sector note who are the potential candidates -...

TRANSCRIPT

Financial Services│Banks

October 15, 2014

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. Designed by Eight, Powered by EFA

MALAYSIA BANKS

SECTOR NOTE

Who are the potential candidates for the next banking mergers? AMMB Holdings is the most likely candidate for the next bank merger based on the recent press reports stating that its major shareholder, ANZ, may have to divest its stakes in other banks to meet higher capital requirements. We also see the possibility of a merger between Public Bank (PBB) and Hong Leong Bank (HLB) due to the former’s succession uncertainties and latter’s ambition to become a bigger bank. We are positive on the potential merger between PBB and HLB given the potential merger synergies.

Figure 1: Ranking of Malaysian banks, by total asset s(end-Jun 2014)

SOURCES: CIMB, COMPANY REPORTS

We remain Underweight on banks, given the: 1) margin contraction, 2) slower loan growth, and 3) upturn in credit costs. Our base case assumes that there will not be industry-wide mergers. We will review our calls for the banks involved if they occur.

AMMB up for sale? There could be M&A activities brewing at AMMB, given the newsflow that ANZ plans to divest its stake. We think that a non-Malaysian bank entity (possibly, foreign party) is the most likely buyer for ANZ’s stake as we do not see strong strategic rationale for a bank merger.

Potential suitors for AMMB If banks are required to merge under any directive by the central bank, we think that Maybank would be the most likely suitor for AMMB due to its interest to expand in the auto financing market. Affin may be keen

but its low P/BV would be a hindrance.

Structure of PBB-HLB M&A We think that any M&A activity involving PBB and HLB would take the form of a merger, rather than an acquisition. PBB has high P/BV, which gives it strong equity “currency” to acquire, but it prefers to expand organically. HLB may be keen on acquisition but buying PBB at a valuation above its own P/BV would lead to significant EPS dilution.

Potential synergies The potential synergies from the PBB-HLB merger include: 1) optimisation of the loan-to-deposit ratio, 2) potential cost savings for the enlarged group, and 3) complementary overseas network, primarily in Greater and Indo China.

Sources: CIMB. COMPANY REPORTS

Notes from the Field

—————————————————————————————————————————

Winson NG Gia Yann, CFA T (60) 3 2261 9071 E [email protected]

Show Style "View Doc Map"

‘‘‘‘ There are now more sellers than buyers for stakes in banks.”

Tan Kong Khoon, CEO of Hong Leong Bank

Highlighted Companies

AMMB Holdings

The Edge and Starbiz stated that ANZ plans to divest its stake in AMMB to meet higher capital requirements in Australia. This would lead to M&A activities in AMMB. If ANZ’s stake is sold to a non-Malaysian banking entity, the minority shareholders would not directly benefit from the deal, although it would act as a temporary catalyst for the share price (if the acquisition price is higher than the market price). If the acquirer is another

Malaysian bank, it would lead to a bank merger and all shareholders would reap the benefits of the potential general offer.

Public Bank

The succession uncertainties may cause the major shareholders of PBB to consider a merger. A merger with HLB would be a good fit due to the similarities in the corporate cultures of both banks, which focus on tight cost and credit controls.

Hong Leong Bank

We believe that HLB has ambitious pans to expand in Malaysia, potentially via M&A. However, it is known to be disciplined in its M&As and the major shareholder/management would not tolerate significant EPS dilution. As such, we think that it would not pay a hefty P/BV of 2.8x or more (higher than its own P/BV of 1.5x) to take over PBB. Based on this, we think that any M&A involving PBB and HLB would take the form of a merger and emergence of a new entity.

Banks│Malaysia

October 15, 2014

2

Figure 2: Sector Comparison

Price Target Price

(local curr) (local curr) CY2014 CY2015 CY2014 CY2015 CY2014 CY2015 CY2016 CY2014 CY2015 CY2014 CY2015DBS Group DBS SP Hold 18.04 19.44 35,018 11.1 10.9 5.3% 1.21 1.15 11.1% 10.8% 11.2% 8.5 7.9 3.3% 3.8%OCBC OCBC SP Add 9.63 11.70 29,689 10.4 9.6 9.7% 1.41 1.14 13.0% 13.1% 12.1% 7.7 7.1 4.2% 4.3%United Overseas Bank UOB SP Hold 22.01 23.55 27,655 11.1 10.3 7.1% 1.32 1.22 12.3% 12.3% 12.4% 8.2 7.8 3.8% 4.1%Singapore average 10.9 10.3 9.5% 1.31 1.17 12.0% 12.0% 11.8% 8.2 7.6 3.7% 4.0%

Agricultural Bank of China 1288 HK Add 3.46 4.96 132,286 4.6 4.0 15.9% 0.91 0.78 21.2% 21.1% 21.1% 2.9 2.6 7.5% 8.7%Bank of China 3988 HK Add 3.53 5.03 123,454 4.6 3.9 15.2% 0.75 0.66 17.4% 18.2% 19.0% 2.8 2.4 7.6% 9.0%Bank of Communications 3328 HK Add 5.48 7.64 51,842 4.9 5.0 7.3% 0.69 0.62 14.8% 12.9% 14.0% 2.9 2.8 5.3% 5.1%China CITIC Bank 998 HK Hold 4.76 4.93 33,197 4.6 3.7 9.6% 0.70 0.61 16.2% 17.5% 16.8% 2.4 2.2 5.5% 6.8%China Construction Bank 939 HK Add 5.56 9.43 178,699 4.6 4.0 13.7% 0.89 0.77 20.8% 20.7% 20.6% 3.0 2.6 7.6% 8.7%China Merchants Bank 3968 HK Reduce 13.42 11.38 43,035 4.7 4.0 9.8% 0.86 0.74 19.3% 19.1% 19.0% 2.6 2.4 4.1% 4.8%China Minsheng Bank 1988 HK Reduce 7.31 6.17 34,236 3.9 3.9 5.5% 0.77 0.65 20.5% 18.2% 18.1% 2.3 2.3 2.3% 2.6%ICBC 1398 HK Add 4.93 7.55 206,424 4.9 4.4 9.3% 0.93 0.82 20.7% 19.8% 19.2% 3.3 2.9 7.2% 8.0%Hong Kong average 4.7 4.1 12.6% 0.85 0.74 19.5% 19.2% 19.2% 2.9 2.6 6.8% 7.8%

Bank Central Asia BBCA IJ Hold 12,675 12,500 25,602 19.9 16.5 12.8% 4.06 3.37 21.8% 22.3% 21.7% 13.9 12.3 1.0% 1.1%Bank Danamon BDMN IJ Reduce 3,955 3,500 3,106 11.7 10.0 -1.9% 1.13 1.05 10.0% 10.9% 11.4% 4.6 4.3 2.9% 2.8%Bank Mandiri BMRI IJ Add 9,650 11,750 18,447 11.8 10.3 8.7% 2.17 1.86 20.0% 19.5% 19.3% 6.7 6.0 2.4% 2.7%Bank Negara Indonesia BBNI IJ Add 5,525 5,600 8,441 10.7 9.7 8.4% 1.88 1.65 18.6% 18.1% 18.5% 6.4 5.8 2.6% 2.9%Bank Panin PNBN IJ Reduce 985 780 1,944 9.9 8.5 8.8% 1.13 1.00 11.7% 12.4% 13.0% 5.7 4.9 0.0% 0.0%Bank Rakyat Indonesia BBRI IJ Add 10,350 12,450 20,918 11.7 10.1 9.4% 2.66 2.21 25.0% 23.9% 23.6% 7.2 6.3 2.5% 2.7%Bank Tabungan Negara BBTN IJ Add 1,110 1,300 961 11.4 9.5 -6.7% 0.97 0.90 8.4% 9.8% 10.8% 5.7 4.7 4.0% 2.6%Bank Tabungan Pensiunan BTPN IJ Hold 4,500 4,250 2,153 13.1 11.3 4.9% 2.20 1.83 18.1% 17.7% 17.4% 7.6 6.7 0.0% 0.0%Indonesia average 13.3 11.5 8.8% 2.43 2.08 19.5% 19.5% 19.5% 8.0 7.1 1.9% 2.1%

