booklet eng final - global financial - home

TRANSCRIPT

Annual Report2004

800 Arrow Road, Suite 1100, Toronto Ontario M9M 2Z8Tel: 416-741-7377 Toll free: 1-877-460-7377 Fax: 416-741-8987

www.globalfinancial.ca

President’s Message 1

About the Global Educational Trust Plan 2

Financial Highlights 3

Maximizing Your Investment Return and Minimizing Your Risk 4The Global Educational Trust PlanHelps Parents Fund Their Children’s Education 6-9

Getting the Most from Your Children’s Education Savings Plans 10-11

Education Savings Plan Contest Winner 11

New and Enhanced Government Funding Announcements 12

Registering Your Education Savings Plan 14

Audited Financial Statements 15-26

Contacting Client Services 27

Table of Contents

Annual Report 2004

President’s Message

Many Canadians and the media continued to stress the importance ofeducation as an electoral issue during 2004. The Global EducationalTrust Foundation (GETF) was pleased to hear news in the FederalBudget and from the Alberta government that would have a positiveimpact on our clients.

Our clients may be eligible for theCanada Learning Bond and/orenhancements to the Canada EducationSavings Grant allowing their children toreceive up to $9,200 each from thefederal government. Also, Albertans maybe able to receive up to an additional$800 through the Alberta CentennialEducation Savings grant. I urge you tocontact your Global* Sales Representativeto learn if you are eligible for thisadditional funding.

Our unwavering mission is to providefamilies with the highest qualityEducation Savings Plan. Increasedscrutiny by regulators throughout thefinancial industry has reinforced GETF’sgoal to meet and exceed regulatorystandards and to continue as an industryleader in serving our clients’ needs.

Since the GETF’s inception, familieshave received $4.0 million to fundtheir children’s education. In 2004,approximately $2.6 million in fundingwas made available to families.

The Foundation has continued to grow.At the end of 2004, Invested Assetstotalled $78.9 million – an increase of51% over the $52.2 million in 2003.The number of children enrolledincreased by approximately 22% at theend of 2004, to approximately 44,000across Canada. The Foundationdistributed realized earnings to clientsof between 4.5% to 5% depending ontheir mix of deposits and grants.

GETF’s current and past achievementshelp build a successful future for ourclients. GETF is proud to be part of thethousands of Canadian families savingfor their children’s limitless educationalopportunities through the GlobalEducational Trust Plan. The dedicatedemployees that administer and managethe Global Plan and SalesRepresentatives who distribute theGlobal Plan look forward to helpingparents fund their children’s educationand to serving valued clients like you.

Sam Bouji, Presidentand Chief Executive Officer

1 2

About the Global EducationalTrustPlanThe Global Educational Trust Plan (Global Plan) is an education savings planthat provides a disciplined approach to saving for a child’s education. Whenregistered, the Global Plan offers tax-deferred growth as well as access togovernment funding of up to $9,200 per child. Recent government changesmay make your child eligible for these additional grants. Please consult yourGlobal Sales Representative or Client Services for details.

The Global Plan combines many of the best features found in individualand group scholarship plans—investments that are low-risk, professionallymanaged, and pooled for potentially higher returns.

In addition, the Global Plan offers many flexible plan options making it easierto save. If you miss a payment you won’t forfeit your benefits or be forced tocancel the Global Plan.

Your children are not restricted to Canada for education if they dream ofan approved program beyond our borders. The Global Educational Trust Planoffers a choice of colleges, universities and other recognized programs aroundthe world.

All these benefits help make the Global Educational Trust Plan a superiorchoice for helping parents save for their children’s education.

Although most Education Savings Plans benefit children, the Global EducationalTrust Plan allows Canadian residents of any age to enroll. While the governmentgrants are only available for resident children up to age 17, adults can stillsave for their own future education by taking advantage of several key benefitsthe Global Plan offers—such as tax-deferred growth.

The FoundationThe Global Educational Trust Foundation (GETF) is a not-for-profit organizationwhose primary objective is to provide financial assistance to students enrolledat approved post-secondary educational institutions. As sponsor and administratorof the Global Educational Trust Plan, the Foundation is considered to be thepromoter.

Global Educational Marketing Corporation (GEMC)GEMC manages and administers the Global Plan and facilitates the applicationfor government grants in behalf of our clients. GEMC is also the primary distributorof the Global Plan.

Incorporated in 1996, GEMC has grown to serve Canadians with approximately1,000 licensed representatives located in regional offices in Vancouver, Calgary,Toronto, Montreal and Halifax as well as in affiliate offices across the country.

If you have any questions, please feel free to visit our Web site atwww.globalfinancial.ca or call us toll free at 1-877-460-7377.

*Global Educational Marketing Corporation, Global Maxfin Investments Inc. or approved distributor.

3 4

Financial Highlights Maximizing Your Investment Returnand Minimizing Your Risk

The Global Educational Trust Foundation understands that our clientsplace a high value on their children’s future education and do not wishto take unnecessary investment risks. That’s why the Global EducationalTrust Plan invests mainly in Provincial Government and Government ofCanada bonds and treasury bills.

In addition, the Global Plan isprofessionally managed to takeadvantage of investment opportunitiesand to help ensure that our clients getthe best return possible. The Global Planinvests larger amounts by combiningclient contributions. This pooling of fundsallows the Global Plan to obtain betterrates than individual investors could ifthey invested with the same degreeof safety.

If someone held a conventional GIC(Guaranteed Investment Certificate)for a five-year term at a major CanadianBank, they would have averaged 2.92%*

for 2004. The GETF net distributions ofrealized income after fees ranged from4.5% to 5.0%, depending on the individual’smix of deposits and grants.

