barking & dagenham : economic development study plan 2

TRANSCRIPT

Barking & Dagenham : Economic Development Study

6788302v3 P25

Plan 2: Existing Retail Provision

Barking & Dagenham : Economic Development Study

P26 6788302v3P26

Retail Capacity Assessment – Methodology and Data

Price Base

All monetary values expressed in this study are at 2011 prices, consistent with

Experian’s base year expenditure figures for 2011 which is the most up to date

information available.

Study Area

The quantitative analysis is based on a defined study area that covers the

catchment areas of the main shopping destinations in London Borough of

Barking & Dagenham (LBBD). The study area is sub-divided into six zones

based on ward boundaries as shown above. The survey zones take into

consideration the extent of the catchment area of the main centres in LBBD.

Retail Expenditure

The level of available expenditure to support retailers is based on first

establishing per capita levels of spending for the study area population.

Experian’s local consumer expenditure estimates for comparison and

convenience goods for each of the study area zones for the year 2011 have

been obtained.

Experian’s EBS national expenditure information (Experian Retail Planner

Briefing Note 11, October 2013) has been used to forecast expenditure within

the study area. Experian’s forecasts are based on an econometric model of

disaggregated consumer spending. This model takes a number of macro-

economic forecasts (chiefly consumer spending, incomes and inflation) and

uses them to produce forecasts of consumer spending volumes, prices and

value, broken down into separate categories of goods. The model incorporates

assumptions about income and price elasticities.

Experian’s EBS growth forecast rates for 2011 to 2014 reflect the current

economic circumstances and provide an appropriate growth rate for the short

term (for convenience goods: -0.6% for 2011-2013, -0.3% for 2013-2014 and

0.1% for 2014 to 2015; for comparison goods: 3.1% for 2011-2012, 3.2% for

2012-2013, 2.3% for 2013-2014 and 2.8% for 2014-2015).

In the longer term it is more difficult to forecast year on year changes in

expenditure. Experian’s longer term growth average forecasts have been

adopted i.e. 0.8% per annum for convenience goods from 2015, and 2.9% per

annum growth for comparison goods from 2015. These growth rates are

relatively cautious when compared with past growth rates, but in our view

represent realistic forecast for future growth. These growth figures relate to real

growth and exclude inflation.

Special Forms of Trading (SFT) or non-store activity is included within

Experian’s Goods Based Expenditure (GBE) estimates. SFT includes other

Barking & Dagenham : Economic Development Study

6788302v3 P27

forms of retail expenditure not spent in shops e.g. mail order sales, some

internet sales, vending machines, party plan selling, market stalls and door to

door selling. SFT needs to be excluded from retail assessments because it

relates to expenditure not spent in shops and does not have a direct

relationship with the demand for retail floorspace. The growth in home

computing, Internet connections and interactive TV may lead to a growth in

home shopping and may have effects on retailing in the high street. Experian

provides projections for special forms of trading and e-tailing. This Experian

information suggests that non-store retail sales in 2011 is:

• 6.2% of convenience goods expenditure; and

• 13.0% of comparison goods expenditure.

Experian predicts that these figures will increase in the future, up to over 20%

by the end of the 2020s. However, Experian recognises that not all of this SFT

expenditure should be excluded from a retail capacity analysis, because some

of it relates to internet sales through traditional retail businesses, rather than

internet companies. The turnover attributable to e-tail through retail businesses

is included in the company average turnovers, and therefore expenditure

figures should not exclude this expenditure. Experian has provided adjusted

deductions for SFT and projections. These projections have been used to

exclude only e-tail expenditure attributed to non-retail businesses, which will

not directly impact on the demand for retail floorspace. The adjusted figures

suggest that SFT sales in 2011 are:

• 1.9% of convenience goods expenditure; and

• 9.7% of comparison goods expenditure.

The projections provided by Experian suggest that these percentages could

increase to 3.5% and 13.8% by 2017, and estimated at 5.2% and 16.0% by

2027. These figures have been adopted in this assessment.

Home/electronic shopping has also emerged with the increasing growth in the

use of personal computers and the Internet. This study makes an allowance for

future growth in e-tailing based on Experian projections. It will be necessary to

monitor the amount of sales attributed to home shopping in the future in order

to review future policies and development allocations.

On-line shopping has experienced rapid growth since the late 1990s but in

proportional terms the latest available data suggests it remains an insignificant

percentage of total retail expenditure. Recent trends suggest continued strong

growth in this sector, but Experian’s projections suggest this growth will level

off by 2016/17.

The implications on the demand for retail space are unclear. For example,

some retailers operate on-line sales from their traditional retail premises eg.

food store operators. Therefore, growth in on-line sales may not always mean

there is a reduction in the need for retail floorspace. Given the uncertainties

relating to internet shopping and the likelihood that it will increase in

Barking & Dagenham : Economic Development Study

P28 6788302v3P28

proportional terms, this assessment has adopted relatively cautious growth

projections for retail expenditure.

Market Shares/Penetration Rates

To assess the capacity for new retail floorspace, penetration rates are

estimated for shopping facilities within the study area. The assessment of

penetration rates are based on a range of factors but primarily information

gathered through the 2013 household survey.

The total turnover of shops within the District is estimated based on penetration

rates. For convenience goods shopping turnover estimates are then compared

to average company benchmark or average sales floorspace densities derived

from Verdict (UK Food and Grocery Retailers 2013) and Mintel (Retail

Rankings 2013) information, which provide an indication of how individual retail

stores and centres are performing against expected turnover averages. This

allows the identification of potential surplus or deficit capacity for retail sales

floorspace.

Benchmark Turnover Levels

Company average turnover to sales floorspace densities are available for

major food store operators and are compiled by Verdict. Company average

sales densities (adjusted to exclude petrol and comparison sales and include

VAT) have been applied to the sales area of the large food stores, and a

benchmark turnover for each store has been calculated. This benchmark

turnover is not necessarily the actual turnover of the food store, but it does

provide a useful benchmark for assessing existing shopping patterns and the

adequacy of current floorspace in quantitative terms.

The estimated convenience goods sales areas have been derived from a

combination of the Institute of Grocery Distribution (IGD), Goad plans and NLP

estimates based on site visits. Estimates for comparison sales floorspace

within large food stores has been deducted, for consistency with the use of

goods based expenditure figures.

Average sales densities are not widely available for small convenience shops,

particularly independent retailers. Based on the mix of shops present in each

centre within the Borough and our experience of trading levels of small

independent shops informed by household shopper surveys elsewhere, we

have adopted an average sales density of £5,000 per sq.m net for convenience

shops/stores in the study area. This is consistent with NLP’s experience of

retail studies across the South and East of England. The total benchmark

turnover of identified convenience sales floorspace within LBBD is £259.62

million (Table 13, Appendix 13).

Mintel’s Retail Rankings provides company average sales density information

for a selection of national comparison retailers. This data suggests a notional

average sales density for national high street comparison retailers of around

£5,000 per sq.m.

Barking & Dagenham : Economic Development Study

6788302v3 P29

Appendix 9 Household Survey Results

Barking & Dagenham : Economic Development Study

6788302v3 P31

Household Survey Results

Survey structure

NEMS Market Research carried out a telephone survey of 1,200 households

across the Barking and Dagenham Borough study area in October 2013. The

study area was split into six zones based on ward boundaries.

The number of interviews undertaken in each zone reflects the relative

population in order to produce statistically reliable sub-samples. The main aims

of the survey were to establish consumer patterns for the following:

• Main food shopping and small scale ‘top up’ shopping;

• Non- food shopping, including:

- Clothes and shoes;

- Domestic electrical appliances and other electric goods;

- Furniture, soft furnishings and flooring;

- DIY/Hardware and garden items;

- Health, Beauty and chemist items; and

- Other comparison goods such as books, CDs, toys and gifts.

Main food shopping

The primary destination for main food shopping are large supermarket stores

(Q.1), Table HS.1 shows the top ten food stores in terms of the percentage of

respondents that visited each.

