beyond the wallet wars - amadeus · beyond the wallet wars ... superman: dawn of justice, which...

TRANSCRIPT

Beyond thewallet warsTowards a holistic mobilepayments strategy

Amadeus Travel Payments

Sale

A01

A01

Introduction: Mobile vs Payments

The Wallet Wars

Why are tech giants suddenly focussed on payments?

How will the wallet wars be won?

Mobile Payments and the airline industry

Is there more to life than wallets?

A suggested framework for mobile commerce

A proposed framework for building a mobile payment strategy

Tying it all together Amadeus and mobile payments

03

04

07

08

10

11

13

15

16

16

Index

02

Introduction: Mobile vs PaymentsHollywood has a tried-and-tested formula for guaranteeing hype: Take two well-known super-heroes and combine in one film. You’ve heard of Batman, right? And Superman? Well now you can see them together in Batman v Superman: Dawn of Justice, which broke box office records on its North American release weekend in March this year.

In the only-slightly-less hyped world of technology innovation, 2016 is the year when two technology super-trends duke it out. The impact of mobile devices on society has been dramatic: over 2.5 billion people own smart phones around the world; the iPhone led Apple to become the most profitable and valuable company in the world; people report anxiety when separated from their phones1. Payments is also a hot technology: earlier this year Ant Financial, the company behind Alipay, completed the largest funding round by a private technology company ever, raising 4.5billion dollars for an overall valuation of 60billion.

Combining these two trends, Mobile Payments, should be a hype-fest. But the story of Batman v Superman carries a warning; a�er a record-breaking opening weekend, poor reviews led the film to slide down the list of box office hits.

In this paper we look at the hype and the fundamentals of Mobile Payments and try to offer some guidance to help airlines build or consolidate a mobile payments strategy that stands the test of time.

1 http://www.cbsnews.com/news/iphone-separation-anxiety-heart-beats-faster-mind-works-slower/

03

2.5BPeople own smartphones around the world in 2016

Dollars raised Alipay for an overall valuation of

60 billion The Wallet WarsIn October 2014, Apple launched iOS 8.1. Along with the normal collection of bug fixes and minor feature upgrades, the upgrade to Apple’s mobile operat-ing system included Apple Pay. It wasn’t the first mobile wallet – that was PayPal– but it has renewed interest in mobile wallets.

Today Apple, Google and Samsung, the first, fourth and nineteenth2 most valuable companies in the world, are slugging it out to win the global wallet wars. Notably, none of them are banks, payment companies or have any history in the arena. As well as pretenders to the global throne, countless local mobile wallets have popped into existence – the largest of them, Alipay or Tencent for example, are very large indeed. By March2016, WeChat Pay had 697 million active users3.

Moreover, the rate of innovation in this space is so fast that, before any of the global tech giants have managed to establish a position worth defending, they are already having to fight off the first wave of disruptive challengers. Facebook, for example, is backing into mobile payments from their very successful chat application; Amazon is backing into the space from its posi-tion in online retail.

4.5B$

2 http://www.statista.com/statistics/263264/top-companies-in-the-world-by-market-value/3 https://techcrunch.com/2016/03/17/messaging-app-wechat-is-becoming-a-mobile-payment-giant-in-china/

04

US, UK, Canada, Australia, China, Singapore, Switzer-land, France, Hong Kong

Expected for 2016/17:Spain, Turkey, India, Belgium, Germany, Italy

• 1M new users p/ week- Clients that register a card in their app

• 5x growth

US, UK, Singapore, Australia (soon)

Apple Pay Android Pay

South Korea, US, China, Spain, Singapore, Australia, Puerto Rico, Brazil

Expected for 2016:UK, Malaysia, Canada, Russia, Hong Kong

Worldwide • 184 million of accounts (27/04/16)

• 4.9 bn payments processed in 2015

Samsung Pay Paypal

China • 450 million active users• 5.2 mn users abroad

Australia • Daily average 1.5 mn trx, valued $1.3bn.

