bibliography - springer978-3-8349-8926-0/1.pdf · bibliography auckenthaler, c. ... barclays...

TRANSCRIPT

144 BIBLIOGRAPHY

Bibliography

Auckenthaler, C. (1991). Trust Banking – Theorie und Praxis des Anlagegeschäfts. Bern: Paul Haupt.

Bank for International Settlements (BIS, 2005). Amendment to the Capital Accord to incorporate market risks. Retrieved December 14, 2009 from http:// www.bis.org/publ/bcbs119.pdf?noframes=1

Bank for International Settlements (BIS, 2004). International Convergence of Capi-tal Measurement and Capital Standards. Retrieved December 14, 2009 from http://www.bis.org/publ/bcbs107.pdf

Barclays Capital (2010). Global family of indices – February 2010. Retrieved March 12, 2010 from www.themarkets.com (restricted access).

BlueOrchard (2009). Fund prospect Dexia Microcredit Fund. Retrieved May 14, 2009 from http://www.blueorchard.com/jahia/Jahia/Products_1/pid/190

Brinson, G. P., Hood, L. R. & G. L. Beebower (1986). Determinants of Portfolio Performance. Financial Analysts Journal, 39-44.

Brooks, C. & H. M. Kat (2002). The Statistical Properties of Hedge Fund Return Index Returns and Their Implications for Investors. The Journal of Alternative Investments, 26-44.

Callaghan, I., Gonazalez, H. Maurice, D. & C. Novak (2007). Microfinance – On the Road to Capital Markets. Journal of Applied Corporate Finance, Morgan Stanley, 115-124.

Campbell, J. Y., Lo, A. W. & A. C. MacKinlay (1997). The econometrics of finan-cial markets. Princeton: Princeton University Press

Citigroup (2010). International market indexes – February 2010 performance. Retrieved March 12, 2010 from www.themarkets.com (restricted access).

P. M. Becker, Investing in Microfinance, DOI 10.1007/978-3-8349-8926-0 © Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2010

BIBLIOGRAPHY 145

Consultative Group to Assist the Poor (CGAP, 2009a). The impact of the financial crisis on microfinance institutions and their clients. CGAP Brief. Retrieved De-cember 14, 2009 from http://www.cgap.org/gm/document-1.9.38570/CGAPBrief _MIV.pdf

Consultative Group to Assist the Poor (CGAP, 2009b). MIV performance and pros-pects: highlights from the CGAP 2009 MIV Benchmark Survey. CGAP Brief. Retrieved December 14, 2009 from http://www.cgap.org/gm/document-1.9.38570/CGAPBrief_MIV.pdf

Consultative Group to Assist the Poor (CGAP, 2009c). Asset and liability manage-ment for deposit-taking microfinance institutions. CGAP focus note. Retrieved December 14, 2009 from http://www.cgap.org/gm/document-1.9.34818/FN 55.pdf

Consultative Group to Assist the Poor (CGAP, 2007). Savings for poor people: good for clients, good for business? Retrieved December 14, 2009 from http://dev.cgap.org/gm/document-1.9.3912/Portfolio_Dec2007.pdf

Chobra, V. & W. Ziemba (1993). The effects of errors in means, variances, and covariances on optimal portfolio choice. Journal of Portfolio Management, 6 -11.

Churchill, C. (2006). What is insurance for the poor. In Churchill, C. (ed.), Protect-ing the poor: a microinsurance compendium, ILO, 12-24.

Coleman, J. (1990). Social capital in the creation of human capital. American Jour-nal of Sociology, 95-120.

Copeland, T. E. & J. E. Weston (1988). Financial theory and corporate policy, 3rd ed. Reading: Addison Wesley.

Credit Suisse First Boston (2010). CSFB/Tremont Hedge Fund Index, www.hedgeindex.com.

Davies, G. (2004). Scenarios come to Davos. A GBN conversation with Ged Davis. Retrieved December 12, 2009 from http://www.weforum.org/pdf/CSI/ GBN_Davis_interview.pdf

146 BIBLIOGRAPHY

Dieckmann, R. (2007). Microfinance: an emerging investment opportunity. Interna-tional Issues. Frankfurt: Deutsche Bank Research.

EFSE (2010). Microcredit for big ideas. EFSE brochure. Retrieved February 2, 2010 from http://www.efse.lu/fileadmin/downloads/publications/brochures/ EFSE_Microcredit.pdf

Fama, E. & K. R. French (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 3-56.

Fama, E. (1965). The behaviour of stock market prices. Journal of Business, 34-105.

Felder-Kozu, N. (2008). Kleiner Einsatz, grosse Wirkung. Mikrofinanzierung und Mikrofranchising – Modelle gegen die Armut. Zürich: rüffer & rub.

Gantenbein, P. Laternser, S. & K. Spremann (2001). Anlageberatung und Portofo-liomanagement. Zürich: NZZ Verlag.

Gottschalk, K. & M. Steinbrecher (2005). Wie Szenarien die strategische Unter-nehmenssteuerung balancieren. Organisationsentwicklung, 24-33.

GPR (2009). GPR construction and maintenance procedures. FTSE NAREIT US real estate index series. Retrieved January 14, 2010 from http://www. propertyshares.com/images/pdf/ConstructionMaintenanceSeptember2006.pdf

Hollis, A. & A. Sweetman (2003). Microfinance and Famine: The Irish Loan Funds during the Great Famine. Working Paper.

Hollis, A. & A. Sweetman (1997). Complementarity, Competition and Institutional Development: The Irish Loan Funds through Three Centuries. Working Paper.

Horneff, W.J., Raimond, H. M., Mitchell, O. S. & M. Z. Stamos (2009). Asset allo-cation over the life cycle with investment-linked survival-contingent payouts. Journal of Banking and Finance, 1688-1699.

J.P.Morgan (2010). Emerging markets bond index monitor. Retrieved March 12, 2010 from www.themarkets.com (restricted access).

BIBLIOGRAPHY 147

Kaduff, J. V. (1996). Shortfall-risk-basierte Portfolio-Strategien: Grundlagen, Anwendungen, Algorithmen. Bern: Paul Haupt.

Kalin, D. & R. Zagst (1999). Portfolio optimization: volatility constraints versus shortfall constraints. OR Spectrum, 97-122.

Kataoka, S. (1963). A stochastic programming model. Econometrica, 181-196.

Kielholz, W. & A. P. Durrer (1997). Insurance derivatives and securitization: new hedging perspectives for the US cat insurance market. The Geneva Papers on Risk and Insurance, 3-16.

Lang, S. (2009). Core Satellite Portfoliomanagement. Bern: Haupt Verlag.

Lhabitant, F. S. (2004). Hedge funds – quantitative insights. Chichester: Wiley.

Lintner, J. (1965). The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. Review of Economics and Statistics, 13-37.

Littlefield, E. & C. Kneiding (2009). The global financial crisis and its impact on microfinance. CGAP Occasional Paper.

LPX (2009). Guide to the LPX equity indices, Version 2.7. Retrieved January 14, 2010 from http://www.lpx-group.com/lpx/fileadmin/images/indices/ LPX_ Guide_to_the_Equity_Indices.pdf

Mandelbrot, B. (1963). New methods in statistical economics. Journal of Political Economy, 207-209.

