 171.6 -3.8%

PTT Global Chem THB 64.25 79.0 +23.0% +0.0% +14.2% -11.4% +19.0% +5.3% 4.05 7.41 7.57 NM +2.2% 6.39 7.27 +16.0% +4.2% 71.1 11.1%

Thai Oil THB 67.00 66.0 -1.5% -0.4% +13.6% -7.6% +11.2% +14.5% 7.45 5.44 7.41 -27.0% +36.2% 7.40 6.59 -26.4% +12.5% 69.1 -4.5%

Bangchak Petro. THB 24.60 18.1 -26.4% +7.0% +5.1% +5.6% +20.6% +30.2% 5.40 3.54 3.02 -34.4% -14.7% 2.68 3.33 +32.1% -9.2% 24.4 -25.9%

NIKKEI INDEX -0.5% +3.2% -9.7% +4.2% +7.7%

Inpex Corp JPY 479,000 720,000 +50.3% +2.1% +5.3% -13.2% -3.8% +0.7% 37,355 23,971 43,979 -35.8% +83.5% 48,497 42,135 -50.6% +4.4% 709,273 1.5%

JX Holdings JPY 433.00 600.0 +38.6% +5.8% +5.3% -16.8% -4.6% -6.5% 127.50 89.70 38.16 -29.6% -57.5% 43.15 64.54 NM -40.9% 533.8 12.4%

Japan Petro. Expln JPY 3,165.00 4,600.0 +45.3% -0.2% +2.9% -18.5% +3.9% +6.1% 248.07 292.49 264.31 +17.9% -9.6% 286.22 290.00 +2.2% -8.9% 4,121.4 11.6%

TWSE Index +3.3% +6.5% -2.8% +2.9% +9.7%

FPCC TWD 87.50 65.0 -25.7% -2.6% +6.9% -5.1% +4.3% -5.9% 2.00 0.34 1.87 -83.2% NM 1.43 3.39 -76.6% -44.8% 72.4 -10.3%

FPC TWD 82.80 68.5 -17.3% -0.5% +4.9% -3.9% +1.5% +3.6% 5.73 2.85 3.80 -50.2% +33.2% 3.94 5.50 -27.5% -30.9% 79.8 -14.1%

NPC TWD 57.60 50.0 -13.2% -0.5% +4.6% -10.4% -14.2% -2.3% 2.87 0.98 2.85 -65.8% NM 1.87 3.40 -47.6% -16.3% 54.9 -9.0%

FCFC TWD 77.70 56.5 -27.3% -3.7% -0.8% -6.6% -4.1% -1.1% 5.68 1.99 3.80 -64.9% +90.9% 3.32 5.25 -40.0% -27.6% 76.4 -26.0%

KOSPI INDEX +3.0% +6.0% -1.2% +8.0% +9.7%

SK Innovation KRW 164,000 222,000 +35.4% +0.0% +16.6% -1.5% -0.9% +18.7% 33,778 16,521 22,020 -51.1% +33.3% 18,077 21,169 -8.6% +4.0% 195,900 13.3%

S-Oil KRW 103,000 105,000 +1.9% -2.8% +12.2% -11.0% -13.9% +5.0% 10,158 8,090 11,971 -20.4% +48.0% 8,794 11,392 -8.0% +5.1% 119,552 -12.2%

GS Holdings KRW 65,000 67,000 +3.1% +2.2% +20.1% +2.3% -6.6% +30.6% 8,143 7,210 9,150 -11.5% +26.9% 6,774 8,384 +6.4% +9.1% 73,970 -9.4%

Honam KRW 255,000 320,000 +25.5% +2.9% +11.2% -16.1% -28.5% -11.9% 31,081 14,602 28,107 -53.0% +92.5% 24,155 35,269 -39.5% -20.3% 296,586 7.9%

LG Chem KRW 323,000 400,000 +23.8% +3.1% +14.2% -10.5% -6.3% +3.8% 28,512 21,971 27,692 -22.9% +26.0% 26,688 33,405 -17.7% -17.1% 383,185 4.4%

Hanwha Chem KRW 21,850 20,000 -8.5% +3.2% +6.4% -15.3% -27.7% -8.5% 1,789 936 2,298 -47.7% NM 1,816 1,720 -48.5% +33.6% 21,529 -7.1%

HK/China +17.9% +2.4% +0.8% -8.8% +9.3% +5.1% -6.3% +22.6% -4.0% +5.9% +4.5%

Australia +18.5% -2.5% +7.6% -2.5% +9.4% +11.5% +0.6% +9.9% -11.4% -3.7% +0.4%

India +2.1% +3.4% +10.3% +6.6% +5.0% +16.7% +1.5% -1.9% +2.3% -5.7% -0.7%

Thailand +14.6% +0.5% +3.9% -7.5% +7.2% +3.6% +10.4% +15.0% +6.6% +9.5% +3.9%

Japan +45.8% +3.3% +5.2% -14.8% -3.6% -1.5% -30.3% +27.0% -29.1% -12.7% +6.1%

Taiwan -21.6% -1.9% +4.5% -6.2% -1.8% -2.1% -68.6% +25.6% -52.3% -32.4% -14.0%

Korea +19.4% +1.2% +14.2% -8.2% -10.2% +7.4% -32.9% +38.8% -15.8% -3.9% +2.2%

APAC +12.9% +1.7% +4.0% -5.9% +6.1% +6.3% -11.2% +18.4% -8.8% -1.1% +1.6%

21 September 12

Absolute Performance EPS (local) Macq. vs. ConsEPS growth Cons EPS (local)

Macquarie Research Asia Oil & Gas

24 September 2012 12

Crude Oil Price & Differentials

Fig 33 Global crude benchmarks Fig 34 Crude Differentials

Fig 35 Brent forward curve at c.$95-100/bbl long-term Fig 36 Crude price summary

21-Sept

14-Sept

3Q12TD

2Q12 Q/Q

%chg

Brent ($/bbl) 111.9 115.8 109.6 108.6 1%

Dubai ($/bbl) 109.7 113.8 105.8 106.0 0%

WTI ($/bbl) 93.7 97.6 92.1 93.1 -1%

Duri ($/bbl) 112.0 116.1 112.3 112.0 0%

Minas ($/bbl) 113.8 117.9 113.2 113.1 0%

Duri - Brent ($/bbl) 0.1 0.2 2.7 3.4 -22%

Arab Light - Heavy ($/bbl)

2.8 2.8 2.5 3.2 -23%

Brent - WTI ($/bbl) 18.2 18.2 17.4 15.5 13%

Source for all charts: Bloomberg, Macquarie Research, September 2012.

