bike share in small & medium-sized cities · bike share in small & medium-sized cities ......

TRANSCRIPT

Bike Share in Small & Medium-Sized Cities

John Cock Vice President, Southeast Region

TRB Tools of the Trade 2016

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

North America has Embraced Bike Share

>50 of the world’s 500+systems are in the US & Canada (not including campus systems)

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Dock-based vs. Smart Lock Systems

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Potential System Goals and Benefits

Improve public health

Reduce vehicle trips

Serve visitors and tourists

Local revenue generation

Community brand and image

Increase number of bicyclists

Meet regional air-quality/mode-share goals

Fill gaps in the transit network

Benefits of Bike Share for All Community Sizes

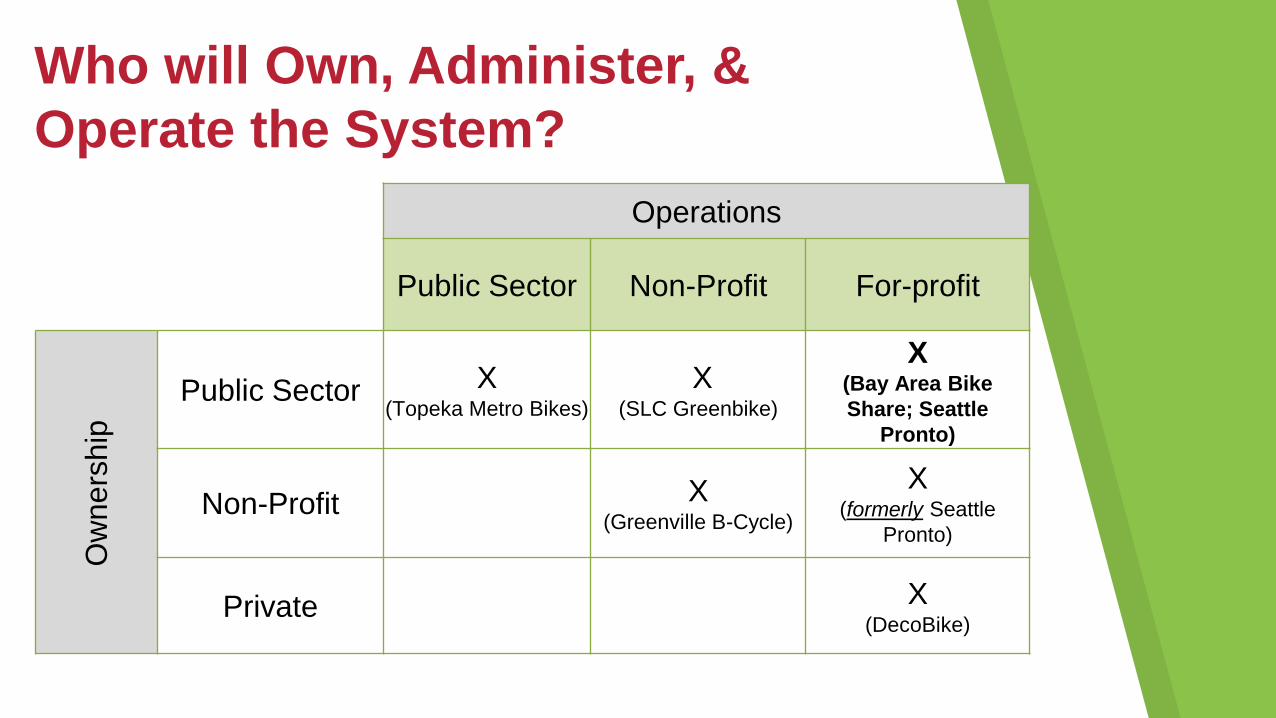

Operations

Public Sector Non-Profit For-profit

Ow

ne

rsh

ip

Public Sector X (Topeka Metro Bikes)

X (SLC Greenbike)

X (Bay Area Bike

Share; Seattle

Pronto)

Non-Profit X (Greenville B-Cycle)

X (formerly Seattle

Pronto)

Private X (DecoBike)

Who will Own, Administer, &

Operate the System?