Markowitz, H. (1987). Mean-variance analysis. Oxford: Basil Blackwell.

Markowitz, H. (1959). Portfolio Selection – Efficient Diversification of Investments. New York: John Wiley.

Markowitz, H. (1952). Portfolio Selection. Journal of Finance, 77-91.

148 BIBLIOGRAPHY

Maslakovic, M. (2009). IFSL report on sovereign wealth funds 2009. Retrieved December 28, 2009 from http://www.ifsl.org.uk/upload/CBS_Sovereign %20Wealth%20Funds%202009.pdf

McKinsey (2006). Optimising capital supply in support of microfinance industry growth. Presentation for Omidyar Network/The SEEP Network, Microfinance Investor Roundtable. Retrieved August 24, 2009 from http://seepstage. forumone.com/content/library/detail/4656

Meehan, J. (2004). Tapping financial markets for microfinance. Working Paper. Retrieved August 25, 2009 from http://www.microcapital.org/downloads/ resourcepapers/GFUSA-CapitalMarkets.pdf

Merton, R. C. (1990). Continuous-time finance. Cambridge: Blackwell.

Merton, R. C. (1969). Lifetime portfolio selection under uncertainty: the continuous time case. Review of Economics and Statistics, 247-257.

Minx, E. & E. Böhlke (2006). Denken in alternativen Zukünften. Internationale Politik Nr. 12, 14-22.

Minx, E. & H. Roehl (2006). Werkzeugkiste für Berater und Change Manager: 9. Szenario-Technik. Organisationsentwicklung, 78-81.

Minx, E. & H. Roehl (1998). Von Inseln und Brücken – Wissensentwicklung durch Szenarien bei der Daimler-Benz AG. zfo no.3, 167-170.

Missler-Behr, M. (2006). Auf der Suche nach Zukunftsbildern – eine Regelbasis zur Szenarienauswahl. In: Wilms, F. (eds.). Szenariotechnik. Vom Umgang mit der Zukunft. Bern: Paul Haupt.

MIX/Microfinance Information Exchange (2009). The MicroBanking Bulleting No. 19. Retrieved January 16, 2010 from http://www.themix.org/sites/ default/files/MBB%2019%20-%20December%202009_0.pdf

BIBLIOGRAPHY 149

MIX/Microfinance Information Exchange (2008). The MicroBanking Bulleting No. 17. Retrieved January 16, 2009 from http://www.themix.org/microbanking-bulletin/mbb-issue-no-17-autumn-2008

Mossin, J. (1966). Equilibrium in a capital asset market. Econometrica, 768-783.

MSCI Barra (2010). Index definitions. Retrieved March 12, 2010 from http://www.mscibarra.com/products/indices/international_equity_indices/definitions.html

Porter, M. (1985). Competitive Advantage. New York: Free Press.

Reilly, F. K. & K. C. Brown (2006). Investment analysis and portfolio management, 8th edition. Mason: Thomson.

responsAbility (2009). Fund prospect responsAbility Global MF Fund. Retreived May 14, 2009 from http://www.responsability.com/site/index.cfm?id_art=42157 &act MenuItemID=20541&vsprache=DE

Ringland, G. (1998). Scenario planning. Managing for the future. Chichester: Wiley & Sons.

Ringland, G. (2002). Scenarios in business. Chichester: Wiley & Sons.

Rosenberg, R., Gonzalez, A. & S. Narain (2009). The New Moneylenders: Are the Poor Being Exploited by High Microcredit Interest Rates? CGAP Occasional Paper.

Roy, A. D. (1952). Safety first and the holding of assets. Econometrica, 431-449.

Scholes, M. & J. Williams (1977). Estimating betas from nonsynchronous data. Journal of Financial Economics, 309-327.

SWP (Stiftung Wissenschaft und Politik, 2008). Europäische Energiesicherheit 2020. Szenarien für mögliche Entwicklungen in Europa und seinen energiepoli-tisch wichtigsten Nachbarregionen. SWP-Studien.

150 BIBLIOGRAPHY

Schwartz, P. (1996). The art of the long view: paths to strategic insight for yourself and your company. New York: Doubleday.

Seibel, H. D. (2005). Does history matter? The old and the new world of microfin-ance in Europe and Asia. Working Paper.

Seibel, H. D. (2003). History matters in microfinance. Working Paper.

Sharpe, W. F., Alexander, G. J. & J. V. Bailey (1999). Investments, 6th ed. Upper Saddle River: Prentice Hall.

Sharpe, W. F. (1964). Capital asset prices: a theory of market equilibrium under conditions of risk. Journal of Finance, 425-442.

Standard & Poor’s (2009). S&P GSCI commodity indices. Retrieved on January 14, 2010 from http://www2.standardandpoors.com/spf/pdf/index/SP_GSCI_ Fact-sheet.pdf

Steiner, M. & C. Bruns (2007). Wertpapiermanagement, 9th ed. Stuttgart: Schäffer-Poeschel.

Spremann, K. & P. Gantenbein (2005). Kapitalmärkte. Stuttgart: Lucius&Lucius.

Spremann, K. (2008). Portfoliomanagement, 4th ed. München: Oldenbourg.

Spremann, K. (1997). Humankapital im Portefeuille privater Investoren. Zeitschrift für Betriebswirtschaft, 145-147.

Spremann, K. (1995). Asset-Allokation im Lebenszyklus und Vintage-Programm. In: Gehrig, G. (eds.): Private Banking, Zürich, 115-146.

Swiss Re (2007). Swiss Re launches the first catastrophe bond indices. Retrieved January 14, 2010 from http://www.swissre.com/resources /a67d68804660790fb 923fd276a9800c6-IDUR_74LC9G_Swis.pdf

Symbiotics (2010). Symbiotics50 index information. Retrieved February 14, 2010 from Symbiotics (restricted access).

BIBLIOGRAPHY 151

Telser, L. G. (1955). Safety first and hedging. The Review of Economic Studies, 1-16.

Treynor, J. (1962). Toward a theory of market value of risky assets. Unpublished manuscript.

Tobin (1965). The theory of portfolio selecting. Brechling, F.B.R & Hahn, F.H. (editors). The theory of interest rates. London: Macmillan.

UBS (2008). UBS global convertible bond index. Index guidelines. Retrieved on March 12, 2010 from www.themarkets.com (restricted access).

Uysal, E., Trainer, F. H. & J. Reiss (2001). Revisiting mean-variance optimization. Journal of Portfolio Management, 71-81.

von Pischke, J. D. (2006). New partnerships for sustainability and outreach. In Matthäus-Maier, I. & von Pischke, J.D. (eds.), New partnerships for innovation in microfinance (pp. 1-13). Berlin: Springer.

von Stauffenberg, D. (2008). The 2007 microfinance investment vehicle survey. Retrieved February 28, 2009 from http://microrate.com/home/publications/ microfinance-research-reports

Wack, P. (1985). Scenarios: shooting the rapids. Harvard Business Review, 139-150.

Wack, P. (1985). Scenarios: unchartered waters ahead. Harvard Business Review, 72-79.

