back to reality - oliver wyman · oliver wyman is the leading management consulting firm, combining...

TRANSCRIPT

Consumer Finance in EuropeBack to Reality

Contents

Executive Summary 3

Introduction 7

Trends in European Consumer Credit Markets 11

Implications for Consumer Credit Players 33

The Emergence of New Business Models 45

Conclusion 53

3Copyright 2008 © Oliver Wyman

Executive Summary

A more challenging environmentConsumer credit was one of the fastest-growing and most profitable sectors until 2006. Following a period of high growth from 2004 to 2006, it has witnessed a further spike, with volume CAGR topping 9% in Europe. The sector has thus attracted the attention of new entrants, whilst a frenetic activity of M&A has pushed valuation of specialised players ever higher.

Last year we observed a turning point due to both contingent and structural conditions, as some mature markets reached saturation and economic conditions worsened. The rise of interest rates – and of credit losses as families become more indebted – has eroded margins. At the same time, intensified competition has pushed prices downward, particularly in mature segments. With the new EU directive and the introduction of SEPA, regulators are impacting the industry as well. Though some initiatives may possibly widen the markets, we believe that the net effect of the new regulation will have a negative impact on the industry’s profit pool. Lastly, the sub-prime crisis has forced players to reconsider funding as a key condition for staying in the game.

As a consequence, contrary to the conventional wisdom of the past years, a decoupling between volume and profit growth is taking place. New volumes will not necessarily bring profits.

Yet, consumer credit is still an attractive area of the European financial services industry. With €1.2 TN outstandings at the end of 2007 it represents 25% of global volumes and is second only to North America as a regional market. Moreover, we believe that EU markets will keep growing, albeit at a slower pace, and that in the next five years, volumes will still increase at 5% CAGR.

Go east – Go southThis overall view hides a wealth of opportunities since the sector, in particular with respect to margin growth, is becoming increasingly polarised by countries, client segments and products. For players able to exploit these skews, consumer credit will still provide high margins and fast growth.

4 Copyright 2008 © Oliver Wyman

From a geographic standpoint, we saw the emergence of new growth engines, within and outside the EU. In a global context, we forecast that, in terms of outstandings, the US and the EU will lose at least 10% global market share in the next five years, whilst the most dynamic regions (China, Latin America, Turkey, Russia and India) will increase from 18% in 2008 to 27% in 2012. In particular, BRIC countries (Brazil, India, Russia, China) will experience annual growth between 20% and 30% and their profit pools will grow even faster. In Europe, mature markets will lose profit and volume shares to maturing countries, such as Italy and Greece, and to emerging countries, such as CEE.

Within the same markets, the profitability skew between product and client segments will widen, fuelled by competitive intensity and regulation. The following trends can already be highlighted:

Point-of-sale finance has often become a no-profit zone in mature �

markets as merchants negotiated better terms

Personal lending has witnessed strong volume growth across �

Europe, but profit grew less than proportionately since many banks have attacked the market with low-price offers

Credit cards proved the most resilient among traditional products, �

registering strong balance growth and high margins across Europe

Opportunities in non-conforming segments and in home equity �

products are currently constrained due to the sub-prime crisis, however their development has only been delayed

A new strategic agenda requiredNeeding to adapt to a tougher environment, winners will change their approach from a primary focus on business development to a more balanced and complex strategic agenda. There will be no magic recipe but we believe the winning agenda should include the following main levers.

Driving efficiency to the next level

Conducting cost reduction efforts �

Implementing Straight-Through Processing (STP) by automating and �

digitalising key processes

Achieving cross-border operating synergies through regional platforms �

and centres of excellence

Responding to worsening credit conditions

Optimizing risk organization, processes and tools along the value chain �

Enhancing collection performance through highly powered analytical tools �

Promoting growth Expanding footprint by entering high potential emerging geographies �

(BRIC, Middle East, South East Asia)

Targeting new client segments with dedicated value propositions �

(migrant populations, youngsters, retirees…)

Innovating the product offer (bundled loans and saving/investment �

products, cards with pre-approved loans that can be activated by SMS…)

Optimising distribution channels with a specific focus on the Internet �

and intermediaries (e.g. agents and brokers)

5Copyright 2008 © Oliver Wyman

Consolidation: From big to huge

Against this background, new business models will emerge. Consolidation both at the global level and within markets will determine a dramatic increase in size of the main players. By 2015 the top 10 players will manage at least €200 BN of outstandings. To exploit economies of scope, as well as manage increasingly complex structures and diverse markets, these players will have to rethink their organisational model and develop regional platforms and centres of excellence.

Another growing phenomenon is the convergence of consumer credit and other forms of retail lending. Leading European specialists tended to focus solely on unsecured consumer lending. As illustrated by recent major initiatives, some players are now trying to sell a broader range of retail lending products, starting with mortgages. It is difficult to say at this stage whether or not retail lending convergence will generalise. We see a scenario where the convergence trend could extend to other asset classes such as SME lending. However, it is worth mentioning that some leading industry specialists still consider that consumer credit should be their sole area of focus.

Lastly, driven by technological progress and the attitude of new consumers, a new breed of entrants has the potential to change the infrastructure on which consumer credit rests, particularly for cards, and could eventually move upstream. The revolution in payment methods (e.g. PayPal) and the rise of social lending (e.g. Zopa) offer both opportunities and challenges to incumbents. Although it is not yet apparent that these innovations will radically alter the consumer credit landscape, players clearly need to understand these trends and be ready to position themselves for competitive advantage.

7Copyright 2008 © Oliver Wyman

Purpose of the reportThis report describes and analyses recent trends in the European consumer credit markets and gives an outlook on future growth and profit sources. It echoes the previous report published by Oliver Wyman in 2005 to the extent that we aim to help financial institutions decide upon where and how to compete. In addition, we want to highlight how a different set of capabilities and business priorities is being brought to the fore, particularly given the emerging market and regulatory trends.

With that in mind, this report aims to present:

An overview of recent evolutions in the European consumer credit �

sector, contrasting sub-segments and local markets

Insights on emerging trends �

An evaluation of market opportunities in light of the current �

situation and the future outlook

An analysis of the emerging key success factors that will �

differentiate future winners

Conclusions on emerging business models and the priorities �

required to develop the right strategic agenda

ApproachAs we noticed three years ago, the European consumer credit market is still an aggregate of heterogeneous local market realities. However, we believe that stronger communalities and convergence trends are taking place. We therefore carried out an analysis of regional consumer credit environments, according to common features such as competition, regulation and demand-side factors.

We then projected these patterns into the future, in order to look at both absolute market growth and evolution of profit pools by product and consumer segment. Finally, we considered these emerging trends to understand the skills needed to meet the challenges they present, and to determine which business models are best suited in the coming environment.

Introduction

8 Copyright 2008 © Oliver Wyman

The analysis in this report are based upon a wide range of sources, including:

Published reports and articles from official national data agencies, �

national central banks, consumer credit associations and the World Bank

Direct interviews with major industry players and experts �

Oliver Wyman’s and Santander’s global expertise and thought �

leadership in consumer credit

Scope of the reportThe report primarily looks at consumer credit markets within the perimeter of EU 27 countries1. For comparison purposes, however, we also consider some non-EU 27 consumer credit markets as well as regional blocks of the world:

North America � 2

Latin America �

North Asia � 3

Middle East �

South Asia � 4

Rest of the World � 5

Rest of Europe � 6

We cover consumer credit products excluding the residential mortgage business. In particular, we focus on general-purpose loans (personal loans), revolving credit (with or without a plastic card) and loans linked to specific purchases (such as point-of-sale finance for cars and consumer durables).

Additionally, we consider products such as home equity loans (HELs) and home equity lines of credit (HELOCs). Currently a minor segment, they will become more important due to emerging trends.

1 EU 27 includes Austria, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, and the United Kingdom

2 North America includes the United States and Canada3 North Asia includes Japan, South Korea, and China4 South Asia includes Singapore, Taiwan, Thailand, Vietnam and Indonesia5 Rest of the World includes Africa, India, Australia and New Zealand6 Rest of Europe includes Russia, Ukraine, Belarus, Moldova and Turkey

9Copyright 2008 © Oliver Wyman

Format of the reportThis report is divided into three main sections:

Trends in European consumer credit markets over the period �

2004-2006: In this section, we compare at country level the recent evolutions in volume, growth and penetration within the consumer credit market. We then analyse profitability drivers to understand the main issues that confront credit institutions before assessing the impact of changes in regulatory environments. Lastly, we describe and explain our volume and profit growth projections per market

Implications for consumer credit players: � A summary of the conclusions that we put forth in the 2005 report are addressed in the light of recent changes in the European consumer credit market. We then describe new key success factors, proposing a winning strategic agenda for players in the consumer credit industry

The emergence of new business models: � In this last section, we present a map of emerging business models and our views on their chances of succeeding in tomorrow’s consumer credit market

11Copyright 2008 © Oliver Wyman

IntroductionIn this section we compare the market growth, penetration and product mix of the various markets, in order to understand the maturity levels and emerging convergence trends among them. Our analysis is conducted from the perspective of non-EU markets so as to draw conclusions on the relative attractiveness of different areas. We also analyse profitability trends and their underlying cost and revenue drivers. Thus, we aim to explain the drivers that are shaping industry profit pools, detailing the emerging key changes in competition and regulation, as well as the consequences for the market.

