aula 7: política e financiamento municipal (material apresentado durante o seminário: nova gestão...

TRANSCRIPT

Aula 7: Política e Financiamento Municipal

(Material apresentado durante o seminário:Nova Gestão Pública e Finanças

New Public Management & Finance)Seminário Especial

FGV-EAESPJeffrey Leifer

Kurt von Mettenheim5–9 Junho 2006

Rua Itapeva 474 Sala 4002 13:00 – 16:00

Lecture Topics

1) Introduction: US Municipal Bond Market

2) Diagnosis 1: Achilles Heel of Brazilian Development = Local Government Finance

3) Diagnosis 2: Economic & Financial Reforms make Brazilian Municipal Bond Market viable

4) Diagnosis 3: Recommendations from Successful Muni Markets in Emerging Economies (& Calif. Model)

5) Proposal: BMBMwg (Brazilian Municipal Bond Market working group) 2nd Semester 2006 CVMM, Comissão de Valores Mobiliários Municipais

1) US Municipal Bond Market“Municipal bonds have been issued by US

local government since 1812” Fahim, Mayraj.

Infrastructure in the United States is generally financed through municipal bonds(all sub-national governments, agencies, quasi-public “special districts”).

1st paper: General obligation bond, i.e. backed by taxing power and revenues of issuer.

“…without the ability of state and local governments to issue debt … today’s America, as we know it, would cease to exist.”

2005 Market Value = 2.0 Trillion US$ = 15% US GDP

History of US “Muni” Bond Market

1902 = 2.1 billion or $27 per capita.

1927 = 14.9 billion or $125 per capita.

Downturn From WWI Great Depression WWII

1945+ “Pent up demand” for infrastructure (urbanization…)

1960 = 66.0 billion If 1/3 per capita US mkt,1981 = 361.0 billion Brazilian Municipal Bond1998 = 1.3 trillion. Market = R$ 6.5 billion

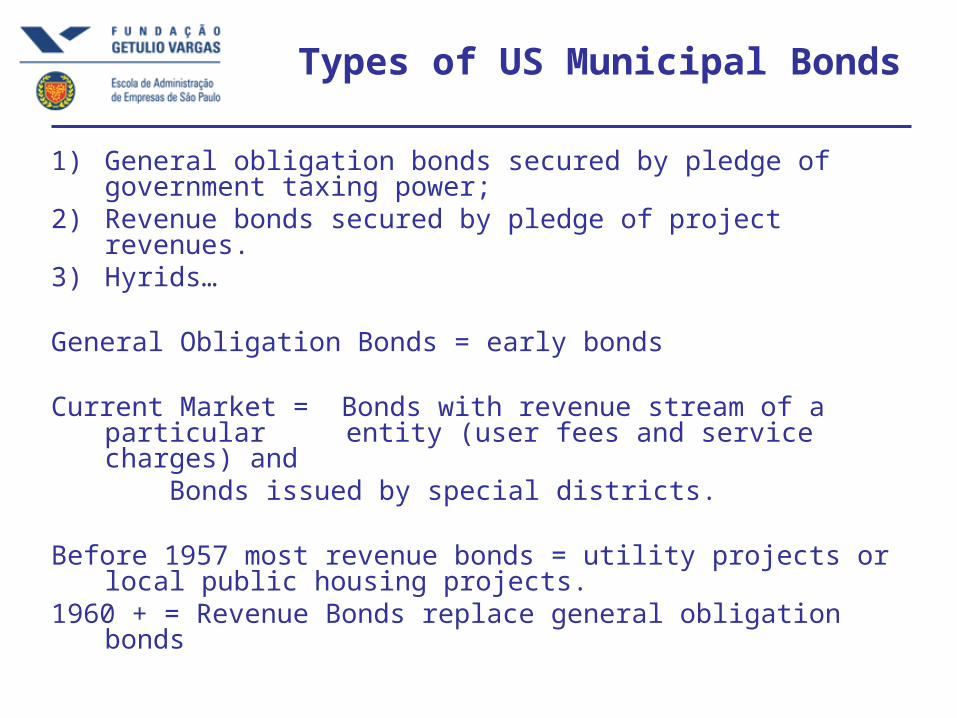

Types of US Municipal Bonds

1) General obligation bonds secured by pledge of government taxing power;

2) Revenue bonds secured by pledge of project revenues.3) Hyrids…

General Obligation Bonds = early bonds

Current Market = Bonds with revenue stream of a particular entity (user fees and service charges) and

Bonds issued by special districts.

