binasat communications not rated -...

TRANSCRIPT

IPO Note

08 January 2018

PP7004/02/2013(031762) Page 1 of 12

Binasat Communications Not Rated Connecting Earnings

IPO Price : RM0.46 Target Price : RM0.46-RM0.58

By Cheow Ming Liang l [email protected]; Lye Zhen Xiong l [email protected]

Binasat Communications Berhad (BINACOM) will be raising RM39.6m with a market capitalisation of RM119.6m. The proceeds arising from the IPO is mainly for setting up a teleport, enhancing operational efficiency and regional expansion. With nearly half of its turnover on average derived from recurring income, this will provide earnings certainty during the contracts’ duration. With a targeted PER range of 11.7x-14.5x, we have derived our fair value range of RM0.46-RM0.58.

BINACOM - telecommunication support services specialist with a proven track record in supporting services across satellite, mobile and fibre optics networks. With the group’s edge of having diverse capabilities, it has become a strong telecommunication networks supporting services partner to MAXIS, U Mobile and HUAWEI.

Dominate market share. The group is currently servicing c.1,750 VSAT (Very small Aperture Terminal) ground stations installed at petrol stations, 4,500 overall VSAT ground stations, and 11,000 mobile BTS sites, representing a market share of 57%, 64% and 28% in the respective area. Note that, VSAT is generally a two-way satellite ground station with a dish antenna that is usually less than three meters in diameter. It is mainly used to connect remote sites for specific industries, applications or geographic areas.

Recurring Income for sustainability. The group’s recurring income makes up of c.49% of total revenue on average, widely owing to its operations and maintenance services for the satellite (including uplink and downlink services), mobile and fibre-optic segments. The recurring income contracts’ duration, however, appears short as it merely comes in at an average 1-4 years.

Fund raising for future expansion. BINACOM expects to raise RM39.6m based on 86.0m new shares at IPO price of RM0.46/share. The IPO proceeds will be utilized mainly for funding of new teleport facility, which could give rise to new satellite services offerings while reducing internal reliance on overseas satellite downlink services. Likewise, existing O&M and fibre optics services capability will be enhanced through establishment of new warehouse, R&D facilities as well as procurement of new vehicles and equipment.

Earnings forecast. Although half of BINACOM’s earnings depends on telecom projects flow (which tends to fluctuate), we expect the group’s top-line to perform better than the country’s GDP growth in FY18. However, its staff costs and depreciation are expected to trend higher in tandem with the higher project flow coupled with more assets acquired. All in, we expect the group’s net profit to grow by 3% in FY18 (to RM10.3m) on the back of 6.8% YoY climb in revenue coupled with similar GP margin of 37%. Although management has yet to outline the dividend policy, we expect BINACOM to continue rewarding its shareholders. By assuming a similar dividend pay-out ratio of c.20% (similar to FY17) in FY18, BINACOM is expected to declare a DPS of 0.8 sen, translating into 1.7% dividend yield.

Target price of RM0.46-RM0.58 based on targeted blended PER range of 11.7x-14.5x. We have decided to use the blended PER basis to better reflect the group’s business nature as the mobile segment tends to enjoy higher PER post listing. Thus, with a segmental mix of 60%/40% ratio (60% on non-mobile (i.e. VSAT, which should be value based on the FBMSC’s valuation) and 40% on the mobile segment), we have derived a blended PER of 11.7x-14.5x (implied a targeted fair value of RM0.46-0.58 range) for BINACOM.

Risks to our call include: (i) higher-than-expected project flows and margins, and (ii) impact from the on-going spectrum reallocation plan.

Share Price Performance

KLCI 1,779.45 YTD KLCI chg 8.4% YTD stock price chg n.a.

Major Shareholders

Na Boon Aik 25.8% NA Boon Tiam 25.8%

IPO proceeds (RM’m)

CAPEX 25.6 Working cap 10.8 Estimated Listing expenses 3.2 Total 39.6

Summary of IPO

Enlarged Share Cap (m) 260.0 IPO Price (RM) 0.46 Market Cap Upon Listing (RM’m) 119.6

Summary Earnings Table

FY Jun (RM‘m) 2016A 2017A 2018E

Turnover 46.4 54.5 58.2 EBIT 9.9 13.9 14.4 PBT 9.7 13.7 14.2 Net Profit (NP) 7.2 10.0 10.3 Core NP 7.2 10.0 10.3 Consensus (CNP) n.a. n.a. n.a. Earnings Revision n.a. n.a. n.a. Core EPS (sen) 7.2 10.0 10.3 Core EPS growth (%) 52% 40% 3% NDPS (sen) 2.3 1.1 0.8 BV/Share (RM) 0.1 0.1 0.3 Core PER (x) 6.4 4.6 4.4 Price/BV (x) 4.7 3.2 1.6 Net Div. Yield (%) 5.0 2.5 1.7

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 2 of 12

BACKGROUND & BUSINESSES

Binasat was incorporated in Malaysia as a private limited company in 2000 under the name NCR Computer Forms Sdn Bhd for the marketing and trading of pre-printed computer forms. The two founding shareholders are Na Bon Tiam and Kee Wei Loang. Na Boon Aik subsequently acquired all of Kee Wei Loang’s shares in the company in 2002. In 2004, the company ceased the pre-printed computer forms business activity and changed the company’s name to BINASAT on 16 February 2004.

