banca imi investment seminar milan, 8 march 2001 2000-2001 exceeding our targets

TRANSCRIPT

Banca IMI Investment SeminarBanca IMI Investment SeminarMilan, 8 March 2001Milan, 8 March 2001

2000-2001 Exceeding our targets2000-2001 Exceeding our targets

Banca IMI Investment Seminar - Milan, 8 Banca IMI Investment Seminar - Milan, 8 March 2001March 2001

• Giovanni RecordatiGiovanni Recordati Chairman and Chief Executive Chairman and Chief Executive OfficerOfficer

• Fritz SquindoFritz Squindo Chief Financial OfficerChief Financial Officer

• Walter BevilacquaWalter Bevilacqua Vice President Corporate Vice President Corporate DevelopmentDevelopment

22

Giovanni RecordatiGiovanni RecordatiChairman and Chief Executive OfficerChairman and Chief Executive Officer

33

44

WHO WE AREWHO WE ARE

• In business for 75 yearsIn business for 75 years• A public company since 1984A public company since 1984• Always profitable, a regular dividend paidAlways profitable, a regular dividend paid• A strong, aggressive marketerA strong, aggressive marketer• A long-lasting commitment to R&DA long-lasting commitment to R&D• R&D success accelerates growthR&D success accelerates growth

55

KEY EVENTS IN 2000KEY EVENTS IN 2000

• Strong improvement in businessStrong improvement in business• Expansion in France completed successfullyExpansion in France completed successfully• ZanidipZanidip®® license for the USA license for the USA• Pharmacia agreement: a strong basis for Pharmacia agreement: a strong basis for

further growthfurther growth

Fritz SquindoFritz SquindoChief Financial OfficerChief Financial Officer

66

• YEAR 2000 RESULTSYEAR 2000 RESULTS• QUARTERLY SALES AND EBITQUARTERLY SALES AND EBIT• COMPOSITION OF SALESCOMPOSITION OF SALES• YEAR 2000 GROWTHYEAR 2000 GROWTH• EBITDA BY BUSINESS AREAEBITDA BY BUSINESS AREA• CAPITAL EMPLOYEDCAPITAL EMPLOYED

77

88

526.3526.3

281.7281.753.5%53.5%

37.237.27.1%7.1%

38.638.67.3%7.3%

23.223.24.4%4.4%

72.272.213.7%13.7%

19991999

58.758.711.2%11.2%

689.1689.1

399.5399.558.0%58.0%

90.390.313.1%13.1%

79.879.811.6%11.6%

53.153.17.7%7.7%

136.7136.719.8%19.8%

20002000

71.471.410.4%10.4%

30.9%30.9%

41.8%41.8%

142.5%142.5%

107.1%107.1%

128.9%128.9%

89.3%89.3%

Change Change %%

21.6%21.6%

YEAR 2000 RESULTSYEAR 2000 RESULTS

Net SalesNet Sales

Gross ProfitGross Profitas % of salesas % of sales

Operating Income Operating Income as % of salesas % of sales

Pretax IncomePretax Incomeas % of salesas % of sales

Net IncomeNet Incomeas % of salesas % of sales

EBITDAEBITDAas % of salesas % of sales

(billion lira)(billion lira)