Before 1957 most revenue bonds = utility projects or local public housing projects.

1960 + = Revenue Bonds replace general obligation bonds

Legal Framework

Origin = financial ruin brought about by the unregulated and uninhibited issuance of municipal debt.

19th Century = 3 Depressions cause = over- issuance of Munis: 1837-43 1873-79 1893-99

Constitutional restrictions imposed on state and local government spending.

Federal System State Level Regulation

1940 1999 HIGHEST DEFAULT RATE = 1.1%

Default History

1839 1969 = 6,195 defaults (4,770 1929-1935)

1940s = 79 municipal defaults1950s = 112 1960s = 300

Transition from “Institutional Investors” toCredit and Risk Analysis & Individual Investors

History = From “Boom & Bust” to stable market,Today = flight to quality...

Bartley & Zorn. “The Evolution of the State and Local Government Municipal Debt

Market over the Past Quarter Century.” Public Budgeting & Finance, December

2005

1986 Tax Reform Act innovations in the market (changing

economic and social conditions) Increase in disclosure requirementsCredit enhancements & efficacy of

municipal securities for US state and local governments.

Innovations 1986 +

Revenue Bonds & Custom Solutions > long-term, fixed-coupon general obligation (GO) bonds.

Creative ways to avoid debt limits and procedural hurdlesLease financing (Certificates of Participation (COPs), Tax increment financing (TIF), Bond banks, Revolving loan funds. Issuers protect investors via letter of credit (LOC)

Reset securities, or floating rate debtInterest rate exposure mitigated via swaps and derivatives.

All above increase liability risks… Simpler instruments needed?