Volume, penetration and product mix of marketsBy the end of 2006, the overall European market passed over the €1 TN mark in outstandings and was the second-largest regional market, representing about one-fourth of the world market and one-half of the US market.

Looking at the distribution of outstandings, high concentration is a characteristic of consumer credit at the international level. Overall, the two main regions represented 77% of consumer credit stock in 2006. The next largest regional block is North Asia (including China, Korea and Japan), which represents only 9% of the total. All other regional blocks each represent 2% to 3% of global shares. Even the Rest of Europe block, which includes the most dynamic countries adjacent to the EU market, represents only 2% of global outstandings.

Trends in European Consumer Credit Markets

12 Copyright 2008 © Oliver Wyman

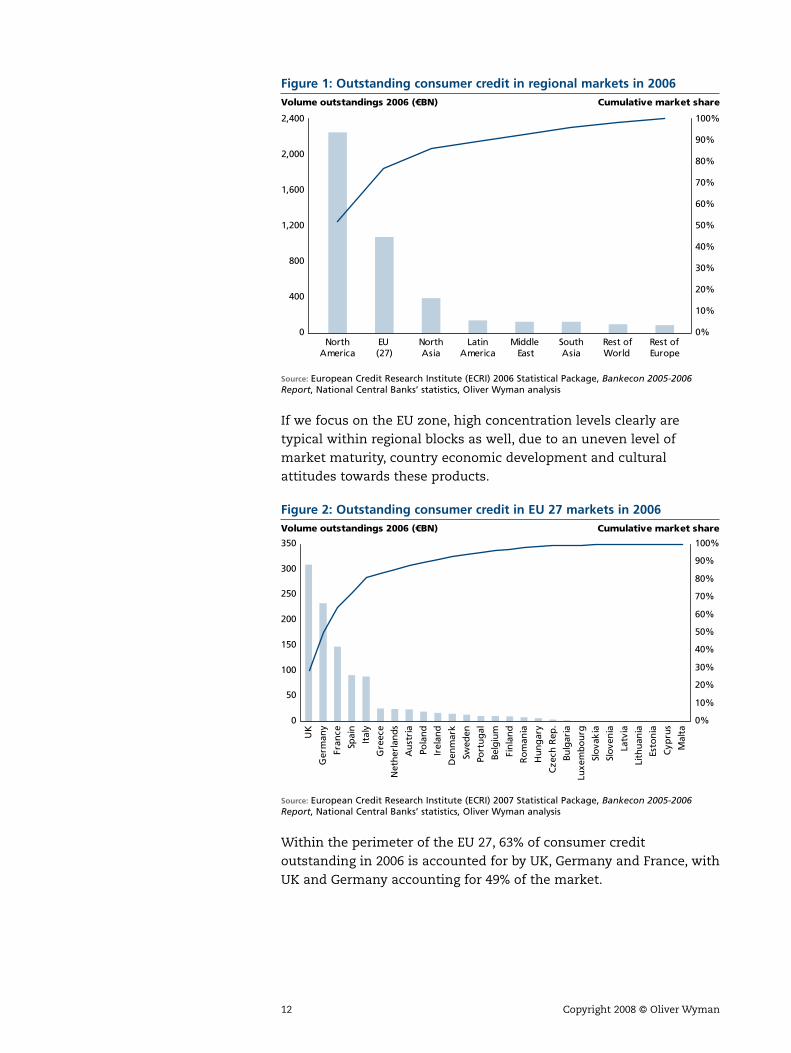

Figure 1: Outstanding consumer credit in regional markets in 2006

0

400

800

1,200

1,600

2,000

2,400

NorthAmerica

EU (27)

NorthAsia

LatinAmerica

Middle East

SouthAsia

Rest ofWorld

Rest ofEurope

Volume outstandings 2006 (€BN)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cumulative market share

Source: European Credit Research Institute (ECRI) 2006 Statistical Package, Bankecon 2005-2006 Report, National Central Banks’ statistics, Oliver Wyman analysis

If we focus on the EU zone, high concentration levels clearly are typical within regional blocks as well, due to an uneven level of market maturity, country economic development and cultural attitudes towards these products.

Figure 2: Outstanding consumer credit in EU 27 markets in 2006

0

50

100

150

200

250

300

350

UK

Ger

man

y

Fran

ce

Spai

n

Ital

y

Gre

ece

Net

her

lan

ds

Au

stri

a

Pola

nd

Irel

and

Den

mar

k

Swed

en

Port

ug

al

Belg

ium

Fin

lan

d

Ro

man

ia

Hu

ng

ary

Cze

ch R

ep.

Bulg

aria

Luxe

mb

ou

rg

Slo

vak

ia

Slo

ven

ia

Latv

ia

Lith

uan

ia

Esto

nia

Cyp

rus

Mal

ta

Volume outstandings 2006 (€BN)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cumulative market share

Source: European Credit Research Institute (ECRI) 2007 Statistical Package, Bankecon 2005-2006 Report, National Central Banks’ statistics, Oliver Wyman analysis

Within the perimeter of the EU 27, 63% of consumer credit outstanding in 2006 is accounted for by UK, Germany and France, with UK and Germany accounting for 49% of the market.

13Copyright 2008 © Oliver Wyman

These differences in market sizes are partly due to the demographic and economic potential, but also are compounded by radical differences in penetration levels as measured by the ratio of outstanding consumer credit over national GDP. From this perspective, we noticed that during the last three years, even though the European “high penetration” group was mainly composed of the largest markets, some smaller countries such as Greece and Ireland also joined the group. Indeed, a process of convergence in relative penetration versus the leaders is quickly taking place in the most dynamic emerging markets; as a consequence, concentration within Europe is decreasing.

Figure 3: Market penetration per consumer credit product in Europe in 2006

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Volume relative to GDP

Auto loans POS/Instalment Personal loans Credit Cards/Revolving

UK

Den

mar

k

Gre

ece

Irel

and

No

rway

Ger

man

y

Spai

n

Au

stri

a

Fran

ce

Swed

en

Hu

ng

ary

Port

ug

al

Fin

lan

d

Ital

y

Pola

nd

Bel

giu

m

Cze

ch R

ep.

Slo

vaki

a

Source: European Credit Research Institute (ECRI) 2006 Statistical Package, Bankecon 2005-2006 Report, IMF statistics, National Central Banks’ statistics, Eurofinas statistics, Oliver Wyman analysis

Penetration varies widely across Europe. Countries with over 10% of penetration mainly are large, mature markets (e.g. UK, Germany and Austria), even though the novelty of recent years is represented by Ireland, Norway, Denmark and Greece, which, despite their young and small markets, quickly have reached the highest levels. The UK is always a separate case, with a penetration of 16%, which is about 30% more than any other EU country.

A heterogeneous group is within 5% and 10%; as for highly penetrated countries, there is a mix of fast-growing markets such as Italy and Spain, as well as slow-moving, traditional ones like France, whose relative importance is declining.

14 Copyright 2008 © Oliver Wyman

This pattern of young and fast-growing versus traditional and static countries repeats itself in the low penetration group (below 5% of volume relative to GDP). For example, Belgium always has been culturally adverse to consumer credit, whilst low volume ratios in Slovakia and Czech Republic are due to very young markets.

However, penetration is only a partial way to understand a country’s attitude and potential in consumer credit.

An analysis of the product mix in European countries shows a strong linkage between the type of products developed in the market, current penetration and future potential.

On one side, we have developed markets in which credit cards account for a high market share, with the UK and Ireland as the most prominent examples. In these countries high penetration mainly is the result of consumer credit products being heavily used as a payment method, not only as a means to borrow money. In itself, this factor significantly increases both actual penetration and latent demand.

Other mature markets are characterised by a low adoption of credit card products. Typical examples of this include Germany, Austria and to a lesser extent France, in which penetration has reached an early plateau at around 10% of GDP.

Italy and Spain both have a similar product mix, with a high share of traditional products (POS and car financing) and low credit card usage. Spain leads Italy in absolute penetration terms, but both are likely to have a similar saturation plateau conditioned by a lower propensity to revolve. Both differ from the mature continental European block in which they are still growing fast whilst starting from a smaller base. Nordic markets (Sweden, Norway, Finland and Denmark) are instead highly concentrated on personal loans as a consequence of their predominant banking distribution channel. They see little development in POS outstandings.

