bsi afs 2009.pdf - sharedata steel_ar_mar09.doc · web viewbsi steel limited group of companies...

TRANSCRIPT

LIMITED

ANNUAL REPORT 2009

2

ProfileBSi Steel Limited group of companies (“BSi Steel” or “BSi” or “BSI” OR “the Company” or “the Group”), operates in the steel and

associated industries with strategically located operations in South Africa, the Democratic Republic of Congo (DRC), Zimbabwe

and Zambia servicing the southern African markets.

The operations are grouped into four distinct activities:-

Processing: providing a primary processing service to the BSi operational businesses;

Stockists: providing a just in time (JIT) service to localized clients;

Bulk Sales: bulk sales to larger end users; and

Exports

The South African and Zimbabwean operations focus on the manufacturing and construction industries, whilst the Zambian and

DRC are largely focused towards mining.

The main products that the group sells are:-

Flat products (hot rolled, cold rolled, galvanized and plate);

Long products (light, medium and heavy mill sections, tubing) and

Structural steel sections

2

ContentsPAGE

Administration 4

Financial Highlights 5

Directorate 6

Chairman’s Report 8

Chief Executive Officer’s Report 11

Human Capital Sustainability Report 14

Corporate Governance Report 17

Remuneration Report 22

Directors Responsibility and Approval Statement 26

Secretarial Certification 26

Independent Auditors Report 27

Directors’ Report 28

Balance Sheets 30

Income Statements 31

Statements of Changes in Equity 32

Cash Flow Statements 34

Notes to the Annual Financial Statements 35

Shareholders Analysis 82

Notice of Annual General Meeting 83

Form of Proxy 87

2

Administration

Company Secretary and registered officeS Hackett, B.Com.

46 Eden Park Drive, Murrayfield ParkMkondeni, Pietermaritzburg, 3201PO Box 101096, Scottsville, 3209

Telephone: (033) 846 2208Facsimile: (033) 346 0870

Transfer SecretariesComputershare Investor Services (Pty) Limited

(Registration number 2004/003647/07)Ground Floor, 70 Marshall Street

Johannesburg, 2001PO Box 61051, Marshalltown, 2107

Telephone: (011) 370 5000Facsimile: (011) 688 5210

Designated AdviserVunani Corporate Finance

Trading as a division of Vunani Capital (Proprietary) Limited (Registration number 1998/001469/07)

Vunani House Block CAthol Ridge Office Park, 151 Katherine Street

Sandown, Sandton, 2196PO Box 652419, Benmore, 2010

Telephone: (011) 263 9500Facsimile: (011) 784 1989

AttorneysVenn Nemeth & Hart Inc.

(Registration number 1994/003593/21)281 Pietermaritzburg Street,

Pietermaritzburg, 3201PO Box 600, Pietermaritzburg, 3200

Telephone: (033) 355 3100Facsimile: (033) 394 1947

Auditors and reporting accountantsDeloitte and Touche

(Practice Number 901482)81 Hoosen Haffejee Street,

Pietermaritzburg, 3201PO Box 365, Pietermaritzburg, 3200

Telephone: (033) 345 0271Facsimile: (033) 345 0285

Commercial BankerNedbank Limited

(Registration number 1951/000009/06)90 Braam Fischer Road, Durban, 4001PO Box 10267, Marine Parade, 4000

Telephone: (031) 364 1111Facsimile: (031) 364 2479

2

Financial Highlights

EBITDA

0.1%

REVENUE

29.7%

EARNINGS PER SHARE

7.1%

HEADLINE EARNINGS PER SHARE

6.2%

The group’s revenue has grown from R1 432 million in 2008 to R1 857 million in 2009

2

DirectorateWilliam Battershill – Executive Director: Group Chairman (48)

William left school aged 17 and commenced his working career with his father, John Battershill, at his manufacturing and

agricultural supply company in Zimbabwe. He immigrated to RSA in 1981 and worked for Way Industries, a manufacturing

company in Qwa Qwa, where he was appointed as a Director at the age of 23. In May 1985, William resigned from Way Industries

and started Discount Steel. This was the founding company from which BSi was spawned. William’s strengths are his broad based

understanding of business and his ability to recognize and convert business opportunities.

Grant Mackenzie – (MBChB) Executive Director: Group CEO (44)

Grant started his working career at a subsidiary of Anglovaal in 1994, after a 5 year stint as a medical doctor (UCT 1989). In 1995

he moved to Lusaka, Zambia, where he was instrumental in starting Discount Steel Zambia in 1997. He returned to South Africa in

2006 as the Managing Director of the Exports Division, and continued to expand the exports operations into overland Africa. Grant

was appointed as the Chief Operating Officer of BSi in May 2007, Joint CEO in April 2008 and Group CEO in April 2009.

James Waller – (BCompt Hons) Executive Director: Group CFO (45)

James completed his articles with KPMG Inc. before moving into commerce. He worked as Financial Director of Positron, Purdon

Murdock and Waller, ATM (Pty) Limited and Terrafin Management Services (Pty) Limited. In 2001 he was appointed as Financial

Director at BSi. James comes with a wealth of experience gained in the industry and has been instrumental in managing the

group’s growth.

Ross Teichmann – Executive Director: BSi STEEL Gauteng (44)

Ross started a fencing business in Pietermaritzburg in 1987. In 1990 he joined McNaughtans where he ran the Empangeni branch

for 18 months and then moved back to Durban as the Sales Manager for the region. Ross joined Discount Steel in 1991 as a Sales

Representative and was responsible for the Durban region for 3 years. He relocated to Johannesburg in 1995 to start Garrison

Steel. Ross has been with BSi for the last 18 years and has contributed to the success of the steel business through his extensive

experience of the steel industry. Ross was appointed as the Executive Director of the SA based BSi Steel Stockists in April 2008.

Craig Parry – Executive Director: BSi STEEL Bulk Sales (40)

Craig commenced his working career at Nampak Limited as the Production Planner for laminated and coated products. Craig

joined Discount Steel in 1992 taking responsibility of the trading division of the group. He has now been with the group for 16 years

and has a wealth of experience in the steel industry. Craig was appointed as the Executive Director of BSi Steel Bulk Sales in April

2008.

Directorate (continued)

2

Nigel Payne – (B.Com (Hons), CA (SA), MBL) Independent Non-Executive Director (49)

Joined the board in 2007. Nigel is an experienced independent non-executive director who currently serves on the boards of a

number of other listed companies, namely the JSE Limited, the Bidvest Group Limited, the Mr Price Group Limited and Glenrand

MIB Limited, where he generally chairs the audit and/or risk committees. He also serves on the boards of some significant non-

listed entities. Nigel is a member of the King Committee on Corporate Governance.

Dr Richard Lewis – (B.A., LL.B., MBA., D.JURIS) Alternate Non-Executive Director (50)

Appointed 12 May 2008. Richard is the principal associate of Richard Lewis, Smith & Associates CC, a firm specialising in

strategic planning, human resources, and leadership development. Richard completed his BA, LLB degrees at the University of

Natal where after he became an advisor with the Natal Chamber of Industries for two years. He then went to live in Germany to

lecture at the Euro-Akademie, Cologne. Whilst there, he completed an MBA degree and a Doctorate in Law. Primarily a strategist,

Richard is also specialised in corporate governance. He is a member of the SA Board of Personnel Practitioners, and was also

past ‘Director: South Africa’, of the German SA Trade Organization. He is a member of the SA Society for Labour Law and the Vice

Chairperson of the Wildlife Society of SA with the Strategy and Corporate Governance portfolio responsibility. Richard is a non-

executive Director of Wynleigh International (a quality compliance management systems company) and of The Evolution

Consulting Group.

Butana Khoza –(B.Com, PGDA, CA(SA)) Independent Non-Executive Director (42)

Appointed 13 June 2008. Butana qualified as chartered accountant in 1994 and has worked in various capacities in the financial

services sector over the last 13 years, first within the Southern Life group and subsequently with African Harvest. He was one of

the founding members of African Harvest’s investment banking subsidiary and a member of the team that led to a management

buyout of African Harvest Limited’s operating businesses that culminated in the establishment of the diversified financial services

group Vunani Limited. He is an executive director of Vunani Limited, responsible for the group asset management cluster.

Mark Anderson - (B.Com (Hons),CA (SA)) Alternate Independent Non-Executive Director (48)

Appointed 13 May 2008. Mark has been involved in corporate finance activities since 1991. Mark joined African Harvest Capital in

1998 and was involved in a management buyout in 2004 which led to the formation of Vunani. He has headed up Vunani’s

investment activities since 2004. Mark is a Director of Vunani Limited, a company listed on the JSE’s AltX.

2

Chairman’s ReportPerformance Overview

Revenue - Up 29.7%

Attributable earnings - Up 1.0% to R100. 3m

Earnings per share - Down 7.1%

HEPS - Down 6.2%

Net tangible asset value - Up 41.0% to R397. 7m

The last 12 months ending March 2009 are recognised as the most volatile period in the history of the steel industry; from extraordinary demand and unprecedented profits from April to August 2008, the world saw a dramatic slump in volumes and pricing, causing massive losses by steel mills and distributors alike.

BSi Steel managed these difficult times by cutting back on inventories, reducing costs and focusing on ex-stock trade. Our stock replenishment program was aimed at ‘same month sales’, thereby ameliorating inventory losses on the back of ongoing steel price drops. Nevertheless, the H2 was characterised by severe stock losses and low trade volumes. Given the extraordinary circumstances, I feel that BSi posted an acceptable profit for the period.

International Steel Industry Outlook

The only certainty at this juncture is uncertainty; volatility will prevail in world markets for at least 12 months. The period will be punctuated by a few false-starts, where pricing will increase, only to slump back within 2 to 5 weeks. Severe production cut backs have already begun to take effect – up to 75% in some regions. Prices seem to have stabilised towards the middle of May, with some products edging up a few percentage points. It is likely that there will be some short-term shortages in certain sectors/products as mills try to balance production with demand. An ongoing reduction in price seems unlikely at this stage, as most mills are losing money and would sooner cut production than sell at a loss.

