behavioural finance and financial markets: micro, macro, and corporate

TRANSCRIPT

UNIVERSITÀ POLITECNICA DELLE MARCHE

FACOLTÀ DI ECONOMIA ____________________________________________________________________________________

Dottorato di Ricerca in Mercati Finanziari e Assicurativi XI° Ciclo PhD in Financial and Insurance Markets

Tesi di Dottorato

Behavioural Finance and Financial Markets:

Micro, Macro, and Corporate

Coordinatore: Dottorando:

Prof. GianMario Raggetti Fergus McGuckian

Anno Accademico 2012/2013

i

Abstract

This thesis consists of four chapters that explore different aspects of the relationship between

behavioural finance, financial decisions and financial markets. Behavioural finance has emerged as a

multidisciplinary research approach which addresses the impact of psychology on individual choice

behaviour and financial decisions, and the subsequent implications for financial markets. The

behavioural models posited build upon classical economic theories to develop alternative approaches

to financial problems, by applying concepts from psychology to create an open-minded line of

scientific enquiry that is more flexible in its assumptions. The conceptualisation of homo

oeconomicus, i.e. the always rational economic man, is refuted in behavioural finance: people are

thought to often behave irrationally, due to the fact that when confronted with a range of alternatives,

they do not always select the choice associated with the optimum payoff, and secondly, because they

regularly fail to make utility maximising decisions in reality. Indeed, behavioural finance has emerged

to be much more than a peripheral way to deliberate financial markets. Over last two decades, the

discipline has provided many fascinating insights about economic agents, and these new notions have

aided the advancement of understanding of both individual level financial decisions, and of macro

level financial market dynamics.

The thesis is structured as follows. The introductory chapter discusses the development of the

academic area, and outlines the context of the thesis. The foundations of both traditional and

behavioural finance are compared and contrasted. Chapter two investigates the micro-level

foundations of behavioural finance, with specific regard to the individual investor. Of particular

interest is research about cognitive heuristics and behavioural biases in financial decision making, and

whether or not measures can be taken to reduce mental errors of this nature. The professional

application of behavioural finance findings to modern portfolio theory, to consumer finance, and also

within the financial advisor/retail investor relationship about decisions pertaining to asset allocation,

buying, selling, borrowing, and saving is deliberated, and a framework for testing and categorising

investors according to their personality is proposed. The research in chapter 3 investigates financial

anomalies, macro behavioural finance, and market efficiency. The study adds to the theoretical debate

and examines whether financial markets are affected by mood variables, and if so, if this is reflected in

asset prices. The final essay discusses a focal corporate finance area, the Initial Public Offering, in the

institutional context of the Italian Stock Exchange from a uniquely behavioural perspective. It is

contended that the primary influence on security prices is emotion, not reason, in that market

sentiment rather than fundamental factors is the biggest explanatory factor in IPO share price

performance.

ii

Table of Contents

Chapter 1. Introduction to Behavioural Finance 1. Origins and Evolution ........................................................................................................................ 1

1.1. Theoretical Pillars of Traditional Finance ............................................................................... 2 1.2. Theoretical Pillars of Behavioural Finance ............................................................................. 7

1.2.1. Psychology and Finance: Social Science Divisions .......................................................... 9 1.2.2. Prospect Theory as a Foundation .................................................................................... 10

2. Shifting Paradigm and the Philosophy of Science ........................................................................... 13 3. Discussion ........................................................................................................................................ 16 4. Bibliography .................................................................................................................................... 18

Chapter 2. BF Micro: Individual level 1. Introduction ..................................................................................................................................... 21 2. The Behavioural Biases which affect Financial Decisions ............................................................. 22

2.1. Financial decision making ..................................................................................................... 22 2.2. Decision heuristics and Cognitive Biases .............................................................................. 24 2.3. Investment Heuristics and Biases ......................................................................................... 27

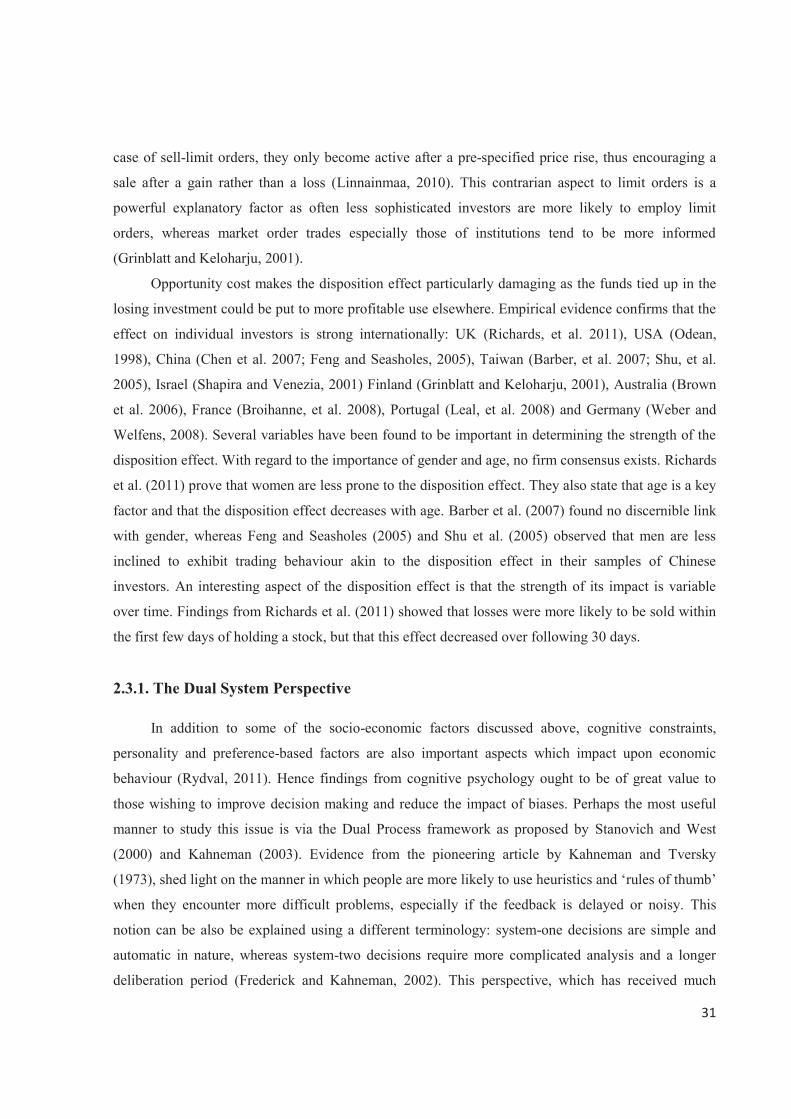

2.3.1. The Dual System Perspective.......................................................................................... 31 2.3.2. Cognitive Load, Capacity and Overload ......................................................................... 34

3. Applied Micro BF ............................................................................................................................ 36 3.1. The Integration of BF into Financial Advice ........................................................................... 37

3.1.1. Bias Blind Spot ............................................................................................................... 38 3.1.2. Caveat Emptor: Let the Buyer Beware ........................................................................... 39

3.2. Practical Steps: can biases be debiased? ................................................................................. 40 3.3. Behavioural Finance and Portfolio Management ................................................................... 49

3.3.1. Behaviouralised Portfolio Theories ................................................................................. 52 3.3.2. How to Measure Risk ...................................................................................................... 54 3.3.3. Risk Tolerance Profiling ................................................................................................. 55

4. Financial Personality ....................................................................................................................... 57 4.1. Personality Profiling ............................................................................................................... 58

4.1.1. Psychological Tests ......................................................................................................... 60 4.1.2. Investor Categorisation Framework ................................................................................ 61

5. Discussion ........................................................................................................................................ 65 6. Bibliography ................................................................................................................................... 67

iii

Chapter 3. BF Macro: Market Level 1. Anomalies in Finance ...................................................................................................................... 73