• Over 290bn worth of pymnts in ‘15

Alipay BPay

n/a n/a India • 35mn active users (wallet)

• 1mn/day (with Snapdeal)

Smart Pay BBVA Freecharge

(bought by Snapdeal)

Country available Total transactions(if available)

Country available Total transactions(if available)

05

India • 2.5mn orders/day

• 120mn registered users

https://paytm.com/about

US, UK, Spain, France, Italy, Japan, Germany, India

n/aIndia • 30+mn users

• 25+ payments/sec

US (just rolled out to 4,600 stores in the US)

PayTM

Amazon PaymentsMobikwik

Walmart Pay

• United States, Canada, United Kingdom, Spain, Sweden, Singapore, Israel, Italy, Australia and now South Africa.

• Recently-announced agreement with EcoBank will roll MasterPass out to 33 African countries.

• 2417 merchants enrolled

• Will soon allow Master-Card card holders that use Android Pay, Samsung Pay, or Microso� Wallet to use the same tokenized credentials and device authentication methods to complete online transac-tions at any merchant site that accepts MasterPass

MasterPass

Argentina, Australia, Brazil, Canada, Chile, China, Colombia, Hong Kong, Malaysia, Mexico, New Zealand, Peru, Singapore, South Africa, UAE

• 250,000 enrolled merchants

• 12 million registered users

• 675 financial institutions All data supplied by Visa

Visa Checkout

Country available Total transactions(if available)

Country available Total transactions(if available)

06

Why are tech giants suddenly focussed on payments?

