barclays ceo energy-power conference · barclays ceo energy-power conference premier operator of...

TRANSCRIPT

1

Barclays CEO Energy-Power Conference

PREMIER OPERATOR OF TOP TIER ASSETS

SEPTEMBER 6, 2017

Please Read This presentation makes reference to:

Forward-looking statements

This presentation contains forward-looking statements within the meaning of securities laws. The words “anticipate,” “assume,” “believe,”

“budget,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “plan,” “project,” “will” and similar expressions are intended to identify forward-

looking statements. These statements involve known and unknown risks, which may cause SM Energy's actual results to differ materially from

results expressed or implied by the forward-looking statements. Forward-looking statements in this presentation include, among other things,

2017 guidance, expectations regarding growth strategy, anticipated drilling plans and capital expenditures, and anticipated growth in cash flows.

General risk factors include the uncertain nature of acquisition, divestiture, joint venture, farm down or similar efforts and the ability to complete

any such transactions; the uncertain nature of expected benefits from the actual or expected acquisition, divestiture, joint venture, farm down or

similar efforts; the uncertainty of negotiations to result in an agreement or a completed transaction; the availability of and access to capital

markets; the availability, proximity and capacity of gathering, processing and transportation facilities; the volatility and level of oil, natural gas,

and natural gas liquids prices, including any impact on the Company’s asset carrying values or reserves arising from price declines;

uncertainties inherent in projecting future rates of production or other results from drilling and completion activities; the imprecise nature of

estimating oil and gas reserves; uncertainties inherent in projecting future drilling and completion activities, costs or results, including from pilot

tests; the availability of additional economically attractive exploration, development, and acquisition opportunities for future growth and any

necessary financings; unexpected drilling conditions and results; unsuccessful exploration and development drilling results; the availability of

drilling, completion, and operating equipment and services; the risks associated with the Company's commodity price risk management

strategy; uncertainty regarding the ultimate impact of potentially dilutive securities; and other such matters discussed in the “Risk Factors”

section of SM Energy's 2016 Annual Report on Form 10-K, as such risk factors may be updated from time to time in the Company's other

periodic reports filed with the Securities and Exchange Commission. In addition, production forecasts and expectations for future periods are

dependent upon many assumptions, including estimates of production decline rates from existing wells and the undertaking and outcome of

future drilling activity, which may be affected by significant commodity price declines or drilling cost increases. The forward-looking statements

contained herein speak as of the date of this announcement. Although SM Energy may from time to time voluntarily update its prior forward-

looking statements, it disclaims any commitment to do so except as required by securities laws.

2

Non-GAAP financial measures: See appendix for reconciliations

3

SM Energy Focused 3-Year Plan

3

Top tier oil in Midland Basin + top tier NGLs and gas in Eagle Ford

Midland Basin> ~89,000 net acres

> 7 Rigs / 3 Frac Crews

Eagle Ford> ~167,500 net acres

> 1 Rig / 1 Frac Crew

4

SM Energy Premier Operator of Top Tier Assets

Value

proposition

Drilling

catalysts

Capital efficiency driving value

►Well results and production continue

to exceed expectations

►Permian and Eagle Ford results

demonstrate top tier asset quality

►Continue to add inventory in

Permian and Eagle Ford while

working to enhance value in other

areas

First Half of 2017 Financial Highlights

5

Outstanding execution – 2017 plan on track or better

EBITDAX ahead of plan despite notably lower

commodity prices

CAPEX less than plan despite more lateral feet

completed

The balance sheet remains in good shape: $560 MM

cash and total liquidity of $1.5 B(1)

(1) As of June 30, 2017.

41

42

43

44

45

46

Original Guidance(includes Divide

County for full year)

1Q17 Revision(predominantly

outperformance)

2Q17 Eagle FordAcceleration

2Q17Outperformance

Pro

du

cti

on

(M

MB

oe)

► Raising full year production guidance by 0.8 MMBoe (midpoint)

► Pace of Permian completions expected to approximately double in second

half, significantly increasing oil mix in 2H17

► Raising 3Q17 production guidance from 10.8 to 11.2 MMBoe (29-30% oil)

2017 Guidance(1) Significant Permian Growth in Second Half

6

Note: Midpoint of production guidance shown.

6%

increase

Facilities

6%

Operated Eagle

Ford

20%

(1)

Capital & Production FY 2017

Total Capital Spend ($MM)(2) (before acquisitions) ~$875

Total Production (MMBoe)

– oil percent in commodity mix

approaches 30% average44.5 – 46.5

Costs

LOE, including Ad Valorem ($/Boe) $4.30 - 4.60

Transportation ($/Boe) $5.40 - 5.65

Production taxes (% of pre-hedge revenue) 4.0 – 4.5%

G&A ($MM) – incl. $20 MM non-cash compensation

$115 – 125

Capitalized Overhead/Exploration ($MM)– before dry hole expense, all of which is

included in capital expenditure guidance

$65 - 70

DD&A ($/Boe) $12.00 - $14.00

(1) As of August 3, 2017.

(2) Total Capital Spend is a non-GAAP financial measure. Please see the reconciliation of this measure in the Appendix.

2017 Production Guidance

Well Hedged Through 2018

7

►~70% of expected 2H17 production volumes hedged(1)

►~50% of expected 2018 volumes hedged(2)

►Credit Agreement allows hedging of up to 85% of projected production for the first

three years

Note: The hedged volumes on this slide do not include any volumes related to basis swaps.

(1) At mid-point of revised guidance.

(2) Based on February 2017 3-year plan revised to include Divide County production.

60% 75% 80%

Oil 2H17

Natural Gas 2H17

NGLs2H17

Balance Sheet Financial Position

8

Liquidity of $1.5 billion, including $560MM cash on hand(1)

Other

86% 8%

Drilling and

Completion

86%

Facilities

6%

Other

8%

(1)

$500$500$500$395

$562

$345

$172.5

$0

$250

$500

$750

$1,000

2026202520242023202220212020201920182017

Debt Maturities(1)

(in millions)

~$0 drawn

Commitments and Borrowing base: $925 million

Corporate ratings: S&P BB-, Moody’s B1

(1) As of June 30, 2017

Balance Sheet offers financial flexibility(1)

> Senior Secured Debt:TTM Adjusted EBITDAX at ~0.0 times; max ratio allowed 2.75 times

