bajaj auto limited - asitmehta.com lt… · bajaj auto limited acmiil 1 ... dual brand strategy...

TRANSCRIPT

Bajaj Auto Limited ACMIIL 1

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

We initiate coverage on Bajaj Auto Ltd (BAL) with “Hold” recommendation and price target of ` 1,509 (based on P/E of 15x its FY13 E core EPS of `89.4 per share, cash and cash equivalent per share of ` 137 and investment in KTM at ` 30 per share). BAL is the second largest two wheeler manufacturer and the largest manufacturer of three wheelers in the country. BAL is also the largest exporter of two and three wheelers and derives about 30% of revenues from exports. BAL has varied product portfolio to choose from, at different power and price points depending on need of customer. Also, BAL thrust on exports (particularly the African market) is likely to maintain sales momentum for the company

Investment Rationale

Wide product portfolio

BAL offers wide product portfolio (at varying price and power combinations addressing different consumer segments). Launch of Discover 150 (commuter bike with greater power), Pulsar 135 (light sports bike) and expected launch of Boxer 150 (targeted towards rural commuter segment) have created new segments and enabled BAL to garner market share.

Exports to be key revenue driver

BAL thrust on exports (particularly the African market) where it has relatively lesser presence, would boost revenues going forward. Increasing motorcycle penetration in the African market and maintaining leadership position in other markets (Bangladesh, Sri Lanka, Phillippines, Colombia) would ensure greater volumes for BAL. Also increasing exports of three wheelers would boost revenues.

Dual brand strategy reaped rich dividends

BAL strategy to focus on brands “Pulsar” for sports segment and “Discover” for commuter segment has reaped rich benefits. Launch of Discover 100,Discover150 and Pulsar 135 have created different segments and has enabled BAL to garner market share (Discover and Pulsar account for 23% of domestic motorcycle market). We believe both the brands will continue to generate significant volumes for BAL.

Outlook and Valuation

The volume outlook for two wheeler industry is robust. However increasing competitive intensity both in two wheeler and three wheeler segment, would result in BAL loosing market share. Also given the replacement of DEPB scheme with Duty Drawback scheme with lower benefits and the impact of falling dollar affecting export realization, we assign multiple of 15x to FY 13E EPS of `89.4 to arrive at value of `1,342 for core business. Adding cash per share of ̀ 137 and ̀ 30 per share for KTM stake, we arrive at value of ` 1,509. We therefore give “Hold” rating on the stock.

Bajaj Auto Limited

AnalystBharat [email protected]: (022) 2858 3404

25 Aug, 2011

H O L D

Key Data (`)

CMP 1,522

Target Price 1,509

Key Data

Bloomberg Code BJAUT IN

Reuters Code BAJA.BO

BSE Code 532977

NSE Code BAJAJ-AUTO

Face Value (`) 10

Market Cap. (` bn) 440.4

52 Week High (`) 1,665

52 Week Low (`) 1,190

Avg. Daily Volume (6m) 447,367

Beta (Sensex) 0.7

Shareholding Pattern June 2011 (%)

Promoters 50.0

Mutual Funds / UTI / Banks 8.1

Foreign Institutional Investors 15.8

Bodies Corporate 8.7

Individuals 16.9

Other 0.5

Total 100.0

(` mn) FY11 FY12E FY13E

Revenues 165,833.8 194,482.3 217,794.0

Operating Profit 32,991.0 36,383.1 39,073.6

OPM (%) 19.9 18.7 17.9

PAT 23,002.5 25,731.8 25,882.5

PAT Margin (%) 13.9 13.2 11.9

EPS (`) 79.5 88.9 89.4

Bajaj Auto Limited ACMIIL 2

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Investment Rationale

Broader product portfolio catering to diverse consumer base

BAL offers wider product portfolio in motorcycles. Customers get varied choices in terms of power and affordability. BAL has created different segments with launch of Discover 150 (bike for commuters wanting more power) and Pulsar 135 LS (light weight sports bike) enabling it to garner greater market share. The bike for the commuter segment has choices in the form of Discover and Platina which offer products at varying power and price points depending on needs of the customer. Similarly for the sports segment the customer can choose from various Pulsar models. Further, with launch of Boxer 150 (slated as Bharat bike with expected price tag of `40,000 and aimed at lower end of rural commuter segment) in August 2011, the product offering would enhance further. We believe the broader product portfolio will enable BAL to increase market share going forward.

Dual strategy brand continue to reap benefits

BAL dual strategy of promoting brands “Discover” and “Pulsar” has reaped rich benefits. BAL had drawn strategy to promote “Discover” in the commuter segment and “Pulsar” in the sports segment. The two brands account for 83% of BAL sales in domestic segment in FY11, as compared to 70% in FY10.

Source: Company, ACMIIL Research

Source: Company, ACMIIL Research

Bajaj Auto Limited ACMIIL 3

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

The Discover brand accounted for sale of 1.24 million units in FY11, thus constituting ~14% market of overall motorcycles. Discover 100 with sale of 8.9 lakh units and Discover 150 with sales of 3.3 lakh units have contributed to growth of the Discover brand.

The Pulsar brand with sales of 7.7 lakh units, constitute 8.6% of the overall market share in FY11. Pulsar 135 LS has enabled overall increase of Pulsar brand sales in FY11.

With the launch of Discover 125 in March 2011 and expected launch of Pulsar and Discover variants in Q4 FY12, both the brands will continue to contribute significantly to sales going forward.

Exports to continue sales momentum, Africa to be the key driver

BAL derives about 30% of revenues from exports and is present in over 50 countries across the globe. BAL has dominant presence in Africa, Latin America and South Asia. BAL is market leader in motorcycles in Colombia, Central America, Sri Lanka, Bangladesh, Philippines, Nigeria, Uganda and Kenya. BAL sees huge opportunity in Africa due to its relatively lesser presence as compared to other markets. Apart from Nigeria (which currently accounts for 60% of African sales), BAL is planning to ramp up presence in other countries such as Kenya, Congo, Sudan and Tanzania. We believe Africa would be key revenue driver for BAL. BAL is also the largest three wheeler commercial vehicles exporter in the world with export of 2.3 lakh units in FY11. We think BAL strategy to focus on exports will continue to drive growth

Source: Crisinfac, ACMIIL Research

Source: Crisinfac, ACMIIL Research

Bajaj Auto Limited ACMIIL 4

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

in revenues going forward.

