bewise'i loeng: ivo vaks "performance management ja laienemine microsofti näitel"...

DESCRIPTION

Ivo Vaks viis läbi BeWise'i projekti raames loengu "Performance Management ja laienemine Microsofti näitel". Ivo Vaks, Westen Europe Area Segment Finance Lead (Mature/developed markets) Microsoftis, käsitles oma loengus neid teemasid: • hetketrendid äris • innovatsiooni koostisosad • eduka äri mõttelaad • väljakutsed uutel turgudel • seigad (äri)kultuuri erinevustest • õppetunnid elust enesest • Q&A jpm Ivo Vaks on omandanud majandusmagistrikraadi Tallinna Tehnikaülikoolis ja praeguseks on ta juba üheksa aastat töötanud Microsoftis nii finantsjuhi kui uute turgude värbajana, seda nii Eestis, Saksamaal kui ka praegu Microsoft Netherlands´s. Ivole meeldivad muuhulgas mootorrattasõit, reisimine ja uute asjade avastamine. http://bewise.jcitallinn.ee/ http://www.facebook.com/jci.bewise http://youtu.be/a-LLAIb65VITRANSCRIPT

Finance Today: reimagined to drive impact (performance&expansion)Ivo Vaks, Finance Lead,Enterprice & Commercial Devices SegmentMicrosoft Corporation, Amsterdam, WE

18 September 2014

The 5 Crucibles of Change

1. The great rebalancing50% of global GDP growth over the next years will come from non-OECD countries

2. The productivity imperativeGrowth = Labor * Productivity

3. The global grid20-50B networked devices by 2014

4. Pricing the planet+30% resource consumption by 2020

5. The market stateGov’t debt levels to increase by 50% by 2015

Ingredients of InnovationA balance of

invention, reinvention and evolution

Hiring the best people

A commitment to openness and partnership

A long-term approach

A focus on breadth and scale

Embracing disruptions

The “New” Reality

Resource Utilization Agility

Resource Optimizatio

n

MoreInnovation

Capture & create new opportunity

Get more out of your people

Increase Productivity

5

The New World

Designed to ChangeGood EnoughSimpleAnyone can buildOutside-in, Bottom-Up

Built to LastHeavily customizedComplexityRequires experts…labcoats Inside-Out, Top-Down