> TTM Adjusted EBITDAX:Interest at ~3.9 times; minimum ratio required 2.0 times

9

Premier Operator of

Top-Tier Assets

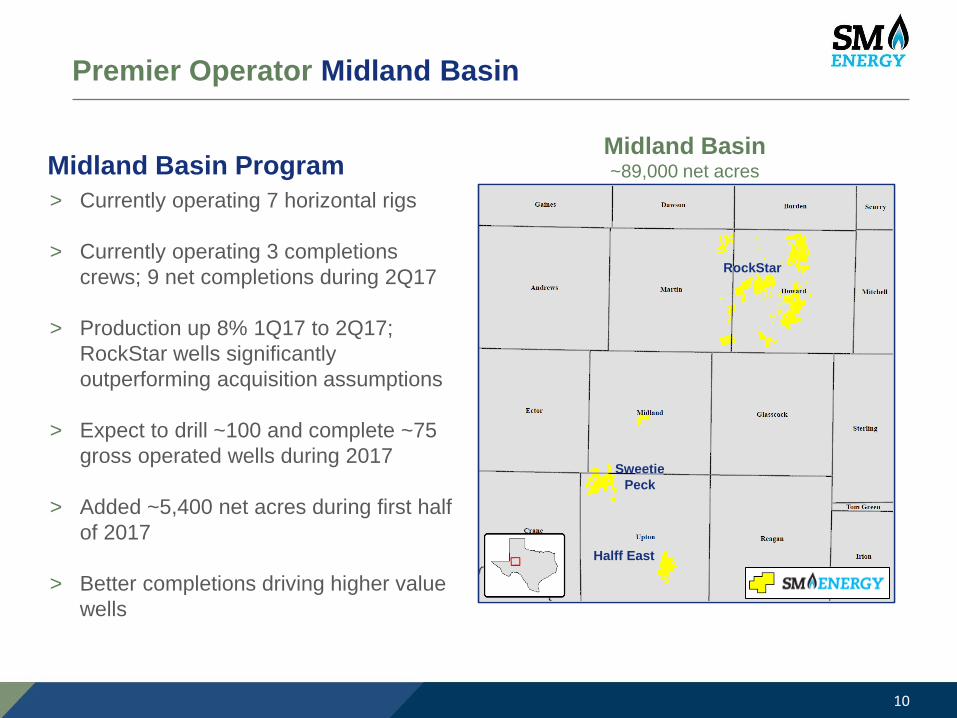

Premier Operator Midland Basin

10

Sweetie

Peck

RockStar

Halff East

> Currently operating 7 horizontal rigs

> Currently operating 3 completions

crews; 9 net completions during 2Q17

> Production up 8% 1Q17 to 2Q17;

RockStar wells significantly

outperforming acquisition assumptions

> Expect to drill ~100 and complete ~75

gross operated wells during 2017

> Added ~5,400 net acres during first half

of 2017

> Better completions driving higher value

wells

Midland Basin ProgramMidland Basin~89,000 net acres

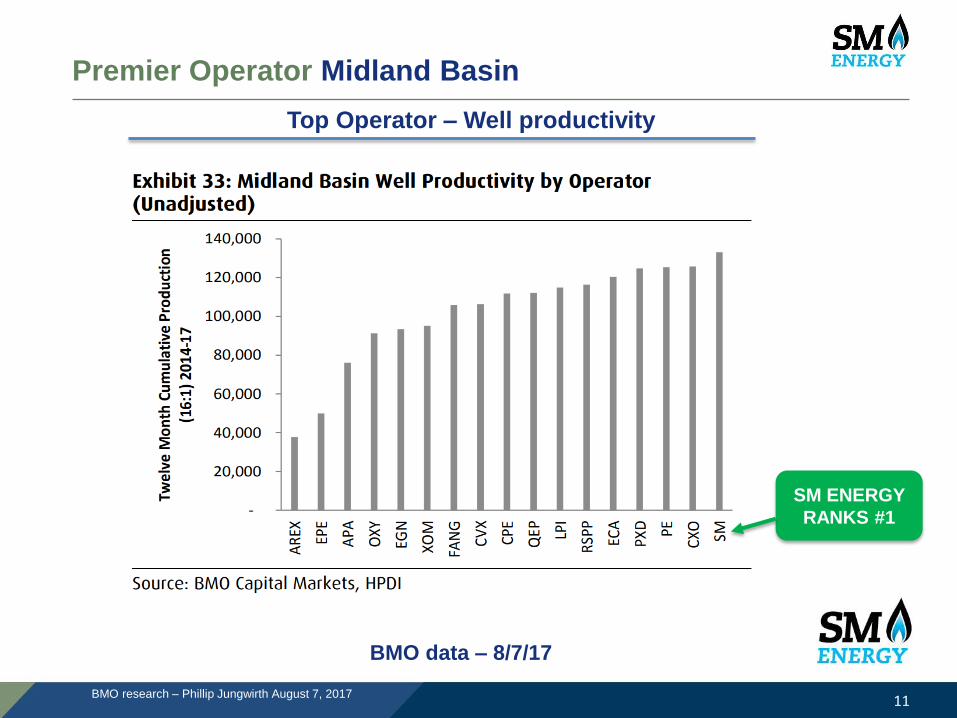

Premier Operator Midland Basin

11BMO research – Phillip Jungwirth August 7, 2017

BMO data – 8/7/17

Top Operator – Well productivity

SM ENERGY

RANKS #1

12

Outstanding Well Results

“Based on our in-depth analysis of historic well data – we see Howard County

as one of the most valuable parts of the Midland Basin given higher oil cuts that

decline slower than other areas”-Credit Suisse(1)

(1) Source: Credit Suisse Equity Research, Nitin Kumar, CFA, June 1, 2017; “Relaunching US E&P Coverage: Sticking with Asset Quality and Balance Sheet”

(2) Source: FBR, Joseph Allman, CFA, June 9, 2017; “Midland Basin: Operator Productivity and Location Analysis – June 2017”

“SM Energy best based on operator revenue ranking…SM ranks no 1 generating

54% more revenue on an absolute basis than the median peer operator”

-FBR(2)

“SM Energy best on revenues per lateral foot…SM is the top operator for the

most recent year’s worth of wells with at least three full months of production

data, with revenues per lateral foot 65% better than the median Midland

Operator.”

-FBR(2)

Premier Operator Midland Basin

13

Applying seismic, core, and geo-chem data to optimize development

Modern 3-D

Seismic Grid

Planned 3-D

Seismic

Acquisition

Premier Operator Midland Basin

14BMO research – Phillip Jungwirth August 7, 2017

BMO data – 8/7/17

Top assets – Howard County

Highest oil content, flattest curve

HOWARD

COUNTY

RANKS #1

Howard County New Well Results – Additional Details

15

Well Name IntervalLateral

Length

Peak IP

Rate

(BOE/d)

IP DaysIP per

1,000’

24 Hour

Peak IP

Rate

Stages

Clusters

per

Stage

Proppant

(lbs./ft)

Oil

%

Tackleberry 43-42 A 1LS LS 7,873’ 1,286 30-day 163 1,426 50 5 1,912 89

Tackleberry 43-42 A 1WA WCA 7,861’ 2,262 30-day 288 2,639 49 5 1,883 90

Tackleberry 43-42 A 2WB WCB 7,885’ 1,412 30-day 179 1,655 50 5 1,728 86

Rambo 3846WA(4) WCA 7,546’ 1,130 30-day 150 1,253 48 5 1,946 89

Rambo 3848WA(5) WCA 7,590’ 1,118 30-day 147 1,228 48 5 1,935 88

Venkman 26-35 B 1WA WCA 7,700’ 1,274 30-day 165 1,529 49 5 1,935 91

Top Gun 1632LS(6) LS 7,711’ 1,270 30-day 165 1,308 44 6 2,018 88

Top Gun 1652WA(7) WCA 7,595’ 1,655 30-day 218 1,839 43 9 2,380 90

Guitar North 2722LS(1) LS 9,692’ 1,497 30-day 154 1,516 59 8 1,958 87

Guitar North 2742WA(2) WCA 9,698’ 1,949 30-day 201 2,542 59 8 1,997 90

Guitar North 2762WB(3) WCB 9,693’ 1,639 30-day 169 1,981 59 8 1,994 87

Papagiorgio 33-40 B 1WA WCA 10,369 1,275 30-day 123 1,606 62 8 1,866 92

Zissou 32-41 A 15WA WCA 10,315 1,351 30-day 131 1,736 62 8 1,861 92

Viper 14-09 1WA WCA 10,422 1,266 30-day 121 1,316 84 8 1,960 91

Average 1,456 89

(1) Name changed from Corinne Elizabeth 26-27 A 1H (4) Name changed from Rambo 38-47 7WA (7) Name changed from Top Gun 1H