WEF Report (2010). The future of the global financial system - navigating the chal-lenges ahead. World Scenario Series. Retrieved February 2, 2010 from http://www.weforum.org/en/initiatives/Scenarios/NFA/index.htm

WEF Report (2009a). The Future of the global financial system: a near-term out-look and long-term scenarios. World Scenario Series. Retrieved March 13, 2009 from http://www.weforum.org/en/initiatives/Scenarios/NewFinancialArchitec- ture/index.htm

152 BIBLIOGRAPHY

WEF (2009b). Scenario planning. Homepage of World Economic Forum. Retrieved April 16, 2009 from http://www.weforum.org/en/initiatives/Scenarios/index.htm

Zimmermann, H. (2004). Sind Kapitalschutzstrategien in der Vorsorge sinnvoll? Überlegungen aus ökonomischer Sicht. Schweizer Personalvorsorge, 19-25.

INTERVIEWS 153

Interviews

De Bleecker, Berg. PGGM, Investment Manager. Telephone interview. Amsterdam: June 30, 2009.

Huber, Patrik. responsAbility Social Investments AG, Member of the Board. Per-sonal interview. Zurich: April 28, 2009 and several more discussions during and after the scenario process.

Krauss, Annette. University of Zurich, Head of Centre for Microfinance. Personal interview. Zurich: April 2, 2009 and several more discussions during the scenario process.

Knöpfel, Ivo. onValues, CEO. Personal interview. Zurich: June 26, 2009.

Mammertz, Rochus. responsAbility Social Investments AG, equity and regulation specialist. Telephone interview. Zurich: June 30, 2009.

von Stauffenberg, Damian. Microrate, CEO. Personal interview. London: October 31, 2008 and several more discussions during the scenario process.

P. M. Becker, Investing in Microfinance, DOI 10.1007/978-3-8349-8926-0 © Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2010

154 APPENDIX

Appendix Appendix– 1: Descriptor essay no. 12 – market structure in MFI segment

P. M. Becker, Investing in Microfinance, DOI 10.1007/978-3-8349-8926-0 © Gabler Verlag | Springer Fachmedien Wiesbaden GmbH 2010

APPENDIX 155

156 APPENDIX

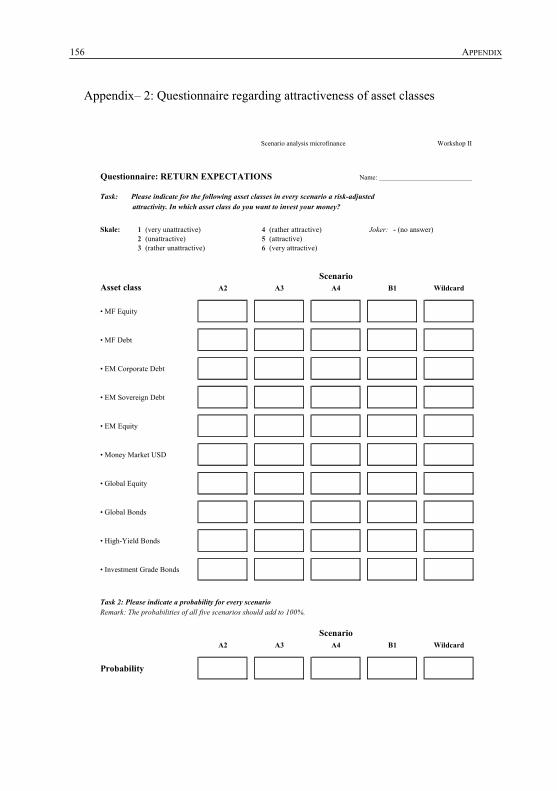

Appendix– 2: Questionnaire regarding attractiveness of asset classes

Scenario analysis microfinance Workshop II

Questionnaire: RETURN EXPECTATIONS Name: ___________________________

Task: Please indicate for the following asset classes in every scenario a risk-adjusted attractivity. In which asset class do you want to invest your money?

Skale: 1 (very unattractive) 4 (rather attractive) Joker: - (no answer) 2 (unattractive) 5 (attractive) 3 (rather unattractive) 6 (very attractive)

Asset class A2 A3 A4 B1 Wildcard

• MF Equity

• MF Debt

• EM Corporate Debt

• EM Sovereign Debt

• EM Equity

• Money Market USD

• Global Equity

• Global Bonds

• High-Yield Bonds

• Investment Grade Bonds

Task 2: Please indicate a probability for every scenarioRemark: The probabilities of all five scenarios should add to 100%.

A2 A3 A4 B1 Wildcard

Probability

Scenario

Scenario

APPENDIX 157

Appendix– 3: Questionnaire regarding correlation measures

Scenario analysis microfinance Workshop II

Questionnarie: CORRELATION Name: ___________________________Idea: Measure correlations of macroeconomic and market factors with different asset classes

Factor Asset class 1 0.5 0 -0.5 -1 no answer

• Increasing EM growth EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing EM inflation EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing EM FX volatility EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing global liquidity EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing political stability (in countries) EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• High debt level EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Negative primary budget EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing commodity prices EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing global political stability EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Increasing acceptance of market economy in EM EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

• Globalisation EM Corporate Bonds � � � � � �EM Bonds � � � � � �EM Equity � � � � � �MF Debt � � � � � �MF Equity � � � � � �

158 APPENDIX

Appendix– 4: Covariance and correlation matrices excluding microfinance

MM

USD

EQ W

orld

EQ

EM

FI W

orld

FI IL

FI E

MFI

CR

EFI

HY

FI C

BFI

CA

TH

FPE

RE

ITs

CO

M

Mon

ey M

arke

t USD

0.00

000.

0000

0.00

00-0

.000

10.

0000

0.00

000.

0000

0.00

000.

0000

0.00

000.

0001

0.00

020.

0000

0.00

01E

quiti

es W

orld

0.00

000.

0323

0.03

980.

0020

0.00

630.

0115

0.00

780.

0149

0.01

950.

0012

0.00

730.

0384

0.03

100.

0181

Equ

ities

EM

0.00

000.

0398

0.06

590.

0016

0.00

800.

0176

0.01

070.

0218

0.02

690.

0017

0.01

170.

0542

0.03

950.

0299

Gov

Bon

ds W

orld

0.00

000.

0020

0.00

160.

0049

0.00

430.

0022

0.00

370.

0013

0.00

250.

0003

0.00

05-0

.002

40.

0040

0.00

23G

ov B

onds

Infla

tion

Lin

ked

-0.0

001

0.00

630.

0080

0.00

430.

0076

0.00

440.

0057

0.00

470.

0056

0.00

070.

0020

0.00

380.

0098

0.00

89G

ov B

onds

EM

0.00

000.

0115

0.01

760.

0022

0.00

440.

0121

0.00

550.

0096

0.00

930.

0008

0.00

370.

0156

0.01

370.

0076

Cre

dit B

onds

0.00

000.

0078

0.01

070.

0037

0.00

570.

0055

0.00

820.

0069

0.00

720.

0008

0.00

260.

0078

0.01

180.

0085

Hig

h Y

ield

Bon

ds0.

0000

0.01

490.

0218

0.00

130.

0047

0.00

960.

0069

0.01

660.

0115

0.00

130.

0047

0.02

080.

0183

0.01

10C

onve

rtib

le B

onds

0.00

000.

0195

0.02

690.

0025

0.00

560.

0093

0.00

720.

0115

0.02

130.

