bridgepoint education by: kannu priya, ryo seob (joseph) kim and rui (cindy) deng mar 27, 2012

TRANSCRIPT

BRIDGEPOINT EDUCATION

By: Kannu Priya, Ryo Seob (Joseph) Kim and Rui (Cindy) Deng Mar 27, 2012

Agenda

Introduction Macroeconomic Review Industry Overview Company and Business Overview Financial Analysis Financial Projections Recommendations

Introduction

Bridgepoint Education

Headquartered in San Diego, California

Provides postsecondary education services

Over $400M in net cash and investments

Market cap: $1.26B

Introduction

Position in GICS (Global Industry Classification Standard)

Education ServicesCompanies providing educational services, either on-line or through conventional teaching methods. Includes, private universities, correspondence teaching, providers of educational seminars, educational materials and technical education. Excludes companies providing employee education programs classified in the Human Resources & Employment Services Sub-Industry

253020Diversified Consumer Services 25302010

Introduction

Screening process BPI COCO APOL

Mkt Cap* 1260000 368440536000

0Ratio 1 1.21 -0.15 0.76Ratio 2 0.28 -0.17 0.22Sum 1.49 -0.32 0.98 PEG* 0.52 -1.83 1.64P/E* 8.04 28.55 12.02Fwd P/E* 8.52 7.75 12.58

Implied 1 yr g -5.63%268.39

% -4.45%Implied 5 yr g 15.46%-15.60% 7.33%Implied 7-10 yr g N/A 10.03% 1.76%*As of Mar 25, 2012 (Source: Yahoo! Finance)

Introduction

Stock Market Prospects P/E (ttm) = 8.04* It seems to be priced

for zero growth and eventual bankruptcy.

But in fact, most analysts who follow the stock see a bright future for Bridgepoint.

*As of Mar 25, 2012 (Source: Yahoo! Finance)

Macroeconomic Review

Unemployment rate: A leading indicator rather than a lagging indicator of recovery and GDP growth

Source: Capital IQ

Macroeconomic Review

Economic growth accelerated recently The labor market stabilized: Unemployment

rate inched down to 8.3% The employment population ratio remain

stable and showed early sign of improvement Outlook for 2012

Unemployment rate will remain between 7.5% and 9% but more volatile due to the growing number of discouraged workers re-entering the labor force.

Macroeconomic Review

Personal income increased $37.4 billion, or 0.3 percent in January 2012.

Source: The Bureau of Economic Analysis

Industry Overview

Education and training service industry is a broad category that encompasses job-specific certification, professional training and classes emphasizing self-fulfillment, leisure and hobbies.

The US education and training service industry includes about 45,000 companies and many more self-employed individuals with combined annual revenue of more than $30 billion.

Industry Overview

Major services Technical and trade schools (nearly 40% of

industry revenue) Business schools and computer training

(nearly 20% of industry revenue) Characteristics

Fragmented: The 50 largest companies represent 30% of total revenue

Labor-intensive: Average annual revenue per worker is around $65,000

Industry Overview

Demand Drivers Employment trend Personal income

Profitability Drivers Number of students recruited Operating costs

Instruction expenses: Faculty salaries, course materials, bad debt expense, lease and occupancy costs, and educational equipment

Administration expenses: Direct marketing, finance and accounting, admission expenses, and legal fees

Company and Business Overview Background

Bridgepoint Education operates through Ashford University and University of the Rockies. The company was founded by Warburg Pincus and current management with an aim of improving upon the online degree market's prevailing value proposition.

The company is a regionally accredited provider of postsecondary education services. It offers associate's, bachelor's, master's and doctoral programs in the disciplines of business, education, psychology, social sciences, and health sciences.

Company and Business Overview Background

Bridgepoint Education’s two academic institutions, Ashford University and University of the Rockies, were named to the 2012 President’s Higher Education Community Service Honor Roll, the highest federal recognition a college or university can receive for its commitment to volunteering, service-learning and civic engagement.

Ashford University is a private, for-profit university located in Clinton, Iowa. It is the largest educational holding of Bridgepoint Education ( 90% revenues from AU, 10% from Rockies) Although the university is regionally accredited by The Higher Learning Commission of the North Central Association of Colleges and Schools, it has begun the process of seeking regional accreditation from the Western Association of Schools and Colleges.

