bsg 2012 14 (bsg lessons from the 2011 european stress tests exercise)

TRANSCRIPT

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

Giovanni Petrella* and Andrea Resti**

December 5, 2011 – DRAFT – COMMENTS WELCOME

Abstract - Supervisory stress tests assess the impact of an adverse macroeconomic scenario on the profitability and capitalisation of a large number of banks (accounting for a significant share of the overall loans and deposits). The results of such stress test exercises have recently been disclosed to the public in an attempt to restore confidence by curbing bank opaqueness, i.e., helping investors distinguish between sound and fragile institutions. The 2011 European Union stress test carried out by the EBA lead to the release of some 3,400 data points for each of the 90 participating banks. Market participants were not only given a predetermined, "black box" outcome, but were also in a position to adjust the supervisors’ “adverse scenario” by simulating further shocks and to assess each bank’s resilience to alternative assumptions. This makes the 2011 EU exercise an ideal empirical experiment to investigate a number of hypotheses on stress tests and bank opaqueness. E.g., were the test’s results deemed relevant by investors or simply ignored? Did they trigger a price adjustment process, and if so, for what banks? To what variables did the market associate the strongest importance? Did investors care about the results of the EBA’s adverse scenario, or did they simply rely on historical, detailed data to run their own stressed simulations? The paper investigates such questions through a thorough econometric analysis of stock-market data.

1 Introduction

A supervisory “stress test” program requires a large number of banks (accounting for a

significant share of the overall loans and deposits) to assess the impact, on their

profitability and capitalisation levels, of an adverse macroeconomic scenario.

Unlike in the internal stress tests used by individual banks for risk management and capital

planning purposes (and required by the so-called “Pillar Two” in the 2004 Basel Accord),

supervisory stress tests are to be run by all involved institutions based on the same

downturn scenario (e.g., a 2% decrease in GDP, a 3% surge in the unemployment rate, a

20% drop in stock prices, etc.) and covering an identical forecast window (typically two

years). This makes supervisory stress test results highly comparable across banks.

The outcome of the test can be kept confidential by the supervisors, but recently results

have often been disclosed to the public, in an attempt to restore confidence and help

investors distinguish between sound and weak institutions (with the latter often being

forced to recapitalise as the stress test results were announced).

* Università Cattolica del Sacro Cuore, Milano ([email protected]); ** Bocconi University,

Milano ([email protected]). Helpful comments by Mario Quagliariello are gratefully acknowledged.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 2 *

It has been argued, however, that such publicly disclosed stress tests are inherently flawed:

on one side, supervisors cannot test adverse scenarios which are extreme enough to provide

a truly “stressed” environment, as they might scare investors or simply be politically

unpalatable (e.g., scenarios involving the default of one or more sovereign entities); on the

other hand, if the downturn scenarios are perceived as too mild by investors, the stress test

results will simply be ignored by market participants. Also, if macroeconomic conditions in

the following months deteriorate more than it was anticipated by the “stressed”

assumptions (possibly leading to the failure of one or more banks which had passed the

test), this might dent the supervisors’ credibility and hence lead to greater market

uncertainty1.

To address such concerns, some supervisors have decided not to disclose the stress test

results, using them only internally, as a way to pre-emptively address capital shortages by

individual banks. Furthermore, even those supervisors who still make results public are

increasingly shifting away from issuing a simple, “binary” signal on “pass” and “fail”

banks, and have considerably increased the depth and width of the data released to the

public, to help investors “decide for themselves”, based on fresh, rich, reliable data.

Namely the 2011 European Union stress test (carried out by the European Banking

Authority, EBA) lead to the release of some 3,400 data points for each of the 90

participating banks. As all banks had to use the same data structure (which was shared with

the public ahead of the results’ publication), market participants were in a position to adjust

the supervisors’ “adverse scenario” by simulating further shocks and assessing each bank’s

resilience to alternative sets of assumptions.

This makes the 2011 EBA stress tests an ideal empirical experiment to investigate a

number of hypotheses on stress tests and bank opaqueness. Were the test’s results deemed

relevant by investors or simply ignored? Did they trigger a price adjustment process, and if

so, for what banks? To what variables did the market attach the strongest importance? Did

1 Furthermore, some banks have argued that, if too many details on balance-sheet composition are made

public, this could damage business confidentiality and give rise to legal risks. Also, other market participants could gain insights into one bank’s risk profile, e.g. by estimating the amount of needed financial hedges and using this information to carry out arbitrage strategies on the CDS market (Bryant 2011).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 3 *

investors care about the results of the EBA’s adverse scenario, or did they simply rely on

newly-available detailed data to run their own stressed simulations?

Another fact that makes the 2011 EU stress test an interesting area of research is that it was

quickly dismissed by some bank analysts as plainly useless, as it failed to reverse the

downward trend experienced by bank stock prices in late 2010 and 2011. Such conclusions

appear somewhat rushed. One one hand, it is hard to see how a supervisory exercise, no

matter how timely and accurate, could by itself stop a long-lasting decline in bank shares

and prevail over market jitters caused by a deep sovereign debt crisis. On the other hand,

stress tests cannot be evaluated by looking at market returns in the following weeks or

months, as they are most likely affected by a number of further news and events (e.g.,

bailout plans for Greece) which go well beyond the stress test exercise. Accordingly, a

rigorous econometric analysis is needed, focusing on the days immediately after the release

of stress test results, before one can claim that the whole exercise was ineffective.

This paper unfolds as follows: §2 summarises previous research results on bank

opaqueness and stress tests; §3 presents the main features of the 2011 European stress test;

§4 states the hypotheses to be tested in our empirical analysis; §5 describes our sample,

methodology and key variables; §6 shows our main results, while further results and

robustness checks are presented in §7; §8 concludes.

2 Literature review

Compared to other companies, banks have an higher share of assets which suffer from a

strong degree of opaqueness: e.g., loans are informationally sensitive and hard to evaluate

for outsiders, while liquid assets are easily sold and replaced, so that the data in financial

statements may rapidly become obsolete. As a result, banks may be harder to assess, for

investors and rating agencies, than non-bank companies.

A proof of bank opacity is the fact that market prices react to supervisory announcements

(Jordan 2000). Also, split ratings tend to occur more often for banks than for non-bank

companies (Morgan 2002; Iannotta 2006), suggesting that the latter are harder to assess,

due to stronger opaqueness. Regressions of bank stock returns on market indices show

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 4 *

higher R-squares (Haggard and Howe 2007); this means that firm-specific information is

harder to extract and therefore plays a less relevant role for bank stock prices2.

Several supervisory tools are usually put in place, including deposit insurance and risk-

based capital requirements, to prevent lenders and depositors from being scared away by

bank opacity. As opacity tends to increase in times of crisis (Flannery, Kwan, and

Nimalendran 2010), additional instruments are needed to reassure the market during a

financial turmoil.

This is the case of the stress testing exercises carried out in the US (20093) and the

European Union (20104 and 20115). The effects of a downturn scenario on a large number

of banks were simulated, with the main results being released to the public (including any

capital shortfalls arising from the simulation). By disclosing information on each bank’s

strengths and vulnerabilities, the supervisors aimed at reducing market uncertainty,

stabilise stock prices and prevent panic6; the idea was that investors, when presented with a

deep and robust flow of data (made comparable across banks and somewhat “certified” by

the supervisors’ intervention in the test), would consider banks less opaque, and therefore

better differentiate among banks when setting the risk premium required to invest in equity

capital, or to lend.

Table 2 illustrates the main characteristics of the three exercises mentioned above7,

highlighting the amount of information released to investors. While the 2009 and 2010

stress tests implied the publication of a limited number of key figures for each bank, the

2011 EU-wide test was significantly more ambitious, as more than 3,400 data-points for

each bank could, in principle, be provided8.

2 The fact that bank prices are driven mostly by easily observable variables (like market indices) also

provides an explanation for the results in (Flannery, Kwan, and Nimalendran 2004), where stockmarket analysts are found to agree more often on bank valuations than they do for other industries.

3 (Federal Reserve 2009a). 4 (Committee of European Banking Supervisors 2010). 5 (European Banking Authority 2011a). 6 To quote the Federal Reserve report whereby the 2009 stress test results were released to the public, “the

decision to depart from the standard practice of keeping examination information confidential stemmed from the belief that greater clarity […] will make the exercise more effective at reducing uncertainty and restoring confidence in our financial institutions” (Federal Reserve 2009b).

7 Stress testing exercises have also been carried out, with different scope and depth, by most national authorities in the European Union. See (Quagliariello 2009) for a complete picture of macro- and micro- stress testing approaches in many European countries.

