benefits at a glance handbook - secure.icbdr.com · the benefits at a glance handbook is designed...

TRANSCRIPT

BENEFITS at a GLANCE

Handbook

Benefit Year: December 1, 2014 – November 30, 2015

This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

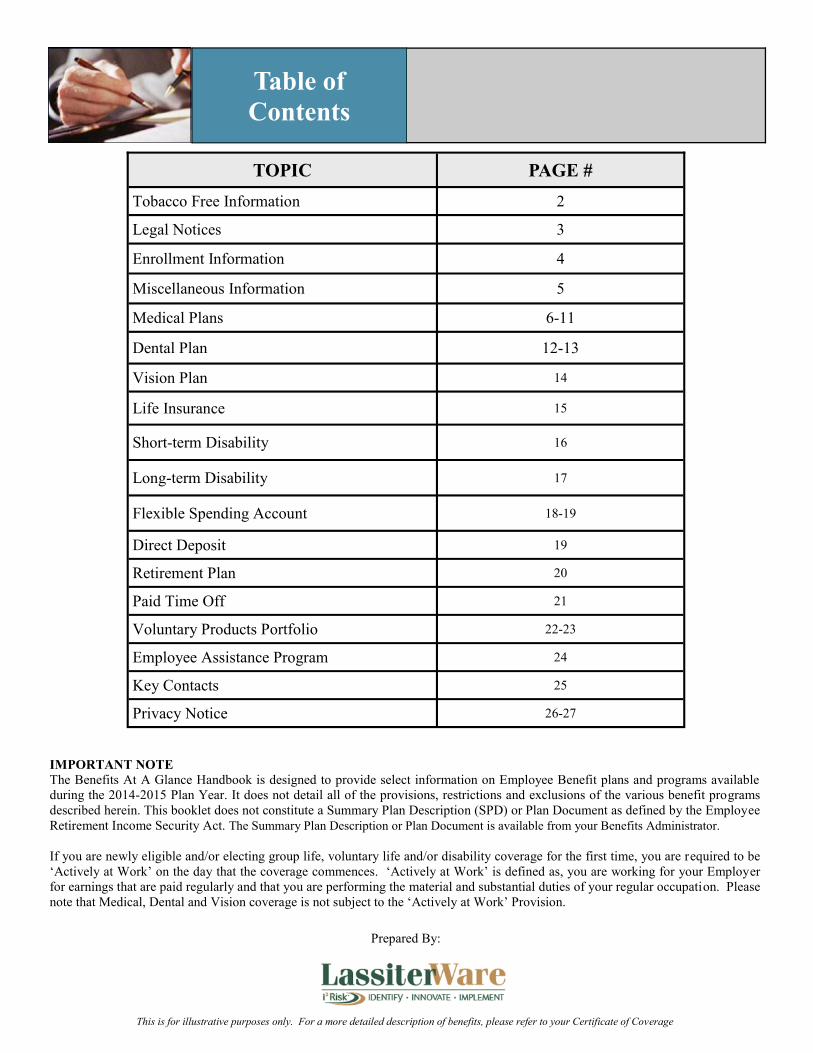

TOPIC PAGE #

Tobacco Free Information 2

Legal Notices 3

Enrollment Information 4

Miscellaneous Information 5

Medical Plans 6-11

Dental Plan 12-13

Vision Plan 14

Life Insurance 15

Short-term Disability 16

Long-term Disability 17

Flexible Spending Account 18-19

Direct Deposit 19

Retirement Plan 20

Paid Time Off 21

Voluntary Products Portfolio 22-23

Employee Assistance Program 24

Key Contacts 25

Privacy Notice 26-27

IMPORTANT NOTE

The Benefits At A Glance Handbook is designed to provide select information on Employee Benefit plans and programs available

during the 2014-2015 Plan Year. It does not detail all of the provisions, restrictions and exclusions of the various benefit programs

described herein. This booklet does not constitute a Summary Plan Description (SPD) or Plan Document as defined by the Employee

Retirement Income Security Act. The Summary Plan Description or Plan Document is available from your Benefits Administrator.

If you are newly eligible and/or electing group life, voluntary life and/or disability coverage for the first time, you are required to be

‘Actively at Work’ on the day that the coverage commences. ‘Actively at Work’ is defined as, you are working for your Employer

for earnings that are paid regularly and that you are performing the material and substantial duties of your regular occupation. Please

note that Medical, Dental and Vision coverage is not subject to the ‘Actively at Work’ Provision.

Prepared By:

Table of

Contents

2 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

TOBACCO USE SURCHARGE

If you used tobacco products in the preceding 6 months (smoke, chew or any other manner) and are enrolled in Aspire

Health Partners’ medical plan, you will be assessed a tobacco-use surcharge.

Not only are we trying to reduce our escalating insurance costs, but we are also striving for a healthier work force. There is

a proven link between smoking and the rising cost of healthcare because smokers / tobacco-users have a higher risk of can-

cer, stroke, heart disease and chronic obstructive pulmonary disease (COPD) than non-tobacco users. You will be required

to complete a Tobacco-Use certification as part of your benefits enrollment.

Aspire Health Partners offers a reasonable opportunity for employees to avoid the smoking premium surcharge upon completion

of an approved tobacco cessation program. This applies to covered employees, for whom it is unreasonably difficult because of a

medical condition, or for whom it is medically inadvisable to be tobacco-free under our standard. Aspire Health Partners has

chosen the standards that the tobacco cessation program must meet such as the timeframe, and the manner in which employees

must certify their completion of the program. An approved tobacco cessation program may be a certified online program, class-

room-based course, or telephonic counseling/support program.

Smoking Premium Surcharge Reasonable Alternative Information

The following information describes Aspire Health Partners “reasonable opportunity” for you to avoid the smoking premi-

um surcharge. It is each employee’s responsibility to pay for the cost of tobacco cessation.

Step 1: Choose an approved online, classroom-based or telephonic tobacco cessation program. Some resources available

to help you locate approved tobacco cessation programs include:

Telephonic Courses: More than 30 states now run tobacco guidelines that are confidential, staffed by trained spe-

cialists and free to residents. Some of these helplines provide over-the-counter support products, such as gum or

patches, at reduced prices or as part of the program. Courses must consist of at least four telephonic counseling /

support sessions to be acceptable. You will have to obtain verification that you completed at least four sessions.

Online Course: Take the online American Lung Association’s Freedom From Smoking Program (make sure to

elect the Premium membership for a nominal fee so you can present a completion certificate.) Go to:

www.ffsonline.org A completion certificate will be required as proof of your online course.

Classroom-Based Courses: Approved classroom-based courses are those offered through a hospital, community

organizations (such as the American Cancer Society) or your state’s Department of Health courses. Courses must

consist of at least four classroom-based meetings to be acceptable. You will have to obtain verification that you

completed at least four sessions.

The Tobacco Free Florida Website is a great place to start www.tobaccofreeflorida.com

If you do not have access to a computer, you may call 877-822-6669 for your options.

Step 2: Enroll in and complete one of the approved tobacco cessation programs listed above.

Step 3: Obtain a completion certificate from your program and submit to your Human Resources Department

Tobacco Free

Discount

3 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

MEDICAID AND THE CHILDREN’S HEALTH IN-

SURANCE PROGRAM (CHIP) If you are eligible for health coverage but are unable to

afford the premiums, some States have premium assistance

programs that can help pay for coverage. These States use

funds from their Medicaid or CHIP programs to help people

who are eligible for employer-sponsored health coverage,

but need assistance in paying their health premiums. If you

or your dependents are NOT currently enrolled in Medicaid

or CHIP, and you think you or any of your dependents

might be eligible for either of these programs, you can con-

tact your State Medicaid or CHIP office or dial 1-877-

KIDSNOW or go to www.insurekidsnow.gov to find out

how to apply. If you qualify, you can ask the State if it has

a program that might help you pay the premiums for an

employer-sponsored plan. Once the State determines that

you or your dependents are eligible for premium assistance

under Medicaid or CHIP, your employer’s health plan is

required to permit you and your dependents to enroll in the

plan – as long as you and your dependents are eligible, but

not already enrolled. This is called a “special enrollment”

opportunity, and you must request coverage within 60 days

of being determined eligible for premium assistance.

