biogas market analysis brazil - eth z · amazonas manaus 3,167,668 42,023,218 13,043 roraima boa...

TRANSCRIPT

Biogas Market Analysis Brazil

Potential of Energy generation through fermentation of municipal solid waste

Nicolas Briner

20.04.2011

2

Table of Contents 1. Introduction ......................................................................................................................................... 3

2. Background .......................................................................................................................................... 3

3. Objectives ............................................................................................................................................ 4

4. The Processes of a dry fermentation plant ......................................................................................... 4

5. General Information Brazil .................................................................................................................. 7

5.1. Demography ................................................................................................................ 7

5.2. General Economy ........................................................................................................ 8

5.3. Economic policy .......................................................................................................... 9

5.4. Political System, government and territorial communities ....................................... 10

6. Waste management systems in Brazil ............................................................................................... 10

6.1. Structure .................................................................................................................... 10

6.2. Per capita and total municipal solid waste generation .............................................. 11

6.3. Municipal solid waste composition ........................................................................... 11

6.4. Collection and transport of household waste ............................................................ 12

6.5. Treatment and disposal of household waste .............................................................. 12

6.6. Separated waste collection and cost development .................................................... 13

6.7. Municipal solid waste streams in Brazil ................................................................... 15

6.8. Waste management plan ............................................................................................ 17

6.8. Compost Market in Brazil ......................................................................................... 17

6.9. Summary for potential biogas plants concerning waste management ...................... 18

7. State of affairs in the renewable energy sector ................................................................................ 19

7.1. Characteristic of the renewable energy market ......................................................... 19

7.2. Development in the Electricity generation ................................................................ 20

7.3. Main companies in the Electricity generation sector ................................................ 21

7.4. Market potential of renewable energies .................................................................... 22

7.5. Development of electricity prices ............................................................................. 22

7.6. Basic conditions for the renewable energy sector ..................................................... 23

7.7. Summary for potential biogas plants concerning renewable energies ...................... 25

8. Summary, Opportunities & Threats .................................................................................................. 26

3

1. Introduction

In times of strong economic growth of large nations such as China, India or Brasil it gets more and

more important for these countries to guarantee the increased demand of electricity. But electricity

production goes often hand in hand with high CO2-Emissions, storage of hazardous waste, invasion

into flora and fauna et cetera.

It is therefore of utmost importance that Politics, Economy and particularly energy supply industry

not only quest for profit, but also take regards to Nature and assume responsibility for future

generations. Incidents such as global warming, western states dependency from the oil or the

recently occurred nuclear accident in Fukushima pushes the focus on a reliable and sustainable

energy supply. The increase in the demand of electricity as an energy type represents one of the

biggest challenges in the 21th century.

The claim for sustainable power supply establishes heavy discussions: Many people nowadays are

convinced, that electricity from nuclear and gas power plants must be substituted by power from the

sun, wind, water or biomass.

2. Background

In line with the lecture "Energy Economics and Policy", this exposition deals with the potential of

production of Biogas in Brazil from dry fermentation process. Biogas can be produced through

fermentation of organic waste such as leftovers from the kitchen or green waste. Due to the demand

of sustainable power supply, this assignment will not cover renewable primary products as an input

material for fermentation. Rather this work will concentrate on the potential of organic municipal

waste.

Municipal waste (MSW) can cause all sorts of problems due to the content of organic material among

other things. It often stinks, attracts vermin and creates eyesores. More seriously, it can release

harmful chemicals into the soil and water when dumped or into the air when burned. It is the source

of almost 4% of the world's greenhouse gases1.

This research focuses on the market opportunities of companies handling with Biogas production

through fermentation. First we will take a closer look at the dry fermentation process, followed by

the macroeconomic environment of Brazil, such as demography, economy and policy. Consecutively

1 The Economist. Talking rubbish (2009)

4

we will analyze the generation of waste in brazil and its potential as an input material for

fermentation plants. Subsequent to this, the actual state of affairs in the renewable energy sector

(such as electricity generation from renewables, legislation, incentives and other things) will be

discussed . At the end a SWOT analysis will summarize this research.

3. Objectives

The objective of this assignment is to evaluate business opportunities within the brazilian renewable

energy sector for firms offering fermentation technology to produce biogas using organic waste from

residential, commercial (restaurants), institutional, or industrial sources as input material. In order

that a Biogas plant through fermentation technology runs cost-effective, the price of waste the

operator gets and the electricity price is of utmost importance. That's why the market potential, the

prices, the competition and the regulative environment in the waste and energy sector will be

analyzed closely in this research.

The main objectives are defined as follows:

General: - what does the macroeconomy in Brazil look like

Waste: - how much municipal waste is generated in Brazil, Composition of waste

- what is the infrastructure and logistics system

- how is the waste disposed or used

- who are the main stakeholders dealing with waste

- what's the regulative environment

Energy: - how much energy is used, how much is produced

- how is the energy market composed

- what are the key regulations affecting the renewable energy market

- who is the key player in the energy market

- what regulations do exist in the energy market

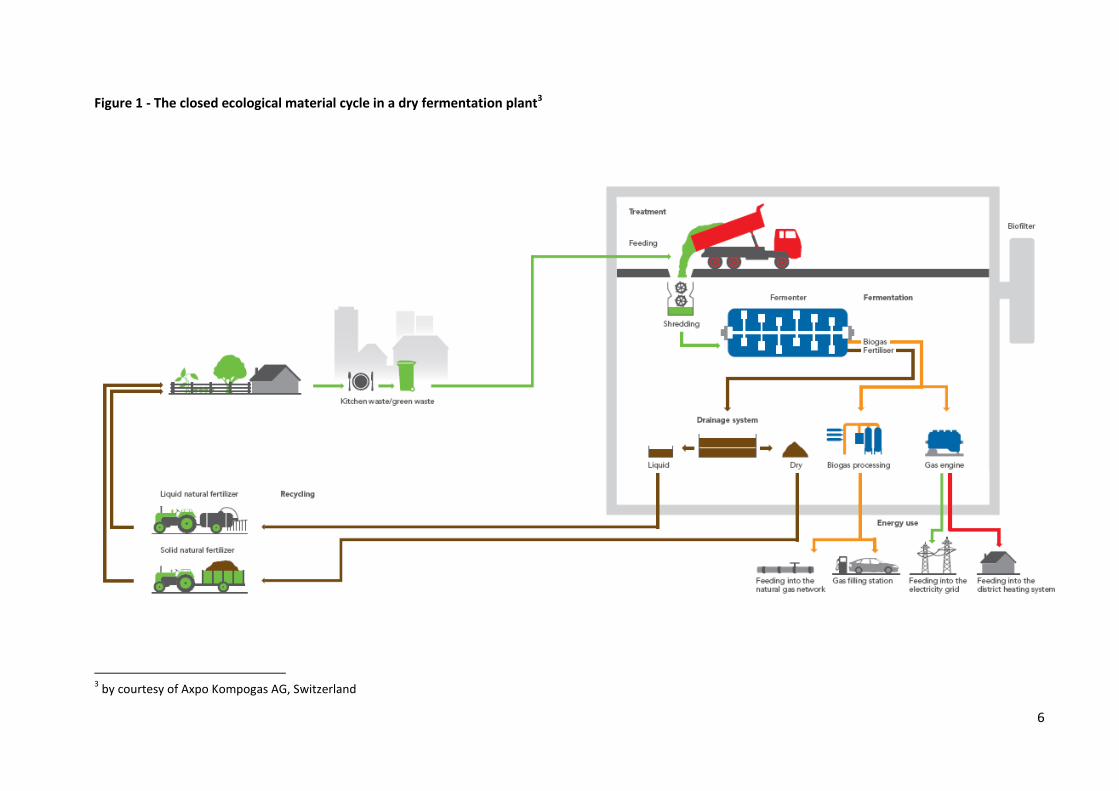

4. The Processes of a dry fermentation plant

As already mentioned, CO2-neutral Biogas can be obtained through fermentation of organic waste as

a renewable source. Under organic waste we understand green waste from local authorities or

private gardens, food waste from household kitchens, catering, restaurants and from industrial or

5

commercial operators. Fermenting solid organic waste can thus be seen as a move away from the

waste economy towards a resource economy.

As an example we will look at the dry anaerobic fermentation process of a Kompogas plant with his

different steps (see Figure 1) 2.

1) The collected organic waste is deposited in a deep bunker. This bunker is equipped with an

automatic crane conveying the biowaste to the next station, where it is shredded and filtered.

2) The shredder hackles the organic waste to a defined maximum particle size. The Filter helps to find

particles with bigger sizes, which are returned back to the deep bunker via an overflow system. The

processed substrate is then weighted and conveyed to the Fermenter.

3) The fermenter is the heart of a fementation plant. The biowaste is fermented by Microorganisms,

which produce CO2-neutral biogas. These Microorganisms work in a thermophilic environment

(55:C) without the presence of oxygen, i.e. anaerobically. This temperature and the fermentation

time of 14 days ensure that the organic waste is freed of germs and spores and hence fully sanitized.

4) The produced CO2-neutral Biogas is than used in a combined heat and power plant to generate

heat and electricity or, after applying a further process, is fed into the natural gas network. A small

amount of the generated heat is used for heating the fermenter. It is also possible to feed the heat

into a district heating network. The generated power is fed into the public electricity grid.

5) The residue leaving the fermenter (fermented product) is conveyed to so called screw presses.

These presses separate the fermented product into solid and liquid components. After sieving, the

solid components can be directly used in the agricultural industry as an organic fertilizer and soil

improver or simply be composted; the liquid component can also be used as an organic fertilizer. In

this way, the ecological material cycle gets closed.

Summing up, we can observe how organic waste is used as a resource to build the following

products:

- CO2-neutral electricity

- CO2-neutral gas

- CO2-neutral heat

- organic fertilizers and compost

2 by courtesy of Axpo Kompogas AG, Switzerland: www.axpo-kompogas.ch

6

Figure 1 - The closed ecological material cycle in a dry fermentation plant3

3 by courtesy of Axpo Kompogas AG, Switzerland

7

5. General Information Brazil

5.1. Demography

The brazilian population is projected by the "Instituto Brasileiro de Geografia e Estatistica" (IBGE) to

be 183'888'895 inhabitants in 2007 (no newer official data available). Estimates already postulate a

population of nearly 200 million in 2011. According to that, Brazil belongs to one of the most

populated nations in the world. It's population growth rate is 1.01%, compared to the European

Union's 0.16%. The birth rate of 16.3 per 1'000 is higher than in any european country.

8

Table 1 - Demographic Data Brazil4 / 5

1 Real = 0.55 USD in 2007

According to this table the highly populated areas are situated on the eastern coast, so that

municipal waste should accumulate in these areas, i.e. these regions offer a good fundament for

building biogas plants working through fermentation of organic and green waste.

5.2. General Economy6

With a GDP of more than 1'600 Billion USD in 2010 Brazil belongs to the 10 biggest economies of the

world. GDP per capita is about 8'300 USD. 67% of GDP is obtained by the service sector, 27% by the

industrial sector and 6% by the agricultural sector.

4 IBGE 2007,

http://www.ibge.gov.br/home/estatistica/populacao/contagem2007/populacao_ufs_05102007.pdf 5 IBGE 2007, http://www.ibge.gov.br/home/estatistica/economia/pibmunicipios/2003_2007/tab01.pdf