TOPIC 2: Diagnosis: Achilles Heel of Brazilian

Development = Local Government Finance

Sequence of Fiscal, Monetary, Banking, and Financial Market reforms

1982 Dual Fiscal & Debt Crises1994 Plano Real, 1999 Inflation

Targeting, Fiscal Adjustment, Flexible FOREX

Financial Deepening without Local Government Finance

Repressed Demand = HUGE MARGINS Easy Start

Desafio da Presidência da FGV (2003 SAP)How to grow Brazilian economy @ 8%

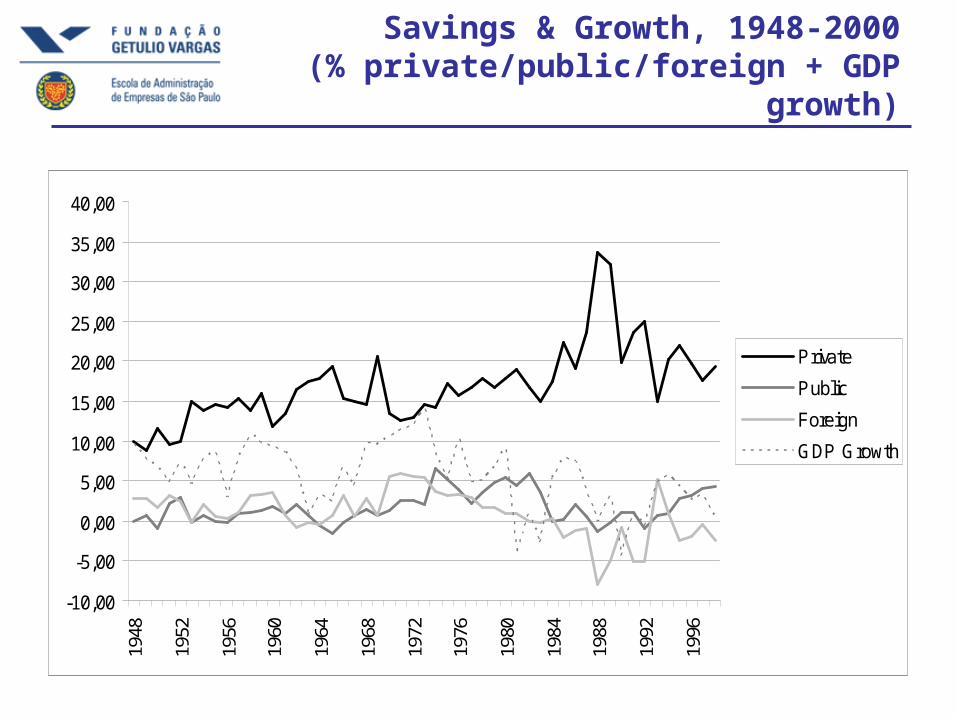

Savings & Growth, 1948-2000(% private/public/foreign + GDP

growth)

-10,00

-5,00

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

Private

Public

Foreign

GDP Growth

Capital Formation & Growth 1948-2000

(% Private, Public + GDP growth)

(10,00)

(5,00)

0,00

5,00

10,00

15,00

20,00

25,00

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996

Private

Public

Other

GDP Growth

Bond Markets = Achilles Heel of Brazilian Development

(BIS report, The Development of Bond Markets

in Emerging Economies)

Bond Markets % GDP 2000 2001 2002 2003 Buenos Aires Total 21.1 19.2 31.4 46.9 Private 2.0 2.5 1.3 1.8 Government 19.2 14.1 27.7 42.4 Foreign 0.0 2.6 2.4 2.7 São Paulo Total 0.0 0.4 1.0 1.9 Private 0.0 0.4 1.0 1.9 Government 0.0 0.0 0.0 0.0 Foreign 0.0 0.0 0.0 0.0

Achilles Heel... %GDP Finance

Domestic Banks Foreign Banks Bond Issues 1995 2000 1995 2000 1995 2000 -------------------------------------------------------------------------------------------------------China 88 125 10 6 15 26 India 23 27 5 5 23 29 Russia 8 12 14 14 1 11

Asia Indonesia 53 21 24 27 2 7 Korea 51 74 17 14 44 73 Philippines 39 45 11 22 3 18 Thailand 98 86 55 23 4 10

Latin America Argentina 20 23 13 17 10 25 Brazil 31 30 10 16 1 7 Chile 53 67 21 26 1 11 Colombia 18 19 11 15 1 8 Mexico 37 12 26 10 12 16 Peru 16 26 9 13 0 0 Venezuela 9 10 15 11 4 9 -------------------------------------------------------------------------------------------------------

Diagnosis 2: Economic & Financial Reforms make Brazilian

Municipal Bond Market viable

1) World Class Transparency & Govt–Market Relations

2) Risk Analysis/IT/Finance: FGV-EAESP Tradition

3) Recentralization = Fiscal Mantra 1990s Decentralization = Financial Mantra of 2000s

4) Market Confidence Municipal Finance* New Public Management = Transparency, Advocacy, Education & Training, Public & Private collaboration...

* Old Public Management Hi Cost of Capital, Slow Economic Growth, Social Exclusion...

Macro-Forecasts & Viability of Brazilian Municipal Bond

Market

1) BCB FOCUS (FGV Brazil Forecast)3-5 Year Forecasts (Econ/Politics/Govt) Consensus: Macro-Fundamentals Foreign & Domestic Debt Structure Improve...

