bank credit freeze shows signs of thawing

TRANSCRIPT

THE WATCH LIST NEWSLETTER 1

A WEEKLY COLUMN FOCUSING ON DISTRESSED MARKET CONDITIONS, COMMERCIAL REAL ESTATE PROPERTIES, MORTGAGES AND CORPORATIONS PUBLISHED BY COSTAR NEWS

IN THIS WEEK'S ISSUE:

Bank Credit Freeze Shows Signs of Thawing ................................................................................................................................... 1 Ventas Strikes $3.1 Billion Deal for Atria Senior Living Group .......................................................................................................... 4 Retail Leasing, Absorption Improves Amid Mixed Economic Signals ................................................................................................ 4 General Growth Set To Emerge from Bankruptcy Split in Two.......................................................................................................... 6 SL Green To Recapitalize Three Columbus Circle ............................................................................................................................ 6 Lenders Start Backing Homebuilders Again ...................................................................................................................................... 7 Real Estate Company Financings ..................................................................................................................................................... 8 Disappointing Quarter Leads to More Store Sell Offs / Closures for A&P ......................................................................................... 9 Regulators Close Seven Banks ....................................................................................................................................................... 10 Local Closures & Layoffs ................................................................................................................................................................. 12 Watch List: Multifamily Borrower Bankruptcies ................................................................................................................................ 14

Bank Credit Freeze Shows Signs of Thawing More Banks Increasing Asset Disposition Activity; Turning an Eye to Renewed Lending

Maybe it is time we start taking bankers at their word that commercial real estate wasn't and isn't a catastrophe waiting to happen. Maybe, just maybe, as they've been telling us for the last four consecutive quarters, there are serious risks but they are manageable and are being dealt with and disposed of. Why, now? Because third quarter commercial bank earnings reports released in the last week seem to back up that talk. Individually, there are definitely still banks in trouble. But collectively banks seem to be on the tail end of their commercial real estate troubles. Distressed loan levels have stabilized, the amount of new delinquencies is decreasing and more banks are beginning to push troubled assets back into the marketplace. CRE has been a source of concern for a lot of observers, said James Abbott, senior vice president, investor relations and external communications for Zions Bancorporation, but "so far that is not playing out in our portfolio and has been reasonably benign around the industry. There are lots of indications the commercial real estate market is stabilizing and even strengthening, Abbott said. "If you look at CMBS spreads and some other indicia of this, it's appearing that maybe we're not going to see the kind of storm some had predicted," he said. "But I think it's going to take another two or three quarters perhaps before it's really clear that there aren't substantial losses around the industry in that product type." And, believe it or not, some banks even reported in their quarterly earnings conference calls that they are gearing up for increasing their commercial real estate lending activity or seeing renewed interest in borrowing. Such banks are still the exception, not the norm, but we haven't heard this kind of chatter since 2007. "I would say that we've continued to be very judicious in the commercial real estate area," said Jerry Plush, senior executive vice president, CFO and chief risk officer of Webster Financial Corp. "[We] continue to look for opportunities that make sense for us, and we're continuing to see that there is definitely some build-up in the pipeline there that we could see in the coming quarters," Plush added. "We're not saying that there is going to be substantial growth, It would be either at to maintain balances or slightly above, but soon you will start to see the emergence of those small business and middle-market numbers rising in the commercial category."