Affin Holdings AHB MK Reduce 3.18 3.11 1,891 9.2 9.0 -4.7% 0.90 0.85 8.8% 9.7% 9.7% 6.6 6.5 3.8% 3.9%Alliance Financial Group AFG MK Hold 4.74 4.88 2,246 11.8 10.5 10.6% 1.64 1.53 14.4% 14.9% 15.3% 9.0 8.1 5.5% 5.7%AMMB Holdings AMM MK Hold 6.63 7.10 6,116 11.2 10.4 6.5% 1.43 1.33 13.2% 13.2% 13.4% 7.7 7.1 4.0% 4.1%BIMB Holdings BIMB MK Hold 4.25 4.50 1,943 10.2 11.0 21.3% 1.43 1.31 14.7% 12.4% 12.4% 6.0 6.5 2.9% 3.2%Hong Leong Bank HLBK MK Reduce 13.94 13.00 7,674 11.5 10.2 12.5% 1.71 1.53 15.5% 15.8% 15.5% 10.4 9.0 3.0% 3.2%Malayan Banking Bhd MAY MK Add 9.58 12.50 26,832 12.4 11.4 6.0% 1.64 1.49 13.8% 13.7% 13.5% 8.5 7.8 5.7% 6.2%Public Bank Bhd PBK MK Reduce 18.46 17.50 21,816 15.5 14.4 6.1% 2.63 2.81 18.2% 18.8% 19.9% 11.0 10.2 2.8% 3.1%Malaysia average 12.5 11.5 9.4% 1.72 1.61 14.2% 14.4% 14.5% 8.8 8.1 4.0% 4.4%

Bangkok Bank BBL TB Hold 197.0 200.0 11,571 10.4 9.4 5.7% 1.18 1.10 11.7% 12.2% 12.5% 7.0 6.4 3.9% 4.3%Bank of Ayudhya BAY TB Reduce 47.0 30.0 8,784 20.1 18.1 17.1% 2.19 1.81 11.2% 11.8% 12.1% 8.3 8.6 1.7% 1.9%Kasikornbank KBANK TB Hold 224.0 230.0 16,496 11.9 10.5 10.3% 2.12 1.84 18.8% 18.8% 18.5% 7.2 6.4 2.1% 2.4%Krung Thai Bank KTB TB Add 23.5 28.0 10,106 9.6 8.3 8.6% 1.45 1.31 15.7% 16.7% 17.2% 5.7 5.0 4.2% 4.8%Thanachart Capital TCAP TB Hold 34.8 38.0 1,290 7.2 6.6 1.9% 0.81 0.75 11.7% 11.9% 12.0% 2.0 1.9 4.0% 4.3%Tisco Financial Group TISCO TB Add 44.3 53.0 1,090 8.5 7.5 5.3% 1.39 1.25 17.0% 17.5% 18.2% 3.5 3.4 4.5% 5.2%TMB Bank TMB TB Reduce 3.0 2.5 4,059 15.4 14.2 21.9% 1.96 1.79 13.1% 13.2% 14.3% 9.4 8.0 2.3% 2.5%Thailand average 11.7 10.5 10.1% 1.62 1.45 14.4% 14.8% 15.1% 6.5 6.0 2.9% 3.2%Average (all) 5.6 5.0 12.2% 0.98 0.86 18.7% 18.5% 18.5% 3.5 3.1 5.8% 6.6%

CompanyBloomberg

TickerRecom.

Market Cap

(US$ m)

P/PPOPS (x) Dividend Yield (%)Core P/E (x) 3-year EPS

CAGR (%)

P/BV (x) Recurring ROE (%)

SOURCES: CIMB, COMPANY REPORTS

Banks│Malaysia

October 15, 2014

3

Who are the potential candidates for the next banking mergers? 1. AMMB UP FOR SALE?

1.1 Pick-up in M&A newsflow for banks

The proposed merger of CIMB Group Holdings (CIMB), RHB Capital and the Malaysian Building Society has stirred investors’ interest in the topic of bank mergers. The M&A newsflow for banks has also picked up recently. As such, we explore the bank merger possibilities in this report.

The potential M&A in the spotlight recently involved AMMB Holdings. The Edge and Starbiz reported that the major shareholders of AMMB Holdings, including ANZ and Tan Sri Azman Hashim (TSAH), are considering the sale of their stakes in the sixth-largest banking group in Malaysia. At 30 Jun 2014, ANZ and TSAH were the biggest shareholders in AMMB, with stakes of 23.8% and 14%, respectively.

Strategically, we see no reason for ANZ to divest its stake in AMMB because: 1) AMMB forms part of its regional network, 2) it has strong control over the AMMB group, with appointed personnel at the top and middle management levels, and 3) it has added value to AMMB by helping the bank to improve its risk management system and low-cost deposits, for example.

However, ANZ may have to sell its AMMB stake for capital reasons. The regulator in Australia now requires the big four Australian banks to have Tier-1 capital ratio of at least 8%. ANZ internally targets Tier-1 capital ratio of 8.5% by end-2014, despite the 15bp decline to 8.33% in 1Q14. In mid-2012, ANZ’s CEO Mike Smith said that the bank would consider selling its stakes in certain Asian banks if the Australian government did not ease its stringent capital requirements. However, he previously stated that ANZ’s partnership with AMMB was “strategic and long-term”.

We think that there is a reasonable chance that TSAH will sell down his stake in AMMB as he has taken a backseat since ANZ emerged as AMMB’s biggest shareholder in 2007. Since then, we understand that ANZ’s control of AMMB has expanded from the commercial banking unit to most of the group’s operations. Furthermore, we gather that none of TSAH’s children are involved in the running of AMMB.

If ANZ were to sell down its stake...

The Starbiz article stated that ANZ has put up its AMMB stake for sale but there has only been lukewarm interest from other Malaysian banks. To a certain extent, this supports our view that there are no strong strategic reasons for bank mergers in Malaysia, given:

The difficulties in achieving revenue synergies and the operational overlap. All banking groups in Malaysia have similar corporate structures, with exposure to almost all segments in the financial market. Certain banks, like PBB, do not have an insurance entity but this is by choice, rather than because of any restrictions. Given that the banks already have licences in all their preferred segments, it would be more cost efficient and effective to expand organically, rather than via M&A,

The unattractive returns, as reflected by the falling ROE, which was primarily caused by the declining net interest margin and higher capital requirements,

More stringent capital requirements under the BASEL III accord, which means that the banking M&As must be financed primarily by the issuance of new equity capital.