R&D ExpensesR&D Expensesas % of salesas % of sales

99

QUARTERLY SALES DEVELOPMENTQUARTERLY SALES DEVELOPMENT

0

50

100

150

200

250

Q1 Q2 Q3 Q4

1999

2000

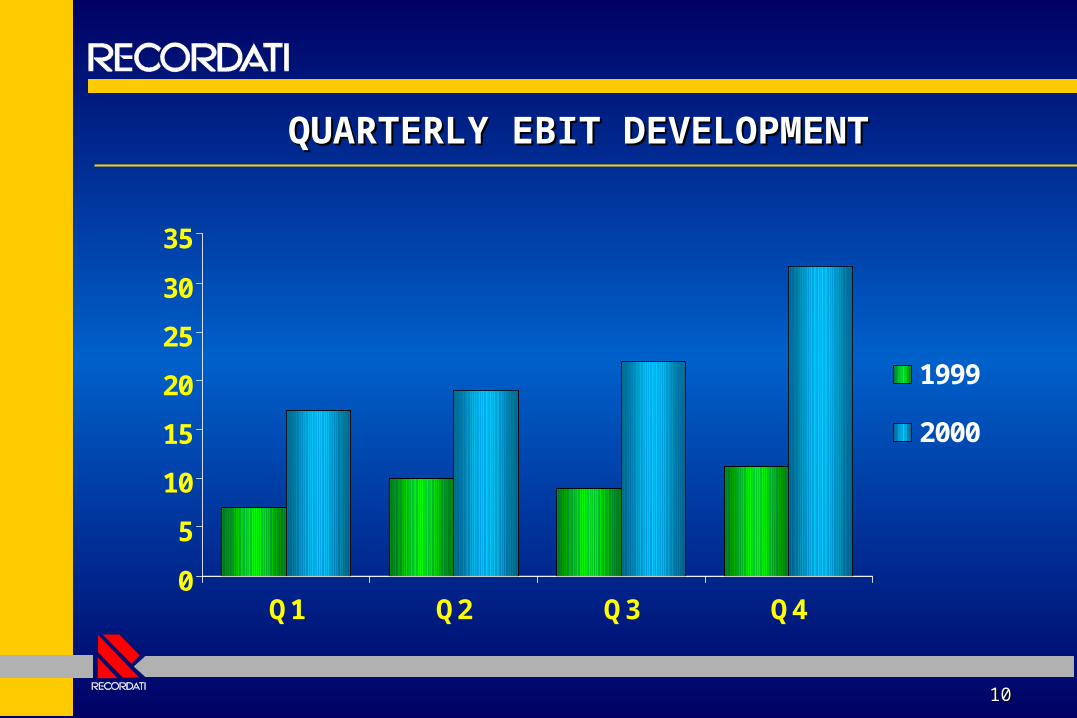

1010

QUARTERLY EBIT DEVELOPMENTQUARTERLY EBIT DEVELOPMENT

0

5

10

15

20

25

30

35

Q1 Q2 Q3 Q4

1999

2000

1111

20002000

393.4393.457.1%57.1%

19991999 Change Change %%

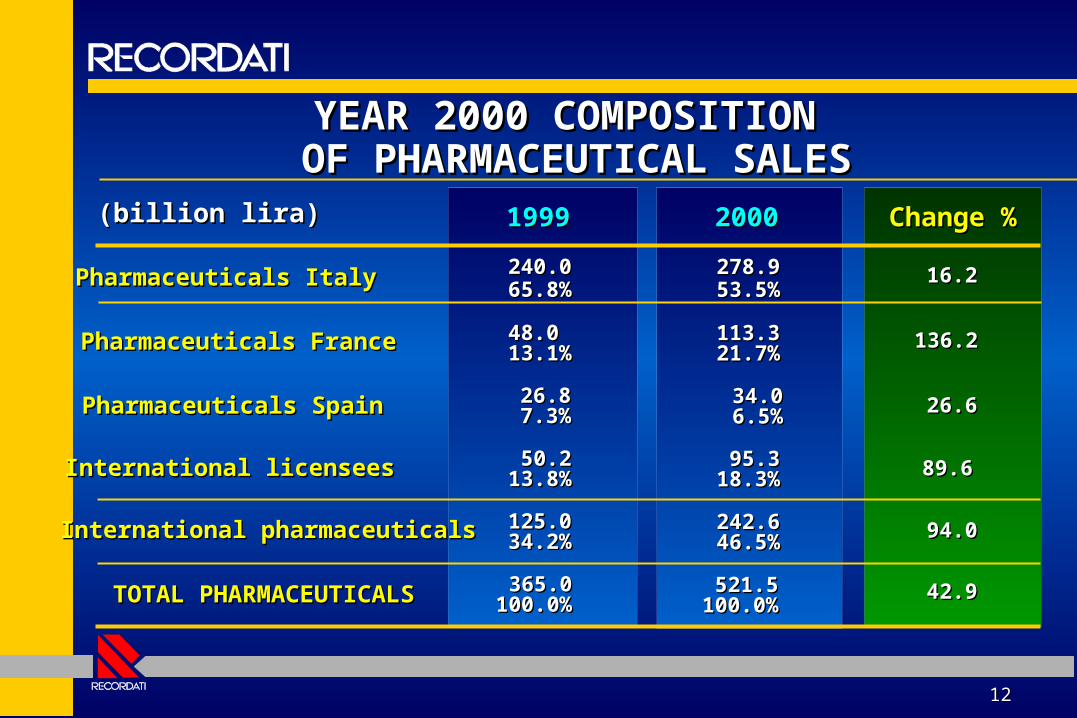

YEAR 2000 COMPOSITION OF SALESYEAR 2000 COMPOSITION OF SALES

(billion lira)(billion lira)

PHARMACEUTICALPHARMACEUTICALSS

365.0365.069.3%69.3%

47.747.7

ACTIVE ACTIVE INGREDIENTS & INGREDIENTS & INTERMEDIATESINTERMEDIATES

TOTATOTALL

ITALYITALY

INTERNATIONAINTERNATIONALL

161.3161.330.7%30.7%

526.3526.3100.0%100.0%

260.0260.049.4%49.4%

266.3266.350.6%50.6%

521.5521.575.7%75.7%

167.6167.624.3%24.3%

689.1689.1100.0%100.0%

295.7295.742.9%42.9%

42.942.9

3.93.9

30.930.9

13.713.7

1212

2000200019991999 Change Change %%

278.9278.953.5%53.5%

113.3113.321.7%21.7%

95.395.318.3%18.3%

242.6242.646.5%46.5%

521.5521.5100.0100.0

%%

34.034.0 6.5%6.5%

240.0240.065.8%65.8%

48.0 48.0 13.1%13.1%

50.250.213.8%13.8%

125.0125.034.2%34.2%

365.0365.0100.0%100.0%

26.826.87.3%7.3%

16.216.2

136.2136.2

89.689.6

94.094.0

42.942.9

26.626.6

YEAR 2000 COMPOSITION YEAR 2000 COMPOSITION OF PHARMACEUTICAL SALESOF PHARMACEUTICAL SALES

Pharmaceuticals ItalyPharmaceuticals Italy

Pharmaceuticals FrancePharmaceuticals France

International licenseesInternational licensees

International pharmaceuticalsInternational pharmaceuticals

TOTAL PHARMACEUTICALSTOTAL PHARMACEUTICALS

Pharmaceuticals SpainPharmaceuticals Spain

(billion lira)(billion lira)