MARK HESCHMEYER, EDITOR WWW.COSTAR.COM OCTOBER 28, 2010

THE WATCH LIST NEWSLETTER 2

Rene Jones, chief financial officer of M&T Bank Corp., said his bank is seeing customers paying down debt and repositioning themselves for future expansion. "We’ve seen in the commercial real estate space a number of pretty well healed commercial real estate folks actually just looking at the liquidity and their portfolio, maybe selling down some projects to improve the overall liquidity position," Jones said. "But overall, our commitments aren't up, so I think people are just on hold. The rates are low, they’re trying to lock in some credit today but they’re not necessarily using it because they’re not yet investing." Beth Mooney, vice chairman of KeyCorp, said they are definitely starting to see stability in commercial real estate, particularly the middle market loan book. "We have obviously seen that client base de-lever over the last seven to eight quarters, but if you look into the trends from the first, to the second, to third quarter, we had the lowest level of decline in this quarter that we’ve seen through the cycle and we are actually starting to see, particularly in our Great Lakes and Northeastern regions, signs of increased new business activity and modest glimmers of loan growth," Mooney said. "However, on net you still see pressures in the Western markets. They were late into the cycle, but we do see some pickup in business activity and clearly signs of stability in the middle market book, as well as in the core leasing portfolio, which intersects with a lot of that same client base of renewed activity." Bank executives chatter on their third quarter earnings conference call also highlighted more willingness and success in disposing of troubled assets. "We’re very pleased with the overall results of our problem assets disposition strategy, and the momentum we are building toward this effort," said Clarke Starnes, chief risk officer and senior executive vice president at BB&T Corp. "In the third quarter, we actually assembled a team of about 12 sales specialists, together with some significant operational and marketing support to begin a sales program for about $1.3 billion in commercial nonperforming loans that were transferred to the held for sale category." "Our effort consists of a four pronged strategy. It’s in this priority, it’s short sells to the borrowers; third-party direct; third-0party bulk, and then some option," Starnes added. "We get our best pricing execution when we’re dealing more directly to the borrowers, but it takes a longer time to do that, so at auctions you can do it much quicker, but you’ve got to do your discounts. So what we’re really trying to do is blend these various liquidation alternatives to achieve the best execution that we can, while balancing the time to liquidate." Bob Kaminski, COO, executive vice president at Mercantile Bank Corp., said: "I think our staff has done a good job of working with borrowers on properties that were even in foreclosure to try to affect sales of those properties so that they may be never make it into the ORE bucket. Loans that do make it into foreclosure due to foreclosure process, many times have buyers that are waiting at the end of the redemption period to complete those sale." "So it’s really page by page basis," Kaminski added. "You have some properties that are little bit hard to sell, may be spending little bit of longer time in the ORE buckets and others that are more attractive from a purchasing standpoint tending to spend a lot less time in those categories." Mary Tuuk, chief risk officer, of Fifth Third Bancorp, said they have been very focused on higher risk portfolios such as non-owner occupied real estate. "We’ve worked hard over time to achieve the best solutions possible on troubled credits," Tuuk said. "As part of that process, [the special assets group] continually identifies the loans most likely to result in a successful workout given enough time and which loans are less likely to result in an acceptable outcome. For that latter group of loans, our options include a long-term workout strategy or a shorter-term solution, one of which is the possibility of selling a loan and the redeploying the resources that would be devoted to a longer-term solution." "We are marketing these loans in several pools targeted at particular (buyer basis). Land loans in one pool, vertical CRE in another, syndicated loans in another and a final pool that we intend to sell to investors, loan-by-loan," Tuuk said. "These loans, particularly the nonperforming ones, would generally represent the more troubled parts of our commercial portfolio with a high content of commercial real estate in general, particularly land and construction."

THE WATCH LIST NEWSLETTER 3

Advertisement

THE WATCH LIST NEWSLETTER 4

Ventas Strikes $3.1 Billion Deal for Atria Senior Living Group Ventas Inc. signed a definitive agreement to acquire $3.1 billion of the real estate assets of privately owned Atria Senior Living Group. Chicago-based Ventas will acquire 118 private-pay seniors housing assets in markets including the New York metropolitan area, New England, Boston and California. The portfolio consists of 110 stable assets and eight redevelopment assets, contains approximately 13,500 units, with a median community size of 110 units, a median community age of 12 years and a current average occupancy rate exceeding 87%. The purchase includes essentially all of Atria's real estate assets. The total purchase price is comprised of $1.35 billion in Ventas common stock (a fixed 24.96 million shares), $150 million in cash and the assumption or repayment of $1.6 billion of net debt. The purchase price implies a cost of $230,000 per unit. "The addition of 118 exceptional seniors housing assets in highly desirable locations will increase the portion of our net operating income ("NOI") received from private pay assets to over two-thirds of our total NOI and will establish Ventas as the largest owner of seniors housing communities in the United States," said Debra A. Cafaro, Ventas chairman, president and CEO. "Moreover, given the inherent growth in the portfolio, we expect that this transaction will improve Ventas's growth rate." Ventas expects the portfolio to generate approximately $640 million in revenues in 2011 and NOI (after management fees and operating expenses) to range between $186 million and $196 million. Louisville, KY-based Atria is the fourth largest operator of assisted living properties in the U.S. Atria is owned by private equity funds managed by Lazard Real Estate Partners. Prior to closing, Atria will spin off its management company, Atria Management Co., which will continue to operate the assets under a management contract with Ventas.Ventas expects a 2011 unleveraged NOI yield of approximately 6.5% on the 110 stabilized assets. "The Atria transaction – our sixth major acquisition during the last six years – advances our strategic vision of building an excellent, high performing enterprise comprised of a portfolio of diverse and productive healthcare and senior living assets," Cafaro said.

Retail Leasing, Absorption Improves Amid Mixed Economic Signals By: Randyl Drummer Retail leasing and occupancy continued to improve across the country in the third quarter and should strengthen over the next two to three years as growth in jobs and consumer spending lead to greater sales and profits for retailers and renewed demand for store space in malls and shopping centers. If recovery continues in the broader economy and the amount of new supply delivered remains low, retail vacancy rates should continue to decline through mid-2013. Absorption of retail space, which has been positive for five straight quarters, should continue through at least mid 2012, CoStar Group forecast in its Third Quarter 2010 Retail Review and Outlook this week. The positive indicators in the retail leasing market in the third quarter follow similar recovery stories in the nation’s office and industrial markets. "If you look at where vacancy rates are headed, we’re expecting a pretty bullish recovery," said Real Estate Strategist Suzanne Mulvee, who co-presented the report with Director of Analytics Jay Spivey. "We see the recovery playing out. Not only are consumers spending more, we’re seeing it translate into positive absorption in the space market." Rents are still declining but at a slower rate, but falling vacancies and shrinking supply will gradually lift retail rental rates and sale prices.