*Average of 5-year Chartered BankAdministered Interest Rates for GICs.Source: Bank of Canada Web site

Global Educational Trust Plan Portfolio Asset Allocation

Invested Assets

53% Government of Canada Federal Guaranteed Bonds

2% Business Development Bank of Canada Index linked notes

8% Corporate Bonds

6% Government of Canada T-Bills, Short-term Deposits and Cash Account

31% Provincial Government Guaranteed Bonds

Nominees

Accumulated CESG deposits Funding to families

2004 $78,901,102*

$17,622,294

$12,396,787

$2.6 million

$1.4 million

$52,207,088* 36,000

44,000

2003

2004

2003

2004

*Investments, cash and accrued income.

2003

2004

2003

6

The Global Educational Trust Plan HelpsParents Fund Their Children’s Education.

Canadian families continue to benefit from the Global Educational TrustPlan (Global Plan) for assistance in paying increasing education costssuch as tuition, books, meals, travel and accommodation. In 2004, theyaccessed approximately $2.6 million in funding for education. The following arejust a few of the families that were helped by the Global Plan.

Mr. Nabil Abu Thuraia andMrs. Shamieh Al KhatibMontreal, QuebecThe family feels fortunate that theyinvested in a Global Education SavingsPlan. Afnan Thuraia, their daughter, wasable to pay for her tuition without havingto apply for student loans. But hermother admits that she was surprisedat the high cost of textbooks.

Afnan is enrolled in the first year ofConcordia’s Arts and Science programmajoring in mathematics. After completingher BSC, she is interested in pursuing acareer in dentistry. Afnan’s parents alsohave Global Educational Trust Plans forher four younger siblings.

Mr. Donald ForteSainte-Thérèse, Quebec The Global Plan’s flexibility gives LysanneForte, his daughter, the option to switchprograms. Lysanne is currently taking atwo-year course at College L’Assomptionto become a notary. However, Lysanne isconsidering changing courses to becomea translator instead.

The Global Plan will continue to fund hereducation. In addition, Lysanne receivedher sister’s unused Global Plan. Mr. Forteis glad that his Insurance SalesRepresentative suggested the Global

Educational Trust Plan and stronglyrecommends that all parents start anEducation Savings Plan for their children.

Mr. Hae Pying Lu andMrs. Chiou Shiang Lo Delta, British ColumbiaCurrently commuting two hours daily,Ya Ting, their daughter, attends theUniversity of British Columbia. Nextsemester, she plans to live on campus.Her parents established the Global Planback in 2001, as they thought the$5,000 tuition (approximately) along witha new computer would be costly to payall at once.

The Global Plan provided stablegrowth that the family could rely on.Ya Ting’s mother is very satisfied withthe outcome. She also admits theypreviously invested in a mutual fundcompany’s Education Savings Plan andlost money.

Mrs. Beverly PylypjukGrunthal, Manitoba Taking the University of Manitoba’stwo-year preliminary veterinary course,Allison, her daughter, plans to continueher studies at the University ofSaskatchewan. The Global Plan offersAllison the flexibility to pursue aneducation at another approved university.Allison’s mother started saving in the

Global Plan back in 1999 when a Global*Sales Representative suggested investinga Child Tax Benefit as a means of saving.The GETP has helped fund Allison’seducation. But Allison’s mother wishesthat she started saving even earlier,especially for Allison’s older sister, nowin medical school. Even with addedbursaries received and the GlobalEducation Savings Plan, the expensesincluding an apartment close to theuniversity are high.

Mr. Eddie Lei and Mrs. Tracy Lei TingVancouver, British Columbia Ying Chen Lei, their son, is attending afour-year engineering program at the

University of British Columbia. Ying liveswith his parents to help offset some ofthe education costs like textbooks whichhis mother finds expensive. The GlobalPlan helped fund Ying’s tuition and othercosts. Ying’s mother wishes she hadEducation Savings Plans for his oldersiblings. She recommends that all newCanadians invest in Education SavingsPlans for their children.

Mr. Faird Sobhy and Mrs. Samia SobhyToronto, OntarioFady, their son, is enrolled in the firstyear of a four year civil engineeringprogram at McMaster University inHamilton. Fady lives in residence but willstart next semester renting an apartmentnear the University. After completing hisengineering studies, Fady is interested intaking management courses. The GlobalPlan can also help fund Fady’s eligiblepost-graduate studies.

Fady’s father feels the expenses forbooks, computer software and projecttools needed for education are costly.Although Fady could work a part-time jobto help with expenses, Fady’s fatheradvocates that his son concentrate onhis studies and only work during thesummer break.

Fady’s father regrets not starting anEducation Savings Plan for Fady’s oldersister who attends Ryerson in Toronto.Fady’s parents value education andencourage their children to attend to andcomplete their post-secondary studies.

Mrs. Mona Yacoub and Mr. Chris YacoubToronto, Ontario Amanda, their daughter, attends YorkUniversity in Toronto taking an Arts andScience program that combines the

Bachelor of Education and Bachelor ofScience degrees. With this education,she plans a career as an educator.

Currently, she lives with her parents andworks twice a week during the schoolyear to help pay for daily expenses.

According to Amanda, her parents wereprepared for the high costs of education.Apparently, her older brother had alreadygone through this process two yearsbefore her. Amanda credits the GlobalPlan for helping tremendously with tuitionand the textbook costs.