0013

0.00

700.

0250

0.01

780.

0148

Cat

Bon

ds0.

0000

0.00

120.

0017

0.00

030.

0007

0.00

080.

0008

0.00

130.

0013

0.01

510.

0007

0.00

190.

0018

0.00

18H

edge

Fun

ds0.

0000

0.00

730.

0117

0.00

050.

0020

0.00

370.

0026

0.00

470.

0070

0.00

070.

0200

0.01

210.

0065

0.00

82Pr

ivat

e E

quity

0.00

010.

0384

0.05

42-0

.002

40.

0038

0.01

560.

0078

0.02

080.

0250

0.00

190.

0121

0.13

070.

0408

0.02

75R

EIT

s0.

0002

0.03

100.

0395

0.00

400.

0098

0.01

370.

0118

0.01

830.

0178

0.00

180.

0065

0.04

080.

0500

0.02

07C

omm

oditi

es0.

0000

0.01

810.

0299

0.00

230.

0089

0.00

760.

0085

0.01

100.

0148

0.00

180.

0082

0.02

750.

0207

0.07

08

Ris

k0.

5%18

.0%

25.7

%7.

0%8.

7%11

.0%

9.1%

12.9

%14

.6%

12.3

%14

.1%

36.2

%22

.4%

26.6

%

MM

USD

EQ W

orld

EQ

EM

FI W

orld

FI IL

FI E

MFI

CR

EFI

HY

FI C

BFI

CA

TH

FPE

RE

ITs

CO

M

Mon

ey M

arke

t USD

1.00

0.01

-0.0

1-0

.08

-0.0

40.

00-0

.04

-0.0

40.

000.

010.

040.

060.

020.

05E

quiti

es W

orld

0.01

1.00

0.86

0.16

0.40

0.58

0.48

0.64

0.75

0.06

0.29

0.59

0.77

0.38

Equ

ities

EM

0.01

0.86

1.00

0.09

0.36

0.62

0.46

0.66

0.72

0.05

0.32

0.58

0.69

0.44

Gov

Bon

ds W

orld

-0.0

30.

160.

091.

000.

710.

290.

580.

140.

250.

030.

05-0

.09

0.25

0.12

Gov

Bon

ds In

flatio

n L

inke

d-0

.07

0.40

0.36

0.71

1.00

0.46

0.72

0.41

0.44

0.07

0.16

0.12

0.51

0.39

Gov

Bon

ds E

M-0

.03

0.58

0.62

0.29

0.46

1.00

0.55

0.68

0.58

0.06

0.24

0.39

0.56

0.26

Cre

dit B

onds

0.00

0.48

0.46

0.58

0.72

0.55

1.00

0.59

0.55

0.07

0.20

0.24

0.58

0.35

Hig

h Y

ield

Bon

ds-0

.03

0.64

0.66

0.14

0.41

0.68

0.59

1.00

0.61

0.08

0.26

0.45

0.64

0.32

Con

vert

ible

Bon

ds-0

.03

0.75

0.72

0.25

0.44

0.58

0.55

0.61

1.00

0.07

0.34

0.47

0.55

0.38

Cat

Bon

ds0.

000.

060.

050.

030.

070.

060.

070.

080.

071.

000.

040.

040.

060.

06H

edge

Fun

ds0.

010.

290.

320.

050.

160.

240.

200.

260.

340.

041.

000.

240.

210.

22Pr

ivat

e E

quity

0.01

0.59

0.58

-0.0

90.

120.

390.

240.

450.

470.

040.

241.

000.

500.

29R

EIT

s0.

100.

770.

690.

250.

510.

560.

580.

640.

550.

060.

210.

501.

000.

35C

omm

oditi

es0.

010.

380.

440.

120.

390.

260.

350.

320.

380.

060.

220.

290.

351.

00

APPENDIX 159

Appendix– 5: Covariance and correlation matrices including microfinance (quan-titative approach)

MM

USD

EQ

Wor

ldEQ

EM

FI W

orld

FI IL

FI E

MFI

CR

EFI

HY

FI C

BFI

CA

TH

FPE

RE

ITs

CO

MFI

MF

Mon

ey M

arke

t USD

0.00

000.

0000

0.00

00-0

.000

10.

0000

0.00

000.

0000

0.00

000.

0000

0.00

000.

0001

0.00

020.

0000

0.00

010.

0000

Equi

ties W

orld

0.00

000.

0323

0.03

980.

0020

0.00

630.

0115

0.00

780.

0149

0.01

950.

0012

0.00

730.

0384

0.03

100.

0181

-0.0

001

Equi

ties E

M0.

0000

0.03

980.

0659

0.00

160.

0080

0.01

760.

0107

0.02

180.

0269

0.00

170.

0117

0.05

420.

0395

0.02

99-0

.000

2G

ov B

onds

Wor

ld0.

0000

0.00

200.

0016

0.00

490.

0043

0.00

220.

0037

0.00

130.

0025

0.00

030.

0005

-0.0

024

0.00

400.

0023

0.00

00G

ov B

onds

Infla

tion

Link

ed-0

.000

10.

0063

0.00

800.

0043

0.00

760.

0044

0.00

570.

0047

0.00

560.

0007

0.00

200.

0038

0.00

980.

0089

0.00

00G

ov B

onds

EM

0.00

000.

0115

0.01

760.

0022

0.00

440.

0121

0.00

550.

0096

0.00

930.

0008

0.00

370.

0156

0.01

370.

0076

0.00

00C

redi

t Bon

ds0.

0000

0.00

780.

0107

0.00

370.

0057

0.00

550.

0082

0.00

690.

0072

0.00

080.

0026

0.00

780.

0118

0.00

850.

0000

Hig

h Y

ield

Bon

ds0.

0000

0.01

490.

0218

0.00

130.

0047

0.00

960.

0069

0.01

660.

0115

0.00

130.

0047

0.02

080.

0183

0.01

100.

0000

Con

vert

ible

Bon

ds0.

0000

0.01

950.

0269

0.00

250.

0056

0.00

930.

0072

0.01

150.

0213

0.00

130.

0070

0.02

500.

0178

0.01

48-0

.000

1C

at B

onds

0.00

000.

0012

0.00

170.

0003

0.00

070.

0008

0.00

080.

0013

0.00

130.

0151

0.00

070.

0019

0.00

180.

0018

0.00

00H

edge

Fun

ds0.

0000

0.00

730.

0117

0.00

050.

0020

0.00

370.

0026

0.00

470.

0070

0.00

070.

0200

0.01

210.

0065

0.00

82-0

.000

1Pr

ivat

e Eq

uity

0.00

010.

0384

0.05

42-0

.002

40.

0038

0.01

560.

0078

0.02

080.

0250

0.00

190.

0121

0.13

070.

0408

0.02

75-0

.000

3R

EIT

s0.

0002

0.03

100.

0395

0.00

400.

0098

0.01

370.

0118

0.01

830.

0178

0.00

180.

0065

0.04

080.

0500

0.02

070.

0001

Com

mod

ities

0.00

000.

0181

0.02

990.

0023

0.00

890.

0076

0.00

850.

0110

0.01

480.

0018

0.00

820.

0275

0.02

070.

0708

-0.0

005

Cre

dit -

Mic

rofin

ance

0.00

00-0

.000

1-0

.000

20.