PATIENT PROTECTION AND AFFORDABLE CARE

ACT

The Patient Protection and Affordable Care Act (PPACA)

requires most US Citizens to obtain health insurance begin-

ning January 1, 2014. Individuals who do not obtain health

insurance will be subject to a penalty of $95 or 1% of your

gross household income (whichever is greater) for each

uninsured adult for 2014. The penalty for each uninsured

child is equal to half of the adult penalty, not to exceed

three times the adult penalty for the calendar year. Penal-

ties will increase in 2015 to $325 or 2% of gross household

income (whichever is greater), in 2016 to $695 or 2.5% of

gross household income (whichever is greater), and for

each year thereafter, it will be increased by the cost-of-

living adjustment. The annual penalty will not exceed the

national average premium for Bronze coverage in an Ex-

change. If you choose not to enroll you can go to

www.healthcare.gov to review and/or obtain coverage

through the federal Marketplace exchange.

Notices

NOTICE REGARDING THE WOMEN’S HEALTH AND

CANCER RIGHTS ACT OF ‘98

Under federal law, group plans providing benefits for a mas-

tectomy must also provide, in connection with the mastecto-

my for which the participant or beneficiary is receiving bene-

fits, coverage for:

Reconstruction of the breast on which the mastectomy

has been performed;

Surgery and reconstruction of the other breast to produce

a symmetrical appearance; and

Prosthesis and physical complications of mastectomy,

including lymph edemas, in a manner determined in con-

sultation between the attending physician and the patient.

PORTABILITY OF COVERAGE

The Health Insurance Portability and Accountability Act

(HIPAA) of 1997 entitles you to a complete transfer of bene-

fits (no pre-existing condition exclusions) if you change jobs

or change health insurance carrier(s). In order to qualify for

this transfer of benefits, your previous coverage must not

have lapsed for more than 63 days prior to your new date of

hire. In order to guarantee the portability of your benefits, you

must provide proof of prior coverage to your new employer at

the time of application or a certificate of coverage can be sent

directly to United Healthcare.

THE NEWBORNS AND MOTHERS’ HEALTH PRO-

TECTION ACT OF 1996 (NMHPA) Under Federal law, you and your newborn child are covered

for a hospital stay following childbirth. The law applies both

to persons enrolled in group health plans and to persons who

have individual health care coverage. In general, plans and

health insurance issuers that are subject to NMHPA may NOT

restrict benefits for a hospital stay in connection with child-

birth to less than 48 hours following a vaginal delivery or 96

hours following a delivery by cesarean section.

UNIFORMED SERVICES EMPLOYMENT AND

REEMPLOYMENT RIGHTS ACT

The Uniformed Services Employment and Reemployment

Rights Act (USERRA) prohibits discrimination against any-

one for serving in the armed forces or for taking military

leave from a civilian job. This includes discrimination in hir-

ing, promotion, reemployment, or any other benefit of em-

ployment. USERRA also prohibits retaliation against anyone

who seeks to enforce their rights under USERRA or assists

another in enforcing those rights.

4 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

The guide is to help you make the benefit choices that are

right for you. Think carefully about which options best suit

your individual needs and budget. The choices that you

make cannot be changed until December 1, 2015, unless you

experience a qualifying life event that is consistent with the

changes you wish to make.

ELIGIBILITY

You are eligible to participate in the benefits program if you are

a full time employee and normally work 30 hours per week.

Your benefits begin on the first day of the month following 60

days of continuous employment.

If you begin work as a part-time employee and become full time

you may participate in the benefits program on the first of the

month following 60 days from the date you became full time. If

your job status changes from full time to part-time (less than 30

hours per week), your benefits will end. You will be offered an

opportunity to continue your medical, vision, FSA and dental

benefits at your own expense per Federal COBRA regulations.

If an employee returns to their full time status within 90 days of

termination, all benefits will be reinstated effective on the full

time rehire date.

Dependents are eligible for coverage under the health plans if

they are the employee’s spouse or domestic partner, or the em-

ployee’s children including adopted, foster, step-children, or

children for whom legal guardianship has been court appointed.

Coverage for the dependent children on the medical, dental and

vision plans continues until end of the month in which they turn

age 26. Please refer to your certificate of coverage for each ben-

efit’s dependent qualification.

A dependent child may also remain covered on the medical plan

after their 26th birthday provided the child is incapable of self-

sustaining employment by reason of mental or physical handi-

cap. Special approval must be obtained from the insurance car-

riers.

DOMESTIC PARTNERS

Domestic partners are eligible to be enrolled for benefits. To

become covered, you must meet the following qualifications:

• Each party is at least 18 years old and competent to con-

tract

• Neither party is married, nor a partner to another domestic

partnership relationship

• Each party is the sole domestic partner of the other person

• Each party is not related to the other by blood

• Both parties consent to the domestic partnership relation-

ship without force, duress or fraud

• Both parties agree to be jointly responsible for each others

basic food, shelter, common necessities of life and welfare

• Neither party has been a member of another domestic part-

nership for the past year

• Each party shares his or her primary residence with the

other

• Each party considers himself/herself to be a member of the

immediate family of the other partner

Please take note that IRS Section 152 states that employees

adding a domestic partner or the child of a domestic –partner

who do not meet the IRS Section 152 definition of qualified

dependents will have additional taxable income, which needs to

be taxed and reported. When an employer provides health in-

surance coverage for the domestic partner or the dependents of

the domestic partner of an employee, federal tax law considers

the fair market value of that coverage, including the employee's

pre-tax contributions, as "imputed income" to the employee.

Additionally, employees cannot use pre-tax dollars to pay for a

domestic partner's coverage, precluding them from the full ben-

efits of a Flexible Spending Account, Health Reimbursement

Account or Health Savings Account.

Enrollment

Information

5 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

CHANGING YOUR BENEFIT CHOICES

Your benefit choices will stay in effect for a full plan year.

If you have a qualified change in family status, you may be able

to change benefit elections. Qualified family status changes

include, but are not limited to:

• Marriage or Divorce

• Birth, Adoption or Legal Custody of an eligible dependent

• Death of your spouse or dependent

• A covered Dependent becomes ineligible

• Change from full time to part-time status, or vice versa, by

you or your spouse

• Unpaid leave of absence by you or your spouse

• Significant change in your spouse's coverage attributable to

employment

• Termination or commencement of spouse's employment

If you experience a qualified family status change and wish to

make changes, you must notify Human Resources within 31

days of the change. If you do not notify Human Resources

within 31 days of the qualifying event, you must wait until the

next annual enrollment period to make any desired changes.

Please keep in mind that documentation may be required.

BENEFIT TERMINATION & THE COBRA

CONTINUATION OPTION

Your benefits will term at the end of the month in which you

either elect not to participate in the plan, or you cease to be a

full-time employee.

The Federal Consolidated Omnibus Budget Reconciliation Act

(COBRA) provides insured employees and their qualified

beneficiaries the opportunity to continue health, dental, vision,

and flexible spending account coverage when a “qualifying

event” would normally result in the loss of coverage eligibility.

Common qualifying events include resignation or termination

from employment, the death of an employee, a reduction in

employee’s hours, an employee’s divorce, and dependent child

no longer meeting eligibility requirements. Under COBRA, the

employee or dependent pays the full cost of coverage at the

current group rates plus an administrative fee of 2%.

PAYING FOR BENEFITS WHILE ON AN APPROVED

FAMILY MEDICAL LEAVE OR A MEDICAL LEAVE

RELATED TO A WORKCOMP INJURY

Employees on an approved leave are still responsible for paying

the same portion of premiums paid prior to the leave. You may

pay your portion of premiums due before starting your leave, or

you may pay monthly during your leave. Payment is due on or

before the first of the month. Failure to make payments in a

timely manner will result in termination of coverage, retroactive

to the day your FMLA began. You should contact your Human

Resources to make payment arrangements prior to your leave.

Employees on an approved leave can stop health coverage alto-

gether and restart it when returning to work.

PRE-TAX OR AFTER-TAX?

For some benefits, you use pre-tax dollars from your pay. For

others, you must use after-tax dollars. When you pay for bene-

fits with pre-tax dollars, money is deducted from your pay be-

fore taxes are taken out. In this way, you avoid paying Federal

Income and Social Security taxes on what you spend on bene-

fits. With after-tax contributions, just the opposite is true. Pre-

miums are deducted from your pay after Federal and Social

Security taxes are calculated and deducted from your gross pay.

A NOTE ABOUT SOCIAL SECURITY

Pre-tax deductions taken from your paycheck lower your taxa-

ble income, your Social Security taxes (and, therefore, your

future Social Security benefits) may be lower. How you are

affected depends on your pay and the amount of pre-tax contri-

butions you make.

The reduction in Social Security benefits, if any, for most em-

ployees will be minimal - a few dollars a month. Younger em-

ployees who use large amounts of tax-free dollars to pay for

benefits over a long period (20 to 30 years) may experience a

greater reduction in benefits when they retire. However, for

most people, the benefit reduction has been more than offset by

the tax savings. For more information, please contact your local

Social Security Administration office.