China Crude Basket

50

65

80

95

110

125

140

De

c-0

9

Feb-1

0

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

De

c-1

0

Feb-1

1

Apr-

11

Jun-1

1

Aug-1

1

Oct-

11

De

c-1

1

Feb-1

2

Apr-

12

Jun-1

2

Aug-1

2

$/bbl

Brent Dubai Cinta WTI China Crude Basket

Crude differentials

-10

-5

0

5

10

15

20

25

30

De

c-0

9

Feb-1

0

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

De

c-1

0

Feb-1

1

Apr-

11

Jun-1

1

Aug-1

1

Oct-

11

De

c-1

1

Feb-1

2

Apr-

12

Jun-1

2

Aug-1

2

$/bbl

Brent-Urals Duri-Brent Arab Light-Heavy Brent-WTI

Brent Forward Curve

25.0

50.0

75.0

100.0

125.0

150.0

Jan-0

8

Jul-08

Jan-0

9

Jul-09

Jan-1

0

Jul-10

Jan-1

1

Jul-11

Jan-1

2

Jul-12

Jan-1

3

Jul-13

Jan-1

4

Jul-14

($/bbl)

Spot T-1 month

T-3 months T-1 year

At 2008 peak ($145/bbl) At 2008 trough ($35/bbl)

Macquarie Research Asia Oil & Gas

24 September 2012 13

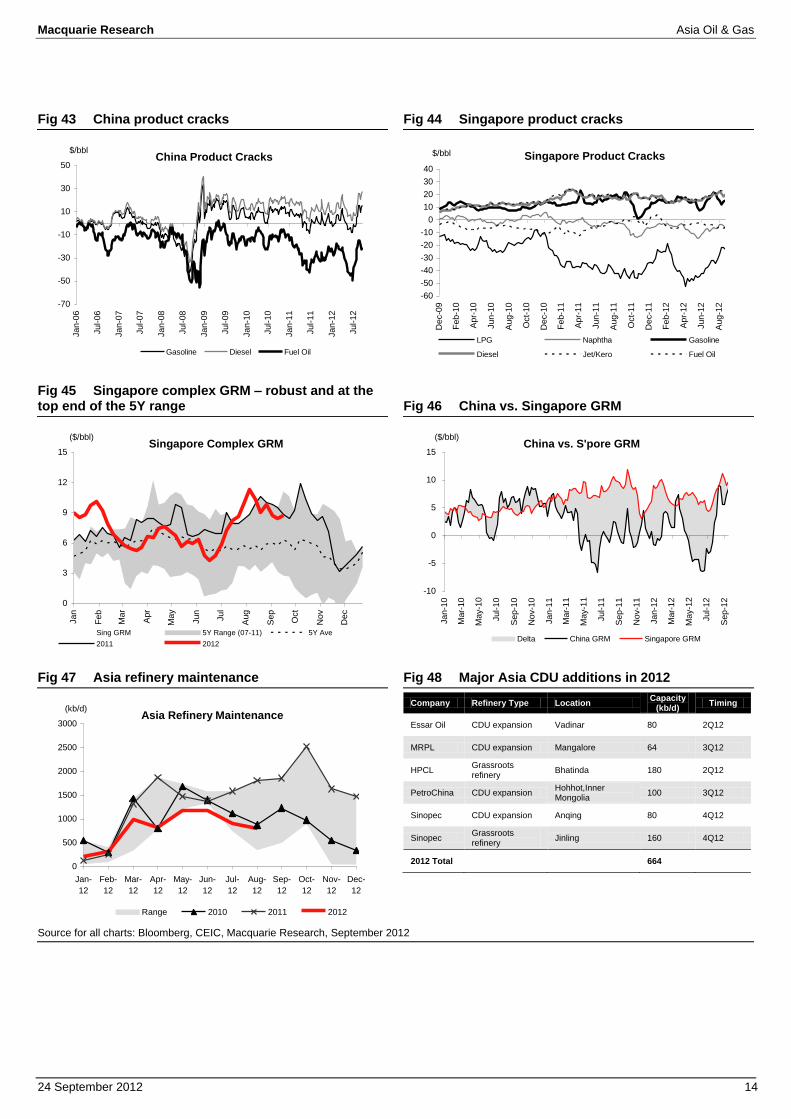

Asia Refining Margins & Cracks

Fig 37 China GRM’s – underlying spot margins turn above EBIT breakeven

Fig 38 MacQ China GRM vs. Sinopec GRM

Fig 39 China regulated ex-factory product price vs. Dubai

Fig 40 Diesel Price: China ex-factory vs. Singapore

Fig 41 China vs. S’pore gasoline price Fig 42 China fuel oil well below Singapore

Source for all charts: Bloomberg, CEIC, Macquarie Research, September 2012

MacQ China GRM

-20.0

-12.0

-4.0

4.0

12.0

20.0

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

($/bbl)

MQ China GRM 5Y Range 5Y Ave

2011 2012 Fwd Margin

MacQ China GRM vs Sinopec Reported

-1200

-800

-400

0

400

800

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

Rmb/t

MQ China GRM Sinopec Reported GRM

Crude vs Regulated Pdt Price

30

60

90

120

150

Jan-0

6

Apr-

06

Jul-06

Oct-

06

Jan-0

7

Apr-

07

Jul-07

Oct-

07

Jan-0

8

Apr-

08

Jul-08

Oct-

08

Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

$/bbl

Gasoline Diesel Fuel Oil Dubai Crude

China (ex-factory) vs S'pore Diesel Prices

30

50

70

90

110

130

150

Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

$/bbl

China Diesel S'pore Diesel (FOB)

China vs S'pore Gasoline Prices

30

50

70

90

110

130

150

Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

$/bbl

China Gasoline S'pore Gasoline (FOB)

China vs S'pore Fuel Oil Prices

0

20

40

60

80

100

120

140

Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

$/bbl

China Fuel Oil S'pore Fuel Oil (FOB)

Macquarie Research Asia Oil & Gas

24 September 2012 14

Fig 43 China product cracks Fig 44 Singapore product cracks

Fig 45 Singapore complex GRM – robust and at the top end of the 5Y range

Fig 46 China vs. Singapore GRM

Fig 47 Asia refinery maintenance Fig 48 Major Asia CDU additions in 2012

Company Refinery Type Location Capacity

(kb/d) Timing

Essar Oil CDU expansion Vadinar 80 2Q12

MRPL CDU expansion Mangalore 64 3Q12

HPCL Grassroots refinery

Bhatinda 180 2Q12

PetroChina CDU expansion Hohhot,Inner Mongolia

100 3Q12

Sinopec CDU expansion Anqing 80 4Q12

Sinopec Grassroots refinery

Jinling 160 4Q12

2012 Total 664

Source for all charts: Bloomberg, CEIC, Macquarie Research, September 2012

China Product Cracks

-70

-50

-30

-10

10

30

50

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Jan-0

8

Jul-08

Jan-0

9

Jul-09

Jan-1

0

Jul-10

Jan-1

1

Jul-11

Jan-1

2

Jul-12

$/bbl

Gasoline Diesel Fuel Oil

Singapore Product Cracks

-60

-50

-40

-30

-20

-10

0

10

20

30

40

De

c-0

9

Feb-1

0

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

De

c-1

0

Feb-1

1

Apr-

11

Jun-1

1

Aug-1

1

Oct-

11

De

c-1

1

Feb-1

2

Apr-

12

Jun-1

2

Aug-1

2

$/bbl

LPG Naphtha Gasoline

Diesel Jet/Kero Fuel Oil

Singapore Complex GRM

0

3

6

9

12

15

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

($/bbl)