BAL has policy of hedging its export revenues. BAL has hedged 90-95% of its FY12E export revenue (based on volume growth assumption of 15-20%). BAL has hedged the revenues at about I US$=` 46.7.

BAL derives majority of export revenues from Africa (Nigeria, Kenya, Egypt and South Africa), followed by Sri Lanka and Bangladesh, Latin America (Argentina, Mexico, Colombia and Peru) and South east Asia (Indonesia and Philippines).

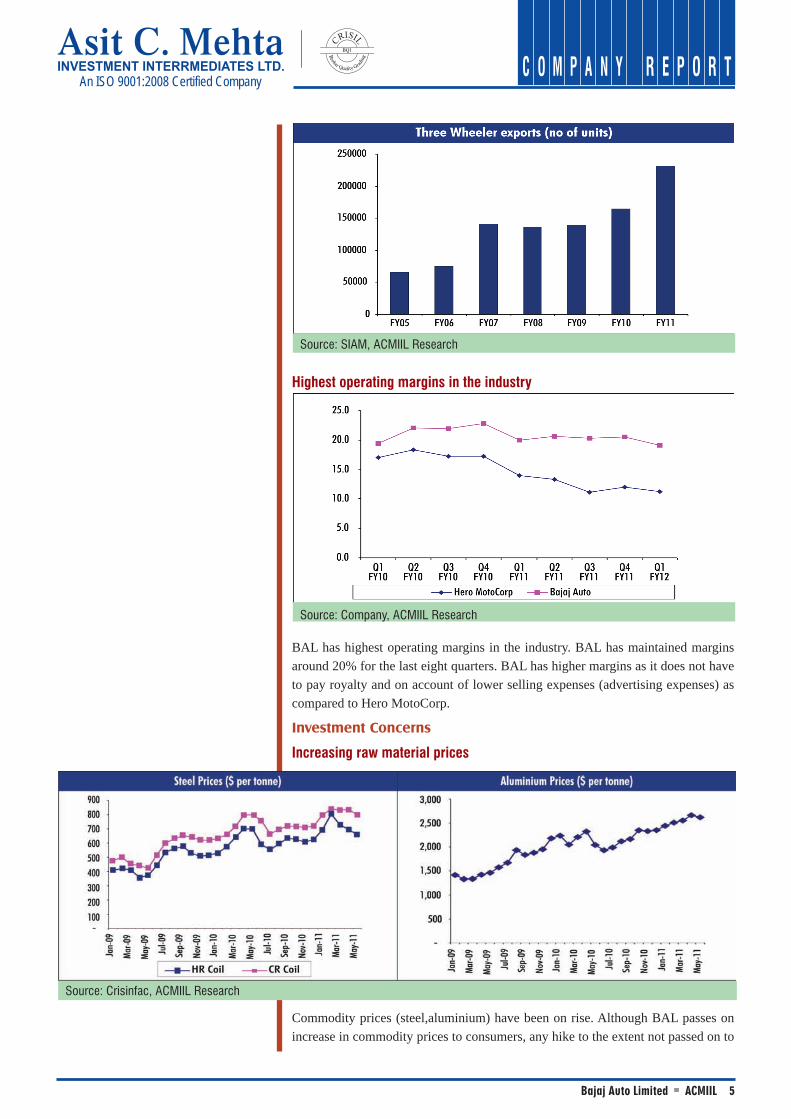

BAL has posted 41% CAGR growth in motorcycle exports. BAL exported 9.72 lakh units in FY11. Apart from the models in the domestic market, (Pulsar, Discover and Platina) BAL sells Boxer 100 and CT 100 exclusively in the export market.

Source: Company, ACMIIL Research

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Bajaj Auto Limited ACMIIL 5

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Highest operating margins in the industry

BAL has highest operating margins in the industry. BAL has maintained margins around 20% for the last eight quarters. BAL has higher margins as it does not have to pay royalty and on account of lower selling expenses (advertising expenses) as compared to Hero MotoCorp.

Investment Concerns

Increasing raw material prices

Commodity prices (steel,aluminium) have been on rise. Although BAL passes on increase in commodity prices to consumers, any hike to the extent not passed on to

Source: SIAM, ACMIIL Research

Source: Company, ACMIIL Research

Source: Crisinfac, ACMIIL Research

Bajaj Auto Limited ACMIIL 6

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

the consumer is likely to impact margins. Commodity prices are, however, expected to soften going ahead

Export realizations to be impacted by Replacement of Duty Entitlement Pass Book (DEPB) Scheme and Falling Dollar

BAL derives about 30% of revenue from exports. The DEPB scheme that provides incentive to exporters (in the form of refund of import duty on inputs used to manufacture the exported product) has received its last extension till Sep 2011. The DEPB scheme is expected to be replaced by the drawback scheme, which would have lower benefits. Currently under the DEPB scheme, BAL receives benefits to the tune of 9% of exports. The drawback scheme is expected to provide lower benefits, which would impact profitability going forward. DEPB benefits currently account for about 9% of FOB value of exports for BAL and contribute about 3% to the overall margins.

Further, the fall of the dollar vis-a-vis INR is likely to impact export realizations for FY13.

Increasing competition

With the termination of joint venture between Hero and Honda, competition has intensified in the domestic market as Honda can now tap entry-level segment. Honda is aggressively expanding capacity from current 1.6 million units to 4 million units by FY13. Honda is likely to gain market share by about 300 basis points in the motorcycle segment. Also, Yamaha and Suzuki are planning to bolster their presence in the domestic market. Thus, competition is expected to intensify going forward.