6 Deutsches auswärtiges Amt and SECO

region capital population GDP (1000 R$) GDP/cap

Rondônia Porto Velho 1,454,237 15,002,734 10,320

Acre Rio Branco 653,620 5,760,501 8,789

Amazonas Manaus 3,167,668 42,023,218 13,043

Roraima Boa Vista 394,192 4,168,599 10,534

Pará Belém 7,070,867 49,507,144 7,007

Amapá Macapá 585,073 6,022,132 10,254

Tocantins Palmas 1,248,158 11,094,063 8,921

Maranhão Saõ Luís 6,117,996 31,606,026 5,165

Piauí Teresina 3,029,916 14,135,870 4,662

Ceará Fortaleza 8,183,880 50,331,383 6,149

Rio Grande do Norte Natal 3,014,282 22,925,563 7,607

Paraíba João Pessoa 3,640,538 22,201,750 6,097

Pernambuco Recife 8,487,072 62,255,687 7,337

Alagoas Maceió 3,014,979 17,793,227 5,858

Sergipe Aracaju 1,938,970 16,895,691 8,712

Bahia Salvador 14,079,966 109,651,844 7,787

Minas Gerais Belo Horizonte 19,261,816 241,293,054 12,519

Espírito Santo Vitória 3,351,327 60,339,817 18,003

Rio de Janeiro Rio de Janeiro 15,406,488 296,767,784 19,245

São Paulo São Paulo 39,838,127 902,784,268 22,667

Paraná Curitiba 10,279,545 161,581,844 15,711

Santa Catarina Florianópolis 5,868,014 104,622,947 17,834

Rio Grande do Sul Porto Alegre 10,582,324 176,615,073 16,689

Mato Grosso do Sul Campo Grande 2,265,021 28,121,420 12,411

Mato Grosso Cuiabá 2,854,456 42,687,119 14,954

Goiás Goiânia 5,644,460 65,210,147 11,548

Distrito Federal Brasília 2,455,903 99,945,620 40,696

Total 183,888,895 2,661,344,525

9

Figure 2 - GDP by sectors

In 2008 the positive development of Brazil's economy has been interrupted by the global financial

crisis. Nevertheless, the country was one of the first emerging markets to leave the path out of the

crisis. The GDP already started to grow in the second term of 2009 and the central Bank states a GDP

growth of about 5% in 2010. Besides this, Brazil's rate of unemployment is quite low and accounted

for about 6.9% in 2010.

One of the biggest challenge for the brazilian economy is still the large inflation and the gap between

a rich, well educated minority and a poor educated majority living at the edge of the poverty line.

5.3. Economic policy7

Brazil is a country benefitting a lot from the raw material market boom in the past few years. It

achieved considerable trade surplus which has been used for reducing the foreign indebtedness. In

addition, the inflation rate has been reduced considerably in the past few years thanks to a stability-

oriented monetary policy.

The brazilian program for Acceleration of the economic growth PAC of 2007 (Programa da

Aceleraςão do Crescimento) planned investments of more than 1.1 trillion R$ (~380 billion Euro) until

2010, mainly into infrastructure. Until the end of 2009, 403 Billion R$ of the investment sum has

already been spent and of 1'500 Projects more than 40% have been completed.

7 Deutsches auswärtiges Amt

67%

27%

6%

service sector

industrial sector

agricultural sector

10

The industrial aid program PDP (Plano de Desenvolvimento Produtivo, 2008-2011) plans to

strengthen the international competitiveness of brazilian companies through tax reduction and

financial subsidies of about 90 billion Euros.

Brazil hopes for a outstanding growth spurt thanks to the world cup 2014, the olympics 2016 and

through the exploitation of crude oil and natural gas-resources, which have been discovered 2008 at

the southeastern atlantic coast.

5.4. Political System, government and territorial communities8

Brazil is a presidential federal republic. It consists of a federal government, federal states and local

authorities. The legislative in the federal government is executed by the national congress (chamber

of deputies and senate). The 513 deputies are voted for 4 years, the senators for 8 years. The

president is elected by an absolute majority of votes from the population for a time of 4 years. He

can be reelected for a second period of office.

Since 2011, Dilma Rousseff from the labor party (PT) displaces Luiz Inácio Lula da Silva as president.

Brazil is segmented into 26 federal states and 1 federal district with the capital Brasilia. The federal

districts exhibit own constitutions, which must conform to the principles of the federal constitution.

6. Waste management systems in Brazil

6.1. Structure

The solid waste management industry provides a vital public service that ensures the health and

safety of citizens across the country.

The most important waste management companies in Brazil are shown in the following table9:

Table 2 - Waste management companies in Brazil

Waste collection Ecourbis Ambiental S.A.

Logística Ambiental des São Paulo S.A. - LOGA

Waste transport

Belgoprocess

Itautec Philco S.A.

Whirlpool

8 Deutsches auswärtiges Amt

9 www.retech-germany.net

11

Waste treatment and recycling

Catadores

Ativa Reciclagem Ltda.

Belmont trading comercial Exportadora Ltda.

GM&C

TCG Recycling Brazil

Waste disposal and elimination

ESSENCIS

ESTRE

PAJUAN

6.2. Per capita and total municipal solid waste generation

In 2007, Brazilians generated about 46 Mio tons of municipal solid waste. This is consistent with an

amount of 243 kg per capita. Municipal solid waste (MSW) is mainly managed by waste management

companies and it is compounded by municipal solid wastes coming from residential, commercial

(restaurants), institutional, or industrial sources. MSW as defined in the following paragraphs does

not include construction and demolition debris, biosolids (sewage sludges), industrial process wastes,

or a number of other wastes that, in some cases, may go to a municipal waste landfill.

Figure 3 - Generation of municipal solid waste in 200710

6.3. Municipal solid waste composition

Native organic makes the largest component of household waste in 200711. The organic fraction,

which can be used as input material for fermentation plants to produce biogas, accounts for more

than 50 percent on average, whereas in poorer regions it can increase to 75 percent. Paper and

cardboard account for about 25 percent, whereas glass, plastic and metal form a very small part in

10

IBGE and CETSB 11

Technische Universität Braunschweig: http://www.lwi.tu-bs.de/abwi/publikationen/Biologische%20Verfahren%20in%20Entwicklungslaendern.pdf

12

the household waste. Other miscellaneous wastes make up approximately 16% percent of the MSW

produced at households.

Figure 4 - Composition of municipal solid waste

6.4. Collection and transport of household waste

There exist a wide gap in the collection and transport structures of MSW: In the wealthier south of

Brazil 100% of citizens are installed to garbage collection, whereas in the poorer north the quota can

be lower than 50%12. Many communes, particularly in the south of Brazil, have privatized the garbage

collection and transport. Only about 14% of citizens are connected to separate waste collection.

Separate waste collection thereby is an important fundament for the successful introduction of

fermentation plants.