Table of Contents

1. AMMB UP FOR SALE? ................................................. 3 2. MERGER SCENARIOS FOR AMMB ............................. 4 3. WHAT ABOUT PRICING FOR AMMB? ......................... 6 4. WILL PBB AND HLB MERGE? ..................................... 6 5. IMPACT ON FINANCIALS FOR PBB AND HLB ........... 9 6. MODE OF M&A FOR PBB AND HLB ............................ 10

7. SYNERGIES FOR PBB-HLB MERGER......................... 11

8 OTHER ISSUES ............................................................. 13 9. VALUATION AND RECOMMENDATION ....................... 13

Show Style "View Doc Map"

Banks│Malaysia

October 15, 2014

4

However, we think that foreign parties would be interested to acquire the controlling stake in AMMB for the following reasons:

Exposure to Malaysia’s stable financial market,

Investment in a full-fledged banking group, with exposure to commercial, Islamic and investment banking, as well as insurance,

AMMB’s decent ROE of 13-14%,

AMMB’s strong investment banking franchise in Malaysia, especially in fixed income.

2. MERGER SCENARIOS FOR AMMB

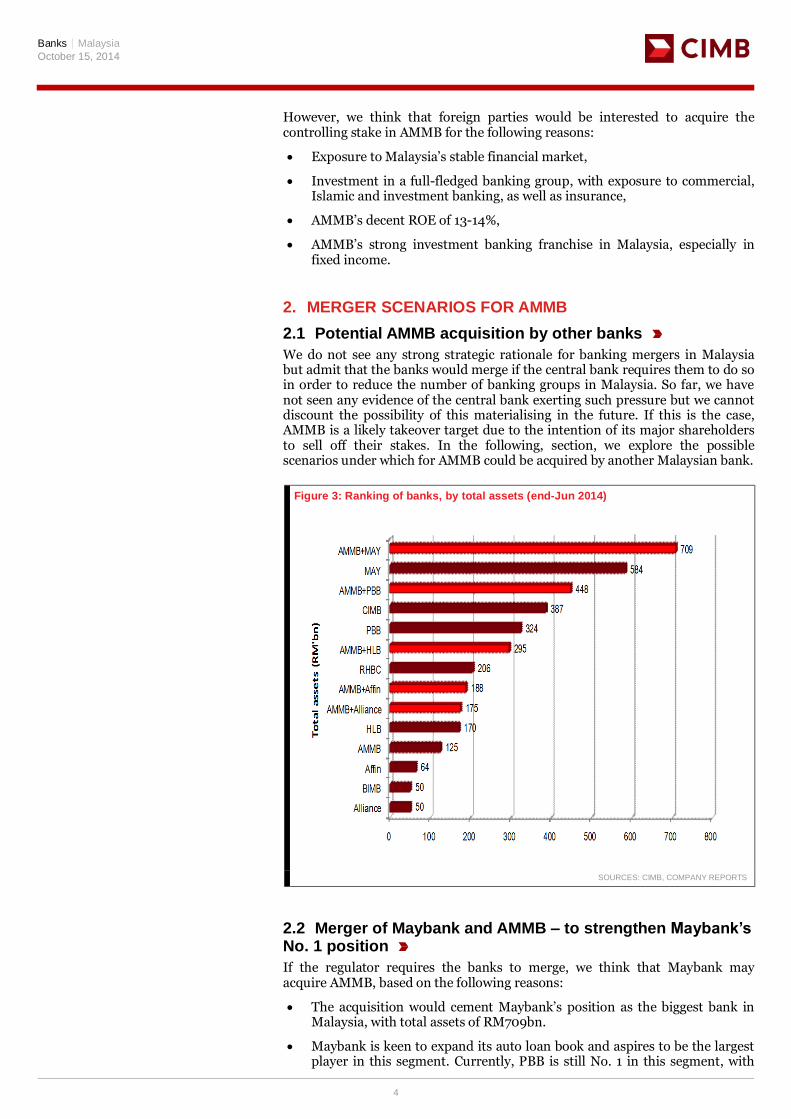

2.1 Potential AMMB acquisition by other banks

We do not see any strong strategic rationale for banking mergers in Malaysia but admit that the banks would merge if the central bank requires them to do so in order to reduce the number of banking groups in Malaysia. So far, we have not seen any evidence of the central bank exerting such pressure but we cannot discount the possibility of this materialising in the future. If this is the case, AMMB is a likely takeover target due to the intention of its major shareholders to sell off their stakes. In the following, section, we explore the possible scenarios under which for AMMB could be acquired by another Malaysian bank.

Figure 3: Ranking of banks, by total assets (end-Jun 2014)

SOURCES: CIMB, COMPANY REPORTS

2.2 Merger of Maybank and AMMB – to strengthen Maybank’s No. 1 position

If the regulator requires the banks to merge, we think that Maybank may acquire AMMB, based on the following reasons:

The acquisition would cement Maybank’s position as the biggest bank in Malaysia, with total assets of RM709bn.

Maybank is keen to expand its auto loan book and aspires to be the largest player in this segment. Currently, PBB is still No. 1 in this segment, with

Banks│Malaysia

October 15, 2014

5

total auto loans of RM46.9bn, followed by Maybank with RM29.5bn (assuming that 60% of its auto loans are from Malaysia) and AMMB with RM24bn. If Maybank takes over AMMB, its auto loan book would rise to RM53.5bn, ahead of PBB’s.

The deal would boost the size of Maybank’s insurance business, especially non-life insurance. In 2012, AMMB acquired Kurnia Insurans, the largest motor insurer in Malaysia.

Maybank would be able to tap into AMMB tie-ups with Insurance Australia Group (non-life insurance business) and Metlife (life insurance business) to improve the operations of its insurance units.

However, the acquisition of AMMB would pose problems for Maybank in the following areas:

AMMB loan-to-deposit ratio of 98.5% at end-Jun 2014 was the highest in the sector and higher than Maybank’s 90.6%. The purchase of AMMB would tighten Maybank’s liquidity position.

There are significant overlaps in investment banking, as both Maybank and AMMB are major players in this segment.

AMMB has a low current account savings account (CASA) ratio of close to 20% compared to Maybank’s mid-30%.

2.3 Merger of PBB and AMMB – low likelihood, given PBB’s focus on organic growth

The merger of PBB and AMMB would create the second-largest banking group in Malaysia, with total assets of RM448bn. However, we think that PBB would be more interested in expanding organically, rather than via acquisition. Hence, there is low likelihood of a PBB-AMMB merger. Although both PBB and AMMB are key players in the auto financing market, a merger between them would not be a good fit as they employ different strategies in this segment. Furthermore, AMMB’s high loan-to-deposit ratio would not be desirable to PBB.

2.4 Merger of HLB and AMMB – huge auto loan portfolio a major turn-off

HLB could be keener on M&A than PBB. Although HLB is price-disciplined in its M&As, AMMB’s valuation of 1.4x P/BV appears reasonable, compared to HLB’s 1.7x. The resulting entity from the merger of HLB and AMMB would be the fourth-largest bank in Malaysia, with total assets of RM295bn. However, AMMB’s high exposure to auto financing would be a major turn-off for HLB. Auto loans accounted for 28% of AMMB’s loan book, although this has declined from 40.8% at end-2009. In contrast, HLB is restrictive in its lending to the auto loan segment. For this reason, we think that there is low likelihood of HLB bidding for AMMB.

2.5 Merger of Affin and AMMB – Affin’s growth ambitions limited by its low valuation

Despite Affin’s small size relative to its peers, we think that it has the appetite to purchase another bank. Last year, Affin beat AMMB to successfully acquire HwangDBS Investment Bank. Capital-wise, we believe that its largest shareholder, Lembaga Tabung Angkatan Tentera (LTAT), supports Affin’s M&As. Affin would be interested in buying AMMB as this would triple the size of its total assets from RM63.6bn now to RM188.3bn. After the merger, the combined group would be larger than HLB.