Lastly, we have emerging countries (CEE countries, Greece and Turkey) which are following an unusual pattern of development. These countries have seen credit cards develop early, often in innovative ways before or at the same time as more traditional sectors (POS and car financing).

15Copyright 2008 © Oliver Wyman

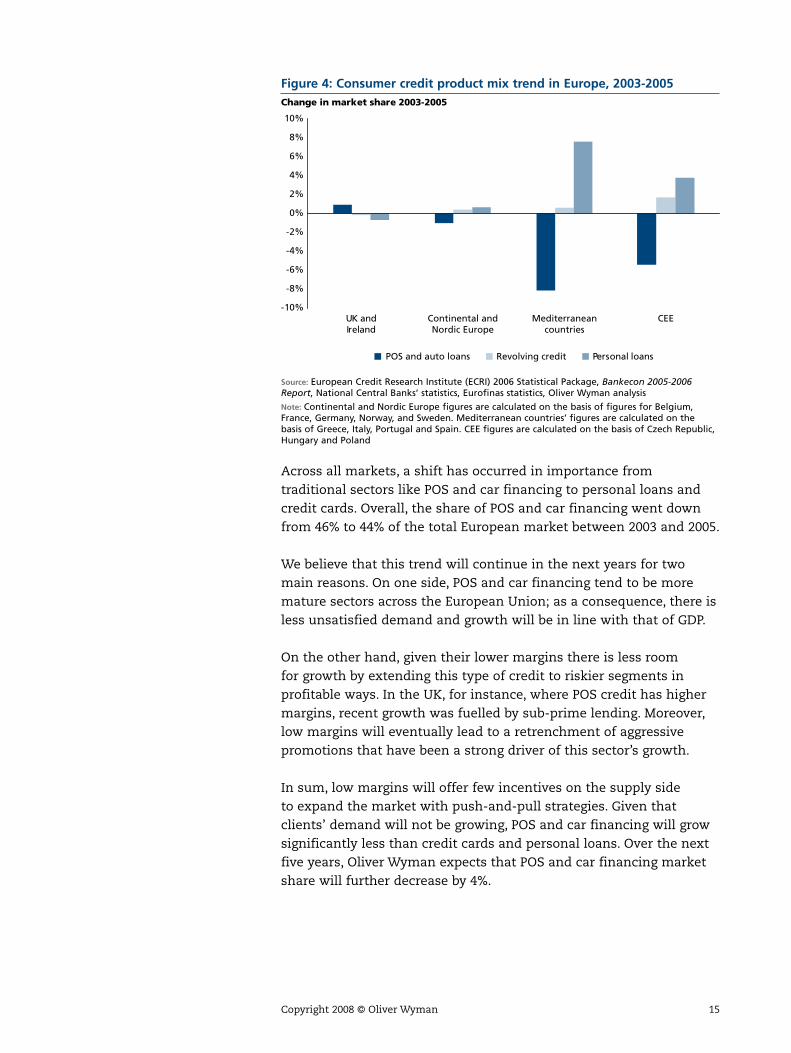

Figure 4: Consumer credit product mix trend in Europe, 2003-2005

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

UK andIreland

Continental andNordic Europe

Mediterraneancountries

CEE

Change in market share 2003-2005

POS and auto loans Revolving credit Personal loans

Source: European Credit Research Institute (ECRI) 2006 Statistical Package, Bankecon 2005-2006 Report, National Central Banks’ statistics, Eurofinas statistics, Oliver Wyman analysis

Note: Continental and Nordic Europe figures are calculated on the basis of figures for Belgium, France, Germany, Norway, and Sweden. Mediterranean countries’ figures are calculated on the basis of Greece, Italy, Portugal and Spain. CEE figures are calculated on the basis of Czech Republic, Hungary and Poland

Across all markets, a shift has occurred in importance from traditional sectors like POS and car financing to personal loans and credit cards. Overall, the share of POS and car financing went down from 46% to 44% of the total European market between 2003 and 2005.

We believe that this trend will continue in the next years for two main reasons. On one side, POS and car financing tend to be more mature sectors across the European Union; as a consequence, there is less unsatisfied demand and growth will be in line with that of GDP.

On the other hand, given their lower margins there is less room for growth by extending this type of credit to riskier segments in profitable ways. In the UK, for instance, where POS credit has higher margins, recent growth was fuelled by sub-prime lending. Moreover, low margins will eventually lead to a retrenchment of aggressive promotions that have been a strong driver of this sector’s growth.

In sum, low margins will offer few incentives on the supply side to expand the market with push-and-pull strategies. Given that clients’ demand will not be growing, POS and car financing will grow significantly less than credit cards and personal loans. Over the next five years, Oliver Wyman expects that POS and car financing market share will further decrease by 4%.

16 Copyright 2008 © Oliver Wyman

Moreover, we can conclude that both Anglo-Saxon and emerging countries are converging towards a product mix in which cards play a larger role. Countries in Continental Europe, however, are likely to plateau at lower penetration level, whilst stabilising around a different product mix characterised by a higher percentage of personal loans.

Lastly, given the strong growth in emerging Europe and the slower growth and sometimes stagnation in mature European countries, smaller markets will continue to represent an ever-increasing share of consumer credit outstandings.

Patterns of growth in European markets As a first step in understanding growth patterns in Europe, we compared the EU with all other regional markets.

Figure 5: Regional consumer credit market shares vs. growth, 2004-2006

NorthAmerica

EU (27)

NorthAsia

LatinAmerica

Middle East

SouthAsia

Rest ofWorld

Rest ofEurope

Market share in 2006

0%

5%

10%

15%

20%

25%

30%

0%

10%

20%

30%

40%

50%

60%

CAGR 2004-2006

Market share 2006 CAGR 2004-2006

Source: European Credit Research Institute (ECRI) 2006 Statistical Package, Bankecon 2005-2006 Report, National Central Banks’ statistics, Oliver Wyman analysis

Europe overall is an attractive market compared to the rest of the world; in 2006 the EU represented 25% of global outstandings and had a period of steady and significant growth. Yet, its market share is decreasing, whilst emerging countries with fast-growing economies and higher latent demand are growing faster.

Consumer credit historically has taken off in order to fuel the spending of the emerging middle class. Thus, those regions with a large demographic pool whose income per capita is growing fast, but is below €5,000, represent the true challenger to the EU’s market share.

17Copyright 2008 © Oliver Wyman

The largest region of this group is the North Asian market (including China, Japan and South Korea), which in 2006 represented 9% of the global market and since 2003 recorded year-on-year growth of 11%. This growth can be largely attributed to the dynamism of the Chinese economy, which exactly fits the profile of the emerging consumer credit market.

Within the same group are all other areas of the developing world that are in a current phase of strong and relatively stable growth, including Latin America, Rest of Europe (particularly Russia and Turkey), Rest of the World (in particular India) and overall, despite political hot spots, the Middle East. This group represents 9% of the global market with a pace of growth since 2003 that has more than doubled Europe’s.

On the other side, the most interesting international example is from the US, the most advanced and largest world market. In the period from 2003 to 2005, despite the world’s highest penetration, the US experienced a spurt of growth with CAGR of 4%. This growth has been driven by the success of HEL and HELOC, which cannibalised the conforming credit card market, and by the growth of high-risk credit card and unsecured loans. The latter is now collapsing due to the sub-prime crisis. Moreover, in 2006 higher interest rates and a shrinking home equity market contributed to reversing the pre-existing buoyant economic condition, and growth eventually stalled.

The lessons learned from the US are that, on the one hand, European consumer credit has a lot of potential headroom both in new segments and in new products; yet, there clearly is an upper limit to the level of indebtedness, even in highly sophisticated markets. This level depends on interest rates, and now is being reached in the US. Although Europe as a whole is far from this level, individual countries such as the UK have achieved a level of saturation that makes growth heavily dependent upon macro-economic conditions.

As a consequence, we forecast that, in terms of outstandings, the US and Europe will lose at least 10% global market share in the next five years, whilst the most dynamic regions (China, Latin America, Turkey, Russia and India) will increase from 18% in 2008 to 27% in 2012. In particular, BRIC countries will experience annual growth between 20% and 30% over the next five years.

18 Copyright 2008 © Oliver Wyman

Within Europe, when jointly analysing growth and penetration in individual markets, current penetration appears to be only one of the many different growth drivers. Current penetration alone is not a good indicator of a market’s potential attractiveness, in terms of unsatisfied credit demand.