MEDICARE PART D ELIGIBLE INDIVIDUALS

If you and/or your dependents have Medicare or will become

eligible for Medicare in the next 12 months, a Federal law gives

you more choices about your prescription drug coverage. This

booklet does not constitute disclosure of creditability status.

Please contact Human Resources for your personalized disclo-

sure notice regarding the credibility status of your plan.

Miscellaneous

Information

6 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

DIRECT ACCESS BENEFITS

Referrals are not usually needed for specialist visits, including

routine eye exams and gynecological/obstetrical care. However,

certain laboratory procedures and X-Ray service care must be

pre-certified by your physician prior to the visit

EMERGENCY CARE

Emergency services are covered anytime, anywhere in an out of

network. If you need emergency care, here are some basic

guidelines:

Go to the nearest emergency room or call 911. If a delay

would not be detrimental to your health, call your doctor

first.

To avoid a long wait in the emergency room, you can visit

any participating urgent care facility in your area.

If you’re admitted to the hospital, you or a family member

should notify your doctor or United Healthcare.

UNITED BEHAVIORAL HEALTH

United Behavioral Health offers confidential, comprehensive

services and a wide array of treatment options from acute inpa-

tient care to individual outpatient counseling. When you call

United Behavioral Health for assistance, you will speak directly

to a mental health professional who can answer questions relat-

ed to the mental health and substance abuse benefits. United

Behavioral Health program specializes in depression, stress &

anxiety, child/adolescent issues, phobias, personality disorders,

anorexia & bulimia, post traumatic syndrome, alcohol and

chemical dependency.

CARE COORDINATION

United Healthcare, is able to identify, quantify and address the

fragmentation of care that comprises health outcomes. Their

Care Coordinationsm approach goes beyond traditional medical

coverage and preventive services and fill gaps in care. Care

Coordination focuses on offering education, accelerating access

to care and providing early identification and monitoring of

chronic conditions. They are:

Health education and reminder programs

Admission counseling

Inpatient care advocacy

Welcome Home!sm (readmission prevention)

IMPACTsm (complex illness support)

PROVIDER DIRECTORIES

To find a participating providers prior to the effective date of

your coverage, go to www.uhc.com. Once you are enrolled you

can access this information at www.myuhc.com.

MYUHC.COM

MyUHC.com gives you access to tools and information so

you may:

View benefit and claim information

Find a physician

Print a temporary ID card

Request a replacement ID card

View preferred drug lists and prescription history

Order prescription and over the counter products through

home delivery service

Set up email reminders for prescription refills

MEMBER SERVICES

Member Service representatives are trained to answer your

questions concerning your health plan benefits. Call the toll-

free number on your ID card to:

Ask about your benefits

Request another ID card

RX HOME DELIVERY

Home delivery saves time and money. Through a partnership

with Optum you can have prescriptions medications and other

health and beauty products sent right to your home. There is

NO added shipping or handling fees for prescriptions.

The following information is provided under your pharmaceu-

tical needs at www.myuhc.com:

View personal benefit coverage information and prescrip-

tion history

Search the Preferred Drug List online

Order Prescription and over the counter drugs for home

delivery

myNurseLineSM

Reliable health information from registered nurses available

24 hours / 7 days a week by calling 800-846-4678. Receive

immediate answers from nurses backed by medical profes-

sionals who can help you:

Understand you current symptoms

Decide if you should see a doctor or go to the ER

Find a network doctor or hospital

Explore treatment options

Learn more about a diagnosis

Understand you medications

Medical

7 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

GOLD Coverage Choice In-Network Only In-Network Out-of-Network

Lifetime Maximum Unlimited

Calendar Year Deductible (CYD) $575 Individual

$1,150 Family No Coverage

Out of Pocket Maximums (Includes deductible, coinsurance, co-pays; excludes Rx)

$2,000 Individual

$4,000 Family No Coverage

Co-Insurance 80% / 20% No Coverage

Well Child Care /Immunizations

100% No Coverage

Routine Adult Physicals 100% No Coverage

Primary Physician Office Visit $25 Copay No Coverage

Specialty Care Physician Office Visit $40 Copay No Coverage

Emergency Room (Facility) $200 Copay $200 Copay

Urgent Care $50 Copay No Coverage

In-Patient Hospitalization CYD then 20% No Coverage

Out-Patient Hospitalization CYD then 20% No Coverage

Laboratory and Radiology Services Covered at 100% No Coverage

Advanced Radiological Imaging (CT Scans, PET Scans, MRI, MRA & Nuclear Medicine) CYD then 20% No Coverage

Chiropractic Care

$40 Copay

No Coverage

In-Patient Mental Health and Substance Abuse (MH/SA) Treatment CYD then 20% No Coverage

Office visit Mental Health and Substance Abuse (MH/SA) Treatment $25 Copay (varies depending on treatment type)

No Coverage

*Prescription Drug Co-Payments

(30 day supply) Tier 1

Tier 2

Tier 3

Mail Order Prescription Drug

(31-90 day supply)

$15 Copay

$25 Copay

$60 Copay

$30/$50/$120 Copay

No Coverage

Medical

Payroll Deductions (26 pay periods)

Coverage Option GOLD - Non-Tobacco GOLD - Tobacco

Employee

Employee & 1

Employee & 2+

$62.40

$210.00

$240.00

$65.90

$213.50

$243.50 GOLD

8 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

SILVER Coverage Choice In-Network Only In-Network Out-of-Network

Lifetime Maximum Unlimited No Coverage

Calendar Year Deductible (CYD) $1,000 Individual

$3,000 Family No Coverage

Out of Pocket Maximums (Includes deductible, coinsurance, co-pays; excludes Rx)

$3,500 Individual

$7,000 Family No Coverage

Co-Insurance 80% / 20% No Coverage

Well Child Care Exams/ Immunization 100% No Coverage

Routine Adult Physical Exams 100% No Coverage

Primary Physician Office Visit $25 Copay No Coverage

Specialty Physician Office Visit $50 Copay No Coverage

Emergency Room Co-Payment (Facility) $200 Copay $200 Copay

Urgent Care $75 Copay No Coverage

In-Patient Hospitalization CYD then 20% No Coverage

Out-Patient Hospitalization CYD then 20% No Coverage

Laboratory and Radiology Services Co-Payment

Covered at 100% No Coverage

Advanced Radiological Imaging Co-Payment (CT Scans, PET Scans, MRI, MRA & Nuclear Medicine)

CYD then 20% No Coverage

Chiropractic Care Co-Payment $50 Copay No Coverage

In-Patient Mental Health and Substance Abuse (MH/SA) Treatment

CYD then 20% No Coverage

Office visit Mental Health and Substance Abuse (MH/SA) Treatment $25 Copay (varies depending on treatment type)

No Coverage

*Prescription Drug Co-Payments

(30 day supply) Tier 1

Tier 2

Tier 3

Mail Order Prescription Drug

(31-90 day supply)

$30 Copay

$50 Copay

$100 Copay

$60/$100/$200 Copay

No Coverage

Medical

Payroll Deductions (26 pay periods)