However, Affin’s P/BV of only 0.9x, which is the lowest among the Malaysian banks and below AMMB’s 1.4x, would be a major hindrance to the merger. For

Banks│Malaysia

October 15, 2014

6

this reason, Affin would suffer significant EPS dilution if it chooses to take control of the bigger and more expensive AMMB.

2.6 Merger of Alliance and AMMB – Alliance shies away from M&As

Looking at its track record, Alliance has not been an active participant in the local banking scene’s M&As. Its strategies are to focus on extracting more value from its existing operations, sustaining its strong loan growth, limiting the impact of margin contraction and expanding its fee income. As such, we do not think that Alliance would be interested in acquiring AMMB.

3. AMMB PRICING?

What about the pricing?

Referring to Figure 4, the average P/BV for Malaysian banking M&A transactions in the past was 1.86x. However, we think that the P/BV valuation of future M&A deals will be lower due to the declining ROEs. By assuming a discount of 15%, we estimate that the target P/BV for future M&As will be 1.6x. By applying our target P/BV of 1.6x to AMMB’s RM4.36 BV/share at end-Mar 2014, we estimate that the acquisition price for AMMB would be RM7.00. This translates into potential share price upside of only 5.6%.

Figure 4: Information on previous banking M&As

Buyer Acquiree Price (RM m) P/NTA (x) P/BV (x) Year

% stake

acquired

Southern Bank Ban Hin Lee Bank 1,079 1.9 1.9 1999 100%

Maybank The Pacific Bank 1,250 1.8 1.4 2000 100%

HL Bank Wah Tat Bank 210 2.9 2.9 2000 100%

Alliance Bank International Bank Malaysia 273 2.1 2.1 2000 100%

Alliance Bank Sabah Bank 256 1.4 1.2 2000 100%

Maybank PhileoAllied Bank 1,280 1.3 1.2 2001 100%

Public Bank Hock Hua Bank 1,249 1.7 1.4 2001 100%

RHB Bank Bank Utama 1,804 2 1.9 2002 100%

Temasek Malaysian Plantations 1,120 2 1.7 2003 15%

BCB Southern Bank-pre-provisioning 6,690 2.5 1.9 2006 100%

Southern Bank-post-provisioning 2.8 2.1

ANZ AMMB 1,290 2 1.8 2007 14%

Bank of Tokyo - Mitsubishi UFJ BCH 1,334 4.2 2.7 2007 4%

BEA Affin Holdings 499 1.3 0.9 2007 20%

Primus EON Capital 1,340 2.3 2.2 2008 20%

Abu Dhabi Commercial Bank RHB Capital 3,876 4.1 2.2 2008 25%

Hong Leong Bank EON Bank 5,060 1.4 1.4 2010 100%

Aabar RHB Capital 5,815 3.8 2.2 2011 25%

Weighted avg 2.59 1.86 SOURCES: CIMB, COMPANY REPORTS

4. WILL PBB AND HLB MERGE?

4.1 Exploring the likelihood and impact of PBB-HLB merger

The idea of a merger between PBB and HLB has been bandied about the market for some time but PBB’s high valuation appears to be a major hindrance. In the following section, we explore the likelihood and impact of a merger between PBB and HLB.

Although there is no urgency for PBB or HLB to embark on any M&A initiatives, we think that there is a reasonable chance of a PBB-HLB merger because of:

The similarities between the major shareholders, both of whom are Chinese tycoons. Tan Sri Teh Hong Piow owns a 24% stake in PBB and Tan Sri Quek Leng Chan holds an effective stake of 49.8% in HLB (HLB is 63.6%-controlled by Hong Leong Financial Group, which in turn, is 78.3%-owned by Hong Leong Company, which is Tan Sri Quek’s private company),

Banks│Malaysia

October 15, 2014

7

Their similar corporate cultures, with focus on strong cost and credit control,

PBB’s succession uncertainties, as Tan Sri Teh is in his 80s and none 0f his children are involved in the running of the bank, and

The ambitions of HLB’s major shareholder to control and run a bigger bank in Malaysia.

The merger would result in Tan Sri Teh taking a back seat, while HLB and PBB’s existing management run the enlarged banking group. This would be a win-win arrangement for both parties.

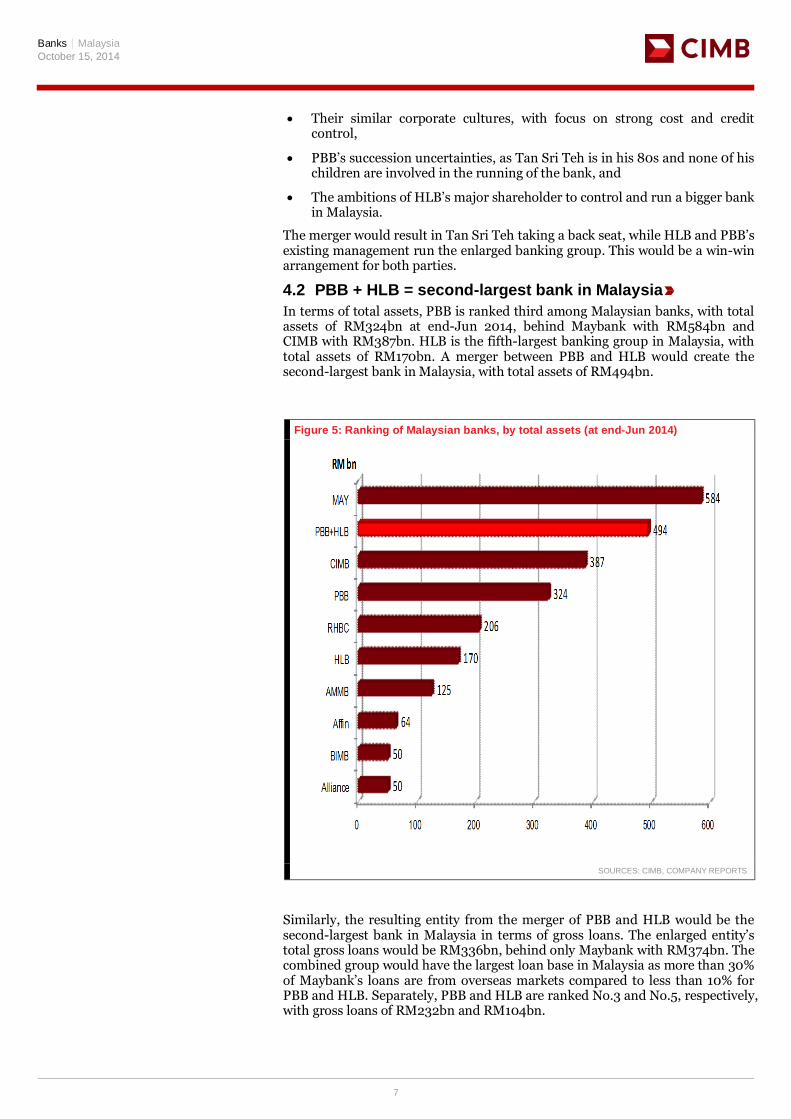

4.2 PBB + HLB = second-largest bank in Malaysia

In terms of total assets, PBB is ranked third among Malaysian banks, with total assets of RM324bn at end-Jun 2014, behind Maybank with RM584bn and CIMB with RM387bn. HLB is the fifth-largest banking group in Malaysia, with total assets of RM170bn. A merger between PBB and HLB would create the second-largest bank in Malaysia, with total assets of RM494bn.

