brazilian market opportunities - b3 - ri...

TRANSCRIPT

December 2010

Forward Looking Statements

This presentation may contain certain statements that express the management’s expectations, beliefs and assumptions about future events or results. Such statements are not historical fact, being based on currently available competitive, financial and economic data, and on current projections about the industries BM&FBovespa works in.The verbs “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “plan,” “predict,” “project,” “target” and other similarverbs are intended to identify these forward-looking statements, which involve risks and uncertainties that could cause actual results to differ materially from those projected in this presentation and do not guarantee any future BM&FBovespa performance.

The factors that might affect performance include, but are not limited to: (i) market acceptance of BM&FBOVESPA services; (ii) volatility related to (a) the Brazilian economy and securities markets and (b) the highly-competitive industries BM&FBovespa operates in; (iii) changes in (a) domestic and foreign legislation and taxation and (b) government policies related to the financial and securities markets; (iv) increasing competition from new entrants to the Brazilian markets; (v) ability to keep up with rapid changes in technological environment, including the implementation of enhanced functionality demanded by BM&FBovespa customers; (vi) ability to maintain an ongoing process for introducing competitive new products and services, while maintaining the competitiveness of existing ones; (vii) ability to attract new customers in domestic and foreign jurisdictions; (viii) ability to expand the offer of BM&FBovespa products in foreign jurisdictions.All forward-looking statements in this presentation are based on information and data available as of the date they were made, and BM&FBovespa undertakes no obligation to update them in light of new information or future development.This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there beany sale of securities where such offer or sale would be unlawful prior to registration or qualification under the securitieslaw. No offering shall be made except by means of a prospectus meeting the requirements of the Brazilian Securities Commission CVM Instruction 400 of 2003, as amended.

2

BRAZILIAN MARKET OPPORTUNITIES

3

Brazil represents a unique investment opportunity

New growth cycle and

investments in infra-structure

Pre-salt Oil Exploration

Development of Mortgage Market

Expansion of Middle Class

Entrepreneurial StimulusGreater Internal Demand

Rio Olympics 2016 and World Cup 2014

Increase in Income Levels

Interest Rate Decline

Brazil will have the 6th

highest world purchasing

power by 2013 (Price

Coopers) (1)

Brazilian per capita income will rise from US$7,900 to US$10,900

in 2011 (Bank of America

Merrill Lynch) (1)

(1) As of Jan/10.4

jan/05 jul/05 jan/06 jul/06 jan/07 jul/07 jan/08 jul/08 jan/09 jul/09 jan/10 jul/10

35-40%

35-40%

5-10%

US EUR BR

(1) Updated until Oct/2010;(2) HFT: High Frequency Trading - Source: Rosemblatt Securities Inc.; Source: WFE

Low penetration of equity and derivatives in the main investors’ portfolios

Stable and “low” interest rate environment would encourage exposure in securities

Recent growth in the number of retail investors, but still low compared to other markets

Low number of listed companies compared to other countries

Nov´10

644,055

128,615

66%

35%

5-10%

US EUR BR

Equities Futures

5

6,408

5,179

3,700 3,472 3,019 2,792

2,335 1,966 1,788

386

Índia USA Canada Spain China /HK London Japan Australia Korea Brazil

Brazilian Capital Markets: high growth potential

High Growth Potential Number of Custody Accounts(1)

HFT to Total Volume Traded(2) 2009 Listed Companies (28th in the World)

MAIN INITIATIVES TO INCREASE GROWTH

6

Brings the concept “quer ser sócio?” (wanna be a shareholder?) as a differential to attract new investors. The campaign will be released in mass medias

All the pieces will have a reference to the campaign web site www.quersersocio.com.br

Main Strategies to Attract Retail Investors2010 – launching of the campaign “Quer ser Sócio?”

New Campaign “Quer ser Sócio?”

Other Popularization and Education Initiatives

Launching of the on line (web) version of the DesafioBM&FBOVESPA

Launching of the Turma da Bolsa, a financial education web site for kids;

Beginning of the second season of the EducaçãoFinanceira program, with 42 episodes to be exhibited from March to December 2010

“ENEF” – printing and distribution of books for the schools which participate of the pilot project, and beginning of the development of the contents for school

“Fica Mais” – mileage and member get member program for investors

7

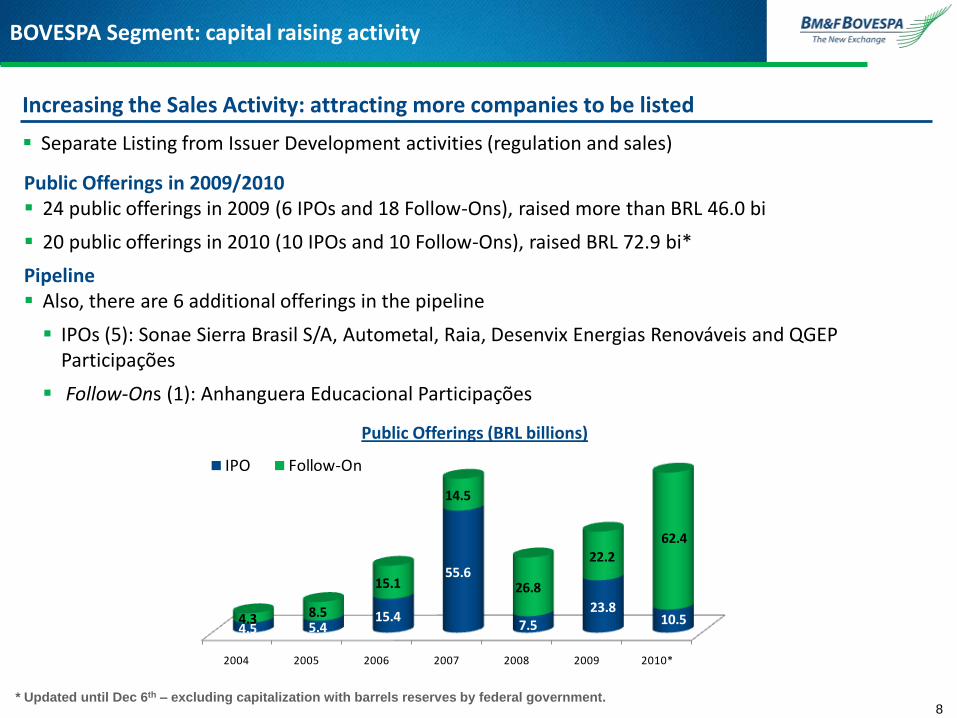

BOVESPA Segment: capital raising activity

Public Offerings (BRL billions)

Public Offerings in 2009/2010 24 public offerings in 2009 (6 IPOs and 18 Follow-Ons), raised more than BRL 46.0 bi

20 public offerings in 2010 (10 IPOs and 10 Follow-Ons), raised BRL 72.9 bi*

Pipeline Also, there are 6 additional offerings in the pipeline

IPOs (5): Sonae Sierra Brasil S/A, Autometal, Raia, Desenvix Energias Renováveis and QGEP Participações

Follow-Ons (1): Anhanguera Educacional Participações

8

Increasing the Sales Activity: attracting more companies to be listed

Separate Listing from Issuer Development activities (regulation and sales)

* Updated until Dec 6th – excluding capitalization with barrels reserves by federal government.

