auto component industry in india · auto component industry in india. 2 contents ... research...

TRANSCRIPT

1

Automotive Component Manufacturers Association of IndiaAutomotive Component Manufacturers Association of India

Auto Component Industry in India

2

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

3

• Largest Democracy in the world with a population of 1,166 mln.•

Age structure:0-14 years: 31.1% 15-64 years: 63.6% 65-over: 5.3% Sex ratio : At birth: 1 : 1.06 male(s)/female

Life expectancy: 69.89 years male67.46 years female

1,562 11,698 140 13 101 216 20 INDIA

StateCentral

Engg., Tech., & Arch.,

Colleges#

Arts, Science & Commerce Colleges

Research Institution

s

Institutions of National

Importance*

Deemed Univers

ity*

University*States/U

Ts

Total no. of telephone connection as on Feb 2009 was 413million (14million subscriber added every month last year)

Indian IT Companies played a vital role in the development of the Airbus A380 and Boeing 787 Dreamlines

IndiaIndia--At a GlanceAt a Glance

4

Chandrayaan-1 a fantastic success: European scientist

National Aeronautics and Space Administration (NASA) astronaut Edward Michael Fincke said on Friday (September 11, 2009) the Chandrayaan Mission of the Indian Space Research Organisation (ISRO) was a success, with 95 per cent of the mission being accomplished.

Taj Mahal it's one of the 7 wonders

IndiaIndia--At a GlanceAt a Glance

Hyundai i-10, Foreign Made vehicle, 1st Launched in India then rest of the world

5

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

6

After decades of low growth, the economy After decades of low growth, the economy moved into a highmoved into a high--growth phasegrowth phase……..

2.9

5.1

7.3

3.64.0

5.6 5.2

7.9

9.2 9.8 9.3

5.75.4

5.9 5.8

4.3

0

2

4

6

8

10

1950's 1960's 1970's 1980's 1990's 2001-03 2004 2005 2006 2007 2008

Gro

wth

(%)

IndiaWorld

Slow growing closed economy Fast growing open economy

Transformation

Real GDP growth rate: India vs. World

Source: IMF Apr’09, Economic Survey 2008-09 & RBI Bulletin

Manufacturing27%

Agriculture21%

Services52%

Composition of GDPAverage Real GDP growth in last 5 years was 8.5%Projected GDP growth in 2009-10 is 6.1%

GDP Per Capita is US $ 680

7

111.5

253

291

252

181.3

149.2

61.4

78.2

182.6163

124.6

103.183.5

63.852.7 27.324.57

15.75.52.63.14.2

281

173.1

142136

107

75.4

0

50

100

150

200

250

300

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Imports(US $ bln)

Exports(US $ Bln)

FDI(US $ bln)

FE Reserves ( US $ bln)

India’s Trade, FDI and Foreign Exchange Reserves

The Indian EconomyThe Indian Economy

Source: Economic Survey 2008-09 & RBI Bulletin

8

48.4

25

46.0

20

44.9

15

44.3

12.5 10

39.5

8.5 7.5

45.549.0

Exchange Rate Import Tariff2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Source: Economic Survey 2007-08

Exchange Rate is Market Driven Continued Import Tariff Reduction

* As on March 31, 2009* As on March 31, 2009

Indian EconomyIndian Economy

Exchange Rate is Market Driven Continued Import Tariff Reduction

9

The Surging – Urban India

10

The Emerging – Rural India

11

Low cost of Skilled Manpower & Rapidly growing Design Capability

Easy access to capital although interest rate is high (There is a Credit Squeeze in Short Term)

Continuously Improving Quality resulting in Export of Automobiles and Auto components

Low penetration rate of Cars (7-8/1000)

According to McKinsey, the middle class will grow from 50 million to 550 million by 2025

Infrastructure development ($500 billion in the next 5-6 years)

Long TermShort TermThe Demand DriversThe Demand Drivers

What does this mean for us?What does this mean for us?

