bank world conference diebold branch transformation presentation_011813

TRANSCRIPT

Branch Transformation: Strategies to Enhance Profitability and the Customer Experience

Chris Gill Senior Director, Diebold Consulting

Key Trends That Are Impacting Retail Financial Services

Future Role of the Branch and Opportunities to Improve Efficiency and the Customer Experience

Branch Transformation Framework

2

Today’s Discussion

Key Trends Impacting Retail

Financial Services

3

Changing Channel Mix

4

Source: CEB TowerGroup 2011, 2012

0

5

10

15

20

25

30

35

2010 2011 2012E 2013E 2014E 2015E

Tra

nsa

ctio

ns

(B)

Retail Financial Services Transactionsby Channel (2010 – 2015E)

Online Teller ATM Mobile

Evolution of the “Experience Economy”

5

Customer expectations are evolving rapidly and being shaped by innovation in other industries

Smartphones and tablets increasingly used to interact with retailers

Use of physical retail outlets to reinforce brand and capture member attention

Use of data analytics to improve the customer experience through preference identification

ONLINE SHOPPING

TRAVEL SERVICES

RETAIL

Increasing Consumer Power

6

ONLINE CONSUMER

RATINGS

NON-TRADITIONAL

COMPETITORS

ELECTRONIC

PAYMENTS

MOBILE BANKING SOCIAL MEDIA RAPID INFORMATION

DISSEMINATION

Social media amplifies the voice of the consumer in significant ways

The leading players in mobile payments are not Fis

Merchants are influencing consumer purchase method selection

Older consumers are rapidly adopting online, mobile and social media

Rise of Gen Y and the Millennials

7

• Will make up 75 percent of the global workforce in 2025

• Expected Gen Y & Millennials inheritance is $17.8 trillion

• $300 Billion in annual spending power

• Will conduct 40 percent of total transactions in five years

• Will have the greatest spending power of all generations by 2017

8%

15%

29%

33%

Use Mobile

Remote Deposit

Deposit a Check

at an ATM

Try New

PaymentMethods

Use Mobile

Banking

As compared to the Boomer generation, Millennials are _% More Likely to…

The “New Normal” in Retail Financial Services

8

Source: Morgan Stanley, SNL Financial, 2012

55% 55% 53%

56% 58%

60% 61%

$0

$100

$200

$300

$400

$500

$600

$700

2005 2006 2007 2008 2009 2010 2011

Retail Financial Services Revenue and Efficiency Ratio Performance (2005-2011)

Revenue ($B) Industry Average Efficiency Ratio

Significant decline in non-interest revenue due to regulatory constraints

Higher operating costs due to increasing labor costs and greater compliance requirements

Typically, branches account for 50% of a retail banking institution’s operating cost and personnel accounts for 54%

Future Role of the Branch

9

10

Branches Remain a Key Delivery Channel

Source: Forrester/Diebold research, Fall 2011

2% 3%

27%

6%

20% 23%

14%

67%

73%

67%

53%

21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Makea deposit

Open adeposit account

Apply for a loan Resolvea problem

Call center Web/Online banking Branch ATM

Consumer Channel Preference for Select Interactions

11

Branches Important in FI Selection

23.8%

44.5%

55.1%

55.6%

56.9%

63.5%

70.1%

83.9%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Mobile banking offering

Local ownership/decision making

ATM locations

Products offered

Branch locations

Web banking offering

Brand reputation

Attractive rates and fees

Importance in choosing a Financial Institution (Important or Very Important)

Source: Forrester/Diebold research, Fall 2011

12

Branches Need to Change

• One-size-fits-all branch designs

• Little in-branch technology enabling self-service

• Rigid staff roles based on transactions, service and sales

Today

• Multiple formats based on demographics and volume

• More self-service and assisted-service options

• Universal staffing models to increase efficiency and effectiveness

Tomorrow

13

Branch Role in a Multi-channel Strategy F

RE

QU

EN

CY

OF

IN

TE

RA

CT

ION

RICHNESS OF EXPERIENCE

THE NEW ROLE OF THE BRANCH

• Financial planning and advising

• One-to-one marketing and sales

• Customer service and issue resolution

• Complex transaction handling

• Local community branch presence

14

Multiple Branch Formats

FLAGSHIP SPOKE HUB IN-STORE/MICRO

• 4,000-5,000 square feet

• High visibility/traffic location

• Full service with full range of product specialists on site

• Showcase for technology

• 2,500-3,500 square feet

• Full service with some product specialists on site

• Located in a high traffic area

• 1,000-1,500 square feet

• Limited service

• Greater use of self-service automation

• Supports hub branches in market

• 300-500 square feet

• Limited service

• Highly automated

• Specialty/high volume locations (e.g. hospitals, supermarkets, malls, urban locations)