2) 15-50 year forecastsa) US Govt National Intelligence Studyb) Goldman Sachs BRIC´s Studyc) Deutsche Bank Scenarios

Long-Term: Brazil & Globalization

US NIC Study: * NAFTA = north, South America new geopolitical zone* Global Firms must build emerging market presence / platforms

Goldman Sachs “Dreaming with the BRICS”* BRIC GDP > G8 Countries in 2040

Deutsche Bank: 2020 projections* @ 2.8 % growth, not so soon…

Diagnosis 3: Recommendations from Successful Muni Markets

in Emerging Economies(& California Model Sale)

1) Preconditions: (Recommendations Brazilian Situation & Viability)

2) Market Structure: (Recommendations Brazilian Situation & Viability)

Bahl, Roy & Sally Wallace. “Public Financing in Developing and Transition Countries” Public Budgeting & Finance. Jan 2005

Pre-Conditions for Muni Market

Recommendation Brazil Situation-------------------------------------------------------------------------------------1. Devolution of sufficient Clear Intragovernmental revenues to encourage Budget Flows, but myth?

ofpayment. no repayment (00s vs 90s)-------------------------------------------------------------------------------------2. Devolution of authority Yes > % Budget = Mun. Govt.for budgeting. (orçamento participativo...)--------------------------------------------------------------------------------------3. Borrowing authority NOto issue short- & long-term debt.-------------------------------------------------------------------------------------4. Provision of public uses Repressed Demandof borrowing. Low Capacity--------------------------------------------------------------------------------------5. Limits on sources LRF: Fed. Ministry of Financeof borrowed funds. (Sec. Treasury & CAE Senate)

Pre-Conditions for Muni Market

Recommendation Brazil Situation-------------------------------------------------------------------------------------6. Requirement that debt Must Design Frame: approximates economic life Cost/Benefit Analysis...asset or project. Revenue Stream-------------------------------------------------------------------------------------7. Transparent and reasonable Transparent YES debt limits % total spending Reasonable NO (2%RLC)on past budget of future.-------------------------------------------------------------------------------------8. Provision for payment Who? 1) Insurance co´sdebt service arrears & default. 2) Govt., 3) Bond Bank -------------------------------------------------------------------------------------9. Budget law distinguishes NO? Accounting culture:capital from recurrent expenditures. From “debt” “capital”

Market Structure

Recommendation Brazil Prospects-------------------------------------------------------------------------------------1. Yields priced for risk. Primary Market Launches...-------------------------------------------------------------------------------------2. Instruments placed in Underwriter? Insurance Co´sMarket with private parties Bond Bank as underwriters or lenders. Consortia-----------------------------------------------------------------------------------3. Risk assessed by institutions, Must Adapt Credit Analysisbanks, insurance, pension, to Municipal

Finance/Budgetsecurities firms.-------------------------------------------------------------------------------------4. Criteria for grants & Policy Discretion for Gov´t.subsidized market loans clear & classified from low to high risk.

Manage Market

Recommendation Brazil Prospects--------------------------------------------------------------------------------------1. Accounting systems that Low Capacitysupport local liability management. (asset management systems>).--------------------------------------------------------------------------------------2. Regular reports to compare Hi Capacity

Budgetplanned-to-actual expenditures and Lo experience financetrack budget progress (debt schedule).--------------------------------------------------------------------------------------3. Projects evaluated individually and Low Capacityaccording to economic criteria. Local units have professional capital programming, budget systems, and apply cost/benefit and net present value techniques.

Tips

Recommendation Brazil Situation-------------------------------------------------------------------------------------Uncertainty stunts market growth. Hi Market Confidence --------------------------------------------------------------------------------------Political commitment critical. Legislative

Alliances--------------------------------------------------------------------------------------1st focus = municipal borrowing Outlawed in LRFframework (municipal credit markets)---------------------------------------------------------------------------------------Example: Mexico via provisions for Who? Fed GovtCollateral & Debt Security Insurance co´s

Bond Bank/Consortia

--------------------------------------------------------------------------------------Remedies for nonrepayment Adapt LRF/ Market

Premium?

Tips, cont.

Recommendation Brazil Situation--------------------------------------------------------------------------------------Central government guarantee NO--------------------------------------------------------------------------------------Devolution of authority to borrow NO--------------------------------------------------------------------------------------Tighter reporting requirements Tight as Stand in on commitments and capital expenditures. Budget/Fical Law---------------------------------------------------------------------------------------National governments and donor BIG ADVANTAGErequirements can direct institutional savings into domestic investments. --------------------------------------------------------------------------------------Can provide subsidies to certain BIG

ADVANTAGEactors and reduce them over time.

