bes: future for hdtv powerpoint - 24_feb_2008... · • cameras/lenses. 34 thomson ldk-6000...

TRANSCRIPT

© Spectrum | Value Partners 2008.

This document is confidential and intended solely for the use and information of the addressee

BES:Future for HDTV

New Delhi

24 February 2008

1© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

Agenda

• HDTV global trends

• HDTV migration – costs and benefits

• Key issues to consider on migration

2© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

Convergencestrategy

Spectrum Value Partners – introduction

1.Public policy and licensing

2.Regulatory and licence bid support

3.Financial advisoryand litigation support

4.Mobile partnering

7.Strategic technology decisions

6.New business execution

8.Business improvement

5.Content partnering

3© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

SVP has strong developing market experience

Select Asian clients

Hong Kong

ChinaJapan

Taiwan

Singapore

Vietnam

Philippines

New Zealand

Macau

India

Nepal

Indonesia

Thailand

MalaysiaSri Lanka

Australia

4© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

Introduction - Where are we on HDTV ?

• Take-up of HD programming has been disappointing so far

– initially constrained by cost of HD sets (but only ~10% of HD sets receive HDTV!)

– geographical fragmentation (esp. in Europe)

– confusion on non broadcast media (but will improve with HD-DVD bowing out)

– regulatory issues (esp. on terrestrial transmission)

– customers not willing to pay for equipment apart from HD sets (esp. STBs)

• Yet awareness is much higher in most markets compared to other technologies (e.g. IP services, mobile telephony)

• Increasingly broadcasters are demanding that programmes be shot in HD

• Take-up of HD sets as a proportion of new purchases is encouraging …

– … but TV set replacement cycle is often 10 years; not 18 months like mobile

5© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

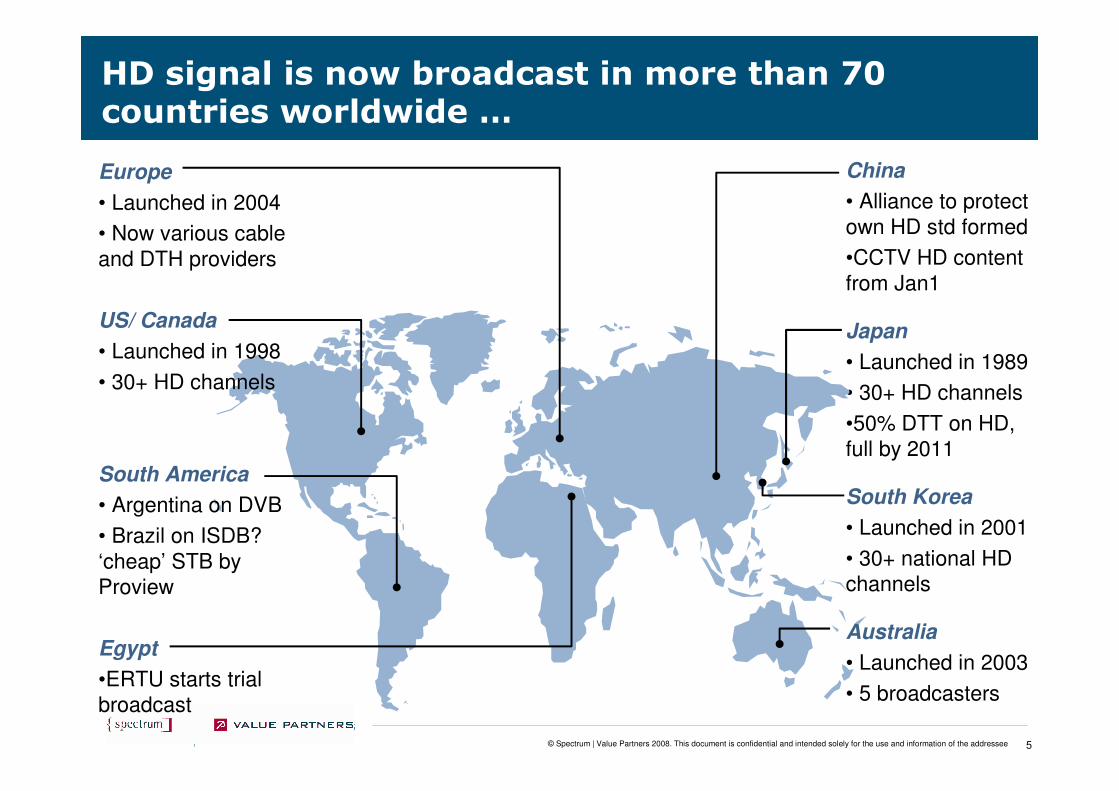

China

• Alliance to protect own HD std formed

•CCTV HD content from Jan1

Japan

• Launched in 1989

• 30+ HD channels

•50% DTT on HD, full by 2011

South Korea

• Launched in 2001

• 30+ national HD channels

Australia

• Launched in 2003

• 5 broadcasters

Europe

• Launched in 2004

• Now various cable and DTH providers

US/ Canada

• Launched in 1998

• 30+ HD channels

South America

• Argentina on DVB

• Brazil on ISDB? ‘cheap’ STB by Proview

Egypt

•ERTU starts trial broadcast

HD signal is now broadcast in more than 70 countries worldwide …

6© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

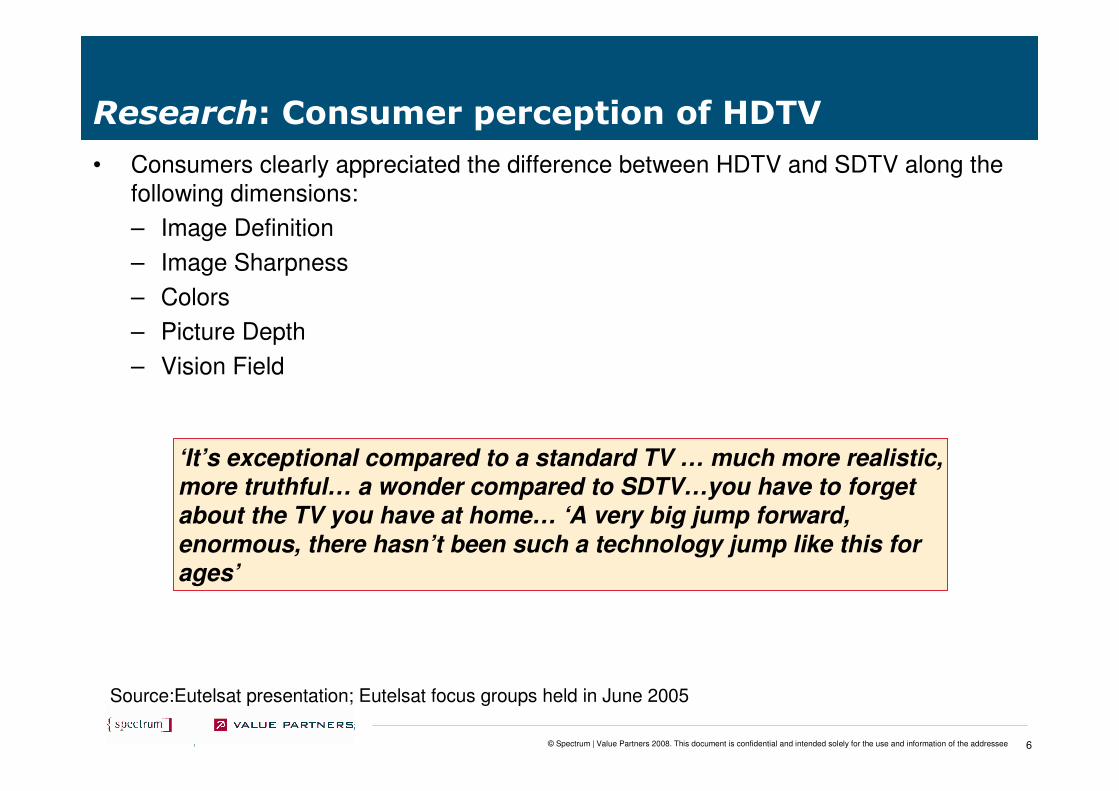

Research: Consumer perception of HDTV

• Consumers clearly appreciated the difference between HDTV and SDTV along the following dimensions:

– Image Definition

– Image Sharpness

– Colors

– Picture Depth

– Vision Field

Source:Eutelsat presentation; Eutelsat focus groups held in June 2005

‘It’s exceptional compared to a standard TV … much more realistic,

more truthful… a wonder compared to SDTV…you have to forget

about the TV you have at home… ‘A very big jump forward,

enormous, there hasn’t been such a technology jump like this for

ages’

7© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

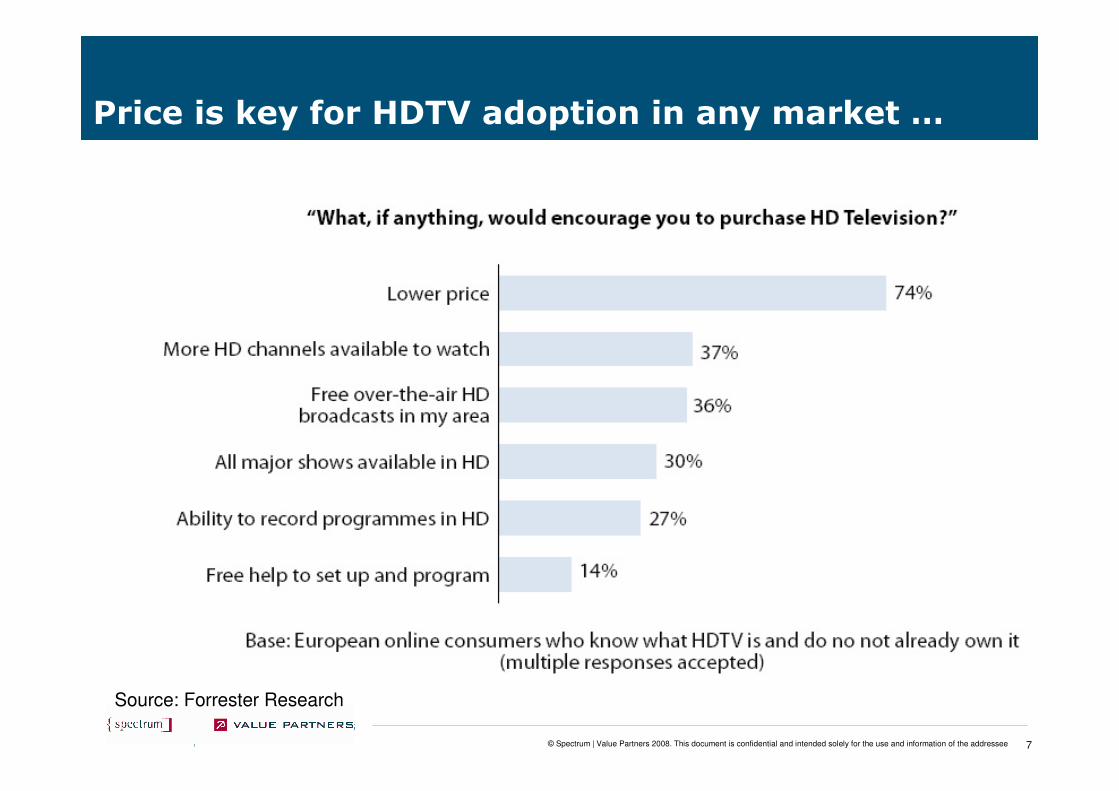

Price is key for HDTV adoption in any market …

Source: Forrester Research

8© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

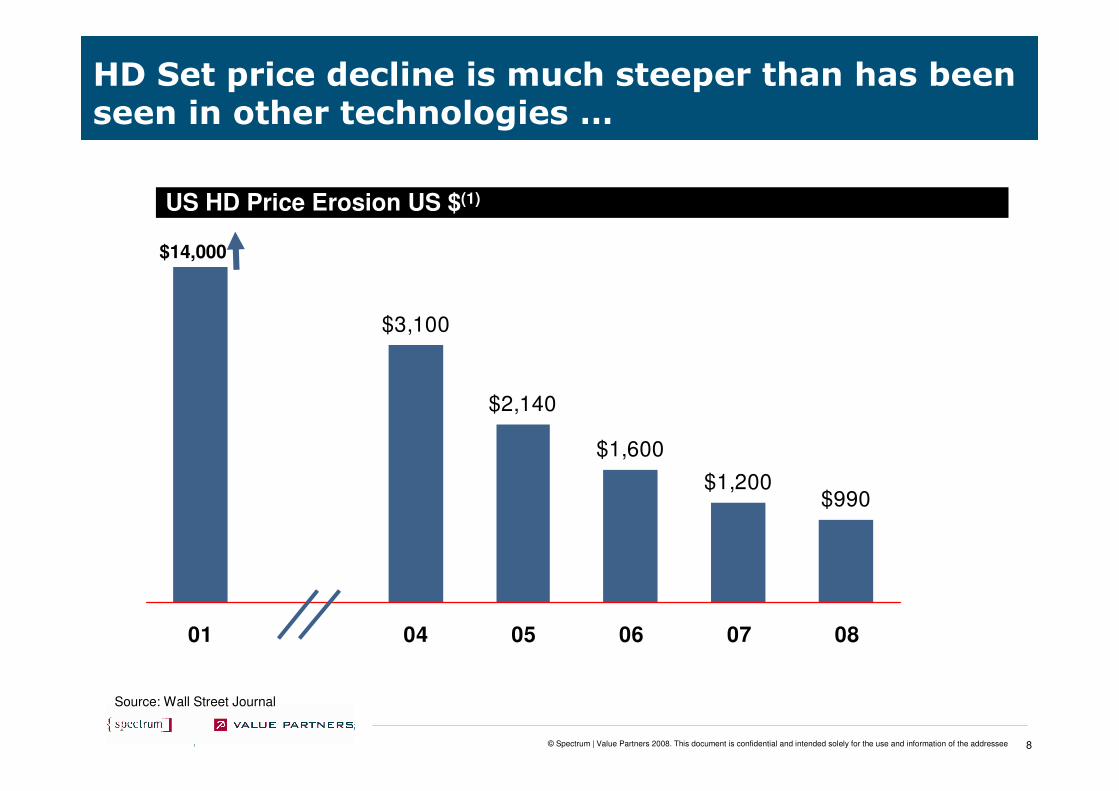

HD Set price decline is much steeper than has been seen in other technologies …

US HD Price Erosion US $(1)