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

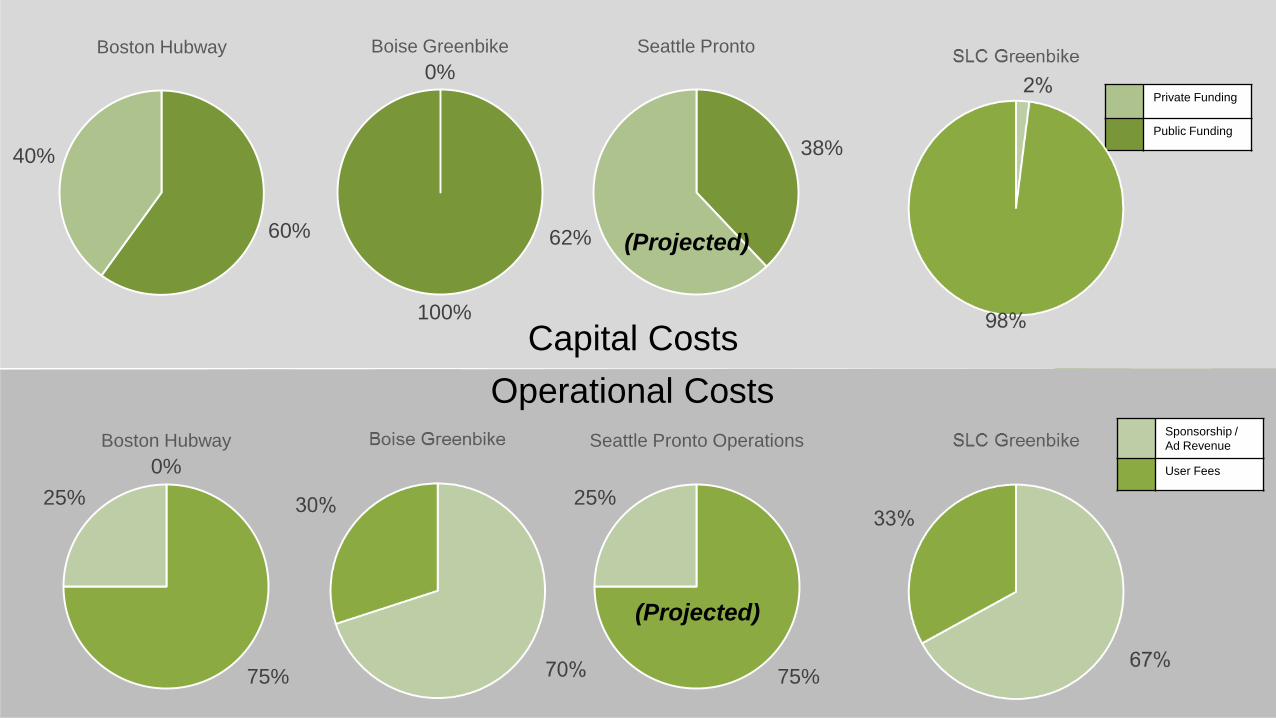

How do communities pay for it?

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

How do communities pay for it?

0%

75%

25%

Boston Hubway

60%

40%

Boston Hubway

38%

62%

Seattle Pronto

75%

25%

Seattle Pronto Operations

0%

100%

Boise Greenbike

Capital Costs

Operational Costs

Private Funding

Public Funding

Sponsorship /

Ad Revenue

User Fees

(Projected)

(Projected)

A Champion (Governmental or Non-Profit Lead)

Committed Partners

(With “skin in the game”)

Solid Funding

(Upfront costs & on-going

operations)

Bike Infrastructure

(ongoing implementation and

contiguous)

Promotional Campaign

(Inspirational and

Relatable)

Elements of a successful

bike share system

implementation

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

North America has Embraced Bike Share

>50 of the world’s 500+systems are in the US & Canada (not including campus systems)