THE WATCH LIST NEWSLETTER 5

The national retail vacancy rate edged down slightly from 7.4% at midyear to 7.3% in the third quarter, although the availability rate -- space that's being marketed but is not yet vacant -- is still hovering around its peak of around 10%. While it pales compared with the peak years of the mid-2000s, the 12.9 million square feet absorbed in the 62 largest U.S. retail markets in the third quarter marks the fifth consecutive quarter of positive absorption since the nation recorded 26.7 million in negative absorption in first half of 2009. While 12 of the top 20 retail markets posted negative absorption in 2009, only three recorded net loss of occupancy in the third quarter, including Phoenix (-749,000 square feet), Atlanta (-408,000 SF) and Chicago (-313,000 SF). As usual, energy rich Houston, largely sheltered from the effects of the housing downturn, absorbed the most space at 3.02 million square feet. Supply constrained markets in the northeast and Mid-Atlantic rounded out the top five markets with positive absorption: Long Island, 2 million square feet; Washington, D.C. 1.83 million SF; Boston, 1.78 million SF and Northern New Jersey, 1.76 million SF. Markets in Texas, where the housing crisis did not hurt the economy as deeply, have fared better in retail leasing and occupancy than residential bust markets like California, Florida, Nevada and Arizona. Markets with a retail space overhangs like Phoenix, Denver and Atlanta may take a bit longer to turn the corner into recovery. Year-to-date leasing statistics show that discount retailers like Dollar Tree continue to dominate leasing activity, both in the number of locations and the square footage leased. Service providers like Verizon Wireless are very active in leasing new, albeit smaller, spaces. The number of retail centers with very high vacancies is also declining. According to a CoStar analysis, the number of properties that fell below 80% occupancy, a sign of severe distress, declined in the third quarter compared with fourth-quarter 2009, which marked the market trough. With mom-and-pop retailers still hurting, the number of community shopping centers with occupancies of less than 80% is still increasing somewhat, as is the number of regional malls with high vacancies. However, the number of power, lifestyle and strip centers with sub-80% occupancies has declined since late 2009. Overall retail investment sales remain among the lowest of the major property types as measured by square feet sold as a percentage of total market size. Sales volume is well below historical levels, and the percentage of sales involving distressed properties has risen steadily for five quarters, Spivey said. That said, retail properties didn’t see the dramatic sales spikes -- and steep declines -- experienced in the office and multifamily markets during the 2004-07 boom era and the subsequent recession. There are some positive signs for retail owners. The average number of days that properties are on the market prior to being sold is leveling off at around seven months. Buyers and sellers appear to be coming closer to agreeing on prices. The final sale price as a percentage of asking price in transactions rose higher in the third quarter. Unsold space withdrawn from the market by sellers is also leveling off. Almost 33% of sales volume was comprised of portfolios in the most recent quarter, even higher than the 28.2% at the height of the market in 2007, Spivey said. Buyers are also going for more conservative investments. Triple-net investment sales, a traditional flight to safety for investors, are higher this year and well above long-term averages as a percentage of total sales volume. Several of the top retail sales in the third quarter were portfolios, and most of them involved REITs as a buyer or seller. They include the following.

Simon Properties bought a portfolio of 20 shopping centers in 15 states from Prime Retail on Aug. 30 for $2.3 billion, or $293 per square foot, at an 8% capitalization rate.

Cedar Shopping Centers bought five shopping centers in Pennsylvania and New Jersey from Pennsylvania REIT on Sept. 29 for $135 million, or $110 per square foot, at a 6% cap rate.

LaSalle Investment Management bought San Jose Market Center in San Jose, CA from Cousins Properties on July 8 for $85 million, or $236 per square foot, at an 8.22% cap.

Cole Credit Property Trust bought Whittwood Town Center in Los Angeles from Morgan Stanley on Aug. 27 for $83.5 million, $123 per square foot, at a 6.5 cap rate.

THE WATCH LIST NEWSLETTER 6

Advertisement

General Growth Set To Emerge from Bankruptcy Split in Two Judge Allan Gropper of the U.S. Bankruptcy Court for the Southern District of New York confirmed General Growth Properties Inc.'s plan of reorganization. GGP expects to emerge from Chapter 11 restructuring by Nov. 8. Upon emergence, GGP will have a significantly improved capital structure, having secured $6.8 billion in equity commitments from Brookfield Asset Management, Fairholme Funds, Pershing Square Capital Management, Blackstone and The Teacher Retirement System of Texas. GGP has also successfully and consensually restructured approximately $15 billion in project-level debt, renegotiating terms and extending maturity dates. As part of its plan of reorganization, GGP will split itself into two separate publicly traded corporations upon emergence, and current shareholders will receive common stock in both companies. The new GGP will remain the second-largest shopping mall owner and operator in the country, with more than 185 regional malls in 43 states, and will focus on largely stable Income-producing shopping malls and other real estate assets.

