better poultry value chain development through microfinance in vietnam · · 2014-11-26better...

TRANSCRIPT

1

BETTER POULTRY VALUE CHAIN DEVELOPMENT

THROUGH MICROFINANCE IN VIETNAM

Student: Ngoc Anh NGUYEN Supervisor: Johan BASTIAENSEN European Microfinance Program 2009-2010

Brussels, September 2010

2

TABLE OF CONTENTS

ACKNOWLEDGEMENT .................................... .............................................................................. 4 ABSTRACT........................................... ........................................................................................... 5 INTRODUCTION.............................................................................................................................. 6

Background .................................................................................................................................. 6 Research question ....................................................................................................................... 6 Scope of work............................................................................................................................... 7 Methodology................................................................................................................................. 7 Report outline ............................................................................................................................. 11

CHAPTER I .................................................................................................................................... 12 Literature review.................................. ......................................................................................... 12

I.1. What is value chain? ............................................................................................................ 12 I.3. Value chain microfinance..................................................................................................... 13

CHAPTER II ................................................................................................................................... 17 Current situation of poultry value chain in Vietnam ................................................................ 17

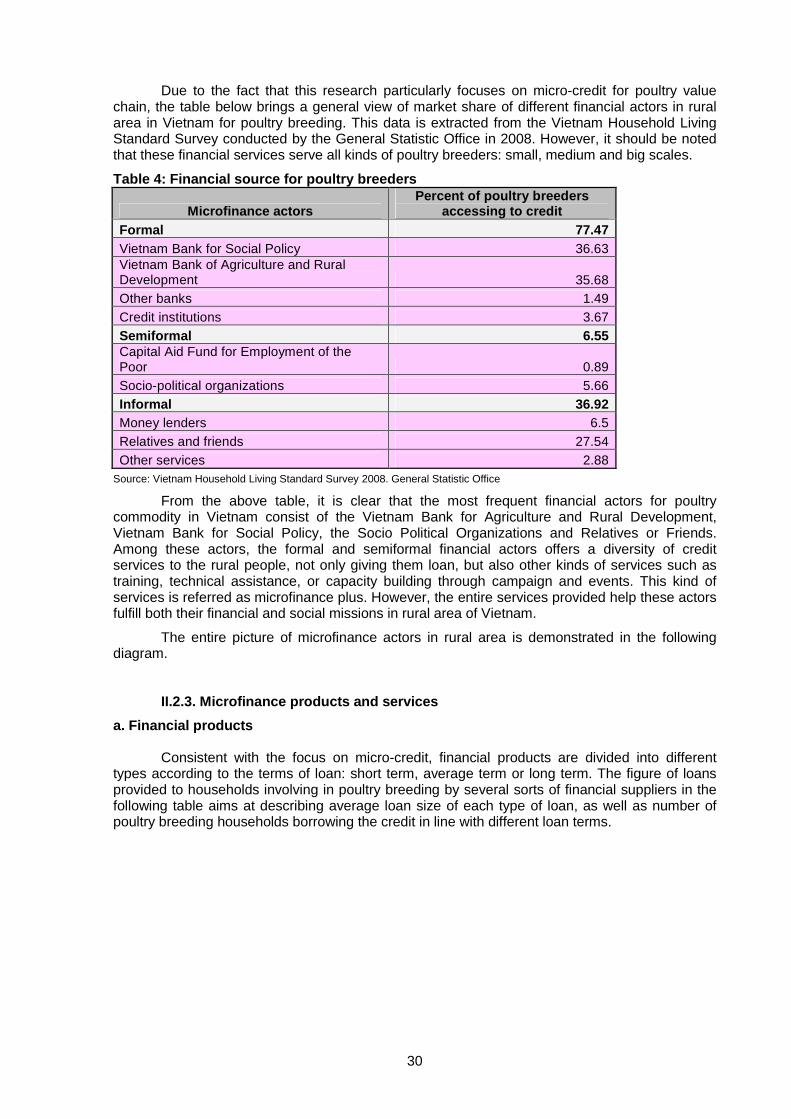

II.1. Analysis of poultry value chain in Vietnam ......................................................................... 17 II.1.1. Poultry production: Facts and Figures......................................................................... 17 II.1.2. Poultry production system............................................................................................ 18 II.1.3. Popular model of poultry value chains in Vietnam ...................................................... 19 II.1.4. Policies for poultry value chain development .............................................................. 26

II.2. Micro-financing poultry value chain in Vietnam .................................................................. 27 II.2.1. Microfinance clients ..................................................................................................... 27 II.2.2. Microfinance suppliers ................................................................................................. 27 II.2.3. Microfinance products and services ............................................................................ 30

CHAPTER III .................................................................................................................................. 33 Analysis of the microfinance in poultry value chain in Vietnam ........................................ .... 33

III.1. Micro-financing poultry value chain in Vietnam ................................................................. 33 III.1.1. Microfinance actors for poultry stakeholders .............................................................. 33 III.1.2. Poultry stakeholders with access to microfinance products and services ................. 37

III.2. Microfinance products and services for poultry value chain in Vietnam............................ 38 III.2.1. Financial services........................................................................................................ 38 III.2.2. Non- financial services................................................................................................ 43

III.3. Methodology providing microfinance services................................................................... 44 III.3.1. Group lending.............................................................................................................. 44 III.3.2. Individual lending ........................................................................................................ 49

III.4. Microfinance and the link with poultry value chain ............................................................ 50 III.5. Case study ......................................................................................................................... 51

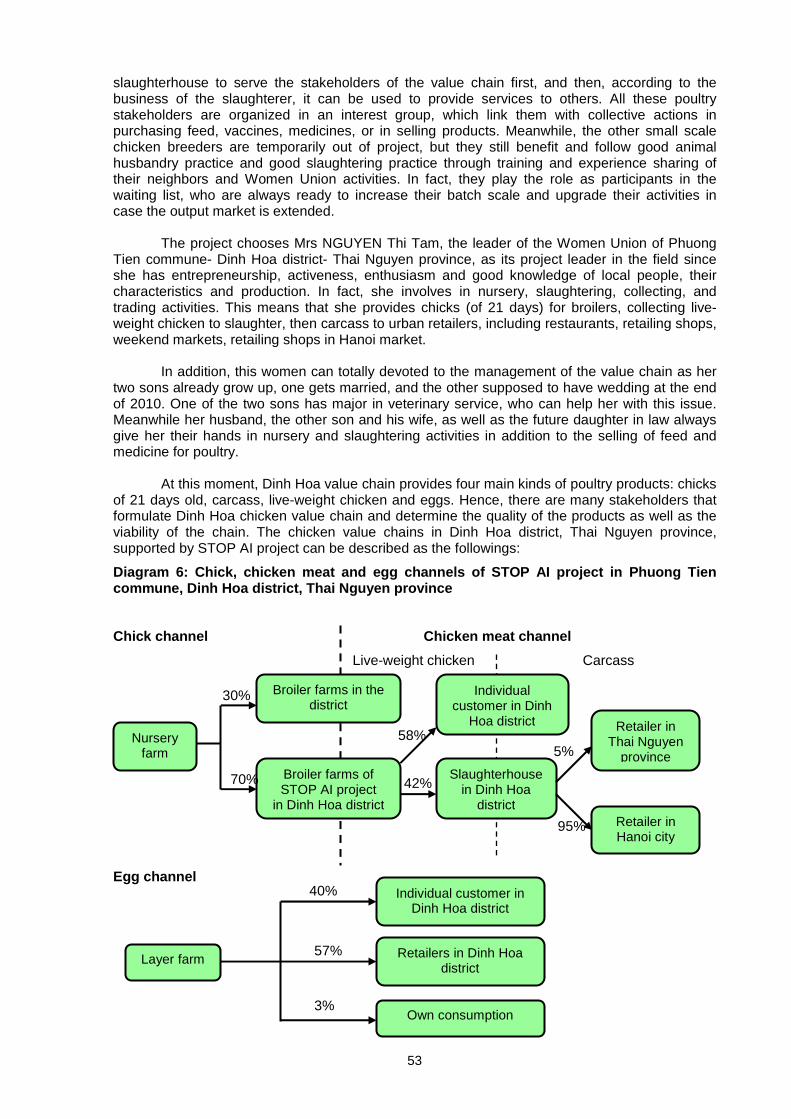

III.5.1. Presentation of ATK Dinh Hoa chicken and egg value chain- Phuong Tien commune, Dinh Hoa district, Thai Nguyen province ............................................................................... 51 III.5.2. Financial flows to and in the value chain .................................................................... 54 III.5.3. Microfinance plus supplied to poultry stakeholders.................................................... 57 III.5.4. How financial and non-financial services address the demand of poultry stakeholders................................................................................................................................................ 60

CONCLUSION ............................................................................................................................... 67 Findings ...................................................................................................................................... 67 Recommendations ..................................................................................................................... 69

BIBLIOGRAPHY....................................... ..................................................................................... 70 APPENDICES ................................................................................................................................ 72