Business Challenges & Finance Imperatives

Business Challenges Finance Imperatives

Innovate & investfor revenue growth

Smart investments &efficiencies

Plan for uncertaintyand risks

Strategic planning & performance management

Productivity &resource optimization

Business risk management

1

2

3

7

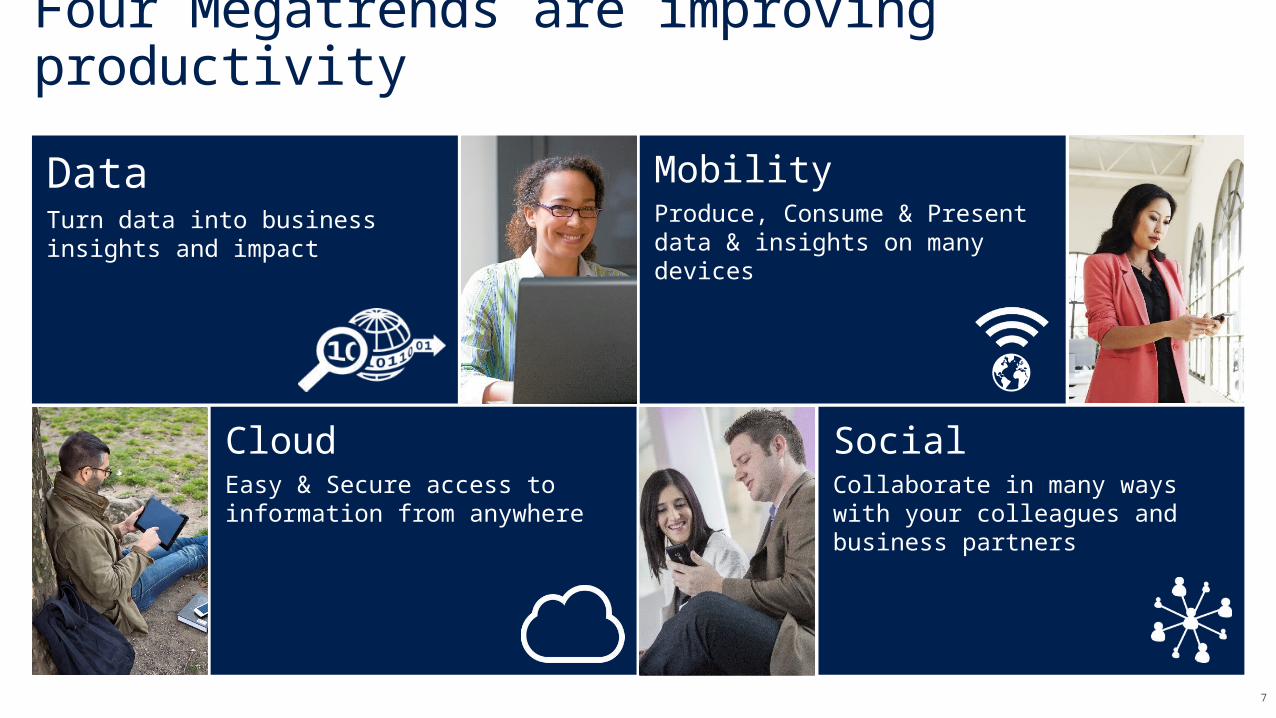

Four Megatrends are improving productivity

DataTurn data into business insights and impact

MobilityProduce, Consume & Present data & insights on many devices

CloudEasy & Secure access to information from anywhere

SocialCollaborate in many ways with your colleagues and business partners

8

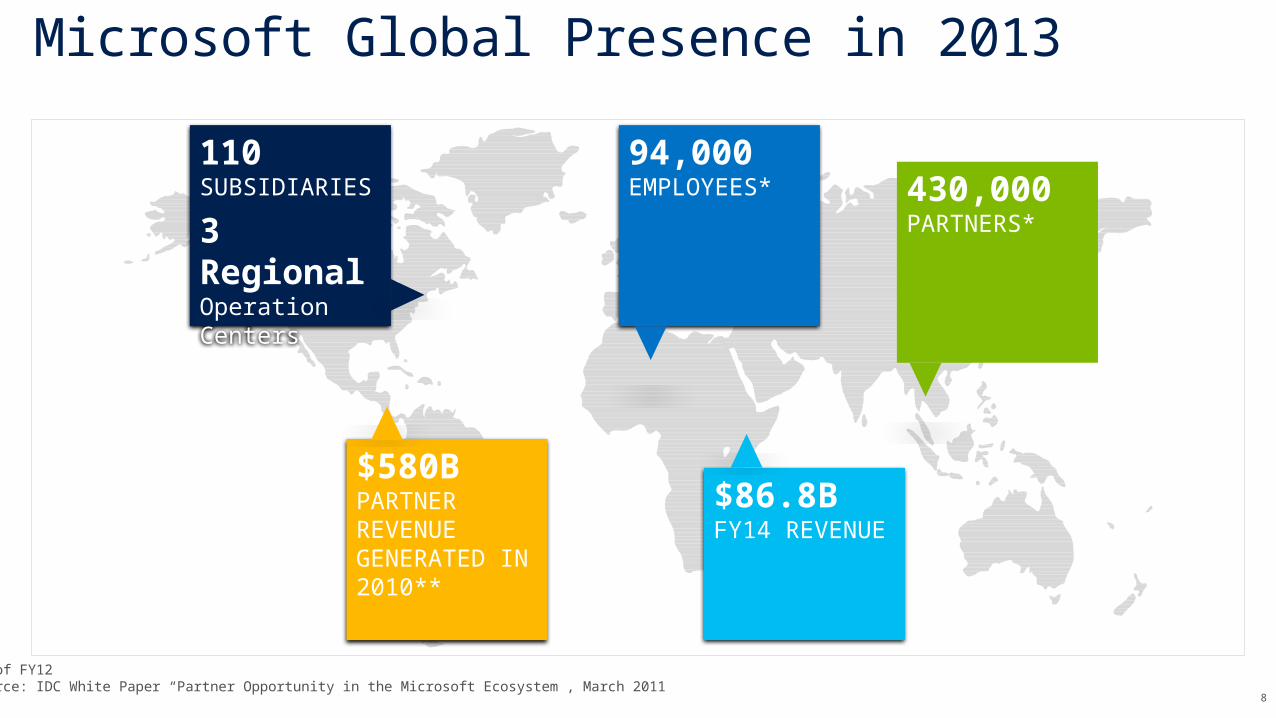

Microsoft Global Presence in 2013

*End of FY12**Source: IDC White Paper “Partner Opportunity in the Microsoft Ecosystem”, March 2011

110 SUBSIDIARIES

3 Regional Operation Centers

94,000EMPLOYEES* 430,000

PARTNERS*

$86.8B FY14 REVENUE

$580BPARTNER REVENUE GENERATED IN 2010**

9

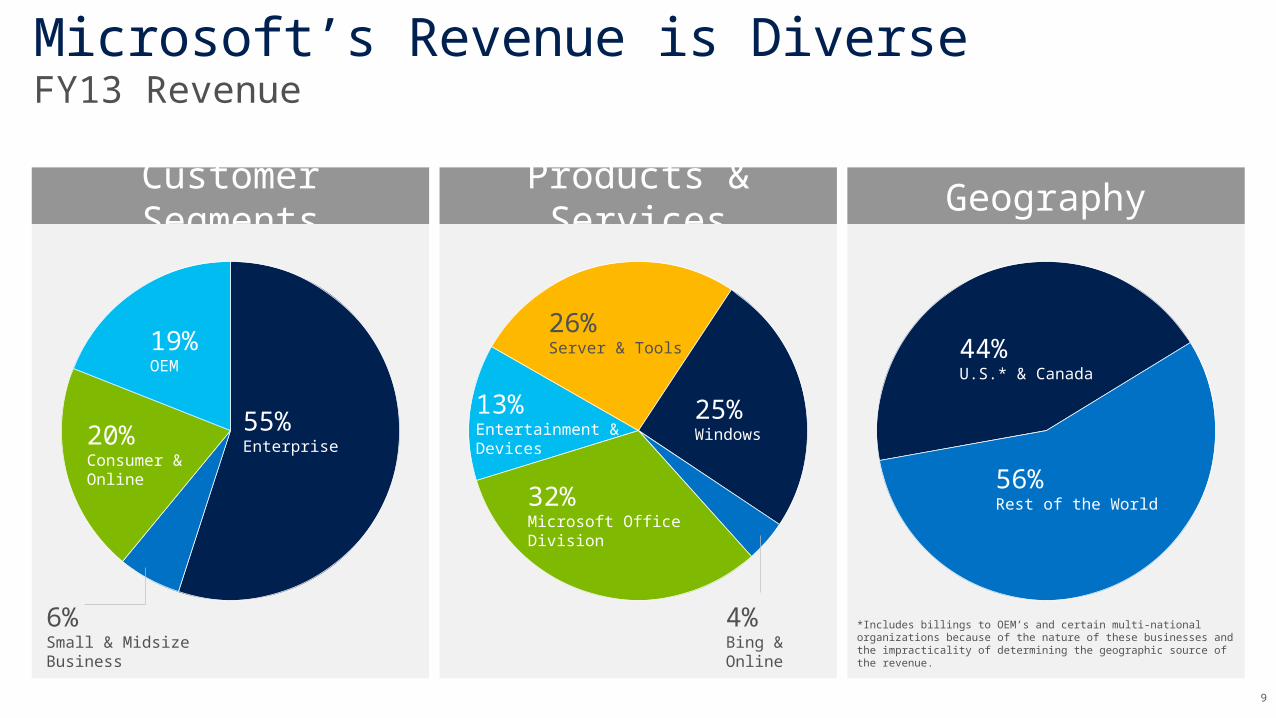

Microsoft’s Revenue is DiverseFY13 Revenue

Customer Segments

Products & Services Geography

*Includes billings to OEM’s and certain multi-national organizations because of the nature of these businesses and the impracticality of determining the geographic source of the revenue.