2004 2005 2006 2007 2008 2009 2010*

4.5 5.4 15.4

55.6

7.5 23.8

10.5 4.3 8.5

15.1

14.5

26.8

22.2

62.4

IPO Follow-On

New Products Pipeline

9

Equity Order Book in Foreign Currencies

BM&FBOVESPA and Chi-X Global Term Sheet for joint development of software

Trading of stocks listed in Brazil with simultaneous FX execution - allows non residents to match stocks in US$ and other currencies

Legal requirements to invest in Brazil keep unchanged

ETFs – BRL million

New DevelopmentsCompany focus on becoming a global marketplace

Only 7 ETFs listed on the Exchange

Financial Index ETF to be launched in 4Q10

Other ETFs under development: Dividends, Utilities and IBRX-20

8.8 5.3

11.4

20.3 22.0 23.5 21.7

21.5

26.625.6

18.3 16.9

22.2

27.1

25.3

33.1

29.1

24.5 26.7 27.2

30.8 32.7 33.1

Jan-

09

Feb-

09

Mar

-09

Apr-

09

May

-09

Jun-

09

Jul-0

9

Aug-

09

Sep-

09

Oct

-09

Nov-

09

Dec-

09

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov-

10

Non-Sponsored BDR – Level 1

Deutsche Bank will be the first depository institution and will list 10 large cap stocks listed in the US (Start of trading in October 5, 2010)

Citibank was chosen to list 10 other large cap stocks (Start of trading in October 5, 2010)

Globally preferred strategic partners

Development of new multi-class trading platform

Reciprocal participation in CME and BVMF Board of Directors

Increase of BVMF stake in CME from 1.8% to 5.0%

Order routing

International market data distribution

Nasdaq OMX product licensing to Brazilian companies

High frequency international link and greater capability to support trading

Exploring global partnership initiatives

10

IT DEVELOPMENT, DMA EVOLUTION AND HIGH

FREQUENCY TRADING ACTIVITY

11

Excellence in IT Solutions and Post-Trading Services

12

Market Access Co-location

Capacity: phase II implemented in Jul’10; Bovespa Segment: launched in Sep’10

Market Data Distribution: Unified Market Data Feed - UMDF for both segments (by 4Q10)

EntryPoint: unified order entry interface for both segments (by 2Q11)

ISVs: Trading Technologies (TT) will provide screens for BM&F Segment in 1Q11

Brazil Easy Investing (partnership with Chi-X): order book in USD and other currencies

Trading Systems (Mega Bolsa and GTS)

New Trading System: project commenced in Feb’10

Schedule: Derivatives and cash FX (1Q11), Equities (1Q12) and Fixed income (2Q12)

Capacity Increasing

BOVESPA Segment: from 1.5 million to 3 million trades / day (by 4Q10)

BM&F Segment: from 200 thousand to 400 thousand trades / day (completed in the 3Q10)

Performance: improving performance in both systems (one digit latency by YE10)

Post-trading Developments

Data Center: rent of a facility for the new back up site and the construction of the main site

Clearing Integration: ongoing delivery of some integration basics and project planning for 2011 new clearing infrastructure

Sungard/GMI (back office for FCMs): to be implemented in 4Q10

IT DevelopmentsInitiatives to support future growth

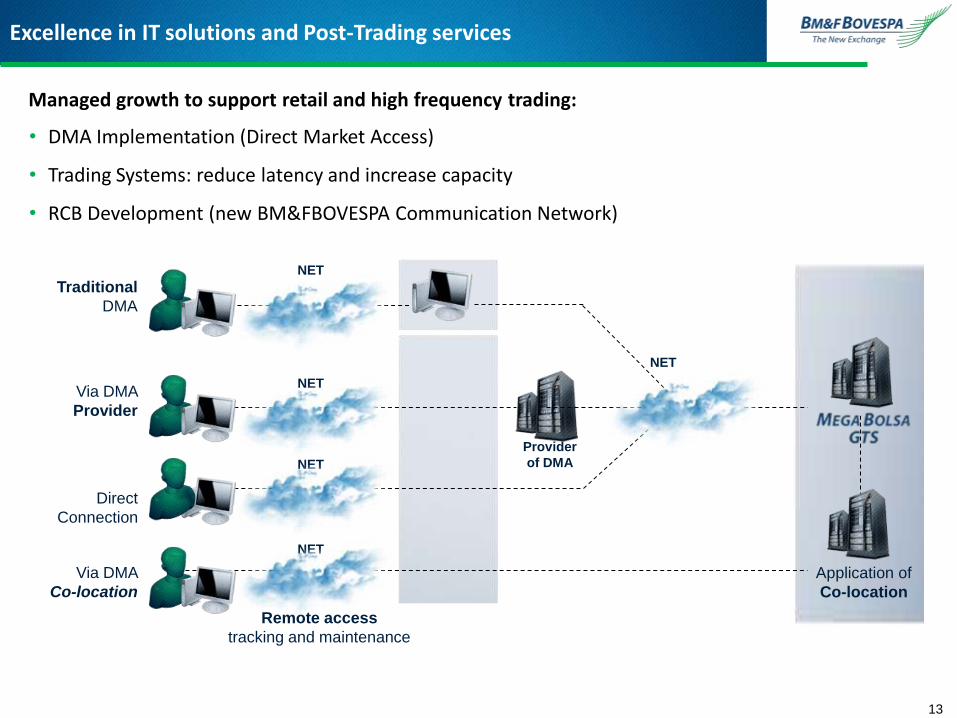

Managed growth to support retail and high frequency trading:

• DMA Implementation (Direct Market Access)

• Trading Systems: reduce latency and increase capacity

• RCB Development (new BM&FBOVESPA Communication Network)

Via DMA

Co-location

Traditional

DMA

Via DMA

Provider

Direct

Connection

NET

NET

NET

NET

Remote access

tracking and maintenance

Application of

Co-location

NET

Provider

of DMA

Excellence in IT solutions and Post-Trading services

13

* Updated until November 30, 201014

BM&F Segment: DMA Order Routing Evolution

DMA ADTV – in thousands of contracts

157 195 197 216327 380 337

451 416

276 367 353 290 350

551 4 30 71

129

156148

44

161 214

70 48 40

46 51

47

51

92

176223

240

279 204

189

254 262 204

270

317

203

13

21138

156

84 164

162

151 156 162

203

161

5.5%

7.5%

11.3%

14.4%

13.9%

17.6%

16.0%

16.0% 20.1%

16.9%

13.5% 16.6%

17.7%

20.4%

19.7%

0%

4%

8%

12%

16%

20%

-100

100

300

500

700

900

1100

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 nov-10

Traditional DMA CME Globex DMA Provider CoLocation % of DMA in overall ADTV

New Products Pipeline

15

High Frequency Trading - HFTNew pricing policy (both segments)

Main Characteristics

Differentiated fees by tier only for day trades transactions executed by a registered HFT

A HFT Committee created to approve and monitor the HFTs

The new pricing policy is being implemented in two steps: Nov’10 and Jan’11 (consolidated volume executed in more than one broker)

Bovespa Segment

In the Bovespa Segment, different tiers were created for individuals and non-individuals HFT investors

IndividualsADTV tier (BRL millions) Trading Fee (%)Up to 4 (inclusive) 0.019From 4 to 12.5 (inclusive) 0.017

From 12.5 to 25 (inclusive) 0.014

From 25 to 50 (inclusive) 0.012Above 50 0.010

Non-individualsADTV tier (BRL millions) Trading Fee (%)

Up to 20 (inclusive) 0.019From 20 to 50 (inclusive) 0.017

From 50 to 250 (inclusive) 0.014

From 250 to 500 (inclusive) 0.012Above 500 0.010

BM&F Segment

In the BM&F Segment, the 70% flat discount was replaced by a volume tiered based discount, only for day trades

0 1 3 7 12 15 13 17 20 25

84

164 162 151 156 162

203

161

Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10

3.2%

1.4%

3.3% 3.2% 2.6% 4.1%

4.8%

2.9%

Seven active investors

22 active participants in Oct’10

16

BM&F Segment: High Frequency Trading (HFT)HFT is playing an important role in derivatives market

•Updated until: November 30h, 2010

HFT(ADTV in thousands of contracts and mkt. share)*

HFT(participation per group of contracts)

Co-location

BM&F Segment (thousands of contracts)

4 20 41 50 69

155 74 92 73 58 75 89

5 18

44 41

50

43 40

45 43 45 38

4 7

22 53

77

93

90 85 87 98 125 92

59

0.3%1.0%

2.8%

4.8%3.8%

6.0%

4.4% 4.0% 4.5% 5.7%6.4%

5.3%

-

100

200

300

400

500

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10

FX Equities Mini contracts Interest Rates % in Overall Volume

BM&F Segment: 28 units

Both Segments: 8 units

Pipeline: 40 units

10.3%

23.7%

60.7%

FX contracts Index-based contracts Mini contracts

Round Trip Time, in milliseconds 2007 2008 2009 2010e

Equity Market 450 300 10 One digit

Derivatives Market 70 25 10 One digit

Throughput in thousands of trades

Equity Market – Average Capacity 390 770 1,500 3,000

Daily Average 153 245 332 432

Market peaks 343 414 591 800

Derivatives Market – Average Capacity 55 200 200 400e

Daily Average 23 29 39 68

Market peaks 42 49 76 152

Network Carrier RCCF`s Sole Provider 8 Networks (RCB)

17

Improving IT Capacity and Performance

OPERATIONAL HIGHLIGHTS

18

Daily Average Number of Trades (Thousands)

Average Daily Traded Value - ADTV (BRL Billions)

Number of Custody Accounts (Thousands) Turnover Velocity** (12 months average)

**Relation of the trading value in the cash market and the market cap of the exchange*Updated until: November 30th, 2010 19

BOVESPA Segment: operational highlights

1.2 1.6

2.4

4.9 5.5 5.3 6.5 6.8 6.6 6.5 6.9 7.3

5.8 5.4 5.6 6.7

7.8

6.3

2.004 2.005 2.006 2.007 2.008 2.009 YTD* jan-10 fev-10 mar-10 abr-10 mai-10 jun-10 Jul-10 Aug-10 Sep-10 Oct-10 nov-10

54 62 87 153

245

332

431 424 409 393 405 489

399 395 408 448

511 463

2.004 2.005 2.006 2.007 2.008 2.009 YTD* jan-10 fev-10 mar-10 abr-10 mai-10 jun-10 Jul-10 Aug-10 Sep-10 Oct-10 nov-10

30.8% 29.4%36.8% 37.6% 38.7%

42.3%

56.4%63.2%

66.6%

64.4%

2001 2002 2003 2004 2005 2006 2007 2008 2009

508 540 551 559 548 543 538

576 581 580

661 645 644

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 Oct´10 Nov´10

* For the overall market, it is the result of the annualized monthly value traded in the cash market on the average market capitalization. For VALE and PETR , it is the result of the annualized monthly number of shares traded in the Brazilian cash market on the average outstanding sharecount.