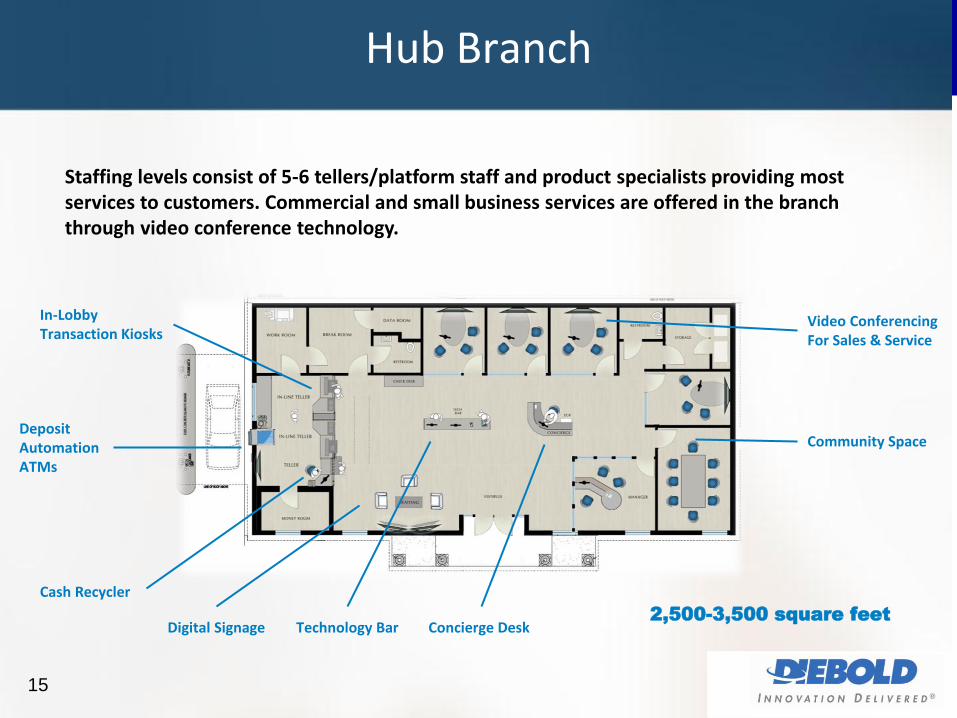

15

Hub Branch

In-Lobby Transaction Kiosks

Cash Recycler

Deposit Automation ATMs

Concierge Desk Technology Bar Digital Signage

Community Space

Video Conferencing For Sales & Service

Staffing levels consist of 5-6 tellers/platform staff and product specialists providing most services to customers. Commercial and small business services are offered in the branch through video conference technology.

2,500-3,500 square feet

16

Spoke Branch

Staffing levels at 4-5 tellers/platform staff. Investment, mortgage and small business product specialists available via video conferencing. High emphasis on technology and self-service training and education.

In-Lobby

Transaction Kiosks

Cash Recyclers

Deposit

Automation

ATMs

Technology Bar

Digital Signage

Video Conferencing For Sales &

Service

1,000-1,500 square feet

17

A New Branch Approach

Management Guidelines and Objectives – Branch Expansion

• Branch associates need to spend more time interacting with members and less time conducting transactions

• Leverage self-service technology for transactions

• Engage new members and get them to use their accounts more quickly

• New branches as part of a hub and spoke footprint – existing UFCU branches located with 3-5 miles of new branch locations

• New branches cannot meet every single customer need

Limited number of transaction types cannot be conducted at the branch and would require a trip to a traditional branch

UNIVERSITY FEDERAL CREDIT UNION (AUSTIN, TX)

18

Increased Focus on Customer Relationships

• Move from transactional to relationship activity

• Change staffing model – use of universal associates (Personal Financial Representatives) – 4 PFRs per branch along with a manager

• Reduce staff turnover and training expenses creating structure for a more defined career path

• Train consumers in self-service usage

• Greatly increase amount of time associates interact with customers rather than conducting transactions

• Seasoned PFRs to assist consumers with life events

• Structure allows an opportunity to explain this service model

NEW BRANCH MODEL

19

Implementing an ‘Assisted Service’ Model

WHAT DOES IT DO?

• Delivering a self-service or partially assisted service capability directly at the teller line, next to a teller pod, or as a stand-alone unit within the lobby.

WHAT VALUE DOES IT PROVIDE?

• Terminal to migrate additional transactions not currently addressed by the ATM

• Facilitate consumer education through partially assisted transactions in the branch, resulting in increased adoption

• Express lane alternative for consumers wanting quicker service

• Increased approachability due to location and proximity of staff

IN-LINE TRANSACTION KIOSK

20

Issues to Address Dimension

Operations

Defining the target customer experience

Changing policies and procedures Integrating with existing systems

Employee Preparation

Communications Training

Execution is Critical

Customer Adoption

Measurement / Tracking

Education / Communications Incentives

Customer behavior Return on investment

Branch Transformation Framework

21

22

Drive Efficiencies

Improve Customer

Experience

Mitigate Risks

Improve Sales

Effectiveness

For most, the primary objective. Consider re-thinking your processes and opportunities to automate

Rethink how you address fraud, electronic security and physical intrusion. Minimize internal theft or errors without burdensome processes

Should be considered from the start when contemplating branch design, process improvement, and self-service automation

Capitalize on efficiency savings by re-purposing branch staff to sell more effectively. Deliver the tools and support needed

Branch Transformation Objectives May Vary

23

Adopt a Comprehensive Branch Transformation Approach

• What is the role of each delivery channel in our retail banking strategy?