Company and Business Overview

FOR THE YEAR ENDED DEC. 31

2007 2008 2009 2010 2011

Total enrollment

12,623 31,558 53,688 77,892 82,100

Revenue* $ 85,709

$ 218,290

$ 454,324

$ 713,233

$ 933,349

Operating income*

$ 3,983 $ 33,420 $ 81,730

$ 216,421

$ 273,747

Net income* $ 3,287 $ 26,431 $ 47,105

$ 127,580

$ 172,764

Earnings per share fully-diluted

$ 0.01 $ 0.16 $ 0.74 $ 2.14 $ 3.02

Cash provided by operations*

$ 10,367

$ 70,748 $ 131,727

$ 189,949

$ 220,808

* In thousandsSource: Annual Report

Financial Highlights

Company and Business Overview

Source: bloomberg

Revenue and EPS Trend

Company and Business Overview

Source: bloomberg

Current Holdings

Company and Business Overview

Rank SchoolSchool Type

Repayment Rate

Retention Rate

Tuition Score

# 1 California University of Pennsylvania Online

Non-Profit

54% 74% $11,914 85.49

# 2 Western Governors UniversityNon-Profit

51% 76% $5,870 80.39

# 3 Iowa Central CollegeNon-Profit

54% 55% $5,790 79.36

# 4 National UniversityNon-Profit

51% 79% $11,088 78.97

# 5 Abilene Christian UniversityNon-Profit

62% 71% $22,760 76.80

# 6 Jones International UniversityFor-

Profit49% 89% $11,880 76.24

# 7 Northcentral UniversityFor-

Profit57% 63% $8,400 76.21

# 8 Bellevue UniversityNon-Profit

55% 38% $6,150 73.70

# 9 Concord Law SchoolFor-

Profit--- 75% $9,984 72.37

# 10 University of the Rockies Online

For-Profit

52% --- $12,096 71.44

College Ranking as per data from US Department of Education

Source: http://www.guidetoonlineschools.com/online-colleges

# 11 Northeastern UniversityNon-Profit

74% 93% $36,792 70.39

# 12 City UniversityNon-Profit

59% 30% $15,474 67.34

# 13 Colorado Technical University - Online Grad

For-Profit

39% 84% $10,665 66.96

# 14 Liberty University OnlineNon-Profit

45% 71% $18,064 62.41

# 15 Western International University

For-Profit

35% 67% $10,480 57.96

# 16 Upper Iowa University Online

Non-Profit

50% 61% $22,350 56.45

# 17 Saint Leo University OnlineNon-Profit

39% 69% $18,150 56.39

# 18 University of PhoenixFor-

Profit44% 52% $10,120 56.38

# 19 Grand Canyon UniversityFor-

Profit52% 25% $16,500 56.29

# 20 Academy of Art University Online

For-Profit

44% 63% $18,050 55.35

Rank SchoolSchool Type

Repayment Rate

Retention Rate

Tuition Score

Company and Business Overview

Source: http://www.guidetoonlineschools.com/online-colleges

Company and Business OverviewRan

kSchool

School Type

Repayment Rate

Retention

RateTuition

Score

Graduation rates for students who have completed at least two courses at Ashford was 51% for bachelors students and 74% for masters students.

Bachelor degree graduate salaries increased 11.6% y/y

# 21

Bryant and Stratton College Online

For-Profit

23% 73% $15,12051.8

7# 22

Ashford University

For-Profit

45% 36%$16,27

049.86

# 23

Capella UniversityFor-

Profit40% 29% $10,980

46.81

# 24

Walden UniversityFor-

Profit41% 29% $9,480

45.98

# 25

Colorado Technical

University - Online

For-Profit

39% 34% $11,66044.5

2

# 26

University of Maryland

University College

Non-Profit

37% 37% $12,28842.9

9

# 27

ECPI College of Technology

Online

For-Profit

29% 51% $13,55041.6

0

# 28

AT Still UniversityNon-Profit

33% --- $24,15636.2

7

# 29

American InterContinental

University

For-Profit

39% 14% $15,46536.2

7

# 30

Argosy University Online

For-Profit

37% 33% $19,81233.1

0

Source: http://www.guidetoonlineschools.com/online-colleges

Company and Business Overview

Source: bloomberg

BPI has among the lowest market cap compared to its competitors

Since the company’s P/E is below the industry average, the stock looks cheap

Company and Business Overview Enrollments

Total student population of 86,642 was ahead of market estimates of 84,570 representing an increase of 11.2% y/y.

Management expects the new student enrollment decline next quarter to be smaller than Q4 before turning positive in Q2, Q3, and Q4.