3

TABLE OF FIGURES

Table 1: Sample scale of the survey ................................................................................................ 9 Table 2: Scale and moment of poultry smuggling from China to Lang Son and Quang Ninh provinces ........................................................................................................................................ 21 Table 3: Quantity and value of chicken meat imported to Vietnam over years ............................. 22 Table 4: Financial source for poultry breeders............................................................................... 30 Table 5: Percentage of borrowers as poultry breeding households and average loan size according to loan term.................................................................................................................... 31 Table 6: Loans for poultry stakeholders offered by formal and semi-formal microfinance actors. 39 Table 7: Credit offered by informal financial actors........................................................................ 42 Table 8: Microfinance plus in poultry value chain .......................................................................... 43 Table 9: Application of group lending model in the Vietnam Bank for Social Policy ..................... 45 Table 10: Comparison of procedure of group lending offered by Vietnam Bank for Social Table 11: Economic data of chicken stakeholders in chicken value chain in Dinh Hoa district- Thai Nguyen province............................................................................................................................. 64 Table 12: Difference in the price of STOP Avian Influenza products and other similar products in the market....................................................................................................................................... 64

TABLE OF DIAGRAMS

Diagram 1: Flow of microfinance services within value chain........................................................ 14 Diagram 2: Popular poultry value chains in Vietnam ..................................................................... 19 Diagram 3: Overview of financial sources for poultry value chain in Vietnam............................... 29 Diagram 4: Main financial sources accessed by poultry stakeholders .......................................... 33 Diagram 5: Individual lending to small and medium poultry stakeholders in Vietnam .................. 49 Diagram 6: Chick, chicken meat and egg channels of STOP AI project in Phuong Tien commune, Dinh Hoa district, Thai Nguyen province........................................................................................ 53 Diagram 7: Model of micro-financing chicken producers in STOP Avian Influenza project .......... 56 Diagram 8: Internal financial flow in ATK Dinh Hoa chicken value chain ...................................... 57

TABLE OF CHARTS

Chart 1: Poultry heads in Vietnam from the period of 2001 and 2007........................................... 17 Chart 2: Weight of poultry meat and eggs produced in Vietnam over the period of 2001-2007 ... 18 Chart 3: Service quality of microfinance sources for poultry value chain in Vietnam.................... 36 Chart 4: Poultry stakeholders with access to microfinance services............................................. 37 Chart 5: Demand of borrowers towards financial services of formal and semi-formal financial actors in poultry value chain........................................................................................................... 41 Chart 6: Demand of borrowers towards non-financial services of financial actors in poultry value chain ............................................................................................................................................... 44 Chart 7: Poultry stakeholders in Dinh Hoa district, Thai Nguyen province with times of loan access to credit of the STOP Avian Influenza project.................................................................... 55

4

ACKNOWLEDGEMENT

First and foremost, I would like to express my sincerest gratitude to my supervisor, Professor Johan Bastiaensen for his valuable guidance and advice. His enthusiasts and carefulness in making comments as well as his continuous encouragement inspired me much to complete the thesis and to make tremendous contribution to the STOP Avian Influenza project that I did the internship.

In addition, my great thanks is sent to Mr. Patrice Gautier- Director of the Company of Asian Veterinary and Livestock Services (ASVELIS) in Hanoi for offering me the internship and giving me opportunity to work with Vietnamese and international experts in poultry value chain. Also, it is my privilege to express my warm regards to the equip of STOP Avian Influenza project, including the ASVELIS staffs, the Women Union of Dinh Hoa district- Thai Nguyen province, Lua Vang cooperative in Yen Dung district- Bac Giang province, Go Cong chicken cooperative in Go Cong town- Tien Giang province, Huong Que chicken cooperative in Phu Giao district- Binh Duong province and all poultry stakeholders taking part in the project for their precious support.

I would like to take this opportunity to thank to all the staffs of the Rural Development Center- Institute of Policy and Strategy for Agriculture and Rural Development and local authorities in Quang Tri, Hung Yen, and Hanoi provinces for helping me with data collection while implementing the project entitled “Pandemic Influenza: Preparedness and Response”.

Last but not least, an honorable mention goes to my families and friends for their understanding and supports. Without helps of the particular mentioned above, I would face many difficulties while doing this thesis.

5

ABSTRACT

Value chain approach has been widely used in agriculture to identify necessary intervention for a better situation of agriculture and rural development in Vietnam. However, there are not many researches studying the micro-financing of agricultural value chains in this country. The thesis takes this opportunity to apply value chain method to analyze the situation of micro-financing in poultry commodity towards the development of poultry value chain.

The data of desk study shows that poultry value chain in Vietnam is dominated by small and medium scale production system. It is now in difficult condition when facing with so many problems associated with avian influenza, uncontrolled import of poultry products, and food safety. However, it also has many opportunities to develop when poultry production has not satisfied domestic demand and pork value chain, which dominates domestic meat consumption, has been in the trouble of the porcine reproductive and respiratory syndrome. Among financial actors operating in Vietnam, the Vietnam Bank and Social Policy, together with the Vietnam Bank for Agriculture and Rural Development and such informal lenders as relatives, friends and neighbors are main actors providing financial services to poultry breeders. And the credit offered to poultry stakeholders is usually in short term (≤1 year) and medium term (1-5 years) with small amount of under VND 30 million.

The data of field study once again raises the importance of the Vietnam Bank and Social Policy, Vietnam bank for Agriculture and Rural Development, and relatives, friends, and neighbors as principal microfinance actors for poultry value chain of small and medium scales. Although these actors is rather weak in providing microfinance plus for poultry stakeholders, national and international programs and projects appear to be very active in this aspect. Their strengths are dug in more detail with case study of ATK Dinh Hoa chicken and egg value chain in Phuong Tien commune- Dinh Hoa district- Thai Nguyen province within the frame of the STOP Avian Influenza project., funded by the United States Agency for International Development. Of various kinds of non-financial products, small and medium poultry stakeholders are most in need of technical assistance and risk support. For financial products, they would like to access bigger loans, and at favorable interest rate due to current difficulty of poultry value chain.

In addition, lending methods and credit issues are synthesized and analyzes to understand its operation and how microfinance address the demand of small and medium scale poultry stakeholders. While individual loans are usually offered to medium and big poultry stakeholders, group loans are for those of small scale, vulnerable, living in difficult condition with very weak voice in the value chain. Due to real situation of poultry value chain in Vietnam with small and medium production and current risk of poultry, the loans taken by poultry stakeholders are quite small, compared with other value chains, for instance pig, tea, coffee, etc.

In general, the quality of microfinance services in Vietnam is accessed to be good, but the borrowers really wants microfinance actors integrate in their value chain to understand their situation to create better products fitting their needs and simplify lending procedure as much as they can. Group loan is a little bit more preferable to individual loan, probably because most of poultry stakeholders are of small scale, and still excluded from formal financial market with collateral requirements. Nevertheless, individual loan remains important to those who would like bigger loan size and motivate their independence and privacy.

Apart from analysis of how the STOP Avian Influenza project microfinance poultry stakeholders of small and medium scale regarding financial and non-financial products, brokerage lending model, the case study with ATK Dinh Hoa chicken and egg value chain attempts to identify changes of these stakeholders before and after the access to this credit with data on their economic performance and social aspect.

In conclusion, it is recommended that financial actors should employ value chain method to better serve the financial and non-financial demand of their customers so that it is profitable for both the borrowers in terms of conducting good business and the lenders in terms of ensuring loan repayment, generating more benefit while reducing transaction cost. Collaboration with technical agencies or projects and programs on poultry value chain is also an ideal solution for financial actors to address clients’ need and mitigate their risk.

6

INTRODUCTION

Background

In the country, where agriculture is the backbone with 80% of the people living on agriculture, poultry breeding in general and chicken raising in particular plays the second role in the total production value of Vietnamese livestock (after pig breeding). As indicated the Vietnam Household Living Standard Survey 2008, 85% of the breeders in Vietnam involve in poultry breeding. In fact, it is always regarded as the traditional activity of rural people in Vietnam.

Before the outbreak of avian influenza in 2003, the development growth of poultry head was 9.02%, but it then reduced 6.67% from 2003 to 2005, the period seriously affected by avian influenza. Since then, the number of poultry head increase slowly, from 0.9 to 2.74%. Chicken always makes up 72-73% of the total poultry head every year.

Throughout Vietnam, poultry breeding develops the most in the Red river delta, Mekong river delta and North West of Vietnam, accounting for 60% of the total chicken. Following is South West and North of centre area (26%). Meanwhile in the North East and Tay Nguyen, it occupies only 4-5% of total national poultry head.