0000

0.00

000.

0000

0.00

000.

0000

-0.0

001

0.00

00-0

.000

1-0

.000

30.

0001

-0.0

005

0.00

73

Ris

k0.

5%18

.0%

25.7

%7.

0%8.

7%11

.0%

9.1%

12.9

%14

.6%

12.3

%14

.1%

36.2

%22

.4%

26.6

%8.

5%

MM

USD

EQ

Wor

ldEQ

EM

FI W

orld

FI IL

FI E

MFI

CR

EFI

HY

FI C

BFI

CA

TH

FPE

RE

ITs

CO

MFI

MF

Mon

ey M

arke

t USD

1.00

0.01

-0.0

1-0

.08

-0.0

40.

00-0

.04

-0.0

40.

000.

010.

040.

060.

020.

050.

02Eq

uitie

s Wor

ld0.

011.

000.

860.

160.

400.

580.

480.

640.

750.

060.

290.

590.

770.

380.

00Eq

uitie

s EM

0.01

0.86

1.00

0.09

0.36

0.62

0.46

0.66

0.72

0.05

0.32

0.58

0.69

0.44

-0.0

1G

ov B

onds

Wor

ld-0

.03

0.16

0.09

1.00

0.71

0.29

0.58

0.14

0.25

0.03

0.05

-0.0

90.

250.

120.

00G

ov B

onds

Infla

tion

Link

ed-0

.07

0.40

0.36

0.71

1.00

0.46

0.72

0.41

0.44

0.07

0.16

0.12

0.51

0.39

0.01

Gov

Bon

ds E

M-0

.03

0.58

0.62

0.29

0.46

1.00

0.55

0.68

0.58

0.06

0.24

0.39

0.56

0.26

0.00

Cre

dit B

onds

0.00

0.48

0.46

0.58

0.72

0.55

1.00

0.59

0.55

0.07

0.20

0.24

0.58

0.35

0.00

Hig

h Y

ield

Bon

ds-0

.03

0.64

0.66

0.14

0.41

0.68

0.59

1.00

0.61

0.08

0.26

0.45

0.64

0.32

0.00

Con

vert

ible

Bon

ds-0

.03

0.75

0.72

0.25

0.44

0.58

0.55

0.61

1.00

0.07

0.34

0.47

0.55

0.38

-0.0

1C

at B

onds

0.00

0.06

0.05

0.03

0.07

0.06

0.07

0.08

0.07

1.00

0.04

0.04

0.06

0.06

0.00

Hed

ge F

unds

0.01

0.29

0.32

0.05

0.16

0.24

0.20

0.26

0.34

0.04

1.00

0.24

0.21

0.22

0.00

Priv

ate

Equi

ty0.

010.

590.

58-0

.09

0.12

0.39

0.24

0.45

0.47

0.04

0.24

1.00

0.50

0.29

-0.0

1R

EIT

s0.

100.

770.

690.

250.

510.

560.

580.

640.

550.

060.

210.

501.

000.

350.

01C

omm

oditi

es0.

010.

380.

440.

120.

390.

260.

350.

320.

380.

060.

220.

290.

351.

00-0

.02

Cre

dit -

Mic

rofin

ance

0.00

0.00

-0.0

10.

000.

010.

000.

000.

00-0

.01

0.00

0.00

-0.0

10.

01-0

.02

1.00

160 APPENDIX

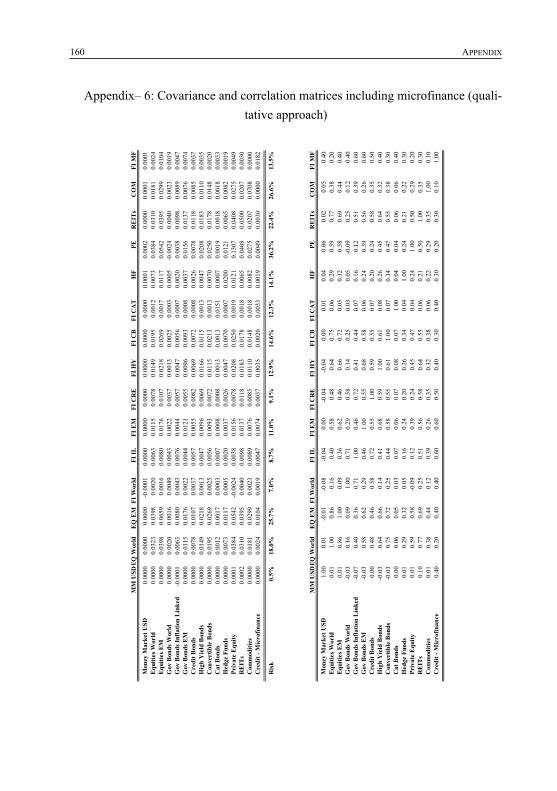

Appendix– 6: Covariance and correlation matrices including microfinance (quali-tative approach)

MM

USD

EQ

Wor

ldEQ

EM

FI W

orld

FI IL

FI E

MFI

CR

EFI

HY

FI C

BFI

CA

TH

FPE

RE

ITs

CO

MFI

MF

Mon

ey M

arke

t USD

0.00

000.

0000

0.00

00-0

.000

10.

0000

0.00

000.

0000

0.00

000.

0000

0.00

000.

0001

0.00

020.

0000

0.00

010.

0001

Equi

ties W

orld

0.00

000.

0323

0.03

980.

0020

0.00

630.

0115

0.00

780.

0149

0.01

950.

0012

0.00

730.

0384

0.03

100.

0181

0.00

24Eq

uitie

s EM

0.00

000.

0398

0.06

590.

0016

0.00

800.

0176

0.01

070.

0218

0.02

690.

0017

0.01

170.

0542

0.03

950.

0299

0.01

04G

ov B

onds

Wor

ld0.

0000

0.00

200.

0016

0.00

490.

0043

0.00

220.

0037

0.00

130.

0025

0.00

030.

0005

-0.0

024

0.00

400.

0023

0.00

19G

ov B

onds

Infla

tion

Link

ed-0

.000

10.

0063

0.00

800.

0043

0.00

760.

0044

0.00

570.

0047

0.00

560.

0007

0.00

200.

0038

0.00

980.

0089

0.00

47G

ov B

onds

EM

0.00

000.

0115

0.01

760.

0022

0.00

440.

0121

0.00

550.

0096

0.00

930.

0008

0.00

370.

0156

0.01

370.

0076

0.00

74C

redi

t Bon

ds0.

0000

0.00

780.

0107

0.00

370.

0057

0.00

550.

0082

0.00

690.

0072

0.00

080.

0026

0.00

780.

0118

0.00

850.

0037

Hig

h Y

ield

Bon

ds0.

0000

0.01

490.

0218

0.00

130.

0047

0.00

960.

0069

0.01

660.

0115

0.00

130.

0047

0.02

080.

0183

0.01

100.

0035

Con

vert

ible

Bon

ds0.

0000

0.01

950.

0269

0.00

250.

0056

0.00

930.

0072

0.01

150.

0213

0.00

130.

0070

0.02

500.

0178

0.01

480.

0020

Cat

Bon

ds0.

0000

0.00

120.

0017

0.00

030.

0007

0.00

080.

0008

0.00

130.