Na Bon Tiam was also the owner of Binacom Telesystem, a sole proprietorship founded in 1999. It was engaged in providing supporting services for satellite networks, including installing satellite TVRO systems for hotels, condominiums, embassies and other premises. It was also engaged by Via Communication Network Sdn Bhd to install one-way satellite modems (downlink only) in Peninsular Malaysia. In early 2000, Binacom Telesystem secured a project from Communication and Satellite Services Sdn Bhd to install and commission VSAT (Very small Aperture Terminal) ground stations at the Selangor Turf Club, Penang Turf Club and Perak Turf Club. In 2002, Binacom Telesystem secured a project from Baycom Sdn Bhd to provide installation and commissioning services for VSAT ground stations in Malaysia.

As Binacom Telesystem grew in size, Na Bon Tiam decided to transfer its business from a sole proprietorship to a private limited company, namely BINASAT. As a result, in 2004 Binacom Telesystem transferred its entire business of providing satellite network installation and commissioning services by transferring all assets, liabilities, customers and contracts from Binacom Telesystem to BINASAT. Binacom Telesystem was terminated in 2005.

Since commencing business, Binasat has established itself as providers of supporting services for the three major telecommunications network mediums in Malaysia, namely satellite, mobile and fibre optic telecommunications. The group provides these services to the major Telcos in Malaysia, either directly or indirectly through equipment suppliers.

Binasat Communications had on 5 June 2017 entered into three conditional share sale and purchase agreements to acquire the entire issued share capital of Binasat and Binasat Sabah as well as 70% of the issued share capital of Satellite NOC for RM17.4m from the respective Binasat vendors, Binasat Sabah Vendors and Satellite NOC vendors. Subsequently, on 21 June 2017, Binasat Communications was converted into a public limited company under the name of Binasat Communications Berhad (BINACOM) to embark on the listing on the ACE Market of Bursa Securities.

Group Structure

Source: Company

BINACOM principal activity is investment holding. Through its subsidiaries, the group is mainly involved in three business segments, namely: (i) satellite network servicing, (ii) mobile network servicing, and (iii) fibre-optic network servicing.

For satellite networks, the group provides installation and commissioning, operations and maintenance, and uplink and downlink services. Installation and commissioning services involve the setting up, aligning and configuring of VSAT ground stations at sites such as petrol stations, self-service banking machines, oil palm plantations, offshore oil and gas platforms and other remote areas. They also install and commission satellite hubs and other related equipment at teleports. When required, the group also supply satellite network equipment as part of its installation and commissioning services. Operations and maintenance services involve providing scheduled and unscheduled maintenance at VSAT ground station sites, as well as operating satellite hubs. The group is also involved in providing uplink and downlink services for live telecasts for turf club, sporting and other events, and on-location news broadcasts. Note that, VSAT is generally a two-way satellite ground station with a dish antenna that is usually less than three meters in diameter. It is mainly used to connect remote sites for specific industries, applications or geographic areas.

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 3 of 12

Business Overview: Satellite Network

Source: Company

The group’s mobile network services, meanwhile, is mainly involved in the installation and commissioning of mobile network equipment and provision of scheduled and unscheduled maintenance services at BTS. For the operations and maintenance services for BTS sites in Malaysia, the group’s market share is estimated to be at 28%.

Business Overview: Mobile Network

Source: Company

The fibre-optic network supporting services involved installation and commissioning, where the group lays fibre-optic cables and install related network equipment. This includes installation outside of buildings (known as outside plant installation), and within buildings (known as inside plant installation). The group also provide operations and maintenance services for fibre-optic network equipment. In addition, the group is engaged by a Telco to provide call centre services involving technical support for its international gateway customers.

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 4 of 12

Business Overview: Fibre Optics Network

Source: Company

IPO DETAILS

Raising RM39.6m. BINACOM will be issuing 86.0m new shares at RM0.46/share where allocation for institutional offering is at 69.7%, whilst retail at 30.3%. Based on IPO price, implied market capitalisation is at RM119.6m which we classify as within the small mid-cap space.

Private placement of 40.0m existing shares. In addition to the newly issued shares, BINACOM’s promoters will privately place out 40.0m existing shares to selected eligible investors.