1313

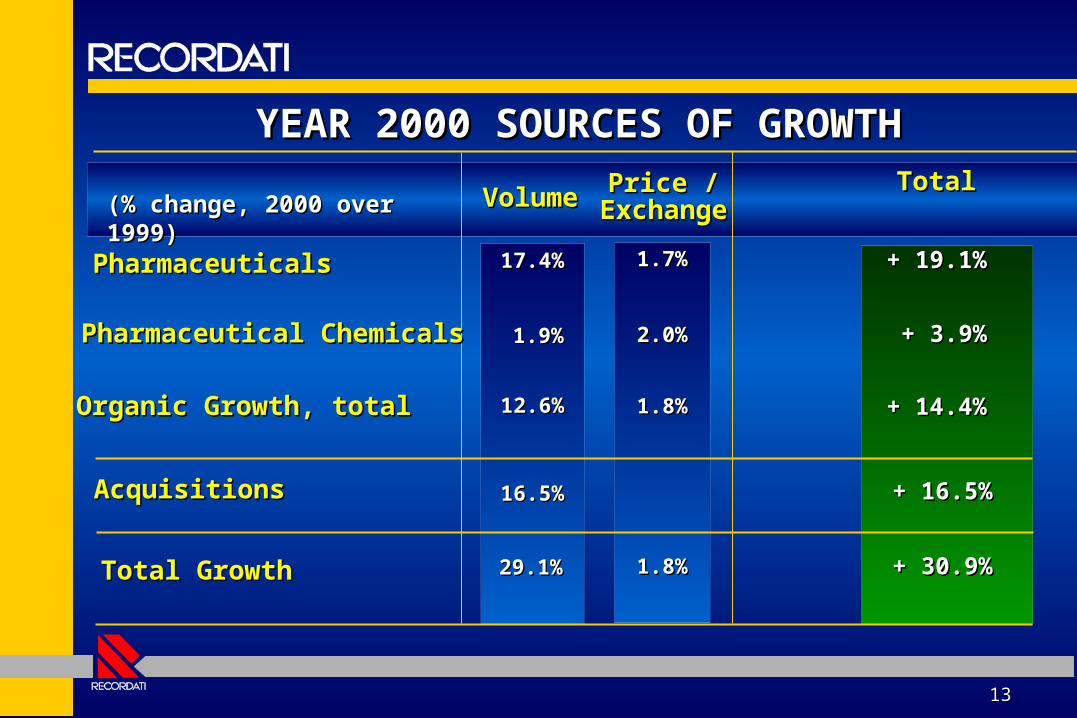

17.4%17.4%

29.1%29.1%

YEAR 2000 SOURCES OF GROWTHYEAR 2000 SOURCES OF GROWTH

PharmaceuticalsPharmaceuticals

Total GrowthTotal Growth

1.7%1.7%

1.8%1.8%

TotalTotal

+ 30.9%+ 30.9%

+ + 14.4%14.4%

(% change, 2000 over (% change, 2000 over 1999)1999)

Price /Price /ExchangExchang

ee

16.5%16.5% + 16.5%+ 16.5%

Pharmaceutical ChemicalsPharmaceutical Chemicals

Organic Growth, totalOrganic Growth, total

1.9%1.9% 2.0%2.0%

12.6%12.6% 1.8%1.8%

AcquisitionsAcquisitions

+ 19.1%+ 19.1%

+ 3.9%+ 3.9%

VolumVolumee

1414

37.537.510.3%10.3%

37.237.2 7.1%7.1%

YEAR 2000 EBITDA BY BUSINESS AREAYEAR 2000 EBITDA BY BUSINESS AREA

PharmaceuticalsPharmaceuticalsas % of salesas % of sales

Operating IncomeOperating Incomeas % of salesas % of sales

99.699.619.1%19.1%

90.390.313.1%13.1%

Change %Change %

+ 142.5%+ 142.5%

+ + 89.2%89.2%

(billion lira)(billion lira)

* Including inter-company sales* Including inter-company sales

20002000

28.428.4 30.930.9 + 8.9%+ 8.9%

Pharmaceutical ChemicalsPharmaceutical Chemicalsas % of sales*as % of sales*

TotalTotalas % of salesas % of sales

34.834.819.9%19.9%

37.137.120.3%20.3%

72.372.313.7%13.7%

136.7136.719.8%19.8%

Operating depreciationOperating depreciation

Goodwill amortizationGoodwill amortization 15.515.56.76.7

+ + 165.8%165.8%

+ 6.6%+ 6.6%

+ 133.0%+ 133.0%

19991999

1515

IMPACT OF ACQUISITION OF BOUCHARAIMPACT OF ACQUISITION OF BOUCHARA

• Consolidated since Q3Consolidated since Q3• Contributes to sales growthContributes to sales growth• Goodwill amortized over 5 years, starting Q3 Goodwill amortized over 5 years, starting Q3

20002000• Contributes to EBIT after amortization of Contributes to EBIT after amortization of

goodwillgoodwill

1616

1999199931/1231/12

103.3103.3

233.5233.550.250.2

(36.5)(36.5)

300.3300.3

86.986.9

213.4213.4

300.3300.3

CAPITAL EMPLOYEDCAPITAL EMPLOYED

Net Working Capital Net Working Capital for Operationsfor OperationsNet Non-current AssetsNet Non-current Assetsof which goodwillof which goodwill