Coverage Option SILVER - Non-Tobacco SILVER - Tobacco

Employee

Employee & 1

Employee & 2+

$41.63

$175.00

$210.00

$45.13

$178.50

$213.50 SILVER

9 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

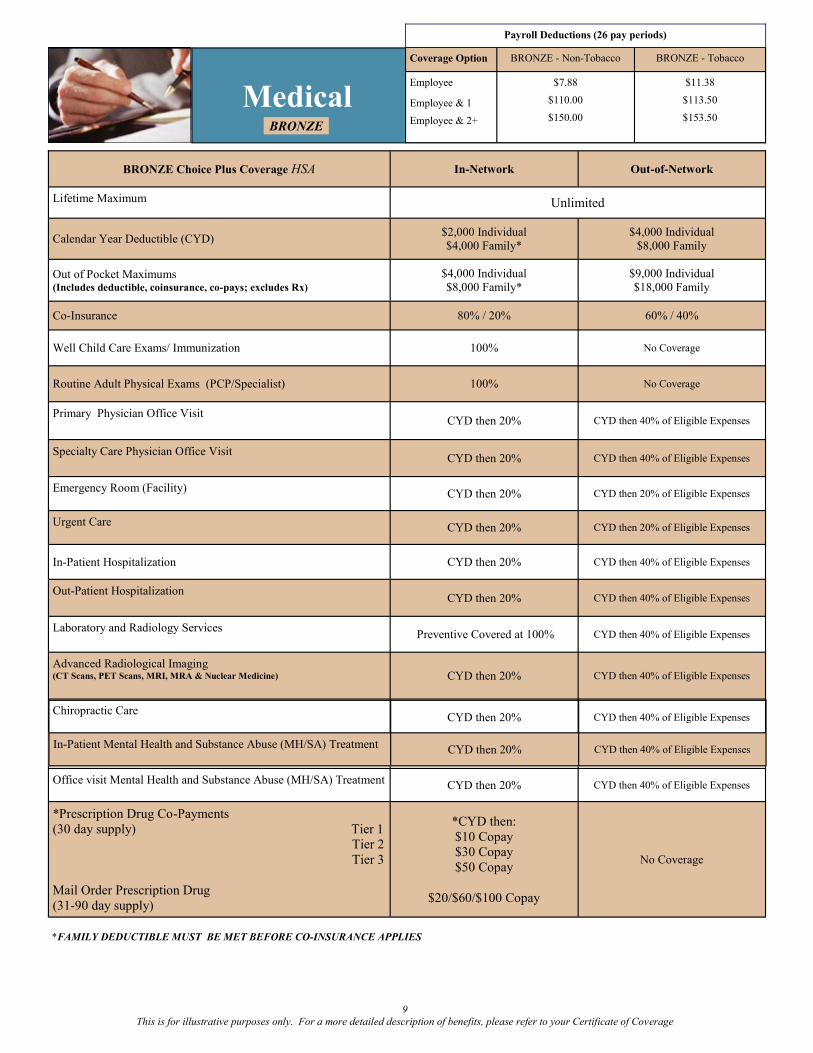

BRONZE Choice Plus Coverage HSA In-Network Out-of-Network

Lifetime Maximum Unlimited

Calendar Year Deductible (CYD) $2,000 Individual

$4,000 Family*

$4,000 Individual

$8,000 Family

Out of Pocket Maximums (Includes deductible, coinsurance, co-pays; excludes Rx)

$4,000 Individual

$8,000 Family*

$9,000 Individual

$18,000 Family

Co-Insurance 80% / 20% 60% / 40%

Well Child Care Exams/ Immunization 100% No Coverage

Routine Adult Physical Exams (PCP/Specialist) 100% No Coverage

Primary Physician Office Visit CYD then 20% CYD then 40% of Eligible Expenses

Specialty Care Physician Office Visit CYD then 20% CYD then 40% of Eligible Expenses

Emergency Room (Facility) CYD then 20% CYD then 20% of Eligible Expenses

Urgent Care CYD then 20% CYD then 20% of Eligible Expenses

In-Patient Hospitalization CYD then 20% CYD then 40% of Eligible Expenses

Out-Patient Hospitalization CYD then 20% CYD then 40% of Eligible Expenses

Laboratory and Radiology Services

Preventive Covered at 100% CYD then 40% of Eligible Expenses

Advanced Radiological Imaging (CT Scans, PET Scans, MRI, MRA & Nuclear Medicine) CYD then 20% CYD then 40% of Eligible Expenses

Chiropractic Care

CYD then 20% CYD then 40% of Eligible Expenses

Office visit Mental Health and Substance Abuse (MH/SA) Treatment CYD then 20% CYD then 40% of Eligible Expenses

*Prescription Drug Co-Payments

(30 day supply) Tier 1

Tier 2

Tier 3

Mail Order Prescription Drug

(31-90 day supply)

*CYD then:

$10 Copay

$30 Copay

$50 Copay

$20/$60/$100 Copay

No Coverage

Medical

*FAMILY DEDUCTIBLE MUST BE MET BEFORE CO-INSURANCE APPLIES

Payroll Deductions (26 pay periods)

Coverage Option BRONZE - Non-Tobacco BRONZE - Tobacco

Employee

Employee & 1

Employee & 2+

$7.88

$110.00

$150.00

$11.38

$113.50

$153.50 BRONZE

In-Patient Mental Health and Substance Abuse (MH/SA) Treatment

CYD then 20% CYD then 40% of Eligible Expenses

10 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Health Savings

Account (HSA)

A Health Savings Account (HSA) is a tax-preferred account that may be opened by individuals covered by a Qualified High Deduct-

ible Health Plan (HDHP). If you are enrolled in Bronze plan, and are otherwise qualified, you have the option of opening an HSA.

HOW AN HSA WORKS

Part 1:

Qualifying High

Deductible Health

Insurance Plan

2015

Employee Only Coverage $ 3,350

Family Coverage $ 6,550

Catch Up Contributions $ 1,000

WHY OPEN A HEALTH SAVINGS ACCOUNT

An HSA can be used to accumulate funds on a tax-free basis

to pay for qualified health care expenses, as defined by the

Internal Revenue Service (IRS). The account acts like a regu-

lar bank account with a debit card and/or checkbook, and ac-

crues interest. Depositing funds in your HSA through pay-

roll deductions can help you be prepared for expenses that

you incur before your deductible is met. The account is

owned by you and funds can accumulate over time. The ac-

count is portable among employers.

WHO CAN OPEN A HEALTH SAVINGS ACCOUNT

The IRS has established guidelines on individuals qualified to

open an HSA. You must be:

Covered by a Qualified High Deductible Health Plan, and

Not covered by any other plan that is not a Qualified

High Deductible Health Plan

Not enrolled in Medicare or Medicaid

Not eligible to be claimed as a dependent on another’s

tax return

Not covered under an unlimited FSA or HRA

PERMISSIBLE INSURANCE WITH A HSA

Coverage under certain types of insurance policies will not

affect your ability to open an HSA. Permissible insurances

include:

Workers Compensation

Disability insurance

Dental insurance

Vision insurance

Specific Disease policies (Accident, Cancer, etc.)

Long Term Care insurance

MAXIMUM CONTRIBUTION LIMITS

The maximum amount that can be deposited, from all sources,

into the HSA each calendar year is established by the IRS and

whether you have employee only coverage or family cover-

age. HSA contributions are separate from, and in addition to,

the premium you pay for your Qualified High Deductible

Health Plan. HSA contributions may be made through pay-

roll deductions on a pre-tax basis, or you can make contribu-

tions directly to your HSA. You may contribute any amount

up to the maximums shown below. Individuals age 55 and

older can make “Catch-Up Contributions” in addition to the

maximum annual contribution limits.

Pays for out-of-pocket

expenses incurred before

the deductible is met.

Part 2:

Health Savings

Account

(HSA)

1. Employee enrolls in a Qualified High Deductible

Health Plan (HDHP).

2. Employee opens an HSA (encouraged, but not re-

quired) and provides account information to Human

Resources.

3. Employee makes deposits to their HSA account

through pre-tax payroll deductions (encouraged, but not

required).

4. Employee or covered Dependent seeks medical

services.

5. Medical services are covered by the HDHP, subject

to a deductible and coinsurance.

6. Employee may use their HSA account to pay for

qualified medical expenses, including those applied to

their deductible and coinsurance.

The Deductible is waived for Preventive care. Refer

to the Benefit Summary for additional information.

Employees may also make deposits directly to their

HSA account without going through payroll.

Intended to cover serious

illness or injury after the

deductible has been met.

11 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

HSA FREQUENTLY ASKED QUESTIONS

What is a qualified High Deductible Health Plan?

The IRS has established guidelines on the minimum in-

network deductibles and out-of-pocket maximums for quali-

fied plans. The plan must also require that the deductible

apply to all services, including prescriptions. The only excep-

tion is that the plan may pay for preventive care without hav-

ing to meet the deductible. The United Healthcare plans are

qualified High Deductible Health Plans.

What happens to the money in my HSA at the end of the

year?

The funds remain in your account, continue to earn interest,

and are available to pay for qualified expenses tax free in the

future.

What happens if I go over the maximum contribution?

If your deposits (including contributions from all sources)

exceed the maximum contribution limit you will be required

to pay income tax and penalty tax on the excess amount. This

is also the case if you do not remain covered for the entire

testing period and your contributions exceed the pro-rated

contribution limit. Excess contributions can be withdrawn

without tax penalties if the withdraw is completed prior to

your tax filing deadline. Contact your HSA trustee and/or

your tax advisor for assistance.

What happens to the money in my HSA if I decide next

year to go back to a non-qualified plan?

The money is yours to keep. You can no longer deposit addi-

tional money into the account if you are not HSA eligible, but

you can continue to use the funds tax-free to pay for qualified

expenses or you can let the funds stay there and accumulate

interest.

What happens to the money in my HSA if I leave my cur-

rent employer?

The money in the HSA is yours to keep. If you remain HSA

eligible, you can continue to make contributions directly to

your HSA. If you do not remain HSA eligible, you can no

longer deposit additional money into the account, but you can

continue to use the funds tax-free to pay for qualified expens-

es or you can let the funds stay there and accumulate interest.