(2) Name changed from Corinne Elizabeth 26-27 A 2H (5) Name changed from Rambo 38-47 9WA

(3) Name changed from Corinne Elizabeth 26-27 A 3H (6) Name changed from Top Gun 2H

Outstanding Results Howard County

16(1) Iceman 6-well pad includes three Wolfcamp A wells and three Lower Spraberry wells.

Howard CountyMartin County

Guitar North 2742WA

IP30: 1,949 BOE/d (90% oil)

Interval: Wolfcamp A

Lateral Length: 9,698’

Guitar North 2722LS

IP30: 1,497 BOE/d (87%oil)

Interval: Lower Spraberry

Lateral Length: 9,692’

Guitar North 2762WB

IP30: 1,639 BOE/d (87% oil)

Interval: Wolfcamp B

Lateral Length: 9,693’

Viper 14-09 1WA

24hr IP: 1,316 BOE/d (91% oil)

IP30: 1,266 BOE/d (91% oil)

Interval: Wolfcamp A

Lateral Length: 10,422’

Great results in multiple intervals across acreage position

Zissou 32-41 A 15WA

IP30: 1,351 BOE/d (92% oil)

Interval: Wolfcamp A

Lateral Length: 10,315’

Papagiorgio 33-40 B 1WA

IP30: 1,275 BOE/d (92% oil)

Interval: Wolfcamp A

Lateral Length: 10,369’

Thumper 14-23

(Sabalo)

Mr. Phillips 11-2 #1SH

(Sabalo)

Peer wells

SM wells flowing back

Iceman 6-well pad(1)

Griswold 3-well pad

Papagiorgio 33-40 B 1LS

Tubb A 1HA

(CrownQuest)

Eastland 15 2WH

(Apache)

17

Outstanding Results Viper 14-9 WA

Viper results to date exceeding expectations

10

100

1,000

10,000

0 50 100 150 200

Pro

du

cti

on

Ra

te (

BO

EP

D)

Days on Production

Viper 14-09 1WA

Western Howard County

Well Average

Premier Operator Eagle Ford

18

> Currently operating 1 horizontal rig

and plan to add a second rig in

August

> Currently operating 1 completions

crew

> Production up 9.5% 1Q17 to 2Q17

(retained properties)

> 14 wells completed during 2Q17

> Expect to drill approximately 30

gross wells and complete 39 gross

wells during 2017

Eagle Ford ProgramEagle Ford Operated

~167,500 net acres

South

Area

East

Area

North

Area

19

Premier Operator Eagle Ford

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

-

50

100

150

200

250

300

350

400

450

500

2012 2013 2014 2015 2016 2017

Av

era

ge L

ate

ral

Len

gth

(ft

)

Dri

llin

g C

ost

Per

Fo

ot

($/f

t)

-

500

1,000

1,500

2,000

2,500

-

100

200

300

400

500

600

700

800

900

1,000

2012 2013 2014 2015 2016 2017

Pro

pp

an

t P

er

Late

ral

Fo

ot

(lb

/ft)

Co

mp

leti

on

Co

st

Per

Fo

ot

($/f

t)

► Drilling longer laterals at faster pace, while achieving lower costs

> Drilling Cost per foot improved ~30% since 2015

► Pumping more sand and fluid into more stages while managing costs

> Improving frac designs leads to better wells

Drilling Costs Completion Costs

Capital efficiency - better wells and lower costs

0

5

10

15

20

25

30

0 30 60 90 120 150 180 210

No

rma

lize

d G

ross C

um

ula

tive

Pro

du

ction

(B

OE

/ft)

Days on Production

Outstanding Results Eagle Ford North

20

Outperformance: new generation completion includes tighter stage and cluster

spacing with increased fluid per foot

6 Wells (A)

Operated Eagle Ford – Recent Well Results

2Q17 North Area co-development (B)

1Q17 North Area co-development (A)

South

Area

North

Area

East

Area

3 Wells (B)

1Q17

Completions

2Q17

Completions

North Type Curve

BOE/FT

Note: 2-stream data; does not reflect ~95-140

Bbls/MMcf NGL yield for type curve shown.

Initial flowback data omitted.

Co-development UEF/LEF

2Q17 Completions

PRB Creating Value Through Successful JV Tests

21

> Utilizing partner services

and capital in current

development activity(1)

> ~156,000 total net acres

(~114,000 contiguous net

acres)

> Positive early well results

> Frontier and Shannon

intervals being tested

> Evaluating Niobrara test for

early 2018 – sizeable

inventory potential

Well

NameLL Reservoir

IP Rate

(Boe/d)

IP

DaysOil

%

Cannon 9,462’ Frontier 1,449 30 83

Buttermilk 9,199’ Frontier 2,237 30 80

Biscuit 9,639’ Frontier 2,387 30 80

Gneiss 9,669’ Shannon 1,657 30 93

Sussex

~10,100’ TVD

Shannon

~10,750’ TVD

Niobrara

~12,000’ TVD

Frontier

~12,500’ TVD

Mowry

~13,500’ TVD

~4,0

00’

Tight sand reservoirs

Source rock reservoirs

New completion technology driving 40% improvement in wells

(1) Third party carry to test multiple intervals and newer completion technologies. Initially, SM will realize nominal production and cash flow from these tests.