Politics & Brazil Muni Market

2007 = New Federal and São Paulo State Governments

“Supercoalitions” after Mensalão

Problem: Link Federal State & Local Politics

(partial) Solution: Municipal Bond Market : * Transform Zero-Sum Budget Disputes into

Positive-Sum collaboration via access to capital markets

* Executive-Legislative-Judiciary + market discipline

* Risk Ratings to Reward 7 years fiscal adjustment< Cost of Capital + Deepen Financial

System

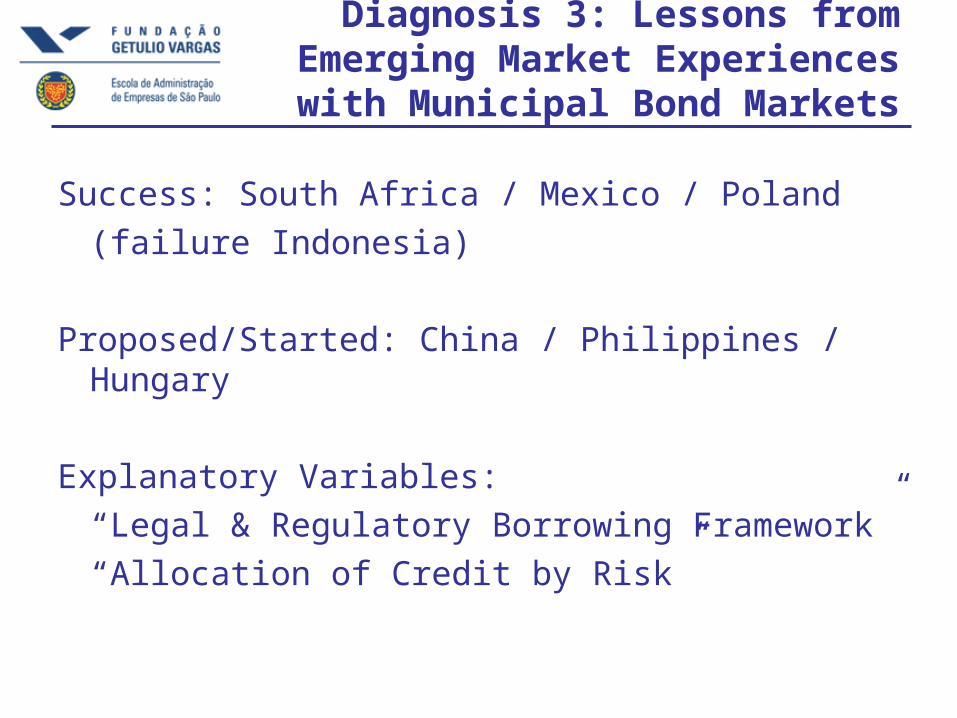

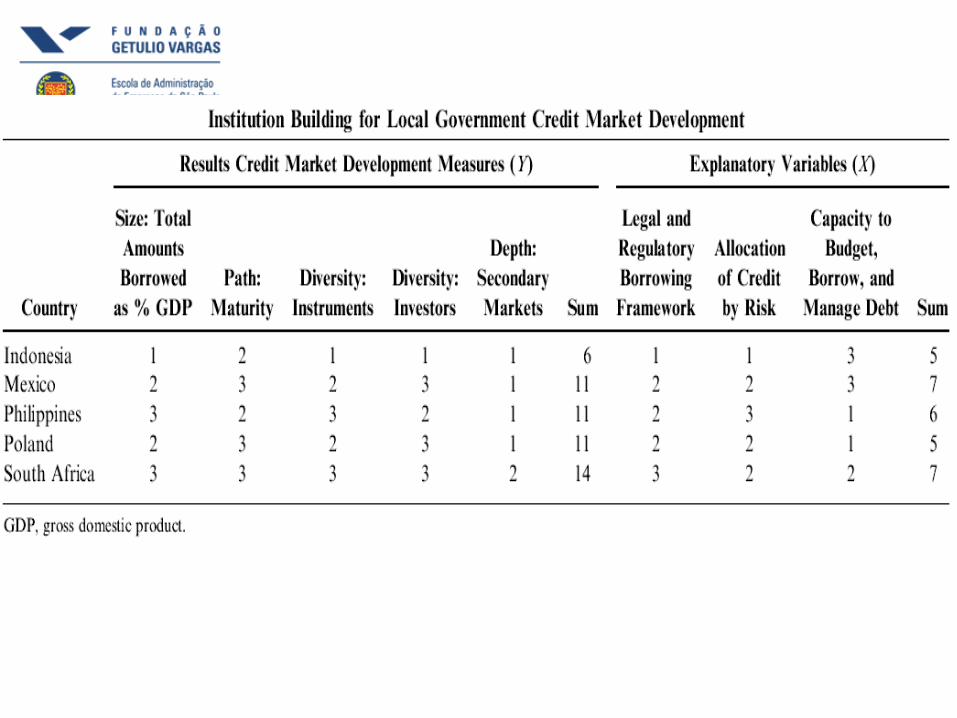

Diagnosis 3: Lessons from Emerging Market Experiences with Municipal Bond Markets

Success: South Africa / Mexico / Poland(failure Indonesia)

Proposed/Started: China / Philippines / Hungary

Explanatory Variables:“Legal & Regulatory Borrowing Framework”“Allocation of Credit by Risk”

California Model Sale

County of Stanislaus 2004 Certificates of Participation, Series 2004 A & B

$15,340,000 Series A COPs $27,455,000 Series B COPs.

A= construction of Gallo Center for the Arts.B = 12th Street Parking Garage and Office

Building, and acquisition and renovation of Salida Regional Library and Community Center.

Security A = pledge Gallo Center for the Arts

Security B = pledge of County assets, (former City Hall building, unencumbered portions of the downtown County jail, Parking Garage to be constructed, and Salida Library).

Bond insurance = commitment from AMBAC, Assurance Corporation.

AAA Moody´s = saved County $667,000 debt service compared to uninsured COPs ‘A3.’

Capitalize Interest of 1st 2 years, 20 term.

Complex Pricing

(i) multiple bond series, one (tax purposes) as 501(c)(3) bonds, 2% cost of issuance limit,

(ii) no underlying ratings for either series(iii) lesser essential asset in the Performing

Arts Center, (iv) complicated private use tax issues and

restrictions(v) a very difficult market for California

paper.

County saved $1.9m 26/3/04 vs two weeks later. Bond Buyer 20-Bond

Index (avg. yield 20 GO bonds 20-year

“A”)

