aviva uk: investor and analyst event part 2, may 2009

TRANSCRIPT

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 1/25

Andrew Moss NUL18.11.08

Investor and Analyst Event, Wednesday 6th May 2009

UK Life, Driving value through excellence

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 2/25

Andrew Moss NUL18.11.08

Disclaimer

This presentation may include oral and written “forward-looking statements” with respect to certainof Aviva’s plans and its current goals and expectations relating to its future financial condition,performance and results. These forward-looking statements sometimes use words such as

‘anticipate’, ‘target’, ‘expect’, ‘estimate’, ‘intend’, ‘plan’, ‘goal’, ‘believe’ or other words of similarmeaning. By their nature, all forward-looking statements involve risk and uncertainty because theyrelate to future events and circumstances which may be beyond Aviva’s control, including, amongother things, UK domestic and global economic and business conditions, market-related risks suchas fluctuations in interest rates and exchange rates, the policies and actions of regulatory

authorities, the impact of competition, the possible effects of inflation or deflation, the timing impactand other uncertainties relating to acquisitions by the Aviva Group and relating to other futureacquisitions or combinations within relevant industries, the impact of tax and other legislation andregulations in the jurisdictions in which Aviva and its affiliates operate, as well as the other risksand uncertainties set forth in our 2008 Annual Report to Shareholders. As a result, Aviva’s actual

future financial condition, performance and results may differ materially from the plans, goals andexpectations set forth in Aviva’s forward-looking statements, and persons receiving thispresentation should not place undue reliance on forward-looking statements.

Aviva undertakes no obligation to update the forward-looking statements made in this presentationor any other forward-looking statements we may make. Forward-looking statements made in this

presentation are current only as of the date on which such statements are made.