• What is the optimal number of branches and ATMs we need to serve our markets?

• What is the target consumer experience in each channel?

• How can we operate our branches more efficiently in order to reduce costs while providing a high-quality consumer experience?

• How profitable are our branches and ATMs?

• How can we better mitigate operational risks?

• Which branch transformation solutions are going to have the greatest impact on our business?

• How do we prioritize various channel investments over the next three years?

• What is the most appropriate branch layout given our retail strategy?

• How do we ensure we maximize the value of investments in branch transformation solutions?

• How do we ensure consumers adopt new solutions?

• How do we engage employees to support new solutions?

• Did we achieve the ROI associated with the investments required?

• What impact did the new solutions have on transaction migration and consumer experience?

• What steps need to be taken to improve performance if expectations are not being met?

24

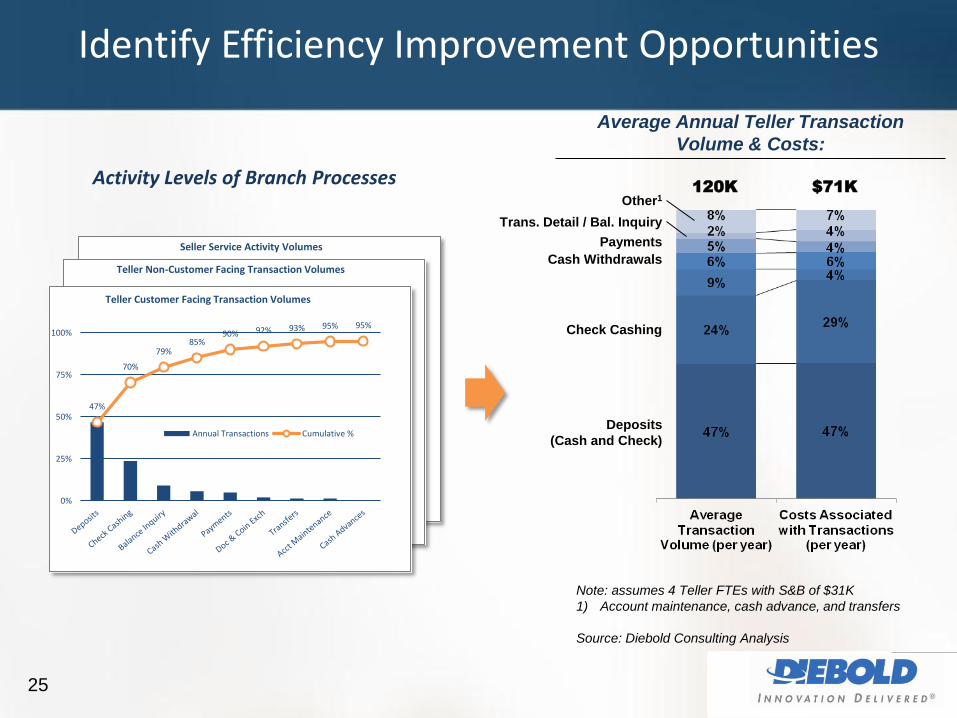

Assess Branch Activities

25

Identify Efficiency Improvement Opportunities

47%

70%

79% 85%

90% 92% 93% 95% 95%

0%

25%

50%

75%

100%

Seller Service Activity Volumes

Annual Transactions Cumulative %47%

70%

79% 85%

90% 92% 93% 95% 95%

0%

25%

50%

75%

100%

Teller Non-Customer Facing Transaction Volumes

Annual Transactions Cumulative %47%

70%

79% 85%

90% 92% 93% 95% 95%

0%

25%

50%

75%

100%

Teller Customer Facing Transaction Volumes

Annual Transactions Cumulative %

Activity Levels of Branch Processes

Average Annual Teller Transaction

Volume & Costs:

Note: assumes 4 Teller FTEs with S&B of $31K

1) Account maintenance, cash advance, and transfers

Source: Diebold Consulting Analysis

Other1

Trans. Detail / Bal. Inquiry

Payments

Cash Withdrawals

Check Cashing

Deposits

(Cash and Check)

120K $71K

26

Opportunities to Consider

• Network optimization planning

• Branch efficiency assessment and customer experience diagnostic

• ‘Test and learn’ for branch automation solutions

• Branch transformation roadmap development

• Implementation planning for new branch technology

28

Diebold Consulting

• Distribution network optimization, including planning for de novo branches

• ATM network optimization

• Market / site analysis

• Channel profiling

• Branch operational assessments

• Branch / ATM physical security risk assessment

• Branch / ATM physical security standards and procedures

• Fraud risk assessments

• Deployment strategy and business case development

• Deployment strategy and business case development for specific branch transformation solutions

• Branch design services and customer experience planning

• In branch self service solutions ‘test and learn’

• Deposit automation implementation

• Teller automation implementation

• Implementation of new branch formats

• Performance measurement and evaluation