company bhd buy - i3investorcdn1.i3investor.com/my/files/dfgs88n/2016/02/15/1483914349... ·...

TRANSCRIPT

Page 1 of 12

15 February 2016

HLIB Research

PP 9484/12/2012 (031413)

Sarawak Elections

MARKET VIEW

15 February 2016

Play on the polls

Highlights Sarawak to hit the polls. The 11th Sarawak Elections must

be held by 20th Sept 2016. However, this is likely to happen

earlier as Chief Minister Adenan Satem (CM Adenan) has

proposed to the Election Commission to hold the polls on

30th April with nominations on 16th April.

BN likely to retain control. Political analysts hold a

consensus view that the Barisan Nasional (BN) coalition will

likely retain control of Sarawak. CM Adenan’s high approval

rating (74%), redelineation exercise resulting to more rural

constituencies and a fragmented opposition are all factors

working in BN’s favour.

Politics of developmentalism. It has been observed that

funding promises, especially for infra increases as election

approaches. This is already happening with Budget 2016

spelling many benefits for “Sarawakians”. We expect more

positive news flow on project rollouts running up to the polls.

What do voters want? A survey by the Merdeka Centre

reveals that “jobs creation” and “improving rural infra” are the

2nd and 3rd most important issues requiring attention from the

State Govt. We believe the State Govt will try and address

these matters through (i) industrialisation of Sarawak’s

economy via SCORE and (ii) building the Pan Borneo

Highway (PHB) to improve connectivity in the state.

SCORE for Sarawak. SCORE has amassed RM33bn worth

of investments from 2008-2014. Most that have set up within

SCORE are energy intensive industries. The key pull factor

here is the availability of cheap electricity generated by

hydro dams. To further harness this potential, Sarawak

Energy has planned to build 12 hydro dams from 2008-2020,

increasing the state’s generation capacity by 7000MW. This

would spur other infra requirements such as transmission

lines and access roads.

Pan Borneo takes off. We reckon that the 1,089km PBH

(RM16bn) will be the most anticipated mega project to kick

start running up to the polls. 17 consortiums are said to have

been prequalified for 10 packages involving the highway’s

main stretch. Initial awards are expected as soon as March.

Stock

Picks

SCable - Beneficiary of ramp up in Sarawak’s generation

capacity via transmission line contracts. Also looking to

supply guardrails and lamp poles for the PBH.

HSL - Marine engineering expertise provides an edge to bid

for PBH given Sarawak’s swampy terrain.

CMS - Beneficiary of PBH via construction and supply of

aggregates. Also a cement monopoly in Sarawak.

Naim - Said to be top contender (JV with Gamuda) for one

of the earlier PBH packages.

TRC - Only Peninsular contractor that can bid for state

funded jobs. Has competed RM1bn jobs in Sarawak.

Harbour – To benefit from Sarawak’s overall development

via increase in demand for project cargo.

Jeremy Goh, CFA

(603) 2168 1138

Approval rating for CM Adenan

Source: Merdeka Centre

Pan Borneo Highway

Source: Lebuhraya Borneo Utara

Potential Sarawak Election plays

Stock Rating Price Target

SCable BUY 1.48 2.57 HSL HOLD 1.93 2.04 CMS Not Rated 5.03 NA Naim Not Rated 2.48 NA TRC Not Rated 0.365 NA Harbour Not Rated 2.70 NA

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 2 of 12

15 February 2016

Highlights

Land of the Hornbills to hit the polls

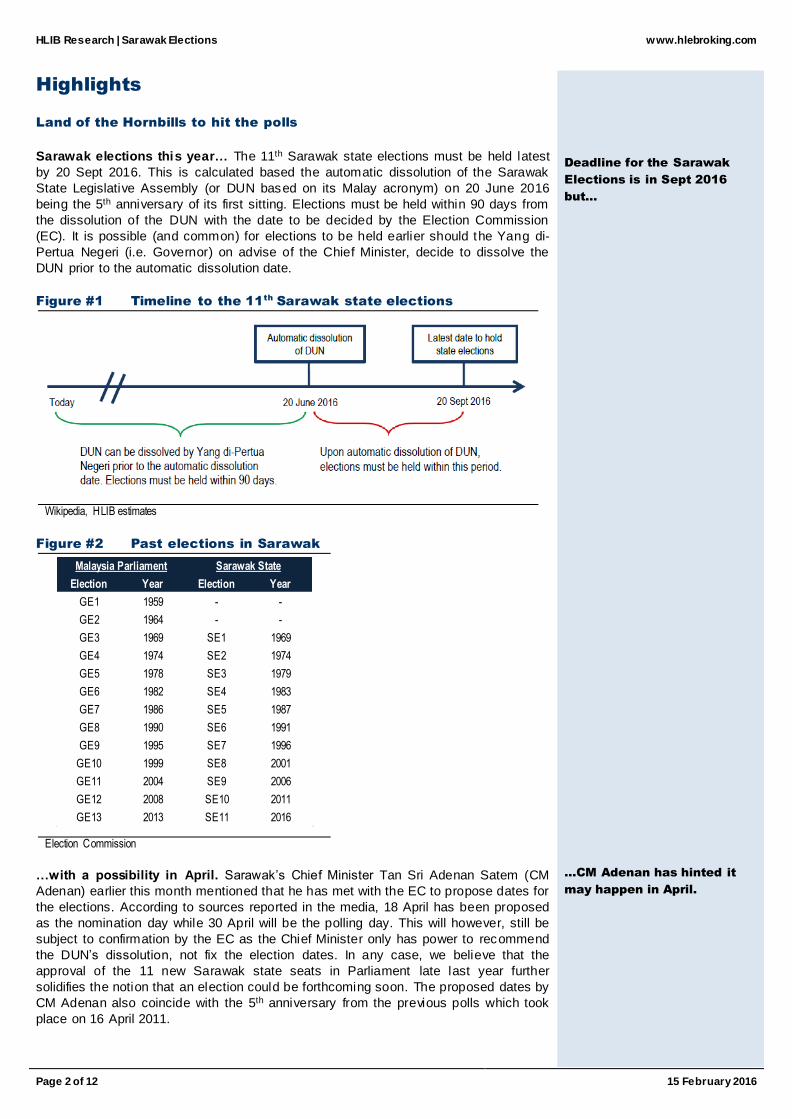

Sarawak elections this year… The 11th Sarawak state elections must be held latest

by 20 Sept 2016. This is calculated based the automatic dissolution of the Sarawak

State Legislative Assembly (or DUN based on its Malay acronym) on 20 June 2016

being the 5th anniversary of its first sitting. Elections must be held within 90 days from

the dissolution of the DUN with the date to be decided by the Election Commission

(EC). It is possible (and common) for elections to be held earlier should the Yang di-

Pertua Negeri (i.e. Governor) on advise of the Chief Minister, decide to dissolve the

DUN prior to the automatic dissolution date.