20

Market OverhangImpacts from the Petrobrás offering

Petro vs. Vale (Brazil trading)

Average Daily Number of Traded Shares (millions)

Average Daily Traded Value (BRL billions)

Overhang in the Market

Turnover Velocity* (%)

Price Level Evolution (Sep’09 = 100)

0.7

0.9 0.9

0.7

0.9 0.9 0.9

1.3

0.9 0.8 0.7

0.9 1.0

0,8 0.7 0.8 0.8

0.7 0.8 0.8

0.9 0.8 0.9

0.7

0.4

0.6

1.3 1.2

0,8

5.4

7.3

6.5 6.7

6.8 6.6

6.5

6.9 7.3

5.8 5.4 5.6

6.7

7.8

6,3

-

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

-

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

VALE PETR Overall Volume

19 22 20

16 20 21 19 21

29

21 20 17

20 20 16

21 21 21 18 22 24 25 24

29

22

15

21

47 45

29

VALE PETR

60

80

100

120

140

160

180

Petr3 Petr4 Vale3 Vale5 Ibovespa

0%

20%

40%

60%

80%

100%

120%

140%

160%

Total do Mercado Vale Petr

30.3.%

26.4%

13.3%

30.0%

Nov´10

Source: Bloomberg (in USD traded value of 35 companies with ADRs programs )

End of CPMF(Financial

Transaction Tax) Sarbanes-Oxley Act(SOX)

*Updated until 10/29/2010

43.3%

56.7%

Novo MercadoLaunching

21

Brazilian´s stock trading breakdown

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010* TotalIPOs - 1 - 7 9 26 64 4 6 10 127 Follow ons 14 5 8 8 10 16 12 8 18 10 109 Total 14 6 8 15 19 42 76 12 24 20 236

Dual Listings - - - 2 1 1 - - 1 - 5

Public Offerings in Number of Companies

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Jan

-10

Feb

-10

Mar

-10

Ap

r-1

0

May

-10

Jun

-10

Jul-

10

Au

g-1

0

Sep

-10

Oct

-10

No

v-1

0

Other USA Venues - Brazilian ADRs NYSE - Brazilian ADRs BM&FBOVESPA - companies with ADRs BM&FBOVESPA (except companies with ADRs)

Average Daily Traded Volume - ADTV (thousands of contracts)

Rate per Contract - RPC (BRL)

*Updated until: November 30th, 201022

BM&F Segment: operational highlights

805852

1,167

1,740 1,573 1,521

2,468

1,9062,184

3,117 3,0542,479

2,063

2,8632,442

1,9802,138

2,738

422 501 711 988 789 843

1,633 1,135 1,255

2,270 2,171 1,483 1,278

2,121 1,669

1,193 1,267

1,988

110 168 266

473 535 447

548

525 642

603 611

670 530

477

479

489 540

467

86 74 68

112 88 80

90

78 106

75 96

106

96

75

97

80 104

79

187 109

124

167 162 150

192

168 181

170 176

220

159

189

197

218 228

202

jun-05 jun-05 jun-05 jun-05 jun-05 jul-05 YTD* jan-10 fev-10 mar-10 abr-10 mai-10 jun-10 Jul-10 Aug-10 Sep-10 Oct-10 nov-10

BRL Int. Rate (Thousands) FX (Thousands) Index (Thousands) Others (Thousands)

2004 2005 2006 2007 2008 2009 YTD* J-10 F-10 M-10 A-10 M-10 J-10 J-10 A-10 S-10 O-10 N-10

Interest rates in BRL 0.887 0.962 0.906 0.950 1.141 0.979 0.907 0.971 0.977 0.722 0.780 0.961 1.044 0.893 0.952 1.054 1.016 0.887

FX rates 4.002 2.858 2.244 1.859 2.065 2.161 1.919 1.968 2.005 1.837 1.872 1.752 1.908 1.983 1.954 2.030 1.926 1.975

Stock Indices 1.561 1.688 1.419 1.501 2.145 1.620 1.536 1.466 1.716 1.372 1.616 1.313 1.643 1.372 1.619 1.466 1.758 1.484

Interest rates in USD 1.999 1.385 1.094 0.965 1.283 1.357 1.150 1.104 1.319 1.239 1.203 1.145 1.137 1.086 1.072 1.071 1.103 1.230

Commodities 7.159 5.693 4.749 3.195 3.587 2.307 2.135 1.711 2.029 1.934 2.281 1.890 2.216 2.021 2.266 2.232 2.544 2.151

Mini contracts - 0.038 0.034 0.054 0.162 0.176 0.127 0.133 0.139 0.129 0.136 0.122 0.133 0.124 0.130 0.121 0.118 0.125

OTC 1.199 1.703 1.571 2.111 2.355 1.655 1.602 1.588 1.408 1.626 1.790 1.646 1.895 1.684 1.973 1.384 1.318 1.384

Total RPC 1.620 1.467 1.247 1.224 1.527 1.365 1.149 1.254 1.308 0.961 1.031 1.171 1.274 1.084 1.167 1.287 1.258 1.092

-

200

400

600

800

1.000

1.200

2007 2008 2009 2010 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10

1st. Maturity 2nd. Maturity 3rd Maturity 4th. Maturity 5th Maturity

23

Interest Rate in BRL ContractsStructural changes behind the growth in volumes

Interest Rate in BRL Contracts Breakdown by Maturity (thousands of contracts)

Uncertainty in consensus

impacts short term contracts

Fixed Rate Credit – in BRL billions Public Debt / Fixed Rate - in BRL billions

Source: Brazilian Central Bank

0

100

200

300

400

500

600

700

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10

0

100

200

300

400

500

600

700

Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10

* Brazilian Hedge Funds

* Others include: Asset backed securities, real estate, FX, off-shore and retirement funds

Source: Anbima

24

Brazilian Investment Funds IndustryRecent development

Investment Funds: Portfolio Breakdown (BRL billions)

Investment Funds: Multimarket and Equities Evolution (BRL billions)

55% 52%63% 54% 47% 48% 44% 45% 45% 44% 44%

28% 29%17%

23% 24% 23%24% 23% 23% 24% 24%

8% 8%8%

10%16%

10%

12% 11% 11% 11% 11%

10% 11%12%

13%14%

18%

21% 21% 21% 21% 21%

770 815 972

1,190

1,361 1,222

1,549 1,604 1,597 1,633 1,654

2003 2004 2005 2006 2007 2008 2009 Jul-10 Aug-10 Sep-10 Oct-10

Fixed Income Multimarkets Equities Others*

212 233

167

270 324

286

368 368 363 389 400

61 67 81 121

211

123

184 179 174 180 181

2003 2004 2005 2006 2007 2008 2009 Jul-10 Aug-10 Sep-10 Oct-10

Multimarkets Equities

BM&F Segment: open interest

Nov/10

41.5MM

Nov/10

34.1MM

25

Derivatives Open Interest (millions of contracts)