7

In all cases, the Global Educational Trust Plan helped with the costs ofeducation. Many of the families said they were happy with the flexibilityof the Global Plan in meeting their needs. In some cases, parents weresurprised at how much an education really costs when they includedtuition, textbooks, residence, a computer, travel and meals. They onlywished that they started saving sooner.

CANADA

NEWFOUNDLAND AND LABRADOR

PRINCE EDWARDISLAND

NOVA SCOTIA

NEW BRUNSWICK

QUEBEC

ONTARIO

MANITOBA

SASKATCHEWAN

ALBERTA

BRITISH COLUMBIA

0 $2000CURRENT $

SOURCE: “UNIVERSITY TUITION FEES,” THE DAILY, STATISTICS

CANADA WEB SITE, SEPT 2, 2004

Note: Consumer Price Index annualized by taking averages from September to AugustSOURCE: “UNIVERSITY TUITION FEES,” THE DAILY, STATISTICS CANADA WEB SITE, SEPT 2, 2004

2004/05 1990/91

$4000 $6000 $8000

1990/91 1992/93 1994/95 1996/97 1998/99 2000/01 2002/03 2004

TUITION FEES

% INCREASE

YEARS

18

16

14

12

10

8

6

4

2

0

CONSUMER PRICE INDEX

8

Average undergraduatetuition fees

Rates of increase in undergraduate

tuition fees versus inflation

*Global Educational Marketing Corporation, Global Maxfin Investments Inc. or approved distributor.

May’s PlanSaving $25 a monthLisa and Alex started saving for May’seducation when she was six years old.Every month, they deposited $25 intotheir daughter’s education savings plan.By the time May turned 17 years old,her plan received a total of $720 ingrant money and was worth about$5,263*.

Daniel’s PlanAdding an extra $59 a month During the same time, Barbara contributed$25 each month into Daniel’s, education savings plan that she startedwhen her son was six years old. WhenDaniel turned 11, Barbara increased herdeposits to $84 a month—an extra$59. When Daniel turned 17 years old,his plan received a total of $1,711 ingrant money and was worth about$12,825*—more than double theamount in May’s plan.

Christine’s PlanAdding an extra $142 a monthMaximizing the remaining CanadaEducation Savings Grant (CESG) Meanwhile, Mary and Mark also started

saving for their daughter’s educationwhen she was six years old. They toocontributed $25 each month into

If you are not maximizing your contributions to your children’s education savings plans,you are not alone. With all the costs related to raising newborns and young children,many parents find it challenging to save for something that is years away.

Saving early continues to be one of the best ways to take advantage of compounded growth. Still, adding more money to your children’s educationsavings plans when they are older can also make a difference. Let’s take alook at some examples of education savings plans. These plans for May,Daniel and Christine, while not real, do represent real ways parents canincrease their investment.

10

Getting the Most from YourChildren’s Education Savings Plans

9

2003/04 to

2004/05

2003/04 2004/05 % change

Agriculture 3,495 3,626 3.7

Architecture 3,587 3,610 0.6

Arts 3,813 3,935 3.2

Commerce 3,985 4,118 3.3

Dentistry 11,681 12,331 5.6

Education 3,149 3,240 2.9

Engineering 4,400 4,617 4.9

Household Sciences 3,669 3,878 5.7

Law 5,995 6,471 7.9

Medicine 9,137 9,977 9.2

Music 3,759 3,883 3.3

Science 3,957 4,094 3.5

Undergraduate 4,018 4,172 3.9

Graduate 5,247 5,475 4.3

Current $

Universities across CanadaAverage tuition fees by faculty

Increasing yourContributions in an

Education Savings Plan$30K

$20K

$10K

ESTI

MAT

ED V

ALU

E

CHRISTINE’SPLAN

$23,462

DANIEL’SPLAN

$12,825

MAY’SPLAN

$5,263

0

2 1/2

7 1/2

5

15

121/2

171/2

221/2

271/2

25

7 9 10 12 14 16 17SOURCE: “UNIVERSITY TUITION FEES,” THE DAILY, STATISTICS CANADA WEB SITE, SEPT 2, 2004

AGE

12

Canada Learning Bond Children are eligible for the CanadaLearning Bond when they are bornJanuary 1, 2004 or later to familiesreceiving the National Child Benefitsupplement (NCB). These families canreceive $500 for each child’s RegisteredEducation Savings Plan (RESP) in the firstyear they qualify for the benefit and maybe eligible for $100 for each subsequentqualifying year to age 15. These fundscould contribute up to $2,000 to aneligible child’s RESP.

Enhanced Canada EducationSavings Grant Families with a net income of $35,000or less are eligible to receive up to $100more CESG yearly for each of theirchildren. The first $500 amountcontributed yearly to an RESP will receivean additional 20% of enhanced CESG(That is over and above the alreadygranted 20% CESG.)

Families with a net income between$35,000 to $70,000 are eligible toreceive an additional 10% enhancedCESG, up to a maximum of $500 yearly(above the existing 20% CESG). Thisprovides up to $50 or more for eachchild’s RESP. The lifetime limit of theGrant is $7,200.

Alberta Centennial EducationSavings PlanChildren born into or adopted by anAlberta family on January 1, 2005 orlater are eligible for up to $800 in grants.Parents will receive a one-time contributionof $500 and will receive subsequentcontributions of $100 for childrenresident and attending school in Albertaat ages 8, 11 and 14.

All government grants are subject tomeeting education savings plan registrationrequirements and Social InsuranceNumber provisions.

The Canada Education Savings Act, passed in 2004, now allowsparents to save more for their children’s education. In addition to theexisting Canada Education Savings Grant (CESG), the new CanadaLearning Bond (CLB) and Alberta Centennial Education Savings (ACES)Plan can provide parents up to $2,300 in additional funding.