8 This included a breakdown of sovereign bonds and credit exposures by country and duration bands; as most banks did not have an exposure to all countries and duration bands, many data points (about 73% of the total) were filled with zeroes; note however that those were meaningful zeroes, informing that a given

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 5 *

Table 1: Main Stress Test Exercises in the US and EU

Exercise Announcement date

Results release

date

Banks covered # of released data items per bank

Minimum capital

target(s)

Capital shortfalls

found

Supervisory Capital Assessment Program (SCAP) by Federal Reserve, FDIC, OCC, OTS

February 10, 2009

May 7, 2009

19 domestic bank holding companies covering 2/3 of

the assets in the US banking system

17 Common Tier 1 at 4%, Tier

1 at 6%

10 banks, USD 75 bn.

2010 EU-wide Stress Testing Exercise by the Committee of European Banking Supervisors

December 2, 2009

July 23, 2010

91 banks, covering 65% of the assets in the EU

banking system and at least 50% for each member

country

27 Tier 1 at 6% 7 banks (+17 “near fail”),

€3.5 bn.

2011 EU-wide Stress Test by the European Banking Authority

January 12, 2011

July 15, 2011

90 banks, covering 65% of the assets in the EU

banking system and at least 50% for each member country

3,456 Core Tier 1 at 5%

8 banks (+16 “near fail”),

€2.5 bn.

These stress tests and their market impact have been discussed by some recent research

papers. (Hirtle, Schuermann, and Stiroh 2009) provide a qualitative assessment of how the

2009 US exercise (the “SCAP”) was received by investors: in the Authors’ opinion, the

process was perceived as rigorous and thorough, transparency was appreciated, the

aggregate estimated capital shortfall was seen as reasonable and consistent with other

analysts’ forecasts, the variation across firms was in line with market expectations. In

short, the SCAP was appreciated by the market because it did not add any major

unforeseen element to the market’s information set; paradoxically, one might say that it

helped reassure markets right because it did not significantly increase transparency9.

A more quantitative assessment of the SCAP’s market impact is provided by (Peristiani,

Morgan, and Savino 2010) using standard event study models. Several dates are analysed,

including the SCAP’s initial announcement, the release of some important clarifications

regarding its methodology and policy implications (in terms of compulsory capital

increases and possible government interventions), and of course the final disclosure of

bank-by-bank figures. The market is found to have reacted only to policy-related

bank was not exposed to that specific combination of duration and nationality. Another 5.3% of the data points included missing values; again most of them were, again, “meaningful missings”, e.g. to indicate that banks did not expect any state aid in the following months, neither through equity nor hybrid securities.

9 In the Authors’ words, “whether the reception would have been positive if […] there had been a negative “surprise” about a firm or a group of firms, remains open to debate”.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 6 *

clarifications and to the publication of stress test results. Investors have been able to guess

in advance what banks would be required to raise extra capital; accordingly, when actual

results were released, the impact on stock prices was not driven by the “gross” capital

shortfall highlighted for each bank, but rather by its “unanticipated” component (net of

market expectations). Overall, the stress test exercise appears to have been informative to

investors, hence to have had a positive effect in terms of dissipating opaqueness and relieve

panic.

(Blundell-Wignall and Slovik 2010) look at the 2010 EU-wide stress test with a special

focus on the treatment of sovereign debt. In the 2010 simulation, government bonds were

subject to a haircut only when held in the trading portfolio (while no credit-related losses

were imposed on sovereign exposures in the banking book10). The Authors show that 83%

of the sovereign debt held by EU banks at end 2009 was instead held in the banking book,

and conclude that this could explain why the encouraging results of the 2010 stress test

failed to reassure the market. To some extent, their critique also applies to the 2011

exercise, as again no proper haircut was imposed on sovereign bonds outside the trading

book; however, the credibility of the final results was somewhat improved by the fact that

losses were imposed also on sovereign exposures held in the banking book, although

indirectly (through a floor on the “expected loss rate” applied to exposures towards banks

and sovereigns located in different countries, see Appendix 1 for details).

(Beltratti 2011) looks at the 2011 EU-wide stress test and concludes that they provides

relevant information to markets, since their outcome (i.e., the capital shortfall associated

with individual banks) could not be forecast by combining variables that were already

known to the market ahead of the stress test exercise.

(Cardinali and Nordmark 2011) analyse the 2010 and 2011 European stress tests by

looking at cumulative abnormal returns for tested and untested banks. However, they not

cover the release of 2011 results, but only the announcement of the new stress test and a

number of methodological clarifications issued by the European Banking Authority while

data were being collected and processed. While the 2010 exercise appears to have been

relatively uninformative to investors, the release of the 2011 methodology (including the

10 Loosely speaking the trading portfolio, or trading book, consists of financial assets held at fair value and

includes the bank’s own position in financial instruments for trading purposes (ie., aimed at generating profits in the short run by buying and selling securities) as well as derivatives held to hedge that position. The banking book includes all other exposures (often long term) which are not held in the trading book.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 7 *

decision to focus on a “core Tier 1” target11 of 5% which was considerably more

conservative than the one used one year before) gave rise to negative CARs for stress-

tested banks, while non-tested institutions remained roughly unaffected. Also, the paper

finds no major differences between PIIGS and non-PIIGS banks12.

3 The 2011 EU-wide stress test

3.1 Scope and assumptions

The 2011 EU-wide stress test was carried out on 90 banks accounting for more than 65%

of the total assets in the EU banking system. For each member state, a variable number of

banks were included, starting from the largest one and stopping when at least 50% of total

assets was covered13.

The starting point was the financial data as of December 31, 2010. The simulation exercise

covered two years (2011 and 2012) and consisted of two scenarios: baseline (designed by

the European Commission) and adverse (set up by the ECB).

Under the baseline scenario a strengthening of macroeconomic recovery was assumed,

with GDP growth of 1.7% and 2% in the EU. Under the adverse scenario, GDP would

shrink by 0.4% in 2011 and stay flat in 2012; meanwhile, equity prices would drop by

15%, short-term risk-free rates would increase by 1.40% and long-term ones by 1.25%.

Credit spreads for sovereign debts in Europe would also pick-up, with different increases

for individual countries. The USD would devaluate by 11%.

Starting from such macroeconomic assumptions, banks were requested to use their internal

models to generate values for balance-sheet items and P&L results. In doing so, however,

they had to follow a detailed methodology specified by EBA. Firm-specific assumptions,

as well as results generated by individual banks, were subsequently cross-checked by

national supervisors and by EBA itself, and further calibrated when necessary.

11 “Core Tier 1” refers to high-quality capital, such as common equity and government-sponsored hybrid

securities, net of a number of deductions to make the final result robust and comparable across different banks and countries. However, it is not equivalent to the “common equity Tier 1” capital dictated by the so-called “Basel 3” agreement.

12 PIIGS banks are those headquartered in Portugal, Ireland, Italy, Greece and Spain. 13 National authorities could add further banks in sample, beyond this minimum requirement (e.g., Spain

included several other minor banks).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

3.2 Key dates

As shown in Figure 1, the stress test was announced by EBA on 13 January 2011 (“the first

announcement date”) with a short press release highlighting the expected duration of the

exercise (“first half of 2011”) and EBA’s commitment to make results public14. No further

details were provided.

On 2 March 2011 (“the detailed announcement date”) EBA outlined the overall logic

underlying the simulation exercise and indicated that EU member states might put in place

“remedial back stop measures” (i.e., capital increases) to address any weaknesses that the

stress test may reveal.

The methodology to be used by banks when carrying out simulations was disclosed on 18

March 2011 (“the methodology date”). This included a 51-page note15 and four annexes,

providing an in-depth description of how all the main items in the banks’ balance-sheets

and P&L accounts had to be generated (including, e.g., haircuts to be applied to sovereign

risk exposures).

14 EU Regulation 1093/2010, whereby EBA was established, mandates the Authority to carry out annual

bank stress tests, but no legal provision requires that the results be released to the public. 15 (European Banking Authority 2011a).

Figure 1: Timeline of the 2011 EU-wide stress test

13 January 2011First announcement date

2 March 2011Detailed announcement date

18 March 2011Methodology date

8 April 2011Capital definition date

9 June 2011Clarification date

15 July 2011Release date

Pre-releasedates

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 9 *

On 8 April 2011 (“the capital definition date”) EBA released the list of banks participating

in the stress test exercise, as well as the definition of bank capital to be used (“core Tier 1

capital” that is, mainly equity capital and reserves from retained profits). It also clarified

that ordinary shares subscribed by governments, as well as other forms of public support,

would be indicated separately upon disclosure of the stress test results, thereby enabling

market participants to appreciate their role in propping up bank capital.

On 9 June 2011 (“the clarification date”) a clarification note16 was released, aimed at

improve consistency across different banks. This addressed several aspects of the stress

testing exercise, mainly the treatment of exposures to banks and sovereigns, and implied an

upward revision of the haircuts applied to sovereign securities in the trading book (making

the test more conservative and consistent with the deterioration experienced by PIIGS

bonds in the last few weeks), as well as minimum loss rates for sovereign exposures in the

banking book.

Stress tests results were released on 15 July 201117 at 6 pm CEST (complete data for all

individual banks was available by 6:30). We call this18 “the release date”, while all other

prior dates are be collectively referred to as “pre-release dates”.