55%Enterprise

19%OEM

20%Consumer &Online

6%Small & Midsize Business

25%Windows

26%Server & Tools

13%Entertainment &Devices

32%Microsoft OfficeDivision

4%Bing & Online

44%U.S.* & Canada

56%Rest of the World

10

What We Do (from Software to Devices and Services) Windows

SearchPhone

Office

XboxSkype

Dynamics

Cloud

Server

11

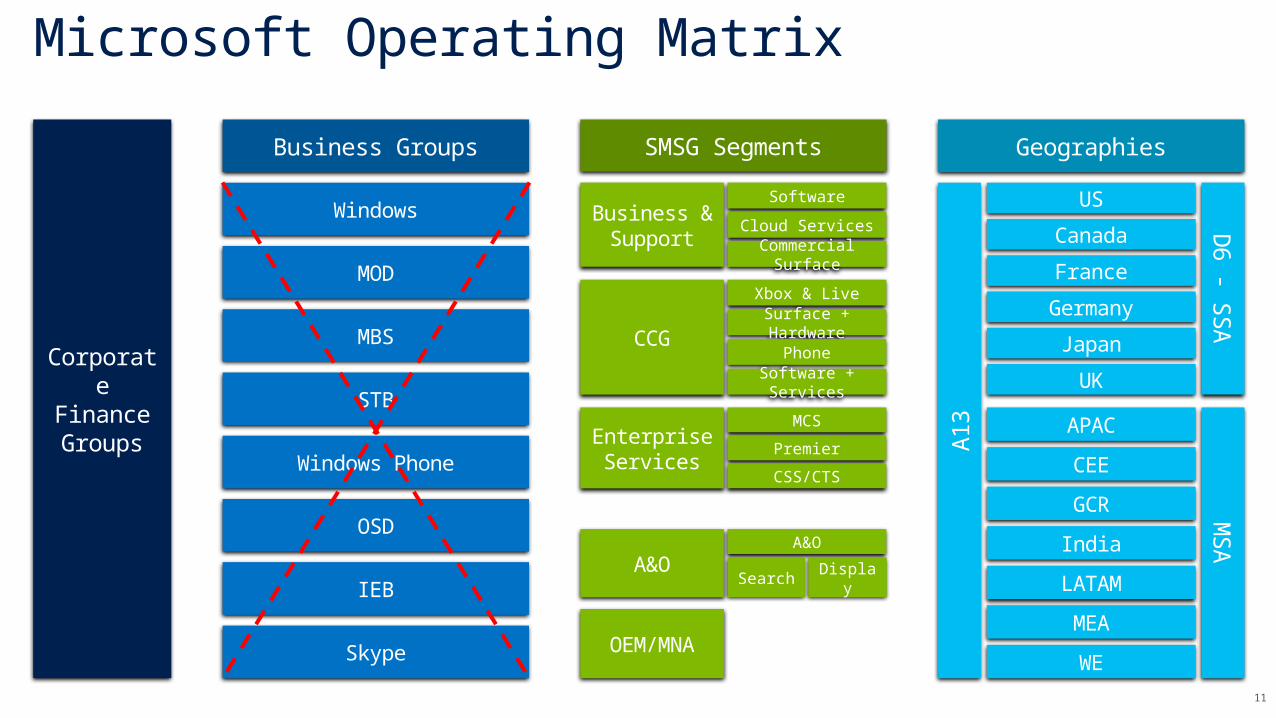

Corporate Finance Groups

Microsoft Operating Matrix

Business Groups

Windows

IEB

MBS

Windows Phone

MOD

OSD

STB

Skype

Enterprise Services

Business & Support

CCG

A&O

SMSG Segments

A&O

Search Display

OEM/MNA

Software

Cloud ServicesCommercial

Surface

Xbox & LiveSurface + Hardware

PhoneSoftware +

Services

MCS

Premier

CSS/CTS

US

Germany

Canada

Japan

France

UK

Geographies

D6 - S

SA

A13

MSA

APAC

India

CEE

LATAM

GCR

MEA

WE

12

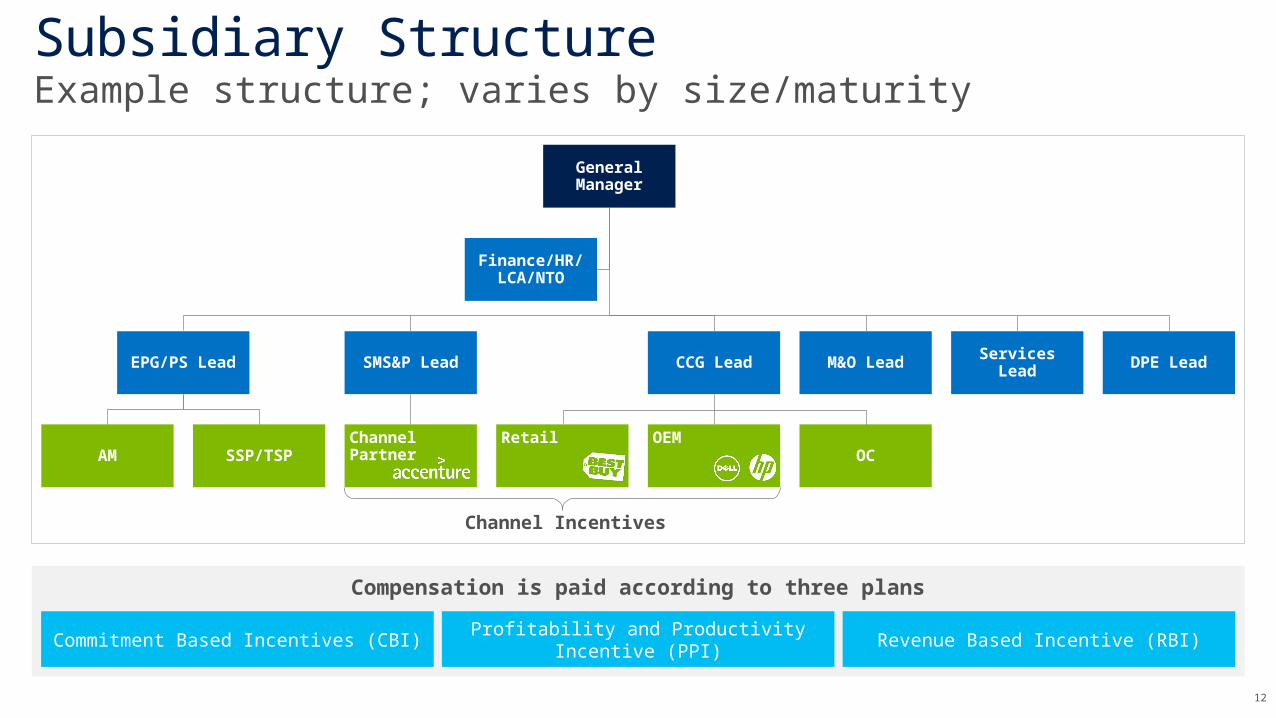

Subsidiary StructureExample structure; varies by size/maturity

Compensation is paid according to three plans

Channel Incentives

General Manager

EPG/PS Lead

AM SSP/TSP

SMS&P Lead

Channel Partner

CCG Lead

Retail OEMOC

M&O Lead Services Lead DPE Lead

Finance/HR/ LCA/NTO

Commitment Based Incentives (CBI)Profitability and Productivity Incentive

(PPI)Revenue Based Incentive (RBI)

