bab 12

TRANSCRIPT

© 2012 McGraw-Hill Education (Asia)Garrison, Noreen, Brewer, Cheng & Yuen

Standard Costs and Operating

Performance Measures

Chapter 12

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 2

Standard Costs

Standards are benchmarks or “norms” for

measuring performance. In managerial accounting,

two types of standards are commonly used.

Quantity standards

specify how much of an

input should be used to

make a product or

provide a service.

Price standards

specify how much

should be paid for

each unit of the

input.

Examples: Firestone, Sears, McDonald’s, hospitals,

construction and manufacturing companies.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 3

Standard Costs

DirectMaterial

Deviations from standards deemed significant

are brought to the attention of management, a

practice known as management by exception.

Type of Product Cost

Am

ou

nt

DirectLabor

ManufacturingOverhead

Standard

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 4

Variance Analysis Cycle

Prepare standard

cost performance

report

Analyze

variances

Begin

Identify

questions

Receive

explanations

Take

corrective

actions

Conduct next

period’s

operations

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 5

Accountants, engineers, purchasing

agents, and production managers

combine efforts to set standards that encourage

efficient future operations.

Setting Standard Costs

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 6

Setting Standard Costs

Should we use

ideal standards that

require employees to

work at 100 percent

peak efficiency?

Engineer Managerial Accountant

I recommend using practical

standards that are currently

attainable with reasonable

and efficient effort.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 7

Learning Objective 1

Explain how direct

materials standards and

direct labor

standards are set.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 8

Setting Direct Material Standards

Price

Standards

Summarized in

a Bill of Materials.

Final, delivered

cost of materials,

net of discounts.

Quantity

Standards

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 9

Setting Standards

Six Sigma advocates have sought to

eliminate all defects and waste, rather than

continually build them into standards.

As a result allowances for waste and

spoilage that are built into standards

should be reduced over time.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 10

Setting Direct Labor Standards

Rate

Standards

Often a single

rate is used that reflects

the mix of wages earned.

Time

Standards

Use time and

motion studies for

each labor operation.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 11

Setting Variable Manufacturing Overhead

Standards

Rate

Standards

The rate is the

variable portion of the

predetermined overhead

rate.

Quantity

Standards

The quantity is

the activity in the

allocation base for

predetermined overhead.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 12

Standard Cost Card – Variable Production Cost

A standard cost card for one unit of

product might look like this:

A A x B

Standard Standard Standard

Quantity Price Cost

Inputs or Hours or Rate per Unit

Direct materials 3.0 lbs. 4.00$ per lb. 12.00$

Direct labor 2.5 hours 14.00 per hour 35.00

Variable mfg. overhead 2.5 hours 3.00 per hour 7.50

Total standard unit cost 54.50$

B

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 13

Price and Quantity Standards

Price and quantity standards are

determined separately for two reasons:

The purchasing manager is responsible for raw

material purchase prices and the production manager

is responsible for the quantity of raw material used.

The buying and using activities occur at different times.

Raw material purchases may be held in inventory for a

period of time before being used in production.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 14

A General Model for Variance Analysis

Variance Analysis

Price Variance

Difference between

actual price and

standard price

Quantity Variance

Difference between

actual quantity and

standard quantity

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 15

Variance Analysis

Materials price variance

Labor rate variance

VOH rate variance

Materials quantity variance

Labor efficiency variance

VOH efficiency variance

A General Model for Variance Analysis

Price Variance Quantity Variance

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 16

Price Variance Quantity Variance

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

A General Model for Variance Analysis

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 17

Price Variance Quantity Variance

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

A General Model for Variance Analysis

Actual quantity is the amount of direct

materials, direct labor, and variable

manufacturing overhead actually used.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 18

Price Variance Quantity Variance

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

A General Model for Variance Analysis

Standard quantity is the standard quantity

allowed for the actual output of the period.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 19

Price Variance Quantity Variance

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

A General Model for Variance Analysis

Actual price is the amount actually

paid for the input used.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 20

A General Model for Variance Analysis

Standard price is the amount that should

have been paid for the input used.

Price Variance Quantity Variance

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 21

A General Model for Variance Analysis

(AQ × AP) – (AQ × SP) (AQ × SP) – (SQ × SP)

AQ = Actual Quantity SP = Standard Price

AP = Actual Price SQ = Standard Quantity

Price Variance Quantity Variance

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 22

Another Way to Look at the Problems

Actual Quantity x Actual Price = AQ x AP

Price variance

Actual Quantity x Standard Price = AQ x SP

Quantity variance

Standard Quantity x Standard Price = SQ x SP

Total Variance

SQ = (Aouput x standard quantity for production)

= standard quantity allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 23

Learning Objective 2

Compute the direct

materials price and

quantity variances and

explain their significance.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 24