Further, with TVS Motors ramping up capacity in the three wheeler segment BAL is likely to loose market share going forward. Also the launch of Tata Magic Iris (Five seater, four wheeled passenger carrier), is likely to create a different segment. Tata Iris being more comfortable, spacious and available at competitive price of ` 1.95 Lacs (ex-showroom Thane, is likely to be threat to three wheelers. Three wheelers being highly profitable business for BAL, we expect pressure on volumes as well as profitability.

Industry Analysis

Source: SIAM, ACMIIL Research

Bajaj Auto Limited ACMIIL 7

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Two wheeler penetration level

Penetration level Adressable Households (Million Vehicle population (Million)

Segment 2005-06 2009-10 2005-06 2009-10 2005-06 2009-10

Motorcycles (overall) 30% 28% 79 159 23.9 45.0

Urban 30% 36% 41 67 12.4 23.8

Rural 30% 23% 38 92 11.5 21.1

Scooters (overall) 16% 9% 79 159 12.6 13.6

Urban 25% 17% 41 67 10.2 11.2

Rural 6% 3% 38 92 2.5 2.4

Mopeds (overall) 4% 2% 79 159 3.1 3.8

Urban 5% 3% 41 67 2.1 2.2

Rural 3% 2% 38 92 1.1 1.6

Source: Crisinfac, ACMIIL Research (Penetration level is defined as ratio of number of two wheelers and number of addressable household). Addressable household is defined as households having income above 90,000 per annum

2005-06 2009-10

Total Two wheelers Urban (million) 24.6 37.3

Total addressable household Urban (million) 41.0 67.0

Penetration Urban (%) 60.0 55.7

Total Two wheelers Rural (million) 15.1 25.1

Total addressable household Rural (million) 38.0 92.0

Penetration Rural (%) 39.6 27.3

Overall Two wheelers (million) 39.7 62.4

Overall addressable household (million) 79.0 159.0

Overall penetration (%) 50.2 39.2

Source: Crisinfac, ACMIIL Research

Urban two wheeler population grew at CAGR of 10.9% between 2005-06 to on back of 13.1% growth in number of addressable households. Rural two wheeler demand outpaced urban segment, growing at CAGR of 13.6% on back of 24.7% growth in addressable rural household.Crisil estimates domestic two wheeler demand to grow at CAGR of 7-9% between 2009-10 to 2014-15. Increase in number of addressable households in the rural market (from 92 million in 2009-10 to 132 million in 2014-15) and higher penetration in urban markets will aid growth in the two wheeler demand.Increased crop output and increase MSP for crops would lead to increase in the number of addressable households in rural areas (CAGR growth of 7.5% between 2009-10 to 2014-15). Similarly increasing model launches, attractive financing options and price points will increase penetration in urban areas.

Source: Crisinfac, ACMIIL Research (no of addressable households is defined as households having income above ` 90,000)

Bajaj Auto Limited ACMIIL 8

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Category % CAGR growth (2009-10 to 2014-15)

Motorcycles 7 to 9

Scooters 10 to 12

Mopeds 7 to 9

Overall two wheelers 8 to 10

Two wheeler segment wise salesSegment wise sales (no of units) FY05 FY06 FY07 FY08 FY09 FY10 FY11 CAGR Growth

(FY05-FY11) %

Scooter/Scooterette 922,428 908,159 940,617 1,050,109 1,148,007 1,462,534 2,073,797 14.5

Motorcycles 4,964,753 5,815,417 6,547,195 5,768,341 5,831,953 7,341,122 9,019,090 10.5

Mopeds 322,584 332,741 354,760 413,759 431,214 564,584 697,418 13.7

Total Two wheelers 6,209,765 7,056,317 7,872,334 7,248,600 7,437,619 9,370,951 11,790,305 11.3

Source: SIAM, ACMIIL Research

Motorcycles constitute largest segment in the two wheeler industry, comprising 76.5% of overall sales. Scooter, the next largest segment has gained its share from 14.9% in FY05 to 17.6% in FY11. Mopeds share has remained stable at about 6% of the overall industry volumes.

Less than 125cc segment is the largest category in the motorcycle segment. This segment has been consistently loosing market to the higher segments. The share of less than 125 cc motorcycles has reduced from 84.5% in FY05 to 71.7% in FY11.

Motorcycle market is relatively concentrated with top two players commanding market share of about 81%. Hero MotoCorp is the market leader commanding share

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Bajaj Auto Limited ACMIIL 9

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

of 54.6%. The dynamics of the segment are expected to change post the split of Honda from Hero MotoCorp. TVS Motors has steadily lost market, with market share falling from 12.9% in FY05 to 7% in FY11.

Player wise productsMotorcycles less than 125 cc Hero MotoCorp Bajaj Auto TVS Motors Honda India Yamaha India Suzuki

Products CD Dawn, CD Delux, Splendor Plus,

Splendor NXG, Passion Pro, Splendor Pro

Platina 100, Discover 100

Jive, Star City, Sport

CB Twister Crux,YBR 110 Slingshot

Motorcycle 125cc and above Hero MotoCorp Bajaj Auto TVS Motors Honda India Yamaha India Suzuki

Products Super Splendor, Glamour, Acheiver,

CBZ Extreme, Hunk, Karizma

Platina 125, Discover 125, Discover 150,

Pulsar 135, Pulsar 150, Pulsar 180,

Pulsar 220, Avenger 220

Flame 125, Apache 160, Apache 180

CB Shine, CBF Stunner, CB Unicorn, CB

Unicorn Dazzler, CBR 250

YBR 125, SS125, SZ, FZ,Fazer, YZF

GS 150

Source: ACMIIL Research

Hero MotoCorp has the most products in the less than 125 cc motorcycles, whilst BAL has more offerings in the 125 cc and above motorcycles. Honda India has only one offering in the less than 125 cc segment, due to the joint venture with Hero which restricted its presence in that category.

Hero MotoCorp is the leader with market share of 71% in the segment. Its leadership position in the less than 125 cc segment has enabled it to remain leader in the overall motorcycle market. Honda Motors has recently marked its presence in this segment. Post split with Hero, Honda no longer has restriction to enter this segment. The launch of Discover 100cc bike has enabled Bajaj Auto to gain market share in last two years.