13

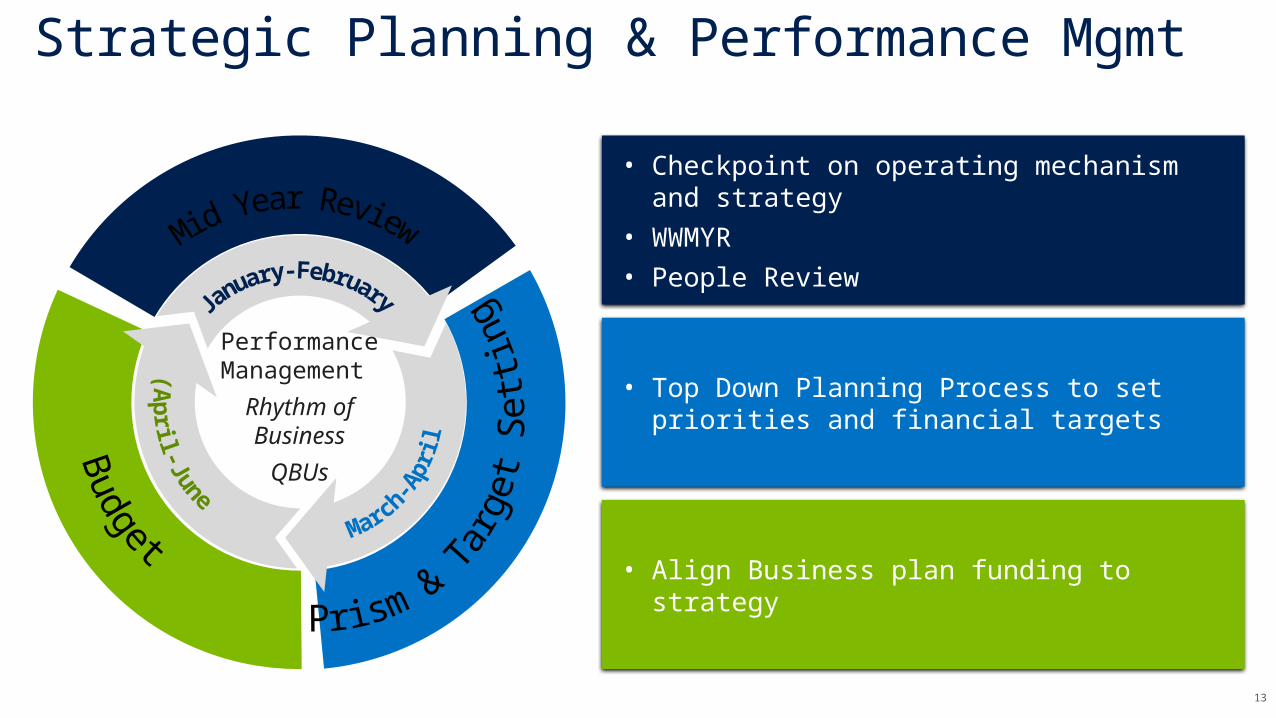

Strategic Planning & Performance Mgmt

Performance Management

Rhythm ofBusiness

QBUs

• Checkpoint on operating mechanism and strategy

• WWMYR• People Review

• Align Business plan funding to strategy

• Top Down Planning Process to set priorities and financial targets

14

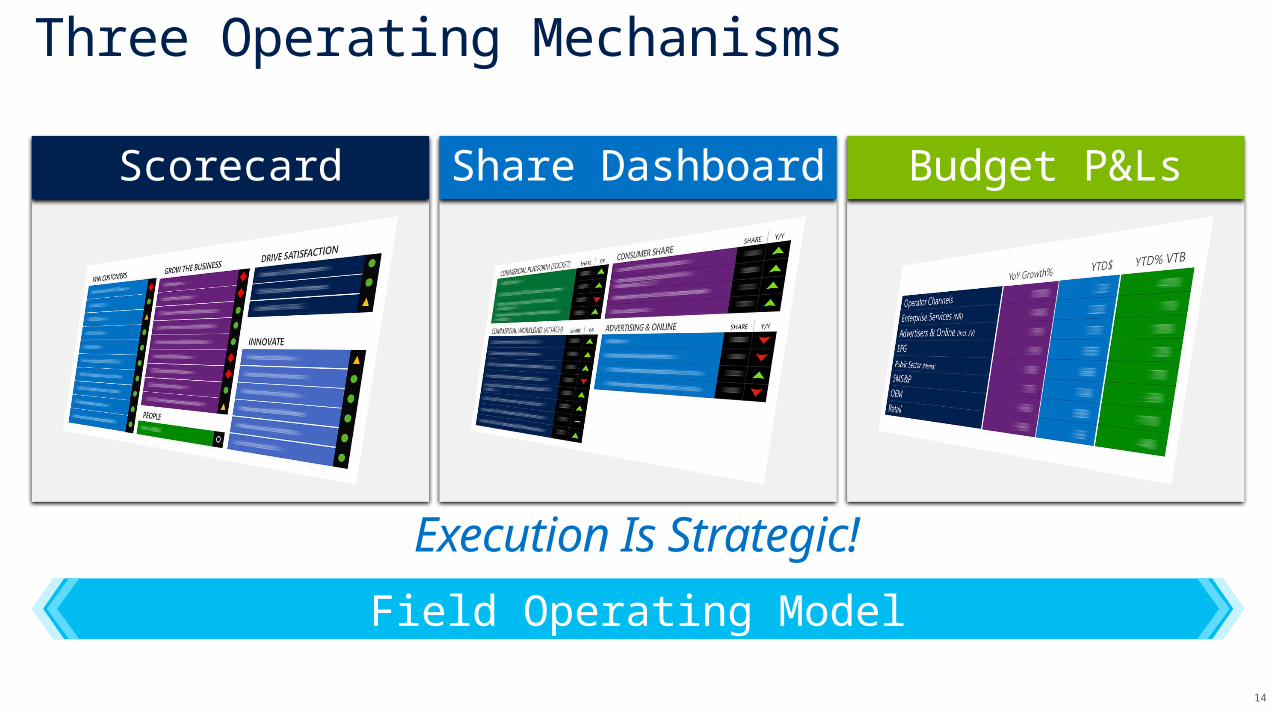

Execution Is Strategic!