Poultry breeding in Vietnam follow three main kinds of breeding: (i) manual and small-scale breeding; (ii) semi-industrial and medium-scale breeding; (iii) industrial and big-scale breeding, in which small and medium scale breeding (under 1000 chickens) dominates. However, breeding households of small and medium scale in poultry commodity in general and chicken in particular face with many challenges, for instance poor breeding and slaughtering techniques; low productivity; disease; limited investment source of poultry breeding (finance and land); high price feed; small scale breeder suppliers; high competitive market, so on so forth. Therefore, the government, together with international and local organizations in Vietnam cooperate to assist the development of poultry value chain in general, and chicken value chain in particular, with the purposes of (i) improve competitiveness of poultry value chains so that they can access to new and higher quality markets (restaurant, supermarket, hotels, instead of normal market selling live-weight chicken); (ii) increase value added for small-scale poultry breeding households; (iii) enhance cooperation and relationship among actors of the chain, especially for small-scale producers so that the risk and benefit can be shared more equally.

Among approaches applied in poultry related projects and programs, micro-financing poultry value chain appears to be one of the efficient methods allowing all actors of the chains to perform smoothly and acquire necessary input and technology for their activities (production, business or trading); providing them with necessary financial source for initial investments, or working capital to start or upgrade their production and business; increasing the voice of each actors of the chain, especially the small ones, as well as of the poultry value chain as a whole. It is paid much attention to, not only by the local and national projects, but also by the international ones.

Research question

Within this study, I would like to analyze the microfinance of poultry value chain, with particular focus on chicken and credit services (financial and non-financial ones). The poultry value chain here includes the production of meat (carcass and live-weight) and eggs for own consumption, for local markets (right at the place of the producers) and for urban markets (restaurants, hotels, selling points in big cities, etc), as well as the production of chicks, or duckling, etc; following the whole value chain, from the hatchery, nursery, broiler, layer farms to collectors, slaughterers, and retailers. However, the poultry producers of interest in this study only involve those of small and medium scale, meaning fewer than 1000 chicken heads. It is conducted in 5 provinces in Vietnam, with representatives from the Northern, and Central provinces. Therefore, the study aims at finding the answer for the following research question:

• What is the situation of poultry value chain in Vietnam? What are problems that poultry stakeholders have to deal with?

7

• Who are main microfinance actors in poultry value chain in Vietnam? What kinds of credit services that they provide (both financial and non-financial ones) for poultry stakeholders and by what ways?

• To what extend do these services address the demand of small and medium poultry stakeholders to develop their activities and towards a poultry value chain of quality?

• What are advantages, constraint and challenges of microfinance services to satisfy the demand of poultry value chain stakeholders and towards the development of poultry value chain in Vietnam?

Scope of work

Above all, it should be noted the scope of the study as the followings:

Area of the study

The study is supposed to be conducted in 5 provinces, which are considered as representatives for different ecological zones in Vietnam, and represent poultry production of different scales (big, medium and small).

The provinces involve in the survey of this study include Hanoi and Hung Yen (representatives for the Red River Delta), Bac Giang and Thai Nguyen (representatives of the North East of Vietnam), and Quang Tri (representative for the Center of Vietnam) in which Bac Giang and Hung Yen are regarded as biggest suppliers of poultry products for domestic market (more than 15,000 ton of meat/year/province and from 80- 120 million eggs/year/province). Meanwhile, Hanoi and Thai Nguyen are those of average poultry production scale with 70-80 thousand ton of meat/year/province and 70-80 million eggs/year/province. Quang Tri in the Central Coast of Vietnam produce poultry meat and eggs at small scale (about 1500 ton of meat and 10 million eggs/year), yet it is reported to be seriously affected by the avian influenza. At this moment, together with Hanoi it is among 10 provinces coping with complicated situation of avian influenza (10 provinces include Quang Ninh, Hai Duong, Nam Dinh, Tuyen Quang, Ninh Binh, Vinh Long, Phu Tho, Ha Nam, Hanoi and Quang Tri).

Object of the study

Poultry commodity is the topic of interest. Therefore, the survey, taken in 5 provinces in Vietnam, deals with actors of the poultry commodity, including chicken, duck, goose, bird, etc. However, with the in-depth study, it only focuses on chicken value chain, rather than other types of poultry because chicken production makes up the largest quantity, compared with others. As well, chicken and chicken eggs are the most popular products for Vietnamese people. Within the chicken commodity, the study takes into account such main products as chicks, live-weight chicken, carcass, and eggs

Poultry stakeholders involving in the study include hatchery, nursery, broiler, and layer farms, collectors, slaughterers and traders. However, the focus of the study are those of small and medium scales (under 1000 poultry heads for breeders and under 500 chickens slaughtered per day for slaughterhouses, under 500 chickens per day for collectors and traders), especially those of low income.

Methodology

In order to conduct the research, both desk-study and field-study are applied to collect secondary data on microfinance and poultry value chain policies; on poultry value chain, and on microfinance services provided for poultry stakeholders in the chosen areas as well as empirical information from poultry stakeholders by survey with qualitative and quantitative approaches, including semi-structure questionnaire, interview, direct and indirect observation, and participatory rural appraisal.

Desk study

This study starts with a desk study collecting secondary data to have a general overview of current situation of poultry value chain in Vietnam, policies for the development of poultry commodity and the micro-financing of this commodity. This is predominantly a collection of documentary data

8

such as reports, public records, books, scientific articles, statistic, etc. from on-line database, libraries, and from direct contact with development and research organizations in Vietnam to extract relevant information of the concerning issue, for example the Institute of Policy and Strategy for Agriculture and Rural Development/ Ministry of Agriculture and Rural Development, the Department of Animal Health/ Ministry of Agriculture and Rural Development, the Department of Husbandry/ Ministry of Agriculture and Rural Development, the Food and Agriculture Organization/ United Nations, as well as from on-going projects on poultry for instance STOP Avian Influenza, Avian and Pandemic Influenza: Preparedness and Response in Vietnam. Accordingly, the tasks at this stage consist of:

• Gather data and analysis to describe poultry commodity in Vietnam with problems and opportunities, especially the study focus on chicken since it dominates the poultry production in Vietnam

• Synthesize policies for the purpose of developing poultry value chain in Vietnam

• Depict the micro-financing of poultry value chain in Vietnam, with main suppliers and clients as well as microfinance products and services for poultry stakeholders. Yet, this study focuses much on micro-credit other than other kinds of financial products. Similarly, it put an emphasis on micro-plus that specially and efficiently serve the poultry value chain for consideration and analysis.

In addition, during the desk study, provinces supposed to conduct survey are identified and a case study for in-depth study is chosen. The provinces involving in the survey of this study include Hanoi, Hung Yen, Bac Giang, Thai Nguyen, and Quang Tri while the area for in-depth study consists of a case study in Dinh Hoa district- Thai Nguyen province.

The desk-study also encompasses the design of methodology that will be employed during the field work stage, for instance Participatory rural appraisal, semi-structure questionnaire, direct interview with poultry stakeholders and observation.

In fact, the desk-study is regarded as the theoretical background for the field study. It provides solid background on the topic of microfinance and poultry value chain but also well-prepared methodology to collect data in reality serving the purpose of analyzing current situation of poultry value chain financing with strengths, drawbacks, challenges, and perspectives after that.

Field study

Field study includes the survey with qualitative and quantitative questionnaire and PRA to collect general information of poultry value chain and the microfinance services for this chain, as well as case study with direct and semi-structure interview and observation for in-depth study.

The survey is conducted in 5 provinces throughout Vietnam, as indicated in the above section: Hanoi (Soc Son, Dong Anh, Thanh Oai districts), Hung Yen (Tien Lu, Yen My, Kim Dong districts), Bac Giang (Yen Dung district), Thai Nguyen (Dinh Hoa district), and Quang Tri (Trieu Phong, Gio Linh and Hai Lang districts) with particular focus on small and medium poultry stakeholders (including hatchery, nursery, broiler and layer farms, slaughterhouses, collectors, traders and concerning all kinds of poultry production) and for the following purposes:

• Gather data on microfinance services (financial and non-financial services), methodology, and main microfinance actors for the poultry value chain, provided in selected locations. At the same time, the availability of microfinance services offered by others actors (for instance the inter-linked credit arrangement, projects or programs, etc.) to stimulate poultry value chain activities of the selected areas will be examined.

• Analyze and map out the principal microfinance services provided in line with poultry value chain in selected areas

• Report on people’s perceived needs, satisfaction, priorities and expectations towards microfinance services to develop poultry value chain

In fact, the survey was carried out thanks to the support of the Rural Development Center- Institute of Policy and Strategy for Agriculture and Rural Development within the frame of their activity in Avian Influenza Risk Assessment, which belongs to the Avian and Pandemic Influenza Initiative project and the assistance of the company named Asian Veterinary and Livestock Services (ASVELIS) under the STOP Avian Influenza project. However, due to limited resources, the number

9

of poultry stakeholders involving in the survey is not so big, ranging from 20 to 30 households each province.