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Bajaj Auto Limited ACMIIL 10

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

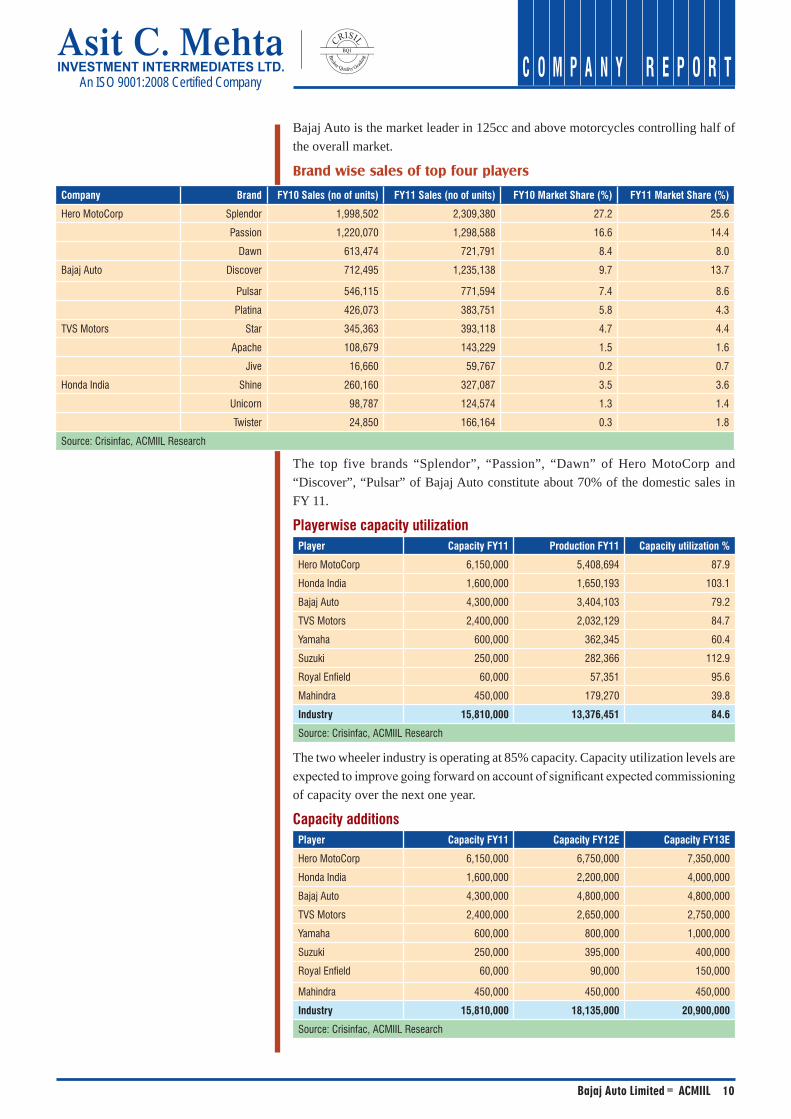

Bajaj Auto is the market leader in 125cc and above motorcycles controlling half of the overall market.

Brand wise sales of top four players

Company Brand FY10 Sales (no of units) FY11 Sales (no of units) FY10 Market Share (%) FY11 Market Share (%)

Hero MotoCorp Splendor 1,998,502 2,309,380 27.2 25.6

Passion 1,220,070 1,298,588 16.6 14.4

Dawn 613,474 721,791 8.4 8.0

Bajaj Auto Discover 712,495 1,235,138 9.7 13.7

Pulsar 546,115 771,594 7.4 8.6

Platina 426,073 383,751 5.8 4.3

TVS Motors Star 345,363 393,118 4.7 4.4

Apache 108,679 143,229 1.5 1.6

Jive 16,660 59,767 0.2 0.7

Honda India Shine 260,160 327,087 3.5 3.6

Unicorn 98,787 124,574 1.3 1.4

Twister 24,850 166,164 0.3 1.8

Source: Crisinfac, ACMIIL Research

The top five brands “Splendor”, “Passion”, “Dawn” of Hero MotoCorp and “Discover”, “Pulsar” of Bajaj Auto constitute about 70% of the domestic sales in FY 11.

Playerwise capacity utilizationPlayer Capacity FY11 Production FY11 Capacity utilization %

Hero MotoCorp 6,150,000 5,408,694 87.9

Honda India 1,600,000 1,650,193 103.1

Bajaj Auto 4,300,000 3,404,103 79.2

TVS Motors 2,400,000 2,032,129 84.7

Yamaha 600,000 362,345 60.4

Suzuki 250,000 282,366 112.9

Royal Enfield 60,000 57,351 95.6

Mahindra 450,000 179,270 39.8

Industry 15,810,000 13,376,451 84.6

Source: Crisinfac, ACMIIL Research

The two wheeler industry is operating at 85% capacity. Capacity utilization levels are expected to improve going forward on account of significant expected commissioning of capacity over the next one year.

Capacity additionsPlayer Capacity FY11 Capacity FY12E Capacity FY13E

Hero MotoCorp 6,150,000 6,750,000 7,350,000

Honda India 1,600,000 2,200,000 4,000,000

Bajaj Auto 4,300,000 4,800,000 4,800,000

TVS Motors 2,400,000 2,650,000 2,750,000

Yamaha 600,000 800,000 1,000,000

Suzuki 250,000 395,000 400,000

Royal Enfield 60,000 90,000 150,000

Mahindra 450,000 450,000 450,000

Industry 15,810,000 18,135,000 20,900,000

Source: Crisinfac, ACMIIL Research

Bajaj Auto Limited ACMIIL 11

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Post split with Hero, HMSI is planning significant capacity additions in FY13. HMSI currently has plant in Gurgaon with capacity of 1.6 million units. It recently commissioned new plant at Rajasthan having annual capacity of 1.2 million units. Thereafter it also plans to open third facility (probably in South) in 2013 which would have annual capacity of 1.2 million units, thereby taking overall capacity to 4 million units by 2013. We believe HMSI would gain market share in motorcycle market as we enter 2013, largely at expense of Hero. This is because post separation with Honda, Hero is likely to take beating on the brand image (as it was and continues to depend on Honda for technology). We believe that Hero position in 125 cc and above motorcycles is most vulnerable, since technology and performance are key differentiators in the segment. (Hero has market share of ~13% in the segment with sale of 3.4 lakh units). We believe Honda can also be threat to BAL (though not as much as to Hero, since BAL has indigenously developed technology) in the segment since BAL is the leader with market share of about 50% in this segment. Again, we believe HMSI would be threat to Hero and BAL in less than 125 cc segment as well. Although HMSI bikes are expensive, we believe HMSI has an upper hand in terms of styling. (the launch of Twister proves the point). Twister with sale of 1.65 lakh units commands market share of 2.6%. We expect HMSI to gain market share of about 300 basis points in motorcycle market in FY13.