Sing GRM 5Y Range (07-11) 5Y Ave

2011 2012

China vs. S'pore GRM

-10

-5

0

5

10

15Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep-1

0

No

v-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

Sep-1

1

No

v-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

Sep-1

2

($/bbl)

Delta China GRM Singapore GRM

Asia Refinery Maintenance

0

500

1000

1500

2000

2500

3000

Jan-

12

Feb-

12

Mar-

12

Apr-

12

May-

12

Jun-

12

Jul-

12

Aug-

12

Sep-

12

Oct-

12

Nov-

12

Dec-

12

(kb/d)

Range 2010 2011 2012

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

24 S

ep

tem

ber 2

01

2

15

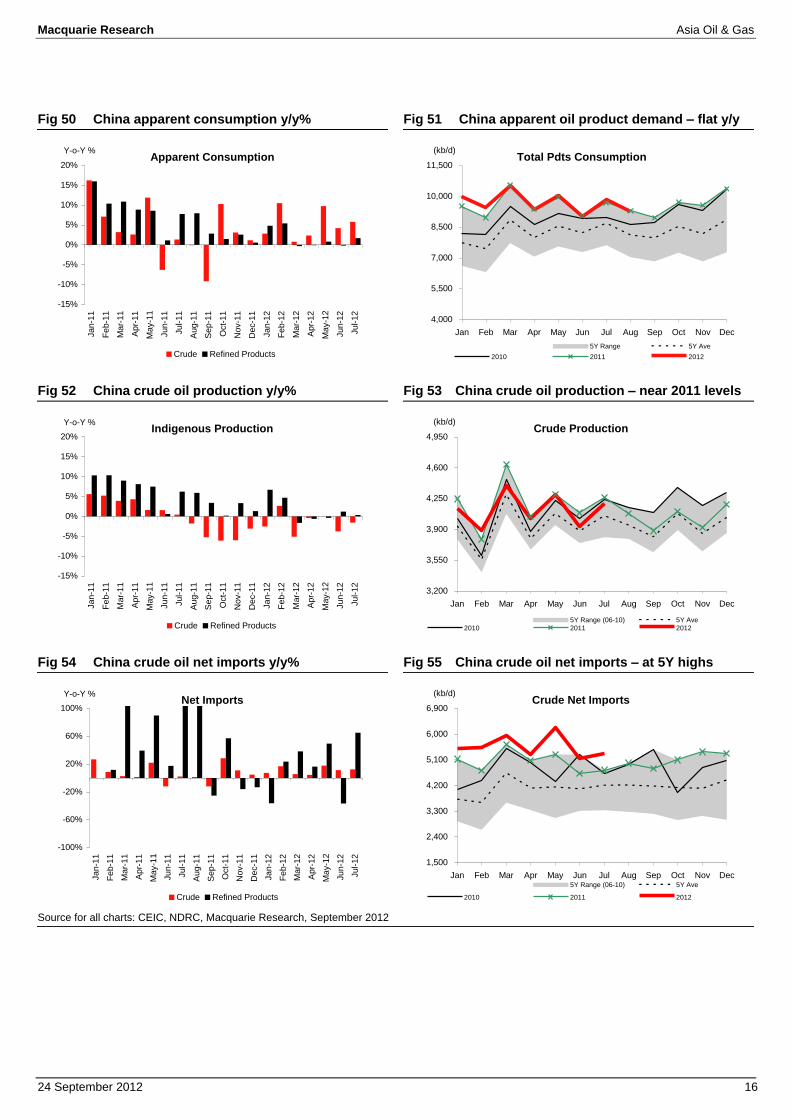

China Oil Demand, Production & Imports Fig 49 China Macro Summary

Source: CEIC, Macquarie Research, September 2012. Note: apparent consumption = production + net imports

Macquarie Research

China Crude & Refined Products Summary

Jul-12 Jun-12 M-o-M % Jul-11 Y-o-Y % 2Q12 1Q12 %chg 2011 2010 %chg

Apparent Consumption (kb/d)

Crude 9,520 9,086 5% 9,000 6% 9,645 9,806 -2% 9,196 8,918 3%

Total Products 9,837 9,011 9% 9,676 1.7% 9,473 9,979 -5% 9,580 9,005 6%

Gasoline 2,075 1,841 13% 1,770 17% 1,901 1,914 -1% 1,792 1,665 8%

Diesel 3,337 3,145 6% 3,394 -2% 3,314 3,438 -4% 3,342 3,113 7%

Kerosene 422 334 27% 341 24% 353 379 -7% 364 349 4%

Fuel Oil 599 544 10% 551 9% 580 650 -11% 604 619 -2%

Lubricants 222 227 -2% 209 7% 242 240 1% 235 232 2%

Naphtha 661 615 8% 588 13% 673 718 -6% 601 611 -2%

LPG 778 767 1% 763 2% 731 739 -1% 745 702 6%

Petcoke 899 824 9% 724 24% 814 781 4% 728 716 2%

Natural Gas (bcm) 11.3 11.1 2% 10.8 5% 33.6 41.0 -18% 128.9 105.9 22%

Production (kb/d)

Crude 4,194 3,933 7% 4,261 -2% 4,085 4,144 -1% 4,128 4,131 0%

Total Products 9,503 8,800 8% 9,474 0% 9,175 9,583 -4% 9,273 8,797 5%

Gasoline 2,112 1,913 10% 1,856 14% 1,951 2,009 -3% 1,886 1,785 6%

Diesel 3,372 3,139 7% 3,400 -1% 3,314 3,433 -3% 3,334 3,170 5%

Kerosene 415 386 8% 395 5% 403 409 -2% 373 341 9%

Fuel Oil 341 322 6% 319 7% 312 317 -2% 342 381 -10%

Lubricants 191 191 0% 177 8% 200 198 1% 194 190 2%

Naphtha 598 591 1% 549 9% 638 639 0% 556 565 -2%

LPG 692 672 3% 699 -1% 677 716 -5% 695 656 6%

Petcoke 712 684 4% 654 9% 695 650 7% 640 614 4%

Natural Gas (bcm) 8.3 8.2 1% 8.4 -1% 25.0 33.2 -25% 103.3 93.6 10%

Net Imports (kb/d)

Crude 5,326 5,153 3% 4,738 12% 5,560 5,663 -2% 5,067 4,786 6%

Total Products 334 210 59% 202 65% 298 396 -25% 308 207 48%

Gasoline (36) (72) NM (86) NM (49) (96) 94% (94) (121) 29%

Diesel (35) 6 NM (5) -85% 0 5 -98% 8 (57) NM

Kerosene 7 (52) NM (54) NM (49) (29) -40% (9) 8 NM

Fuel Oil 258 222 17% 232 11% 268 332 -19% 262 238 10%

Lubricants 31 35 -12% 32 -1% 43 42 3% 41 42 -1%

Naphtha 64 24 NM 39 NM 34 79 -57% 44 46 -4%

LPG 86 94 -9% 64 33% 54 23 NM 50 46 8%

Petcoke 187 139 34% 70 NM 119 131 -9% 88 103 -14%

LNG (bcm) 1.8 1.6 10% 1.6 13% 4.6 4.4 4% 16.6 12.7 31%

Pipe Gas (bcm) 1.3 1.3 0% 0.8 56% 4.0 3.3 21% 8.9 (0.4) NM

Month Quarter Year

Macquarie Research Asia Oil & Gas

24 September 2012 16

Fig 50 China apparent consumption y/y% Fig 51 China apparent oil product demand – flat y/y