Figure #1 Timeline to the 11th

Sarawak state elections

Wikipedia, HLIB estimates

Figure #2 Past elections in Sarawak

Election Year Election Year

GE1 1959 - -

GE2 1964 - -

GE3 1969 SE1 1969

GE4 1974 SE2 1974

GE5 1978 SE3 1979

GE6 1982 SE4 1983

GE7 1986 SE5 1987

GE8 1990 SE6 1991

GE9 1995 SE7 1996

GE10 1999 SE8 2001

GE11 2004 SE9 2006

GE12 2008 SE10 2011

GE13 2013 SE11 2016

Malaysia Parliament Sarawak State

Election Commission

…with a possibility in April. Sarawak’s Chief Minister Tan Sri Adenan Satem (CM

Adenan) earlier this month mentioned that he has met with the EC to propose dates for

the elections. According to sources reported in the media, 18 April has been proposed

as the nomination day while 30 April will be the polling day. This will however, still be

subject to confirmation by the EC as the Chief Minister only has power to recommend

the DUN’s dissolution, not fix the election dates. In any case, we believe that the

approval of the 11 new Sarawak state seats in Parliament late last year further

solidifies the notion that an election could be forthcoming soon. The proposed dates by

CM Adenan also coincide with the 5th anniversary from the previous polls which took

place on 16 April 2011.

Deadline for the Sarawak

Elections is in Sept 2016

but…

…CM Adenan has hinted it

may happen in April.

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 3 of 12

15 February 2016

Sarawak’s political landscape

Diverse demographics. Sarawak has a headcount of 2.6m people, making up 9% of

Malaysia’s population. Compared to its Peninsular counterpart, Sarawak is very

diverse comprising over 40 sub-ethnic groups, each with its own distinct language,

culture and lifestyle. These various ethnicities are broadly categorised into 6 groups

which are Iban (30%), Malay (24%), Chinese (24%), Bidayuh (8%), Orang Ulu (7%)

and Melanau (5%). Apart from the Malays and Chinese, the other mentioned ethnic

groups are indigenous to Sarawak which are categorised as non-Malay Bumiputeras.

Comprising mainly of non-Malay Bumiputeras, Christianity is the most professed

religion in Sarawak at 43% compared to the national level of only 9%. Islam on the

other hand, is the 2nd largest religion in Sarawak at 23% (Malaysia: 61%).

Figure #3 Ethnic composition in Sarawak (3Q13)

Iban30%

Malay24%

Chinese24%

Bidayuh8%

Melanau5%

Orang Ulu7%

Others1%

Sarawak state statistics

The ruling coalition. Sarawak has always been under the Barisan Nasional (BN)

administration which has also ruled Malaysia since independence. Unlike BN in

Peninsular Malaysia which mainly comprises the United Malays National Organisation

(UMNO), Malaysian Chinese Association (MCA) and Malaysian Indian Congress

(MIC), the component parties in Sarawak are different. In Sarawak, the BN component

parties officially consists of Parti Pesaka Bumiputera Bersatu (PBB), Sarawak United

People’s Party (SUPP), Parti Rakyat Sarawak (PRS) and Sarawak Progr essive

Democratic Party (SPDP) which are all home grown “Sarawakian” parties. The BN

coalition in Sarawak is officially led by none other than CM Adenan from the PBB.

Figure #4 BN component parties in Sarawak

Barisan Nasional

The opposition parties. On the other hand, Sarawak opposition parties that currently

hold seats in the DUN are the Democratic Action Party (DAP) and Parti Keadilan

Rakyat (PKR). Other opposition parties that do not hold seats in the DUN include the

newly formed Parti Amanah Negara (PAN), Parti Islam Se-Malaysia (PAS) and smaller

state-centric parties such as the Sarawak National Party (SNAP). Currently, the

opposition leader in the DUN is helmed by Chong Chieng Jen from the DAP.

Sarawak is ethnically more

diverse than its Peninsular

counterpart

BN component parties in

Sarawak are all “home

grown”

DAP and PKR are the only

opposition parties with seats

in the DUN

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 4 of 12

15 February 2016

Predicting the polls

Recap of the previous polls. The previous (i.e. 10th) Sarawak State Elections was

held on 16 April 2011 which saw BN winning 55 of the 71 seats. This however, came

with a reduced margin as the coalition lost 8 seats. Amongst opposition parties, the

DAP gained most ground by doubling its seats from 6 to 12. Whist BN retained its

traditional two-thirds majority seats in the DUN, it only captured 55% of the popular

vote while the now defunct Pakatan Rakyat managed to garner 41%.

Figure #5 Results of the previous Sarawak State Elections

Political Party Votes % Seats %

Parti Pesaka Bumiputera Bersatu (PBB) 192,785 28.7% 35 49.3%

Sarawak United People's Party (SUPP) 111,781 16.6% 6 8.5%

Parti Rakyat Sarawak (PRS) 35,120 5.2% 8 11.3%

Sarawak Progressive Democratic Party (SPDP) 32,693 4.9% 6 8.5%

Barisan Nasional 372,379 55.4% 55 77.5%

Democratic Action Party (DAP) 134,847 20.0% 12 16.9%

Parti Keadilan Rakyat (PKR) 117,100 17.4% 3 4.2%

Sarawak National Party (SNAP) 15,663 2.3% - 0.0%

Parti Islam Se-Malaysia (PAS) 9,719 1.4% - 0.0%

Pakatan Rakyat (now defunct) 277,329 41.2% 15 21.1%

Independents 20,064 3.0% 1 1.4%

Parti Cinta Malaysia (PCM) 2,895 0.4% - 0.0%

Others 22,959 3.4% 1 1.4%

Total 672,667 100.0% 71 100.0%

Election Commission

Popularity of the new Chief Minister. CM Adenan has been the Chief Minister for

almost 2 years since he took the oath of office in Feb 2014. His predecessor, Tan Sri

Abdul Taib Mahmud, who is also the longest serving Chief Minister in Malaysian

history, now helms the role of Sarawak’s Yang di-Pertua Negeri (i.e. Governor). A

survey conducted by independent opinion research firm Merdeka Centre in April 2015

depicts the popularity of CM Adenan amongst Sarawakians who has an approval rating

of 74%, higher than the 68% for the overall Sarawak State Government.