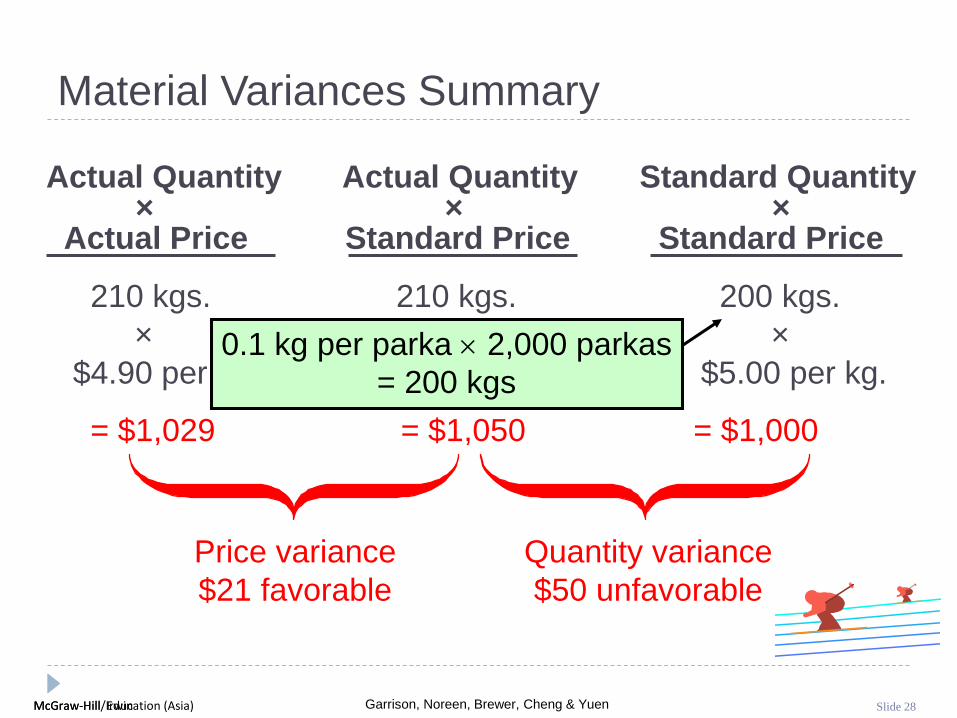

Glacier Peak Outfitters has the following direct

material standard for the fiberfill in its mountain

parka.

0.1 kg. of fiberfill per parka at $5.00 per kg.

Last month 210 kgs. of fiberfill were purchased and

used to make 2,000 parkas. The material cost a

total of $1,029.

Material Variances – An Example

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 25

Material Variances: The Line-by-line Method

AQ x AP = 210 x AP = 1,029

(21) F Price variance

AQ x SP = 210 x 5 = 1,050

50 U Quantity variance

SQ x SP = (2000 x 0.1) x 5 = 1,000

29 U Total Variance

SQ = (Aouput x standard quantity for production)

= standard quantity allowed for the actual output

Calculation of Actual Purchase Price (AP) per unit can be done but is

not necessary because AP will not be used in subsequent calculation

and the total actual purchase cost in total is sufficient for the variance

calculation.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 26

210 kgs. 210 kgs. 200 kgs.

× × ×

$4.90 per kg. $5.00 per kg. $5.00 per kg.

= $1,029 = $1,050 = $1,000

Price variance

$21 favorable

Quantity variance

$50 unfavorable

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

Material Variances Summary

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 27

210 kgs. 210 kgs. 200 kgs.

× × ×

$4.90 per kg. $5.00 per kg. $5.00 per kg.

= $1,029 = $1,050 = $1,000

Price variance

$21 favorable

Quantity variance

$50 unfavorable

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

$1,029 210 kgs

= $4.90 per kg

Material Variances Summary

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 28

210 kgs. 210 kgs. 200 kgs.

× × ×

$4.90 per kg. $5.00 per kg. $5.00 per kg.

= $1,029 = $1,050 = $1,000

Price variance

$21 favorable

Quantity variance

$50 unfavorable

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

0.1 kg per parka 2,000 parkas

= 200 kgs

Material Variances Summary

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 29

Material Variances:Using the Factored Equations

Materials price variance

MPV = AQ (AP - SP)

= 210 kgs ($4.90/kg - $5.00/kg)

= 210 kgs (-$0.10/kg)

= $21 F

Materials quantity variance

MQV = SP (AQ - SQ)

= $5.00/kg (210 kgs-(0.1 kg/parka 2,000 parkas))

= $5.00/kg (210 kgs - 200 kgs)

= $5.00/kg (10 kgs)

= $50 U

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 30

Isolation of Material Variances

I need the price variancesooner so that I can better

identify purchasing problems.

You accountants just don’tunderstand the problems thatpurchasing managers have.

I’ll start computing

the price variance

when material is

purchased rather

than when it’s used.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 31

Material Variances

Hanson purchased and used 1,700 pounds.

How are the variances computed if the amount purchased differs from

the amount used?

The price variance is computed on the entire

quantity purchased.

The quantity variance is computed only on

the quantity used.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 32

Materials Price VarianceMaterials Quantity Variance

Production Manager Purchasing Manager

The standard price is used to compute the quantity variance

so that the production manager is not held responsible for

the purchasing manager’s performance.

Responsibility for Material Variances

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 33

I am not responsible forthis unfavorable material

quantity variance.

You purchased cheapmaterial, so my peoplehad to use more of it.