Table HS.1 Main Food Shopping Destinations

Food Store Percentage

Asda, Merrielands Crescent, Dagenham 14.5%

Asda, Vicarage Field, Barking 5.6%

Morrisons, Beacontree Heath, Wood Lane 5.3%

Tesco Extra, Rainham, Essex 5.0%

Tesco Barking Superstore 5.0%

Tesco Extra, Romford, Essex 5.0%

Sainsbury's Claps Gate Lane, Beckton 4.5%

Tesco Extra Gallions Reach 4.3%

Asda, Tollgate Road, Beckton 3.6%

Sainsbury's High Street, Chadwell Heath 3.6%

Source: NEMS Household Survey, October 2013

Barking and Dagenham Heathway both have a high market share of main food

shopping; 14.5% of respondents visited major food stores in Dagenham

Heathway and 10.6% of respondents visited major food stores in Barking. Out

Barking & Dagenham : Economic Development Study

P32 6788302v3P32

of the 10 most popular food stores however a relatively high proportion of main

food shopping (totalling 18.1%) was carried out outside the Borough.

Mode of travel for main food shopping

16 Figure HS.1 showos that in the study area 65.6% of respondents travel to

do their main shopping by car. This is lower than the NLP average of

74.6% which has been derived from similar surveys (around 40 surveys

conducted in city and rural local authorities across the UK over the past 8

years). The second most popular way to travel to do food shopping was

by bus (17%) this is significantly higher than the NLP average of 8.6%.

The third most popular way to travel to food stores was walking (11.9%)

this figure is similar to the NLP average of 11.7%.

Figure HS.1. Mode of travel in study area

Source: NEMS Household Survey, October 2013

Top-Up Food shopping

Top-up food shopping trips are normally made to supplement main food trips to

larger stores and are undertaken on a more frequent basis for staples such as

bread and milk. Approximately 65% of households stated that they undertake

top-up food shopping in addition to their main food shopping. The market share

of top up food shopping for each major centre and district centre is shown in

Figure HS.2 below. Only 0.2% of respondents did top-up food shopping online

compared to 2.1% who did their main food shopping online.

65.6%

17.0%

0.9% 0.3% 1.1%11.9%

1.2% 2.0%

Barking & Dagenham : Economic Development Study

6788302v3 P33

Figure HS.2. Most popular destinations for top-up food shopping

Source: NEMS Household Survey, October 2013

Non-food shopping

Respondents were asked where they did the most of their non-food household

shopping, the most popular destinations and the proportion of respondents

who visited the centre is shown in Figure HS.3 below. For the study area as a

whole, Romford was the most popular destination with 27.1% of all

respondents shopping there, followed by Ilford and Lakeside (13.2% each),

Barking (6.8%) and Dagenham Heathway (6.5%). This demonstrates that the

majority of non-food shopping is carried out outside the Borough.

Figure HS.3 Top 10 most popular destinations for non-food shopping

Source: NEMS Household Survey, October 2013

Overall, 2.8% of respondents buy most of their non-food shopping on the

internet. The Dagenham zone has the highest proportion of respondents who

buy most of their non-food shopping on the internet (4.5%), followed by the

18.8%

10.2%

4.8%6.7%

3.0% 3.1% 2.8%

6.4%

27.1%

13.2% 13.2%

6.8% 6.5%5.1% 4.5%

2.8% 2.7% 2.2%

Barking & Dagenham : Economic Development Study

P34 6788302v3P34

Barking zone (3.9%). The Havering West zone undertakes the lowest

proportion of non-food shopping on the internet (0.8%).

Mode of travel for non-food shopping

The predominant mode of travel for non-food shopping was the car (both driver

and passenger) with 56.6% of respondents indicating that they use this form of

transport. The second most popular mode of transport for non-food shopping

was bus/coach (27.6%) followed by walking (7.2%).

Figure HS.4 Mode of travel for non-food shopping

Source: NEMS Household Survey, October 2013

Non-food Shopping Destinations

Respondents were also asked at which locations they last did various

categories of non-food shopping. The top 10 retail destinations for each

category are shown in Figures HS.5 – HS.11 below.

56.6%

1.7%3.9%

27.6%

0.7%7.2% 2.2%

Car

Tube

Train

Bus/ Coach

Taxi

Walk

Goods delivered

Barking & Dagenham : Economic Development Study

6788302v3 P35

Figure HS.5 Clothes and Shoes

Source: NEMS Household Survey, October 2013

Figure HS.6 Domestic electrical appliances

Source: NEMS Household Survey, October 2013

28.7%

16.4%

11.9%

6.8%5.1% 3.7% 3.4% 2.9% 2.8% 2.4%

14.5%

7.8%7.0% 6.6% 6.2%

5.1% 4.7% 4.2%3.4% 3.3%

Barking & Dagenham : Economic Development Study

P36 6788302v3P36

Figure HS.7 Non-domestic electric goods

Source: NEMS Household Survey, October 2013

Figure HS.8 Furniture, Soft furnishings and floor covering

Source: NEMS Household Survey, October 2013

11.2% 11.1%

8.7%

7.0% 6.6%

5.3%

4.0% 3.9%2.8% 2.5%

12.3%

10.2%

6.1%5.3%

4.6% 4.6% 4.2%

2.3% 2.0% 1.5%

Barking & Dagenham : Economic Development Study

6788302v3 P37

Figure HS.9 DIY, hardware and garden items

Source: NEMS Household Survey, October 2013

Figure HS.10 Health, beauty and chemist items

Source: NEMS Household Survey, October 2013

17.1%

10.7%8.9%

5.9% 5.6% 4.9%3.3% 2.9%

2.0% 2.0%

12.5%11.4%

10.4% 10.1% 9.9%

3.2% 3.0% 3.0% 2.7% 2.7%

Barking & Dagenham : Economic Development Study

P38 6788302v3P38

Figure HS.11 Books, CDs, toys and gifts

Source: NEMS Household Survey, October 2013

Internet Shopping

Respondents were asked what goods they regularly buy on the internet.

48.5% of respondents stated that they did not regularly buy items on the

internet. The most popular response was “other” goods including books, CDs

and toys (31.7%), followed by clothes and shoes (18.8%) and electrical goods

including TV, Hi-Fi and computers (10.8%). Only 3.7% stated that they

regularly buy groceries on the internet.

Community Facilities

Respondents were asked where their household normally visits to use

community facilities such as libraries and community halls. The most popular

destination was Dagenham Heathway (11.8%), followed by Barking (11.5%)

and Ilford (10.6%).

Leisure Activities

Cinema

Respondents were asked which cinema they or their family last visited. 63% of

respondents said they visited the cinema, which was the second most popular

leisure activity after visiting restaurants. This response rate is higher than NLPs

average of 51% (derived from similar studies from across the country). The

most popular cinema destinations visited by respondents from across the study

area were Vue Romford (13%), Vue Dagenham (12.9%), Showcase

Dagenham (9.0%) and Cineworld Ilford (6.3%).

23.1%

13.3%

6.9% 6.0%3.9% 3.4% 2.9% 2.3% 2.1% 1.9%

Barking & Dagenham : Economic Development Study

6788302v3 P39

Theatre

55% of respondents said that they had visited the theatre, and this was the

third most popular leisure activity overall. Again, this figure is higher than the

NLP average which is 42.5%. The high level of theatre visits is probably due to

the high number of facilities in close proximity in Central London. When asked

where they had visited the theatre, Central London was the most popular

destination (33.3%). Respondents also visited theatres in Hornchurch (5.2%),

Ilford (4.7%) and Barking (2.9%).

Pub/Bar

45% of respondents from across the Borough indicated that they visited pubs

and bars. This is slightly lower than the NLP average from other surveys which

is 47.5%. When asked where they had most recently visited pubs or bars,

6.5% of respondents answered Central London. The most popular local

destinations included Romford (5.1%), Hornchurch (4.2%), Dagenham

Heathway (3.4%) and Chadwell Heath (3.2%).

Restaurant

Visiting restaurants was the most popular leisure activity across the study area

with 78% of respondents indicating that they has recently visited a restaurant.

This is higher than the NLP average for other surveys which is 67.9%. When

asked where they had most recently visited a restaurant, 10.7% of respondents

answered Romford. Central London was the second most popular destination

(8.6%), followed by Hornchurch (7.6%), Dagenham Heathway (4.8%),

Chadwell Heath (4.3%) and finally Barking Town Centre (3.4%).

Nightclubs

Only 11% of respondents said that they had visited nightclubs, and this was

the least popular leisure activity across the study area. This participation rate

is higher than the NLP average of 9.9% derived from similar surveys. The

sample of visitors in each zone was relatively small, however the most popular

location for respondents who had last visited a nightclub was Central London

(3.7%) followed by Romford (2.7%).