0013

0.01

510.

0007

0.00

190.

0018

0.00

180.

0033

Hed

ge F

unds

0.00

000.

0073

0.01

170.

0005

0.00

200.

0037

0.00

260.

0047

0.00

700.

0007

0.02

000.

0121

0.00

650.

0082

0.00

19Pr

ivat

e Eq

uity

0.00

010.

0384

0.05

42-0

.002

40.

0038

0.01

560.

0078

0.02

080.

0250

0.00

190.

0121

0.13

070.

0408

0.02

750.

0049

RE

ITs

0.00

020.

0310

0.03

950.

0040

0.00

980.

0137

0.01

180.

0183

0.01

780.

0018

0.00

650.

0408

0.05

000.

0207

0.00

30C

omm

oditi

es0.

0000

0.01

810.

0299

0.00

230.

0089

0.00

760.

0085

0.01

100.

0148

0.00

180.

0082

0.02

750.

0207

0.07

080.

0000

Cre

dit -

Mic

rofin

ance

0.00

000.

0024

0.01

040.

0019

0.00

470.

0074

0.00

370.

0035

0.00

200.

0033

0.00

190.

0049

0.00

300.

0000

0.01

82

Ris

k0.

5%18

.0%

25.7

%7.

0%8.

7%11

.0%

9.1%

12.9

%14

.6%

12.3

%14

.1%

36.2

%22

.4%

26.6

%13

.5%

MM

USD

EQ

Wor

ldEQ

EM

FI W

orld

FI IL

FI E

MFI

CR

EFI

HY

FI C

BFI

CA

TH

FPE

RE

ITs

CO

MFI

MF

Mon

ey M

arke

t USD

1.00

0.01

-0.0

1-0

.08

-0.0

40.

00-0

.04

-0.0

40.

000.

010.

040.

060.

020.

050.

40Eq

uitie

s Wor

ld0.

011.

000.

860.

160.

400.

580.

480.

640.

750.

060.

290.

590.

770.

380.

20Eq

uitie

s EM

0.01

0.86

1.00

0.09

0.36

0.62

0.46

0.66

0.72

0.05

0.32

0.58

0.69

0.44

0.40

Gov

Bon

ds W

orld

-0.0

30.

160.

091.

000.

710.

290.

580.

140.

250.

030.

05-0

.09

0.25

0.12

0.40

Gov

Bon

ds In

flatio

n Li

nked

-0.0

70.

400.

360.

711.

000.

460.

720.

410.

440.

070.

160.

120.

510.

390.

60G

ov B

onds

EM

-0.0

30.

580.

620.

290.

461.

000.

550.

680.

580.

060.

240.

390.

560.

260.

60C

redi

t Bon

ds0.

000.

480.

460.

580.

720.

551.

000.

590.

550.

070.

200.

240.

580.

350.

50H

igh

Yie

ld B

onds

-0.0

30.

640.

660.

140.

410.

680.

591.

000.

610.

080.

260.

450.

640.

320.

40C

onve

rtib

le B

onds

-0.0

30.

750.

720.

250.

440.

580.

550.

611.

000.

070.

340.

470.

550.

380.

30C

at B

onds

0.00

0.06

0.05

0.03

0.07

0.06

0.07

0.08

0.07

1.00

0.04

0.04

0.06

0.06

0.40

Hed

ge F

unds

0.01

0.29

0.32

0.05

0.16

0.24

0.20

0.26

0.34

0.04

1.00

0.24

0.21

0.22

0.30

Priv

ate

Equi

ty0.

010.

590.

58-0

.09

0.12

0.39

0.24

0.45

0.47

0.04

0.24

1.00

0.50

0.29

0.20

RE

ITs

0.10

0.77

0.69

0.25

0.51

0.56

0.58

0.64

0.55

0.06

0.21

0.50

1.00

0.35

0.30

Com

mod

ities

0.01

0.38

0.44

0.12

0.39

0.26

0.35

0.32

0.38

0.06

0.22

0.29

0.35

1.00

0.10

Cre

dit -

Mic

rofin

ance

0.40

0.20

0.40

0.40

0.60

0.60

0.50

0.40

0.30

0.40

0.30

0.20

0.30

0.10

1.00

APPENDIX 161

Appendix– 7: Optimized portfolio weights excluding microfinance

0.5

0.75

11.

251.

52

2.5

3.25

45

710

Mon

ey M

arke

t USD

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

20.0

%20

.0%

20.0

%20

.0%

20.0

%E

quiti

es W

orld

0.0%

0.0%

3.4%

6.7%

8.2%

7.7%

7.1%

5.5%

5.1%

4.7%

4.0%

3.1%

Equ

ities

EM

81.1

%64

.3%

44.5

%31

.9%

24.5

%16

.5%

12.1

%9.

2%6.

7%4.

5%1.

7%0.

0%G

ov B

onds

Wor

ld0.

0%0.

0%0.

0%0.

0%0.

0%11

.1%

20.7

%17

.9%

23.4

%28

.3%

34.2

%38

.9%

Gov

Bon

ds In

flatio

n L

inke

d0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%G

ov B

onds

EM

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Cre

dit B

onds

0.0%

0.0%

0.0%

0.1%

9.2%

11.5

%10

.6%

8.3%

7.8%

6.8%

4.2%

2.2%

Hig

h Y

ield

Bon

ds0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

8%3.

9%6.

2%C

onve

rtib

le B

onds

0.0%

1.7%

8.4%

11.7

%10

.2%

7.8%

6.2%

4.9%

3.9%

3.1%

1.8%

0.8%

Cat

Bon

ds0.

0%5.

3%15

.0%

20.6

%21

.8%

21.7

%21

.2%

16.8

%16

.6%

16.2

%15

.7%

15.3

%H

edge

Fun

ds0.

0%14

.5%

18.0

%20

.1%

19.7

%18

.4%

17.3

%13

.7%

13.1

%12

.5%

11.7

%11

.1%

Priv

ate

Equi

ty18

.9%

14.1

%10

.2%

7.7%

6.5%

5.3%

4.8%

3.7%

3.4%

3.1%

2.7%

2.4%

RE

ITs

0.0%

0.0%

0.5%

1.2%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Com

mod

ities

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Ret

urn

p.a.

11.5

9%10

.22%

8.85

%8.

02%

7.37

%6.

47%

5.90

%5.

05%

4.73

%4.

44%

4.09

%3.

83%

Ris

k p.

a.25

.42%

20.9

3%16

.66%

14.2

4%12

.45%

10.1

3%8.

79%

6.87

%6.

18%

5.63

%5.

07%

4.76

%

Shor

tfal

l in

year

s13

.00

11.3

39.

598.

537.

726.

646.

005.

014.

634.

364.

164.

16

lam

bda

162 APPENDIX

Appendix– 8: Optimized portfolio weights including microfinance (quantitative approach) – risk factor set to 8.5%

0.5

0.75

11.

251.