Three Operating Mechanisms

Budget P&LsShare DashboardScorecard

Field Operating Model

15

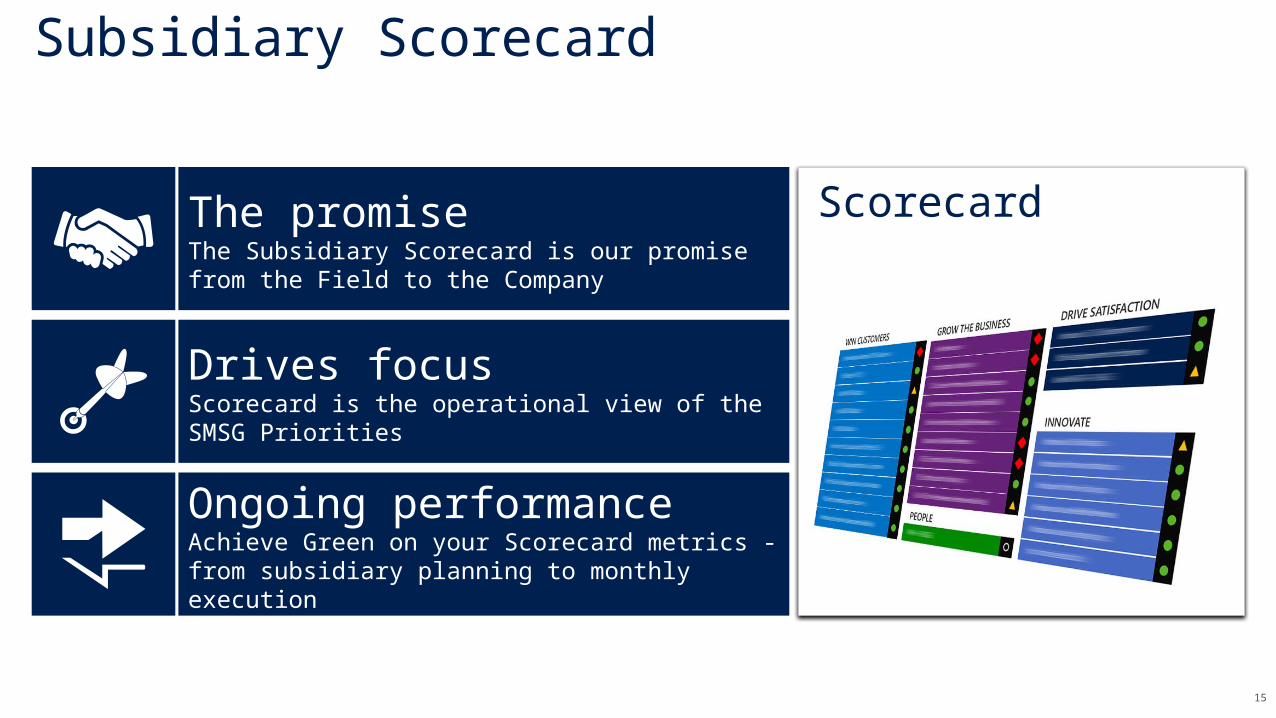

Scorecard

Subsidiary Scorecard

Drives focusScorecard is the operational view of the SMSG Priorities

Ongoing performanceAchieve Green on your Scorecard metrics - from subsidiary planning to monthly execution

The promiseThe Subsidiary Scorecard is our promise from the Field to the Company

16

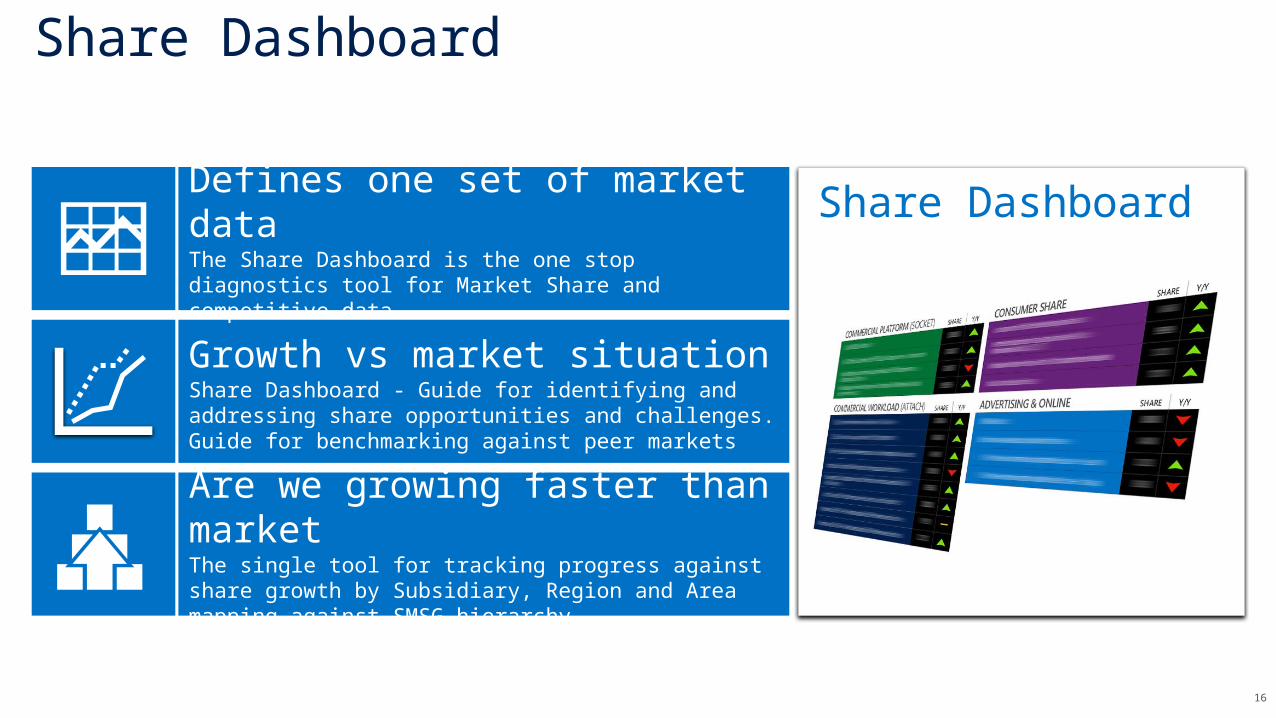

Share Dashboard

Share Dashboard

Growth vs market situationShare Dashboard - Guide for identifying and addressing share opportunities and challenges. Guide for benchmarking against peer markets

Are we growing faster than marketThe single tool for tracking progress against share growth by Subsidiary, Region and Area mapping against SMSG hierarchy

Defines one set of market dataThe Share Dashboard is the one stop diagnostics tool for Market Share and competitive data

17

Budget & P&L

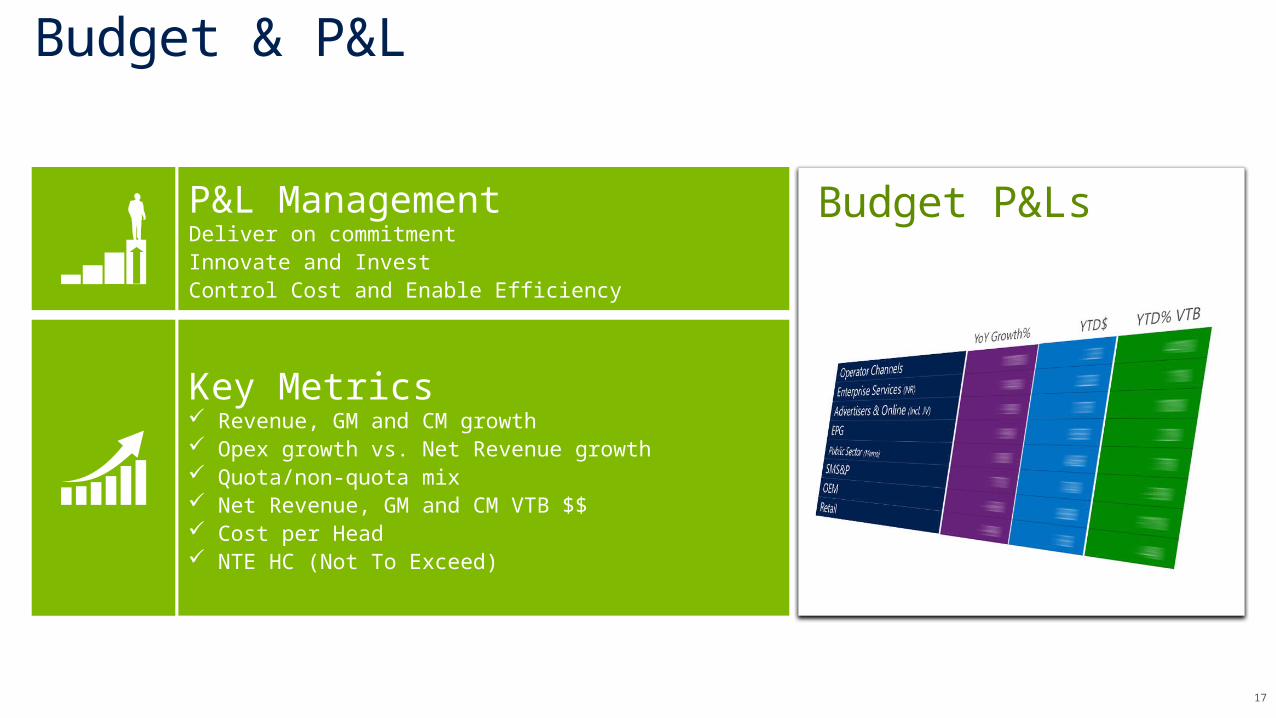

Budget P&Ls

Key Metrics Revenue, GM and CM growth Opex growth vs. Net Revenue growth Quota/non-quota mix Net Revenue, GM and CM VTB $$ Cost per Head NTE HC (Not To Exceed)