New and Enhanced GovernmentFunding Announcements

Christine’s education savings plan. When Christine turned 11 her parentsstarted contributing $167 a month—anextra $142 which also maximized herremaining annual CESG. By the timeChristine turned 17 years old, her planreceived a total of $3,106 in grantmoney and was worth about$23,462*—over four times more theamount in May’s plan.

As you can see in the plans for May,Daniel and Christine, increasing yourcontributions in your child’s later years

can still make a significant differencein funding their college and universityeducation.

If you have questions about contributingmore into your children’s Global EducationalTrust Plan, contact your SalesRepresentative or Global Client Services.

*Assuming an annual 5% gross rateof return with contributions startingJanuary 1 of each year and being fullyinvested until December 31. Alsoassumes CESG eligibility.

This year, the winning ballot is from Montreal, Quebec. The Bhuiyan family name wasrandomly drawn from several thousand entries received across Canada.

When their one-year-old daughter, Soumiyah, is ready to go to college or university,she’ll have up to $20,000 to pay for her tuition, books, accommodation, meals and othereligible education expenses. Congratulations to Soumiyah and the Bhuiyan family!

Global Educational Marketing Corporation is proud to help families fundtheir children’s education. During the year, Global offers parents thechance to win a Global Educational Trust Plan worth up to $20,000.

11

Education Savings Plan Contest Winner

The government requires that your child have a valid S.I.N. to register aneducation savings plan, making it eligiblefor tax-deferred growth and governmentgrants. If you opened your GlobalEducational Trust Plan without your child’sS.I.N., any earnings are subject to taxation.It’s in your interest to ensure your childhas a S.I.N. as soon as possible and toprovide that number to Global* ClientServices. If you have not providedyour child’s S.I.N. by December 31stof the second year following the yearof enrollment, GETF is required toclose the Global Plan.

A few years ago, children usuallydidn’t need to have a S.I.N. until theywere ready to start working. The S.I.N.program was introduced in 1964 toregister people for EmploymentInsurance (previously known asUnemployment Insurance) and the Canada

Pension Plan (CPP). Three years later, theS.I.N. was used by Revenue Canada(now known as Canada Revenue Agency)for tax-reporting purposes.

Today, the nine-digit number is used toadminister various Canadian governmentprograms, including the Canada EducationSavings Grant (CESG), Canada LearningBond (CLB) and the Alberta CentennialEducation Savings (ACES) Plan.

If you are not sure if you provided yourchild’s S.I.N., refer to your most recentAnnual Statement of Account and checkif you received any CESG benefits. If not,then you will need to obtain a S.I.N. foryour child.

If you need more information on how toapply for one, contact your Global SalesRepresentative or Client Services.

Registering YourEducation Savings Plan

14

Whether your children are newborns, new immigrants or youngCanadians, make sure your children have their Social InsuranceNumbers (S.I.N.)

*Global Educational Marketing Corporation, Global Maxfin Investments Inc.

15 16

STATEMENTS OF NET ASSETS As at December 31, 2004 and 2003

Assets

Cash and short-term investmentsAccounts receivable (note 5)Investments - at market value (cost -$71,518,268; 2003 - $48,010,456) (notes 2 and 4)

Accrued interest

Liabilities

Accounts payable (note 5)CESG payableSubscribers’ Savings Account(notes 2 and 6)

Net Assets

Represented bySubscribers’ Savings Account (notes 2 and 6)

Accumulated CESG deposits (note 7)Accumulated and undistributed investment income

Unrealized appreciation of investments

Approved by the Board of Directors of Global Educational Trust Foundation

The accompanying notes are an integral part of these financial statements.

2004$

5,487,282690,427

73,036,642

377,17879,591,529

124,434–

54,331,232

54,455,66625,135,863

–

17,622,2945,995,195

1,518,37425,135,863

2003$

3,283,988145,145

48,588,942

334,15852,352,233

1,247,05553,409

–

1,300,46451,051,769

34,661,913

12,396,7873,414,583

578,48651,051,769

Donald Harrington, DirectorSam Bouji, Director

STATEMENTS OF OPERATIONS For the years ended December 31, 2004 and 2003

Investment incomeInterestExpensesAdministration fees and other charges (note 5)

Net investment income

Realized and unrealized gains on investments

Realized gain on sale of investmentsChange in unrealized appreciation of investments (note 2)

Net realized and unrealized gains on investments

Increase in net assets from operations for the year

The accompanying notes are an integral part of these financial statements.

2004$

3,141,010

664,815

2,476,195

371,522939,888

1,311,410

3,787,605

2003$

2,156,186

411,572

1,744,614

179,136139,053

318,189

2,062,803

We have audited the statements of net assets of Global Educational Trust Planas at December 31, 2004 and 2003, the statements of operations and changesin net assets for the years then ended and the statement of educational financialassistance agreements as at December 31, 2004. These financial statements arethe responsibility of management. Our responsibility is to express an opinion onthese financial statements based on our audits.We conducted our audits in accordance with Canadian generally accepted auditingstandards. Those standards require that we plan and perform an audit to obtainreasonable assurance whether the financial statements are free of materialmisstatement. An audit includes examining, on a test basis, evidence supportingthe amounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimates made bymanagement, as well as evaluating the overall financial statement presentation.In our opinion, these financial statements present fairly, in all material respects,the financial position of Global Educational Trust Plan as at December 31, 2004and 2003 and the results of its operations and changes in its net assets for the yearsthen ended in accordance with Canadian generally accepted accounting principles.