Figure #6 Satisfaction survey with the Sarawak Chief Minister

Merdeka Centre

BN won the previous

Sarawak Elections with a

two-third majority

CM Adenan is popular with a

high approval rating of 74%

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 5 of 12

15 February 2016

Figure #7 Satisfaction survey with the Sarawak State Government

Merdeka Centre

An uphill battle for the opposition. Sarawak’s redelineation exercise by the EC was

passed in Parliament last Dec which will see the number of state constituencies for the

upcoming polls increased by 11 to 82 from the current 71. Out of the 11 new seats, 10

are considered rural or semi -rural areas which traditionally, have been BN stronghold

areas. The strength of the opposition DAP and PKR on the other hand, are in the urban

seats. Apart from trying to penetrate the rural seats, the key challenge for the

opposition is to avoid multi cornered fights. The newly formed Pakatan Harapan

opposition coalition consists of DAP, PKR and PAN while PAS and SNAP remain

standalone. Unless a consensus can be achieved between all opposition parties to

ensure straight fight against BN in every seat, a fragmented opposition is unlikely to

gain much traction during the polls. CM Adenan on the other hand, has claimed that

BN has resolved the conflicting seat allocation between its component parties.

Figure #8 New state constituencies

New Constituency Code Constituents Ethnic majority

Batu Kitang N13 20,819 Chinese

Stakan N17 12,761 Iban

Serembu N18 8,965 Bidayuh

Bukit Semuja N23 12,753 Bidayuh

Gedong N26 6,712 Malay / Melanau

Kabong N40 9,157 Malay / Melanau

Tellian N57 8,698 Malay / Melanau

Bukit Goram N63 11,459 Iban

Murum N66 7,648 Orang Ulu

Samalaju N70 12,927 Iban

Mulu N78 8,048 Orang Ulu

Election Commission, Wikipedia

BN likely to retain control. The consensus view amongst political analysts is that BN

will likely retain control of Sarawak in the upcoming polls. A renowned analyst on

Malaysian politics, Professor James Chin of the Asia Institute, University of Tasmania

commented in his recent article, Sarawak 's "Wayang Kulit", that “There is little doubt

that Adenan and Sarawak BN will win big in this year’s vote. In the last state election,

Sarawak BN won 55 of 71 seats. Thirteen of the 16 seats won by the opposition were

in urban, largely Chinese-majority constituencies. A repeat is expected in the 2016

race.” This stance is also echoed by Ibrahim Suffian, Director of the Merdeka Centre

who commented “Given high rating for the CM and the state, it gives us an ink ling of

how they will vote. It looks quite positive at the moment...”

The upcoming polls will see

11 new constituencies, 10 of

which are rural

Political analysts feel that

BN is likely to retain control

in the polls

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 6 of 12

15 February 2016

Politics of developmentalism

Churning the feel good factor. We expect positive news flow on Sarawak’s project

implementations to gain momentum as the polls draw closer. Several academic papers

on Sarawak politics suggest that a party’s control over state finances has been an

essential ingredient in winning support at the polls. They argued that in the months

running up to the elections and during the campaign period, promises for funding,

especially for infrastructure projects such as roads increases. This phenomenon has

been termed as the “politics of developmentalism”.

A “Sarawak Election” Budget. Budget 2016 which was tabled in Oct last year

contained many measures targeted at Sarawak. Opposition leaders such as Selangor

Menteri Besar Azmin Ali and Penang Chief Minister Lim Guan Eng both said that

Budget 2016 was clearly an attempt by BN to win the upcoming Sarawak Elections.

Their views were surprisingly echoed by Deputy Prime Minister Datuk Seri Ahmad

Zahid. Budget 2016 saw a specific section that was dedicated towards “intensifying

development in Sabah and Sarawak” with 7 key measures. These are (i) implementing

the RM29bn Pan Borneo Highway, (ii) GST exemption for Rural Air Services routes,

(iii) interest free loans for building longhouses, (iv) RM70m fertiliser subsidies for hill

paddy farmers, (v) RM260m to for price uniformity programmes, (vi) RM115m for the

Special Programme for Bumiputera and (vii) 1Malaysia Mobile Clinics in the interior

areas of the states. Apart from these directly mentioned measures, other nationwide

initiatives that are likely to benefit Sarawak are those that are rural development centric

such as the upgrading of 700km of roads (RM1.4bn) and provision of rural

electrification and water supply (RM878m).