3.3 Disclosed outputs

Results for each bank participating in the test were disclosed to the public through a MS

Excel template including several sections. The main areas covered were the following

data on risk-weighted assets and own funds; the latter included a breakdown of

items recognised as “core Tier 1” by EBA, compulsory deductions, governmental

support, mitigating measures not yet in place but fully committed before 30 April

2011;

key P&L figures, including net interest income, trading income, impairments, other

income/losses and net profit after tax;

16 (European Banking Authority 2011b). 17 The publication date for the stress test results was announced on 8 July 2011 and marked a delay

compared to the original schedule (results were expected to disclosed in June), mainly due to the need of further review and data quality-assurance work.

18 As the results were in fact released after market close, we use the following trading day (18 July) as the actual “release date”:

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 10 *

details on provisions, loss rates and coverage ratios for performing and non-

performing exposures (with separate evidence on retail, corporate, bank and

sovereign portfolios);

a breakdown of credit exposures by geographic area, counterparty and default

status (i.e., defaulted vs. non-defaulted);

a breakdown of sovereign exposures by geographic area, accounting treatment (e.g.

trading book, fair value option, available for sale, etc.), duration band. This

included derivative exposures at fair value. Short positions were also partially

accounted for, although in a conservative manner.

4 Testable hypotheses

This paper analyses the market reaction to the 2011 EU-wide exercise in order to

empirically test a number of (partly alternative) hypotheses.

The simplest one is that the market did not react to the stress test (either upon the pre-

release announcements or when bank-by-bank results were published). This would signal

that the whole stress testing process had no information content or lacked credibility, e.g.

because of the political constraints which prevented the implementation of an adequately

conservative scenario and/or due to the inadequacy of the supervisory bodies charged with

its design and implementation. This cannot be ruled out, given the sharp critiques that have

accompanied the 2010 stress tests, the constraints met by EBA in terms of IT and human

resources, and the fact that some national supervisors were sometimes seen as only half-

heartedly committed to the data gathering and validation process. We name this the

irrelevance hypothesis: when a round of stress tests is announced and/or its results are

released to the public, no price impact can be observed over the relevant event window.

Alternatively, stress tests could trigger a market response. Investors could e.g. appreciate

the increased transparency brought about by the tests and let prices react as opaqueness is

reduced19. If that occurs, then equity returns should be higher for banks which emerge as

relatively stronger from the test. We call this the

19 One might also argue that investors fear the dilution effect arising from the possible new rights issues

imposed upon under-capitalised banks. As well-capitalised banks can hardly be expected to shrink their capital basis, the aggregate effect would be an increase in the supply of bank stock and a decrease in

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 11 *

disclosure hypothesis: when a round of stress test is announced, implying the

dissemination of bank-by-bank results to investors, the tested banks’ stocks will rise in

anticipation of the benefits associated with lower opaqueness. When stress test results

are released, some banks will react more favourably than others, and the difference will

be explained by the stress test results

If the above is true, however, the market might be using two types of information to decide

what banks are stronger.

Investors may, in fact, distrust simulated figures (because the starting assumptions are seen

as too mild, heterogeneity across the banks’ internal models is perceived as too high, etc.)

and instead focus on the detailed historical data that come with the stress test results (e.g.,

the breakdown of sovereign exposures to peripheral euro-zone countries) to assess the

likely impact of their own downturn scenarios. This is what we call the

zoom hypothesis: the market reaction to stress test results is mainly driven by new

information concerning historical financial data, that is, by a “zoom” on the banks’

current financial statements which provides investors with further details, previously

undisclosed to the public.

Alternatively, the price reaction might be mostly driven by simulated results if such

forecasts, although possibly affected by political constraints which prevent supervisors

from adopting overly pessimistic scenarios, are deemed technically sound and overall

credible (e.g., they might be underestimating the total impact of a downturn scenario, but

still point into the right direction and highlight individual strengths and weaknesses

looking at differences across banks). We name this is as the

stress hypothesis: the market reaction to stress test results is mainly driven by the

information concerning the individual banks’ resilience to the simulated downturn

scenario.

market prices. While such a process is likely to affect undercapitalised banks in the first place, all bank stocks (including not-tested ones) might become cheaper as investors underweight the banking industry in their portfolios, in view of the forthcoming equity offerings. When presenting our results, we refer to this as the dilution explanation.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 12 *

The practical relevance of distinguishing between the zoom and the stress hypothesis

should not be overlooked: if the former were correct and the latter were rejected, there

would be no sound justification to release simulation results to the market. Supervisory

resources should then be devoted to confidential stress test programs without wasting time

and efforts in cleaning, releasing, explaining simulated data. Enhanced data flows on the

banks’ current financial situation (possibly published under Pillar 3 in the Basel Accord)

would be the best way to address opacity; while downturn scenarios and their expected

effects would only be shared by bankers and their supervisors.

5 Sample and methodology

5.1 Sample

We start by looking at all banks included in the Thomson Reuters European Banks index

(g#LBANKSER) which is composed by a set of stocks covering at least 75% of the total

market capitalization of the European banking industry20. This index includes 201 banks,

51 of which participate in the stress test exercise and 150 do not. We use 45 institutions

that are included in the index and incorporated in countries considered in the stress test

exercise, but do not participate in it, as our control sample21 (“non tested banks”).

We then complete our sample of “stressed banks” by including three listed institutions that

took part in the 2011 exercise but were not included in the Thomson Reuters European

Banks index22. This brings the number of stressed banks to 54 (out of 90 banks

20 Agri.Bank Of Greece, Alpha Bank, Banca Monte Dei Paschi, Banco Bpi, Banco Comercial Portugues,

Banco De Sabadell, Banco Espirito Santo, Banco Pastor, Banco Popolare, Banco Popular Espanol, Banco Santander, Bank Of Cyprus, Bank Of Ireland, Bank Of Piraeus, Bank Of Valletta, Bankinter, Barclays, BBVA, Bnp Paribas, Caixabank, Caja De Ahorros Del Mediterraneo, Commerzbank, Credit Agricole, Danske Bank, Deutsche Bank, Dexia, DNB Nor, Efg Eurobank Ergasias, Erste Group Bank, Hsbc Hdg, Intesa Sanpaolo, Jyske Bank, Kbc Group, Landesbank Bl.Hldg., Lloyds Banking Group, Marfin Popular Bank, National Bk.Of Greece, Nordea Bank, Otp Bank, Pko Bank, Pohjola Pankki A, Raiffeisen Bank Intl., Royal Bank Of Sctl.Gp., Seb 'A', Societe Generale, Svenska Handbkn.'A', Swedbank 'A', Sydbank, Tt Hellenic Postbank, Ubi Banca, Unicredit..

21 Attica Bank, Banca Carige, Banca Finnat, Banca Popolare Di Milano, Banca Popolare Etruria, Banca Popolare di Sondrio, Banca Popolare dell’Emilia Romagna, Banco De Valencia, Banco Espanol De Credito, Banif-Sgps, Bank Bph, Bank Coop, Bank Millennium, Bank of Greece, Bank Zachodni Wbk, Banque Nale.De Belgique, Bgz, Banco di Desio, BRE Bank, CIC, Crcam Brie Pic2Cci, Crcam Nord De France Cci, Credit Agr. Ile De France, Credito Artigiano, Credito Bergamasco, Credito Emiliano, Credito Valtellinese, Deutsche Postbank, General Bank Of Greece, Getin Holding, Getinoble Bank, Handlowy, Ikb Deutsche Indstrbk., Ing Bank Slaski Bsk, KBC Ancora, Kredyt Bank, Mediobanca, Natixis, Oldenburgische Lb., Pekao, Spar Nord Bank, Sparebank 1 Smn, Sparebank 1 Sr Bank, Standard Chartered, Van Lanschot.

22 Allied Irish Banks, Banca Civica and Bankia.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 13 *

participating in the stress test, the other 36 being unlisted). When investigating the link

between market reactions and stress test results, we may have to drop a few banks from the

sample if their published results do not include the variables that we wish to test (e.g.,

some banks did not release detailed data on new provisions by portfolio type) or if the

closing price does not change for five consecutive trading days.

5.2 Methodology

Our tests will be based on standard event study techniques (Campbell, Lo, and MacKinlay

1997); the abnormal return ARjt for bank i at time t will therefore be defined as the

difference between the actual stockmarket return Rjt and a measure of “normal” return

(NRjt) generated by a market model. As concerns the latter, two alternative specification

will be tested:

a one-factor model based on country-specific stock-market indices23, rather than on

just one pan-European index for all banks; this is motivated by the fact that in 2011

sovereign risk represented a major driver behind price movements for European

stocks. Hence, if our market model did not properly account for country-specific

effects, large abnormal returns would emerge, due to national dynamics rather than

to bank-related factors. By using national stock-market indices, instead, one can be

confident that residuals will only include idiosyncratic effects.

a two-factor model including both national stockmarket indices (as above) and an

industry-specific index (the Morgan Stanley Capital International – MSCI Europe

Banks); while this might not be appropriate when one’s goal is to highlight market

reactions which affect all banking institutions, controlling for industry-wide effects

could be helpful when we want to highlight differences across individual banks

(e.g., to see if the price impact was somehow correlated with each bank’s capital

gap).