New share issuance and offer for sale

Categories Number of shares

(‘m) % of new shares % of enlarged share cap

Retail offering

Malaysian Public (for ballot) 6.5 7.6% 2.5%

Bumi allocation (for ballot) 6.5 7.6% 2.5%

Eligible directors and employees 13.0 15.1% 5.0%

Institutional offering 60.0 69.7% 23.1%

Total 86.0 100.0% 33.1%

Existing shares Offer for sale 40

15.4%

Source: Company

Utilisation of IPO proceeds and IPO timeline. With the fund raised, main bulk of the IPO proceeds will be allocated for CAPEX (65%) comprising of: (i) establishing a teleport station, (ii) improving on existing maintenance service and fibre network capabilities, and (iii) to fund the group’s regional expansion with emphasis towards Vietnam, Myanmar and Laos. Beyond this, 27% would be utilised for working capital needs with the balance (8%) of the proceeds allocated for the listing expenses of the IPO. The closing date for shares subscription was on 26

th December 2017, while the listing is on 8

th January 2018.

Utilisation of IPO Proceeds

Details Estimated timeframe

for utilisation RM’m % Setting up a teleport Within 24 months 14.4 36.3% Enhancing operations and maintenance services capability Within 12 months 4.9 12.4% Enhancing fibre optic network capability installation and commissioning service capability Within 12 months 4.8 12.1% Regional business expansion particularly into Vietnam, Myanmar and Laos Within 18 months 1.5 3.8% Working capital Within 24 months 10.8 27.3% Estimated listing expenses Within 3 months 3.2 8.1%

39.6 100%

Source: Company

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 5 of 12

Breakdown of Proceeds for setting up a teleport

Details Projected Capital Expenditure (RM m)

Land purchase and construction of teleport building 10.5 Purchase of satellite uplink and downlink network equipment 2.0 Purchase of high-definition DSNG system 1.5 Purchase of satellite dish (transmission and reception) 0.3 Purchase of satellite TVRO systems 0.1

Total 14.4

Source: Company

INVESTMENT MERITS

Telecommunications supporting service's specialist with the proven and established track record. BINACOM has been in the telecommunication network supporting services for 13 years, and carry with it a proven track record of serving customer in the ICT industry, including major telcos in Malaysia (either directly or indirectly through equipment suppliers), and equipment suppliers. Such achievement is largely attributed to BINACOM’s network of experienced in-house technical personnel coupled with management team’s strategic direction. Besides, as a provider of maintenance services for telecommunications networks, the group have a total 264 technical personnel stationed in all states in Malaysia to provide quality service in a timely manner. The group’s experienced in-house technical personnel have undergone relevant job training, and possess the appropriate certifications such as the CIDB green card and working at heights competency card.

Edge from service offerings across three different network mediums. Presently, BINACOM is one of the few players in Malaysia, who provides supporting services across three main telecommunication mediums namely, satellite network, mobile network and fibre-optic networks. These have resulted in the group’s strength of having diverse growth opportunity where it can address a wider potential market, thus better position its business direction. Likewise, such capabilities also provide the ability of risk mitigation by removing over dependency on any one telecommunication medium. In the event of an industry slowdown on any one medium, other mediums could still support the sustainability of BINACOM’s business.

Leading satellite network's service provider. BINACOM’s accumulated experience from handling satellite networks has enabled the group to offer a wide range of satellite services, including installation and commissioning, operations and maintenance, and uplink and downlink services. As of mid-November 2018, BINACOM has provided operations and maintenance services for approximately 4,500 VSAT ground stations (of which c.1,750 are VSAT ground stations at petrol stations) and c.10,500 BTS sites for mobile networks. As at October 2017, BINACOM’s market share for the maintenance of satellite ground stations at petrol stations in Malaysia is estimated at 57%.

Recurring Income for sustainability. The group’s recurring income makes up of c.49% of group’s total revenue on average, widely owing to its operations and maintenance services for the satellite (including uplink and downlink services), mobile and fibre-optic segments. The table below summarised the contracts that have recurring income in nature. All in, while these contracts are renewable (subject to the level of performance and pricing, as well as resource capability), it has provided the group with some assurance of cash flow during such contract periods.

Contracts with Recurring Income

Type of Services Network Medium Number of Contracts Contract Duration

Operations & Maintenance Satellite 4 1-2 years

Mobile 4* 1-2 years

Fibre Optic 1 1-2 years

Uplink & Downlink Services Satellite 4 3-4 years

* One of the contracts for mobile network also includes O&M services for fibre optic networks Source: Company

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 6 of 12

FUTURE PLANS & STRATEGIES

Setting up new teleport facility. BINACOM plans to construct a new teleport facility in Klang Valley, in order to expand its range of in-house solutions into satellite downlink services for video content and managed satellite network services for VSAT ground station. IPO proceeds amounting to RM14.4m is allocated towards funding the construction and purchase of land for the teleport site. With an expected construction period of 12-15 months, BINACOM aims to begin the construction by second half of 2018 and operationalized the facility by fourth quarter of 2019. Overall, we believe BINACOM would benefit from the facility with more satellite network service offerings to customers while reducing internal reliance on overseas service providers for satellite downlink services.

Enhancing existing capabilities. BINACOM intends to enhance its O&M (Operations and Maintenance) services and fibre optic services capabilities by investing into new warehouse/workshop facilities, R&D facilities as well as the procurement of new vehicles and equipment amounting to RM9.7m from the IPO proceeds. Such investments are made as BINACOM aims to substitute its leased storage facilities with permanent warehouse set up in EM, to replace its aging fleets as well as to develop in-house civil works capabilities for underground & above ground installation and fibre optic cable splicing instead of having to outsource them. With the improved in-house resources, the group is set to improve its operational efficiency further.