Your poor scheduling sometimes requires me to

rush order material at a higher price, causing

unfavorable price variances.

Responsibility for Material Variances

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 34

Hanson Inc. has the following direct material standard to manufacture one Zippy:

1.5 pounds per Zippy at $4.00 per pound

Last week, 1,700 pounds of material were purchased and used to make 1,000 Zippies. The

material cost a total of $6,630.

Zippy

Quick Check

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 35

Quick Check

AQ x AP = 1,700 x AP = 6,630

(170) F Price variance

AQ x SP = 1,700 x 4 = 6,800

800 U Quantity variance

SQ x SP = (1000 x 1.5) x 4 = 6,000

630 U Total Variance

SQ = (Aouput x standard quantity for production)

= standard quantity allowed for the actual output

Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 36

Quick Check Zippy

Hanson’s material price variance (MPV)

for the week was:

a. $170 unfavorable.

b. $170 favorable.

c. $800 unfavorable.

d. $800 favorable.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 37

Hanson’s material price variance (MPV)

for the week was:

a. $170 unfavorable.

b. $170 favorable.

c. $800 unfavorable.

d. $800 favorable.

MPV = AQ(AP - SP)

MPV = 1,700 lbs. × ($3.90 - 4.00)

MPV = $170 Favorable

Quick Check Zippy

AQ x AP = 1,700 x AP = 6,630

(170) F Price variance

AQ x SP = 1,700 x 4 = 6,800

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 38

Quick Check

Hanson’s material quantity variance (MQV)

for the week was:

a. $170 unfavorable.

b. $170 favorable.

c. $800 unfavorable.

d. $800 favorable.

Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 39

Hanson’s material quantity variance (MQV)

for the week was:

a. $170 unfavorable.

b. $170 favorable.

c. $800 unfavorable.

d. $800 favorable.MQV = SP(AQ - SQ)

MQV = $4.00(1,700 lbs - 1,500 lbs)

MQV = $800 unfavorable

Quick Check Zippy

AQ x SP = 1,700 x 4 = 6,800

800 U Quantity variance

SQ x SP = (1000 x 1.5) x 4 = 6,000

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 40

1,700 lbs. 1,700 lbs. 1,500 lbs.

× × ×

$3.90 per lb. $4.00 per lb. $4.00 per lb.

= $6,630 = $ 6,800 = $6,000

Price variance

$170 favorable

Quantity variance

$800 unfavorable

Actual Quantity Actual Quantity Standard Quantity× × ×

Actual Price Standard Price Standard Price

Zippy

Quick Check

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 41

Hanson Inc. has the following material standard to

manufacture one Zippy:

1.5 pounds per Zippy at $4.00 per pound

Last week, 2,800 pounds of material were

purchased at a total cost of $10,920, and 1,700

pounds were used to make 1,000 Zippies.

Zippy

Quick Check Continued

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 42

Quick Check Continued

AQp x AP = 2,800 x AP = 10,920

(280) F Price variance

AQp x SP = 2,800 x 4 = 11,200

4,400 U Inventory @ Std cost

AQu x SP = 1,700 x 4 = 6,800

800 U Usage variance

SQ x SP = (1000 x 1.5) x 4 = 6,000 (Quantity variance)

4,920 U Total Variance

AQp = Actual Quantity Purchased

AQu = Actual Quantity used

SQ = (Aouput x standard quantity for production use)

= standard quantity allowed for the actual output

Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 43

Actual Quantity Actual QuantityPurchased Purchased

× ×Actual Price Standard Price

2,800 lbs. 2,800 lbs.

× ×

$3.90 per lb. $4.00 per lb.

= $10,920 = $11,200

Price variance

$280 favorable

Price variance increases

because quantity

purchased increases.

Zippy

Quick Check Continued

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 44

Actual QuantityUsed Standard Quantity

× ×Standard Price Standard Price

1,700 lbs. 1,500 lbs.

× ×

$4.00 per lb. $4.00 per lb.

= $6,800 = $6,000

Quantity variance

$800 unfavorable

Quantity variance is

unchanged because

actual and standard

quantities are unchanged.

Zippy

Quick Check Continued

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 45

Learning Objective 3

Compute the direct labor

rate and efficiency

variances and explain

their significance.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 46

Glacier Peak Outfitters has the following direct labor

standard for its mountain parka.

1.2 standard hours per parka at $10.00 per hour

Last month, employees actually worked 2,500 hours

at a total labor cost of $26,250 to make 2,000

parkas.