Prospects for the year ahead

Despite the prevailing sense of gloom and doom, we believe these tough times present BSi with some excellent opportunities. Our new Klipriver operation now provides us with a much needed platform to grow the business for many years, with relatively low future CAPEX requirements.

Our 5-point growth program remains unchanged, albeit with a shift of emphasis from last year:

1. Organic Growth:

Remains central to our growth program. Relative to other growth initiatives, it provides us with the lowest risk and highest return.

2. New Products and Services:

Are extensions of organic growth. Adding new products to our marketing platform is relatively easy to do. This includes ongoing growth in structural sections and plate, with the addition of corrugated roofing, slit strip and blanks this year. The processing plant bears special mention; as we intend to increase our value proposition through increasing the capacity and variety of our processing equipment. We have now installed our RBI cut-to-length line, the refurbished slitting line and batch blanking line.

2

Chairman’s Report (continued)

Our 3 new roofing lines will be installed in June/July, followed by our new 2000 x 6mm cut-to-length line in Sept/Oct 2009. This additional capacity and new processes will give us the tools to support an ongoing growth campaign, both in existing and new lines.

3. Geographic:

We continue to drive geographic growth, aiming at increasing our US Dollar based earnings. Our new office in Mauritius offers us a platform to grow our USD balance sheet.We opened an operation in Zimbabwe on 1st May and will continue to increase our direct export trading markets.

4. Acquisitions:

The climate for successful acquisitions is upon us and is likely to prevail for at least 12 months. Price expectations will be moderated significantly from previous unrealistic highs.We will target companies offering us geographic diversity, a synergistic fit, good management and a proven profit record.We will pay special attention to how such companies have performed in the tough conditions.

5. BBBEE:

Opportunities will kick in this year, now we are officially compliant (level 7). It is our intention to improve our rating over the next 3 to 4 years.

This growth drive will be for new business, where we were previously unable to quote BBBEE sensitive buyers and markets.

Directorate

The following changes were made to the Board:

Name Change

W L Battershill 01 April 2009: Steps down as Joint CEO, remains as Group Chairman

G D G Mackenzie 01 April 2009: Takes over as Group CEO, was Joint CEO

The remaining Board members retain their positions.

Note of appreciation

It is in tough times that the true mettle of a man is tested; I can say without reservation that the Directors and staff of BSi have resolutely stuck to their posts whilst the business world as we know it deteriorated before our eyes.

I convey my heartfelt and sincere appreciation to each and every one of you for your unstinting efforts; you are an inspiration to me and pleasure to work with.

To our clients; I thank you for your support, especially during our move, where service levels were not up to our desired standards. We remain committed to improving our service and quality to ensure we remain your supplier of choice.

Chairman’s Report (continued)

2

To the shareholders, a special thanks for standing by us through these turbulent times. We have promised you long-term growth and we will deliver; be assured of this. Your investment remains in the hands of a capable, dedicated and ambitious team.

We remain committed to building a centre of excellence in the steel industry. These tough times will not dull our blade, merely reinforce our will and serve to hone our skills.

Mine’s a Hansa,

Love Will

W L BattershillCHAIRMAN

2

Chief Executive Officer’s Report

Introduction

BSI Steel Limited is a distributor of primary steel products within South Africa and the Southern African region. We play a buying, importing, coil processing, stocking, distribution, financing and exporting role within the value chain.

Our business is divided into three segments:

1. Bulk sales

2. RSA Stockists

3. Exports

These segments are under-pinned by our growing investment in the primary processing of steel coils. This value-added service allows us to access more customers and therefore more volume.

Bulk Sales

This division based in Pietermaritzburg acts as a wholesaler and volume trader of steel to larger end-users right across South Africa. Material is procured from both local and international sources and offers an alternative to mill supply to our customers.

RSA Stockists

This division comprises two stocking operations, BSI Gauteng based in Klipriver (south of Johannesburg) and BSI KZN in Pietermaritzburg in Kwazulu Natal. These merchants typically offer a just-in-time service to our customers delivering same or next day, with our own fleet of trucks. Emphasis is on high service levels and customer loyalty. Product diversification is an important theme of our growth strategy for these businesses, particularly borne out of our increasing capacity from our processing division.

Exports

We divide this segment into stockists and export trading:

The stockists are based in Zambia (Lusaka and Kitwe) and the Democratic Republic of Congo, (Lubumbashi and Kolwezi), and recently in Zimbabwe (Harare and Bulawayo). These businesses provide a JIT service to their customers and source from SA and regional mills and occasionally from blue-water imports. Their customer mix is both cash sale walk-in trade as well corporate customers requiring credit. The DRC and Kitwe customer base is predominantly mining, while Lusaka is construction, manufacturing and agribusiness. BSI Klipriver provides the logistics service in getting the steel consolidated and shipped to the African operations.

The export trading division handles bulk sales of steel for the larger users within overland Africa, including Namibia, Botswana, Zimbabwe, Zambia, DRC, Malawi and Mozambique. They complement the stocking operations and typically have a different client mix and handle a much wider range of products. Each region has specialist traders concentrating on those markets and regular trips into Africa are made by these traders to maintain customer loyalty and keep abreast of developments. The new office in Mauritius plays a sourcing role for our African operations, buying from South Africa, regional African mills as well as blue-water imports. It will also look for export opportunities into the Indian Ocean Island markets in due course.

Chief Executive Officer’s Report (continued)

2

The year in reviewThe year April 2008 to March 2009 can be divided into 2 markedly different trading environments. The first half was characterised by unprecedented steel price increases and a huge surge in apparent demand. This demand was not able to be met by the mills resulting in significant rationing of product by the steel mills.

The second half sparked by the global financial crisis saw steel prices collapse and apparent demand drop severely as a result of aggressive de-stocking right through the steel supply chain. Sectors most severely affected were automotive, mining, white goods, housing and certain sub-sectors within manufacturing. Only those manufacturers exposed to the government infrastructural spend continued relatively unaffected.

While BSI Steel endeavoured to maximise the favourable trading conditions between April and August 2008, the severe supply constraints from the mills prevented us from meeting customer demand to our satisfaction. While this was mitigated by imports and regional buying, this did result in some lost opportunity. Nevertheless we did manage to post a record after tax profit for the period to September 30th of R127m.

When world steel prices started decreasing in September 2008, the local mills started cutting prices in unison and this continued for the remainder of our financial year until March 2009. This resulted in BSI incurring significant and successive stock write downs in the second half of the financial year. In addition due to severe industry-wide de-stocking, our margins came under pressure as the stockists competed with one another to dump depreciating stock. Stock in fact became a liability – the more stock one carried at month-end, the more one wrote down. The de-stocking exercise took longer than projected due to the lag in the mill pipeline and this hit us and our competitors further, the material arriving at historically high prices further aggravating the write-downs and depressing margins.

We have thus had a very interesting and challenging year from a trading point of view! We remain, however, a company committed to sustainable growth, and are continually looking to improve our product offering and our geographic footprint.

During the frenetic trading activity of F2009, we managed three significant projects that will give us the platform to continue growing sustainably in South Africa and Africa.

1. We relocated all our Gauteng-based operations to a purpose-built 23 ha site in the south of Johannesburg. This comprises a new office block for all our employees, 20,000 square metres of warehousing, housing both our stock and our expanding processing facility

2. We moved our cut to length & blanking line and installed our refurbished slitting line within the new facility. We are now gearing up to install our second CTL line in August 2009.

3. We did a full new ERP implementation across the group which will give us the business intelligence to properly manage our business and drive our growth strategy. In addition, all our African operations are being linked to our single instance via VSAT allowing greater control, rationalising staff functions and costs and improving synergies with the rest of the group.

The distracting nature of these projects cannot be under-estimated and we probably lost opportunity and some efficiencies as a result. However, they are now completed and we can now look forward to the competitive edge they will give us.

Broad Based Black Economic EmpowermentWe remain fully committed to BBBEE and see it as an important mechanism for creating opportunity for the previously

disadvantaged sectors of our society. We also see it as an opportunity and we will endeavour to improve on our level 7 score,

targeting level 4 within 4 years.

Chief Executive Officer’s Report (continued)

Health and safety

2

With our move to our purpose-built processing and distribution centre in Klipriver, we have a world class facility that is staff-friendly, ergonomic and has huge potential for expansion. It also allows us to expand on our vision of excellence, quality and safety.

Health and safety in particular is an absolute priority at BSI Steel at all our branches and sites.

Word of thanksI’d like to thank the staff of BSI for the way you have remained positive in what have been very difficult times both from a business point of view, but also I am sure, in your own personal situations. Recessions are like winter – they are harsh and severe and tough to live through; but there is also a sense of renewal that comes from the die-off, the old leaves making way for the new. All things in life are cyclical and economies are no different. Things will get better and we need to prepare ourselves for the next growth cycle.

Thank you to our shareholders who have also been through very challenging times. Your support has been much appreciated and I can assure you that BSI Steel remains a driving force within the SA and SADC steel fraternity. Your executive and management team remain committed to growing this business sustainably and profitably.

Lastly, thank you to our customers. We have had a very volatile year with much change and thankfully the big projects are behind us. We will continue to expand our product offering and strive to exceed your expectations of service and quality.

Yours,

G D G MackenzieGROUP CEO

2

Human Capital Sustainability ReportIntroduction

BSi Steel has the vision to build our reputation with all our key stakeholders as being the “employer of choice” within the steel industry. It’s with this vision in mind that we have contextualised the unique, unprecedented challenges that have been faced by the company in recent times and the impact these changes are having on the performance and sustainability of our human capital.

