asia’s infrastructure trends and case study...

TRANSCRIPT

Asia’s infrastructuretrends and Case Studydiscussions

Lee Seng CheePartnerCapital Projects andInfrastructure

October 2014

www.pwc.com

PwC

Contents

Section 1: Asia’s infrastructure trends and the Singapore Journey 3

Section 2: Case Study – Sport and Culture Category 10

Section 3: Case Study – Water Category 19

2

PwC

Section 1

Asia’s infrastructure trends and theSingapore Journey

第5节:案例研究 - 体育及文化类项目3

PwC

Despite clear infrastructure deficits, APAC still under-invests

Infrastructure investment as % of GDP (latest data available)World

3.8USA

2.6Philippines

2.7Indonesia

3.2

India

4.7Japan

5China

8.5Vietnam

10

Under-investingin the future oftheir economies

Source: Economist Intelligence Unit

4

PwC

Infrastructure: growth in spending

555

2.0

2.5

3.0

3.5

4.0

4.5

2006 2007 2008 2009 2010 2011 2012 2013

$ trillions, current prices

Source : Oxford Economics/Haver Analytics

0

1

2

3

4

5

6

7

8

9

10

2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

$ trillions, current prices

Source : Oxford Economics/Haver Analytics

Forecast

• Government is a key driver of all infrastructure spend – public andprivate

PwC

Asia – Infrastructure spend

666

50.1%

17.0%

10.2%

9.7%

5.2%

3.1%

1.3%

3.4%

China

Japan

India

Australia

South Korea

Indonesia

Thailand

Others

Percent of regional infrastructure spend

Source : Oxford Economics/Haver Analytics

•Government across region recognise needfor continued Infra spend.

• US9trn per annum by 2025

• US$78trn between now and 2025Overall, the Asia-Pacific infrastructuremarket will grow by 7% to 8% a year overthe next decade, approaching US$5.3trillion by 2025

•Government requires private sectorfinance and expertise to deliver on theinfrastructure promise

•Private sector capital and capabilitycritical to sustained delivery

11.1%8.5%

19.7% 22.6%

23.8% 25.6%

34.7% 30.4%

10.6% 12.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2025

Extraction

Utilities

Manufacturing

Transport andComms

Social

Percent of total infrastructure investment

Source : Oxford Economics/Haver Analytics

PwC 7

The Asian Infrastructure Gap: Forecast (2009)

7

Infrastructure Deficitof US$8 trillion (2010-2020)

Sectors Amt (US$ trn)

Telecom 1.1

Power 4.1

Transport 2.5

- Rail 0.04

- Road 2.3

- Others 0.09

Water &Sanitation

0.4

Total 8.0

Source: ADBi (2009),Bhattacharya (2008)

Investment Barrier

• Poor project preparation

• Legal & Regulatory Framework

• Poorly Defined and UnstructuredProcurement Processes

• Haphazard Pipeline Management

• Risk Allocation and CommercialStructure – imbalanced risks vsreward

• Lack of Capacity

• Political risks – stability and cycles

• Lack of investment subsidy incertain jurisdictions

Supply of Capital

• Government

• Multi-laterals

• Commercial lending

• Private sector(15-30%, Indonesia-65%)