SL Green To Recapitalize Three Columbus Circle SL Green Realty Corp. and The Moinian Group reached an agreement to recapitalize Three Columbus Circle – a midtown Manhattan office tower in the final stages of a major redevelopment. The loan is currently is special servicing after the borrower quit making loan payments last February.

THE WATCH LIST NEWSLETTER 7

The recapitalization includes a standby mortgage commitment and a potential future investment by SL Green that will make funds available for the completion of the redevelopment and lease-up of the property. The current loan on the property was originated at the start of 2006 in the amount of $250 million. It is scheduled to mature in January 2016. The loan is held by Wachovia Bank Comm. Mortgage Trust 2006-C23. The Moinian Group will direct the completion of the $175 million transformation of Three Columbus Circle. The property is a 26-story 768,565-square-foot property at 1775 Broadway that occupies the entire block between Broadway and Eighth Avenue and between 57th and 58th streets. It overlooks Columbus Circle and the southwest entrance to Central Park. The complete modernization, which is near completion, will reposition Three Columbus Circle as a Class A property expected to attract office and retail tenants seeking high-quality space in a prestigious location. FTI Schonbraun McCann acted as advisors for this transaction.

Advertisement

Lenders Start Backing Homebuilders Again Toll Brothers Inc. finalized a new 4-year $885 million bank credit facility. The unsecured facility matures in October 2014 and replaces the company's existing $1.89 billion revolving credit facility, which was scheduled to mature in March 2011. Toll Bros. repaid a $331.7 million term loan that was part of that facility. The new credit

THE WATCH LIST NEWSLETTER 8

facility has an accordion feature under which it can increase to a maximum of $2 billion, subject to certain conditions set forth in the Credit Agreement and the availability of additional bank commitments. "This is the first new unsecured credit facility completed by a publicly traded homebuilding company since the financial crisis of 2008," said Martin P. Connor, the company's CFO. "As such, we believe this transaction is recognition by the banking community of the prudent manner in which we have navigated these difficult economic times, and, more importantly, is a strong vote of confidence in our future." Citigroup Global Markets, Deutsche Bank Securities and RBS Securities acted as joint lead arrangers and joint bookrunners. Other participating lenders included Citibank, Deutsche Bank Securities, The Royal Bank of Scotland, SunTrust Bank, PNC Bank, Capital One, Bank of Montreal, Sumitomo Mitsui Banking Corp., Wells Fargo Bank, Comerica Bank, U.S. Bank and California Bank & Trust.

Real Estate Company Financings CB Richard Ellis Group Inc. is in discussions with its lenders about the potential to refinance $1.5 billion of total debt outstanding as of Sept. 30, 2010 under its existing credit agreement. This debt would be pre-paid or refinanced with $500 million of cash on hand, net proceeds from a $350 million notes offering and up to $650 million of secured term loans under new senior secured credit facilities. In addition, the company is targeting a new $700 million secured revolving credit facility. The company's subsidiary, CB Richard Ellis Services Inc., has entered into an engagement letter with Credit Suisse Securities (USA), Banc of America Securities and HSBC Securities (USA) to arrange such new senior secured credit facilities. U-Store-It Trust closed an amendment to its $450 million credit facility consisting of a $200 million unsecured term loan and a $250 million unsecured revolving credit facility. The amended credit facility has a 3-year term expiring on Dec. 7, 2013. At closing, the $200 million term loan is outstanding and there were no amounts outstanding on the revolver. The amended facility is an unsecured facility compared to the prior secured facility. The amended facility pricing is based on 30-day LIBOR compared to a 1.5% LIBOR floor in the prior facility. First Industrial Realty Trust Inc. amended its senior unsecured revolving credit facility agreement. As part of the agreement, First Industrial made a $100 million paydown and the capacity of the credit facility now totals $400 million, comprised of a $200 million term loan and a $200 million revolving facility. The interest rate on the term loan is LIBOR plus 325 basis points, with no facility fee. The interest rate on the revolving facili ty has been increased from LIBOR plus 100 basis points to LIBOR plus 275 basis points at the Company's current credit ratings, plus a 50 basis point facility fee. The maturity date remains September 2012. Associated Estates Realty Corp. closed on a $250 million senior unsecured revolving credit facility. This facility will replace the company's current $150 million line of credit and the new facility will have a 3-year term, with a 1-year extension option. PNC Capital Markets and Wells Fargo Securities acted as co-lead arrangers of the facility. The other participating banks are US Bank, Raymond James Bank, The Huntington National Bank, Citibank, Compass Bank, and RBS Citizens. Hersha Hospitality Trust signed a commitment letter with TD Bank and TD Securities (USA) for a proposed $225 million senior secured revolving credit facility, which would replace Hersha's current $135 million senior secured credit facility. TD Bank will serve as the sole administrative agent and TD Securities (USA) LLC will serve as lead arranger and book manager. The proposed $225 million senior secured revolving credit facility matures in three years with an extension option for an additional year and may be upsized to $250 million. Borrowings will bear interest at a rate determined by a leverage-based pricing grid. LIBOR loans will bear interest at LIBOR plus an applicable margin of either 350 or 375 basis points per year, subject to a LIBOR floor of 75 basis points per year. Hersha expects that other terms, conditions and covenants of the new credit facility will be generally consistent with the terms of its existing credit facility. The company expects to close on the revolving credit facility during the fourth quarter of 2010. Healthcare Trust of America Inc. entered into a new credit agreement with JPMorgan Chase Bank, as administrative agent, and Wells Fargo Bank and Deutsche Bank Securities, as syndication agents, for an unsecured $200 million revolving credit facility. The agreement will have an initial term of 12 months, with two three-month extension options. The maximum principal amount may be increased by an additional $200 million