P&L ManagementDeliver on commitmentInnovate and InvestControl Cost and Enable Efficiency

18

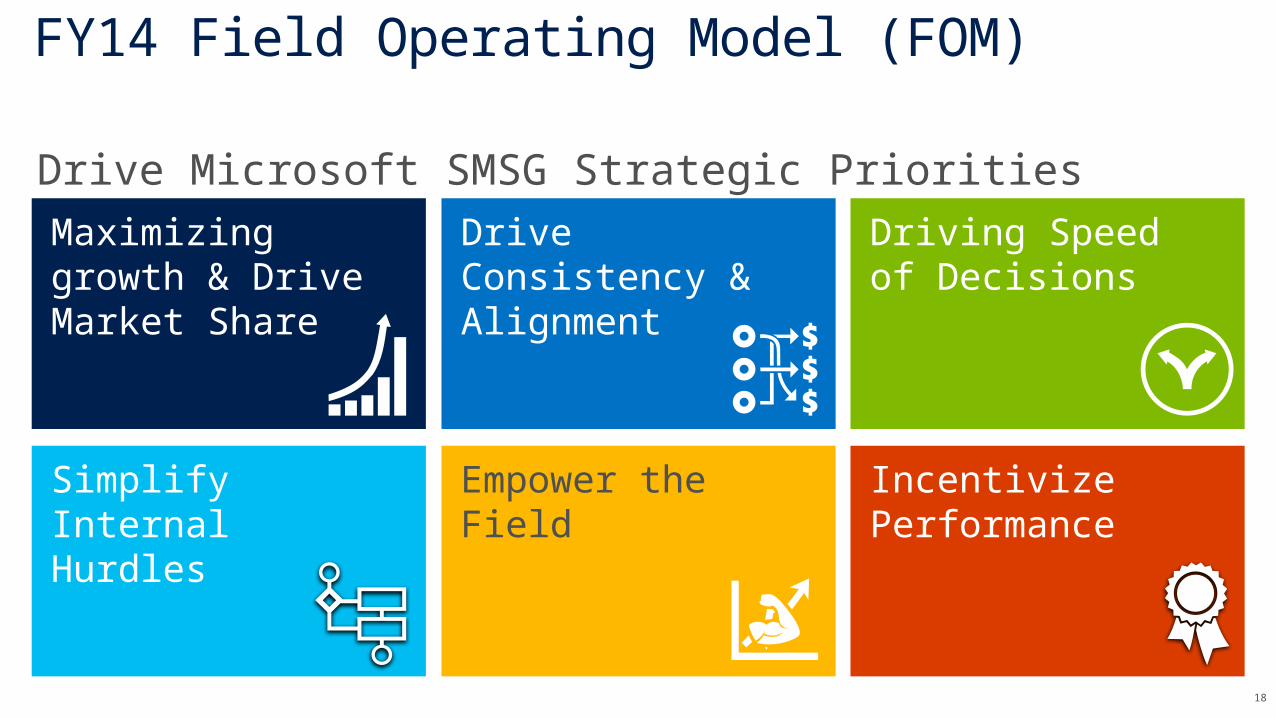

FY14 Field Operating Model (FOM)

Maximizing growth & Drive Market Share

Drive Consistency & Alignment

Driving Speed of Decisions

Simplify Internal Hurdles

Empower the Field Incentivize Performance

Drive Microsoft SMSG Strategic Priorities

19

Geo expansion

SEA New Markets

WECA New Markets

LATAM New Markets

CEE New Markets – 15 countries

(Albania, Armenia, Azerbaijan, Belarus, Bosnia&Herzegovina, Georgia, Kosovo, Kirgizstan, Macedonia, Moldova, Mongolia, Montenegro, Tajikistan, Turkmenistan,

Uzbekistan)