Looking to expand into regional countries. BINCOM plans to expand into regional countries, particularly into Vietnam, Myanmar and Laos to grow its business moving forward. RM1.5m of IPO proceeds is allocated to support the expansion where BINACOM’s representative office in Vietnam and Myanmar are expected to be set up by 3Q2018, whilst Laos by 2Q2019. The penetration into new markets shall be done through strategic partnerships and/or joint collaborations with telcos, equipment suppliers, and supporting service providers in respective countries. According to market research conducted by Vital Factor Consulting, users in these markets are still underserved. Hence, the anticipated high growth potential in mobile phone subscribers and Internet users could spur demand for network supporting services. At present, the mobile penetration rate in Myanmar and Laos lies below 100 subscriptions per 100 persons, whilst Internet users as percentage of populations in all three countries are well below 100%. While we believe that these new markets will provide further income streams, we do not foresee any contributions in the near term given the preliminary stages of these negotiations with BINACOM’s partners in addition to further time required for implementation.

MARKET SIZE AND SHARE

Dominant market share. In view of limited substantiated data on market size of BINACOM’s business space, Vital Factor Consulting settled to gauge aforementioned market size with the use of following measurements; which are maintenances of VSAT ground station at petrol station, maintenance of overall VSAT ground station and maintenance of active infrastructure at BTS sites in Malaysia. Hence, with BINACOM currently servicing approximately 1,750 VSAT ground station installed at petrol station, 4,500 overall VSAT ground station, and 11,000 mobile BTS sites; Vital Factor analysis estimated BINACOM’s current market share to be 57%, 64% and 28%, respectively. In view of the dominant market share, BINACOM is indeed one of the leaders in its areas of service, particularly on the satellite network.

INDUSTRY OUTLOOK

Riding on general economic factors and technological advancement. According to the research firm Vital Factor Consulting, prospect of telecommunication supporting service's provider is expected to be underpinned by healthy GDP growth (at CAGR of 4.8% during 2017-2021) and moderate population growth of c.1.3% per annum. Moreover, technological advancement, where newer technologies are continuously being introduced into telecommunications industry could also act as a growth catalyst for greater demand in installation and maintenance services (arises from need for new equipment).

Spectrum reallocation. On-going spectrum reallocation exercise has been taken by MCMC to improve spectral efficiency and support the wireless industry. Consequently, we believe implementation of these exercises could benefit telecommunication network supporting service’s players, i.e. BINACOM as telcos could engage them to carry out network equipment recalibration work, and to install and commission new network equipment.

Government Initiative. We believe the local telecommunication supporting service's provider will benefit from various initiatives implemented by Malaysian government that aim to drive and strengthen network connectivity. Aforementioned initiatives are Universal Service Provision (USP) that aims to provide telecommunication services access to remote and sparsely populated areas of Malaysia as well as 11

th Malaysia Plan that aspired to improve coverage, quality and affordability of digital infrastructure

through deployment of the High-Speed Broadband 2 and Suburban Broadband plans. In addition, under Budget 2018, RM1.0b has been allocated to develop infrastructure and broadband facilities in Sabah and Sarawak. Stemming from these initiative's implementation, we expect increased developmental activities in the telecommunication industries, thus subsequently give rise to greater needs of telecommunication supporting services in the short to medium term.

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 7 of 12

RISKS

High dependency on major customers. Currently, at least c.70% of the group’s revenue is dependent on three major customers, namely Maxis, U Mobile and Huawei. While we do not expect the loss of these customers in the short-to-medium term given the length of their relationships as well as the contractual nature of services rendered, the non-renewal of service contracts with these customers would negatively affect the group’s financial performance.

Major clients Client name Revenue contribution FY14 FY15 FY16 FY17 RM’m % RM’m % RM’m % RM’m % Maxis 25.5 80.0% 23.3 59.1% 26.9 58.0% 27.0 49.6%

Huawei 4.1 12.8% 5.9 15.0% 14.0 30.1% 14.3 26.2%

Others 2.2 7.2% 10.2 25.9% 5.5 11.9% 13.2 24.2%

Total Revenue 31.8 100.0% 39.4 100.0% 46.4 100.0% 54.5 100.0%

Source: Company

High dependency on major suppliers. In its day-to-day operations, the group sources bulk of its satellite network equipment from a single supplier, making up c.25-50% of total group purchases between FY14-17. Due to this high dependency, we believe any disruption in operations experienced by this supplier could interrupt the group’s supply chain and could affect project delivery.

Risk of frame agreement as business contracts. Owing to segment’s norm, a majority of BINACOM’s material business contracts are in the form of frame agreement. While we do not expect significant loss or termination of such business contracts, the typical nature of the contracts which is non-exclusive and has no value assigned inherently give rise to uncertainty of future purchase from customers.