1.1. What determines Asset Prices? ................................................................................................ 75 1.2. Financial Anomalies ................................................................................................................ 76

1.2.1. Fundamental Anomalies ................................................................................................. 76 1.2.2. Technical Anomalies ....................................................................................................... 78 1.2.3. Calendar Anomalies ........................................................................................................ 78 1.2.4. Mood Variables ............................................................................................................... 79

1.3. Anomaly Explanations ............................................................................................................. 81 2. Friday the 17th .................................................................................................................................. 82

2.1. Data and Research Hypothesis ................................................................................................ 84 2.2. Results ...................................................................................................................................... 85

3. Discussion and Concluding Remarks .............................................................................................. 92 4. Appendices ...................................................................................................................................... 96 5. Bibliography ................................................................................................................................. 100

Chapter 4. BF Corporate: Italian IPO Market 2000-2010 1. Introduction and Paper Scope ........................................................................................................ 105 2. Italian Institutional Context and Background ................................................................................ 108

2.1. Going Public in Italy .............................................................................................................. 110 3. Literature Review of the Main IPO Puzzles .................................................................................. 115

3.1. Positive Initial Returns and Under-Pricing ............................................................................ 115 3.2. IPOs and Market Timing ....................................................................................................... 120 3.3. Long-run underperformance of IPOs ..................................................................................... 121 3.4. Book-building and Price Range ............................................................................................. 123 3.5. Behavioural Explanations ...................................................................................................... 125 3.6. Market Sentiment ................................................................................................................... 128

4. Hypothesis Development ............................................................................................................... 132 5. Research Design ............................................................................................................................ 134

5.1. Data Sample ........................................................................................................................... 134 5.2. Empirical analysis .................................................................................................................. 135

6. Model Set-Up ................................................................................................................................ 158 6.1. Regression Analysis ............................................................................................................... 158 6.2. Market Survey Data Indices vs. IPO Performance ................................................................ 168

7. Discussion of Results ..................................................................................................................... 172 8. Final Remarks ................................................................................................................................ 178 9. Appendices .................................................................................................................................... 181 10. Bibliography .................................................................................................................................. 183

1

Chapter 1. Introduction to Behavioural Finance

1. Origins and Evolution

Financial economics, the dynamics of international markets, and the operation of agents therein

(individuals as well as firms), are topics which are ultimately scrutinised differently by various people.

Over the past 20 years or so an important debate has been on-going between ‘rationalists’ who assume that

economic agents behave rationally, against ‘behaviourists’, who assume that they behave in systematically

irrational ways. There is a certainly plethora of alternative views, with many of these advocating a more

psychologically realistic stance in economics and currently we are in a transition phase between two

paradigms (Stiglitz, 2010). Theories developed by researchers in traditional or classical finance tend to

accept as valid that decisions are a maximisation of objective functions subject to individual budgetary

constraints, and that investors only evaluate risk and expected returns when making investment decisions.

Indeed, standard approaches in financial economics make few assumptions about agents’ psychology, and

typically this has been considered as a great strength.

To supporters of behavioural finance, the role of human conduct in modelling markets is of

fundamental importance, and there is thought to be an innate relationship between the two. It is felt that

contemporary economics seriously under-values and ignores, the importance of emotions, whereas it holds

in high esteem the orderly mathematical models which emphasise the full rationality of decision makers.

The behaviourists consider the rational model to be an unrealistic precept for human judgment. These

people believe that the phrase behavioural finance – the most widely made definition of which, is that it is

fundamentally the application of psychology to understand human behaviour in finance or investing –

itself is a pleonastic expression; finance is inherently behavioural in nature (pleonasm: “the use of more

words than are necessary to express an idea”, Oxford English Dictionary).1 As of late, and in an ever

increasing manner, other disciplines such as psychology have become more included into economics in

pursuit of new and more realistic theories.2 A wider range of factors and subjective elements, which are

important to the financial decision making process of households and the aggregate dynamics of financial

markets, are taken into account by these people (such as psychological, social, and emotional factors,

beliefs, demographic traits, internal factors such as neural processes, cognitive ability, mood states, and

environmental factors like information sources, fashions/fads, social networks, crowd psychology herding,

information cascades, person-to-person, social learning and media contagion of sentiment/behaviour).

1 Behavioural finance is analogous to the phrase ‘wet water’ – it is implicitly known that the water is wet. 2 This has mostly occurred because it is thought by many that evaluating real world economic behaviour without including the findings of psychology is like dealing with quantitative relationships without using readily available techniques of mathematics (Schwartz, 2007).

2

These factors lead economic agents to depart from the rational behaviour that is presumed by traditional

economists and that many of the economic decisions and responses which happen in daily life are not

accurately depicted or accounted for in traditional economic models.

A main contention is that economics has become too theoretical and is not descriptive enough of the

world around us. Subsequently it is thought that theoretical models in finance should be verified against

the actual experimental evidence, i.e. financial data; this necessitates that economists employ more of a

bottom up approach, whereby cognitive and emotional states are taken into consideration when

developing models of human behaviour and decision models for individuals in the real world. This

perspective develops a fundamentally new and important way to understand financial markets and the

behaviour seen in them. Behavioural finance models argue that there are more intrinsically important

factors in the decision making process, pertaining to how we should invest, value assets and adjust for

risk. Psychologically based assumptions, which emanate from individual/collective psychology and

decision making research, are more descriptive and it is thought that a larger variety of factors introduce

distortions and prevent rational financial decision making from taking place on an aggregate scale. In

short, behavioural finance is the study of the influence of psychology on the behaviour of economic agents

and the subsequent effects of this behaviour on financial markets (Sewell, 2007). To make any

comparisons and to understand what behavioural finance is, we should first discuss the main concepts of

classical finance

1.1. Theoretical Pillars of Traditional Finance

“It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest”, (Adam Smith, 1776; Book One, Chapter Two)

From the very beginning of modern economic writing by the likes of Adam Smith and David

Ricardo in the 1700s and to later work by John Stuart Mill in the 1800s, the concept of the rational

economic agent or homo oeconomicus, he who is motivated by self-interest and seeks to maximise his

own utility (wealth) in decisions for the lowest possible expenditure of work/labour, has been a central

tenet to understanding the economic system in which we live in. The rational economic man is the

theoretical backbone or according to the economist F.Y. Edgeworth “the first principle of economics is

that every agent is actuated only by self-interest” (1881; p.16). In addition to this however, as a formal

discipline since the 1940s economics has been mostly free of psychological notions; economic agents are

considered to be utility optimisers. Influential economists trained in mathematics such as Paul Samuelson

(1938) John Hicks (1939) and Lionel Robbins (1952) where advocates of this approach for the simple

reason that for the discipline to be initially accepted, it needed to supply empirical evidence without the

3

complications of actual human action.3 Perhaps the main reason for this early development was that

traditional models, with rational and unemotional economic agents, were easier to build (Thaler, 2000).

In truth economics has always attempted to explain economic behaviour and how people choose

under scarcity and at the centre of the traditional mainstream paradigm – and also by association modern

financial economics – lays this assumption of rationality and the belief that agents manage any quantity of

information they receive according to Bayes rule.4 Finance studies decision making under uncertainty and

asks the question of how an individual should choose when faced with uncertain outcomes. To examine

the financial decision making process traditional models have utilised concepts such as conditional

probabilities and the goal of optimisation. When confronted with a choice, the rational agent assesses the

probability and determines the utility payoff of each potential outcome; the option chosen has the optimal

combination of these two factors. In addition, people are thought to be selfish and only interested in their

own welfare (utility function maximisation), to have complete access to all available information, to be

well informed and to possess sufficient reasoning ability to solve complex problems (Schwartz, 2007).