Management expects total population growth to be positive in all four quarters of 2012, in part reflecting strong improvements in retention.

Source: Annual Report 2010

Company and Business Overview Positives

Low tuition price results in a favorable student proposition and limits private loan exposure. It is one of the distinctive aspects of the company (~26% less expensive than comparable publicly traded online schools). Its credit-hour prices are comparable to those of state-funded institutions and its liberal credit transfer policy brings the cost even lower.

The low price point benefits Bridgepoint’s students as tuition is mostly covered by federal financial aid (Title IV), leaving only a minimal need (<1%) for private loans.

Ashton University brings with it, the heritage and long established traditions, both of which appeal to potential students. The traditional feel is an important competitive advantage.

Approximately 77% of Ashford’s students pursue bachelor’s programs, as they provide the right balance of revenue duration and market size, it brings advantage for the company

Company and Business Overview Innovation in productivity- Strengths

Constellation Bridgepoint’s proprietary suite of web-based course materials, is

replacing third-party textbooks in many of Ashford University’s courses.

This contributes to student affordability, allows students to save money on course materials approximately 50% over traditional textbooks while enhancing the overall learning experience

It is expected to save 80% by the end of 2012

Rockies Mobile Anytime and anywhere access to systems and content Mobile app for Apple’s iPhone and other mobile devices. With

convenient, anytime and anywhere access to information, this app allows

University of the Rockies students to connect with courses, post to discussions, follow threads, interact with

instructors, monitor school news and events, and stay on top of enrollment and academic matters.

Company and Business Overview New Technology- Strengths

In January, Bridgepoint showcased the external version of Constellation, called Thuze, and announced partnerships with three major textbook publishers for a beta test of 850 students at 200 public and private universities across the U.S.

While management commented that it is too early for specific feedback from the trial, management believes that Thuze has been well received by educators and publishers and management is enthusiastic that the technology has large potential for mobile platforms

The company believes that its focus on innovation and technology is a significant differentiator in providing a quality education to its students.

The company plans to continue branding efforts in 2012 to build awareness. It has also decided to shift toward more expensive lead sources, which its own data analysis has shown results in students that retain at higher rates and ultimately are more profitable in the long run.

Company and Business Overview Internal & External Challenges

BPI and its peers have become the focus of increased regulatory scrutiny from the regulators.

The gainful employment regulations effective July 1st 2011, require that, for-profit institutions comply with certain marketing and incentive compensation policies and adhere to specific levels of graduate salaries and student debt in order to remain eligible under the Title IV federal student aid program.

BPI’s has historically focused on growth in enrollments and the revenue, which may distract the management from ensuring proper reinvestments in academic quality and infrastructure. BPI currently boasts of the highest gross margin in the sector (72% in 2011). Therefore, its important for investors to monitor that proper reinvestments are made into the instructional costs (faculty esp., admissions counselors and content) that reinforce academic quality and productive academic outcomes.

Also, online schools, such as the ones owned by Bridgepoint, The recently completed Office of Inspector General (OIG) audit at Ashford University has identified certain Title IV compliance issues, which seem manageable but may have negative regulatory consequences for the company.

Management expects 2012 net income to decline 17%-20% y/y (to $138.2-$143.7 million), due to increased investments in branding, data analytics, and class size reductions, among others.

Company and Business Overview Title IV and Cohort Default Rates

As of the year-end December 31, 2011, Ashford University derived 86.8% of its revenues and University of the Rockies derived 85% of its revenues from Title IV funds. Management is confident that it can continue to manage this metric going forward.

Ashford University’s two-year cohort default rate (CDR) for 2009 was 15.3%, and the just released draft two-year CDR for 2010 was 10.4%. For the University of the Rockies, the two-year CDR for 2009 was 3.3% and the 2010 draft CDR was 3.9%. The Regulations require less than 25% CDR for the trigger of the rule against the company

Earlier this week, the company received draft three-year CDRs, which were 20.2% for Ashford and 3.3% for the University of the Rockies. Management expects these rates to trend lower in the future as the company continues to invest in attracting and retaining better-performing students.

(of Total Rev) 2007 2008 2009 2010

Ashford U 13.30% 13.30% 15.30% 10.40%U of R 0.00% 2.50% 3% 3.90%

Title IV Programs (the 90/10 rule) - 2011(of total rev.) 2009 2010 2011

Ashford U 85.50% 85.00% 86.60%U of R 84.60% 85.90% 85%

Financial Analysis

- Cash and Investment Assets are worth 0.41 bn (66.4% of total assets) with its M. Cap 1.26 bn. - BPI’s capital expenditure is expected to be stable in future (4% of total Rev.) . Therefore, the increase in Cash and Investment Assets are expected to continue (but at a lower rate).