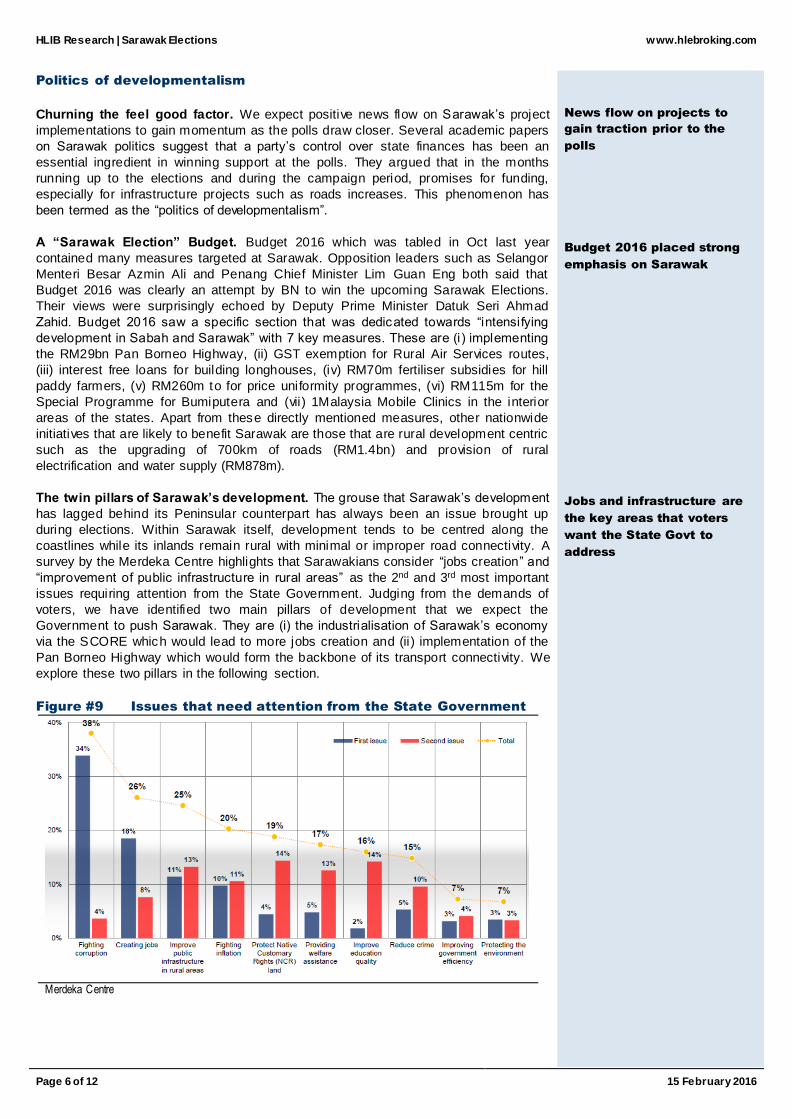

The twin pillars of Sarawak’s development. The grouse that Sarawak’s development

has lagged behind its Peninsular counterpart has always been an issue brought up

during elections. Within Sarawak itself, development tends to be centred along the

coastlines while its inlands remain rural with minimal or improper road connectivity. A

survey by the Merdeka Centre highlights that Sarawakians consider “jobs creation” and

“improvement of public infrastructure in rural areas” as the 2nd and 3rd most important

issues requiring attention from the State Government. Judging from the demands of

voters, we have identified two main pillars of development that we expect the

Government to push Sarawak. They are (i) the industrialisation of Sarawak’s economy

via the SCORE which would lead to more jobs creation and (ii) implementation of the

Pan Borneo Highway which would form the backbone of its transport connectivity. We

explore these two pillars in the following section.

Figure #9 Issues that need attention from the State Government

Merdeka Centre

News flow on projects to

gain traction prior to the

polls

Budget 2016 placed strong

emphasis on Sarawak

Jobs and infrastructure are

the key areas that voters

want the State Govt to

address

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 7 of 12

15 February 2016

SCORE: Sarawak’s industrialisation drive

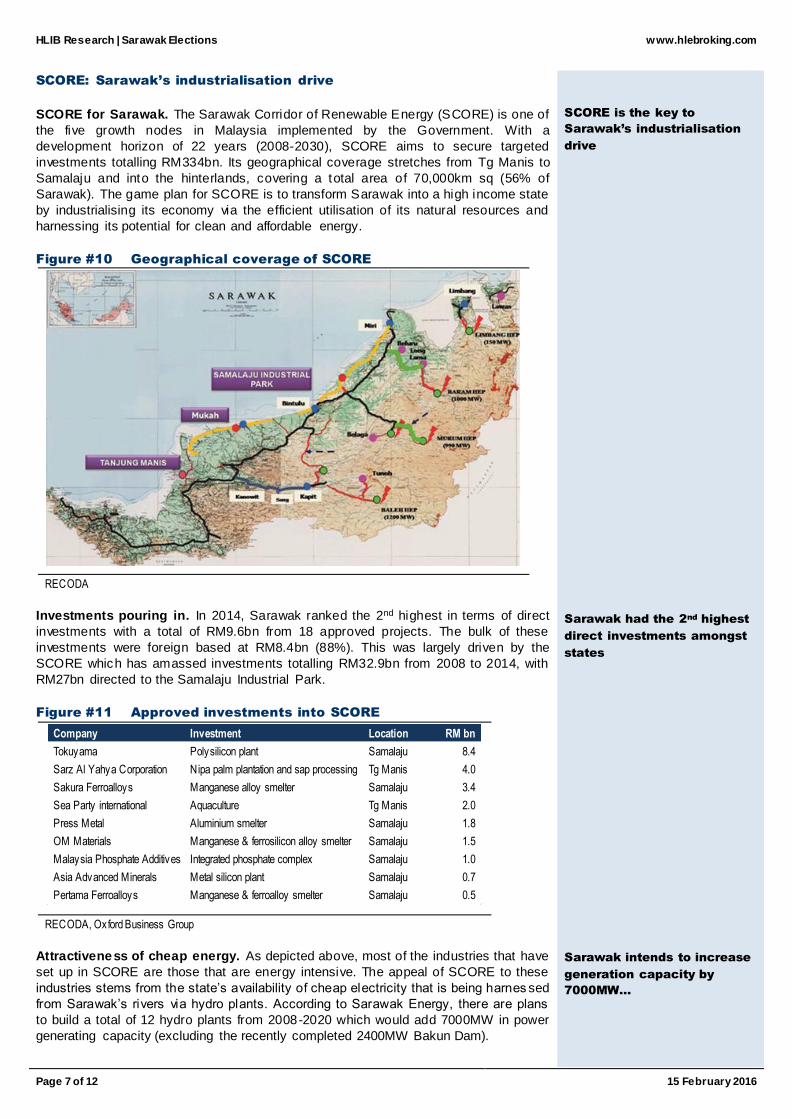

SCORE for Sarawak. The Sarawak Corridor of Renewable Energy (SCORE) is one of

the five growth nodes in Malaysia implemented by the Government. With a

development horizon of 22 years (2008-2030), SCORE aims to secure targeted

investments totalling RM334bn. Its geographical coverage stretches from Tg Manis to

Samalaju and into the hinterlands, covering a total area of 70,000km sq (56% of

Sarawak). The game plan for SCORE is to transform Sarawak into a high income state

by industrialising its economy via the efficient utilisation of its natural resources and

harnessing its potential for clean and affordable energy.