6.5. Treatment and disposal of household waste13

The situation in the treatment and disposal of household waste is very unequal and dependent on

the region, state or city people live. In 2008, only 39% of cities or communes countrywide (15% in the

12

www.retech-germany.net 13

http://earth911.com/news/2009/08/17/trash-planet-brazil/

0%

10%

20%

30%

40%

50%

60%

Brazil

Rio de Janeiro

Ilhabela

13

North) exhibited adequate landfill dumps. But as can be observed in the following picture, using the

example of São Paulo, much has been done in the past few years to improve the landfills. 14

Figure 5 - Classes of waste disposal in Saõ Paulo

In countries like Brazil where waste management systems are run by individual municipalities rather

than the federal government, the nation’s larger cities are often at an advantage. This is because a

large city will likely have more resources and a greater revenue stream to apply to its waste

operations.

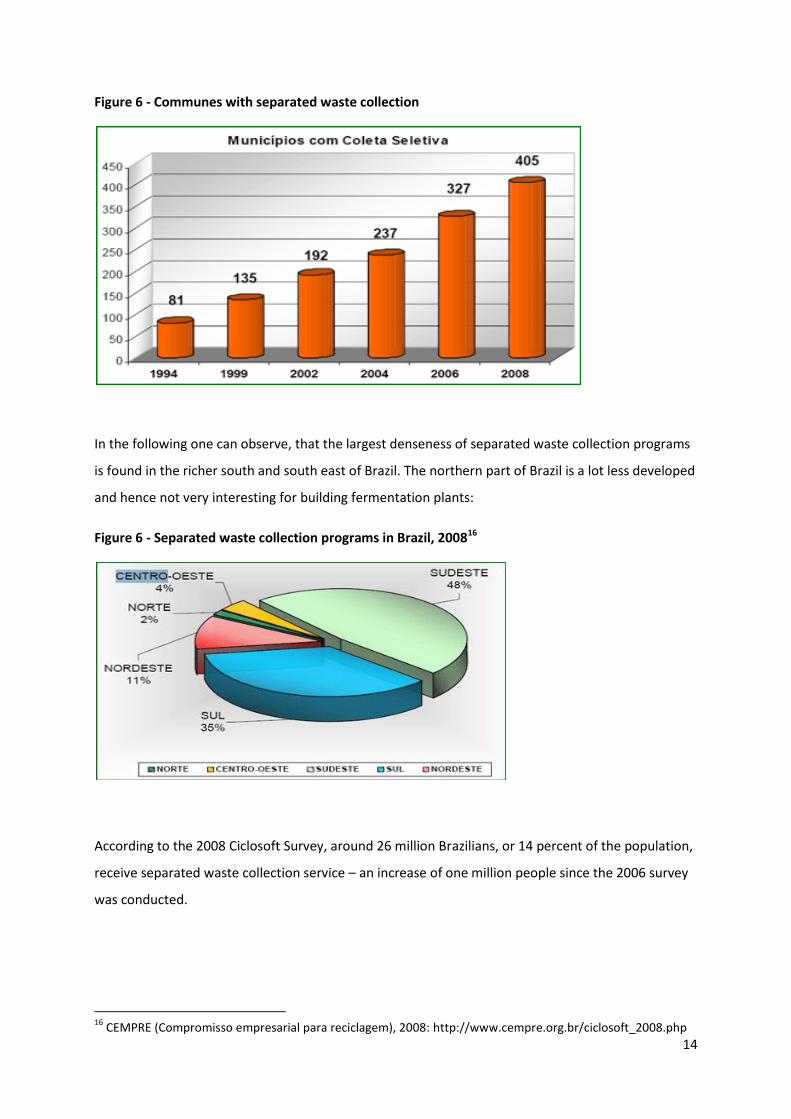

6.6. Separated waste collection and cost development

As already mentioned, the separated waste collection in Brazil is still in his initial status. Data

collected in the2008 Ciclosoft survey15, reported by CEMPRE News, reveals that 405 Brazilian

municipalities do separate waste materials, representing 7 percent of the country’s total

municipalities. The number of municipalities separating their waste increased nearly 25 percent since

the 2006 survey, which reported that only 327 were sorting their trash.

The waste collection systems in these 405 municipalities use a combination of operating methods.

According to CEMPRE News, 50 percent of the municipalities use door-to-door service, 26 percent

use collection points and 43 percent collaborate with street waste picker cooperatives.

14

www.retech-gernamy.net 15

CEMPRE (Compromisso empresarial para reciclagem), 2008: http://www.cempre.org.br/ciclosoft_2008.php

14

Figure 6 - Communes with separated waste collection

In the following one can observe, that the largest denseness of separated waste collection programs

is found in the richer south and south east of Brazil. The northern part of Brazil is a lot less developed

and hence not very interesting for building fermentation plants:

Figure 6 - Separated waste collection programs in Brazil, 200816

According to the 2008 Ciclosoft Survey, around 26 million Brazilians, or 14 percent of the population,

receive separated waste collection service – an increase of one million people since the 2006 survey

was conducted.

16

CEMPRE (Compromisso empresarial para reciclagem), 2008: http://www.cempre.org.br/ciclosoft_2008.php

15

The average costs of collection and sorting of separated waste has been increasing in the past ten

years and account for about 221 USD in 2008 according to a cyclosoft survey of CEMPRE17. The costs

per ton are about 5 times higher than for conventional waste collection.