52

2.5

3.25

45

710

Mon

ey M

arke

t USD

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

13.5

%20

.0%

20.0

%E

quiti

es W

orld

0.0%

0.0%

0.0%

0.0%

0.0%

2.0%

3.5%

3.9%

3.6%

3.0%

2.6%

2.2%

Equ

ities

EM

81.1

%61

.9%

47.9

%38

.9%

31.8

%22

.0%

15.9

%10

.8%

8.1%

6.3%

3.9%

1.7%

Gov

Bon

ds W

orld

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

3.5%

10.4

%11

.1%

15.5

%21

.1%

Gov

Bon

ds In

flatio

n L

inke

d0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%G

ov B

onds

EM

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Cre

dit B

onds

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

2.2%

6.7%

6.4%

5.4%

4.7%

3.2%

Hig

h Y

ield

Bon

ds0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%1.

9%C

onve

rtib

le B

onds

0.0%

0.0%

0.0%

0.0%

2.6%

5.6%

6.3%

5.2%

4.3%

3.5%

2.6%

1.7%

Cat

Bon

ds0.

0%0.

0%0.

0%1.

2%4.

8%9.

1%11

.4%

12.3

%12

.5%

10.8

%10

.2%

10.2

%H

edge

Fun

ds0.

0%0.

0%3.

7%7.

5%8.

6%10

.0%

10.7

%10

.6%

10.3

%8.

8%7.

9%7.

6%Pr

ivat

e Eq

uity

18.9

%13

.8%

10.6

%8.

5%7.

1%5.

1%4.

0%3.

2%2.

9%2.

5%2.

1%1.

8%R

EIT

s0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%C

omm

oditi

es0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%M

icro

finan

ce d

ebt

0.0%

24.2

%37

.8%

43.9

%45

.0%

46.2

%46

.1%

43.8

%41

.4%

35.0

%30

.6%

28.6

%

Ret

urn

p.a.

11.5

9%9.

87%

8.68

%7.

93%

7.39

%6.

70%

6.26

%5.

77%

5.42

%4.

86%

4.39

%4.

12%

Ris

k p.

a.25

.42%

19.3

4%15

.33%

12.9

6%11

.31%

9.36

%8.

24%

7.13

%6.

41%

5.36

%4.

52%

4.13

%

Shor

tfal

l in

year

s13

.00

10.3

88.

447.

226.

345.

284.

694.

133.

783.

292.

862.

73

lam

bda

APPENDIX 163

Appendix– 9: Optimized portfolio weights including microfinance (qualitative approach) – risk factor set to 13.5%

0.5

0.75

11.

251.

52

2.5

3.25

45

710

Mon

ey M

arke

t USD

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

20.0

%20

.0%

20.0

%20

.0%

20.0

%E

quiti

es W

orld

0.0%

0.0%

3.4%

6.7%

8.2%

7.9%

8.2%

6.3%

6.5%

6.6%

5.8%

3.4%

Equ

ities

EM

81.1

%64

.3%

44.5

%32

.0%

24.4

%16

.3%

11.1

%8.

3%5.

4%2.

7%0.

0%0.

0%G

ov B

onds

Wor

ld0.

0%0.

0%0.

0%0.

0%0.

0%10

.9%

19.4

%16

.3%

21.8

%26

.3%

31.9

%37

.5%

Gov

Bon

ds In

flatio

n L

inke

d0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%G

ov B

onds

EM

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Cre

dit B

onds

0.0%

0.0%

0.0%

0.0%

9.2%

11.1

%9.

7%8.

2%6.

6%5.

5%2.

5%0.

5%H

igh

Yie

ld B

onds

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.5%

3.6%

5.6%

Con

vert

ible

Bon

ds0.

0%1.

7%8.

4%11

.7%

10.2

%8.

0%6.

8%5.

5%4.

7%4.

0%2.

9%1.

5%C

at B

onds

0.0%

5.3%

15.0

%20

.7%

21.8

%21

.5%

20.5

%16

.3%

15.7

%15

.2%

14.4

%14

.2%

Hed

ge F

unds

0.0%

14.5

%18

.0%

20.1

%19

.7%

18.4

%17

.2%

13.6

%12

.9%

12.3

%11

.4%

10.7

%Pr

ivat

e Eq

uity

18.9

%14

.1%

10.2

%7.

7%6.

5%5.

3%4.

7%3.

7%3.

3%3.

0%2.

6%2.

2%R

EIT

s0.

0%0.

0%0.

6%1.

1%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%C

omm

oditi

es0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%M

icro

finan

ce d

ebt

0.0%

0.0%

0.0%

0.0%

0.0%

0.6%

2.5%

1.9%

3.1%

3.9%

4.8%

4.5%

Ret

urn

p.a.

11.5

9%10

.22%

8.85

%8.

02%

7.37

%6.

46%

5.89

%5.

04%

4.71

%4.

42%

4.07

%3.

84%

Ris

k p.

a.25

.42%

20.9

3%16

.66%

14.2

4%12

.45%

10.1

2%8.

76%

6.86

%6.

14%

5.58

%5.

02%

4.73

%

Shor

tfal

l in

year

s13

.00

11.3

39.

598.

537.

726.

645.

985.

004.

594.

314.

114.

10

lam

bda

164 APPENDIX

Appendix– 10: Optimized portfolio weights including microfinance with risk fac-tor set to 10%

0.5

0.75

11.

251.

52

2.5

3.25

45

710

Mon

ey M

arke

t USD

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

12.6

%20

.0%

20.0

%20

.0%

20.0

%E

quiti

es W

orld

0.0%

0.0%

3.4%

6.9%

10.1

%12

.4%

12.3

%10

.6%

9.6%

9.5%

6.3%

3.8%

Equi

ties E

M81

.1%

64.3

%44

.5%

31.5

%22

.2%

12.0

%7.

2%4.

3%2.

4%0.

0%0.

0%0.

0%G

ov B

onds

Wor

ld0.

0%0.

0%0.

0%0.

0%0.

0%3.

4%12

.1%

14.4

%16

.0%

20.3

%27

.8%

32.7

%G

ov B

onds

Infla

tion

Lin

ked

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Gov

Bon

ds E

M0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%C

redi

t Bon

ds0.

0%0.

0%0.

0%0.

0%2.

5%7.

3%5.

9%4.

6%3.

8%3.

2%0.

6%0.

0%H

igh

Yie

ld B

onds

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

2.4%

4.0%

Con

vert

ible

Bon

ds0.

0%1.

7%8.

4%11

.5%

11.6

%10

.3%

9.0%

7.3%

6.3%

5.7%

3.8%

2.2%

Cat

Bon

ds0.

0%5.

3%15

.0%

19.2

%18

.9%

18.0

%17

.1%

14.6

%13

.1%

12.6

%12

.4%

12.3

%H

edge

Fun

ds0.

0%14

.5%

18.0

%19

.4%

18.6

%17

.2%

16.0

%13

.4%

11.9

%11

.3%

10.5

%9.

9%Pr

ivat

e Eq

uity

18.9

%14

.1%

10.2

%7.

8%6.

4%5.

0%4.

4%3.

6%3.

1%2.

8%2.

3%1.

9%R

EITs

0.0%

0.0%

0.6%

1.1%

0.7%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Com

mod

ities

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Mic

rofin

ance

deb

t0.

0%0.

0%0.

0%2.

7%9.

0%14

.4%

16.0

%14

.5%

13.8

%14

.6%

13.9

%13

.2%

Ret

urn

p.a.