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 3/25

3

Agenda

• UK Life in excellent shape Mark Hodges, Chief Executive Officer

• Driving up profitability & generating capital John Lister, Finance Director

• Delivering operational excellence Toby Strauss, Chief Operating Officer

• Break and innovation demonstrations UK Life Management Team

• Strategic outlook Mark Hodges, Chief Executive Officer

• Strategic focus David Barral, Marketing Director

Questions & answers

Lunch

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 4/254

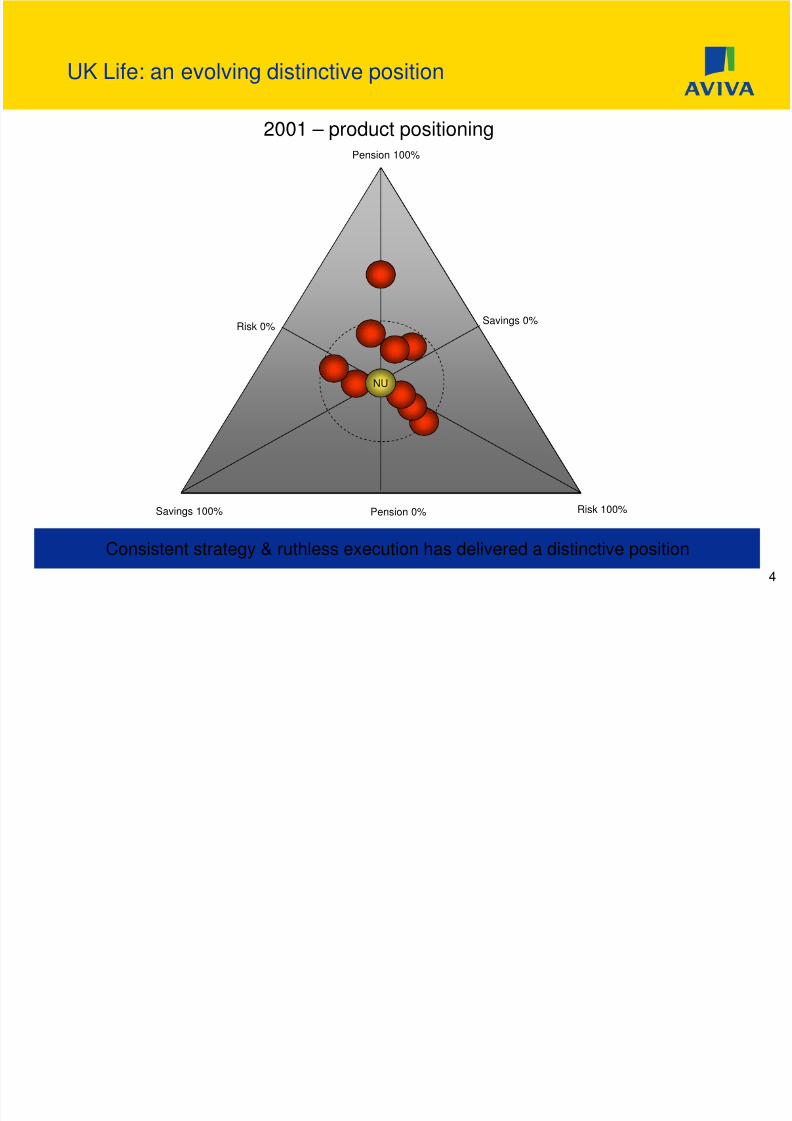

UK Life: an evolving distinctive position

2001 – product positioning

Consistent strategy & ruthless execution has delivered a distinctive position

Pension 100%

Pension 0%

Risk 0%

Risk 100%

Savings 0%

Savings 100%

NU

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 5/255

UK Life: an evolving distinctive position

2008 – product positioning

Consistent strategy & ruthless execution has delivered a distinctive position

Pension 100%

Pension 0%

Risk 0%

Risk 100%

Savings 0%

Savings 100%

NU

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 6/256

Context for strategy: factors shaping the mid term

Industry past

• Growth funded bycapital

• Single premium drivingvolume

• IFA channel pre-dominant

• A Day boom inpersonal pensions

• Steady growth inretirement needs

Distributorconsolidation

DB / DC

NPSS

Recession

Demographics

RDR & TCF

Forces for change Threats & opportunities

• Capital conservation

• Margin squeeze

• Smaller IFA shopwindow

• IFA channel orphans

• Growing role ofworkplace in retirement

• Acceleration in at-retirement provision

The next 3 - 5 years presents a mixture of opportunity and challenge

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 7/257

Our strategy will drive consistent outcomes

We are now in a position to make choices for the next 3 – 5 years

Successful outcomes

• Driving in-force value

• Improved capital efficiency• Cash generation

• Profitable growth

Choices on future

direction and focus

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 8/258

Five key strengths

These advantages will form the basis of our strategic priorities

A large and distinctive customer base

Brand

Risk capability

Momentum in Corporate

Distribution strength and depth

Global re-brand

Distribution reach and

flexibility

All-round propositionstrength

Unrivalled data andcapability

Scale of Aviva customerbase opportunity

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 9/259

Agenda

• UK Life in excellent shape Mark Hodges, Chief Executive Officer

• Driving up profitability & generating capital John Lister, Finance Director

• Delivering operational excellence Toby Strauss, Chief Operating Officer

• Break and innovation demonstrations UK Life Management Team

• Strategic outlook Mark Hodges, Chief Executive Officer

• Strategic focus David Barral, Marketing Director

Questions & answers

Lunch

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 10/25

10

Purpose

Prosperity &peace of mind

VisionOne Aviva,twice the

value

• Manage compositeportfolio

• Build global AssetManagement

• Allocate capitalrigorously

• Increase customerreach

• Boost productivity

• 98% meet or beat COR

• £500m cost savings by2010

• Double IFRS EPS by2012 at the latest

• 1.5 – 2 x dividend coveron IFRS post taxoperating earnings

Aviva Investors• Globally integrated business • Transform the investment model • Increase third party business