Rapid change in technology. The telecommunication network supporting service's segment is characterised as a fast-paced and ever-changing segment, where swift technological development influence and change customer’s requirement. In particular, the group is affected by the evolving industry standard on satellite, mobile and fibre optic network which may result customers opting to upgrade their existing infrastructure to newer and improved technologies. Therefore, the group’s future depends heavily on its ability to remain relevant by developing or enhancing its existing services to keep abreast with the latest technology advancement.

Failure to secure properties for expansion plans. With the proceeds from the IPO, the group intends purchase land for the construction of the new teleport facility in Selangor in addition to purchase a warehouse in Johor to support its fibre-optic network operations. At present, the group is in the midst of short listing the said properties, which we believe could also be pending the availability of funds. Failure to acquire suitable properties after the listing of the stock could delay the group’s expansion timeline and adversely affect the group’s forward prospects.

700MHz spectrum could potential change telcos’ capex plans. The announcement of the 700Mhz spectrum re-farming guidelines could result in the mobile incumbents reviewing their respective capex plan and reduce the number of required base stations as well as VSAT moving forward. This is due to the said spectrum having a much stronger indoor signal penetration and wider coverage that would allow Cellcos to optimise their capex, especially in the rural areas.

FINANCIAL ANALYSIS

At present, more than half of BINACOM’s earnings are dependent on the projects/contracts secured while the remaining (c.49%) is contributed by recurring revenue. Its engineering division (which mainly comprise of installation and commissioning), meanwhile, accounted for 54%/53% of the group’s FY16/FY17 turnover while the O&M division (which consist of scheduled and unscheduled maintenance and provide recurring income) contributed 40%/41%, respectively.

BINACOM’s turnover recorded a 3-year CAGR of 19.7% to RM54.5m in FY17. Besides, the group’s gross profit margin has shown an upward trend over the past four years and recorded 26.5%/29.2%/34.1%/37.7% from FY14 to FY17, which we believe was mainly driven by better economic of scale in its VSAT division. Likewise, its PBT margins also shown a similar direction and recorded 14.7%/16.3%/20.8%/25.1% from FY14 to FY17 and significantly higher as compared to one of its unlisted VSAT peers – TS Global Network S/B (at c.6%-9%).

BINACOM has released its 1Q18 numbers subsequently post the prospectus launched. The group recorded RM10.1m turnover with a net profit of RM1.5m, which made up 17% and 15% of our full-year estimates. While the quarterly contribution (to the full-financial year) appears low, we are not overly concerned on our earnings forecast for now given the group’s earnings tends to mirror the telecommunication incumbents’ performance.

On the balance sheet front, BINACOM’s current ratio stood at 2.91 times as of the end FY17, well above the business general rule of thumb of two times. Such healthy working capital position was attributed to proportionally large trade receivables and cash balances, of which suggested that BINACOM had a strong ability to meet its short-term obligation. In addition, the group’s gearing ratio has improved to 0.34x in FY17 (vs. 0.52x a year ago, following higher shareholders’ fund as a result of better retained earnings) and is set to reduce to 0.14x post listing.

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 8 of 12

Segmental Revenue Breakdown

Segment, FYE June Revenue contribution

FY14 FY15 FY16 FY17

RM’m % RM’m % RM’m % RM’m %

Satellite 18.6 58.4% 24.5 62.1% 23.0 49.6% 27.9 51.1%

- Engineering 9.3 29.3% 11.8 29.9% 11.5 24.9% 14.0 25.7%

- Operations & Maintenance 7.8 24.4% 9.7 24.5% 8.5 18.4% 10.9 20.0%

- Uplink & Downlink 1.5 4.7% 3.0 7.7% 2.9 6.3% 2.9 5.4%

Mobile 8.1 25.4% 8.1 20.5% 14.7 31.6% 15.7 28.9%

- Engineering 0.1 0.2% 2.0 5.0% 6.2 13.4% 5.3 9.7%

- Operations & Maintenance 8.0 25.2% 5.7 14.3% 8.3 18.0% 10.3 18.9%

- Others - - 0.5 1.2% 0.1 0.2% 0.1 0.2%

Fibre Optic 5.2 16.2% 6.8 17.4% 8.7 18.8% 10.9 20.0%

- Engineering 4.7 14.6% 6.1 15.4% 7.2 15.4% 9.5 17.5%

- Operations & Maintenance 0.5 1.6% 0.8 2.0% 1.6 3.4% 1.4 2.5%

Total Revenue 31.8 100.0% 39.4 100.0% 46.4 100.0% 54.5 100.0%

*Source: Company

Historical group’s income statement

FYE June FY14 FY15 FY16 FY17 1Q18

RMm RMm RMm RMm RMm

Revenue 31.82 39.44 46.43 54.52 10.15

COGS (23.38) (27.93) (30.59) (33.96) (6.18)

GP 8.44 11.51 15.84 20.55 3.98

Other Income 0.04 0.22 0.02 0.12 0.08

8.48 11.73 15.86 20.68 4.06

Administrative Exp. (2.81) (3.32) (4.70) (5.65) (1.82)