Reserves for Long - termReserves for Long - termLiabilitiesLiabilities

FINANCING OF FINANCING OF CAPITAL EMPLOYEDCAPITAL EMPLOYED

Net DebtNet Debt

Shareholders’ EquityShareholders’ Equity

CAPITAL EMPLOYEDCAPITAL EMPLOYED

(billion lira)(billion lira)

182.2182.2

376.5376.5135.0135.0

(43.1)(43.1)

515.6515.6

250.2250.2

265.4265.4

515.6515.6

2000200031/1231/12

Walter BevilacquaWalter BevilacquaVice President Corporate DevelopmentVice President Corporate Development

1717

ZANIDIPZANIDIP®® WORLDWIDE WORLDWIDESITUATION AND OUTLOOKSITUATION AND OUTLOOK

1818

1919

ZANIDIPZANIDIP®® (LERCANIDIPINE) (LERCANIDIPINE)A COMPARATIVE PRODUCT PROFILEA COMPARATIVE PRODUCT PROFILE

• Latest generation calcium-channel blockerLatest generation calcium-channel blocker

• Natural once a day Natural once a day

• Efficacy comparable to best competitorsEfficacy comparable to best competitors

• Excellent / superior tolerability and safety Excellent / superior tolerability and safety

profileprofile

2020

ZANIDIPZANIDIP®® (LERCANIDIPINE) (LERCANIDIPINE)THE REFERENCE MARKETTHE REFERENCE MARKET

• Hypertension is the largest indication Hypertension is the largest indication

worldwide - over $30 billionworldwide - over $30 billion

• Addressed by several classes of drugsAddressed by several classes of drugs

• CCBs are one of the largest, about $10 billionCCBs are one of the largest, about $10 billion

• The leading brand is NorvascThe leading brand is Norvasc® (amlodipine), (amlodipine),

sold by Pfizer, about $3.4 billion sold by Pfizer, about $3.4 billion

2121

LERCANIDIPINE IN ITALYLERCANIDIPINE IN ITALYMARKET SHARE AS A % OF NORVASCMARKET SHARE AS A % OF NORVASC®®

0%

10%

20%

1998 1999 2000

Zanedip® as a% of Norvasc®

lercanidipineas a % ofamlodipine

2222

LERCANIDIPINE IN ITALYLERCANIDIPINE IN ITALYMARKET SHARE AS A % OF OTHER CCBsMARKET SHARE AS A % OF OTHER CCBs

0%

5%

10%

15%

1998 1999 2000

Zanedip® as a% of otherCCBs

lercanidipineas a % of otherCCBs

(amlodipine (amlodipine excluded)excluded)

2323

19991999 20002000

YEAR 2000 LERCANIDIPINE SALESYEAR 2000 LERCANIDIPINE SALES

SALES TO LICENSEES*SALES TO LICENSEES*

(billion lira)(billion lira) Change Change %%

30.130.1 50.350.3

25.125.115.015.0

75.475.4

+67.1+67.1

+67.3+67.3

+67.2+67.245.145.1

10.9%10.9%8.6%8.6%

* Excluding licensing income* Excluding licensing income

DIRECT SALESDIRECT SALES

% OF TOTAL SALES% OF TOTAL SALES

TOTALTOTAL

2424

ROLL OUT HISTORYROLL OUT HISTORY

19981998

AUSTRIAAUSTRIAGREECEGREECEISRAELISRAELITALYITALYLUXEMBOURGLUXEMBOURGNETHERLANDSNETHERLANDS**

SPAINSPAINUKUK

19991999

BELGIUMBELGIUMBRAZIL BRAZIL LEBANONLEBANON

1H-20001H-2000

CHILE CHILE DENMARKDENMARKFINLANDFINLANDKOREAKOREAPHILIPPINESPHILIPPINESSWEDENSWEDEN

2H-20002H-2000

CYPRUSCYPRUSGERMANYGERMANYKUWAITKUWAITNORWAYNORWAYPAKISTANPAKISTAN

EXPECTEDEXPECTED20012001

ARGENTINAARGENTINAFRANCEFRANCEECUADORECUADORHONG KONGHONG KONGMEXICOMEXICOSINGAPORESINGAPORETAIWANTAIWANTURKEYTURKEYVENEZUELAVENEZUELAVIETNAMVIETNAM