Figure 6: Consumer credit market penetration vs. growth in Europe, 2003-2006CAGR outstandings 2003-2006

Outstanding/GDP 2006

AustriaBelgium

Czech Republic

DenmarkFinland

France Germany

Greece

Hungary

IrelandItaly

Luxembourg Norway

Poland

Portugal

Russia

SlovakiaSpain

Sweden

Turkey

UK0%

0%

20%10%

30%40%50%60%70%80%90%

100%110%120%130%140%150%

2% 4% 6% 8% 10% 12% 14% 16% 18%

Source: European Credit Research Institute (ECRI) 2006 Statistical Package, Bankecon 2005-2006 Report, National Central Banks’ statistics, IMF statistics, Oliver Wyman analysis

Volume growth was strong across the whole of Europe until 2005, driven not only by the impetus of emerging countries, but also by the largest ones, barring Germany.

After 2005, changes in fundamentals heavily impacted the three main European markets. On the demand side, in particular, rising interest rates have impacted consumer credit appetite. On the supply side, worsening credit quality and the recent liquidity/sub-prime crisis have reduced the aggressiveness of some players, particularly in the UK.

Within this worsened macro- and micro-economic context, Germany and France had less room for growth due to their product mix structure. In fact, Germany’s growth was almost flat between 2005 and 2006; the effect of product innovation thus far has not been strong enough to break through market inertia. In France, personal loans and low APRs have driven volume growth. In both countries growth perspectives are being stifled by regulation that eventually limits access within conforming perimeters.

Italy and Spain have grown significantly, albeit from different penetration bases. On the supply side, a more active banking approach, the opening of new segments (non-conforming) and the

19Copyright 2008 © Oliver Wyman

broadening of existing channels (such as the Internet and agents) have led to an 18% year-on-year growth between 2003 and 2006 in both countries. On the demand side, consumers increasingly are willing to raise their indebtedness to support their living standards. Italy and Spain are proving that overall a convergence towards penetration plateaus differs from country to country, but is at a minimum above 10% of GDP.

Lastly, CEE countries and other emerging markets are displaying very high growth rates. Between 2003 and 2006, the fastest-growing countries have been Russia, Hungary, Czech Republic, Slovakia, Greece, Poland, Turkey and Estonia. Russia and Turkey, in particular, have proven to be the most dynamic markets, nearly doubling their penetration over the last two years. In these countries, strong economic growth is insulating consumers from feeling the effects of rising interest rates, whilst competition is expanding accessible markets buoyed by light regulation and high margins. Moreover, although the countries in this group are highly differentiated in terms of penetration – ranging from high penetration levels (Greece with 12% in 2006) to relatively low penetration levels (Czech Republic with 4% in 2006) – they all share fast growth trajectory, full-range product development and high saturation levels, thereby ensuring a strong growth potential. If we then consider their recent take-off, we realise that the current gaps in penetration are only due to their different stages within a broader, faster convergence process.

Profitability of consumer credit

Profit landscapeUntil the end of 2004, consumer credit was seen as both a revenue and a profit growth engine. Based on this assumption, banks have increased their investments in consumer credit, and new players have entered the arena. Yet, over the last three years we witnessed an increasing decoupling of volume and profit growth.

Overall profit margins have decreased and become more variable by country and product segment. Moreover, the skews in profitability have widened dramatically between the best players – those who are capable of adapting quickly to new challenges – and the laggards. “Free lunch” is no longer available in consumer credit, and volume growth is not sufficient to be profitable for players with capabilities’ gaps.

Profit pools overall have increased since 2004, but at a slower pace than volumes and with stark and growing differences between segments and countries.

20 Copyright 2008 © Oliver Wyman

In POS and car financing segments, profit pools have been shrinking, although this data is heavily dependent on how price transfers for new client acquisition are computed.

Personal loan profit pools have grown strongly due to booming volumes offsetting decreased margins, whilst credit card profit pools have grown at the same pace as volumes.

Figure 7: Global evolution of profit pools by product segment in Europe, 2004-2006

0

2

4

6

8

10

12

14

16

18

2004 2005 2006

Profit pools (€BN)

Auto POS Personal loans Credit cards

Source: Oliver Wyman analysis

From a geographic perspective, mature non-Anglo-Saxon markets within the EU have been hit hardest by shrinking margins; the worst evolution of the profit pool was registered in Germany with an overall reduction of economic profit.

In the UK, profit pools increased in line with volumes due to a product mix skewed towards high profit products, the shift from focusing on Net Interest Margins (NIM) to higher fees and commissions (particularly late fees and commissions on CPI) and high profitability in new risky segments. On the other hand, the UK also is the most competitive market, and the skew between best practices and laggards is the highest.

In maturing countries, strong volume growth and a shift in the product mix are offsetting lower margins, producing a healthy 9% growth p.a. in economic profit.

21Copyright 2008 © Oliver Wyman

Lastly, in emerging countries booming volumes have driven an explosive growth in economic profit, but starting from a small base and consequently still accounting for a minor share of the European pool. As seen in Figure 8, though the most mature markets have lost ground in relative terms, they still remain the main profit pools.

Figure 8: Evolution of profit pools in Europe between 2004 and 2006Profit pools (€BN)

5.0

Cumulative market share

100%

Profit pool 2004 Profit pool 2006

Cumulative profit pool 2004 Cumulative profit pool 2006

Net

her

lan

ds

Luxe

mb

ou

rg

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0%

20%

40%

60%

80%

UK

Fran

ce

Ger

man

y

Ital

y

Spai

n

Pola

nd

Swed

en

Port

ug

al

No

rway

Ro

man

ia

Au

stri

a

Irel

and

Gre

ece

Fin

lan

d

Den

mar

k

Belg

ium

Cze

ch R

ep.

Hu

ng

ary

Slo

vak

ia

Source: ECRI, Bankecon, National Central Banks’ statistics, Oliver Wyman analysis

If we broaden our view to other regional markets, we can see that the US and the EU are still the dominant economic profit pools. However, emerging regions are growing faster, and some regions, such as the BRIC countries, already represent significant opportunities.

Figure 9: Evolution of regional profit pools in the world between 2004 and 2006

0

10

20

30

40

NorthAmerica

EU(27)

NorthAsia

LatinAmerica

SouthAsia

MiddleEast

Rest ofEurope

Rest ofWorld

Profit pools (€BN)

0%

20%

40%

60%

80%

100%

Cumulative market share

Profit pool 2004 Profit pool 2006

Cumulative profit pool 2004 Cumulative profit pool 2006

Source: Oliver Wyman analysis

22 Copyright 2008 © Oliver Wyman

By analysing the trends of profitability drivers, we can better understand the reasons behind this fundamental change. Thus, we will look at the evolution of:

Pricing and margins �

Funding costs and availability �

Risk �

Pricing and marginsGross margins have been shrinking in the EU by approximately 12% since 2004, particularly in mature and maturing countries, and for most products barring credit cards.

Margin evolution mainly has been driven by three factors: price levels compressed by competition, funding costs determined by interest rates and additional fees and commissions. These factors have had diverging evolutions, causing a highly differentiated situation across countries and product segments.

Pricing pressure has increased on average in Europe, driven by strong competition from banks and new entrants. Despite strong differences in absolute terms across countries, we notice an overall convergence at lower levels. At the EU level, the weighted average APR decreased by 5% between 2004 and 2006, and funding rates, weighted by national outstanding amounts of consumer credit, increased overall by 9% between 2004 and 2006.

On the one side, we have emerging countries with much higher but rapidly deflating prices. Typically, players in new markets tend to have higher gross margins to protect themselves from unknown credit quality and to exploit fast growth in red-hot economies without recurring to price competition.

Maturing markets already are at US price levels and are converging towards lower ones; yet, at the bottom, mature markets have slim margins that can hardly be further compressed.

The main difference between maturing and mature markets is that in the latter, price competition has already been exploited as a growth lever in the last four years and that the intensity of margin compression, due to obvious economic limits, is tapering off. In maturing markets such as Italy and Spain, players more recently have started to recur to this type of competition, particularly as the Internet – a low-price/high-transparency channel – has become an important conduit of volumes; thus, further compression is easy to forecast.

23Copyright 2008 © Oliver Wyman

Figure 10: Net interest margins in European markets vs. growth of outstandings

0%

5%

10%

15%

20%

25%

Net interest marginfor personal loans

0%

10%

20%

30%

40%

50%

60%

Consumer credit outstandingsCAGR 2004-2006

NIM for personalloans in 2004

NIM for personalloans in 2007

Credit outstandingsCAGR 2004-2006

Pola

nd

Hu

ng

ary

Cze

ch R

ep.