Powder River Basin

22

SM Energy Why Invest in SM

Value

proposition

Drilling

catalysts

Premier operator of top tier assets

Drilling

catalysts

Doubling cash flow

over two years

Liquidity –

cash on hand;

zero bank debt

Hedging

provides

stability

RockStar wells

outperforming

Rapid,

high-margin

growth

23

Appendix

2nd Quarter and YTD 2017 Performance Solid Execution

24

Production 2Q17 2017 YTD

Total Production (MMBoe) 11.3 23.4

Average Daily Production (MBoe/d) 124.6 129.5

Pre-Hedge Realized Price ($/Boe) $25.13 $26.38

Post-Hedge Realized Price ($/Boe) $26.57 $27.08

Costs

LOE ($/Boe) $4.11 $3.96

Ad Valorem ($/Boe) $0.16 $0.36

LOE including Ad Valorem ($/Boe) $4.27 $4.32

Transportation ($/Boe) $5.71 $5.79

Production Taxes (% of pre-derivative oil, gas & NGL

revenue)

4.0% 4.1%

Total Cash Production Expenses ($/Boe) $10.98 $11.20

Production Margin (pre-hedge) ($/Boe) $14.15 $15.18

G&A – Cash ($/Boe) $2.21 $2.15

G&A – Non Cash ($/Boe) $0.30 $0.31

Total G&A ($/Boe) $2.51 $2.46

DD&A ($/Boe) $13.52 $12.42

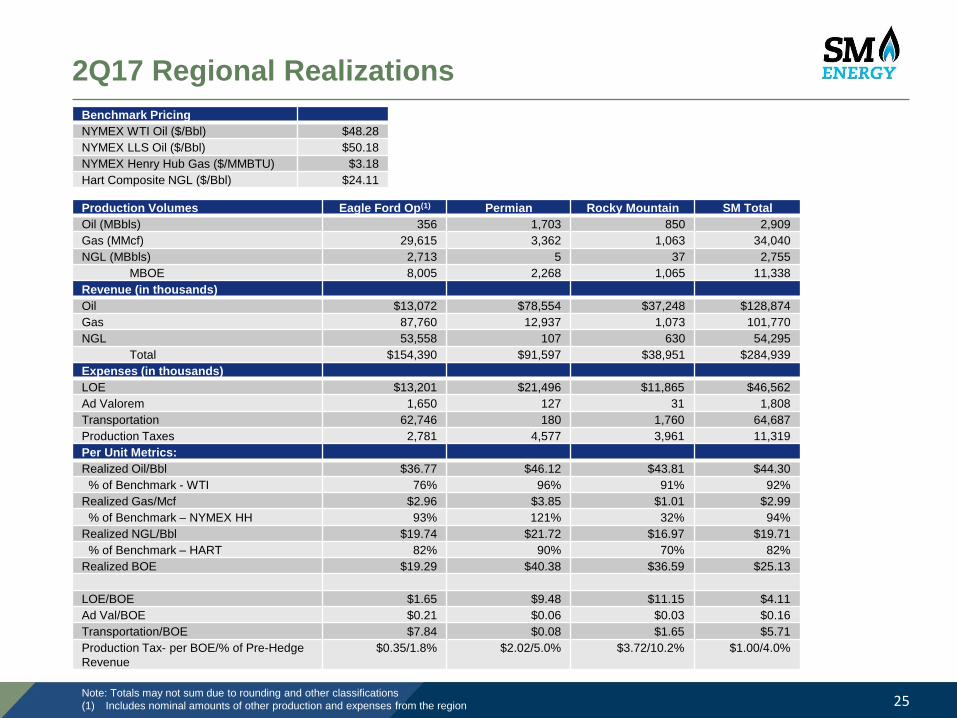

2Q17 Regional Realizations

25

Benchmark Pricing

NYMEX WTI Oil ($/Bbl) $48.28

NYMEX LLS Oil ($/Bbl) $50.18

NYMEX Henry Hub Gas ($/MMBTU) $3.18

Hart Composite NGL ($/Bbl) $24.11

Production Volumes Eagle Ford Op(1) Permian Rocky Mountain SM Total

Oil (MBbls) 356 1,703 850 2,909

Gas (MMcf) 29,615 3,362 1,063 34,040

NGL (MBbls) 2,713 5 37 2,755

MBOE 8,005 2,268 1,065 11,338

Expenses (in thousands)

LOE $13,201 $21,496 $11,865 $46,562

Ad Valorem 1,650 127 31 1,808

Transportation 62,746 180 1,760 64,687

Production Taxes 2,781 4,577 3,961 11,319

Revenue (in thousands)

Oil $13,072 $78,554 $37,248 $128,874

Gas 87,760 12,937 1,073 101,770

NGL 53,558 107 630 54,295

Total $154,390 $91,597 $38,951 $284,939

Note: Totals may not sum due to rounding and other classifications

(1) Includes nominal amounts of other production and expenses from the region

Per Unit Metrics:

Realized Oil/Bbl $36.77 $46.12 $43.81 $44.30

% of Benchmark - WTI 76% 96% 91% 92%

Realized Gas/Mcf $2.96 $3.85 $1.01 $2.99

% of Benchmark – NYMEX HH 93% 121% 32% 94%

Realized NGL/Bbl $19.74 $21.72 $16.97 $19.71

% of Benchmark – HART 82% 90% 70% 82%

Realized BOE $19.29 $40.38 $36.59 $25.13

LOE/BOE $1.65 $9.48 $11.15 $4.11

Ad Val/BOE $0.21 $0.06 $0.03 $0.16

Transportation/BOE $7.84 $0.08 $1.65 $5.71

Production Tax- per BOE/% of Pre-Hedge

Revenue

$0.35/1.8% $2.02/5.0% $3.72/10.2% $1.00/4.0%

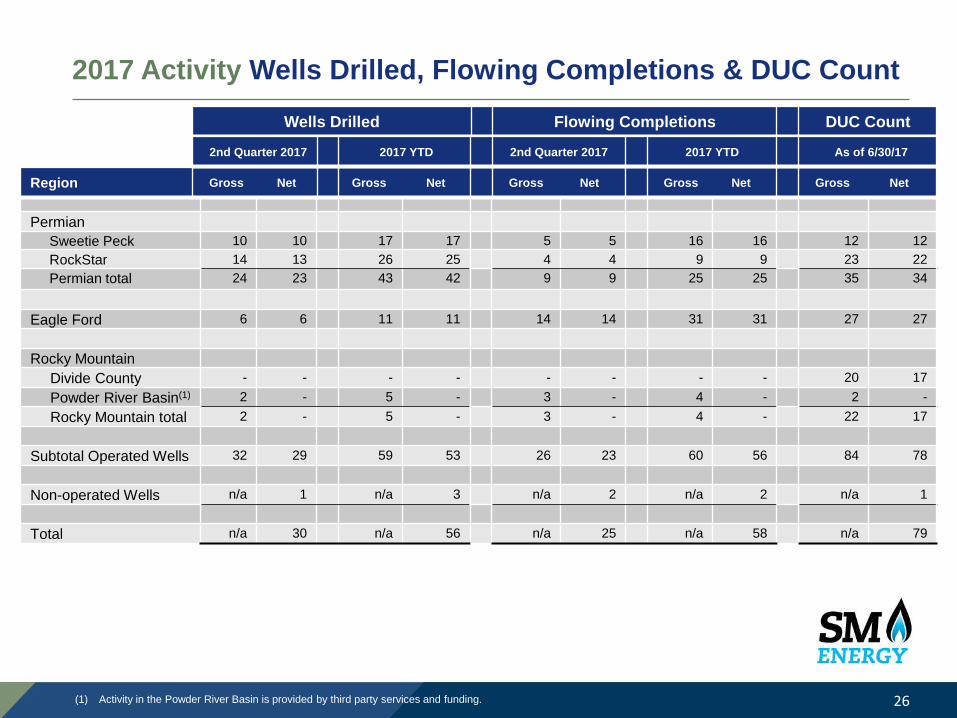

2017 Activity Wells Drilled, Flowing Completions & DUC Count

26

Wells Drilled Flowing Completions DUC Count

Permian

Sweetie Peck 10 10 17 17 5 5 16 16 12 12

RockStar 14 13 26 25 4 4 9 9 23 22

Permian total 24 23 43 42 9 9 25 25 35 34

Eagle Ford 6 6 11 11 14 14 31 31 27 27

Rocky Mountain

Divide County - - - - - - - - 20 17

Powder River Basin(1) 2 - 5 - 3 - 4 - 2 -

Rocky Mountain total 2 - 5 - 3 - 4 - 22 17

Subtotal Operated Wells 32 29 59 53 26 23 60 56 84 78

Non-operated Wells n/a 1 n/a 3 n/a 2 n/a 2 n/a 1

Total n/a 30 n/a 56 n/a 25 n/a 58 n/a 79

Region Gross Net Gross Net Gross Net Gross Net Gross Net

2nd Quarter 2017 2017 YTD 2nd Quarter 2017 2017 YTD As of 6/30/17

(1) Activity in the Powder River Basin is provided by third party services and funding.