12

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

13

Investments are well BalancedInvestments are well Balanced

CARS & MUVs

CVs

2/3 WHEELERS

TRACTORS

14

16201532

132311131028

842

608564218

246222196182146114105

18381778

15451309

1210988

722669

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09Cars MUVs Total Pass Veh

Source: SIAM & ACMA-McKinsey Report

2014-15

2654

277

2001-2008 CAGRCars =16.3%MUV’s = 11%Overall=15.5%

PROJECTED CAGR2008-2014Cars = 8.6%MUV’s = 4%

Overall=8.5%

3.0m

Passenger Vehicle ProductionPassenger Vehicle Production(Qty in (Qty in ‘‘000 Nos.)000 Nos.)

15

Others1.9%

Ford 1.7%

GM3.0%Honda Siel

3.2%

Tata Motors10.7%

SkodaAuto 0.9%

Maruti45.5%

Hyundai 32.1%

M.- Renault 1.0%

2007-08(Apl-Mar)

2008-09(Apl-Mar)

Market Share- Passenger Cars

Ford 2.4%

GM3.2%Honda Siel

4.2%

Tata Motors12.7%

Others2.9%

Maruti47.4%Hyundai

25.5%

M.- Renault 1.6, 2%

16

95

64

121

81

166

109

211

139

219

172

294

226

295

254

193

224

0

50

100

150

200

250

300

350

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

M&HCVs LCVs

159

202

275

350 391

5202001-2008 CAGRM & HCVs =10.7%LCV’s = 19.6%Overall=14.8%

Commercial Vehicles ProductionCommercial Vehicles Production(Qty in (Qty in ‘‘000 Nos.)000 Nos.)

549

417

17

8.48.08.47.66.55.65.14.3

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-092009-10 2014-15

13 ?

??

CAGR2001-200810%

22--Wheeler ProductionWheeler Production

(Qty in million Nos.)(Qty in million Nos.)