Actually, economists have needed to assume that human behaviour is both rational and predictable so that

economic decisions could be mapped mathematically. Classically trained economists have often employed

thinking from this positivist view, emanating from falsification and instrumentalism advocated by the

likes of Popper and Friedman; specifically that research should use logic in the development of testable

theories, whilst typically avoiding analysis of the realism of the assumptions underpinning their scientific

inquiry (Whalley, 2004). To this end most of the theoretical constructs within modern economics employ

the concept of rationality to some degree or other, in that market participants make balanced

decisions/choices to maximise personal utility based on the best available information.5 From this

scientific worldview, people are thought to make financial decisions based on logical reason, not emotion,

and individuals are deemed to make decisions and behave in a rational manner. Classical economists

believe that theories that are not laden thick with numerical workings, and don’t lend credence to standard

finance assumptions, are considered less academically robust and to a certain degree less relevant.6

Historically, economic constructs have often depicted a stylised representation of the real world in order to 3 According to Slutsky (1915; p.27), “...if we wish to place economic science upon a solid basis, we must make it completely independent of psychological assumptions”. 4 The reference here is an article from the Economist published in 2000 which gives an introduction to Bayes Theorem and probabilities in decision making, available at: www.economist.com/PrinterFriendly.cfm?Story_ID=382968 5 According to List and Haigh (2005), who cite Schoemaker (1982), expected utility or EU theory still endures as the prevailing approach for modelling risky decision-making. In fact, it has been the main decision making paradigm for the last 70 years, being used “predictively in economics and finance, prescriptively in management science, and descriptively in psychology decision making” (p.945). 6 Stanovich (1999) refers to this group as “Panglossians” in homage to a protagonist character in Voltaire’s “Candide”.

4

assemble meaningful and useful hypotheses. It is true to say that since it is not easy to quantify factors –

such as emotion and human thoughts – traditional economic research has usually ignored such influences.

Traditionally, the belief was held that every individual within the free market economic system will

consider all of the information available an act on this to maximise their own utility.

A prime example of an important traditional finance theory is the Efficient Market Hypothesis

(EMH)7 developed by Eugene Fama (1965 and 1970). In this preeminent model, several simplifying

assumptions are made regarding both market conditions and also about the nature of participants within

them. Firstly, markets are assumed to be rational and that rational investors always have the goal of ‘utility

maximisation’. Firstly, this assumption requires that investors always act in an unbiased manner:

expectations of the future are formed and given these expectations, they buy and sell in the securities

markets at prices which they believe will maximise the future value of their portfolios and their wealth

(Fuller, 1998). Secondly, financial market prices are public information and no market frictions are

assumed to exist, i.e. entry into security markets is unlimitedly easy and accessible, and transaction costs

are zero. Under such conditions, security prices equal ‘fundamental values’ whereby they are ‘correct’ in

the sense that all public information has been incorporated into their formation. No free lunches are said to

exist and no investment strategy can consistently earn excess risk adjusted average returns; in other words

investment returns should in theory always reflect the precise amount of compensation for accepting risk

and delaying expenditure. From the behavioural finance standpoint however, although useful as an

abstract tool for analysis, the EMH is widely considered to be largely inaccurate in the context of being

able to describe price movements in world financial markets.8 In other words, markets do not fully reflect

all publicly available information (they are often informationally inefficient) and markets do not perfectly

price assets correctly at all times: this is partly due to the fact that investors given their own specific

preferences and other constraints, are not unfailingly rational utility maximisers.

Another cornerstone of traditional finance is The Law of One Price, which is a key principle on

which some very important finance theories are based upon – for example the Modigliani-Miller capital

structure propositions, the Black-Scholes option pricing formula and the arbitrage pricing theory – Lamont

and Thaler (2003: p.192) stipulate that the Law of One Price is “...the basis of almost all modern financial

theory, including option pricing and corporate capital structure”. Relating to capital markets, the Law

says that identical securities (that is, securities with identical state-specific payoffs) must have identical 7 The efficient markets model can be stated as asserting that the price Pt of a share (or of a portfolio of shares representing an index) equals the mathematical expectation, conditional on all information available at the time, of the present value P*t of actual subsequent dividends accruing to that share (or portfolio of shares). P*t is not known at time t and has to be forecasted. Efficient markets say that price equals the optimal forecast of it (Shiller, 2005). 8 The counter argument to this, as Friedman (1953) has argued, is based upon the idea that all useful theories rely on unrealistic assumptions because they seek simplicity.

5

prices otherwise smart investors could make unlimited profits by buying the cheap one and selling the

expensive one. So in effect there should be an absence of arbitrage opportunities. However, often this

stylised outcome does not play out so seamlessly in actuality.9

One more centrally important theory to modern finance is the CAPM – developed by Sharpe (1964)

and Lintner (1965) – which suggests the relationship between risk and return. The mathematical finance

algorithm proposed in this model is an integral part of the Modern Portfolio Theory of investment (MPT),

which is widely used in portfolio asset allocation to obtain the required compensation for risk. Basically,

the equation prices assets and determines expected returns. Every investor has one single unified

motivation and that is to maximise portfolio value for a given amount of risk. The simple example of a

Two-Asset Portfolio, depicted in figure 1, involves weightings, rates of return, and risk to incorporate the

mathematical formulation of the concept of diversification to investing:

Figure 1: Two Asset Portfolio

E(RP) = w1R1+w2R2

σp = √w12σ1

2 w22σ2

2 +2w1w2σ1σ2ρ1,2

CAPM: E(Ri) = Rf + βi(E(Rm) – Rf

It is true that the majority of economic agents favour a reward now more than a reward in the

future, as the world is uncertain and we don’t know what is going to happen in the future. However it is

widely known that the conditions needed for this model to function properly are too abstract, simplifying,

and unrealistic to be analogous of the real world: in the world of finance, investors cannot actually borrow

all they want at the risk free rate (they have limited borrowing capacity) and they cannot sell- short

without limit. According to the model, investors put all their assets in one portfolio and investors are

always seen as risk averse. What’s more, this theory, and many of the other most prominent models in

financial economics, employ the ceteris paribus (‘all else being equal’) clause in their assumptions. In

other words it is as if the theories stand in a vacuum – as Harry Markowitz himself has stressed (2005;

p.28): “The CAPM is like studying the motion of objects on earth under the assumption that the earth has

no air”. These theories are all primarily based upon the Von Neumann-Morgenstern Expected Utility

framework (EU) – investors evaluate choices and gambles according to this model, and if preferences

9 One example pertains to closed-end funds, where prices and net asset values (NAV) can vary across funds and across times with both discounts and premia of greater than 30 per cent commonly observed; mispricing can persist for long periods. Another example relates to Royal Dutch/Shell which is a merged company that trades on two exchanges as ‘twin shares’. Royal Dutch/Shell is strictly speaking only one firm, and according to the merger contract, the ratio of market value of the Royal Dutch to the market value of Shell should be 1.5 – however this ratio often varies considerably sometimes being too low by as much as 30% in 1981, to sometimes being too bloated, 15 % excessive in 1996 (Lamont and Thaler, 2003).

6

satisfy a number of plausible axioms, namely completeness, transitivity, continuity and independence,

they can be represented by the expectation of a utility function. Most models of asset pricing employ the

rational expectations equilibrium framework (REE), which sequentially means that individual rationality

and consistent beliefs is assumed (agents are thought to process new information correctly).

Fundamentally, the utility function (see Bernoulli, 1738; Von Neumann and Morgenstern, 1944) is a

particular mathematical expression informing about the preference an economic agent shows about

different choice alternatives.10 The utility of a lottery event is given by the average of the utility values of

possible outcomes weighted by their probabilities. Furthermore, the economic theory of choices states that

all choices are basically economic decisions and an investor chooses among the different opportunities by

specifying a series of curves (called utility functions or indifference curves). So, given an opportunity set

and trade-off between the different options an investor can choose among, the preferences the investors

exhibit for the different alternatives allow the building of a set of indifference curves informing about the

investor’s degree of risk aversion (Elton and Gruber, 1995). Figure 2 illustrates the utility of wealth (Max

∑ prob, Ui), which when looked at another way, is basically the psychological response to wealth. At time

t, agents are typically assumed to maximise: . Where U(cs) is the instantaneous

utility of consumption at time s, and b is a constant discount factor (source: Stracca, 2004). If future

consumption is unknown, agents maximize the expectation of the last equation using either the ‘objective’

(or ‘true’) probability distribution for cs, which they are assumed to know (expected utility, EU), or

subjective probabilities (subjective expected utility, SEU): .