Labor Variances – An Example

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 47

Labor Variances

AH x AR = 2,500 x AR = 26,250

1,250 U Rate variance

AH x SR = 2,500 x 10 = 25,000

1,000 U Efficiency variance

SH x SR = (2000 x 1.2) x 10 = 24,000

2,250 U Total Variance

AH = Actual hour paid (and worked in this case)

AR = Actual rate per hour

SR = Standard rate per hour

SH = (Aouput x standard hours for the production)

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 48

Rate variance

$1,250 unfavorable

Efficiency variance

$1,000 unfavorable

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

Labor Variances Summary

2,500 hours 2,500 hours 2,400 hours

× × ×

$10.50 per hour $10.00 per hour. $10.00 per hour

= $26,250 = $25,000 = $24,000

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 49

Labor Variances Summary

2,500 hours 2,500 hours 2,400 hours

× × ×

$10.50 per hour $10.00 per hour. $10.00 per hour

= $26,250 = $25,000 = $24,000

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

$26,250 2,500 hours

= $10.50 per hour

Rate variance

$1,250 unfavorable

Efficiency variance

$1,000 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 50

Labor Variances Summary

2,500 hours 2,500 hours 2,400 hours

× × ×

$10.50 per hour $10.00 per hour. $10.00 per hour

= $26,250 = $25,000 = $24,000

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

1.2 hours per parka 2,000

parkas = 2,400 hours

Rate variance

$1,250 unfavorable

Efficiency variance

$1,000 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 51

Labor Variances:Using the Factored Equations

Labor rate variance

LRV = AH (AR - SR)

= 2,500 hours ($10.50 per hour – $10.00 per hour)

= 2,500 hours ($0.50 per hour)

= $1,250 unfavorable

Labor efficiency variance

LEV = SR (AH - SH)

= $10.00 per hour (2,500 hours – 2,400 hours)

= $10.00 per hour (100 hours)

= $1,000 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 52

Responsibility for Labor Variances

Production Manager

Production managers are

usually held accountable

for labor variances

because they can

influence the:

Mix of skill levels

assigned to work tasks.

Level of employee

motivation.

Quality of production

supervision.

Quality of training

provided to employees.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 53

I am not responsible forthe unfavorable laborefficiency variance!

You purchased cheapmaterial, so it took more

time to process it.

I think it took more time to process the

materials because the Maintenance

Department has poorly maintained your

equipment.

Responsibility for Labor Variances

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 54

Hanson Inc. has the following direct laborstandard to manufacture one Zippy:

1.5 standard hours per Zippy at$12.00 per direct labor hour

Last week, 1,550 direct labor hours wereworked at a total labor cost of $18,910

to make 1,000 Zippies.

Zippy

Quick Check

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 55

Quick Check

AH x AR = 1,550 x AR = 18,910

310 U Rate variance

AH x SR = 1,550 x 12 = 18,600

600 U Efficiency variance

SH x SR = (1000 x 1.5) x 12 = 18,000

910 U Total Variance

AH = Actual hour paid (and worked in this case)

AR = Actual rate per hour

SR = Standard rate per hour

SH = (Aouput x standard hours for the production)

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 56

Hanson’s labor rate variance (LRV) for the

week was:

a. $310 unfavorable.

b. $310 favorable.

c. $300 unfavorable.

d. $300 favorable.

Quick Check Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 57

Hanson’s labor rate variance (LRV) for the

week was:

a. $310 unfavorable.

b. $310 favorable.

c. $300 unfavorable.

d. $300 favorable.

Quick Check

LRV = AH(AR - SR)

LRV = 1,550 hrs($12.20 - $12.00)

LRV = $310 unfavorable

Zippy

AH x AR = 1,550 x AR = 18,910

310 U Rate variance

AH x SR = 1,550 x 12 = 18,600

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 58

Hanson’s labor efficiency variance (LEV)

for the week was:

a. $590 unfavorable.

b. $590 favorable.

c. $600 unfavorable.

d. $600 favorable.

Quick Check Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 59

Hanson’s labor efficiency variance (LEV)

for the week was:

a. $590 unfavorable.

b. $590 favorable.

c. $600 unfavorable.

d. $600 favorable.

Quick Check

LEV = SR(AH - SH)

LEV = $12.00(1,550 hrs - 1,500 hrs)

