brasil-canada agriculture forum

TRANSCRIPT

WWW.INSPER.EDU.BR

BRASIL-CANADA AGRICULTURE FORUMBrazil-Canada Trade in the Agri-Food Sector (Session 2)

GLOBAL CHALLENGES FOR BILATERAL TRADE(KEYNOTE SPEECH)

Marcos Sawaya JankProfessor of Global Agribusiness

May 25th, 2021

WWW.INSPER.EDU.BR

✓ Senior Professor of Global Agribusiness and coordinator of Insper Agro Global.

✓ Chair Professor of the Luiz de Queiroz Chair on Integrated Agri-Food Systems at ESALQ-USP (2019/2020)

✓ President of the Asia-Brazil Agro Alliance (ABAA), an initiative to represent the Brazilian trade associations in Asia, located in Singapore (2017-19)

✓ Vice-President of Corporate Affairs and Business Development of BRF Asia-Pacific (2013-16)

✓ CEO of the Brazilian Sugarcane Industry Association (UNICA) – (2007-12)

✓ President of the Brazilian Institute for International Trade Negotiations (ICONE) - 2002-07

✓ Associate Professor at the University of São Paulo’s (USP) Colleges of Economics (FEA), Agricultural Sciences (ESALQ) and International Relations (IRI) – 1989-2007

✓ Board Member of RUMO Logistics, COMERC Energy, Agrotools and at Minerva and Cargill Global Committees on Sustainability and Forest Protection.

✓ Education: Tenure in Agricultural Economics at ESALQ-USP, Doctorate in Business Economics at USP Scholl of Economics and Business (FEA), M.Sc. in Ag Policy in Montpellier-France, and a B.Sc. degree in Agronomy at ESALQ

BIO

WWW.INSPER.EDU.BR

Canada & BrazilCompetitive Advantages in the Agri-Food Sector

CANADA BRAZIL• 5th ag exporter and 9th in total ag area.

• Trade agreements covering most ag exports: market access, lower tariffs.

• Reputation and differentiation: quality, food safety, traceability.

• Long-term international presence →

government and private sector.

• Commodity based exports, value-added products and branding.

• Food Chain organization.

• Regulatory system: simple, focused.

• 3rd ag exporter and 5th in total ag area.

• Availability of natural resources: land, water, climate conditions.

• “Tropicalization”: genetic improvement (soy, grasses, zebu), double cropping, crop-livestock integration, no-till, large scale farming systems, integrated supply chains

• Benchmark in biofuels (ethanol biodiesel).

• Commodity based exports: volumes and low costs, value-added still a challenge.

• Farmers: young entrepreneurs, motivated, risk takers, intense internal migrations.

• New agricultural frontiers, especially pasture conversions and MAPITOBA).

More complementarities than competition!

WWW.INSPER.EDU.BR

Agricultural trade balances by regionFood surpluses and deficits (contant value 1990–2025)