Can my spouse have an HSA?

Yes, provided he/she is covered under a qualified High De-

ductible Health Plan. If both spouses have HSA’s, the maxi-

mum family contribution as defined by the IRS each year is

divided equally between them unless both spouses agree on a

different division. If both spouses are 55 or over, they can

both make “Catch-Up Contributions” in addition to the fami-

ly maximum.

Can I use my HSA to pay for my family’s qualified ex-

penses if they are not covered under my health plan?

Yes, as long as the expense is not reimbursed by another

health plan, you may use your HSA to pay for qualified ex-

penses incurred by you, your spouse, and your dependent

children., even if they are not covered on the qualified health

plan.

What happens if I don’t have enough money in my HSA to

cover the charge?

You will need to pay the provider from another source. You

can later reimburse yourself when the funds are available in

your HSA, if you choose to do so. Remember to keep all

receipts to show that the funds were withdrawn for a qualified

expense.

If I use all the money in my HSA early in the year can I

put more in?

You can not exceed the maximum contribution limits for the

calendar year, even if some of that money was taken out to

pay for qualified expenses. You will be able to deposit addi-

tional funds in the next calendar year, if you remain HSA

eligible.

Can I use my HSA to pay for my dental and expenses?

Yes, as long as the expense was not reimbursed by another

plan. However, dental expenses will not help you meet the

deductible on your health plan.

Why should I choose an HSA?

1. Cost Savings

Reduction in medical plan premium (payroll deduction)

Tax benefits

HSA contributions are excluded from federal income

tax

Withdrawals for eligible expenses are exempt from

federal income tax

Unused money is held in an interest-bearing account

2. Long-term financial benefits

Save for future medical expenses

Unused funds roll over year to year

This is your account, you take it with you

3. Choice

You control and manage your health care expenses.

You choose whether to use your HSA dollars to pay

your health care expenses or to save them for future use.

12 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Dental

PPO DMO

(Co-Payment Schedules)

Benefit Description In-Network Out-of Network In-Network Only

YOU PAY YOU PAY YOU PAY

Preventive Services

Cleanings, oral exams

0%

Deductible Waived

0%

Deductible Waived

See schedule of benefits

(see next page)

Basic Services

Oral Surgery-Simple extractions, fillings

Periodontics

Deductible then 20% Deductible then 20%

of eligible expenses

See schedule of benefits

(see next page)

Major Services Crowns, Dentures, Bridges

Deductible then 50% Deductible then 50%

of eligible expenses

See schedule of benefits

(see next page)

Orthodontic Services

50%

Child to Age 19 Only

$1,000 Lifetime Maximum 50%

See schedule of benefits,

Adult and Child Ortho is covered

Calendar Year Maximum $1,500 Per Person No Annual Maximum

Calendar Year Deductible

Per Person

Per Family

$50

$150

$50

$150

No Deductible

Payroll Deduction (26 pay periods)

Coverage Option Dental PPO Plan DMO Plan

Employee

Employee & 1

Employee & 2+

$13.72

$26.85

$45.37

$6.93

$12.15

$18.02

PRE-DETERMINATION REVIEW

When the expected cost of a proposed course of treatment is

$200 or more, United Healthcare will review the treatment plan

and let your dentist know what benefits could be payable. Simp-

ly ask your dentist to fax your treatment plan to United

Healthcare and request a Pre-Determination Review prior to re-

ceiving care.

SPECIAL LIMITATION

Teeth lost or missing before a covered person becomes insured

by this plan. The plan won’t pay for a prosthetic device which

replaces such teeth unless the device also replaces one or more

natural teeth lost or extracted after the covered person became

insured by this plan.

WWW.MYUHCDENTAL.COM

You can access your dental plan 24 hours a day, 7 days a

week at www.myuhcdental.com. Once registered you can

search for a participating dentist, review your claims, view

your remaining Calendar Year Benefit, and much more!

LATE ENTRANT PENALTIES

If you decline this coverage now, and choose to enroll later,

you may be subject to late entrant penalties. Late Entrant

penalties may be waived during Open Enrollment.

13 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Dental (DMO Sample Fee Schedule)

14 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Eye Examination In-Network Out-of-Network

Co-Payment $10 No Coverage

Frequency Every 12 months No Coverage

Frames In-Network Out-of-Network

Coverage $25 Co-Payment

$130 retail allowance $61 retail allowance

Frequency Every 24 months Every 24 months

Lenses In-Network Out-of-Network

Coverage $25 Co-Payment then Covered in Full –

plastic or glass lenses

Allowance

$40 Single Lens

$60 Bifocal Lens

$80 Trifocal Lens

$80 Lenticular Lens

Frequency Every 12 months Every 12 months

Contacts In-Network Out-of-Network

Coverage

$25 Co-Payment

$125 retail allowance if Elective

Covered in Full if Therapeutic

$125 retail allowance if Elective

$210 retail allowance if Therapeutic

Frequency Every 12 Months in lieu of glasses Every 12 Months in lieu of glasses

Vision

SUMMARY OF BENEFITS

Vision Coverage is available through United Healthcare. Please register at myuhcvision.com to print your Vision ID card.

Payroll Deduction (26 pay periods)

Coverage Option

Employee

Employee & 1

Employee & 2+

$2.63

$4.79

$8.30

15 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

BASIC LIFE COVERAGE

Aspire Health Partners provides all full time employees (at no

cost to you) with basic life insurance coverage equal to one

times your annual salary up to $300,000. Lincoln Financial is

the carrier for your basic life benefit.

VOLUNTARY LIFE

Full time employees may purchase additional voluntary life

insurance for themselves and their dependents.

AGE REDUCTION

(Applies to Basic & Voluntary Life) At age 70, the benefit amount will be reduced by 40% and at

age 75 the benefit amount will be reduced by an additional

10%. Benefits will terminate upon retirement.

CONVERSION POLICY

(Applies to Basic & Voluntary Life)

Allows a covered person whose life insurance coverage ends to

obtain an individual policy at his/her expense, without provid-

ing evidence of insurability. A covered person may convert all

or part of the coverage. The premiums will be based on the

amount of coverage and the covered person’s age and class of

risk at the time of conversion (Subject to state requirements).

PORTABILITY COVERAGE

(Applies to Voluntary Life ONLY)

This feature allows a covered employee, whose optional life

coverage ceases, the right to continue all or a portion of his/her

optional life benefit. A covered employee may make a written

request to continue his or her benefits during the Request Peri-

od, which is 31 days after coverage ceases.

GUARANTEE ISSUE

If you are enrolling during your initial eligibility period Medical

Underwriting is required for amounts over the guarantee issue.

• Employee: $250,000 under age 70

• Spouse: $30,000 for your spouse.

• Children: $10,000 from 6 months to age 19

• Dependent children up to age 25 if unmarried and

a full time student

Life Insurance

You must complete an Evidence of Insurability form for

submission to be approved in the following circumstances:

A) If you are electing coverage for yourself or your spouse

over the guarantee issue amounts.

PLEASE NOTE THAT YOU MUST BE APPROVED FOR COV-

ERAGE BEFORE YOUR PAYROLL DEDUCTIONS WILL

BEGIN. You can obtain an Evidence of Insurability Form by con-

tacting Human Resources.

COVERAGE CHOICES

Age Spouse Rate is determined by using

Employee’s Age

Payroll Deduction Rates Per

$1,000

of Coverage

Under 30 0.028

30-34 0.028

35-39 0.042

40-44 0.069

45-49 0.106

50-54 0.203

55-59 0.318

60-64 0.346

65-69 0.637

70+ 1.306

All Children (over 6 months of age

to age 19 or 25 if full time student)

0.92/ $10,000

Employee Spouse Child (ren)

Increments 1, 2, 3, 4, 5x Salary $1,000 $10,000

Minimum Amount $10,000 $5,000 $10,000

Maximum Amount

5x annual salary

(rounded to the nearest

$1,000) or $500,000,

whichever is lower

50% of Employee

amount (rounded

down to the nearest

$1,000) or $100,000,

whichever is lower

$10,000

Guarantee Issue

Amount

$250,000 under age 70 $30,000 under age 60 $10,000

To Calculate Payroll Deduction: 1) Determine if you want to elect 1, 2, 3, 4 or 5 x your salary

2) Round up to the next $1,000

3) Divide the amount you elect by 1,000 4) Multiply the amount in # 2 times the corresponding rate in the table

Example: John is 42, his salary is $40,000. He elects the amount of

$80,000:

1) $80,000

2) $80,000 / 1,000 = 80

3) 80 x 0.069 = $5.52 = payroll deduction

16 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Disability coverage is designed to replace a portion of your

income should you become unable to work due to a non-work

related accident or illness. Please refer to your summaries for

additional details, including limitations and exclusions.