Two wheelers Financing

Finance penetration (defined as ratio of two wheelers purchased on finance and two wheeler sales) of two wheelers has declined from about 56% in 2007-08 to 32% in 2010-11. Loan to value ratio has remained constant at 70%.Given the significant number of vehicles purchased on cash basis and less impact on EMI on account of increase in interest rate, the rising interest rate scenario is likely to have minimal impact on two wheeler demand.Calculation of EMI in scenario of rising interest rate

Price of the product 60,000 60,000 60,000

Down payment 18,000 18,000 18,000

Loan amount 42,000 42,000 42,000

Loan tenure (mths) 24 24 24

Interest Rate (% p.a) 24 27 30

Monthly EMI 2,221 2,284 2,348

Source: ACMIIL Research

Source: Crisinfac, ACMIIL Research

Bajaj Auto Limited ACMIIL 12

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Dealership network Dealers (nos) Service centres

(nos)Sales FY11 Sales/Dealer

Hero MotoCorp 700 3,600 5,269,381 7,528

Bajaj Auto 600 1,800 2,414,630 4,024

TVS Motors 650 2,500 1,777,676 2,735

Honda Motors 400 790 1,551,402 3,879

Source: Crisinfac, ACMIIL Research

Hero MotoCorp has the strongest dealer network comprising of 700 dealers and 3,600 service centers across the country. The dealership network of Hero MotoCorp has highest sales per dealer of 7,528 units

Raw Material analysis FY11 Price per Kg Weight in bike (Kg) Cost per unit

Hot Rolled steel 36.9 16 589.7

Cold Rolled steel 41.8 40 1671.0

Galvanised steel 45.6 10 455.8

Aluminium 125.1 15 1876.7

Plastics 75.0 7 525.0

Tyre 700

Cost of basic raw material (per unit) 5818.2

Conversion cost and taxes (per unit) 14961.1

Cost of raw material (per unit) 20779.3

Raw material cost accounts for about 65-70% of net sales value. Basic raw material cost account for about 25-28% of the overall raw material cost, whilst the rest is accounted for by conversion cost (cost of converting the metal to required component in line with design specification of OEM), margin of auto component manufacturer and taxes.

Company Background

Bajaj Holdings & Investment Limited (BHIL) – erstwhile Bajaj Auto Limited was de-merged on 18 December 2007, whereby its manufacturing undertaking was transferred to the new Bajaj Auto Limited (BAL) and its strategic business undertaking consisting of wind farm business and financial services business was vested with Bajaj Finserv Limited (BFS). All the businesses and all properties, assets, investments and liabilities of erstwhile Bajaj auto Ltd, other than the manufacturing undertaking and the strategic business undertaking, now remain with BHIL. BAL is the second largest two wheeler manufacturer and the largest manufacturer of three wheelers in the country. BAL is also the largest exporter of two and three wheelers and derives about 30% of revenues from exports. BAL has two subsidiaries PT Bajaj Auto Indonesia which assembles and markets motorcycles in Indonesia and Bajaj Auto International holdings BV which acts as a holding company. BAL holds 39% in Austrian motorcycle manufacturer KTM Power Sports AG through this subsidiary

Bajaj Auto Limited ACMIIL 13

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Company Analysis

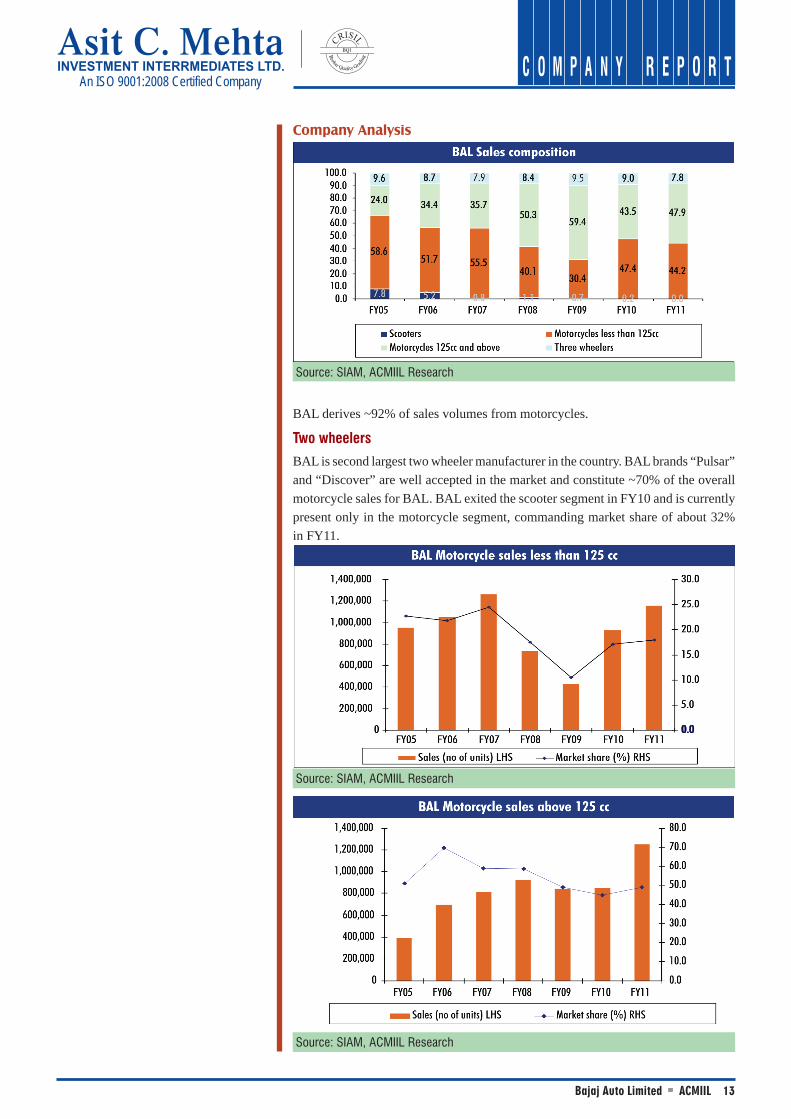

BAL derives ~92% of sales volumes from motorcycles.