Slo

vaki

a

Port

ug

al

Gre

ece

Net

her

lan

ds

Spai

n

Ital

y

Bel

giu

m

Irel

and

Den

mar

k

UK

Fran

ce

Au

stri

a

Ger

man

y

Luxe

mb

ou

rg

Fin

lan

d

No

rway

Source: ECRI, Bankecon, National Central Banks’ statistics, DataStream, Reuters, Oliver Wyman analysis

Notes: NIM for Eurozone countries is calculated as the difference between APR for Personal Loans of one to five years’ maturity and straight average of ECB base repo rate. For all other countries, NIM is calculated as the difference between the straight average of APR on loans to households for consumption and the straight average of overnight repo rates. NIM for Norway includes overdrafts. NIM for Sweden is based on available data

Specialists have been able to recoup some of the margin compression with higher commissions and fees from insurance products such as CPI and PPI. Instead, banks thus far have been less able to cross-sell these products, with penetration oscillating between 10% and 30%. The profit share of these highly profitable products is increasing steadily and can represent over 30% of total economic profits for specialists.

However, this aggregated view hides profound differences across sectors and segments.

POS and car financing already were characterised by slim margins in 2004, and the increased competition from inexperienced players looking for quick volume growth has driven down prices, significantly increasing the negotiating power of retailers and merchants. Thus, frequent promotions aiming to facilitate retailers’ sales have significantly lowered average prices. As a consequence, car financing and POS, with the exception of the UK and emerging high margin markets, has become a no-profit zone for players without the right partnership and cross-selling capabilities.

Personal loans were most affected by the renewed competition from banks; in fact, this product is the easiest to sell for non-specialists, and branch networks are powerful platforms for gaining volumes.

24 Copyright 2008 © Oliver Wyman

Moreover, many large banks tend to approach personal lending with a low-price customer-friendly positioning to avoid any potential reputation hazards, thus further pushing down prices.

As a result, personal loans for conforming segments have become significantly cheaper. This trend is stronger in mature markets where banks have been more proactive in entering the sector. Even in this case, however, different segments (such as non-conforming) have bucked the trend.

Figure 11: Net interest margins on personal loans between 2003 and 2007

0%

2%

4%

6%

8%

10%

12%

Net interest margin on personal loans

2003 200620052004 2007

Eurozone US

Source: The US NIM is calculated as the annual difference between the 24-month average interest rate on personal loans and the US Federal Funds target rate, both communicated by the Fed. The Eurozone NIM is calculated as the annual difference between APRC rates on loans to households for consumption and Euro short-term repo rates, both communicated by the ECB

Credit cards have best resisted price compression, though that sort of competition is present in the most advanced markets. The main difference being that in such markets, more players are capable of exploiting demand elasticity and risk-based pricing to optimise penetration and defend prices at the same time. Moreover, in Anglo-Saxon countries players have turned towards higher fees, especially late fees, as an important source of profits.

25Copyright 2008 © Oliver Wyman

Funding costs and availabilitySince 2005, the second trend compressing margins has been a steady increase of interest rates and therefore of the funding costs. Over the past two years, short-term ECB repurchase agreement rates have doubled, starting from a historically low level of 2%.

Figure 12: Eurozone funding rates

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2003 2004 2005 2006 2007

Euro Short Term Repo (ECB) – Middle Rate

Credit Yield to Maturity for AAA Financial Institutions

Source: Monthly interest rates provided by DataStream

Worsening this situation, the recent sub-prime crisis has dried liquidity from the Interbank and ABS markets, pushing spreads higher. Since the beginning of 2007, access to liquidity and cost of funding have become essential factors for business sustainability, particularly for those companies lacking banking support.

In a first phase, mortgage lenders and insurers have been hit by rising sub-prime defaults, whilst risks on RMBS and CMBS increased. This first wave started with a series of shocking news: HSBC issued a profit warning of over US$10.6 BN of charges on bad US mortgages, and was followed by New Century’s bankruptcy and Bear Stearns having to inject US$3.2 BN into a hedge fund over-exposed to sub-prime.

During summer 2007, we assisted with the inevitable downgrading of a number of RMBS, and with further news regarding risky exposures of hedge funds. Although national central banks started injecting liquidity into the repo market last August, the situation has not yet stabilised. Rather, the US housing bubble is being pricked, lowering home equity and increasing the likelihood of further credit losses for sub-prime mortgages.

26 Copyright 2008 © Oliver Wyman

Moreover, whilst the main direct actors of the crisis operated in the mortgage US sub-prime sector, the financial contagion – through the investors buying RMBS and particularly highly leveraged hedge funds – has spread globally and impacted the ability to access credit, both in the wholesale and in the ABS space.

This downturn in credit accessibility has been particularly damaging since it followed a period of abundant and cheap liquidity during which many players, particularly those not backed by a deposit base, started to rely on and take for granted those credit sources. Thus, a whole segment of the industry depends on the resolution of this crisis, with respect not only to their margin, but also to their long-term viability.

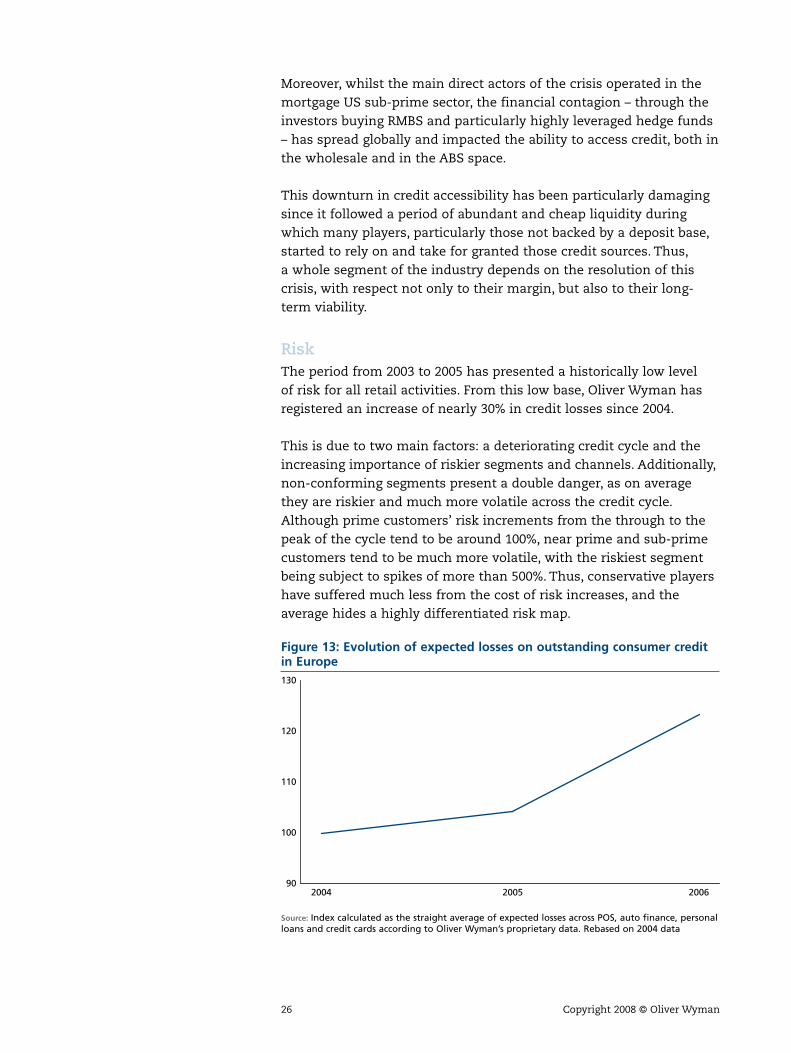

RiskThe period from 2003 to 2005 has presented a historically low level of risk for all retail activities. From this low base, Oliver Wyman has registered an increase of nearly 30% in credit losses since 2004.

This is due to two main factors: a deteriorating credit cycle and the increasing importance of riskier segments and channels. Additionally, non-conforming segments present a double danger, as on average they are riskier and much more volatile across the credit cycle. Although prime customers’ risk increments from the through to the peak of the cycle tend to be around 100%, near prime and sub-prime customers tend to be much more volatile, with the riskiest segment being subject to spikes of more than 500%. Thus, conservative players have suffered much less from the cost of risk increases, and the average hides a highly differentiated risk map.

Figure 13: Evolution of expected losses on outstanding consumer credit in Europe

90

100

110

120

130

2004 2005 2006

Source: Index calculated as the straight average of expected losses across POS, auto finance, personal loans and credit cards according to Oliver Wyman’s proprietary data. Rebased on 2004 data

27Copyright 2008 © Oliver Wyman

Going forward, we believe that the most likely scenario is a generalized worsening risk outlook, with profound differences by country. The European credit environment as a whole will worsen significantly but there will be no generalized collapse. Some countries, such as UK, Ireland and Spain, present a high likelihood of a more severe and rapid deterioration of credit quality, while others such as Germany, Austria and Poland should enjoy a stable situation.