Source: OECD and FAO agricultural outlook 2016–2025

WWW.INSPER.EDU.BR

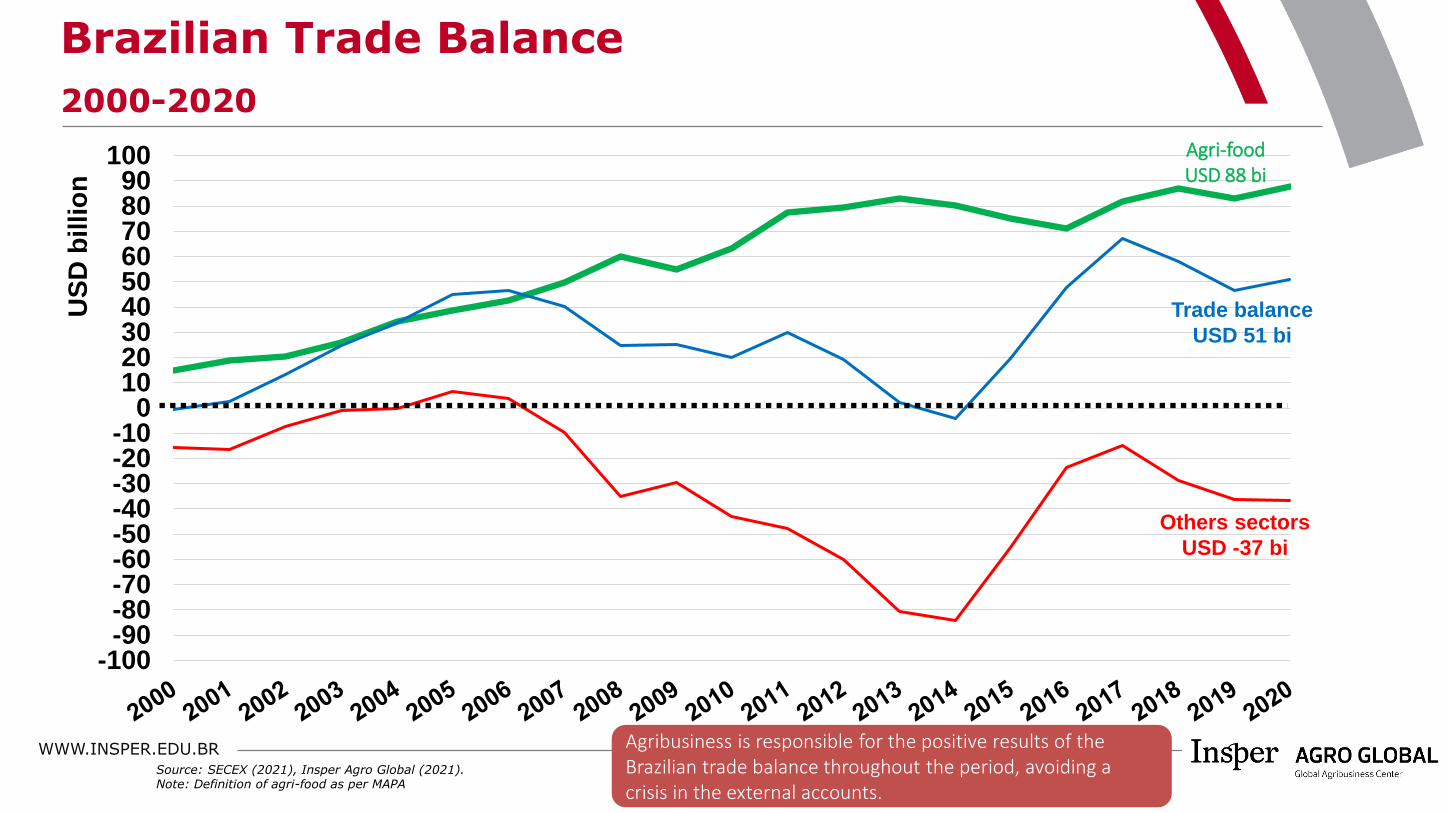

-100-90-80-70-60-50-40-30-20-10

0102030405060708090

100

US

D b

illio

n

Trade balance

USD 51 bi

Others sectors

USD -37 bi

Agri-foodUSD 88 bi

Source: SECEX (2021), Insper Agro Global (2021).Note: Definition of agri-food as per MAPA

Agribusiness is responsible for the positive results of the Brazilian trade balance throughout the period, avoiding a crisis in the external accounts.

Brazilian Trade Balance

2000-2020

WWW.INSPER.EDU.BR

0

10

20

30

40

50

60

70

80

90

100

110

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

US$

Bill

ion

Fonte: SECEX (2021), Insper Agro Global (2021).Definition of Agribusiness from MAPA, which considers 2949 agri-food products.