18

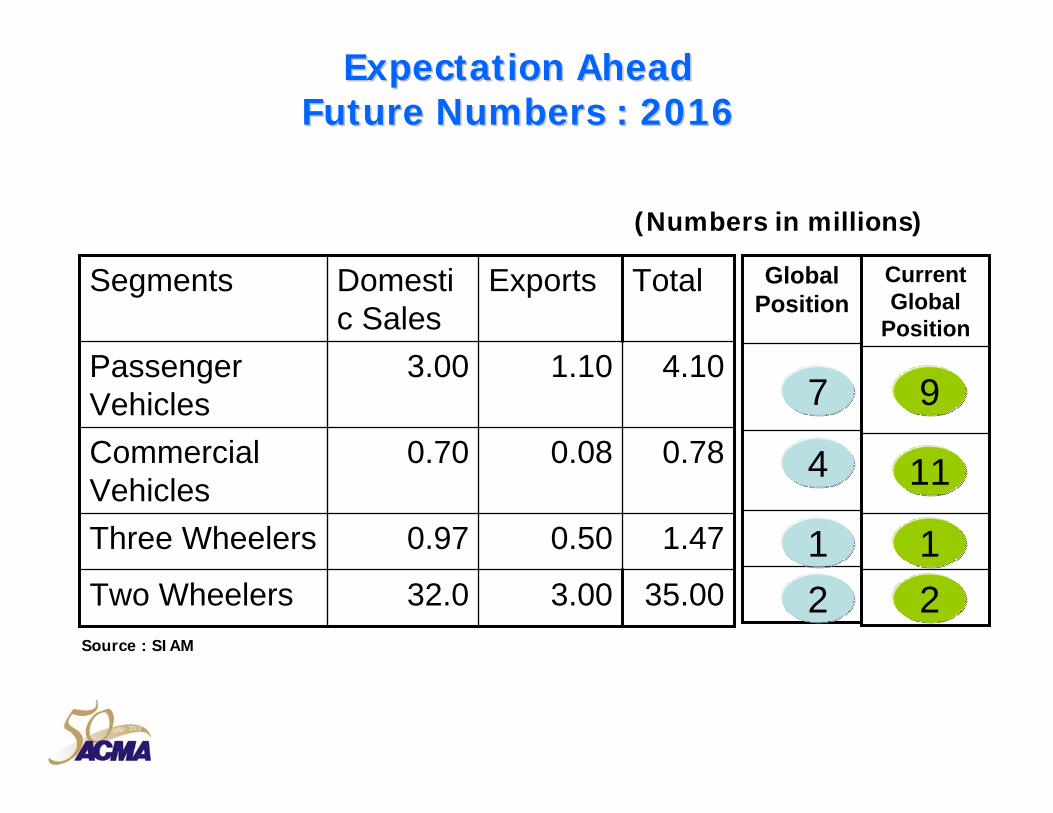

Expectation AheadExpectation AheadFuture Numbers : 2016Future Numbers : 2016

3.00

0.50

0.08

1.10

Exports TotalDomestic Sales

Segments

35.0032.0Two Wheelers

1.470.97Three Wheelers

0.780.70Commercial Vehicles

4.103.00Passenger Vehicles

(Numbers in millions)

Global Position

Source : SIAM

7

4

12

Current Global

Position

9

11

12

19

““INDIAINDIA”” –– A Base for Compact CarsA Base for Compact Cars

Maruti Suzuki :• New car plant• Capacity 250K

Hyundai :• Increase capacity to 600K cars.

Tata Motors :• New plant to manufacture Nano Car,• Selling price USD 2000• investment US $ 240 million.• Capacity 500K

Toyota :• New Capacity 200K cars by 2008

General Motors :• New plant capacity 140K.• SOP Q3 2008.

Nissan-Renault : • 50:50 JV, • Capacity 400K• Investment USD 1 Billion

VW :

• New plant Investment Euro 400 millionSOP Q3 2009.

Honda :

• New Capacity 60K Investment $ 250 SOP Q1 2009.

Ford :

• New Investment US$ 500 million

20

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

21

Auto Component Industry Auto Component Industry

41

42

84

206

211

> 100 Million US $

> 50 ~ 100 Million US $

> 25 ~ 50 Million US $

> 5 ~ 25 Million US $

< 1 ~ 5 Million US $

Annual Turnover in Million US $

AC

MA

’sm

embe

rsh

ip c

ompr

ises

584

com

pan

ies.

Number of Companies

TS 16949TS 16949TS 16949TS 16949

OHSAS 18001

Suppliers Embracing Modern Shop-FloorPractices:

- 5-S, 7-W- Kaizen- TQM- TPM- 6-Sigma- Lean Manufacturing

Deming Award

TPM Awards 151160

18656397564

151160

18656397564

The Industry is graduating to worldThe Industry is graduating to world--classclass

22

Turnover 6.730 8.700 12.0 15.0 18.0 19.1

Exports

Investment 3.100 3.750 4.400 5.400 7.200 7.70 7%

Export as % of 18.9% 19.5% 20.5% 19.2% 19.6%Turnover

2004-05 2005-06 2006-07 2007-08

(Value in US $ Billion)

1.274 1.692 2.469 2.673 3.520

2003-04

24.6% 29% 38% 25% 20% 6%

37% 34% 47% 16% 32%

Auto Component Industry - Statistics

Imports 1.428 1.902 2.482 3.600 5.220

2008-09

3.808%

6.80

19.9%

40% 33% 30% 31% 45% 30%

Estimated

23

Electrical Parts9%

Equipments10%

Suspension & Braking Parts

12%

Body & Chassis12%

Drive Transmission & Steering Parts

19%

Engine Parts31%

Others7%

Comprehensive Product RangeComprehensive Product Range

24

18

5.46.7

8.7

15

12

19.1

0

5

10

15

20

25

2002 2003 2004 2005 2006 2007 2008

Source : MOHI Automotive Mission Plan (AMP)