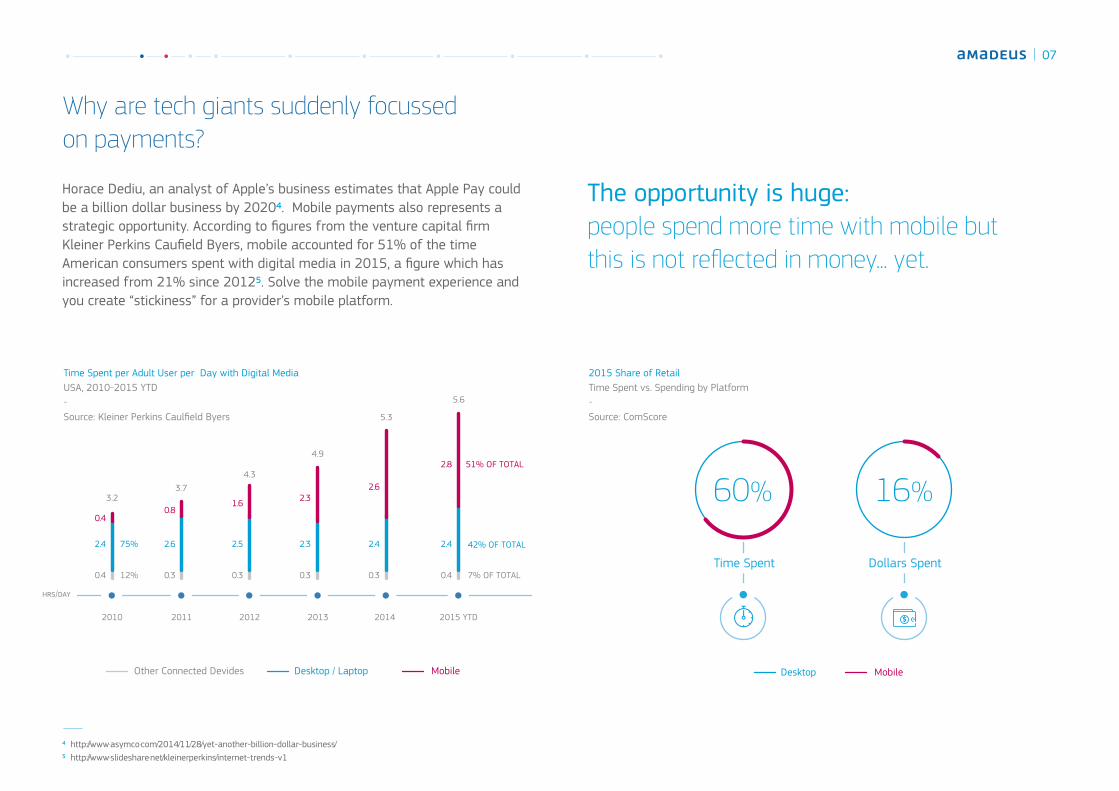

Horace Dediu, an analyst of Apple’s business estimates that Apple Pay could be a billion dollar business by 20204. Mobile payments also represents a strategic opportunity. According to figures from the venture capital firm Kleiner Perkins Caufield Byers, mobile accounted for 51% of the time American consumers spent with digital media in 2015, a figure which has increased from 21% since 20125. Solve the mobile payment experience and you create “stickiness” for a provider’s mobile platform.

The opportunity is huge: people spend more time with mobile but this is not reflected in money... yet.

2015 Share of Retail Time Spent vs. Spending by Platform-Source: ComScore

Time Spent per Adult User per Day with Digital Media USA, 2010-2015 YTD-Source: Kleiner Perkins Caulfield Byers

2010 2011 2012 2013 2014 2015 YTD

/

Other Connected Devides Desktop / Laptop Mobile Desktop Mobile

42% OF TOTAL

7% OF TOTAL

3.74.3

75%

12%

51% OF TOTAL

60%

Time Spent

16%

Dollars Spent

$

3.2

0.4 0.3 0.3 0.3 0.3 0.4

2.4 2.6 2.5 2.3 2.4 2.4

0.40.8

1.6 2.32.6

2.84.9

5.3

5.6

4 http:⁄⁄www.asymco.com⁄2014⁄11⁄28⁄yet-another-billion-dollar-business⁄ 5 http:⁄⁄www.slideshare.net⁄kleinerperkins⁄internet-trends-v1

07

The opportunity lies in the fact that mobile spend still lags behind mobile attention. According to comScore, mobile accounts for 60% of the time US consumers spent with retail sites but only 16% of the money spent. Tech giants are betting on mobile wallets to close this gap. The opportunity lies in harvesting transaction revenues, creating a defensive moat around their mobile businesses and, for some, monetising payment-associated data. Alex Rampell, a partner at venture capital firm Andreessen Horowitz, predicts,

For the technology giants competing in this space, winning the wallet wars will create an important moat to defend their position in the smartphone market.

How will the wallet wars be won? Mobile wallet developers are pursuing three main strategies to become ‘top of wallet’:

1. Reducing payment friction

Entering a sixteen digit credit card number, name expiry date and CVV code is far from a frictionless experience. Even less so on a mobile phone. Improving this experience with card details saved on file and alternative methods of authentication, like biometrics, improves the attractiveness of a given wallet as well as increasing the wallet owner’s propensity to use his or her wallet once installed.

“As digital wallets increasingly become the origination point for consumer spending, they will become THE platform for down-stream financial services — creating an op-portunity for start-ups and a problem for established players.” ⁶

Pay withyour finger

6 https:⁄⁄techcrunch.com⁄2016⁄04⁄24⁄why-your-wallet-is-becoming-the-next-platform⁄

08

Suppliers which perfect the mobile payment experience create an opportunity to extend the scope to other channels beyond mobile commerce, thus further growing the usage of the mobile payments applications. For example, banks have already begun to blur the boundaries between channels when they verify your identity when using internet banking by sending a one-time password to your phone. And recently, Apple announced that people shopping on an ecommerce site from their desktop or laptop can pay using the Apple Pay wallet on their iPhone.