Figure 5: Ranking of Malaysian banks, by total assets (at end-Jun 2014)

SOURCES: CIMB, COMPANY REPORTS

Similarly, the resulting entity from the merger of PBB and HLB would be the second-largest bank in Malaysia in terms of gross loans. The enlarged entity’s total gross loans would be RM336bn, behind only Maybank with RM374bn. The combined group would have the largest loan base in Malaysia as more than 30% of Maybank’s loans are from overseas markets compared to less than 10% for PBB and HLB. Separately, PBB and HLB are ranked No.3 and No.5, respectively, with gross loans of RM232bn and RM104bn.

Banks│Malaysia

October 15, 2014

8

Figure 6: Ranking of Malaysian banks, by gross loans (at end-Jun 2014)

SOURCES: CIMB, COMPANY REPORTS

The resulting entity from the merger of PBB and HLB would also be the second-largest bank in Malaysia for total deposits, with RM395bn. This is not far below Maybank, the largest with RM407bn. Individually, PBB’s total deposits of RM265bn puts it in the third position and HLB’s RM130bn puts it in the fifth position in the industry.

Figure 7: Ranking of Malaysian banks, by total deposits (at end-Jun 2014)

SOURCES: CIMB, COMPANY REPORTS

Banks│Malaysia

October 15, 2014

9

5. IMPACT ON PBB’s and HLB’s FINANCIALS

5.1 Balancing loan mix

As shown in Figure 8, both banks have high exposure to residential mortgages, which accounted for 32.2% of PBB’s total loans and 37.4% of HLB’s at end-Jun 2014. Naturally, the highest proportion of the combined group’s loan base would be residential mortgages (33.8% of total loans). However, PBB is a larger financier in the non-residential mortgages segment, which constituted a quarter of its total loans at end-Jun 2014 compared to only 11.9% for HLB. On a combined basis, the proportion of non-residential mortgages (as a percentage of total loans) would drop to around 21%. Overall, property loans would account for more than half (55%) of the enlarged PBB-HLB group’s loan portfolio.

Both banks also have big proportions of auto loans, which comprised 20.2% of PBB’s total loans at end-Jun 2014 and 16.6% for HLB. After the merger, the share of auto loans would still be a high 19.1%.

As for non-property-financing business loans, the proportion of working capital loans is larger for HLB (21.7% of total loans at end-Jun 2014) than PBB (12.9%). The share of working capital loans for the combined group would be 15.6%.

Figure 8: Breakdown of loans for PBB, HLB and the combined group

Loans (RM 'm) (end-Jun 14) PBB HLB PBB+HLB

Loans by purpose

Construction 3,374.8 1,163.0 4,537.8

Residential mortgages 74,809.6 39,000.3 113,809.9

Non-residential mortgages 58,265.2 12,370.1 70,635.3

Purchase of securities 3,855.5 762.7 4,618.2

Auto loans 46,942.5 17,292.2 64,234.7

Purchase of fixed assets 255.5 0.0 255.5

Personal use 9,081.3 3,370.7 12,452.0

Credit cards 1,580.4 4,192.2 5,772.6

Purchase of consumer durables 7.4 0.4 7.8

Working capital 30,018.8 22,573.4 52,592.2

Merger and acquisition 197.5 0.0 197.5

Others 3,770.2 3,443.6 7,213.8

TOTAL 232,158.7 104,168.6 336,327.3

Loans (RM 'm) (end-Jun 14) PBB HLB PBB+HLB

% Breakdown of loans

Construction 1.5% 1.1% 1.3%

Residential mortgages 32.2% 37.4% 33.8%

Non-residential mortgages 25.1% 11.9% 21.0%

Purchase of securities 1.7% 0.7% 1.4%

Auto loans 20.2% 16.6% 19.1%

Purchase of fixed assets 0.1% 0.0% 0.1%

Personal use 3.9% 3.2% 3.7%

Credit cards 0.7% 4.0% 1.7%

Purchase of consumer durables 0.0% 0.0% 0.0%

Working capital 12.9% 21.7% 15.6%

Merger and acquisition 0.1% 0.0% 0.1%

Others 1.6% 3.3% 2.1%

TOTAL 100.0% 100.0% 100.0% SOURCES: CIMB, COMPANY REPORTS

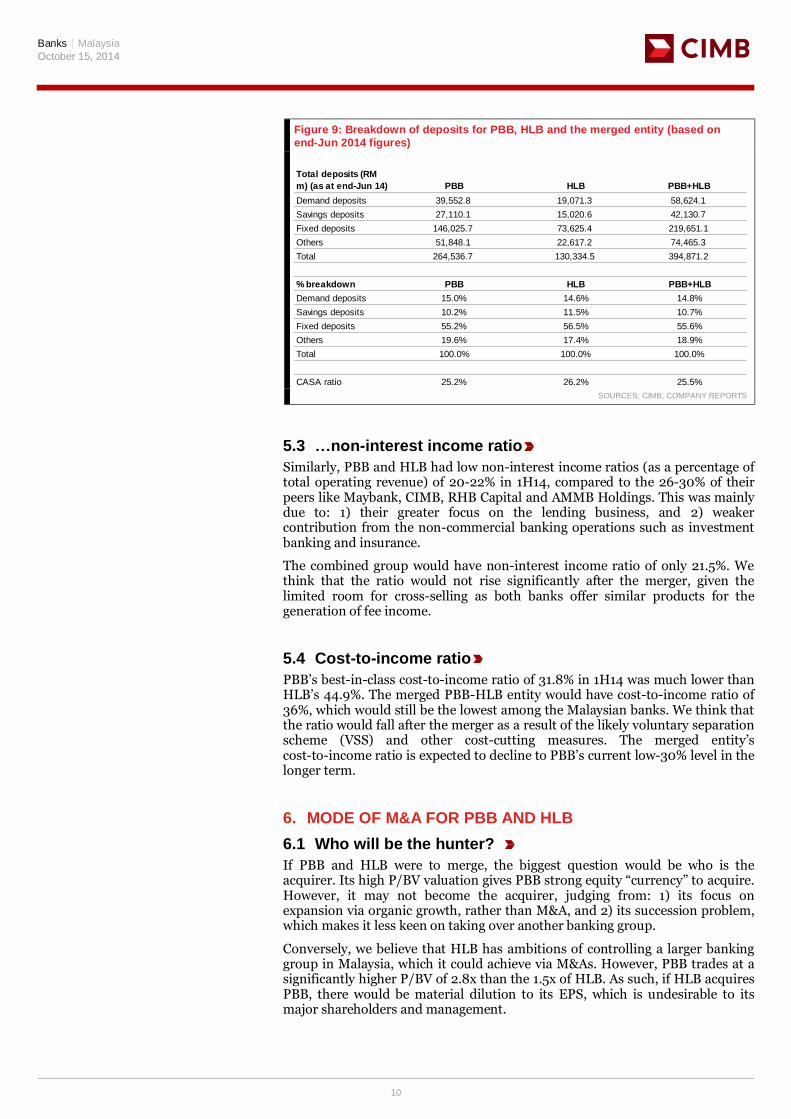

5.2 Low CASA and…

Figure 9 shows that both PBB and HLB have low current account, savings account (CASA) ratios of 25-26%. CASA are bank’s low-cost deposits. Following the merger, the combined CASA ratio would still be 25-26%. That said, the funding for the operations of PBB, HLB and PBB-HLB would primarily come from fixed deposits, which comprised 55-56% of their total deposits at end-Jun 2014.