Table 1: Sample scale of the survey

Province Hatchery household

Breeder

(Nursery, layer,

fattener)

Collector/

Trader

Slaughter-house

Retailer Total Note

Hung Yen 4 20 3 - 4 31 Retailers

and also

slaughterer

Bac Giang - 18 1 1 2 22 Retailers

and also

slaughterer

Thai Nguyen - 16 1 1 3 21 Retailers

and also

slaughterer

Quang Tri 2 19 2 3 4 30 Retailers

and also

slaughterer

Hanoi - 16 3 - 5 24 Retailers

and also

slaughterer

Total 6 89 10 5 18 128

Furthermore, two participatory rural appraisals are taken place, one with the poultry breeders, slaughterers, collectors and traders in Yen My district/ Hung Yen province, and the other with some leaders of poultry value chains in Thai Nguyen, Bac Giang, Soc Son, Tien Giang and Binh Duong provinces to have different points of view towards the economic situation and micro-financing of poultry value chain in Vietnam and to clarify some issues that has not mentioned in detail in the survey questionnaire, for example the procedure of lending, applied by different microfinance service suppliers, advantages and disadvantages of some microfinance services, their needs towards financial and non-financial services,etc.

After that, based on the result of the survey, a case study with chicken value chains are conducted in Phuong Tien commun- Dinh Hoa district-Thai Nguyen province for in-depth study. The reason is that in this area, chicken production plays an important role for the local people, especially the low-income one. The microfinance serving chicken stakeholders is evaluated to be best facilitating low income poultry stakeholders to generate income and to develop quality chicken products. It is also due to the availability and potentiality of microfinance products for local poultry value chain and the willingness of local authority and people to take part in the study as well as social embeddedness of microfinance in the local poultry value chain. The case study aims at:

• Collect data related to production, processing, markets and prices of selected chicken of quality in selected provinces before and after certain offers of microfinance services for comparative purposes.

• Report on the differences and changes of local livelihood and product quality in chicken value chain in selected area before and after the access to microfinance services in view of provincial and more importantly of gender differences.

All databases of case study will be maintained for the purpose of organizing, documenting, and analyzing collected data. It is also considered as evidences of the research.

The field study includes several techniques to extract data and information on microfinance and poultry value chain efficiently, namely questionnaire, Participatory rural appraisal (PRA) and interview. Each methodology is demonstrated in detail as below:

10

- Questionnaire

Questionnaire with a series of questions concerning microfinance and poultry value chain is designed for different types of actors to collect information from them. It is regarded as an efficient research instrument that required less efforts, time and financial budget to gather data. In this research, the questionnaire will be simplified and comprehensive since it deals with poultry commodity, where the participants of the chain (producers, processors, traders…) are not so well educated.

- Interview

The actors of poultry value chain like producers (hatchery, nursery, broiler and layer farms) slaughterers, and traders, local authorities and microfinance actors are key persons that will all provide valuable information and opinions towards the research topic. Therefore, it is essential to conduct interviews with these actors. Semi-structure interviews aim at following the needed line of inquiry while still keeping the interview open and going, a suitable method of case study (Yin, 2003). In this research, semi-structured interviews are designed for both individual and group to maximize the information and ideas of the stakeholders.

Besides, the interview in this research is very crucial when it is not practical for some demographic groups conducting a survey by questionnaire

- Observation

The technique of observation here consists of both direct and indirect observation. With the direct observation, it is collected from personal observation when visiting the field, from group meetings of poultry value chain actors or microfinance practitioners, farming and production practices, or project meeting. In terms of indirect observation, it is in fact the indirect evaluation of microfinance and poultry value chain. To clarify, the researcher observes participants of poultry value chain microfinance to check the validity of the information provided, to understand their opinion towards the issues questioned to them, as well as to identify the limitation of the research itself with the field study to draw out experience.

- Participatory rural appraisal

Two participatory rural appraisals (PRA) were done quickly and intensively with the application of a series of methods, for instance interviews, focus groups, events. It is a short-cut method of data collection, involving both local people and outsiders, in which outsiders facilitates local people in analyzing information, practicing critical self-awereness, taking responsibility and sharing their knowledge of life and conditions to plan and to act1 (Bishnu B. Bhandari: 2003, pg 10).

The first PRA was taken place at the house of the leader of the Farmer Union in Yen Hoa commune, Yen My district, Hung Yen province with participants of poultry stakeholders of small and medium scale, both taking and not taking in poultry related projects in the province (for example, the representative from Rural Department of Yen My district, and the representative of the Rural Development Center/ Institute of Policy and Strategy for Agriculture and Rural Development. It included interview, observation, and discussion to exchange information and opinions towards microfinance products and services, suppliers, etc. to dig out current situation of microfinance for poultry stakeholders, credit policy implementation, perspective and solutions.

The second PRA dealt with focus group, regrouping leaders of some poultry value chains in Soc Son district- Hanoi, Dinh Hoa district- Thai Nguyen province, Yen Dung district- Bac Giang province, Phu Giao district- Binh Duong province, Go Cong town- Tien Giang province. It is the combination of workshop, field trip, chicken tasting events, weekend market, interview, discussion and observation, in which poultry stakeholders share information, and critical comments towards the issues and process of microfinance in poultry value chain throughout Vietnam.

The objective of PRA in this study is to increase the engagement of local community concerning poultry value chain and microfinance in the research and to understand their views on the research topic. The final aim of this technique is to enable local people, like poultry producers, or processors to assess the issue of microfinance, particularly micro-credit, for poultry value chain, and articulate their own demand, satisfaction and suggestion to address it.

It is an intensive approach to community engagement, which allows obtaining precious findings on microfinance within poultry value chain for the purpose of commodity development over a short period of time.

1 Bishnu B. Bhandari (2003) Participatory Rural Appraisal (PRA) Institute for Global Environmental Strategies (IGES)

11

Report outline

The report of this research starts with abstract and introduction of the research. Meanwhile, its main body includes three chapters. The first one deals with literature review of value chain, value chain approach and value chain microfinance in general. Then the second chapter brings an overview of Vietnamese poultry commodity in general and chicken in particular, policies for poultry value chain development, microfinance market with clients and suppliers for poultry stakeholders, and types of microfinance products. The third chapter describes the results of the field work, with particular focus on micro-financing for poultry value chain of small and medium scale in Vietnam, especially for chicken value chain. It consists of the sections on current actors of microfinance services in poultry value chain, types of microfinance services, methodology providing microfinance services, the link between microfinance and poultry value chain and a case study of micro-financing chicken value chain. Finally, the conclusion present the findings of the study, discusses the advantages, constraints and challenges of providing microfinance services to the actors of poultry value chain and gives some recommendations for good application of micro-financing poultry stakeholders with value chain approach for the purpose of better poultry value chain development.

12

CHAPTER I

Literature review

I.1. What is value chain?

Value chain, or supply chain, commodity chain, production chain in other terminology, is defined as a range of activities conducted by individual or organizational stakeholders of the same chain to provide product or service from the very beginning conception to the end users. These stakeholders normally include input providers, producers, processors, collectors, traders, wholesalers, retailers, consumers as well as third parties providing such additional services as finance, market research and logistic to these stakeholders. These participants of the value chain have close vertical linkages with each other for the final purpose of ensuring efficient product flow to meet the demand of their target clients, developing the value chain, creating a fair competitiveness in the value chain, optimizing productivity, better the position of the products and value chain stakeholders in the market, and maximizing profit. The activities of these actors within a value chain are classified into different stages, for example production, processing, distribution, etc. in which at each stage a new value is added to the value chain.

This definition derives from the point of view of Raphael Kaplinsky and Mike Morris, who considered value chain as “the full range of activities which are required to bring a product or service from conception, through the different phases of production (involving a combination of physical transformation and the input of various producers services), delivery to final consumers and final disposal after use” [Kaplinsky.R & Morris.M, 2000, 4].

According to these authors, the notion of a value chain can be understood in different ways. Interpreted in a narrow fashion, the value chain is a set of activities that take place within a manufacturing unit like firm or enterprise to produce a certain product or service. These activities create a connection or linkage between producers and customers. Interpreted in broader manner, however, a value chain is an assemblage of activities carried out by different actors (namely producers, processors, collectors, wholesalers, service suppliers, retailers, etc.) in order to turn raw materials into finished products that satisfy the needs of customers.

This broad conception of value chain embraces a large number of issues related to value chains and development more generally, including organization, coordination, strategies and interaction among participants and even social problems (community relation, habits, and production standpoint, consumption attitudes, etc) and environment (land degradation, water pollution, and biographical diversification, etc.)

What is more, the definition above keeps the emphasis on the close linkage among different economic actors to improve the value chain by adding value to the chain with their own activities as indicated Mr. Golletti Francesco- Consultant of Agrifood Consulting International in the project Marking Markets Work Better for the Poor, funded by the Asian Development Bank in 2004

Nevertheless, it also highly appreciates the authors John T. Mentzer et al., who defined value chain as “a set of three or more entities (organizations or individuals) directly involved in the upstream and downstream flows of products, services, finances, and/or information from a source to a customer” in their article “Defining value chain management”, in the Journal of Business Logistic [John T. Mentzer et al., 2001, 4].

I.2. Value chain approach

From the definition of value chain, it is easier to understand the value chain approach, which has been applied into different fields, especially very common in agriculture and rural development to analyze a certain commodity for the purpose of management and development of the value chain.