Chartered Accountants Toronto, Canada

AUDITORS’ REPORTTo the Directors of Global Educational Trust Foundation February 25, 2005

Financial Statements

17 18

STATEMENTS OF CHANGES IN NET ASSETSFor the years ended December 31, 2004 and 2003

Subscribers’ Savings Account (notes 2 and 6)

Subscribers’ depositsEnrollment fees (note 5)Depository fees (note 5)Insurance premiums (note 5)Special services fees (note 5)Principal withdrawals on terminations or return of deposits

Net increase in Subscribers’ Savings Account

CESG deposits

Increase in net assets from operations for the year

Payments to nomineesEducation Assistance PaymentsCESGCESG income

Increase in net assets during the year

Net assets - Beginning of year, originally reported

Section 1100 adjustment (note 2)AcG-18 adjustment (note 2)

Net assets - Beginning of year, restated

Net assets - End of year

The accompanying notes are an integral part of these financial statements.

2004$

––––––

–

5,572,265

3,787,605

(224,310)(346,758)(42,795)

8,746,007

50,473,283

(34,661,913)578,486

16,389,856

25,135,863

2003$

27,459,710(10,464,319)

(280,826)(178,760)(62,763)

(1,214,973)

15,258,069

4,489,430

2,062,803

(99,880)(159,055)(17,697)

21,533,670

29,078,666

–439,433

29,518,099

51,051,769

STATEMENT OF EDUCATIONAL FINANCIAL ASSISTANCE AGREEMENTSAs at December 31, 2004

The accompanying notes are an integral part of these financial statements.

Number of unitsoutstanding

76102476

1,8945,1279,187

15,14021,40225,88631,05639,00043,05553,07956,26860,42965,96367,46573,47679,82181,43089,07577,94362,23721,80028,50729,067

1,038,961

847,266

Principal plusinterest

$

36,99532,83283,799

286,7841,182,4042,843,3184,197,9224,655,4244,573,7654,385,9984,616,1573,913,8714,270,7893,643,7963,469,7003,268,0643,042,6713,068,6502,557,6491,651,7411,401,425

764,625357,85865,00144,4957,744

58,423,477

37,089,306

CESG plus interest

$

8,5725,736

14,45342,576

197,835520,356855,170

1,032,4861,103,4441,125,6631,268,5621,187,5091,341,8211,239,4861,260,7521,289,2771,268,1421,319,5741,248,8311,017,842

965,765620,312305,593141,395113,44430,648

19,525,244

13,383,977

Year of eligibility

20002001200220032004200520062007200820092010201120122013201420152016201720182019202020212022202320242025

December 31, 2003

19 20

investment income and realized andunrealized gains were reported in thestatements of changes in net assets.

Furthermore, in 2004, the Global Planhas adopted the recommendationscontained within Accounting Guideline18 (AcG-18) of the CICA, which requiresthat the Global Plan report itsinvestments at fair values. Previously, theGlobal Plan reported its investments atcost with market values disclosed assupplemental information. The changein unrealized appreciation ofinvestments is reported in thestatements of operations. AcG-18permits retroactive application ofthis change in accounting policy.Accordingly, investments reported as atDecember 31, 2003 have been restatedto market value in the statements of

net assets with the change in unrealizedappreciation of investments for 2003reflected in the statements of operations.

Certain other prior year figures havebeen reclassified to conform with thefinancial statement presentation adoptedin the current year.

3. SUMMARY OF SIGNIFICANTACCOUNTING POLICIES

Basis of accounting

These financial statements, preparedby management in accordance withCanadian generally accepted accountingprinciples, include estimates andassumptions made by managementthat affect the reported amounts.Actual results could differ from theseestimates and the differences couldbe significant. The following is asummary of significant accountingpolicies followed by the Global Plan.

Subscribers’ Savings Account

The Subscribers’ Savings Accountbalance reflects only amounts receivedfrom subscribers net of deductions anddoes not include amounts receivableon outstanding agreements.

Deductions from subscribers’ deposits

The Foundation deducts from depositsmade by subscribers the insurancepremiums, special services fees, depositoryfees and the enrollment fees prior todepositing the balance of the depositsin the Subscribers’ Savings Account.

Investments

Investments in bonds are stated at marketvalues, determined using prices quotedby dealers active in trading such bonds.

Realized and unrealized gains (losses) oninvestments are determined using theaverage cost method. Discounts on zerocoupon bonds are amortized over thelives of such bonds on a straight-line basis.

Short-term investments

Short-term investments consist ofinvestments in money market fundsand Government of Canada treasurybills maturing within one year from thedate of the statements of net assets.These are valued at amortized cost,which approximates market value.

1. ORGANIZATION AND GENERAL

The Global Educational Trust Plan (theGlobal Plan) was established onOctober 14, 1998. It is administered bythe Global Educational Trust Foundation(the Foundation), a not-for-profitorganization, incorporated withoutshare capital, under the laws ofCanada. The Plan provides post-secondary education financialassistance to nominees named in theEducational Financial AssistanceAgreements (EFA Agreements). GlobalEducational Marketing Corporation(GEMC), a company incorporated underthe Canada Business Corporations Act,is the registered distributor of theGlobal Plan.

The Foundation has had a specimencopy of the EFA Agreement approved byCanada Revenue Agency (CRA) suchthat EFA Agreements may be submittedto CRA for registration as RegisteredEducation Savings Plans. The Plan is aneducation savings plan and not aRegistered Education Savings Plan(RESP). An EFA Agreement is not anRESP until the applicable conditions ofthe Income Tax Act (Canada) are met.