Evolutions in the regulatory environmentDuring 2008, the regulatory environment for consumer credit will change significantly. The European Union will issue its new directive in mid-2008; consequently, individual states already have started to strengthen local regulations consistent with the content of the draft directive, which is focused on enhanced consumer protection via greater transparency and lender responsibility. The sales of ancillary insurance products, such as CPI, are under increasing regulatory scrutiny due to consumer association pressure. Lastly, SEPA will progressively come into force, unifying the European card payment system.

Consumer credit directive and local regulationsThe regulatory framework for consumer credit in Europe has been subject to numerous changes that aim to enhance consumer rights and promote a harmonised European consumer credit market.

The 1987 European consumer credit directive set the first regulatory framework for consumer credit, defining the content and the form of credit agreements. However, it left considerable discretion to each Member State in setting up appropriate measures to ensure sufficient consumer protection. Following several amendments, a new proposal was published in 2002. The adopted approach included the creation of an “optimal harmonisation level,” leaving each Member State in control of some aspects of the credit process. The latest proposal for a new directive on consumer credit was adopted in January 2008; as such, each Member State now has two years to implement the directive into national law.

The objective of the new directive is to enhance consumer protection on a fully harmonised European level, by allowing consumers to make informed choices when buying credit. This objective is achieved by ensuring that lenders provide adequate information prior to, during and after the stipulation of the agreement. From the lenders’ perspective, the EU Directive regulates the whole customer-facing credit process: advertising, some phases of risk assessment, credit agreement and servicing.

28 Copyright 2008 © Oliver Wyman

In particular, the EU Directive sets a clear definition of the standard information which must be included in any advertisement: the borrowing rate, total amount of credit, APR, duration, total amount payable by customer, instalments and the obligation to acquire ancillary services (e.g. insurance).

The directive also sets the obligations of the lender in terms of the consumer creditworthiness assessment, which must be based on all reliable information available within the EU (both internal and external), and which must be revised consistently with the new conditions if the total amount of credit is changed after the conclusion of the credit agreement.

During the entire agreement phase, a high level of transparency is required: lenders must provide adequate information to the consumer (i.e. a detailed explanation of product characteristics and its potential effects, including consequences of default in payment), in order to enable the consumer to assess whether the proposed credit agreement is adapted to the consumer’s needs, and whether it fits with the consumer’s financial situation. In addition to any information needed to compare different offers, lenders also must provide a full pre-agreement form replicating the official agreement contract.

Finally, the consumer’s information rights also have been widely extended during servicing. The consumer must be informed of any substantial contractual changes (e.g. changes in borrowing rate) before they are enforced. Consumers are granted new rights relative to early repayment and withdrawal from the agreement, and are allowed to withdraw from the agreement freely in the case of open-ended credit agreements or within the first 14 calendar days from the signing date. Further protection is provided in case of linked credit agreements7: if the goods/services covered by a linked credit agreement are not fully supplied as stated on the contract, the consumer can pursue remedies against the creditor if the consumer has already pursued all remedies against the supplier but has failed to obtain satisfaction. In terms of early repayment, the consumer is entitled at any time to discharge fully or partially his or her obligations, by paying only the interest (relative to the repaid part of the loan) accrued to that date.

7 Art. 15 of the latest European Directive on consumer credit states that “Where the goods or services covered by a linked credit agreement are not supplied, or are supplied only in part, or are not in conformity with the contract for the supply thereof, the consumer shall have the right to pursue remedies against the creditor if the consumer has pursued his remedies against the supplier but has failed to obtain satisfaction to which he is entitled according to the law or the contract for the supply of goods or services”

29Copyright 2008 © Oliver Wyman

Whilst waiting for approval of the new directive, the national regulatory bodies of many European countries have increasingly focused on this sector and have tightened their consumer protection framework.

Continental European countries are on track with the latest directive, and some have anticipated it. In July 2007, for instance, Italy issued a new consumer credit law, anticipating most of the contents recently discussed by the EU Directive. France is another country with an advanced and restrictive consumer credit regulation: six new laws aiming to enhance consumer protection were issued in the last five years. Nordic countries also have advanced regulation in terms of customer protection. Finland, Denmark and Sweden have already issued regulations compliant with the new European Directive, and Norway is working on its new consumer credit law.

Following this trend – and as a consequence of the increasing pressures from consumer groups and public opinion – Anglo-Saxon countries, traditionally characterised by a less restrictive framework, recently have amended old regulations, aiming to establish a more transparent and more competitive market.

Lastly, European emerging countries are still working on new regulations compliant with the EU directive, and their legislation often has considerable grey areas to be completed. For instance, Turkish regulation provides lenders with a detailed list of information to be included in the contract as well as a comprehensive explanation of consumers’ early repayment rights. The law, on the other hand, does not set any specific requirements on minimum advertisement information or on consumers’ withdrawal rights.

In sum, the trend clearly is toward an overall EU convergence into a more regulated market in which increased transparency will be granted.

Business implications of the new directiveEuropean lenders involved in the consumer credit market are concerned that the new EU directive will over-regulate the market, causing a margin squeeze due to shrinking revenues and rising costs. By focusing only on transparency the directive will be an obstacle to lender’s efficiency, thus limiting potential decrease in prices for customers.

30 Copyright 2008 © Oliver Wyman

The new directive will have two main effects on revenues. First, lenders will be asked to apply more stringent consumer creditworthiness assessments, potentially leading to a decrease in volumes. Secondly, new transparency requirements likely will enhance competition driven by price.

Lenders also have concerns regarding the increase of administrative costs, since a compliant credit process will require providing the consumer with a growing amount of information, thereby increasing processing needs. To that extent the new directive could result in limiting price decrease for customers given its negative impact on lenders efficiency.

Finally, new operational risks for lenders also will come from the enhanced level of protection guaranteed to the consumer. For example, in the case of linked credit agreements, when the goods or services subject to the agreement are not fully supplied (or are not in conformity with the agreement), the consumer could pursue remedies against the lender if he or she failed to obtain satisfaction from the supplier. This will also impact lenders’ efficiency as these operational risks will impact their economics.

Regulatory scrutiny effects on CPI salesInsurance products often are attached to consumer credit products and sold as a package. The objective is to cover the consumer from adverse events that could prejudice the consumer’s ability to repay the credit (Creditor Protection Insurance – CPI). CPI is a key product for the consumer credit industry given its obvious benefits for customers and positive impact on lenders’ profitability.

Increasing consumer association and regulatory pressure on CPI sales is expected to squeeze lenders’ margins on these products. On the revenue side, the combined effect of negative publicity and the forced use of less proactive sales practices could decrease volumes. Instituting greater transparency in pricing across comparable offers and ensuring that consumers clearly understand the costs versus benefits of CPI also are expected to drive down prices and revenues. On the cost side, lenders will need to increase spending on the governance of the sales process to ensure compliance. This will include rolling out:

Training programmes aimed at developing compliant yet effective �

sales approaches

Incentive systems with concrete goals including satisfaction of �

compliance requirements

Control systems ensuring that the POS sales approach is fair �

towards the consumer

31Copyright 2008 © Oliver Wyman

SEPA’s impact on card paymentsUntil the end of 2007, retail payments throughout Europe were processed via different systems, multiplying the number of payment instruments, standards and processing infrastructures required. The local fragmentation of issuing lenders, acquirers, processors and card schemes has increased the costs of paying via card, ultimately hampering the diffusion of card-based products.

The SEPA (Single Euro Payment Area) project aims to unify the many fragmented national payment systems for the three SEPA payment instruments (credit transfers, direct debits and cards) to a common, interoperable system. SEPA countries include the EU member states plus Iceland, Norway, Liechtenstein and Switzerland. Card issuers, acquirers, processors and card schemes will have to adapt to the SEPA principles starting from January 2008. SEPA will coexist with national payment systems until 2010, when the migration will be completed in full.

As a result of SEPA, consumers will be able to use the same card for all payments throughout Europe. Thus, the use of cards versus cash as a preferred payment means is expected to grow considerably. Moreover, a decrement of processing costs is expected due to the fact that acquirers will be able to process all card transactions within a single system, facilitating cross-border competition. The Eurosystem Payments Council, SEPA’s governing body, has already stated that a key SEPA objective is to harmonise card payment costs without penalising those countries with lower rates than others. Merchants consequently are expected to increase acceptance of card payments, as the decrement of processing costs should have a positive impact on merchant passive fees.

Lenders, too, may benefit from SEPA, although the new environment would have contrasting effects on their profits.

In terms of revenues, SEPA’s objective to enhance the diffusion of cards as a means of payment clearly benefits lenders. Furthermore, the unification of the European market from a processing standpoint provides an easier opportunity for lenders to expand their footprint at the pan-European level. Increased competition in formerly protected local markets, however, may offset extra revenues opportunities via downward pricing pressure.