2009

20

40

2016

In US$ Billion

Auto Component TurnoverAuto Component Turnover

2002 – 2008 CAGR 23.4%

POTENTIAL CAGR 2008 – 2015

11%

25

3.83.6

1.21.7

2.5 2.9

2003 2004 2005 2006 2007 2008

POTENTIAL EXPORT CAGR

2008-201527%

2009

20-22

2016

CAGR2003-2008

Exports : 26%

Projected

Auto Component Industry Auto Component Industry –– ExportsExports

5.9

(in US$ billion)

26

Aftermarket20%

OEM/TIER 180%OEM/TIER 1

35%

Aftermarket65%

1990s 2008

COMPOSITION OF EXPORTS

CONTINENT-WISE EXPORT OF AUTO COMPONENT 2007-08

Direction of Exports Direction of Exports

Middle East7%

North America22%

Africa7% Europe

44%

South America4%

Oceania1%

Asia15%

27

Increase in Sourcing Components Increase in Sourcing Components from Indiafrom India

28

Auto Component Sourcing Auto Component Sourcing

29

Auto Component Sourcing Auto Component Sourcing

30

Auto Component Import by Major Countries

2006 2007 2008United States 100.98 97.72 91.27 -6.60

EU(27 Members) 47.24 54.93 61.13 11.29China 25.99 28.05 32.35 15.32Japan 17.75 17.53 19.81 13.00South Korea 10.92 10.32 11.48 11.28India 3.60 5.34 7.43 39.00

% Share

% Change

2006 2007 2008 20082008/200

7

World 47.24 54.93 61.13 100.00 11.3Japan 10.52 11.65 12.45 20.36 6.8United States 8.43 8.37 8.88 14.52 6.1China 5.28 6.65 8.39 13.72 26.2Turkey 3.57 4.84 5.53 9.04 14.3South Africa 2.81 3.50 3.80 6.21 8.6Switzerland 2.79 3.13 3.33 5.44 6.1Korea South 1.33 2.27 2.62 4.28 15.3India 1.24 1.69 2.22 3.62 31.2Taiwan 1.48 1.72 1.95 3.19 13.7

Auto Component Import by European Union(27 Members) Year To Date: January - December

Partner CountryValue in US $ Billion

Auto Component Import by Major Countries

Year To Date: January - December

Reporting Country Value in US $ Billion % Change

31

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

32

Increase export revenueTo $ 35 billion by 2016 from

$ 4.1 billion at present

On 29.01.07, the Prime Minister released Automobile Plan 2006 -2016 to give a road

map to Indian Automobile Industry

Automotive Mission Plan 2016Automotive Mission Plan 2016

Increase turnover to$145 billion by 2016

from $ 35 billionat present

Provide employment toadditional 25 million people

by 2016

Automotive Plan 2016

By 2016, the Automotive sector is expected to contribute

10% of the country’s GDP and 30~35% of the Industry

Government of IndiaSIAMACMA

33

2020

11

2020

Achieve $20 billion in Domestic SalesAchieve $20 billion in Domestic Sales

Achieve $20 billion in Exports SalesAchieve $20 billion in Exports Sales

Create 1 million additional JobsCreate 1 million additional Jobs

20:20:120:20:1

ACMA Vision for 2016ACMA Vision for 201620 : 20 : 120 : 20 : 1

Growth of the Automotive Component Industry directly linked with the growth of Automobile Industry.

Over 70% sales to the OEM

34

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

35

Hybrid Scorpio: First in SE Asia!Hybrid Scorpio: First in SE Asia!