Leasehold Summary

27

As of June 30, 2017

Net Acres(1)

6/30/17

Midland Basin

Sweetie Peck 17,255

RockStar(2) 65,950

Halff East (Upton County) 5,985

Midland Basin Total 89,190

Eagle Ford

Operated 167,465

Rocky Mountain

Divide 121,520

Powder River Basin 156,550

Rocky Mountain Other(3) 187,155

Other Areas/Exploration 24,915

Total 746,795

(1) Includes developed and undeveloped oil and gas leasehold, fee properties, and mineral servitudes held as of June 30, 2017. Sweetie Peck

acreage includes 2,650 net acres of drill-to-earn acreage.

(2) Includes correction from previously reported acreage total.

(3) Rocky Mountain Other includes non-core acreage located in North Dakota, Montana, Wyoming, and Utah.

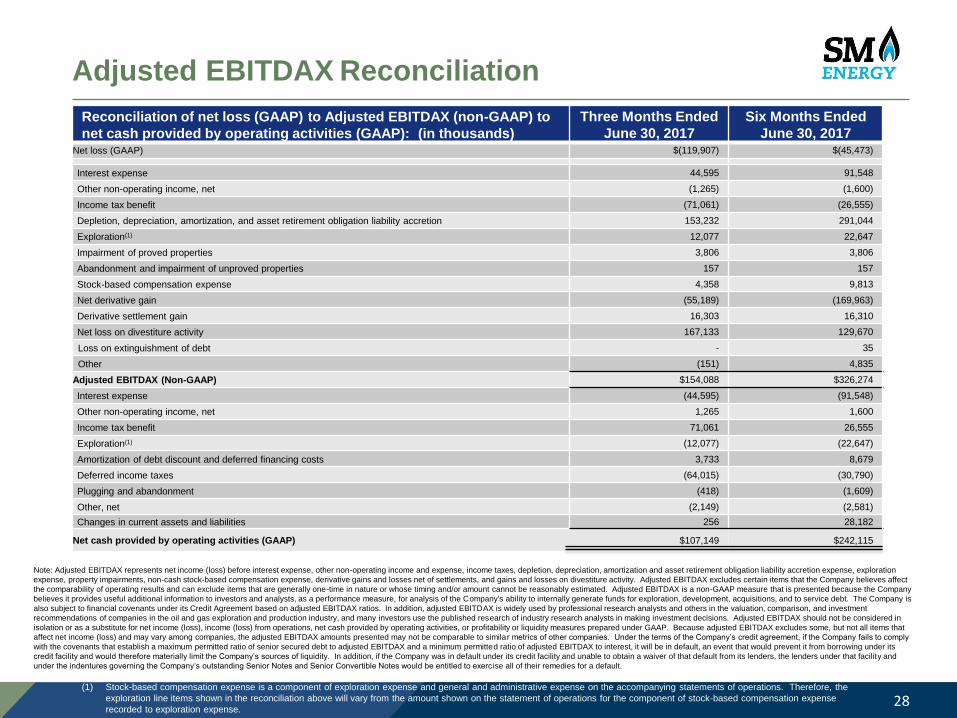

Adjusted EBITDAX Reconciliation

28

Reconciliation of net loss (GAAP) to Adjusted EBITDAX (non-GAAP) to

net cash provided by operating activities (GAAP): (in thousands)

Three Months Ended

June 30, 2017

Six Months Ended

June 30, 2017Net loss (GAAP) $(119,907) $(45,473)

Interest expense 44,595 91,548

Other non-operating income, net (1,265) (1,600)

Income tax benefit (71,061) (26,555)

Depletion, depreciation, amortization, and asset retirement obligation liability accretion 153,232 291,044

Exploration(1) 12,077 22,647

Impairment of proved properties 3,806 3,806

Abandonment and impairment of unproved properties 157 157

Stock-based compensation expense 4,358 9,813

Net derivative gain (55,189) (169,963)

Derivative settlement gain 16,303 16,310

Net loss on divestiture activity 167,133 129,670

Loss on extinguishment of debt - 35

Other (151) 4,835

Adjusted EBITDAX (Non-GAAP) $154,088 $326,274

Interest expense (44,595) (91,548)

Other non-operating income, net 1,265 1,600

Income tax benefit 71,061 26,555

Exploration(1) (12,077) (22,647)

Amortization of debt discount and deferred financing costs 3,733 8,679

Deferred income taxes (64,015) (30,790)

Plugging and abandonment (418) (1,609)

Other, net (2,149) (2,581)

Changes in current assets and liabilities 256 28,182

Net cash provided by operating activities (GAAP) $107,149 $242,115

Note: Adjusted EBITDAX represents net income (loss) before interest expense, other non-operating income and expense, income taxes, depletion, depreciation, amortization and asset retirement obligation liability accretion expense, exploration

expense, property impairments, non-cash stock-based compensation expense, derivative gains and losses net of settlements, and gains and losses on divestiture activity. Adjusted EBITDAX excludes certain items that the Company believes affect

the comparability of operating results and can exclude items that are generally one-time in nature or whose timing and/or amount cannot be reasonably estimated. Adjusted EBITDAX is a non-GAAP measure that is presented because the Company

believes it provides useful additional information to investors and analysts, as a performance measure, for analysis of the Company's ability to internally generate funds for exploration, development, acquisitions, and to service debt. The Company is

also subject to financial covenants under its Credit Agreement based on adjusted EBITDAX ratios. In addition, adjusted EBITDAX is widely used by professional research analysts and others in the valuation, comparison, and investment

recommendations of companies in the oil and gas exploration and production industry, and many investors use the published research of industry research analysts in making investment decisions. Adjusted EBITDAX should not be considered in

isolation or as a substitute for net income (loss), income (loss) from operations, net cash provided by operating activities, or profitability or liquidity measures prepared under GAAP. Because adjusted EBITDAX excludes some, but not all items that

affect net income (loss) and may vary among companies, the adjusted EBITDAX amounts presented may not be comparable to similar metrics of other companies. Under the terms of the Company’s credit agreement, if the Company fails to comply

with the covenants that establish a maximum permitted ratio of senior secured debt to adjusted EBITDAX and a minimum permitted ratio of adjusted EBITDAX to interest, it will be in default, an event that would prevent it from borrowing under its

credit facility and would therefore materially limit the Company’s sources of liquidity. In addition, if the Company was in default under its credit facility and unable to obtain a waiver of that default from its lenders, the lenders under that facility and

under the indentures governing the Company’s outstanding Senior Notes and Senior Convertible Notes would be entitled to exerc ise all of their remedies for a default.