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10

Interest Rates in BRL

Total Open Interest

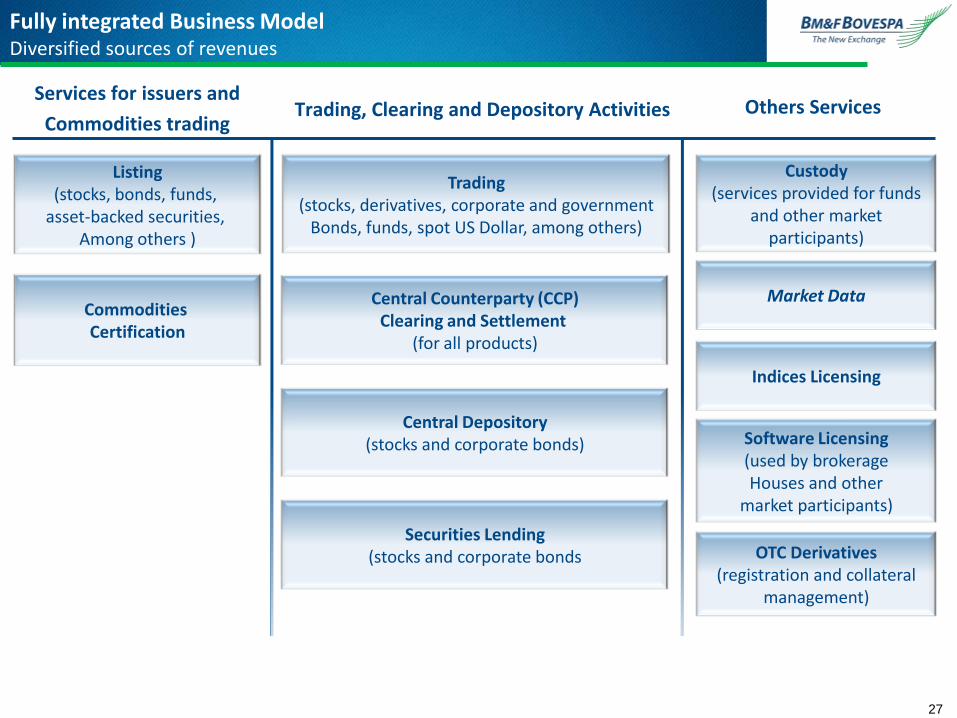

BUSINESS MODEL

26

Listing(stocks, bonds, funds,

asset-backed securities, Among others )

Commodities Certification

Trading(stocks, derivatives, corporate and government

Bonds, funds, spot US Dollar, among others)

Central Counterparty (CCP)Clearing and Settlement

(for all products)

Central Depository(stocks and corporate bonds)

Securities Lending(stocks and corporate bonds

Custody(services provided for funds

and other marketparticipants)

Market Data

Indices Licensing

Software Licensing(used by brokerageHouses and other

market participants)

OTC Derivatives(registration and collateral

management)

Fully integrated Business ModelDiversified sources of revenues

Services for issuers and

Commodities tradingTrading, Clearing and Depository Activities Others Services

27

Brokers & investors

Trading

Pos-Trading

Business Model, regulation and competition

Regulation prohibits internalization of orders, dark pools and ATS/MTFs, stocks trading in both exchange and OTC simultaneously

Settlement and clearing of stocks trading must be done through a CCP

Settlement and clearing at the beneficial owner level make the Brazilian market safer and more resilient

Under the regulation in place, potential competitors would be obliged to provide the same integrated solution, with the same rules and transparency

The final investor pays the exchange fee

Other exchanges have been seeking integrated models (self clearing models)

Naked access is not allowed

Naked short selling is not possible

28

Updated until: 12/03/2010

Market Capitalization (US$ billions) and 2009 EBITDA Margin (%)

Listed Exchange Business Model

Diversified and Integrated Integrated Derivatives Diversified but Not Integrated*

* Do not provide post-trading services for the equity market

Diversified and integrated Derivatives Diversified but not integrated

Business Model

29

Source: Bloomberg

25.620.8

16.312.8

8.5 7.6 7.1 6.6 4.5 3.4 2.6 2.1

80.2%

71.3%64.9%

51.9%

62.7%

43.1%

60.8%

74.3%

48.7%

39.0%

56.7%

66.5%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

80,0%

-

5

10

15

20

25

30

35

HKEx CME BVMF Deutsche Boerse

ICE Nyse Euronext

SGX ASX Nasdaq LSE TMX BME

EBITDA Margin 2009

28.6% 27.2%

36.3% 34.4%

11.5% 10.9%

23.7% 27.6%

Broker trading Fee Exchange Trading fee Exchange Clearing fee Exchange Depository fee

Brasil USA

Trading

Trading

Clearing

Central Counterparty (CCP)

Intermediary in the trading activity

Clearing

Securities Lending s activity

Counterparty risk on the Internalization of orders (1)

Intermediary in the trading activity

Central Depository

Securities Lending

Brokerage House

Stock Exchange

All-in Transaction Cost Comparison / Services Offered to

Investors

(1) Not allowed according to Brazilian regulation.Assumptions: 3 months holding period; Brazilian Investment fund trade; 1.5 Bp Broker Fee; and Securities lending not considered.

Total Cost5.3 bps

Exchange Cost3.8 bps

1.3 Bp

0.6 Bp

1.9 Bp

1.5 Bp Broker Cost1.5 bps

USD14.0 – Stock Price

All-in cost: USD0.008

USD28.0 – Stock Price

All-in cost: USD0.015

Fully integrated Business ModelCompetitive all-in cost

30

BRAZIL USA

BVMF

BVMF

BVMF

DTCC

DTCC

NYSE Nasdaq

BATS Direct Edge

TRF Dark Pools

Beneficial Owner Level

Broker Level

All the trades must be

matched on an exchange

environment

Brokers can internalizeorders

Central Depository

Clearing (CCP)

Trading on the Exchange

Broker

Equity market settlement structure: Brazil compared with USA

31

32

Appendix

Source: Rosenblatt Securities Inc. – Trading Talk

33

USA Consolidated Equities Volume Breakdown (Oct’10)

US Exchanges and Trading Venues: market share

19.4%

27.4%

18.2%

13.5%

8.9%

10.2%

2.4%Nasdaq + BX

NYSE + Arca

TRF (Adjusted)