2. Increasing wallet utility

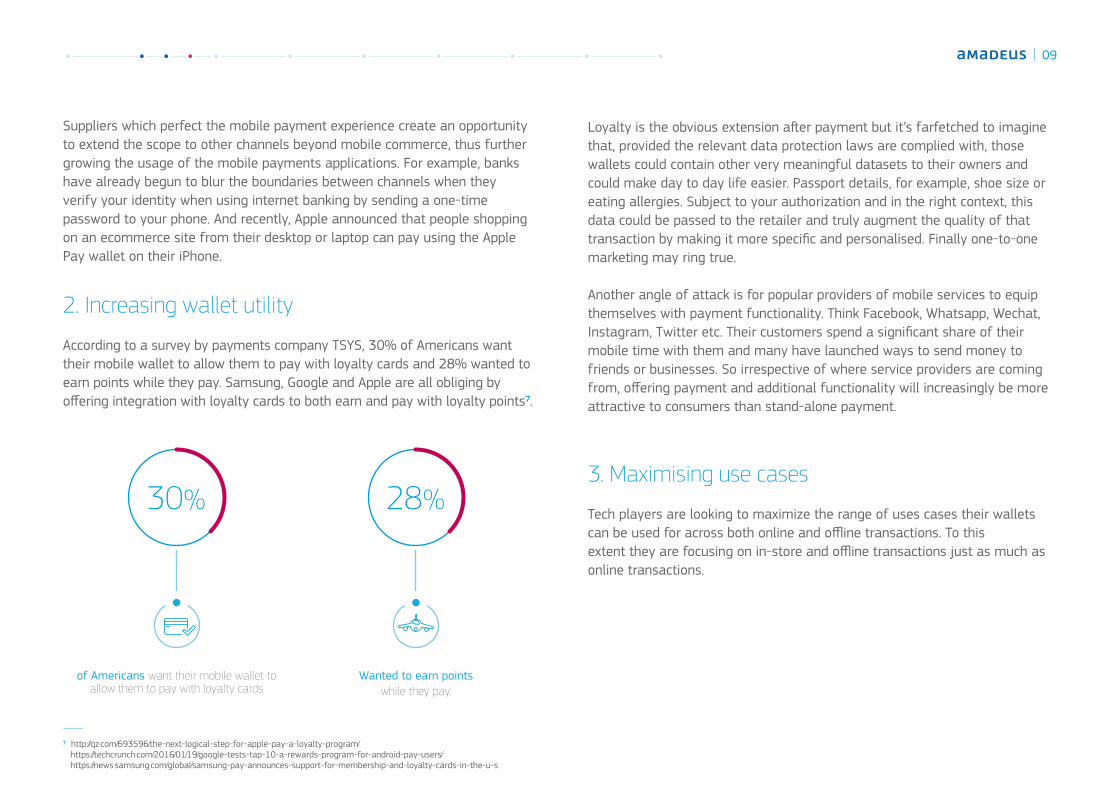

According to a survey by payments company TSYS, 30% of Americans want their mobile wallet to allow them to pay with loyalty cards and 28% wanted to earn points while they pay. Samsung, Google and Apple are all obliging by offering integration with loyalty cards to both earn and pay with loyalty points7.

Loyalty is the obvious extension a�er payment but it’s farfetched to imagine that, provided the relevant data protection laws are complied with, those wallets could contain other very meaningful datasets to their owners and could make day to day life easier. Passport details, for example, shoe size or eating allergies. Subject to your authorization and in the right context, this data could be passed to the retailer and truly augment the quality of that transaction by making it more specific and personalised. Finally one-to-one marketing may ring true.

Another angle of attack is for popular providers of mobile services to equip themselves with payment functionality. Think Facebook, Whatsapp, Wechat, Instagram, Twitter etc. Their customers spend a significant share of their mobile time with them and many have launched ways to send money to friends or businesses. So irrespective of where service providers are coming from, offering payment and additional functionality will increasingly be more attractive to consumers than stand-alone payment.

3. Maximising use cases

Tech players are looking to maximize the range of uses cases their wallets can be used for across both online and offline transactions. To this extent they are focusing on in-store and offline transactions just as much as online transactions.

7 http:⁄⁄qz.com⁄693596⁄the-next-logical-step-for-apple-pay-a-loyalty-program⁄ https:⁄⁄techcrunch.com⁄2016⁄01⁄19⁄google-tests-tap-10-a-rewards-program-for-android-pay-users⁄ https:⁄⁄news.samsung.com⁄global⁄samsung-pay-announces-support-for-membership-and-loyalty-cards-in-the-u-s

of Americans want their mobile wallet to allow them to pay with loyalty cards

Wanted to earn pointswhile they pay.