Two wheelers

BAL is second largest two wheeler manufacturer in the country. BAL brands “Pulsar” and “Discover” are well accepted in the market and constitute ~70% of the overall motorcycle sales for BAL. BAL exited the scooter segment in FY10 and is currently present only in the motorcycle segment, commanding market share of about 32% in FY11.

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Bajaj Auto Limited ACMIIL 14

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

BAL is also the largest exporter of motorcycles in the country. It commands market share of ~ 65 % in overall motorcycle exports.

Three Wheelers

BAL is the largest manufacturer and exporter of three wheeler passenger carriers in the country commanding overall market share of about 62%.

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Source: SIAM, ACMIIL Research

Bajaj Auto Limited ACMIIL 15

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Three wheeler goods carrier industry has been under pressure due to structural shift in movement of goods from three wheelers to sub one tonne four wheelers.

BAL has three manufacturing locations two in Maharashtra at Waluj and Chakan and one in Pantnagar, Uttaranchal.

Plantwise capacity no of units (Mn) Products Manufactured

Waluj 1.8 (incl 0.5 for three wheelers) Motorcycle, Three wheelers

Chakan 1.2 Motorcycles

Pantnagar 1.8 Motorcycles

Source: Company

BAL Pantnagar plant has fiscal incentives in form of zero excise and zero income tax. The excise benefit can be availed till 2017, whilst the income tax benefit would partially expire in 2012 (post 2012 only 30% of profits would be exempt from income tax). In FY11, production at Pantnagar plant was 0.92 million. (representing 24% of overall production).

SWOT Analysis

Strengths·

● Largest three wheeler and second

largest two wheeler manufacturer

having established brand and extensive

dealer network

● Strong presence in expor t markets

( e x p o r t s c o n t r i b u t e 3 0 % o f

revenues)

● Market leader in 125cc and above

segment havng market share of

49%

● Technological collaboration with

KTM to bolster presence in spor ts

segment

● Captive finance support sales.

Weakness·

● No presence in the fast growing scooter

segment·

● No presence in sub one tonne four

wheeler goods carrier

● Less service centers compared to peers

Opportunities·

● Low penetration of two wheelers

● Rising rural and urban income·

● Large youth population

Threats·

● Intense competition from existing

players.

● Competition from low cost cars (Tata

Nano)·

● Replacement of expor t incentive

scheme

● \Withdrawal of fiscal incentive (income

tax exemption) from Pantnagar plant

Valuation and recommendation

The growth in domestic market is expected to remain robust. Given broader product portfolio we expect BAL to gain market share. Also BAL thrust on exports will enable it to increase revenues going forward. We assign multiple of 15x to BAL FY13E core business EPS of 89.4 to arrive at value of 1,342 for core business. Adding Cash and investment per share of 137 and investment in KTM at 30 (based on 20% discount to market Cap), we arrive at value of 1,509 for BAL. We assign “Hold” rating on the stock.

Bajaj Auto Limited ACMIIL 16

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Financials Profit and loss statement in ` Million

Particulars FY09 FY10 FY11 FY12E FY13E

Net Sales 84,460.3 115,431.6 160,287.0 188,916.1 213,183.2

Add : Other operating income 3,313.9 4,031.4 5,546.8 5,566.2 4,610.8

Operating income 87,774.2 119,463.0 165,833.8 194,482.3 217,794.0

less: Expenditure 77,049.2 94,026.1 132,842.8 158,099.2 178,720.5

Operating Profit 10,725.0 25,436.9 32,991.0 36,383.1 39,073.6

Other income 1,592.9 1,503.5 4,246.7 3,819.4 4,191.2

less: Depreciation 1,306.2 1,374.1 1,238.9 1,309.1 1,413.8

PBIT 11,011.7 25,566.3 35,998.8 38,893.5 41,850.9

less:Interest 218.9 67.5 23.9 20.0 22.0

PBT before exceptional items 10,937.0 25,655.5 36,141.5 39,050.1 42,015.5

Exceptional item -2,051.0 -1,615.0 8,268.2

PBT 8,886.0 24,040.5 44,409.7 39,050.1 42,015.5

Income from associate -622.4 -1,027.6 231.1

less:Tax 2,888.8 7,034.5 10,092.9 10,528.7 13,265.1

Net Profit 5,374.8 15,978.4 34,547.9 28,521.4 28,750.4

Adj Net Profit (excl Excep item and Other income)