On the local front the steel market has moved from an artificially buoyant position of high demand and high profit down to a sluggish trading market in under six months. This sudden change in operating condition has resulted in immediate action being taken to boost staff morale and provide secure, inspirational leadership in these changing times. The positive attitude and proactive behaviour of our people is as important to the business in these difficult trading conditions as prudently managing our stock levels and cash flow.

Our steadfast commitment to continue undeterred with transformation and B-BBEE initiatives, company culture unification, skills transfer and development, talent sourcing and retention, diligent performance management, health and safety awareness and employee well being programs have given us the competitive edge over the rest of the market to face these operational pressures head on at full speed with a supportive team behind us.

BSi Steel Culture

At the forefront of our human capital intervention is to ensure that the True North principals contained in our Vision, Mission and Behaviour Code are positively reinforced on a regular basis across the Group. It’s through this approach that we have continued to build a proactive, empowered, positive and synergistic team spirit within BSi Steel, despite tough trading conditions.

All our new staff go through Covey’s “personal effectiveness” training during their induction to make sure that the way we operate throughout each division of the business is centered on teamwork values and principles.

Our feedback and communication with staff is frequent and informal, allowing them insight into future plans for the organisation so that a sense of belonging is fostered within our work teams. Our company magazine, “Steel Talking”, is published to all staff with the intention of making sure that everyone feels involved and informed with regard to company performance and that they build a sense of community spirit across all our regions, both on the local and export markets.

Annual perception surveys are run by the HR Team to gauge exactly how engaged staff are within the various teams and to help identify any weak areas, which are then actively targeted for improvement by corrective action plans.

Talent sourcing and retention

BSi Steel is critically aware that the competition for talent is of primary importance to our future success. It’s imperative that we bring the best people into the organisation and make sure that we retain them in a fiercely competitive market.

The company prides itself on a rigorous recruitment process wherein every attempt is made to match potential recruits to the job function as well as to the culture of the business. Much success has been achieved by making use of referral based recruitment and other more creative recruitment strategies.

We have recently introduced a graduate development programme, where young talent is brought into the business to gain valuable work experience and at the same time for the company to have the ideal opportunity to select those graduates with the most potential to fill any vacancies. This is a win-win initiative for both parties and ensures that we build our leadership and priority skills pipeline today so that we have no shortfall in the future.

Retention of talent is as complex and difficult as sourcing the talent and as such we have put in place mechanisms such as career paths, regular performance measurement and feedback, incentives, recognition bonuses and aggressive development plans to ensure that we retain our talent and don’t have them leave to join other employers.

2

Human Capital Sustainability Report (continued)

Leadership development

In order for our staff to have a meaningful, fulfilling experience working at BSi Steel we need to ensure that staff have the best leaders possible. All our leaders from middle management level and above have a uniquely tailored Personal Development Plan, are mentored regularly by a personal coach and are continually evaluated on the impact of their leadership effectiveness through our strong focus on leadership in our performance management system.

Succession planning

At BSi Steel we believe in preparing for the future today and as such we have recently undertaken to introduce a comprehensive Succession Plan for each position in the Group on a middle management and above level.

All key performance area, itemised per position, is outlined in this plan with a breakdown of which other person within the business is capable of assuming this function in time to come. The exact timeline is then plotted out in terms of when the successor will be ready to fill the role so that we can co-ordinate the urgency of such placements to coincide with when these people are operationally needed to take over the reins.

Training and Development plans are geared around this information to ensure alignment to group strategy and if a gap is identified where no candidate is seen as a possibility from within the company relevant recruitment measures are indentified and projected according to time frame to make certain of no manpower planning shortfalls in any key position throughout our operations.

Employment equity

As an organisation we subscribe to the unique, dynamic richness of a diverse workforce equitably representative of the national demographic profiles of the countries we operate in. We believe in employing the best person for the job, irrespective of race, gender, age, or any other classification. Our behavior code guides us in selecting people with a positive attitude and strength of personal character that elevate them above the masses out there on the job market. Strong target areas that we would like to improve on will be to recruit and develop African Female and Disabled employees across all levels.

We have an Employment Equity Committee, which sits once a quarter to give feedback to top management on the progress made towards the EE Plan targets, as well as to discuss any attitudes/perceptions in the workplace to do with employment equity. A mutually beneficial relationship with our Trade Union, NUMSA, is utilised to embark on meaningful conversations on how to ensure that there is no discrimination in any policy or practice within the business. Our current Employment Equity Plan runs through to October of 2010, at which time the next 5 year plan and equity targets will be established by the committee.

Transformation and Broad Based Black Economic Empowerment

A stable, demographically representative economic market in South Africa is fundamental to the sustainability of the business and our future growth on the local market. BSi Steel has embraced transformation within the organisation and we are proud to have been independently rated by EMEX as a LEVEL 7 B-BBEE contributor as at April 2009.

Most important to us is that Transformation is not a stand-alone strategy/committee and therefore we have woven our Transformation and B-BBEE strategic plan into our overall Company Strategy so that the alignment of the two strategies is guaranteed to make business sense at all times.

It is our intention to work toward achieving a LEVEL 6 rating in our next assessment at the end of the 2010 fiscal. In order to achieve this improved rating we will be prioritising skills development initiatives (learnerships, internships, experiential learning and disabled training) and undertaking more synergistic enterprise development initiatives that feed directly into the business synergies. With our commitment to Employment Equity and Skills Development our objective is to improve our management control scorecard element over time and continue to look at economically sound B-BBEE ownership measures.

Our preferential procurement practices will continue to focus on developing business links with black owned and black SMME suppliers and further to this we hope to see Arcelor Mittal coming through with a B-BBEE rating before our next rating is concluded mid 2010.

Human Capital Sustainability Report (continued)

2

BSi Steel is a community focused business and we have always contributed extensively to non-profit organisations across our operating regions. Beneficiaries include Hospice, Reach out with Love, PMB Community Chest, Icare, Little Eden, the Starfish Foundation and many more.

It’s our intention to continue helping those in need over the coming year, however in addition for the coming year we are going to be awarding bursaries to under privileged students and making sure that such bursary awards feed sustainably into our graduate development programme wherever possible.

Skills development and training

In order to remain competitive, stay abreast with current technology and be seen as an employer of choice, BSi has recognised the utmost importance of strategically aligned skills development and training for all our staff. Of primary focus within our training and development strategy is to ensure that we facilitate the advancement of staff to reach their own personal stretch goals of developing within the company over a long term career.

Much of our training budget is spent on the training of interns and learners, on leadership development, ERP systems and on staff in the lower echelons of the business who need basic education skills training (ABET) in order to improve their quality of life. Our Skills Development Committee ensures that all training is approved by line management and our trade union representatives in order to offer meaningful training to uplift all levels of the organisation.

Our challenge for the coming year is the introduction of internally created training interventions for every position in the organisation to increase efficiency and knowledge base at core level within the company without having to rely exclusively on generic external training programs. Our vision is to be a centre of excellence and in order to do so we need to have a system of continual evaluation and improvement with appropriate learning interventions that maximise the transfer of skills and competencies.

Safety, health and the environment

Working with steel products and heavy machinery requires that we put safety first at all times. Our safety procedures have recently been fully audited and our documentation updated to reflect current best practice that is being rolled out to all staff via our health and safety committees on each base.

In addition we take care of employee well being by offering wellness campaign free medical testing, stress management, counseling, HIV and AIDS awareness and give advice on matters of personal finance.

New HR information system

Over the course of the last year BSi Steel has invested in developing, testing and installing a new HR Information System – VIP Genesis. This new system will automate and standardise HR reporting and at the same time give line managers direct access to staff information in order to make quick, empowered decisions with regard to their Human Capital.

BSi Steel has had a challenging 2009 year with many peaks and troughs, but one thing that has remained constant throughout this last year and will remain unchanged as we look forward into the coming year is that our people make BSi Steel what it is and what we invest into our people is the level of success we can expect to see from our results.

A very simple concept, but then again one of our main Behaviour Code elements at BSi Steel is to KEEP IT SIMPLE!

Chantal LombaardGROUP HR EXECUTIVE

2

Corporate Governance ReportIntroduction

The Board of directors subscribe to the principles of good corporate governance including discipline, independence, accountability and responsibility as set out in the 2002 King Report on Corporate Governance for South Africa (King II). BSI has complied in all material respects with the recommendations contained in King II and the requirements for corporate governance of the JSE Limited.

Board of directors

The Board operates in terms of a formally approved charter which sets out its role and responsibilities including:

retain full and effective control of the company

give strategic direction to the company

ensuring that an adequate and effective process of corporate governance is established and maintained

identify and regularly monitor key risk areas and key performance indicators of the business

ensure that the group communicates with shareowners and relevant stakeholders openly and promptly

regularly review processes and procedures to ensure effectiveness of internal systems of control and accept responsibility for

the total process of risk management

assessing the performance of the Board, its committees and its individual members on a regular basis

appointments to and removals from the Board including the appointment of the chairman, chief executive officer, executive

directors and non-executive directors, and the approval of nominations of alternate directors

the formulation if recommended of policies in relation to equal opportunity employment, black empowerment, environment,

health and safety

As at 1 April 2009 Mr. WL Battershill relinquished the role of joint of Joint CEO, and Mr. G D G Mackenzie was appointed CEO.

There have been no other changes to the Board.

The Board has a unitary structure, and at the time of publishing this report, comprised an executive chairman, W L Battershill, four executive directors, G D G Mackenzie (CEO), C Parry, W R Teichmann, and J R Waller (CFO), and two independent non- executive directors, N G Payne (alternate R G Lewis) and B M Khoza (alternate N M Anderson). All directors have attended the AltX Directors Induction programme. King II recommends that the majority of a Board of directors should consist of non-executive directors; however the Board considers the BSI structure to be appropriate for a company of this size and nature. A brief CV of each director can be found on page 6 and 7 of this report.