Fig 52 China crude oil production y/y% Fig 53 China crude oil production – near 2011 levels

Fig 54 China crude oil net imports y/y% Fig 55 China crude oil net imports – at 5Y highs

Source for all charts: CEIC, NDRC, Macquarie Research, September 2012

Apparent Consumption

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

Nov-1

1

Dec-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Y-o-Y %

Crude Refined Products

Total Pdts Consumption

4,000

5,500

7,000

8,500

10,000

11,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(kb/d)

5Y Range 5Y Ave

2010 2011 2012

Indigenous Production

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

Nov-1

1

Dec-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Y-o-Y %

Crude Refined Products

Crude Production

3,200

3,550

3,900

4,250

4,600

4,950

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(kb/d)

5Y Range (06-10) 5Y Ave

2010 2011 2012

Net Imports

-100%

-60%

-20%

20%

60%

100%

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

Nov-1

1

Dec-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Y-o-Y %

Crude Refined Products

Crude Net Imports

1,500

2,400

3,300

4,200

5,100

6,000

6,900

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(kb/d)

5Y Range (06-10) 5Y Ave

2010 2011 2012

Macquarie Research Asia Oil & Gas

24 September 2012 17

Fig 56 China diesel apparent consumption y/y%

Fig 57 China diesel consumption – top end; but flat y/y

Fig 58 China gasoline apparent consumption y/y%

Fig 59 China gasoline consumption – the lonely bright spot

Fig 60 China fuel oil apparent consumption y/y% Fig 61 China fuel oil consumption – near 5Y lows

Source for all charts: CEIC, NDRC, Macquarie Research, September 2012

Diesel Apparent Consumption

-5%

0%

5%

10%

15%

20%

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Y-o-Y %Diesel Consumption

1,800

2,200

2,600

3,000

3,400

3,800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(kb/d)

5Y Range 5Y Ave

2010 2011 2012

Gasoline Apparent Consumption

-5%

0%

5%

10%

15%

20%

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Y-o-Y %Gasoline Consumption

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(kb/d)

5Y Range 5Y Ave.

2010 2011 2012

Fuel Oil Apparent Consumption

-35%

-20%

-5%

10%

25%

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Y-o-Y %Fuel Oil Consumption

-

250

500

750

1,000

1,250

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(kb/d)

5Y Range 5Y Ave

2010 2011 2012

Macquarie Research Asia Oil & Gas

24 September 2012 18

Fig 62 China crude inventories Fig 63 China diesel inventories

Fig 64 China gasoline inventories Fig 65 China kerosene inventories

Source for all charts: CEIC, NDRC, Macquarie Research, September 2012

China Crude Oil Inventory

25.0

26.0

27.0

28.0

29.0

30.0

31.0

32.0

33.0

Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

Nov-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

Nov-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Aug-1

2

(mt)

China Diesel Inventory

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

No

v-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

No

v-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Aug-1

2

(mt)

China Gasoline Inventory

5.0

5.5

6.0

6.5

7.0

7.5

Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

No

v-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

No

v-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Aug-1

2

(mt)China Kerosene Inventory

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

Nov-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

Nov-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Aug-1

2

(mt)

Macquarie Research Asia Oil & Gas

24 September 2012 19

China Gas Demand, Production & Imports

Fig 66 China gas apparent consumption y/y%

Fig 67 China natural gas apparent consumption – 2012-TD up 17% y/y; despite the slowdown in 2Q

Fig 68 China natural gas production y/y%

Fig 69 China natural gas production – remains flat for a fourth consecutive month

Fig 70 China natural gas net imports (pipe + LNG) y/y%

Fig 71 China natural gas net imports (pipe + LNG) – at record highs on Turkmen vols + imported LNG

Source for all charts: CEIC, NDRC, Macquarie Research, September 2012

Gas Apparent Consumption

0%

5%

10%

15%

20%

25%

30%

35%

40%

Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

Nov-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

Nov-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Y-o-Y %Gas Apparent Consumption

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(bcm)

5Y Range 5Y Ave

2010 2011 2012

Gas Indigenous Production

-5%

0%

5%

10%

15%

20%

25%

30%

Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

Nov-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

Nov-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Y-o-Y %Gas Indigenous Production

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(bcm)

5Y Range 5Y Ave

2010 2011 2012

Gas Imports (pipe + LNG)

0%

50%

100%

150%

200%

250%

Jan-1

0F

eb-1

0M

ar-

10

Apr-

10

May-1

0Jun-1

0Jul-10

Aug-1

0S

ep-1

0O

ct-

10

Nov-1

0D

ec-1

0Jan-1

1F

eb-1

1M

ar-

11

Apr-

11

May-1

1Jun-1

1Jul-11

Aug-1

1S

ep-1

1O

ct-

11

Nov-1

1D

ec-1

1Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2Jul-12

Y-o-Y %Gas Imports (pipe + LNG)

(0.5)

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

(bcm)

5Y Range 5Y Ave

2010 2011 2012

Macquarie Research Asia Oil & Gas

24 September 2012 20

Singapore Oil Product Inventories

Fig 72 S’pore total oil product inventory – near the 5Y average

Fig 73 S’pore middle distillate inventory – bottom end

Fig 74 S’pore light distillate inventory – back below the 5Y average

Fig 75 S’pore fuel oil inventory – above the 5Y average

Source for all charts: Bloomberg, Macquarie Research, September 2012

S'pore Total Oil Inventories

10,000

18,000

26,000

34,000

42,000

50,000

58,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb)

Sing Total Oil Inv 5Y Range 5Y Ave

2010 2011 2012

S'pore Middle Distillate Inventories

3,000

6,000

9,000

12,000

15,000

18,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

(kb)

Sing MD Inv 5Y Range 5Y Ave

2010 2011 2012

S'pore Light Distillate Inventories

5,000

6,500

8,000

9,500

11,000

12,500

14,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb)

Sing LD Inv 5Y Range 5Y Ave

2010 2011 2012

S'pore Fuel Oil Inventories

5,000

10,000

15,000

20,000

25,000

30,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

(kb)

Sing FO Inv 5Y Range 5Y Ave

2010 2011 2012

Macquarie Research Asia Oil & Gas

24 September 2012 21

US Oil Demand & Inventories

Fig 76 US total product dmd – at 5Y lows Fig 77 US crude inventories – at historic highs

Fig 78 US diesel demand – near the 5Y average Fig 79 US diesel inventories – bottom end

Fig 80 US gasoline demand Fig 81 US gasoline inventories

Source for all charts: EIA, Macquarie Research, September 2012

US Total Product Demand

16,000

17,400

18,800

20,200

21,600

23,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb/d)

US Total Pdt Dmd 5Y range 5Y ave.