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

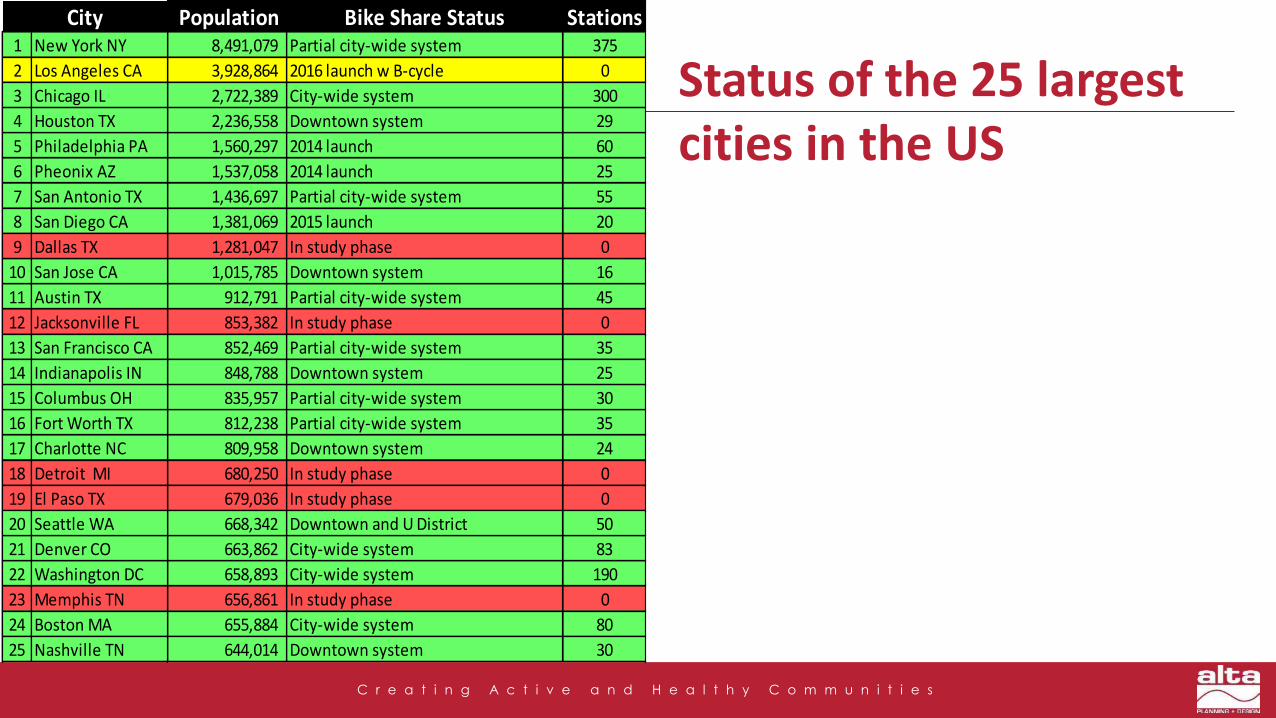

Status of the 25 largest cities in the US

Population Bike Share Status Stations1 New York NY 8,491,079 Partial city-wide system 375

2 Los Angeles CA 3,928,864 2016 launch w B-cycle 0

3 Chicago IL 2,722,389 City-wide system 300

4 Houston TX 2,236,558 Downtown system 29

5 Philadelphia PA 1,560,297 2014 launch 60

6 Pheonix AZ 1,537,058 2014 launch 25

7 San Antonio TX 1,436,697 Partial city-wide system 55

8 San Diego CA 1,381,069 2015 launch 20

9 Dallas TX 1,281,047 In study phase 0

10 San Jose CA 1,015,785 Downtown system 16

11 Austin TX 912,791 Partial city-wide system 45

12 Jacksonville FL 853,382 In study phase 0

13 San Francisco CA 852,469 Partial city-wide system 35

14 Indianapolis IN 848,788 Downtown system 25

15 Columbus OH 835,957 Partial city-wide system 30

16 Fort Worth TX 812,238 Partial city-wide system 35

17 Charlotte NC 809,958 Downtown system 24

18 Detroit MI 680,250 In study phase 0

19 El Paso TX 679,036 In study phase 0

20 Seattle WA 668,342 Downtown and U District 50

21 Denver CO 663,862 City-wide system 83

22 Washington DC 658,893 City-wide system 190

23 Memphis TN 656,861 In study phase 0

24 Boston MA 655,884 City-wide system 80

25 Nashville TN 644,014 Downtown system 30

City

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Status of the 25 largest cities in the US