The non-executive directors hold shares directly and indirectly in the company, and receive no benefits from the company other than director’s fees. They are high calibre individuals with a wealth of knowledge and experience, and are fully independent of management.

A clear division of responsibility is maintained across the Board, precluding any one director from exercising unfettered powers of decision making.

Current executive director’s service contracts are for a period of 5 years and non-executives for two years. In terms of the articles of association of the company, Messrs G D G Mackenzie, N G Payne and C Parry retire by rotation at the annual general meeting, but being eligible will offer themselves for re-election.

The Board meets quarterly, and where considered necessary ad-hoc meetings are convened. The Designated Adviser attends Board meetings.

2

Corporate Governance Report (continued)

The following is a schedule of Board and Board committee meetings held and attended by the directors during the year ended 31 March 2009. The number in brackets denotes the number of meetings attended.

Directors Board Audit Committee

Risk Committee Remuneration Committee

W L Battershill 5 (5) 4 (4) ^ 3 (3) 5 (4)G D G Mackenzie 5 (5) 4 (4)^ 3 (3) 5 (5)J R Waller 5 (5) 4 (4)^ 3 (3) 5 (4)W R Teichmann 5 (5) 1 (1)^C Parry 5 (5) 1 (1)^N G Payne*# 5 (5) 4 (4) 3 (3)N M Anderson* (alt) 1(1) 1 (1)B M Khoza* 4 (4) 3 (3)R G Lewis*@ (alt) 5(5) 1 (1)^ 5 (5)

*Non-executive# Chairman Audit and Risk Committees@ Chairman Remuneration Committee^ Invitee to committee meetings

Board Processes

Board Appointments

The Board from time to time assesses the skills and experience within the Board and when deemed necessary may wish to appoint new Board members.

The Chairman in consultation with the non-executive directors identifies suitable candidates and makes recommendations to the Board. All new Board members that have not already done so are required to attend the AltX Directors Induction programme.

Share dealings

Directors are required to obtain clearance from the Chairman before trading in the company’s shares. The company secretary together with the Designated Adviser ensures that these trades are published on SENS as required by the JSE Listing Requirements.

Directors, and management and staff with access to financial information and other price sensitive information, may not trade in the company’s shares during a closed period. The company secretary informs directors and staff via email when these periods are in effect.

Self-evaluation

The Board has conducted its first self-evaluation exercise reviewing its performance and strategic planning, board composition, relationship with management and other stakeholders, and succession planning. Areas requiring improvement have been identified, and these are receiving attention.

Corporate Governance Report (continued)

Company Secretary

2

The duties and responsibilities of the company secretary are set out in Section 238G of the Companies Act. The Board has appropriately empowered the company secretary to fulfill these duties. Where necessary, the company secretary will involve the Designated Adviser and other experts in this regard.

All directors have access to the advice and services of the company secretary. All directors are entitled to obtain independent professional advice regarding the company’s affairs at the expense of the company.

Board Committees

1. Risk Committee

The risk committee comprises the Chairman, CEO, CFO, Company Secretary and is chaired by independent non-executive director N G Payne. This risk committee meets three times per annum.

The terms of reference of the Risk Committee include the following:

to assist the Board in setting risk strategy policies in liaison with management and in the discharge of its duties relating to

corporate accountability and associated risk in terms of management assurance and reporting

to review and assess the quality, integrity and effectiveness of the risk management systems and ensure that the risk policies

and strategies are effectively managed

to ensure that the company has implemented an effective ongoing process to identify risk, to measure its potential impact

against a broad set of assumptions and then to activate what is necessary to pro-actively manage these risks, and to decide

the company’s appetite or tolerance for risk

to oversee formal reviews of activities associated with the effectiveness of risk management and internal control processes. A

comprehensive system of control should be established to ensure that risks are mitigated and that the company’s objectives

are attained

to review processes and procedures to ensure the effectiveness of internal systems control so that decision-making capability

and accuracy of reporting and financial results are always maintained at an optimal level

A risk matrix recording significant risks, the probability of occurrence, potential impact on the company and steps taken to mitigate these risks is maintained on an ongoing basis. The risk committee reports to the Board.

2. Audit Committee

The Audit Committee comprises the two independent non-executive directors and the Designated Adviser and is chaired by N G Payne. The committee meets four times per annum and ad-hoc meetings are called when deemed necessary. The Chairman of the Board, CEO and CFO are invited to attend audit committee meetings.

The terms of reference of the Audit committee include the following:

assist the Board in discharging its duties relating to the safeguarding of assets, the operation of adequate systems, control

procedures, and the preparation of accurate financial reporting and statements in compliance withal legal requirements and

accounting standards

recommend to the Board which firm should be appointed as external auditors

evaluate the independence and effectiveness of the external auditors and consider any non- audit services rendered by such

auditors as to whether this substantially impairs their independence, and to pre-approve any such services

Corporate Governance Report (continued)

review the interim and annual financial statements, as well as any announcement of results ensure that financial statements are prepared on appropriate accounting policies consistently applied and supported by

reasonable and prudent judgments and estimates

2

review the accounting policies and procedure adopted by the company and any changes made or contemplated thereto review the effectiveness of management information, the annual audit, the internal audit function and other systems of internal

control

The audit committee members have unrestricted access to all information and reports necessary to discharge their duties.

The audit committee has considered the appropriateness and is satisfied with the expertise and experience of the financial director.

The external auditors have unrestricted access to the audit committee and the chairman, and are given opportunities for discussion with the audit committee without executives present.

A qualified CA (SA) internal auditor has recently been appointed. He reports to the audit committee and is responsible to the CFO on day to day matters.

The audit committee reports to the Board.

3. Remuneration Committee

See Remuneration report on page 22 of this report.

Auditing and Accounting

1. External Audit

The audit committee recommends the appointment of external auditors to the Board. It considers the independence of the external auditors and is required to pre-approve the use of the external auditors for non-audit services.

The external auditors provide an independent assessment of internal financial controls, and are responsible for reporting whether the financial statements are fairly presented in accordance with IFRS. The preparation of the financial statements is the responsibility of the directors.

Subject to shareholder approval, Deloitte and Touche (Partner – C Sagar) have been re-appointed as external auditors for the year ending 31 March 2010

2. Internal Audit

The Board has decided to implement an internal audit function.

A qualified CA (SA) internal auditor has recently been appointed. He reports to the audit committee and is responsible to the CFO on day to day matters.

An internal audit charter is to be drawn up and will define the responsibility, scope and authority of the internal audit function.

3. Internal Control

The Board is responsible for the company’s systems of financial and operating controls and monitoring their effectiveness. These systems are designed to provide reasonable, but not absolute assurance as to the integrity of the financial statements, and to safeguard the company’s assets.

During the year under review, nothing has come to the attention of management to indicate any material failure of the internal control systems.

Corporate Governance Report (continued)

4. Going Concern

The Board has every reason to believe that the company has adequate resources in place to continue in operation for the foreseeable future, and accordingly the financial statements were prepared on the going concern basis.

2

5. Stakeholder Communication

The company is committed to open and timely communication with all stakeholders. Company results and announcements are published on SENS and are available on the company’s website, and there have been a number of presentations of the company’s results and strategy to investors.

6. Code of Ethics

The Group is committed to a policy of fair dealing and integrity in the conduct of its business. This commitment, which is endorsed by the Board, is based on the fundamental belief that business should be conducted honestly, fairly and legally. The company expects all employees to share its commitment to high moral, ethical and legal standards.

A formal Code of Ethics has been adopted by the Board and includes the following:

Compliance with laws and regulations

Conflicts of interest

Anti-competitive behaviour

Employment equity

Safety, health and environment

Social responsibility

Privacy and confidentiality

All directors and employees are expected to comply with the code. A process to deal with possible contraventions of the code is included.

Stephen HackettCOMPANY SECRETARY

2

Remuneration Report

During the past year, the Remuneration Committee, which is an executive committee with approved Terms of Reference, has been extremely active in ensuring that BSi has been able to secure and retain the right people in order to ensure its continued success. As in the past, the Committee has continued to maintain that the company’s directors and senior executives are fairly rewarded for their individual contributions to the company’s overall performance, whilst applying its mind to various other issues pertaining to the annual salary increase, performance incentive schemes and other benefits.

The Remuneration Committee is chaired by Dr. Richard Lewis, a non-executive director, who is a strategy and human resources specialist.

The current members are:

Dr. Richard Lewis – non-executive director – Chair

Mr. William Battershill – Group Executive Chairman

Mr. Grant Mackenzie – Group CEO

Mr. James Waller – Group CFO

Ms. Chantal Lombaard – Group HR Executive

Mr. Steve Hackett – Committee Secretary – Group Secretary

During this past year, the Committee met five times and applied its mind in particular to the following:

The determination of the annual staff salary and wage increases

The assessment of director’s increases according to national survey benchmark data

The drawing up and approval of a Remuneration Policy

The implementation of a flexible discretionary profit share bonus for staff

The determination of appropriate elements of evaluation for the Director’s profit share

The development and approval of a Key Staff Retention Scheme

The implementation of a Warehouse bonus scheme – based on a scorecard of both personal and company performance to

pay out a target related bonus each quarter

The review of the earnings of all staff as compared to the market median.

The approval of a new Travel Policy, and travel rates were reviewed

The introduction of a new BSI Share Appreciation Rights Scheme and a new MTIP/LTIP executive director incentive scheme

to replace the old long term “BSI Share Incentive” scheme.

At listing, BSI initiated a long term incentive scheme that senior managers participated in. The long term scheme was a “share purchase scheme” administered by a share trust and trustees, and essentially allowed the participant to buy shares at the current share price, on extended credit of three years, with interest.