In fact, value chain approach was pioneered by the economist Michael Porter in1985, who focused on how value chain analysis could help companies recognize their position in the market, and its relationships with suppliers, clients, and competitors. Based on this analysis, enterprises

13

could identify their own competitive advantage to facilitate their product design, inputs, logistic, marketing, sales, after sales services, and/or resources management, etc. However, the limitation of this initiative is that it can applied optimally to develop corporate policies concerning administration and business management at enterprise level, or at higher level of highly typical branches such as industrial crops, processing materials with the involvement of all companies producing, processing, or distributing products or services, but not for all stakeholders or all rural and agricultural value chains.

Therefore, based on the “enterprise perspective” of “value chain” of the economist Michael Porter in 1985, in the “Commodity chains and global capitalism” in 1994, Gereffi brought new initiative when convincing that the value chain should be coherent, and well analyzed by studying not only organization but also individuals that play crucial role in the development and management of the value chain, not only within manufacturing system but also distribution one, and not only within domestic market but also at international market if the value chain has connection at global level.

However, the truly applied value chain approach for agriculture was described in “A Hand Book for Value Chain Research” by Raphael Kaplinsky and Mike Morris in 2000 when they proposed to analyze value chain by studying sequence of activities of different actors in the frame of a value chain, with the focus on linkage and value distribution in a vertically organized system to identify the value or the benefit acquired by each stakeholder.

Then in 2002, John Humphrey once again insisted on the importance of relationship and interaction of stakeholders with value chain approach for the purpose of defining dynamics, opportunities and constraint of markets for a certain product.

In short, value chain approach analyzes the flow of commodities and linkage among actors of a specified sub-sector and contributes to the identification of opportunities of constraints of a particular value chain for its growth. This approach has been widely applied by non-governmental organizations and research institutes in agriculture and rural development throughout the world.

I.3. Value chain microfinance

Value chain microfinance is in fact the application of value chain approach in microfinance sector to provide microfinance services, such as micro-credit, micro-savings, micro-insurance, services of money transfer, or microfinance plus (non-financial products/services which include technical assistance, training, exchange activities, etc.) to different stakeholders within a particular value chain, for example rice value chain, horticultural value chain, litchi value chain, catfish value chain, poultry value chain, pig value chain, and so on so forth.

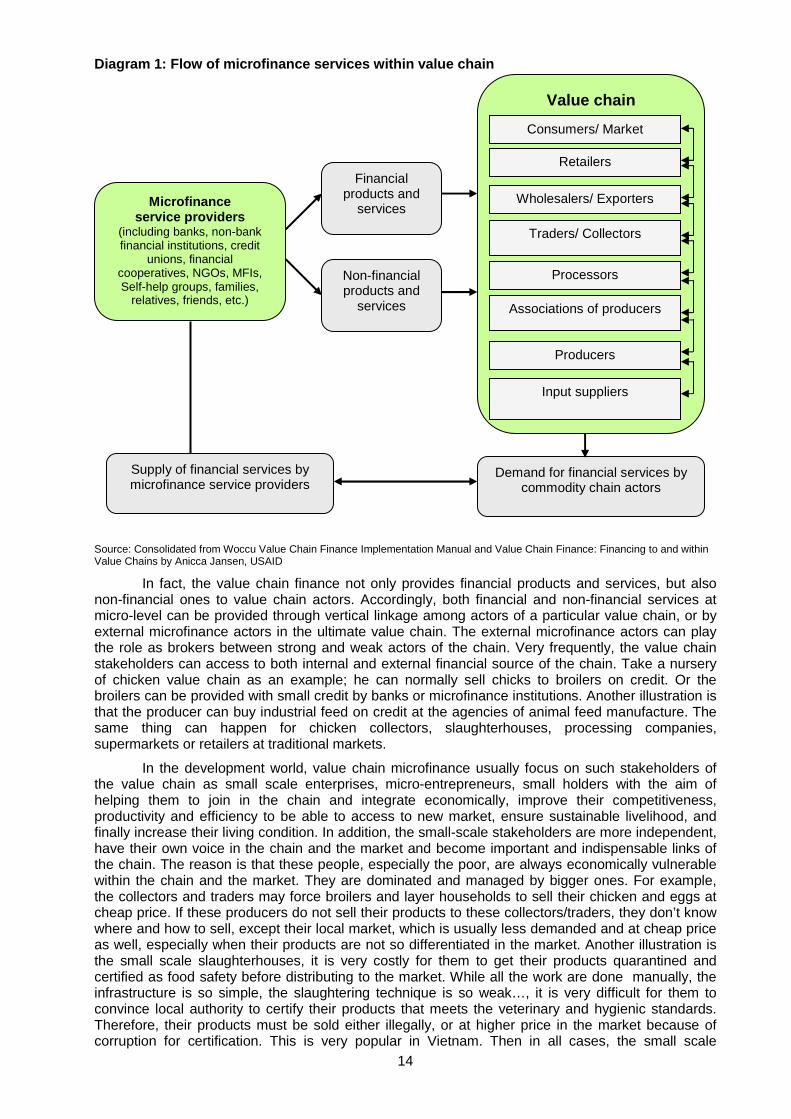

The financial flow into a value chain can come from both internal and external sources. In case of internal value chain finance, it refers to the vertical flow from a stakeholder of the value chain to others in the same chain. In other words, it is the interlinked credit arrangement among value chain actors, or buying and selling on credit. This kind of financing is good in the sense that it reduces transaction cost since it is embedded in economic transaction among value chain stakeholders. In case of external value chain finance, it means that the financial actors provide financial services to stakeholders in the chain, based on their demand, for the purpose of running their production and business. The flow of microfinance services within the value chain can be described in the following diagram:

14

Diagram 1: Flow of microfinance services within val ue chain Source: Consolidated from Woccu Value Chain Finance Implementation Manual and Value Chain Finance: Financing to and within Value Chains by Anicca Jansen, USAID

In fact, the value chain finance not only provides financial products and services, but also non-financial ones to value chain actors. Accordingly, both financial and non-financial services at micro-level can be provided through vertical linkage among actors of a particular value chain, or by external microfinance actors in the ultimate value chain. The external microfinance actors can play the role as brokers between strong and weak actors of the chain. Very frequently, the value chain stakeholders can access to both internal and external financial source of the chain. Take a nursery of chicken value chain as an example; he can normally sell chicks to broilers on credit. Or the broilers can be provided with small credit by banks or microfinance institutions. Another illustration is that the producer can buy industrial feed on credit at the agencies of animal feed manufacture. The same thing can happen for chicken collectors, slaughterhouses, processing companies, supermarkets or retailers at traditional markets.

In the development world, value chain microfinance usually focus on such stakeholders of the value chain as small scale enterprises, micro-entrepreneurs, small holders with the aim of helping them to join in the chain and integrate economically, improve their competitiveness, productivity and efficiency to be able to access to new market, ensure sustainable livelihood, and finally increase their living condition. In addition, the small-scale stakeholders are more independent, have their own voice in the chain and the market and become important and indispensable links of the chain. The reason is that these people, especially the poor, are always economically vulnerable within the chain and the market. They are dominated and managed by bigger ones. For example, the collectors and traders may force broilers and layer households to sell their chicken and eggs at cheap price. If these producers do not sell their products to these collectors/traders, they don’t know where and how to sell, except their local market, which is usually less demanded and at cheap price as well, especially when their products are not so differentiated in the market. Another illustration is the small scale slaughterhouses, it is very costly for them to get their products quarantined and certified as food safety before distributing to the market. While all the work are done manually, the infrastructure is so simple, the slaughtering technique is so weak…, it is very difficult for them to convince local authority to certify their products that meets the veterinary and hygienic standards. Therefore, their products must be sold either illegally, or at higher price in the market because of corruption for certification. This is very popular in Vietnam. Then in all cases, the small scale

Microfinance service providers

(including banks, non-bank financial institutions, credit

unions, financial cooperatives, NGOs, MFIs, Self-help groups, families,

relatives, friends, etc.)

Financial products and

services

Non-financial products and

services

Value chain

Consumers/ Market

Retailers

Traders/ Collectors

Processors

Associations of producers

Producers

Input suppliers

Wholesalers/ Exporters

Demand for financial services by commodity chain actors

Supply of financial services by microfinance service providers

15

stakeholders are the ones who suffer the most, then followed by the medium scale ones. Therefore, microfinance actors, together with their financial and non-financial products and services, are certainly useful in upgrading the situation and position of the small and medium scale actors of the value chain by (i) opening them opportunities to access to credit and become financially independent from the buyers; (ii) improving their bargaining position either by brokering contacts with other buyers that are also their clients or organizing collective actions like collective sales; (iii) enhance their knowledge, skills and technologies in their activities; (iv) assisting them to achieve standards required for poultry and poultry based products, to get certifications, and to develop their own label and trademark; or (v) to reduce the risk associated with their business. When well done, it will equip value chain stakeholders with not only financial source, but also technical skill, entrepreneurship and partnership, etc. to conduct their business confidently. What value chain microfinance is helpful is that it can take advantage of the relationship among value chain stakeholders to reduce operational cost and the risks related to credit.