LEV = $600 unfavorable

Zippy

AH x SR = 1,550 x 12 = 18,600

600 U Efficiency variance

SH x SR = (1000 x 1.5) x 12 = 18,000

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 60

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

Rate variance

$310 unfavorable

Efficiency variance

$600 unfavorable

1,550 hours 1,550 hours 1,500 hours

× × ×

$12.20 per hour $12.00 per hour $12.00 per hour

= $18,910 = $18,600 = $18,000

Zippy

Quick Check

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 61

Learning Objective 4

Compute the variable

manufacturing overhead

rate and efficiency

variances.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 62

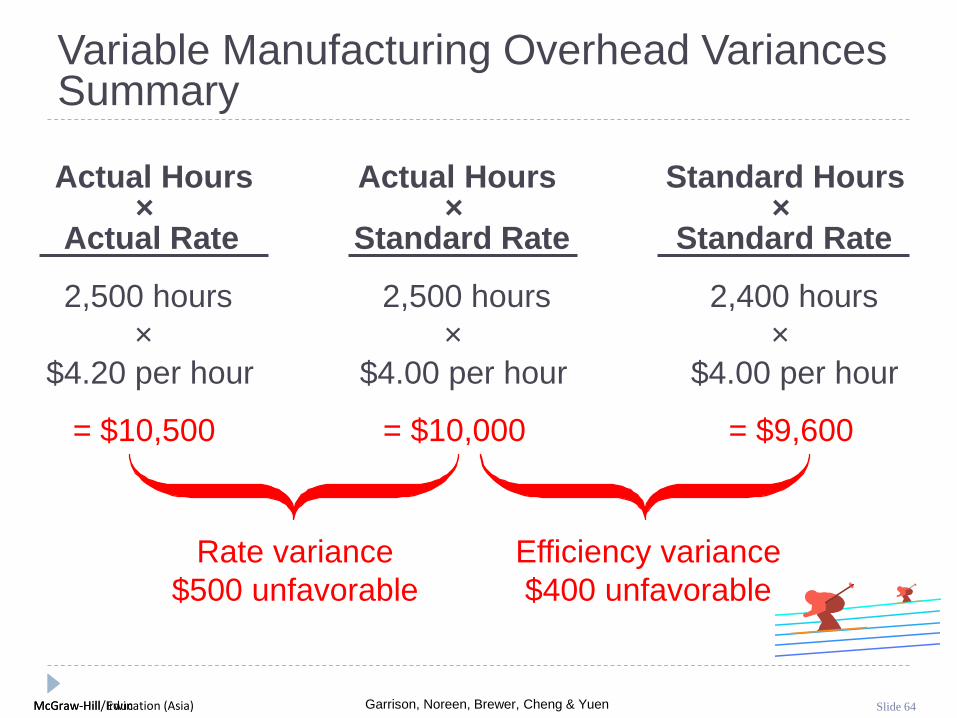

Glacier Peak Outfitters has the following direct variable manufacturing overhead labor standard for its mountain

parka.

1.2 standard hours per parka at $4.00 per hour

Last month, employees actually worked 2,500 hours to make 2,000 parkas. Actual variable manufacturing

overhead for the month was $10,500.

Variable Manufacturing Overhead Variances – An Example

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 63

Variable Manufacturing Overhead Variances

AH x AR = 2,500 x AR = 10,500

500 U Rate variance

AH x SR = 2,500 x 4 = 10,000

400 U Efficiency variance

SH x SR = (2000 x 1.2) x 4 = 9,600

900 U Total Variance

AH = Actual hour paid (and worked in this case)

AR = Actual rate per hour

SR = Standard rate per hour

SH = (Aouput x standard hours for the production)

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 64

2,500 hours 2,500 hours 2,400 hours

× × ×

$4.20 per hour $4.00 per hour $4.00 per hour

= $10,500 = $10,000 = $9,600

Rate variance

$500 unfavorable

Efficiency variance

$400 unfavorable

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

Variable Manufacturing Overhead Variances Summary

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 65

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

2,500 hours 2,500 hours 2,400 hours

× × ×

$4.20 per hour $4.00 per hour $4.00 per hour

= $10,500 = $10,000 = $9,600

Rate variance

$500 unfavorable

Efficiency variance

$400 unfavorable

$10,500 2,500 hours

= $4.20 per hour

Variable Manufacturing Overhead Variances Summary

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 66

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

2,500 hours 2,500 hours 2,400 hours

× × ×

$4.20 per hour $4.00 per hour $4.00 per hour

= $10,500 = $10,000 = $9,600

Rate variance

$500 unfavorable

Efficiency variance

$400 unfavorable

1.2 hours per parka 2,000

parkas = 2,400 hours

Variable Manufacturing Overhead Variances Summary

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 67

Variable Manufacturing Overhead Variances: Using Factored Equations

Variable manufacturing overhead rate variance

VMRV = AH (AR - SR)

= 2,500 hours ($4.20 per hour – $4.00 per hour)

= 2,500 hours ($0.20 per hour)

= $500 unfavorable

Variable manufacturing overhead efficiency variance

VMEV = SR (AH - SH)

= $4.00 per hour (2,500 hours – 2,400 hours)

= $4.00 per hour (100 hours)

= $400 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 68

Hanson Inc. has the following variablemanufacturing overhead standard to

manufacture one Zippy:

1.5 standard hours per Zippy at$3.00 per direct labor hour

Last week, 1,550 hours were worked to make1,000 Zippies, and $5,115 was spent for

variable manufacturing overhead.

Zippy

Quick Check

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 69

Quick Check

AH x AR = 1,550 x AR = 5,115

465 U Rate variance

AH x SR = 1,550 x 3 = 4,650

150 U Efficiency variance

SH x SR = (1000 x 1.5) x 3 = 4,500

615 U Total Variance

AH = Actual hour paid (and worked in this case)

AR = Actual rate per hour

SR = Standard rate per hour

SH = (Aouput x standard hours for the production)

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 70

Hanson’s rate variance (VMRV) for variable

manufacturing overhead for the week was:

a. $465 unfavorable.

b. $400 favorable.

c. $335 unfavorable.

d. $300 favorable.

Quick Check Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 71

Hanson’s rate variance (VMRV) for variable

manufacturing overhead for the week was:

a. $465 unfavorable.

b. $400 favorable.

c. $335 unfavorable.

d. $300 favorable.

Quick Check

VMRV = AH(AR - SR)

VMRV = 1,550 hrs($3.30 - $3.00)

VMRV = $465 unfavorable

Zippy

AH x AR = 1,550 x AR = 5,115

465 U Rate variance

AH x SR = 1,550 x 3 = 4,650

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 72

Hanson’s efficiency variance (VMEV) for

variable manufacturing overhead for the week

was:

a. $435 unfavorable.

b. $435 favorable.

c. $150 unfavorable.

d. $150 favorable.