Bingo

Bingo facilities were visited by 13% of respondents making this the second

least popular leisure activity across the Borough. This figure is however

significantly higher than the NLP average of 5.1% derived from similar studies.

The most popular destinations respondents went to play bingo were Mecca

Bingo at Dagenham Leisure Park (5.6%), Mecca Bingo Chadwell Heath (1.4%)

and Mecca Bingo Romford (1.2%).

Barking & Dagenham : Economic Development Study

P40 6788302v3P40

Tenpin bowling

28% of respondents indicated that their household visited tenpin bowling

facilities, and this is significantly higher than the NLP average of 18.1% derived

from similar surveys. The most popular destinations for bowling are Dagenham

bowling (10%), Namco Romford (4.2%) and The City Pavilion Romford (3.9%).

Health club/gym

28% of respondents from across the study area also indicated that they visited

health clubs/gyms. This is slightly higher than the NLP average of 25.6%

derived from similar surveys. Figure HS.12 below shows the most popular

destinations for respondents using health club/gym facilities.

Figure HS.12 Health and gym facility destinations

Source: NEMS Household Survey, October 2013

3.0%

2.7%

2.4%

1.6%1.5%

1.3%

1.0%

Beacontree Dagenham East Ham Barking Ilford Newham Central

London

Barking & Dagenham : Economic Development Study

6788302v3 P41

Appendix 10 Audit of Centres

Barking & Dagenham : Economic Development Study

6788302v3 P43

Barking Town Centre

Barking is defined as a major centre and is located to the west of the Borough.

It is the largest town centre in the Borough as such it has a stronger

comparison offer and more national retailers than any other centre surveyed

for this study. The main retail areas in the centre include Vicarage Fields

Shopping Centre, East Street, Ripple Road and the Station Quarter which is

located around Barking train and underground station. The recently

redeveloped Town Square comprises several modern retail units and a new

community learning centre.

Barking Town Centre’s key roles include:

• Comparison shopping: a good selection of national multiple retailers

and independent shops selling a range of both low and high order

comparison goods.

• Convenience shopping: Asda located within the Vicarage Fields

Shopping Centre, Lidl on Ripple Road and Iceland on East Street provide

the main convenience offer within the centre. These are complimented by

a diverse range of independent food stores.

• Services: good selection of retail services including restaurants, cafes,

banks, post office, dry cleaners, internet café and bureau de change.

• Leisure: snooker club, theatre, and leisure centre.

• Community uses: community halls, health centre, learning centre, local

Council offices, dental surgery and places of worship.

Mix of Uses and Occupier Representation

Barking has a total of 266 retail/service uses. The diversity measured by

number of units is set out against the national average in Table B.1.

Table B.1 Barking Use Class Mix by Unit

Type of Unit Units

% of Total Number of Units

% National Average (1)

Comparison Retail 97 36.5 36.0

Convenience Retail 33 12.4 8.1

A1 Services (2)

33 12.4 14.1

A2 Services 30 11.3 12.1

A3/A5 41 15.4 14.7

A4 Pubs/bars 5 1.9 2.9

Vacant 27 10.1 12.1

Total 266 100.0 100.0

Source: Goad Plans, updated by NLP November 2013

Notes: (1) UK average for all town centres surveyed by Goad Plans (March 2014) (2) incl. hairdressers, travel agents and other Class A1 uses not selling comparison/convenience goods

Barking & Dagenham : Economic Development Study

P44 6788302v3P44

Figure B.1 Goad Plan of Barking Town Centre (Ground Floor Only)

The composition of Barking town centre is very similar to the national average

in the majority of categories. The greatest deviation from the national average

is the proportion of convenience goods retail units which is 4.3 percentage

points higher. The vacancy rate is marginally lower than the national average.

Barking & Dagenham : Economic Development Study

6788302v3 P45

Retailer Representation

Table B.2 Barking Breakdown of Comparison Units

Type of Unit Barking % UK Average*

Units %

Clothing and footwear 29 29.9 25.6

Furniture, carpets and textiles 5 5.2 8.3

Booksellers, arts, crafts and stationers 4 4.1 10.9

Electrical, gas, music and photography 16 16.5 9.5

DIY, hardware and homewares 9 9.3 6.2

China, glass, gifts and fancy goods 0 0.0 3.9

Cars, motorcycles and motor access 0 0.0 2.9

Chemists, drug stores and opticians 16 16.5 9.4

Variety, department and catalogue 1 1.0 1.4

Florists, nurserymen and seedsmen 1 1.0 2.2

Toys, hobby, cycle and sport 3 3.1 5.1

Jewellers 4 4.1 4.9

Other comparison retailers 9 9.3 9.7

Total 97 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Overall the selection of comparison retail stores in Barking is reasonable. Of

the 97 comparison retailers 21 are national multiples (excluding six charity

shops). Key multiple stores include Argos, Boots, QS, Peacocks, Superdrug,

Wilkinson, WH Smith and fashion stores include Evans, Dorothy Perkins, New

Look and Burton, which in terms of market position are lower middle. There are

70 independent comparison shops selling a range of products. There are a

number of gaps in the general clothing sector i.e. middle/mass market level

and upper market/luxury sectors e.g. Next, Clarkes, Topshop and Monsoon.

Table B2 indicates that most of the key Goad goods categories are

represented in Barking, however the centre does not have any shops which fall

within two categories i.e. china/glass/gifts/fancy goods and

cars/motorcycles/motor accessories. The choice of shops in other categories is

poor with less than 5 shops in five other categories. Barking does not contain

a department store such as Debenhams or Marks & Spencer.

The choice of shops within the clothing/footwear, electrical/music/

photography, DIY/hardware/homewares and chemists/drug stores/opticians is

reasonable.

Barking comparison shopping provides a mix of lower order comparison goods

purchased on a day to day basis and higher order comparison goods bought

on a more occasional basis where customers generally shop around/window

shop e.g. adult clothes and footwear. The town centre has a duel higher and

lower order comparison shopping role, but the higher order comparison

shopping role is focused on lower middle and discount sectors of the market.

Barking & Dagenham : Economic Development Study

P46 6788302v3P46

The Barking Town Centre Study 2012 undertook a detailed gap analysis of

missing retailers. This benchmarked Barking town centre against other

comparable centres. The list of missing retailers included Clinton cards, British

Heart Foundation, Cancer Research UK, Clarks, Mothercare, Oxfam, Ryman,

the Body Shop, Marks & Spencer, Millets, Poundstretcher, Robert Dyas,

Savers, Waterstone’s, Age UK, Early Learning Centre, F Hinds, H Samuel,

Monsson, Next, The Works, Babygap, Dreams, M&Co, Primark, Store Twenty

One and Topshop.

These retailers are predominantly charity, discount or lower middle sector

retailers with some middle sector retailers. However the gap analysis suggests

there is future scope for Barking town centre to expand without a step change

in its market position, which is unlikely based on the town centre’s position in

the shopping hierarchy.

The gap analysis also identified Sainsbury’s who are now proposing a store at

Abbey Retail Park on the edge of the town centre.

Barking Street Market

The Council operates a street market in Barking Town Centre in partnership

with Charfleets Limited. It is held every week on Saturdays, Tuesdays and

Thursdays and Fridays. It is a traditional East London general market with a

multi-cultural theme. The market has up to 180 stalls which provide a good

range of products including clothing, household products, foods and hardware.

The market appears to be busy and vibrant. It is an important part of the town

centre’s attraction, and gives Barking added local distinctiveness. There is a

strong community feel within most parts of the market and it serves as a

focal/meeting point, as well as growing as attraction to many shoppers from

outside the local area.

Retail Rents

Prime Zone A retail rents in Barking declined between 2008 and 2009, from

£861 per sq.m to £700 per sq.m. Rents remained the same, at £700 per sq.m

in 2010 (source: Colliers International Retail Rents, 2010).

Service Uses

Barking has a good range of service uses with all the Goad categories being

present and well represented, and the split of service uses by category

generally reflects the national averages. The proportion of takeaways and

betting shops are higher than the national averages.

The gap analysis within the 2012 Barking Town Centre study identified 30 non-

comparison goods operators. Many of these were cafés, coffee shops or fast

food outlets (e.g. Costa, Burger King and Pizza), travel agents (Thomas Cook)

and Co-op travel), opticians and betting shops.