Other Op. Exp. (0.86) (1.79) (1.27) (1.15) -

EBIT 4.81 6.61 9.88 13.89 2.24

Finance Costs (0.13) (0.19) (0.23) (0.22) (0.06)

PBT 4.68 6.42 9.66 13.66 2.18

Taxation (1.31) (1.68) (2.49) (3.64) (0.58)

PAT 3.37 4.73 7.17 10.02 1.60

Attributed to:

-Owners of the Parent 3.37 4.73 7.17 10.03 1.53

-Non-controlling interests (0.00) (0.00) (0.00) (0.00) 0.07

Margin

GP 26.5% 29.2% 34.1% 37.7% 39.2%

EBIT 15.1% 16.8% 21.3% 25.5% 22.0%

PBT 14.7% 16.3% 20.8% 25.1% 21.5%

PAT 10.6% 12.0% 15.4% 18.4% 15.8%

* Source: Company

DIVIDEND POLICY

No firm dividend policy for now. BINACOM does not have any formal dividend policy presently. However, the group intends to retain adequate reserves for the future growth as well as to reward its shareholders. For FY17, the group have declared and paid a first interim single tier dividend of RM2.0m on 26 May 2017, which represents c.20% dividend payout.

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 9 of 12

EARNING PROSEPCTS

No firm order book. BINACOM does not maintain an order book due to the nature of its business in which it usually signed frame agreements with its customers, in particular, telecommunications operators and equipment suppliers for the provision of its telecommunication network supporting services. These frame agreements typically have no contract value assigned, and set out the delivery timeframes and type of services and equipment to be provided.

Mirror the big boys’ performance. In general, Malaysia’s telecommunication players tend to ramp up their capex spending in the 2H of each financial year. Thus, BINACOM which is playing a vital role of supporting the local telecommunication sector is expected to benefit from the higher project/contract flow during the said period.

Earning is expected to grow by 3% in FY18. While we do not have a firm revenue visibility in FY18 (given the group’s engineering division’s reliance on telecom projects flow, which tends to fluctuate), we do expect the group’s top-line to perform better than the country’s GDP growth (at 5%). Besides, its staff costs and depreciation are expected to trend higher in tandem with the higher project flow coupled with more assets acquired. All in, we expect its net profit to grow 3% in FY18 (to RM10.3m) on the back of 6.8% YoY climb in revenue with similar GP margin of 37%.

VALUATIONS

Thus far, the closest peer listed on Bursa Malaysia is OCK Group Bhd (OCK). Nevertheless, it is not a direct comparable given that OCK is mainly involved in the design, build, lease and maintaining mobile infrastructures (whereas BINACOM’s mobile segment merely contributed c.29% of turnover in FY17) of which regional markets accounted for 35% of the group’s total turnover in 9MCY17.

Satellite segment, meanwhile, was the largest revenue contributor to BINACOM, accounted for c.51% to the group’s total turnover as of the end FY17. Thus, we believe BINACOM’s direct comparable pees are some unlisted private companies such as Baycom S/B, Numix Engineering S/B, Scopetel S/B, SpeedCast Malaysia S/B and TS Global Network S/B.

Network supporting services players for the satellite, mobile and fibre optic networks.

I&C = Installation and Commissioning; O&M = Operations and Maintenance; U&D Serv = Uplink and Downlink Services; (1) Formerly known as IPSAT S/B; (2) Formerly known as REDtone Marketing S/B, (3) Formerly known as Broadband Satellite Solutions S/B. Source: Company, Vital Factor analysis, Kenanga Research

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 10 of 12

The average forward PER of the FBMSC usually trades at 4x to 8x discount against the FBMKLCI, based on our valuation gaps study on the mid-small caps and the big caps. Thus, in view of our index target of 1,860, which implies 16.8x/16.0x at FY18E/FY19E earnings, this suggests that the fair FBMSC forward PER is likely to fall at the 12.8x/8.8x range.

On the other hand, we understand that a listed entity (i.e. OCK) of the network supporting service provider for the mobile segment experienced forward PER (of c.17x) akin to FBMKLCI valuation post listing. As a result, we have decided to value BINACOM based on the blended PER basis to better reflect the group’s business nature.

With a segmental mix of 60%/40% ratio (60% on non-mobile (i.e. VSAT, which should value based on the FBMSC’s valuation) and 40% on the mobile segment), we have derived a blended PER of 11.7x-14.5x for BINACOM.

Based on the indicative IPO price of RM0.46, BINACOM will be listed at a forward PER of 11.3x, which is slightly below our targeted blended PER range of 11.7x to 14.5x and target price range of RM0.46-RM0.58.