(1) Stock-based compensation expense is a component of exploration expense and general and administrative expense on the accompanying statements of operations. Therefore, the

exploration line items shown in the reconciliation above will vary from the amount shown on the statement of operations for the component of stock-based compensation expense

recorded to exploration expense.

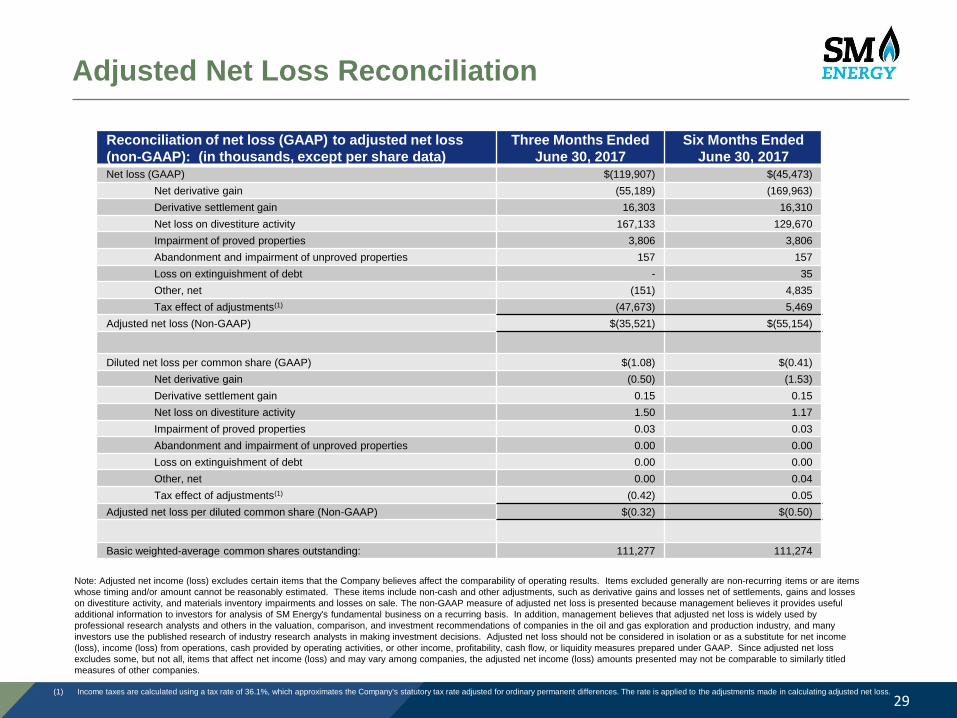

Adjusted Net Loss Reconciliation

29

Note: Adjusted net income (loss) excludes certain items that the Company believes affect the comparability of operating results. Items excluded generally are non-recurring items or are items

whose timing and/or amount cannot be reasonably estimated. These items include non-cash and other adjustments, such as derivative gains and losses net of settlements, gains and losses

on divestiture activity, and materials inventory impairments and losses on sale. The non-GAAP measure of adjusted net loss is presented because management believes it provides useful

additional information to investors for analysis of SM Energy's fundamental business on a recurring basis. In addition, management believes that adjusted net loss is widely used by

professional research analysts and others in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and production industry, and many

investors use the published research of industry research analysts in making investment decisions. Adjusted net loss should not be considered in isolation or as a substitute for net income

(loss), income (loss) from operations, cash provided by operating activities, or other income, profitability, cash flow, or liquidity measures prepared under GAAP. Since adjusted net loss

excludes some, but not all, items that affect net income (loss) and may vary among companies, the adjusted net income (loss) amounts presented may not be comparable to similarly titled

measures of other companies.

(1) Income taxes are calculated using a tax rate of 36.1%, which approximates the Company's statutory tax rate adjusted for ordinary permanent differences. The rate is applied to the adjustments made in calculating adjusted net loss.

Reconciliation of net loss (GAAP) to adjusted net loss

(non-GAAP): (in thousands, except per share data)

Three Months Ended

June 30, 2017

Six Months Ended

June 30, 2017Net loss (GAAP) $(119,907) $(45,473)

Net derivative gain (55,189) (169,963)

Derivative settlement gain 16,303 16,310

Net loss on divestiture activity 167,133 129,670

Impairment of proved properties 3,806 3,806

Abandonment and impairment of unproved properties 157 157

Loss on extinguishment of debt - 35

Other, net (151) 4,835

Tax effect of adjustments(1) (47,673) 5,469

Adjusted net loss (Non-GAAP) $(35,521) $(55,154)

Diluted net loss per common share (GAAP) $(1.08) $(0.41)

Net derivative gain (0.50) (1.53)

Derivative settlement gain 0.15 0.15

Net loss on divestiture activity 1.50 1.17

Impairment of proved properties 0.03 0.03

Abandonment and impairment of unproved properties 0.00 0.00

Loss on extinguishment of debt 0.00 0.00

Other, net 0.00 0.04

Tax effect of adjustments(1) (0.42) 0.05

Adjusted net loss per diluted common share (Non-GAAP) $(0.32) $(0.50)

Basic weighted-average common shares outstanding: 111,277 111,274

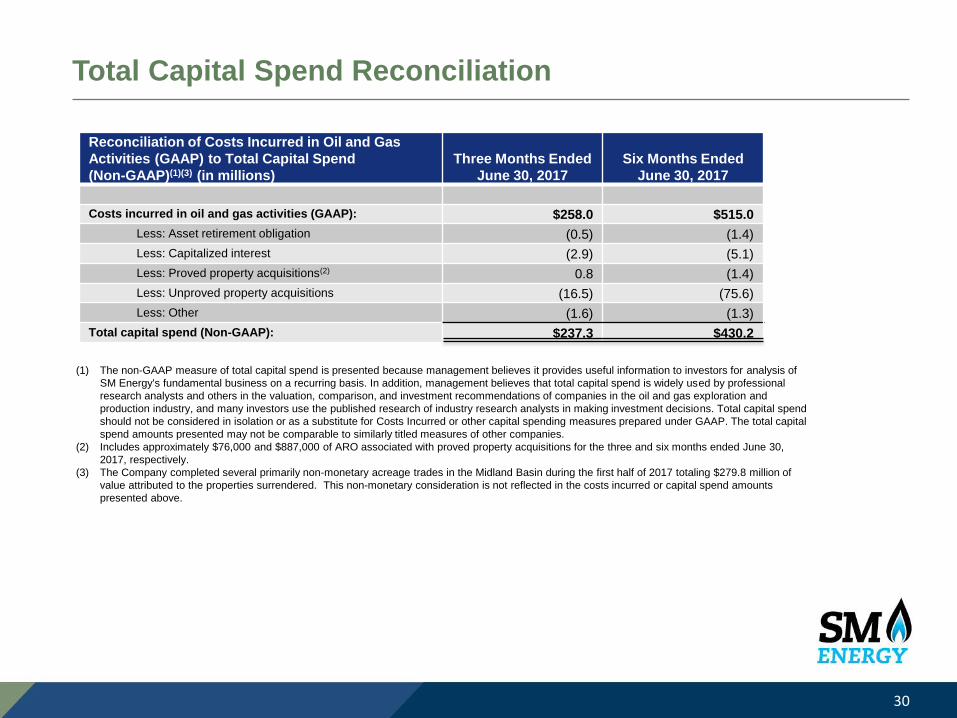

Total Capital Spend Reconciliation

30

Reconciliation of Costs Incurred in Oil and Gas

Activities (GAAP) to Total Capital Spend

(Non-GAAP)(1)(3) (in millions)