Dark Pools

BATS

EDGX + EDGA

Other

R$46.7bi

R$163.8bi

2002 May/10

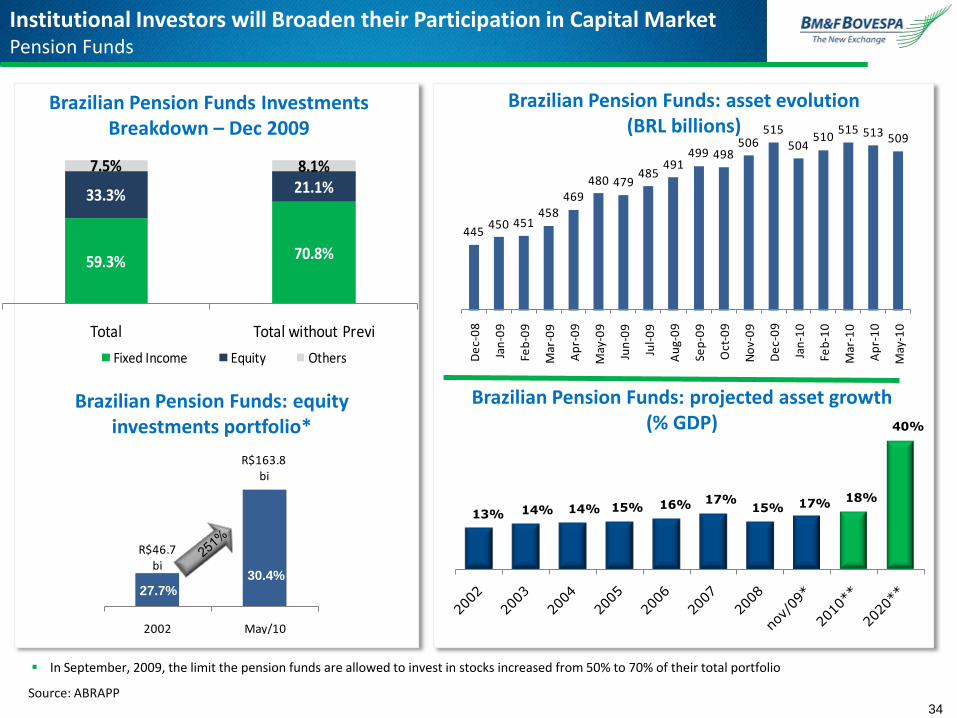

13% 14% 14% 15% 16% 17%15% 17% 18%

40%

Brazilian Pension Funds: projected asset growth(% GDP)

Brazilian Pension Funds: asset evolution(BRL billions)

Brazilian Pension Funds: equity investments portfolio*

27.7%30.4%

Source: ABRAPP

59.3% 70.8%

33.3% 21.1%7.5% 8.1%

Total Total without Previ

Fixed Income Equity Others

Brazilian Pension Funds InvestmentsBreakdown – Dec 2009

In September, 2009, the limit the pension funds are allowed to invest in stocks increased from 50% to 70% of their total portfolio

34

Institutional Investors will Broaden their Participation in Capital MarketPension Funds

445450 451

458469

480 479485

491499 498

506515

504510

515 513 509

De

c-0

8

Jan

-09

Feb

-09

Mar

-09

Ap

r-0

9

May

-09

Jun

-09

Jul-

09

Au

g-0

9

Sep

-09

Oct

-09

No

v-0

9

De

c-0

9

Jan

-10

Feb

-10

Mar

-10

Ap

r-1

0

May

-10

On Line Trading

Performance of BOVESPA Segment – Individual investors

35

Nov´1015.8%

Nov´1027.1%

0%

5%

10%

15%

20%

25%

30%

35%

Jan-03 Aug-03 Mar-04 Oct-04 May-05 Dec-05 Jul-06 Feb-07 Sep-07 Apr-08 Nov-08 Jun-09 Jan-10 Aug-10

% traded value % number of trades

*Includes regular trades and public offering; updated until November 30th, 2010.

Monthly Net Flow of Foreign Investments* (in BRL billions)

BOVESPA Segment: foreign investment flow

36

-1.0

0.9

-0.6

6.0

2.9

-2.8

-7.3

5.3

-1.8

-4.7

-1.2-0.4-0.6

0.51.4

5.7 6.1

4.2

5.5

2.5

5.2

9.1

2.11.4

-2.1

0.7

5.8

1.5

-1.5

-0.1

7.3

-0.6

10.0

4.4

2.1

BM&F Segment (Investor’s Participation in Total Volume)

Bovespa Segment (Investor’s Participation in Total Value)

Operational highlights: investor s participation in Total Volume

37

25% 25% 23% 27% 31% 31% 32% 31% 25% 27% 26% 28% 27% 24% 23% 24%

27% 27% 30% 27% 26% 29% 29% 30% 35% 34% 35% 36% 35% 35% 32% 32%

33% 36% 35% 35% 34% 28% 28% 27% 28% 30% 28% 28% 28% 31% 33% 35%

12% 10% 10% 8% 7% 9% 9% 9% 9% 7% 8% 7% 8% 7% 9% 8%2% 2% 2% 3% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 3% 2%

2005 2006 2007 2008 2009 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10

Individuals Institutional Investors Foreign Investors Financial Insitutions Companies Others

56% 51% 49% 48% 45% 43% 43% 42% 44% 43% 40% 41% 42% 44% 40% 39%

24%25%

23% 23% 24% 27% 26% 30% 26% 25% 29% 32% 29% 28% 31% 34%

12% 15% 17% 19% 20% 22% 23% 22% 24% 26% 25% 22% 23% 22% 22% 22%

7% 7% 9% 8% 8% 5% 5% 3% 4% 4% 4% 3% 4% 4% 4% 4%

2% 2% 2% 3% 3% 2% 3% 2% 2% 2% 1% 1% 1% 2% 2% 2%

2005 2006 2007 2008 2009 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10

Central Bank Companies Individuals Foreign Investors Institutional Investors Financial Institutions

Income Statement

38

(in thousands of BRL) 3Q10 3Q09Change

3Q10/3Q092Q10

Change

3Q10/2Q109M10 9M09

Change

9M10/9M09

Operational Revenues 541.609 426.505 27,0% 526.986 2,8% 1.579.255 1.199.004 31,7%

Trading / Clearing Systems - BM&F 186.802 132.017 41,5% 184.139 1,4% 541.154 403.930 34,0%

Trading / Clearing Systems-Bovespa 274.812 219.019 25,5% 259.309 6,0% 790.615 575.534 37,4%

Other Operational Revenues 79.995 75.469 6,0% 83.538 -4,2% 247.486 219.540 12,7%

Revenue deductions (54.743) (43.510) 25,8% (53.365) 2,6% (159.640) (121.219) 31,7%