6,540.9 16,906.4 23,002.5 25,731.8 25,882.5

Sales Growth (%) 36.7 38.9 17.9 12.8

Operating Profit Growth (%) 137.2 29.7 10.3 7.4

Adj Net profit growth 158.5 36.1 11.9 0.6

Operating Margin (%) 12.2 21.3 19.9 18.7 17.9

Net Profit Margin (%) 7.5 14.2 13.9 13.2 11.9

Source: Company, ACMIIL Research

Balance Sheet in ` Million

Particulars FY09 FY10 FY11 FY12E FY13E

Share Capital 1,446.8 1,446.8 2,893.7 2,893.7 2,893.7

Reserves & Surplus 16,681.1 25,722.5 45,178.5 53,443.4 61,937.4

Total Shareholders Fund 18,127.9 27,169.3 48,072.2 56,337.1 64,831.1

Total Loans 15,953.6 13,610.3 3,474.5 3,300.8 3,135.7

Deferred Tax Liability 41.9 16.9 297.1 297.1 297.1

Total Sources of Fund 34,123.4 40,800.3 51,846.7 59,937.9 68,266.8

Gross Block 33,395.1 33,855.0 33,984.2 36,363.1 39,272.1

less:Depreciation 18,093.9 19,021.6 19,160.5 20,469.6 21,883.4

Net Block 15,301.2 14,833.4 14,823.7 15,893.5 17,388.8

Investments 14,231.9 34,452.3 42,842.1 51,410.5 64,263.2

Goodwill on investment in associate 3,672.3 3,289.9 3,685.6 3,685.6 3,685.6

Total Current Assets 23,019.2 16,112.9 29,054.0 43,032.7 43,778.4

Total Current Liabilities 24,581.0 28,641.6 39,669.1 55,346.2 61,860.9

Net Current Assets -1,561.8 -12,528.7 -10,615.1 -12,313.5 -18,082.5

Total Application Of Fund 34,123.4 40,800.3 51,846.7 59,937.9 68,266.8

Source: Company, ACMIIL Research

Bajaj Auto Limited ACMIIL 17

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Cash Flow statement in ` Million

Particulars FY09 FY10 FY11 FY12E FY13E

Profit Before Tax 8,263.6 23,012.9 44,640.8 39,050.1 42,015.5

Depreciation 1,306.2 1,374.1 1,238.9 1,309.1 1,413.8

Net Operating Profit Before working capital change

10,780.6 24,791.4 34,253.0 37,504.3 40,326.1

Working capital changes -2,161.9 8,028.4 -3,924.5 6,374.0 4,438.3

Taxes paid -3,237.9 -6,997.4 -9,749.0 -10,528.7 -13,265.1

Net Cash Flow from Operating activities 3,286.8 25,640.8 20,393.7 33,349.6 31,499.3

Net Cash used in Investment Activities -1,730.1 -19,350.4 -11,004.8 -8,223.9 -12,386.4

Net Cash from Financing activities -1,105.9 -6,126.3 -8,628.5 -20,450.2 -20,443.5

Net Increase/decrease in cash & cash equivalent 714.0 -353.4 679.5 4,675.5 -1,330.7

Cash at Beginning 712.4 1,426.4 1,073.0 1,752.5 6,428.0

Cash at End of Period 1,426.4 1,073.0 1,752.5 6,428.0 5,097.4

Source: Company, ACMIIL Research

Valuation ratios

Particulars FY09 FY10 FY11 FY12E FY13E

Profitability Ratios

Operating Margins (%) 12.2 21.3 19.9 18.7 17.9

PAT Margin(%) 6.1 13.4 20.8 14.7 13.2

RONW % (excl exceptional item) 42.2 66.1 54.1 50.6 44.3

ROCE % 32.3 62.7 69.4 64.9 61.3

Capital Structure Ratios

Debt-Equity

Turnover Ratios 0.9 0.5 0.1 0.1 0.0

Fixed Assets

Inventory 2.5 3.4 4.7 5.2 5.4

Debtors 22.7 25.2 27.8 28.5 28.3

Creditors 30.1 48.4 46.9 48.0 47.5

Solvency Ratios 9.4 6.0 7.8 8.8 8.6

Current Ratio

Interest Coverage Ratio 0.9 0.6 0.7 0.8 0.7

Valuation Ratios 50.3 378.8 1506.2 1944.7 1902.3

EPS 45.2 116.9 79.5 88.9 89.4

BV/Share 125.3 187.8 166.1 194.7 224.0

EV/EBIDTA (x) 10.0 9.3

Source: Company, ACMIIL Research

Bajaj Auto Limited ACMIIL 18

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Motorcycle comparison

Comparison Matrix

Less than 125 cc motorcyclesParticulars Engine Power (ps) Gearbox Pick UP (0-60) sec Fuel

EfficiencykmplPrice Mumbai Ex

Showroom (in 000)

Hero MotoCorp

CD Dawn 97.2 7.8 4 7.8 82.9 35.65

CD Deluxe 97.2 7.8 4 7.8 82.9 41.3

Splendor Plus (Cast Wheell) 97.2 7.51 4 12.2 80.6 44.2

Splendor NXG (Cast Self) 97.2 7.7 4 8.6 87.7 45.75

Splendor Pro (Cast Self) 97.2 7.4 4 12.2 90.1 46.86

Passion Pro (Cast Self) 97.2 7.5 4 12.2 84.0 49.33

Passion Plus (Cast Wheel) 97.2 7.5 4 12.2 NA 46.18

Bajaj Auto

Discover 100 DTS-SI 94.38 7.7 5 8.6 90.3 44.61

Platina 100 99 8.3 4 9.68 76.0 37.89

TVS Motors

TVS Star City Mag ES 109.7 9.2 4 10 77.1 42.96

TVS Star City Mag KS 109.7 9.2 4 10 77.1 38.98

TVS Sports 99.7 7.4 4 9.4 82.9 34.53

Jive 109 8.4 4 7.2 82.0 42.68

Honda India

Twister Self Disc 109 9 4 6.5 85.7 53.35

Twister Self Drum 109 9 4 6.5 85.7 50.14

Twister Kick Drum 109 9 4 6.5 85.7 47.21

Source : Industry, SIAM, ACMIIL Researc

Hero MotoCorp has dominant presence in the 100 cc segment, with its flagship brands Dawn and Deluxe. The Dawn is available at attractive price point of 35.65 thousand, offering highest mileage of 82.9 Km/per litre at that price point. Dawn with sale of 7.2 lakh units in FY11 has enabled Hero MotoCorp to garner 8% market share of overall motorcycles. TVS Star City as well as Bajaj Platina 100 are available at that price point but offer lower mileage, leading to Hero MotoCorp dominance in that segment.