$3,100

$2,140

$1,600

$1,200$990

01 04 05 06 07 08

$14,000

Source: Wall Street Journal

9© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

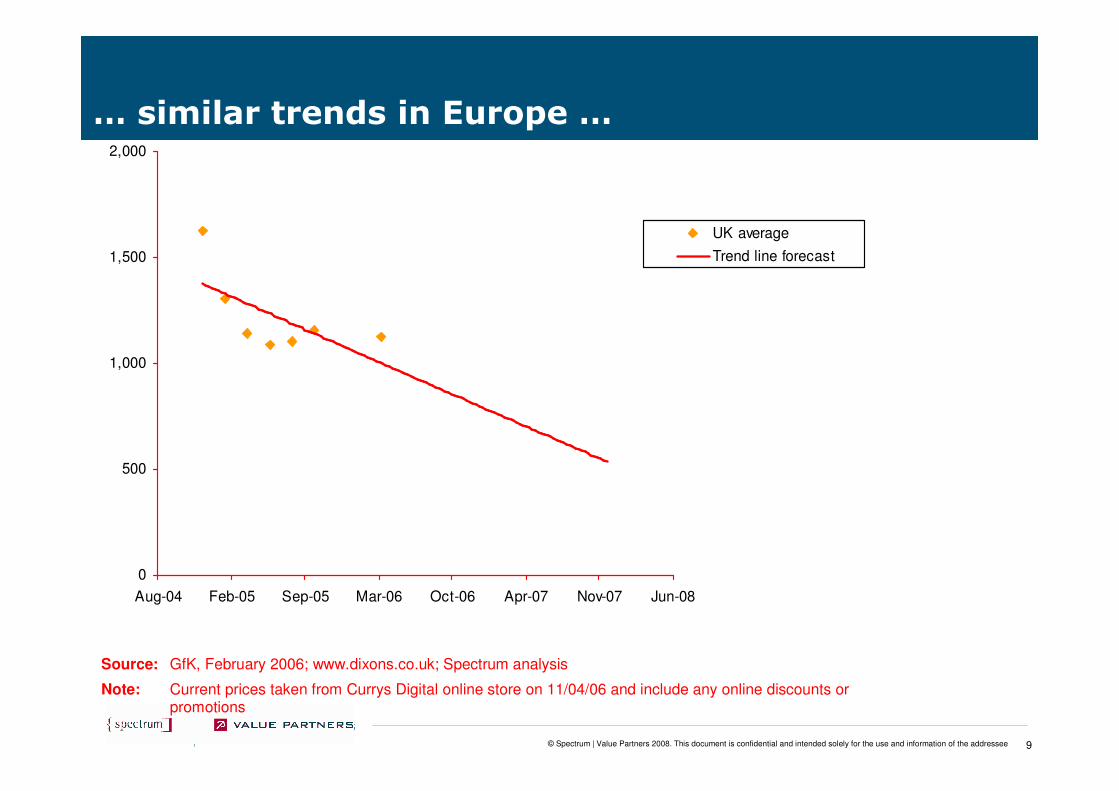

… similar trends in Europe …

0

500

1,000

1,500

2,000

Aug-04 Feb-05 Sep-05 Mar-06 Oct-06 Apr-07 Nov-07 Jun-08

UK average

Trend line forecast

Source: GfK, February 2006; www.dixons.co.uk; Spectrum analysis

Note: Current prices taken from Currys Digital online store on 11/04/06 and include any online discounts or promotions

10© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

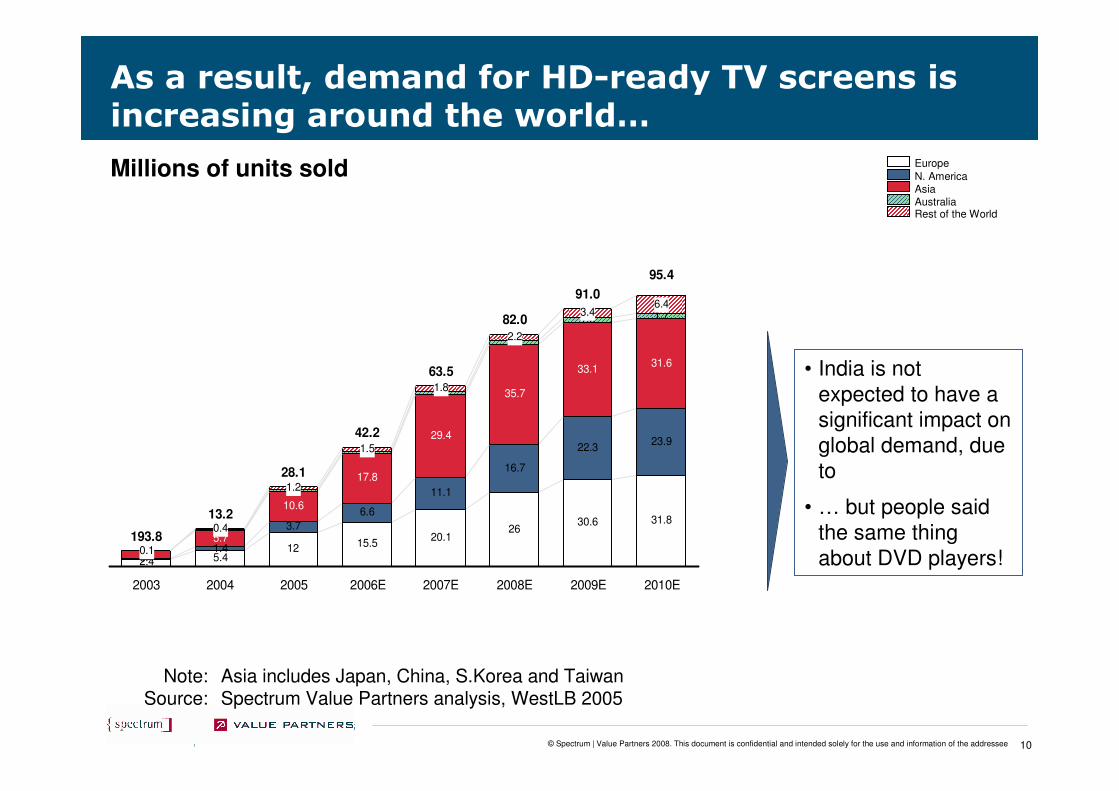

As a result, demand for HD-ready TV screens is increasing around the world…

2.4 5.412 15.5

20.126

30.6 31.8

0.41.4

3.7

6.6

11.1

16.7

22.323.9

2.5

5.7

10.6

17.8

29.4

35.7

33.131.6

0.1

0.3

0.6

0.8

1.1

1.4

1.6 1.7

0.1

0.4

1.2

1.5

1.8

2.2

3.46.4

193.8

13.2

28.1

42.2

63.5

82.0

91.0

95.4

2003 2004 2005 2006E 2007E 2008E 2009E 2010E

EuropeN. AmericaAsiaAustraliaRest of the World

Note:Source:

Asia includes Japan, China, S.Korea and TaiwanSpectrum Value Partners analysis, WestLB 2005

Millions of units sold

• India is not expected to have a significant impact on global demand, due to

• … but people said the same thing about DVD players!

11© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

Similar trend seen for other main CPE cost – STBs…

12© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

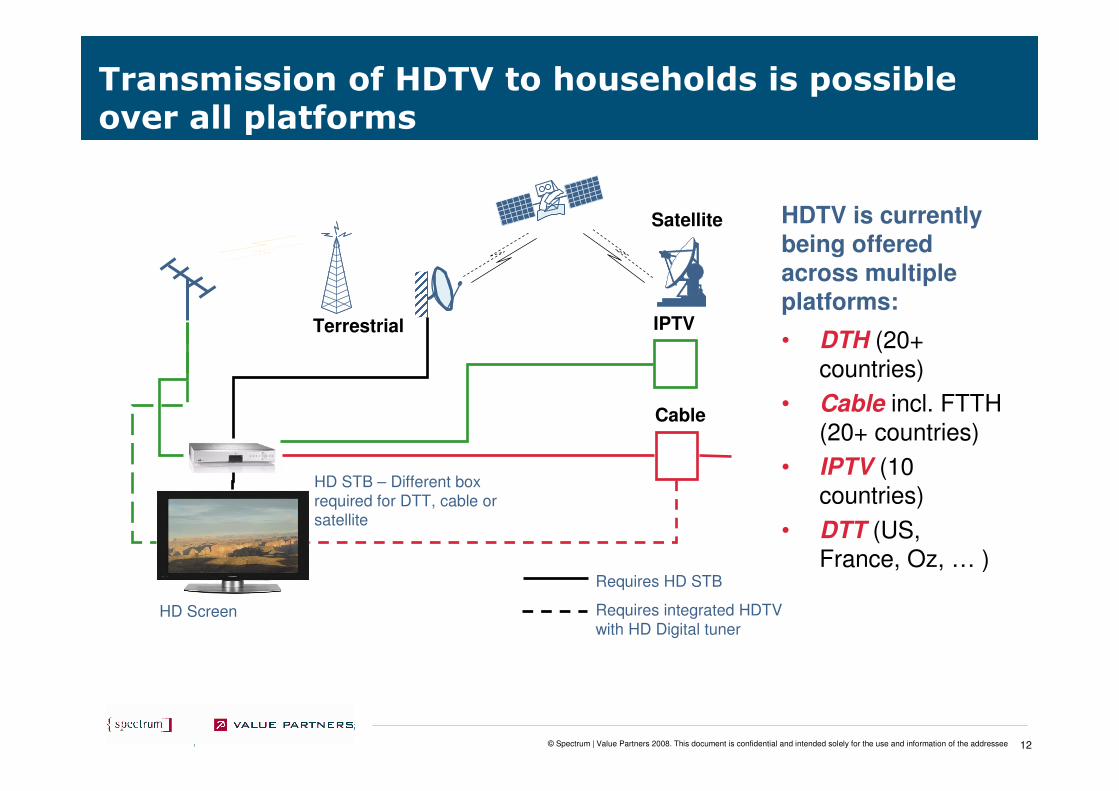

Transmission of HDTV to households is possible over all platforms

Satellite

Terrestrial

Cable

Requires HD STB

Requires integrated HDTV with HD Digital tuner

HD Screen

HD STB – Different box required for DTT, cable or satellite

IPTV

HDTV is currently being offered across multiple platforms:

• DTH (20+ countries)

• Cable incl. FTTH (20+ countries)

• IPTV (10 countries)

• DTT (US, France, Oz, … )

13© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

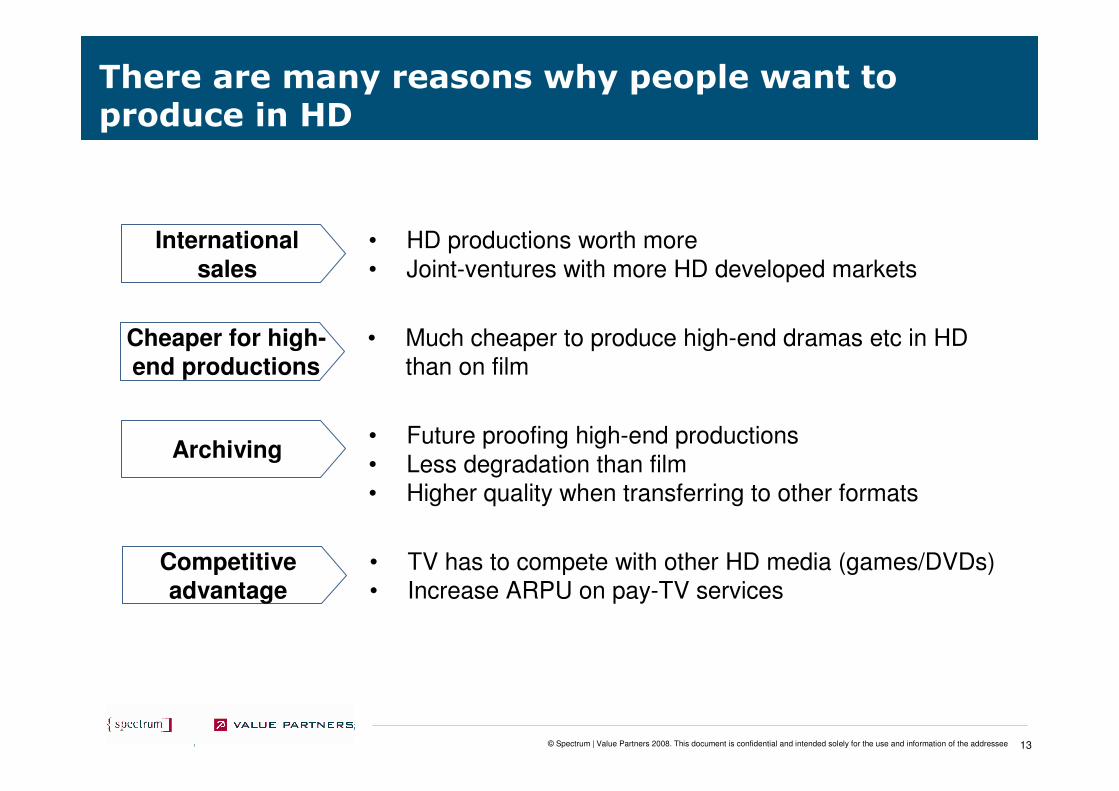

• TV has to compete with other HD media (games/DVDs)• Increase ARPU on pay-TV services

Competitive advantage

There are many reasons why people want to produce in HD

• HD productions worth more• Joint-ventures with more HD developed markets

International sales

• Future proofing high-end productions• Less degradation than film• Higher quality when transferring to other formats

Archiving

• Much cheaper to produce high-end dramas etc in HD than on film

Cheaper for high-end productions

14© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

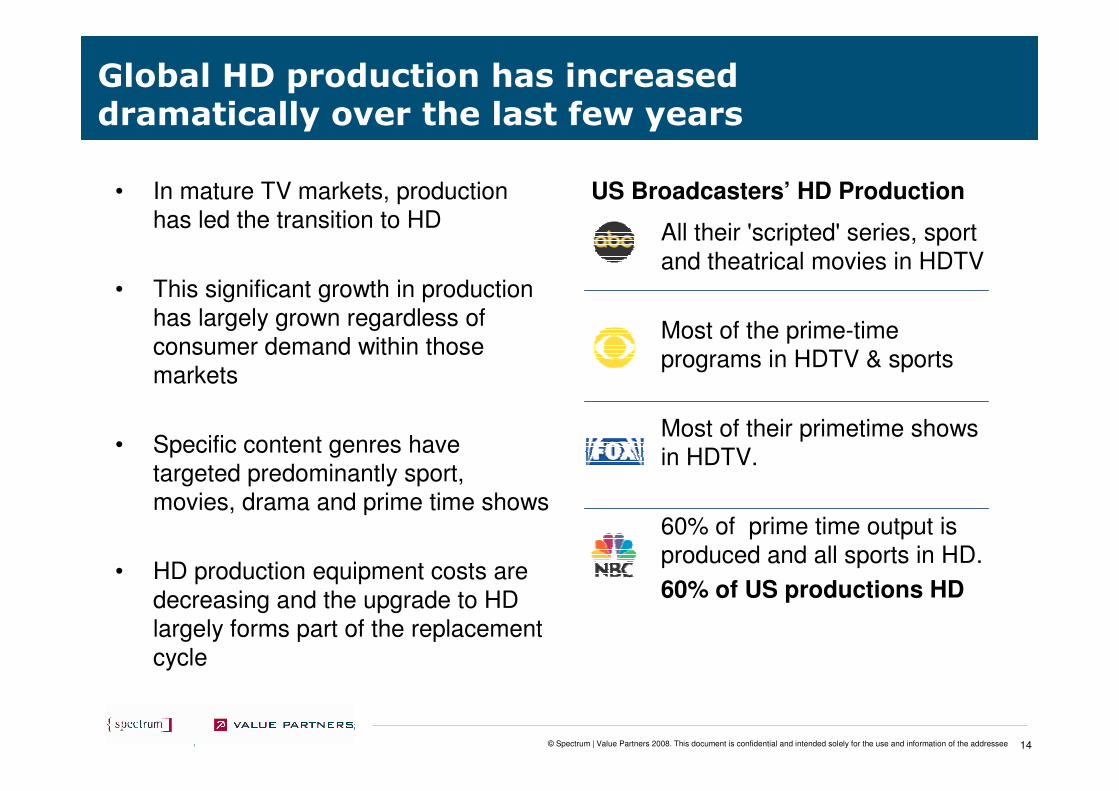

Global HD production has increased dramatically over the last few years

• In mature TV markets, production has led the transition to HD

• This significant growth in production has largely grown regardless of consumer demand within those markets

• Specific content genres have targeted predominantly sport, movies, drama and prime time shows

• HD production equipment costs are decreasing and the upgrade to HD largely forms part of the replacement cycle

All their 'scripted' series, sport and theatrical movies in HDTV

Most of the prime-time programs in HDTV & sports

Most of their primetime shows in HDTV.

60% of prime time output is produced and all sports in HD.