Barking & Dagenham : Economic Development Study

6788302v3 P47

Table B.3 Barking Analysis of Selected Service Uses

Type of Unit Barking % UK Average*

Units %

Restaurants/cafés 22 24.2 25.2

Takeaways 19 20.9 16.4

Banks/other financial services 13 14.3 14.0

Betting Shops/Casinos 7 7.7 4.3

Estate agents/valuers 6 6.6 10.3

Travel agents 2 2.2 2.7

Hairdressers/beauty parlours 21 23.1 24.8

Laundries/dry cleaners 1 1.0 2.4

Total 91 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Vacant Units

The vacancy rate in Barking is lower than the national average at 10.1%

compared to 12.1%. It should be noted that the vacant units includes shop

units on London Road that are part of the redevelopment proposals. A

significant proportion of the vacant units are located within the Vicarage Field

Shopping Centre, including the upper floor. The number of vacant units within

the pedestrianised section of East Street is relatively low. The overall vacancy

rate has returned to near pre-recession levels. The 10.1% vacancy rate is

probably not a true reflection of the health of the town centre.

Other Non-Retail Uses

Barking town centre has an excellent provision of non-retail uses including

leisure and community uses. These uses include: a library/learning centre,

council offices, health centres, sports/leisure centre, theatre, places of worship,

Travelodge hotel, nightclubs, snooker hall, kindergarten and citizens advice

bureau.

Shopper Views

When asked ‘what if anything would make you shop in Barking Town Centre

more often’ 68.4% of respondents made no suggestions of improvements

which could be made to the centre. 13.3% of respondents said a better choice

of shops in general and 3.8% responded better quality shops. 6.1% of

respondents replied more or better parking and 3.95% replied free parking.

The following comments; more food supermarkets, more large shops and

better maintenance/cleanliness were each suggested by 2.2% of respondents.

Accessibility

Barking town centre has excellent public transport accessibility. The station is

located in the heart of the town centre and is served by the District,

Barking & Dagenham : Economic Development Study

P48 6788302v3P48

Hammersmith & City lines), overland rail and 10 bus routes. The town centre

is also well connected to the road network with easy access to the A12, A13,

M25 and north circular. Less than 1% of household survey respondents

indicated that better bus or transport links would make them shop more often in

Barking town centre.

The town centre has a number of car parks, including London Road multi-

storey (650 spaces), Asda car park (330 spaces), Vicarage Field (200 spaces)

and Axe Street car park (200 spaces). Only 6% of household survey

respondents said more car parking would make them shop more often in

Barking town centre, and only 4% suggested cheaper car parking.

Environmental Quality

The environmental quality in the centre is mixed. Station Parade a linear route

with fairly heavy traffic flow, with HGVs regularly passing through the street.

As a result this shopping street has reduced pedestrian accessibility and safety

and reduced overall environmental quality due to noise and air pollution

associated with traffic.

Ripple Road, East Street and the Vicarage Field shopping centre are all highly

accessible for pedestrians. East Street is fully pedestrianized and hosts a

weekly street market selling a range of convenience and comparison goods.

The paving, street furniture and upkeep of some shop fronts in this part of the

centre however is poor which detracts from the quality of public realm.

Pedestrian access and safety has been improved along Ripple Road as a

result of recent traffic calming measures such as new pedestrian crossings and

on-road parking. The quality of public realm has been significantly upgraded as

a result of the development of new high quality, well designed modern

buildings and the implementation of street scene improvements including

planting, paving and seating. The Vicarage Field shopping centre offers a safe

and highly accessible shopping environment for pedestrians. The centre has a

number of vacancies and is occupied by many low quality retailers, this,

together with the aged internal fixtures and fittings in the centre significantly

reduces quality of the public realm.

The centre contains a wide range of buildings in terms of use and architectural

design. The most historic buildings are located along East Street and all

contain A1, A2, A3 and A5 uses. A number of new and retrofitted modern

buildings contain a wider range of uses including a new Travelodge hotel,

community learning centre, residential flats with ground floor commercial units,

a religious centre and theatre.

The centre has fully integrated and linked CCTV coverage and the

environment is safe and comfortable.

Barking & Dagenham : Economic Development Study

6788302v3 P49

Dagenham Heathway

Dagenham Heathway is a linear shopping centre which extends north to south

along the main shopping street ‘The Heathway’. It is defined as a district centre

which is centrally located to the South of the Borough surrounded by

residential areas. The centre has a good offer of retail and service uses as well

as complimentary community uses. Recently it has received a significant

amount of investment in new buildings such as the library and improvements to

landscaping and paving. The centre also functions as a transport hub;

Dagenham Heathway Station is located at the mid-point of the shopping

parade which is well served by local bus routes.

Dagenham Heathway’s key roles include:

• Convenience shopping: Lidl and Iceland provide the main supermarket

offer, located along the main shopping street the Heathway. The main

supermarket offer is supplemented by a broad range of small

independent food stores, butchers, bakers and fishmongers.

• Comparison shopping: a small number of national multiple retailers

selling a range of high and low order goods are located in the centre. The

comparison shopping offer is mainly made up of smaller independent

shops.

• Retail services: a fairly good selection of retail service units including a

national high street bank, estate agents, travel agents, cafes,

restaurants, beauticians and hairdressers.

• Community facilities: limited to the new library and a community police

unit.

Mix of Uses and Occupier Representation

Dagenham Heathway has a total of 113 retail/service uses. The diversity

measured by number of units is set out against the national average in Table

D.1.

Table D.1 Dagenham Heathway Use Class Mix by Unit

Type of Unit Units

% of Total Number of Units

% National Average (1)

Comparison Retail 34 30.0 36.0

Convenience Retail 16 14.2 8.1

A1 Services (2)

14 12.4 14.1

A2 Services 25 22.1 12.1

A3/A5 13 11.5 14.7

A4 Pubs/bars 1 0.9 2.9

Vacant 10 8.8 12.1

Total 113 100.0 100.0

Source: Goad Plans, updated by NLP November 2013

Notes: (1) UK average for all town centres surveyed by Goad Plans (March 2014) (2) incl. hairdressers, travel agents and other Class A1 uses not selling comparison/convenience goods

Barking & Dagenham : Economic Development Study

P50 6788302v3P50

Figure D.1 Goad Plan of Dagenham Heathway

Dagenham Heathway has a high proportion of Class A2 services, particularly

betting shops, estate agents and banks. Dagenham Heathway’s proportion of

comparison retail is significantly lower than the national average, whilst the

proportion of convenience shops is higher than average. The proportion of

vacant units is lower than average, which suggests that the health of the centre

is satisfactory in this respect.

Retailer Representation

Dagenham Heathway has a relatively small selection of comparison shops (34)

reflecting the centre’s primary role as a local shopping destination. There are

Barking & Dagenham : Economic Development Study

6788302v3 P51

five charity shops and eight main comparison multiples including Peacocks,

Wilkinson, Boots, JD Sports and Shoe Zone. Table D.2 provides a breakdown

of comparison shop uses by Goad categories.

The centre provides all of the main Goad comparison categories apart from

variety, department and catalogue, however the choice of shops within each

category is very limited with five or less in most categories. The centre has a

good provision of chemists and opticians.

Dagenham Heathway’s comparison shopping provides a mix of lower order

comparison goods purchased on a day to day basis and higher order

comparison goods, but the choice of shops is relatively limited.

Table D.2 Dagenham Heathway Breakdown of Comparison Units

Type of Unit Dagenham Heathway % UK Average*

Units %

Clothing and footwear 5 14.7 25.6

Furniture, carpets and textiles 2 5.9 8.3

Booksellers, arts, crafts and stationers 1 2.9 10.9

Electrical, gas, music and photography 2 5.9 9.5

DIY, hardware and homewares 3 8.8 6.2

China, glass, gifts and fancy goods 1 2.9 3.9

Cars, motorcycles and motor access 1 2.9 2.9

Chemists, drug stores and opticians 8 23.5 9.4

Variety, department and catalogue 0 0.0 1.4

Florists, nurserymen and seedsmen 1 2.9 2.2

Toys, hobby, cycle and sport 3 8.8 5.1

Jewellers 2 5.9 4.9

Other comparison retailers 5 14.7 9.7

Total 34 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

The proportion of clothing and footwear and booksellers, arts, crafts and

stationers units are all significantly lower than the national average.

Conversely the proportion of chemists, drug stores and opticians and ‘other’

comparison retailers including charity shops is higher than the national

average. This reflects the fact that the centre’s main role is for convenience

shopping and services. The centre does not perform well compared to national

averages in terms of variety of comparison units.