Figure #10 Geographical coverage of SCORE

RECODA

Investments pouring in. In 2014, Sarawak ranked the 2nd highest in terms of direct

investments with a total of RM9.6bn from 18 approved projects. The bulk of these

investments were foreign based at RM8.4bn (88%). This was largely driven by the

SCORE which has amassed investments totalling RM32.9bn from 2008 to 2014, with

RM27bn directed to the Samalaju Industrial Park.

Figure #11 Approved investments into SCORE

Company Investment Location RM bn

Tokuyama Polysilicon plant Samalaju 8.4

Sarz Al Yahya Corporation Nipa palm plantation and sap processing Tg Manis 4.0

Sakura Ferroalloys Manganese alloy smelter Samalaju 3.4

Sea Party international Aquaculture Tg Manis 2.0

Press Metal Aluminium smelter Samalaju 1.8

OM Materials Manganese & ferrosilicon alloy smelter Samalaju 1.5

Malaysia Phosphate Additives Integrated phosphate complex Samalaju 1.0

Asia Advanced Minerals Metal silicon plant Samalaju 0.7

Pertama Ferroalloys Manganese & ferroalloy smelter Samalaju 0.5

RECODA, Oxford Business Group

Attractiveness of cheap energy. As depicted above, most of the industries that have

set up in SCORE are those that are energy intensive. The appeal of SCORE to these

industries stems from the state’s availability of cheap electricity that is being harnes sed

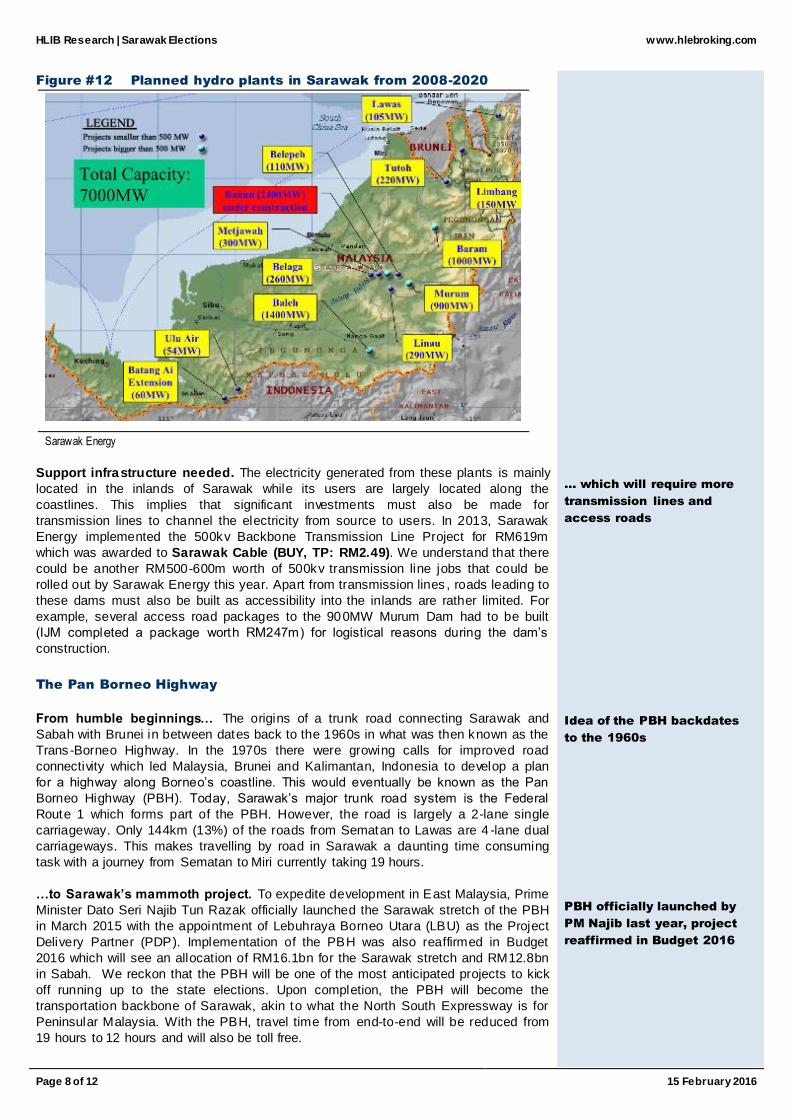

from Sarawak’s rivers via hydro plants. According to Sarawak Energy, there are plans

to build a total of 12 hydro plants from 2008-2020 which would add 7000MW in power

generating capacity (excluding the recently completed 2400MW Bakun Dam).

SCORE is the key to

Sarawak’s industrialisation

drive

Sarawak had the 2nd highest

direct investments amongst

states

Sarawak intends to increase

generation capacity by

7000MW…

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 8 of 12

15 February 2016

Figure #12 Planned hydro plants in Sarawak from 2008-2020

Sarawak Energy

Support infrastructure needed. The electricity generated from these plants is mainly

located in the inlands of Sarawak while its users are largely located along the

coastlines. This implies that significant investments must also be made for

transmission lines to channel the electricity from source to users. In 2013, Sarawak

Energy implemented the 500kv Backbone Transmission Line Project for RM619m

which was awarded to Sarawak Cable (BUY, TP: RM2.49). We understand that there

could be another RM500-600m worth of 500kv transmission line jobs that could be

rolled out by Sarawak Energy this year. Apart from transmission lines , roads leading to

these dams must also be built as accessibility into the inlands are rather limited. For

example, several access road packages to the 900MW Murum Dam had to be built

(IJM completed a package worth RM247m) for logistical reasons during the dam’s

construction.