23 These are the DAX 30 (Germany), Belgium 20 (Belgium), Bulgaria SE SOFIX (Bulgaria), Cyprus General

(Cyprus), Prague SE (Czech Republic), OMX Copenhagen (Denmark), IBEX 35 (Spain), OMX Helsinki (Finland), SBF 120 (France), Athex Composite (Greece), Budapest BUX (Hungary), Ireland SE ISEQ (Ireland), FTSE Italia All Share (Italy), Malta SE MSE (Malta), AEX (Netherlands), OSLO SE OBX (Norway), Wiener Borse (Austria), Warsaw General Index 20 (Poland), Portugal PSI 20 (Portugal), Romania BET (Romania), Russian MICEX (Russian Federation), SBI 20 (Slovenia), OMX General (Sweden), Swiss Market (Switzerland), Istanbul SE 100 (Turkey), FTSE All Share (UK).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 14 *

Both models are estimated on a 200-day window ranging from t*-210 to t*-11, where t* is

the event date to be tested (e.g., the “release date” or the “first announcement date”, see

§3.2 for details). Although the length of this estimation window is to some extent arbitrary,

our choice appears consistent with previous research24.

Once “normal returns” are estimated, we look at CARs (cumulative abnormal returns) over

the event window, that is, the window where each event can reasonably be expected to

have affected market prices.

We use a 5-day event window (-2,+2) including 2 days before the event and 2 days

thereafter. It looks general enough to be applied across all announcements without

tampering with individual dates, as it incorporates both the risk of a news leak before the

formal announcement and the possibility that investors have reacted slowly, over a few

days, as the concrete details and technical implications of the news were properly digested.

We will run our multivariate analysis on post-event days only, using a (0,+2) window

covering the announcement day25 and the following two trading days. A three-day event

window is consistent with the other empirical studies on the stress tests’ market impact,

both in the US and in Europe (Peristiani, Morgan, and Savino 2010; Cardinali and

Nordmark 2011). While those authors choose a (-1, +1) window, we do not include any

pre-announcement day. There are several reasons for that. First, univariate results (see

below, §6.2.1) rule out the risk a news leak in the days leading to the announcement (as

confirmed by a thorough inspection of press articles and news releases). Second, a (0, +2)

window, while possibly too long to capture market reactions in liquid, informed markets,

takes into account the vastness and complexity of the information that investors were

called to factor in, allowing enough time for equity analysts to update their models with the

new data and to issue new reports26 triggering price adjustments. Also, stopping at t*+2

eliminates the risk that our results be disturbed by subsequent news27.

24 (Weston, Mitchell, and Mulherin 2004) suggest an estimation window of 200 trading days; (Boehmer,

Broussard, and Kallunki 2002) indicate that such estimation window is used by most researchers; (MacKinlay 1997) suggests a 120-day window; (Thompson 1995) supports using 60 observations for monthly data and 250 observations for daily data.

25 As indicated in footnote , as the actual announcement took place on Friday at 6 p.m. (when markets were closed and no reaction could take place), we use the following Monday as announcement date. Hence our [0, +2] window consists of 18, 19 and 20 July.

26 According to I/B/E/S 52 recommendations on the European banks in our sample were issued by equity analysts between July 15 (average release time: 6:43 PM GMT) and July 20; two thirds of them concerned stress-tested institutions. While most analyses were published late on Friday 15, reports

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 15 *

5.3 Explanatory variables

To test the zoom hypothesis and the stress hypothesis we are going to regress CARs (on the

release date) on a set of indicators based on the stress test results. As the latter included

more than 3,000 data items, a clear selection strategy is needed in order to focus on the

most relevant regressors and avoid the risk of data mining.

Figure 2 outlines our approach. We start (on the left) with the capital adequacy ratio at end

2012 under the stressed scenario (“stressed core tier 1 ratio in 2012”). This summarises

most factors captured by the stress test exercise (initial capital ratio at end 2010,

profitability expectations, credit and market losses, etc.). Also, this indicator (which

focused on high quality capital, also known as “core tier 1” or CT1) was the one used by

EBA as a benchmark: a value below 6% was most likely to prompt a request for additional

capital; as such, it was most likely to trigger market reactions.

continued in the first days of the following week, with 13, 6 and 8 recommendations issued on Monday, Tuesday and Wednesday. This compares with 20 recommendations issued in the same period of 2010 (from Friday 16 to Wednesday 21 July 2010).

27 On day t*+3 (July 21) an additional €109bn bail-out plan was agreed by EU Leaders for Greece (Spiegel and Peel 2011), which had a strong positive impact on bank stock prices (Dennis 2011).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

Moving left to right in the figure, we decompose the stressed capital ratio into its two main

drivers: the initial capital ratio at end 2010 and the drop in capital adequacy caused by the

stress scenario.

The former indicator (“CT1 ratio in 2010”) may have no impact on market prices, as it

hardly represents a surprise for investors (information on own funds were already available

in the 2010 statements); however, not all items which would qualify as supervisory capital

under the current Basel 2 rules were deemed acceptable by EBA, as further filters and

deductions were imposed in order to ensure conservatism and cross-country consistency.

Although the criteria used to define “core Tier 1” had been released by EBA a few weeks

before the stress test results, their application to individual banks involved some

discretionary choices and the final result was still, to some extent, uncertain. In this sense,

the information on eligible capital might not have been fully anticipated by the market; this

Figure 2: Main variables to be tested

Stressed CT1 ratio in 2012

CT1 ratio in 2010

CT1 ratio in 2011-2(stressed)

Net Incomein 2011-2(stressed)

Risk Weighted

Assets in 2011-2

(stressed)

Operating income in

2011-2 (stressed)

Writedowns/ writeoffsin 2011-2 (stressed)

Sovereign Exposures to PIIGS in 2010

Trading income in

2011-2 (stressed)

Net Interest Margin in

2011-2 (stressed)

Funding Costs

in 2011-2 (stressed)

Coverage of defaulted

exposures at end 2012

Stressed_CT1

DCT1_stress

CT1_2010

DNetInc_stress

DRWA_stress

DExpCover

DOpInc_stress

D_FC_stress

DNII_stress

DTI_stress

PIIGS_loss_CT1

DefExpCover

Mod

el

Ris

kL

iqu

idit

y R

isk

Pro

fita

bil

ity

and

Cap

ital

Ad

equ

acy

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 17 *

could be more true for smaller institutions, as less information on their capital items is

usually available and less analyses are provided on them on a continuous basis .

The second indicator (the change in CT1 capital caused by the stress scenario) could in

turn be decomposed into two factors: the net profits/losses in stressed 2011 and 2012

(affecting capital, i.e., the numerator of the capital ratio) and the change in risk-weighted

assets at end 2012 (the denominator) foreseen by the bank in the event of a stress. The

latter, although quite relevant in principle, might have played a limited role in the EBA

stress test since the simulation methodology required banks to assume that total assets

would remain unchanged over the whole forecast window28. Note however that, keeping

total assets unchanged, risk-weighted assets may still have increased following a shift in

the risk-weights (e.g., due to massive downgrades of the borrowers)

As shown in the figure, net profits/losses may be due to operational profits29 (“ Operating

Income in 2011-2 (stressed)”) and/or to extraordinary credit losses and provisions against

credit risk (“Writedowns/writeoffs in 2011-2 (stressed)”). The former are mainly driven by

net interest margin and trading income. Under the simulation scheme designed by EBA,

interest-based income was strongly affected by the possible increase in the bank’s funding

costs. The idea was that the upward shift in market rates associated with the stressed

scenario would immediately translate into higher wholesale funding costs for the banks,

while retail deposits would remain partly unaffected; hence institutions relying heavily on

interbank facilities would suffer from a sharper increase in the average cost of funds. Thus,

the change in funding costs associated with the stress scenario (“ Funding Costs in 2011-

2 (stressed)”) can also be seen as an indirect measure of liquidity risk30 and hence may

even prove more significant than net interest income as a whole.

Although the EBA and the national supervisors paid considerable attention to the way that

individual banks estimated credit losses and write-downs, one area where the stress test

28 This was meant to prevent banks from stating that they would achieve capital adequacy through

deleveraging (asset cuts) rather than through new capital. 29 As argued by (Onado 2011), when stress test results were released stock prices may have reacted more to

the announcement of a structural drop in the profitability of the traditional banking business (namely, a decrease in net interest margin triggered by higher funding costs) than to the risk of significant one-off losses due to extraordinary events (like sovereign defaults, turmoil in equity and currency markets, etc.).