60% of US productions HD

US Broadcasters’ HD Production

15© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

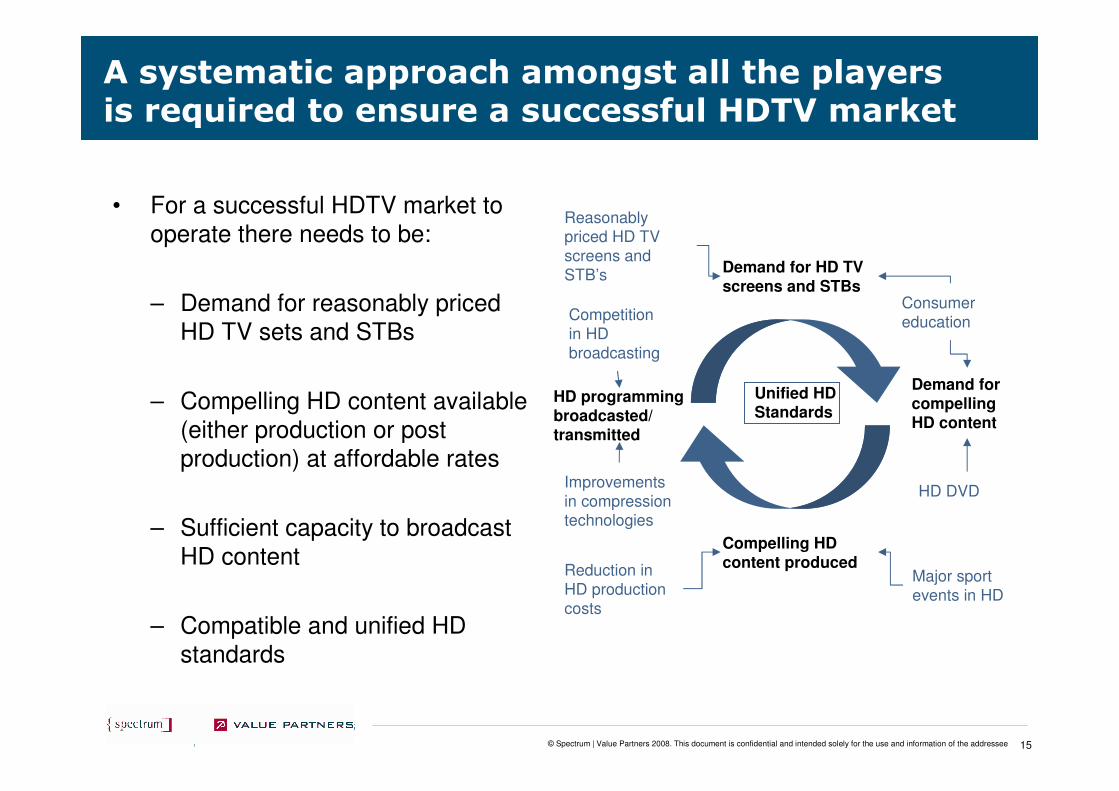

A systematic approach amongst all the players is required to ensure a successful HDTV market

• For a successful HDTV market to operate there needs to be:

– Demand for reasonably priced HD TV sets and STBs

– Compelling HD content available (either production or post production) at affordable rates

– Sufficient capacity to broadcast HD content

– Compatible and unified HD standards

Unified HD Standards

Demand for HD TV screens and STBs

Demand for compelling HD content

Compelling HD content produced

HD programming broadcasted/ transmitted

Major sport events in HD

HD DVD

Competition in HD broadcasting

Improvements in compression technologies

Reduction in HD production costs

Consumer education

Reasonably priced HD TV screens and STB’s

16© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

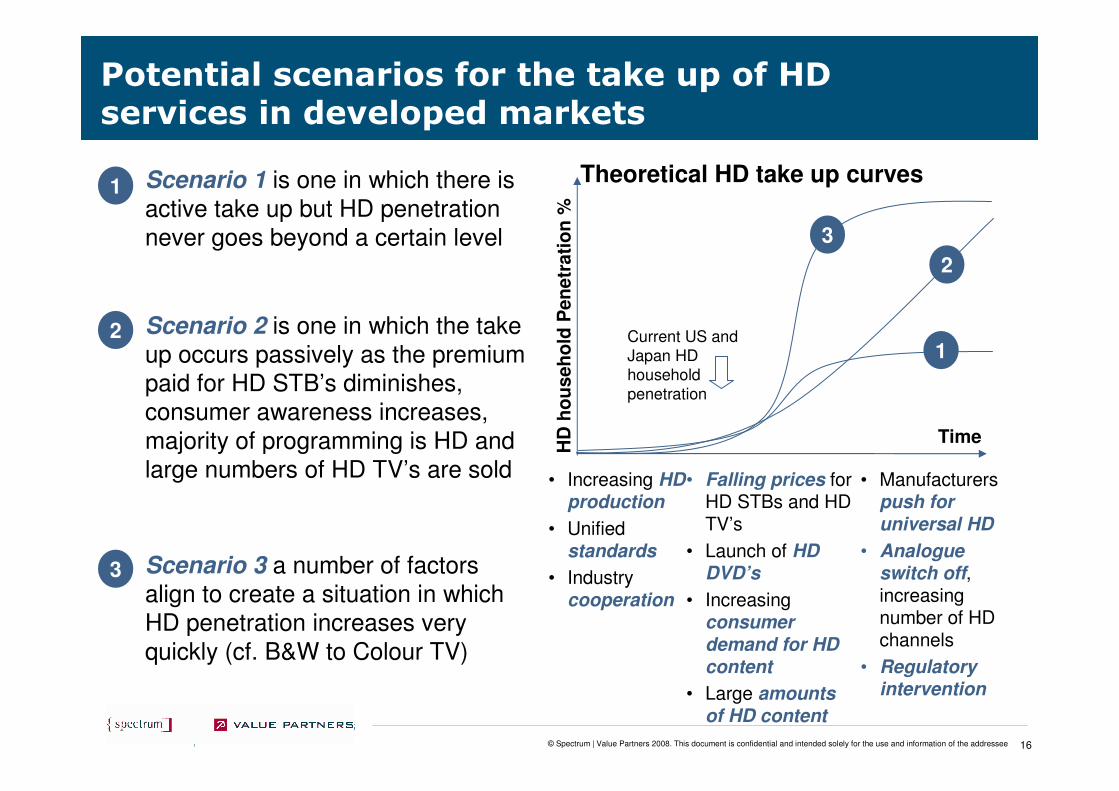

Scenario 1 is one in which there is active take up but HD penetration never goes beyond a certain level

Scenario 2 is one in which the take up occurs passively as the premium paid for HD STB’s diminishes, consumer awareness increases, majority of programming is HD and large numbers of HD TV’s are sold

Scenario 3 a number of factors align to create a situation in which HD penetration increases very quickly (cf. B&W to Colour TV)