Infrastructure costs for lenders may decrease, as they may be able to negotiate more favourable conditions with service providers. What remains to be seen is how these savings will be distributed among the various players in the card payment value chain – lenders, acquirers, processors, card schemes, merchants and consumers.

33Copyright 2008 © Oliver Wyman

IntroductionAs exposed in the previous section, the current environment is significantly more difficult than it was in 2005. European markets will still be experiencing growth, but at a slower pace and in a more skewed way. The combination of price pressure, rising risk and higher cost of funds has resulted in decreasing margins. Moreover, the sub-prime crisis has radically changed the availability of funds, which had always been taken for granted, particularly for players such as mono-liners who had no direct access to a deposit base. Finally, regulatory pressure is resulting in pressure on revenue and margins, as well as increased operating cost.

In our 2005 European Consumer Credit report, we identified key capabilities for each segment of the industry, with particular attention to the marketing/business development side. Though these key capabilities apply today, considering the more challenging environment, there will be a shift from a primary focus on business development to a more balanced and complex strategic agenda that integrates risk management, operational efficiency and innovation around products, channels and target segments.

In this section, we first will review the key capabilities required to succeed in the consumer credit industry, and then will propose a winning strategic agenda for both today and tomorrow.

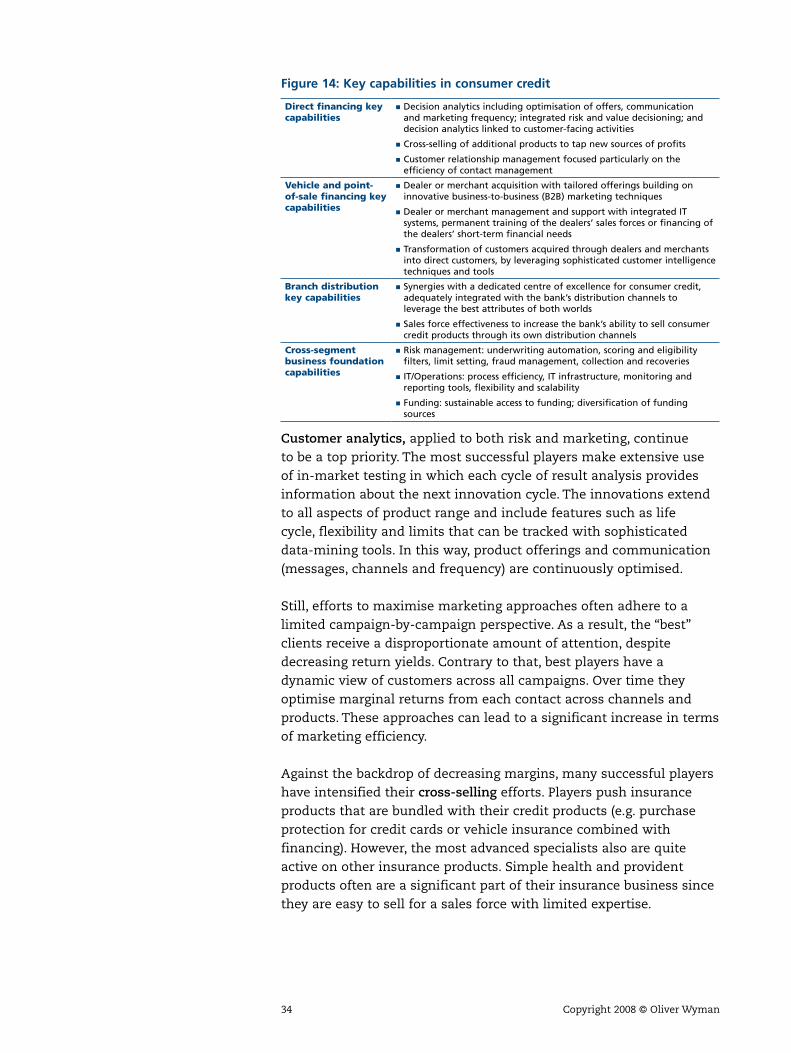

Key capabilities in consumer creditConsumer credit is a highly contested space, with strong differences among its sub-segments: vehicle financing, point-of-sale financing, direct financing and distribution through banking channels. Each requires specific know-how and capabilities. These are summarised in Figure 14 below, together with cross-segment business foundation capabilities.

Implications for Consumer Credit Players

34 Copyright 2008 © Oliver Wyman

Figure 14: Key capabilities in consumer credit

Direct financing key capabilities

Decision analytics including optimisation of offers, communication �

and marketing frequency; integrated risk and value decisioning; and decision analytics linked to customer-facing activities

Cross-selling of additional products to tap new sources of profits �

Customer relationship management focused particularly on the �

efficiency of contact management

Vehicle and point-of-sale financing key capabilities

Dealer or merchant acquisition with tailored offerings building on �

innovative business-to-business (B2B) marketing techniques

Dealer or merchant management and support with integrated IT �

systems, permanent training of the dealers’ sales forces or financing of the dealers’ short-term financial needs

Transformation of customers acquired through dealers and merchants �

into direct customers, by leveraging sophisticated customer intelligence techniques and tools

Branch distribution key capabilities

Synergies with a dedicated centre of excellence for consumer credit, �

adequately integrated with the bank’s distribution channels to leverage the best attributes of both worlds

Sales force effectiveness to increase the bank’s ability to sell consumer �

credit products through its own distribution channels

Cross-segment business foundation capabilities

Risk management: underwriting automation, scoring and eligibility �

filters, limit setting, fraud management, collection and recoveries

IT/Operations: process efficiency, IT infrastructure, monitoring and �

reporting tools, flexibility and scalability

Funding: sustainable access to funding; diversification of funding �

sources

Customer analytics, applied to both risk and marketing, continue to be a top priority. The most successful players make extensive use of in-market testing in which each cycle of result analysis provides information about the next innovation cycle. The innovations extend to all aspects of product range and include features such as life cycle, flexibility and limits that can be tracked with sophisticated data-mining tools. In this way, product offerings and communication (messages, channels and frequency) are continuously optimised.

Still, efforts to maximise marketing approaches often adhere to a limited campaign-by-campaign perspective. As a result, the “best” clients receive a disproportionate amount of attention, despite decreasing return yields. Contrary to that, best players have a dynamic view of customers across all campaigns. Over time they optimise marginal returns from each contact across channels and products. These approaches can lead to a significant increase in terms of marketing efficiency.

Against the backdrop of decreasing margins, many successful players have intensified their cross-selling efforts. Players push insurance products that are bundled with their credit products (e.g. purchase protection for credit cards or vehicle insurance combined with financing). However, the most advanced specialists also are quite active on other insurance products. Simple health and provident products often are a significant part of their insurance business since they are easy to sell for a sales force with limited expertise.

35Copyright 2008 © Oliver Wyman

In the area of Customer Relationship Management, best-in-class players use customer information to build relationship marketing programmes and event-driven communication. Moreover, these systems also are used to deploy “tiered” service levels, ranging from automated call centres to expert responses, to better serve high-value requests and clients. Thus, resources can be liberated for more effective sales and service activities, thereby increasing productivity.

In vehicle and point-of-sale financing, best players have professionalised their approach to acquiring and retaining merchants. Leading players have established B2B marketing intelligence groups that support the efforts of the sales teams by designing value propositions to each specific merchant segment. High service levels and a tailored approach are provided for key merchants, whilst less strategic partners are served with a standardised approach.

In this sub-sector, it is also essential to offer a seamless IT platform that allows merchants to process a credit request and obtain approval or refusal within minutes. In grey-zone cases, an immediate connection is made to the credit company’s hotline. Accompanying measures include the training of merchant sales forces to explain how the products are sold and processed.

Finally, the ability to transform customers acquired through merchants into direct customers is a key driver of profitability. In a number of European markets, merchants are in a position to impose very tight financial conditions to their consumer credit provider. It is therefore essential for credit players to maximise the return on their partnership investment by optimising the revenues generated by each customer. Best players follow a very systematic and sophisticated approach to target, segment and market their customers acquired via merchants or dealers.

In branch distribution, the most advanced banks establish a centre of excellence to inject consumer credit know-how into their system in the form of decision analytics, product design expertise, high levels of automated underwriting and collection capabilities. Acknowledging the importance of this know-how, many banks have established partnerships with specialists when their size or capabilities did not allow internal development. Specialists on their side have gained an alternative source of revenue and, in the case of Joint Ventures, a powerful channel.

On the front end, the key challenge is to improve branch distribution sales effectiveness. Unlike specialists, banks need to sell a very complex set of products and must serve their clients more

36 Copyright 2008 © Oliver Wyman

extensively. To improve sales performance, and in particular the ability to cross-sell CPI, best practices are introducing performance incentive schemes and training programmes (often with the help of specialists) to boost their productivity.