Table 3 - Costs of separated waste collection

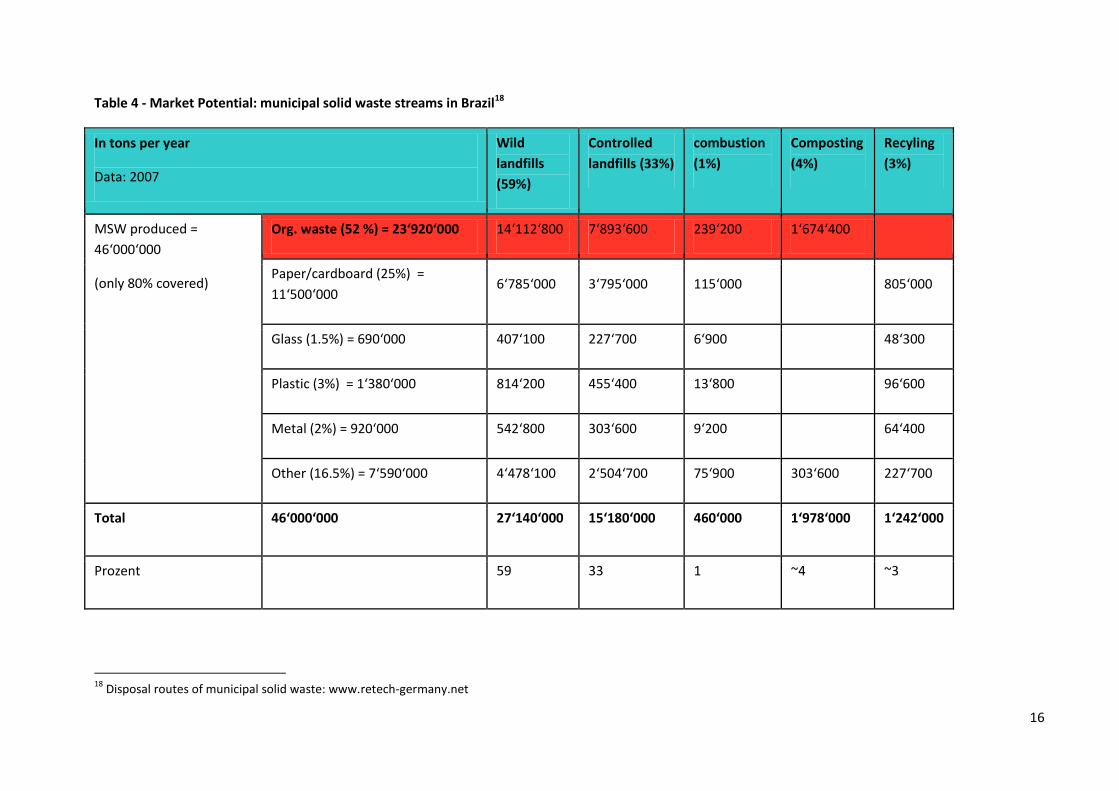

6.7. Municipal solid waste streams in Brazil

The following table shows a summary of the municipal solid waste streams in Brazil. As we can see,

brazil relies on dumps and landfills. Mainly all the waste (>90%) is still landiflled and not used for

energy recovery, composting or recycling. Incineration is a relatively effective method, however

incinerators are expensive to purchase, operate and maintain, eliminating them as an option for

most of the cities in Brazil. The same applies to fermentation plants.

17

CEMPRE (Compromisso empresarial para reciclagem), 2008: http://www.cempre.org.br/ciclosoft_2008.php

16

Table 4 - Market Potential: municipal solid waste streams in Brazil18

In tons per year

Data: 2007

Wild

landfills

(59%)

Controlled

landfills (33%)

combustion

(1%)

Composting

(4%)

Recyling

(3%)

MSW produced =

46‘000‘000

(only 80% covered)

Org. waste (52 %) = 23‘920‘000 14‘112‘800 7‘893‘600 239‘200 1‘674‘400

Paper/cardboard (25%) =

11‘500‘000 6‘785‘000 3‘795‘000 115‘000

805‘000

Glass (1.5%) = 690‘000 407‘100 227‘700 6‘900

48‘300

Plastic (3%) = 1‘380‘000 814‘200 455‘400 13‘800

96‘600

Metal (2%) = 920‘000 542‘800 303‘600 9‘200

64‘400

Other (16.5%) = 7‘590‘000 4‘478‘100 2‘504‘700 75‘900 303‘600 227‘700

Total 46‘000‘000 27‘140‘000 15‘180‘000 460‘000 1‘978‘000 1‘242‘000

Prozent 59 33 1 ~4 ~3

18

Disposal routes of municipal solid waste: www.retech-germany.net

17

6.8. Waste management plan19

After 21 years of discussions, the Senate has determined a draft law for the national solid waste

industry. This law has been signed by the president. With this project, the storage of waste on not

allowed open dumps has been forbidden. Each commune is obligated to provide a a state of the art

disposal. Furthermore the communes and citizens are pledged to separate the waste. A further

action introduced is the producer responsibility: Industry and commerce are committed to take back

their packages and in particular products harmful to the environment such as batteries, waste oil,

electric bulbs and so forth. The overriding aim however is the cleansing of open dumps and the

improvement of the dump standards. It is enjoyable, that multiple states have already developed

waste management plans (i.e. São Paulo, Pernambuco, Rio Grande do Sul). This gives hope for a

positive evolution in the health and waste management sector.

6.8. Compost Market in Brazil

The compost market in Brazil is still very small and not developed: only about 4% of organic waste is

composted. Nevertheless, the Potential is enormous, since the organic fraction possesses a high

share in the household wast. Nevertheless, there are a few landfill-composting CDM(clean

development mechanism) projects in Brazil. With higher sensibility for the waste problems caused by

open dumps, the compost market will achieve a positive development in the next years.

19

Handelskammer Niederösterreich: http://portal.wko.at/wk/format_detail.wk?AngID=1&StID=563904&DstID=680&titel=Brasilien:,Wird,es,ernst,mit,der,%E2%80%9Eordentlichen%E2%80%9C,M%C3%BCllverwertung?

18

6.9. Summary for potential biogas plants concerning waste management

Market potential Price development Competitive environment Regulative environment

► large population

► high share of the organic

fraction in municipal

solid waste

► new legislation brings

drive in the separated

waste collection

dynamic

► price for waste is between

30 und 130 USD/t,

depending on the region

► insufficient information to

determine a trend

► wide regional discrepances

► Competition exists mainly

between Recycling

companies

► competition on organic

waste still quite small

► compost market not really

existent, no competition

► new waste management

plan is introduced

► Encouragement in

separated waste collection

► landfill-ban of waste brings

potential for other disposal

possibilities

► Implementation has to be

wait and seen

19

7. State of affairs in the renewable energy sector

7.1. Characteristic of the renewable energy market

As shown in the following figure, total primary energy supply in 2007 accounts for 235'556 ktoe20 .

Oil, comb. renew. & waste and hydro represent the biggest share, whereas the rest only sums up for

about 15 percent.

Figure 7: - Share of total primary energy supply in 2007

Concerning the electricity generation, Brazil has a comparatively CO2-emission poor energy system.