Banks│Malaysia

October 15, 2014

10

Figure 9: Breakdown of deposits for PBB, HLB and the merged entity (based on end-Jun 2014 figures)

Total deposits (RM

m) (as at end-Jun 14) PBB HLB PBB+HLB

Demand deposits 39,552.8 19,071.3 58,624.1

Savings deposits 27,110.1 15,020.6 42,130.7

Fixed deposits 146,025.7 73,625.4 219,651.1

Others 51,848.1 22,617.2 74,465.3

Total 264,536.7 130,334.5 394,871.2

% breakdown PBB HLB PBB+HLB

Demand deposits 15.0% 14.6% 14.8%

Savings deposits 10.2% 11.5% 10.7%

Fixed deposits 55.2% 56.5% 55.6%

Others 19.6% 17.4% 18.9%

Total 100.0% 100.0% 100.0%

CASA ratio 25.2% 26.2% 25.5% SOURCES: CIMB, COMPANY REPORTS

5.3 …non-interest income ratio

Similarly, PBB and HLB had low non-interest income ratios (as a percentage of total operating revenue) of 20-22% in 1H14, compared to the 26-30% of their peers like Maybank, CIMB, RHB Capital and AMMB Holdings. This was mainly due to: 1) their greater focus on the lending business, and 2) weaker contribution from the non-commercial banking operations such as investment banking and insurance.

The combined group would have non-interest income ratio of only 21.5%. We think that the ratio would not rise significantly after the merger, given the limited room for cross-selling as both banks offer similar products for the generation of fee income.

5.4 Cost-to-income ratio

PBB’s best-in-class cost-to-income ratio of 31.8% in 1H14 was much lower than HLB’s 44.9%. The merged PBB-HLB entity would have cost-to-income ratio of 36%, which would still be the lowest among the Malaysian banks. We think that the ratio would fall after the merger as a result of the likely voluntary separation scheme (VSS) and other cost-cutting measures. The merged entity’s cost-to-income ratio is expected to decline to PBB’s current low-30% level in the longer term.

6. MODE OF M&A FOR PBB AND HLB

6.1 Who will be the hunter?

If PBB and HLB were to merge, the biggest question would be who is the acquirer. Its high P/BV valuation gives PBB strong equity “currency” to acquire. However, it may not become the acquirer, judging from: 1) its focus on expansion via organic growth, rather than M&A, and 2) its succession problem, which makes it less keen on taking over another banking group.

Conversely, we believe that HLB has ambitions of controlling a larger banking group in Malaysia, which it could achieve via M&As. However, PBB trades at a significantly higher P/BV of 2.8x than the 1.5x of HLB. As such, if HLB acquires PBB, there would be material dilution to its EPS, which is undesirable to its major shareholders and management.

Banks│Malaysia

October 15, 2014

11

6.2 Merger via creation of a newco

In this case, we think that the most feasible method is a merger that involves the injection of both PBB and HLB into a newco. This could be based on predetermined share prices for PBB and HLB on certain dates.

6.3 More balanced shareholding structure after the merger

Currently, PBB’s biggest shareholders are Tan Sri Teh Hong Piow and EPF, with stakes of 24.1% and 14.8%, respectively. Hong Leong Financial Group (HLFG) controls HLB, with majority shareholding of 64.4%, followed by EPF with 14.9%. Following the merger, the shareholding structure will be more balanced, with Tan Sri The Hong Piow owning a stake of 17.6%, HLFG holding 17.4% and EPF owning 14.8% in the merged entity. This is based on the assumption that the merger will be based on the 26 Sep 2014 closing share prices of RM18.90 for PBB and RM14.50 for HLB.

Figure 10: Shareholding structures of PBB, HLB and PBB-HLB group

Share price as at end-26

Sep 14 (RM)

PBB 18.90

HLB 14.50

Number of shares

PBB 3,882.1

HLB 1,879.9

Market capitalisation (RM m)

PBB 73,371.7

HLB 27,258.7

PBB+HLB 100,630.3

Major shareholders

% shareholding Value of shareholding

PBB (as at 27 Jan 2014)

Tan Sri Teh Hong Piow 24.1% 17,682.6

EPF 14.8% 10,859.0

HLB (as at 2 Sep 2013)

Hong Leong Financial Group 64.4% 17,554.6

EPF 14.9% 4,056.1

PBB+HLB

Tan Sri Teh Hong Piow 17.6% 17,682.6

Hong Leong Financial Group 17.4% 17,554.6

EPF 14.8% 14,915.1

Others 50.2% SOURCES: CIMB, COMPANY REPORTS

7. SYNERGIES FROM PBB-HLB MERGER

We believe that synergies would arise from the merger of PBB and HLB, apart from the strengthening presence in the retail banking space, which may not have a significant impact on financial performance. However, we stick to our view that the revenue synergies for bank mergers in Malaysia are not easily attained.

7.1 Synergy 1 – optimising the LD ratio

PBB’s liquidity position is tighter than HLB’s as PBB’s loan-to-deposit (LD) ratio was 87.1% at end-Jun 2014 compared to HLB’s 78.8%. The LD ratio for the combined group would be a more optimal 84.3%. Although this would not expand its margin, the more comfortable liquidity position would shield the group from any rate competition for deposits in the short term.

Banks│Malaysia

October 15, 2014

12

7.2 Synergy 2 – cost savings

PBB is known for its strong cost discipline, as shown by its unrivalled cost-to-income ratio of c.30%. A merger with HLB would provide opportunities to improve the operating efficiency of the enlarged group by the implementation of various cost-cutting measures. We estimate that every 1% reduction in total costs would boost the combined group’s total net profit by around 0.5%.

7.3 Synergy 3 – good fit in terms of overseas network

PBB’s overseas operations are located mainly in Hong Kong [housed under Public Financial Holding Group (PFHG)] and Indochina (Cambodia and Vietnam). It has 3-4 branches in China now and can only speed up its expansion in the country when PFHG’s asset size reaches US$6bn. This has been delayed due to the slow growth of its Hong Kong unit in the past 2-3 years.

In comparison, HLB’s biggest overseas unit is Bank of Chengdu, which contributed 14-15% of pretax profit. HLB also has operations in Singapore and Vietnam but they are relatively small. As such, a merger between PBB and HLB would be a good fit in terms of overseas network.

Following the merger, opportunities would arise for the enlarged bank to build on the business flow between Bank of Chengdu and PFHG. Given its strong capability in retail banking (especially in the property, auto and SME loan segments), PBB could add value by aiding Bank of Chengdu’s expansion. We note that HLB has done a remarkable job in transforming the bank over the past few years.

8. OTHER ISSUES

In order for the merger between PBB and HLB to be successful and fruitful, the parties involved would have to iron out the following issues.

8.1 Auto financing business

PBB and HLB have different stances on the auto financing business. PBB is the biggest and consistent player in this segment, while HLB is more conservative and restrictive in terms of its exposure to car financing. The management teams of both banks must decide on their respective strategies in this area after the merger. If the merged PBB-HLB group decides to wind down its exposure to this segment, keener players like Maybank would benefit.

8.2 Investment banking

PBB owns an investment banking unit, Public Investment Bank (PIB), while the investment banking business of Hong Leong Financial Group (HLFG), HLB’s holding company, is housed under a separate entity called Hong Leong Capital (HLC). If PBB and HLB were to merge, HLFG would own two investment banking licences, which would violate central bank regulations. Hence, the two investment banking units must be consolidated, either by injecting HLC into PIB or vice versa.

8.3 Insurance

Neither PBB nor HLB have direct insurance units but sell third-party insurance products. PBB channels most of its general insurance business to its sister company, LPI Capital, and has tie-ups with AIA for the life insurance business. We believe that HLB mostly sells the general and life insurance products of its sister company, Hong Leong Assurance. If PBB and HLB were to merge, the key questions are: 1) whether the merged entity would continue to have a life insurance tie-up with AIA, and 2) whether LPI would forgo its business from PBB.