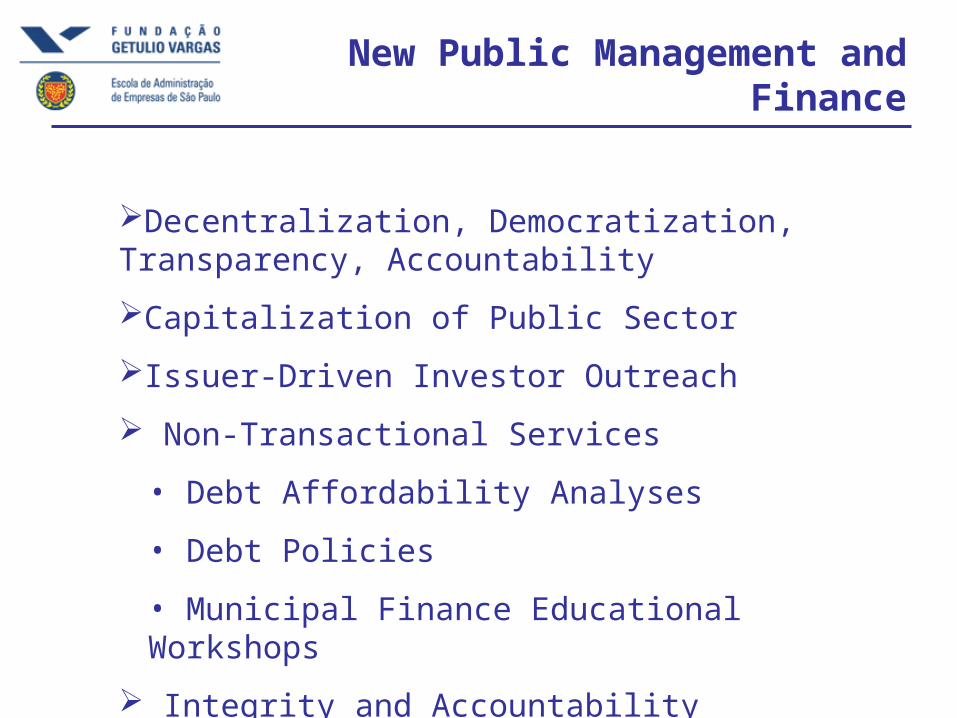

New Public Management and Finance

Decentralization, Democratization, Transparency, Accountability

Capitalization of Public Sector

Issuer-Driven Investor Outreach

Non-Transactional Services

• Debt Affordability Analyses

• Debt Policies

• Municipal Finance Educational Workshops

Integrity and Accountability

Principles of Prudent Municipal Debt Management

Due Diligence andEnhanced Disclosure

Independent FA(No conflicts)

Informed Decision Making

InvestorOutreach

Debt Affordability

CompetitiveSale

4) Proposal: Brazilian Municipal Bond Market

working group

Working Group Creation of Muni Debt Authority(ies)

?= CVMM, Comissão de Valores Mobiliários Municipais (MBA, Municipal Bond Authority)

Challenge: Write Strategic Plan for Municipal Bond Market (December 2006)

Challenge: Attract Membership: Academic, Public, Private Sector Leaders

Critical Juncture

1) Brazil = Successful Sequence of Economic Reforms, but loosing out on international capital movements & confidence among international investors.

2) Brazil = World Class IT / Risk / Accounting practices.* Private Sector Public Sector * New Public Management = Debt Capacity Analysis /

Cost- Benefit / IT / Capital Planning / Cash Management / New Public-Private dynamic...

3) Can Build Virtual Cycle via Positive Sum: * Lower Cost of Capital (Hi spreads Hi marginal

returns).* Increase Transparency / Accountability /

Democratization* Reverse Brain Drain to Private Sector* Develop Bank Capacity & Market Differentiation

4) “Relational Financial Management” = Pre-Sale Post-Sale, education / training < cost of capital new issues education / training < cost of capital... INVESTMENT GRADE...

From Vision to Market

BMBMwg Monthly Meetings, 2nd ½ 2006

Market Design, 2007

Primary Market Launches, 2007 & 2008

Secondary Market 2009+

2007 2008 2009-10a=investor b=federal c=local govtrelations govt. tasks tasks

BMBMwg: Tasks / Schedule

June 5-9: Seminar Today´s PPT = Test Baloon...

June 24: List of Projects for “Pearl” launches, test market, build confidence, demonstration effect (47 São Paulo State Strategic Projects? Package Refinance existing?)

August 31: Presentation & Discussion: Market Design

September 30: Approve Draft Memorandum: Market Design

October 28: Roundtable and Discussion: Veto/Amend Market Design

November 25: Present Proposal to FGV Presidency, Public Opinion, Fed & State Finance Authorities 2007+

Thank You

* GVpesquisa, Prof. Peter Spink

* FGV-EAESP CDAPG, Coordenador, Fernando Abrucio& Research Groups

Transformação do Estado e Políticas Públicas (Prof´s Bresser- Pereira, Pacheco, Abrucio,

Loureiro, Martes, B.Taschner)Finanças Públicas (Prof´s Arvate, Biderman,

Avelino)

* FGV-SP : EAESP EDSP EESP (professors, students, staff...)

* Jeffrey Leifer; Financial Advocate of California Municipalities Best Practices

* Antonio Roberto Bono Olenscki, CDAPG & New Public Management São Paulo State Government