2020 (US bi)

2020 (%)

CAGR (10-20)

13.1 12.9% -2.3%

Soybean complex

Meat

Forest products

Sugar and EthanolCorn

Cotton

Others

3.2 3.2% 8.0%

6.0 5.9% 7.0%5.5 5.5% -2.9%

10.1 10.0% -6.7%

11.4 11.3% 3.5%

16.4 16.3% 1.1%

35.2 34.9% 5.6%

Coffee

US$ 101 bi

Brazil: Agri-Food Exports by productsValue, 2010 to 2020 (USD billion)

Top 4 agri-food chains → 73%

WWW.INSPER.EDU.BR

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

US$

Bill

ion

Canada: Agri-Food Exports by productsValue, 2009 to 2019 (USD billion)

2019 (US bl)

2019 (%)

CAGR (09-19)

11.7 18.5% 3.5%Forest products

Others 18.2 28.7% 4.2%

Source: UN COMTRADE (2021), Insper Agro Global (2021).

Fish products

Wheat

Vegetables

RapeseedPork

Vegetable oilsBeef

PulsesSoy

ChocolateLive animals

5.6 8.9% 5.0%

5.5 8.8% 0.1%3.4 5.3% 4.7%3.2 5.1% 1.2%3.0 4.8% 1.5%2.9 4.6% 2.6%2.4 3.9% 7.2%2.3 3.7% 2.5%1.8 2.8% 5.0%1.6 2.6% 7.9%1.5 2.4% -0.5%

WWW.INSPER.EDU.BR

Brazil: Agri-Food Exports by destinationValue, 2000 to 2020 (USD billion)

European Union (17%)

Asia ex-China (17%)

MENA (9%)

Latin America (8%)USA/Canada (8%)

SSA Africa (6%)

Source: SECEX (2021), Insper Agro Global (2021). Note: Asia ex-China includes East Asia (ex. China), South Asia, ASEAN, Russia and Central Asia. Definition of Agribusiness from MAPA, which considers 2949 agri-food products.MENA is Middle East and North Africa. SSA Africa is Sub-Saharan Africa.

0

5

10

15

20

25

30

35

40

US$

Bill

ion

China & HK

(34%)

WWW.INSPER.EDU.BR

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

China & HK

European Union

MENA

Latin America

USA/Canada

SSA Africa

4%

41%

11%

6%

14%

19%

2%

34%

18%

16%

12%

8%

8%

3%

Asia (ex-China)

Brazil: Agri-Food Exports by destinationShare, 2000 to 2020 (%)

Source: SECEX (2021), Insper Agro Global (2021). Note: Asia ex-China includes East Asia (ex. China), South Asia, ASEAN, Russia and Central Asia. Definition of Agribusiness from MAPA, which considers 2949 agri-food products.MENA is Middle East and North Africa. SSA Africa is Sub-Saharan Africa.

WWW.INSPER.EDU.BR

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

US$

Bill

ion

2019 (US bl)

2019 (%)

CAGR (09-19)

37.9 60.0% 4.7%USA

EU-28

Source: UN COMTRADE (2021), Insper Agro Global (2021).

China & HK

Others Asia

ex-China

Latin America

Others

9.1 14.4% 0.6%

6.5 10.3% 6.8%

3.5 5.5% 0.5%3.0 4.7% 0.0%

3.2 5.1% -1.3%

Canada: Agri-Food Exports by destinationValue, 2009 to 2019 (USD billion)

WWW.INSPER.EDU.BR

0

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

US$

Bill

ion

2019 (US bl)

2019 (%)

CAGR (09-19)

24.1 55.9% 2.5%

Others

Source: UN COMTRADE (2021), Insper Agro Global (2021).

OceaniaChinaASEANMexico

Latin America (ex-MEX)

EU-28

USA

5.2 12.1% 3.9%

3.6 8.4% 1.0%

2.4 5.5% 7.7%2.0 4.7% 2.4%1.9 4.3% 2.7%0.9 2.1% 2.2%3.0 7.1% 7.6%

Canada: Agri-Food Imports by originValue, 2009 to 2019 (USD billion)

WWW.INSPER.EDU.BRSource: SECEX (2021), Insper Agro Global (2021).