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Population Bike Share Status Stations1 New York NY 8,491,079 Partial city-wide system 375

2 Los Angeles CA 3,928,864 2016 launch w B-cycle 0

3 Chicago IL 2,722,389 City-wide system 300

4 Houston TX 2,236,558 Downtown system 29

5 Philadelphia PA 1,560,297 2014 launch 60

6 Pheonix AZ 1,537,058 2014 launch 25

7 San Antonio TX 1,436,697 Partial city-wide system 55

8 San Diego CA 1,381,069 2015 launch 20

9 Dallas TX 1,281,047 In study phase 0

10 San Jose CA 1,015,785 Downtown system 16

11 Austin TX 912,791 Partial city-wide system 45

12 Jacksonville FL 853,382 In study phase 0

13 San Francisco CA 852,469 Partial city-wide system 35

14 Indianapolis IN 848,788 Downtown system 25

15 Columbus OH 835,957 Partial city-wide system 30

16 Fort Worth TX 812,238 Partial city-wide system 35

17 Charlotte NC 809,958 Downtown system 24

18 Detroit MI 680,250 In study phase 0

19 El Paso TX 679,036 In study phase 0

20 Seattle WA 668,342 Downtown and U District 50

21 Denver CO 663,862 City-wide system 83

22 Washington DC 658,893 City-wide system 190

23 Memphis TN 656,861 In study phase 0

24 Boston MA 655,884 City-wide system 80

25 Nashville TN 644,014 Downtown system 30

City Population Bike Share Status Stations26 Baltimore MD 622,793 Much-delayed 0

27 Oklahoma City OK 620,602 Downtown system 7

28 Portland OR 619,360 2016 launch w SoBi 0

29 Las Vegas NV 613,599 unknown 0

30 Louisville KY 612,780 (only available to Humana associates) 3

31 Milwaukee WI 599,642 Downtown system 10

32 Albuquerque NM 557,169 Downtown system 13

33 Tucson AZ 527,972 In study phase 0

34 Fresno CA 515,986 In study phase 0

35 Sacramento CA 485,199 In study phase 0

36 Long Beach CA 473,577 2016 launch w SoBi 0

37 Kansas City MO 470,800 Downtown system 12

38 Mesa AZ 464,704 2016 launch w SoBi 0

39 Atlanta GA 456,002 2016 launch w SoBi 0

40 Virginia Beach VA 450,890 unknown 0

41 Omaha NE 446,599 Downtown system 28

42 Colorado Springs 445,830 In study phase 0

43 Raleigh NC 439,896 In study phase 0

44 Miami FL 430,332 City-wide system 66

45 Oakland CA 413,775 Planned expansion of BABS 0

46 Minneapolis MN 407,207 City-side system 170

47 Tulsa OK 399,682 Likely expansion in 2016-17 3

48 Cleveland OH 389,521 Downtown system 11

49 Wichita KS 388,413 Coming soon 0

50 New Orleans LS 384,320 In study phase 0

City

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

What About Small Cities (<200k)?