Hydro makes by far the biggest part in the production of electricity, as shown in the following figure:

Figure 8 - Electricity generation by fuel

20

iea.org

20

7.2. Development in the Electricity generation21

When we look at the development in the electricity generation of the past few years, we can discover an increase in the fossil fired thermal power plants,

whereas a decrease in electricity generated by hydro power can be detected. The following figure constitutes this development:

Table 5 - Installed electricity generation capacity in kW

21

ANEEL: Agencia Nacional de Energia Elétrica, http://www.aneel.gov.br/aplicacoes/capacidadebrasil/capacidadebrasil.asp

Installed capacity: 31. 12. 2009

Typ # Plants Capacity %

Large scale hydropower plants 165 75‘657 70.98

Thermo electrical plants 1‘313 25‘350 23.79

Small scale hydropower plants 356 2‘953 2.77

Nuclear power plants 2 2‘007 1.99

Wind power plants 36 602 0.39

Solar power plants 1 0 0.00

Total 1‘873 106‘569 100.0

Installed capacity: 31. 12. 2001

Type # Plants Capacity %

Large scale hydropower plants 133 61‘554 82.21

Thermo electrical plants 600 10‘481 14.00

Small scale hydropower plants 303 855 1.14

Nuclear power plants 2 1‘966 2.63

Wind power plants 7 21 0.03

Solar power plants 0 0 0.00

Total 1‘045 74‘877 100.0

21

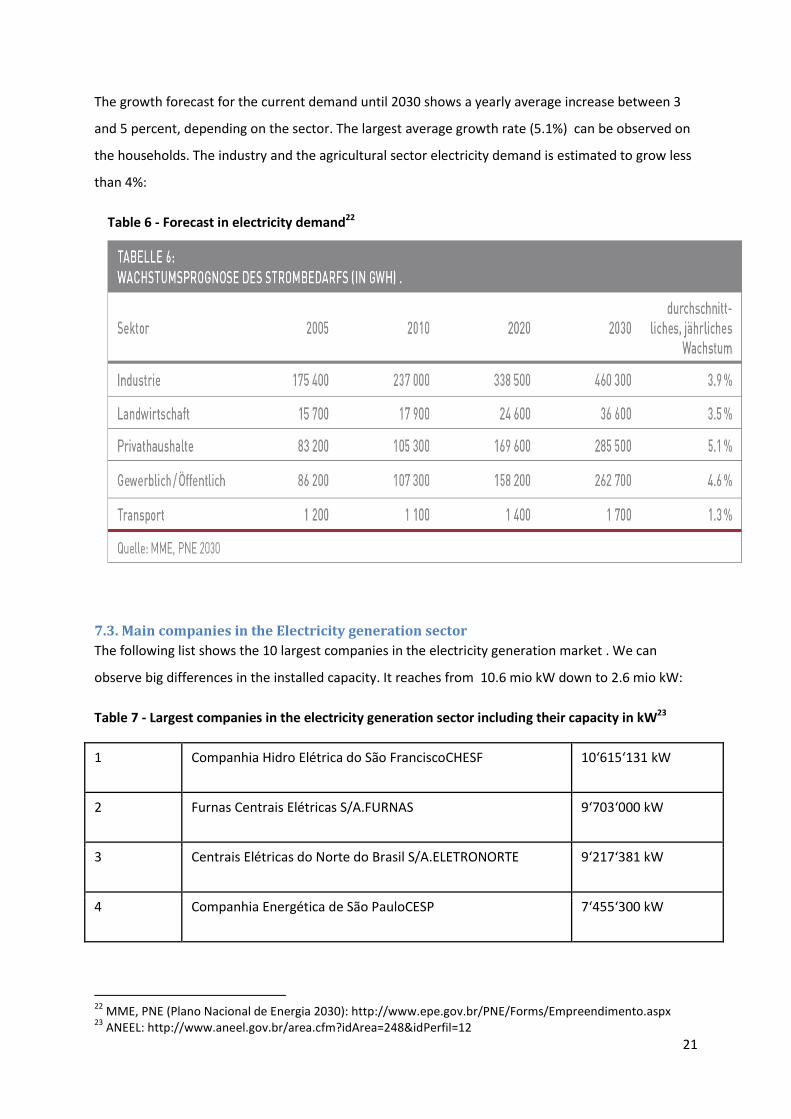

The growth forecast for the current demand until 2030 shows a yearly average increase between 3

and 5 percent, depending on the sector. The largest average growth rate (5.1%) can be observed on

the households. The industry and the agricultural sector electricity demand is estimated to grow less

than 4%:

Table 6 - Forecast in electricity demand22

7.3. Main companies in the Electricity generation sector

The following list shows the 10 largest companies in the electricity generation market . We can

observe big differences in the installed capacity. It reaches from 10.6 mio kW down to 2.6 mio kW:

Table 7 - Largest companies in the electricity generation sector including their capacity in kW23

1 Companhia Hidro Elétrica do São FranciscoCHESF 10‘615‘131 kW

2 Furnas Centrais Elétricas S/A.FURNAS 9‘703‘000 kW

3 Centrais Elétricas do Norte do Brasil S/A.ELETRONORTE 9‘217‘381 kW

4 Companhia Energética de São PauloCESP 7‘455‘300 kW

22

MME, PNE (Plano Nacional de Energia 2030): http://www.epe.gov.br/PNE/Forms/Empreendimento.aspx 23

ANEEL: http://www.aneel.gov.br/area.cfm?idArea=248&idPerfil=12

22

5 Itaipu Binacional I TAIPU 7‘000‘000 kW

6 Tractebel Energia S/ATRACTEBEL 6‘965‘350 kW

7 CEMIG Geração e Transmissão S/ACEMIG-GT 6‘781‘584 kW

8 Petróleo Brasileiro S/APETROBRÁS 5‘291‘067,60 kW

9 Copel Geração e Transmissão S.A.COPEL-GT 4‘544‘870 kW

10 AES Tietê S/AAES TIETÊ 2‘645‘050 kW

7.4. Market potential of renewable energies

The CO2-emission poor electricity generation system in Brazil provokes the government to guarantee

the power supply for the future with increased construction of large scale hydropower plants,

nuclear power plants and fossil fired thermal power plants. Because of the high rate in hydropower

(~75% of total electricity generation), the substitution of power through electricity from waste is not

very attractive for investors interested in CDM-projects (Clean Development Mechanism). The

electricity generation and electricity efficiency projects in Brazil exhibit a much lower CER (carbon

emission reduction) potential than in other countries, which have a high share in fossil electricity

production. Therefore one could think that the Market for electricity generation through

fermentation of Biomass hasn't optimal basic conditions. Nevertheless we can find about 70% of all

CDM-validation projects in the field of renewable energies and energy efficiency24. This development

is based on outstanding conditions in the field of renewable energies: There is a booming agriculture,

large water resources, intensive solar irradiation and good wind potentials. Furthermore Brazil

possesses a deep tradition and experience in Biomass- and hydropowerprojects.