Subscribers to the Global Plan enter intoEFA Agreements with the Foundation.Under an EFA Agreement, the subscriberpurchases units in the Global Plan. Thesubscriber authorizes the Foundation todeduct fees, as outlined in the prospectus,for the purpose of providing services tothe Global Plan. At maturity, paymentsare made to the nominee through the

conditions as set out in the EFAAgreements. Income paid to thesubscribers is considered AccumulatedIncome Payments (AIP) and is subject toincome taxes.

2. GENERALLY ACCEPTEDACCOUNTING PRINCIPLES

On January 1, 2004, the Global Planadopted the recommendations of TheCanadian Institute of CharteredAccountants (CICA) Handbook Section1100 (Section 1100), “GenerallyAccepted Accounting Principles” (GAAP).Section 1100 has established the relativehierarchy within Canadian GAAP and haseliminated common industry practice asa GAAP basis.

The following are the significant areas ofimpact to the financial statements as aresult of adopting Section 1100:

(a)The Subscribers’ Savings Account,described further in note 3, meets thedefinition of a liability and has beenrecognized as such in the statements ofnet assets. Previously, the Subscribers’Savings Account was included as acomponent of net assets of the GlobalPlan. The change has been reflected asan adjustment in the statements ofchanges in net assets. Note 6 detailsthe changes in the Subscribers’ SavingsAccount balance for the year.

(b)Statements of operations have beenincluded in the financial statements.Previously, the components of net

Notes to Financial Statements, December 31, 2004 and 2003

21 22

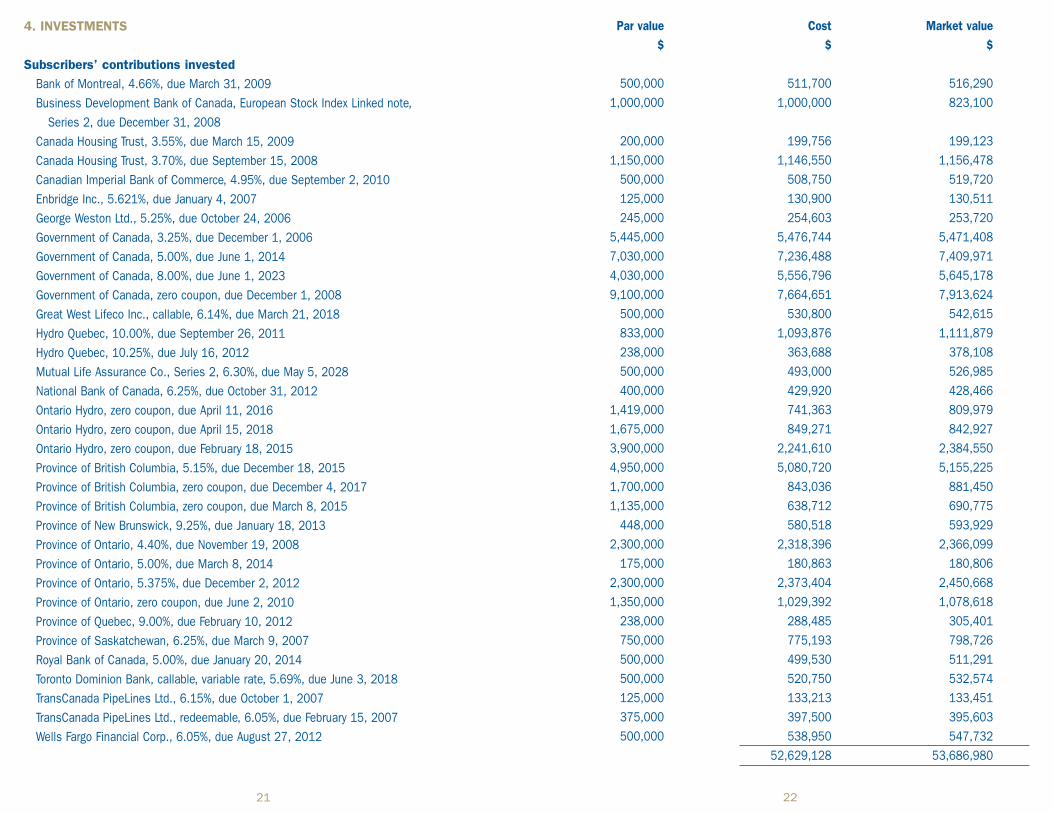

4. INVESTMENTS

Subscribers’ contributions investedBank of Montreal, 4.66%, due March 31, 2009Business Development Bank of Canada, European Stock Index Linked note,