– Infrastructurefunds

– Pension funds

– Strategic investors

o Constructors

o Operators

• Others

7

PwC 8

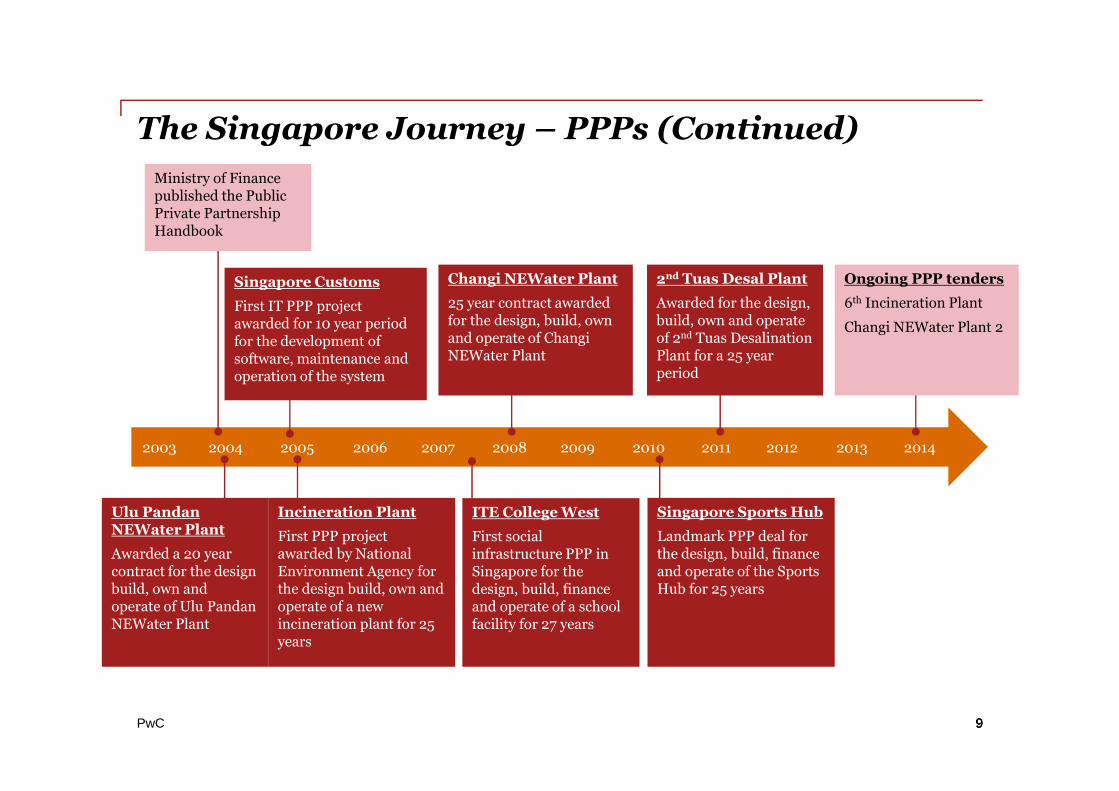

The Singapore Journey - PPPs

88

• First PPP handbook issued by theMinistry of Finance (Singapore) inOct 2004

• Provided guidance to allimplementing governmentagencies

• Introduction to PPP – settingout the rationale

• Structuring a PPP deal• PPP Procurement Process• Managing a PPP – critical

success factors

• Promoted the use of PPP for allprojects above S$50m

PwC 9

The Singapore Journey – PPPs (Continued)

99

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Incineration Plant

First PPP projectawarded by NationalEnvironment Agency forthe design build, own andoperate of a newincineration plant for 25years

Singapore Customs

First IT PPP projectawarded for 10 year periodfor the development ofsoftware, maintenance andoperation of the system

Changi NEWater Plant

25 year contract awardedfor the design, build, ownand operate of ChangiNEWater Plant

2nd Tuas Desal Plant

Awarded for the design,build, own and operateof 2nd Tuas DesalinationPlant for a 25 yearperiod

Ministry of Financepublished the PublicPrivate PartnershipHandbook

Ongoing PPP tenders

6th Incineration Plant

Changi NEWater Plant 2

Ulu PandanNEWater Plant

Awarded a 20 yearcontract for the designbuild, own andoperate of Ulu PandanNEWater Plant

ITE College West

First socialinfrastructure PPP inSingapore for thedesign, build, financeand operate of a schoolfacility for 27 years

Singapore Sports Hub

Landmark PPP deal forthe design, build, financeand operate of the SportsHub for 25 years

2003 2004

PwC

PPP – Common Sectors (globally)

10

Sectors of Expertise – Across the PPP and Deals Advisory space

Water Power & Energy Transport Housing

Water treatment

Waste water

Desalination

Inside the fence

IPPs/PPA projects

Merchant plants

Inside the fence

District heating

Oil & Gas

•Light rail

•Roads

•Bridges

•Rail

•Airports

•Ports

Low income

Affordable

Defence accommodations

Healthcare Education Prison Other Sectors

New facilities

Refurbishment

Facilities management

New facilities

Refurbishment

Facilities management

New facilities

Refurbishment

Facilities management

Sports Infrastructure

Properties and Real Estate

PwC

Section 2

Case Study – Sport and Culture Category

第5节:案例研究 - 体育及文化类项目11

PwC

Case Study – Sports and Culture CategorySingapore Sports Hub

Project Brief

The project cost of the Singapore Sports Hub was

c.S$1.8billion, making it the largest sports PPP project in the

world. The project included the construction of a national

sports stadium with capacity of 55,000, swimming complex

with capacity of 6,000, aqua centre, a 41,000 square meter

business development park, taking over the Singapore Indoor

Stadium constructed in 1989, and other supporting facilities.