2010 2011 2012

US crude inventories (ex SPR)

240,000

270,000

300,000

330,000

360,000

390,000

420,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb)

US Crude Inv 5Y Range 5Y Ave

2010 2011 2012

US Distillate Demand

2,500

3,000

3,500

4,000

4,500

5,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb/d)

US Distillate Dmd 5Y Range 5Y ave.

2010 2011 2012

US Distillate Inventories

80,000

104,000

128,000

152,000

176,000

200,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb)

US Dist Inv 5Y Range 5Y Ave.

2010 2011 2012

US Gasoline Demand

7,800

8,300

8,800

9,300

9,800

10,300

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb/d)

US Gasoline Dmd 5Y Range 5Y ave.

2010 2011 2012

US Gasoline Inventories

150,000

172,000

194,000

216,000

238,000

260,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

No

v

De

c

(kb)

US Gaso Inv 5Y Range 5Y Ave

2010 2011 2012

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

24 S

epte

mb

er 2

01

2

22

Global Oil & Gas Comparables Valuation

Fig 82 Global Oil and Gas Comparables Valuation

Source: Bloomberg, Macquarie Research, September 2012. Note: Averages are calculated on a market cap weighted basis.

Macquarie Research

Global Oil & Gas Sector - Valuation, Performance and Operational Metrics

Company Local Price Mcap Reco.Price

TargetUpside

Curr (local) (US$ bn) (local) 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E

Exxon USD 91.9 424.3 Outperform 97.0 +6% 4.2 x 4.4 x 12.2 x 11.0 x 2.3 x 2.1 x 2.4% 2.5% 5.9% 4.6% 19.3% 19.4% 0.9% 3.4%

RD Shell GBp 2,202 133.8 Outperform 2,550 +16% 4.6 x 3.3 x 8.2 x 7.0 x 1.2 x 1.1 x 4.8% 4.9% 10.4% 13.3% 13.1% 14.5% 7.9% 4.5%

BP GBp 441 136.5 Outperform 570 +29% 5.2 x 3.7 x 8.0 x 6.4 x 1.3 x 1.1 x 4.6% 5.1% 1.0% 9.1% 11.7% 13.6% 23.7% 18.5%

Chevron USD 117.8 231.1 Outperform 123.0 +4% 3.6 x 3.4 x 9.1 x 9.1 x 1.6 x 1.5 x 3.0% 3.2% 3.9% 2.7% 17.9% 16.1% -6.2% -2.0%

TOTAL EUR 40.8 125.3 Neutral 42.0 +3% 3.4 x 3.3 x 8.5 x 8.5 x 1.2 x 1.2 x 5.7% 5.7% 2.1% 3.8% 11.2% 10.6% 18.4% 18.8%

Conoco USD 57.4 69.7 Neutral 55.0 -4% 3.7 x 3.8 x 10.1 x 10.7 x 1.0 x 0.9 x 4.6% 4.6% -3.3% -0.1% 8.4% 7.4% 16.0% 18.1%

Eni EUR 18.6 87.6 Neutral 19.0 +2% 3.1 x 2.9 x 8.7 x 8.0 x 0.9 x 0.9 x 5.8% 5.9% 5.0% 8.1% 12.9% 11.8% -2.0% -5.0%

Statoil NOK 153.3 85.2 Neutral 160.0 +4% 4.1 x 4.7 x 9.4 x 9.6 x 1.5 x 1.3 x 4.2% 4.5% 1.3% 4.5% 12.0% 11.1% 8.3% 7.4%

BG Group GBp 1,246 68.9 Outperform 1,950 +57% 7.3 x 5.3 x 14.9 x 12.2 x 2.1 x 1.8 x 1.3% 1.4% -5.5% -2.5% 10.3% 11.1% 22.1% 23.5%

Occidental USD 87.4 70.8 Outperform 137.0 +57% 5.2 x 4.4 x 12.4 x 10.1 x 1.7 x 1.5 x 2.4% 2.7% 1.1% 4.6% 12.6% 14.1% 8.6% 5.2%

Repsol EUR 16.3 26.6 Underperform 13.5 -17% 5.0 x 4.7 x 10.4 x 10.0 x 0.7 x 0.6 x 4.0% 4.3% 0.6% 5.1% 6.5% 6.0% 33.3% 30.2%

Marathon Oil USD 30.8 21.7 Neutral 34.0 +10% 3.2 x 3.0 x 12.0 x 8.8 x 1.1 x 1.0 x 2.2% 2.3% -0.5% 3.7% 8.0% 9.4% 23.1% 20.1%

Galp EUR 13.0 14.0 Outperform 16.0 +23% 9.6 x 7.5 x 29.1 x 21.2 x 1.9 x 1.8 x 1.8% 2.2% -6.8% -3.3% 6.6% 6.2% -9.9% -2.2%

OMV EUR 28.1 11.9 Neutral 26.5 -6% 3.4 x 3.4 x 6.1 x 6.0 x 0.7 x 0.6 x 3.9% 3.9% 7.1% 6.9% 10.1% 9.2% 10.2% 7.9%

PetroChina HKD 10.0 240.3 Outperform 12.0 +20% 5.3 x 5.0 x 10.8 x 8.7 x 1.3 x 1.2 x 3.9% 4.8% -8.9% 4.3% 10.2% 10.6% 27.0% 26.0%

Sinopec HKD 7.1 80.3 Neutral 7.1 +1% 4.1 x 3.2 x 9.2 x 6.5 x 1.0 x 0.9 x 2.7% 3.8% -9.0% 4.8% 9.5% 11.7% 28.1% 26.2%

CNOOC HKD 15.7 90.6 Outperform 21.0 +33% 4.4 x 4.1 x 8.0 x 7.6 x 1.7 x 1.5 x 2.0% 3.1% 3.7% 4.0% 20.4% 18.3% 8.6% 5.5%

RIL INR 850 51.4 Neutral 759 -11% 7.9 x 7.5 x 11.8 x 11.7 x 1.4 x 1.3 x 1.1% 1.1% 18.1% 1.5% 9.7% 9.3% 19.8% 16.2%

ONGC INR 294.5 46.9 Outperform 325.0 +10% 3.8 x 4.4 x 9.5 x 9.6 x 2.0 x 1.9 x 3.3% 3.4% 6.2% 5.7% 19.9% 18.5% -16.2% -18.1%

Woodside AUD 33.8 29.5 Neutral 37.5 +11% 8.2 x 7.1 x 16.5 x 15.5 x 2.0 x 1.9 x 3.7% 4.1% 5.5% 10.0% 9.8% 10.1% 12.4% 5.6%