On discussion with Price Waterhouse Coopers our tax advisers as well as independent legal opinion and specialist advice, Remco discovered significant anomalies that made the scheme unworkable, particularly in the context of a recent change in JSE rules with respect to share schemes. In addition it was found to be tax-inefficient and proved very complex to administrate.

It was therefore felt that this scheme would not serve its original intentions, which were principally to retain senior staff by providing a long-term investment in the company and to allow new ‘rising stars’ to make a significant long-term contribution to the company.

The Remuneration Committee recognises its responsibility for ensuring due compliance with the King Code of Corporate Practice and Conduct in respect of remuneration and related matters, and for reporting thereon to the Board.

Remuneration Report (continued)

2

Remuneration Policy and Philosophy

The remuneration philosophy of BSI Steel is to attract, develop and retain high performing individuals while also reinforcing, encouraging and promoting superior performance. Remuneration policies are aligned with the strategic direction and operational objectives of the business.

The objective is to establish a level of guaranteed remuneration that is competitive, short-term incentives that reward directors and management for achieving profit targets and medium and long-term share incentive schemes that serve as a retention and motivational mechanism for directors and senior management, and align them with shareholders’ interests.

The most important challenge facing BSI Steel is how to attract and RETAIN quality employees that will grow with the company and stick with the team. The world is becoming more fluid and mobile, and people (especially the younger generation) are more inclined to leave jobs on a whim. We therefore need sound retention mechanisms that give people the upside of an appreciating share price to give them long term value and share ownership in return for their service.

Senior Executive Incentive and Retention Performance Plans

Four executive directors, Grant Mackenzie (CEO), James Waller (CFO), Ross Teichmann and Craig Parry qualify.

Objectives of the performance plans

1. The objectives of these plans are - to encourage, recognise and reward entrepreneurial flair, to more closely align the interests of the executive with those of shareholders in the medium and long term, and as part of the company’s risk management retention strategy to retain a highly competent and motivated team at the helm of the company’s operations on an ongoing basis.

2. Two incentive plans were introduced with effect from 1st April 2008 recommended by Remco and approved by the board, to be referred to respectively as the Medium Term Incentive Plan and the Long Term Incentive Plan.

The Medium Term Incentive Plan (MTIP)

Equity growth units (‘equity units’) are allocated annually by the Board on the first day of each financial year to senior executives as defined who are in the employ of the company on that date. Determination of ‘share price’ for allocation purposes will always be at the volume weighted average price (VWAP) for the month of March (the last month of the financial year).

Allocations are made in respect of a calculated grant value of equity units equal to an approved multiple, being a nominated ratio of equity unit value to guaranteed pay for each position.

The equity units will have a value per unit during the holding period which is equal to the share price ruling from day to day.

The grantee is entitled to a cash bonus on a future date equal to the escalation in value of the equity units in to the extent that this exceeds the movement in the Consumer Price Index over the holding period.

For these purposes, the future date will be deemed to be -

1. the end of a period of three years from the date of allocation, provided that the grantee remains in employment on that date, or

2. on an earlier date, being the date of termination of employment where such termination occurs as a result of retrenchment for operational reasons, ill-health or incapacity, or death, in each case under and in terms of the employment contract applying on that date, or

3. at the option of the company the date of a change of control of the company

4. The ‘share price’ for exercise purposes will in all cases be at the March VWAP.

The grantee is therefore not able to “time” the market and is limited to exercising at the March VWAP at the end of each 3 year holding period.

Remuneration Report (continued)

2

The Long Term Incentive Plan

Earnings growth units (‘earnings units’) have been allocated by the Board to the above senior executives on a once-off basis in lieu of compensation for agreeing to enter into a fixed-term restraint agreement with the company in grant values to be nominated and approved by the Board.

The earnings units allocated have a value per unit at the outset equal to the share price ruling at the effective date of grant. The value per unit is revalued thereafter at the end of each financial year on the basis of the headline earnings per share (HEPS) for that year, the value equalling the value of the units in the base year multiplied by the ratio of the inflation-adjusted HEPS in the most recent financial year divided by the HEPS in the base year.

The grantee is entitled to a bonus on the agreed future date equal to the escalation in value of the earnings units, but however subject to compliance with the performance condition defined in below.

The agreed future date will be the earlier of –

1. the date of the expiry of the restraint agreement, provided that the grantee remains in employment on that

date, or

2. the date of earlier termination of employment where such termination occurs as a result of retrenchment for

operational reasons, ill-health or incapacity, or death, in each case under and in terms of the restraint

agreement, or

3. at the option of the company the date of a change of control of the company.

No bonus will accrue unless the HEPS growth during the holding period has exceeded the movement in the Consumer Price Index over the holding period by more than 10% (ten percent) per annum; provided that, if the grantee so elects before the end of the holding period, and if the grantee remains in employment for a further year after the expiry of the restraint agreement, the holding period may be extended by one year, namely for the financial year following the expiry of the restraint agreement, and if the HEPS growth rate exceeds the stated 10% (ten percent) condition over the extended holding period, the cash bonus will be calculated in respect of the extended holding period and paid out on that basis.

Summary of allocations:

1st April 2008 1st April 2009Long Term Incentive PlanHEPS at grant 14.91 13.99

Medium Term Incentive PlanShare price at grant R1.00 R0.76

Grant MackenzieLTIP 13 592 064

MTIP 3 398 016 3 750 864

James WallerLTIP 9 952 416

MTIP 1 866 078 1 865 255

Craig ParryLTIP 9 470 208

MTIP 1 775 664 1 810 244

Ross TeichmannLTIP 9 401 568

MTIP 1 762 794 1 917 782

Remuneration Report (continued)

Senior Management Incentive and Retention Scheme

2

Shareholder approval was obtained on 27 March 2009 for a Share Appreciation Rights Scheme for senior managers and key staff as both a retention and incentive scheme and to create better alignment with shareholders.

Herewith some details of the scheme:

1. The Share Appreciation Right Scheme includes participation by divisional executives and selected senior employees of the

Group to ensure that the Group attracts and retains the core competencies required for formulating and implementing the

Group’s business strategies.

2. As the primary intent of the new share incentive plan will be to purchase shares in the market to settle the benefits, the new

share incentive plan will not be as dilutive as conventional share option schemes.

3. The new share incentive plan also supports the principle of alignment of management and shareholder interests with

Performance Conditions governing the vesting of instruments.

4. Employees will receive annual Grants of Share Appreciation Rights, which are conditional rights to receive Shares equal to the

value of the difference between the Exercise Price and the Grant Price. Vesting of the Share Appreciation Rights is subject to

Performance Conditions.

5. Upon exercise by a Participant the relevant Employer Company will settle the value of the difference between the Exercise

Price and the Grant Price by delivering Shares, alternatively, as a fall back provision only, by settling the value in cash. Share

Appreciation Rights not exercised within the SAR period will lapse.

In terms of the rules of the Share Appreciation Right Scheme, a maximum of 73 000 000 shares may be allotted.

The first SAR awards were made on the 31st March 2009. A total of 6 072 500 SAR were awarded at a Grant price of R 0.76

As at 31 March 2009 assuming that every two SAR awards result in the allotment of one share, a total of 3 036 250 shares are reserved, leaving a balance of 69 963 750 shares available to be allotted.

Not all of the vesting conditions relating to any of these schemes have been met during the current financial year and no provisions have therefore been made in the financial statements.

Directors’ Responsibility and Approval StatementThe directors are required by the Companies Act of South Africa, 1973, to maintain adequate accounting records and are responsible for the content and integrity of the annual financial statements and related financial information included in this report.

2

It is their responsibility to ensure that the annual financial statements fairly present the state of affairs of the group as at the end of the financial year and the results of its operations and cash flows for the period then ended, in conformity with International Financial Reporting Standards. The external auditors are engaged to express an independent opinion on the annual financial statements.

The annual financial statements are prepared in accordance with International Financial Reporting Standards and are based upon appropriate accounting policies consistently applied and supported by reasonable and prudent judgments and estimates.

The directors acknowledge that they are ultimately responsible for the system of internal financial control established by the group and place considerable importance on maintaining a strong control environment. To enable the directors to meet these responsibilities, the board sets standards for internal control aimed at reducing the risk of error or loss in a cost effective manner. The standards include the proper delegation of responsibilities within a clearly defined framework, effective accounting procedures and adequate segregation of duties to ensure an acceptable level of risk. These controls are monitored throughout the group and all employees are required to maintain the highest ethical standards in ensuring the group’s business is conducted in a manner that in all reasonable circumstances is above reproach. The focus of risk management in the group is on identifying, assessing, managing and monitoring all known forms of risk across the group. While operating risk cannot be fully eliminated, the group endeavors to minimise it by ensuring that appropriate infrastructure, controls, systems and ethical behaviour are applied and managed within predetermined procedures and constraints.

The directors are of the opinion, based on the information and explanations given by management that the system of internal control provides reasonable assurance that the financial records may be relied on for the preparation of the annual financial statements. However, any system of internal financial control can provide only reasonable, and not absolute, assurance against material misstatement or loss.

The directors have reviewed the group’s cash flow forecast for the year to 31 March 2010 and, in the light of this review and the current financial position, they are satisfied that the group has or has access to adequate resources to continue in operational existence for the foreseeable future.

The external auditors are responsible for independently reviewing and reporting on the group's annual financial statements. The annual financial statements have been examined by the group's external auditors and their report is presented on page 27.

The annual financial statements set out on pages 28 to 81, which have been prepared on the going concern basis, were approved by the board on 19 June 2009 and were signed on its behalf by:

WL Battershill JR Waller

Pietermaritzburg19 June 2009

Secretarial Certification I certify, to the best of my knowledge and belief, that the company has, in respect of the period under review, lodged with the Registrar of Companies all returns that are required by a Public Company, and that all returns are true, correct and up to date.