Three Months Ended

June 30, 2017

Six Months Ended

June 30, 2017

Costs incurred in oil and gas activities (GAAP): $258.0 $515.0

Less: Asset retirement obligation (0.5) (1.4)

Less: Capitalized interest (2.9) (5.1)

Less: Proved property acquisitions(2) 0.8 (1.4)

Less: Unproved property acquisitions (16.5) (75.6)

Less: Other (1.6) (1.3)

Total capital spend (Non-GAAP): $237.3 $430.2

(1) The non-GAAP measure of total capital spend is presented because management believes it provides useful information to investors for analysis of

SM Energy's fundamental business on a recurring basis. In addition, management believes that total capital spend is widely used by professional

research analysts and others in the valuation, comparison, and investment recommendations of companies in the oil and gas exploration and

production industry, and many investors use the published research of industry research analysts in making investment decisions. Total capital spend

should not be considered in isolation or as a substitute for Costs Incurred or other capital spending measures prepared under GAAP. The total capital

spend amounts presented may not be comparable to similarly titled measures of other companies.

(2) Includes approximately $76,000 and $887,000 of ARO associated with proved property acquisitions for the three and six months ended June 30,

2017, respectively.

(3) The Company completed several primarily non-monetary acreage trades in the Midland Basin during the first half of 2017 totaling $279.8 million of

value attributed to the properties surrendered. This non-monetary consideration is not reflected in the costs incurred or capital spend amounts

presented above.

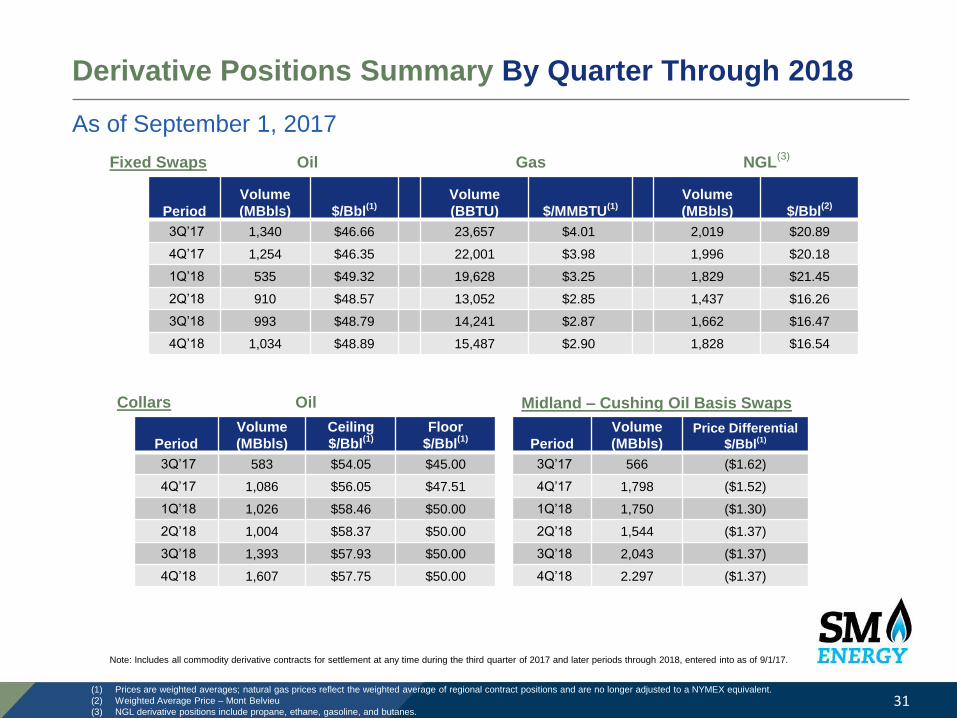

Derivative Positions Summary By Quarter Through 2018

31

As of September 1, 2017

Period

Volume

(MBbls) $/Bbl(1)

Volume

(BBTU) $/MMBTU(1)

Volume

(MBbls) $/Bbl(2)

3Q’17 1,340 $46.66 23,657 $4.01 2,019 $20.89

4Q’17 1,254 $46.35 22,001 $3.98 1,996 $20.18

1Q’18 535 $49.32 19,628 $3.25 1,829 $21.45

2Q’18 910 $48.57 13,052 $2.85 1,437 $16.26

3Q’18 993 $48.79 14,241 $2.87 1,662 $16.47

4Q’18 1,034 $48.89 15,487 $2.90 1,828 $16.54

Period

Volume

(MBbls)

Ceiling

$/Bbl(1)

Floor

$/Bbl(1)

3Q’17 583 $54.05 $45.00

4Q’17 1,086 $56.05 $47.51

1Q’18 1,026 $58.46 $50.00

2Q’18 1,004 $58.37 $50.00

3Q’18 1,393 $57.93 $50.00

4Q’18 1,607 $57.75 $50.00

Fixed Swaps

Collars

Oil

Oil

Gas NGL(3)

(1) Prices are weighted averages; natural gas prices reflect the weighted average of regional contract positions and are no longer adjusted to a NYMEX equivalent.

(2) Weighted Average Price – Mont Belvieu

(3) NGL derivative positions include propane, ethane, gasoline, and butanes.

Note: Includes all commodity derivative contracts for settlement at any time during the third quarter of 2017 and later periods through 2018, entered into as of 9/1/17.

Period

Volume

(MBbls)Price Differential

$/Bbl(1)

3Q’17 566 ($1.62)

4Q’17 1,798 ($1.52)

1Q’18 1,750 ($1.30)

2Q’18 1,544 ($1.37)

3Q’18 2,043 ($1.37)

4Q’18 2.297 ($1.37)

Midland – Cushing Oil Basis Swaps

NGL Derivative Position Detail(1)

32

Period

Volume

(MBbls) $/Bbl(2)

3Q’17 906 $9.48

4Q’17 966 $9.65

2017 Total 1,872

1Q’18 923 $10.90

2Q’18 915 $10.87

3Q’18 1,033 $10.99

4Q’18 1,146 $11.18

2018 Total 4,017

NGL Swaps OPIS Eth Purity Mt Belv NGL Swaps OPIS Propane Mt Belv Non-TET NGL Swaps Natural Gasoline Mt Belv Non TET

NGL Swaps OPIS IsoButane Mt Belv Non TETNGL Swaps OPIS NButane Mt Belv Non TET

(1) Includes all commodity derivative contracts for settlement at any time during the third quarter of 2017 and later periods through 2018 entered into as of September 1, 2017.