UK

Market leadership

• Address legacy• Transform business

model• Exploit UK synergies

• Generate capital

Europe

Scale, growth, capital

• Seize unique growthopportunities

• Leverage scale• Generate capital

N. America

• Optimise business mix,growth & margin

• Generate net capitalreturns

• Contribute to doublingIFRS EPS by 2012

Asia Pacific

Scale, growth

• Prioritised portfolio• Regional operating

model• Investment required

Strategicpriorities

Targets

UK Life, Driving Value Through Excellence

Driving differentiation

• A distinctive customer heartland• 5 areas of strategic focus & action

• Summary of strategic direction

UK LifeMarket leadership

Drive up profitabilityGenerate capital

Operational excellenceCompetitive advantage

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 11/25

11

We have a distinctive customer heartland

Targeting the mid market – plays to our strengths and less competitively crowded

High net worth£500k +

Mass affluent£100 – £500k

Complex wealthmanagement

Wealth managersBanks, insurers

Distributors

Fund managers

PerformanceAdvice

Planning

Middle market£30k – £100k

Mass market

£0 – £30k

Packaged solutions

Building wealthProtection

Retirement income

InsurersRetail banks

Scale

ReachProduct range

Brand

Aviva UK Life customer heartland

LoansShort term savings

Customers Main needs Competitors Basis of competition

Retail banks Reach

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 12/25

12

Positioning based on deep insight

Our heartland is not only distinctive but also more profitable

Overweight for UK

Strong growth predicted

8.6m unserved

Higher average value

Poor Comforta

ble

Wealth

y

Achievers

Getting By

Low

Earners Super Rich

Family

Pre-retired

Retired

Non-Family

Life Stage

Wealth

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 13/25

13

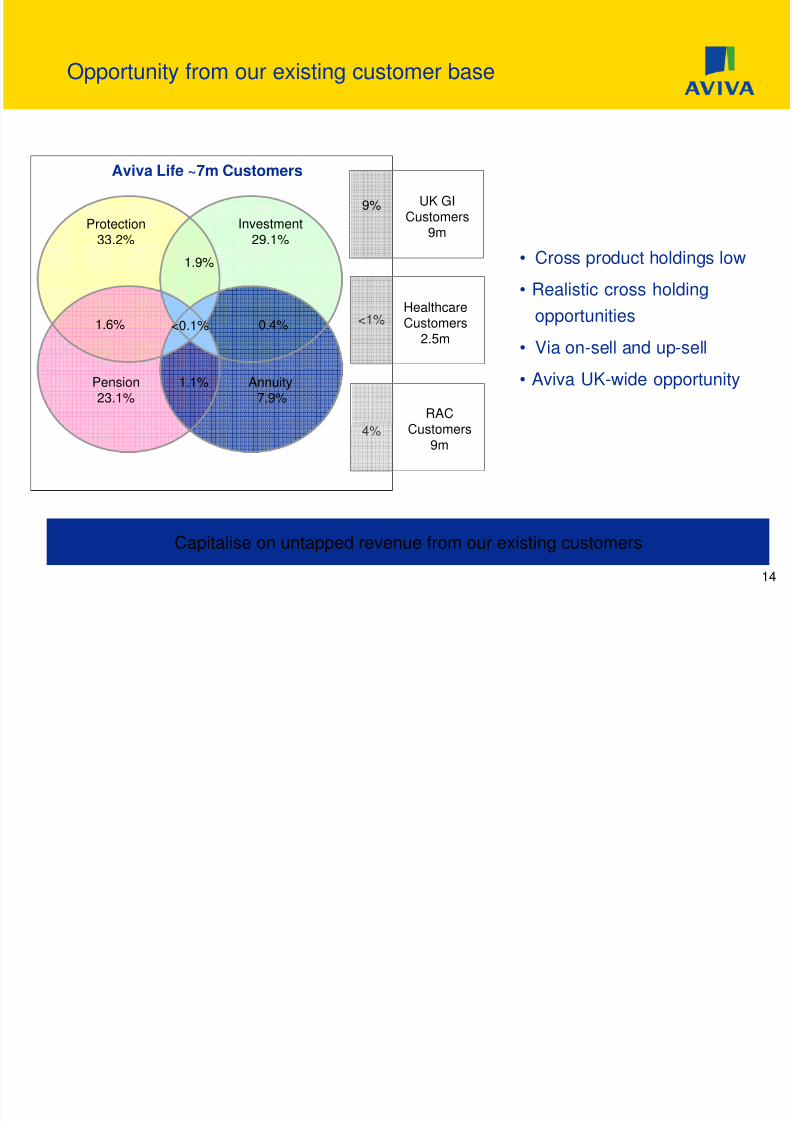

Opportunity from our existing customer base

Capitalise on untapped value from our existing customers

40% have no active adviser

Scaling back direct acquisition

Re-directing advisory resource Generating leads from existing

customers

Industrialise to matchopportunity

UK Life customers by source, m

Direct, 1.3

No current

advisor, 1.4

Partner

customers, 0.7

Have IFA, 3.5

Existing UK Life Customers (Millions)

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 14/25

14

Opportunity from our existing customer base

Capitalise on untapped revenue from our existing customers

<1%

• Cross product holdings low

• Realistic cross holding

opportunities

• Via on-sell and up-sell

• Aviva UK-wide opportunity

UK GICustomers

9m

RACCustomers9m

Aviva Life ~7m Customers

9%

4%

Protection33.2%

Pension23.1%

Annuity7.9%

0.4%1.6%

1.9%

1.1%

<0.1%

Investment29.1%

HealthcareCustomers

2.5m

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 15/25

15

Opportunity from our unique Risk capability

We will drive significant growth in our high margin Risk lines of business

Underlying market growth

Annuity

WP annuity

Life cover - underprovided UK

Unrivalled capability

Mortality and morbidity

Asset / liability expertise

Cutting edge risk science Combined understanding from

Life, GI and healthcare

Market share 2008

0% 5% 10% 15% 20%

PMI

Protection

WP Annuities

Annuities

Source: ABI.