Net Operational Revenues 486.866 382.995 27,1% 473.621 2,8% 1.419.615 1.077.785 31,7%

Operating Expenses (167.561) (132.502) 26,5% (143.494) 16,8% (444.839) (409.460) 8,6%

Operating Income 319.305 250.493 27,5% 330.127 -3,3% 974.776 668.325 45,9%

Equity account 23.142 - - - - 23.142 - -

Financial Income 77.407 57.042 35,7% 77.546 -0,2% 222.649 179.758 23,9%

Income before Taxes 419.854 307.535 36,5% 407.673 3,0% 1.220.567 848.083 43,9%

Net Income 293.208 246.795 18,8% 307.614 -4,7% 882.643 661.949 33,3%

Net Margin 60,2% 64,4% -4.2 pp 64,9% -4.7 pp 62,2% 61,4% 0.8 pp

EBITDA 336.375 262.039 28,4% 341.671 -1,5% 1.012.672 698.709 44,9%

EBITDA Margin 69,1% 68,4% 0.7 pp 72,1% -3.1 pp 71,3% 64,8% 6.5 pp

Adjusted Net Income 389.205 338.377 15,0% 426.272 -8,7% 1.217.945 909.523 33,9%

Adjusted net Margin 79,9% 88,4% -8.4 pp 90,0% -10.1 pp 85,8% 84,4% 1.4 pp

Adjusted Operational Expenses (145.846) (108.062) 35,0% (124.418) 17,2% (384.846) (313.006) 23,0%

Revenues Growth due to the market recovery

In BRL thousands 3Q10 3Q09% Change

3Q10/ 3Q09

Gross operating revenues 541,609 426,505 27.0%

BOVESPA Trd. / Sttmnt 232,890 210.117 10.8%

BOVESPA – Others* 41,922 8,902 370.9%

BM&F Trd. / Sttmnt 186,802 132,017 41.5%

Other operating revenues 79,995 75,469 6.0%

Depository and custody 21,447 17,235 24.4%

Vendors 15,352 16,082 -4.5%

Trading access (Brokers) 11,317 11,491 -1.5%

Listing 10,928 9,562 14.3%

Securities lending 12,714 8,866 43.4%

Bolsa Brasileira de Mercadorias 1,762 3,535 -50.2%

Settlement Bank 2,117 2,194 -3.5%

Other 4,358 6,504 -33.0%

Operating performance 3Q10 3Q09% Change

3Q10/3Q09

BM&F ADTV (thousands) 2,428.1 1,422.3 70.7%

BM&F RPC (in BRL) 1.167 1.391 -16.1%

BOVESPA ADTV (in BRL million) 5,905.8 5,214.4 13.3%

BOVESPA Margin (in bps) 6.162 6.296 -0.134bp

39

Bovespa segment revenues

BM&F segment revenues

Other revenues

219.0

274.8

3Q09 3Q10

132.0

186.8

3Q09 3Q10

75.5 80.0

3Q09 3Q10

25.5%

41.5%

6.0%

* It includes the fee from the settlement of the Petrobras Offering

13.3%

-0.13bp

BOVESPA SegmentStrong market recovery in the last two months

40

Revenue share Average Daily Traded Value (ADTV)

Average market capitalization 18.0% higher than 3Q09

52.7% growth in the ADTV of local institutional investors

Turnover velocity decreased to 59.2% in 3Q10 from 62.6% in 3Q09

(it was 71% in Oct´10 )

Trading / Settlement margin

Decrease to 6.16bps from 6.30bps, due mainly to the increase in

the participation of local institutional investors in the overall volume,

once this group of investors pay a lower fee in comparison with

other investors

Recent recovery in the equity market – ADTV (BRL billions)

51%

-11.6%

13.3%

31.7%

5.2 6.8 6.6 6.7 5.9 5.4 5.6

6.7 7.8

3Q09 4Q09 1Q10 2Q10 3Q10 Jul-10 Aug-10 Sep-10 Oct-10

1.7 1.6 1.5

2.4

1.4 1.3 1.7 1.6 1.5

1.9 1.4 1.4 1.5 1.7

1.4 1.6 1.9

2.2

3.1 3.1 2.5

2.1

2.9 2.4

2.0 2.1 0.3

2007

2008

2009

YTD

*

Jan-0

9

Feb

-09

Mar-0

9

Ap

r-09

May-0

9

Jun-0

9

Jul-0

9

Aug

-09

Sep

-09

Oct-0

9

No

v-0

9

Dec-0

9

Jan-1

0

Feb

-10

Mar-1

0

Ap

r-10

May-1

0

Jun-1

0

Jul-1

0

Aug

-10

Sep

-10

Oct-1

0

Additional ADTV from outlier months - Mar'10, Apr'10 and Jul'10 (millions)

ADTV excluding outlier months (millions)

2.1

70.7%

BM&F SegmentDespite the reduction of uncertainty in the market, volumes are still high

41

Revenue share Average Daily Traded Volume – ADTV

Climb in interest rates in BRL volumes (119.8% growth)

4.0% increase of FX volume and 21.2% increase of index based

contracts

Average Revenue per Contract - RPC

Increase in the participation of interest rates in BRL contracts in the

overall volume, to 68.4% from 53.1%

Negative impact due to FX appreciation (FX, interest rates in USD

and commodities contracts)

The higher the volume, the lower the RPC (volume tier based pricing)

Growth of HFT and DMA in the overall volume

Structural growth in the derivatives market (ADTV in millions of contracts)

34%

-16.1%

* Updated until October 2010

3Q10

In BRL thousands 3Q10 3Q09% Change

3Q10/ 3Q09

Operating Expenses (167,561) (132,502) 26.5%

Personnel (71,687) (63,883) 12.2%

Data processing (27,400) (24,233) 13.1%

Deprec. and amortization (15,067) (11,546) 30.5%

Outsourced services (12,293) (9,370) 31.2%

Communication (6,622) (6,219) 6.5%

Marketing (15,772) (5,841) 170.0%

Maintenance (2,529) (2,750) -8.0%

Board compensation (1,507) (1,184) 27.3%

Other (14,684) (7,476) 96.4%

3Q09

42

In BRL thousands 3Q10 3Q09% Change

3Q10/3Q09

Operating expenses (167,561) (132,502) 26.5%

Depreciation 15,067 11,546

Stock option plans 5,489 11,937

Tax related to equity accounting 2,003 -

Provision for doubtful accounts (845) 957

Adjusted operating expenses (145,846) (108,062) 35.0%

Operating Expenses Breakdown

Expense breakdown

43%

16%9%

7%

10%

15%

Personnel Data processing

Dep. and Amort. Third party serv.