Series 2, due December 31, 2008Canada Housing Trust, 3.55%, due March 15, 2009Canada Housing Trust, 3.70%, due September 15, 2008Canadian Imperial Bank of Commerce, 4.95%, due September 2, 2010Enbridge Inc., 5.621%, due January 4, 2007George Weston Ltd., 5.25%, due October 24, 2006Government of Canada, 3.25%, due December 1, 2006Government of Canada, 5.00%, due June 1, 2014Government of Canada, 8.00%, due June 1, 2023Government of Canada, zero coupon, due December 1, 2008Great West Lifeco Inc., callable, 6.14%, due March 21, 2018Hydro Quebec, 10.00%, due September 26, 2011Hydro Quebec, 10.25%, due July 16, 2012Mutual Life Assurance Co., Series 2, 6.30%, due May 5, 2028National Bank of Canada, 6.25%, due October 31, 2012Ontario Hydro, zero coupon, due April 11, 2016Ontario Hydro, zero coupon, due April 15, 2018Ontario Hydro, zero coupon, due February 18, 2015Province of British Columbia, 5.15%, due December 18, 2015Province of British Columbia, zero coupon, due December 4, 2017Province of British Columbia, zero coupon, due March 8, 2015Province of New Brunswick, 9.25%, due January 18, 2013Province of Ontario, 4.40%, due November 19, 2008Province of Ontario, 5.00%, due March 8, 2014Province of Ontario, 5.375%, due December 2, 2012Province of Ontario, zero coupon, due June 2, 2010Province of Quebec, 9.00%, due February 10, 2012Province of Saskatchewan, 6.25%, due March 9, 2007Royal Bank of Canada, 5.00%, due January 20, 2014Toronto Dominion Bank, callable, variable rate, 5.69%, due June 3, 2018TransCanada PipeLines Ltd., 6.15%, due October 1, 2007TransCanada PipeLines Ltd., redeemable, 6.05%, due February 15, 2007Wells Fargo Financial Corp., 6.05%, due August 27, 2012

Par value$

500,000 1,000,000

200,0001,150,000

500,000125,000245,000

5,445,0007,030,0004,030,0009,100,000

500,000833,000238,000500,000400,000

1,419,0001,675,0003,900,0004,950,0001,700,0001,135,000

448,0002,300,000

175,0002,300,0001,350,000

238,000750,000500,000500,000125,000375,000500,000

Cost$

511,7001,000,000

199,7561,146,550

508,750130,900254,603

5,476,7447,236,4885,556,7967,664,651

530,8001,093,876

363,688493,000429,920741,363849,271

2,241,6105,080,720

843,036638,712580,518

2,318,396180,863

2,373,4041,029,392

288,485775,193499,530520,750133,213397,500538,950

52,629,128

Market value$

516,290823,100

199,1231,156,478

519,720130,511253,720

5,471,4087,409,9715,645,1787,913,624

542,6151,111,879

378,108526,985428,466809,979842,927

2,384,5505,155,225

881,450 690,775593,929

2,366,099180,806

2,450,6681,078,618

305,401798,726511,291532,574133,451395,603547,732

53,686,980

23 24

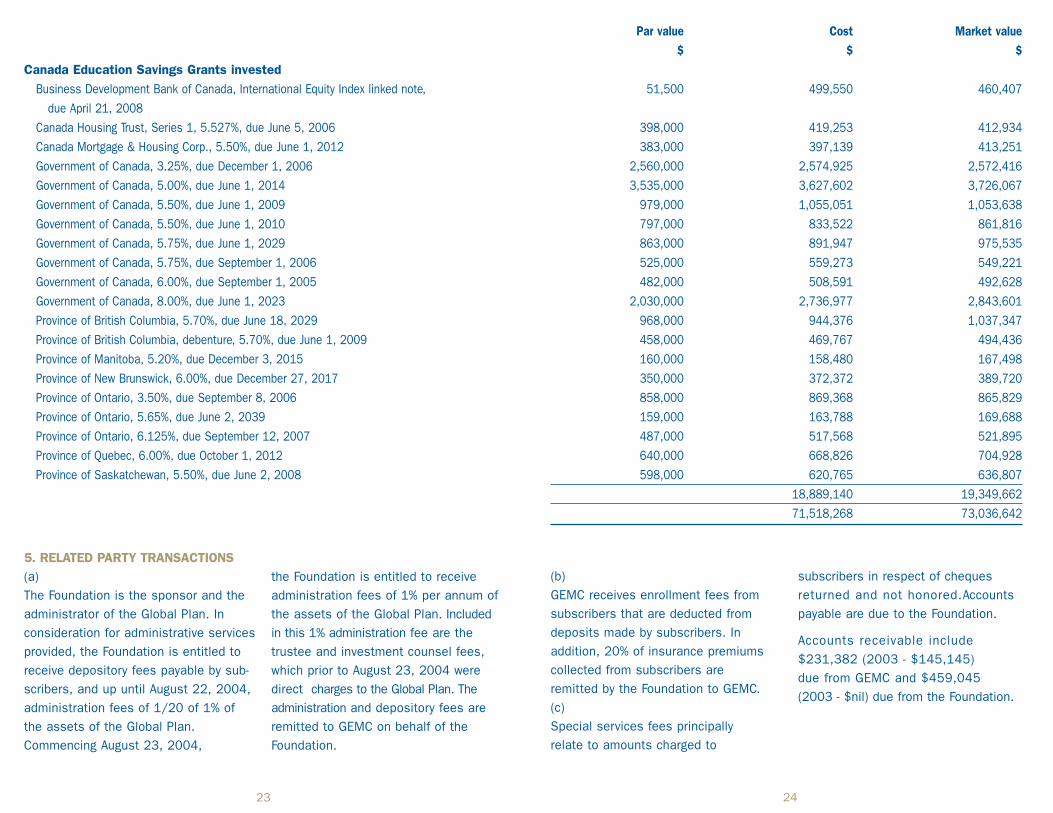

Canada Education Savings Grants investedBusiness Development Bank of Canada, International Equity Index linked note,

due April 21, 2008Canada Housing Trust, Series 1, 5.527%, due June 5, 2006Canada Mortgage & Housing Corp., 5.50%, due June 1, 2012Government of Canada, 3.25%, due December 1, 2006Government of Canada, 5.00%, due June 1, 2014Government of Canada, 5.50%, due June 1, 2009Government of Canada, 5.50%, due June 1, 2010Government of Canada, 5.75%, due June 1, 2029Government of Canada, 5.75%, due September 1, 2006Government of Canada, 6.00%, due September 1, 2005Government of Canada, 8.00%, due June 1, 2023Province of British Columbia, 5.70%, due June 18, 2029Province of British Columbia, debenture, 5.70%, due June 1, 2009Province of Manitoba, 5.20%, due December 3, 2015Province of New Brunswick, 6.00%, due December 27, 2017Province of Ontario, 3.50%, due September 8, 2006Province of Ontario, 5.65%, due June 2, 2039Province of Ontario, 6.125%, due September 12, 2007Province of Quebec, 6.00%, due October 1, 2012Province of Saskatchewan, 5.50%, due June 2, 2008