Start-up – Incubation – Clustering - Maturing

Mindset

Using insight toInfluence

Partnering for Impact

Delivering business insight

Access to ONE version of the

truth

Business Impact

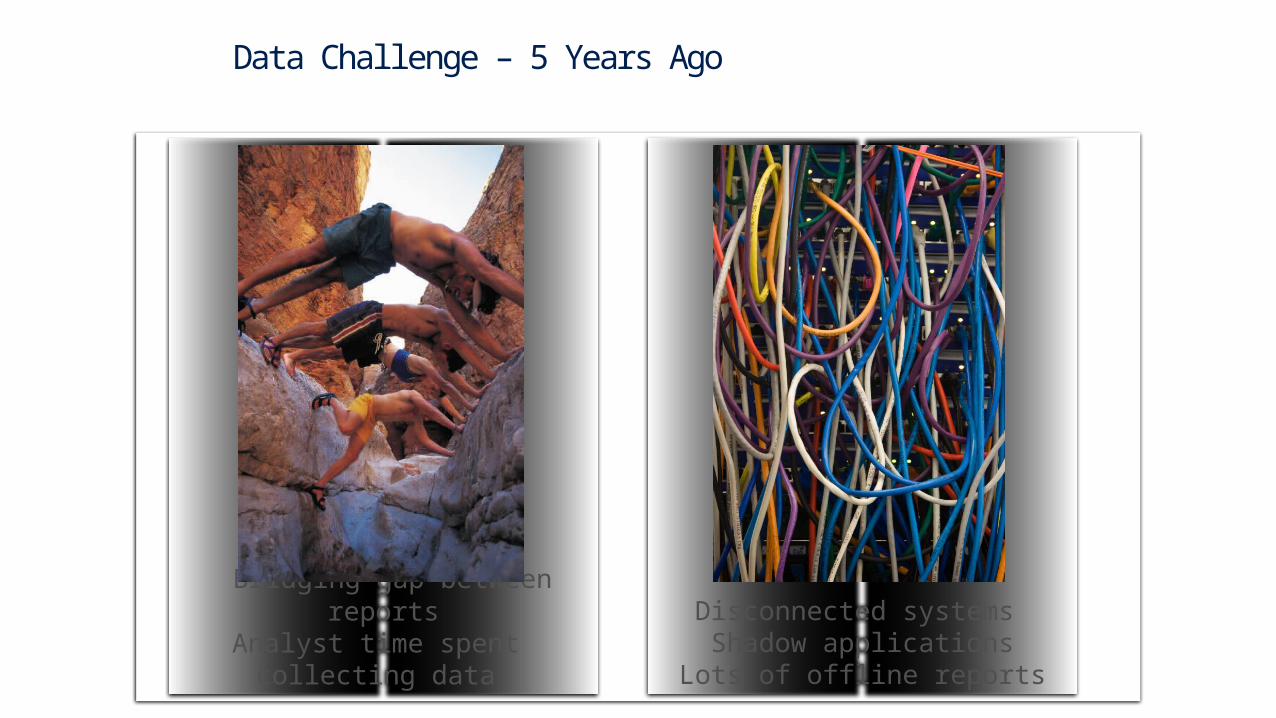

Bridging gap between reportsAnalyst time spent

collecting data

Disconnected systems Shadow applicationsLots of offline reports

Data Challenge – 5 Years Ago

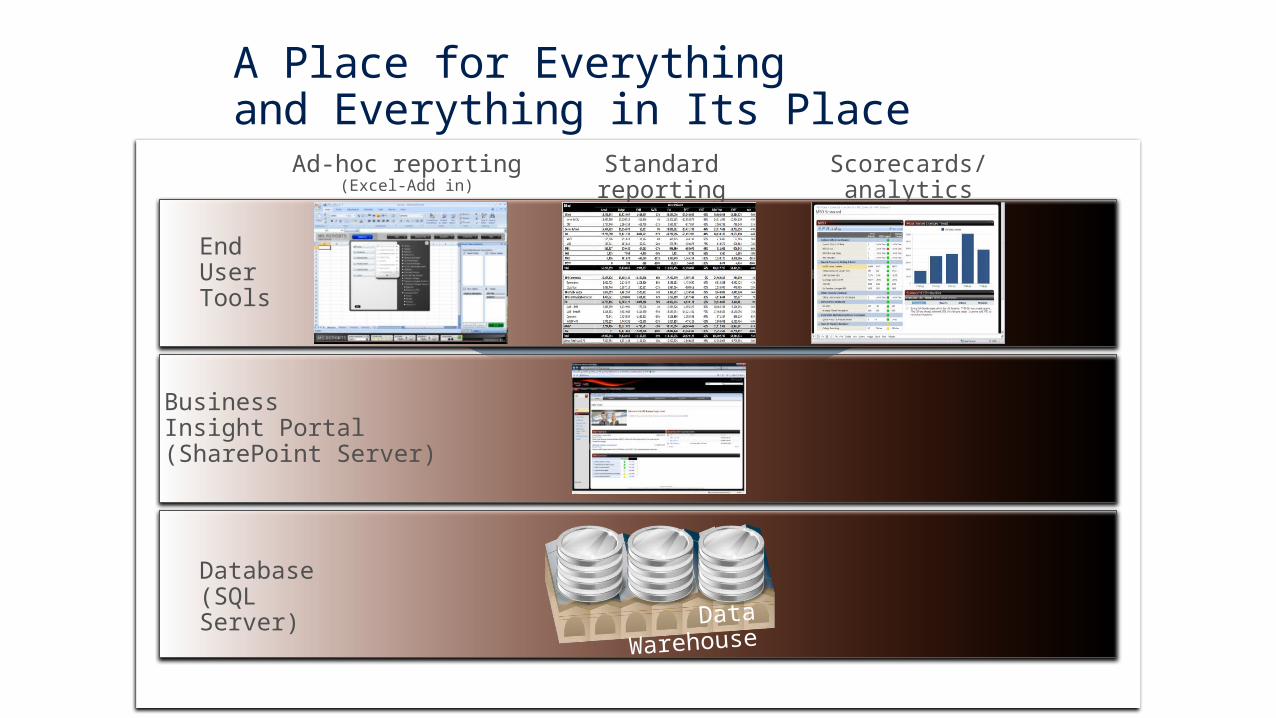

A Place for Everything and Everything in Its Place

Ad-hoc reporting(Excel-Add in)

Standard reporting

(Excel and SRS)

Scorecards/analytics

(Performance Point)

Business Insight Portal(SharePoint Server)

Database (SQL Server)

End User Tools

Data

Warehouse

Data OverloadData

Insight

Influence

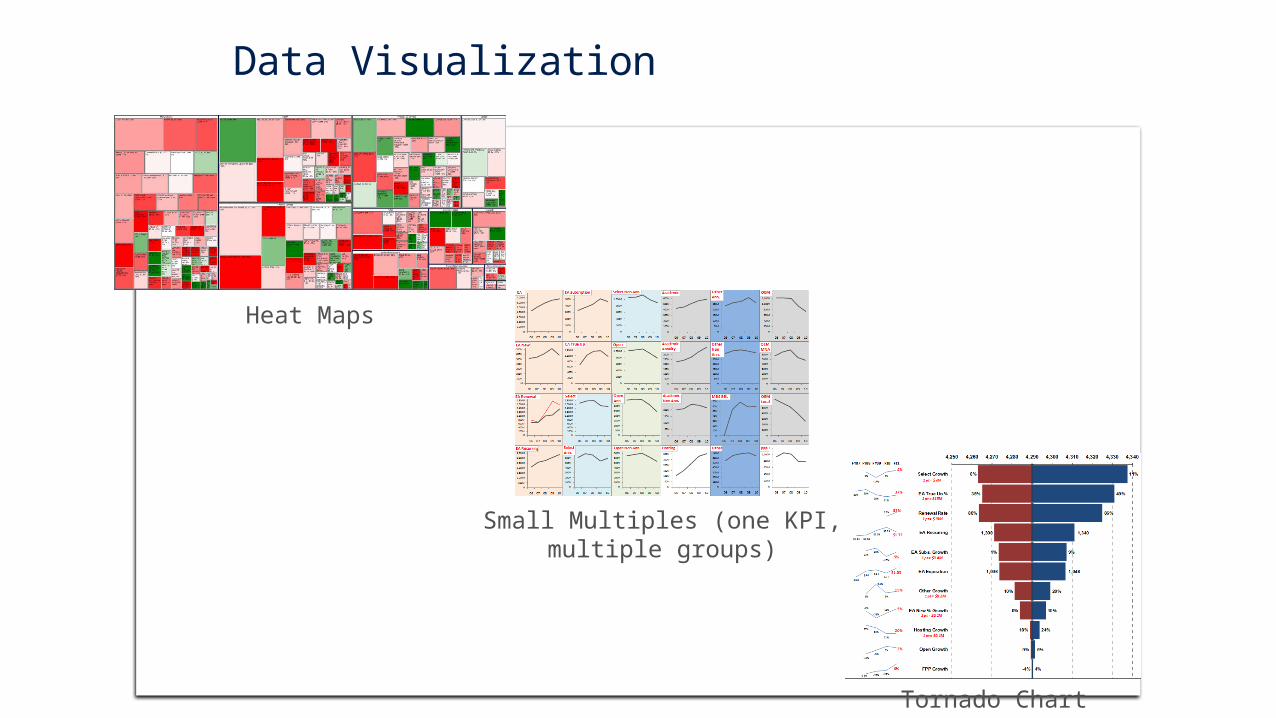

Data Visualization

Heat Maps

Small Multiples (one KPI, multiple groups)