SJ HackettCompany Secretary

Pietermaritzburg19 June 2009

2

Independent Auditors ReportTo the members of BSI Steel Limited

Report on the Financial StatementsWe have audited the annual financial statements and group annual financial statements of BSI Steel Limited which comprise the directors’ report, the balance sheet and consolidated balance sheet as at 31 March 2009, the income statement and consolidated income statement, the statement of changes in equity and consolidated statement of changes in equity and cash flow statement and consolidated cash flow statement for the year then ended, a summary of significant accounting policies and other explanatory notes, as set out on pages 28 to 81.

Directors’ Responsibility for the Financial StatementsThe company’s directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and in the manner required by the Companies Act of South Africa. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the directors, as well as evaluating the overall financial statement presentation.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the financial statements present fairly, in all material respects, the financial position of the company and the group as at 31 March 2009 and the results of their operations and their cash flows for the year then ended in accordance with International Financial Reporting Standards, and in the manner required by the Companies Act of South Africa.

Deloitte & TouchePer CA Sagar PietermaritzburgPartner 19 June 2009

National Executive: GG Gelink (Chief Executive), AE Swiegers (Chief Operating Officer), GM Pinnock (Audit), DL Kennedy (Tax & Legal and Financial Advisory), L Geeringh (Consulting), L Bam (Corporate Finance), CR Beukman (Finance), TJ Brown (Clients & Markets), NT Mtoba (Chairman of the Board), CR Qually (Deputy Chairman of the Board).

Regional Leader: GC Brazier

Pietermaritzburg19 June 2009Directors’ Report

2

The directors submit their report for the year ended 31 March 2009

1. Review of activities - Main business and operations

The group is engaged in sale, processing and distribution of steel and allied products and operates principally in South Africa, Zambia and the Democratic Republic of Congo.

The operating results and state of affairs of the company are fully set out in the attached annual financial statements and do not in our opinion require any further comment.

Net profit of the group was R 100,311,697 (2008: profit R 99,367,479), after taxation of R 25,129,264 (2008: R 34,166,758).

2. Going concern

The annual financial statements have been prepared on the basis of accounting policies applicable to a going concern. This basis presumes that funds will be available to finance future operations and that the realisation of assets and settlement of liabilities, contingent obligations and commitments will occur in the ordinary course of business.

3. Post balance sheet events

Steel prices decreased by R500 and R1, 000 per ton on 1 April 2009 and 1 May 2009 respectively and is to increase by R250 per ton effective 1 July 2009. The net realisable value of inventory at year end has been adjusted accordingly.

Business activities have been extended to Zimbabwe as from 1 May 2009 and the operation will constitute a subsidiary of BSI Steel Africa Limited.

Land and buildings classified as held for sale at year end as per note 16 have been disposed of after year end.

4. Authorised and issued share capital

Refer to note 9 of this report and note 17 of the annual financial statements for details of the changes in the above during the year.

5. Dividends Paid

No dividends were declared or paid to shareholders during the year as the directors decided that more value would be added to shareholders wealth given the current economic climate by utilising cash resources in buying back shares during the current financial year and will continue to do so during the following financial year if the current circumstances continue.

6. Directors

The directors of the company during the year and to the date of this report are as follows:

Name Nationality Changes

WL Battershill South AfricanJR Waller South AfricanC Parry South African Appointed 1 April 2008GDG MacKenzie South AfricanNG Payne (Non Executive) South AfricanEG Dube (Non Executive) South African Resigned 13 June 2008WR Teichmann South African Appointed 1 April 2008RG Lewis (Alternate Non Executive) South African Appointed 12 May 2008BM Khoza (Non Executive) South African Appointed 12 May 2008NM Anderson (Alternate Non Executive) South African Appointed 13 May 2008

Directors’ Report (continued)

2

7. Secretary

The secretary of the company is Stephen Hackett of:

Business Address: Eden Park DriveMurrayfield ParkMkondeniPietermaritzburg3201

Postal Address: P.O. Box 101096ScottsvillePietermaritzburg3209

8. Interest in subsidiaries

Details of the company's investment in subsidiaries are set out in note 8.

9. Special Resolutions

At a general meeting of the shareholders on 12 December 2008 it was resolved that the property described as erf number 710, Alrode Ext 4, Johannesburg be sold.

At a general meeting of the shareholders on 11 September 2008 the following resolutions were approved:

the name of the company be changed from BSI (SA) Limited to BSI Steel Limited;the company increase its existing authorised ordinary share capital from R10,000 divided into 1,000,000,000 ordinary shares of 0.001 cent to R100,000 divided into 10,000,000,000 ordinary share of 0.001 cent each by the creation of 9,000,000,000 ordinary shares of 0.001 cent each; and

the directors of the company be authorised until the next annual general meeting of the company to acquire the company's own shares, upon such terms and conditions and in such amounts as the directors may from time to time decide.

At a general meeting of the shareholders on 26 March 2009 it was resolved that the company would repurchase from the BSI Share Incentive Trust 17,620,232 ordinary shares with a par value of 0.001 cent each at an average price of 89.5 cents per share and to cancel such shares.

10.Directors interest in shares

2

GROUP COMPANY2009 2008 2009 2008 R R R R

Directly beneficialNG Payne 5,526,000 1,606,176 5,526,000 1,606,176WL Battershill 1,081,953 574,914 1,081,953 574,914GDG Mackenzie 9,755,937 11,437,434 9,755,937 11,437,434JR Waller 3,000,000 3,000,000 3,000,000 3,000,000WR Teichmann 21,782,165 - 21,782,165 - NM Anderson 86,000 - 86,000 -RG Lewis 100,000 - 100,000 -

Indirectly beneficialE Dube and associates - 50,240,000 - 50,240,000WL Battershill and associates 336,075,214 328,727,332 336,075,214 328,727,332GDG Mackenzie and associates 81,331,349 84,949,740 81,331,349 84,949,740JR Waller and associates 9,213,469 8,967,178 9,213,469 8,967,178C Parry and associates 56,195,147 - 56,195,147 -BM Khoza and associates 50,390,000 - 50,390,000 -

574,537,234 489,502,774 574,537,234 489,502,774

Between the year end and the date of this report Mr. C Parry and associates have sold 1,500,000 shares leaving a balance of 54,695,147 shares. There have been no other changes in directors’ interest in shares.