PPP Project Company is responsible for the design,

construction, financing, operations and maintenance of the

Singapore Sports Hub, concession length 25 years. PPP

Project Company will create a multi purpose sports,

recreation and lifestyle location to attract internationally

renowned sports events and performances from all over the

world.

PwC acted as the lead financial advisor to the government,

and led other legal, technical and operational consultants in

the advisory consortium.

12

PwC

Case Study – Sports and Culture CategorySingapore Sports Hub – 2010 Awards

13

Asia Pacific PPP Deal ofthe Year by《 PFI 》

Deal of the Year – PPPby Infrastructure Journal

《IJ》

Deal of the Year by《Euromoney》

Other awards include:

- Asia Pacific PPP Deal of the Year by《Euromoney》

- Asia Pacific PPP Deal of the Year by 《Infrastructure Investor》

- Financing Deal of the Year by 《The Asset》

- Asia Pacific Financing Deal of the Year by 《Asiamoney》

- Asia Pacific Financing Deal of the Year by 《Euroweek Asia》

- Asia Pacific Leisure Deal of the Year by 《Euromoney》

PwC

Case Study – Sports and Culture CategorySingapore Sports Hub – Vision

14

Fully integrated sports entertainment and lifestyle hub as a landmark

Objectives

1.Integrated Lifestyle Hub forWorld-Class Sports &Entertainment Events

2.Commercially ViableBusiness Model

3.National & GlobalLandmark

1.Thriving sports & entertainmentecosystem

2.Key driver for ‘Sporting Singapore’ vision

3.Platform for business partnerships

4.Preferred sports & entertainmentdestination

5.Urban regenerator of Kallang area

6.Vibrant lifestyle hub with world-classcustomer service

Desired Outcomes

PwC

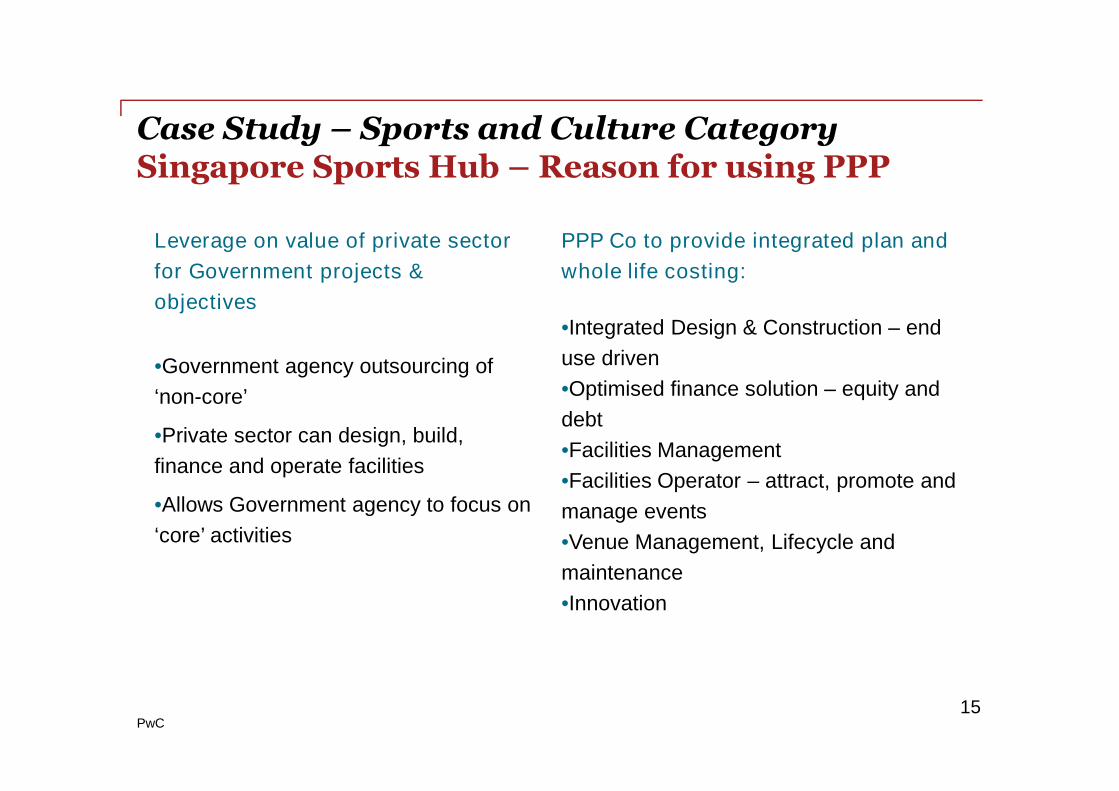

Case Study – Sports and Culture CategorySingapore Sports Hub – Reason for using PPP

15

Leverage on value of private sector

for Government projects &

objectives

•Government agency outsourcing of

‘non-core’

•Private sector can design, build,