Quick Check Zippy

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 73

Hanson’s efficiency variance (VMEV) for

variable manufacturing overhead for the week

was:

a. $435 unfavorable.

b. $435 favorable.

c. $150 unfavorable.

d. $150 favorable.

Quick Check

VMEV = SR(AH - SH)

VMEV = $3.00(1,550 hrs - 1,500 hrs)

VMEV = $150 unfavorable

1,000 units × 1.5 hrs per unit

Zippy

AH x SR = 1,550 x 3 = 4,650

150 U Efficiency variance

SH x SR = (1000 x 1.5) x 3 = 4,500

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 74

Rate variance

$465 unfavorable

Efficiency variance

$150 unfavorable

1,550 hours 1,550 hours 1,500 hours

× × ×

$3.30 per hour $3.00 per hour $3.00 per hour

= $5,115 = $4,650 = $4,500

Actual Hours Actual Hours Standard Hours× × ×

Actual Rate Standard Rate Standard Rate

Zippy

Quick Check

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 75

Variance Analysis and Management by Exception

How do I know

which variances to

investigate?

Larger variances, in dollar amount or as a percentage of the

standard, are investigated first.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 76

A Statistical Control Chart

1 2 3 4 5 6 7 8 9

Variance Measurements

Favorable Limit

Unfavorable Limit

••

•• •

••

••

Warning signals for investigation

Desired Value

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 77

Advantages of Standard Costs

Management by

exception

Advantages

Promotes economy

and efficiency

Simplified

bookkeeping

Enhances

responsibility

accounting

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 78

Potential

Problems

Emphasis onnegative may

impact morale.

Emphasizing standardsmay exclude other

important objectives.

Favorablevariances may

be misinterpreted.

Continuousimprovement maybe more important

than meeting standards.

Standard costreports may

not be timely.

Invalid assumptionsabout the relationship

between laborcost and output.

Potential Problems with Standard Costs

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 79

Learning Objective 5

Compute delivery cycle

time, throughput time, and

manufacturing cycle

efficiency (MCE).

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 80

Process time is the only value-added time.

Delivery Performance Measures

Wait TimeProcess Time + Inspection Time

+ Move Time + Queue Time

Delivery Cycle Time

Order Received

ProductionStarted

Goods Shipped

Throughput Time

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 81

Manufacturing

Cycle

Efficiency

Value-added time

Manufacturing cycle time=

Wait TimeProcess Time + Inspection Time

+ Move Time + Queue Time

Delivery Cycle Time

Order Received

ProductionStarted

Goods Shipped

Throughput Time

Delivery Performance Measures

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 82

Quick Check

A TQM team at Narton Corp has recorded the

following average times for production:

Wait 3.0 days Move 0.5 days

Inspection 0.4 days Queue 9.3 days

Process 0.2 days

What is the throughput time?

a. 10.4 days.

b. 0.2 days.

c. 4.1 days.

d. 13.4 days.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 83

A TQM team at Narton Corp has recorded the

following average times for production:

Wait 3.0 days Move 0.5 days

Inspection 0.4 days Queue 9.3 days

Process 0.2 days

What is the throughput time?

a. 10.4 days.

b. 0.2 days.

c. 4.1 days.

d. 13.4 days.

Quick Check

Throughput time = Process + Inspection + Move + Queue

= 0.2 days + 0.4 days + 0.5 days + 9.3 days

= 10.4 days

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 84

Quick Check

A TQM team at Narton Corp has recorded the

following average times for production:

Wait 3.0 days Move 0.5 days

Inspection 0.4 days Queue 9.3 days

Process 0.2 days

What is the Manufacturing Cycle Efficiency (MCE)?

a. 50.0%.

b. 1.9%.

c. 52.0%.

d. 5.1%.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 85

A TQM team at Narton Corp has recorded the

following average times for production:

Wait 3.0 days Move 0.5 days

Inspection 0.4 days Queue 9.3 days

Process 0.2 days

What is the Manufacturing Cycle Efficiency (MCE)?

a. 50.0%.

b. 1.9%.

c. 52.0%.

d. 5.1%.

Quick Check

MCE = Value-added time ÷ Throughput time

= Process time ÷ Throughput time

= 0.2 days ÷ 10.4 days

= 1.9%

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 86

Quick Check

A TQM team at Narton Corp has recorded the

following average times for production:

Wait 3.0 days Move 0.5 days

Inspection 0.4 days Queue 9.3 days

Process 0.2 days

What is the delivery cycle time (DCT)?

a. 0.5 days.

b. 0.7 days.

c. 13.4 days.

d. 10.4 days.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 87

A TQM team at Narton Corp has recorded the

following average times for production:

Wait 3.0 days Move 0.5 days

Inspection 0.4 days Queue 9.3 days

Process 0.2 days

What is the delivery cycle time (DCT)?

a. 0.5 days.

b. 0.7 days.

c. 13.4 days.

d. 10.4 days.