Figure 2: The Utility of Wealth

(Source: Elton and Gruber, 1995)

10 Another important paper by Savage (1954) later expanded on the Von Neumann and Morgensten expected utility model by giving it axiomatic foundations.

7

1.2. Theoretical Pillars of Behavioural Finance

"Even apart from the instability due to speculation, there is the instability due to the characteristic of human nature that a large proportion of our positive activities depend on spontaneous optimism rather than mathematical expectations, whether moral or hedonistic or economic. Most, probably, of our decisions to do something positive, the full consequences of which will be drawn out over many days to come, can only be taken as the result of animal spirits – a spontaneous urge to action rather than inaction, and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities."…“A conventional valuation which is established as the outcome of the mass psychology of a large number of ignorant individuals is liable to change violently as a result of the sudden fluctuation of opinion due to factors which do not really make much difference to the prospective yield; since there will be no strong roots of conviction to hold it steady.” (John M. Keynes, 1936; p.154 and pp.161-162).

These quotes from the seminal work of J.M Keynes, draw attention to a main element of the

behavioural finance doctrine – that ‘animal spirits’, instinct and feeling, are often the most important

drivers in the financial decision making process, financial markets and the economy as a whole. Humans

are emotional creatures and they are cognitively susceptible to a wide range of factors. When a deliberate

action is made (whether it be in stock trading, buying or selling, deciding to spend/save/borrow, the asset

allocation process, real estate market transactions, or futures trading etc.) an internal decision process must

be employed. Additionally it is inherently true that these decision processes cannot be reduced to a series

of mathematical equations: the human condition is much more complex and sporadic in nature. At the

same time, memory and learnt experience may not be fully exploited either. This along with frequent

irrational behaviour, and the existence of systemic errors in judgment and problems in the way all humans

try to recall information, when aggregated across investor groups and world markets, can lead to a range

of inefficient outcomes and systemic mispricing in financial markets. These occurrences are unexplainable

utilising thinking from the ‘modern’ financial economics paradigm.

Some argue that the origins of BF can be traced back to the Friedman and Savage (1948) paper

which discussed why someone might purchase insurance and a lottery ticket concurrently – someone

could be risk-loving and risk-averse at the same time – although most agree that the foundations of BF be

followed back to the concept of bounded rationality11 which asserts that: “…decision makers and their

politics are rational: that is, they are goal orientated and adaptive, but because of human cognitive and

emotional architecture, they sometimes fail occasionally in important decisions” (Jones, p.297). In other

words, this basically means that people attempt to act rationally but they have limitations in terms of the

information they possess (partial expectations and incomplete knowledge of possible outcomes), the

cognitive limitations of their minds, and the finite amount of time they have to make decisions. Herbert

11 The term bounded rationality was first coined by Herbert Simon in the 1950s. See for example the article published in 1955, “A Behavioural Model of Rational Choice” which appeared in the Quarterly Journal of Economics, Vol. 69.

8

Simon in 1955 contended that economic agents, as opposed to always being optimisers on the other hand

often seek to satisfice: survival is seen as the key driver of behaviour. Simon rejected the concept of full

rationality; he stated that individuals reason and choose rationally, but that this is done under the

constraints imposed by their own limited search and mental computation abilities. Decision-makers do not

possess the resources or aptitude to reach optimal solutions; instead they only employ their rationality

after having substantially simplified the available choices. This is in contrast to the mainstream economics

assumption of maximisation, which as Simon thought, can lead to behaviour which is overly risk taking in

nature and can lead to a failure to survive.

More recently however, the field of behavioural economics/finance first started in a more formal

way around the mid-1980s by way of the Russell Sage Foundation which acted as a sponsor for research

(Sent, 2004). Later the field began to formulate in a more recognised way in the 1990s with the formation

of the Behavioural Economics Roundtable which was made up of the most prominent researchers

including the like of Kahneman, Tversky, Thaler, Camerer, Loewenstein, Rabin, and Laibson. Since then

BF has gathered further momentum with increasing research contributions and academic articles in the

2000s. Over the last 15 years there has been a marked increase in the amount of economists, and social

scientists, who are investigating ways in which the traditional vision of humans as rational decision

makers can be adapted to bring in irrational elements.

Behavioural Finance contrasts to traditional finance at a fundamental in that it departs from the REE

approach by relaxing the postulation of individual rationality (EU may be a good approximation to how

people evaluate a risky gamble, such as stock market investing, but it doesn’t explain attitudes to the kinds

of gambles studied in experimental settings).12 After all as Park and Zak contend, “Underneath its

mathematical sophistication, economics is fundamentally the study of human behaviour” (2007; p.47).

Traditionally speaking in economics, understanding this behaviour begins from the basic assumption that

agents have objectives and always chooses the most optimal or correct way to accomplish them (this is

more or less what economists mean they use the term ‘rationality’). However, empirical observations have

demonstrated that the rational choice theory of conceptualising human actions often does a poor job of

depicting actual behaviour and it has been shown that people in the real world violate one or more of the

Von Neumann/Morgenstern assumptions (Glimcher, 2003) which are so core to modern economic

thinking. As Stanovich and West (2000; p.645) have stated: “human responses deviate from the

performance deemed normative according to various models of decision making and rational judgment

(e.g. the basic axioms of utility theory)”. This is partly due to the fact that many important aspects of

12 Meir Statman, a leading finance academic contends (1999; p.20): “In standard finance people are modelled as ‘rational’, whereas behavioural finance people are modelled as normal”

9

human nature are overlooked.13 Research has shown (see for example Larrick, 2004) that descriptive

behaviour of economic agents falls systematically short of the normative ideals: essentially, a gap between

the normative predictions and the descriptive exists.14 Given that the models using expected utility as a

foundational base may not be entirely explanatory of real world financial market outcomes a number of

contrasting non-EU theories have been developed: Weighted utility Theory (Chew and MacCrimmon,

1979), Implicit EU (Chew and Epstein, 1989; Dekel, 1986), Disappointment Aversion (Gul, 1991), Regret

Theory (Bell, 1982), Rank Dependant Utility Theories (Quiggan, 1982; Seagal, 1987) Hyperbolic

Discounting15 (Ainslie, 1992; Loewenstein and Prelec, 1992) and Prospect Theory (Kahneman and

Tversky, 1979). Most of these models recognise, and are critical of the fact, that traditional economics

upholds a mechanistic concept of human actions and reasoning which is too unrealistic and not

empirically sustainable. Unquestionably the most influential and widely acknowledged model in

behavioural finance is Prospect Theory which is discussed in section 1.2.2.

1.2.1. Psychology and Finance: Social Science Divisions

"I think of behavioural finance as simply open-minded finance", (Thaler, 1993; p.17)

This sub-section examines the psychological foundations of behavioural economics/finance, and

how psychological findings have been relevant to financial economics. The two academic areas are not

incompatible as psychology analytically investigates human judgment, behaviour, and well-being, while

economics and finance primarily deals with explaining human economic behaviour and choice under

scarcity. Although, behavioural finance has been more active in this sense than classical finance Statman

(1999; p.19) argues that: “Some people think that behavioural finance introduced psychology into finance,

but psychology was never out of finance. Although models of behaviour differ, all behaviour is based on

13 This facet has been identified by the work of Sanfey et al. (2003;p.1755) who say: “Standard economic models of human decision-making (such as utility theory) have typically minimized or ignored the influence of emotions on people’s decision-making behaviour, idealising the decision-maker as a perfectly rational cognitive machine”. 14 For instance, the endowment effect where a higher value is placed on objects owned than on objects not owned, is a case in point which illustrates how findings from the psychology/economics collaboration are sometimes inconsistent with standard economic theory. Here we can identify that the evidence is in contrast to the foundational concepts behind consumer choice and indifference curves; that is according to traditional economic theory, a person’s willingness to pay for a good should equal their willingness to accept compensation to be deprived of the good. 15 “In behavioural economics, hyperbolic discounting is a particular mathematical model thought to approximate this discounting process; that is, it models how humans actually make such valuations. Given two similar rewards, humans show a preference for one that arrives sooner rather than later. They also show a tendency to prefer smaller payoffs now over larger payoffs later. Humans are said to discount the value of the later reward, by a factor that increases with the length of the delay” (Thaler, 1981; p. 202).