ELIMINATION PERIOD:

Benefits begin on the 8th day after a non work related injury

or illness.

INCOME BENEFIT:

66.67% of your income to a maximum of $1,000 per week if

you are unable to work due to an injury or illness.

DURATION:

You may receive benefits for up to 13 week if you continue to

be disabled and are unable to work.

PRE-EXISTING CONDITIONS:

If you have been treated for a condition in the 3 months prior

to the effective date, that condition will not be covered for

the first 6 months of coverage.

EVIDENCE OF GOOD HEALTH

If you are enrolling during an annual open enrollment period

and previously waived this coverage you must first complete

an Evidence of Insurability Form prior to benefits being ap-

proved. Coverage and/or Payroll Deductions will not begin

until this approval process is complete.

HOW TO CALCULATE YOUR PAYROLL

DEDUCTION

The cost for the voluntary short term disability plan is based

upon your weekly benefit. If you would like to calculate your

payroll deduction, please follow the formula outlined below.

The amount is based on your weekly rate excluding overtime

compensation.

Short-Term

Disability

APPROXIMATE BIWEEKLY PAYROLL DEDUCTION

COSTS FOR VOLUNTARY SHORT TERM DISABILITY

(Use this chart to determine the approximate

payroll deductions )

HOW TO CALCULATE VOLUNTARY STD PAYROLL DEDUCTIONS

Base Annual Income Weekly Income STD Weekly Benefit Per $10 Increment Multiply by Rate Payroll Deduction

$24,000

(÷) Divide by 52

$461.54

(x) Multiply by 0.6667

$307.71

(÷) Divide by $10

$30.77

(x) Multiply by 0.83

$25.54

(x) Multiply by 12 and divide by 26

$11.79

Weekly Earnings STD Weekly Benefit

Rate $0.83

$200 $133 $5.11

$250 $167 $6.38

$300 $200 $7.66

$350 $233 $8.94

$400 $267 $10.22

$450 $300 $11.49

$500 $333 $12.77

$550 $367 $14.05

$600 $400 $15.32

$650 $433 $16.60

$700 $467 $17.88

$750 $500 $19.15

$800 $533 $20.43

$850 $567 $21.71

$900 $600 $22.99

$950 $633 $24.26

$1,000 $667 $25.54

$1,050 $700 $26.82

$1,100 $733 $28.09

$1,200 $800 $30.65

$1,250 $833 $31.92

$1,300 $867 $33.20

$1,350 $900 $34.48

$1,400 $933 $35.76

17 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Disability coverage is designed to replace a portion of your in-

come should you become unable to work due to a non-work re-

lated accident or illness. Please refer to your summaries for addi-

tional details, including limitations and exclusions.

ELIMINATION PERIOD:

Benefits begin on the 91st day after a non work related injury or

illness.

INCOME BENEFIT:

60% of your income to a maximum of $6,000 per month if you

are unable to work due to injury or illness.

DURATION:

Benefits are payable to your normal social security retirement

age if you continue to be disabled and unable to work.

PRE-EXISTING CONDITIONS:

If you have been treated for a condition in the 3 months prior to

the effective date, that condition will not be covered for the first

6 months of coverage.

EVIDENCE OF GOOD HEALTH

If you are enrolling during an annual open enrollment period and

previously waived this coverage you must first complete an Evi-

dence of Insurability Form prior to benefits being approved. Cov-

erage and/or Payroll Deductions will not begin until this approval

process is complete.

EVIDENCE OF GOOD HEALTH

If you are enrolling for the first time and still within your ini-

tial eligibility period, you will not be required to complete an

Evidence of Insurability Form. If you are enrolling during an

annual open enrollment period and previously waived this

coverage you must first complete an Evidence of Insurability

Form prior to benefits being approved. Coverage and/or Pay-

roll Deductions will not begin until this approval process is

complete.

Please note that you do not have to enroll in both Short Term

Disability and Long Term Disability. You may choose both

plans or just one of the plans.

Long-Term

Disability

HOW TO CALCULATE LTD PAYROLL DEDUCTIONS

(determine the approximate payroll deductions )

Annual

Income

Monthly Income Per $100 Increment Multiply by Rate 0.93 Convert monthly deduction to 26 Pay Periods

$24,000

(÷) Divide by 12

$2,000

(÷) Divide by $100

$20.00

(x) Multiply by 0.93

$18.60

(x) Multiply by 12 months and (÷) divide by the 26 pay periods

$8.58

18 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

FLEX SPENDING ACCOUNTS

JANUARY 1, 2015 TO DECEMBER 31, 2015

Employees have a choice of two FSA plans, which create an

opportunity to save on taxes. Money is deducted from you

pay and contributed to the accounts on a pre-tax basis so that

taxes aren't paid on eligible expenses.

HEALTHCARE ACCOUNT

Allows you to reimburse yourself with pre-tax dollars, from a

minimum of $300 up to $2,500 in eligible expenses not reim-

bursed under any healthcare plan.

HOW IT WORKS

During the enrollment period, you decide how much

you want to contribute to each account.

Each pay period, the appropriate amount is deducted

(before taxes) and contributed to your account.

When incurring an eligible expense you may either pay

for the services at that time and then submit the expense

for reimbursement or use the debit MasterCard.

If you do not use your debit card, you must submit a claim

form to in order to be reimbursed. You must attach either a

copy of your Explanation of Benefits or a paid receipt.

You have three months after the end of the plan year to submit

claims incurred during the previous year. Claims incurred during

one plan year cannot be submitted for reimbursement from con-

tributions made to your account during any other plan year.

CARRYOVER PROVISION

Amounts allocated to the Health FSA that are unused at the

end of the Plan Year (determined as of the last day of the Run

-Out Period for that Plan Year) up to a maximum of $500

may be used to reimburse Eligible Medical Expenses incurred

in the current Plan Year.

ELIGIBLE HEALTHCARE EXPENSES

The general rule is that any medical expense that is deductible

on your federal income tax return may be reimbursed through

the healthcare flex spending account.

Flexible Spending

Account

HOW THE FLEX ACCOUNT WORKS WITH THE HSA

ACCOUNT (Limited Flex Account)

You may continue to use your debit MasterCard to pay for un-

reimbursed expenses on anything other than medical expenses.

You must use the funds in your HSA account to cover any out of

pocket expenses you incur as a result of obtaining medical care.

Out of pocket expenses for things like dental work and eyeglass-

es would still be covered under the debt MasterCard.

You are responsible to provide receipts, if request-

ed for all transactions processed by the Debit Card.

EXAMPLES OF ELIGIBLE EXPENSES

Alcoholism treat-

ment

Artificial limbs

Car control for the

handicapped

Chiropractor fees

Christian Science

practitioner fees

Contact Lenses

Crutches

Dental fees

Doctor fees

Eyeglasses

Guide Dog

Hearing Aids

Hospital Services

In vitro fertilization

Lab fees

Learning disability

tuition, if referred by

a physician

Nursing services

Optometrist fees

Orthopedics shoes

Oxygen

Orthodontics

Psychoanalysis

Special school for

the handicapped

Sterilization

Surgery

Telephones for

the deaf

Therapy

(medical)

Transplants of

organs

Transportation for

medical care

Wheelchairs

X-rays

EXAMPLES OF INELIGIBLE

HEALTHCARE EXPENSES

Health Clubs, spas,

and non prescribed

weight loss pro-

gram

Expenses covered

by another plan

Smoking cessation

education materi-

als and programs

Hair transplants

Over the counter

medications

Electrolysis

Teeth Whiten-

ing

Cosmetic Sur-

gery unless

medically nec-

essary

19 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

FSA (cont.) &

Direct Deposit

DEPENDENT CARE ACCOUNT

Allows you to reimburse yourself with pre-tax dollars for day-

care expenses for your children under age 13 and other quali-

fied dependents. You may contribute from a minimum of

$300 up to $5,000 a year.

MONEY LEFT IN THE ACCOUNT AFTER

TERMINATION OF EMPLOYMENT

If you have unused money in your account and you terminate

your employment, you must elect to continue the plan through

the COBRA program in order to have access to the unused

healthcare account funds.

EASY BALANCE ACCESS

An automated voice response system designed to provide parti

cipants of the Flexible Spending Account (FSA) and Depend-

ent Care Assistance (DCAP) easy access to their account bal-

ance. You may call Medcom’s regular number 800-523-7542

and continue to “press 1” until you enter the Easy Balance

System which is available around the clock 24/7. Participants

only need to enter their MasterCard debit number, type of

plan (FSA or DCAP), and zip code for primary card holder.