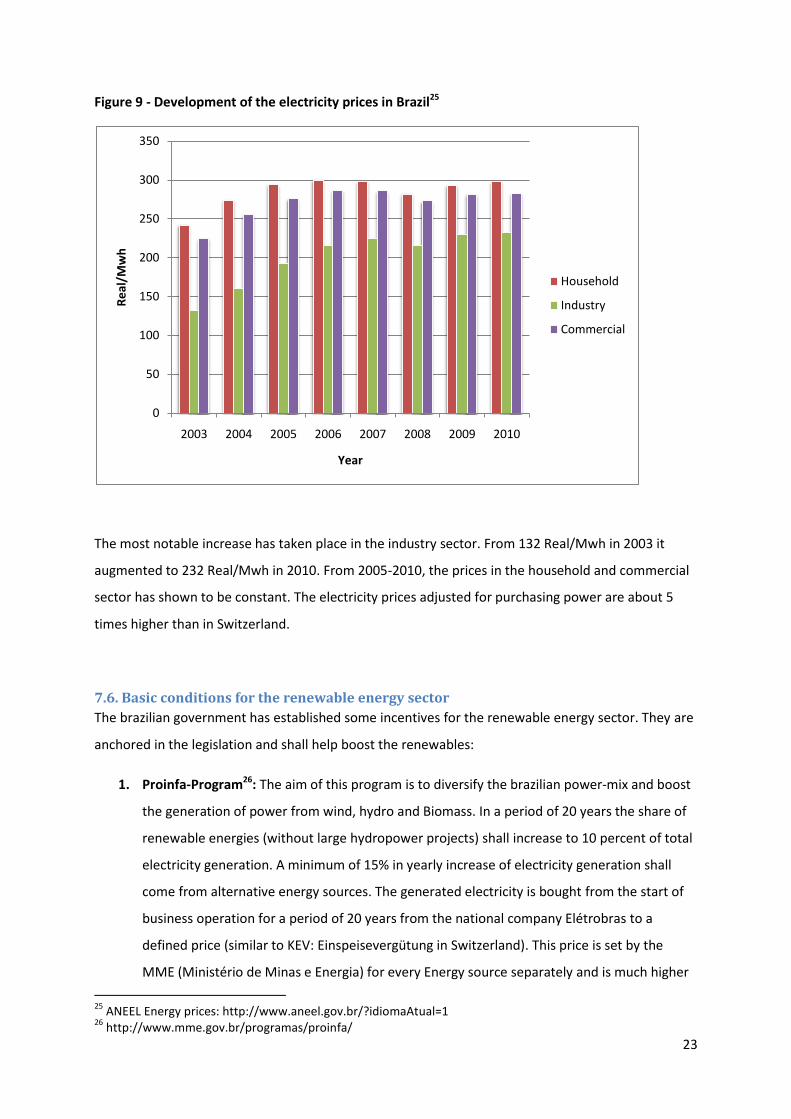

7.5. Development of electricity prices

A good indicator for the potential of renewable energies is the electricity price. High prices make

projects in renewable energies more cost-effective. As we can observe in the following figure, the

prices have been increasing in the past few years:

24

http://www.jiko-bmu.de/files/basisinformationen/application/pdf/cdm_market_overview_brasilien.pdf

23

Figure 9 - Development of the electricity prices in Brazil25

The most notable increase has taken place in the industry sector. From 132 Real/Mwh in 2003 it

augmented to 232 Real/Mwh in 2010. From 2005-2010, the prices in the household and commercial

sector has shown to be constant. The electricity prices adjusted for purchasing power are about 5

times higher than in Switzerland.

7.6. Basic conditions for the renewable energy sector

The brazilian government has established some incentives for the renewable energy sector. They are

anchored in the legislation and shall help boost the renewables:

1. Proinfa-Program26: The aim of this program is to diversify the brazilian power-mix and boost

the generation of power from wind, hydro and Biomass. In a period of 20 years the share of

renewable energies (without large hydropower projects) shall increase to 10 percent of total

electricity generation. A minimum of 15% in yearly increase of electricity generation shall

come from alternative energy sources. The generated electricity is bought from the start of

business operation for a period of 20 years from the national company Elétrobras to a

defined price (similar to KEV: Einspeisevergütung in Switzerland). This price is set by the

MME (Ministério de Minas e Energia) for every Energy source separately and is much higher

25

ANEEL Energy prices: http://www.aneel.gov.br/?idiomaAtual=1 26

http://www.mme.gov.br/programas/proinfa/

0

50

100

150

200

250

300

350

2003 2004 2005 2006 2007 2008 2009 2010

Re

al/M

wh

Year

Household

Industry

Commercial

24

than the usual price. The Proinfa-Program can be found in the paragraphs 10438/02 and

10762/03 of the brazilian legislation. The program has finished in 2010 and doesn't seem to

be renewed.

2. "Luz para todos"27: The aim of this program is the electrification of the rural areas in Brazil.

The majority of people living in rural areas shall be supplied with electricity until the end of

2011. The government offers thereby incentives for plants working with renewable energy :

Subsidies up to 85% of total project costs can be obtained.

3. National program for generation and use of Biodiesel: Since 2009, a share of 4% of Biodiesel

has to be added to the normal Diesel. The share shall increase to 5% until 2013. Producers of

Biodiesel obtain different tax incentives and diverse financing options.

4. Clean Development Mechanism (CDM)28: According to the UNFCCC-Website there exists a

portfolio of 190 registered CDM-projects in Brazil. The emission reduction certificates , which

are effectuated by CDM-projects, account for a share of 44% in latin america. Nevertheless,

the attractiveness of Markets like China or India will never be achieved by Brazil. As already

mentioned, the hydropower accounts for more than 2/3 of the brazilian electricity

generation. Therefore, the baseline in the power sector is very disadvantageous.