finance and operate facilities

•Allows Government agency to focus on

‘core’ activities

PPP Co to provide integrated plan and

whole life costing:

•Integrated Design & Construction – end

use driven

•Optimised finance solution – equity and

debt

•Facilities Management

•Facilities Operator – attract, promote and

manage events

•Venue Management, Lifecycle and

maintenance

•Innovation

PwC

Case Study – Sports and Culture CategorySingapore Sports Hub – Input vs. Output

16

Input Specification

(Technical Brief)

Output Specification

(Performance Brief)

---------------------------------- ----------------------------------Compliance Based

Excludes Innovation

Building focused

Predictable outcomes

“more of the same”

RETAINS design RISK

LIMITS CREATIVITY

Architect/Builder Driven

Strategic Delivery

Performance Based

Encourages Innovation

Business focused

Optimised outcomes

TRANSFERS design RISK

PROMOTES CREATIVITY

End User Driven

E.g. In order to ensure the comfort of thespectators, the national sports stadium shouldhave an ambient temperature maintained at23-25 degrees celsius during operations.

E.g. In order to ensure the comfort of thespectators, the national sports stadium shouldhave 10 large air conditioners per seatingzone.

PwC

Case Study – Sports and Culture CategorySingapore Sports Hub – Evaluation Criteria

17

Appeal of sports,leisure, andentertainmentprogramming

Ability of the Bidder to deliver an appropriateprogramming calendar, including proposedevents programs, facility promotion &community development

40%

Functionality andQuality of Design

Design and technical evaluation, includingprogram, deliverability, functionality andurban integration

25%

Financial and LegalAppeal

Compliance with the PPP Contract drafted bySSC; legal & commercial qualifications;financing of the construction program

25%

Facility ManagementSupport service proposals for themanagement and operation of the facilities