Petrobras* BRL 22.7 149.1 Not Rated NM NM 6.4 x 6.1 x 9.3 x 7.8 x 0.7 x 0.7 x

Rosneft* USD 6.7 70.8 Not Rated NM NM 4.6 x 4.6 x 6.6 x 6.6 x 0.9 x 0.8 x

Big Four 925.7 +10.2% 4.4 x 3.7 x 9.4 x 8.4 x 1.6 x 1.5 x 3.7% 3.9% 5.3% 7.4% 15.5% 15.9% 6.6% 6.1%

Europe 689.9 +15.6% 5.1 x 4.3 x 11.5 x 9.8 x 1.3 x 1.2 x 4.0% 4.2% 1.7% 5.0% 10.5% 10.5% 12.5% 11.5%

US 817.6 +9.0% 4.0 x 3.8 x 11.2 x 9.9 x 1.6 x 1.4 x 2.9% 3.1% 1.4% 3.1% 13.3% 13.3% 8.5% 9.0%

APAC & EM 758.9 +15.0% 5.6 x 5.3 x 10.2 x 9.3 x 1.4 x 1.3 x 2.8% 3.4% 2.6% 5.1% 13.2% 13.1% 13.3% 10.2%

Global 2,266.4 +13.0% 5.0 x 4.5 x 10.9 x 9.7 x 1.4 x 1.3 x 3.4% 3.7% 1.9% 4.5% 12.0% 11.9% 11.7% 10.5%

Gearing

21 September 12

EV/EBITDA Ratio P/E Ratio P/B Ratio Dividend Yield FCF Yield ROACE

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

24 S

epte

mb

er 2

01

2

23

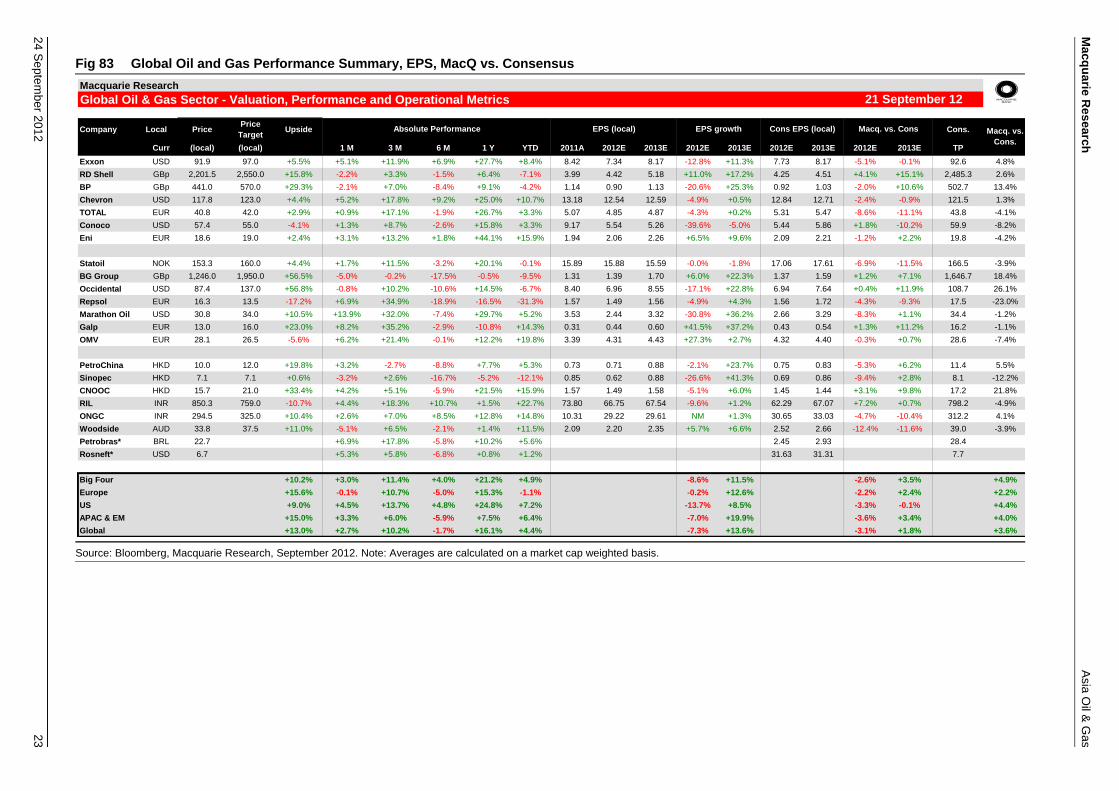

Fig 83 Global Oil and Gas Performance Summary, EPS, MacQ vs. Consensus

Source: Bloomberg, Macquarie Research, September 2012. Note: Averages are calculated on a market cap weighted basis.

Macquarie Research

Global Oil & Gas Sector - Valuation, Performance and Operational Metrics

Company Local PricePrice

TargetUpside Cons.

Curr (local) (local) 1 M 3 M 6 M 1 Y YTD 2011A 2012E 2013E 2012E 2013E 2012E 2013E 2012E 2013E TP

Exxon USD 91.9 97.0 +5.5% +5.1% +11.9% +6.9% +27.7% +8.4% 8.42 7.34 8.17 -12.8% +11.3% 7.73 8.17 -5.1% -0.1% 92.6 4.8%

RD Shell GBp 2,201.5 2,550.0 +15.8% -2.2% +3.3% -1.5% +6.4% -7.1% 3.99 4.42 5.18 +11.0% +17.2% 4.25 4.51 +4.1% +15.1% 2,485.3 2.6%

BP GBp 441.0 570.0 +29.3% -2.1% +7.0% -8.4% +9.1% -4.2% 1.14 0.90 1.13 -20.6% +25.3% 0.92 1.03 -2.0% +10.6% 502.7 13.4%

Chevron USD 117.8 123.0 +4.4% +5.2% +17.8% +9.2% +25.0% +10.7% 13.18 12.54 12.59 -4.9% +0.5% 12.84 12.71 -2.4% -0.9% 121.5 1.3%

TOTAL EUR 40.8 42.0 +2.9% +0.9% +17.1% -1.9% +26.7% +3.3% 5.07 4.85 4.87 -4.3% +0.2% 5.31 5.47 -8.6% -11.1% 43.8 -4.1%

Conoco USD 57.4 55.0 -4.1% +1.3% +8.7% -2.6% +15.8% +3.3% 9.17 5.54 5.26 -39.6% -5.0% 5.44 5.86 +1.8% -10.2% 59.9 -8.2%

Eni EUR 18.6 19.0 +2.4% +3.1% +13.2% +1.8% +44.1% +15.9% 1.94 2.06 2.26 +6.5% +9.6% 2.09 2.21 -1.2% +2.2% 19.8 -4.2%

Statoil NOK 153.3 160.0 +4.4% +1.7% +11.5% -3.2% +20.1% -0.1% 15.89 15.88 15.59 -0.0% -1.8% 17.06 17.61 -6.9% -11.5% 166.5 -3.9%

BG Group GBp 1,246.0 1,950.0 +56.5% -5.0% -0.2% -17.5% -0.5% -9.5% 1.31 1.39 1.70 +6.0% +22.3% 1.37 1.59 +1.2% +7.1% 1,646.7 18.4%