30 Information on liquidity risk was collected by EBA during the 2011 stress test, but no results were disclosed to the public. Hence “ Funding Costs in 2011-2” was one of the few proxies for liquidity risks (possibly the only one) provided to investors. Also, unlike other liquidity indicators (e.g., the ratio of liquid assets to short term claims) which might quickly become obsolete as banks continuously recalibrate their portfolios, this is structural in nature, so it conveys a more stable type of information.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 18 *

may not have been adequately conservative is sovereign risk. As it clearly would be

politically unacceptable, for the European bank supervisor, to assume that one or more EU

countries could default, the simulation scheme only required that a set of fixed loss rates be

applied to bonds issued by euro-zone peripheral countries. This approach was seen as too

mild by most analysts and financial columnists31. However, as pointed out by EBA itself,

the stress test results offered an unprecedented degree of detail on sovereign bonds held by

individual banks (including gross and net positions broken down by country and duration

bands); hence, any investor could carry out her own simulations based on more

conservative assumptions. To see if that really occurred, we will include in our list of

relevant variables one or more indicators based on the banks’ exposure to PIIGS (at end

2010); the main one will be a rough estimate of the possible losses (equal to 25% of the

booked amount) on net exposures towards PIIGS countries, scaled by core Tier 1 capital at

end 2010. Setting a uniform loss rate across all PIIGS countries32 ensures that this variable

can also be used as an indicator of PIIGS debt holdings (as losses and holdings differ by a

constant).

The last indicator to be tested is the coverage ratio on defaulted exposures at end 2012. The

idea is that, for any amount of defaulted exposures, a bank is safer if a large share of them

has already been written-down and/or covered with provisions; hence, all other things

being equal, a higher coverage ratio on defaulted exposures makes capital adequacy data

more credible and easier to sustain. Note that, just like the increase in funding costs could

be seen as a proxy for liquidity risk, the coverage ratio provides some (indirect)

information on model risk (loosely speaking, the risk that the internal models used by

individual banks prove overly optimistic when simulating stressed results). A low coverage

means a stronger risk of extra losses if recovery rates turn out to be worse than expected;

conversely, a coverage ratio close to 100% suggests that very low recoveries have already

been factored in, hence there is limited scope for bad surprises.

31 See e.g.(Jenkins 2011; The Economist). Notably, just a few weeks after the stress tests results were

released even the IMF claimed that bank capital in Europe had to be raised significantly above the thresholds used as a safety level in the test (Financial Times 2011).

32 It may be argued that applying a flat 25% loss rate across all five PIIGS countries (and a 0% loss rate to the remaining ones) may over-simplify the market’s view of sovereign credit risk. We will therefore also test an alternative ratio, where possible losses are estimated by applying the haircuts set by EBA not only to the trading book (as was required in the 2011 stress test) but instead to the banks’ overall net exposures to each country (both PIIGS and non-PIIGS).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 19 *

Table 2: Main explanatory variables

Variable Legend

Stressed_CT1 Core Tier 1 ratio at end 2012 in the downturn scenario

CT1_2010 Core Tier 1 ratio at end 2010, including mitigating measures up to April 30 2011

DCT1_stress Decrease in Core Tier 1 moving from 2010 to 2012 (stressed)

DNetInc_stress Decrease in 2012 net income moving from baseline to stressed, scaled by 2010 total assets

DRWA_stress Increase in risk-weighted assets moving from 2010 to stressed 2012

DOpInc_stress Decrease in 2012 operating income moving from baseline to stressed, scaled by 2010 total assets

DNII_stress Decrease in 2012 net interest margin moving from baseline to stressed, scaled by 2010 total assets

DTI_stress Decrease in 2012 trading income moving from baseline to stressed, scaled by 2010 total assets

Delta_FC_stress Increase in the cost of funding (in basis points) moving from 2010 to stressed 2012

DExpCover Increase in coverage ratio for credit exposures (due to write-downs and provisions) moving from 2010 to stressed 2012

PIIGS_loss_CT1 Estimated loss on sovereign bonds issued by PIIGS (set to 25% of current value) over Core Tier 1 at end 2010

DefExpCover Coverage ratio for defaulted exposures in stressed 2012

The black boxes in Figure 2 show the names of the main variables to be tested in the

following pages; the same labels are shown in Table 2, where further clarifications are

provided. These variables will be complemented by other indicators when necessary, to

check robustness and/or to test further assumptions.

6 Results

6.1 Non-release dates

We compute cumulative abnormal returns around non-release dates and compare the

reactions of tested and “non tested” banks. Also, to check whether the market anticipated

what banks would be deemed weaker by the stress test, we rank tested banks by

Stressed_CT1 (the Core Tier 1 ratio at end 2012 in the downturn scenario, a piece of

information that would become available only upon disclosure of the stress test results) and

compute average CARs for the bottom 20% and the top 20% banks; we then test whether

the difference between the two is statistically different from zero.

Table 3 summarises our results for the various dates listed in Figure 1. For each

announcement we provide CARs over the (-2,+2) window, as well as a breakdown between

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 20 *

pre-event and post-event days. To check for robustness, abnormal returns estimated with

two different market models are shown.

Most announcements had an impact on stock market prices.

The first announcement (with the commitment to publicly disclose the results) had a

positive impact on the prices of tested banks33. However, the market seems not to have

been able to anticipate what banks were worse equipped to withstand a stressed scenario,

although highly capitalised banks (those for which an increase in transparency would be

most beneficial) experience a positive abnormal return in the post-event window.

On the detailed announcement date, EBA made reference to “remedial backstop measures”

to be put in place for weaker institutions. This might have increased the perception of a

dilution risk, in case new rights issues were pushed through by supervisors at heavily

discounted prices. While non-tested banks did not react, tested ones showed an average

negative CAR of 2%. Again, no special pattern can be observed regarding the difference

between “top” and “bottom” banks.

When the actual stress test methodology was shared with the market, tested banks

experienced a negative return again, while no reaction occurred in the control sample.

Additionally, while stronger banks did not react, weaker banks displayed negative and

statistically significant abnormal returns. This could be due to the fact that the 2011

methodology was both more conservative and more detailed than the one used one year

before, so it would be more difficult for vulnerable banks to hide their weaknesses34.

33 Although the list of participating banks was only released at a later stage, these were almost identical to

those enrolled in the 2010 exercise, so investors were in a position to make an educated guess. 34 Furthermore, upon release of the methodological note EBA clarified that only legally binding

recapitalisation plans signed before 30 April 2011 would be incorporated in the assessment; this reinforced the trend towards raising capital ahead of the end-April deadline and might have spurred further fears of dilution. During the following weeks many large banks (e.g., Commerzbank and Intesa Sanpaolo) announced capital increases for several tens of billions.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 21 *

Table 3: Market Reactions around the pre-release dates

One-Factor Model Two-Factor Model CAR (-2,2) CAR (-2,-1) CAR (0,2) CAR (-2,2) CAR (-2,-1) CAR (0,2) # obs Avg p-val Avg p-val Avg p-val Avg p-val Avg p-val Avg p-val

(a) First announcement date (January 13, 2011) Full Sample 96 0,02 0,00 0,01 0,00 0,01 0,01 0,01 0,01 0,00 0,14 0,01 0,03Non Tested Banks 45 0,01 0,16 0,00 0,23 0,00 0,37 0,00 0,41 0,00 0,65 0,00 0,41Tested Banks 51 0,03 0,00 0,02 0,00 0,01 0,01 0,01 0,01 0,01 0,12 0,01 0,03Bottom 20% by Stressed_CT1 9 0,03 0,08 0,03 0,02 0,00 0,96 0,03 0,08 0,03 0,03 0,00 0,94Top 20% by Stressed_CT1 9 0,01 0,24 -0,01 0,39 0,01 0,00 -0,01 0,18 -0,02 0,00 0,01 0,06Bottom - Top . 0,02 0,31 0,03 0,01 -0,02 0,29 0,04 0,03 0,05 0,00 -0,01 0,48

(b) Detailed announcement date (March 2, 2011) Full Sample 103 -0,01 0,00 -0,01 0,00 -0,01 0,00 -0,01 0,16 0,00 0,61 0,00 0,17Non Tested Banks 51 0,00 0,59 0,00 0,73 0,00 0,39 0,00 0,39 0,00 0,17 0,00 0,93Tested Banks 52 -0,02 0,00 -0,01 0,00 -0,01 0,00 -0,01 0,01 -0,01 0,08 -0,01 0,04Bottom 20% by Stressed_CT1 9 -0,02 0,11 -0,01 0,07 -0,01 0,34 -0,02 0,17 -0,01 0,09 -0,01 0,39Top 20% by Stressed_CT1 10 -0,02 0,00 -0,01 0,05 -0,01 0,05 -0,01 0,03 0,00 0,52 -0,01 0,15Bottom - Top . 0,00 0,40 0,00 0,49 0,00 0,65 -0,01 0,88 -0,01 0,45 0,00 0,89

(c ) Methodology date (March 18, 2011)