* Dec. 1997* Dec. 1997

2525

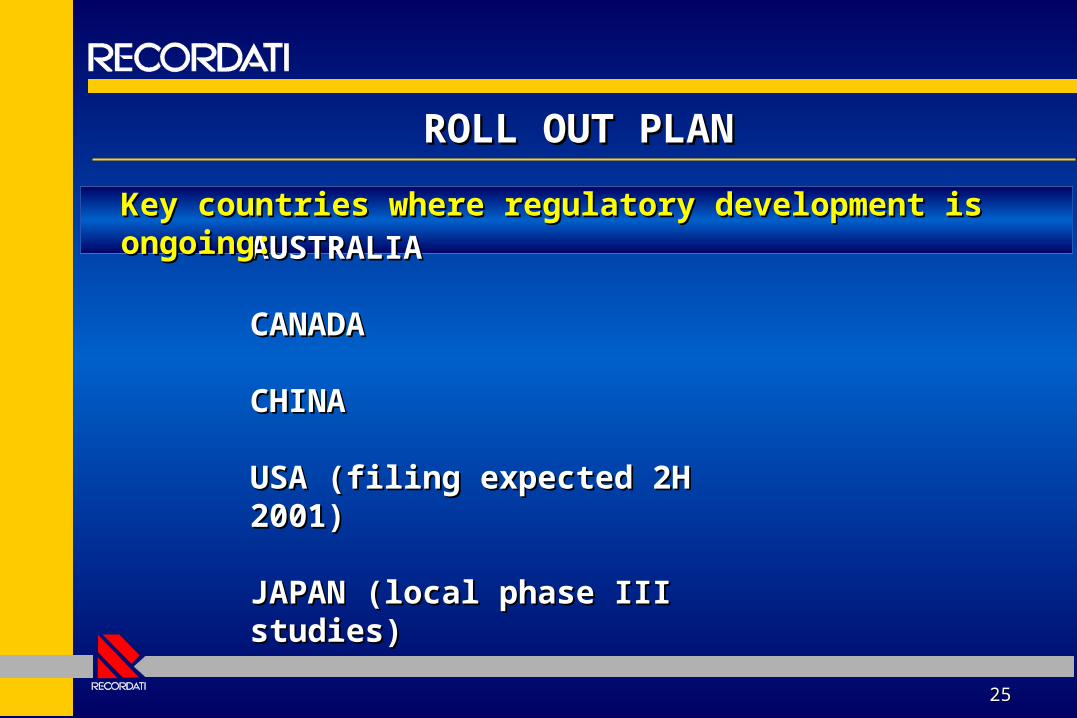

ROLL OUT PLANROLL OUT PLAN

AUSTRALIAAUSTRALIA CANADACANADA

CHINACHINA USA (filing expected 2H USA (filing expected 2H 2001)2001)

JAPAN (local phase III JAPAN (local phase III studies)studies)

Key countries where regulatory development is Key countries where regulatory development is ongoing:ongoing:

2626

LICENSING / ROLL OUT TARGETS LICENSING / ROLL OUT TARGETS

ANNOUNCED FOR 2003ANNOUNCED FOR 2003

TO BE MET IN 2001TO BE MET IN 2001

ROLL OUT PLANROLL OUT PLAN

ZANIDIPZANIDIP®® IN THE USA IN THE USAFOREST LABORATORIES LICENSE AGREEMENTFOREST LABORATORIES LICENSE AGREEMENT

2727

2828

THE HYPERTENSION MARKET IN THE THE HYPERTENSION MARKET IN THE USAUSA

• Hypertension affects over 50 million people in Hypertension affects over 50 million people in the U.S. the U.S.