THE WATCH LIST NEWSLETTER 9

subject to such additional financing being offered and provided by existing lenders or new lenders under the Credit Agreement. Sunstone Hotel Investors Inc. finalized terms with its lead banks on a new senior corporate credit facility. The initial facility size is expected to be $150 million and will include an option to increase the size of the facility by $100 million subject to lender approval. The lender group is expected to be led by Bank of America Merrill Lynch and J.P. Morgan, and the company expects several of its key relationship banks to commit as co-lenders. The company expects to close the new facility during the fourth quarter. Separately, the company has agreed to preliminary terms for a new non-recourse mortgage on its Hilton Times Square. The new mortgage is expected to have a 10-year term and an interest rate locked at 4.97%. The total principal amount of the new mortgage is expected to be $90 million. The proceeds from the new mortgage will be used in part to repay the existing $81 million mortgage, which bears an interest rate of 5.915% and which matures on Dec. 1. Excess proceeds will be used for general corporate purposes. Chatham Lodging Trust closed an $85 million revolving secured line of credit. The credit facility carries a 3-year term and an interest rate of LIBOR plus a margin based on the company's leverage ratio; at levels less than 30% the margin is 325 basis points, subject to a LIBOR floor of 1.25 %. The line of credit has an accordion feature that provides the company with the ability to increase the facility to $110 million. Participating lenders for the secured line of credit include Barclays Capital, Regions Capital Markets, Credit Agricole Corporate and Investment Bank, UBS Securities and US Bank National Association. Kennedy Wilson's joint venture with The LeFrak Organization has refinanced a portfolio of three multifamily properties with new debt in the amount of $71.2 million at an interest rate of 4.39%. Terms include 10-year fixed-rate financing. The refinanced properties are in California and Oregon. CB Richard Ellis, through its Fannie Mae DUS lending program, served as the lender. Forest City Enterprises Inc. closed a 10-year, $62 million loan for the company's Station Square mixed-use property in Pittsburgh, PA. The CMBS financing carries a 5.85% interest rate and allowed repayment of three separate bank loans totaling $58.6 million. The 652,800-square-foot Station Square is on Pittsburgh's south side along 1.2 miles of the Monongahela River. Tenants include Hard Rock Cafe, the Gateway Clipper Fleet and U.S. Bank.

Disappointing Quarter Leads to More Store Sell Offs / Closures for A&P The Great Atlantic & Pacific Tea Co. (A&P) in Montvale, NJ, reported a second quarter loss from continuing operations of $143 million versus last year's loss of $62 million. Sales for the second quarter were $1.9 billion versus $2.1 billion a year earlier. Comparable store sales decreased 6.6%. "Our second quarter financial results are disappointing. But, we have developed a comprehensive turnaround plan and have quickly begun to implement it," said Sam Martin, president and CEO. The company has identified significant opportunities for reducing its structural and operating costs by working with its key operating partners, rationalizing its store footprint and eliminating overhead costs, Martin said. A portion of the plan includes the sale of properties. For example, the retailer has contracted to sell seven 'non-core" stores in Connecticut. That transaction is scheduled to close Nov. 1. A&P also said it continues to pursue additional financing initiatives including sale-leaseback transactions and sales of additional non-core and/or non-performing assets, as well as reviewing its store portfolio for additional opportunities. The company also recently announced it was closing 25 underperforming stores across five states. These stores include locations in close proximity to other stores, those facing real-estate and cost issues and underperforming non-core stores. The stores should also be closed by Nov. 1. In addition, the company is in discussions with its labor union partners to identify opportunities to reduce its store costs.

THE WATCH LIST NEWSLETTER 10

Finally, A&P has completed the first phase of a talent assessment and taken steps to flatten its organization to lower general and administrative costs, improving the efficiency within its corporate headquarters. The company reduced headcount, saving roughly $10 million annually.

Regulators Close Seven Banks Regulators closed another seven banks in the past week, bringing the total number of failures for 2010 to 136 banks -- just four banks shy of the 140 closed in 2009. Last week's closures could result in losses to the Federal Deposit Insurance Corp. (FDIC) of $478 million. The banks combined had total assets of $2.43 billion.