Quick Check

DCT = Wait time + Throughput time

= 3.0 days + 10.4 days

= 13.4 days

© 2012 McGraw-Hill Education (Asia)Garrison, Noreen, Brewer, Cheng & Yuen

Generalized Model of the Row by Row Approach

and Its Preparation of the Performance Report

(Reconcile Actual Results to the Budgeted Figures)

Supplementary Note

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 89

Generalized Model of the Row by Row Approach and Its

Preparation of the Performance Report

(Reconcile Actual Results to the Budgeted Figures)

Actual Quantity x Actual Price = AQ x AP

Price variance

Actual Quantity x Standard Price = AQ x SP

Quantity variance

Standard Quantity x Standard Price = SQ x SP

Total Flexible Variance

Activity Variance

Budgeted Quantity x Standard Price = BQ x SP

Static variance

SQ = (Aouput x standard quantity for production)

= standard quantity allowed for the actual output

BQ = Budgeted quantity

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 90

Performance Report for Variance Analysis:

Recall Example from Chapter 11

© 2012 McGraw-Hill Education (Asia)Garrison, Noreen, Brewer, Cheng & Yuen

Predetermined Overhead Rates and Overhead

Analysis in a Standard Costing System

Appendix 12A

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 92

Learning Objective 6

(Appendix 12A)

Compute and interpret the

fixed overhead budget and

volume variances.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 93

Fixed Manufacturing Overhead Variances:

The Line-by-line method

Actual Fixed Overhead

Budget variance

Budgeted Fixed Overhead = BH x SR (Spending variance)

Volume variance

Applied Fixed Overhead = SH x SR

Total Variance

BH = Budgeted hours (a.k.a. Denominator hours)

SH = (Aouput x standard hours for the production)

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 94

Budget variance

Fixed Overhead Budget Variance

Actual

Fixed

Overhead

Fixed

Overhead

Applied

Budgeted

Fixed

Overhead

Budget

variance

Budgeted

fixed

overhead

Actual

fixed

overhead

= –

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 95

Volumevariance

Fixed Overhead Volume Variance

Actual

Fixed

Overhead

Fixed

Overhead

Applied

Budgeted

Fixed

Overhead

Volume

variance

Fixed

overhead

applied to

work in process

Budgeted

fixed

overhead

= –

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 96

FPOHR = Fixed portion of the predetermined overhead rateDH = Denominator hoursSH = Standard hours allowed for actual output

SH × FRDH × FR

Fixed Overhead Volume Variance

Actual

Fixed

Overhead

Fixed

Overhead

Applied

Budgeted

Fixed

Overhead

Volume variance FPOHR × (DH – SH)=

Volumevariance

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 97

Computing Fixed Overhead Variances

Budgeted production 30,000 units

Standard machine-hour per unit 3 hours

Budgeted machine-hour 90,000 hours

Actual production 28,000 units

Standard machine-hour allowed for the actual production 84,000 hours

Actual machine-hour 88,000 hours

Production and Machine-Hour Data

ColaCo

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 98

Computing Fixed Overhead Variances

Budgeted variable manufacturing overhead 90,000$

Budgeted fixed manufacturing overhead 270,000

Total budgeted manufacturing overhead 360,000$

Actual variable manufacturing overhead 100,000$

Actual fixed manufacturing overhead 280,000

Total actual manufacturing overhead 380,000$

ColaCo

Cost Data

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 99

Predetermined Overhead Rates

Predetermined

overhead rate

Estimated total manufacturing overhead cost

Estimated total amount of the allocation base=

Predetermined

overhead rate

$360,000

90,000 Machine-hour=

Predetermined

overhead rate= $4.00 per machine-hour

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 100

Predetermined Overhead Rates

Variable component of the

predetermined overhead rate

$90,000

90,000 Machine-hour=

Variable component of the

predetermined overhead rate= $1.00 per machine-hour

Fixed component of the

predetermined overhead rate

$270,000

90,000 Machine-hour=

Fixed component of the

predetermined overhead rate= $3.00 per machine-hour

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 101

Applying Manufacturing Overhead

Overhead

applied

Predetermined

overhead rate

Standard hours allowed

for the actual output= ×

Overhead

applied

$4.00 per

machine-hour84,000 machine-hour= ×

Overhead

applied$336,000=

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 102

Fixed Manufacturing Overhead Variances

Actual = = 280,000

10,000 U Budget variance

Budgeted = = 270,000

18,000 U Volume variance

SH x SR = (28000 x 3) x 3 = 252,000

28,000 U Total Underapplied overhead

SH = (Aouput x standard hours for the production)

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 103

Computing the Budget Variance

Budget

variance

Budgeted

fixed

overhead

Actual

fixed

overhead

= –

Budget

variance= $280,000 – $270,000

Budget

variance= $10,000 Unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 104

Computing the Volume Variance

Volume

variance

Fixed

overhead

applied to

work in process

Budgeted

fixed

overhead

= –

Volume

variance= $18,000 Unfavorable

Volume

variance= $270,000 –

$3.00 per

machine-hour( ×$84,000

machine-hour)

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 105

Computing the Volume Variance

FPOHR = Fixed portion of the predetermined overhead rateDH = Denominator hoursSH = Standard hours allowed for actual output