APPENDIX

Key Management Team

Name Designation Background and Key Achievements

Na Boon Aik Managing Director - Appointed to Board on 6 June 2017. - Founder of Binasat that was established in 2004 - He is responsible for the Group’s overall business development which includes setting the Group’s strategic direction, formulating corporate development plan and driving business growth. - He is well recognised and is awarded with “Brand Technopreneur of the year ‘ in 2017

Na Boon Tiam Executing Director - Appointed to Board on 6 June 2017 - Founder of Binacom Telesystem established in 1999 which provides support services to satellite network, prior transferring asset to Binasat and subsequently terminated in 2005. - Founder of Binasat that was established in 2004. - He is responsible for the overall strategic management, and day-to-day operations related matters including marketing and business development, technical and customer relationship management.

Zulamran bin Hamat Chief Operating Officer - With approximately 19 years of working experience in the satellite and telecommunication industry, he is responsible for the overall operations of the Group which include project management and overseeing in-house technical personnel. - He is also a 30.0% shareholder of BINACOM’s subsidiary Satellite NOC.

Source: Company

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 11 of 12

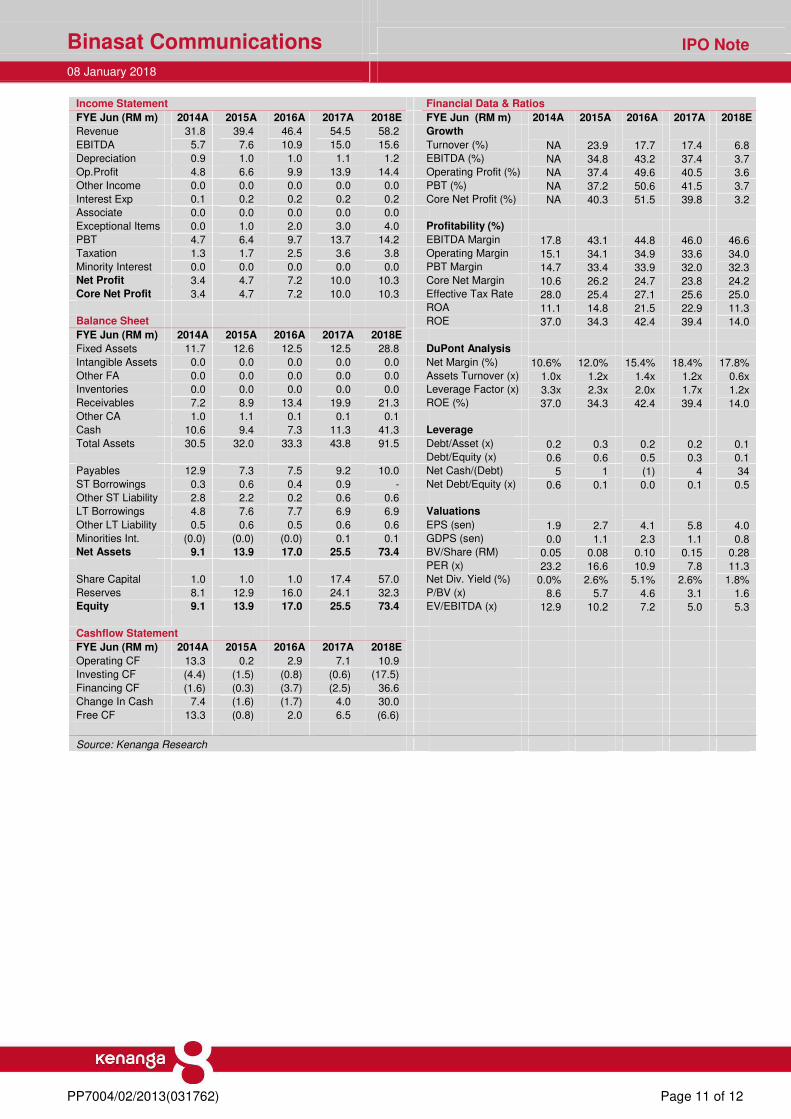

Income Statement Financial Data & Ratios

FYE Jun (RM m) 2014A 2015A 2016A 2017A 2018E FYE Jun (RM m) 2014A 2015A 2016A 2017A 2018E

Revenue 31.8 39.4 46.4 54.5 58.2 Growth

EBITDA 5.7 7.6 10.9 15.0 15.6 Turnover (%) NA 23.9 17.7 17.4 6.8

Depreciation 0.9 1.0 1.0 1.1 1.2 EBITDA (%) NA 34.8 43.2 37.4 3.7

Op.Profit 4.8 6.6 9.9 13.9 14.4 Operating Profit (%) NA 37.4 49.6 40.5 3.6

Other Income 0.0 0.0 0.0 0.0 0.0 PBT (%) NA 37.2 50.6 41.5 3.7

Interest Exp 0.1 0.2 0.2 0.2 0.2 Core Net Profit (%) NA 40.3 51.5 39.8 3.2 Associate 0.0 0.0 0.0 0.0 0.0

Exceptional Items 0.0 1.0 2.0 3.0 4.0 Profitability (%)