HILLCREST BANK, OVERLAND PARK, KS

NBH Holdings Corp. in Boston, MA, purchased Hillcrest Bank, a state chartered, commercial bank in Overland Park, KS. Hillcrest Bank was closed by the Kansas Office of the State Bank Commissioner, which appointed the FDIC as receiver. The FDIC sold the bank to NBH. The Hillcrest acquisition will include its nine full-service branches in four states – Kansas, Missouri, Texas and Colorado – and 32 retirement centers where it offers retail banking products and services to the residents of assisted living centers. NBH will operate as Hillcrest Bank until it applies to merge it into its Bank Midwest charter in 2011. "This acquisition is exactly the type of transaction we had in mind when we announced the Bank Midwest acquisition," said Tim Laney, president and CEO of NBH. "Our interest is in banks that expand our footprint in community banking in key markets and give us a strong and stable platform for growth." As of June 30, 2010, Hillcrest Bank had approximately $1.65 billion in total assets. It reported having more than $308 million in distressed commercial real estate-related estates, including $113 million in construction and land development loans in nonaccrual status and another $73 million in foreclosed construction projects. The bank also listed about $17 million in foreclosed multifamily properties. The FDIC and Hillcrest Bank entered into a loss-share transaction on $1.15 billion of Hillcrest Bank's assets. Hillcrest Bank will share in the losses on the asset pools covered under the loss-share agreement. The FDIC estimates that the cost to its Deposit Insurance Fund (DIF) will be $329.7 million.

FIRST ARIZONA SAVINGS, SCOTTSDALE, AZ

The Office of Thrift Supervision (OTS) closed First Arizona Savings of Scottsdale, AZ, and appointed the FDIC as receiver. The FDIC could find no buyer for the institution and approved the payout of the insured deposits. First Arizona, which began operations in 1988 as First Arizona Savings and Loan Association, was critically undercapitalized. First Arizona had 90 employees, assets of $272.2 million. It had a home office and six branches in Arizona. The bank did little commercial real estate lending. The FDIC estimates the cost of the failure to its DIF will be approximately $32.8 million.

FIRST SUBURBAN NATIONAL BANK, MAYWOOD, IL

The Office of the Comptroller of the Currency (OCC) appointed the FDIC as receiver for First Suburban National Bank in Maywood, IL, and First National Bank of Barnesville in Barnesville, GA. The OCC acted after finding that the banks had experienced substantial dissipation of assets and earnings due to unsafe and unsound practices. The OCC also found that the banks incurred losses that depleted its capital, the bank was significantly undercapitalized, and there was no reasonable prospect that the bank will become adequately capitalized without Federal assistance.

THE WATCH LIST NEWSLETTER 11

The FDIC sold First Suburban to Seaway Bank and Trust Co. in Chicago As of June 30, First Suburban National Bank had approximately $148.7 million in total assets. The FDIC and Seaway Bank and Trust entered into a loss-share transaction on $116.6 million of First Suburban's assets. The FDIC estimates that the cost to its DIF will be $31.4 million.

FIRST NATIONAL BANK OF BARNESVILLE, BARNESVILLE, GA

The FDIC sold First National Bank of Barnesville to United Bank in Zebulon, GA. "I have lifelong friendships with many of First National's directors, officers and staff and the past week has been the most emotional and difficult in my 35 year banking career," said Doug Tuttle, United Bank's COO. "First National is an outstanding financial institution with an experienced staff, long-standing customer relationships and a strong community reputation. In the final analysis, we felt that this was the only decision that we could make under these unfortunate circumstances. We will make the transition as easy and seamless as possible." As of June 30, The First National Bank of Barnesville had approximately $135.5 million in total assets. The FDIC and United Bank entered into a loss-share transaction on $107.3 million of The First National Bank of Barnesville's assets. The FDIC estimates that the cost to its DIF will be $33.9 million.

PROGRESS BANK OF FLORIDA, TAMPA, FL

Bay Cities Bank in Tampa, FL, was the successful bidder to acquire Progress Bank of Florida, also in Tampa, under a loss sharing agreement with the FDIC. Progress Bank was closed by the Florida Office of Financial Regulation, which appointed the FDIC as receiver. As of June 30, Progress Bank of Florida had approximately $110.7 million in total assets. The FDIC and Bay Cities Bank entered into a loss-share transaction on $82.6 million of Progress Bank of Florida's assets. The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $25 million.

FIRST BANK OF JACKSONVILLE, JACKSONVILLE, FL

Ameris Bank in Moultrie, GA, acquired First Bank of Jacksonville, a full-service bank with two branches in Jacksonville, FL. The Florida Office of Financial Regulation closed First Bank of Jacksonville and appointed the FDIC as receiver. The FDIC entered into a loss-share transaction and sold the assets and deposit liabilities of First Bank of Jacksonville to Ameris. As of June 30, First Bank of Jacksonville had approximately $81 million in total assets. The FDIC and Ameris Bank entered into a loss-share transaction on $60 million of First Bank of Jacksonville's assets. The FDIC estimates that the cost to its DIF will be $16.2 million.

THE GORDON BANK, GORDON, GA

The Georgia Department of Banking and Finance closed The Gordon Bank in Gordon, GA, and appointed the FDIC as receiver.

THE WATCH LIST NEWSLETTER 12

The FDIC sold the bank to Morris Bank in Dublin, GA. As of June 30, The Gordon Bank had approximately $29.4 million in total assets. Morris Bank will purchase approximately $11.5 million of those assets, consisting of cash and cash equivalents and the FDIC will retain the remaining assets for later disposition. The FDIC estimates that the cost to its DIF will be $9 million.