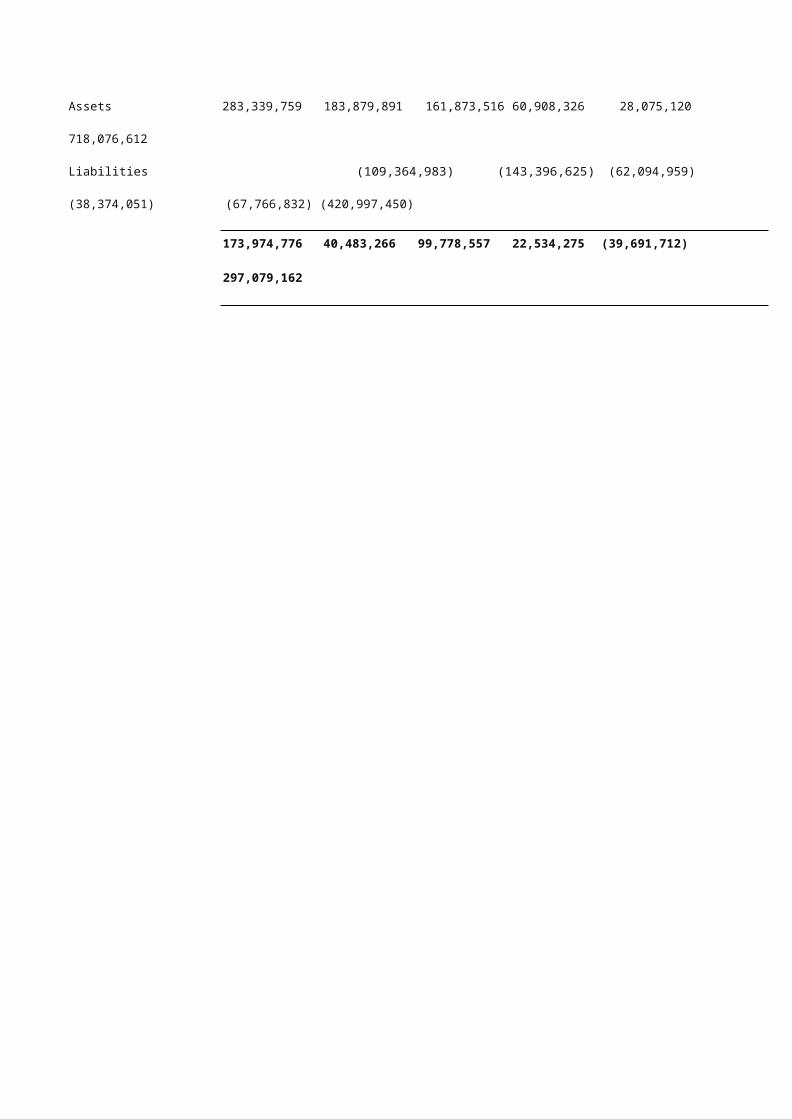

Balance Sheetsas at 31 March 2009

GROUP COMPANYNote(s) 2009 2008 2009 2008

R R R R

Assets

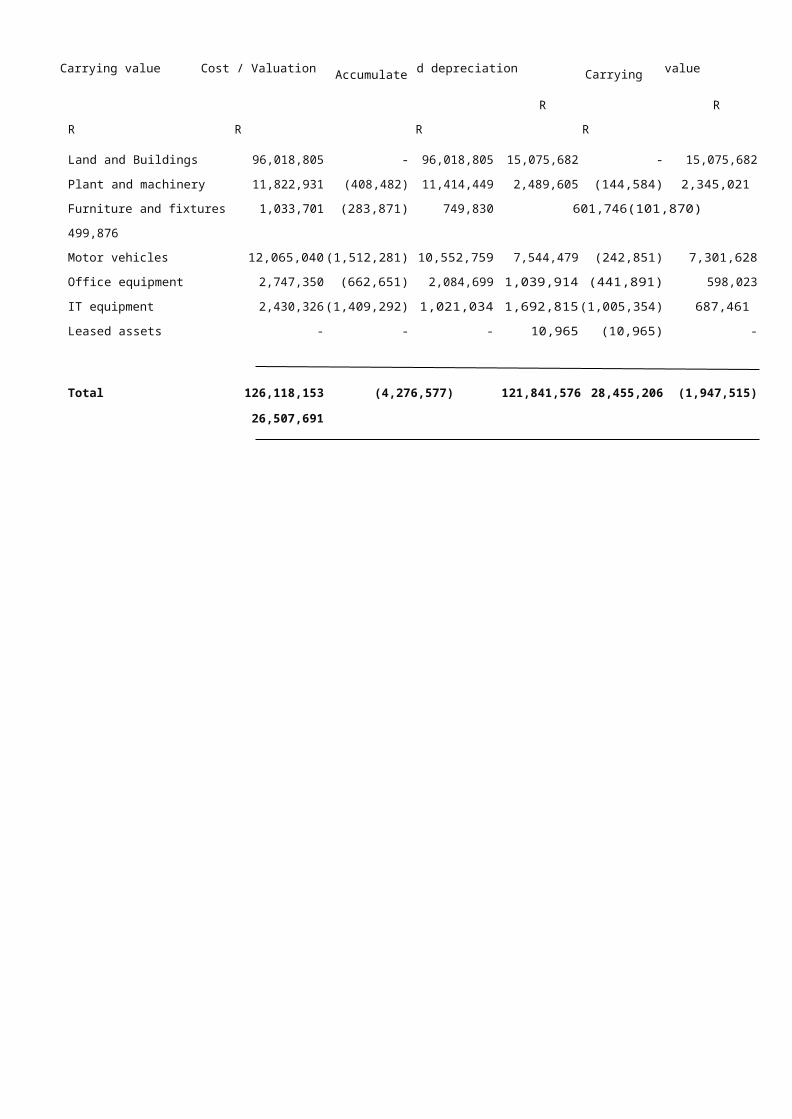

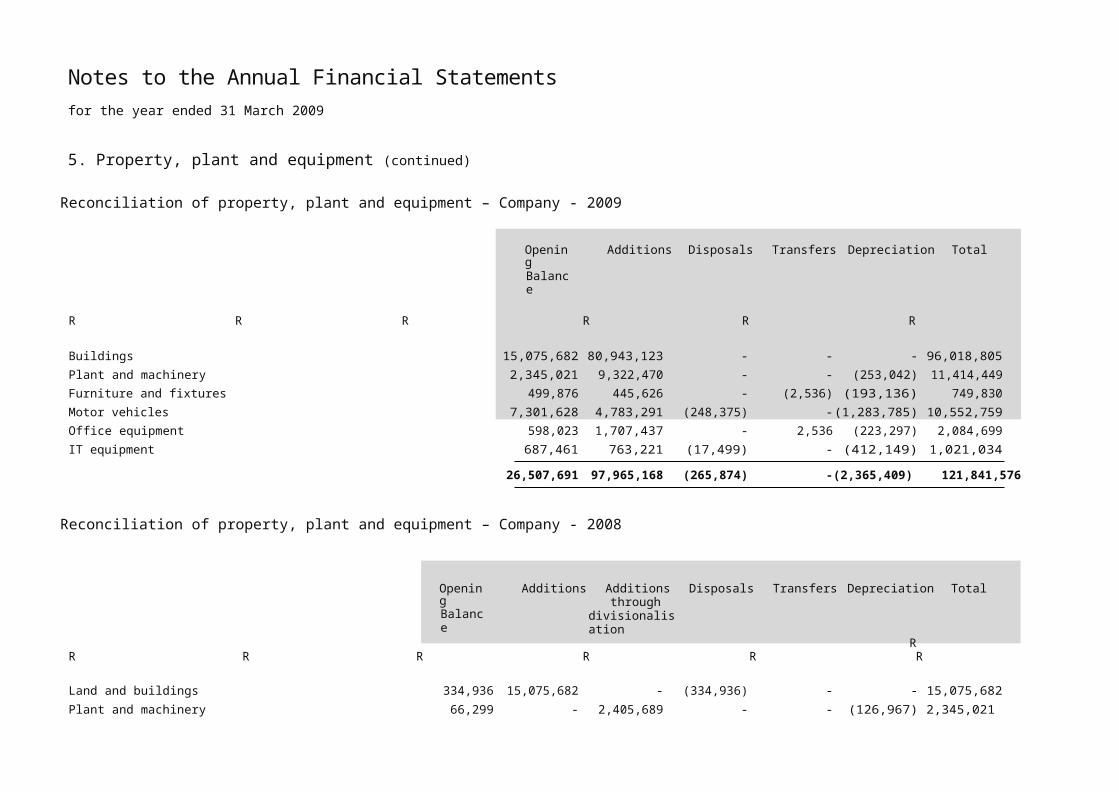

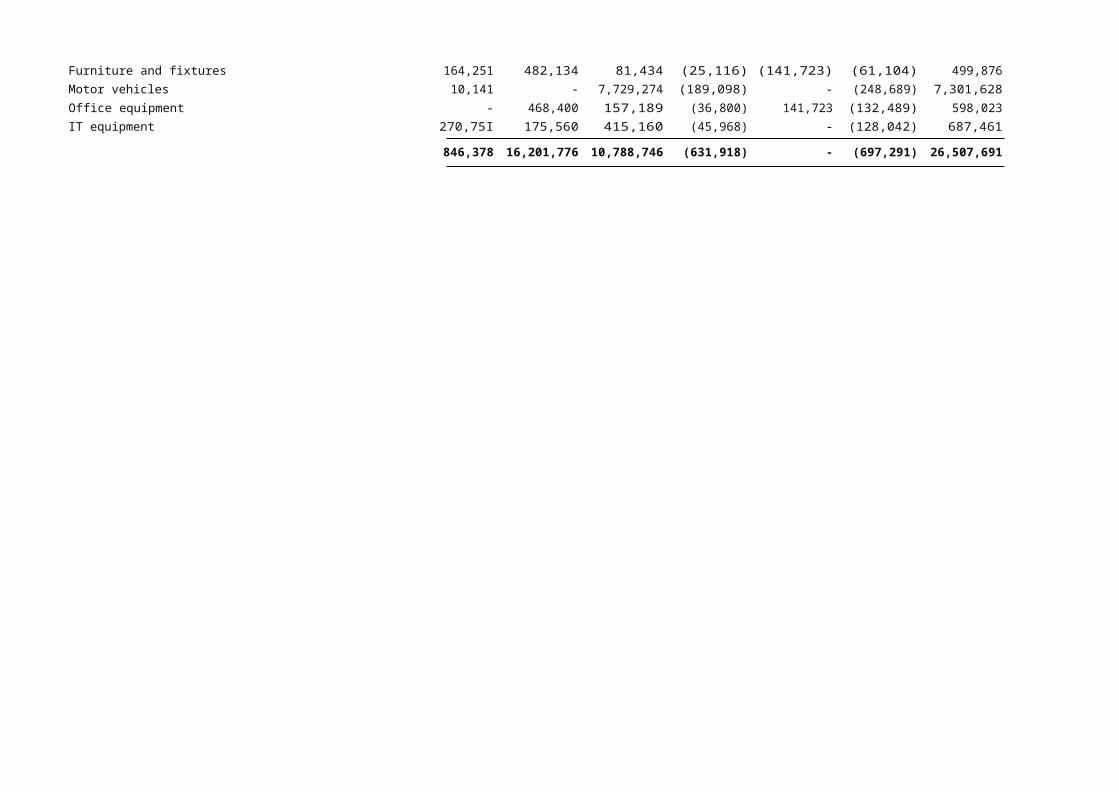

Non-Current AssetsProperty, plant and equipment 5 193,427,366 103,082,234 121,841,576 26,507,691Goodwill 6 13,442,080 13,442,080 - - Intangible assets 7 4,768,448 1,527,489 4,754,141 1,527,497Investments in subsidiaries 8 - - 29,040,703 59,699,153Other financial assets 10 - - - 1,920,232Deferred tax 12 3,447,406 2,859,549 - -