Hence, following the value chain approach for the purpose of development like increasing income of small stakeholders of the value chain and those considered as economically active poor, value chain microfinance shows that all the actors of the chains need to be provided with appropriate and prompt financial services. In other words, providing access to credit for the stakeholders within the value chain is vital to guarantee a smooth product flow, and then can help to enhance the competitiveness of a value chain in the whole, and ensure successful business. As a result, lack of credit at any stage of the value chain has impact on all other actors. Similar to the example presented above, if the broilers can not buy chicks or industrial feed on credit, or do not access to any financial sources, the number of chicken supposed to provide for collectors and slaughterhouses will be certainly limited. Consequently, all the actors of that chicken value chain will suffer from this shortage. However, such financial sources are not always available and easily accessed for all stakeholders of the chain. Many of actors working in agricultural and rural development in general and in poultry value chain in particular claim for lack of financial sources while they need financial services from banks and other financial agents to keep operating and growing their businesses. Therefore, providing microfinance products and services through the value chain approach helps to identify these shortcomings and assists in finding appropriate interventions.

While Robert Fries & Banu Akin have a rather narrow point of view on “value chain finance” when he considers it as financial mechanisms and products within and among the actors of the value chain itself, the other authors show that there is evidently link between value chains and microfinance provided by outside institutions, interacting with the stakeholders in the chain.

For Robert Fries & Banu Akin, they described value chain finance with three main characteristics. The first is chain governance: interaction and relationship among series of activities in a chain as well as rule that govern these activities and linkage are critical issues since one may be a leader or a dependent player. “In order to ensure consistent, reliable and adequate supply, lead firms may be motivated not only to dictate specifications, but also to embed such services as technical assistance, training, and finance into the marketing services they provide. Finance can be an incentive for contracts that ensure supply, as well as fund the working capital a producer needs to upgrade a product to meet a buyer’s standards.” [Fries, R. & Banu. A, 2004, 6]

The second is upgrading as a central concept because a player or group of players can bring more value for the chain and/or get more value from the chain. “Value chain financing, focused more on seasonal working capital than longer term investment capital, is more likely to facilitate product upgrades than process upgrades. One exception is warehouse receipts, which can build significant efficiencies into the marketing process itself and allow a farmer access to scale efficiencies typically available only to players further up the value chain” [Fries, R. & Banu. A, 2004:18]. Bastiaensen. J et al. even clarify four types of upgrading in the Rural Microfinance & Agriculture Value Chains: Strategies and Perspectives of the Fondo de Desarrollo Local in Nicaragua, including “(1) process upgrading (increasing the efficiency of internal process within individual links in the chain and between the links in the chain); (2) product upgrading (introducing new products or improving old products); (3) functional upgrading (increasing value added by changing the mix of activities conducted within firms of moving the locus of activities to different links in the value chain); and (4) chain upgrading (moving to a new, qualitatively better value chain)” [Armendariz*, B., and Labie*, M. 2010].

The third is techniques applied to value chain analysis, which consist of: (i) mapping: showing the flow, cost, value added and importance of each stage of transformation and transactions of product/service from initial input to final sale; and (ii) participatory approach to tackle

16

and pursue bottlenecks and opportunities within the value chain through the participation of stakeholders.

However, for the authors, besides the interlinked among stakeholders of the chain, value chain finance also represents “the link between chain actors and financial institutions”, which is regarded as “a means to deepen financial services for value chains” built on the established relationships in the chain and strong relationship between chain actors and financial service providers “to support the product flow”, with the aim of addressing “perceived constraints and risks by providing innovative ways of delivering financial services to rural producers and agribusinesses”. Then, the product flow in the value chain plays the role as the carrier to provide financial services. “This way of financing can spread risk among the financial institutions and chain actors and provides alternatives to traditional collateral requirements. It provides tremendous potential for unleashing capital, scaling up and sustaining chain prospects, but it needs to be managed and organized well.” Accordingly, the financial service providers need to “have a deep understanding of the realities in the chain and of the need for timely and flexible finance” while the actors of the value chain need to “understand the business realities and mentalities of banks and microfinance institutions looking at risk mitigation and cost coverage for their services.” [KIT & IIRR, 2010, xii].

In addition, another kind of link should be set up; it is the vertical linkages in the financial sector, meaning that financial actors collaborate to provide different stakeholders of the value chain with a variety of sizes ad types of financial products, for example insurance, overdrafts, factoring and leasing models, as well as investment loans, guarantees and venture capital. For example, microfinance institutions can link with producer organizations to provide small input loans to producers, while banks simultaneously provide an investment loan to a processing company in the chain. The microfinance institutions and banks need to link up to align their services in this chain for potential overdraft facilities to small traders. (KIT & IIRR: 2010. pg xiii).

In reality, financial institutions find that microfinance and the value chain converging. As indicated in the Innovation in Financing Value Chain: Using Market Agreements to Reduce Povert- WOCCU/FENACREP experience in Peru, financial institutions integrate financial products into the value chain since they, together, can helps reducing “the risk of rural and agricultural finance while maintaining an adequate financial margin and low risk of loan default”. Furthermore, it can be implemented “without the need for operating subsidies or guarantee funds”. Therefore, It is used to “design a variety of financial products, to evaluate and finance all types of value chains and adapted to other environments” [Luis J.G., 2009]

What is more, providing microfinance services through microfinance can be considered as a powerful strategy for mitigating rural finance constraints. For example it defines business as integrated units rather than one single activity of an individual borrower recognizing interactions of small scale producers and rural small and medium enterprises with each other and with larger domestic or foreign firms. Another advantage is that it is a demand-driven approach, reacts to market forces by responding the specific needs for financial products at any point in the chain.

To sum up, the application of value chain into microfinance is quite relevant. As Robert Fries & Banu Akin explained, firstly because “it starts with what is already happening in the field—the actors, relationships, rules of play, range of services (including embedded financial services), and bottlenecks to growth. This increases the likelihood that interventions and innovations will help to close the insufficiency and inefficiency gaps of rural finance, by recognizing and incorporating market realities rather than distorting them” [Fries, R. & Banu. A, 2004, 7].

Secondly, it encourages to regard “expanded financial services not as ends in themselves, but as inputs for increasing the competitiveness and earnings of particular value chains—specialty coffee, grains, horticulture, for example—and particular actors within them” [Fries, R. & Banu. A, 2004, 7].

Last but not least, “to the extent that a participatory approach is used, it incorporates the perspectives and taps the energy of critical stakeholders and champions of promising interventions, increasing the likelihood that interventions will build on existing innovations and relationships and receive the buy-in they need to be successful” [Fries, R. & Banu. A, 2004, 7]. .

17

CHAPTER II

Current situation of poultry value chain in Vietnam

This section aims at presenting a general overview of poultry value chain in Vietnam by analyzing it through facts and figures of production, characteristics of poultry production system, modeling it with popular poultry value chain based on types of products, digging it in SWOT analysis, together with a summary of policies for its development with particular focus on financial issue. Also, the situation of micro-financing for poultry value chain, particularly for stakeholders of small and medium scale are presented through secondary data on service providers, borrowers, financial and non-financial products.