Banks│Malaysia

October 15, 2014

13

9. VALUATION AND RECOMMENDATION

9.1 Still Underweight on banks

Overall, we are still Underweight on Malaysian banks, given the concerns about: 1) slower loan growth, 2) ongoing margin contraction, and 3) an upturn in credit costs. Their valuations are also less attractive, with sector average CY15 P/E of 11.5x. This is on par with the 11.5x of the Indonesian banks but above the 10.5x of the Thai banks, despite the Malaysian banks’ weaker growth prospects in the longer term.

9.2 Not expecting industry-wide bank mergers

Our Underweight rating is underpinned by our base case scenario that assumes that there will not be industry-wide bank mergers as there are no strong reasons for the banks to merge in Malaysia. However, we do not rule out the possibility of mergers materialising due to potential directive by Bank Negara in order to reduce the number of banks in Malaysia. We understand that the central bank’s current stance is that it will leave M&A activities to market forces. We would review our calls on the sector and the banks involved if M&A momentum picks up.

9.3 Potential M&A participants not top picks

The three banks with the M&A potential that we have highlighted in this report are not our top picks for the sector due to their unfavourable growth prospects and pricey valuation (PBB):

Public Bank (Reduce) – PBB is overvalued at its high CY15 P/E of 14.4x compared to the sector average of 11.5x. The rich valuation is not justified, given its weak projected single-digit EPS growth in FY14-16 and below-sector average dividend yields of 3.1%. Other factors that underpin our cautious stance on the stock are: 1) its ongoing margin contraction, which would have negative impact on topline growth, 2) the weak expansion of its business in Hong Kong due to intense industry competition, and 3) the succession uncertainties as Tan Sri Teh Hong Piow, the founder and controlling shareholder of the group, is already in his 80s.

Hong Leong Bank (Reduce) – HLB is known for its prudent management but we have major concerns about the group’s slow topline growth. Its loan growth of 7-8% in 2012-2013 was below the industry average. The CEO guides for loan growth of 10%, closer to the industry average, but we think that the expected industry-wide slowdown in residential mortgage growth (biggest component of HLB’s loan base) will make this challenging. The expected upward reversal in credit costs is another possible drag on HLB’s earnings growth, as its credit charge-off rate was only 5-7bp in the past five quarters (even net write-back in 1QFY6/14), well below the sustainable level of 20-30bp, in our view.

AMMB Holdings (Hold) – Despite its below-sector average P/E valuation, AMMB is not our pick for the sector given its pedestrian loan growth. Its loan growth was low-to-mid single digits in the past one year (+1.5% yoy in Jun 2014). We are cautious on AMMB’s earnings outlook, as reflected in our core net profit growth projection of only 0.4% for FY3/15. Apart from the weak loan growth, we think that AMMB faces earnings risks of: 1) margin contraction, and 2) a rise in credit costs.

We would review our ratings on these stocks if they start embark on M&As. However, we think that any M&A impact would hinge on: 1) the mode of the M&A activities, 2) the potential acquirers and acquirees, 3) pricing, and 4) the potential post-merger synergies, based on management guidance.

Banks│Malaysia

October 15, 2014

14

DISCLAIMER #03

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the “Restrictions on Distributions” set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments.

CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term “CIMB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by

Australia CIMB Securities (Australia) Limited Australian Securities & Investments Commission Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI) Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

(i) As of October 14, 2014, CIMB has a proprietary position in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report:

(a) Affin Holdings, Agricultural Bank of China, Alliance Financial Group, AMMB Holdings, ANZ Banking Group, Axis Bank, Bank Central Asia, Bank Danamon, Bank Mandiri, Bank of Baroda, Bank of China, Bank Rakyat Indonesia, BIMB Holdings, BS Financial Group, China Construction Bank, China Merchants Bank, DBS Group, E.Sun Financial, Federal Bank, Hana Financial Group, HDFC Bank, Hong Leong Bank, Housing Development Fin., ICBC, ICICI Bank, Industrial Bank of Korea, Kasikornbank, KB Financial Group, Krung Thai Bank, LIC Housing Finance, Malayan Banking Bhd, National Australia Bank, OCBC, Oriental Bank of Commerce, Public Bank Bhd, RHB Capital Bhd, Samsung Card, Shinhan Financial Group, State Bank of India, United Overseas Bank, Westpac Banking Corp, Woori Finance Holdings, Yes Bank

Banks│Malaysia

October 15, 2014

15

(ii) As of October 15, 2014, the analyst(s) who prepared this report, has / have an interest in the securities (which may include but not limited to shares, warrants, call warrants and/or any other derivatives) in the following company or companies covered or recommended in this report:

(a) -

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments thereof.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Australia) Limited (“CSAL”) (ABN 84 002 768 701, AFS Licence number 240 530). CSAL is a Market Participant of ASX Ltd, a Clearing Participant of ASX Clear Pty Ltd, a Settlement Participant of ASX Settlement Pty Ltd, and, a participant of Chi X Australia Pty Ltd. This research is only available in Australia to persons who are “wholesale clients” (within the meaning of the Corporations Act 2001 (Cth)) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. This research has been prepared without taking into account the objectives, financial situation or needs of the individual recipient.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (“CHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CHK. Unless permitted to do so by the securities laws of Hong Kong, no person may issue or have in its possession for the purposes of issue, whether in Hong Kong or elsewhere, any advertisement, invitation or document relating to the securities covered in this report, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong).

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (“CIMB India”) which is registered with SEBI as a stock-broker under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992 and in accordance with the provisions of Regulation 4 (g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required to seek registration with SEBI as an Investment Adviser.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.

Indonesia: This report is issued and distributed by PT CIMB Securities Indonesia (“CIMBI”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBI has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBI. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBI. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesia residents except in compliance with applicable Indonesian capital market laws and regulations.

Malaysia: This report is issued and distributed by CIMB Investment Bank Berhad (“CIMB”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMB has no obligation to update

Banks│Malaysia

October 15, 2014

16

its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMB. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

New Zealand: In New Zealand, this report is for distribution only to persons whose principal business is the investment of money or who, in the course of, and for the purposes of their business, habitually invest money pursuant to Section 3(2)(a)(ii) of the Securities Act 1978.

Singapore: This report is issued and distributed by CIMB Research Pte Ltd (“CIMBR”). Recipients of this report are to contact CIMBR in Singapore in respect of any matters arising from, or in connection with, this report. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBR has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only. If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBR.

As of October 14, 2014, CIMBR does not have a proprietary position in the recommended securities in this report.

South Korea: This report is issued and distributed in South Korea by CIMB Securities Limited, Korea Branch ("CIMB Korea") which is licensed as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea.

The views and opinions in this research report are our own as of the date hereof and are subject to change, and this report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial investment instruments and it is not intended as a solicitation for the purchase of any financial investment instrument.

This publication is strictly confidential and is for private circulation only, and no part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB Korea.

Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer or a placement within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Thailand: This report is issued and distributed by CIMB Securities (Thailand) Company Limited (CIMBS). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBS has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBS. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBS.

CIMB Securities (Thailand) Co., Ltd. may act or acts as Market Maker and issuer including offering of Derivative Warrants Underlying securities of the following securities. Investors should carefully read and study the details of the derivative warrants in the prospectus before making investment decisions.