Brazil-Canada Agri-Food TradeValue, 2009 to 2019 (USD billion)

-

100

200

300

400

500

600

700

800

900

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

USD

Mill

ion

NET exports Exports Imports

BRASILCAGR Exports: -3.5%

CANADACAGR Imports: -10.1%

WWW.INSPER.EDU.BR

0

100

200

300

400

500

600

700

800

900

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

US$

Mill

ion

Source: SECEX (2021), Insper Agro Global (2021).

2020 (USD mi)

2020 (%)

CAGR (10-20)

282.9 47.2% -7.0%Sugar

118.0 19.7% 0.4%

Coffee

Forest productsPoultryFruitsBeef

Others44.2 7.4% 0.7%26.1 4.4% -4.7%18.0 3.0% 5.5%12.8 2.1% 1.8%97.1 16.2% 0.4%

Brazil: Agri-Food Exports to CanadaValue, 2009 to 2019 (USD billion)

WWW.INSPER.EDU.BR

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

US$

Mill

ion

Source: SECEX (2021), Insper Agro Global (2021).

2020 (USD mi)

2020 (%)

CAGR (10-20)

26.1 21.3% 4.1%Wheat

PulsesFeeds & Fodders

Paper & Cellulose

Others

18.6 15.2% 0.3%16.9 13.8% 13.3%13.3 10.8% -22.3%

47.7 38.9% 1.5%

Brazil: Agri-Food Imports from CanadaValue, 2009 to 2019 (USD billion)

WWW.INSPER.EDU.BR

100

120

140

160

180

200

220

240

260

280

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Ín

dic

e (

19

80

=1

00

)

Brazil

India

Australia

World Average

Canada

USA

Total Factor Productivity (TFP) growthin Agriculture

TFP → Land, Labor and Capital efficiency

Brazil´s TFP: 2.4% p.a.

Source: USDA/ERS, International Agricultural Productivity data productNote: The TFP (Total Factor Productivity) representes the aggregate efficiency of land, labor and capital resources. Higher TFP means more efficient the production outcomes.

WWW.INSPER.EDU.BR

Land Potential and Water Availability

0

1

2

3

4

5

6

7

8

9

10

0

10

20

30

40

50

60

70

80

90

100

Wat

er

(Tri

llio

n m

3/y

ear

)

Lan

d (

Mill

ion

He

ctar

e)

Arable LAND Available WATER

Note: LAND: available, non-protected and non cultivated, include pastures that could be converted into agriculture. WATER: all sources of renewable water. Sources: Fischer e Shah (2010), mentioned in World Bank, 2010 (Rising Global Interest in Farmland: Can it Yield Sustainable and Equitable Benefits?), ICONE, FAO.

WWW.INSPER.EDU.BR

Native vegetation: 565 M ha (66% of the total area)

Pastures: 175 M ha (20%)

Urbanization: 4 M ha (0,5%)

Agriculture: 85 M ha (10%)

Source: Mapbiomas (2020)

Land Use in Brazil

Current sustainability challenges

Agriculture + livestock + planted forests: 260 M ha (30%)

TOTAL: 850 M ha

Agriculture

Others: 21 M ha (2,5%): mining, waters, dunes, etc.

WWW.INSPER.EDU.BR

0

5

10

15

20

25

30

35

40

45

50

164

166

168

170

172

174

176

178

180

182

184

186

Kg/

ha/

year

Mill

ion

he

ctar

es Productivity

Pasture area

Sustainability governance Productivity gains and the proliferation of integrated systems

Pasture area and productivity Crop-Livestock-Forest Integration and double cropping

Source graph 1:Source graph 2: 2: Athenagro, dados da Kleffmann / Rede Fomento, IBGE (Censo, 2017) e Agroconsult

Incresing beef production doesn´t need new land. It needs inputs, improvements and technology!