(2) Weighted-Average Contract Price

Note: Totals may not sum due to rounding; reference 10-Q for future period detail

Period

Volume

(MBbls) $/Bbl(2)

3Q’17 222 $48.43

4Q’17 203 $48.41

2017 Total 425

1Q’18 189 $49.40

2Q’18 35 $47.36

3Q’18 39 $47.36

4Q’18 42 $47.36

2018 Total 305

Period

Volume

(MBbls) $/Bbl(2)

3Q’17 163 $32.42

4Q’17 149 $32.34

2017 Total 312

1Q’18 138 $35.41

2Q’18 26 $31.71

3Q’18 29 $31.71

4Q’18 32 $31.71

2018 Total 225

Period

Volume

(MBbls) $/Bbl(2)

3Q’17 588 $21.91

4Q’17 550 $21.91

2017 Total 1,138

1Q’18 460 $23.35

2Q’18 440 $23.38

3Q’18 538 $23.36

4Q’18 583 $23.41

2018 Total 2,021

Period

Volume

(MBbls) $/Bbl(2)

3Q’17 140 $33.28

4Q’17 128 $33.23

2017 Total 268

1Q’18 119 $35.44

2Q’18 21 $30.35

3Q’18 23 $30.35

4Q’18 25 $30.35

2018 Total 188

NGL Realizations

33

• 22% increase in realized price (before hedges) from 2Q16 to 2Q17

• SM NGL price realizations are predominately tied to Mont Belvieu, fee based contracts

• Differential reflects NGL barrel product mix and transportation and fractionation fees

2Q16 3Q16 4Q16 1Q17 2Q17

Mt. Belvieu ($/Bbl) $20.04 $19.74 $24.11 $26.74 $24.11

SM Realization

($/Bbl)$16.12 $16.58 $20.02 $22.06 $19.71

% Differential to

Mt. Belvieu80% 84% 83% 82% 82%

42%

28%

9%

9%

12%

SM Typical NGL Bbl(1)

Ethane PropaneIso Butane Normal ButanePentane

(1) Includes the effects of ethane rejection.

0%

20%

40%

60%

80%

100%

$0.55 $0.60 $0.65

IRR

Mt. Belvieu $/Gal

0%

20%

40%

60%

80%

100%

120%

$40 $45 $50 $55 $60

IRR

NYMEX WTI

7,600' 10,000'

0%

20%

40%

60%

80%

100%

120%

$40 $45 $50 $55 $60

IRR

NYMEX WTI

7,600' 10,000'

Top-Tier Assets Regional Well Projected Economics

34

2017 capital program focusing on areas with top tier returns

RockStar – Wolfcamp A

Well Cost: $5.6MM

Well Spacing: 660’Well Cost: $6.8MM

Well Spacing: 660’Well Cost: $5.9MM

Well Spacing: 660’

Well Cost: $7.0MM

Well Spacing: 660’

Sweetie Peck – Lower Spraberry

Note: well costs include drill, complete, and equip; sensitivities at $3.00/MMBtu NYMEX; Eagle Ford East oil flat at $50/Bbl

WTI. Well economics are not updated to reflect most recent well performance and completion enhancements at 8/1/17.

Eagle Ford East

Well Cost: $5.2MM, Lateral Length: 8,000’, Well Spacing: 625’, Sand Loading: 2,000 lbs/ft, Stage Spacing: 150’

Sand loading: 1,900 lbs/ft; Stage Spacing: 167’ Sand loading: 1,900 lbs/ft; Stage Spacing: 167’

Eagle Ford East

~35% NGLs1H17 Average

Mt. Belvieu ($/Gal)

Howard County Operators

35

SM Energy

Callon

Encana

Surge/Yantai Xinchao

Diamondback

Oxy

Energen

Breitburn

Sabalo

Sweetie Peck Operators

36

SM Energy

Apache

Chevron

Concho

Devon

Diamondback

Discovery

Endeavor

Exxon

Legacy

Oxy

Pioneer

Summit

Miscellaneous

Eagle Ford Operators

37

Fasken

AreaNorth

AreaEast

AreaSouth

DimmitWebb

Dim

mit

Maverick

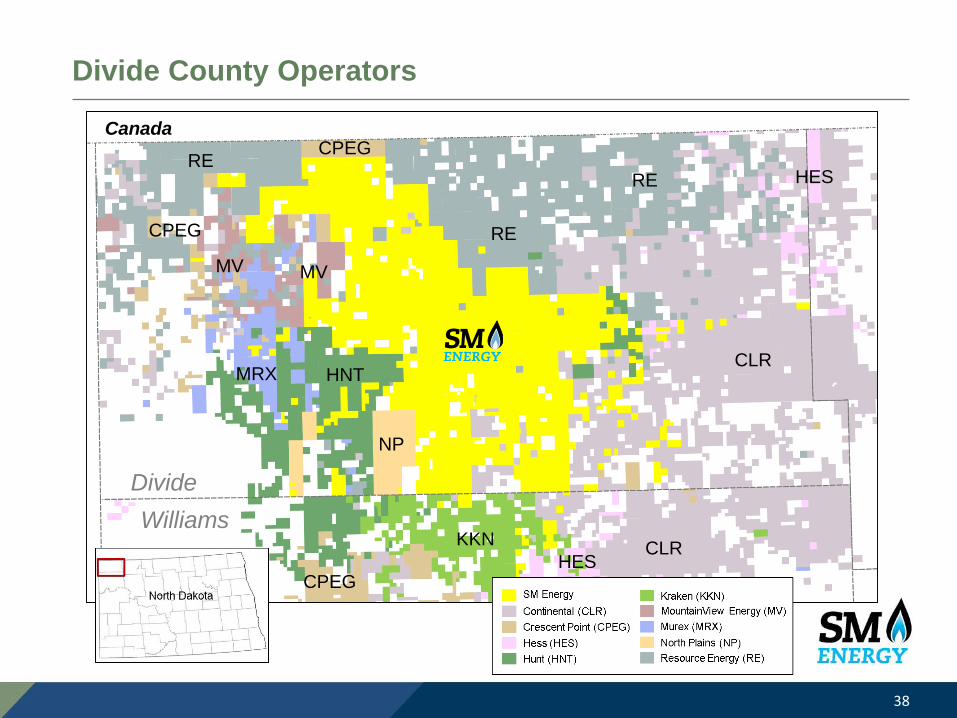

Divide County Operators

38

Canada

Divide

Williams

RECPEG

RE

HES

CLR

CLR

RE

HES

KKN

CPEG

HNT

NP

MRX

MV MV

CPEG

Powder River Basin Operators

39

SM ENERGY (SME)

ANSCHUTZ (ANS)

CHESAPEAKE (SHK)

DENBURY (DEN)

DEVON (DEV)

EOG

FLEUR DE LIS (FDL)

HELIS (HEL)

LIBERTY RESOURCES (LIB)

SAMSON (SSN)

WOLD (WLD)

OTHERS

Campbell

ConverseNatrona

Johnson