- BPI has a strong cash generating business and has built excess amount of cash from last few years’ high growth in its business. (FCF in 2011 = 186.3 mn, N/I in 2011 = 172.8 mn.)

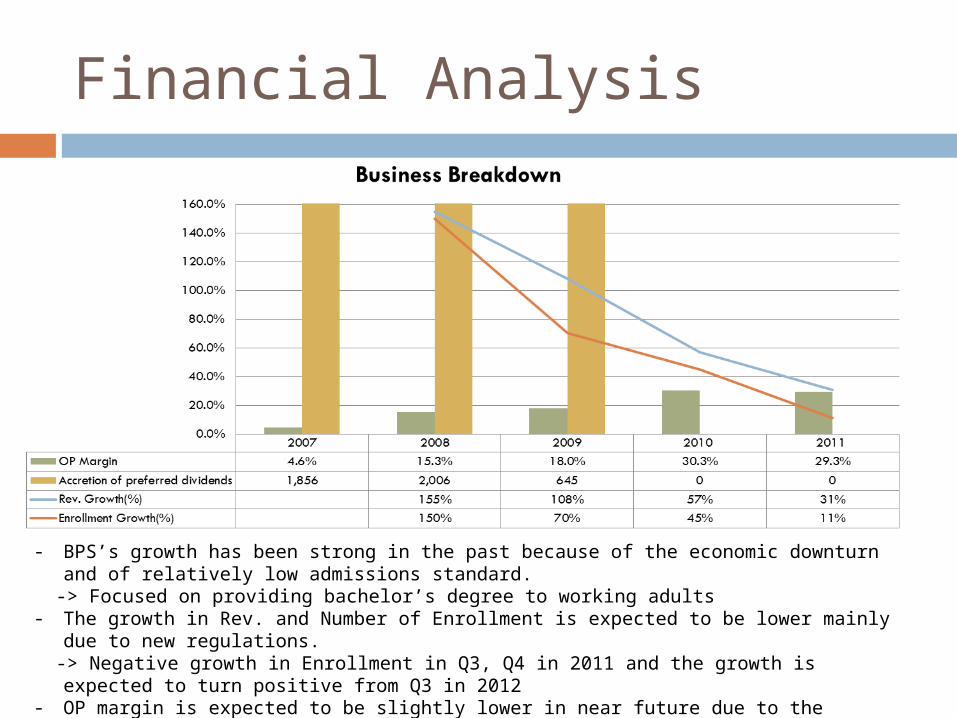

Financial Analysis

- BPS’s growth has been strong in the past because of the economic downturn and of relatively low admissions standard.

-> Focused on providing bachelor’s degree to working adults - The growth in Rev. and Number of Enrollment is expected to be lower mainly due to

new regulations. -> Negative growth in Enrollment in Q3, Q4 in 2011 and the growth is expected to turn

positive from Q3 in 2012 - OP margin is expected to be slightly lower in near future due to the increase in

Instructional and marketing cost.- Growth rate of Rev. is expected to be higher than that of Enrollment. (Increase in tuition

fee and other sources of Rev.)

Financial Analysis

2010 2011

NP Margin 17.89% 18.51%

Total Asset Turnover

1.86 1.72

Equity Multiplier

2.06 1.83

ROE 68.44% 58.38%- Current P/B ratio is 3.60, but with BPI’s high ROE, high P/B ratio seems justifiable

(58.38%/3.6 = 16.21% return).- However, ROE in the future is expected to be slightly lower in near future because of lower

NP margin and lower TAT.<Outlook for 2012> - 2012 will be a new stage for companies in the education sector because of the new regulations and improvement of labor market in the states. - Hard to project figures, especially with the new situation for the company. - According to the management’s guidance, 10% growth in rev. and enrollment, 24% as OP margin, 17% decrease in EPS in 2012.

Conservative Management

Actual Earnings have always been higher than the management’s guidance.

Source: Earnings.com

Multiple Valuation

Rev Growt

h

EPS Growt

h

OP Margi

n

ROE P/E P/B P/S

Industry Avg.