10%

PwC

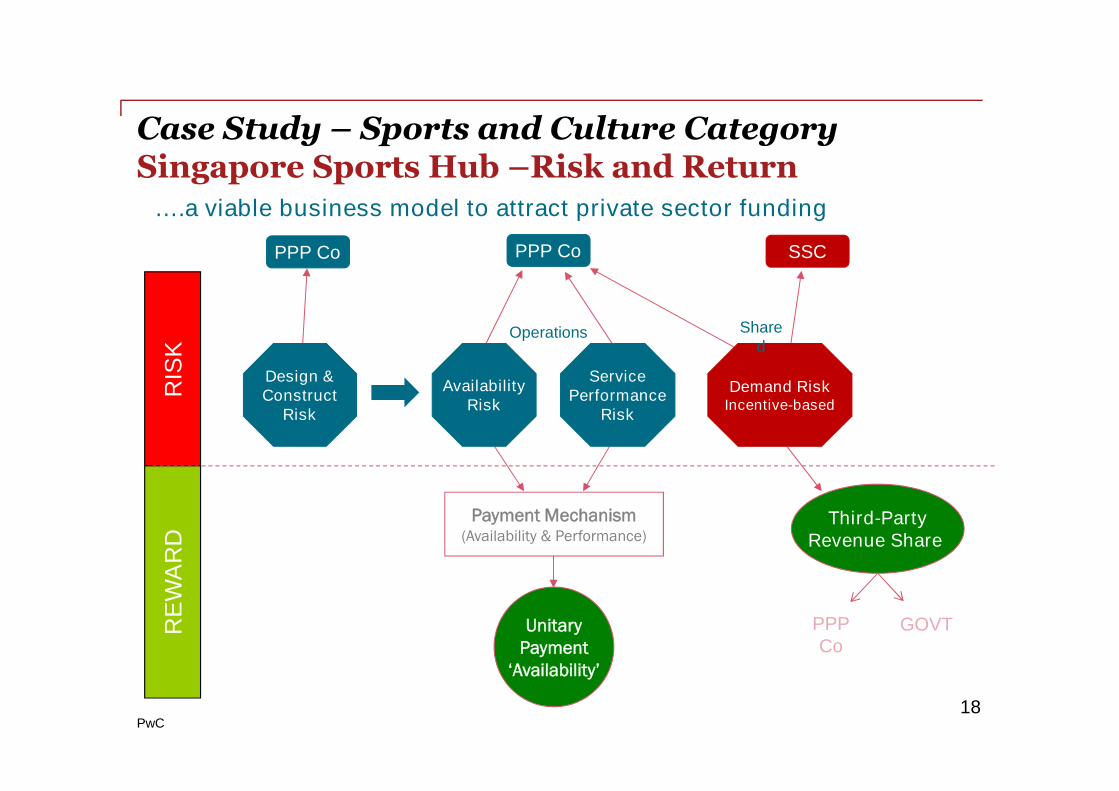

Case Study – Sports and Culture CategorySingapore Sports Hub –Risk and Return

18

….a viable business model to attract private sector funding

RIS

KR

EW

AR

D

SSCPPP Co

UnitaryPayment

‘Availability’

Third-PartyRevenue Share

Payment Mechanism(Availability & Performance)

Demand RiskIncentive-based

Design &Construct

Risk

AvailabilityRisk

ServicePerformance

Risk

Shared

PPP Co

PPPCo

GOVT

Operations

PwC

Case Study – Sports and Culture CategorySingapore Sports Hub – Paymech

19

Revenue

AvailabilityPayment

VariablePayment

Debt service

Capital CostRecoverypayment

Fixed O&MPayment

Variable O&Mpayment

Not linked to usage

Linked to usage

Deductions

3rd party revenue(SSC Share)

3rd PartyRevenue

(Shared withPPP Co)

minus

• 3rd party revenue sharedwith authority

• Incentivise sports events(over leisure events)

Reduced Availability

• Frequency ofoccurrence

• Importance ofperformance indicator

• Severity of performancefailure

ReducedPerformance

• Importance ofperformanceindicator

• Severity ofperformance failure

PwC

Section 3

Case Study – Water Category

20

PwC

New waterplant

New waterplant

PUB

User

Case Study – Water CategorySingapore Water Industry Value Chain

21

plantWaste water

plant

DesalinationPlant

DesalinationPlant

WatersourceWatersource

SP Services

PPP framework

Outsourcingcontract

Meter reading/billing/ collection of

water charges

Payment Bill

Waterprovision

Water provisionnetwork

Water provisionnetwork

PaymentDeductions

Water provision flow

Payment/ cash flow

PwC

Case Study – Water CategorySingapore Water PPP Case Study

Singapore has successfully introduced the private sector in its water

industry

Common BOT structure for water and wastewater treatment- NEWater,

Desal, raw water

Private player is paid through a payment mechanism which has fixed and

variable components. Private player does not take on volume risk on water

consumption level

Public Utilities Board (PUB) is the regulator as well as the off taker

22

The relatively simple and robust structures for these PPPs mean that PUB isable to attract wide interests from the private sector to participate

PwC

Case Study – Water CategorySingapore Changi New Water

• After 3 months of competitivetender, the consortium SembcorpNewater Pte Ltd was selected asPreferred Bidder out of 5 bidders in2008

• Contract term :27 years

• Responsibility of consortium:Design, construct, operate andmaintain Newater Plant, andfinancing for initial design andcapex costs during construction