Eligible Day Care Expenses

Childcare/Adult Care by a licensed childcare facility for children

under age 13 who qualify as dependents on your federal income

tax return

Childcare/Adult Care for children or adult of any age who are

physically or mentally unable to care for themselves and who

qualify as dependents.

Ineligible Day Care Expenses

Child support payments

Food, clothing and entertain-

ment

Educational supplies and

activity fees

Cleaning and cooking services

not provided by the day care

provider

Overnight camp

DIRECT DEPOST & PAY CARDS

Aspire requires direct deposit, which means the electronic

deposit of your paycheck to a bank account or other account.

For employees with or without existing bank accounts, a

paycard is an alternative to using a bank account. Aspire has

teamed with two banks to offer a safe and convenient alterna-

tive to paper payroll checks.

FAQs

How does the Paycard VISA work?

Your net pay is automatically deposited to your paycard every

payday. You no longer have to come in person to Human Re-

sources to pick up a paper check. The paycard is a Visa pre-

paid card that will allow you to withdraw your money from

the bank, or use it for purchases at grocery stores, restaurants,

online, and other places you find the Visa logo.

When you pick up your first paycard, you will also get in-

structions for using the card and a schedule of fees. You will

need to call and activate your card before using it for the first

time. You will be asked to confirm personal information to

ensure you are truly the cardholder. If you do not activate the

card, you will not be able to use it.

How does the paycard benefit me?

Having a paycard means no check-cashing fees, no more wor-

ry about how you will pick up your paycheck in the rain or if

you are on vacation, and you have instant access to your mon-

ey on payday instead of waiting for a paper check to be depos-

ited to your account! All of your pay stub information can be

viewed on the employee portal.

How much does it cost? Your paycard is free for most transactions. There are no

monthly charges and you are only charged a fee if you exceed

the free transaction limits. The schedule of fees will be pro-

vided when you receive your paycard.

More information on Direct Deposit and Paycards can be ob-

tained from your HR or PR office.

20 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Retirement Plan

403(b) RETIREMENT PLAN

Providing a retirement plan that lets you save for the future is

important to us. To better serve all of our Aspire employees

and offer the best possible services and benefits we have

teamed up with Transamerica Retirement Solutions.

WHAT YOU NEED TO DO:

Step 1: Review the highlights of the Aspire Health Partners

Retirement Plan. You can find them along with other

valuable information in the enrollment book located under the

plan information tab at aspire2retire.trsretire.com.

Step 2: Join the plan by visiting aspire2retire.trsretire.com and

selecting "New user? Get started now." Establish a customer

ID and password.

Step 3: You may choose to make pretax contributions up to

the maximum allowed by law. Transamerica Retirement Solu-

tion's free auto-increase service allows you to raise your plan

contribution rate once a year by an amount you choose. You

can sign up for the auto-increase service online at aspire2re-

tire.trsretire.com.

You may designate your contributions as traditional pretax

contributions, after-tax Roth contributions, or a combination

of both.

You should evaluate your ability to continue the auto-increase

service in the event of a prolonged market decline, unexpected

expenses, or an unforeseeable emergency.

Step 4: Contribute enough to take full advantage of your em-

ployer's total contribution.

Aspire Health Partners provides a plan contribution of 2% of

compensation. You will receive the 2% plan contribution re-

gardless of whether you elect to defer into the plan or not.

You will begin receiving this contribution once you have

completed one year and 1,000 hours of service.

After one year and 1,000 hours of service, you are also eligible

to take advantage of your employer's matching contribution

which is based on your level of contribution:

• 4% Employee Contribution (payroll deduction)

2% (50% match on Employee's 4%)

+ 2% Employer Contribution

4% total Employer Contribution

8% Employee Contribution (payroll deduction)

4% (50% match on Employee's 8%)

+ 2% Employer Contribution

6% total Employer Contribution

Employer contributions will begin on either January 1 or July 1

-whichever date occurs first after you meet eligibility. You will

be 100% vested (all employer contributions belong to you)

once you have completed three years of service with any As-

pire Health Partners affiliate.

Matching contributions are subject to plan vesting require-

ments.

Step 5: Decide how your contributions will be invested among

the available investment options.

Designating a beneficiary: Designate at least one beneficiary

for your retirement account, so that your assets can be distrib-

uted according to your wishes upon your death. You can find

the Beneficiary Designation form under the plan information

tab at aspire2retire.trsretire.com.

.

21 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

WHAT IS PAID TIME OFF?

To reward employees for loyal and continuous service, Aspire

Health Partners provides a pre-determined number of paid days

off to observe such occasions as vacations, illness, medical

appointments, personal business or leave of absence.

The Paid Time Off (PTO) program gives you flexibility in

taking paid time off from work. Time away from work will

make you more productive when you are working. Under the

PTO program, you decide, with your supervisor’s approval at

least two weeks in advance, when and how you will use your

PTO hours.

HERE’S HOW IT WORKS

Time off for vacation, personal business, or personal and family

illness is taken utilizing PTO hours. You need to schedule your

time off at least two weeks in advance to allow more efficient

staffing throughout Aspire Health Partners.

ELIGIBILITY

If you are classified as a Full-Time (30+ hours) employee you

are eligible to accrue PTO based upon length of service to the

organization. A staff member is not eligible to use PTO hours

for the first 90 days of employment. You may schedule time off

based on your available hours. Under no circumstances will you

be able to borrow against PTO hours to be earned in the future,

or paid in advance of the regular payday for PTO hours.

PAYMENT METHOD

PTO hours are paid at your base hourly rate of pay in effect at

the time you use the hours.

PERIOD OF ACCRUAL

You accrue hours each pay period to a maximum amount of

320. When your accrued hours fall below 320, you will start

accruing again. The CSD (normally your date of hire) will

change if your status changes from a regular to a non-benefit

eligible position or vice versa.

ACCRUAL AMOUNTS

The chart at the bottom of the page details the maximum

number of hours you accrue in the PTO plan. The maximums

are based on a 80 hours per pay period.

SCHEDULED TIME OFF

Earned PTO hours will be used for personal business any time

during the year, provided such time off has management’s

approval. Jury duty and bereavement times are covered under

separate policies and do not come from the PTO bank.

Requests for PTO hours must be submitted on the appropriate

form with management authorization obtained in advance.

Approvals are made by the employee’s manager based on

periods convenient to the operations of the department.

Preferences for PTO hours will be granted whenever possible.

The approval of request for PTO hours is based on departmental

needs.

OBSERVED HOLIDAYS

Aspire Health Partners observes the following seven holidays:

New Year’s Day, Memorial Day, Independence Day (July 4th),

Labor Day, Thanksgiving Day, Christmas Day and “Floating

Holiday”.

PTO HARDSHIP CASH-OUT PROVISIONS

A PTO hardship is defined as an unexpected expense which

would cause an interruption in the course of everyday living

such as a foreclosure or repossession of property, major repair

for living quarters or transportation. In order to be eligible to

cash out PTO hours due to a hardship case, the employee must

complete a PTO Hardship Request Form and have it approved

by Human Resources. The employee needs to have been

employed for over one year and leave a minimum balance of 80

hours after the cash out of PTO for hardship. Details explaining

the hardship will be required when completing the PTO

Hardship Request Form. Please note a PTO hardship is paid at

75% of the gross amount. A Hardship is not defined as:

Needing to lower the balance of PTO to prevent stoppage

of accrual

Payments for recurring expenses

Purchase of personal merchandise such as a car or furniture

Paid

Time Off

Years of Service Hours per pay period ANNUAL

Hour Days Weeks

0-1.99 3.85 100 12.50 2.5

2-4.99 6.15 160 20.00 4.0

5-8.99 7.08 184 23.00 4.6

9-13.99 8.00 208 26.00 5.2

14+ 9.24 240 30.00 6

22 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Critical Illness AFLAC

Voluntary Products

Benefits With Cancer Benefit

Heart Attack 100% Percentage of Principal Sum

Stroke 100% Percentage of Principal Sum

Major Organ Transplant 100% Percentage of Principal Sum

End-Stage Kidney Failure 100% Percentage of Principal Sum

Coronary Artery Bypass Graft Surgery 25% Percentage of Principal Sum

Diagnosis of Cancer - Invasive 100% Percentage of Principal Sum

Diagnosis of Cancer In Situ 25% Percentage of Principal Sum

Subsequent Diagnosis of Different Illness Original Percentage of face amount

Time separation for recurrence 90 Days between different illnesses

Available Coverage

Employee 20,000

Spouse 10,000

Child $5,000 at no charge

Guarantee Issue

Employee $20,000

Spouse $10,000

Child (to age 26) None

Health Assessment Benefit (Wellness) $50 subject to 30 day waiting period

Pre-Existng Conditional Limitations 6/12

Benefit Reduction None

Limit on Number / Amount of Claims Each claim category will be paid once

Waiting Period 30 Days

CRITICAL ILLNESS

A critical illness plan helps prepare you for the added costs of battling a specific critical illness. The good news is that many peo-

ple with a specified critical illness survive these life-threatening battles. Unfortunately, as the recovery process begins, people

become aware of the unexpected bills that have piled up. Your recovery doesn’t have to be spoiled by unexpected bills. With this

plan, our goal is to help you and your family cope with and recover from the financial stress of surviving a specified critical ill-

ness. Listed below is a brief summary of the benefits.