PBT 4.7 6.4 9.7 13.7 14.2 EBITDA Margin 17.8 43.1 44.8 46.0 46.6 Taxation 1.3 1.7 2.5 3.6 3.8 Operating Margin 15.1 34.1 34.9 33.6 34.0 Minority Interest 0.0 0.0 0.0 0.0 0.0 PBT Margin 14.7 33.4 33.9 32.0 32.3 Net Profit 3.4 4.7 7.2 10.0 10.3 Core Net Margin 10.6 26.2 24.7 23.8 24.2 Core Net Profit 3.4 4.7 7.2 10.0 10.3 Effective Tax Rate 28.0 25.4 27.1 25.6 25.0 ROA 11.1 14.8 21.5 22.9 11.3 Balance Sheet ROE 37.0 34.3 42.4 39.4 14.0

FYE Jun (RM m) 2014A 2015A 2016A 2017A 2018E

Fixed Assets 11.7 12.6 12.5 12.5 28.8 DuPont Analysis

Intangible Assets 0.0 0.0 0.0 0.0 0.0 Net Margin (%) 10.6% 12.0% 15.4% 18.4% 17.8%

Other FA 0.0 0.0 0.0 0.0 0.0 Assets Turnover (x) 1.0x 1.2x 1.4x 1.2x 0.6x Inventories 0.0 0.0 0.0 0.0 0.0 Leverage Factor (x) 3.3x 2.3x 2.0x 1.7x 1.2x Receivables 7.2 8.9 13.4 19.9 21.3 ROE (%) 37.0 34.3 42.4 39.4 14.0 Other CA 1.0 1.1 0.1 0.1 0.1

Cash 10.6 9.4 7.3 11.3 41.3 Leverage

Total Assets 30.5 32.0 33.3 43.8 91.5 Debt/Asset (x) 0.2 0.3 0.2 0.2 0.1 Debt/Equity (x) 0.6 0.6 0.5 0.3 0.1 Payables 12.9 7.3 7.5 9.2 10.0 Net Cash/(Debt) 5 1 (1) 4 34 ST Borrowings 0.3 0.6 0.4 0.9 - Net Debt/Equity (x) 0.6 0.1 0.0 0.1 0.5 Other ST Liability 2.8 2.2 0.2 0.6 0.6

LT Borrowings 4.8 7.6 7.7 6.9 6.9 Valuations

Other LT Liability 0.5 0.6 0.5 0.6 0.6 EPS (sen) 1.9 2.7 4.1 5.8 4.0 Minorities Int. (0.0) (0.0) (0.0) 0.1 0.1 GDPS (sen) 0.0 1.1 2.3 1.1 0.8 Net Assets 9.1 13.9 17.0 25.5 73.4 BV/Share (RM) 0.05 0.08 0.10 0.15 0.28 PER (x) 23.2 16.6 10.9 7.8 11.3 Share Capital 1.0 1.0 1.0 17.4 57.0 Net Div. Yield (%) 0.0% 2.6% 5.1% 2.6% 1.8% Reserves 8.1 12.9 16.0 24.1 32.3 P/BV (x) 8.6 5.7 4.6 3.1 1.6 Equity 9.1 13.9 17.0 25.5 73.4 EV/EBITDA (x) 12.9 10.2 7.2 5.0 5.3

Cashflow Statement

FYE Jun (RM m) 2014A 2015A 2016A 2017A 2018E

Operating CF 13.3 0.2 2.9 7.1 10.9

Investing CF (4.4) (1.5) (0.8) (0.6) (17.5)

Financing CF (1.6) (0.3) (3.7) (2.5) 36.6

Change In Cash 7.4 (1.6) (1.7) 4.0 30.0

Free CF 13.3 (0.8) 2.0 6.5 (6.6)

Source: Kenanga Research

Binasat Communications IPO Note 08 January 2018

PP7004/02/2013(031762) Page 12 of 12

Stock Ratings are defined as follows: Stock Recommendations OUTPERFORM : A particular stock’s Expected Total Return is MORE than 10% MARKET PERFORM : A particular stock’s Expected Total Return is WITHIN the range of -5% to 10% UNDERPERFORM : A particular stock’s Expected Total Return is LESS than -5% Sector Recommendations*** OVERWEIGHT : A particular sector’s Expected Total Return is MORE than 10% NEUTRAL : A particular sector’s Expected Total Return is WITHIN the range of -5% to 10% UNDERWEIGHT : A particular sector’s Expected Total Return is LESS than -5% ***Sector recommendations are defined based on market capitalisation weighted average expected total return for stocks under our coverage.

This document has been prepared for general circulation based on information obtained from sources believed to be reliable but we do not make any representations as to its accuracy or completeness. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may read this document. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees. Kenanga Investment Bank Berhad accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. Kenanga Investment Bank Berhad and its associates, their directors, and/or employees may have positions in, and may effect transactions in securities mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealings with respect to these companies.

Published and printed by: KENANGA INVESTMENT BANK BERHAD (15678-H) Level 12, Kenanga Tower, 237, Jalan Tun Razak, 50400 Kuala Lumpur, Malaysia Chan Ken Yew Telephone: (603) 2172 0880 Website: www.kenanga.com.my E-mail: [email protected] Head of Research