• Market size exceeding 10 bn US$ in annual salesMarket size exceeding 10 bn US$ in annual sales

• Calcium Channel Blockers account for well over Calcium Channel Blockers account for well over one third of the anti-hypertensive market…one third of the anti-hypertensive market…

• NorvascNorvasc® ® sales exceed $1.5 billionsales exceed $1.5 billion

Source: Recordati / Forest LaboratoriesSource: Recordati / Forest Laboratories

2929

FOREST LABORATORIES: THE RIGHT FOREST LABORATORIES: THE RIGHT PARTNERPARTNER

• Annual sales exceeding 1.1 billion US$Annual sales exceeding 1.1 billion US$

• Sales force of over 1400 RepsSales force of over 1400 Reps

• Established presence in the cardiovascular marketEstablished presence in the cardiovascular market

• TiazacTiazac®® sales exceeding 150 ml US$ (5% market sales exceeding 150 ml US$ (5% market share)share)

• Strong track record in European partnerships & Strong track record in European partnerships & collaborations in FDA filingscollaborations in FDA filings

Source: Forest LaboratoriesSource: Forest Laboratories

3030

TIAZACTIAZAC®® SALES DEVELOPMENT SALES DEVELOPMENT

0

20

40

60

80

100

120

140

1997 1998 1999 2000

(million USD)(million USD)

25

85

130

158

5% market 5% market shareshare

Source: Forest LaboratoriesSource: Forest Laboratories Fiscal year ending MarchFiscal year ending March

3131

FILLING THE PIPELINE: ONGOING R&DFILLING THE PIPELINE: ONGOING R&D

• LERCANIDIPINELERCANIDIPINE- CLINICAL PROFILE- CLINICAL PROFILE- PATENT EXTENSIONS- PATENT EXTENSIONS- NEW COMBINATION PRODUCT- NEW COMBINATION PRODUCT- GENE EXPRESSION STUDIES- GENE EXPRESSION STUDIES

• GENITO-URINARY DISORDERS • GENITO-URINARY DISORDERS - URINARY INCONTINENCE/ UNSTABLE - URINARY INCONTINENCE/ UNSTABLE BLADDERBLADDER- BENIGN PROSTATIC HYPERPLASIA- BENIGN PROSTATIC HYPERPLASIA- FEMALE SEXUAL DYSFUNCTION- FEMALE SEXUAL DYSFUNCTION

3232

Genitourinary AllianceGenitourinary AllianceRecordati - PharmaciaRecordati - Pharmacia

1.1. The alliance takes advantage of each partner's strength in this The alliance takes advantage of each partner's strength in this area. It aims at gaining a leadership position in the area. It aims at gaining a leadership position in the pharmacological treatment of a number of genitourinary disorders, pharmacological treatment of a number of genitourinary disorders, particularly of micturition.particularly of micturition.

2.2. The initial announcement concerns the overactive bladder The initial announcement concerns the overactive bladder program.program.

3.3. The alliance has started work based on Recordati's discoveries. The alliance has started work based on Recordati's discoveries.

4.4. Research will be mainly conducted at Recordati. Pharmacia will be Research will be mainly conducted at Recordati. Pharmacia will be responsible for development. Recordati will manufacture the active responsible for development. Recordati will manufacture the active ingredients based on its compounds.ingredients based on its compounds.

5.5. Pharmacia will have worldwide marketing rights with Recordati co- Pharmacia will have worldwide marketing rights with Recordati co-marketing in certain territories.marketing in certain territories.