215,085,300 120,911,352 155,636,420 89,654,573

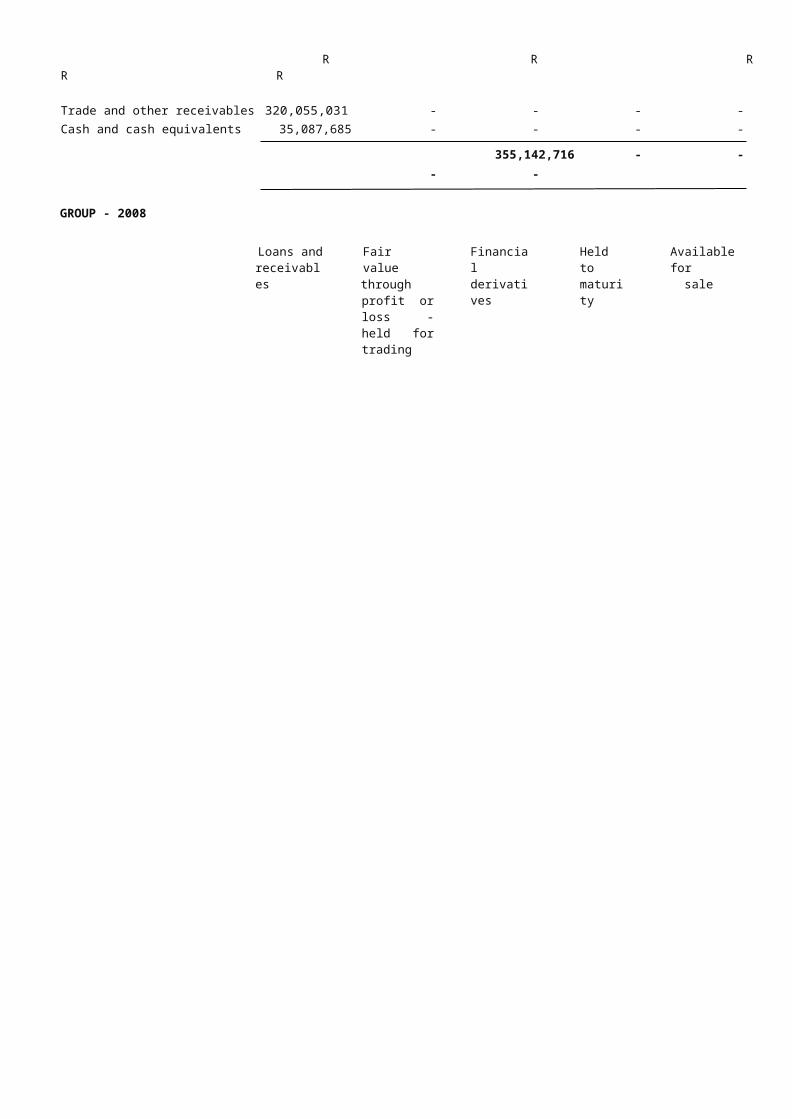

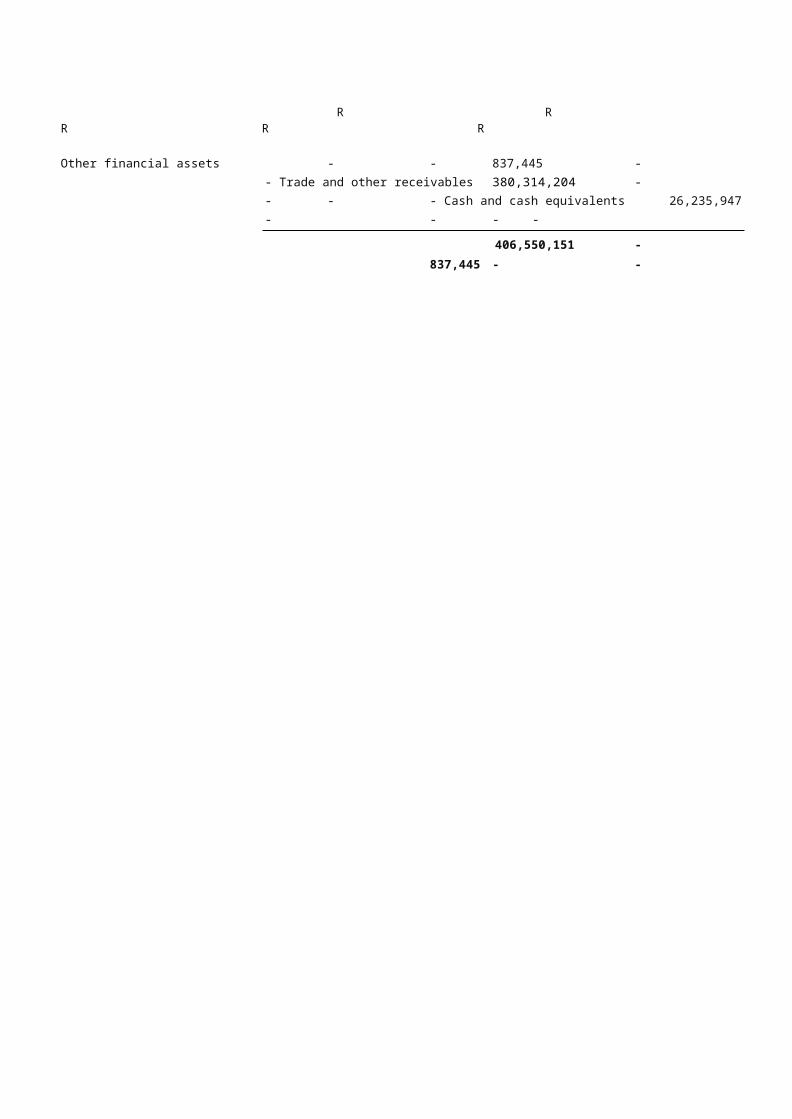

Current AssetsInventories 13 244,757,617 188,440,437 188,702,740 134,155,794Loans to group companies 9 - - 46,594,253 27,915,989Other financial assets 10 - 837,445 - 837,445Current tax receivable 6,946,650 1,337,228 6,722,275 - Trade and other receivables 14 320,055,031 380,314,204 245,645,659 294,226,160Cash and cash equivalents 15 35,087,685 26,235,946 10,163,282 15,073,425

606,846,983 597,165,260 497,828,209 472,208,813

Non-current assets held for sale 16 19,416,346 - - -

Total Assets 841,348,629 718,076,612 653,464,629 561,863,386

Equity and Liabilities

EquityShare capital and share premium 17 117,433,439 124,301,168 124,301,165 126,221,396Reserves 37,811,463 12,373,001 - - Accumulated profit 260,716,690 160,404,993 159,810,460 50,878,606

415,961,592 297,079,162 284,111,625 177,100,002

Liabilities

Non-Current LiabilitiesOther financial liabilities 20 111,965,130 43,836,319 91,811,055 15,763,175Deferred tax 12 3,534,084 6,101,235 419,063 214,934

115,499,214 49,937,554 92,230,118 15,978,109

Current LiabilitiesLoans from group companies 9 - - 5,736,278 - Other financial liabilities 20 10,596,706 16,131,253 9,360,262 8,626,535Current tax payable 6,374,042 23,668,998 - 8,446,837Finance lease obligation 21 1,202,840 1,989,400 - - Trade and other payables 23 165,854,339 188,314,635 161,116,269 245,185,941Provisions 22 - 1,202,211 - 1,202,211Bank overdraft 15 119,736,255 139,753,399 100,910,077 105,323,751

303,764,182 371,059,896 277,122,886 368,785,275

Non-current liabilities held for sale 16 6,123,641 - - -

Total Liabilities 425,387,037 420,997,450 369,353,004 384,763,384Total Equity and Liabilities 841,348,629 718,076,612 653,464,629 561,863,386

Income Statementsfor the year ended 31 March 2009

GROUP COMPANY

Note(s) 2009 2008 2009 2008 R R R R

Revenue 25 1,856,988,671 1,432,302,478 1,565,069,073 404,438,359Cost of sales 26 (1,497,974,467) (1,135,268,482) (1,344,729,171) (316,645,436)

Gross (loss) profit before exceptional items 359,014,204 297,033,996 220,339,902 87,792,923Exceptional items 26 (51,443,768) - (41,692,659) -

Gross profit 307,570,436 297,033,996 178,647,243 87,792,923

Other income 780,013 3,322,951 912,013 3,164,454Operating expenses (154,912,010) (145,923,374) (95,444,048) (45,586,829)

Operating profit before interest and taxation 27 153,438,439 154,433,573 84,115,208 45,370,548

Investment income 28 1,358,188 1,487,349 63,645,726 11,885,662Finance costs 29 (29,355,666) (22,386,685) (18,907,674) (12,166,653)

Profit before taxation 125,440,961 133,534,237 128,853,260 45,089,557

Taxation 30 (25,129,264) (34,166,758) (19,921,406) (12,987,559)

Profit for the year attributable to BSi Steel Limited shareholders 100,311,697 99,367,479 108,931,854 32,101,998

Basic and diluted earnings per share (cents) 40 13.98 15.05

Statements of changes in equityfor the year ended 31 March 2009

Share capital Share premium Foreign currency translation

Revaluation reserve

Accumulated profit

Total attributable to equity holders

Minority interest

Total shareholders

equity

R R

reserve

R R R

of the group

R R R

GroupBalance at 01 April 2007 1,000 - 2,834,731 1,473,616 60,521,785 64,831,132 18,621,575 83,452,707

Profit for the year - - - - 99,367,479 99,367,479 - 99,367,479Issue of shares 6,221 127,377,655 - - - 127,383,876 - 127,383,876Purchase of own / treasury shares

(19) (1,920,213) - - - (1,920,232) - (1,920,232)

Purchase of minority interests - - - 532,444 - 532,444 (18,188,242) (17,655,798)Reversal of NDR to accumulated profit

- - - (515,729) 515,729 - - -

Listing expenses - (1,163,476) - - - (1,163,476) - (1,163,476)Revaluation of property, plant and equipmentPurchase of Discount SteelZambia Limited

- - - 4,650,625 - 4,650,625 - 4,650,625

- - 2,827,451 569,863 - 3,397,314 - 3,397,314

Dividends paid - - - - - - (433,333) (433,333)

Total changes 6,202 124,293,966 2,827,451 5,237,203 99,883,208 232,248,030 (18,621,575) 213,626,455

Balance at 01 April 2008 7,202 124,293,966 5,662,182 6,710,819 160,404,993 297,079,162 - 297,079,162

Revaluation of property, plantand equipment

- - - 2,900,000 - 2,900,000 - 2,900,000

Currency translation differences - - 22,538,462 - - 22,538,462 - 22,538,462Profit for the year - - - - 100,311,697 100,311,697 - 100,311,697Issue of shares 157 13,848,843 - - - 13,849,000 - 13,849,000Purchase of treasury shares (157) (13,848,843) - - - (13,849,000) - (13,849,000) Purchase of own shares (75) (6,867,654) - - - (6,867,729) - (6,867,729)Total changes (75) (6,867,654) 22,538,462 2,900,000 100,311,697 118,882,430 - 118,882,430

Balance at 31 March 2009 7,127 117,426,312 28,200,644 9,610,819 260,716,690 415,961,592 - 415,961,592

Note(s) 17 17 18 19