The Pan Borneo Highway

From humble beginnings… The origins of a trunk road connecting Sarawak and

Sabah with Brunei in between dates back to the 1960s in what was then known as the

Trans-Borneo Highway. In the 1970s there were growing calls for improved road

connectivity which led Malaysia, Brunei and Kalimantan, Indonesia to develop a plan

for a highway along Borneo’s coastline. This would eventually be known as the Pan

Borneo Highway (PBH). Today, Sarawak’s major trunk road system is the Federal

Route 1 which forms part of the PBH. However, the road is largely a 2-lane single

carriageway. Only 144km (13%) of the roads from Sematan to Lawas are 4 -lane dual

carriageways. This makes travelling by road in Sarawak a daunting time consuming

task with a journey from Sematan to Miri currently taking 19 hours.

…to Sarawak’s mammoth project. To expedite development in East Malaysia, Prime

Minister Dato Seri Najib Tun Razak officially launched the Sarawak stretch of the PBH

in March 2015 with the appointment of Lebuhraya Borneo Utara (LBU) as the Project

Delivery Partner (PDP). Implementation of the PBH was also reaffirmed in Budget

2016 which will see an allocation of RM16.1bn for the Sarawak stretch and RM12.8bn

in Sabah. We reckon that the PBH will be one of the most anticipated projects to kick

off running up to the state elections. Upon completion, the PBH will become the

transportation backbone of Sarawak, akin to what the North South Expressway is for

Peninsular Malaysia. With the PBH, travel time from end-to-end will be reduced from

19 hours to 12 hours and will also be toll free.

… which will require more

transmission lines and

access roads

Idea of the PBH backdates

to the 1960s

PBH officially launched by

PM Najib last year, project

reaffirmed in Budget 2016

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 9 of 12

15 February 2016

Figure #13 Spin-offs from the Pan Borneo Highway

Lebuhraya Borneo Utara

Proposed alignment. Once completed in 2023, the Sarawak PBH will have a total

length of 1,089km. The highway’s main section begins at Tg Datu in the South West of

Sarawak and ends at Miri in the North East. In between these two points, the PBH will

cover areas such as Sematan, Samarahan, Sri Aman, Betong, Sarikei, Sibu and

Bintulu. Commencement of this main section is slated to begin sometime this year. The

other sections of the PBH will be at Limbang and Lawas which are across the other

end of Brunei and are targeted to begin only in 2018.

Some works have started. Within the PBH’s main section, works have begun on 2

stretches last year which are undertaken by 2 unlisted Sarawakian contractors. The

43km section from Nyabau to Bakun was awarded to a subsidiary of Shin Yang

Corporation and scheduled for completion in 2017. On the other hand, the 40km route

from Tg Datu to Sematan was dished out to a subsidiary of Samling Group and

targeted to be finished in 2018.

Figure #14 Alignment of the Sarawak Pan Borneo Highway

Lebuhraya Borneo Utara

PBH will be Sarawak’s

transportation backbone

Works on 2 stretches have

been awarded and started

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 10 of 12

15 February 2016

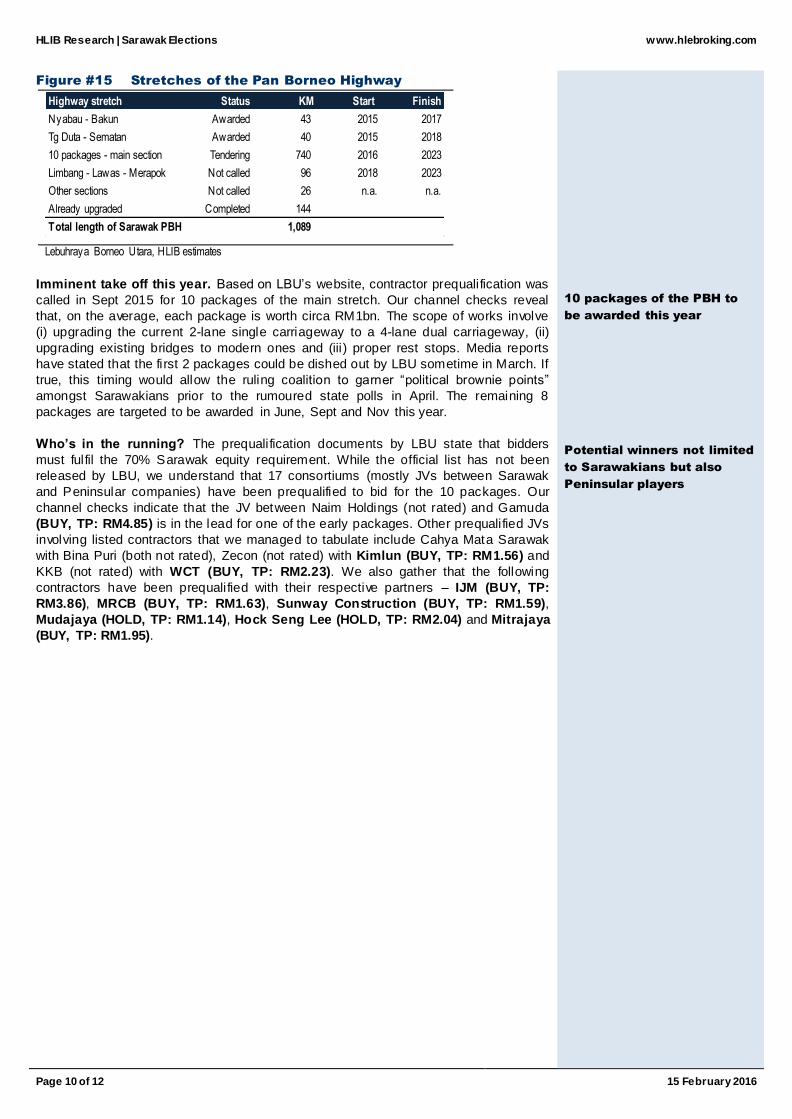

Figure #15 Stretches of the Pan Borneo Highway

Highway stretch Status KM Start Finish

Nyabau - Bakun Awarded 43 2015 2017

Tg Duta - Sematan Awarded 40 2015 2018

10 packages - main section Tendering 740 2016 2023

Limbang - Lawas - Merapok Not called 96 2018 2023

Other sections Not called 26 n.a. n.a.