Nevertheless, Experts determine the perspectives of projects in the renewable energy sector

as budding, particularly in the fields of bioenergy and wind power.

27

http://luzparatodos.mme.gov.br/luzparatodos/asp/ 28

http://unfccc.int/2860.php

25

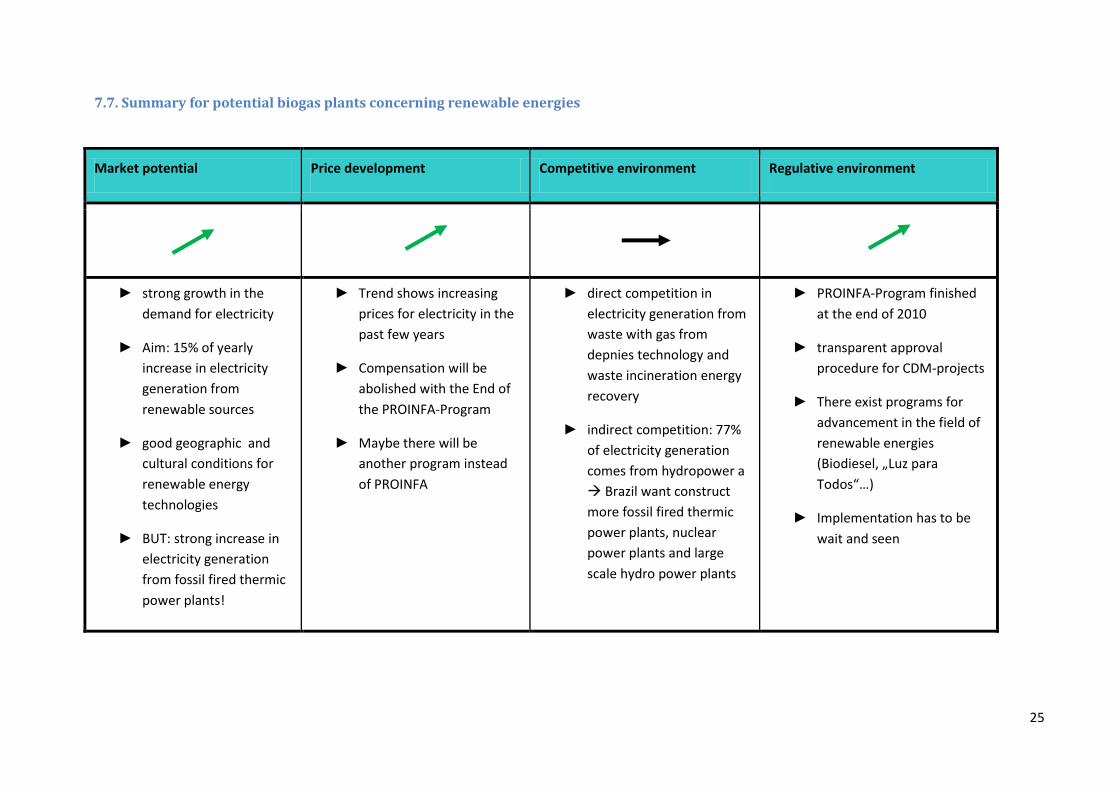

7.7. Summary for potential biogas plants concerning renewable energies

Market potential Price development Competitive environment Regulative environment

► strong growth in the

demand for electricity

► Aim: 15% of yearly

increase in electricity

generation from

renewable sources

► good geographic and

cultural conditions for

renewable energy

technologies

► BUT: strong increase in

electricity generation

from fossil fired thermic

power plants!

► Trend shows increasing

prices for electricity in the

past few years

► Compensation will be

abolished with the End of

the PROINFA-Program

► Maybe there will be

another program instead

of PROINFA

► direct competition in

electricity generation from

waste with gas from

depnies technology and

waste incineration energy

recovery

► indirect competition: 77%

of electricity generation

comes from hydropower a

Brazil want construct

more fossil fired thermic

power plants, nuclear

power plants and large

scale hydro power plants

► PROINFA-Program finished

at the end of 2010

► transparent approval

procedure for CDM-projects

► There exist programs for

advancement in the field of

renewable energies

(Biodiesel, „Luz para

Todos“…)

► Implementation has to be

wait and seen

26

8. Summary, Opportunities & Threats

It seems that the majority of Brazil’s municipal authorities are aware that efficient waste

management is important to citizens. As shown by their willingness to participate in multi-

country conferences, strides towards improvements are being made. As brazilian authorities

continue to seek information regarding better technology and safer practices, and strive to

apply them to waste management operations, the country hopes to continue on a path

toward responsible urban living.

The Energy sector provides a good fundament for a positive evolution of renewably energy

technologies. Many programs and often perfect geographic conditions allow the growth of the

renewable energy market. The following Summary shows the Opportunities & Threats for companies

planning to invest in Biogas Plants producing Energy from municipal solid waste:

Opportunities:

Stable democracy, strong economic growth, solid bank system, advanced industrialization,

"cultural closeness" to Europe and USA.

Huge potential in organic waste from households and industrial & commercial sector,

particularly in eastern and southeastern Brazil. Separated collection in these regions is in

advance.

Earnings from sale of CO2-Emission reduction certificates (CER) according to CDM.

Earning through the sale of fertilizers: The agriculture sector in Brazil is big.

High electricity prices provide a good fundament for cost-effectiv power plants.

Good regulative environment in the field of renewable energies, experience with biomass-

projects are existent.

World cup 2014 and Olypmics 2016 could boost the efforts to present clean cities (reduction

of open dumps) and advancements in the renewable energy sector.

Brazil can act for the investors as a door opener for latin america.

27

Threats:

Insufficient implementation of the regulative environment.

Social problems in city agglomerations.

"green" electricity is already existent. Developments tend to go into fossil fired thermic and

nuclear power plants.

Strong differences in the stages of development in distinct regions (Prices for electricity,

waste management and so forth).

High capital costs in Brazil: about 12% p.a.

Lack of skilled workers.

Malfunctioning of Logistics in Brazil.