Potential scenarios for the take up of HD services in developed markets

Time

HD

ho

useh

old

Pen

etr

ati

on

%

1

2

3

Current US and Japan HD household penetration

• Increasing HD production

• Unified standards

• Industry cooperation

• Falling prices for HD STBs and HD TV’s

• Launch of HD DVD’s

• Increasing consumer demand for HD content

• Large amounts of HD content

• Manufacturers push for universal HD

• Analogue switch off, increasing number of HD channels

• Regulatory intervention

1

2

3

Theoretical HD take up curves

17© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

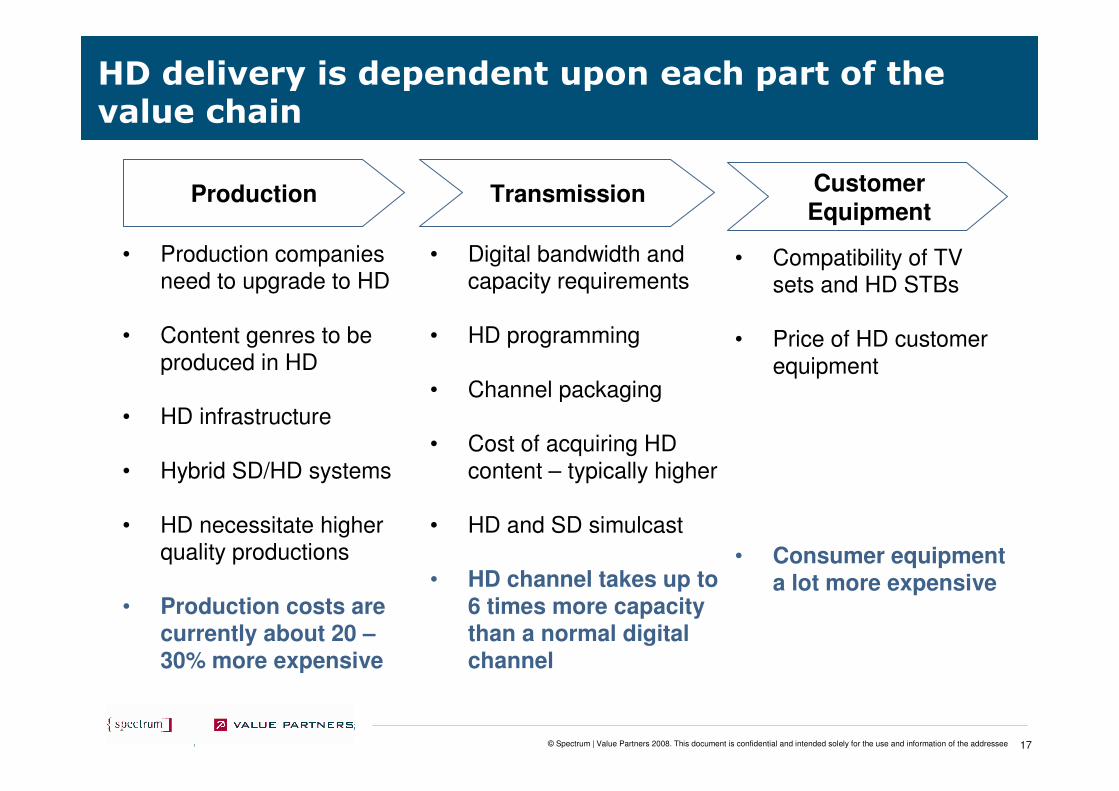

HD delivery is dependent upon each part of the value chain

Production Transmission CustomerEquipment

• Production companies need to upgrade to HD

• Content genres to be produced in HD

• HD infrastructure

• Hybrid SD/HD systems

• HD necessitate higher quality productions

• Production costs are currently about 20 –30% more expensive

• Digital bandwidth and capacity requirements

• HD programming

• Channel packaging

• Cost of acquiring HD content – typically higher

• HD and SD simulcast

• HD channel takes up to 6 times more capacity than a normal digital channel

• Compatibility of TV sets and HD STBs

• Price of HD customer equipment

• Consumer equipment a lot more expensive

18© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

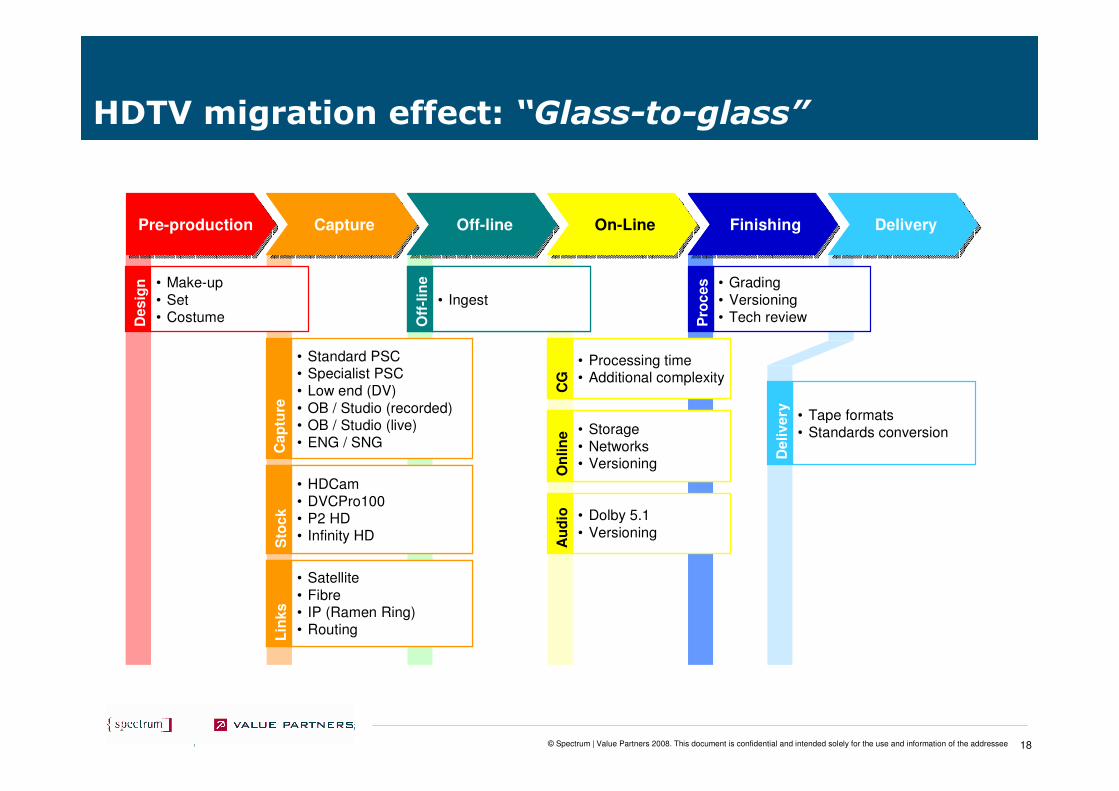

HDTV migration effect: “Glass-to-glass”

Pre-productionPre-production CaptureCapture Off-lineOff-line On-LineOn-Line FinishingFinishing DeliveryDelivery

Des

ign • Make-up

• Set• Costume

• Tape formats• Standards conversion

De

livery

• Dolby 5.1• Versioning

Au

dio

• Ingest

Off

-lin

e

• Ingest

Off

-lin

e

• HDCam• DVCPro100• P2 HD• Infinity HD

Sto

ck

• HDCam• DVCPro100• P2 HD• Infinity HD

Sto

ck

• Standard PSC• Specialist PSC• Low end (DV)• OB / Studio (recorded)• OB / Studio (live)• ENG / SNGC