10

psychology”. Correspondingly so, psychology can provide us with important truths about how people

disagree from traditional economic conjectures. In stark contrast to the classical line of thinking, an ever

growing number of academics have argued that financial economics as a discipline has been out of touch

with reality; these people contest the notion commonly held by many economists that simple models of

optimisation are realistic. It must be said however, that criticism of this nature, namely that orthodox

economic theory is unrealistic, is not new as such objections have been around since the 1850s when

economics first became known as the ‘dismal science’ – prior to the mathematical revolution in

economics, prominent economists such as Irving Fisher and John Maynard Keynes in the early 1900s

actually encouraged the role of psychology in explaining economic behaviour (Loewenstein, 1992;

DeBondt, and Thaler, 1985). Part of the responsibility for the underpinnings of traditional theoretical has

been placed upon ‘physics envy’ (Lo and Mueller, 2010) although a more important factor perhaps is the

contribution of Milton Friedman and the Chicago school of neo-classical economics.16 In conflict to his

core assessment written in the 1950s, namely that judgment of a theory should be based upon on the value

of its assumptions, rather, behavioural finance research contends that an economic theory should be

assessed on how accurately it depicts reality.

1.2.2. Prospect Theory as a Foundation

The grand surveys of the BF literature by Thaler (1993, 2005); Simon, (1987); Baberis and Thaler,

(2003); De Bondt and Thaler (1985); Odean (1998); Rabin, (1998) are useful introductions to the field,

which in essence was founded on the work of two Israeli academics, namely Daniel Kahneman and Amos

Tversky. Their Prospect Theory is arguably the jewel in the behavioural finance crown since it has

provided a firm platform and alternative launching pad for new research that helps explain better the

complexities of human behaviour.17 Principally, the main idea behind Prospect Theory is that the manner

in which people make choices and decisions is based on the value function as opposed to the utility

function. As highlighted in the prior section, the rational expected utility concept is the foundation of

modern finance (whereby everybody has a utility function that they use to make decisions). According to

this function a value of utility to each payoff is assigned. It is also thought that agents derive utility from

16 Friedman (1953) argued that all useful theories rely on unrealistic assumptions because they seek simplicity. 17 Effort in this area has made many valuable inputs into the wider field of financial economics; indeed, a key acknowledgment of this statement occurred when Daniel Kahneman won the 2002 Bank of Sweden Prize in Economic Sciences in Memory of Alfred Nobel for his work on prospect theory, despite being a research psychologist and not an economist. This particularly recognition and honour reinforces the fact that cross discipline collaboration can lead to substantial academic contributions; in this case economics and psychology combined to create an innovative model.

11

consumption, and the notion of diminishing marginal utility, which implies that people get more relative

satisfaction with wealth increases, specifies that the utility function is concave.

Prospect theory (Kahneman and Tversky, 1979) is essentially a critique of expected utility theory.

In contrast to the utility function, Prospect Theory’s value function replaces probability with decision

weights (Max ∑WiVi). The value function, depicted in figure 3, is a key tenet of prospect theory and

incorporates the idea that people do not occupy finite wealth states; rather they evaluate different decision

outcomes in terms of gains and losses, value is assigned to gains and losses rather than to final assets. The

possibility and fear of losses dominates actions; losses tend to be given much more significance than

gains.18 In other words, in any but especially risky decisions, there is a greater sensitivity to losses than to

gains – or as Meir Statman (1999) refers to, a ‘Fear of Regret’ is often evident in the human mind. The

value function is determined on deviations from a reference point and is normally concave for gains

(implying risk aversion), commonly convex for losses (risk-seeking)19 and is generally steeper for losses

than for gains (loss aversion). There are two-phases to decision making: an initial editing phase and a

subsequent evaluation phase. The editing phase allows for the information to be organised and

reformulated, thereby simplifying the evaluation phase. Here, the given representation of the decision

problem is transformed into a formal decision. The second evaluation phase is based on the value and the

probability weighting functions (figure 4). From this, the gamble with the highest value is chosen. This

process is based upon the assumption that values are attached to changes rather than final states and that

decision weights do not coincide with stated probabilities. The theory predicts that when outcomes are

framed in a positive manner (gains), there is an n observable propensity for decision makers to be risk-

averse, and conversely when the frame is negative (losses), decision makers are more likely to be risk-

seeking (Kahneman and Tversky, 1979; Tversky and Kahneman, 1981, 1986). This decision framing has

also been related to mental accounting, whereby individuals form psychological accounts of the

advantages and disadvantages of an event or choice; which infers that individuals create mental images

that influence their decision making process (Laing, 2010). The authors found in simple psychological

experiments that we rely too much on reference points, mental frames, and anchors. People tend to distort

probabilities in their mind – see the ‘Allais Paradox’ (Allais, 1953): which draws attention to the violation

of expected utility and shows that we prefer certainty – and because of this, conservative behaviour often

materialises. Furthermore, people put things into mental compartments and they often conduct a form of

mental framing which tends to distort decision making. This kind of behaviour has many applications and

18 For example, if we remember how we felt on a day in the last year in which we gained 5% on our portfolio and compare it to how we felt on a day where when we lost 5%, we would almost certainly report that the unhappiness experienced with the loss was felt much more strongly. 19 A general illustration of risk-seeking behaviour is the case where an investor decides to shift a larger proportion of their portfolio into high risk non-domestic stocks rather than into government bonds.

12

the fact that normal people are unable to ascertain relative qualities and probabilities accurately leads to

market outcome effects not predicted by the EMH. Hence, the manner in which agents form expectations

should be considered a crucial component of any model of financial markets. Prospect theory takes these

thoughts into consideration.

Figure 3: The Hypothetical Value function

(Source: Kahneman and Tversky, 1979)

Figure 4: The Hypothetical Weighting function (1979) and Weighting functions for gains (w+) and losses (w−)

(Source: Kahneman and Tversky, 1979 and 1992)

Later Tversky and Kahneman developed a new version of prospect theory, which they called

cumulative prospect theory (Figure 4 illustrates the weighting function in 1979, left hand side, and then

the newer version created in 1992 on the right hand side). In both versions, which were produced by way

of experiment, probabilities are replaced by decision weights and these decision weights are generally

lower than the corresponding probabilities, except in the range of low probabilities (Sewell, 2007). The

decision weight represents the impact of a given probability valuation of a prospect. It was empirically

found that people usually under weigh outcomes that are merely probable (low probabilities) in

comparison with outcomes that are obtained with certainty. Additionally, they under weigh med-high

probabilities. The newer version, based on median estimates of y and delta, employed cumulative rather

13

than separate decision weights.20 In addition the idea that cumulative weight can apply to uncertain as

well as to risky prospects with any number of outcomes allowing for different weighting functions for

gains and for losses was introduced. The 1992 theory envisaged a unique fourfold pattern of risk attitudes:

risk aversion for gains and risk seeking for losses of high probability; risk seeking for gains and risk

aversion for losses of low probability (Sewell, 2007).