Farg

o N

D

Salt

Lak

e C

ity

UT

Gre

en

ville

SC

Top

eka

KS

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

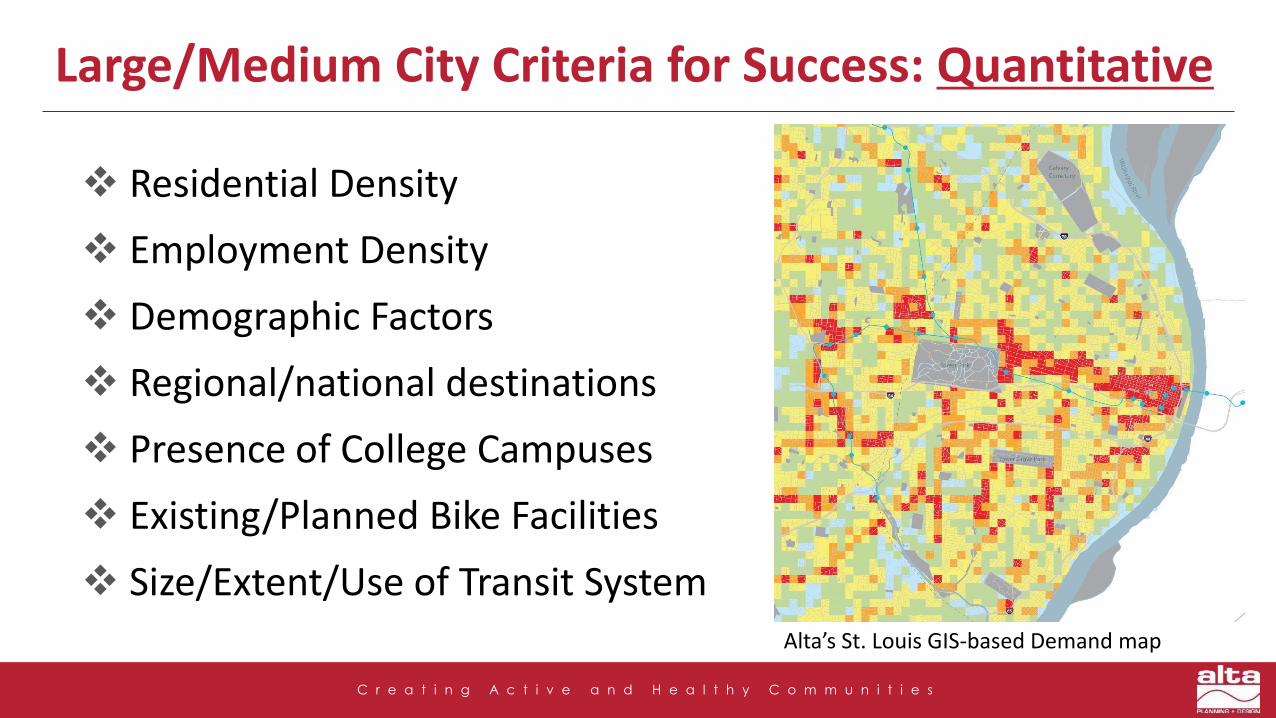

Large/Medium City Criteria for Success: Quantitative

Alta’s St. Louis GIS-based Demand map

Residential Density

Employment Density

Demographic Factors

Regional/national destinations

Presence of College Campuses

Existing/Planned Bike Facilities

Size/Extent/Use of Transit System

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria for Success: Quantitative

Residential Density

Employment Density

Demographic Factors

Regional/national destinations

Presence of College Campuses

Existing/Planned Bike Facilities

Size/Extent/Use of Transit System

X X

X

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Large/Medium City Criteria for Success: Qualitative

Land use and/or infrastructure barriers

Topography

Expense/availability of parking

Barriers to bicycle ownership/storage

Strength of local car culture

Nearby recreational areas with strong

trail connections

Region’s “Primary market” (media and

potential sponsors)

Alta’s St. Louis barriers analysis map

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria for Success: Qualitative

Land use and/or infrastructure barriers

Topography

Expense/availability of parking

Barriers to bicycle ownership/storage

Strength of local car culture

Nearby recreational areas with strong

trail connections

Region’s “Primary market” (media and

potential sponsors)

X

X

Source:

Greenbikeslc.org

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria to Leverage for Success

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Recreational Areas

Region’s Primary Market

Topography

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria to Leverage for Success

Fargo ND Great Rides

• 100 bikes/11 stations • 100,000 rides in six months • >90% of 2,800 users were

students (no cost membership)

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Recreational Areas

Region’s Primary Market

Topography

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria to Leverage for Success

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Topography

Recreational Areas

Region’s Primary Market

Salt Lake City GREENbike

• 150 bikes/20 stations • 46,000 trips in 2014 • Expansion to 100 stations by

2020 is in the works

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria to Leverage for Success

Greenville SC B-Cycle

• 80 bikes/8 stations • 85% of trips by casual users • Highest use: rec/exercise trips