Full Sample 99 -0,01 0,00 -0,01 0,01 0,00 0,08 -0,01 0,05 0,00 0,24 0,00 0,16Non Tested Banks 47 0,00 0,87 0,00 0,76 0,00 0,95 0,00 0,82 0,00 0,94 0,00 0,84Tested Banks 52 -0,02 0,00 -0,01 0,00 -0,01 0,00 -0,01 0,01 -0,01 0,13 -0,01 0,02Bottom 20% by Stressed_CT1 9 -0,02 0,04 -0,01 0,08 -0,01 0,27 -0,02 0,04 -0,01 0,08 -0,01 0,21Top 20% by Stressed_CT1 10 0,00 0,85 0,00 0,93 0,00 0,90 0,01 0,42 0,00 0,52 0,00 0,88Bottom - Top . -0,02 0,12 -0,01 0,27 -0,01 0,49 -0,02 0,04 -0,01 0,13 -0,01 0,43

(d) Capital definition date (April 8, 2011)

Full Sample 96 0,01 0,00 0,01 0,00 0,00 0,17 0,01 0,00 0,01 0,00 0,00 0,03Non Tested Banks 45 0,00 0,40 0,00 0,08 0,00 0,66 0,00 0,59 0,00 0,29 0,00 0,88Tested Banks 51 0,02 0,00 0,02 0,00 0,00 0,04 0,01 0,00 0,01 0,00 0,01 0,01Bottom 20% by Stressed_CT1 9 -0,01 0,61 0,01 0,25 -0,01 0,39 -0,01 0,64 0,01 0,28 -0,01 0,39Top 20% by Stressed_CT1 9 0,04 0,00 0,02 0,01 0,02 0,00 0,03 0,00 0,01 0,03 0,02 0,00Bottom - Top . -0,04 0,08 -0,01 0,72 -0,03 0,01 -0,04 0,12 0,00 0,82 -0,04 0,00

(e) Clarification date June 9, 2011)

Full Sample 92 -0,01 0,00 -0,01 0,00 0,00 0,12 -0,01 0,00 -0,01 0,00 0,00 0,17Non Tested Banks 45 -0,01 0,01 -0,01 0,01 0,00 0,59 -0,01 0,01 -0,01 0,01 0,00 0,56Tested Banks 47 -0,01 0,01 0,00 0,06 -0,01 0,06 -0,01 0,05 0,00 0,19 -0,01 0,12Bottom 20% by Stressed_CT1 8 -0,02 0,12 -0,01 0,07 0,00 0,88 -0,02 0,12 -0,01 0,07 0,00 0,81Top 20% by Stressed_CT1 9 -0,02 0,02 -0,01 0,09 -0,01 0,01 -0,01 0,02 -0,01 0,12 -0,01 0,01Bottom - Top . 0,00 0,75 -0,01 0,46 0,01 0,19 0,00 0,79 -0,01 0,53 0,01 0,23

This table reports the number of observations and the average cumulative abnormal returns (CARs) estimated over the event windows (-3,3), (-3,1) and (0,3) centered on pre-release dates, with a one-factor model as well as a two-factor model for the full sample, non tested banks, tested banks, bottom 20% banks and top 20% banks based on the variables defined in Table 2. This table also reports the p-value of the t test of the null hypothesis that the average standardized CAR (i.e., the CAR divided by the standard deviation of the estimation period adjusted for the length of the event window) is zero and the difference between average standardized CARs of bottom and top 20% banks is zero.

On April 8 the EBA clarified that the definition of capital to be used in the stress test

exercise would be more conservative than the one currently adopted under the Basel 2

agreement, and would somehow anticipate the additional constraints and limitations

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 22 *

brought about by the Basel 3 framework. This announcement had a positive impact on the

sample of tested banks as a whole and this effect was stronger for the most capitalised ones

(“Top 20% by Stressed_CT1”) in the post-event window. This evidence might be due to

the fact that more resilient banks would benefit from receiving a supervisory “certification”

based on higher capital-quality standards (hence closer to the perspective of equity analysts

and rating agencies).

The market reaction on the clarification date is negative and statistically significant for

both tested and untested banks. This suggests that other events may have occurred, which

do not relate to the stress test exercise. Indeed, in the first week of June the worsening of

the sovereign crisis took toll on bank stock throughout the continent, with Italian, Greek

and French bank shares being especially hit by sales.

To sum up, early announcements regarding the stress test exercise seem to have

significantly affected tested banks, while banks in the control sample did not react. A

positive impact came from the commitment to transparency, consistent with the disclosure

hypothesis; the asymmetric reaction of strongest and weakest banks on capital definition

date lends further support to this hypothesis. Lastly, the risk of remedial measures and the

imposition of a stricter, more detailed methodology seem to have affected prices

negatively.

6.2 The release date

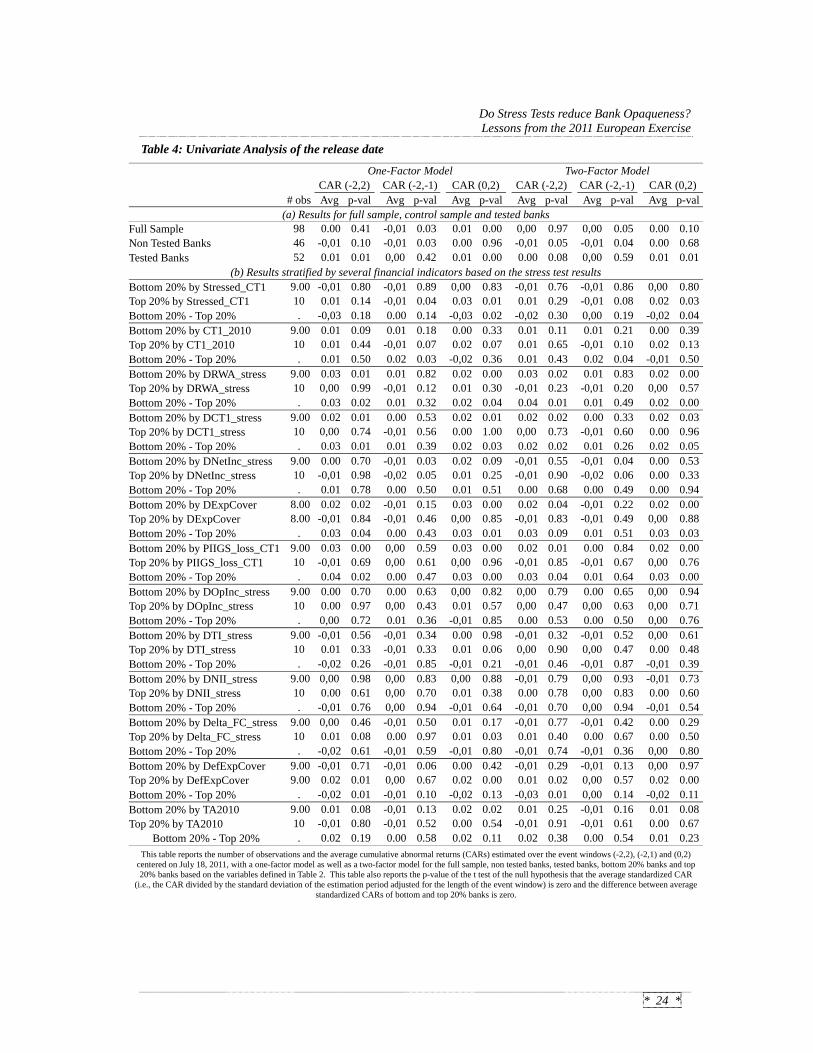

6.2.1 Univariate analysis

Table 4 provides detailed univariate tests on the release date. The layout is similar to Table

3, except that we do not rank banks only by Stressed_CT1, but instead use all the variables

in Table 2, since full details for all key indicators were known to the market at that time.

Tested banks show a positive reaction over the (-2, +2) window; this effect, however, is

statistically significant only in the post-event period (0,+2). The opposite is true for non-

tested banks: they experience weakly negative abnormal returns throughout the whole

event window, but price movements are significant only in the pre-event period.

Accordingly, tested banks are the only ones to experience a positive and statistically

significant reaction in the post-event period, most likely because of the results released by

EBA.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 23 *

This interpretation of the evidence is corroborated by the fact that, in the pre-event period,

almost no significant difference can be found between “top” and “bottom” tested banks

ranked according to several financial indicators35.

In the post-event period, instead, abnormal returns36 reward institutions which, under the

stressed scenario, manage to preserve a higher amount of Core Tier 1 capital

(Stressed_CT1), experience a lower drop in capital adequacy (DCT1_stress) and show a

less sharp increase in risk-weighted assets, write-downs and provisions (DRWA_stress,

DExpCov). Also, returns are better for banks less exposed to PIIGS sovereign debt

(PIIGS_loss_CT1).