Giovanni RecordatiGiovanni RecordatiChairman and Chief Executive OfficerChairman and Chief Executive Officer

3333

3434

2000-2003 TARGETS2000-2003 TARGETS (Milan, May 2000)(Milan, May 2000)

2000200019991999

Net SalesNet Sales

Gross ProfitGross Profitas % of salesas % of sales

EPS (lira)EPS (lira)

Operating IncomeOperating Incomeas % of salesas % of sales

526.3526.3

281.7281.753.5%53.5%

37.237.27.1%7.1%

593.5593.5

329.9329.955.6%55.6%

931931

R&DR&Das % of salesas % of sales

58.758.711.2%11.2%

65.365.311.0%11.0%

61.661.610.4%10.4%

15421542

20032003

10001000

56156156.1%56.1%

10010010.0%10.0%

13013013.0%13.0%

30923092

CAGRCAGR1999-20031999-2003

17.4%17.4%

18.8%18.8%

14.2%14.2%

36.7%36.7%

35.0%35.0%

(billion lira)(billion lira)

3535

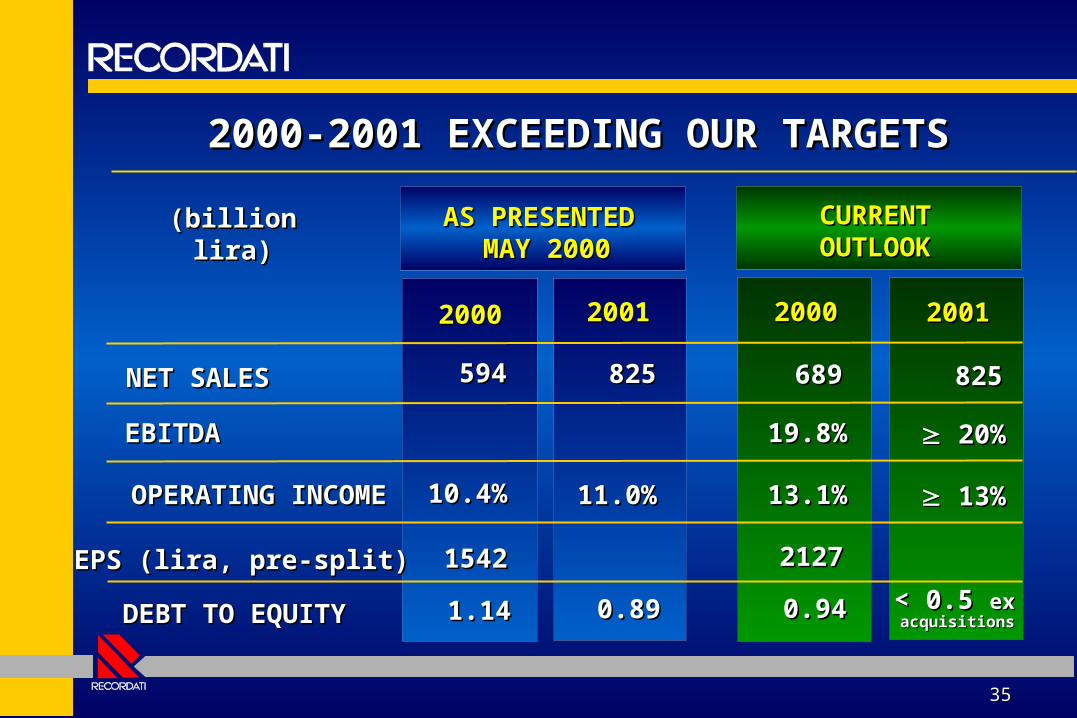

2000-2001 EXCEEDING OUR TARGETS2000-2001 EXCEEDING OUR TARGETS

2001200120002000

NET SALESNET SALES 594594 825825

OPERATING INCOMEOPERATING INCOME 10.4%10.4% 11.0%11.0%

20002000

689689

13.1%13.1%

20012001

825825

13%13%

(billion lira)(billion lira)AS PRESENTED AS PRESENTED

MAY 2000MAY 2000CURRENTCURRENTOUTLOOKOUTLOOK

EPS (lira, pre-split)EPS (lira, pre-split)

DEBT TO EQUITYDEBT TO EQUITY 0.940.940.890.891.141.14

15421542

< 0.5 < 0.5 exexacquisitionsacquisitions

21272127

EBITDAEBITDA 19.8%19.8% 20%20%

Banca IMI Investment SeminarBanca IMI Investment SeminarMilan, 8 March 2001Milan, 8 March 2001

2000-2001 Exceeding our targets2000-2001 Exceeding our targets