2. Shifting Paradigm and the Philosophy of Science

“Directly testing the validity of a model’s assumptions is not common practice in economics, perhaps because of Milton Friedman’s influential argument that one should evaluate theories based on the validity of their predictions rather than the validity of their assumptions. Whether or not this is sound scientific practice, we note that much of the debate over the past 20 years has occurred precisely because the evidence has not been consistent with the theories, so it may be a good time to start worrying about the assumptions. If a theorist wants to claim that fact X can be explained by behaviour Y, it seems prudent to check whether people actually do Y”. Baberis and Thaler (2003; p.65)

It could be said that the underlying principles behind the philosophy of science are often overlooked

in the research of many academics within a diverse range of scholarly disciplines; no more so is this true

than in financial economics. The basic tenets of why academic research is conducted in the first place are

frequently brushed aside in favour of maintaining the pre-existing accepted generalizations about

economic phenomena. The status quo is preserved longer than it should be. As Thomas Kuhn the

American intellectual and philosopher posited, “Science undergoes periodic paradigm shifts instead of

progressing in a linear and continuous way” (Kuhn, 1996). Moreover, these paradigm shifts open up new

approaches to understanding that scientists would never have considered valid before. The legitimacy of

this statement is concrete and the vast majority of scientists would concur with Kuhn here.21 So, given

that there is much to be gained from scientific disunity and the subsequent paradigm shifts, it should be

useful to examine the potential benefits of a mixed disciplinary approach. From the previous section we

have seen that behavioural economics/finance was born out of the perceived doubts and qualms with

regard to the assumptions of modern neoclassical economics. It has been primarily informed by inputs

from psychology, and from behavioural decision research. In a Kuhnian sense, this new line of thinking

will hopefully be incorporated into a new paradigm which will add to the explanatory power of the

20 A related concept to value weighted theory is the notion of bounded rationality; which implies the retention of individual rationality but relaxation of the consistent beliefs assumption (investors don’t always apply Bayes Law in relation to probability). 21 The counter argument of this thought relates to the famous Charles Darwin saying “Natura non facit saltum”, which is Latin for "nature does not make jumps" – see Alfred Marshall, ‘Principles of Economics’ (1890) for more on this.

14

discipline. This would naturally imply that the basic object of study would have to be changed, which

entails that at a very abstract level, the central economic science axioms must be rethought also.22

An important question posed in the behavioural finance literature is whether economics is a positive

science. The quote above from Baberis and Thaler (2003) readdresses the fact that when discussing any

work within the extensive area of economics academia, it is worthy to reiterate that research can be

positive or normative in nature. Positive research (descriptive and explanatory enquiry) outlines what

economic agents actually do, while normative research stipulates what they should do. In other words,

positive research describes what is, whereas normative research prescribes what should be.23 Let’s take

the investment decision process for instance. Behavioural finance employs positive methods whereas

traditional economic analysis uses more normative methodologies; this key difference entails that BF can

provide more viable explanations about the missing gaps between what we ought do and what we do do.

In fact, the discrepancy between the normative traditional theories and behavioural descriptive models can

be construed to represent systematic irrationalities in human reasoning and cognitive abilities. In an ever

increasing number of empirically based studies in the heuristics and biases literature, which started in the

1970s and 1980s, it has been shown time and time again that individual behaviour strays from the

normative predictions (Stanovich and West, 2000). This division between the normative and the

descriptive is important as the traditional models can be maintained as the normative theory, while the

alternatives provided by behavioural models can be understood as descriptive theory. A prominent

example of this incongruence is the Allais Paradox (1953), which shows that choices regularly violate the

two foundational axioms of expected utility, the independence axiom and the sure-thing principle (Savage,

1954). The search for more realistic alternative assumptions to improve the predictive accuracy of an

economic model requires a testing of which factors make the biggest difference to the underlying variable

under observation: a theory ought to yield predictions about phenomena. For the test of realism,

methodological principles and an understanding of what features of the problem or of the circumstances

have the greatest effect on the accuracy of the predictions yielded by the particular theory are needed. A

key goal is the development of new assumptions that are more realistic as Herbert Simon argued that

Friedman’s idea of ‘Positive Economics’ is fundamentally flawed and that economists should directly test

economic model assumptions in addition to model implications: “In imagining that theories are used in

their simplest idealized form, ignoring real world complications, Friedman has drawn a fictitious picture

of how theories are actually employed in physical science and engineering, and given bad advice as to 22 As highlighted recently by Nobel Prize winner Joseph Stiglitz: “If science is defined by its ability to forecast the future, the failure of much of the economics profession to see the crisis coming should be a cause of great concern....economists must search for new paradigms” (Stiglitz, 2010; p.1). 23 This distinction has its roots in the fact-value distinction in philosophy, for more information in this area the reader is directed towards the work of Karl Popper.

15

how they should be employed in economics” (Simon, 1982; p.19). These apparent strengths lead to a

glaring weakness however: the reliance on traditional finance as a paradigm, and its increased intellectual

flexibility, makes it difficult to disprove and to validate some of the most prevalent behavioural models.

That being said, it is nigh on impossible to fully model every aspect of economic phenomena and human

economic behaviour as they are varied and complex, however that doesn’t entail that one should not

endeavour to do so.

In spite of the opinion expressed by Thaler (1999; p.12): “The controversy surrounding BF is dying

out as scholars accept it as simply a new way of doing economic research”, the battle between the

standard finance camp and other contrasting notions of finance that has raged on for the last two decades,

still continues. Thaler’s statement was made in 1999, however since then it is partly true that the

incorporation of psychology and finance has become more widely tolerated. Many new ideas have been

proffered and a plethora of articles have been written on the debate. Of these, a most famous input came

from Eugene Fama who described behavioural finance as “the anomalies literature” (1998). His

proclamation, at the time, was considered to be derogatory but it could now be deemed legitimate and

complimentary in another sense: the fact that Fama (being the spearhead of traditional finance academia)

dismissed such contrary work to the traditional/modern finance paradigm indicates that he felt that the

status quo was being threatened. What he was referring to was that much of BF is based on weak data and

evidence which was found using inaccurate methodologies. In truth this rebuttal is analogous to much of

the criticism of the discipline – detractors of behavioural economics/finance point to four explanations

which uphold the idea that human behaviour is largely rational and that the gap often found in studies

between rational economic predictions and actual behaviour is due to: performance errors, computational

limitations, the wrong norm being applied by the experimenter, and a different construal of the task by the

subject (Stanovich, 2000).

This denial of is course a common response to anomalies, however Fama’s assessment is incorrect

and calling BF the anomaly literature is a “means of discrediting” important evidence (Frankfurter and

McGoun, 2001). Furthermore, the majority of anomalies (which we will discuss more closely in a

proceeding ‘micro’ and ‘macro’ sections) have undergone rigorous data triangulation (Lucey, 2000).

Therefore, under the light of the scientific process, empirical falsification, and critical rationalism, which

strongly postulates that anomalies contribute significantly to the development of new and ultimately more

successful theories, these findings should not be dismissed. Anomalies can be scientifically significant as

the identification of departures, deviations, and discrepancies from existing theories helps in the

formulation of original improved theories. New and unexpected phenomena can often light the way for

future direction research; therefore if this is indeed the case, then different lines of enquiry and multi

perspective academic research in pursuit of better theories must be encouraged. However, even though

16

this may be so, it should also be remembered that a theory tends to be accepted not only due to the

empirical evidence/test but also because “researchers persuade one another that the theory is correct and

relevant” (Black, 1986; p.537).