Other determinants of net income (DOpInc_stress, DTI_stress, DNII_stress) prove less

significant; the same happens with the amount of eligible capital at end 2010 (CT1_2010)

and with variables which could indirectly capture some form of liquidity risk and model

risk (Delta_FC_stress, DefExpCover). It could well be that, while these relatively more

sophisticated indicators are not strong enough to explain CARs on a univariate basis, they

prove relevant when considered within a multivariate framework; further tests on this will

be produced in the next Section.

35 When one looks at the p-values for inter-quintile differences, only one out of 13 indicators falls below the

5% threshold (the Core Tier 1 ratio at end 2010). In this case, however, none of the two subgroups (Bottom and Top 20%) shows CARs that are different from zero at 5%. Accordingly, as mentioned in §5.2, in the next Section our multivariate analysis will focus on the post-event window only.

36 Results are robust to the market model used to generate abnormal returns (single-factor vs. two-factor model); further robustness checks across models will be produced in the multivariate analysis (§7).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 24 *

Table 4: Univariate Analysis of the release date

One-Factor Model Two-Factor Model CAR (-2,2) CAR (-2,-1) CAR (0,2) CAR (-2,2) CAR (-2,-1) CAR (0,2) # obs Avg p-val Avg p-val Avg p-val Avg p-val Avg p-val Avg p-val

(a) Results for full sample, control sample and tested banks Full Sample 98 0.00 0.41 -0,01 0.03 0.01 0.00 0,00 0.97 0,00 0.05 0.00 0.10Non Tested Banks 46 -0,01 0.10 -0,01 0.03 0.00 0.96 -0,01 0.05 -0,01 0.04 0.00 0.68Tested Banks 52 0.01 0.01 0,00 0.42 0.01 0.00 0.00 0.08 0,00 0.59 0.01 0.01

(b) Results stratified by several financial indicators based on the stress test results Bottom 20% by Stressed_CT1 9.00 -0,01 0.80 -0,01 0.89 0,00 0.83 -0,01 0.76 -0,01 0.86 0,00 0.80Top 20% by Stressed_CT1 10 0.01 0.14 -0,01 0.04 0.03 0.01 0.01 0.29 -0,01 0.08 0.02 0.03Bottom 20% - Top 20% . -0,03 0.18 0.00 0.14 -0,03 0.02 -0,02 0.30 0,00 0.19 -0,02 0.04Bottom 20% by CT1_2010 9.00 0.01 0.09 0.01 0.18 0.00 0.33 0.01 0.11 0.01 0.21 0.00 0.39Top 20% by CT1_2010 10 0.01 0.44 -0,01 0.07 0.02 0.07 0.01 0.65 -0,01 0.10 0.02 0.13Bottom 20% - Top 20% . 0.01 0.50 0.02 0.03 -0,02 0.36 0.01 0.43 0.02 0.04 -0,01 0.50Bottom 20% by DRWA_stress 9.00 0.03 0.01 0.01 0.82 0.02 0.00 0.03 0.02 0.01 0.83 0.02 0.00Top 20% by DRWA_stress 10 0,00 0.99 -0,01 0.12 0.01 0.30 -0,01 0.23 -0,01 0.20 0,00 0.57Bottom 20% - Top 20% . 0.03 0.02 0.01 0.32 0.02 0.04 0.04 0.01 0.01 0.49 0.02 0.00Bottom 20% by DCT1_stress 9.00 0.02 0.01 0.00 0.53 0.02 0.01 0.02 0.02 0.00 0.33 0.02 0.03Top 20% by DCT1_stress 10 0,00 0.74 -0,01 0.56 0.00 1.00 0,00 0.73 -0,01 0.60 0.00 0.96Bottom 20% - Top 20% . 0.03 0.01 0.01 0.39 0.02 0.03 0.02 0.02 0.01 0.26 0.02 0.05Bottom 20% by DNetInc_stress 9.00 0.00 0.70 -0,01 0.03 0.02 0.09 -0,01 0.55 -0,01 0.04 0.00 0.53Top 20% by DNetInc_stress 10 -0,01 0.98 -0,02 0.05 0.01 0.25 -0,01 0.90 -0,02 0.06 0.00 0.33Bottom 20% - Top 20% . 0.01 0.78 0.00 0.50 0.01 0.51 0.00 0.68 0.00 0.49 0.00 0.94Bottom 20% by DExpCover 8.00 0.02 0.02 -0,01 0.15 0.03 0.00 0.02 0.04 -0,01 0.22 0.02 0.00Top 20% by DExpCover 8.00 -0,01 0.84 -0,01 0.46 0,00 0.85 -0,01 0.83 -0,01 0.49 0,00 0.88Bottom 20% - Top 20% . 0.03 0.04 0.00 0.43 0.03 0.01 0.03 0.09 0.01 0.51 0.03 0.03Bottom 20% by PIIGS_loss_CT1 9.00 0.03 0.00 0,00 0.59 0.03 0.00 0.02 0.01 0.00 0.84 0.02 0.00Top 20% by PIIGS_loss_CT1 10 -0,01 0.69 0,00 0.61 0,00 0.96 -0,01 0.85 -0,01 0.67 0,00 0.76Bottom 20% - Top 20% . 0.04 0.02 0.00 0.47 0.03 0.00 0.03 0.04 0.01 0.64 0.03 0.00Bottom 20% by DOpInc_stress 9.00 0.00 0.70 0.00 0.63 0,00 0.82 0,00 0.79 0.00 0.65 0,00 0.94Top 20% by DOpInc_stress 10 0.00 0.97 0,00 0.43 0.01 0.57 0,00 0.47 0,00 0.63 0,00 0.71Bottom 20% - Top 20% . 0,00 0.72 0.01 0.36 -0,01 0.85 0.00 0.53 0.00 0.50 0,00 0.76Bottom 20% by DTI_stress 9.00 -0,01 0.56 -0,01 0.34 0.00 0.98 -0,01 0.32 -0,01 0.52 0,00 0.61Top 20% by DTI_stress 10 0.01 0.33 -0,01 0.33 0.01 0.06 0,00 0.90 0,00 0.47 0.00 0.48Bottom 20% - Top 20% . -0,02 0.26 -0,01 0.85 -0,01 0.21 -0,01 0.46 -0,01 0.87 -0,01 0.39Bottom 20% by DNII_stress 9.00 0,00 0.98 0,00 0.83 0,00 0.88 -0,01 0.79 0,00 0.93 -0,01 0.73Top 20% by DNII_stress 10 0.00 0.61 0,00 0.70 0.01 0.38 0.00 0.78 0,00 0.83 0.00 0.60Bottom 20% - Top 20% . -0,01 0.76 0,00 0.94 -0,01 0.64 -0,01 0.70 0,00 0.94 -0,01 0.54Bottom 20% by Delta_FC_stress 9.00 0,00 0.46 -0,01 0.50 0.01 0.17 -0,01 0.77 -0,01 0.42 0.00 0.29Top 20% by Delta_FC_stress 10 0.01 0.08 0.00 0.97 0.01 0.03 0.01 0.40 0.00 0.67 0.00 0.50Bottom 20% - Top 20% . -0,02 0.61 -0,01 0.59 -0,01 0.80 -0,01 0.74 -0,01 0.36 0,00 0.80Bottom 20% by DefExpCover 9.00 -0,01 0.71 -0,01 0.06 0.00 0.42 -0,01 0.29 -0,01 0.13 0,00 0.97Top 20% by DefExpCover 9.00 0.02 0.01 0,00 0.67 0.02 0.00 0.01 0.02 0,00 0.57 0.02 0.00Bottom 20% - Top 20% . -0,02 0.01 -0,01 0.10 -0,02 0.13 -0,03 0.01 0,00 0.14 -0,02 0.11Bottom 20% by TA2010 9.00 0.01 0.08 -0,01 0.13 0.02 0.02 0.01 0.25 -0,01 0.16 0.01 0.08Top 20% by TA2010 10 -0,01 0.80 -0,01 0.52 0.00 0.54 -0,01 0.91 -0,01 0.61 0.00 0.67

Bottom 20% - Top 20% . 0.02 0.19 0.00 0.58 0.02 0.11 0.02 0.38 0.00 0.54 0.01 0.23This table reports the number of observations and the average cumulative abnormal returns (CARs) estimated over the event windows (-2,2), (-2,1) and (0,2)

centered on July 18, 2011, with a one-factor model as well as a two-factor model for the full sample, non tested banks, tested banks, bottom 20% banks and top 20% banks based on the variables defined in Table 2. This table also reports the p-value of the t test of the null hypothesis that the average standardized CAR

(i.e., the CAR divided by the standard deviation of the estimation period adjusted for the length of the event window) is zero and the difference between average standardized CARs of bottom and top 20% banks is zero.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 25 *

6.2.2 Multivariate analysis

Our multivariate testing strategy is straightforward: we look at Figure 2 and take all

variables located on the final “leaves” of the tree starting from the stressed 2012 CT1 ratio.

These are: CT1_2010, DRWA_stress, DexpCover, DNII_stress and DTI_stress. By

focusing on variables which are not embedded into each other, we ensure that

multicollinearity issues are kept under control (see the pairwise correlations in Table 537).