30% 28%

09

Mobile Payments and the airline industry

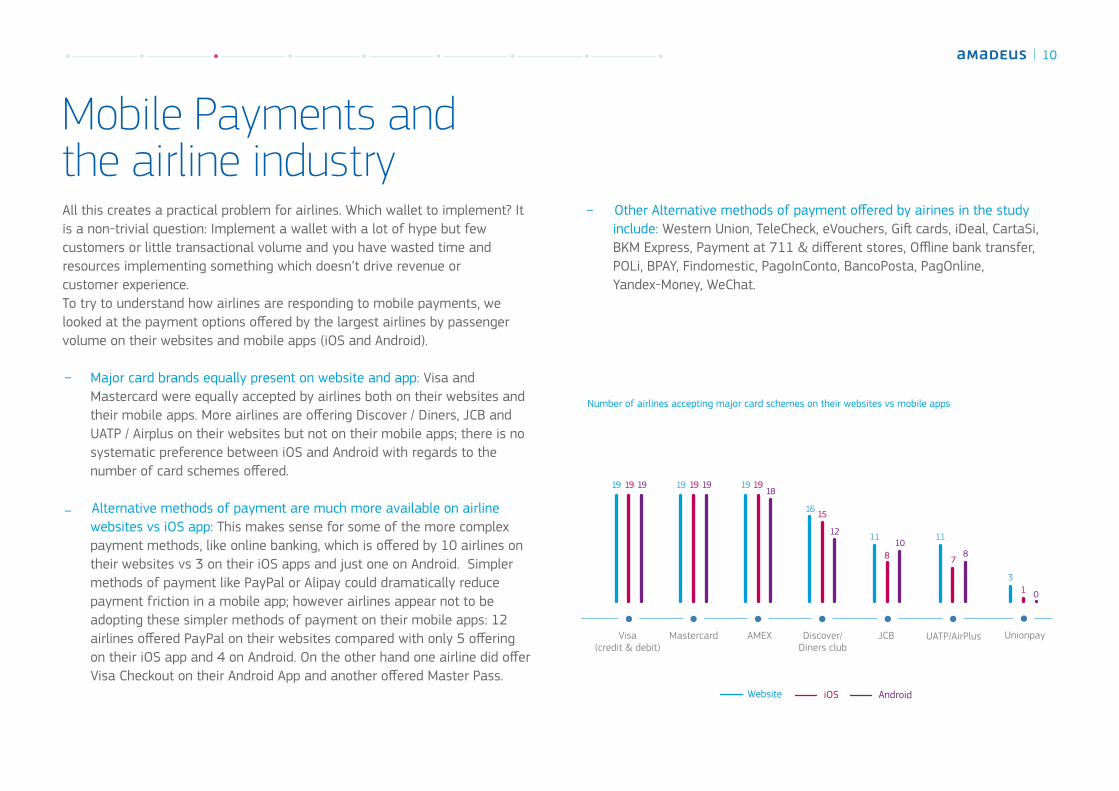

Number of airlines accepting major card schemes on their websites vs mobile apps

Visa(credit & debit)

Mastercard AMEX Discover/Diners club

UATP/AirPlusJCB Unionpay

Website iOS Android

Other Alternative methods of payment offered by airines in the study include: Western Union, TeleCheck, eVouchers, Gi� cards, iDeal, CartaSi, BKM Express, Payment at 711 & different stores, Offline bank transfer, POLi, BPAY, Findomestic, PagoInConto, BancoPosta, PagOnline, Yandex-Money, WeChat.

All this creates a practical problem for airlines. Which wallet to implement? It is a non-trivial question: Implement a wallet with a lot of hype but few customers or little transactional volume and you have wasted time and resources implementing something which doesn’t drive revenue orcustomer experience. To try to understand how airlines are responding to mobile payments, we looked at the payment options offered by the largest airlines by passenger volume on their websites and mobile apps (iOS and Android).