Service Uses

Dagenham Heathway has a good range of service uses with all the Goad

categories being present and well represented. The centre has low provision

of restaurants/cafés but a higher provision of takeaways. The proportion of

betting shops is nearly double the national average. Banks/other financial

services and estate agents is notably higher than the national average and

reflects Dagenham Heathway’s role as a local service centre.

Barking & Dagenham : Economic Development Study

P52 6788302v3P52

Table D.3 Dagenham Heathway Analysis of Selected Service Uses

Type of Unit Dagenham Heathway % UK Average*

Units %

Restaurants/cafés 5 10.2 25.2

Takeaways 8 16.3 16.4

Banks/other financial services 11 22.4 14.0

Betting Shops/Casinos 4 8.2 4.3

Estate agents/valuers 9 18.4 10.3

Travel agents 2 4.1 2.7

Hairdressers/beauty parlours 9 18.4 24.8

Laundries/dry cleaners 1 2.0 2.4

Total 49 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Vacant Units

There were 10 vacant units in Dagenham Heathway when NLP surveyed the

centre in November 2013. This gives the centre a vacancy rate of 8.8% which

is much lower than the national average at 12.1%.

Other Non-Retail Uses

Dagenham Heathway has a limited range of non-retail uses, including a library,

health and fitness club and post office. The library is an important asset in

terms of attracting customers to the centre.

Shopper Views

When asked what would make them shop more often in Dagenham Heathway,

63% of residents responded ‘nothing’ and 14.6% responded ‘don’t know’,

therefore overall 77.6% of residents did not suggest any improvements to the

centre. The most common suggestion was ‘a better choice of shops’ (10.5%)

and the second most common ‘a better choice of clothing shops’. No other

suggestion achieved more that 5%.

Accessibility

Dagenham Heathway has good public transport accessibility. The underground

station is located in the heart of the centre and provides east-west linkages via

the District line. The centre is served by 5 bus routes i.e. 3 north-south routes

and two east-west routes. The centre has excellent road connections to the

A13, M25 and north circular. Less than 1% of household survey respondents

indicated that better bus links would make them shop more often in Dagenham

Heathway. Less than 5% of household survey respondents said more car

parking would make them shop more often in the centre, and only 1%

suggested free or cheaper car parking.

Barking & Dagenham : Economic Development Study

6788302v3 P53

Environmental Quality

The majority of retail units along Dagenham Heathway occupy the ground floor

of post-war terraced properties. Some retail units to the north of the station

however occupy purpose built single storey built retail units. The recently

developed modern library building with residential units above located at the

junction at the southern end of the Heathway with associated public realm

improvements create an impressive gateway entrance to the shopping street.

Overall however quality of the built environment along the Heathway is poor

and many of the shop unit buildings appear to require maintenance.

Substantial public realm improvements extend along the Heathway to the north

and along adjoining streets: Parsoles Avenue to the west and Reede Road to

the east. These improvements, which include new planters, high quality

paving, lighting and cycle storage facilities, all significantly add to the quality of

the public realm. Recent traffic calming measures such as road narrowing have

improved pedestrian safety and accessibility although the roads still have

heavy traffic flows.

Barking & Dagenham : Economic Development Study

6788302v3 P55

Chadwell Heath

Chadwell Heath district centre is predominantly a linear shopping street

extending approximately 1 kilometre west to east along High Road. The centre

also incorporates the northern ends of Station Road and Wangey Road, where

they both join High Road. It is defined as a district centre and is located in the

far north of the Borough. The far western end of the centre overlaps into the

neighbouring LB of Redbridge.

The key roles of Chadwell Heath include:

• Convenience shopping: Sainsbury’s provides the main convenience

supermarket offer, in addition to Tesco Express. Convenience provision

is supported by a number of independent grocery stores, newsagents,

off-licences, bakeries and food specialists.

• Comparison shopping: Only one of the national multiple retailers is

present in the centre – Peacocks. The majority of comparison provision is

made up of small, independent businesses.

• Services: Provides a good range and choice of services including high

street banks, estate agents, hairdressers, cafes, restaurants, takeaways,

dry cleaners, launderettes and beauty parlours.

• Entertainment: Mecca Bingo hall in an old cinema building.

• Community facilities: Chadwell Heath Community Centre and a place

of worship.

Mix of Uses and Occupier Representation

Chadwell Heath has a total of 119 retail/service units. Table CH.1 sets out the

mix of uses in Chadwell Heath district centre, compared with the Goad national

average.

Table CH.1 Chadwell Heath Use Class Mix by Unit

Type of Unit Units

% of Total Number of Units

% National Average (1)

Comparison Retail 31 26.1 36.0

Convenience Retail 13 10.9 8.1

A1 Services (2)

23 19.3 14.1

A2 Services 18 15.1 12.1

A3/A5 23 19.3 14.7

A4 Pubs/Bars 4 3.4 2.9

Vacant 7 5.9 12.1

Total 119 100.0 100.0

Source: Goad Plans, updated by NLP November 2013

Notes: (1) UK average for all town centres surveyed by Goad Plans (March 2014) (2) incl. hairdressers, travel agents and other Class A1 uses not selling comparison/convenience goods

Barking & Dagenham : Economic Development Study

P56 6788302v3P56

Figure CH.1 Goad Plan of Chadwell Heath

The centre has a much lower proportion of comparison retail units when

compared against the national average, whilst the proportion of convenience

retail units is above the UK average. The proportion of retail service units is

Barking & Dagenham : Economic Development Study

6788302v3 P57

higher than the national average for all use types, due in part to the much

lower vacancy rate.

Retailer Representation

Chadwell Heath has a relatively small selection of comparison shops (31)

reflecting the centre’s primary role as a local shopping destination. A part from

four charity shops nearly all these shops are small independent traders.

Peacocks is the only major national comparison multiple. Table CH.2 provides

a breakdown of comparison shop uses by Goad categories.

The centre provides all of the main Goad comparison categories apart from

variety, department and catalogue, however the choice of shops within each

category is very limited with five or less in each.

Chadwell Heath’s comparison shopping offer is focuses on lower order

comparison goods purchased on a day to day basis e.g. pharmaceutical

products, cards, flowers, children’s clothes and small household items, rather

than higher order comparison goods bought on a more occasional basis where

customers generally shop around/window shop.

Table CH.2 Chadwell Heath Breakdown of Comparison Units

Type of Unit Chadwell Heath % UK Average*

Units %

Clothing and footwear 4 12.9 25.6

Furniture, carpets and textiles 2 6.5 8.3

Booksellers, arts, crafts and stationers 2 6.5 10.9

Electrical, gas, music and photography 2 6.5 9.5

DIY, hardware and homewares 2 6.5 6.2

China, glass, gifts and fancy goods 1 3.2 3.9

Cars, motorcycles and motor access 1 3.2 2.9

Chemists, drug stores and opticians 4 12.9 9.4

Variety, department and catalogue 0 0.0 1.4

Florists, nurserymen and seedsmen 1 3.2 2.2

Toys, hobby, cycle and sport 5 16.1 5.1

Jewellers 2 6.5 4.9

Other comparison retailers 5 16.1 9.7

Total 31 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Service Uses

Chadwell Heath has a very good range of service uses, with all but one of the

Goad categories (Travel agents) represented, as shown in Table CH.3. The

centre has a relatively high proportion of hairdressers/beauty parlours, estate

agents and launderettes/dry cleaners. The proportion of units within the banks/

other financial services, and restaurants/cafes/takeways categories is lower

than the UK average.

Barking & Dagenham : Economic Development Study

P58 6788302v3P58

Three high street banks (HSBC, Barclays and Natwest) are represented, but

none of the national restaurant and café operators are present.

Table CH.3 Analysis of Selected Service Uses

Type of Unit Chadwell Heath % UK Average*

Units %

Restaurants/cafés 9 15.8 25.2

Takeaways 14 24.6 16.4

Banks/other financial services 4 7.0 14.0

Betting Shops/Casinos 3 5.3 4.3

Estate agents/valuers 8 14.0 10.3

Travel agents 0 0.0 2.7

Hairdressers/beauty parlours 16 28.1 24.8

Laundries/dry cleaners 3 5.2 2.4

Total 57 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Vacant Units

The vacancy rate of Chadwell Heath is less than half the national average

which suggests the health of the centre in this respect is good. The main

cluster of vacant units is towards the extreme eastern end of the district centre,

near the junction with Whalebone Lane North.