Occidental USD 87.4 137.0 +56.8% -0.8% +10.2% -10.6% +14.5% -6.7% 8.40 6.96 8.55 -17.1% +22.8% 6.94 7.64 +0.4% +11.9% 108.7 26.1%

Repsol EUR 16.3 13.5 -17.2% +6.9% +34.9% -18.9% -16.5% -31.3% 1.57 1.49 1.56 -4.9% +4.3% 1.56 1.72 -4.3% -9.3% 17.5 -23.0%

Marathon Oil USD 30.8 34.0 +10.5% +13.9% +32.0% -7.4% +29.7% +5.2% 3.53 2.44 3.32 -30.8% +36.2% 2.66 3.29 -8.3% +1.1% 34.4 -1.2%

Galp EUR 13.0 16.0 +23.0% +8.2% +35.2% -2.9% -10.8% +14.3% 0.31 0.44 0.60 +41.5% +37.2% 0.43 0.54 +1.3% +11.2% 16.2 -1.1%

OMV EUR 28.1 26.5 -5.6% +6.2% +21.4% -0.1% +12.2% +19.8% 3.39 4.31 4.43 +27.3% +2.7% 4.32 4.40 -0.3% +0.7% 28.6 -7.4%

PetroChina HKD 10.0 12.0 +19.8% +3.2% -2.7% -8.8% +7.7% +5.3% 0.73 0.71 0.88 -2.1% +23.7% 0.75 0.83 -5.3% +6.2% 11.4 5.5%

Sinopec HKD 7.1 7.1 +0.6% -3.2% +2.6% -16.7% -5.2% -12.1% 0.85 0.62 0.88 -26.6% +41.3% 0.69 0.86 -9.4% +2.8% 8.1 -12.2%

CNOOC HKD 15.7 21.0 +33.4% +4.2% +5.1% -5.9% +21.5% +15.9% 1.57 1.49 1.58 -5.1% +6.0% 1.45 1.44 +3.1% +9.8% 17.2 21.8%

RIL INR 850.3 759.0 -10.7% +4.4% +18.3% +10.7% +1.5% +22.7% 73.80 66.75 67.54 -9.6% +1.2% 62.29 67.07 +7.2% +0.7% 798.2 -4.9%

ONGC INR 294.5 325.0 +10.4% +2.6% +7.0% +8.5% +12.8% +14.8% 10.31 29.22 29.61 NM +1.3% 30.65 33.03 -4.7% -10.4% 312.2 4.1%

Woodside AUD 33.8 37.5 +11.0% -5.1% +6.5% -2.1% +1.4% +11.5% 2.09 2.20 2.35 +5.7% +6.6% 2.52 2.66 -12.4% -11.6% 39.0 -3.9%

Petrobras* BRL 22.7 +6.9% +17.8% -5.8% +10.2% +5.6% 2.45 2.93 28.4

Rosneft* USD 6.7 +5.3% +5.8% -6.8% +0.8% +1.2% 31.63 31.31 7.7

Big Four +10.2% +3.0% +11.4% +4.0% +21.2% +4.9% -8.6% +11.5% -2.6% +3.5% +4.9%

Europe +15.6% -0.1% +10.7% -5.0% +15.3% -1.1% -0.2% +12.6% -2.2% +2.4% +2.2%

US +9.0% +4.5% +13.7% +4.8% +24.8% +7.2% -13.7% +8.5% -3.3% -0.1% +4.4%

APAC & EM +15.0% +3.3% +6.0% -5.9% +7.5% +6.4% -7.0% +19.9% -3.6% +3.4% +4.0%

Global +13.0% +2.7% +10.2% -1.7% +16.1% +4.4% -7.3% +13.6% -3.1% +1.8% +3.6%

Absolute Performance EPS (local) Macq. vs.

Cons.

Macq. vs. ConsEPS growth Cons EPS (local)