• It is Diesel Electric • Parallel, Full Hybrid Vehicle• Offers

• Start – Stop• Electric Launch• Torque Augmentation• Regenerative Braking

• Seamless, enhanced driving experience

Capacity 500K

• The Price Rs 100,000~($ 2000)

Tata Tata NanoNano: The Low Cost Car of The World: The Low Cost Car of The WorldCapability of Indian ManufacturersCapability of Indian Manufacturers

36

Capability of Indian Capability of Indian Component SuppliersComponent Suppliers

1. Conversant in all Global Automotive Standards

2. Investments in R&D to meet OE Customer requirements

3. Flexibility in small-batch production.

4. Growing IT Capability for Design, Development & Simulation.

5. Respect for Intellectual Property

37

Some Design & Research Some Design & Research CentresCentres in Indiain India

38

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Auto Component Industry of IndiaAuto Component Industry of India

39

The Way Forward

1. Auto-Component Sector needs US $ 1.5 billion of new investments every year for next 8 years.

2. Overseas auto-component manufacturers, especially SMEsshould invest more in capacity enhancements and green-field manufacturing in India – to meet growing domestic demand for auto-components.

3. Investments in Auto-IT sector is a high potential area.

4. To encourage new wave of partnerships at the Tier 2/3 level covering the entire automotive supply chain to address not only product technology, but also “Process Technology”.

40

• Manufacturing

• Technology

• Research & Development

• Quality

• Environment

Areas of Cooperation

41

The Addressable Opportunity…

• Establish Partners/JV in India for

- Safety Components

- Auto Electronics, Electromechanical Sub assemblies

- Embedded Systems

- Informatics & Telematics

- New Material

- Simulation Technology

• Collaboration for Manufacturing Excellence and Process Design

• Production Sharing in India & Germany for a Holistic Service Capability

• Partnering for Global Requirements

• Merger & Acquisition •

42

ContentsContents

The Indian EconomyThe Indian Economy

The Automotive IndustryThe Automotive Industry

Growing Capabilities of the Indian IndustryGrowing Capabilities of the Indian Industry

The Way ForwardThe Way Forward

IndiaIndia--At a GlanceAt a Glance

ACMA & Its ServicesACMA & Its Services

Automotive Mission PlanAutomotive Mission Plan

Supply Industry of India & Global ExperiencesSupply Industry of India & Global Experiences

43

Introduction

Automotive Component Manufacturers Association of India

Role

Members

Quality System

Re-Christened

Inception

An apex agency of the Indian Automotive Industry

570+ companies forming majority of the auto component output in the organized sector

ACMA operates on Quality System basedon ISO 9001:2000

In the year 1959 as The All India Automobile & Ancillary IndustriesAssociation (AIA & AIA)

As Automotive Component Manufacturers Association of India in the year 1982

44

Collection &Dissemination of

Information

QualityEnhancement

TechnologyUp-gradation

Promotes IndianAutomotive Component Industry

Vital Catalyst for Industrial Development

Trade Promotion

ACMA and Its ServicesACMA and Its Services

45

Promote India as a Brand

Promote India as a Brand

Organize Business Development Delegation

Overseas

Organize Business Development Delegation

Overseas

Undertake ExportPromotional

Projects

Undertake ExportPromotional

Projects

Organize Participation in Overseas Automobile

Exhibitions & Fairs

Organize Participation in Overseas Automobile

Exhibitions & Fairs

Global Interaction through

Counterpart Association

Global Interaction through

Counterpart Association

Dissemination of Export Enquiries

Dissemination of Export Enquiries

Organize Private Exhibitions &

Suppliers Conference

Organize Private Exhibitions &

Suppliers Conference

Facilitate potentialBusiness Partnership of

JV / Strategic Alliance

Facilitate potentialBusiness Partnership of

JV / Strategic Alliance

Providing International

Sourcing Forums

Providing International

Sourcing Forums

Working closelywith IPOs in IndiaWorking closely

with IPOs in India

International Business DevelopmentInternational Business Development

46

5th – 11th January, 2010, India

AUTO EXPO 2010AUTO EXPO 2010

47

ACMA OfficeThe Capital Court, 6th Floor, Olof Palme Marg, Munirka,

New Delhi – 110 067Tel: 011-26160315, 26175873, 74

Fax: 011-26160317E-mail: [email protected],

Website: www.acmainfo.com