Prior to launch of Discover 100 cc, BAL presence was miniscule in less than 125 cc segment. Launch of Discover 100 turned around BAL position in this space. The Discover 100 cc has highest fuel efficiency of 90.3 kmpl in this segment, albeit with higher price of 44.61 thousand. Nonetheless, this has lead to higher sales of Discover 100 cc (8.9 lakh units in FY11).

Hero MotoCorp brands Splendor and Passion account for major chunk of its sales 23.1 lakh and 13 lakh in FY11. The newly launched Splendor NXG with superior mileage has resulted in continued higher sales of Splendor bikes.

Honda India marked entry in less than 125 cc segment with launch of Twister. Twister is expensive product in this segment, but offers superior performance (higher power and pick up).

Bajaj Auto Limited ACMIIL 19

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

125 cc and above motorcyclesParticulars Engine Power (ps) Gearbox Pick UP (0-60) sec Fuel

EfficiencykmplPrice Mumbai Ex

Showroom (in 000)

125 cc and above

Hero MotoCorp

Super Splendor (Db Es) 124.7 9.13 4 7.4 83.1 50.28

Glamour (Disc) 125 9.13 4 7.4 81.1 53.64

Glamour (FI) 125 9.13 4 7.4 81.1 61.79

CBZ Extreme 149.1 14.4 5 5.7 65.1 65.53

Hunk 149.1 14.4 5 5.6 65.1 65.26

Karizma ZMR (FI) 223 17.8 5 4.5 51.0 99.26

Bajaj Auto

Platina 125 DTS-SI 124.5 8.5 5 6.8 80.2 40.97

Discover 125 DTS-SI 124.6 11 5 6.21 NA 45.9

Pulsar 135 LS 134.6 13.5 5 5.5 68.1 55.4

Discover 150 DTS-SI 144.8 13 5 5.39 72.3 50.7

Pulsar 150 DTS i 149 15.06 5 5.6 62.1 65.28

Pulsar 180 DTS i 179 17 5 5.08 58.5 69.07

Pulsar 220 DTS i 220 19.2 5 4.5 54.0 75.1

TVS Motors

Flame SR 125 10.6 4 8.11 85.8 48.6

Flame DS 125 10.3 4 7.9 85.8 45.76

Apache RTR 160 159.7 15.5 5 5.27 60.1 63.52

Apache RTR 160 FI 159.7 15.9 5 4.73 NA 66.72

Apache RTR 180 177.4 17.3 5 4.5 55.7 70.47

Honda India

Shine Kick Drum 124.6 10.3 4 5.84 74.7 48.33

Shine Self Drum 124.6 10.3 4 5.84 74.7 52.6

Shine Self Disc 124.6 10.3 4 5.84 74.7 55.8

CBF Stunner ES 124.7 11.1 5 6.2 70.3 55.12

CBF Stunner FI 124.7 11.6 5 6.2 68.5 76.71

CB Unicorn 149.1 13.5 5 5.9 71.2 64.93

Unicorn Dazzler 149.1 14 5 5.48 62.2 68.39

Source : Industry, SIAM, ACMIIL Research

Bajaj Auto has dominant presence in 125cc and above segment.

125-150 cc segmentIn 125 to 150 cc segment, BAL has Platina 125 cc which comes at attractive price point of 40.97 thousand. BAL bike have superior performance in the 125-150 cc segment as well as come with lower price tag as compared to competition. The launch of Pulsar 135 has created a different segment, offering better performance and affordability. Pulsar 135 has ensured increased sale of Pulsar bikes and gain in market share for BAL. Honda India bestseller Shine is attractively priced and offers superior performance than competition (after BAL Discover 125).Hero MotoCorp and TVS Motors offer higher fuel efficiency but are low on performance (which is of importance in this segment), leading to lower sales.150 cc and above segmentThe flagship Pulsar 150 cc has slightly superior performance as compared to peers. The launch of Discover 150 cc by BAL has once again created a different segment

Bajaj Auto Limited ACMIIL 20

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

(more power at astonishing price of 50.7 thousand, which is the lowest in this segment). Discover 150 cc sold 3.3 lakh units in FY11 and contributed to higher market share of BAL in the segment.Honda India CB Unicorn offers higher fuel efficiency at attractive price point resulting in higher sales. Although it has lower performance than Pulsar 150, better fuel efficiency and attractive price has made it strong contender in the segment.TVS Motors Apache RTR 160 FI has created niche of its own in the segment clocking sales of 1.5 lakh units in FY11.

Bajaj Auto Limited ACMIIL 21

C O M P A N Y R E P O R TAn ISO 9001:2008 Certified Company

INVESTMENT INTERRMEDIATES LTD.

1

Disclaimer:

This report is based on information that we consider reliable, but we do not represent that it is accurate or complete and it should not be relied upon such. ACMIIL or

any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information

contained in the report. ACMIIL and/or Promoters of ACMIIL and/or the relatives of promoters and/or employees of ACMIIL may have interest/position, financial or

otherwise in the securities mentioned in this report. To enhance transparency we have incorporated a Disclosure of Interest Statement in this document. This should

however not be treated as endorsement of the views expressed in the report

Disclosure of Interest Bajaj Auto Ltd

1. Analyst ownership of the stock NO

2. Broking Relationship with the company covered NO

3. Investment Banking relationship with the company covered NO

4. Discretionary Portfolio Management Services NO

This document has been prepared by the Research Desk of Asit C Mehta Investment Interrmediates Ltd. and is meant for use of the recipient only and is not for

circulation. This document is not to be reported or copied or made available to others. It should not be considered as an offer to sell or a solicitation to buy any security.

The information contained herein is from sources believed reliable. We do not represent that it is accurate or complete and it should not be relied upon as such. We

may from time to time have positions in and buy and sell securities referred to herein.

SEBI Regn No: BSE INB 010607233 (Cash); INF 010607233 (F&O), NSE INB 230607239 (Cash); INF 230607239 (F&O)

Notes:

Institutional Sales:

Prakash Diwan, Tel: 91 22 2858 3400

Kirti Bagri, Tel: +91 22 2858 3731

K.Subramanyam, Tel: +91 22 2858 3739

Email: [email protected]

Institutional Dealing:

Email: [email protected]