Major card brands equally present on website and app: Visa and Mastercard were equally accepted by airlines both on their websites and their mobile apps. More airlines are offering Discover / Diners, JCB and UATP / Airplus on their websites but not on their mobile apps; there is no systematic preference between iOS and Android with regards to the number of card schemes offered.

Alternative methods of payment are much more available on airline websites vs iOS app: This makes sense for some of the more complex payment methods, like online banking, which is offered by 10 airlines on their websites vs 3 on their iOS apps and just one on Android. Simpler methods of payment like PayPal or Alipay could dramatically reduce payment friction in a mobile app; however airlines appear not to be adopting these simpler methods of payment on their mobile apps: 12 airlines offered PayPal on their websites compared with only 5 offering on their iOS app and 4 on Android. On the other hand one airline did offer Visa Checkout on their Android App and another offered Master Pass.

–

–

–

19 19 19 19 19 19

11

810

11

78

16 15

12

19 1918

31 0

10

Is there more to life than wallets?Important as it is, it may be that the focus on which mobile wallet to implement online is distracting airlines from building a holistic mobile payments strategy. Far more than a new distribution channel, mobile is driving significant changes in behaviour and the way that consumers interact with businesses. Here are just a few examples.

Alternative Methods of Payment offered on airline websites vs mobile apps

The smaller screens and the fact that people use mobile devices while on-the-go means that convenience drives significant competitive advantage on mobile. The success of Uber, which stores cards on file to reduce the payment moment almost to zero, and Starbucks, whose mobile payment app can be used to speed through queues can partly be attributed to understanding the importance of convenience on mobile.

To emulate the success of Uber, airlines should make the payment step as seamless as possible on their mobile apps by implementing mobile-optimised payment methods and offering their customers the option to securely store their card details on file. The Starbucks example suggests launching the possibility to pay for excess baggage in the airport on a mobile app instead of queuing up at the sales counter.

Convenience is mandatoryPaypal

12

5

4

Sofort

0

3

1

Cash at offices

0

3

0

Online Banking

1

10

3

Website iOS Android

Alipay

4

2

0

11

The rise of messaging apps combined with advances in artificial technology have led to conversational commerce, where a transaction takes place in a messaging app and is managed on the merchant’s side by commerce “bots” using artificial intelligence to interpret customers’ messages and provide responses.In the travel space, KLM launched flight confirmation by chat, in Facebook’s messaging app, in March 2016.

Conversational commerce

Although mobile bookings still lag behind those made on the desktop (in Europe and the US, at least), those bookings that are made on smartphones tend to be last-minute bookings. Booking.com reports that mobile accounts for 30% of all bookings; that figure rises to 50% for travelers who are booking hotel within 48 hours of arrival. The key opportunity for airlines’ mobile apps, therefore, lies in providing a streamlined on-trip servicing and upselling platform to manage, for example, flight changes and ancillary sales – and associated payments.

Instant on demandSome of the biggest winners in mobile commerce have been gaming companies (think King’s “Candy Crush” or Pokémon Go). Companies are looking at how to introduce gaming concepts, like competition, into their e-commerce and marketing activities to drive engagement.

Airlines are getting in on the act mainly as a mechanism for promotions. For example Qantas frequent flyers can earn miles when they exercise thanks to a tie-up with a fitness app8.

Gamification

8 www.airlinetrends.com/tag/gamification/

12

This is the most basic kind of mobile commerce experience and is a direct translation of a desktop e-commerce experience into the mobile environment. Examples include mobile-responsive websites and in-app purchases. We would include conversational commerce in this category.

Use different payment options and cards stored securely on file to increase ancillary sales conversion by reducing payment friction and pushing offers to customers on the move.

Calibrate your website functionality to the constraints of thedevice environment.

A suggested framework for mobile commerceAt Amadeus we think of mobile driving three main categories of commerce behavior. This approach allows you to consider how mobile can create new opportunities to improve the experience in the full range of online and offline touch-points between an airline and its customers.