11.6

%10

.2%

8.8%

8.0%

7.3%

6.4%

5.9%

5.1%

4.7%

4.4%

4.1%

3.9%

Ris

k p.

a.25

.4%

20.9

%16

.7%

14.2

%12

.4%

10.2

%8.

8%7.

2%6.

2%5.

7%5.

2%4.

9%

Shor

tfal

l in

year

s13

.00

11.3

39.

598.

517.

756.

766.

145.

324.

764.

514.

334.

31

lam

bda

APPENDIX 165

Appendix– 11: Optimized portfolio weights including microfinance with risk fac-tor set to 12%

0.5

0.75

11.

251.

52

2.5

3.25

45

710

Mon

ey M

arke

t USD

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

18.1

%20

.0%

20.0

%20

.0%

20.0

%E

quiti

es W

orld

0.0%

0.0%

3.4%

6.6%

8.5%

9.7%

9.8%

7.9%

7.8%

7.7%

6.0%

3.5%

Equ

ities

EM

81.1

%64

.3%

44.5

%31

.9%

24.2

%14

.6%

9.5%

6.9%

4.2%

1.7%

0.0%

0.0%

Gov

Bon

ds W

orld

0.0%

0.0%

0.0%

0.0%

0.0%

8.6%

17.1

%15

.9%

20.0

%24

.3%

30.7

%36

.2%

Gov

Bon

ds In

flatio

n L

inke

d0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%G

ov B

onds

EM

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Cre

dit B

onds

0.0%

0.0%

0.0%

0.0%

8.6%

9.7%

8.3%

6.5%

5.6%

4.6%

1.8%

0.0%

Hig

h Y

ield

Bon

ds0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

3%3.

2%5.

1%C

onve

rtib

le B

onds

0.0%

1.7%

8.4%

11.8

%10

.3%

8.8%

7.6%

6.0%

5.3%

4.7%

3.2%

1.8%

Cat

Bon

ds0.

0%5.

3%15

.0%

20.7

%21

.5%

20.3

%19

.4%

15.7

%14

.8%

14.3

%13

.7%

13.6

%H

edge

Fun

ds0.

0%14

.5%

18.0

%20

.1%

19.6

%18

.0%

16.8

%13

.5%

12.6

%12

.0%

11.1

%10

.5%

Priv

ate

Equ

ity18

.9%

14.1

%10

.2%

7.7%

6.5%

5.2%

4.6%

3.6%

3.2%

2.9%

2.5%

2.1%

REI

Ts0.

0%0.

0%0.

5%1.

2%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%C

omm

oditi

es0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%M

icro

finan

ce d

ebt

0.0%

0.0%

0.0%

0.0%

0.8%

5.0%

6.8%

5.8%

6.6%

7.5%

7.7%

7.3%

Ret

urn

p.a.

11.6

%10

.2%

8.8%

8.0%

7.4%

6.4%

5.9%

5.1%

4.7%

4.4%

4.1%

3.9%

Ris

k p.

a.25

.4%

20.9

%16

.7%

14.2

%12

.4%

10.1

%8.

7%6.

9%6.

1%5.

6%5.

0%4.

8%

Shor

tfal

l in

year

s13

.00

11.3

39.

598.

537.

726.

635.

995.

044.

604.

334.

134.

12

lam

bda

166 APPENDIX

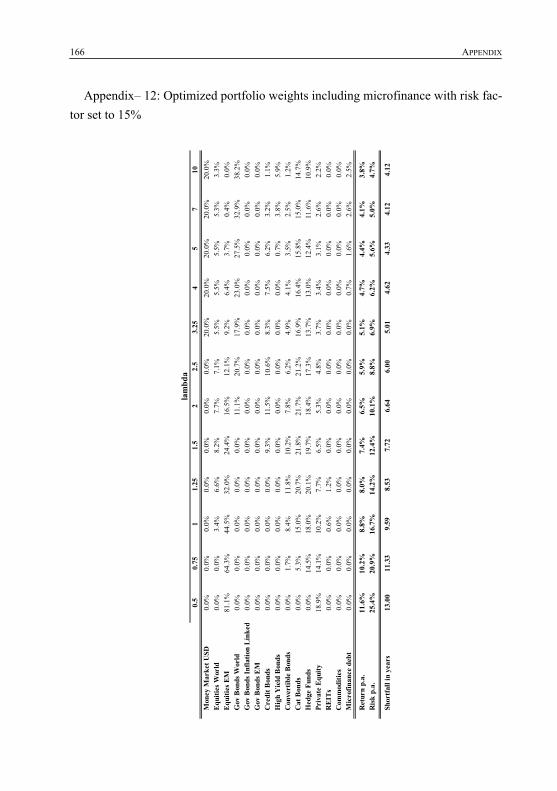

Appendix– 12: Optimized portfolio weights including microfinance with risk fac-tor set to 15%

0.5

0.75

11.

251.

52

2.5

3.25

45

710

Mon

ey M

arke

t USD

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

20.0

%20

.0%

20.0

%20

.0%

20.0

%E

quiti

es W

orld

0.0%

0.0%

3.4%

6.6%

8.2%

7.7%

7.1%

5.5%

5.5%

5.5%

5.3%

3.3%

Equ

ities

EM

81.1

%64

.3%

44.5

%32

.0%

24.4

%16

.5%

12.1

%9.

2%6.

4%3.

7%0.

4%0.

0%G

ov B

onds

Wor

ld0.

0%0.

0%0.

0%0.

0%0.

0%11

.1%

20.7

%17

.9%

23.0

%27

.5%

32.9

%38

.2%

Gov

Bon

ds In

flatio

n L

inke

d0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%G

ov B

onds

EM

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

Cre

dit B

onds

0.0%

0.0%

0.0%

0.0%

9.3%

11.5

%10

.6%

8.3%

7.5%

6.2%

3.2%

1.1%

Hig

h Y

ield

Bon

ds0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

7%3.

8%5.

9%C

onve

rtib

le B

onds

0.0%

1.7%

8.4%

11.8

%10

.2%

7.8%

6.2%

4.9%

4.1%

3.5%

2.5%

1.2%

Cat

Bon

ds0.

0%5.

3%15

.0%

20.7

%21

.8%

21.7

%21

.2%

16.9

%16

.4%

15.8

%15

.0%

14.7

%H

edge

Fun

ds0.

0%14

.5%

18.0

%20

.1%

19.7

%18

.4%

17.3

%13

.7%

13.0

%12

.4%

11.6

%10

.9%

Priv

ate

Equ

ity18

.9%

14.1

%10

.2%

7.7%

6.5%

5.3%

4.8%

3.7%

3.4%

3.1%

2.6%

2.2%

REI

Ts0.

0%0.

0%0.

6%1.

2%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%C

omm

oditi

es0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%M

icro

finan

ce d

ebt

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

0.7%

1.6%

2.6%

2.5%

Ret

urn

p.a.

11.6

%10

.2%

8.8%

8.0%

7.4%

6.5%

5.9%

5.1%

4.7%

4.4%

4.1%

3.8%

Ris

k p.

a.25

.4%

20.9

%16

.7%

14.2

%12

.4%

10.1

%8.

8%6.

9%6.

2%5.

6%5.

0%4.

7%

Shor

tfal

l in

year

s13

.00

11.3

39.

598.

537.

726.

646.

005.

014.

624.

334.

124.

12

lam

bda