Other Non-Retail Uses

Chadwell Heath a reasonable provision of non-retail uses, including a bingo

hall (in LB Redbridge), community centre, dentist, places of worship, post office

and educational institutions.

Shopper views

Respondents to the household survey were asked what, if anything would

make them shop more often in Chadwell Heath district centre. In the study

area as a whole 66.9% said ‘nothing’ would make them shop more often in

Chadwell Heath and a further 19.4% did not know, therefore 86.3% did not

suggest any improvements. Just under 6% stated a better choice of shops in

general, followed by 3.9% who would like to see more car parking. No other

answer achieved more than 2%.

Accessibility

Chadwell Heath has reasonable public transport accessibility. The over-ground

railway station is within a short walking distance of the High Road and provides

east-west linkages. The centre is served by 5 bus routes. The centre has good

road connections to the A12 and M25.

Chadwell Heath Station is on the Cross Rail route now under construction,

which will provide improved linkages and capacity to Central and West London,

Barking & Dagenham : Economic Development Study

6788302v3 P59

with completion expected in 2018. The Cross Rail will enhance the attraction of

the Chadwell Heath Station as a place to live and commute, which in turn

should have economic benefits for Chadwell Heath Centre. In total it is

estimated that Crossrail could help create £5.5 billion in added value to

residential and commercial real estate along its route between 2012 and 2021

(source: research for Crossrail by GVA).

Less than 1% of household survey respondents indicated that better

bus/transport links would make them shop more often in Chadwell Heath. Only

4% of household survey respondents said more car parking would make them

shop more often in the centre, and only 1% suggested free or cheaper car

parking.

Environmental Quality

The buildings to the east of Sainsbury’s in general were of a poorer quality to

those to the west. This could be down to the fact that the highest concentration

of vacant units was found at the eastern end. The majority of buildings are pre-

Second World War terraces, interspersed with semi-detached and terraced

housing. Towards the eastern end there have been a couple of very large

residential developments over the last decade, which has helped to improve

the environmental quality.

There is unique street lighting throughout the centre which improves the

environmental quality, as do the pavement benches. The centre is mainly

linear along the High Road, focused along the A118. This results in heavy

traffic flows through the centre which can impede pedestrian movements and

reduces the overall attractiveness of the centre. However, there are a number

of pedestrian crossings throughout the centre.

Barking & Dagenham : Economic Development Study

P60 6788302v3P60

Green Lane

Green Lane is a linear shopping street extending west to east. It is defined as a

district centre and is located in the north of the borough, straddling the

boundary with the LB of Redbridge. The centre has a variety of retail and

service uses and fulfils a local shopping role for shoppers from the surrounding

residential areas.

The key roles of Green Lane include:

• Convenience shopping: Tesco Express and The Co-operative Food are

the two main food store destinations. Convenience provision is supported

by a number of grocery stores, newsagents, an off-licence, bakery and a

food specialist;

• Comparison shopping: Only one of the national multiple retailers are

present on the street - Superdrug. The comparison provision is

overwhelmingly made up of small independent businesses that are

spread throughout the centre;

• Services: provides a good range and choice of services including high

street banks, estate agents, hairdressers, cafes, restaurants, takeaways,

dry cleaners, launderette and beauty parlours;

• Entertainment: amusement arcade;

• Community facilities: including a health club and a place of worship.

Mix of Uses and Occupier Representation

Green Lane has a total of 121 retail/service units. Table GL.1 sets out the mix

of uses in Green Lane district centre, compared with the Goad national

average.

Table GL.1 Green Lane Use Class Mix by Unit

Type of Unit Units

% of Total Number of Units

% National Average (1)

Comparison Retail 38 31.4 36.0

Convenience Retail 18 14.9 8.1

A1 Services (2)

18 14.9 14.1

A2 Services 12 9.9 12.1

A3/A5 17 14.0 14.7

A4 Pubs/Bar 1 0.8 2.9

Vacant 17 14.0 12.1

Total 121 100.0 100.0

Source: Goad Plans, updated by NLP November 2013

Notes: (1) UK average for all town centres surveyed by Goad Plans (March 2014) (2) incl. hairdressers, travel agents and other Class A1 uses not selling comparison/convenience goods

The centre has a significantly lower proportion of comparison retail units when

compared against the national average, whilst the proportion of convenience

Barking & Dagenham : Economic Development Study

6788302v3 P61

units is higher than average. The proportion of other non-retail service units is

broadly similar to the national average.

Green Lane is the only main centre in LBBD with a vacancy rate higher than

the national average.

Figure GL.1 Goad Plan of Green Lane

Barking & Dagenham : Economic Development Study

P62 6788302v3P62

Retailer Representation

Green Lane has a relatively small selection of comparison shops (38) reflecting

the centre’s primary role as a local shopping destination. Table GL.2 provides

a breakdown of comparison shop uses by Goad categories.

The centre has three charity shops and only two comparison multiples i.e.

Lloyds Pharmacy and Superdrug.

The centre provides all of the main Goad comparison categories apart from

variety/department/catalogue and China/glass/gifts/fancy goods, however the

choice of shops within each category is very limited with five or less in most

categories. The centre has a good provision of electrical shops.

The proportion of units in a large number of categories is notably different from

the UK averages. Furniture, carpets and textiles; electrical, gas, music and

photography; chemists, drug stores and opticians; toys, hobby, cycle and sport;

and ‘other’ comparison retailers are all above the national average. Similarly,

there are a number of categories in which the proportion of units within Green

Lane district centre is significantly lower than the national average, including

clothing and footwear; and booksellers, arts, crafts and stationers. Two

categories (china, glass, gifts and fancy goods; and variety, department and

catalogue) are not represented at all within the centre.

Table GL.2 Green Lane Breakdown of Comparison Units

Type of Unit Green Lane % UK Average*

Units %

Clothing and footwear 3 7.9 25.6

Furniture, carpets and textiles 5 13.2 8.3

Booksellers, arts, crafts and stationers 2 5.3 10.9

Electrical, gas, music and photography 7 18.4 9.5

DIY, hardware and homewares 2 5.3 6.2

China, glass, gifts and fancy goods 0 0.0 3.9

Cars, motorcycles and motor access 1 2.6 2.9

Chemists, drug stores and opticians 5 13.2 9.4

Variety, department and catalogue 0 0.0 1.4

Florists, nurserymen and seedsmen 2 5.3 2.2

Toys, hobby, cycle and sport 4 10.5 5.1

Jewellers 1 2.6 4.9

Other comparison retailers 6 15.8 9.7

Total 38 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Service Uses

Green Lane has a good range of service uses, with all but one category (travel

agents) represented, as shown in Table GL.3. The centre has a relatively low

proportion of banks and financial services; and a relatively high proportion of

hairdressers/beauty parlours, estate agents and laundries/dry cleaners.

Barking & Dagenham : Economic Development Study

6788302v3 P63

Two high street banks (Santander and Barclays) are represented, but none of

the national restaurant and café operators are present.

Table GL.3 Analysis of Selected Service Uses

Type of Unit Green Lane % UK Average*

Units %

Restaurants/cafés 5 11.4 25.2

Takeaways 12 27.3 16.4

Banks/other financial services 4 9.1 14.0

Betting Shops/Casinos 3 6.8 4.3

Estate agents/valuers 6 13.6 10.3

Travel agents 0 0.0 2.7

Hairdressers/beauty parlours 12 27.2 24.8

Laundries/dry cleaners 2 4.5 2.4

Total 44 100.0 100.0

Source: Goad Plans, updated by NLP November 2013 *UK average for all town centres surveyed by Goad Plans (March 2014)

Vacant Units

Green Lane district centre has 17 vacant units, a vacancy rate of 14%, which is

higher than the national average (12.1%). The main cluster is on both sides of

the road in the middle of the district centre between the junctions with Mayfield

Road and Dunkeld Road.

Other Non-Retail Uses

Green Lane has a limit range of non-retail uses. Facilities present include a

post office, dentist, Islamic Society hall, place of worship and a primary school.

Shopper Views

Respondents to the household survey were asked what, if anything would

make them shop more often in Green Lane district centre. In the study area as

a whole, 67.3% indicted nothing would make them shop more often in Green

Lane and 21% did not know, therefore 88% did not suggest any improvements.

A better choice of shops in general was mentioned by 4.7% of respondents,

followed by 4% indicating they would like to see more car parking. No other

answer achieved more than 2%.