23

34

56

78

910

1113

1415

1617

3 35 5

55

68

910 10

11

13 12

1415

0

2

4

6

8

10

12

14

16

18

20

Mill

ion

he

ctar

es

Integratedsystems

Double cropping

WWW.INSPER.EDU.BR

Current Projected

Aratu

Santarém

BR-364 BR-158

BR-163

Itacoatiara

VDC/Bacarena

Itaqui/São Luís

Santana

Vitória (Tubarão)

Aratu

PortoRodoviaHidroviaFerroviaTransbordo

LEGENDA:

Santos

Paranaguá

Rio Grande

São Francisco

Ilhéus

Aratu

Santarém

BR-364 BR-158

BR-163

Itacoatiara

VDC/Bacarena

Itaqui/São Luís

Santana

Vitória (Tubarão)

Aratu

PortoRodoviaHidroviaFerroviaFerrovia ProjetosTransbordo

LEGENDA:

Santos

Paranaguá

Rio Grande

São Francisco

Ilhéus

Ferrogrão

Fico

Rumo Fiol

VLI

Logistics InfrastructureRailways expansion projects

Source: CONAB (2019), Wall Street Research Reports (2019), CNT (2019), RUMO (2019).

WWW.INSPER.EDU.BRSource: UN´s Food & Agriculture Organization Global Perspectives Studies, Bloomberg.

Food DependenceTrade as a share of domestic food supply

WWW.INSPER.EDU.BR

Source: from Derek Headey’s presentation, Senior Research Fellow from the International Food Policy Research Institute (IFPRI). Note: estimated on basis of price data from the ICP reference for a healthy diet EAT-Lancet (2011).

Challenge: access to healthy diets

+1,5 billion people do not have access to

healthy diets in Africaand AsiaCost of a healthy diet

as % of medium family income

CHEAPEST AND MOST DURABLE PRODUCTS:➢ Carbs, snack foods, tubers, sugar, vegetable oils, soft drinks MORE EXPENSIVE AND LESS DURABLE PRODUCTS:➢ Fruits & vegetables, eggs, meats, fresh fish

WWW.INSPER.EDU.BR

Meat ConsumptionAnnual Average (Kg/year)

Source: FAO (2019), Insper Agro Global (2019). Note: Data for meat, pork, poultry and sheep.

Meat consumption(per capita - Kg/year)

WWW.INSPER.EDU.BR

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pork Soybeancomplex

Corn Poultry Rice Cotton Milkproducts

Wheat Beef Sugar

Top 5 Exporters

Top 5 Importers

Top 5 exporters and importersShare by commodity (2017-2019)

Top net exporters: US, Brazil, Argentina, Canada, Australia, NZ, Indonesia, Thailand, IndiaTop net importers: China/HK, Japan, Korea, EU, Middle East, Mexico, US, Russia

Source: UN COMTRADE (2021), Insper Agro Global (2021).

WWW.INSPER.EDU.BR

How to achieve?

…with import restrictions and self-sufficiency policies?

Food Security Food Safety & Nutrition

AffordabilityLow Inflation

Sustainability

Trade is still very limited in the agri-food sector…

Top priority issues are challengingtrade-offs

WWW.INSPER.EDU.BR

Final RemarksCanada-Brazil Potential Areas of Bilateral Cooperation

1. Fighting global ag protectionism: reinforce the WTO, coalitions on sectoral agendas (grains, animal protein, etc.)

2. WTO Reform and work on bilateral trade negotiations (Canada-Mercosur agreement).

3. Research and innovation: genetics, biotechnology, mechanization, geo-technologies, precision agriculture, big data, drones, blockchains.

4. Value-added products and branding.

5. Food safety, quality, traceability.

6. Sustainability, climate-smart agriculture, bioenergy.

7. Building integrated agri-food value chains to address global food security and food safety challenges: exploring competitive advantages, cross-investments, consolidation.

Note: WTO (World Trade Organization), GSA (Global Sugar Alliance)

WWW.INSPER.EDU.BR

Thank you / Obrigado

Marcos Jank

https://www.insper.edu.br/pesquisa-e-conhecimento/centro-de-agronegocio-global/