from the YMCA station and along the Swamp Rabbit Trail

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Recreational Areas

Region’s Primary Market

Topography

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

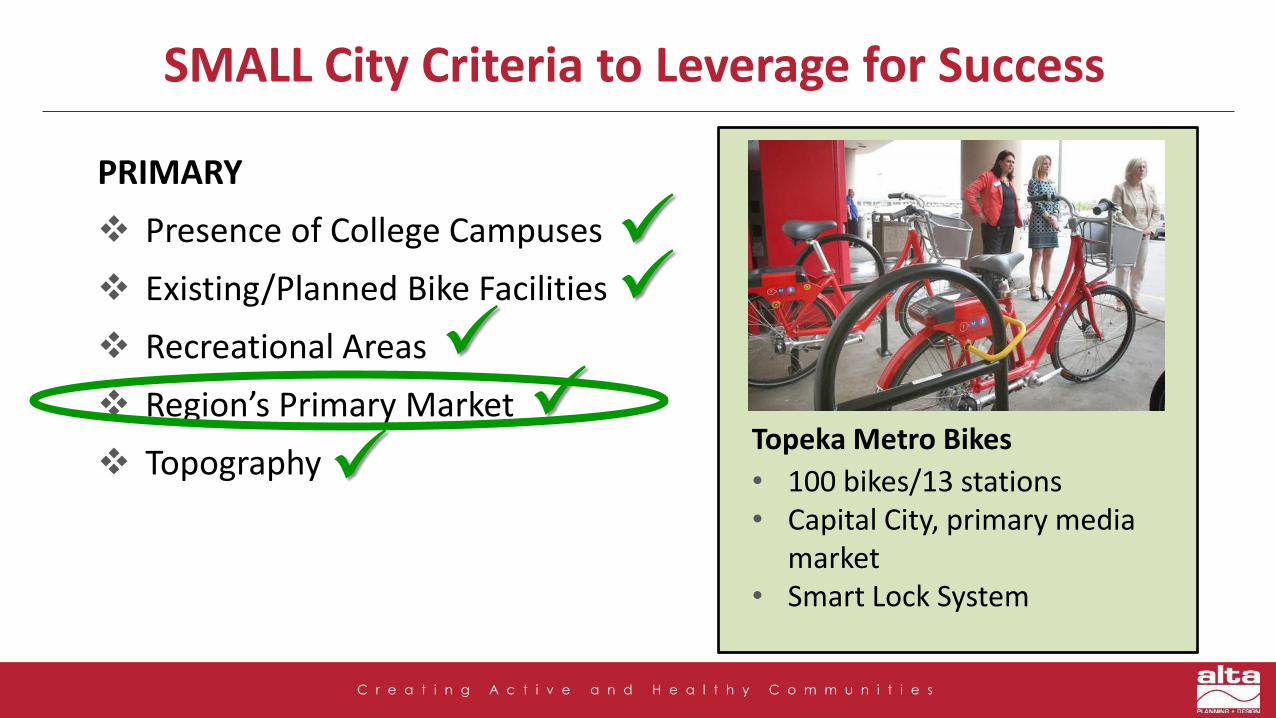

SMALL City Criteria to Leverage for Success

Topeka Metro Bikes

• 100 bikes/13 stations • Capital City, primary media

market • Smart Lock System

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Recreational Areas

Region’s Primary Market

Topography

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria to Leverage for Success

Topeka Metro Bikes

• 100 bikes/13 stations • Capital City, primary media

market • “FLAT AS A PANCAKE”

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Recreational Areas

Region’s Primary Market

Topography

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Other Intangibles for Small City Success

Capitalize on lower-cost equipment

Potential of successful non-profit

governance?

Easier permitting and deployment

Simplicity of rebalancing operations

Higher probability of replacing car trips

with bike trips

Plan for a dense network of stations

(over city-wide dispersal)

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

Plan for a Dense Network of Stations

Salt Lake City GREENbike

Ridership has nearly

tripled since 2013

Averages 2.5 daily trips

per bike, (higher than

many larger cities)

After NYC, the densest

network of stations in

North America

C r e a t i n g A c t i v e a n d H e a l t h y C o m m u n i t i e s

SMALL City Criteria to Leverage for Success

PRIMARY

Presence of College Campuses

Existing/Planned Bike Facilities

Recreational Areas

Region’s Primary Market

Topography

Small City Intangibles