Already upgraded Completed 144

Total length of Sarawak PBH 1,089

Lebuhraya Borneo Utara, HLIB estimates

Imminent take off this year. Based on LBU’s website, contractor prequalification was

called in Sept 2015 for 10 packages of the main stretch. Our channel checks reveal

that, on the average, each package is worth circa RM1bn. The scope of works involve

(i) upgrading the current 2-lane single carriageway to a 4-lane dual carriageway, (ii)

upgrading existing bridges to modern ones and (iii) proper rest stops. Media reports

have stated that the first 2 packages could be dished out by LBU sometime in March. If

true, this timing would allow the ruling coalition to garner “political brownie points”

amongst Sarawakians prior to the rumoured state polls in April. The remaining 8

packages are targeted to be awarded in June, Sept and Nov this year.

Who’s in the running? The prequalification documents by LBU state that bidders

must fulfil the 70% Sarawak equity requirement. While the official list has not been

released by LBU, we understand that 17 consortiums (mostly JVs between Sarawak

and Peninsular companies) have been prequalified to bid for the 10 packages. Our

channel checks indicate that the JV between Naim Holdings (not rated) and Gamuda

(BUY, TP: RM4.85) is in the lead for one of the early packages. Other prequalified JVs

involving listed contractors that we managed to tabulate include Cahya Mata Sarawak

with Bina Puri (both not rated), Zecon (not rated) with Kimlun (BUY, TP: RM1.56) and

KKB (not rated) with WCT (BUY, TP: RM2.23). We also gather that the following

contractors have been prequalified with their respective partners – IJM (BUY, TP:

RM3.86), MRCB (BUY, TP: RM1.63), Sunway Construction (BUY, TP: RM1.59),

Mudajaya (HOLD, TP: RM1.14), Hock Seng Lee (HOLD, TP: RM2.04) and Mitrajaya

(BUY, TP: RM1.95).

10 packages of the PBH to

be awarded this year

Potential winners not limited

to Sarawakians but also

Peninsular players

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 11 of 12

15 February 2016

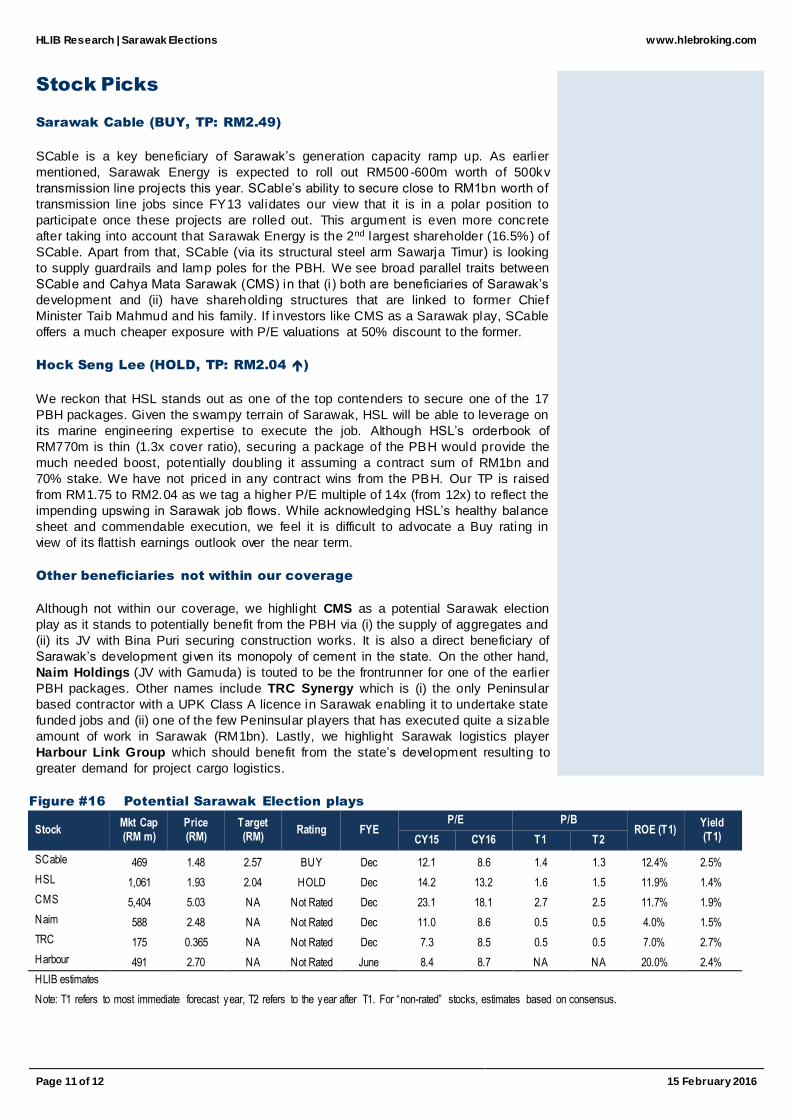

Stock Picks

Sarawak Cable (BUY, TP: RM2.49)

SCable is a key beneficiary of Sarawak’s generation capacity ramp up. As earlier

mentioned, Sarawak Energy is expected to roll out RM500 -600m worth of 500kv

transmission line projects this year. SCable’s ability to secure close to RM1bn worth of

transmission line jobs since FY13 validates our view that it is in a polar position to

participate once these projects are rolled out. This argument is even more concrete

after taking into account that Sarawak Energy is the 2nd largest shareholder (16.5%) of

SCable. Apart from that, SCable (via its structural steel arm Sawarja Timur) is looking

to supply guardrails and lamp poles for the PBH. We see broad parallel traits between

SCable and Cahya Mata Sarawak (CMS) in that (i) both are beneficiaries of Sarawak’s

development and (ii) have shareholding structures that are linked to former Chief

Minister Taib Mahmud and his family. If investors like CMS as a Sarawak play, SCable

offers a much cheaper exposure with P/E valuations at 50% discount to the former.

Hock Seng Lee (HOLD, TP: RM2.04 )

We reckon that HSL stands out as one of the top contenders to secure one of the 17

PBH packages. Given the swampy terrain of Sarawak, HSL will be able to leverage on

its marine engineering expertise to execute the job. Although HSL’s orderbook of

RM770m is thin (1.3x cover ratio), securing a package of the PBH would provide the

much needed boost, potentially doubling it assuming a contract sum of RM1bn and

70% stake. We have not priced in any contract wins from the PBH. Our TP is raised

from RM1.75 to RM2.04 as we tag a higher P/E multiple of 14x (from 12x) to reflect the

impending upswing in Sarawak job flows. While acknowledging HSL’s healthy balance

sheet and commendable execution, we feel it is difficult to advocate a Buy rating in

view of its flattish earnings outlook over the near term.