Tornado Chart

Hard to Stay Connected

Sr. Leadership Scorecard

Aligning Goals & Shared Accountabilities

Organization Scorecard

Subsidiary Scorecard

27

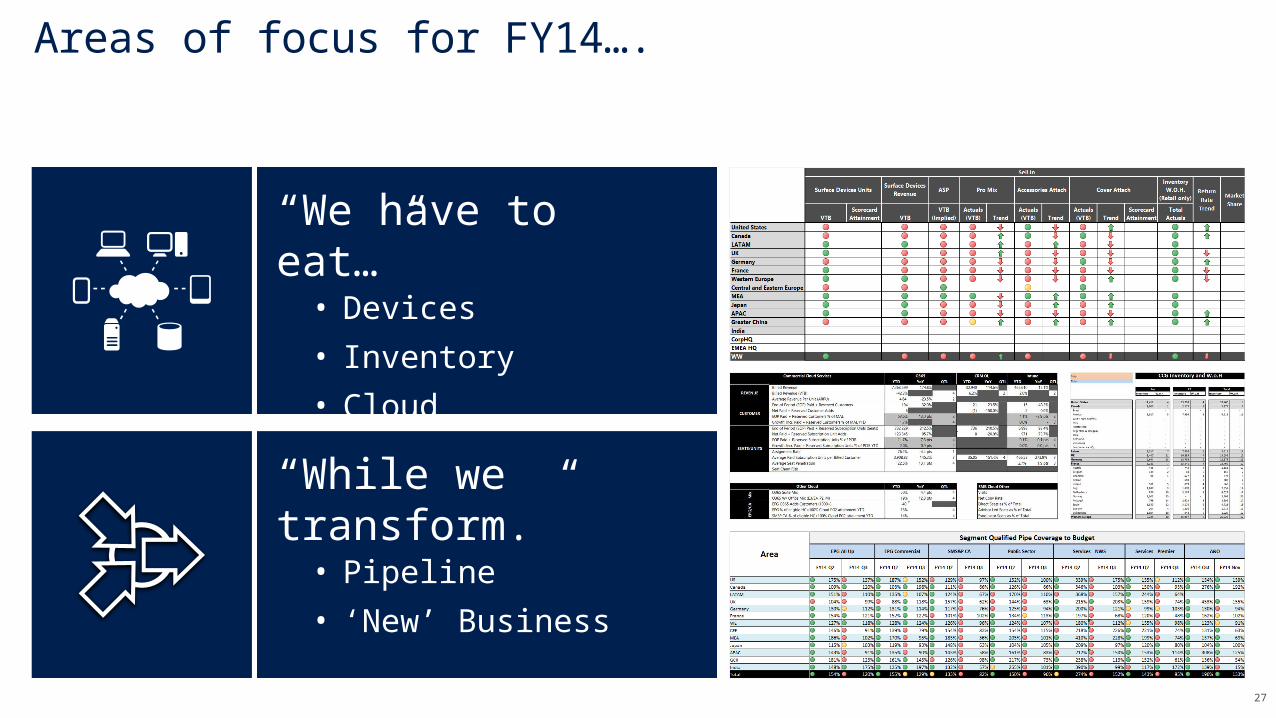

Areas of focus for FY14….

“While we transform.”• Pipeline

• ‘New’ Business

“We have to eat…”• Devices

• Inventory

• Cloud

28

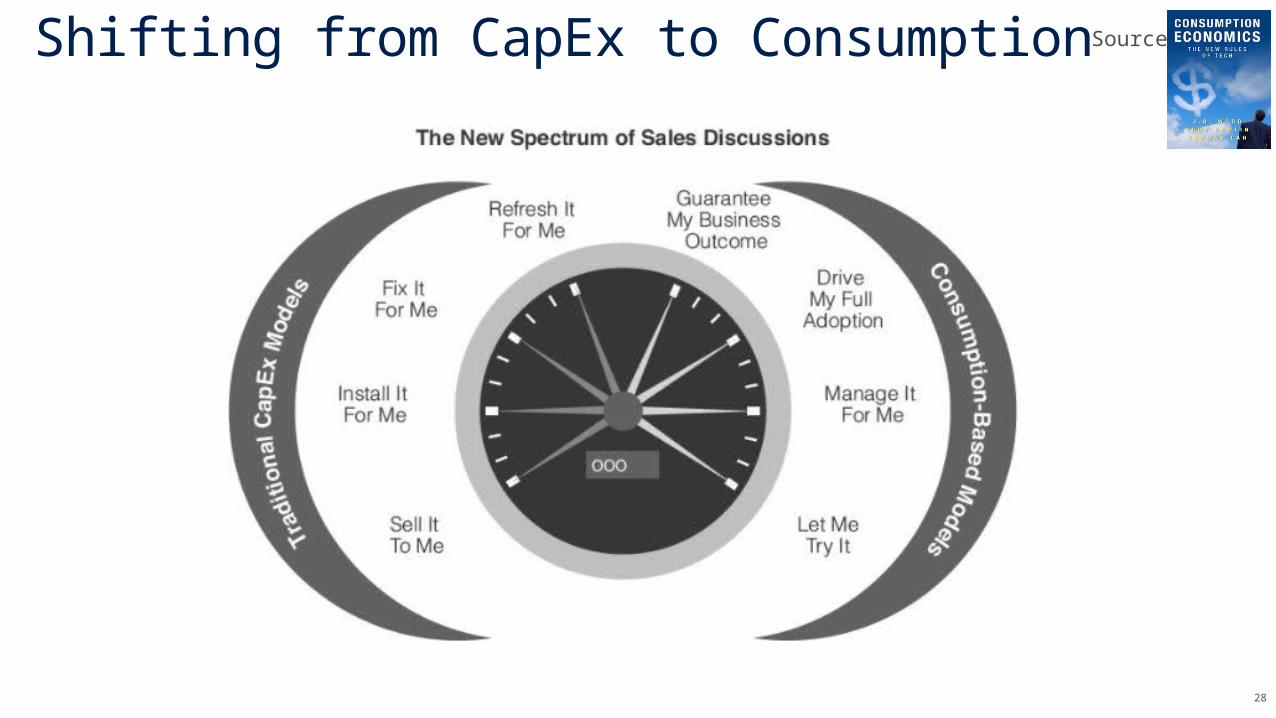

Shifting from CapEx to Consumption Source:

29

“You are going to be making a very significant bet on each customer you take on. You will have an expensive sales cycle. You will have a big services investment to get that customer and its end users ready…you might have little or no revenue from any of these steps. You are betting on the future.”--J. B. Wood “Consumption Economics: The New Rules of Tech”