Volume variance FPOHR × (DH – SH)=

Volume

variance=

$3.00 per

machine-hour (× 90,000

machine-hour

– 84,000

machine-hour)

Volume

variance= 18,000 Unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 106

A Pictorial View of the Variances

Actual

Fixed

Overhead

Fixed Overhead

Applied to

Work in Process

Budgeted

Fixed

Overhead

252,000270,000280,000

Total variance, $28,000 unfavorable

Budget variance,

$10,000 unfavorable

Volume variance,

$18,000 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 107

Fixed Overhead Variances –A Graphic Approach

Let’s look at a

graph showing

fixed overhead

variances. We will

use ColaCo’s

numbers from the

previous example.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 108

Graphic Analysis of FixedOverhead Variances

Machine-hours (000)

Budget

$270,000

90

Denominator

hours

0

0

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 109

Graphic Analysis of FixedOverhead Variances

Actual

$280,000

Machine-hours (000)

Budget

$270,000

90

Denominator

hours

0

0

Budget Variance 10,000 U{

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 110

Actual

$280,000

Applied

$252,000

Machine-hours (000)

Budget

$270,000

Graphic Analysis of FixedOverhead Variances

90840

0

Standard

hoursDenominator

hours

Budget Variance 10,000 U

Volume Variance 18,000 U

{{

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 111

Reconciling Overhead Variances and Underapplied or Overapplied Overhead

In a standard

cost system:

Unfavorablevariances are equivalent

to underapplied overhead.

Favorablevariances are equivalentto overapplied overhead.

The sum of the overhead variances

equals the under- or overapplied

overhead cost for the period.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 112

Reconciling Overhead Variances and Underapplied or Overapplied Overhead

Predetermined overhead rate (a) 4.00$ per machine-hour

Standard hours allowed for the actual output (b) 84,000 machine hours

Manufacturing overhead applied (a) × (b) 336,000$

Actual manufacturing overhead 380,000$

Manufacturing overhead underapplied or

overapplied 44,000$ underapplied

Computation of Underapplied Overhead

ColaCo

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 113

Variable Overhead Variances

AH x AR = = 100,000

12,000 U Rate variance

AH x SR = 88,000 x 1 = 88,000

4,000 U Efficiency variance

SH x SR = 84,000 x 1 = 84,000

(= 28,000 x 3) 16,000 U Total Variance

SR = Standard rate per hour = Total underapplied

SH = (Aouput x standard hours for the production) variable overhead

= standard hours allowed for the actual output

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 114

Computing the Variable Overhead Variances

Variable manufacturing overhead rate varianceVMRV = (AH × AR) – (AH × SR)

= $100,000 – (88,000 hours × $1.00 per hour)

= $12,000 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 115

Computing the Variable Overhead Variances

Variable manufacturing overhead efficiency varianceVMEV = (AH × SR) – (SH × SR)

= $88,000 – (84,000 hours × $1.00 per hour)

= $4,000 unfavorable

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 116

Computing the Sum of All Variances

Variable overhead rate variance 12,000$ U

Variable overhead efficiency variance 4,000 U

Fixed overhead budget variance 10,000 U

Fixed overhead volume variance 18,000 U

Total of the overhead variances 44,000$ U

Computing the Sum of All variances

ColaCo

© 2012 McGraw-Hill Education (Asia)Garrison, Noreen, Brewer, Cheng & Yuen

Journal Entries to Record

Variances

Appendix 12B

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 118

Learning Objective 7

(Appendix 12B)

Prepare journal entries

to record standard

costs and variances.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 119

Appendix 12BJournal Entries to Record Variances

We will use information from the Glacier Peak Outfitters

example presented earlier in the chapter to illustrate journal

entries for standard cost variances. Recall the following:

Material

AQ × AP = $1,029

AQ × SP = $1,050

SQ × SP = $1,000

MPV = $21 F

MQV = $50 U

Labor

AH × AR = $26,250

AH × SR = $25,000

SH × SR = $24,000

LRV = $1,250 U

LEV = $1,000 U

Now, let’s prepare the entries to record

the labor and material variances.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 120

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Raw Materials 1,050

Materials Price Variance 21

Accounts Payable 1,029

To record the purchase of material

Work in Process 1,000

Materials Quantity Variance 50

Raw Materials 1,050

To record the use of material

Appendix 12BRecording Material Variances

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 121

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Work in Process 24,000

Labor Rate Variance 1,250

Labor Efficiency Variance 1,000

Wages Payable 26,250

To record direct labor

Appendix 12BRecording Labor Variances

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 122

Cost Flows in a Standard Cost System

Inventories are recorded at standard cost.

Variances are recorded as follows:

Favorable variances are credits, representing

savings in production costs.

Unfavorable variances are debits, representing

excess production costs.

Standard cost variances are usually closed out

to cost of goods sold.

Unfavorable variances increase cost of goods sold.

Favorable variances decrease cost of goods sold.

McGraw-Hill Education (Asia) Garrison, Noreen, Brewer, Cheng & YuenMcGraw-Hill/Irwin Slide 123

End of Chapter 12