Advertisement

Local Closures & Layoffs

Company Address Closure or Layoff

Leased or Owned

No. Impacted Impact Date

Life Technologies 542 Flynn Road, Camarillo, CA Closure Leased 28 11/1/2010

Di-Pro Inc. 1550 N. Peach Ave., Fresno, CA Closure Leased 114 11/30/2010

Hines Nurseries 12621 Jeffrey Road, Irvine, CA Layoff Leased 59 11/8/2010

JAL Trans 6041 Imperial Highway, Los Angeles, CA Closure Leased 30 11/30/2010

Freedom Debt Relief 3947 Lennane Drive, Sacramento, CA Layoff Leased 123 11/15/2010

Medimpact Healthcare Systems

10680 Treena St., San Diego, CA Layoff Leased 22 11/14/2010

THE WATCH LIST NEWSLETTER 13

Company Address Closure or Layoff

Leased or Owned

No. Impacted Impact Date

Medimpact Healthcare Systems

10181 Scripps Gateway Court, San Diego, CA Layoff Owned 80 11/14/2010

Medimpact Healthcare Systems

10636 Scripps Summit Court, Suite 210, San Diego, CA Layoff Leased 16 11/14/2010

The Coca-Cola Company 7100 N.E. County Road, Suite 340, High Springs, FL Unknown Owned 87 4/15/2011

Constar, Inc. 901 W. Landstreet Road, Orlando, FL Unknown Leased 121 12/21/2010

M&N Plastics 2706 Turkey Creek Road, Plant City, FL Unknown Owned 85 immediately

Elbit Systems of America 1721 W. Paul Dirac Drive, Tallahassee, FL Unknown Owned 192 3/31/2011

Capital One 8705 Henderson Road, Tampa, FL Unknown Leased 24 12/18/2010

PricewaterhouseCoopers 3109 W. Dr. M.L. King, Jr. Blvd., Tampa, FL Unknown Leased 280 12/31/2010

Windstream Communications 403 W. 4th St., Newton, IA Layoff Owned 146 12/31/2010

MetoKote 2320 Northeast Drive, Waterloo, IA Closure Owned 109 12/22/2010

Principal Financial Group 8909 Purdue Road, Indianapolis, IN Closure Leased 30 12/10/2010

Principal Financial Group 8902 Vincennes Circle, Suite D-2, Indianapolis, IN Closure Leased 30 12/10/2010

Redland Brick 15718 Clear Spring Road, Williamsport, MD Layoff Owned 60 11/22/2010

EcoWater Systems 1890 Woodlane Drive, Woodbury, MN Unknown Leased 76 11/13/2010

Home Services Systems 32-75 Steinway St., Astoria, NY Closure Leased 2,065 12/31/2010

Watson Laboratories 1033 Stoneleigh Ave., Carmel, NY Closure Owned 66 12/31/2010

Interstate Brands Corp. (Wonder) Bakery

168-23 Douglas Ave., Jamaica, NY Closure Owned 222 1/21/2011

MHN Government Services (subsidiary of Health Net)

40 Wall St., 6th Floor, New York, NY Layoff Leased 20 1/10/2011

Bice Ristorante/Da Ecib USA, Inc. 7 E. 54th St., New York, NY Closure Leased 82 1/31/2011

Hypo Real Estate Capital 622 Third Ave., New York, NY

Potential Closure Leased 37 11/1/2010

Rite Aid Distribution Center 5865 Success Drive, Rome, NY Closure Owned 355 1/22/2011

Kmart 5750 Harrison Ave., Cincinnati, OH Closure Leased 102 1/2/2011

Avon Products 175 Progress Place, Springdale, OH Closure Owned 407 12/13/2010

Silver Eagle Manufacturing 5825 NE Skyport Way, Portland, OR Layoff Owned 55 12/15/2010