ap

ture

• Storage• Networks• Versioning

On

lin

e • Storage• Networks• Versioning

On

lin

e

• Processing time• Additional complexity

CG

• Processing time• Additional complexity

CG

• Satellite• Fibre• IP (Ramen Ring)• RoutingL

inks

• Satellite• Fibre• IP (Ramen Ring)• RoutingL

inks

• Grading• Versioning• Tech reviewP

roc

es

s

19© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

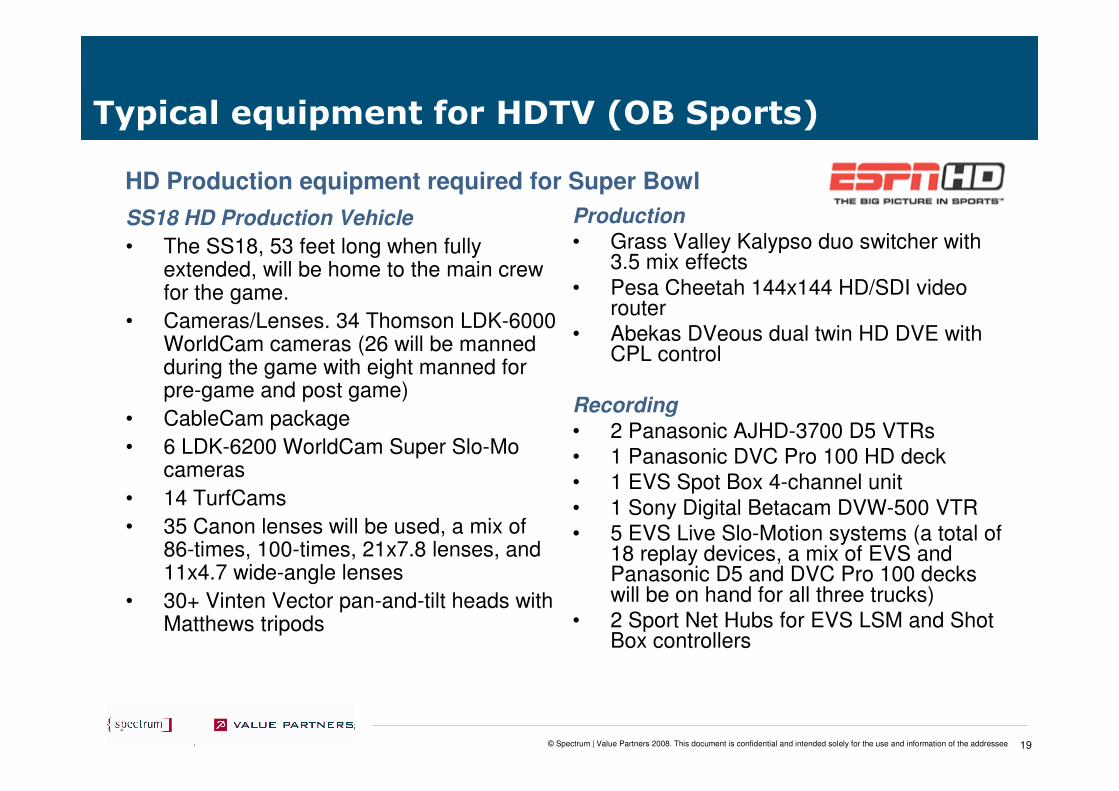

Typical equipment for HDTV (OB Sports)

HD Production equipment required for Super Bowl

SS18 HD Production Vehicle

• The SS18, 53 feet long when fully extended, will be home to the main crew for the game.

• Cameras/Lenses. 34 Thomson LDK-6000 WorldCam cameras (26 will be manned during the game with eight manned for pre-game and post game)

• CableCam package

• 6 LDK-6200 WorldCam Super Slo-Mo cameras

• 14 TurfCams

• 35 Canon lenses will be used, a mix of 86-times, 100-times, 21x7.8 lenses, and 11x4.7 wide-angle lenses

• 30+ Vinten Vector pan-and-tilt heads with Matthews tripods

Production

• Grass Valley Kalypso duo switcher with 3.5 mix effects

• Pesa Cheetah 144x144 HD/SDI video router

• Abekas DVeous dual twin HD DVE with CPL control

Recording

• 2 Panasonic AJHD-3700 D5 VTRs• 1 Panasonic DVC Pro 100 HD deck• 1 EVS Spot Box 4-channel unit• 1 Sony Digital Betacam DVW-500 VTR• 5 EVS Live Slo-Motion systems (a total of

18 replay devices, a mix of EVS and Panasonic D5 and DVC Pro 100 decks will be on hand for all three trucks)

• 2 Sport Net Hubs for EVS LSM and Shot Box controllers

20© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

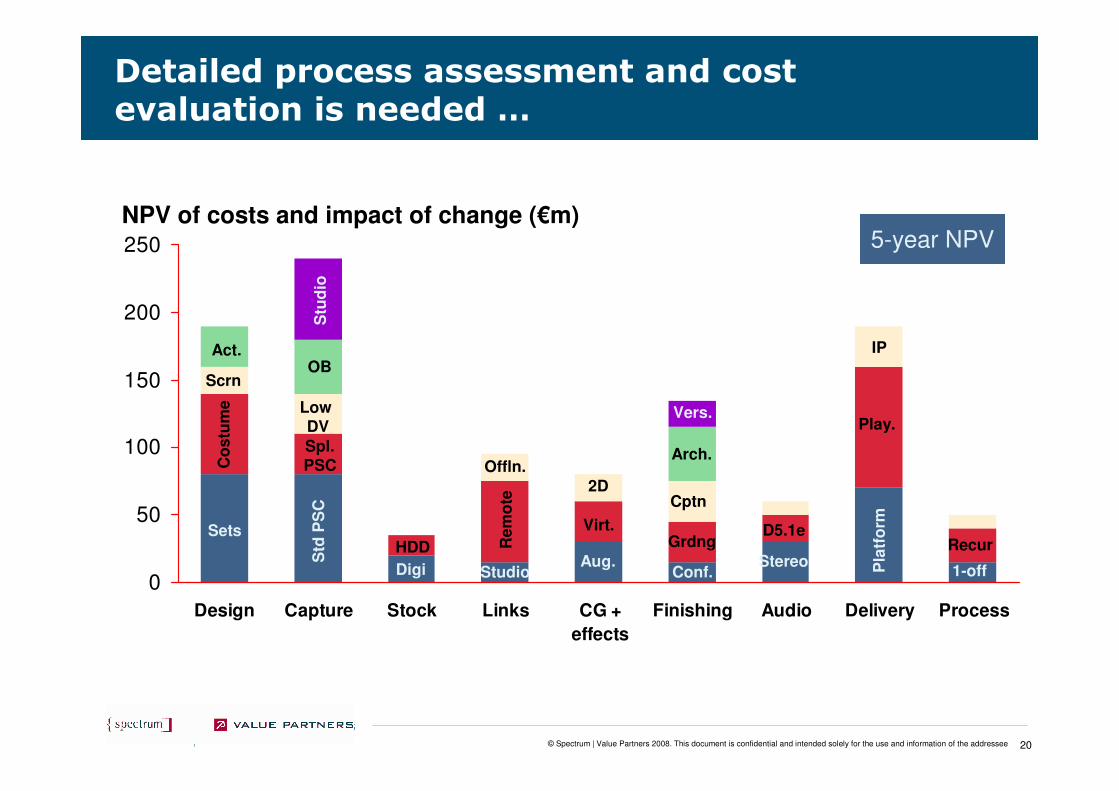

0

50

100

150

200

250

Design Capture Stock Links CG +

effects

Finishing Audio Delivery Process

Detailed process assessment and cost evaluation is needed …

NPV of costs and impact of change (€m)

Sets

Co

stu

me

Scrn

Act.

Std

PS

C

Spl.PSC

Low DV

OB

Stu

dio

Digi

HDD

Studio

Re

mo

te

Offln.

Aug.

Virt.

2D

Conf.

Grdng

Cptn

Arch.

Vers.

Stereo

D5.1e

Pla

tfo

rm

IP

Play.