Marketing Other

48%

18%

9%

7%

5%

13%

520 540

2010 old 2010e

272 250

2010 old 2010e

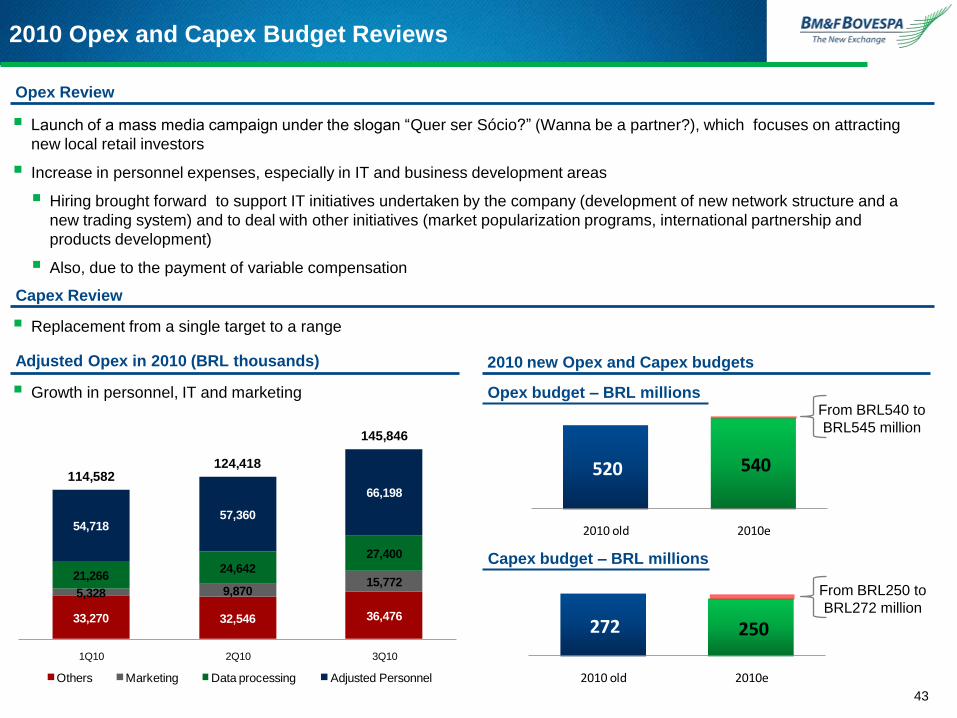

2010 Opex and Capex Budget Reviews

Adjusted Opex in 2010 (BRL thousands)

43

Opex Review

Launch of a mass media campaign under the slogan “Quer ser Sócio?” (Wanna be a partner?), which focuses on attracting

new local retail investors

Increase in personnel expenses, especially in IT and business development areas

Hiring brought forward to support IT initiatives undertaken by the company (development of new network structure and a

new trading system) and to deal with other initiatives (market popularization programs, international partnership and

products development)

Also, due to the payment of variable compensation

2010 new Opex and Capex budgets

From BRL540 to

BRL545 million

33,270 32,546 36,476

5,328 9,870 15,772

21,266 24,642

27,400

54,718 57,360

66,198

1Q10 2Q10 3Q10

Others Marketing Data processing Adjusted Personnel

124,418

145,846

114,582

Growth in personnel, IT and marketing

Capex Review

Replacement from a single target to a range

From BRL250 to

BRL272 million

Opex budget – BRL millions

Capex budget – BRL millions

BRL44.1 million in 3Q10: BRL36.2 million in IT and BRL7.9

million in other areas. The main projects were capacity increase

and the new trading platform

9M10: BRL138.1 million

3,659

3,688

•*Includes market participants cash collateral, earnings and rights on securities in custody and dividends and interest on capital pending payment

•** Includes third-party deposits (BRL175 million in 2Q10 and BRL142 million in 3Q10) and restricted funds (BRL10 million in both 2Q10 and 3Q10) from BM&F

Settlement Bank.

Financial HighlightsSolid financial position with strong cash generation

44

Cash, cash equivalents and investments (BRL millions) Financial income

BRL77.4 million in 3Q10: 35.7% higher than 3Q09

Financial revenues: BRL100.6 million in 3Q10, 52.7%

increase compared to 3Q09, mainly due to the increase of the

average interest rate

Financial expenses: BRL23.2 million in 3Q10, 162.4% higher

than 3Q09, mainly due to the financial cost of debt

Capex

From Aug’10 to Nov’10, 26.4 million shares were bought within

the program (BRL362 million)

The company can buy up to 31 million shares until Dec’10

Buyback program

BRL235.9 million as dividends, representing 80% of the GAAP

Net income in 3Q10

To be paid on November 25, 2010, based on the ownership

prevailing as of November 11, 2010

Earnings distribution (payout)

939

1,022

487

491

309

264

1,924

1,911

2Q10

3Q10

Market participants cash collateral and others*

Restricted funds

Subsidiaries**

Available funds

In BRL thousands

ASSETS Sep’ 10 Dec’09LIABILITIES AND

SHAREHOLDERS' EQUITYSep'10 Dec’09

Current assets 3,143,141 3,474,540 Current liabilities 1,422,836 1,142,076

Cash and cash equivalents 42,890 50,779 Collateral for transactions 984,766 810,317

Financial investments 2,917,792 3,295,356 Others 438,070 331,759

Others 182,459 128,405 Non-current liabilities 1,698,725 352,872

Non-current assets 19,217,204 17,383,299 Financing 1,027,188 2,495

Long-term receivables 1,099,771 973,305 Deferred Inc. Tax and Social Contrib. 616,448 300,930

Financial investments 727,517 605,648 Others 55,089 49,447

Others 372,254 367,657 Minority interest in subsidiaries 15,905 16,356

Investments 1,643,962 39,723

Shareholders' equity 19,238,784 19,362,891

Property and equipment 287,869 241,939 Capital 2,540,239 2,540,239

Capital reserve 16,533,760 16,512,260

Intangible assets 16,185,602 16,128,332 Others 148,880 294,036

TOTAL ASSETS 22,360,345 20,857,839 TOTAL LIAB. AND SHAREHOLDERS'

EQUITY22,360,345 20,857,839

Balance Sheet

45