Strong positions in key product sectors

Protection Annuities

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 16/25

16

Opportunity from our momentum in Corporate sector

Drive profitable growth in the Corporate sector

Momentum• Proposition innovation

• Case and tender sizes up

• 82 schemes Q1

• BPA foothold• Global brand

• Full wind down solutions

• Unrivalled combined

capability pensions, BPAand healthcare

Aviva UK Life PVNBP £m(1)

(1) Aviva UK Life PVNBP on an EEV basis

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008

Corporate pensions BPA

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 17/25

17

Opportunity from our distribution reach post RDR

Independents

c. 10,000

General Advisors10,000

Banks, direct19,000

IFAc. 21,000

Tied / multi tied9,000

Banks, direct15,000

High net worth£500k +

Mass affluent£100k – £500k

Middle market

£30k – £100k

Mass market£0 – £30k

Advisers Today Advisers 2013

Provision gap

We will shape our distribution portfolio for value and low cost of acquisition

UK Life Strategy

Commercial focus

Leverage ‘One-to-many’channels

CorporateBulk acquisition (eg BPA)

RBS JVBanks / building socs

Post OfficeOther partners

Grow in-house channel

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 18/25

18

We will seize re-brand opportunity to become the UK’s most recommended insurer

73%

28%

10%

9%

8%

6%

2%

1%

11%

Insurance (home or motor insurance)

Banking/ financial services

Life insurance

Mortgages

Pensions

Savings/ investments

Equity release / Lifetime mortgage

Transport/ travel

Other

What Does Norwich Union Do?

Opportunity for synergy from Aviva’s re-brand

Jan Mar Jul

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 19/25

19

A strategy that delivers on economic realities

Brand

Growth above market

Capital efficiency

Margin and profitability

Distribution control

Back book value creation

% PVNBP growth

Strain / PVNBP

MCEV marginIFRS profit

Own customers

added

VIF per customer

3 year outcome Metric

2010 strategy will drive the same value outcomes as our 2006 focus

Customer base value

Risk businesses

Distribution portfolio

Corporate leadership

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 20/25

20

Our strategic focus

We have clear strategic focus for 2010 - 2012

5. Seize opportunity to become most recommended insurer

4. Shape distribution portfolio for value & low cost acquisition

3. Drive significant profitable growth in Corporate sector

2. Drive significant profitable growth in our Risk business

1. Capitalise on untapped value from existing customers

Focussing

on ourdistinctivecustomerheartland

Global re-brand

Distribution reachand flexibility

All roundproposition strength

Unrivalled data andcapability

Scale of customerbase opportunity

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 21/25

21

Delivery, positioning and a clear way forward

• Rationalise costs

• Simplify the legacy

• Value out of service

• Manage retention

• Develop the business

• Strong balance sheet

• Capital efficiency

Delivering our 2006 strategic promises

UK Life is in excellent shape – for now and the future

5. Seize opportunity to become most recommended insurer

4. Shape distribution portfolio for value & low cost acquisition

3. Drive significant profitable growth in Corporate sector

2. Drive significant profitable growth in our Risk business

1. Capitalise on untapped value from existing customers

Focussingon our

distinctive

customer

heartland

Global re-brand

Distribution reachand flexibility

All roundproposition strength

Unrivalled data andcapability

Scale of customerbase opportunity

Trading through the

recession

Brand re-launch

Commercial mortgages

Re-attribution of the

inherited estate

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 22/25

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 23/25

Andrew Moss NUL18.11.08

Questions & answers

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 24/25

Andrew Moss NUL18.11.08

Thank you and lunch

8/7/2019 Aviva UK: Investor and Analyst Event Part 2, May 2009

http://slidepdf.com/reader/full/aviva-uk-investor-and-analyst-event-part-2-may-2009 25/25

Andrew Moss NUL18.11.08

Investor and Analyst Event, Wednesday 6th

May 2009

UK Life, Driving value through excellence