21 September 12

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

24 S

epte

mb

er 2

01

2

24

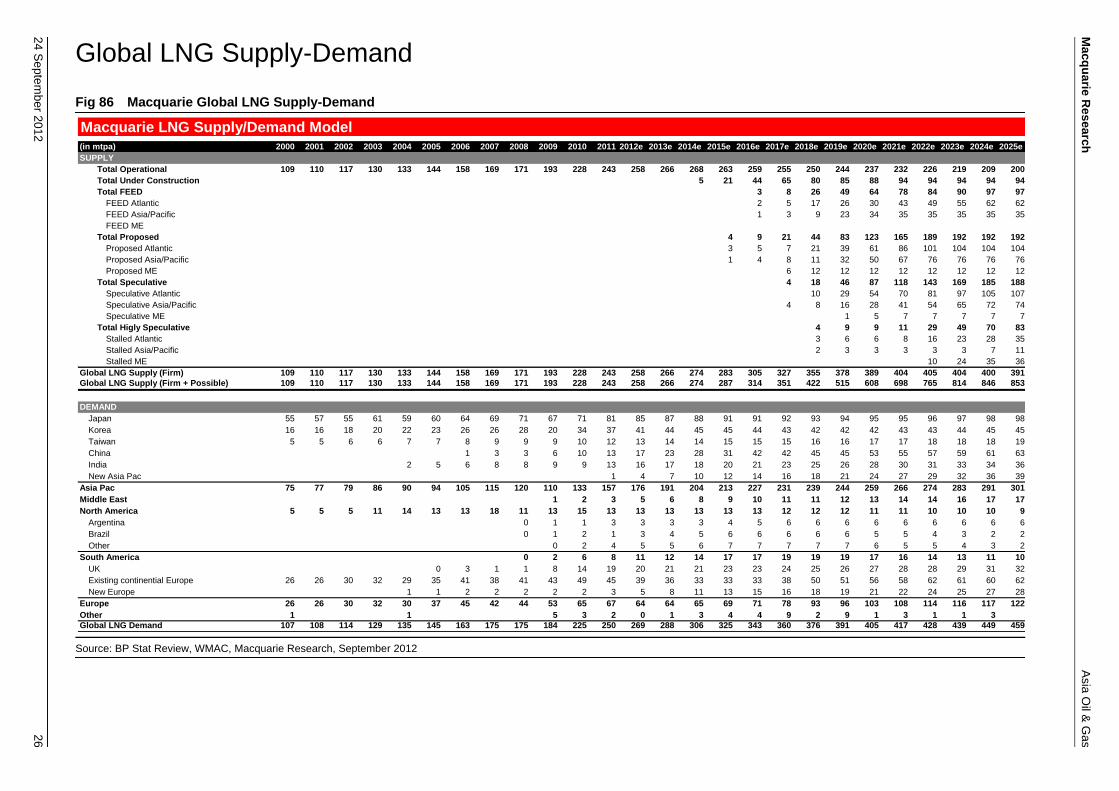

Global Oil Supply-Demand

Fig 84 Macquarie Oil Demand-Supply Model

Source: IEA, BP Stat Review, JODI, Macquarie Research, September 2012

Macquarie Research

Global Oil Supply-Demand

(mb/d) 2009 2010 2011e 2012e 2013e 2014e 2015e 2016e 2017e

North America 23.3 23.8 23.5 23.3 23.0 23.0 23.1 23.1 23.0

Europe 14.7 14.6 14.4 14.1 14.1 14.2 14.2 14.5 14.7

OECD APAC 7.7 7.8 7.9 8.0 8.0 8.1 8.2 8.2 8.1

OECD 45.6 46.1 45.8 45.3 45.2 45.3 45.5 45.8 45.9

Non-OECD Europe 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7

Non-OECD APAC 10.1 10.4 10.7 10.8 10.9 11.0 11.1 11.2 11.1

FSU 4.2 4.5 4.7 4.8 5.0 5.2 5.4 5.6 5.8

China 8.1 9.1 9.5 10.1 10.7 11.3 12.0 12.5 13.1

Latin America 6.0 6.3 6.5 6.7 6.9 7.0 7.2 7.4 7.6

Africa 3.3 3.4 3.4 3.5 3.7 3.9 4.1 4.3 4.5

Middle East 7.5 7.8 7.9 8.3 8.6 9.0 9.4 9.8 10.2

Non-OECD 39.9 42.1 43.4 44.9 46.5 48.2 49.9 51.6 53.1

Total Demand 85.6 88.3 89.2 90.3 91.7 93.5 95.4 97.3 99.0

North America 13.6 14.1 14.4 14.7 15.2 15.5 16.0 16.3 16.5

Europe 4.5 4.2 3.9 3.9 3.8 3.8 3.8 3.9 3.9

OECD APAC 0.6 0.6 0.5 0.5 0.5 0.5 0.4 0.4 0.4

FSU 13.3 13.5 13.6 13.7 13.8 14.0 14.3 14.3 14.3

Europe 0.1 0.1 0.1 0.1 0.0 0.0 0.0 0.0 0.0

China 3.9 4.1 4.2 4.1 4.1 4.1 4.1 4.1 4.1

Other Asia 3.6 3.7 3.5 3.5 3.4 3.4 3.4 3.4 3.4

Latin America 3.9 4.1 4.2 4.4 4.7 4.9 5.2 5.7 6.1

Middle East 1.7 1.7 1.6 1.6 1.6 1.7 1.7 1.7 1.7

Africa 2.6 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5

Global Biofuels 1.6 1.8 1.9 1.9 1.9 2.0 2.0 2.1 2.1

Processing Gains 2.0 2.1 2.2 2.2 2.2 2.3 2.3 2.3 2.3

Non-OPEC Supply 51.5 52.6 52.7 53.1 53.9 54.7 55.8 56.6 57.3

OPEC crude 29.1 29.5 29.9 30.6 31.3 31.5 31.7 31.7 31.7

OPEC NGLs + non-conventionals 4.9 5.3 5.9 6.2 6.6 6.8 7.1 7.1 7.1

OPEC Supply 34.1 34.8 35.7 36.8 37.8 38.3 38.7 38.7 38.7

Total Supply 85.6 87.4 88.5 89.9 91.7 93.0 94.5 95.3 96.0

Supply-Demand 0.0 -0.8 -0.7 -0.4 0.0 -0.5 -0.9 -2.0 -3.0

Demand Growth (y/y) -1.0 2.7 0.9 1.1 1.4 1.8 1.9 1.9 1.7

Supply Growth (y/y) -1.1 1.9 1.0 1.4 1.8 1.3 1.5 0.8 0.7

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

24 S

epte

mb

er 2

01

2

25

China Gas Supply-Demand

Fig 85 Macquarie China Gas Supply-Demand

Source: CEIC, WMAC, Macquarie Research, September 2012

Macquarie Research

China Gas Supply-Demand

(bcm) 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E2011-

15e

2011-

20e

Demand

Residential 8 10 14 17 18 23 29 34 41 48 56 64 71 78 84 89 18% 13%

Industrial 30 34 40 45 44 49 59 69 80 92 107 116 125 135 146 157 16% 11%

Power Generation 3 4 8 8 13 19 23 27 31 34 38 42 46 49 53 57 13% 11%

Transport (NGVs) 1 1 1 2 3 5 6 7 11 14 19 25 31 40 49 60 33% 29%

Other 5 6 7 9 11 11 12 13 14 15 16 18 19 21 22 24 8% 8%

China Gas Demand 47 56 71 81 90 108 129 150 176 205 237 264 292 323 354 388 16% 13%

y/y% 18% 20% 26% 15% 10% 20% 20% 16% 17% 16% 16% 11% 11% 10% 10% 9%

Supply

Tarim 5 11 14 16 17 17 20 23 26 30 35 40 46 50 54 58

Changqing 7 7 9 11 15 16 18 20 23 26 29 33 38 42 46 51

Sichuan 11 13 14 14 14 14 15 17 18 20 21 23 25 27 29 31

Puguang (Sichuan) 0 0 0 0 0 4 6 9 9 10 12 12 12 12 12 12

Xinjiang 1 1 1 1 2 2 2 3 3 4 4 5 5 6 7 7

E-S China Sea Others 0 0 0 0 1 1 2 2 2 3 3 4 4 4 4 4

Liwan 0 0 0 0 0 0 0 0 0 1 2 2 2 2 2 2

Legacy fields 27 27 31 38 37 43 42 39 41 43 44 45 45 45 45 46

China Indigenous Pdtn 51 59 69 80 85 97 103 110 120 132 145 158 171 181 192 205 9% 8%

y/y% 23% 15% 18% 16% 6% 13% 7% 7% 9% 10% 10% 8% 8% 6% 6% 6%

Turkmenistan 0 0 0 0 0 3 9 20 25 40 40 40 50 60 60 60

Russia/Central Asia 0 0 0 0 0 0 0 0 0 0 0 0 15 22 30 30

Myanmmar 0 0 0 0 0 0 0 4 12 12 12 12 12 12 12 12

China Pipeline Imports 0 0 0 0 0 3 9 24 37 52 52 52 77 94 102 102 55% 31%

y/y% 0% 0% 0% 0% 0% 0% 256% 170% 54% 41% 0% 0% 48% 22% 9% 0%

LNG Imports 0 0 0 0 4 8 17 16 18 20 39 54 45 48 60 81 23% 19%

Contracted LNG 0 1 1 1 3 7 9 20 25 41 41 47 47 46 46 46

Implied Spot LNG 0 0 0 0 1 1 8 0 0 0 0 7 0 1 14 35

LNG imports y/y% 0% 0% 0% 0% NM 96% 103% -6% 16% 10% 95% 37% -17% 7% 27% 35%

China Gas Supply 51 59 69 80 90 108 129 150 176 205 237 264 292 323 354 388 16% 13%

y/y% 23% 15% 18% 16% 11% 20% 20% 16% 17% 16% 16% 11% 11% 10% 10% 9%

Ma

cq

ua

rie R

esea

rch

A

sia

Oil &

Ga

s

24 S

epte

mb

er 2

01

2

26