In this use case, “mobile devices are used to enhance the experience of an ‘offline’ transaction. It includes:

In-store ecommerce: customers in Apple’s offline stores can pay for items using Apple Pay. For Apple this is obviously a way to showcase their wallet but is also a way to avoid queues.

Tap & Pay: use of Near Field Communication (contactless) to smooth the offline payment process. For example travellers on the London Underground can now pay using Apple Pay. In an airport environment, someone could pay for an upgrade at check-in whilst in the queue by tapping their phone on the mobile point of sale of a roaming agent.

Mobile-enabled e-commerce Mobile-enabled offline commerce

–

–

–

–

13

Call-centre m-commerce: globally between 10% and 15% of airline bookings are made in a call centre. Providing a seamless and secure payment experience, and being able to offer alternative methods of payment, is a challenge which smart phones can help to overcome. This is one trend we’ve highlighted further up in this report whereby the payment part of a transaction takes place in a different channel than the one where the transaction was initiated.

Use the specific qualities of mobile devices (highly personal, always connected, always with the traveller, can be geo-located) to reduce friction in ‘offline’ transactions.

Leverage mobile to simplify authentication for face-to-facce transactions with biometric authentication (fingerprint, behavioural, etc).

Offer travellers already at an airport the option to pay for a class upgrade, seat change, fast track boarding anywhere in the airport between check-in and boarding.

The previous two categories apply to use cases where the customer is paying using a mobile device. In this category it is the merchant point of sale which is mobile. Examples include iZettle or Square used primarily by taxi drivers.

Use roaming agents to collect payment transactions in the airport to reduce queues and improve ancillary sales conversion. In other words, use this as an opportunity to proactively reach out to your customers rather than wait for them to come to you.

Mobile-enabled point-of-sale

amadeus.com

–

–

–

–

–

14

24 / 48hA�er Booking

Shop

48 / 24hBefore Departure

Check-In

BookInspire Airport Post-Trip

On-Trip

A I R P O R T

H O T E L

02

03 0907

0806

05

04

01

Shop

A proposed framework for building a mobilepayment strategy

When planning a mobile payments strategy, the second axis to examine is the trip journey. This enables us to tease out the broader opportunities to improve the experience throughout the journey. Key opportunities for mobile to enhance the customer experience throughout the journey.

BookTouch point Between Bookingand Check-in Check-In

Trip stage

Airport In flight On-Trip Post-Trip

Mobile-enablede-commerce

m-commerce category

Mobile enabledpoint of sale

Mobile-enabledoffline commerce

Mobile app

Mobile web

Call centre

Airport agents Queue-busting airport agents

Seamless mobile payment (AMOP, cards on file, mobile wallet)

Improve security, customer experience and additional methods of payment

Seamless NFC payment

Improve security, customer experience and

additional methodsof payment

Increase digital sales in addition to food & dutry free payment by card

Flight changes, customer service, cross-sell (destination services)

Seamless mobile payment for ancillary services (AMOP, cards on file, mobile wallet)