3. Discussion The majority of observers would agree that the on-going global financial crisis which started in

2008 has once again highlighted the role of psychology in financial markets, and how susceptible they are

to asset price inflation, market instability, and indeed the overall welfare of society. For example, the sub-

prime mortgage debacle which occurred in the US presents a copious amount of proof of defective

consumer decision-making. In addition, few academics in traditional economics were able to foresee the

massive bubble and tremendous overvaluations which were developing in the US housing market; some

within behavioural finance did (such as Robert Shiller in 2005). With regard to individual investors in this

period, many of those who were deemed risk tolerant by their advisors had investment portfolios over-

weighted towards equity assets. However, once volatility in the markets increased many investors

panicked and sold at the market bottom. This behaviour, which was contrary to that envisioned by the risk

assessments used by the financial advisors to appraise and steer investors, has shown many of the classical

finance tools available to advisors to be lacking. From an ex-post perspective clearly many economic

predictions were disastrously wrong and the mainstream discipline was unable to predict the economic

dynamics of the phenomenon with such a small number of rules and laws. Overconfidence in the power of

traditional economic models that have been out of synch with real-world data, has been shown to be quite

dangerous. Evidence indicates that we depart from rationality in our economic decisions and behaviours in

predictable patterns, but what is required is a more sophisticated explanation of how emotions and relative

reason enable us to perform in the challenges we face. This undermining of homo oeconomicus (i.e. the

economic rational man who acts in his own self-interest and always maximises his own personal payoffs)

has many important consequences. These implications can assist policymakers recognising which

dynamics, apart from solely economic ones, may impact upon the financial behaviour of individuals and

markets. There are other crucial elements within financial economics, and understanding them is

elementarily important to the improvement of both financial market analysis and the formulation of

systemic risk presentation measures by governments.

As touched upon previously, the model most responsible for the emergence of behavioural finance

as a reputable academic area is Prospect Theory. Perhaps the most valuable aspect of prospect theory is

that it is construction model which wholly attempts to incorporate this facet of the human decision making

process into its thinking. Prospect Theory is undoubtedly an important basis of behavioural finance but we

need to ask ourselves whether it is justifiably so. Of course in absence of an alternative theory which can

17

better describe behaviour, decisions and risk attitudes, behavioural finance researchers have used this

model as a main foundation of thinking. To examine how psychology and economics has evolved, it is

evidently clear that the first behavioural economists considered that the mind is an ‘imperfect machine’ of

sorts. From this initial concept they then developed further models based upon the idea that this imperfect

machine is systematically encouraged into error by the duplication by psychological bias mechanisms and

cognitive heuristics (Frey and Stutzer, 2007), many of which will be detailed in chapter two. One main

reason as to why Prospect Theory has attained such approval and admiration is that it codifies these

irrational behavioural processes into a formal decision making model. The anomalies, cognitive heuristics,

emotional biases, psychological traps etc. are converted into more uniform and regular patterns of human

conduct. What’s more, this model has also enhanced our ability to make predictions about how people will

act in a given situation. On the other hand, one largely acknowledged criticism of this model of behaviour

is that it takes a ‘black box’ type approach in its thinking. That is to say it does not specifically consider

the inner workings and cognitive intricacies of the human brain. Prospect theory aims to predict behaviour

rather than to fully understand the mind’s internal processes that generate the behaviour – this perhaps is

where the research of another newer but fundamentally related field called neuroeconomics, which does

consider the internal processes, can be of most use into the future.

18

4. Bibliography

Ainslie, G. 1992, Picoeconomics: The Strategic Interaction of Successive Motivational States Within the Person, New York: Cambridge University Press.

Allais, M. 1953, Le Compartement de l’Homme Rational Devant le Risque, Critique des Postulates et Axiomes de l’Ecole Americaine, Econometrica, no. 21; pp.503-546.

Barberis, N. and Thaler, R.H. 2003, A Survey of Behavioural Finance, in Constantinides, G.M, Harris, M. and Stulz, R. eds., Handbook of the Economics of Finance. North Holland, Amsterdam.

Bell, D.E. 1982, Regret in decision making under uncertainty, Operations Research, Vol. 30, pp.961–981. Belsky, G. and Gilovich, T. 1999, Why Smart People Make Big Money Mistakes and how to correct them: lessons

from the new science of Behavioural Economics, Simon & Schuster: New York, ISBN: 0684844931 Bernoulli, D. 1738, Specimen Theoriae Novae de Mensura Sortis, Commentarri Academiae Scientiarum Imperialis

Petropolitanae, Tomus V, pp.175-92. Black, F. 1986, Noise, Journal of Finance, Vol. 41. No. 3, pp.529-543. Chew, S. H. and MacCrimmon, K.R. 1979, ‘Alpha utility theory, lottery composition and the Allais Paradox’,

University of British Columbia Faculty of Commerce and Business Administration, No. 686. Chew, S. H. and Epstein, L.G. 1989, The Structure of Preferences and Attitudes towards the Timing of the

Resolution of Uncertainty,International Economic Review, Vol. 30, pp.103 117. Dekel, E. 1986, Axiomatic Characterization of Preferences under Uncertainty: Weakening the Independence Axiom,

Journal of Economic Theory 40 304-318 DeBondt, W.F.M. and Thaler, R.H. 1985, Does the stock market overreact?, Journal of Finance, Vol.40, No.3,

pp.793-805. DeBondt, W.F.M. and Thaler, R.H. 1994, Financial Decision-Making in Markets and Firms: A Behavioural

Perspective, NBER Working Papers, 4777, National Bureau of Economic Research, Inc. Edgeworth, F.Y. 1881. Mathematical Psychics: An Essay on the Application of Mathematics to the Moral Sciences,

Publisher: C.K. Paul, London. Elton, E.J. and Gruber, M.J. 1995, Modern portfolio theory and investment analysis, New York: Wiley ISBN: 978-

0470388327. Fama, E.F. 1965, The Behaviour of Stock-Market Prices, Journal of Business, vol. 38, no. 1, pp.34-105. Fama, E.F. 1970, Efficient Capital Markets: A Review of Theory and Empirical Work, Journal of Finance, vol. 25,

no. 2, pp.383-417. Fox C.R 2006, Neuroeconomics: Week 4 Decision Under Risk, UCLA Seminar, available for download

at:www.poldracklab.org/.../neuroeconomics/neuroec-week4-5-risk-uncert.ppt Fox, C.R., & Tversky, A. 1995, Ambiguity Aversion and Comparative Ignorance, The Quarterly Journal of

Economics, Vol. 110, No. 3. Aug., 1995; pp.585-603. Frankfurter, G.M., McGoun, E.G and Allen, D.E, 2004, The prescriptive turn in behavioural finance, Journal of

Socio-Economics, Vol. 33, pp.449-468. Frankfurter, G. M. and McGoun, E. G. 2001, Anomalies in Finance: What Are They and What Are They Good For?,

International Review of Financial Analysis, Vol. 10, No. 4, pp.407 429. Frey, B.S. and Stutzer, A. 2002, What Can Economists Learn from Happiness Research?, Journal of Economic

Literature, Vol. 40, pp.402-35. Friedman, M. and Savage, L.J. 1948, Utility Analysis of Choices Involving Risk, Journal of Political Economy, Vol.

56, No. 4, pp.279–304. Friedman, M. 1953, Essays in Positive Economics, University of Chicago Press Fuller, R.J. 1998. Behavioural Finance and the Sources of Alpha, Journal of Pension Plan Investing, Winter, Vol. 2,

No. 3. Gigerenzer, G. 1993, From metaphysics to psychophysics and statistics, The Behavioural and Brain Sciences, 161,

139-140. Glimcher, P.W. 2003, Decisions, uncertainty, and the brain: The science of neuroeconomics, Cambridge, MA: MIT

Press. Grinblatt, M. and Keloharju, M. 2001, What Makes Investors Trade?, The Journal of Finance, Vol. 56, pp.589-616. Gul, F. 1991, A theory of disappointment aversion, Econometrica, Vol. 59, pp.667-686. Hands, D.W. 2010, Economics, Psychology, and the History of Consumer Choice Theory, Cambridge Journal of

Economics, Vol. 34, no. 4, pp.633-648. Heukelom, F. 2007, Kahneman and Tversky and the Origin of Behavioural Economics, Tinbergen Institute

Discussion Paper, TI 2007-003/1, available at. http://www.tinbergen.nl.

19

Hicks, J.R. 1939, Value and Capital: An Inquiry into Some Fundamental Principles of Economic Theory, Oxford: Clarendon Press.