II.1. Analysis of poultry value chain in Vietnam

II.1.1. Poultry production: Facts and Figures

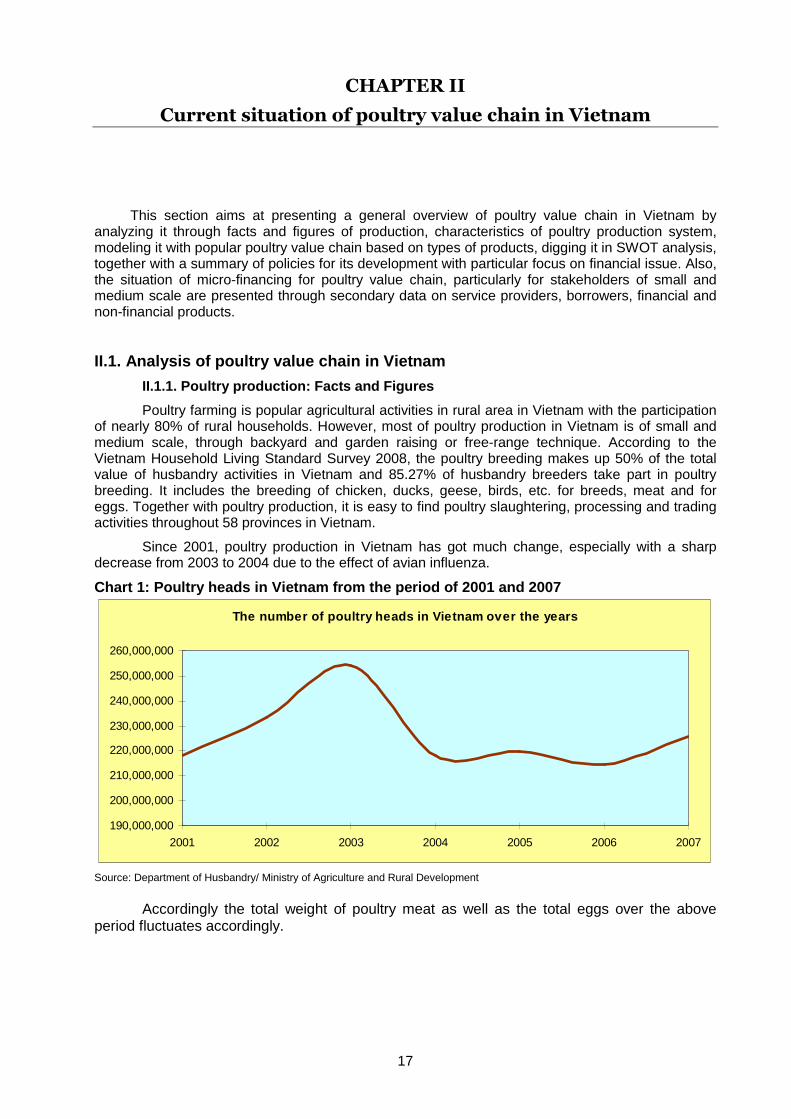

Poultry farming is popular agricultural activities in rural area in Vietnam with the participation of nearly 80% of rural households. However, most of poultry production in Vietnam is of small and medium scale, through backyard and garden raising or free-range technique. According to the Vietnam Household Living Standard Survey 2008, the poultry breeding makes up 50% of the total value of husbandry activities in Vietnam and 85.27% of husbandry breeders take part in poultry breeding. It includes the breeding of chicken, ducks, geese, birds, etc. for breeds, meat and for eggs. Together with poultry production, it is easy to find poultry slaughtering, processing and trading activities throughout 58 provinces in Vietnam.

Since 2001, poultry production in Vietnam has got much change, especially with a sharp decrease from 2003 to 2004 due to the effect of avian influenza.

Chart 1: Poultry heads in Vietnam from the period o f 2001 and 2007

The number of poultry heads in Vietnam over the yea rs

190,000,000

200,000,000

210,000,000

220,000,000

230,000,000

240,000,000

250,000,000

260,000,000

2001 2002 2003 2004 2005 2006 2007

Source: Department of Husbandry/ Ministry of Agriculture and Rural Development

Accordingly the total weight of poultry meat as well as the total eggs over the above

period fluctuates accordingly.

18

Chart 2: Weight of poultry meat and eggs produced i n Vietnam over the period of 2001-2007

Poultry meat and eggs produced in Vietnam over the years

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2001 2002 2003 2004 2005 2006 2007

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Carcass

Egg

Unit: ton Unit: egg

Source: Department of Husbandry/ Ministry of Agriculture and Rural Development

In poultry commodity, chicken makes up a great part. In fact, chicken and eggs are products much more popular for the Vietnamese people than other kinds of poultry like duck, goose, birds, etc. Just take 2007 as an example (latest data on poultry), chicken heads accounted for 69.89% of total poultry heads.

Now that dealing with a more up-to-date data on poultry, the recent husbandry survey in April 2010 of the General Statistics Office of Vietnam shows that the number of poultries all over the country is 277.4 million, up 8.1% from the same period of the previous year. Then, it can be said that poultry production has recovered from serious disease of avian influenza.

II.1.2. Poultry production system Poultry breeding in Vietnam follow three main kinds of breeding: (i) Manual and small-scale breeding (under 50 chickens): very traditional and popular, with

participation of 65% of households raising chicken extensively and accounting for more than 50% of total chicken head per year2. The main characteristics include free range, letting poultries scavenging in the garden, taking advantage of by-product in agriculture (rice brand, sesame, maize, cassava…), hatching and nursing chicks by themselves. This method is very suitable with economic condition of local households, as well as with local breeds (like Ri, Mia, H’mong, Tre, Ho, Dong Tao, Tau Vang etc.), that produce poultry and eggs of quality, but low productivity and long production cycle (6-7 months to reach 1.2 to 1,5kg for chicken);

(ii) Semi-industrial breeding: with medium scale of 50-1000 poultry heads, and participation of 10-15% of poultry breeders, producing 25-30% of poultry quantity annually. This is rather modern method, using semi solid or solid shelters, semi-automatic drinker and feeder system, good productivity chicken breed (high breeds or crossed breeds) (such as Luong Phuong, Sacso, Kabir, etc.) of short production cycle (70-90 days), and industrial feed;

(iii) Industrial breeding: big scale of 2000- 30,000 poultry heads/ farm (but up to 60,000- 100,000 poultry for some), develop very fast since 2001, but makes up only 20% of the total chicken production. This kind of breeding usually use high-breed poultry (like Isa, Lormann, Ross, Hiline chickens etc.) fed with industrial feed completely, solid shelter, actively control the temperature and humidity of breeding area, short production cycle (for instance, 42-45 days to raise chicken until they weight 2.2- 2.4 kg/chicken). However, industrial chicken breeding involves only those with strong financial capacity.

The size of herd in these three kinds of production systems often increases before Tet

2 General Statistic Office

19

festival (New lunar year) and reduce in the period of June to July because of the summer heat. While the small breeding rather serves households’ own consumption, the medium and big ones are for commercial purpose. However, the majority of poultry breeding in Vietnam is of small and medium scales. Within this study, only small and medium scale poultry stakeholders, who raise poultry for commercial purpose, are concerned.

II.1.3. Popular model of poultry value chains in Vi etnam Different types of poultry products and different locations can have their own model of poultry

value chain. Nevertheless, popular models of poultry value chain in Vietnam can be illustrated as the following, based on three main products: meat, egg and day old chick.

Diagram 2: Popular poultry value chains in Vietnam Poultry meat value chain

Poultry egg value chain Day old chick value chain

It is crucial to know that the day old chick value chain is particularly rather complicated since

the eggs are usually collected regardless origin before selling to hatchery farms. For all the three value chains, although some enterprise tries to develop their trade-marks, product quality, quality controlling and traceability system to persuade customers in the market, the matter of quality and origin still challenge the authorities, entrepreneurs and customers. And despite the fact that some attempts to integrate in international market and export to some neighboring countries, the market for poultry products produced in Vietnam is mainly domestic.

II.1.4. SWOT analysis

a. Strength

Popular product

Poultry is a popular product and highly consumed by Vietnamese consumers. According to the International Egg and Poultry Review of the USDA in July 2010, poultry meat accounts for 13% of meat consumed in Vietnam (preceded by pork with 76% and followed by red meat of 9%). At this moment, the average annual meat consumption of Vietnamese people is about 40 kg/capital and estimated to reach the number of 57 kg/capita in 2020. The General Statistics Office of Vietnam also places poultry in the list of popular livestock products. Furthermore, in Vietnamese tradition, chicken is very demanded in all festivals throughout the year and usually used as special offerings.

Poultry breeding is also a popular activity in rural area in Vietnam. It is executed by all ethnics in all provinces in Vietnam, regardless delta or mountainous areas. Therefore, it is not surprised when poultry is an important source of cash income for more than 4 million households in Vietnam currently.

Product diversification

Consumer

Input supplier

Poultry breeder

Collector and trader

Processor/ Slaughter-house

Distributor/ Wholesaler

Retailer

Input supplier

Poultry breeder

Collector and trader

Distributor/ Wholesaler

Retailer

Consumer

Input supplier

Collector and trader

Hatchery

Assembler/ chick keeper

Retailer

Consumer

20

Poultry products in Vietnam are much diversified. They can be chicks, chickens or pullets. They can be ducks, geese, quail, pigeon, and thousands of others kinds of birds. They can be normal eggs or incubated eggs (usually for duck and quail). They can be imported breed like Cob 707, Ross 308, Kabir, AA, Hubbard ISA, or crossed breed (Luong Phuong x Sasso, Luong Phuong x local breeds), or local breed (Tau Vang in the South; Ri, Mia, Tre, Dong Tao, H’mong/ black bone chicken, and fighting chicken in the North). All can be cooked deliciously and believed to have many health benefits over other sources of protein. For rural dwellers, poultry is a cheap source of protein. In the market, live-weigh poultries, fresh and frozen carcass, or poultry based products (like gio, sausage…) can be all found easily. The diversification of poultry products can then satisfy different types of customers.

b. Weakness

Vulnerable to disease

The small scale breeding with less investment in housing and facilities, less vaccination coverage, and garden backyard technique, dominates poultry commodity in Vietnam and show high resistant to disease. This has been showed during the outbreak of avian influenza since 2003 (more details can be found in the threat of avian influenza). The ability of disease infection is especially high for duck production, in which the animals are gathered in rice fields during the day and brought back to their shelters at night, and they can move from one province to another.

Vulnerability to disease is not only shown in breeding technique, but also in poultry commodity management. Following the whole value chain, it is easy to find the existence of unqualified hatchery farms and slaughterhouses where quarantining and veterinary services are carelessly taken cared of; or the broiler farms with mixed poultries of different types, and ages without separate production areas, without vacuum period and sterilized entrance; or poultry traders using motorbikes to transport live-weight poultries and carcass; or retailers selling poultry and poultry based products in dirty condition. These unqualifications help increasing the possibility of disease transmission in poultry flock. While at initial stage, the quality and standard can not be controlled, how can final products be ensured with quality in the market! To make the matter worse, private hatching using unknown origin eggs was blooming out of control after the first waves of avian influenza, while hatching was limited but there is a high demand in restructuring poultry herd. At this moment, the authority can not control the origin of poultry in Vietnam with complicated poultry movements. It is even much more difficult while many eggs or chicks are transported illegally through all borders of the country.