Par value$

51,500

398,000383,000

2,560,0003,535,000

979,000797,000863,000525,000482,000

2,030,000968,000458,000160,000350,000858,000159,000487,000640,000598,000

Cost$

499,550

419,253397,139

2,574,9253,627,6021,055,051

833,522891,947559,273508,591

2,736,977944,376469,767158,480372,372869,368163,788517,568668,826620,765

18,889,14071,518,268

Market value$

460,407

412,934413,251

2,572,4163,726,0671,053,638

861,816975,535549,221492,628

2,843,6011,037,347

494,436167,498389,720865,829169,688521,895704,928636,807

19,349,66273,036,642

5. RELATED PARTY TRANSACTIONS(a)The Foundation is the sponsor and theadministrator of the Global Plan. Inconsideration for administrative servicesprovided, the Foundation is entitled toreceive depository fees payable by sub-scribers, and up until August 22, 2004,administration fees of 1/20 of 1% ofthe assets of the Global Plan.Commencing August 23, 2004,

the Foundation is entitled to receiveadministration fees of 1% per annum ofthe assets of the Global Plan. Includedin this 1% administration fee are thetrustee and investment counsel fees,which prior to August 23, 2004 weredirect charges to the Global Plan. Theadministration and depository fees areremitted to GEMC on behalf of theFoundation.

(b)GEMC receives enrollment fees fromsubscribers that are deducted fromdeposits made by subscribers. Inaddition, 20% of insurance premiumscollected from subscribers areremitted by the Foundation to GEMC. (c)Special services fees principallyrelate to amounts charged to

subscribers in respect of chequesreturned and not honored.Accountspayable are due to the Foundation.

Accounts receivable include$231,382 (2003 - $145,145)due from GEMC and $459,045 (2003 - $nil) due from the Foundation.

25 26

6. SUBSCRIBERS’ SAVINGS ACCOUNT

The changes in the Subscribers’ Savings Account for the year are as follows:

Subscribers’ Savings Account

– Beginning of year

Subscribers’ deposits

Enrolment fees (note 5)

Depository fees (note 5)

Insurance premiums (note 5)

Special services fees (note 5)

Principal withdrawals on

terminations or return of deposits

Subscribers’ Savings Account

– End of year

2004

$

34,661,913

33,240,482

(10,545,838)

(354,628)

(189,817)

(53,335)

(2,427,545)

54,331,232

2003

$

19,403,844

27,459,710

(10,464,319)

(280,826)

(178,760)

(62,763)

(1,214,973)

34,661,913

7. CANADA EDUCATION SAVINGSGRANTS

The federal government encouragessaving for post-secondary education byproviding Canada Education SavingsGrants (CESG) on RESP contributionsmade subsequent to 1997 for childrenunder 18 years of age. The maximumCESG per child is 20% of RESP contributionsof up to $2,000 made on behalf ofeach nominee in a year (i.e., maximumCESG of $400).

The maximum lifetime CESG is $7,200.Upon maturity of an EFA Agreement andfulfillment of certain criteria establishedby the federal government, the CESGdeposits and accumulated investmentincome thereon will be added toeducation assistance payments madeto qualified students.

Additional federal and certain provincialgovernment educational savings programsand initiatives were announced duringthe year, which increase subsidiesavailable to qualifying families. Theseadditional benefits are expected tocome into effect in 2005.

8. INCOME TAXESThe income on the Subscribers’ SavingsAccount is currently exempt from incometaxes under the Income Tax Act (Canada).Education assistance payments,comprising CESG and all accumulatedinvestment income, made to qualifiednominees will be included in theirincome for the purposes of theIncome Tax Act (Canada).

The amounts deposited by subscribersare not deductible to the subscribers

for income tax purposes and are nottaxable when returned to subscribersor their designated nominees.

9. FINANCIAL INSTRUMENTS

The Plan’s financial instruments,consisting of cash and short-terminvestments, accounts receivable,accrued interest and accounts payableare carried at cost which, unlessotherwise noted, approximates fairvalue. Investments are carried atmarket values as described in note 3.It is management’s opinion that theGlobal Plan is not exposed to significantcredit or foreign exchange risks.Investments in fixed income securities,such as bonds and short-terminvestments, are inherently subject torisks from interest rate fluctuations.

• Obtaining a Social Insurance Number (S.I.N.)• Updating your personal information in our records• Changing your Global Plan terms or payment• Educational Financial Assistance (EFA) documents• Or any other questions concerning correspondence and/or documents you

received or need to provide.

To ensure a prompt response, please make sure you have your agreementnumber and any existing correspondence handy as reference.

Contact your Global* Sales Representative or Client Services at416-740-1622 or toll-free at 1-877-460-7377 or bye-mail at [email protected].

Contacting Client Services

If you have any questions about your Global Educational Trust Planor need to make changes to it, Client Services can help you with:

27

NotesContacting Client Services

*Global Educational Marketing Corporation, Global Maxfin Investments Inc. or approved distributor.