Accessibility

Green Lane is less accessible by rail/underground than the other three main

centres, although Goodmayes and Chadwell Heath railway stations are within

walking distance. The centre is served by 4 bus routes. The centre has good

road connections to the A12 and M25.

Green Lane will be within walking distance of the Cross Rail route now under

construction, which will provide improved linkages to Central and West

London. Cross Rail will enhance the attraction of the Green Lane area as a

Barking & Dagenham : Economic Development Study

P64 6788302v3P64

place to live and commute, which in turn should have economic benefits for

Green Lane.

Less than 1% of household survey respondents indicated that better bus/ links

would make them shop more often in Green Lane. Only 4% of household

survey respondents said more car parking would make them shop more often

in the centre, and only 1% suggested free or cheaper car parking.

Environmental Quality

The buildings within the centre are mostly in a good and well maintained

condition. The buildings on either side of the road form a terrace of similar

design to most London High Streets. There are a few newer infill buildings,

scattered throughout. The most striking building on the street is the Church of

Pentecost-UK which is a completely different style to the rest of the buildings.

The centre is linear in nature, focused along the A1083. This means traffic

through the centre is moderate-heavy which can impede pedestrian

movements and reduces the overall attractiveness of the centre. However,

there are a number of pedestrian crossing which help to encourage

pedestrians to use both sides of the street.

The northern end of Goodmayes Park abuts the centre towards the western

end. This helps to improve the environment and reduce the congested feel of

the street.

Retail Warehouse and Leisure Parks

There are three retail warehouse parks and one leisure park within the

Borough. The role of these parks is set out below.

Abbey Retail Park

Abbey Retail Park is located on the edge of Barking town centre. It has

declined in recent years, due to company failures (e.g. Comet and MFI) and

the growth of retail warehouse operators at Beckton. Retail Parks at Beckton

Triangle, Galleons Reach, and Gateway Retail Parks in Newham have an

extensive provision of bulky goods retail warehouse operators, which serve the

Borough, particularly the south west and west of the Borough. Their

accessibility from Barking restricts retail warehouse operator demand for

premises in Barking.

The retail park is currently occupied by a large Dreams Clearance store and

Halfords. There are current proposals to redevelop the retail park to

accommodate a large Sainsbury’s food superstore.

Whalebone Lane Retail Park

This Retail Park is located in the north of the Borough to the east of Chadwell

Heath. It has also declined in recent years, due to company failures (e.g.

Barking & Dagenham : Economic Development Study

6788302v3 P65

Comet) and the closure of B&Q. A McDonald drive-thru remains on the site. An

Asda food superstore now has planning permission on the site.

Merrielands Crescent

Merrielands Crescent is located in the south the Borough on the A1306. This

park provides a good mix of bulky comparison goods retailing (totalling around

6,600 sq.m gross, including Homebase (DIY), Dreams (beds), Carpetright,

Topps Tiles and Halfords (motor accessories parts and cycles).

There are Asda and Aldi stores which attracts main and bulk food shopping

trips. The Dagenham Leisure Park is nearby, with leisure centre, bingo hall and

cinema. Together these uses provide a significant cluster of facilities that have

a wide draw. In addition to residents within the Borough, this location’s

excellent access via the A13 and A1306 enables these facilities to serve

residents within Tower Hamlets, Newham and Havering.

This retail park is relatively dated and there may be redevelopment potential in

the future to provide a higher quality shopping environment and more modern

accommodation for operators.

Dagenham Leisure Park

Dagenham Leisure is located in the south the Borough to the west of

Merrielands Crescent on the A13.The area provides a cluster of leisure and

entertainment uses anchored by a Vue multiplex cinema, Mecca bingo hall and

tenpin bowling (20 lanes) facility. These uses are supported by ancillary uses

including a drive thru McDonalds, two Class A3 uses and a nightclub. Sports

facilities are provided nearby at the Goresbrook Leisure Centre, sports pitches

and Goals football centre.

The leisure park is accessed via the A1306 but is poorly integrated with nearby

retail stores and public transport nodes in terms of pedestrian access. The

leisure park is predominantly a car borne destination.

Together these uses provide a significant cluster of facilities that have a wide

draw. In addition to residents within the Borough, this location’s excellent

access via the A13 and A1306 enables these facilities to serve residents within

Tower Hamlets, Newham and Havering.

Local Centres

The existing provision of local shopping centres within the Borough

(neighbourhood centres and parades) offers a balanced distribution of local

facilities serving local communities. These facilities complement the four main

centres and have an important role in serving the day-to-day needs in their

local areas.

In addition to the audit of the main centres in LBBD, we have undertaken a

local needs index of the neighbourhood centres and parades within the

Borough. Our analysis splits the centres into “large” (more than 45 commercial

Barking & Dagenham : Economic Development Study

P66 6788302v3P66

units), “medium” (between 16 and 44 commercial units) or “small” (15

commercial units or less).

The shopping centres, parades and clusters vary in size, from only four

commercial units (Movers Lane) to as large as 261 (Barking town centre). In

summary, LBBD contains:

• 14 centres classified as small;

• 16 centres classified as medium; and

• 6 centres classified as large.

The key focus in auditing local centres has been in assessing the “needs” of

local residents and to what extent each is meeting these “needs”. There is no

clear definition of need, but it is considered that residents could expect to find

some or all of the following shops, services and community uses within easy

walking distance of their home:

1 food or convenience store suitable for top-up shopping;

2 bank;

3 post office;

4 newsagent;

5 off licence;

6 chemist;

7 takeaway, café or restaurant;

8 public house;

9 bookmakers;

10 laundrette/dry cleaners;

11 hairdressers/beauty salon;

12 florist;

13 estate agents;

14 community hall;

15 doctor’s surgery; and

16 library.

Each local centre has been allocated a score out of 16, based on the number

of categories of shops and services listed above (one point per category

represented) that are available in the centre.

There is a wide range of scores across the centres. These scores are based

on the representation of key retail/service provision within the centre. The

larger town centres have the highest scores (10 or more on the local needs

index).

In addition to this it is important to consider the ability of these centres in

meeting top-up shopping needs. Therefore, the number of convenience stores

Barking & Dagenham : Economic Development Study

6788302v3 P67

with the ability to provide local top-up shopping (e.g. a grocers, local corner

shop or small supermarket) in the parade is also considered.

Barking town centre provides all of the identified categories of shops and

services, scoring 16 on the local needs index, which would suggest the local

residents of the this area are relatively well served by their local shopping

centre. By contrast, Winifred Parade, Reede Road, East Road, Althorne Way

and Movers Lane only attract a score of 3 or less on the local needs index,

which would suggest a very limited level of local needs being met.

Local Needs Index Summary

Centre Name Size of Centre

Total No. of units

Local Needs Index

No of conv. stores

No. of vacant units

Barking Large 261 16 15 27

Chadwell Heath Large 115 14 7 7

Green Lane Large 120 14 10 17

Dagenham Heathway Large 112 13 5 10

Owlow Road/Hunters Hall Medium 36 11 8 4

Faircross Parade Medium 35 11 10 2

Robin Hood NC Large 45 9 7 4

Martin’s Corner Medium 38 9 8 3

Five Elms Small 22 9 4 2

Whalebone Lane South Medium 36 8 3 4

Merry Fiddlers Medium 28 8 4 2

Broad Street Large 45 7 12 4

St. Andrews Corner Medium 30 7 7 2

Ripple Road Medium 27 7 4 3

Gale Street Medium 25 7 5 0

Lodge Avenue Medium 31 6 6 7

Dagenham East Medium 21 6 3 5

Rainham Road South Medium 18 6 3 5

Rose Lane Small 14 6 3 4

Goresbrook Road Medium 32 5 5 4

Fanshawe Avenue Medium 18 5 2 4

Farr Avenue Medium 17 5 5 7

Ripple Road Medium 16 5 4 1

Eastbrook NC Small 14 5 3 0

Upney Lane Small 10 5 2 1

Rush Green Small 7 5 1 0

Church Street Medium 25 4 3 8

Lodge Avenue Small 14 4 2 3

New Road Small 12 4 1 1

Stansgate Road Small 8 4 2 3

Gascoigne Road Small 8 4 2 4

Winifred Parade Small 12 3 2 2

Reede Road Small 11 3 2 3

East Road Small 7 3 1 3

Althorne Way Small 7 2 1 3

Movers Lane Small 4 1 1 2

Barking & Dagenham : Economic Development Study

P68 6788302v3P68

The local needs index is not a precise measure of whether a local shopping

centre is meeting the needs of local residents, as there are many other factors

to consider:

i the relative size a local parade will dictate the range of shops and

services each centre can offer;

ii the close proximity of other town centres, local centres and ‘stand alone’

shops means that local need may be met at an alternative location within

walking distance and local needs are therefore still being met;

iii the quality of the shopping centre or parade, in terms of its environment,

type and range of retailers will affect how it is perceived and used by

local residents; and

iv the relative accessibility of each centre will be an important factor in how

local people use the local shops and services. For example, a major

traffic route, which is difficult for pedestrians to cross, may influence

shopping patterns in the area.