Jallais, S., and Pradier, P.C., 2005, The Allais Paradox and Its Immediate Consequences for Expected Utility Theory, in P. Fontaine and R. Leonard eds, The Experiment in the History of Economics, London: Routledge, pp.25-49.

Jones, B.D, 1999, Bounded Rationality, Annual Review Political Science, Vol. 2, pp.297-321. Kahneman, D. 2003, A Psychological Perspective on Economics, American Economic Review, Vol. 93, pp.162-68. Kahneman, D. and Frederick, S. 2002, Representativeness Revisited: Attribute Substitution in Intuitive Judgment, in

Gilovich, T., Griffin, D. and Kahneman, D. eds, Heuristics and Biases: The Psychology of Intuitive Judgment pp.49-81, New York: Cambridge Uni Press.

Kahneman, D., Knetsch, J.L. and Thaler, R.H. 1991, The Endowment Effect, Loss Aversion, and Status Quo Bias: Anomalies, Journal of Economic Perspectives, Vol. 5, no. 1, pp.193–206.

Kahneman, D. and Thaler, R.H. 1991, Economic Analysis and the Psychology of Utility: Applications to Compensation Policy, The American Economic Review, Vol. 812, pp.341-346.

Kahneman, D. and Sugden, R. 2005. Experienced Utility as a Standard of Policy Evaluation. Environmental & Resource Economics, 32, 161-181.

Kahneman, D. and Tversky, A 1992, Advances in Prospect theory: Cumulative Representation of Uncertainty, Journal of Risk and Uncertainty, Vol. 5, no. 4.

Kahneman, D. and Tversky, A. 1972. Subjective Probability: A Judgment of Representativeness, Cognitive Psychology, Vol. 3, pp.430-454.

Kahneman, D. and Tversky, A. 1973, On the Psychology of Prediction. Psychological Review, vol. 80, pp.237-251. Kahneman, D. and Tversky, A. 1979, Prospect Theory: An Analysis of Decision under Risk, Econometrica, vol. 47,

pp.313-327. Kahneman, D., Walker, P. and Sarin, R. 1997. Back to Bentham? Explorations of Experienced Utility. The Quarterly

Journal of Economics, Vol. 112, No.2, pp.375-405. Keynes, J.M. 1936, The General Theory of Employment, Interest, and Money, London: Macmillan. Kuhn. T. 1996, The structure of scientific revolutions, 3rded., Chicago: University of Chicago Press. Laibson, D. 1997, Golden Eggs and Hyperbolic Discounting, Quarterly Journal of Economics, Vol. 112, pp.443–

477. Laing, G.K. 2010, Impact of Cognitive Biases on Decision Making by Financial Planners: Sunk Cost, Framing and

Problem Space, International Journal of Economics and Finance, Vol. 2, No. 1. Lamont, O.A. and Thaler, R.H. 2003, Can the market add and subtract? Mispricing in tech stock carve-outs, Journal of Political Economy, Vol. 111, pp.227-268. Larrick, R.P. 2004, Debiasing, Chapter 16 in Blackwell Handbook of Judgment and Decision Making, Koehler, D.J.

and Harvey, N. Eds., Blackwell Publishing Ltd. List, J. A. and Haigh, M.S. 2005, A simple test of expected utility theory using professional traders, Proceedings of

the National Academy of Sciences, January, Vol. 102, no. 3, pp.945–948. Lintner, J. 1965 The valuation of risk assets and selection of risky investments in stock portfolios and capital

budgets, Review of Economics and Statistics, Vol.47, pp.13-37. Lo, A.W. and Mueller, M.T. 2010, Warning: Physics Envy May be Hazardous to Your Wealth!, Available at SSRN:

http://ssrn.com/abstract=1563882 Loewenstein, G. 1992 The Fall and Rise of Psychological Explanations in the Economics of Intertemporal Choice, In

Choice Over Time, Loewenstein, George and Jon Elster, ed. New York: Russell Sage Foundation, pp.3–34 Loewenstein, G., and Prelec, D. 1992, Anomalies in Intertemporal Choice: Evidence and an Interpretation, Quarterly

Journal of Economics, Vol.107, pp.573–597. Lucey, B. 2000, Friday the 13th and the Philosophical Basis of Financial Economics, Journal of Economics and

Finance, Vol. 24, No. 3, Fall, pp.294-301. MacKay. C. 1841, Extraordinary Popular Delusions And The Madness Of Crowds, Harriman House Limited. Marshall, A. 1890, Principles of Economics, Publisher, London: Macmillan and Co. Markowitz, H. 2005,Market Efficiency: A Theoretical Distinction and So What?, Financial Analysts Journal, Vol.

61, No. 5, pp.17-30, September/October Neumann, J. V., and Morgenstern, O. 1944, Theory of Games and Economic Behaviour, Princeton: Princeton

University Press. Odean, T. 1998, Are Investors Reluctant to Realize Their Losses?, The Journal of Finance, Vol.53, no.5,pp.1775-

1798. Quiggin, J. 1982, A theory of anticipated utility, Journal of Economic Behaviour& Organization, Vol. 3,

pp.323 343.

20

Rabin, M. 1998, Psychology and Economics, Journal of Economic Literature, Vol. 36, pp.11-46. Ritter, J. 2003, Behavioural Finance, Pacific-Basin Finance Journal, Vol. 11, No. 4, September; pp.429-437. Sanfey, A.G., Rilling, J.K., Aronson, J.A., Nystrom, L.E., and Cohen, J.D. 2003, The neural basis of economic

decision-making in the Ultimatum Game, Science, Vol. 300, pp.1755–1758. Samuelson, P.A. 1938, A Note on the Pure Theory of Consumer's Behaviour, Economica, Vol. 5, pp.61-71. Robbins, L. 1952, An Essay on the Nature and Significance of Economic Science, 2nd edition, London: Macmillan,

first edition published in1932. Savage, L. J. 1954, The foundations of statistics, John Wiley & Sons Inc., New York. Schoemaker, P. 1982, The expected utility model: its variants, purposes, evidence and limitations, Journal of

Economic Literature, Vol. 20 June, pp.529-563. Segal U. 1989, Anticipated Utility. A Measure Representation Approach, Annals of operations Research, Vol.19,

pp.359-373. Sent, E.M. 2004, Behavioural Economics: How psychology made its limited way back into economics, History of

Political Economy, Vol. 364, pp.735-760. Sewell, M. 2007, An Introduction: Behavioural Finance, University College London, available at

http://www.cs.ucl.ac.uk/staff/M.Sewell/publications.html Schwartz, H.H. 2007, An Introduction to Behavioural Economics: The Complicating but Sometimes Critical

Considerations, Available at SSRN: http://ssrn.com/abstract=960222 Sharpe, W.F. 1964, Capital Asset Prices: A Theory of Market Equilibrium under Conditions of Risk, Journal of

Finance. Vol.19, No. 3, pp.425–442. Shiller, R.J. 2005, Irrational Exuberance, Second Edition, Princeton University Press. Simon, H.A. 1955, A Behavioural Model of Rational Choice, Quarterly Journal of Economics, 69; pp.99-118. Simon, H.A. 1982, Models of bounded rationality 2 vols., Cambridge, MA: MIT Press. Simon, H.A. 1987., Rational Decision Making in Business Organisations, in Advances in Behavioural Economics:

Vol. 1, ed. L. Green and J. H. Kagel, 18–47. Norwood, NJ: Ablex. Simonson, I. and Tversky, A. 1992, Choice in Context: Trade-off Contrast and Extremeness Aversion, Journal of

Marketing Research, Vol. 293, pp.281-295. Slutsky, Eugene E. 1915, Sulla Teoria del Bilancio del Consonatore, Giornale degli Economisti, Vol. 51, pp.1-26, the

translated version in appeared Readings in Price Theory, G. J. Stigler and K. E. Boulding eds., Homewood, IL: R.D. Irwin, 1952, pp.27-56.