Weak management in poultry value chain

Weak management from farms to markets

The bad management can be illustrated somehow in the previous paragraph. In addition, the place of breeding poultry is not well organized, just taking advantage of free place for breeding, close to living place, without bio-security, without vacuum period, etc. It should be added that the good production practice is not well ensured, and then it is found that many poultry has not been vaccinated. This is also a reason why the avian influenza can spread so fast in Vietnam for the last years. Furthermore, the way of slaughtering and processing poultry. Throughout Vietnam, it is easy to witness the sellers killing chicken in dirty manner, meaning that right at the point of sale, or in slaughterhouses but at dirty places (for example near the sewerage and the dust bin). Even it is prohibited by law, this still happens illegally. Even with the way of importing poultry production, it is claimed that the placement of poultry imported boxes is next to the plant protection chemicals, or the old ones next to the new ones.

The reason lies in the fact that administrative works in epidemic prevention, slaughterer control, and check ups by veterinarians care not highly appreciated. All levels of the veterinary department operate ineffectively. Slaughterhouses break veterinary ordinances, are not being licensed by the licensing authority, and run out of veterinary department control. For years, food has not been inspected and is often circulated in the market without a control stamp. In addition, the spread and frequency of disease outbreaks are proof of the poor veterinary system at the grassroots level, particularly with respect to epidemic diagnosis and detection and epidemic prevention. There is interest in daily and periodic cleaning by large-scale farmers, but not small scale producers, who also seldom use chemicals to prevent disease.

21

Apart from that, vaccines and inoculations are administered mostly by large and medium-scale farmers, but not small scale producers. In addition, some farmers use different vaccines for preventing the same disease because of the various vaccines and their inability to distinguish between them. What is more, responsible agencies for quality control are limited, operate independently, and cooperate very weakly. The control system only emphasizes administrative procedures, and lacks professional tools. To make the matter worse, individual farmer have little interest in quality control. Cooperatives have attempted to address this problem, but have largely failed to encourage farmers to follow a collective production process. Processing companies and farmers have not succeeded in contractual production. In addition, slaughtering systems in rural areas as well as urban areas are not sanitary. Slaughterers are not proactive with respect to hygiene. The retail faces the same situation. Quality control system has been out of hand.

Weak management in poultry import

The import of poultry product includes two ways, legally and illegally. The following section is supposed to discuss problem of poultry smuggling into Vietnam as well as the cold poultry imported that has dramatic effect on domestic poultry market.

Poultry smuggling

The poultry smuggling is a headache for the local and national authorities and poultry breeders in Vietnam because it not only affect the domestic poultry market, competitiveness and income for poultry breeders, but also leads to the trans-boundary spread of avian influenza (this is really serious in the borders between Vietnam and China, when poultry is smuggled from Quangxi and Guangdong in China to Quang Ninh and Lang Son provinces in Vietnam). Normally, poultry products are imported illegally from China to Vietnam, not only for consumption of the border provinces, but also transported deeply to the inner provinces like Bac Giang, Bac Ninh, Hanoi, Hai Phong, Nam Dinh, Thai Binh, Hai Duong, Thanh Hoa and Nghe An provinces.

The study entitled “Cross Border Poultry Movement Analysis Between Lang Son and Quang Ninh provinces in Vietnam and Quangxi and Quangdong provinces in China” conducted by the Rural Development Center of the Institute of Policy and Strategy for Agriculture and Rural Development and the Food and Agriculture Organization in 2009 shows that poultry and poultry products smuggled into Lang Son and Quang Ninh provinces since 2005 include pullets (after their production cycle), chicks and ducklings (of 10 to 15 days old), chicken eggs (including eggs for sitting and for eating), ready-to-cook chicken and duck, chicken ovaries and duck feather.

Among these products, pullets, chicken eggs (both for daily food and for sitting) and poultry breed are 3 main and frequent products imported in Vietnam. Pullets are those used to produce eggs but excluded after being exploited. Every year, thousands of large-scale breeding farms in Quang Tay discard millions of this kind of chicken, which is then smuggled to Vietnam for consumption. The fact is that Vietnamese consumers, especially food kiosks and restaurant, are fond of them because their meat is as tough and resistant as Vietnamese ones, but the price is much lower, compared with domestic chicken. Chicken eggs include eggs for daily consumption and eggs for sitting. The quality of Chinese eggs for daily consumption is evaluated to be lower than the one of domestic eggs, some are claimed to be artificial, on contrary; their eggs for sitting have better quality. In terms of chicks and ducklings imported for breeding and producing meat, normal the one of 10-15 days old are often imported illegally.

The others like chicken ovaries, duck feather and ready-to-cook poultry are infrequent product imported (in fact smuggled) and with small quantity. To have an overview of the quantity of the main poultry products smuggles into Vietnam, please see the data collected in the borders between Vietnam and China in Lang Son and Quang Ninh provinces in the following tables:

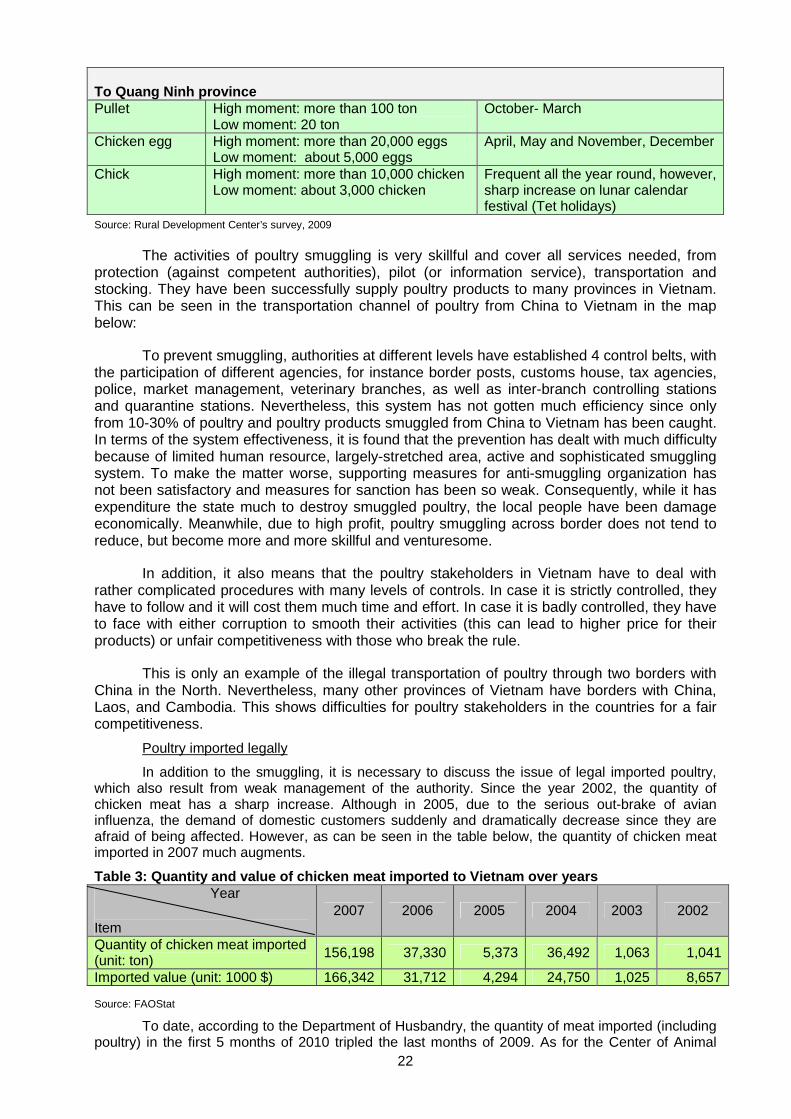

Table 2: Scale and moment of poultry smuggling from China to Lang Son and Quang Ninh provinces

Type of product

Quantity Months with high rate of importation

To Lang Son province Pullet High peak: 10-15 ton/day

Low moment: 1-2 ton/day October- March

Chicken egg Chi Ma border gate: 30,000 eggs/day May, June, July Chick and duckling

Huu Nghi border gate: 30,000-40,000 heads/day Chi Ma border gate: 50,000 heads/day

March- July (double the quantity compared with other months)

22

To Quang Ninh province Pullet High moment: more than 100 ton

Low moment: 20 ton October- March

Chicken egg High moment: more than 20,000 eggs Low moment: about 5,000 eggs

April, May and November, December

Chick High moment: more than 10,000 chicken Low moment: about 3,000 chicken

Frequent all the year round, however, sharp increase on lunar calendar festival (Tet holidays)

Source: Rural Development Center’s survey, 2009