6.71% 10.15% 19.10% 42.51% 11.04 5.13 1.22

BPI 30.86% 39.24% 32.80% 58.38% 8.03 3.53 1.35

APOL -3.91% 7.75% 23.80% 35.29% 10.05 4.04 1.26

DV 13.95% 20.66% 19.30% 17.87% 10.47 1.73 1.12

EDMC 15.11% 35.77% 15..80%

9.25% 10.42 0.95 0.73

BPI is being traded at discount even with its higher-than-industry average growth, margin, and ROE.

BPI looks competitive because BPI has retained its margin higher than its competitors even with its low price strategy.

Because of the new regulations, its long-term future growth rate is expected to be around 11%, so it is justifiable for BPI’s valuation to be 13 times its earnings.

Target price for BPI is 36.70 with expected EPS 2.77 in 2012. (47% upside potential)

Ownership Structure

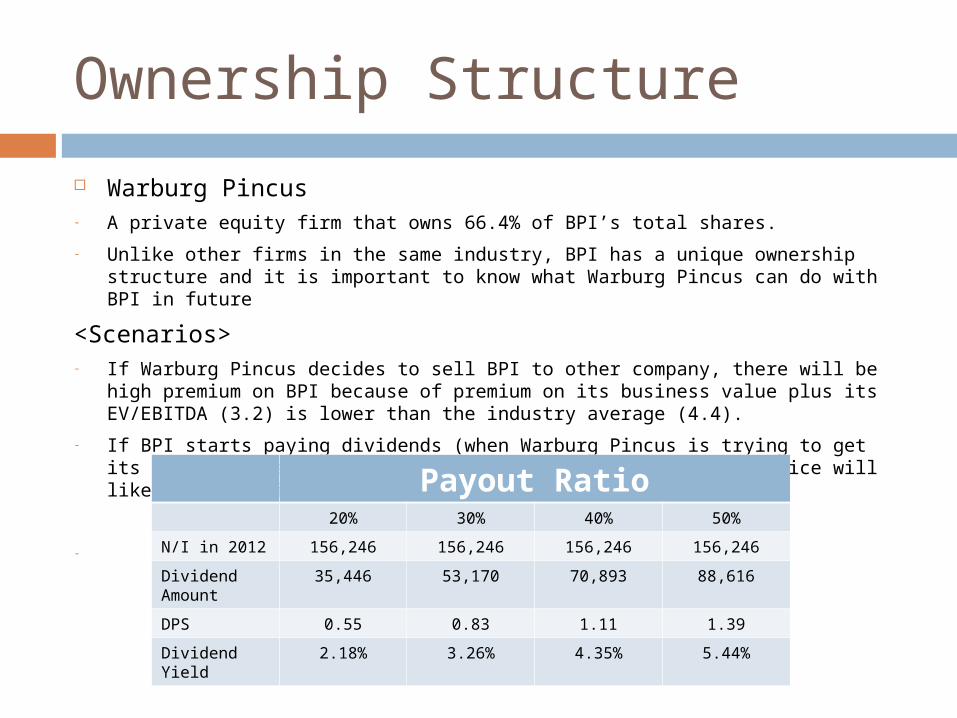

Warburg Pincus - A private equity firm that owns 66.4% of BPI’s total shares.

- Unlike other firms in the same industry, BPI has a unique ownership structure and it is important to know what Warburg Pincus can do with BPI in future

<Scenarios>- If Warburg Pincus decides to sell BPI to other company, there will be high premium

on BPI because of premium on its business value plus its EV/EBITDA (3.2) is lower than the industry average (4.4).

- If BPI starts paying dividends (when Warburg Pincus is trying to get its initial investment back by receiving dividends), stock price will likely go up (without any harm to BPI’s business operation.)

-

Payout Ratio20% 30% 40% 50%

N/I in 2012 156,246 156,246 156,246 156,246

Dividend Amount

35,446 53,170 70,893 88,616

DPS 0.55 0.83 1.11 1.39

Dividend Yield

2.18% 3.26% 4.35% 5.44%

Recommendation

- Even with expected negative growth in 2012, the current price is attractive. (Both down-side risk and up-side potential exit)

- Projection for future is difficult with new regulations and a relatively short history of the on-line for-profit education industry.

- But BPI has its own strength over its competitors and proved its competitiveness during the last 3rd and 4th quarters.

- BPI’s ownership structure seems positive rather than negative to equity investors.

- Therefore, we recommend to buy 500 shares of BPI at a market price, which is worth about $12,735.

Q&A