We also test three other variables which, as shown in §5.3, are likely to add further insight

to the model: PIIGS_loss_CT1 (to express market concerns that the EBA approach on

sovereign losses may not have been conservative enough), Delta_FC_stress (impact on

funding costs of the stressed scenario, to proxy liquidity risk) and DefExpCov (coverage

ratio on defaulted exposures, which captures the “robustness” of the simulated losses to

worse-than-anticipated loss rates, and hence provides an indication, albeit very partial,

about each bank’s model risk).

Table 5: Pairwise correlations among regressors

CET1 ratio 2010

DRWAstress

DExp Cover

PIIGS loss

CET1

DNIMstress

DTI stress

Delta_FC stress

DefExpCover

CT1_ratio_2010 1 1% 21% 3% 19% -21% 8% 3%

DRWA_stress 1% 1 -28% -22% -28% 36% 10% -20%

DExpCover 21% -28% 1 54% 28% -48% -18% 30%

PIIGS_loss_CET1 3% -22% 54% 1 -4% -21% -19% 14%

DNII_stress 19% -28% 28% -4% 1 -21% 34% 5%

DTI_stress -21% 36% -48% -21% -21% 1 -16% -21%

Delta_FC_stress 8% 10% -18% -19% 34% -16% 1 0%

DefExpCover 3% -20% 30% 14% 5% -21% 0% 1

We start by testing all these potentially-relevant variables, and then move to a more

parsimonious model by gradually removing those which are not statistically significant.

The first and last step of this procedure are shown in Table 6; as a dependent variable we

use CARs on the (0, 2) window based on both a single-factor and a two-factor market

model (see columns I-II and III-IV, respectively).

37 Variance Inflaction Factors (VIFs) for the variables in Table 6 range from 1.1 to 2.3.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 26 *

Table 6: Cross-Sectional Determinants of the Market Reaction to the Stress Test Results

One-factor model

(local index) Two-factor model

(local and banks index)

(I) (II) (III) (IV)

Intercept -0,01 -0,03 0,00 -0,02 0,60 0,07 0,82 0,35

CT1_2010 0,51 0,57 0,45 0,48 0,00 0,00 0,01 0,00

DRWA_stress -0,02 -0,06 -0,07 0,31 0,03 0,00

DExpCover -1,01 -0,89 -0,91 -0,83

0,00 0,00 0,00 0,00

PIIGS_loss_CT1 -0,01 -0,01

0,23 0,54

DNII_stress 0,66 0,93

0,75 0,70

DTI_stress -7,17 -6,17

0,11 0,24

Delta_FC_stress [ x 103 ] -0,12 -0,11 -0,14 -0,12 0,02 0,05 0,03 0,04

DefExpCover 0,07 0,07 0,06 0,06 0,01 0,01 0,03 0,02

F-test 8,14 13,03 5,28 8,26

Prob > F 0,00 0,00 0,00 0,00

Adj R^2 0,58 0,58 0,44 0,46

# of obs 43 43 43 43

This table reports the results of weighted least squares (WLS) regressions of cumulative abnormal returns (CARs) over the (0, 2) event window, where 0 is the first trading day following the disclosure of the stress test results (i.e., July 18, 2011). The weight is the

inverse of the square root of the market model residual variance. The table shows the value of the coefficient estimates along with the p-value of their t-statistic (in italics). See Table 2 for

the definition of the explanatory variables.

The main results38 in the table are the following:

the models explain about half of the cross-sectional variance in CARs;

as shown in columns I and III, all tested variables have the expected sign, except

DNII_stress (which, however, is not statistically significant). Namely, a positive

market reaction appears to be associated with a higher amount of eligible capital at

end 2010, a decrease in the risk weights used to compute RWAs, lower credit

losses, lower involvement in PIIGS countries, a smaller drop in trading income

38 Results based on slightly wider or narrower event windows confirm most findings shown in Table 6,

although the significance of CET1_RATIO_2010 and Delta_FC_stress may sometimes decrease.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 27 *

(and a smaller increase in funding costs) under the stressed scenario, a higher

coverage of defaulted exposures;

the significance of DRWA_stress is weak and depends on the model used to

generate abnormal returns; this is not overly surprising, given that the change in

risk-weighted assets was only driven by changes in risk weights (the simulation

recipe prevented banks from de-leveraging);

besides net interest income, two other variables are consistently dropped when

moving from the complete model to the compact one; while DTI_stress may lack

relevance simply because trading income data was affected by the way each bank

had allocated securities between the trading and the banking book,

PIIGS_loss_CT1 (estimated losses on PIIGS exposures scaled by core Tier 1

capital) deserves further investigation, as data on sovereign exposures is thought to

have been one of the most noteworthy portion of the stress test results (and proved

relevant also in our univariate analysis); in §7.1 we control for a number of

alternative specifications;

variables proxying for liquidity risk and model risk prove significant across both

market models, suggesting that this type of information was appreciated by

investors (and more disclosure on those profiles would probably prove useful to the

market).

The above results have clear implications for the “stress hypothesis” stated in §4: variables

based on simulated data appear to be highly significant in driving the market reaction to

stress test results. Hence, the simulation exercise coordinated by EBA, while being openly

criticised by many analysts and commentators, seems to have provided investors with

relevant information.

The relevance of CT1_2010 provides support for the “zoom hypothesis”; however, it is

striking that the most important example of “zoomed” financial data included in the results

(the breakdown of sovereign exposures towards peripheral euro-zone countries) is

somewhat overriden by other indicators when tested on a multivariate basis. This will be

further investigated in the next Section.

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 28 *

7 Further results and robustness checks

7.1 Sovereign risk and the zoom hypothesis39

As noted above, the lack of significance for PIIGS_loss_CET1 in Table 6 is somewhat

surprising. Details on sovereign debt holdings across countries and maturity bands were

considered highly informative by some equity analysts40, as they allowed to simulate the

impact of alternative stressed scenarios based on more severe assumptions. Indeed, EBA’s

chairman reportedly invited investors to “do the modelling themselves” based on such raw

data41. It is therefore important to verify whether such anecdotal evidence is confirmed by

abnormal price movements.

It could be that data on sovereign debt was in fact relevant, but PIIGS_loss_CT1 does not

capture the type of information actually used by investors . This could be due to a number

of reasons:

1. we are testing the wrong variable and a different specification would get different

results;

2. we are looking at data on sovereign debt holdings, but instead we should be

focusing on the unexpected component of such data, as only new information can

trigger price adjustments;

3. data on sovereign debt holdings partially duplicates information which is common

to other independent variables in Table 6, so one should look only at original

(orthogonal) information.

These possible explanations are now examined and tested in detail.

Different specifications - PIIGS_loss_CT1 might simply be a wrong way of capturing

sovereign risk, so different ratios could get better results. To address this concern we

experimented with a number of alternative variables. We first changed the numerator,

estimating possible losses on sovereign securities by multiplying the banks’ overall net

exposures (trading and banking book) to each country by the haircuts set by EBA for the

trading book (instead of applying a flat 25% loss rate to PIIGS countries and a 0% loss rate

the other ones). We then changed the denominator and used total assets as a scale variable,

39 This paragraph reports results for CARs generated through the two-factor market model. Results for the

single factor-based CARs are qualitative similar and available upon request. 40 See e.g. the reports by Goldman Sachs and Barclays quoted in (Onado 2011). 41 (Jenkins 2011).

Do Stress Tests reduce Bank Opaqueness? Lessons from the 2011 European Exercise

* 29 *

since using CT1 might duplicate information which already enters the model through

CT1_2010. Finally, we applied both changes jointly. Regression outcomes (available from

the authors) were similar to those shown in Table 6; hence our results appear robust across

alternative specifications for PIIGS-related losses42.

Unexpected information - Only new information reaching the market can cause abnormal

price adjustments, but sovereign debt holdings are not, per se, an unexpected piece of

news. Everybody expects Greek banks to hold a lot of Athens’ Treasury bonds, just like

OATs are most likely to be found in a French bank’s portfolio. What might matter more, in

our case, is whether an individual bank is holding an amount of PIIGS debt above or below

the average national level. To extract such unexpected component, we regress

PIIGS_loss_CT143 on a set of country dummies (see Table 7) and save the residuals

(measuring the gap between each institution and the country-specific mean) into a new

variable called Unexp_PLO (unexpected PIIGS-related losses).

Table 7: Estimation of unexpected losses on PIIGS exposures

Independent Variables:

AT BE CY DE DK ES FI FR GB GR HU IE IT MT NO PL PT SE

Coefficient 0,03 0,29 0,41 0,13 0,01 0,47 0,00 0,13 0,03 0,83 0,00 0,10 0,63 0,02 0,00 0,00 0,47 0,01

p-value 0,88 0,10 0,10 0,37 0,93 0,00 0,99 0,36 0,81 0,00 1,00 0,68 0,00 0,93 1,00 1,00 0,00 0,96

F-test 8,20