It is considered that the local needs index provides a useful indicator of

whether a local centre or important local parade is meeting some or all the

needs of local residents.

The local centres and their respective scores are plotted on a plan overleaf. A

500 metres and 800 metres radius from each centre is also shown, which

represents what should be considered to be a reasonable and maximum

walking distance.

Barking & Dagenham : Economic Development Study

6788302v3 P69

Local Needs Index

Barking & Dagenham : Economic Development Study

6788302v3 P71

Appendix 11 Business Survey Results

Barking & Dagenham : Economic Development Study

6788302v3 P73

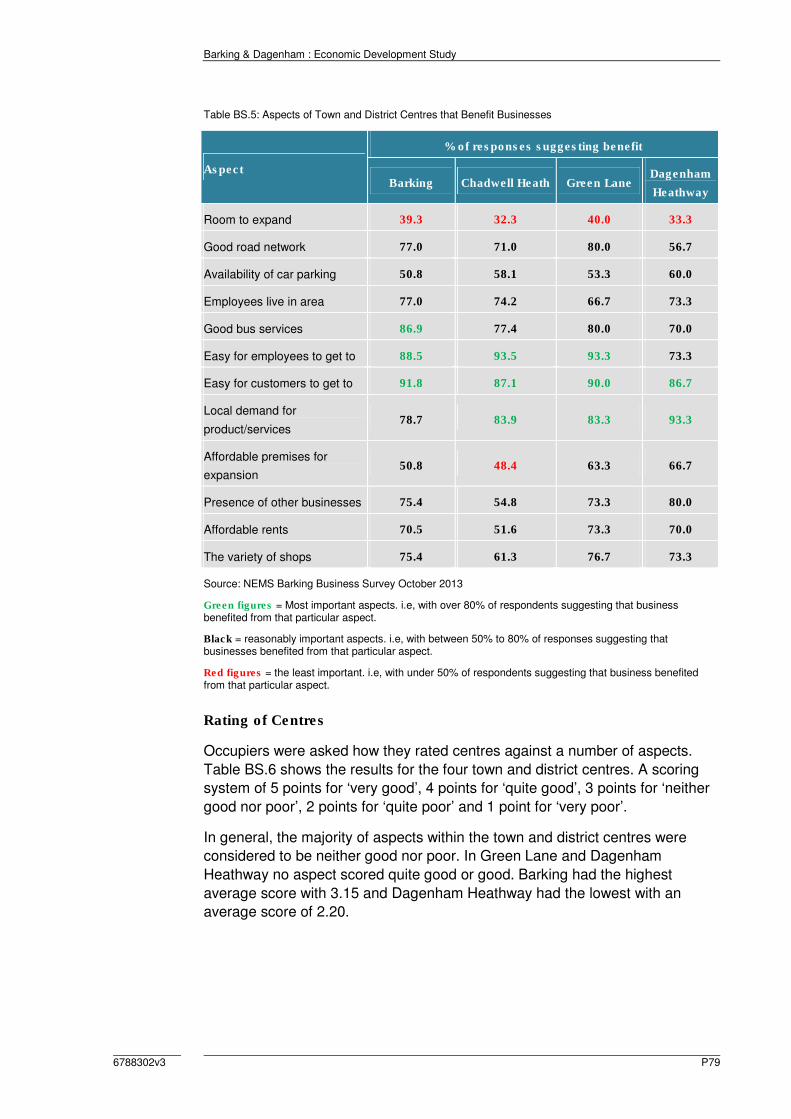

Business Occupier Perceptions

A survey of business occupiers was undertaken by NEMS in October 2013. In

total 152 businesses were interviewed in the London Borough of Barking and

Dagenham, and the number of interviews were broadly proportional to the size

of each centre. These were broken down as follows:

• Barking Town Centre 61 interviews;

• Chadwell Heath District Centre 31 interviews;

• Green Lane District Centre 30 interviews;

• Dagenham Heathway District Centre 30 interviews.

The occupiers were asked to give their views on a number of issues, including:

a Current and future trading performance;

b Future plans to improve or rationalise their premises;

c Which aspects of the town centre benefited businesses;

d What issues constrain the operation and performance of their business

and how these could be addressed;

e How important affordable rents and premises/business rates are to their

business;

f How the town centres were rated against a number of aspects, and;

g Opinions on town centre shopping and service mix.

Length of Trading in Current Location

Figure BS.1 shows the number of years businesses surveyed have been

trading in the borough. Just over half of businesses have been trading in

Barking and Dagenham for over ten years (51.4%), with the average length of

time 17 years, indicating that there are a substantial proportion of well

established businesses in the borough. This is typical of long established

shopping centres across the country.

Barking & Dagenham : Economic Development Study

P74 6788302v3P74

Figure BS.1: Length of Trading in Borough

Source: NEMS Barking Business Survey October 2013

Legal Status of Businesses

The legal status of the businesses surveyed is summarised in Figure BS.2.

The highest proportion of occupiers in LBBD were private limited companies

(49%). 27% of businesses are sole proprietorships and 16% are public limited

companies.

Figure BS.2: Legal Status of Businesses

Source: NEMS Barking Business Survey October 2013

Future Property Requirements

Businesses were asked what current plans, if any, they had to change their

business premises. The majority of occupiers in all the centres appeared to be

content with their existing premises, with an average of 80.9% having no plans

to change. A low number of businesses (4.6%) are intending to close or

7.2%

27.0%

13.2%

31.6%

14.5%

5.3%

1.3%

0%

5%

10%

15%

20%

25%

30%

35%

Less than

1 year

1 to 5

years

6 to 10

years

Over 10

years

Over 25

years

Over 50

years

Don’t

know

27%

4%

49%

16%

1%

3%

A sole Proprietorship

A Partnership

A private limited company

A public limited company

A co-operative/social

enterprise

Don’t know/no answer

Barking & Dagenham : Economic Development Study

6788302v3 P75

relocate to new premises outside the local area. There was a big variation

across the borough in the numbers of businesses looking to re-fit, extend or

improve their premises. 13.3% in Green Lane intend to improve premises,

whereas only 3.2 and 3.3% intend to do the same in Chadwell Heath and

Barking.

Trading Performance

Businesses were asked to describe their current trading performance and

performance over the last 12 months, as shown in Table BS.1. A scoring

system of 3 points for ‘good’ trading, 2 points for ‘stay the same’ and 1 point for

a ‘decline’ in trading is used to calculate an average.

Table BS.1: Last 12 Month Trading Period

Centre

Performance (% of respondents in each centre) Average

Score

(3 to 1) Good (3)

Stayed the

same (2) Declined (1)

Don’t know /

Refused

Barking 39.3 24.6 32.8 4.0 2.07

Chadwell

Heath 32.3 25.8 38.7 3.2 1.93

Green Lane 33.3 36.7 23.3 6.6 2.11

Dagenham

Heathway 23.3 30.0 43.3 3.3 1.79

Source: NEMS Barking Business Survey October 2013

(Average score based on 3 for good, 2 for stayed the same and 1 for declined)

The highest proportion of the occupiers in Chadwell Heath and Dagenham

Heathway felt that trading had declined over the last 12 months. In Green Lane

the highest proportion considered performance had stayed the same, while in

Barking almost 40% of businesses considered business had improved over the

12 month period to October 2013.

Opinions on expected future trading performance are summarised in Table

BS.2. The majority of businesses expected trading to improve over the next 12

months, and all centres received an average score above 2. 70% of

respondents in Barking expect trading to improve, and under 10% expect it to

decline. Very similar margins are recorded in Chadwell Heath and Green Lane.

Dagenham Heathway is the only centre where less than 50% of business

expected trading performance to improve.

Barking & Dagenham : Economic Development Study

P76 6788302v3P76