1-off

Recur

5-year NPV

21© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

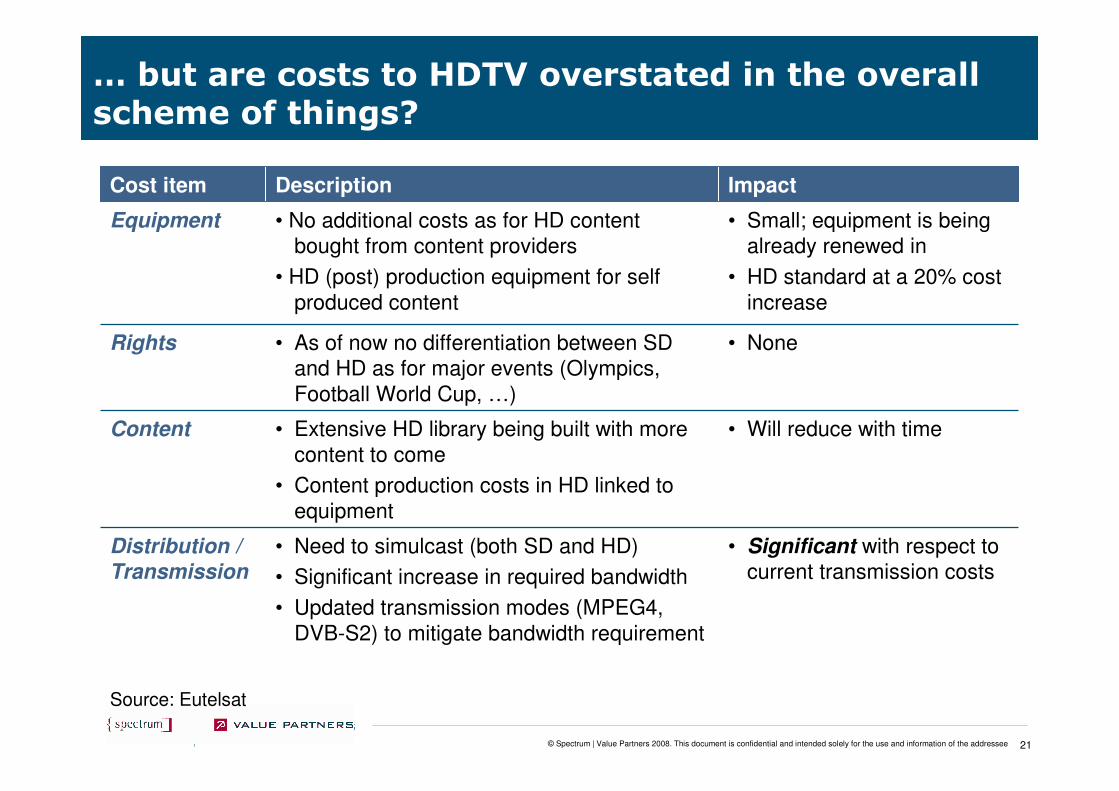

… but are costs to HDTV overstated in the overall scheme of things?

• Significant with respect to current transmission costs

• Need to simulcast (both SD and HD)

• Significant increase in required bandwidth

• Updated transmission modes (MPEG4, DVB-S2) to mitigate bandwidth requirement

Distribution /

Transmission

• None • As of now no differentiation between SD and HD as for major events (Olympics, Football World Cup, …)

Rights

• Extensive HD library being built with more content to come

• Content production costs in HD linked to equipment

• No additional costs as for HD content bought from content providers

• HD (post) production equipment for self produced content

Description

Content

Equipment

Cost item

• Will reduce with time

• Small; equipment is being already renewed in

• HD standard at a 20% cost increase

Impact

Source: Eutelsat

22© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

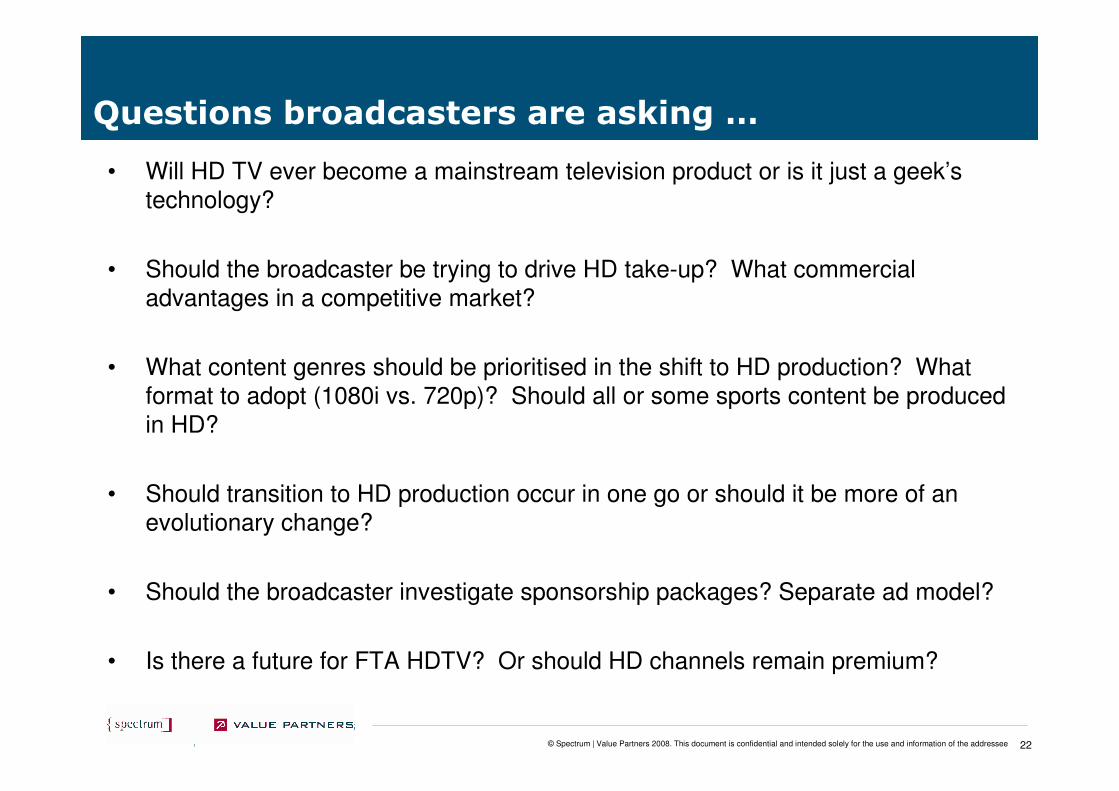

Questions broadcasters are asking …

• Will HD TV ever become a mainstream television product or is it just a geek’s technology?

• Should the broadcaster be trying to drive HD take-up? What commercial advantages in a competitive market?

• What content genres should be prioritised in the shift to HD production? What format to adopt (1080i vs. 720p)? Should all or some sports content be produced in HD?

• Should transition to HD production occur in one go or should it be more of an evolutionary change?

• Should the broadcaster investigate sponsorship packages? Separate ad model?

• Is there a future for FTA HDTV? Or should HD channels remain premium?

23© Spectrum | Value Partners 2008. This document is confidential and intended solely for the use and information of the addressee

Contact information

SydneyKing Street Wharf, Suite 30245 Lime StreetSydney NSW 2000AustraliaTel. +61 2 9279 0072Fax +61 2 9279 0551

Mumbai8°floor, C blockDevchand House, Shiv Sagar EstateDr. Annie Besant RoadWorli, 400 018Tel. +91 22 6611 9700 Fax +91 22 6611 9988

Singapore7 Temasek BoulevardSuntec Tower One #26-04038987Tel. +65 6820 3388Fax +65 6820 3389

ShanghaiFortune Gate office building, Unit 02, 25/F1701 Beijing Rd (W)200040 Tel. +86 21 6132 4230Fax +86 21 6132 4238

San PaoloRua Padre João Manuel 7551°e 2°andares - cj. 11, 12 e 21Cerqueria CesarSan Paolo - BrasileCEP 01411 - 001Tel. +55 11 306 809 99Fax +55 11 308 141 38

New DelhiLevel 12, Building No. 8, Tower C, Cyber City DLF Phase – II Gurgaon 122002 Haryana, India Tel. +91 124 469 6902 Fax +91 124 469 6970

IstanbulSunplazaDereboyu Sk. No:24 Maslak34398 Istanbul – Turchia Tel. +90 212 276 98 86

Hong KongRoom 2602, 26/F, Vicwood Plaza,199 Des Voeux Road. Central Hong KongTel. + 852 2103 1000Fax + 852 2805 1310

Buenos AiresAlicia Moreau de Justo 550 - 4 PisoC1107AAL Buenos Aires - ArgentinaTel. +54 11 4314 4222Fax +54 11 4314 6111

BarcelonaPasseig de Gracia 12, 1er pis08007 BarcelonaSpain Tel. +34 93 492 0370Fax +34 93 492 0351

RomeVia di Porta Pinciana 100187 RomeTel. +39 06 697 6481Fax +39 06 697 648 51

LondonGreencoat HouseFrancis StreetLondonSW1P 1DHTel. +44 (0) 20 7630 1400Fax +44 (0) 20 7630 7011

MilanVia G. Leopardi 3220123 MilanTel. +39 02 485 481Fax +39 02 480 090 10

www.spectrumstrategy.comwww.valuepartners.com