Airport check-in

15

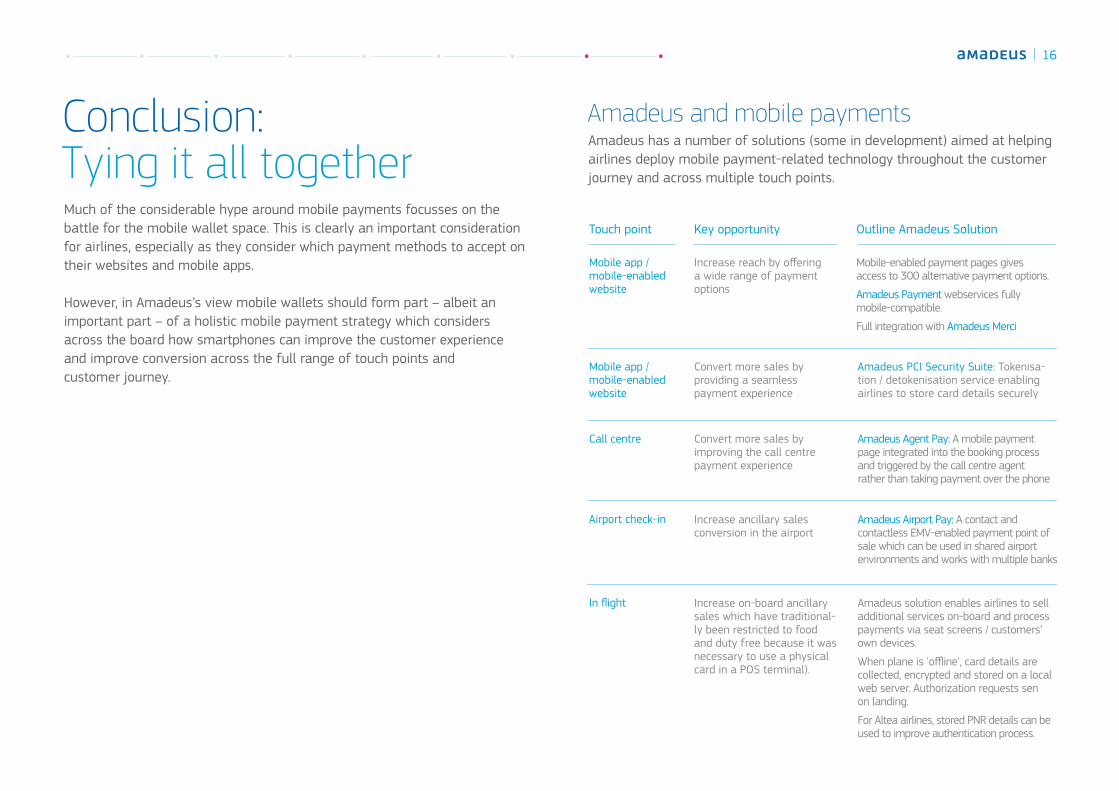

Conclusion: Tying it all togetherMuch of the considerable hype around mobile payments focusses on the battle for the mobile wallet space. This is clearly an important consideration for airlines, especially as they consider which payment methods to accept on their websites and mobile apps.

However, in Amadeus’s view mobile wallets should form part – albeit an important part – of a holistic mobile payment strategy which considers across the board how smartphones can improve the customer experienceand improve conversion across the full range of touch points and customer journey.

Mobile app / mobile-enabledwebsite

Increase reach by offering a wide range of payment options

Mobile-enabled payment pages gives access to 300 alternative payment options.

Amadeus Payment webservices fully mobile-compatible. Full integration with Amadeus Merci

Touch point Key opportunity Outline Amadeus Solution

Mobile app / mobile-enabledwebsite

Convert more sales by providing a seamless payment experience

Amadeus PCI Security Suite: Tokenisa-tion / detokenisation service enabling airlines to store card details securely

Call centre

Airport check-in

Convert more sales by improving the call centre payment experience

Amadeus Agent Pay: A mobile payment page integrated into the booking process and triggered by the call centre agent rather than taking payment over the phone

Increase ancillary sales conversion in the airport

Amadeus Airport Pay: A contact and contactless EMV-enabled payment point of sale which can be used in shared airport environments and works with multiple banks

In flight Increase on-board ancillary sales which have traditional-ly been restricted to food and duty free because it was necessary to use a physical card in a POS terminal).

Amadeus solution enables airlines to sell additional services on-board and process payments via seat screens / customers’ own devices.

When plane is 'offline', card details are collected, encrypted and stored on a local web server. Authorization requests senon landing.

For Altea airlines, stored PNR details can be used to improve authentication process.

Amadeus and mobile paymentsAmadeus has a number of solutions (some in development) aimed at helping airlines deploy mobile payment-related technology throughout the customer journey and across multiple touch points.

16

Thank you!

amadeus.comAmadeusITgroupYou can follow us on:

Website:amadeuspayments.com/travel-payments/

Twitter account:@amadeuspayments

The LinkedIn showcase page: linkedin.com/company/amadeus-travel-payments