Other beneficiaries not within our coverage

Although not within our coverage, we highlight CMS as a potential Sarawak election

play as it stands to potentially benefit from the PBH via (i) the supply of aggregates and

(ii) its JV with Bina Puri securing construction works. It is also a direct beneficiary of

Sarawak’s development given its monopoly of cement in the state. On the other hand,

Naim Holdings (JV with Gamuda) is touted to be the frontrunner for one of the earlier

PBH packages. Other names include TRC Synergy which is (i) the only Peninsular

based contractor with a UPK Class A licence in Sarawak enabling it to undertake state

funded jobs and (ii) one of the few Peninsular players that has executed quite a sizable

amount of work in Sarawak (RM1bn). Lastly, we highlight Sarawak logistics player

Harbour Link Group which should benefit from the state’s development resulting to

greater demand for project cargo logistics.

Figure #16 Potential Sarawak Election plays

Stock Mkt Cap (RM m)

Price (RM)

Target (RM)

Rating FYE P/E P/B

ROE (T1) Yield (T1) CY15 CY16 T1 T2

SCable 469 1.48 2.57 BUY Dec 12.1 8.6 1.4 1.3 12.4% 2.5%

HSL 1,061 1.93 2.04 HOLD Dec 14.2 13.2 1.6 1.5 11.9% 1.4%

CMS 5,404 5.03 NA Not Rated Dec 23.1 18.1 2.7 2.5 11.7% 1.9%

Naim 588 2.48 NA Not Rated Dec 11.0 8.6 0.5 0.5 4.0% 1.5%

TRC 175 0.365 NA Not Rated Dec 7.3 8.5 0.5 0.5 7.0% 2.7%

Harbour 491 2.70 NA Not Rated June 8.4 8.7 NA NA 20.0% 2.4%

HLIB estimates

Note: T1 refers to most immediate forecast year, T2 refers to the year after T1. For “non-rated” stocks, estimates based on consensus.

HLIB Research | Sarawak Elections

www.hlebroking.com

Page 12 of 12

15 February 2016

Disclaimer

The information contained in this report is based on data obtained from sources believed to be reliable. However, the data and/or sources have not been independently verified and as such, no representation, express or implied, is made as to the accuracy, adequacy, completeness or reliability of the info or opinions in the report.

Accordingly, neither Hong Leong Investment Bank Berhad nor any of its related companies and associates nor person connected to it accept any liability whatsoever for any direct, indirect or consequential losses (including loss of profits) or damages that may arise from the use or reliance on the info or opinions in this publication.

Any information, opinions or recommendations contained herein are subject to change at any time without prior notice. Hong Leong Investment Bank Berhad has no obligation to update its opinion or the information in this report.

Investors are advised to make their own independent evaluation of the info contained in this report and seek independent financial, legal or other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise represent a personal recommendation to you.

Under no circumstances should this report be considered as an offer to sell or a solicitation of any offer to buy any securities referred to herein.

Hong Leong Investment Bank Berhad and its related companies, their associates, directors, connected parties and/or employees may, from time to time, own, have positions or be materially interested in any securities mentioned herein or any securities related thereto, and may further act as market maker or have assumed underwriting commitment or deal with such securities and provide advisory, investment or other services for or do business with any companies or entities mentioned in this report. In reviewing the report, investors should be aware that any or all of the foregoing among other things, may give rise to rea l or potential conflict of interests.

This research report is being supplied to you on a strictly confidential basis solely for your information and is made strictly on the basis that it will remain confidential. All materials presented in this report, unless specifically indicated otherwise, is under copyright to Hong Leong Investment Bank Berhad. This research report and its contents may not be reproduced, stored in a retrieval system, redistributed, transmitted or passed on, directly or indirectly, to any person or published in whole or in part, or altered in any way, for any purpose.

This report may provide the addresses of, or contain hyperlinks to, websites. Hong Leong Investment Bank Berhad takes no responsibility for the content contained therein . Such addresses or hyperlinks (including addresses or hyperlinks to Hong Leong Investment Bank Berhad own website material) are provided solely for your convenience. The information and the content of the linked site do not in any way form part of this report. Accessing such website or following such link through the report or Hong Leong Investment Bank Berhad website shall be at your own risk. 1. As of 15 February 2016, Hong Leong Investment Bank Berhad has proprietary interest in the following securities covered in this report: (a) -. 2. As of 15 February 2016, the analysts, Jeremy Goh, who prepared this report, have interest in the following securities covered in this report: (a) -.

Published & Printed by

Hong Leong Investment Bank Berhad (10209-W)

Level 23, Menara HLA No. 3, Jalan Kia Peng 50450 Kuala Lumpur Tel 603 2168 1168 / 603 2710 1168

Fax 603 2161 3880

Equity rating definitions

BUY Positiv e recommendation of stock under coverage. Expected absolute return of more than +10% ov er 12-months, with low risk of sustained downside. TRADING BUY Positiv e recommendation of stock not under coverage. Expected absolute return of more than +10% ov er 6-months. Situational or arbitrage trading opportunity . HOLD Neutral recommendation of stock under coverage. Expected absolute return betw een -10% and +10% over 12-months, with low risk of sustained downside. TRADING SELL Negativ e recommendation of stock not under coverage. Expected absolute return of less than -10% ov er 6-months. Situational or arbitrage trading opportunity.

SELL Negativ e recommendation of stock under coverage. High risk of negative absolute return of more than -10% ov er 12-months. NOT RATED No research coverage and report is intended purely for informational purposes.

Industry rating definitions

OVERWEIGHT The sector, based on weighted market capitalization, is expected to have absolute return of more than +5% ov er 12-months. NEUTRAL The sector, based on weighted market capitalization, is expected to have absolute return betw een –5% and +5% over 12-months. UNDERWEIGHT The sector, based on weighted market capitalization, is expected to have absolute return of less than –5% ov er 12-months.