AFLAC Critical Illness Bi-Weekly Payroll Deductions

EMPLOYEE $20,000 SPOUSE $10,000

ISSUE AGE BI WEEKLY ISSUE AGE BI WEEKLY

18-29 10.67 18-29 5.60

30-39 10.67 30-39 5.60

40-49 20.83 40-49 10.67

50-54 31.94 50-54 16.34

55-59 43.11 55-59 21.92

60-64 69.42 60-64 35.08

65-69 75.60 65-69 38.17

23 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Emergency Care

Ambulance $450

Emergency Room $300

Treatment Care

Hospital Admission $1,000

Hospital Confinement Daily Benefit $300 / Day up to 365 Days

Intensive Care Unit Daily Benefit $500 / Day up to 30 Days

Specific Injuries or Treatments

Blood $250

Joint Dislocation $400-$4,500 Closed / $600-$6,750

Spouse & Children paid at 50% of Employee Amount

Dental Crown $250

Laceration $50 - $400

Ruptured Disc $100 - $400

Fractures (Per Fracture)

Leg (knee to ankle) $3,600 / $5,400

Ankle, arm, bones of face, collarbone, elbow, foot,

hand, jaw, kneecap, shoulder blade, wrist $1,800-$3,000 / $2,700-$4,500

Accidental Death & Dismemberment

Accidental Death of Employee $75,000

Accidental Death of Spouse $37,500

Accidental Death of Child $10,000

Loss of or loss of use of one: hand, foot , arm, leg or

eye $18,750 EE / $9,375 SP / $2,500 CH

Catastrophic loss $37,500 EE / $18,750 SP / $10,000

Health Assessment Benefit (Wellness) $60 Subject to 12 month wait period

Pre-Existing Condition Limitations 6/12

Limit on Number / Amount of Claims Limited to 150% for multiple fractures or dislocations

Off Job Coverage

Payroll Deductions

Employee Only $5.84

Employee & Spouse $7.61

One Parent Family $10.75

Employee & Family (children to age 26) $12.52

Accident AFLAC

Voluntary Products

ACCIDENT

An accident insurance plan provides benefits to help cover the costs associated with unexpected bills. You don’t budget for accidents

if you’re like most people. When a Covered Accident occurs, the last thing on your mind is the charges that may be accumulating

while you’re at the emergency room. These costs add up—fast. You hope they never happen, but at some point you may take a trip to

your local emergency room. If that time comes, wouldn’t it be nice to have an insurance plan that pays benefits regardless of any

other insurance you have? This group accident plan does just that. Listed below is a brief summary of the Accident Policy.

24 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Employee

Assistance Plan

EmployeeConnect Services There are times when we all need a little help. No matter

what the issue, EAP Plus counseling services are availa-

ble 24 hours a day, seven days a week with confidential

support, guidance, and resources.

Assistance for you or an immediate household

family member.

Six in-person counseling sessions per person

per issue per year.

24 x 7 x 365 telephone and Web access.

Unlimited phone access to legal counsel.

25% discount for in-person legal services.

Work/life services for assistance with:

Parenting and Childcare

Eldercare

Relationships

Work and career

Financial

To learn more about the Lincoln Financial EmployeeConect

program visit:

www.Lincoln4Benefits.com or

www.GuidanceResources.com

(User name=LFGsupport; password=LFGsupport1)

or talk with a specialist at 1-888-628-4824.

LifeKeys Services When you choose life insurance, you’re planning for your

family’s future assuring their comfort and securing their

plans. With Lincoln Term Life Insurance, you can also access

services that make a real difference now as well as in the fu-

ture. LifeKeys services, included at no additional cost with all

Lincoln Term Life and Accidental Death and Dismemberment

Insurance policies, provide assistance to you, your family and

your beneficiaries.

EstateGuidance® Will Preparation

GuidanceResources® Online

Identity Theft

Legal Support

Other support services

To utilize LifeKeys services, please contact 1-855-891-3684

or visit GuidanceResources.com or

www.lincoln4benefits.com (WebID= LifeKeys)

TravelConnect Traveling just got easier.

An employee benefit that includes travel, medical, and safety

related services while traveling. Lincoln Financial has part-

nered with MEDEX Assistance Corporation, a worldwide

leader in travel assistance, to make this valuable benefit avail-

able to you and your immediate family members.

Business or leisure travel – it’s covered.

The TravelConnect benefit is provided at no cost to you and

includes a wealth of services when traveling just 100 miles or

more from home. These services are provided regardless if

you’re traveling for business or leisure. Whether you simply

want the weather forecast for your travel destination or you

need emergency medical assistance halfway around the

world, MEDEX has the professional staff and resources to

provide support, 24 hours a day, seven days a week.

Comprehensive coverage.

Just a sampling of the services includes:

Destination info – weather, currency, etc.

Emergency travel arrangements and funds transfer.

Lost or stolen travel documents assistance.

Language translation services.

Emergency medical evacuation and transportation.

Dependent child transportation if left unattended.

Medical and dental referrals.

Assistance with corrective lenses or medical device re-

placement.

Treatment monitoring of a medical situation.

Arrange delivery of medications, vaccines, or blood.

Updates to family, employer, and/or home physician.

Repatriation of a deceased traveler.

Security and political evacuation assistance.

Travel assistance services are subject to specific terms, condi-

tions and limitations. A program description is available at

www.lincoln4benefits.com. To use TravelConnect services,

call MEDEX at (800) 527-0218 or (410) 453-6330.

25 This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

Key

Contacts COMPANY CONTACT INFORMATION WEBSITE/ EMAIL

UNITED HEALTHCARE

Customer Service

866-844-4864 Gold and Silver

866-734-7970 Bronze

Claims: PO Box 740835

Atlanta, GA 30374

www.myuhc.com.

United Behavioral Mental Health:

800-582-8220 or 800-557-5745

UNITED HEALTHCARE

Dental 800-445-9090 www.myuhcdental.com

Vision 800-638-3120 www.myuhcvision.com

OPTUM BANK

Health Savings Account 866-234-8913 www.optumbank.com

LINCOLN FINANCIAL

Life Claims & Customer Service

Short-Term & Long-Term Disability 800-423-2765 www.lfg.com

LINCOLN FINANCIAL

Employee Assistance Program

EmployeeConnect Services 877-757-7587

LifeKeys Services 855-891-3684

TravelConnect 800-527-0218

www.lincoln4benefits.com

FLEXIBLE SPENDING ACCOUNT

Medcom

Customer Service

800-523-7542

Email claims to:

Check your debit card:

www.mywealthcareonline.com/medcom

LASSITER-WARE INSURANCE

Employee Customer Service

800-845-8437 ext. 605

Fax 888-883-8680 [email protected]

AFLAC VOLUNTARY PRODUCTS PORTFOLIO

AFLAC 800-443-3036

WebSite: www.aflac.com

Email: [email protected]

TRANSAMERICA RETIREMENT SOLUTIONS

Transamerica 800 755-5801 aspire2retire.trsretire.com

ASPIRE HEALTH PARTNERS

Human Resources Department

Jannette Mulero

407-875-3700 x6025

Linda Lovett

407-875-3700 x3222

This is for illustrative purposes only. For a more detailed description of benefits, please refer to your Certificate of Coverage

This Notice is provided as required by the Federal Health Insurance Portability and Accountability Act of 1996, as amended (“HIPAA”) and its regulations issued at 45 CFR Parts 160 through 164 (the “Privacy Regulations”). It is for partici-pants and beneficiaries in the (referred to as the “Plan”).

You are entitled to receive a notice of our procedures for protecting the privacy of your health information. “Protected Health Information” is information that identifies you and is related to your medical history for health care you receive or the payment for that care. We must follow the terms of the notice currently in effect. This notice describes how we may use or disclose your Protected Health Information and your rights regarding the use and disclosure of that information.