CDM Long-Term Care Services

11818 SE Mill Plain Blvd., Suite 415, Vancouver, WA Layoff Leased 100 11/1/2010

John Hancock Financial Services

333 W. Everett St., Milwaukee, WI Closure Leased 90 12/17/2010

THE WATCH LIST NEWSLETTER 14

Advertisement

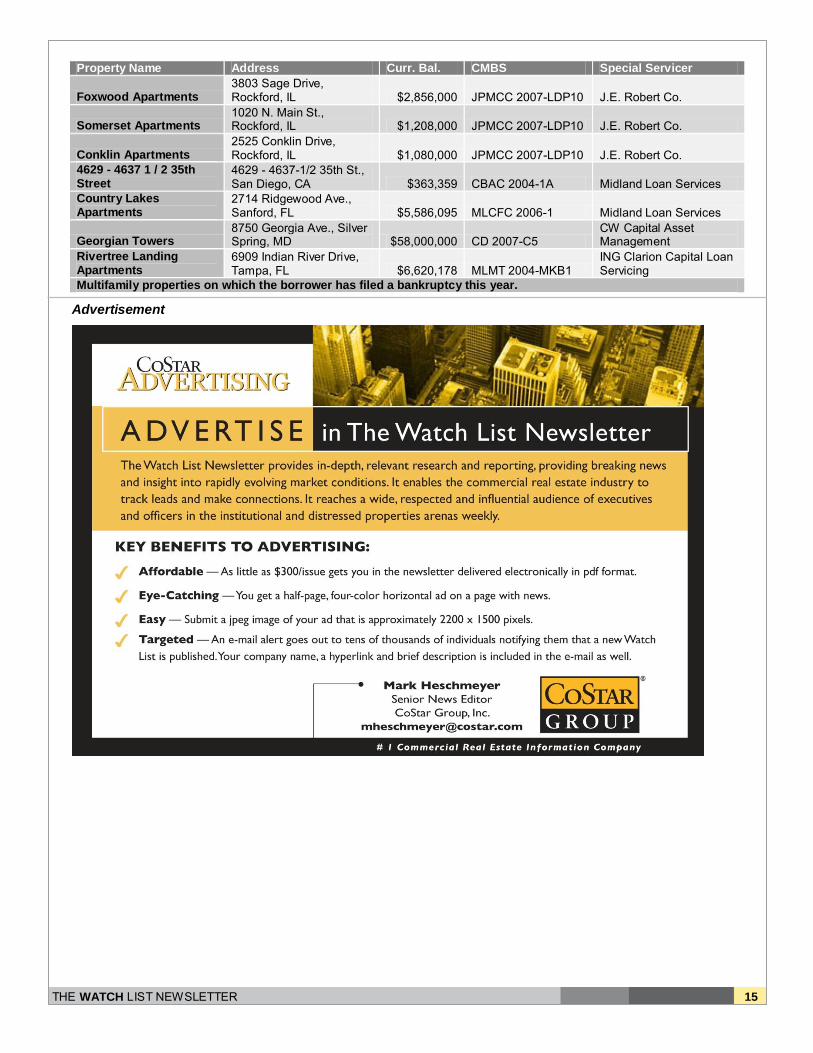

Watch List: Multifamily Borrower Bankruptcies The following information for these lead listings was provided by Investcap Advisors LLC, an industry leader in providing surveillance data on loan and commercial real estate performance underlying the CMBS market.

Property Name Address Curr. Bal. CMBS Special Servicer

Woodchase Condominiums

4060 N. Beltline Road, Irving, TX $1,979,941 DLJCM 1999-CG1 C-III Asset Management

325 South Story Road 325 Story Road, Irving, TX $1,041,778 LASL 2005-MF1

Berkadia Commercial Mortgage

3500 Sanborn Avenue Units A B C D

3500 Sanborn Ave.Units A B C D, Lynwood, CA $397,645 CBAC 2004-1A Midland Loan Services

653 Dix Street 653 Dix St., Manchester, NH $359,292 LASL 2006-MF4 Midland Loan Services

Tiburon Pointe Apartments

16895 Oakmont Drive, Omaha, NE $2,625,796 CSFB 2003-C5

ING Clarion Capital Loan Servicing

Bear Creek Apartments - Phase I

1600 Bear Creek Lane, Petoskey, MI $9,600,000 MLCFC 2007-6

CW Capital Asset Management

Woodbridge Apartments 6635 N. 19th Ave., Phoenix, AZ $8,350,352 CSFB 2005-C4 C-III Asset Management

2302 North 27th Street 2302 N. 27th St., Phoenix, AZ $2,575,518 LASL 2006-MF3 Crown Northcorp

70 Highland Street 70 Highland St., Plymouth, NH $260,582 CBAC 2005-1A Midland Loan Services

472 Cometa Court 472 Cometa Court, Rio Rico, AZ $521,600 CBAC 2004-1A Midland Loan Services

THE WATCH LIST NEWSLETTER 15

Property Name Address Curr. Bal. CMBS Special Servicer

Foxwood Apartments 3803 Sage Drive, Rockford, IL $2,856,000 JPMCC 2007-LDP10 J.E. Robert Co.

Somerset Apartments 1020 N. Main St., Rockford, IL $1,208,000 JPMCC 2007-LDP10 J.E. Robert Co.

Conklin Apartments 2525 Conklin Drive, Rockford, IL $1,080,000 JPMCC 2007-LDP10 J.E. Robert Co.

4629 - 4637 1 / 2 35th Street

4629 - 4637-1/2 35th St., San Diego, CA $363,359 CBAC 2004-1A Midland Loan Services

Country Lakes Apartments

2714 Ridgewood Ave., Sanford, FL $5,586,095 MLCFC 2006-1 Midland Loan Services

Georgian Towers 8750 Georgia Ave., Silver Spring, MD $58,000,000 CD 2007-C5

CW Capital Asset Management

Rivertree Landing Apartments

6909 Indian River Drive, Tampa, FL $6,620,178 MLMT 2004-MKB1

ING Clarion Capital Loan Servicing

Multifamily properties on which the borrower has filed a bankruptcy this year.

Advertisement