Beyond segment-specific key success factors, players need to master three foundation capabilities: risk management, IT/operations and funding. The former two items will be developed in the following section of this report, as they should be at the top of all players’ strategic agenda, particularly given the current environment.

Funding is a pre-requisite, albeit an oft-forgotten one. Until the sub-prime crisis, the rise of securitisation and of ABS products had apparently made funding a non-issue. As the current crisis evolves, access to liquidity has become a crucial factor for business survival. A number of players have faced serious difficulties in recent times because of funding shortages. Likewise, several recent decisions to exit some European consumer credit markets have been made in part due to the need to reallocate scarce capital resources. As illustrated by these recent developments, funding requirements are a necessary condition for the survival and expansion of consumer credit players.

Building a winning strategic agenda

IntroductionAs leading players have already understood, the current environment requires new business initiatives that combine optimisation of foundation requirements and tailored business development capabilities. We have summarised these in three main challenges:

Driving efficiency to the next level �

Responding to worsening credit conditions �

Promoting growth �

Driving efficiency to the next levelIn recent years, the strategic priority clearly was around business development and expansion into new markets and new segments. Though increasing revenue is still on the agenda, efficiency will become the name of the game for a number of players, especially in mature markets.

Efficiency is sought through different levers. At its most basic level, efficiency is achieved by cost reduction efforts that focus on the main operating and marketing expense items. As a starting point,

37Copyright 2008 © Oliver Wyman

this entails renewed cost awareness; investments and operating expenses are coming under scrutiny and cost reduction programmes are being launched.

New IT development, above-the-line expenses and new hiring typically are the first items to be cut. The risk in these cost-cutting programmes is rushing into measures that have short-term effectiveness, but negative long-term impact.

To achieve further and more sustainable efficiency gains, best practice players are investing in automating and digitalising their key processes. Organisations adhere to a Straight-Through Processing (STP) model across all channels and groups of clients (i.e. obtaining all applications or information requests in electronic format). In general, customers’ applications should be processed on a non-paper basis with manual intervention levels remaining very low (below 5%).

The front-end data-capturing process is the main focus of this endeavour. Capturing all data directly at the front line – ideally the key is to retrieve the existing customer data automatically from current accounts or other products. Front-end data-capturing models are superior to models that include the transport of paper forms to central processing units. On one side, they are significantly more cost-effective. We observed that the application of STP models generated improvements in cost/income in the order of 10% to 15%. On the other side, STP allows faster servicing, particularly in the underwriting process.

Automation in this sense not only applies to web-based customer application, but also to every transaction through any channel. Examples include:

Direct finance: capture of all web-based information �

Branch distribution: capture of all customer information on �

dedicated terminals with guidance of support staff

Point of sale: capture through web-based applications for strategic �

merchants, whilst providing simple terminals for non-strategic merchants

Best practices go beyond STP and now focus their efforts on creating cross-border operating synergies. Although a number of players have been operating in several European markets for a long time, they once ran each market as an independent unit. The differences in local regulations and cultural attitudes were often invoked as a reason

38 Copyright 2008 © Oliver Wyman

for maintaining a multi-local model. With the progressive regulatory convergence and worsening market conditions, this philosophy is now increasingly challenged.

The first step in creating cross-border synergies entails implementing effective knowledge-sharing processes between geographies. The usual way of achieving this is to create centralised corporate functions structured around key capabilities (e.g. marketing, risk management, collection). These functions have the role of exchanging best practices, setting policies and supporting geographies in implementing them. Within this function typically reside experts who are in charge of supporting knowledge sharing and suggesting standard approaches to be used as blueprints in local markets.

A more advanced approach involves having these corporate functions in charge of developing tools and processes with a view to implementing them in several markets. This is the concept of centres of excellence, which typically focus on risk and propensity scorecards, monitoring systems, underwriting or recovery processes. Reporting templates for each process are then supported with little variations across most countries to allow for better centralised visibility and control. Key Performance Indicators (KPIs) and Service Level Agreements (SLAs) are common across the whole organisation.

However, building regional platforms is the most effective way to achieve economies of scope and scale in a pan-European environment. A platform is a generic concept and can include a number of different realities; it can refer to an IT system being used across geographies or to an operating unit servicing customers in different markets.

Deciding the level of centralisation of different functions (i.e. global, regional, national) is crucial, as each company might have a different set of core expertise that is relevant to different countries. Moreover, different markets have varying degrees of diversity, thus the geographical footprint is determinant in deciding how to allocate functions. For instance, Nordic markets are quite homogeneous in terms of the availability of high-quality public data; thus a regional platform of risk and marketing functions is an interesting option that is applicable even to small players.

In general, IT systems, risk management, financial management, decisioning analytics and HR policies are candidates for centralisation, whilst sales and marketing tend to stay at a local level.

39Copyright 2008 © Oliver Wyman

Responding to worsening credit conditionsIn times of worsening credit conditions, it is essential to ensure optimal effectiveness of risk management. This is generally achieved by working on risk organisation, processes and tools.

Having effective risk organisations is no longer a “nice to have” – it’s a “must have” to ensure the performance of the entire institution. Many consumer credit players have integrated risk into their marketing and commercial operations and are now using this as a core source of competitive advantage. New regulatory requirements, from Basel II in particular, as well as best practices, stipulate a clear separation between risk and front office, right up to senior management. As a consequence, the key organisational imperative is ensuring appropriate independence on the core credit side, whilst allowing sufficient integration in the commercial organisation to deliver the value-adding agenda. Overall, this is an issue where the detailed combination of organisational structure, resources and individuals define what is realistic.

Since consumer credit processes are typically complex (see chart below), there are often gaps in the process that allow bad loans or credit to get through. Good lenders have an effective lending process that trades complexity against controllability, and that is able to adapt as the credit environment deteriorates. This allows the lender to be fast to manage early signs of account deterioration and to move arrears balances quickly into recovery. It also allows the lender to apply more sophisticated approaches in areas such as reactive limit setting and card authorisations.

40 Copyright 2008 © Oliver Wyman

Figure 15: Example of loan origination process

Failseligibilitycriteria

formonthlyscoring

Newcustomers

Monthlyscoringprocess

Outcomeparameters

Customersystem

Policy rulesset 1

Policy rulesset 2

Policy rulesset 2

Policy rulesset 1

Policy rules1 and

eligibilityrules

Shortsanction

withlimits

Shortsanction

withsuppressed

limits

Shortapplicationfor specific

product

Limitcalculation

for allproducts

Fullsanction

% factorsExposure

caps

Repaymentcapacity

Classification into

segments

Riskscorecards

Policyrules

scorecards

Outcomedriven

adjustments

Calculationof customeraffordability

Credit bases(Cred T/O,

Repayments,Deposits)

Riskscore

Segmentationrules

Scorecardweightings

Data feeds(internalbureau, credit risk

datawarehouse)

Outcomes

2

Decisiontrees

1

Allocationto

scorecards

Output to affordability calculation

Upload customer affordability on customer system for approval/limit setting

Newcustomerscoring

Newcustomerscoring

Existingcustomers

1. Risk scoring/segmentation 2. Affordability calculation 3. Approval/limit setting

App

Acc Ref Dec Acc Ref Dec

App

Calibratetrees

Any policies and procedures will need credit tools for scoring, calculating debt capacity/limit setting and infrastructure to deliver them to the relevant decision point. In best practice organisations, the following observations can be made:

Tools are highly decision supporting, in that they can discriminate �

between “good” and “bad” customers. Performance is monitored regularly, and updates are frequent as the market changes. They also are designed around specific decisions (e.g. new to credit origination, existing customers’ line extensions, collections, bankruptcy etc.)

All information available on the client is used to assess �

creditworthiness, especially across products whenever possible

Tools are easy to use and avoid multiple data entry �

The end-to-end workflow is automated, and decisions are taken �

within minutes

41Copyright 2008 © Oliver Wyman

As the credit situation worsens best practices are the first to spot changing conditions through standardised delinquency reports and to react by optimising their underwriting criteria and focusing on collection. In credit downturns, being the first to collect, particularly among over-indebted segments, often makes the difference between being and not being paid. In the current environment, collection is a function that requires special attention.

To this extent the difference between the most experienced players and others can be profound. Rather than consider investment in collection from a simple efficiency/cost perspective, best practices apply a value approach and favour effectiveness over pure efficiency. We typically observed that investment in collection has extremely low cost/benefit ratios ranging from 1/5 to 1/30.

Collection is not considered a simple “practitioner’s game.” Highly powered analytical tools, such as behavioural scores, are integrated to achieve the highest level of performance. The extended usage of statistical analysis drives continuous test-and-learn cycles and produces innovation at all levels, from processes to organisation to performance system. This model of continuous improvement is the distinctive characteristic of the best collection groups, and is the key to reducing credit losses, particularly when vintages have already turned bad.