• Project Cost:SGD 120 million

23

PwC

Case Study – Water CategorySingapore Changi New Water

Commercial Structure

24

Procuring Entity:Public Utilities Board

PPP Project CoSembcorp NEWater

Equity:Sembcorp Utilities

Pte Ltd

Debt: Financingbanks

Design & Construction:Black & Veatch

(Technical Consultant)and other contractors

Operator:Project Co

PwC

Case Study – Water CategorySingapore Changi New Water

• Construction period:PUB does not make payment to PPP Co. PPP Co willneed to finance costs during construction

25

Uses of funds:- Capex

- Design fees- Financing interests

Others

Sources of funds:

- Equity from sponsors- Debt from financiers

Water provision flow

Payment/ cashflow

PUBPUB

Changi NewWater Plant

WaterSource

Water

Network

WaterProvisionNetwork

PPPCo

• Operations period:PUB will make payment PPP Co. in accordance toagreed payment mechanism and price

PwC

Case Study – Water CategorySingapore Changi New Water - Paymech

26

Tariff

Availabilitypayment

Outputpayment

Capital CostRecoveryPayment

Fixed O&MPayment

Fixed PowerPayment

Variable O&MPayment

Variable PowerPayment

Not linked to usage

Linked to usage

ReducedAvailability

Reduced storage

ExcessiveResidual Waste

Deviation fromNEWater Quality

ReportingFailures

ReducedAvailability

ReportingFailures

ReducedAvailability

ReportingFailures

Deductions

PwC

Case Study – Water CategorySingapore Changi New Water - Paymech

27

Capital CostRecovery

Variable powerpayment (indexed)

Variable O&M payment(indexed)

Fixed O&M payment(indexed)

Fixed power payment(indexed/ unindexed)

PwC Contact

Seng-Chee LEE, FCA

李成志

Partner 合伙人

Advisory – Capital Projects &Infrastructure

PricewaterhouseCoopers (Singapore)

Tel: +65 6236 4178 (Direct)

+65 92330780 (Mobile)

Email: [email protected]

LinkedIn: Seng Chee Lee

Seng-Chee Lee is a Partner of PricewaterhouseCoopers (Singapore) and heprovides financial advisory services to support complex transactions inparticular in the Capital & Infrastructure projects

He has more than 17 years of experience in financial structuring , financeraising and M&A activities in both buy and sell side, government and privatesector advisory roles, including expertise in Public Private Partnerships(“PPP”), Private Finance Initiatives (“PFI”) frameworks.

He has advised in the development of a number of milestone infrastructureprojects and transactions in Singapore, Asia and Europe covering sectorsincluding power, water/waste water treatment, transport infrastructure (tollroads, bridges, ports, mass rapid transport, airport etc). Seng-Chee hasworked with many government agencies, major projects finance institutions,infrastructure funds, strategic investors (eg developers) and multilaterals/bilaterals donor agencies on infrastructure development, investments anddivestments.

In Singapore, he has supported many government agencies (includingPublic Utilities Board, Singapore Sports Council, Ministry of Education,Ministry of Trade & Industry, Singapore Cooperation Enterprise, IESingapore) in many projects involving the promotion of Public PrivatePartnership to attract private sector expertise and investments intoSingapore’s public infrastructure. Seng Chee has also advised private sectorconsortiums in selected PPP projects tenders in Singapore includingwastewater, desalination, transportation, and education campus.

Seng Chee graduated from the London School of Economics (UK) and is aFellow of the Institute of Chartered Accountants in England and Wales.

Thank you!

This publication has been prepared for general guidance on matters of interest only, and doesnot constitute professional advice. You should not act upon the information contained in thispublication without obtaining specific professional advice. No representation or warranty(express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers CorporateFinance Pte Ltd, its members, employees and agents do not accept or assume any liability,responsibility or duty of care for any consequences of you or anyone else acting, or refrainingto act, in reliance on the information contained in this publication or for any decision based onit.

© 2013 PricewaterhouseCoopers Corporate Finance Pte Ltd. All rights reserved. In thisdocument, “PwC” refers to [insert legal name of the PwC firm] which is a member firm ofPricewaterhouseCoopers International Limited, each member firm of which is a separate legalentity.