AAV, ADVANC, AMATA, ANAN, AOT, AP, ASP, BANPU, BAY, BBL, BCH, BCP, BEC, BECL, BGH, BH, BIGC, BJC, BJCHI, BLA, BLAND, BMCL, BTS, CENTEL, CK, CPALL, CPF, CPN, DCC, DELTA, DEMCO, DTAC, EARTH, EGCO, ERW, ESSO, GFPT, GLOBAL, GLOW, GUNKUL, HEMRAJ, HMPRO, INTUCH, IRPC, ITD, IVL, JAS, KBANK, KCE, KKP, KTB, KTC, LH, LOXLEY, LPN, M, MAJOR, MC, MCOT, MEGA, MINT, NOK, NYT, PS, PSL, PTT, PTTEP, PTTGC, QH, RATCH, ROBINS, RS, SAMART, SCB, SCC, SCCC, SIRI, SPALI, SPCG, SRICHA, STA, STEC, STPI, SVI, TASCO, TCAP, TFD, THAI, THCOM, THRE, THREL, TICON, TISCO, TMB, TOP, TPIPL, TTA, TTCL, TTW, TUF, UMI, UV, VGI, TRUE, WHA.

Corporate Governance Report:

The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CIMBS does not confirm nor certify the accuracy of such survey result.

Score Range: 90 - 100 80 - 89 70 - 79 Below 70 or No Survey Result

Description: Excellent Very Good Good N/A

Banks│Malaysia

October 15, 2014

17

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates.

United Kingdom and Europe: In the United Kingdom and European Economic Area, this report is being disseminated by CIMB Securities (UK) Limited (“CIMB UK”). CIMB UK is authorised and regulated by the Financial Conduct Authority and its registered office is at 27 Knightsbridge, London, SW1X 7YB. This report is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are persons that are eligible counterparties and professional clients of CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”); (c) are persons falling within Article 49 (2) (a) to (d) (“high net worth companies, unincorporated associations etc”) of the Order; (d) are outside the United Kingdom; or (e) are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with any investments to which this report relates may otherwise lawful ly be communicated or caused to be communicated (all such persons together being referred to as “relevant persons”). This report is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons.

Only where this report is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not constitute independent "investment research" under the applicable rules of the Financial Conduct Authority in the UK. Consequently, any such non-independent report will not have been prepared in accordance with legal requirements designed to promote the independence of investment research and will not subject to any prohibition on dealing ahead of the dissemination of investment research.

United States: This research report is distributed in the United States of America by CIMB Securities (USA) Inc, a U.S.-registered broker-dealer and a related company of CIMB Research Pte Ltd, CIMB Investment Bank Berhad, PT CIMB Securities Indonesia, CIMB Securities (Thailand) Co. Ltd, CIMB Securities Limited, CIMB Securities (Australia) Limited, CIMB Securities (India) Private Limited, and is distributed solely to persons who qualify as "U.S. Institutional Investors" as defined in Rule 15a-6 under the Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds and associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CIMB Securities (USA) Inc, is a FINRA/SIPC member and takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered representative of CIMB Securities (USA) Inc.

Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

Rating Distribution (%) Investment Banking clients (%)

Add 54.9% 5.0%

Hold 29.5% 2.3%

Reduce 15.6% 1.0%

Distribution of stock ratings and investment banking clients for quarter ended on 30 September 2014

1552 companies under coverage for quarter ended on 30 September 2014

CustomSpitzerKR_KRSpitzer

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2013. AAV - Good, ADVANC - Excellent, AMATA - Very Good, ANAN – Good, AOT - Excellent, AP - Very Good, BANPU - Excellent , BAY - Excellent , BBL - Excellent, BCH – Good, BCP - Excellent, BEAUTY – Good, BEC - Very Good, BECL - Excellent, BGH - not available, BH - Very Good, BIGC - Very Good, BJC – Very Good, BMCL - Very Good, BTS - Excellent, CCET – Very Good, CENTEL – Very Good, CHG – not available, CK - Excellent, CPALL - Very Good, CPF - Excellent, CPN - Excellent, DELTA - Very Good, DTAC - Excellent, EA - Good, EGCO - Excellent, GFPT - Very Good, GLOBAL - Good, GLOW - Very Good, GRAMMY - Excellent, HANA - Excellent, HEMRAJ - Excellent, HMPRO - Very Good, ICHI - not available, INTUCH - Excellent, ITD – Very Good, IVL - Excellent, JAS – Very Good, KAMART – not available, KBANK - Excellent, KCE - Very Good, KKP – Excellent, KTB - Excellent, LH - Very Good, LPN - Excellent, M - not available, MAJOR - Very Good, MAKRO – Very Good, MC - not available, MCOT - Excellent, MEGA – not available, MINT - Excellent, OFM – Very Good, PS - Excellent, PSL - Excellent, PTT - Excellent, PTTGC - Excellent, PTTEP - Excellent, QH - Excellent, RATCH - Excellent, ROBINS - Excellent, RS - Excellent, SAMART - Excellent, SAPPE - not available, SC – Excellent, SCB - Excellent, SCC - Excellent, SCCC - Very Good, SIM - Excellent, SIRI - Very Good, SPALI - Excellent, STA - Good, STEC - Very Good, SVI – Excellent, TASCO – Very Good, TCAP - Excellent, THAI - Excellent, THCOM – Excellent, TICON – Very Good, TISCO - Excellent, TMB - Excellent, TOP - Excellent, TRUE - Excellent, TTW - Excellent, TUF - Very Good, VGI – Excellent, WORK – Good.

Banks│Malaysia

October 15, 2014

18

CIMB Recommendation Framework

Stock Ratings Definition:

Add The stock’s total return is expected to exceed 10% over the next 12 months.

Hold The stock’s total return is expected to be between 0% and positive 10% over the next 12 months.

Reduce The stock’s total return is expected to fall below 0% or more over the next 12 months.

The total expected return of a stock is defined as the sum of the: (i) percentage difference between the target price and the current price and (ii) the forward net dividend yields of the stock. Stock price targets have an investment horizon of 12 months.

Sector Ratings Definition:

Overweight An Overweight rating means stocks in the sector have, on a market cap-weighted basis, a positive absolute recommendation.

Neutral A Neutral rating means stocks in the sector have, on a market cap-weighted basis, a neutral absolute recommendation.

Underweight An Underweight rating means stocks in the sector have, on a market cap-weighted basis, a negative absolute recommendation.

Country Ratings Definition:

Overweight An Overweight rating means investors should be positioned with an above-market weight in this country relative to benchmark.

Neutral A Neutral rating means investors should be positioned with a neutral weight in this country relative to benchmark.

Underweight An Underweight rating means investors should be positioned with a below-market weight in this country relative to benchmark.

*Prior to December 2013 CIMB recommendation framework for stocks listed on the Singapore Stock Exchange, Bursa Malaysia, Stock Exchange of Thailand, Jakarta Stock Exchange, Australian Securities Exchange, Taiwan Stock Exchange and National Stock Exchange of India/Bombay Stock Exchange were based on a stock’s total return relative to the relevant benchmarks total return. Outperform: expected to exceed by 5% or more over the next 12 months. Neutral: expected to be within +/-5% over the next 12 months. Underperform: expected to be below by 5% or more over the next 12 months. Trading Buy: expected to exceed by 3% or more over the next 3 months. Trading Sell: expected to be below by 3% or more over the next 3 months. For stocks listed on Korea Exchange, Hong Kong Stock Exchange and China listings on the Singapore Stock Exchange. Outperform: Expected positive total returns of 10% or more over the next 12 months. Neutral: Expected total returns of between -10% and +10% over the next 12 months. Underperform: Expected negative total returns of 10% or more over the next 12 months. Trading Buy: Expected positive total returns of 10% or more over the next 3 months. Trading Sell: Expected negative total returns of 10% or more over the next 3 months.